f3 expedite notes dec 2010 - · pdf fileexpedite notes acca f3 financial accounting ch 1 | 7...

TRANSCRIPT

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 1 | 1 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

Chapter�1�

Financial�Statements�

�

STARTThe Big Picture

�Financial�statements�(more�colloquially�called�accounts)�are�a�crucial�part�of�managing�a�business�and�reporting�to�shareholders.��A�set�of�financial�statements�will�need�to�be�produced�at�least�annually�for�presentation�to�external�stakeholders,�but�generally�much�more�frequently�for�management�control�within�the�business.���Frequent�and�accurate�financial�statements�can�add�a�great�deal�to�the�efficient�running�of�a�business.��A�set�of�financial�statements�is�produced�periodically�(often�once�a�year�for�smaller�businesses�but�as�frequently�as�the�users�want�them).��A�full�set�of�financial�statements�for�a�limited�company�comprises�a�number�of�statements:��

� A�statement�of�financial�position,�generally�called�a�balance�sheet.��This�lists�all�the�assets�and�liabilities�of�the�business�plus�the�equity�of�the�business�(which�explains�where�the�assets�and�liabilities�came�from).��The�statement�of�financial�position�is�a�snapshot�of�the�assets�and�liabilities�of�a�business�at�a�moment�in�time.�

� A�statement�of�comprehensive�income,�often�referred�to�as�profit�and�loss�account.��This�shows�all�the�gains�and�losses�that�the�business�has�experienced�in�the�period.��The�statement�of�comprehensive�income�is�a�record�of�what�happened�over�a�period�to�the�net�assets�of�a�business.�

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 1 | 2 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

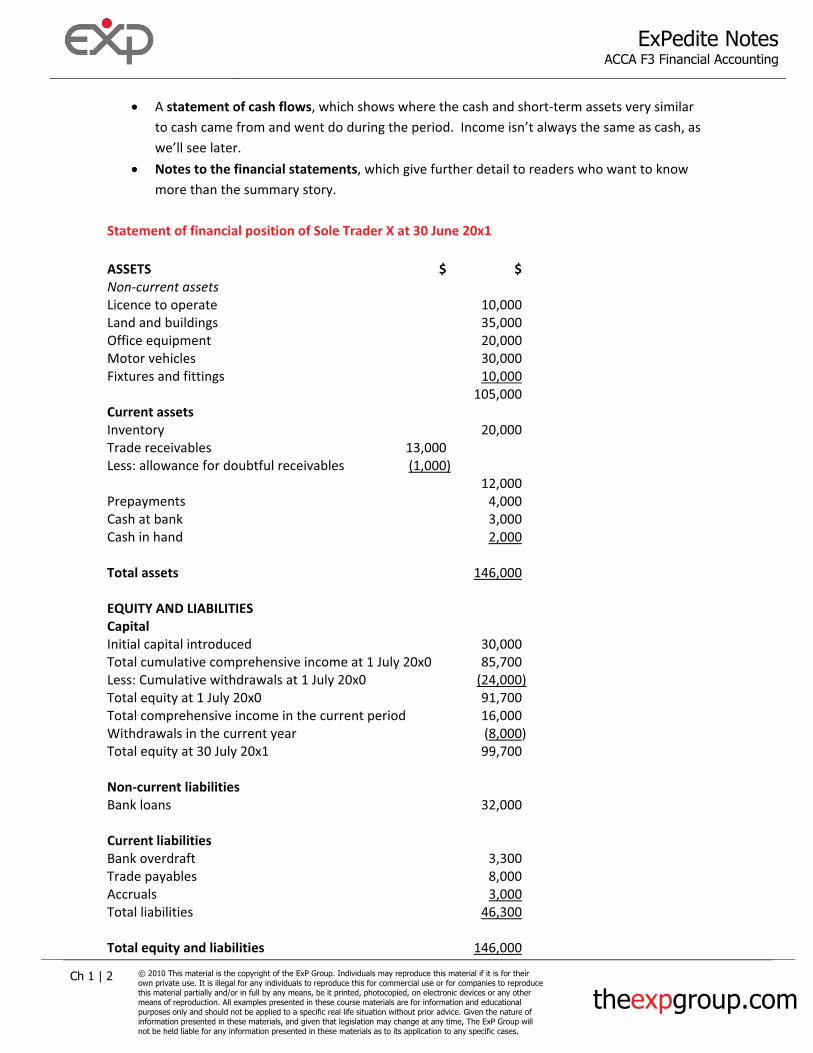

� A�statement�of�cash�flows,�which�shows�where�the�cash�and�short�term�assets�very�similar�to�cash�came�from�and�went�do�during�the�period.��Income�isn’t�always�the�same�as�cash,�as�we’ll�see�later.�

� Notes�to�the�financial�statements,�which�give�further�detail�to�readers�who�want�to�know�more�than�the�summary�story.�

�Statement�of�financial�position�of�Sole�Trader�X�at�30�June�20x1��ASSETS� $� $�Non�current�assets�Licence�to�operate� � 10,000�Land�and�buildings�� � 35,000�Office�equipment�� � 20,000�Motor�vehicles�� � 30,000�Fixtures�and�fittings� �� 10,000�� � 105,000�Current�assets�Inventory� � 20,000�Trade�receivables�� 13,000�Less:�allowance�for�doubtful�receivables�� (1,000)�� � 12,000�Prepayments�� � 4,000�Cash�at�bank� � 3,000�Cash�in�hand�� � 2,000�� � �Total�assets�� � 146,000��EQUITY�AND�LIABILITIES�Capital�Initial�capital�introduced� � 30,000�Total�cumulative�comprehensive�income�at�1�July�20x0� � 85,700�Less:�Cumulative�withdrawals�at�1�July�20x0� � (24,000)�Total�equity�at�1�July�20x0� � 91,700�Total�comprehensive�income�in�the�current�period� � 16,000�Withdrawals�in�the�current�year� � (8,000)�Total�equity�at�30�July�20x1� � 99,700��Non�current�liabilities�Bank�loans�� � 32,000��Current�liabilities�Bank�overdraft�� � 3,300�Trade�payables�� � 8,000�Accruals�� � 3,000�Total�liabilities� � 46,300��Total�equity�and�liabilities�� � 146,000�

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 1 | 3 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

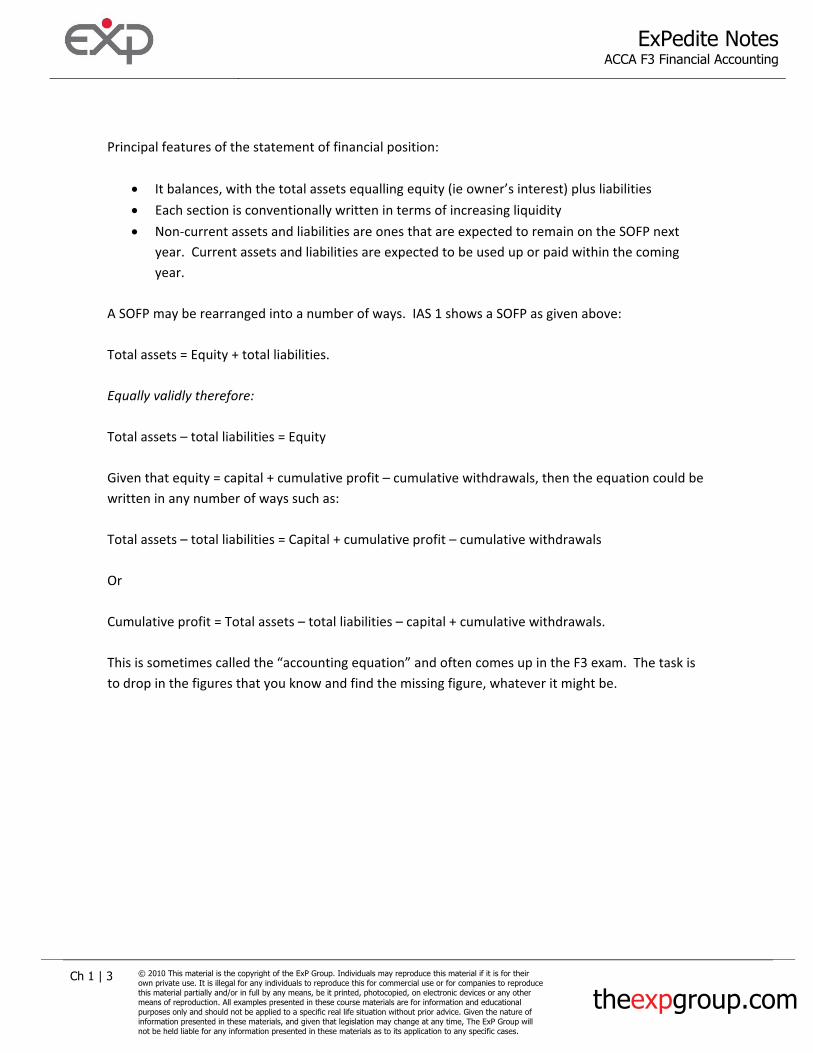

It�balances,�with�the�total�assets�equallingrms�of�increasing�liquidity�

Non�current�assets�and�liabilities�are�onesilities�are�expected�to�be�used�up�or�paid�within�the�coming�

year.�

�SOFP�as�given�above:�

es�=�Equity�

e�profit�–�cumulative�withdrawals,�then�the�equation�could�be�ritten�in�any�number�of�ways�such�as:�

�profit�–�cumulative�withdrawals�

ulative�profit�=�Total�assets�–�total�liabilities�–�capital�+�cumulative�withdrawals.�

m.��The�task�is��drop�in�the�figures�that�you�know�and�find�the�missing�figure,�whatever�it�might�be.�

��Principal�features�of�the�statement�of�financial�position:��

� �equity�(ie�owner’s�interest)�plus�liabilities�� Each�section�is�conventionally�written�in�te� �that�are�expected�to�remain�on�the�SOFP�next�

year.��Current�assets�and�liab

�A�SOFP�may�be�rearranged�into�a�number�of�ways.��IAS�1�shows�a�Total�assets�=�Equity�+�total�liabilities.��Equally�validly�therefore:��Total�assets�–�total�liabiliti�Given�that�equity�=�capital�+�cumulativw�Total�assets�–�total�liabilities�=�Capital�+�cumulative�Or���Cum�This�is�sometimes�called�the�“accounting�equation”�and�often�comes�up�in�the�F3�exato�������������

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 1 | 4 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

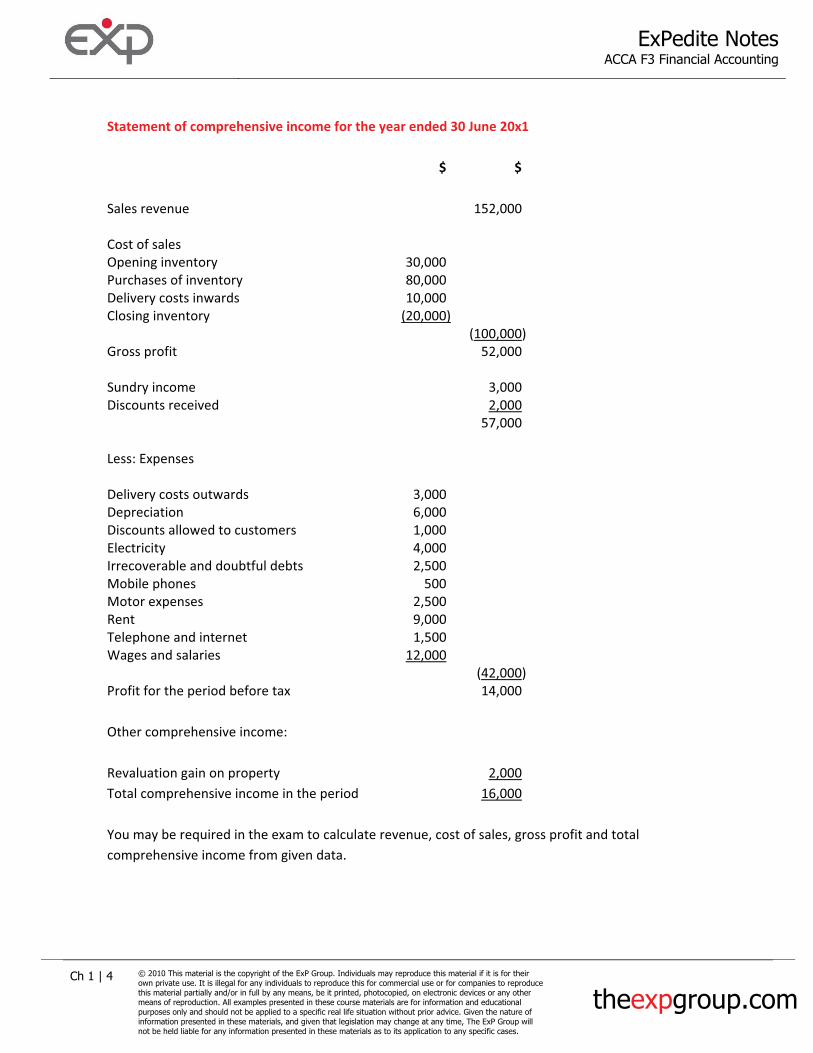

tatement�of�comprehensive�income�for�the�year�ended�30�June�20x1�

ales�revenue� � 152,00

pening�inventory� �30,000�� 80,000�

�S�� � $� $��S 0��Cost�of�sales�OPurchases�of�inventoryDelivery�costs�inwards� 10,000�Closing�inventory� (20,000)�� � (100,000)�

52,000�

e����

Gross�profit�� ��Sundry�incom � 3,000�iscounts�received � 2,000D �

� � 7,000�5

utwards�� 3,000�epreciation�� 6,000�

omers��

ernet���� 1

�Less:�Expenses��Delivery�costs�oDDiscounts�allowed�to�cust 1,000�Electricity�� 4,000�Irrecoverable�and�doubtful�debts�� 2,500�

nes�Mobile�pho 500�Motor�expenses�� 2,500�

9Rent�� ,000�Telephone�and�int 1,500�

�and�salariesWages 2,000�� � (42,000)�

�tax� � 14,000�

� 2,000

Profit�for�the�period�before�Other�comprehensive�income:��Revaluation�gain�on�property�� �otal�comprehensive�income�in�the�period� � 16,000T � � �

rofit �total�omprehensive�income�from�given�data.�

�You�may�be�required�in�the�exam�to�calculate�revenue,�cost�of�sales,�gross�p �andc����

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 1 | 5 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

�

theexpgroup.com

�REVIEW�AND�SELF�TEST�1�

�Using�the�financial�statements�above,�calculate�the�following�ratios:��

� Gross�profit�%�� Net�profit�%�� Total�comprehensive�income�%�

��Unusual�items��Sometimes,�it�is�necessary�for�one�off�items�to�be�disclosed�separately�in�the�financial�statements�if�they�are�very�large�or�arise�from�an�unusual,�often�non�recurring,�source.��Typical�examples�might�be�write�off�of�an�unusually�large�debt�as�irrecoverable,�or�business�relocation�costs.��Disclosing�it�separately�allows�readers�of�the�accounts�a�more�in�depth�understanding�of�what�the�business�is�doing.���

KEY�KNOWLEDGEElements�of�financial�statements�

�There�are�five�elements�of�financial�statements,�from�which�all�financial�statements�are�produced.��These�definitions�are�very�useful�throughout�your�ACCA�studies�and�could�easily�be�part�of�a�question�in�paper�F3.��Elements�of�the�statement�of�financial�position:��

� An�asset�is�a�resource�that�is�controlled�by�an�entity�as�a�result�of�past�events�and�from�which�future�economic�benefits�are�expected�to�flow�to�the�entity.�

�� A�liability�is�a�present�obligation�of�the�entity�arising�from�past�events,�the�settlement�of�

which�is�expected�to�result�in�an�outflow�from�the�entity�of�resources�embodying�economic�benefits.�

�� Equity�is�the�residual�interest�in�the�assets�of�the�entity�after�deducting�all�its�liabilities.���

Depending�on�the�type�of�business,�this�may�be�called�just�capital�(sole�trader),�partners’�current�account�(partnership)�or�share�capital�and�reserves�(for�a�limited�company).��For�a�limited�company,�reserves�show�the�net�cumulative�gains�above�cumulative�losses,�less��all�

�

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 1 | 6 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

dividends�paid.��This�therefore�explains�the�difference�between�what�the�net�assets�were�when�the�share�capital�was�originally�paid�in�and�what�the�net�assets�are�at�the�reporting�date.�

��Elements�of�the�statement�of�comprehensive�income:��

� Income�is�an�increase�in�economic�benefits�during�the�accounting�period�in�the�form�of�inflows�or�enhancements�of�assets�or�decreases�of�liabilities�that�result�in�increases�in�equity,�other�than�those�relating�to�contributions�from�equity�participants.�

�� An�expense�is�a�decrease�in�economic�benefits�during�the�accounting�period�in�the�form�of�

outflows�or�depletions�of�assets�or�incurrence�of�liabilities�that�result�in�decreases�in�equity,�other�than�those�relating�to�distributions�to�equity�participants.�

�Note�that�income�and�expenditure�are�defined�effectively�as�the�reason�that�a�change�in�net�assets�happened.����

KEY�KNOWLEDGERelationship�between�the�statements:�the�business�equation�

�An�increase�in�net�assets�of�a�business�will�come�from�a�mixture�of�these�sources:��

� Total�comprehensive�income�made�in�the�period�(a�profit�will�increase�net�assets)�� New�capital�introduced�by�the�owner�(will�always�increase�net�assets)�� Withdrawals�made�in�the�period�(will�always�reduce�net�assets).�

�This�is�sometimes�called�the�accounting�equation�or�the�business�equation.��It�is�a�frequent�exam�question�and�can�be�summarised:��Closing�net�assets�=�� Opening�net�assets�+�total�comprehensive�income�in�the�period�+�new�

capital�introduced�in�the�period�–�withdrawals�in�the�period.��This�is�also�a�frequent�exam�question,�with�some�figures�given�and�the�others�having�to�be�deduced.��Remember�that�net�assets�=�equity�+�liabilities,�by�definition.��So�net�assets�may�be�given�in�a�question�separately�as�equity�and�liabilities.�

� �

�

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 1 | 7 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

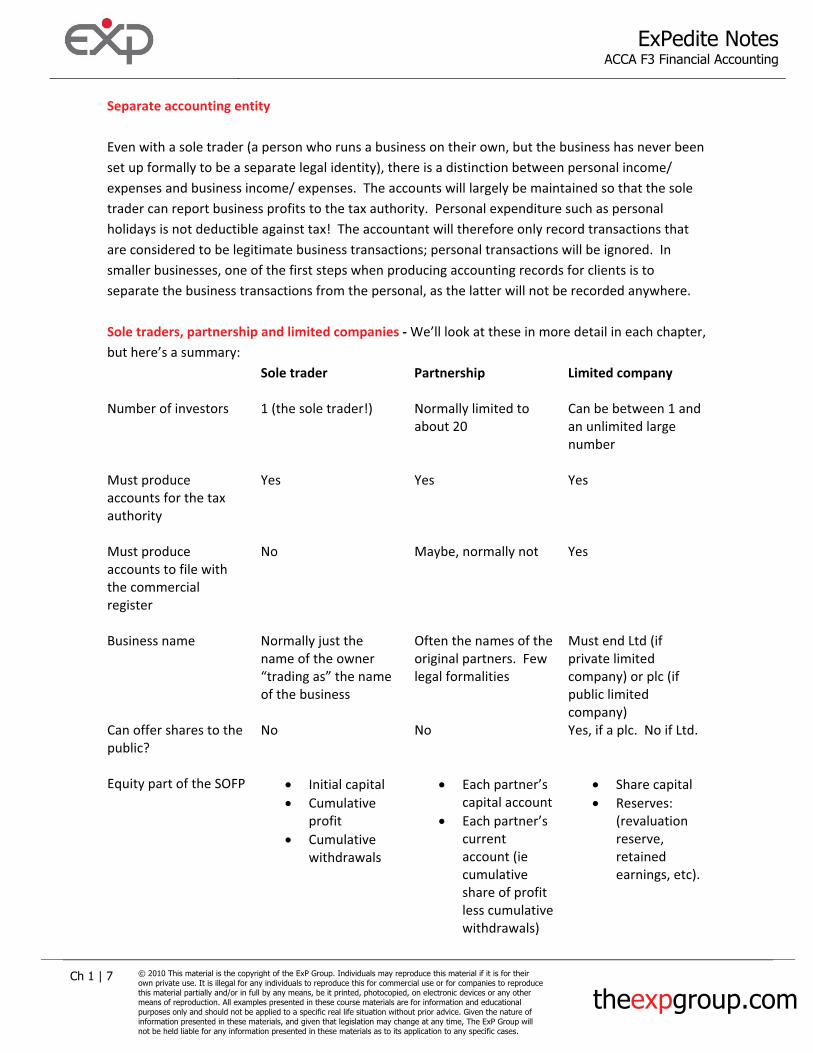

Separate�accounting�entity��Even�with�a�sole�trader�(a�person�who�runs�a�business�on�their�own,�but�the�business�has�never�been�set�up�formally�to�be�a�separate�legal�identity),�there�is�a�distinction�between�personal�income/�expenses�and�business�income/�expenses.��The�accounts�will�largely�be�maintained�so�that�the�sole�trader�can�report�business�profits�to�the�tax�authority.��Personal�expenditure�such�as�personal�holidays�is�not�deductible�against�tax!��The�accountant�will�therefore�only�record�transactions�that�are�considered�to�be�legitimate�business�transactions;�personal�transactions�will�be�ignored.��In�smaller�businesses,�one�of�the�first�steps�when�producing�accounting�records�for�clients�is�to�separate�the�business�transactions�from�the�personal,�as�the�latter�will�not�be�recorded�anywhere.��Sole�traders,�partnership�and�limited�companies���We’ll�look�at�these�in�more�detail�in�each�chapter,�but�here’s�a�summary:�� Sole�trader� Partnership� Limited�company�

�Number�of�investors� 1�(the�sole�trader!)� Normally�limited�to�

about�20�Can�be�between�1�and�an�unlimited�large�number��

Must�produce�accounts�for�the�tax�authority��

Yes� Yes� Yes�

Must�produce�accounts�to�file�with�the�commercial�register��

No� Maybe,�normally�not� Yes�

Business�name� Normally�just�the�name�of�the�owner�“trading�as”�the�name�of�the�business�

Often�the�names�of�the�original�partners.��Few�legal�formalities�

Must�end�Ltd�(if�private�limited�company)�or�plc�(if�public�limited�company)�

Can�offer�shares�to�the�public?��

No� No� Yes,�if�a�plc.��No�if�Ltd.�

Equity�part�of�the�SOFP� � Initial�capital��� Cumulative�

profit�� Cumulative�

withdrawals�

� Each�partner’s�capital�account

� Each�partner’s�current�account�(ie�cumulative�share�of�profit�less�cumulative�withdrawals)�

� Share�capital�� Reserves:�

(revaluation�reserve,�retained�earnings,�etc).�

�

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 1 | 8 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

�Solution�to�review�and�self�test�1��Gross�profit�%�=�52/152�=�34.2%�Net�profit�%�=�14/�152�=�9.2%�Total�comprehensive�income�%�=�16/152�=�10.5%��

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 2 | 1 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

Chapter�2�

Objectives�of�financial�reporting�

��

��

STARTThe Big Picture

�Financial�reporting�is�the�business�of�collecting�financial�information,�analysing,�summarising�it�and�presenting�it�in�a�useful�form�to�a�wide�range�of�different�users.��Different�users�will�have�different�objectives�and�therefore�slightly�different�needs.��Financial�statements�are�aimed�at�giving�useful�information�to�a�wide�range�of�different�users,�though�the�investor�is�the�most�significant�user.���

�REVIEW�AND�SELF�TEST�1�

�For�each�of�the�different�stakeholders�below,�state�what�their�principal�interest�will�be�in�a�business�and�then�suggest�which�information�within�a�set�of�financial�statements�will�principally�interest�them.����

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 2 | 2 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

�1. Investors�2. Bank�lender�3. Government�statistical�office�4. Tax�authority�5. Employees�6. Suppliers�7. Customers�8. Management�

��For�internal�users�such�as�management,�the�accounting�system�may�be�used�to�produce�management�accounts.��These�are�produced�much�more�frequently�than�the�accounts�sent�to�shareholders�and�contain�much�more�detailed�information.���The�accounting�system�may�be�used�to�monitor�lots�of�things,�such�as�profitability�of�different�products�and�services�and�thus�add�a�lot�to�the�efficient�running�of�the�business.��For�financial�information�to�be�useful,�it�must�exhibit�a�number�of�characteristics.��It’s�important�to�understand�what�these�are�because�you�may�be�asked�for�a�definition�of�them�in�the�exam.��

Qualitative�characteristic� Our�definition�

Fair�presentation� Items�are�described�in�accordance�with�their�true�nature.��For�example,�loans�repayable�within�six�months�are�classified�as�current�rather�than�non�current.�

Going�concern� The�business�is�expected�to�trade�into�the�foreseeable�future.�This�means�that�assets�will�not�have�to�be�sold�in�a�hurry,�which�would�be�likely�to�result�in�significant�impairments�in�value.�

Accruals� A�key�concept�covered�in�chapter�[x].��It�means�recording�transactions�in�the�period�when�they�happened;�not�necessarily�when�the�cash�was�settled.��It�also�means�matching�costs�and�associated�revenues.�

Consistency� Items�should�be�reported�the�same�way�between�periods,�so�that�it’s�possible�to�make�meaningful�comparisons�between�years.��Similar�transactions�must�be�reported�the�same�way�within�the�same�accounting�period.�

Materiality� Materiality�means�large�enough�to�influence�the�user’s�opinion�on�the�financial�statements.��Immaterial�information�should�not�be�disclosed,�as�it’s�a�distraction.��Material�information�must�be�presented�accurately�and�fairly.�

Relevance� Irrelevant�information�is�a�distraction�and�should�not�be�presented.���

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 2 | 3 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

Substance�over�form�

Reliability� Information�is�useless�if�it’s�not�considered�to�be�reliable.��Eg�an�external�valuation�of�property�is�more�reliable�than�a�biased�director’s�valuation.�

Faithful�representation� Items�should�be�described�in�accordance�with�their�true�nature.��Eg�an�expense�for�repairs�should�not�be�classified�as�research�costs,�even�though�research�costs�are�more�favourably�viewed�by�investors.�

Items�should�be�reported�in�accordance�with�their�commercial�substance,�rather�than�their�legal�form.��Eg�if�a�sale�is�made�on�credit�but�legal�title�remains�with�the�seller�until�the�goods�are�paid�for,�it�should�still�be�recorded�as�a�sale/�purchase�at�the�time�of�the�transaction,�since�this�is�when�the�obligation�arises.�

Neutrality� Unbiased�–�neither�excessively�optimistic�nor�excessively�prudent.�

Prudence� Conservatism.��This�is�no�longer�a�core�concept�in�IFRS�accounting,�but�broadly�losses�should�be�recognised�more�readily�than�gains.�

Completeness� All�information�that�needs�to�be�presented�in�order�to�give�a�full�picture�has�been�presented.�

Comparability� Financial�statements�this�period�should�be�presented�using�similar�principles�to�previous�years,�so�that�valid�comparisons�may�be�made.��Company�accounts�should�be�comparable�with�each�other.��This�means�that�if�a�company�changes�its�accounting�policy,�it�must�restate�its�previous�years’�accounts�using�the�new�accounting�policy,�in�order�to�facilitate�comparison�between�years.�

Understandability� Information�should�be�presented�in�a�way�that�users�can�understand.��Excessive�complication�reduces�usefulness.�

Business�entity�concept� See�chapter�1.��Even�if�there�is�no�separate�legal�entity,�as�with�a�sole�trader,�the�business�is�still�considered�to�be�separate�to�its�owners�for�accounting�purposes.�

��Sometimes,�it’s�not�possible�to�deliver�all�of�these�desirable�characteristics.��For�example,�an�investor�is�principally�interested�in�future�profits,�so�this�is�what�is�relevant�to�them.��However,�estimates�of�future�profit�are�unreliable,�so�historical�information�is�given,�even�though�it�is�less�relevant.�� �

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 2 | 4 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

�

�

KEY�KNOWLEDGEHistorical�accounting��

Accounting�is�derived�from�recording�information�about�transactions�that�have�happened.��This�means�that�assets�are�recorded�at�their�historical�cost;�ie�what�the�business�paid�for�them.��This�has�the�advantage�of�being�objective�and�relatively�easy,�but�has�a�number�of�disadvantages,�including:��

� It�can�give�out�of�date�asset�valuations�for�long�lived�assets�� This�can�result�in�an�unrealistically�low�depreciation�charge�� Profit�trends�can�be�misleading�(eg�a�profit�growth�of�10%�per�year�isn’t�so�impressive�as�it�

first�seems�if�inflation�is�12%�per�year!)�� Where�there’s�significant�inflation�and�inventory�is�held�for�a�long�time,�profit�can�be�

reported�simply�by�matching�today’s�revenues�with�yesterday’s�costs.��There�are�some�large�advantages�of�historical�cost�accounting,�however;�principally�the�fact�that�people�understand�it�and�it�is�objective.����During�periods�of�modest�inflation,�the�weaknesses�of�historical�cost�accounting�are�generally�outweighed�by�its�advantages.��There�are�alternative�systems�of�accounting,�such�as�replacement�cost�accounting.��Replacement�cost�accounting�records�inventories�in�the�SOFP�and�at�the�point�of�sale�at�the�cost�that�would�be�incurred�to�replace�them�today.��This�has�many�advantages�but�is�complicated�to�apply�so�is�not�common�in�practice.��You�will�only�have�to�apply�historical�cost�accounting�in�the�paper�F3�exam.���

�

KEY�KNOWLEDGERegulation�of�financial�reporting��

�Some�entities�have�to�report�under�regulated�accounting�standards.��Different�countries�may�have�their�own�systems�of�GAAP�(generally�accepted�accounting�practice)�or�may�follow�International�Financial�Reporting�Standards�(IFRS)�or�IFRS�for�SMEs�(SME�means�smaller�and�medium�sized�enterprises).��It�is�a�matter�of�national�regulation�which�financial�reporting�standards�an�entity�must�use�when�producing�their�financial�reports.��Large�plc’s�will�have�to�report�under�a�much�more�extensive�financial�reporting�framework�than�sole�traders.��

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 2 | 5 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

There�are�a�number�of�bodies�that�you�need�to�be�aware�of�for�the�Paper�F3�exam.��Their�roles�are�given�below.��

IASCF:�the�International�Accounting�Standards��

This�has�recently�been�renamed�the�IFRS�Foundation.��The�Foundation�is�made�up�of�trustees,�who�appoint�the�members�of�the�bodies�below.���

IASB:�International�Accounting�Standards�Board�

The�IASB�issues�International�Financial�Reporting�Standards�and�the�IFRS�for�SMEs.��It�employs�a�permanent�staff�to�draft�new�accounting�standards�and�amendments�considered�necessary�to�extant�accounting�standards.�

SAC:�Standards�Advisory�Council� This�has�recently�been�renamed�the�IFRS�Advisory�Council.��It�is�made�up�of�a�cross�section�of�advisors�from�different�user�groups.��It�advises�the�IASB�on�the�IASB’s�work�programme.�

IFRIC:�International�Financial�Reporting�Interpretations�Committee�

This�has�recently�been�renamed�the�IFRS�Interpretations�Committee.��This�body�is�designed�to�respond�quickly�where�there�are�significant�differences�in�interpretation�of�an�extant�IFRS.��For�example,�it�issued�guidance�on�how�to�account�for�loyalty�programmes,�where�users�were�uncertain�to�follow�the�extant�accounting�standard�on�revenue�recognition,�or�provisions.���

��� �

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 2 | 6 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

Solution�to�review�and�self�test�1��For�each�of�the�different�stakeholders�below,�state�what�their�principal�interest�will�be�in�a�business�and�then�suggest�which�information�within�a�set�of�financial�statements�will�principally�interest�them.��

1. Investors�will�be�interested�in�what�profit�they�can�expect�to�get�from�a�business,�what�the�cash�flow�health�of�the�business�is�(ie�what�risk�of�failure)�and�how�much�of�a�premium�equity�investors�are�getting�over�providers�of�secured�finance,�such�as�secured�loans.��They�will�be�interested�in�growth�of�profit�that�is�expected,�as�this�will�most�probably�be�the�primary�influence�on�the�value�of�shares�in�the�company.��They�will�therefore�be�interested�in�all�the�financial�statements,�in�some�detail.�

2. Bank�lenders�will�be�interested�in�whether�the�company�is�generating�enough�profit�and�cash�flow�to�pay�interest�on�the�loans�and�be�able�to�repay�the�loans�as�they�fall�due�for�repayment.��They�will�primarily�be�interested�in�the�statement�of�comprehensive�income�and�statement�of�cash�flows.�

3. Government�statistical�office�will�be�interested�in�collecting�statistics�for�gross�domestic�product,�etc.��They�will�primarily�be�interested�in�statement�of�comprehensive�income.�

4. Tax�authority�will�be�interested�in�taxable�profit,�which�will�be�an�amended�form�of�reported�profit�to�investors.�They�will�primarily�be�interested�in�the�SOCI�as�the�basis�for�the�tax�return.�

5. Employees�will�be�interested�in�job�security�and�whether�the�company�is�doing�very�well.��If�it’s�doing�very�well,�they�are�likely�to�be�in�a�stronger�position�to�push�for�pay�rises.��They�are�likely�to�be�primarily�interested�in�SOCI�and�certain�notes�to�the�accounts,�such�as�directors’�pay.�

6. Suppliers�will�want�to�know�that�the�company�is�a�stable�customer�and�good�for�credit�risk.��Their�focus�will�be�very�similar�to�that�of�a�bank�lender.�

7. Customers�will�wish�to�see�security�of�supply�and�will�not�be�primarily�interested�in�profit.��They�will�have�similar�interests�to�a�bank.�

8. Management�will�be�interested�in�a�great�deal�of�detail,�as�this�is�likely�to�help�them�in�managing�the�business.��They�will�be�interested�in�cash�flow�primarily�day�by�day,�but�also�all�other�aspects�of�the�company’s�performance�and�position.��It�is�likely�that�special�management�accounts�will�be�produced,�frequently�and�in�greater�detail�than�the�accounts�provided�to�investors.�

���

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 3 | 1 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

Chapter�3�

Sources�of�financial�information�

�

��

STARTThe Big Picture

�The�accounting�system�must�naturally�be�fed�with�raw�source�data.��This�data�is�then�analysed,�categorised�and�recorded�in�the�accounting�system�itself,�which�may�be�a�fully�manual�(paper�based)�system�or�may�be�maintained�using�software.��Both�use�the�same�system�of�double�entry�bookkeeping�that�we�will�see�later�on.��For�an�accounting�system�to�work�well,�it�must�be�simple�to�operate�and�be�capable�of�being�fed�by�non�specialist�staff.��A�key�step�is�therefore�ensuring�that�the�right�stationery�and�documentation�is�in�place.��The�F3�syllabus�requires�you�to�be�able�to�define�the�following:��Document� Purpose� Often�feeds�the�accounting�

information�on....�Quotation� To�give�a�potential�customer�an�indication�of�

what�a�product�or�service�would�be�likely�to�cost.��It�may�be�a�binding�quote�or�just�an�indicative�quote.�

Nowhere.��At�this�stage,�there�has�been�no�transaction�to�record;�it’s�still�at�the�state�of�being�a�prospective�transaction.

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 3 | 2 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

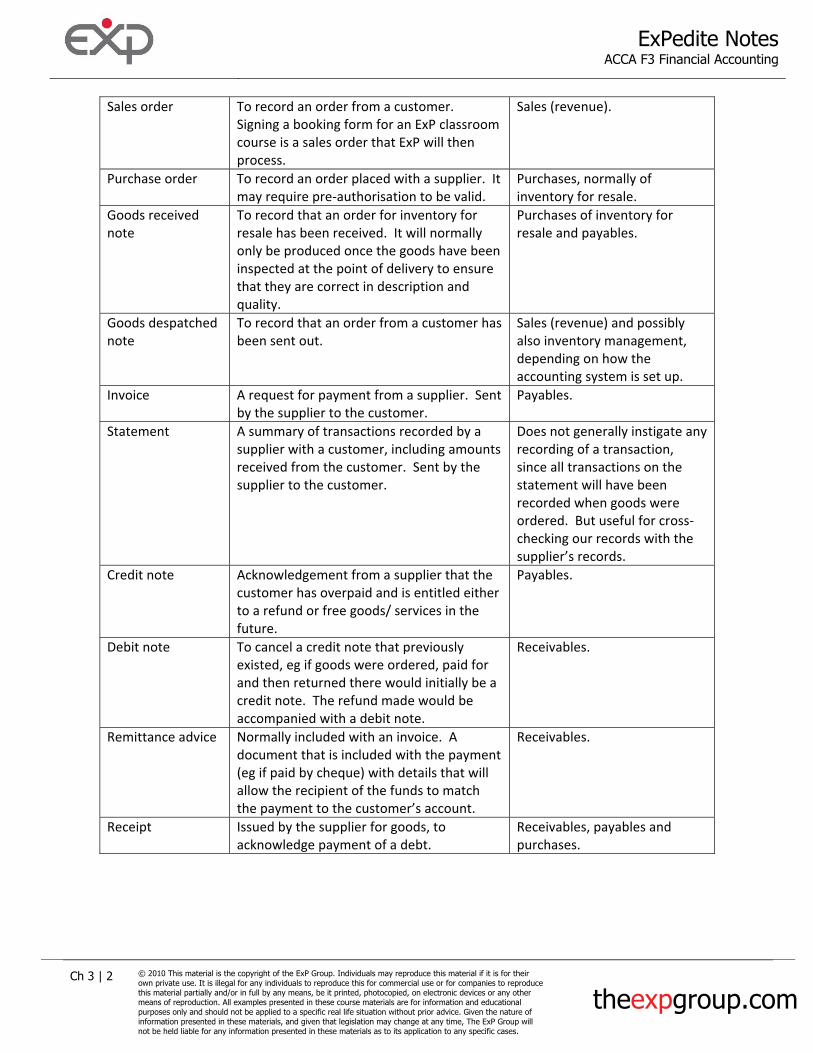

Sales�order� To�record�an�order�from�a�customer.��Signing�a�booking�form�for�an�ExP�classroom�course�is�a�sales�order�that�ExP�will�then�process.�

Sales�(revenue).�

Purchase�order� To�record�an�order�placed�with�a�supplier.��It�may�require�pre�authorisation�to�be�valid.���

Purchases,�normally�of�inventory�for�resale.�

Goods�received�note�

To�record�that�an�order�for�inventory�for�resale�has�been�received.��It�will�normally�only�be�produced�once�the�goods�have�been�inspected�at�the�point�of�delivery�to�ensure�that�they�are�correct�in�description�and�quality.�

Purchases�of�inventory�for�resale�and�payables.�

Goods�despatched�note�

To�record�that�an�order�from�a�customer�has�been�sent�out.�

Sales�(revenue)�and�possibly�also�inventory�management,�depending�on�how�the�accounting�system�is�set�up.�

Invoice� A�request�for�payment�from�a�supplier.��Sent�by�the�supplier�to�the�customer.�

Payables.�

Statement� A�summary�of�transactions�recorded�by�a�supplier�with�a�customer,�including�amounts�received�from�the�customer.��Sent�by�the�supplier�to�the�customer.�

Does�not�generally�instigate�any�recording�of�a�transaction,�since�all�transactions�on�the�statement�will�have�been�recorded�when�goods�were�ordered.��But�useful�for�cross�checking�our�records�with�the�supplier’s�records.�

Credit�note� Acknowledgement�from�a�supplier�that�the�customer�has�overpaid�and�is�entitled�either�to�a�refund�or�free�goods/�services�in�the�future.���

Payables.�

Debit�note� To�cancel�a�credit�note�that�previously�existed,�eg�if�goods�were�ordered,�paid�for�and�then�returned�there�would�initially�be�a�credit�note.��The�refund�made�would�be�accompanied�with�a�debit�note.�

Receivables.�

Remittance�advice� Normally�included�with�an�invoice.��A�document�that�is�included�with�the�payment�(eg�if�paid�by�cheque)�with�details�that�will�allow�the�recipient�of�the�funds�to�match�the�payment�to�the�customer’s�account.�

Receivables.�

Receipt� Issued�by�the�supplier�for�goods,�to�acknowledge�payment�of�a�debt.�

Receivables,�payables�and�purchases.�

��� �

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 3 | 3 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

�

KEY�KNOWLEDGEData�sources�/�data�capture��

�When�a�business�transaction�happens,�it�is�essential�that�the�source�data�is�captured�immediately.��This�does�not�necessarily�mean�immediately�writing�up�the�books,�but�it�does�involve�some�record�being�made�of�the�transaction�happening.��In�very�simple�accounting�systems�for�sole�traders�(eg�a�self�employed�builder)�it�may�involve�the�proprietor�keeping�pocket�books�to�record�things�like�quotes�given�and�a�shoe�box�used�to�collect�receipts�for�business�expenses.��From�this�source�data,�the�accounting�records�can�then�be�produced�each�period.��The�accountant�is�often�not�physically�present�at�the�time�that�transactions�happen,�so�it�is�essential�that�there�are�simple�and�fool�proof�systems�to�ensure�a�complete�and�accurate�record�of�business�transactions.���

�

KEY�KNOWLEDGEBooks�of�original�entry��

�Alternatively�called�books�of�prime�entry,�these�will�be�the�bridge�between�the�raw�data�(eg�receipt�for�cash�purchase�of�some�building�materials�and�the�accounting�system.��They�may�be�written�up�by�the�accountant,�or�by�a�semi�trained�member�of�staff�within�the�client’s�business.��The�most�commonly�used�books�of�original�entry�are:��

Book�of�original�entry:�

Used�to�record�data�on:� Data�typically�used�to�feed:�

Cash�in�book� Cash�received�into�the�business�bank�account.� All�sorts�of�things!��Anything�that�may�generate�cash�for�the�business.�

Cash�payments�book�

Cash�paid�from�the�business�bank�account.� All�sorts�of�things!��Anything�that�results�in�cash�being�paid�out�of�the�business.�

Petty�cash�book� Cash�in�and�out�of�the�balance�of�cash�held�in�notes�and�coins�by�the�business�(normally�small).��This�is�often�controlled�using�the�imprest�system�(see�later).�

Typically,�small�expenses�(eg�Friday�cakes�for�staff!)�and�sundry�income.�

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 3 | 4 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

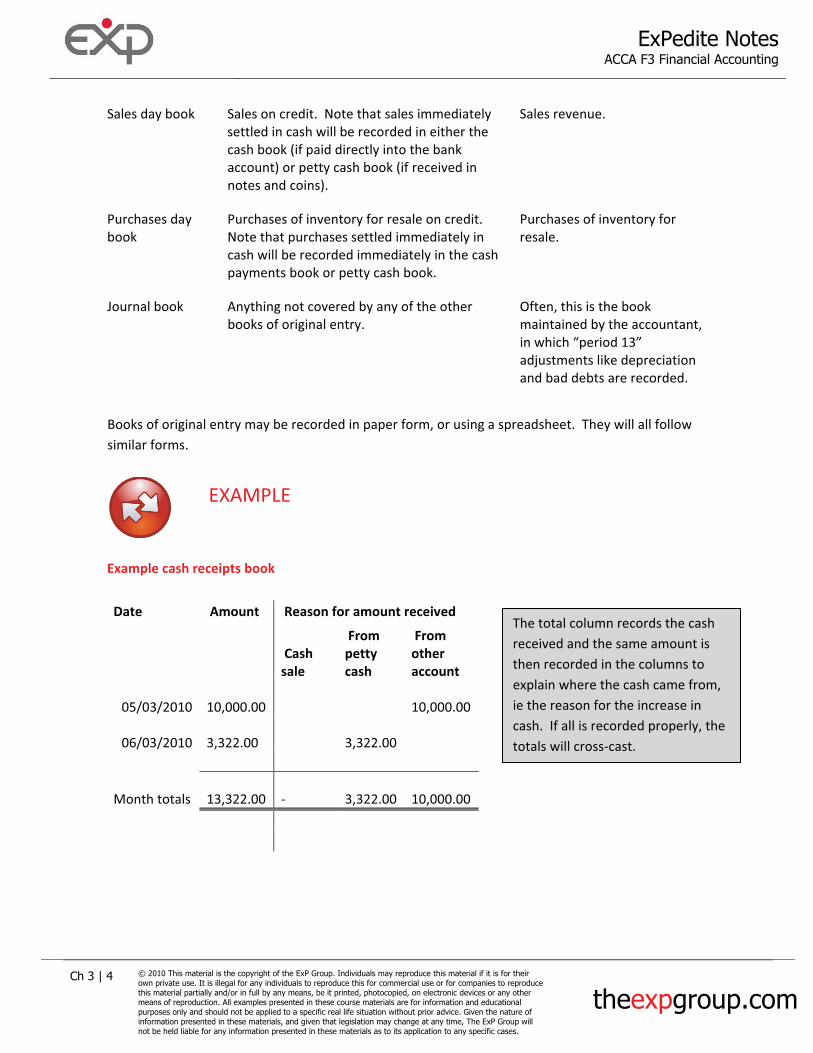

Sales�day�book� Sales�on�credit.��Note�that�sales�immediately�settled�in�cash�will�be�recorded�in�either�the�cash�book�(if�paid�directly�into�the�bank�account)�or�petty�cash�book�(if�received�in�notes�and�coins).�

Sales�revenue.�

Purchases�day�book�

Purchases�of�inventory�for�resale�on�credit.��Note�that�purchases�settled�immediately�in�cash�will�be�recorded�immediately�in�the�cash�payments�book�or�petty�cash�book.�

Purchases�of�inventory�for�resale.�

Journal�book� Anything�not�covered�by�any�of�the�other�books�of�original�entry.�

Often,�this�is�the�book�maintained�by�the�accountant,�in�which�“period�13”�adjustments�like�depreciation�and�bad�debts�are�recorded.�

�Books�of�original�entry�may�be�recorded�in�paper�form,�or�using�a�spreadsheet.��They�will�all�follow�similar�forms.��

�

EXAMPLE��

�Example�cash�receipts�book���Date� �Amount�� �Reason�for�amount�received��

�Cash�sale��

�From�petty�cash��

�From�other�account��

05/03/2010����10,000.00�� ��

���10,000.00�

06/03/2010������3,322.00�� ��

���3,322.00�

��

Month�totals����13,322.00��

��������������������

���3,322.00�

���10,000.00�

����

The�total�column�records�the�cash�received�and�the�same�amount�is�then�recorded�in�the�columns�to�explain�where�the�cash�came�from,�ie�the�reason�for�the�increase�in�cash.��If�all�is�recorded�properly,�the�totals�will�cross�cast.���

�����

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 3 | 5 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

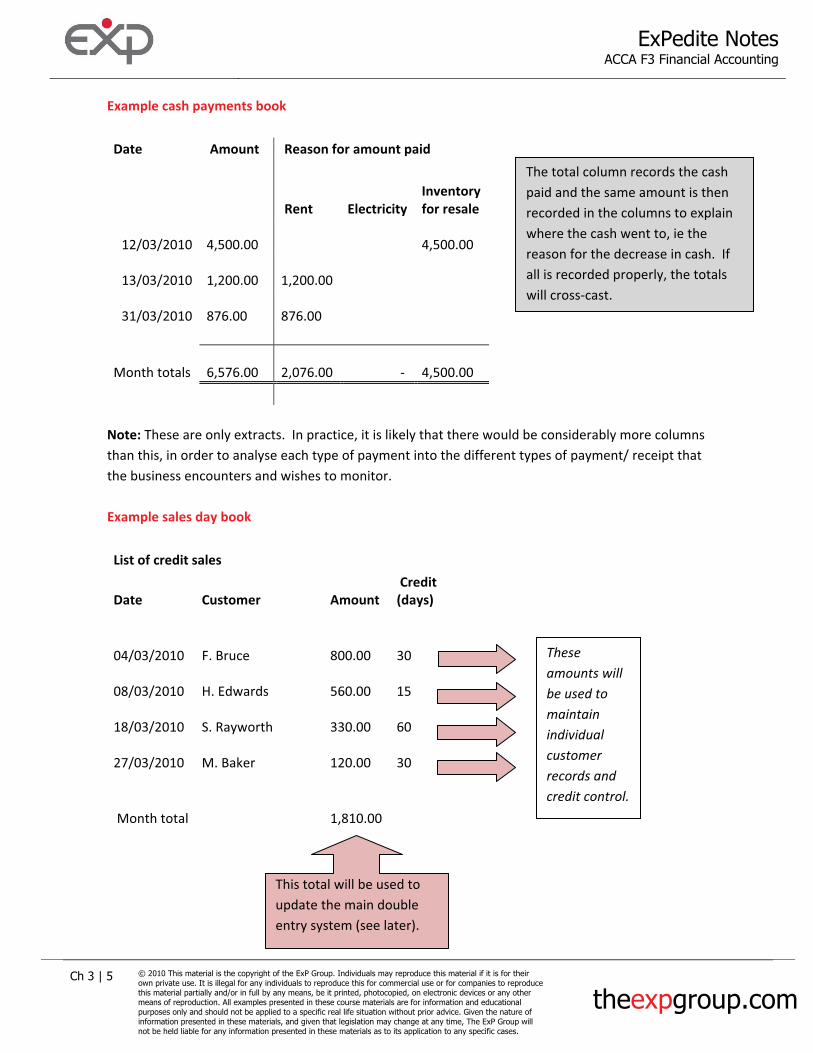

Example�cash�payments�book��Date� �Amount�� �Reason�for�amount�paid��

�Rent���Electricity�

�Inventory�for�resale�

12/03/2010������4,500.00�� ��

�����4,500.00��

13/03/2010������1,200.00��

���1,200.00��

31/03/2010����������876.00��

������876.00����

Month�totals������6,576.00��

���2,076.00�� ����������������� ��

�����4,500.00��

��

The�total�column�records�the�cash�paid�and�the�same�amount�is�then�recorded�in�the�columns�to�explain�where�the�cash�went�to,�ie�the�reason�for�the�decrease�in�cash.��If�all�is�recorded�properly,�the�totals�will�cross�cast.���

�Note:�These�are�only�extracts.��In�practice,�it�is�likely�that�there�would�be�considerably�more�columns�than�this,�in�order�to�analyse�each�type�of�payment�into�the�different�types�of�payment/�receipt�that�the�business�encounters�and�wishes�to�monitor.��Example�sales�day�book��List�of�credit�sales�

Date� �Customer���Amount�

�Credit�(days)��

04/03/2010� �F.�Bruce��������800.00��

��������������30��

08/03/2010� �H.�Edwards��������560.00��

��������������15��

18/03/2010� �S.�Rayworth��������330.00��

��������������60��

27/03/2010� �M.�Baker��������120.00��

��������������30��

�Month�total�����1,810.00�

These�amounts�will�be�used�to�maintain�individual�customer�records�and�credit�control.�

This�total�will�be�used�to�update�the�main�double�entry�system�(see�later).�

������

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 3 | 6 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

�

�

KEY�KNOWLEDGEComputerised�systems��

Computerised�systems�are�common�and�can�be�cheap.��They�still�require�rigorous�systems�for�data�capture�at�the�point�when�transactions�happen,�as�the�maxim�“garbage�in,�garbage�out”�very�much�applies!��Input�to�a�computerised�system�will�not�look�like�a�book�of�original�entry,�but�will�require�the�same�data.��Software�may�be�more�user�friendly,�for�example�asking�“how�much�cash�was�spent?”�and�“what�was�this�for?”,�whilst�then�offering�a�drop�down�menu�of�choices.��The�software�will�still�prepare�records�using�the�same�methodology�as�the�manual�recording�systems�above.��Advantages�of�using�a�computerised�system�include:�

� Back�ups�can�be�made�easily�� Makes�producing�periodic�frequent�accounts�much�less�laborious�than�a�manual�system�� Can�be�user�friendly�� Analyses�sales�taxes�more�easily�than�manual�systems�(see�later)�� Can�be�used�to�quickly�produce�lots�of�reports�such�as�VAT�returns�and�interim�management�

accounts.��Disadvantages�of�a�computerised�system�include:�

� Cost�� May�not�be�tailored�very�well�to�the�business�own�needs�� Still�requires�effective�data�capture�and�maintenance�of�the�underlying�records.�

��

�

KEY�KNOWLEDGEJournal�book��

The�journal�book�is�the�book�of�original�entry�that�captures�transactions�not�covered�by�other�books�of�original�entry.��Often,�it�includes�adjustments�and�correction�of�errors�and�omissions�in�the�other�books�of�original�entry.��In�a�computerised�system,�there�are�often�restrictions�on�who�can�access�the�journal�book.��The�journal�book�records�double�entry�records�(see�later),�with�an�explanation�of�the�reason.��We’ll�see�an�example�of�it�after�tackling�double�entry�bookkeeping.����

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 3 | 7 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

�

KEY�KNOWLEDGECredit�control�and�memorandum�accounts��

�In�parallel�with�(and�thus�duplication�of)�the�main�accounting�system,�it�is�likely�that�an�accounting�system�will�maintain�separate�records�of�individual�records�of�customer�and�supplier�balances.��This�duplicates�effort�and�increases�costs,�but�provides�useful�information�for�credit�control�and�a�check�on�the�accuracy�of�data�input.��Each�supplier�or�customer�will�have�a�supplier�or�customer�code�and�individual�record�of�transactions�with�them.��This�is�outside�the�general�ledger�(ie�double�entry�system)�and�in�a�simple�accounting�system�may�be�kept�using�a�simple�card�index�box.���

�EXAMPLE�

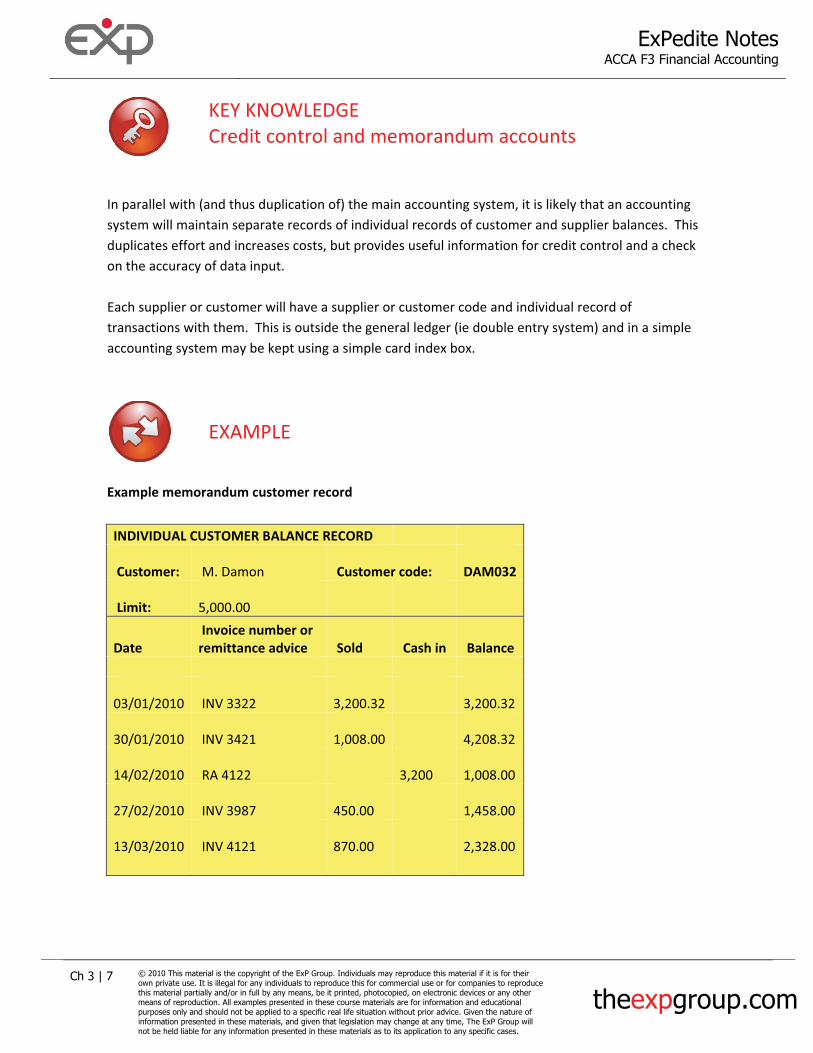

�Example�memorandum�customer�record��

INDIVIDUAL�CUSTOMER�BALANCE�RECORD�� �� ��

�Customer:��� �M.�Damon�� �Customer�code:���DAM032�

�Limit:��������������������������5,000.00�� �� �� ��

Date��Invoice�number�or�remittance�advice�� �Sold�� �Cash�in� �Balance�

�� �� �� �� ��

03/01/2010� �INV�3322�����3,200.32� ��

���3,200.32�

30/01/2010� �INV�3421�����1,008.00� ��

���4,208.32�

14/02/2010� �RA�4122�� ����������3,200��

���1,008.00�

27/02/2010� �INV�3987��������450.00�� ��

���1,458.00�

13/03/2010� �INV�4121��������870.00�� ��

���2,328.00�

�� �� �� �� ������

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 3 | 8 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

�Similar�(but�opposite!)�records�will�be�kept�for�balances�with�individual�suppliers.��The�purpose�of�a�credit�limit�is�to�reduce�credit�risk�to�within�tolerable�limits.��New�customers�are�likely�to�be�given�standard�low�credit�limits�and�will�need�to�build�up�a�record�of�prompt�payment�before�larger�credit�is�extended�to�them.��Sales�staff�should�be�required�to�check�that�any�proposed�sale�will�not�exceed�the�current�credit�limit�before�committing�the�company�to�making�the�sale�(or�requesting�that�the�credit�controller�increase�the�credit�limit).��This�information�will�also�allow�for�preparation�of�an�aged�debtors�analysis,�which�is�an�important�piece�of�information�in�deciding�an�appropriate�figure�for�an�allowance�for�doubtful�debts,�since�the�longer�a�debt�goes�unpaid,�the�greater�the�chance�that�it�will�not�be�recoverable�in�full.��Offering�credit�to�customers�increases�risk�of�non�payment�and�may�put�a�company’s�cash�flows�under�strain,�but�it�is�also�likely�to�generate�more�sales�than�a�business�that�refuses�credit�sales.����If�suppliers�provide�supplier�statements,�then�it�will�be�possible�for�accounts�staff�to�reconcile�the�balance�on�the�supplier�statement�with�the�balance�on�the�memorandum�supplier�account.��This�gives�further�comfort�that�the�accounting�system�contains�accurate�information.��Statements�may�be�sent�to�customers�from�the�memorandum�ledgers,�which�may�prompt�customers�into�paying�more�quickly�in�the�event�that�they�have�forgotten�a�payment�to�be�made.���

�

KEY�KNOWLEDGEControlling�petty�cash�–�the�imprest�system��

�Cash�balances�are�prone�to�error,�theft�and�poor�record�keeping.��A�way�to�ensure�that�any�cash�payments�out�of�the�petty�cash�box�are�recorded�is�to�use�the�imprest�system.��The�imprest�system�has�these�features:��The�cash�box�has�a�pre�set�limit�of�maximum�cash�that�it�ever�contains,�eg�$1,000�

� Before�any�cash�is�taken�out�of�the�cash�box�(which�should�be�guarded�by�a�very�diligent�and�ideally�slightly�frightening�person),�the�person�claiming�the�cash�must�provide�a�receipt�and�complete�an�expense�voucher.�

� As�an�expense�record�is�submitted,�the�same�amount�of�cash�is�taken�out�of�the�box.���� Under�no�circumstances�is�anybody�ever�allowed�to�take�money�out�of�the�tin�without�

completing�a�petty�cash�voucher.����

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 3 | 9 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

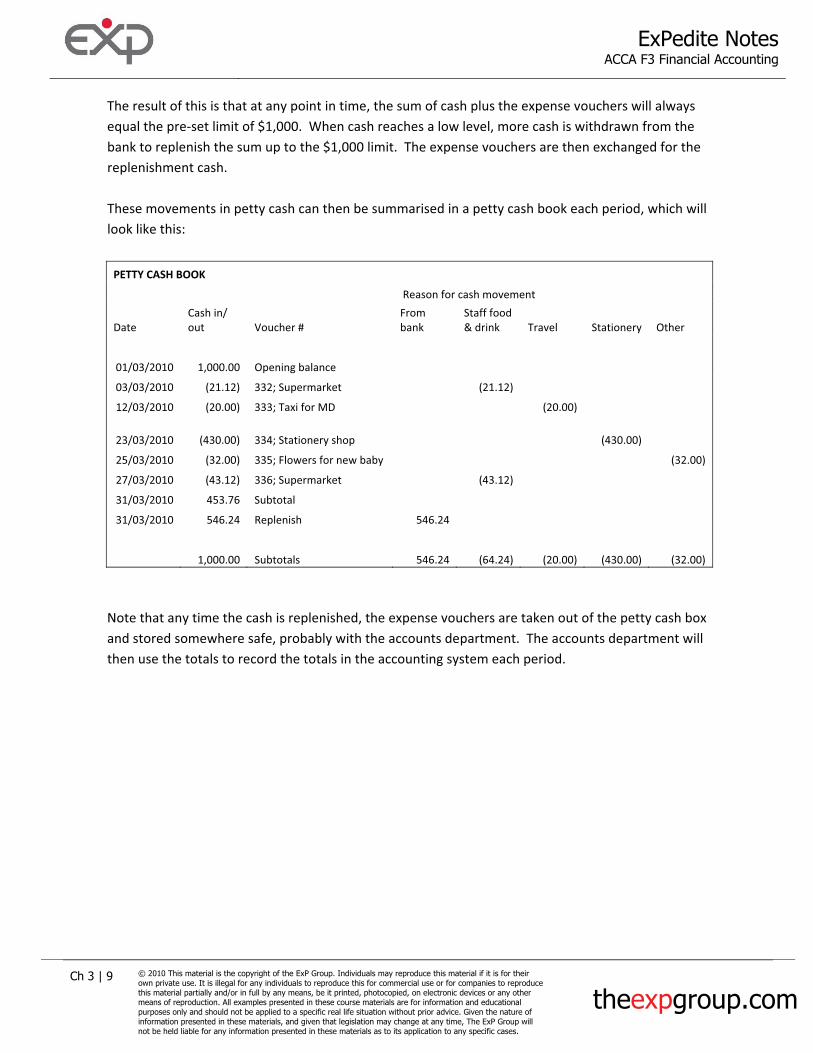

The�result�of�this�is�that�at�any�point�in�time,�the�sum�of�cash�plus�the�expense�vouchers�will�always�equal�the�pre�set�limit�of�$1,000.��When�cash�reaches�a�low�level,�more�cash�is�withdrawn�from�the�bank�to�replenish�the�sum�up�to�the�$1,000�limit.��The�expense�vouchers�are�then�exchanged�for�the�replenishment�cash.��These�movements�in�petty�cash�can�then�be�summarised�in�a�petty�cash�book�each�period,�which�will�look�like�this:��

PETTY�CASH�BOOK��

�Reason�for�cash�movement��

Date�Cash�in/�out� Voucher�#�

From�bank�

Staff�food�&�drink� Travel� Stationery� Other�

01/03/2010� 1,000.00� Opening�balance�

03/03/2010� (21.12)� 332;�Supermarket� (21.12)�

12/03/2010� (20.00)� 333;�Taxi�for�MD� (20.00)�

23/03/2010� (430.00)� 334;�Stationery�shop� (430.00)�

25/03/2010� (32.00)� 335;�Flowers�for�new�baby� (32.00)�

27/03/2010� (43.12)� 336;�Supermarket� (43.12)�

31/03/2010� 453.76� Subtotal�

31/03/2010� 546.24� Replenish� 546.24�

1,000.00� Subtotals� 546.24� (64.24)� (20.00)� (430.00)� (32.00)���Note�that�any�time�the�cash�is�replenished,�the�expense�vouchers�are�taken�out�of�the�petty�cash�box�and�stored�somewhere�safe,�probably�with�the�accounts�department.��The�accounts�department�will�then�use�the�totals�to�record�the�totals�in�the�accounting�system�each�period.����

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 4 | 1 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

Chapter�4�

Double�entry�bookkeeping:�the�debits�and�credits�

��

STARTThe Big Picture

�The�starting�point�for�double�entry�bookkeeping�is�to�think�about�assets�and�liabilities,�ie�net�assets.��If�there�is�a�change�in�an�asset,�there�must�be�an�explanation�for�why�it�changed.��

� If�you�win�the�lottery,�you�have�more�cash�because�you�have�lottery�income.�� If�you�buy�lunch,�you�have�less�cash�because�you�spent�money�on�lunch�(ie�more�

expenditure).�� If�you�decide�that�the�home�you�own�is�worth�more,�you�have�more�assets�because�you’ve�

recognised�a�revaluation�gain.��Many�textbooks�explain�double�entry�bookkeeping�in�the�framework�of�double�entry�meaning�that�for�each�transaction,�there�is�an�equal�and�opposite�transaction.��We�think�that�this�is�needlessly�confusing.��The�key�word�in�double�entry�is�because.���

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 4 | 2 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

�

�

KEY�KNOWLEDGESo�why�debits�and�credits?��

Imagine�that�we�call�assets�“debits”,�only�so�that�people�who�speak�different�languages�can�communicate�more�effectively�with�each�other.��If�we�now�say�that�we�have�an�asset,�or�more�of�an�asset�because�you’ve�been�paid�your�salary.��This�would�be�recorded�as�“recognise�new�or�increased�asset�of�cash”.��It’s�shorter�just�to�say�“debit�cash”.����There�must�be�a�reason�for�this�increase�in�cash.��The�reason�is�that�there’s�been�some�income.��This�can’t�be�a�debit,�as�what�we’re�trying�to�do�is�explain�where�the�debit�came�from.��The�explanation�is�arbitrarily�called�a�credit.��You�may�have�encountered�the�words�debit�and�credit�in�the�context�of�your�bank�statement.��This�brings�danger,�since�the�bank�statement�is�a�record�from�their�own�records.��This�means�that�it’s�upside�down.��This�can�cause�confusion,�so�it’s�best�for�the�moment�if�you�try�to�unlearn�everything�you’ve�ever�come�to�think�of�debits�and�credits�as�being.��The�truth�is�the�opposite�way�round�to�the�way�that�lay�people�use�the�terms.���

�

KEY�KNOWLEDGEBuilding�up�the�rules��

Here�are�the�core�concepts�that�you�need�to�be�happy�with:��

� An�asset,�or�an�increase�in�an�asset,�is�a�debit.�� The�opposite�of�an�asset�is�a�liability.��The�opposite�of�a�debit�is�a�credit.��So�a�liability�is�a�

credit.�� If�you�have�more�assets�(debit�assets),�the�explanation�will�be�to�credit�income.�

�So�you�may�have�started�to�think�“debits�good,�credits�bad”�or�even�the�other�way�round.��That’s�not�the�way�to�look�at�it.��Neither�is�good�or�bad.��A�debit�can�be�an�asset,�but�it�can�also�be�an�expense.��So�it’s�not�correct�to�think�of�one�being�good�and�the�other�bad.��It’s�simpler�than�that.��Here’s�a�table�to�summarise�the�rules.��Review�this�and�then�try�to�produce�is�yourself,�using�the�logic�of�explaining�movements�in�net�assets�and�things�being�opposites�(eg�a�liability�is�a�credit�because�an�asset�is�a�debit).����� �

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 4 | 3 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

It�will�take�a�while�to�become�familiar�with�this�system,�just�the�way�that�it�takes�a�while�to�become�familiar�with�riding�a�bicycle.��Don’t�panic�–�it�comes�and�don’t�feel�pressured�to�rush�it.��There’s�not�much�intrinsically�to�actually�understand�here�–�it’s�just�a�task�and�a�system�that�becomes�really�easy�with�repetition.����

Debits�mean� Credits�mean�

What�happens�to�net�assets:�

An�increase�in�assets� A�decrease�in�assets�

An�increase�in�liabilities� An�increase�in�liabilities�

�

And�the�reason�for�that�increase�in�net�assets:�

An�item�of�expenditure� An�item�of�income�

�

�If�you’re�asked�to�record�a�transaction,�the�first�step�is�to�identify�what�assets�and/�or�liabilities�are�in�question.��Decide�one�of�these�first�(it’s�often�easiest�at�first�to�start�with�cash�if�it’s�a�cash�transaction)�and�decide�if�this�is�a�debit�or�a�credit.��Then�work�out�the�explanation�why.��If�you�think�that�there’s�a�new�liability,�that�must�be�a�credit�to�liabilities.��That�means�that�the�explanation�must�be�a�debit,�which�could�be�either�an�asset�(eg�if�you’ve�just�got�some�cash�in�your�hand�because�you�borrowed�it),�or�an�expense�(eg�if�you�just�bought�dinner�on�your�credit�card).��

�REVIEW�AND�SELF�TEST�1�

Determine�what�the�debits�and�credits�would�be�in�these�situations:��

1. You�receive�your�net�salary�of�$2,000�into�your�bank�account.�2. You�withdraw�$100�at�an�ATM.�3. You�spend�$10�on�lunch.�4. You�give�$2�to�a�beggar�in�the�street.�5. You�find�that�you�had�the�other�$8�taken�from�your�pocket�stolen.�6. You�go�online�and�buy�a�HD�camcorder�for�$800�using�your�credit�card.�7. You�find�the�$8�that�you�thought�you’d�lost�in�another�pocket�in�your�jacket.�8. Your�brother�repays�you�the�$120�that�he�borrowed�from�you�interest�free�last�week.�9. You�borrow�$100,000�from�a�bank�to�buy�your�home.�10. You�pay�the�$100,000�to�buy�your�home;�$99,000�to�the�seller�and�$1,000�to�the�lawyer�who�

administered�the�transaction�for�you.�

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 4 | 4 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

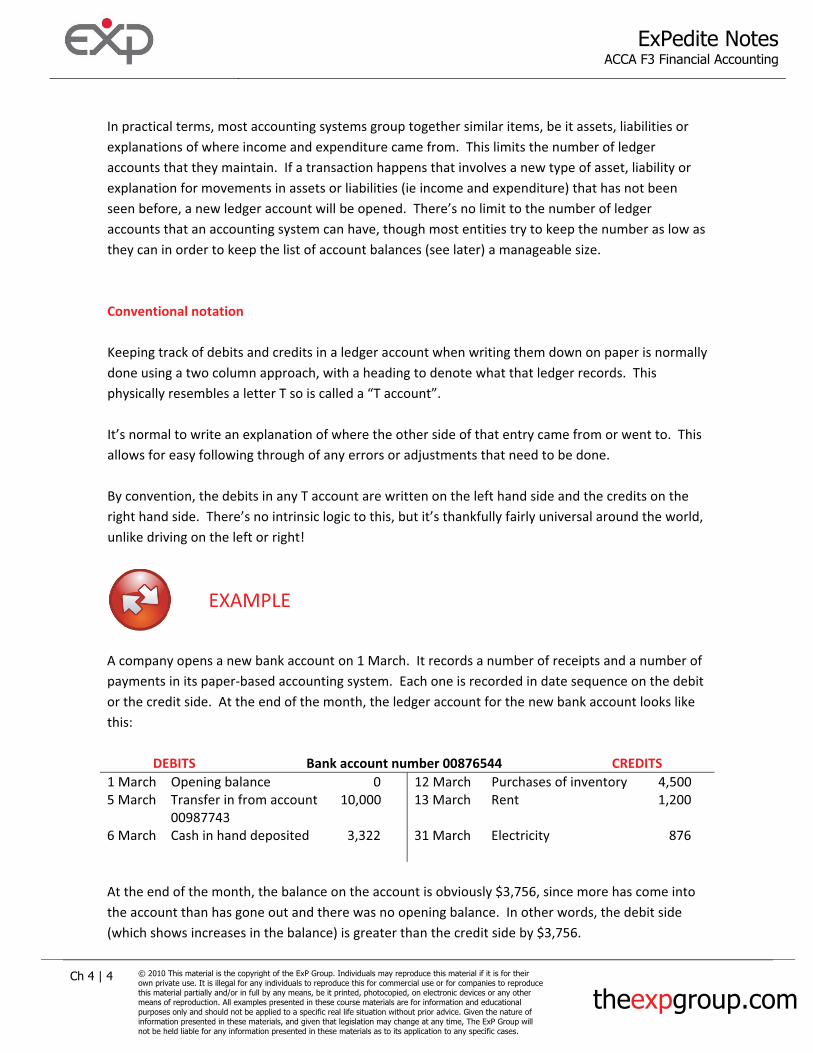

�In�practical�terms,�most�accounting�systems�group�together�similar�items,�be�it�assets,�liabilities�or�explanations�of�where�income�and�expenditure�came�from.��This�limits�the�number�of�ledger�accounts�that�they�maintain.��If�a�transaction�happens�that�involves�a�new�type�of�asset,�liability�or�explanation�for�movements�in�assets�or�liabilities�(ie�income�and�expenditure)�that�has�not�been�seen�before,�a�new�ledger�account�will�be�opened.��There’s�no�limit�to�the�number�of�ledger�accounts�that�an�accounting�system�can�have,�though�most�entities�try�to�keep�the�number�as�low�as�they�can�in�order�to�keep�the�list�of�account�balances�(see�later)�a�manageable�size.���Conventional�notation��Keeping�track�of�debits�and�credits�in�a�ledger�account�when�writing�them�down�on�paper�is�normally�done�using�a�two�column�approach,�with�a�heading�to�denote�what�that�ledger�records.��This�physically�resembles�a�letter�T�so�is�called�a�“T�account”.����It’s�normal�to�write�an�explanation�of�where�the�other�side�of�that�entry�came�from�or�went�to.��This�allows�for�easy�following�through�of�any�errors�or�adjustments�that�need�to�be�done.��By�convention,�the�debits�in�any�T�account�are�written�on�the�left�hand�side�and�the�credits�on�the�right�hand�side.��There’s�no�intrinsic�logic�to�this,�but�it’s�thankfully�fairly�universal�around�the�world,�unlike�driving�on�the�left�or�right!����

�EXAMPLE�

�A�company�opens�a�new�bank�account�on�1�March.��It�records�a�number�of�receipts�and�a�number�of�payments�in�its�paper�based�accounting�system.��Each�one�is�recorded�in�date�sequence�on�the�debit�or�the�credit�side.��At�the�end�of�the�month,�the�ledger�account�for�the�new�bank�account�looks�like�this:��

DEBITS� Bank�account�number�00876544� CREDITS�1�March� Opening�balance� 0� 12�March� Purchases�of�inventory� 4,500�5�March� Transfer�in�from�account�

00987743�10,000� 13�March� Rent� 1,200�

6�March� Cash�in�hand�deposited� 3,322� 31�March� Electricity� 876�� � � � � ��At�the�end�of�the�month,�the�balance�on�the�account�is�obviously�$3,756,�since�more�has�come�into�the�account�than�has�gone�out�and�there�was�no�opening�balance.��In�other�words,�the�debit�side�(which�shows�increases�in�the�balance)�is�greater�than�the�credit�side�by�$3,756.�

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 4 | 5 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

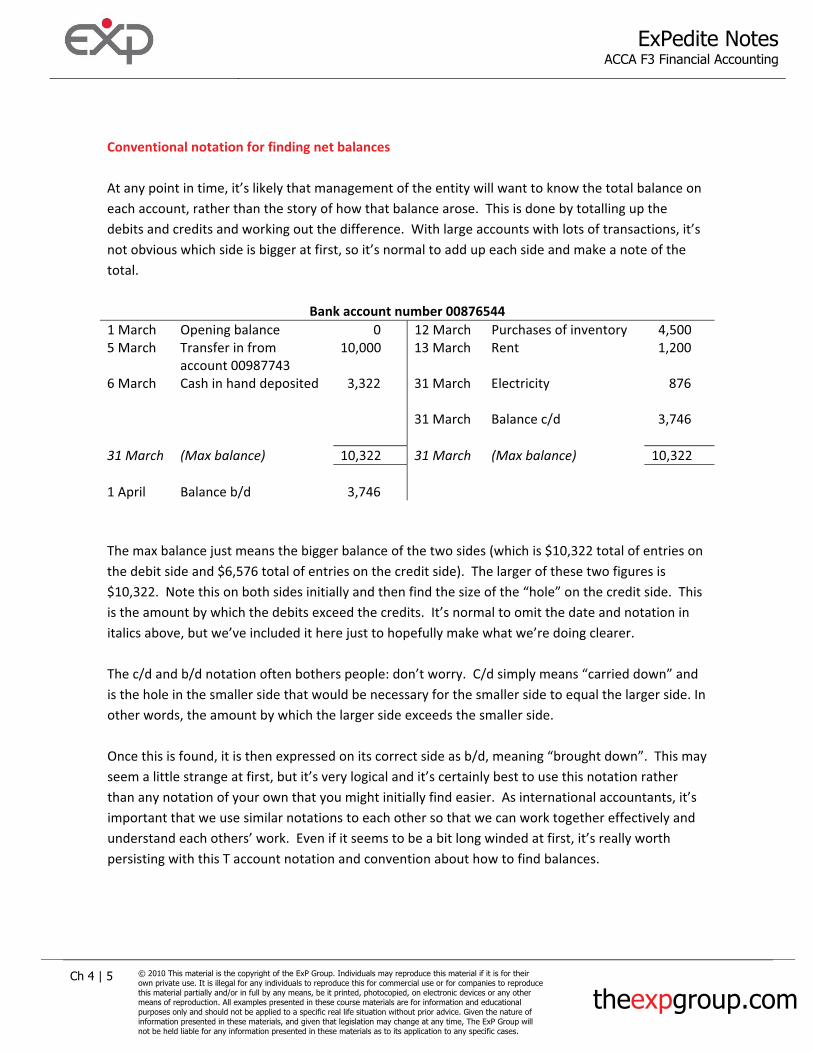

��Conventional�notation�for�finding�net�balances��At�any�point�in�time,�it’s�likely�that�management�of�the�entity�will�want�to�know�the�total�balance�on�each�account,�rather�than�the�story�of�how�that�balance�arose.��This�is�done�by�totalling�up�the�debits�and�credits�and�working�out�the�difference.��With�large�accounts�with�lots�of�transactions,�it’s�not�obvious�which�side�is�bigger�at�first,�so�it’s�normal�to�add�up�each�side�and�make�a�note�of�the�total.����

Bank�account�number�00876544�1�March� Opening�balance� 0� 12�March� Purchases�of�inventory� 4,500�5�March� Transfer�in�from�

account�00987743�10,000� 13�March� Rent� 1,200�

6�March� Cash�in�hand�deposited� 3,322� 31�March� Electricity� 876�� � � � � �� � � 31�March� Balance�c/d� 3,746�� � � � � �31�March�� (Max�balance)� 10,322� 31�March� (Max�balance)� 10,322�� � � � � �1�April� Balance�b/d� 3,746� � � ���The�max�balance�just�means�the�bigger�balance�of�the�two�sides�(which�is�$10,322�total�of�entries�on�the�debit�side�and�$6,576�total�of�entries�on�the�credit�side).��The�larger�of�these�two�figures�is�$10,322.��Note�this�on�both�sides�initially�and�then�find�the�size�of�the�“hole”�on�the�credit�side.��This�is�the�amount�by�which�the�debits�exceed�the�credits.��It’s�normal�to�omit�the�date�and�notation�in�italics�above,�but�we’ve�included�it�here�just�to�hopefully�make�what�we’re�doing�clearer.��The�c/d�and�b/d�notation�often�bothers�people:�don’t�worry.��C/d�simply�means�“carried�down”�and�is�the�hole�in�the�smaller�side�that�would�be�necessary�for�the�smaller�side�to�equal�the�larger�side.�In�other�words,�the�amount�by�which�the�larger�side�exceeds�the�smaller�side.��Once�this�is�found,�it�is�then�expressed�on�its�correct�side�as�b/d,�meaning�“brought�down”.��This�may�seem�a�little�strange�at�first,�but�it’s�very�logical�and�it’s�certainly�best�to�use�this�notation�rather�than�any�notation�of�your�own�that�you�might�initially�find�easier.��As�international�accountants,�it’s�important�that�we�use�similar�notations�to�each�other�so�that�we�can�work�together�effectively�and�understand�each�others’�work.��Even�if�it�seems�to�be�a�bit�long�winded�at�first,�it’s�really�worth�persisting�with�this�T�account�notation�and�convention�about�how�to�find�balances.���

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 4 | 6 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

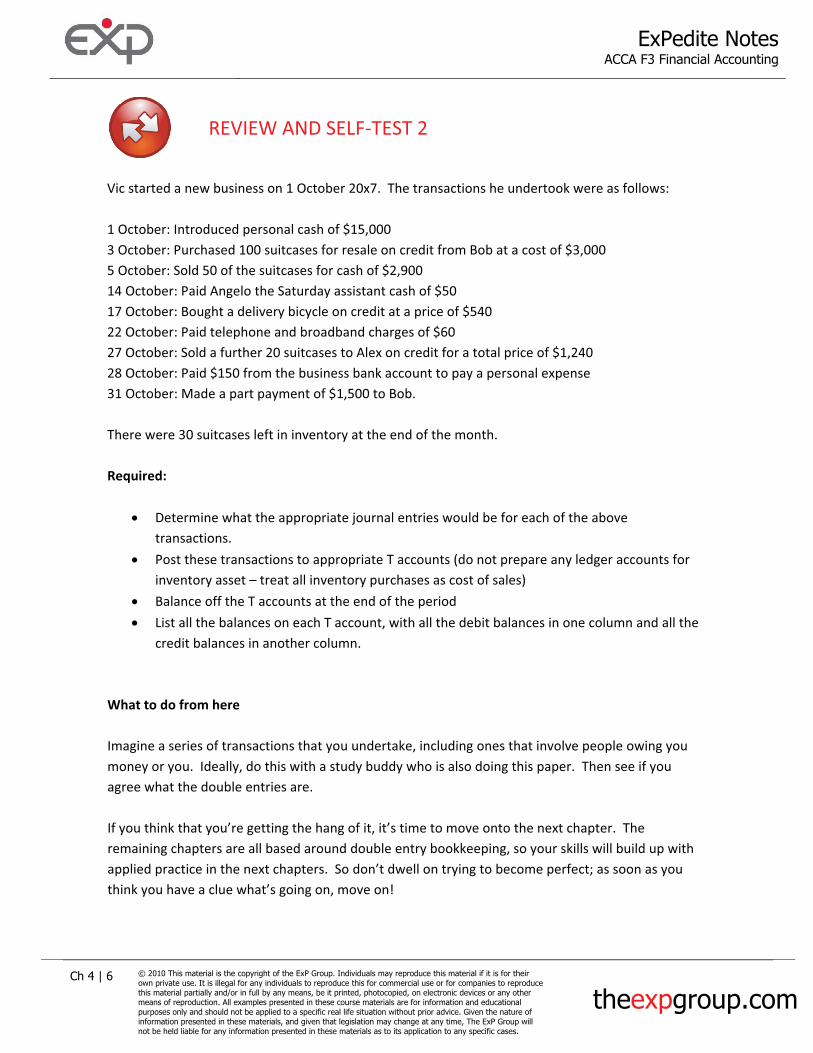

�REVIEW�AND�SELF�TEST�2�

�Vic�started�a�new�business�on�1�October�20x7.��The�transactions�he�undertook�were�as�follows:��1�October:�Introduced�personal�cash�of�$15,000�3�October:�Purchased�100�suitcases�for�resale�on�credit�from�Bob�at�a�cost�of�$3,000�5�October:�Sold�50�of�the�suitcases�for�cash�of�$2,900�14�October:�Paid�Angelo�the�Saturday�assistant�cash�of�$50�17�October:�Bought�a�delivery�bicycle�on�credit�at�a�price�of�$540�22�October:�Paid�telephone�and�broadband�charges�of�$60�27�October:�Sold�a�further�20�suitcases�to�Alex�on�credit�for�a�total�price�of�$1,240�28�October:�Paid�$150�from�the�business�bank�account�to�pay�a�personal�expense�31�October:�Made�a�part�payment�of�$1,500�to�Bob.��There�were�30�suitcases�left�in�inventory�at�the�end�of�the�month.��Required:��

� Determine�what�the�appropriate�journal�entries�would�be�for�each�of�the�above�transactions.�

� Post�these�transactions�to�appropriate�T�accounts�(do�not�prepare�any�ledger�accounts�for�inventory�asset�–�treat�all�inventory�purchases�as�cost�of�sales)�

� Balance�off�the�T�accounts�at�the�end�of�the�period�� List�all�the�balances�on�each�T�account,�with�all�the�debit�balances�in�one�column�and�all�the�

credit�balances�in�another�column.���What�to�do�from�here��Imagine�a�series�of�transactions�that�you�undertake,�including�ones�that�involve�people�owing�you�money�or�you.��Ideally,�do�this�with�a�study�buddy�who�is�also�doing�this�paper.��Then�see�if�you�agree�what�the�double�entries�are.��If�you�think�that�you’re�getting�the�hang�of�it,�it’s�time�to�move�onto�the�next�chapter.��The�remaining�chapters�are�all�based�around�double�entry�bookkeeping,�so�your�skills�will�build�up�with�applied�practice�in�the�next�chapters.��So�don’t�dwell�on�trying�to�become�perfect;�as�soon�as�you�think�you�have�a�clue�what’s�going�on,�move�on!���

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 4 | 7 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

theexpgroup.com

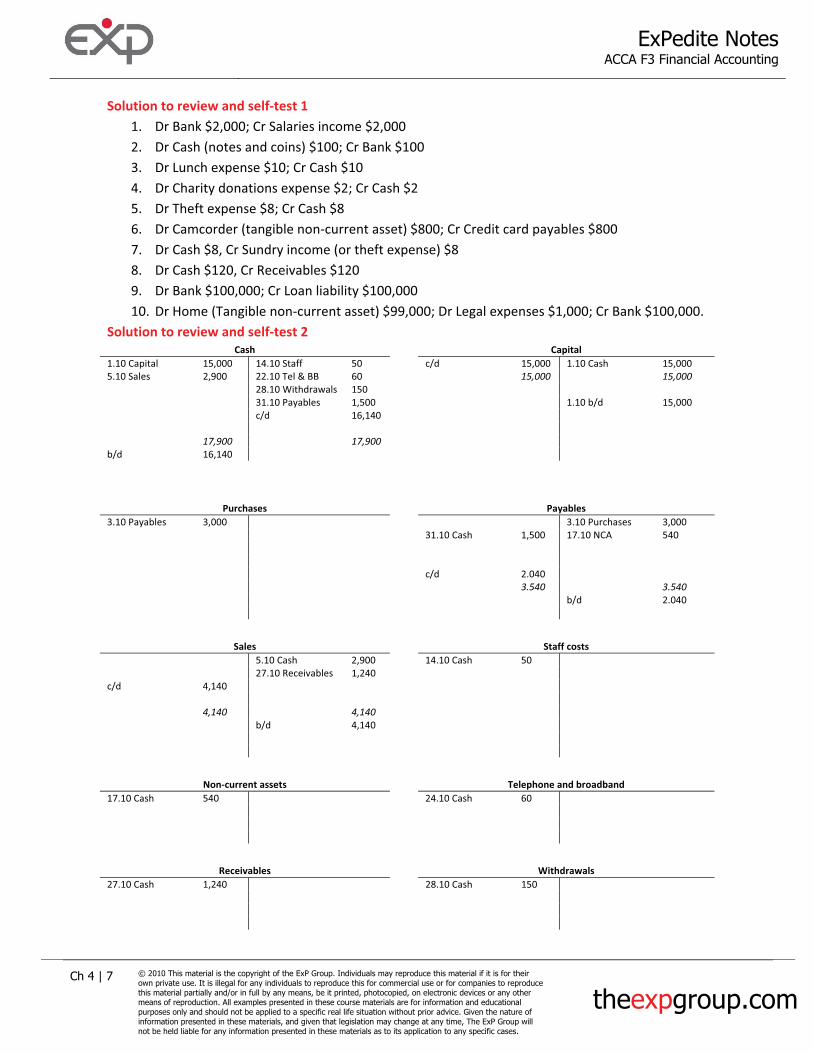

Solution�to�review�and�self�test�1�1. Dr�Bank�$2,000;�Cr�Salaries�income�$2,000�2. Dr�Cash�(notes�and�coins)�$100;�Cr�Bank�$100�3. Dr�Lunch�expense�$10;�Cr�Cash�$10�4. Dr�Charity�donations�expense�$2;�Cr�Cash�$2�5. Dr�Theft�expense�$8;�Cr�Cash�$8�6. Dr�Camcorder�(tangible�non�current�asset)�$800;�Cr�Credit�card�payables�$800�7. Dr�Cash�$8,�Cr�Sundry�income�(or�theft�expense)�$8�8. Dr�Cash�$120,�Cr�Receivables�$120�9. Dr�Bank�$100,000;�Cr�Loan�liability�$100,000�10. Dr�Home�(Tangible�non�current�asset)�$99,000;�Dr�Legal�expenses�$1,000;�Cr�Bank�$100,000.�

Solution�to�review�and�self�test�2�Cash Capital�

1.10�Capital� 15,000� 14.10�Staff�� 50 c/d 15,000 1.10�Cash� � 15,0005.10�Sales� � 2,900� 22.10�Tel�&�BB� 60 15,000 � 15,000� 28.10�Withdrawals� 150� 31.10�Payables� 1,500 1.10�b/d� � 15,000� c/d� � 16,140�� � 17,900� � 17,900b/d� � 16,140�

��

Purchases� Payables�3.10�Payables� 3,000� 3.10�Purchases� 3,000� 31.10�Cash� 1,500 17.10�NCA�� 540��� c/d 2.040� 3.540 � 3.540� b/d� � 2.040�

�Sales Staff�costs�

� 5.10�Cash� � 2,900 14.10�Cash 50� 27.10�Receivables� 1,240c/d� � 4,140��� � 4,140� � 4,140� b/d� � 4,140��

�Non�current�assets� Telephone�and�broadband�

17.10�Cash�� 540� 24.10�Cash 60���

�Receivables� Withdrawals�

27.10�Cash�� 1,240�� 28.10�Cash� 150���

�

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 5 | 1 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

Chapter�5�

Tangible�non�current�assets

�

STARTThe Big Picture

�An�asset�is�a�resource�controlled�by�an�entity�that�is�expected�to�give�inflow�of�benefits.��Many�assets�will�have�a�period�of�expected�benefit�over�more�than�one�period.��These�are�non�current�assets.���

�REVIEW�AND�SELF�TEST�1�

�Suggest�four�examples�of�tangible�non�current�assets�and�four�examples�of�current�assets�that�you�would�expect�to�find�in�a�business.�������

theexpgroup.com

�

ExPedite NotesACCA F3 Financial Accounting

�

Ch 5 | 2 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

� �

�

KEY�KNOWLEDGECapital�and�revenue�expenditure��

�In�slang�terms,�capital�expenditure�means�any�cash�paid�to�acquire�assets�that�will�result�in�the�acquisition�of�a�new�asset,�or�an�increase�in�the�earning�capacity�of�an�existing�asset.��Revenue�expenditure�means�money�paid�to�maintain�the�existing�earning�capacity�of�an�existing�asset.��The�terminology�is�very�confusing�here,�since�it�has�nothing�to�do�with�share�capital/�equity�or�sales�revenue!��They�are�commonly�used�terms,�however�inaccurately.���

�REVIEW�AND�SELF�TEST�2�

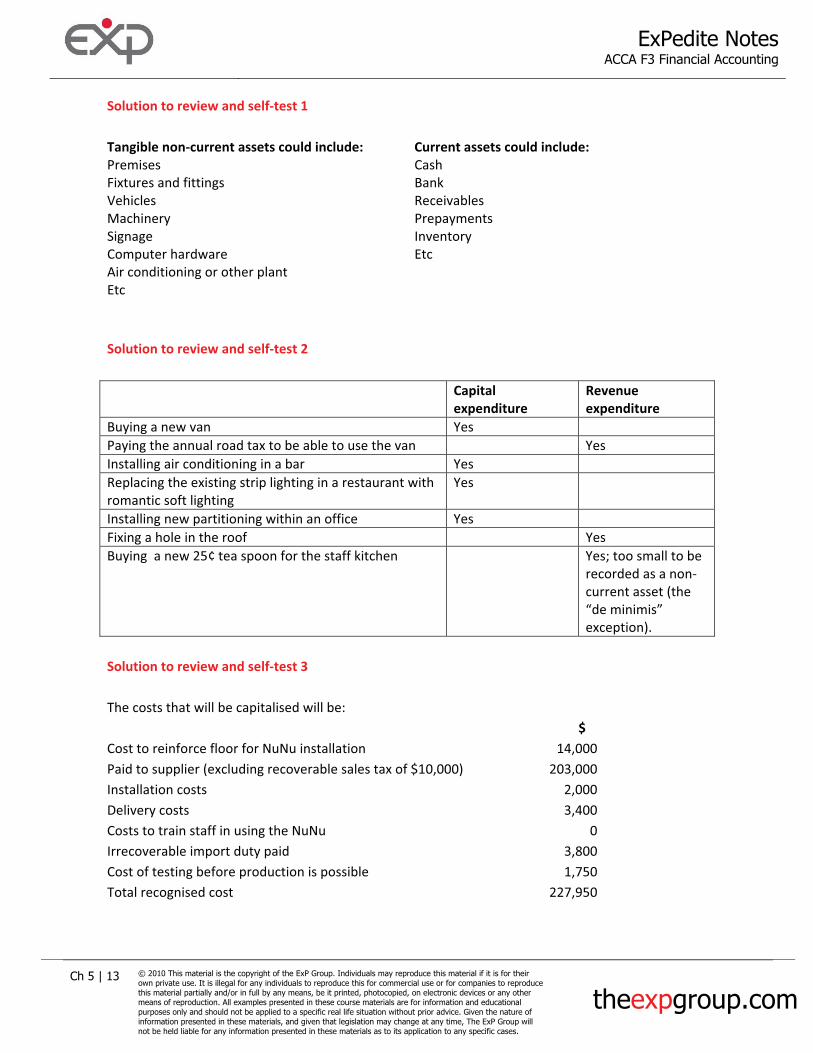

�Classify�each�of�the�transactions�below�as�capital�or�revenue�expenditure�and�explain�your�choice�of�classification.��� Capital�

expenditure�Revenue�expenditure�

Buying�a�new�van� � �Paying�the�annual�road�tax�to�be�able�to�use�the�van� � �Installing�air�conditioning�in�a�bar� � �Replacing�the�existing�strip�lighting�in�a�restaurant�with�romantic�soft�lighting�

� �

Installing�new�partitioning�within�an�office� � �Fixing�a�hole�in�the�roof� � �Buying��a�new�25¢�tea�spoon�for�the�staff�kitchen� � ���

�