acca f3 revision notes opentuition.pdf

TRANSCRIPT

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

ACCOUNTING CONCEPTS

Fundamental AssumptionsFair presentation

Going concern

Accruals

Consistency

Materiality / Aggregation

Faithful representation

Substance over form

Neutrality

Prudence

Completeness

Comparability

Understandability

Separate entity

Money measurement

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

BASES OF VALUATION

Historic cost

Replacement cost

Net realisable value

Economic value

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

IAS 8: ACCOUNTING POLICIES, ChANGES IN ACCOUNTING ESTImATES ANd ErrOrS

1. Changes in accounting policy should only be made if required by a standard, or if the change will result in a more appropriate presentation

2. The change should be applied retrospectively (unless not practical).

Adjustments in respect of previous periods should be made to the opening balance of retained earnings, and to comparative figures.

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

IAS 2: INVENTOrIES

1. Value at lower of cost and net realisable value

2. Measurement of costs:

• actual cost

• standard cost

• retail method

• FIFO

• average cost

3. If we produce our own goods, the inventory is valued at the full cost of production. ie including all factory overheads.

But, do not include any non-production costs (selling and administrative costs)

4. (Not in IAS 2, but remember) If we reduce closing inventory, then the profit for the year will reduce. (However, Opening Inventory of next year will reduce, so next years profit will increase)

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

IAS 38 - rESEArCh & dEVELOPmENT

research: searching for new knowledge / searching for new product

development: developing an idea into a new product

Treatment:

Research must be written off in the year of expenditure in the income statement.

Development expenditure must be written off in the year of expenditure, unless:• clearly defined product

• expenditure is measurable

• market exists for the product

• adequate resources exist

in which case, expenditure must be capitalised as non-current asset, and amortised (depreciated).

(Note: tangible non-current assets involved in research & development (e.g. research building) treated as normal non-current assets - capitalised and depreciated over expected useful life)

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

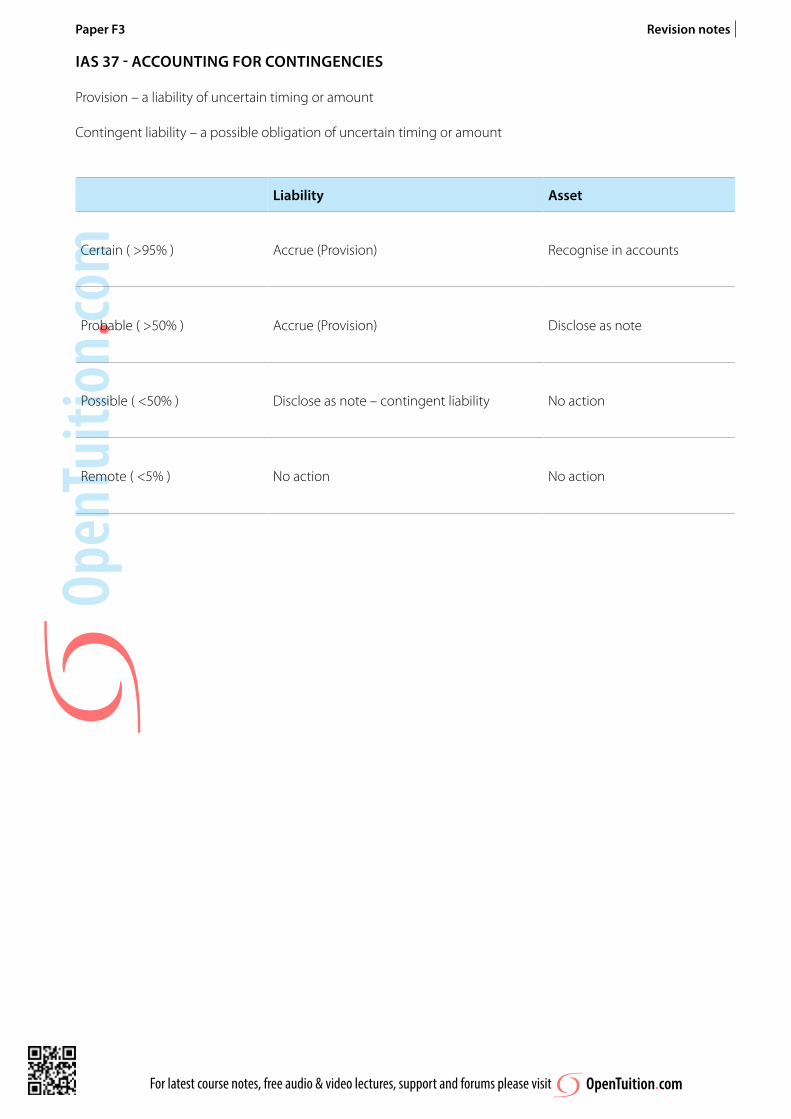

IAS 37 - ACCOUNTING FOr CONTINGENCIES

Provision – a liability of uncertain timing or amount

Contingent liability – a possible obligation of uncertain timing or amount

Liability Asset

Certain ( >95% ) Accrue (Provision) Recognise in accounts

Probable ( >50% ) Accrue (Provision) Disclose as note

Possible ( <50% ) Disclose as note – contingent liability No action

Remote ( <5% ) No action No action

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

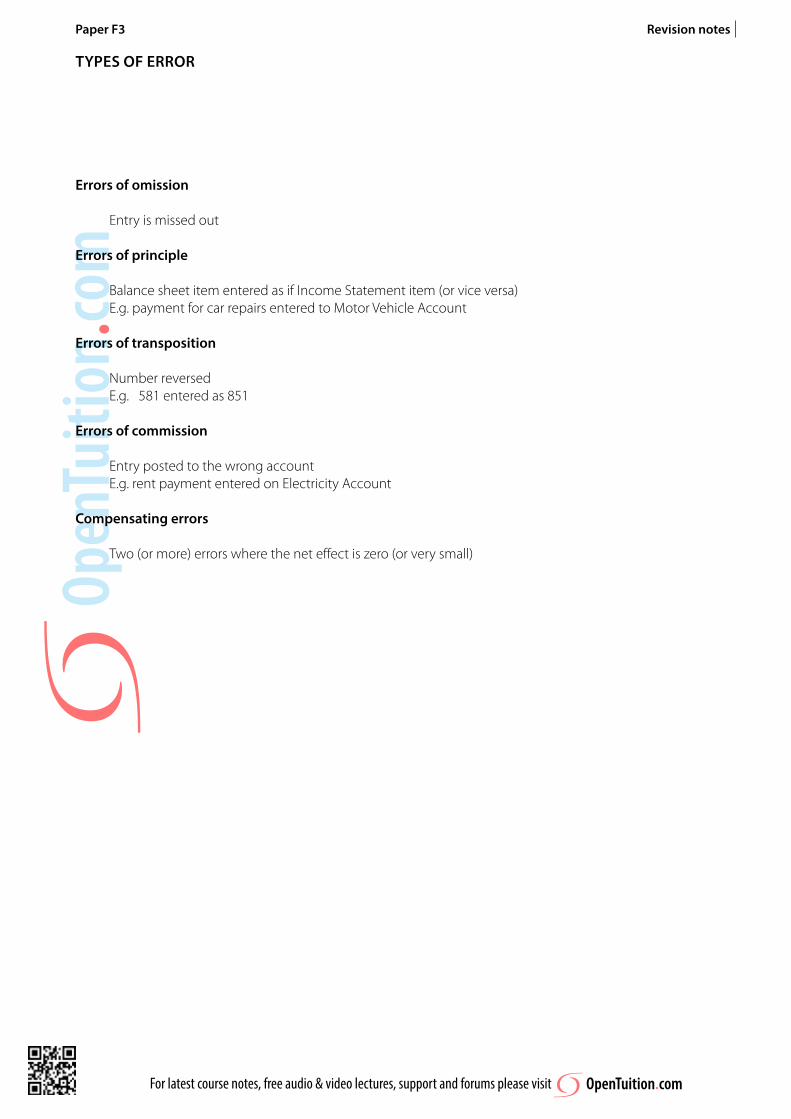

TYPES OF ErrOr

Errors of omission

Entry is missed out

Errors of principle

Balance sheet item entered as if Income Statement item (or vice versa) E.g. payment for car repairs entered to Motor Vehicle Account

Errors of transposition

Number reversed E.g. 581 entered as 851

Errors of commission

Entry posted to the wrong account E.g. rent payment entered on Electricity Account

Compensating errors

Two (or more) errors where the net effect is zero (or very small)

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

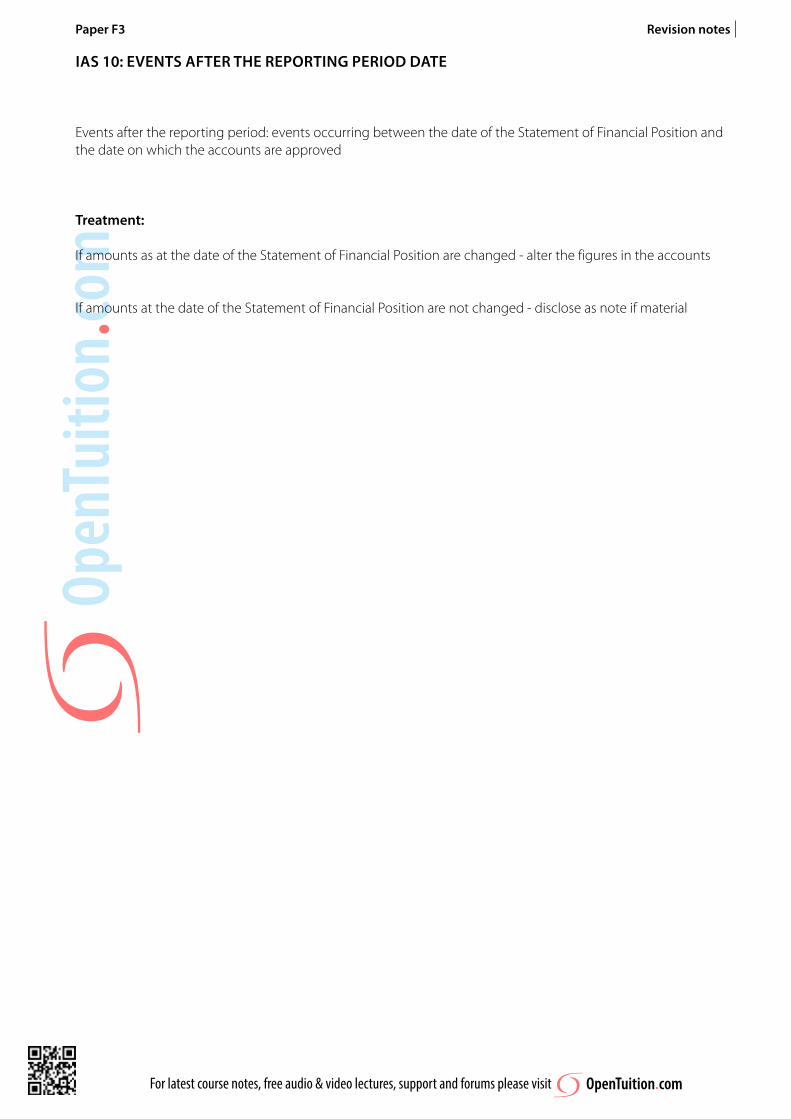

IAS 10: EVENTS AFTEr ThE rEPOrTING PErIOd dATE

Events after the reporting period: events occurring between the date of the Statement of Financial Position and the date on which the accounts are approved

Treatment:

If amounts as at the date of the Statement of Financial Position are changed - alter the figures in the accounts

If amounts at the date of the Statement of Financial Position are not changed - disclose as note if material

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

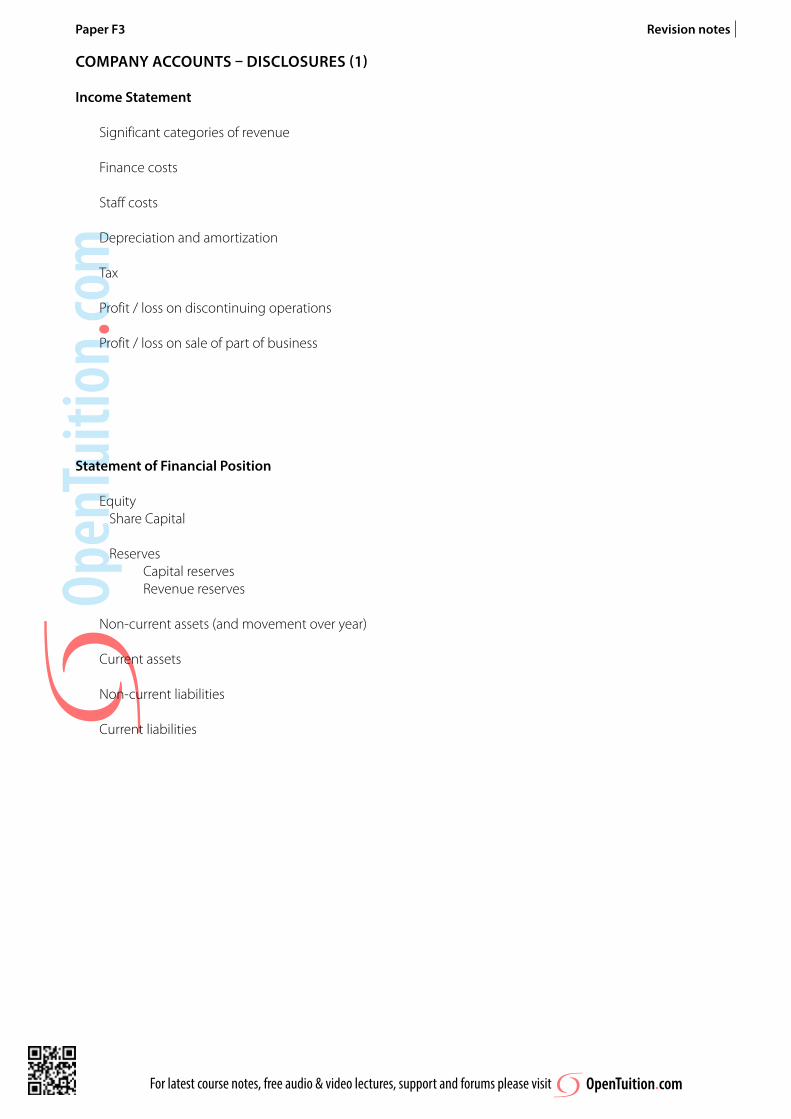

COmPANY ACCOUNTS – dISCLOSUrES (1)

Income Statement

Significant categories of revenue

Finance costs

Staff costs

Depreciation and amortization

Tax

Profit / loss on discontinuing operations

Profit / loss on sale of part of business

Statement of Financial Position

Equity Share Capital

Reserves Capital reserves Revenue reserves

Non-current assets (and movement over year)

Current assets

Non-current liabilities

Current liabilities

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

COmPANY ACCOUNTS – dISCLOSUrES (2)

Statement of changes in equity

Profit / loss for the year

Proceeds of issue of shares

Profit on revaluation

Dividends

Prior year adjustments

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

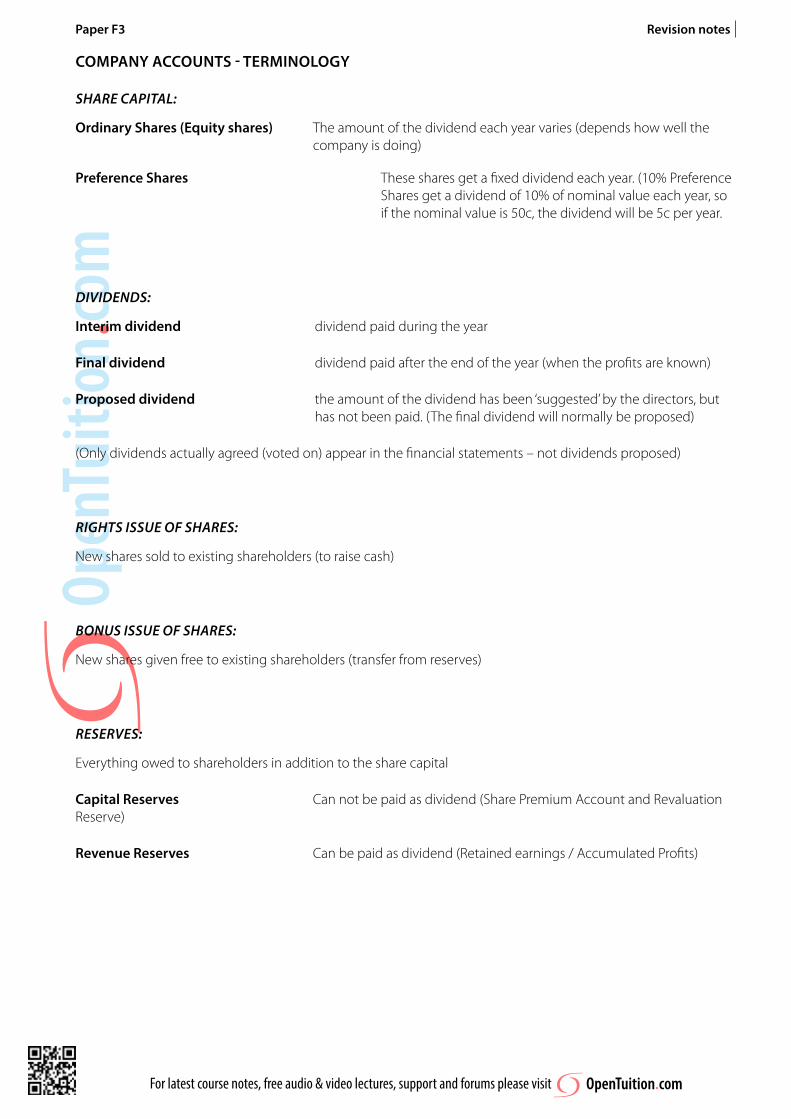

COmPANY ACCOUNTS - TErmINOLOGY

Share capital:

Ordinary Shares (Equity shares) The amount of the dividend each year varies (depends how well the company is doing)

Preference Shares These shares get a fixed dividend each year. (10% Preference Shares get a dividend of 10% of nominal value each year, so if the nominal value is 50c, the dividend will be 5c per year.

DiviDenDS:

Interim dividend dividend paid during the year

Final dividend dividend paid after the end of the year (when the profits are known)

Proposed dividend the amount of the dividend has been ‘suggested’ by the directors, but has not been paid. (The final dividend will normally be proposed)

(Only dividends actually agreed (voted on) appear in the financial statements – not dividends proposed)

rightS iSSue of ShareS:

New shares sold to existing shareholders (to raise cash)

BonuS iSSue of ShareS:

New shares given free to existing shareholders (transfer from reserves)

reServeS:

Everything owed to shareholders in addition to the share capital

Capital reserves Can not be paid as dividend (Share Premium Account and Revaluation Reserve)

revenue reserves Can be paid as dividend (Retained earnings / Accumulated Profits)

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

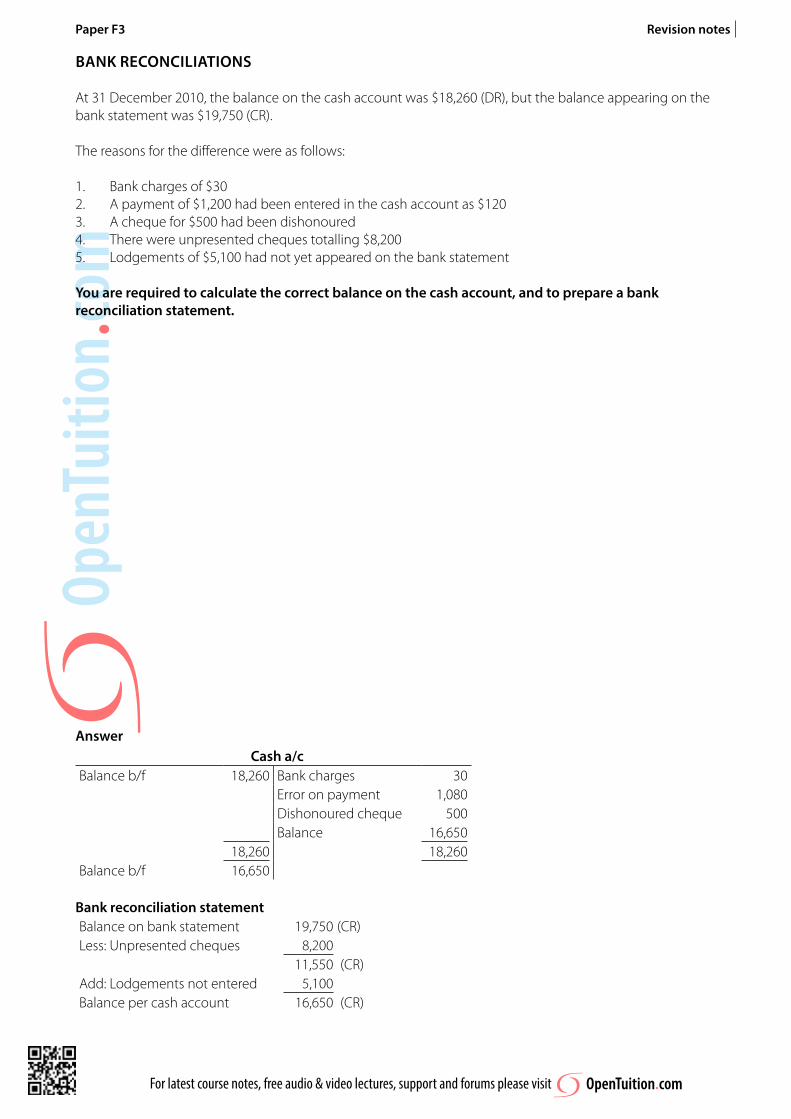

BANK rECONCILIATIONS

At 31 December 2010, the balance on the cash account was $18,260 (DR), but the balance appearing on the bank statement was $19,750 (CR).

The reasons for the difference were as follows:

1. Bank charges of $302. A payment of $1,200 had been entered in the cash account as $1203. A cheque for $500 had been dishonoured4. There were unpresented cheques totalling $8,2005. Lodgements of $5,100 had not yet appeared on the bank statement

You are required to calculate the correct balance on the cash account, and to prepare a bank reconciliation statement.

AnswerCash a/c

Balance b/f 18,260 Bank charges 30Error on payment 1,080Dishonoured cheque 500

Balance 16,65018,260 18,260

Balance b/f 16,650

Bank reconciliation statementBalance on bank statement 19,750 (CR)Less: Unpresented cheques 8,200

11,550 (CR)Add: Lodgements not entered 5,100Balance per cash account 16,650 (CR)

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

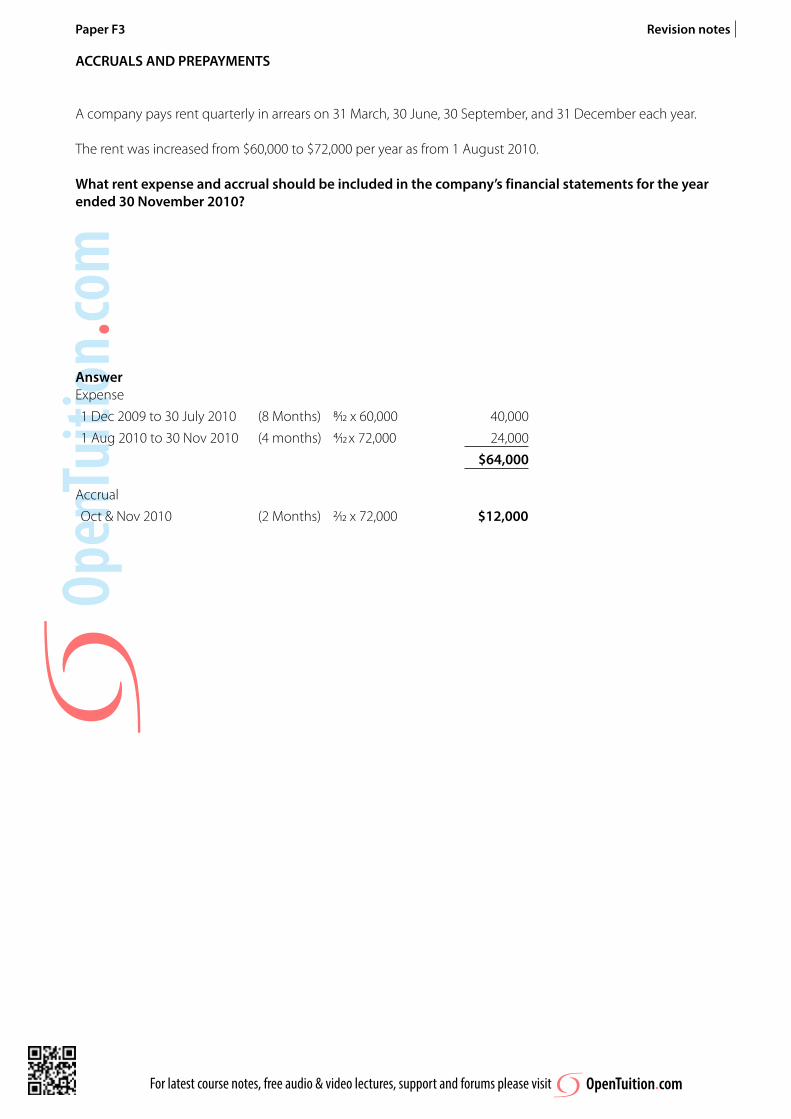

ACCrUALS ANd PrEPAYmENTS

A company pays rent quarterly in arrears on 31 March, 30 June, 30 September, and 31 December each year.

The rent was increased from $60,000 to $72,000 per year as from 1 August 2010.

What rent expense and accrual should be included in the company’s financial statements for the year ended 30 November 2010?

AnswerExpense1 Dec 2009 to 30 July 2010 (8 Months) 8/12 x 60,000 40,0001 Aug 2010 to 30 Nov 2010 (4 months) 4/12 x 72,000 24,000

$64,000

AccrualOct & Nov 2010 (2 Months) 2/12 x 72,000 $12,000

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

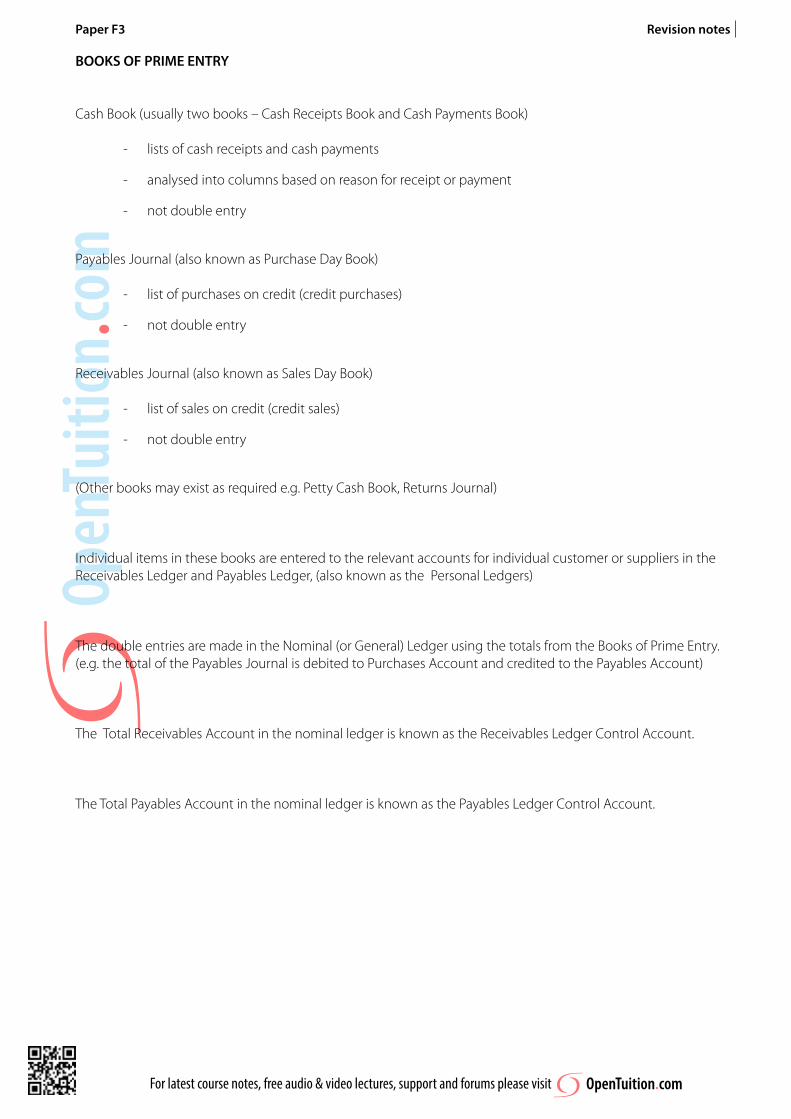

BOOKS OF PrImE ENTrY

Cash Book (usually two books – Cash Receipts Book and Cash Payments Book)

- lists of cash receipts and cash payments

- analysed into columns based on reason for receipt or payment

- not double entry

Payables Journal (also known as Purchase Day Book)

- list of purchases on credit (credit purchases)

- not double entry

Receivables Journal (also known as Sales Day Book)

- list of sales on credit (credit sales)

- not double entry

(Other books may exist as required e.g. Petty Cash Book, Returns Journal)

Individual items in these books are entered to the relevant accounts for individual customer or suppliers in the Receivables Ledger and Payables Ledger, (also known as the Personal Ledgers)

The double entries are made in the Nominal (or General) Ledger using the totals from the Books of Prime Entry.(e.g. the total of the Payables Journal is debited to Purchases Account and credited to the Payables Account)

The Total Receivables Account in the nominal ledger is known as the Receivables Ledger Control Account.

The Total Payables Account in the nominal ledger is known as the Payables Ledger Control Account.

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

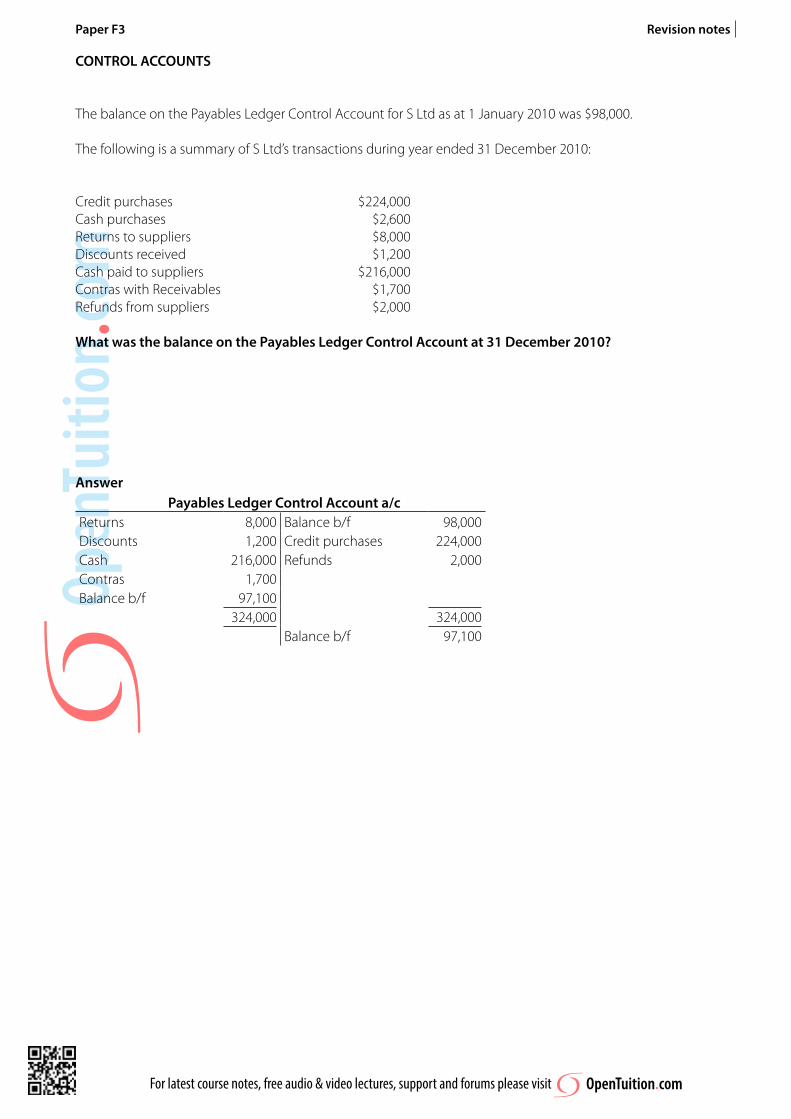

CONTrOL ACCOUNTS

The balance on the Payables Ledger Control Account for S Ltd as at 1 January 2010 was $98,000.

The following is a summary of S Ltd’s transactions during year ended 31 December 2010:

Credit purchases $224,000Cash purchases $2,600Returns to suppliers $8,000Discounts received $1,200Cash paid to suppliers $216,000Contras with Receivables $1,700Refunds from suppliers $2,000

What was the balance on the Payables Ledger Control Account at 31 december 2010?

AnswerPayables Ledger Control Account a/c

Returns 8,000 Balance b/f 98,000Discounts 1,200 Credit purchases 224,000Cash 216,000 Refunds 2,000Contras 1,700Balance b/f 97,100

324,000 324,000Balance b/f 97,100

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

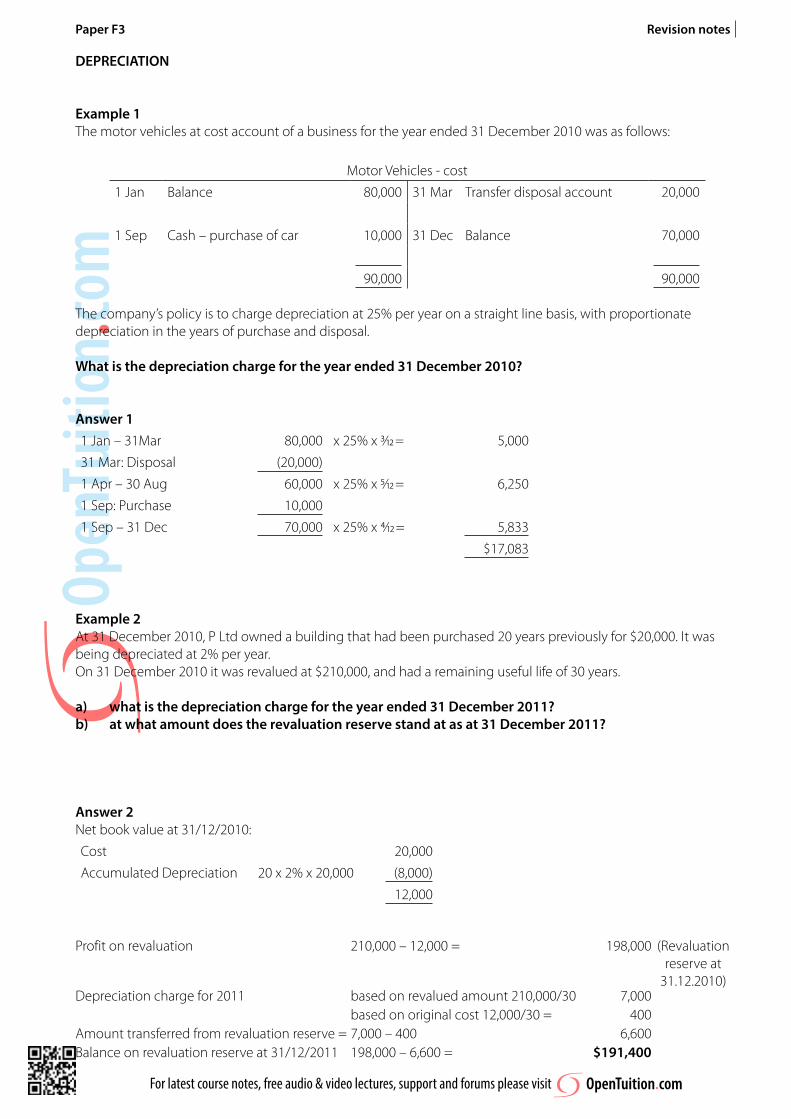

dEPrECIATION

Example 1The motor vehicles at cost account of a business for the year ended 31 December 2010 was as follows:

Motor Vehicles - cost1 Jan Balance 80,000 31 Mar Transfer disposal account 20,000

1 Sep Cash – purchase of car 10,000 31 Dec Balance 70,000

90,000 90,000

The company’s policy is to charge depreciation at 25% per year on a straight line basis, with proportionate depreciation in the years of purchase and disposal.

What is the depreciation charge for the year ended 31 december 2010?

Answer 11 Jan – 31Mar 80,000 x 25% x 3/12 = 5,00031 Mar: Disposal (20,000)1 Apr – 30 Aug 60,000 x 25% x 5/12 = 6,2501 Sep: Purchase 10,0001 Sep – 31 Dec 70,000 x 25% x 4/12 = 5,833

$17,083

Example 2 At 31 December 2010, P Ltd owned a building that had been purchased 20 years previously for $20,000. It was being depreciated at 2% per year.On 31 December 2010 it was revalued at $210,000, and had a remaining useful life of 30 years. a) what is the depreciation charge for the year ended 31 december 2011?b) at what amount does the revaluation reserve stand at as at 31 december 2011?

Answer 2Net book value at 31/12/2010:Cost 20,000Accumulated Depreciation 20 x 2% x 20,000 (8,000)

12,000

Profit on revaluation 210,000 – 12,000 = 198,000 (Revaluation

reserve at 31.12.2010)

Depreciation charge for 2011 based on revalued amount 210,000/30 7,000based on original cost 12,000/30 = 400

Amount transferred from revaluation reserve = 7,000 – 400 6,600Balance on revaluation reserve at 31/12/2011 198,000 – 6,600 = $191,400

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

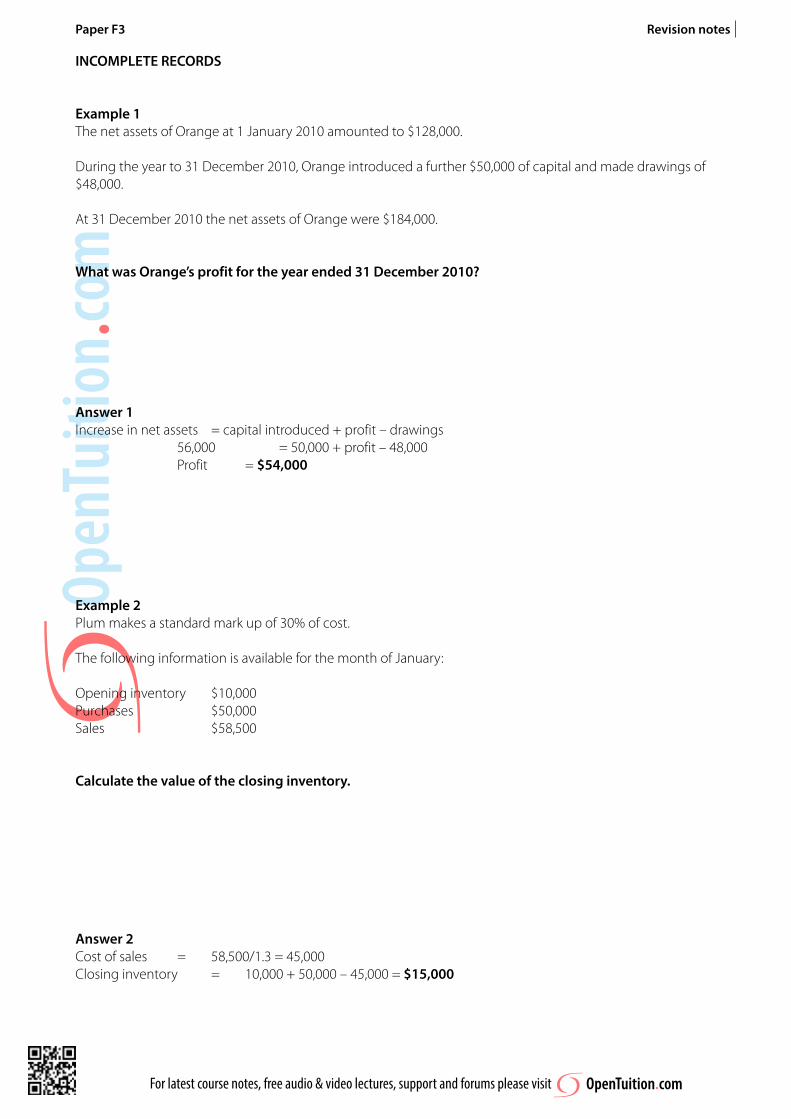

INCOmPLETE rECOrdS

Example 1The net assets of Orange at 1 January 2010 amounted to $128,000.

During the year to 31 December 2010, Orange introduced a further $50,000 of capital and made drawings of $48,000.

At 31 December 2010 the net assets of Orange were $184,000.

What was Orange’s profit for the year ended 31 december 2010?

Answer 1Increase in net assets = capital introduced + profit – drawings 56,000 = 50,000 + profit – 48,000 Profit = $54,000

Example 2Plum makes a standard mark up of 30% of cost.

The following information is available for the month of January:

Opening inventory $10,000Purchases $50,000Sales $58,500

Calculate the value of the closing inventory.

Answer 2Cost of sales = 58,500/1.3 = 45,000Closing inventory = 10,000 + 50,000 – 45,000 = $15,000

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

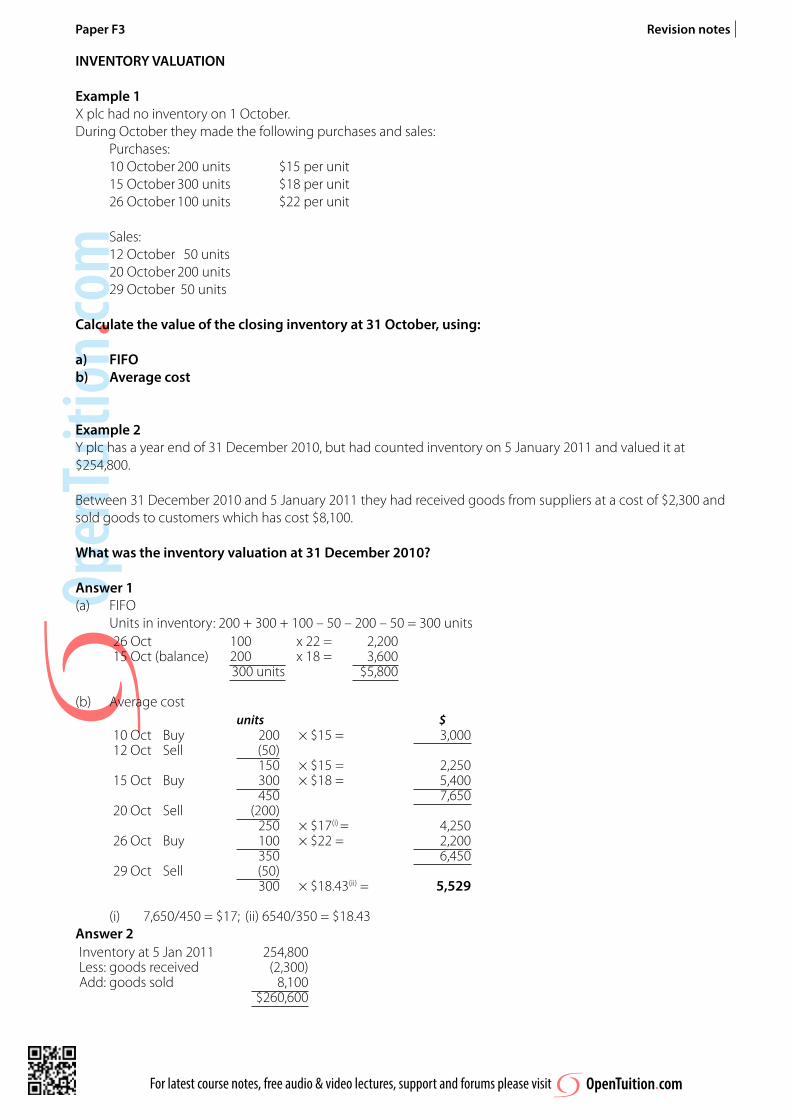

INVENTOrY VALUATION

Example 1X plc had no inventory on 1 October.During October they made the following purchases and sales:

Purchases:10 October 200 units $15 per unit15 October 300 units $18 per unit26 October 100 units $22 per unit

Sales:12 October 50 units20 October 200 units29 October 50 units

Calculate the value of the closing inventory at 31 October, using:

a) FIFOb) Average cost

Example 2Y plc has a year end of 31 December 2010, but had counted inventory on 5 January 2011 and valued it at $254,800.

Between 31 December 2010 and 5 January 2011 they had received goods from suppliers at a cost of $2,300 and sold goods to customers which has cost $8,100.

What was the inventory valuation at 31 december 2010?

Answer 1(a) FIFO

Units in inventory: 200 + 300 + 100 – 50 – 200 – 50 = 300 units26 Oct 100 x 22 = 2,20015 Oct (balance) 200 x 18 = 3,600

300 units $5,800

(b) Average costunits $

10 Oct Buy 200 × $15 = 3,00012 Oct Sell (50)

150 × $15 = 2,25015 Oct Buy 300 × $18 = 5,400

450 7,65020 Oct Sell (200)

250 × $17(i) = 4,25026 Oct Buy 100 × $22 = 2,200

350 6,45029 Oct Sell (50)

300 × $18.43(ii) = 5,529

(i) 7,650/450 = $17; (ii) 6540/350 = $18.43Answer 2Inventory at 5 Jan 2011 254,800Less: goods received (2,300)Add: goods sold 8,100

$260,600

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

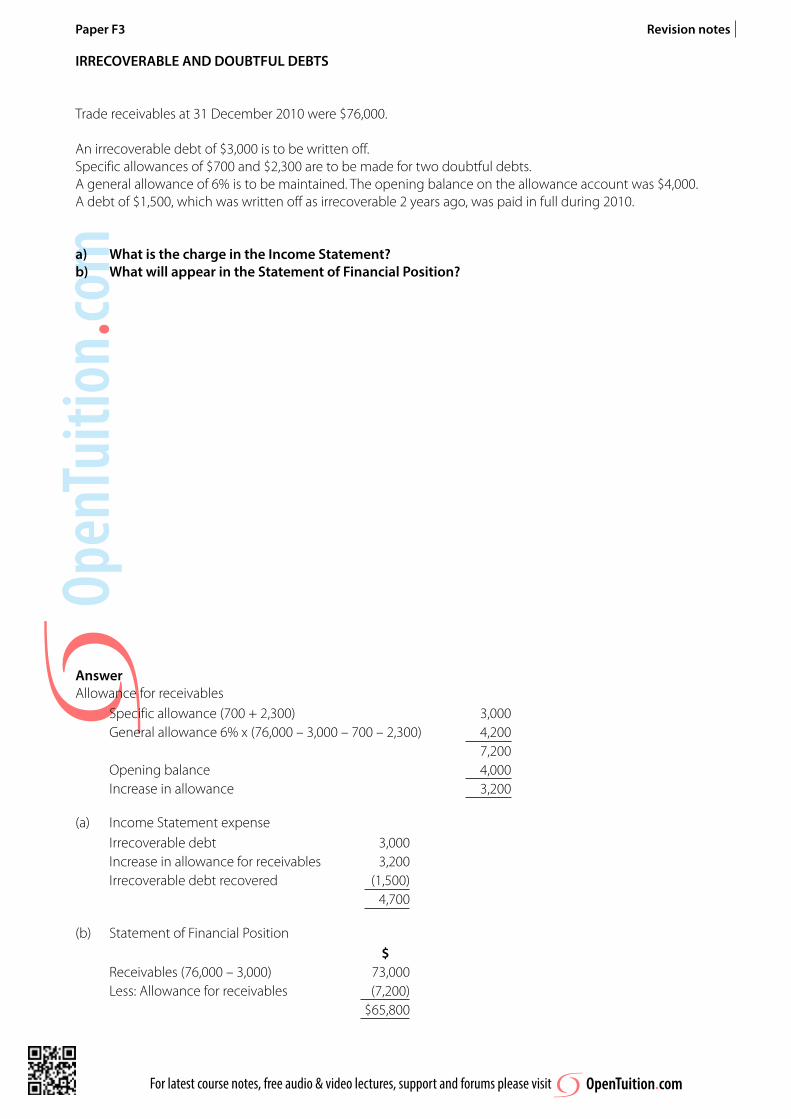

IrrECOVErABLE ANd dOUBTFUL dEBTS

Trade receivables at 31 December 2010 were $76,000.

An irrecoverable debt of $3,000 is to be written off.Specific allowances of $700 and $2,300 are to be made for two doubtful debts.A general allowance of 6% is to be maintained. The opening balance on the allowance account was $4,000.A debt of $1,500, which was written off as irrecoverable 2 years ago, was paid in full during 2010.

a) What is the charge in the Income Statement?b) What will appear in the Statement of Financial Position?

AnswerAllowance for receivables

Specific allowance (700 + 2,300) 3,000General allowance 6% x (76,000 – 3,000 – 700 – 2,300) 4,200

7,200Opening balance 4,000Increase in allowance 3,200

(a) Income Statement expenseIrrecoverable debt 3,000Increase in allowance for receivables 3,200Irrecoverable debt recovered (1,500)

4,700

(b) Statement of Financial Position$

Receivables (76,000 – 3,000) 73,000Less: Allowance for receivables (7,200)

$65,800

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

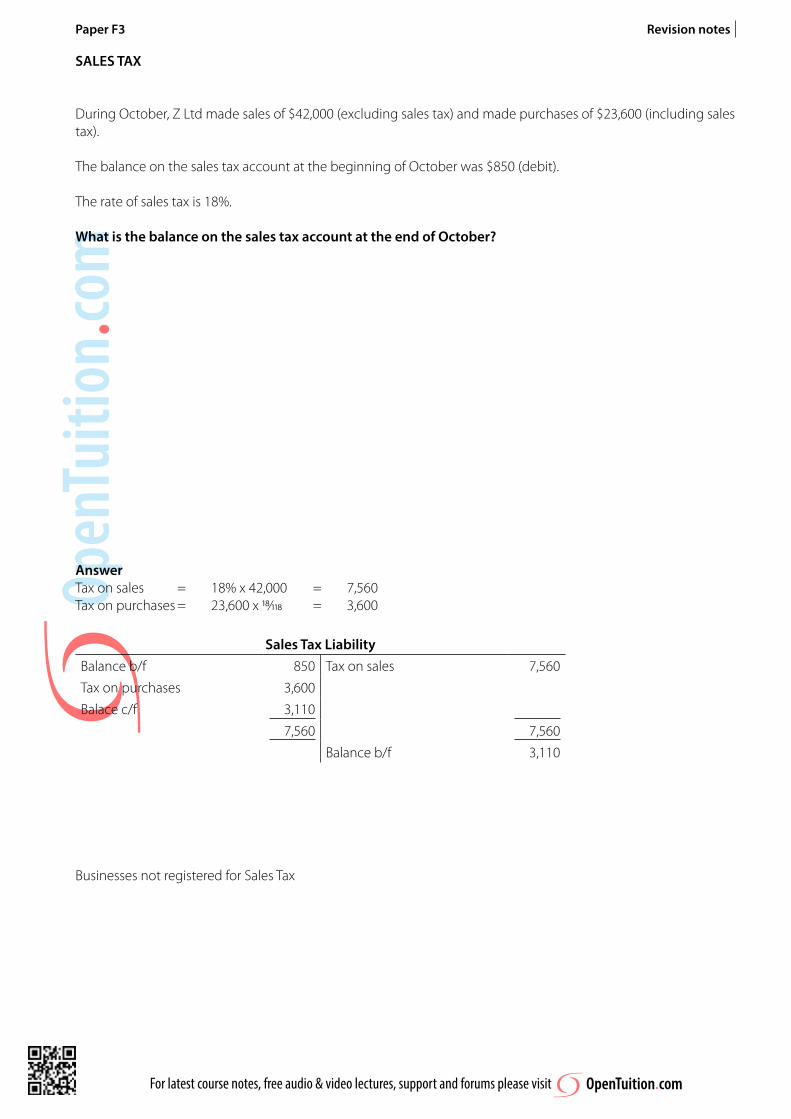

SALES TAX

During October, Z Ltd made sales of $42,000 (excluding sales tax) and made purchases of $23,600 (including sales tax).

The balance on the sales tax account at the beginning of October was $850 (debit).

The rate of sales tax is 18%.

What is the balance on the sales tax account at the end of October?

AnswerTax on sales = 18% x 42,000 = 7,560Tax on purchases = 23,600 x 18/118 = 3,600

Sales Tax LiabilityBalance b/f 850 Tax on sales 7,560Tax on purchases 3,600Balace c/f 3,110

7,560 7,560Balance b/f 3,110

Businesses not registered for Sales Tax

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

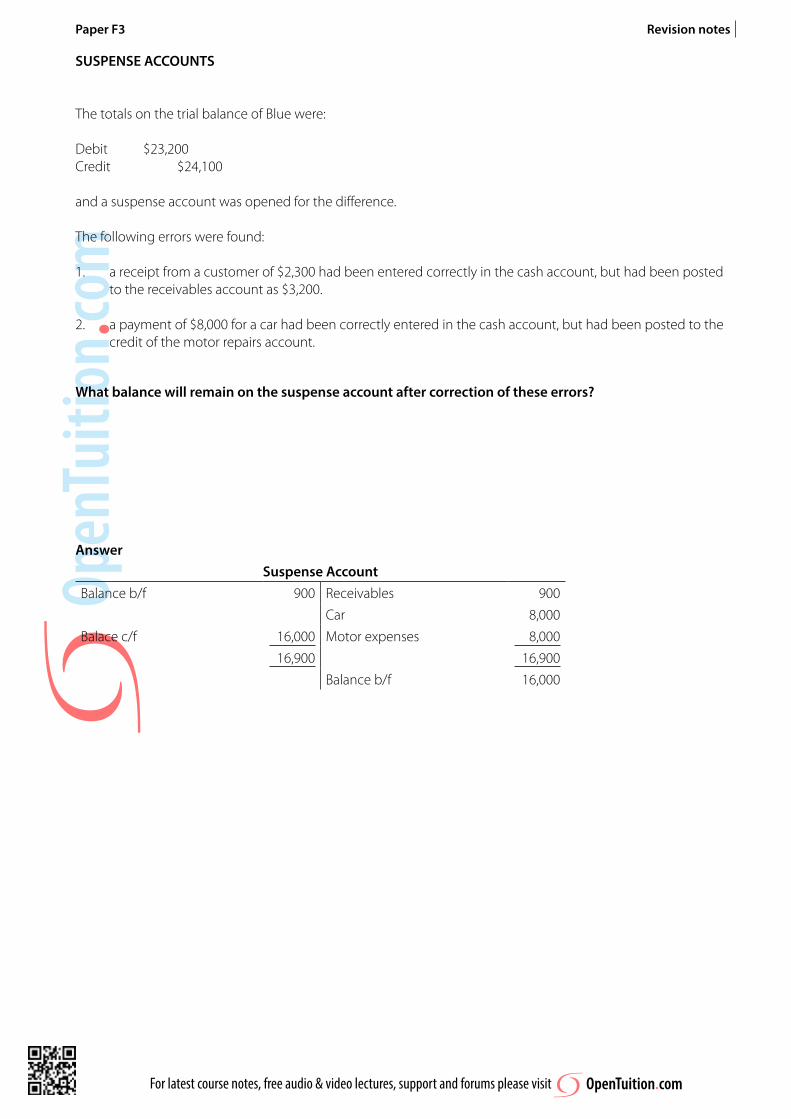

SUSPENSE ACCOUNTS

The totals on the trial balance of Blue were:

Debit $23,200Credit $24,100

and a suspense account was opened for the difference.

The following errors were found:

1. a receipt from a customer of $2,300 had been entered correctly in the cash account, but had been posted to the receivables account as $3,200.

2. a payment of $8,000 for a car had been correctly entered in the cash account, but had been posted to the credit of the motor repairs account.

What balance will remain on the suspense account after correction of these errors?

AnswerSuspense Account

Balance b/f 900 Receivables 900Car 8,000

Balace c/f 16,000 Motor expenses 8,00016,900 16,900

Balance b/f 16,000

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

FINANCIAL rATIOS

Profitability:

Return on Capital Employed

Net Profit Margin

Asset Turnover

Gross Profit Margin

Liquidity:

Current ratio

Acid-test / Quick ratio

Receivables Days

Inventory Days

Payables Days

Gearing:

Gearing Ratio

For latest course notes, free audio & video lectures, support and forums please visit

Paper F3 Revision notes

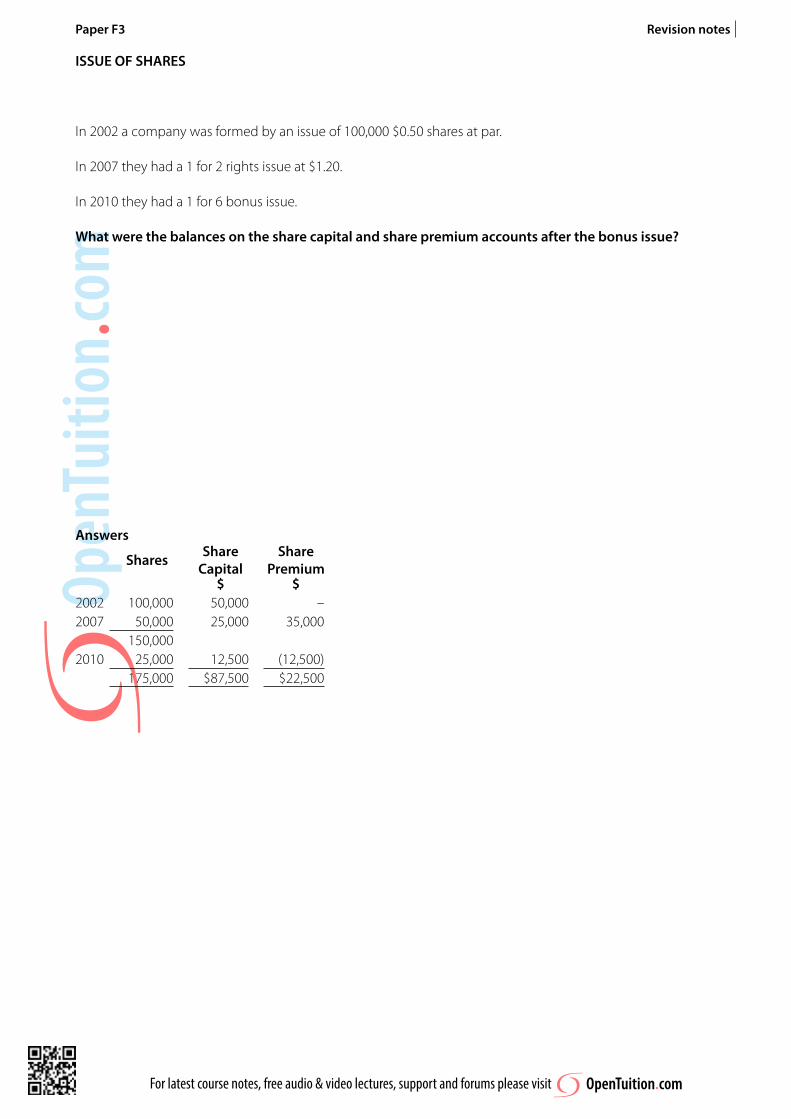

ISSUE OF ShArES

In 2002 a company was formed by an issue of 100,000 $0.50 shares at par.

In 2007 they had a 1 for 2 rights issue at $1.20.

In 2010 they had a 1 for 6 bonus issue.

What were the balances on the share capital and share premium accounts after the bonus issue?

Answers

Shares Share Capital

Share Premium

$ $2002 100,000 50,000 –2007 50,000 25,000 35,000

150,0002010 25,000 12,500 (12,500)

175,000 $87,500 $22,500