extension of social protection: community-based health insurance céline peyron, itc- ilo, trade...

TRANSCRIPT

Extension of Social Protection:

Community-based health insurance

Céline Peyron, ITC- ILO, Trade Union Training on Social Protection, 13 May 2004

Extension of Social Protection:

Community-based health insurance

Céline Peyron, ITC- ILO, Trade Union Training on Social Protection, 13 May 2004

ContentContentContentContent

1. Health micro-insurance : a strategy for the extension of social security

2. Definition, principles and models of HMIS

3. Linkages

4. Limitations and impact of HMIS

1. Health micro-insurance: a

strategy for the extension

of social security

1. Health micro-insurance: a

strategy for the extension

of social security

ILO objective on Social Protection

ILO objective on Social Protection

Enhance

the coverage and effectiveness of the Social Protection

for

ALL

Strategies for extending health Strategies for extending health insuranceinsurance

Strategies for extending health Strategies for extending health insuranceinsurance

Strengthening of national health insurance schemes:

– Extending social insurance coverage

– Universal benefits

– Social assistance

Encouraging decentralized mechanisms

Creation of linkages between both

2. Definition, principles and

models of health micro-

insurance schemes

2. Definition, principles and

models of health micro-

insurance schemes

Health micro-insurance schemes: Objectives

Health micro-insurance schemes: Objectives

To support populations’ initiatives in organizing themselves their access to health :

Providing access to health to members

Negotiating with health care providers quality services at lowest possible costs

Prevention and information on Health problems

Income security and stability

Reinforcing solidarity and equity

Participation of all beneficiaries in social matters

Health Micro-Insurance Schemes: Definition

Health Micro-Insurance Schemes: Definition

“Micro-insurance refers to various schemes set up by self-employed and informal economy

workers to meet their priority social protection needs. The mechanism used in these schemes is generally the provision of

mutual support through the pooling of resources based on the principals of

insurance. “

Source: ILO, World Labour Report 2000: Income security and social protection in a changing world, (ILO: Geneva).

Growth statistics in West AfricaGrowth statistics in West Africa

1997 2000 ProjectsBenin 11 23 19Burkina Faso 6 26 18Cameroon 18 20 7Ivory Coast 29Guinea 6 27 5Mali 7 22MauritaniaNiger 6 12 3Senegal 19 29 31Tchad 3 4Togo 0 + 8 projects 7 5

76 199 88

Health micro-insurance:Schemes

Health micro-insurance:Schemes

Mutual Benefits Association (Trade Union)

Community Based Schemes Integrated Schemes in an Hospital

managementMicro-finance Institutes

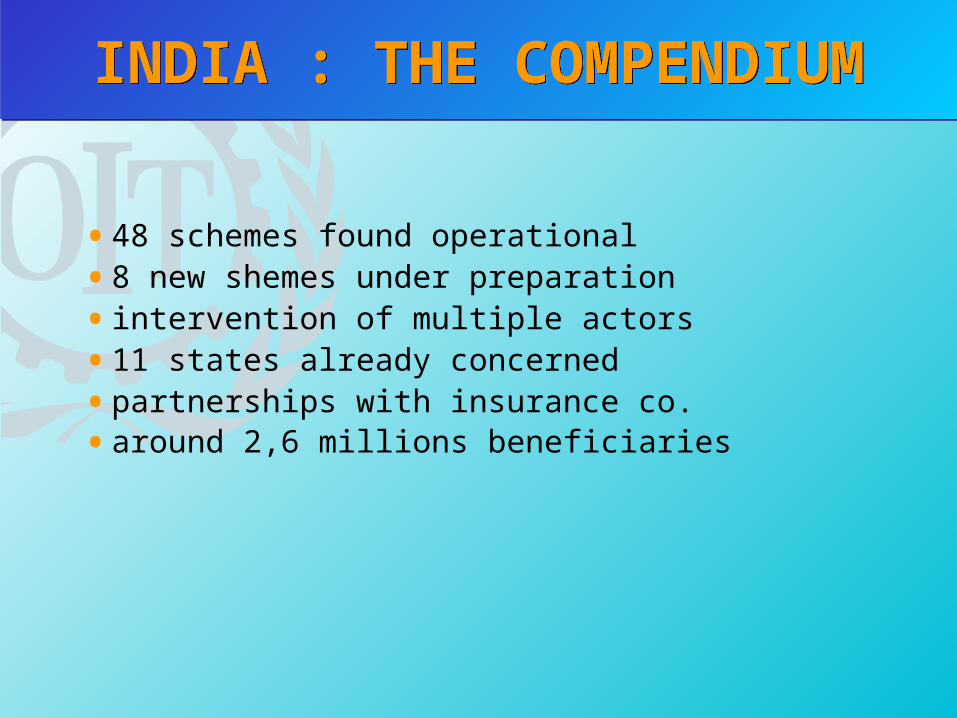

INDIA : THE COMPENDIUMINDIA : THE COMPENDIUM

• 48 schemes found operational

• 8 new shemes under preparation

• intervention of multiple actors

• 11 states already concerned

• partnerships with insurance co.

• around 2,6 millions beneficiaries

OWNERSHIPOWNERSHIP

0%

10%

20%

30%

40%

MFO NGO CBO HPR

OWNERSHIP OF THE SCHEMES

INDIA, 2003INDIA, 2003

LEVEL OF EXPERIENCELEVEL OF EXPERIENCE

0

5

10

15

< 2y. 3-4y. 5-6y. 7-10y. More

LEVEL OF EXPERIENCE

INDIA, 2003INDIA, 2003

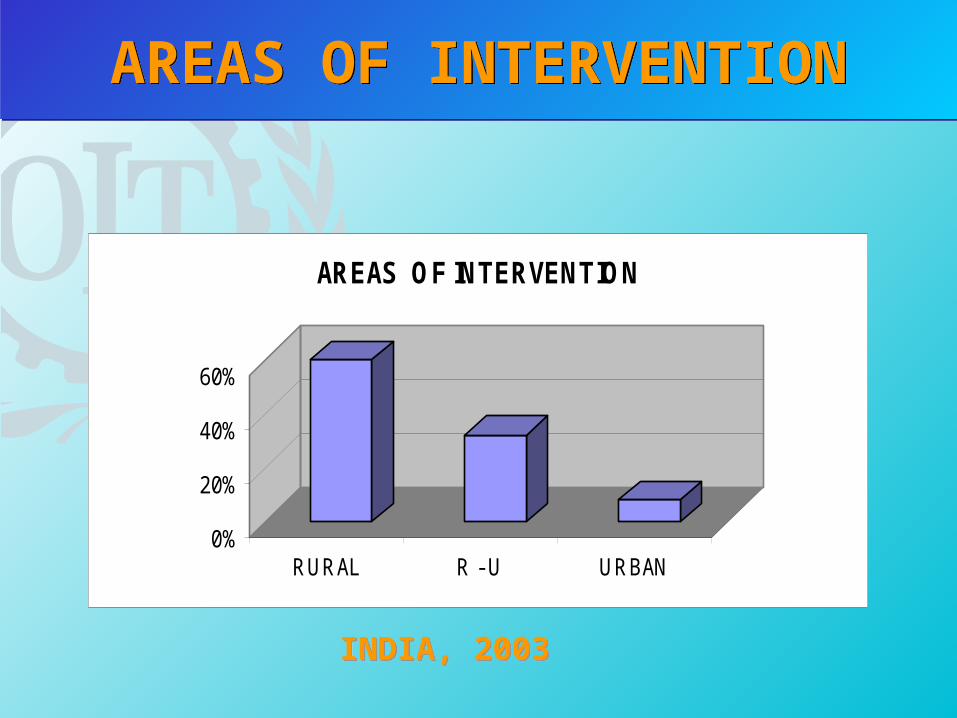

AREAS OF INTERVENTIONAREAS OF INTERVENTION

0%

20%

40%

60%

RURAL R - U URBAN

AREAS OF INTERVENTION

INDIA, 2003INDIA, 2003

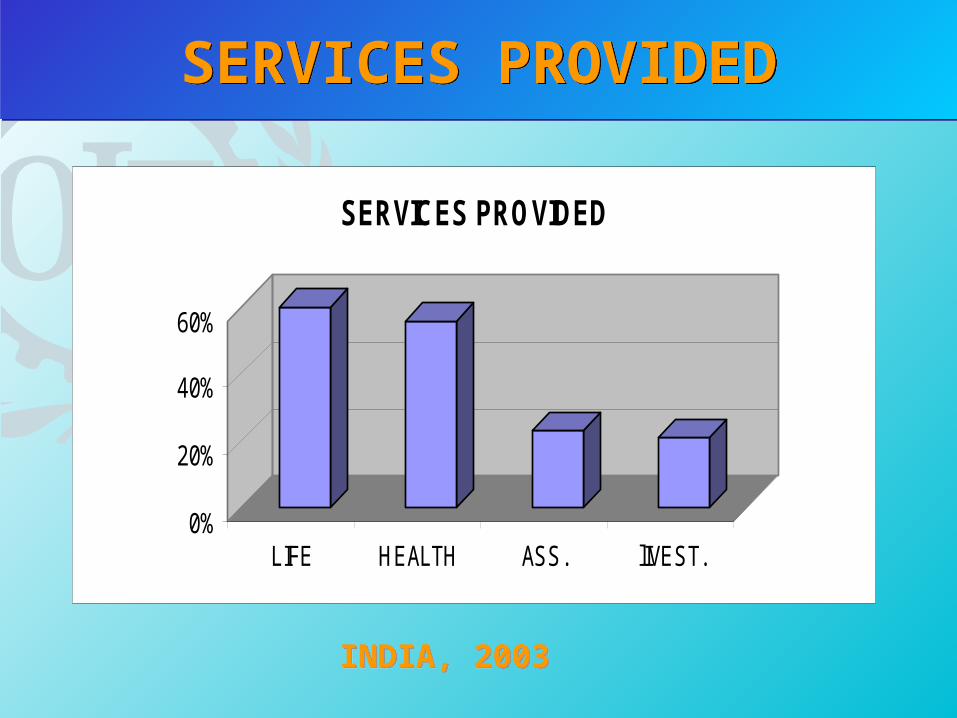

SERVICES PROVIDEDSERVICES PROVIDED

0%

20%

40%

60%

LIFE HEALTH ASS. lIVEST.

SERVICES PROVIDED

INDIA, 2003INDIA, 2003

BENEFICIARIESBENEFICIARIES

NUMBER OF BENEFICIARIES

0

5

10

15

<1000 1001-5000 5001-10000

10001-100000

100001-500000

More

INDIA, 2003INDIA, 2003

TYPE OF CONTRIBUTIONTYPE OF CONTRIBUTION

0

10

20

30

VOLUNT. COMPUL. MIX

TYPE OF CONTRIBUTION

INDIA, 2003INDIA, 2003

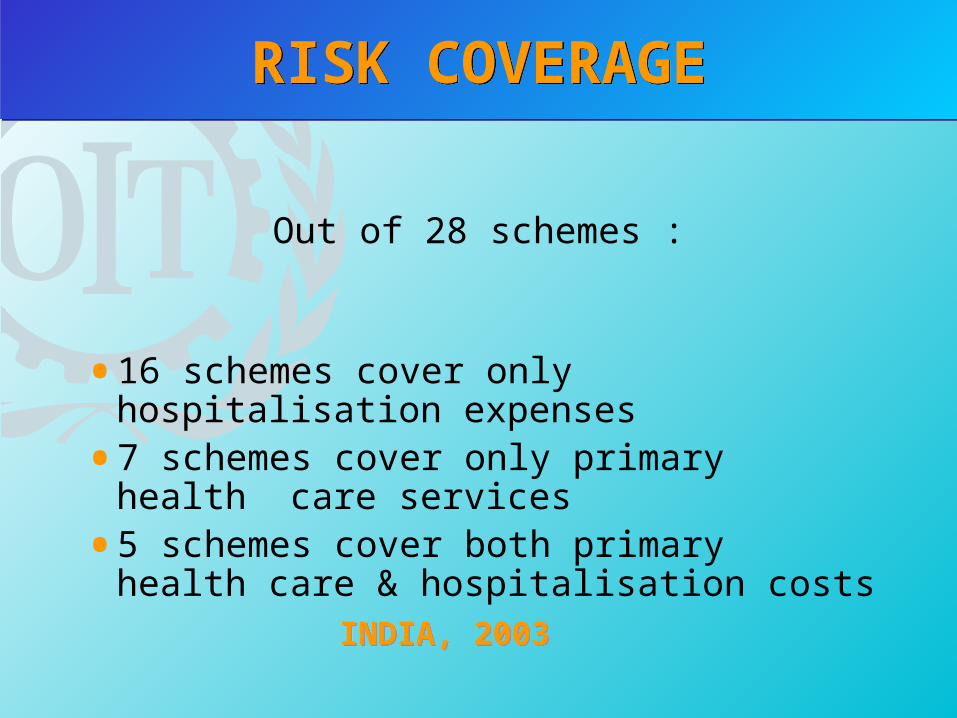

RISK COVERAGERISK COVERAGE

Out of 28 schemes :

• 16 schemes cover only hospitalisation expenses

• 7 schemes cover only primary health care services

• 5 schemes cover both primary health care & hospitalisation costs

INDIA, 2003INDIA, 2003

SCHEDULE OF CONTRIBUTIONSCHEDULE OF

CONTRIBUTION

0

10

20

30

40

YEARLY MONTH W.ACT.

SCHEDULE OF CONTRIBUTIONS

INDIA, 2003INDIA, 2003

Which are the main characteristics of health

micro-insurance schemes in India?

THE CURRENT TRENDS, IN INDIA…THE CURRENT TRENDS, IN INDIA…

all insurance companies (both public and private) involved in the provision of health micro-insurance products to the poor mainly cover hospitalisation costs…

while…there is a world-wide recognition that the overriding need in developing countries is for primary health care…

Health micro-insurance: Health micro-insurance: PrinciplesPrinciples

Health micro-insurance: Health micro-insurance: PrinciplesPrinciples

population excluded from formal social security

schemes, often low incomes and vulnerable

solidarity and non-profit organisation

voluntary & contributory schemes

pooling of a group’s resources to share risks

(health, pregnancy, death, accidents, belongings)

& organize protection adapted to their needs

benefits package and contributions adapted

Health micro-insurance:Actors

Health micro-insurance:Actors

BeneficiariesHealth care providers (Public services

and private providers)Finance institutesAuthorities (local and national)

Health micro-insurance: Different models

Health micro-insurance: Different models

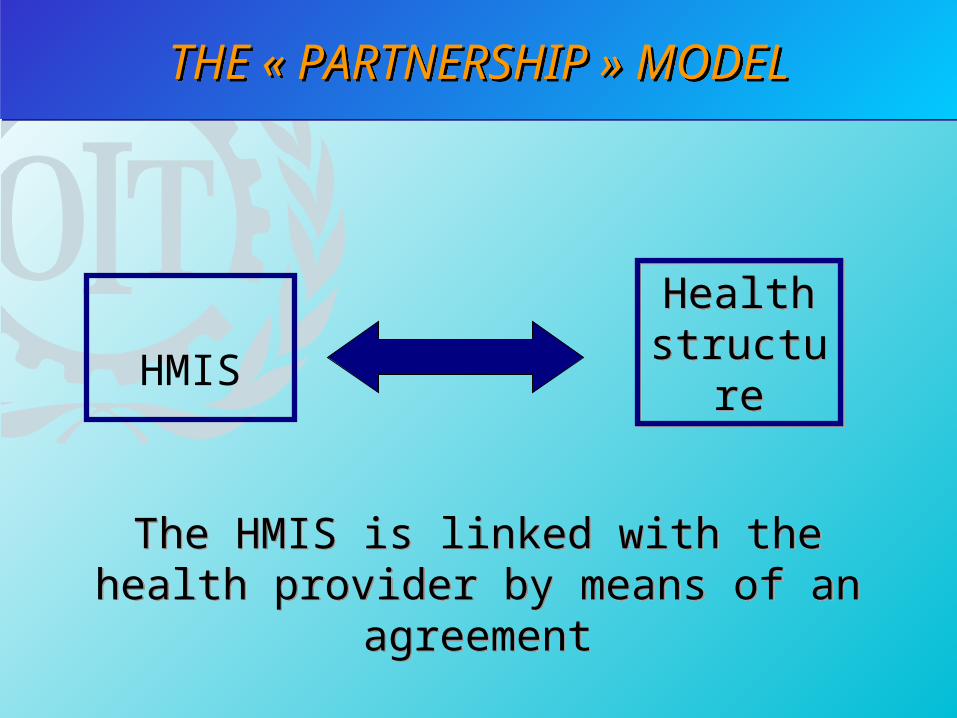

THE « PARTNERSHIP » MODEL

THE « INTEGRATED » MODEL

THE « INDEPENDENT » MODEL

THE « PARTNERSHIP » MODELTHE « PARTNERSHIP » MODEL

HMISHealth

structureHealth

structure

The HMIS is linked with the health provider by means of an agreementThe HMIS is linked with the health

provider by means of an agreement

5000 MEMBERSCollaboration with 5 hospitals IT developed management

MicroCare Health Plan,MicroCare Health Plan,UGANDAUGANDA

MicroCare Health Plan,MicroCare Health Plan,UGANDAUGANDA

THE « PARTNERSHIP » MODELTHE « PARTNERSHIP » MODEL

HEALTH CARE PROVIDED medical consultations hospitalisations specialized tests surgery diagnostics and check-up medicine delivery services dental care ophtalmological consultations COVERAGE Of HEALTH CARE COST 100% ANNUAL CONTRIBUTION PER FAMILY : 60 $US (6 members)

MicroCare Health Plan,MicroCare Health Plan,UGANDAUGANDA

MicroCare Health Plan,MicroCare Health Plan,UGANDAUGANDA

THE « PARTNERSHIP » MODELTHE « PARTNERSHIP » MODEL

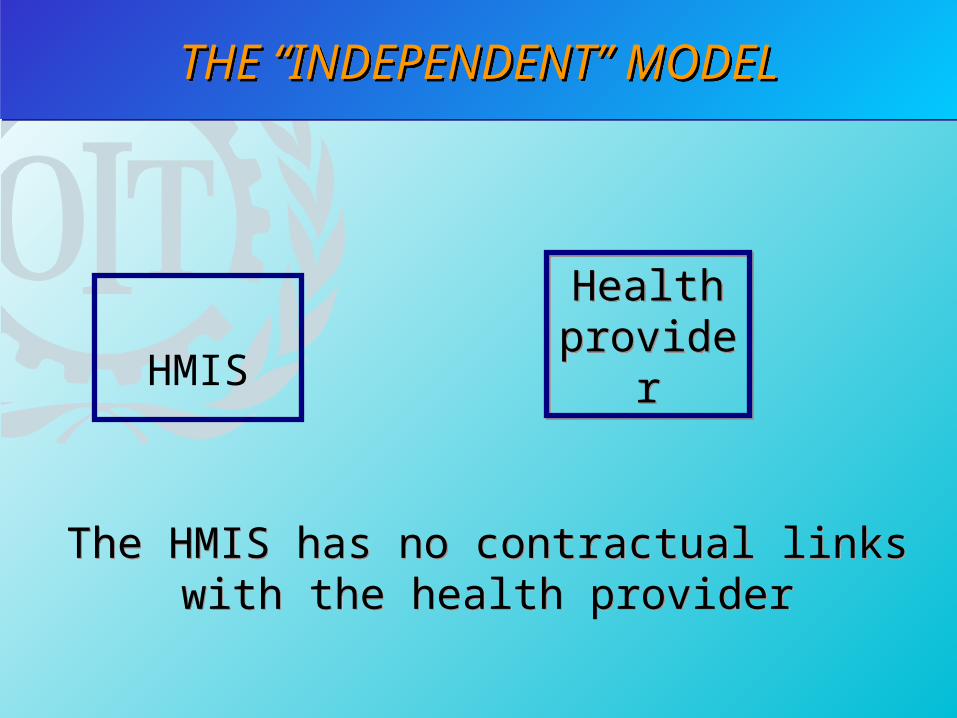

THE “INDEPENDENT” MODELTHE “INDEPENDENT” MODEL

The HMIS has no contractual links with the health provider

The HMIS has no contractual links with the health provider

HMISHealth

providerHealth

provider

Created in 1992 From a Women

Workers ’ Trade Union, of the informal economy (created in 1972)

90.000 beneficiaries

Vimo SEWA- INDIAVimo SEWA- INDIAVimo SEWA- INDIAVimo SEWA- INDIA

THE “INDEPENDENT” MODEL

CARE SERVICES PACKAGE INCLUDING : Health Insurance (hospitalization), including services for delivery

protection, Life Insurance, including insurance in case of invalidity, and Belongings Insurance (lost or damages to property or working

material) HEALTH CARE COVERED : 30 $USMAX PER YEAR MATERNITY PROTECTION : 7,5 $US on the 8th month of

pregnancy CONTRIBUTION : 1,5 $US / Year

Vimo SEWA- INDEVimo SEWA- INDEVimo SEWA- INDEVimo SEWA- INDE

THE “INDEPENDENT” MODEL

THE « INTEGRATED » MODELTHE « INTEGRATED » MODEL

HMISHealth

providerHealth

provider

The HMIS has developed its own health provision structure

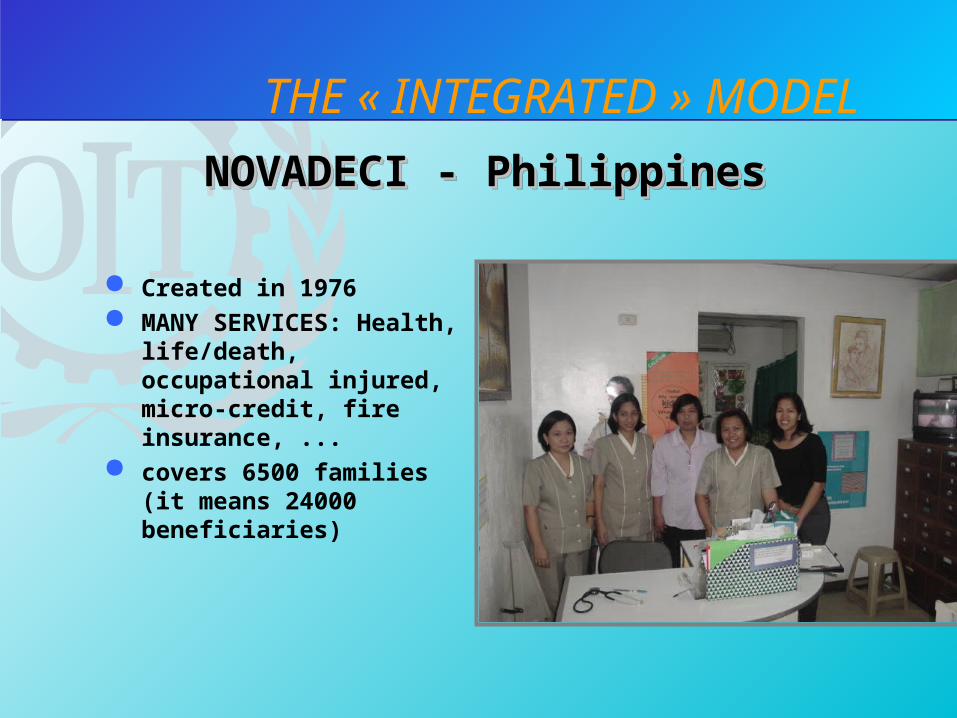

Created in 1976 MANY SERVICES: Health,

life/death, occupational injured, micro-credit, fire insurance, ...

covers 6500 families (it means 24000 beneficiaries)

NOVADECI - PhilippinesNOVADECI - PhilippinesNOVADECI - PhilippinesNOVADECI - Philippines

THE « INTEGRATED » MODEL

NOVADECI - NOVADECI -

Philippines PharmacyPhilippines Pharmacy

NOVADECI - NOVADECI -

Philippines PharmacyPhilippines Pharmacy

THE « INTEGRATED » MODELTHE « INTEGRATED » MODEL

Steps in setting up health micro-insurance scheme

Steps in setting up health micro-insurance scheme

Diagnostic - informationSetting up steering committeePre- and feasibility studyAgreement-preparation providersPreparation of management and monitoring

toolsLauching schemeFunctionning and monitoring HMIS

3. Linkages

Social dialogue and the extension of SPSocial dialogue and the extension of SP

GovernmentWorkersEmployers

Providers of services

Workers and their families

Community-based organizations

NGOs

International organizations

Citizens

Conclusion: linkages HMIS with Trade-Unions

Conclusion: linkages HMIS with Trade-Unions

• Promotion

• Setting-up their own HMIS system

• Negotiation to improve health care services (quality and quantity)

• Campaign for prevention and health education

4- Limitations and impact of health micro-insurance schemes

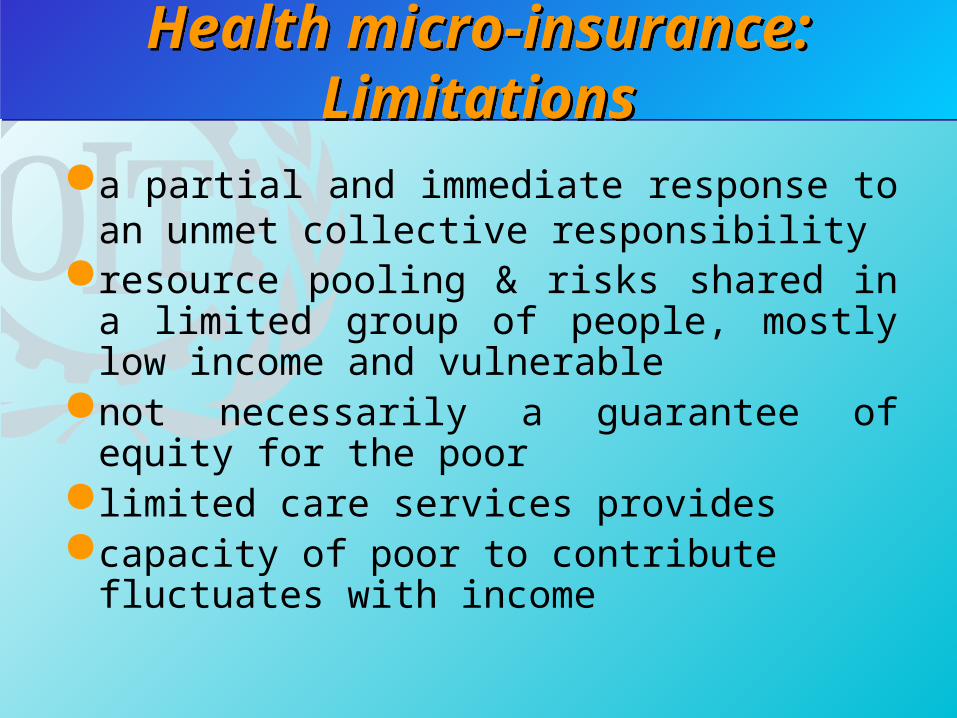

Health micro-insurance:Limitations

Health micro-insurance:Limitations

a partial and immediate response to an unmet collective responsibility

resource pooling & risks shared in a limited group of people, mostly low income and vulnerable

not necessarily a guarantee of equity for the poor

limited care services providescapacity of poor to contribute fluctuates

with income

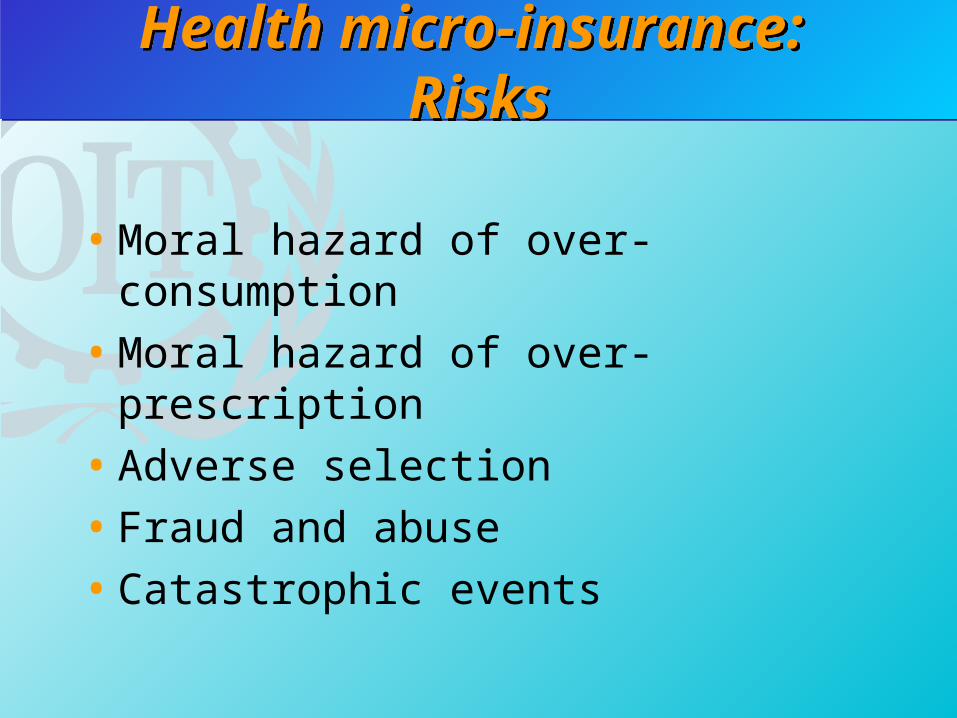

• Moral hazard of over-consumption

• Moral hazard of over-prescription

• Adverse selection

• Fraud and abuse

• Catastrophic events

Health micro-insurance: Risks

Health micro-insurance: Risks

Group workGroup work

1. What can be the relevance of HMIS in terms of gender equality?

2. Is HMIS possible for HIV/AIDS affected targets?

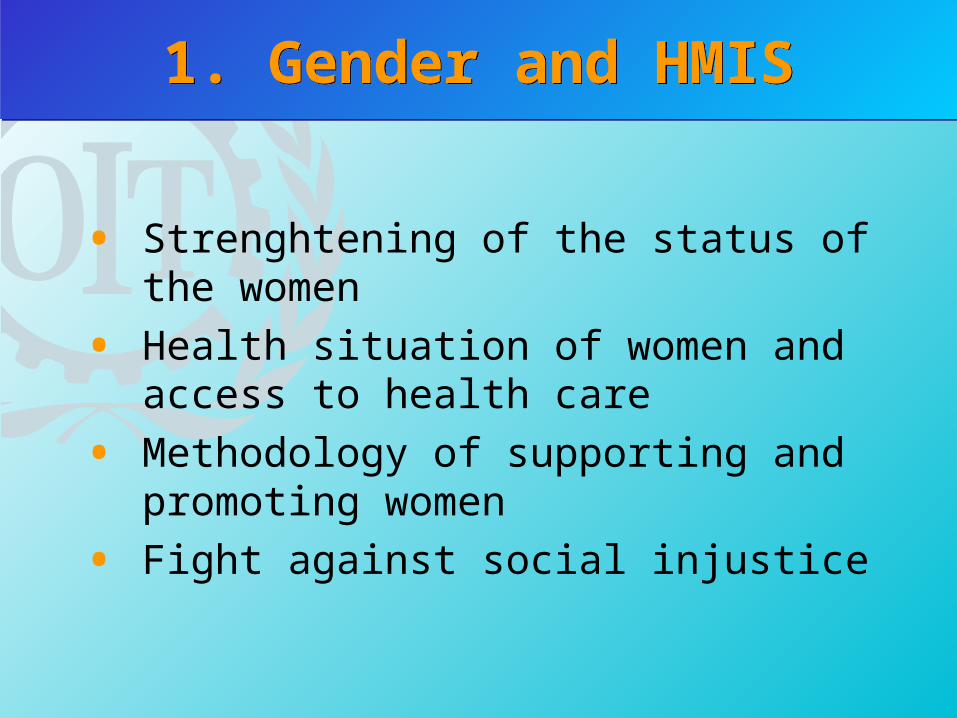

1. Gender and HMIS1. Gender and HMIS

• Strenghtening of the status of the women

• Health situation of women and access to health care

• Methodology of supporting and promoting women

• Fight against social injustice

1. Gender and HMIS1. Gender and HMIS

Participation of women in management of HMIS

Reduce poverty and inequity between sexes

Protection of domestic workers Women mainly employed in informal

economy

2.- HMIS and HIV/AIDS2.- HMIS and HIV/AIDS

Suitable if: Expansion of the members (Affected /

Infected) Benefits package limited to primary

health care Funds from National campaigns and

NGO’s projects

2. Advantages of HMIS to prevent HIV/AIDS

2. Advantages of HMIS to prevent HIV/AIDS

Access to health care Prevention Voluntary and confidential counselling

and testing Improvement capacity of health

providers Address stigma and discrimination Channel ressources to the local level

THANK YOU ! !THANK YOU ! !