expectation errors and exchange-rate volatility

TRANSCRIPT

Expectation Errors and Exchange-Rate Volatility

1. Introduction What happens whon speculators make wild exchange-rate

hwasts? ‘I‘hc mswtt~ to this question depends, of coIIt-se, on the reactions of the monetarj~ authorities.

‘l‘here lias bcxen mulch discussion in 11~ literatilre rrccntly of‘ the private sector’s reaction to monetary policy changes, but in this paper we are concerned with the reverse direction of causation. We show that exchange rates will exhibit overshooting when disturbanc- es ernanatc from the private sector; but, the type of overshooting is qualitatively different firom that which can 1~ expected when clis- furbanccs initiate from policy changes. This should allow an en- pirical test of the relative importance of private and public sector as sources of exchange-rate variability. WC also show that the op- tiuiizing monetary authority will rcvisc its c~xchangc-rale targets in an enduring El&ion in response to transitory fi)rccusting errors OII the part of’ the private sector.

In o&r to analyze disturbances to tht: t&r:ign c:xchangc: mar- ;jet Corning from the behavior of spc:c*ulators. it is app’opriatc to :make sonlo departure from the standard assumption of rational ex- ‘pectations. In particular, we will IX assuming that the inarket’s ex- pectation of f’uturc oxcliunge rates may deviate frown the rnathc- matical expectation.

It Illigllt I)0 chjwtcd that, wliik tlworetically possible, tliere woi11~1 be no tendc~1cy fbr fvqwxt~~tio~is to sliift without the stiniulus of ;III CW~CIKNS shock, SIICII as ii change in policy. Ilowcver the cxpcricww of market prticipa11ts c:tsts clol1bt on any such objection. On the Iwis of :I recent survey of fbrcign excllallge market partic- ipits 1 Hnschna~!cl ctt al. (198O)j it is reportctl that, at times of cx- trc1ne volatility, “professionals abanclon their view ant1 concentrate illstcad oii pressing what the i1m;ifeurs art: going to do.” In s11c11 circunistaiiccs, rumors antl “irrelevant” iliformation could easily gcrieratc unwarr.;intcttl ~~xclia1igc~-ratc inovemc11ts.

Such “extrinsic” soIIrws of volatility have l)een discussed in the context of rational cxpcctations motlels, for example 13~ Cass and Shell (1983) anti by Azsriadis (1981). Those papers examine whethw cxpectatiolis may fluctuate without any intrinsic or fun- clamcntal reiison and still rcniain “rational.” In contrast, we explore Iwro wllnt happens when expwtatiolis fluctuate and may 1~2 subject to error. (However we will impose some restrictions on the cxpcc- tation errors, having the cfbA of ensuring tllat expectations are not systematically biased.)

III or&r to ~riotlcl c3pcctatirm errors as it sourc’e of exclwigc- rate: disllirl)a~iw wc’ fi1.Q com~~~itc: the mathcrtiatic~tl expectation of tllc: c:xc:ha~~gc r;ltc‘ and tlwu ;wu~no that tlw nlarkct c>xpectation may cl(*viiltc front tlie Iilatlicui;itiwl espwtation. As Xlwsa (1976) has

pointed 0111, “large up and clowii ~novcwle~lts of excli;mge rates . . do not Lwovitlc c.5:itleliw of ;I ci1p1cit): to Illak(\ l)cttcr pwlictions

. \~:lOrc: tlir fAct.” Our prowdurc of strippi11g aw;i!’ all other sourws 01‘ \Ad)ility tiolll 111(* IlIOdcl i\llO\VS 115 to foCUS 011 till! Spt!-

c:ific role of‘ “I)ctli)i.e-tlic:-fl\~t” errors. Swtiori 2 outlines the model ant1 points out thr scope for ex-

change-rate volatility eve11 under fully rational cxpcctations if no long-run patli for tlie 1110ncy silpply is specificcl.

Sec*tion 3 cxalr1ines the co11st*qucnce of a siilglc tralisicnt ex- pwtutioli error on tlio sul,seclllcnt exdiarige rntc: path. ‘I’hc pattern of o\wdwoting is illustrated. C~oncluding remarks arc prescntccl in, Section 4.

2. The Model Ollr 111odc1 tlescritws an cconon~y which is a price taker for

imports, hut not for t!xports, but \vhere the real exchange rate can vary due to clonicstir pric*e sluggishness, Icading to output vari- ations.

‘I‘he five basic eqtiations of the inodcl are

nl, = ap, + (1 - a)c, -I U(r,) (I>eiriancl for Morley) ; (1)

PI = &I, 1 + (1 - f.3)C, (Price Detcrmiuatiou); (2)

e, = s, - I’, + r’ (Exchange-Hate l)ctcrrrii~latiori); (3)

.sI = E(e,, ,) + 14, (Lxchange-Rate IZxpectations); (4)

y, = $cl - ~1,) (Output Deteriniualioi~): (5)

where

r, = uoriiinal interest rate at tinle t: f?, = t)rice of furcign exchange; p1 = t>ricc of clornestic output;

1U, = uotnittal money stuck; yt = (real) output;

= market extmztatiou of c,+,; S’ = foreign nominal interest rate (assumed constant);

E( ) = mathematical expectation (given 1~~ .,).

All time subscripted variables except r re:prcseut logarithms; greek letters denote curistant parameters; u is a randoin disturl)ance.

The first eqiiatiori iudicalcs that the dcrr~and fbr real balailces depends’ ou the nominal interest rate r,. A fixed-weight price index is used to deflate nomiual tnoney. The price of’ irllports is assumed proportional to (lie price of fbreign exchange-i.e., inl~mt prices are assumed fixed in foreign exchange. ‘I’his justifies sul)stituting e for the (log- ) price of imports.

Equation (2) rcpreseuts the sluggisll evolutiori uf domestic prices. IIomcstic prices do riot resporid fully to exchiijic rates in one period.’ The speed of arljustmertt is measu~d hy the parameter (I - p). Equatiou (3) is a statement of the intcrost parity condition in the almnce of risk aversion. We take the interest rate t; to 1~: an exogenous policy variable.

13~ E(tuatiotr (4): exchange-rate cxpcctations c’au deviate from

their rnati~cmatical expectation by the disturbance tcrtn u,. Note that this 1llCiltlS that expectations may bc incorrect cx ante. ‘l’hcre should IW no tlilficlilty in inlagiliing that there coiiltl bc an expec- tatioll error. i.c., tllat the market‘s expectation of tile future cx- change rate might dcviatc frown the mathematical expectation, when we know that so much inli)rmation is constantly being rcccived by the foreign exchange market and interpreted by participants as best they can. A Mse rumor, or an ambiguous statement, concerning the authorities’ policy intentions is an especially plarisible example of something that nlight cause a disturbance of the type envisaged.

Finally output, recursive to the rest of the model, is propor- tional to the real exchange rate by Equation (5).

A stationary equilibrillin of this model, in the absence of dis- turbances, would bc consistent with r, = r’ and would involve

y=o.

The stationary value of 13 is arbitrary in the absence of further con- ditions. The same arbitrariness applies a fortiori to the current ex- change rate out of stationary equilibrium. An extra condition is re- quired to eliminate the indeterminacy. Consequently, if the interest rate were the only variable tlctcrmined by the monetary authorities (the money stock being completely passive), an arbitrarily large de- gree of exchange-rate volatility could be consisteilt with perfect foresight.

The additional equation reyuirccl to rule out this indetermi- ilacy is a long-term consistency or “transvcrsality” condition. In par- ticillar, we assume that the authorities have a target for the long- rut1 level of the money stock, and WC restrict the expectations by requiring that the sequence of exchange rates determined by Equa- tions (2)-(4) ensures, througli (I.), convergence of the nominal money stock to the given target le~el.~

31t may be noted that the tmnsversality conclition is hvofdd: not only does it require that the exchange-rate path be :I convergent one [thereby ruling out the speculative “bubble” type of path, cf. Hahn (1966). Sargent and Wallace (1973) and, in the context of exchange-rate models. Gray and Turnovsky (1979)], but it also requires that the convcrgont path be consistent with thr authorities plans for the long run or asymptotic’ money stock. In this latter rcsprct it rloscly resemhlcs the policy discusted by McCallum (1981).

Expectation Errors, Excha,nge-Kate Vokdity

3. Response to a Single Shock We now consider how the optimizing monetary authorities will

revise their plans for the long-run money stock in response to dis- turbances. We examine the effects of a single shock and we simplify by assuming that the authorities hold the interest rate fixed” at the exogenous foreign level

rt = rf (6)

We assume that the authorities are concerned both with output and the price level. We assume that the economy is in a stationary equilibrium before the shock, with

e=p=y=O.

If a shock at time one leads to the authorities revising their long-term money stock plans’ so that the new stationary equilib- rium has

p=pm>o,

then p, measures the net amount of inflation which will occur in the passage to the new stationary equilibrium.

The net output loss resulting from the shock is measured as

We therefore assume that the authorities act as though they were maximizing an objective function of the form

U(CYt, -pm) .

4The fixed interest rate assumption means that monetary policy is not fully op- timal unless the perceived cost of fluctuations is very high. However, apart from providing a considerable analytical simplification, this assumption serves to model the behavior of monetary authorities which are averse to interest-rate fluctuations for reasons of structural efficiency in the financial markets. The traditional function of central banks as lender of last resort tends to inhibit the authorities from allowing interest-rate fluctuations which can adversely affect “both the functioning of these markets and the liquidity of the banking system” [HM Treasury and the Bank of England (1980)].

5By choosing a long-term money stock m,, the authorities are also implicitly choosing a long-term price level p, and exchange rate e, with p, = e,, and p- = m, - e(d).

327

Patrick Honohan

Since the output change in period one resulting from the distur- bance is a bygone so far as policy is concerned, the summation is taken from period two on.

Let the shock at time one be represented by U, = a # 0. We prefer to interpret this shock as an expectation error, as specified in Equation (4).

If the expectation error is completely eliminated after one pe- riod, we have u2 = 0. More generally, we may assume

uf = pl-‘a , t = 2, 3, . . . ; (8)

where 0 5 F < 1. Kecalling Equations (2) and (5) we see that, as an immediate

consequence of the disturbance u1 = a, prices and output both jump from zero to

Pl = (1 - Pkl ;

YI = he1 . (9

Hut the relationship between a and e, depends on the authorities’ response to the shock. For instance, if a > 0, so that the exchange rate depreciates, it would involve a loss of output from now on to claw back the depreciation and rise in domestic prices which has occurred. While there has been a transitory gain in output it is the future losses which must concern the authorities. The price/output trade-off has shifted. Accordingly, the authorities will wish to change the target asymptote for the price level. In order to evaluate their choice, we need to obtain expressions for e,, p,, and yt as functions of p, = lim pt. This is done by solving (2)-(5) taking into account

(6) and (8TmIn particular (8) makes the system deterministic, so that

E(e,+J = e,+, .

The solution is as follows

e, = pm +- [a/(1 - i41Pt-’ ; (10)

(11)

and

328

Expectation Errors, Exchange-Rate Volatility

yt = Pr{[al(P - 141~~~ + (A + PJP”~‘~) ; (12)

where

A = 41 - PI/b- - PN - CL) . In particular, from (10) we have

e, = lim e, = p, t--t=

e, = e, + a/(1 - A

Also

(13)

04)

C Yt = PrUPI(l - P)lpx - a/(1 - 1.4) 1=2

= lMl/(l - p)]& - e,} . (15)

Equation (IS) is the trade-off facing the authorities following the disturbance U, = a. As compared with the trade-off before the dis- turbance, it has the same slope, hut a different intercept (see Fig- nre 1).

If the authorities want to avoid any output loss they must tol- eratc a value of p, = (1 - P)e,. If they want to retain the old asymptote p, = 0, then they must tolerate an output loss of @yel. In general they will choose some intermediate point, accepting some inflation

0 5 e, = p, 5 (1. - f3)el

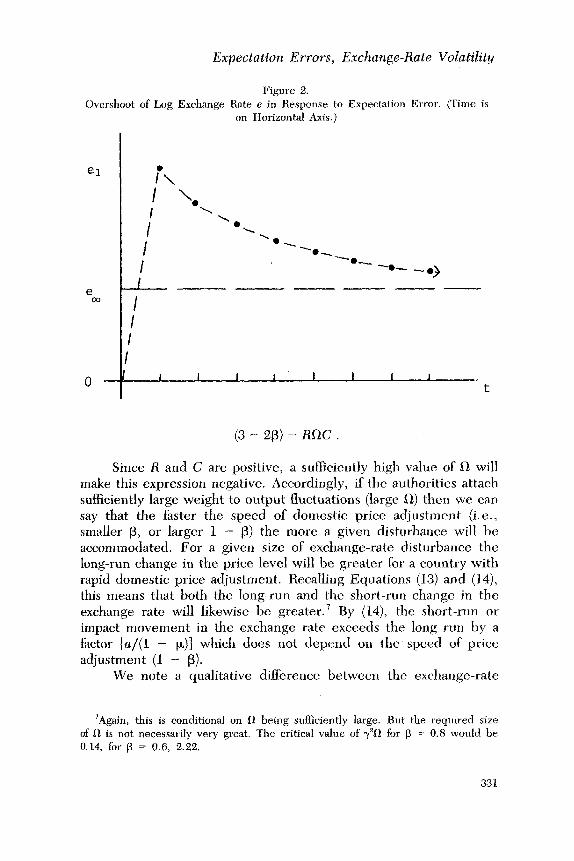

and some output loss. The fact that e, lies between 0 and e, means that ei is an overshoot: the shuck to the exchange rate will be par- tially reversed. The time path of the exchange rate (for a > 0) is illustrated in Figure 2.

Specializing the objective function (7) to

(min) p: 4 fl(Zy)” , Q > 0 .

‘This variable e, acts like an income effect in the sense that it shifts the gov- ernment’s trade-off or “budget line” without altering its slope-the relative “price” of output and inflation.

Patrick Honohan

Figure 1. ‘rrade-off between Change in Price Level (pJ and Change in Output (-Z,Xy),

before (n = 0) and after (a > 0) Shock. (Dotted Line Represents Social Indifference Curve.)

we can easily use (15) to evaluate the optimal choice of p- as

Rf1B n pffi=l+RRC’

where

R = @y)” > 0 ;

c = [P/(1 - P)]" > 0 ;

B = [P/U - P)ld(l - d .

It is of interest to know whether an increase in the speed of do- mestic price adjustment increases or reduces the response of firn to a given shock a. Some manipulation reveals that the sign of a@,/ ap equals the sign of

330

Expectation Errors, Exchange-Rate Volatility

Figure 2. Overshoot of Log Exchange Rate e in Response to Expectation Error. (Time is

on Horizontal Axis.)

el l

I’\.

;

\ ‘e

I ‘*

-. l N

I -@-

-*- -*

I 3

e ---- co

I

I

I

I

0 I I I I I I I 1 I

t

(3 - Z(3) - Rfi2C .

Since R and C are positive, a sufficiently high value of R will make this expression negative. Accordingly, if the authorities attach sufficiently large weight to output fluctuations (large 0) then we can say that the faster the speed of domestic price adjustment (i.e., smaller B, or larger 1 - R) the more a given disturbance will be accommodated. For a given size of exchange-rate disturbance the long-run change in the price level will be greater for a country with rapid domestic price adjustment. Recalling Equations (13) and (14), this means that both the long-run and the short-run change in the exchange rate will likewise be greater.7 By (14), the short-run or impact movement in the exchange rate exceeds the long run by a factor [a/(1 - k)] which d oes not depend on the speed of price adjustment (1 - B).

We note a qualitative difference between the exchange-rate

‘Again, this is conditional on II being sufficiently large. But the required size of 0 is not necessarily very great. The critical value of ~‘0 for p = 0.8 would be 0.14, for p = 0.6, 2.22.

331

volatility occurrittg ltcrc attd that itt the well-kttowtt models of Nie- hairs (1975) and 11 ottt Busch (1976). III their tttodcls, government ac- - I tiott cs~ablishcs ;t ttew ec~ttilibriutn and, because of diffcrcntial speeds of adjttstmcttt itt &II&rent sectors of the economy, the fastest ad- jttstittg sector, i.e., dtc foreign exchange market, experiences a greater price change ittitially Ihart in &c ultimate equilibrium. The Dortt- busch-Nichatts type of overshoot is thus an instance of the Sam- uelsort--(7hatclicr principle. In the present model, by contrast, the private sector initiates the disturbance which is an overshoot bc- ca~tsc the authoritic:s choose not to ac:cornrrtoclate it fttlly. Indeed, our cottclusiott that the tlcgrcc of cxchatigc-rate rrtovetrtcnt for a given shock (1 is likely to bc positively cot-related with the speed of dontcslic price adjrtsttttent, is quilt opposite to what is implied by the I>oriil)ttslt--Nicllnlls fratttcwork.R

To suttttttat-izc the argutrtettt of this scdion, a sudden deprc- ciatiott itt the r~xdtattge I-ate, tluc lo a cltange in expectations itt- volvittg 3 1r;msitory dcvialion fi.otr-t ratiortal expectations, causes the authorities lo react l)y iticrcasittp ltteir targel for the: nominal money st-ock. They do this becattse, although there Iias bcert art initial ottt- pttt- gain due to the cotttpe’titive advantage conferred by the dcpre- ciation, getting back lo the origind tttoney stock and price level t;irget would ittvolvct otttput sacrifices iii stibsequcnt periods. As il result, the cscltnngc rate rc:turtts some of die way towards ils orig- ittal Icvel. Tltc patIt of‘ the cxcl~at~ge note is ~.hus att ovcrshoot.Y

4. Conclusions Wtcrc att ottt~)ul-sc~ttsitivc tttottc:tary authority is surrounded

bv a jtttttl)y. rttnior-prottc forcigrt exchattgc tttnrket, tlte COIISF- quet~ccs for exthangc~-rate variability can be scvcrc. It is hard to think of arty rcasot~ why fi)recastittg errors co111~l nuf be very large, especially c~onsitlc!t-ittg the 0bscrvet-l variabilily of exchange rates. Accordittgly, the ft-acliott of‘ exchange rate variat-ion attributable to f&casting errors tttay ttc sttl~st;inti~tl. While the existing literature does ilttril)lllC sotnc cxchartgc-rate v;triability to r;indotn fluotrtations

Expectation Errors, Exchange-Rate Volatility

in information concerning the long-run equilibrium exchange rate [e.g., Mussa (1976) and Helliwell (1979)l it seems to attach much more importance to the Dornbusch-Niehans overshooting with its source in money market shocks.

Our main conclusion is that private sector expectation shocks will lead to an enduring revision of price objectives by the author- ities. Exchange rates will overshoot in response to these shocks and the resulting volatility of exchange rates may be positively corre- lated with the speed of domestic price adjustments. This result sug- gests an empirical test of the relative importance of, on the one hand, shocks initiated by monetary policy-and leading to over- shooting of the Dornbusch-Niehans type-and, on the other hand, shocks coming from private sector expectational errors-leading to our type of overshooting. If exchange-rate volatility is positively correlated with the speed of domestic price adjustment, then this would seem to indicate that shocks emanate mainly from, private sector expectational errors. Some tentative evidence for this prop- osition already exists in Honohan (1983), where variability of both nominal and real exchange rates (measured around the expected path of the exchange rate) are found to be strongly positively correlated across countries with the average rate of inflation. This suggests that carrying out a more direct test (related to speed of adjustment rather than inflation) would be worthwhile.

Receiued: Jtrne 1982 Final version received: Februcwy 1984

References Aoki, M. Optimal Colatrol and System Theory in Dynamic Eco-

nomic Analysis. Amsterdam: North-Holland, 1976. Azariadis, C. “Self-Fulfilling Prophecies.” Journal of Economic The-

oy 25 (December 1981): 380-96. Baschnagel, H., G. Bell, H. Evers, H.K. Goeltz, S.E. Pardee, D.

Weatherstone, V.R. Blake, and R.D. Pringle. The Foreign Ex- change Market under Floating Rates. New York: Group of Thirty, 1980.

Cass, D., and K., Shell. “Do Sunspots Matter?’ Journal of Political Economy 91 (April 1983): 193-227.

Dornbusch, R. “The Theory of Flexible Exchange Rate Regimes and Macroeconomic Policy. Scandinavian Journal of Economics 78 (1976): 255-75.

333

Patrick Honohan

-. “Expectations and Exchange Rate Dynamics.” Journal of Political Economy 84 (December 1976): 1161-76.

Feldstein, M.S., “The Welfare Cost of Permanent Inflation and Op- timal Short-Run Economic Policy.” Journal of Political Economy 87 (August 1979): 749-68.

Gray, M.R., and S. J. Turnovsky. “The Stability of Exchange Rate Dynamics under Perfect Myopic Foresight.” Znt~mational Eco- nomic Review 20 (October 1979): 643-60.

Hahn, F.H. “Equilibrium Dynamics with Heterogeneous Capital Goods. ” Quarterly J ozcrnal of Economics 80 (November 1966): 633-46.

Helliwell, J. F. “Policy Modelling of Foreign Exchange Rates.” Journal of Policy ModelZing 1 (September 1979).

HM Treasury and the Bank of England. Monetary Control. London: HMSO, 1980.

Honohan, I?. “Measures of Exchange Rate Variability for One Hundred Countries.” AppZied Economics 15 (October 1983): 583- 602.

McCallum B.T. “Price Level Determinancy with an Interest Rate Policy Rule and Rational Expectations,” JournuZ of Monetury Economics 8 (November 1981): 319-29.

Mussa, M. “The Exchange Rate, the Balance of Payments and Monetary and Fiscal Policy under a Regime of Controlled Float- ing.” Scanadinavian Journal of Economics 78 (1976): 229-48.

Niehans, J. “Some Doubts about the Efficacy of Monetary Policy under Flexible Exchange Rates.” Journal of International Eco- nomics 5 (August 1975): 275-81.

Sargent, T. J., and N. Wallace. “The Stability of Models of Money and Growth with Perfect Foresight.” Econometrica 41 (Novem- ber 1973): 1043-48.

334