existing revenue sources of the municipal council · pdf fileexisting revenue sources of the...

TRANSCRIPT

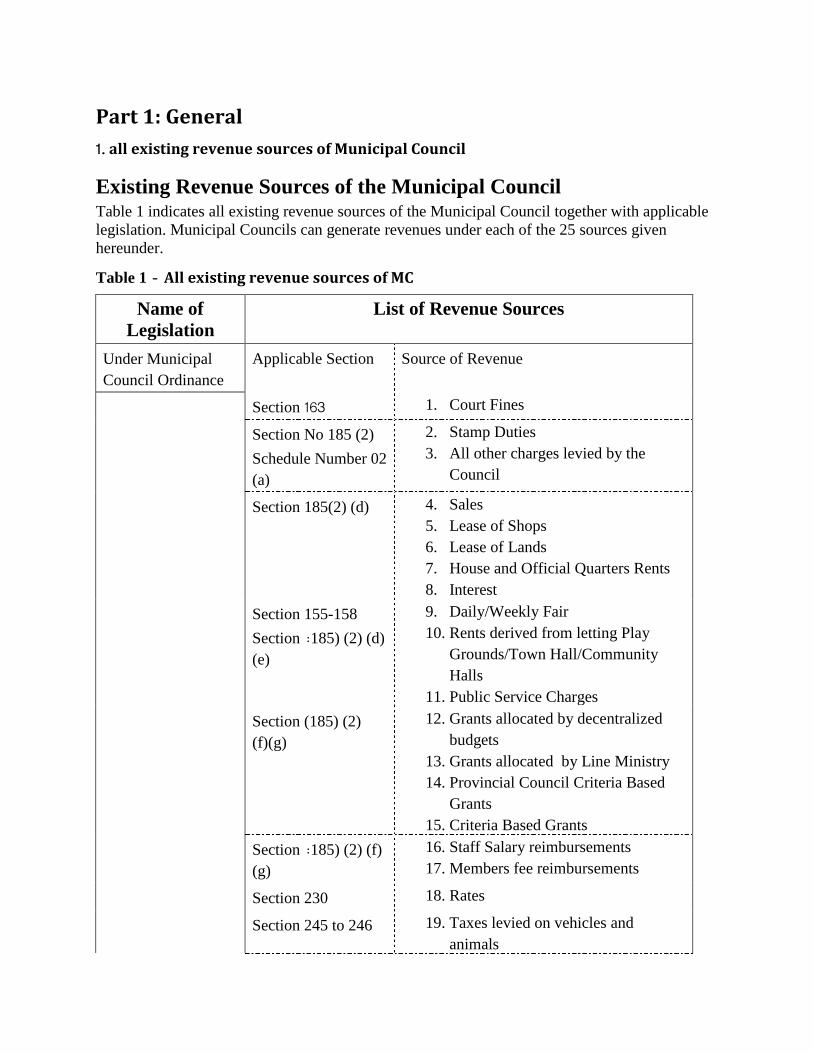

Part 1: General

1' all existing revenue sources of Municipal Council

Existing Revenue Sources of the Municipal Council Table 1 indicates all existing revenue sources of the Municipal Council together with applicable

legislation. Municipal Councils can generate revenues under each of the 25 sources given

hereunder.

Table 1 - All existing revenue sources of MC

Name of

Legislation

List of Revenue Sources

Under Municipal

Council Ordinance

Applicable Section Source of Revenue

Section 163 1. Court Fines

Section No 185 (2)

Schedule Number 02

(a)

2. Stamp Duties

3. All other charges levied by the

Council

Section 185(2) (d) 4. Sales

5. Lease of Shops

6. Lease of Lands

7. House and Official Quarters Rents

8. Interest

Section 155-158

Section (185) (2) (d)

(e)

9. Daily/Weekly Fair

10. Rents derived from letting Play

Grounds/Town Hall/Community

Halls

11. Public Service Charges

Section (185) (2)

(f)(g)

12. Grants allocated by decentralized

budgets

13. Grants allocated by Line Ministry

14. Provincial Council Criteria Based

Grants

15. Criteria Based Grants

Section (185) (2) (f)

(g)

16. Staff Salary reimbursements

17. Members fee reimbursements

Section 230 18. Rates

Section 245 to 246 19. Taxes levied on vehicles and

animals

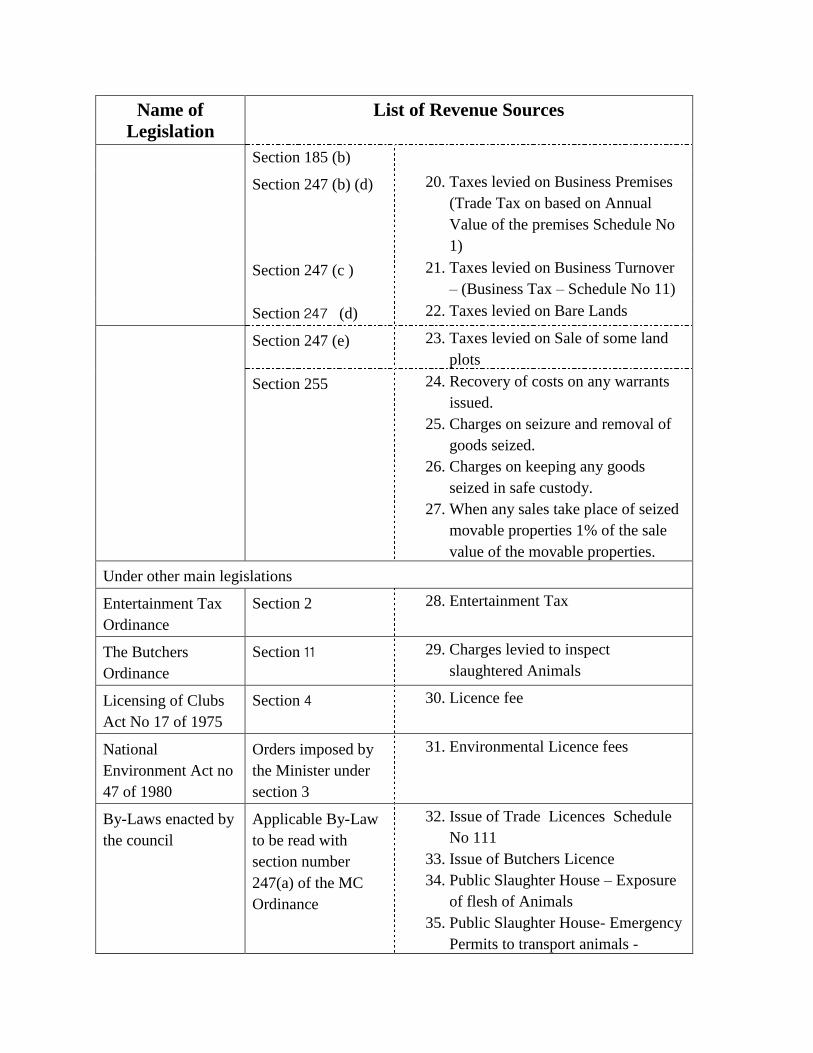

Name of

Legislation

List of Revenue Sources

Section 185 (b)

Section 247 (b) (d) 20. Taxes levied on Business Premises

(Trade Tax on based on Annual

Value of the premises Schedule No

1)

Section 247 (c ) 21. Taxes levied on Business Turnover

– (Business Tax – Schedule No 11)

Section 247 (d) 22. Taxes levied on Bare Lands

Section 247 (e) 23. Taxes levied on Sale of some land

plots

Section 255 24. Recovery of costs on any warrants

issued.

25. Charges on seizure and removal of

goods seized.

26. Charges on keeping any goods

seized in safe custody.

27. When any sales take place of seized

movable properties 1% of the sale

value of the movable properties.

Under other main legislations

Entertainment Tax

Ordinance

Section 2 28. Entertainment Tax

The Butchers

Ordinance Section 11 29. Charges levied to inspect

slaughtered Animals

Licensing of Clubs

Act No 17 of 1975 Section 4 30. Licence fee

National

Environment Act no

47 of 1980

Orders imposed by

the Minister under

section 3

31. Environmental Licence fees

By-Laws enacted by

the council Applicable By-Law

to be read with

section number

247(a) of the MC

Ordinance

32. Issue of Trade Licences Schedule

No 111

33. Issue of Butchers Licence

34. Public Slaughter House – Exposure

of flesh of Animals

35. Public Slaughter House- Emergency

Permits to transport animals -

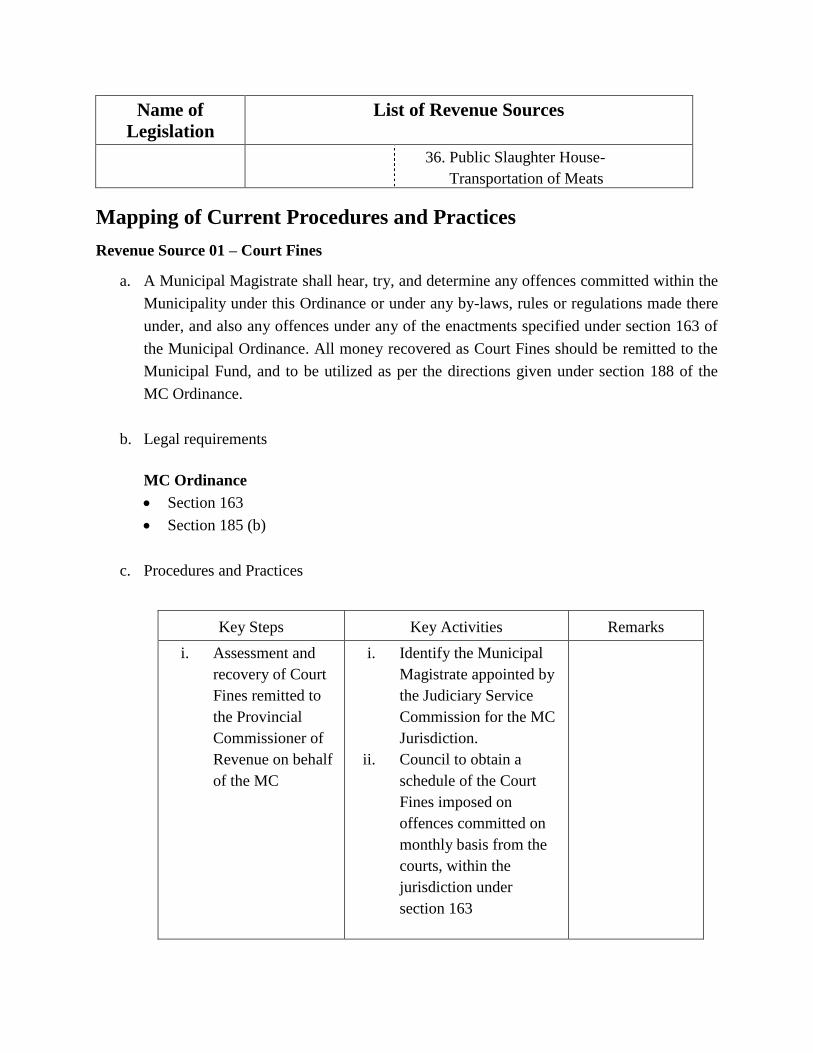

Name of

Legislation

List of Revenue Sources

36. Public Slaughter House-

Transportation of Meats

Mapping of Current Procedures and Practices

Revenue Source 01 – Court Fines

a. A Municipal Magistrate shall hear, try, and determine any offences committed within the

Municipality under this Ordinance or under any by-laws, rules or regulations made there

under, and also any offences under any of the enactments specified under section 163 of

the Municipal Ordinance. All money recovered as Court Fines should be remitted to the

Municipal Fund, and to be utilized as per the directions given under section 188 of the

MC Ordinance.

b. Legal requirements

MC Ordinance

Section 163

Section 185 (b)

c. Procedures and Practices

Key Steps Key Activities Remarks

i. Assessment and recovery of Court

Fines remitted to

the Provincial

Commissioner of

Revenue on behalf

of the MC

i. Identify the Municipal

Magistrate appointed by

the Judiciary Service

Commission for the MC

Jurisdiction. ii. Council to obtain a

schedule of the Court

Fines imposed on

offences committed on

monthly basis from the

courts, within the

jurisdiction under

section 163

iii. Council to prepare a

schedule of fines

receivable.

iv. Council to submit the

schedule to the

provincial commissioner

of revenue for

reimbursement.

v. Council to maintain a

register for “Court

Fines” to reconcile the

amount

receivable/received from

the Provincial

Commissioner of

Revenue.

Revenue Source 02– Stamp Duty

a. Municipal Council can recover all Stamp Duties accorded to the Council as per the

Second Schedule of the MC Ordinance. All such revenue should be remitted to the

“Municipal Fund” and to be utilized as per the directions given under section 188 of the

MC Ordinance.

b. Legal requirements

MC Ordinance

Section 185 (2) (c)

Second Schedule

c. Procedures and Practices

Key Steps Key Activities Remarks

i. Identify the offices of

the Land Registrar

assigned to register

the property deeds

for the council area.

i. Identify the additional

district registrar’s

office within the

jurisdiction of the

council.

ii. Identify the District

registrar’s office for

the jurisdiction of the

council

Deeds could

be registered

in any one of

these offices

within the

jurisdiction of

the council.

ii. Identify the lands

registered in these

offices

i. Visit the above offices

at least once in two

weeks and inspect the

registration schedules.

ii. Identify the lands

registered within the

jurisdiction of the

council

iii. Record the

information and the

stamp duties

applicable to each

property register

iii. Request for the

stamp duty

receivable by the

council.

i. Prepare a schedule of

stamp duty receivable

by the council.

ii. Obtain a confirmation

from the registrar of

lands

iii. Submit the schedule

confirmed by the

registrar of lands to

the Provincial

Commissioner of

Revenue for

reimbursement.

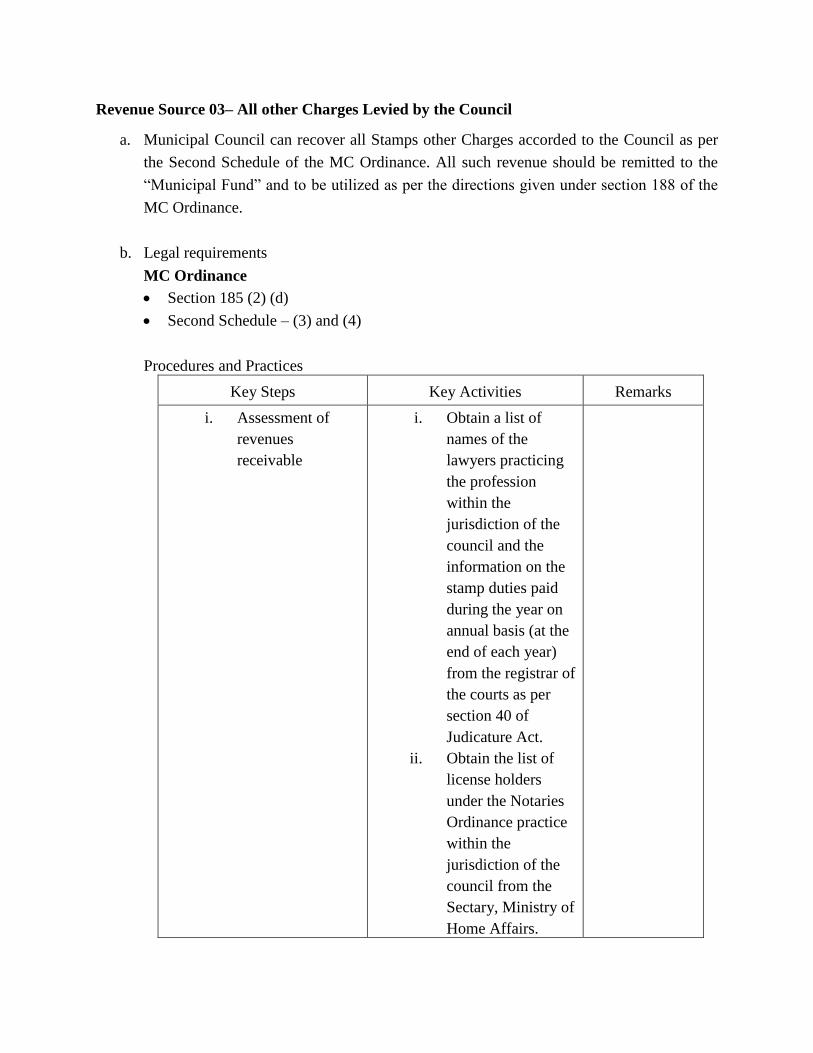

Revenue Source 03– All other Charges Levied by the Council

a. Municipal Council can recover all Stamps other Charges accorded to the Council as per

the Second Schedule of the MC Ordinance. All such revenue should be remitted to the

“Municipal Fund” and to be utilized as per the directions given under section 188 of the

MC Ordinance.

b. Legal requirements

MC Ordinance

Section 185 (2) (d)

Second Schedule – (3) and (4)

Procedures and Practices

Key Steps Key Activities Remarks

i. Assessment of

revenues

receivable

i. Obtain a list of

names of the

lawyers practicing

the profession

within the

jurisdiction of the

council and the

information on the

stamp duties paid

during the year on

annual basis (at the

end of each year)

from the registrar of

the courts as per

section 40 of

Judicature Act. ii. Obtain the list of

license holders

under the Notaries

Ordinance practice

within the

jurisdiction of the

council from the

Sectary, Ministry of

Home Affairs.

iii. Obtain a names of

the auditors

registered within

the jurisdiction

from the Provincial

registrar of

Companies.

Request for stamp duties

receivable under other

Acts and Ordinances.

i. As per above

information prepare

a list of stamp

duties receivable

from each

institution

ii. Forward the

schedule to the

assistant secretary

of the treasury for

reimbursement

Revenue Source 04 – Sales

a. Municipal Council can generate additional revenue by sale or lease of items belonging to

the council E.g.; Discarded items, old newspapers, produce from home gardens, compost

produced by the council, sale of recycle items collected by the council etc.

b. Legal requirements

MC Ordinance

Section 185 (2) (d)

c. Procedures and Practices

Key Steps Key Activities Remarks

i. Identification of items to

be sold by the council

i. Conduct an annual

survey to identify the

items that are usable,

discarded and written

off.

ii. Submit the schedule

of items to the Board

of Sale for initial

authorization

Key Steps Key Activities Remarks

ii. Sale of items iii. Appoint a suitable

person to carry out the

valuation iv. Obtain the council

approval. v. Decide the mode to

advertise the sale E.g.-

Newspaper

advertisement,

handbills, notice board

etc. vi. Set the lowest bid and

sell the items by

tenders/auctions any

other method

approved by the

council.

Revenue Source 05 – Lease of Shops

a. Municipal Council can generate additional revenue by lease of shops belonging to the

council

b. Legal requirement

MC Ordinance

Section 185 (2) (d)

c. Procedures and Practices

Key Steps Key Activities Remarks

i. Calling for Tenders

at the initial leasing

of shops

i. Allocation of Shops for

trading purposes. ii. Prepare Tender Notice

and Draft copy of

Agreement iii. Obtain Council

Approval for Tender

notice and Draft

Agreement

Key Steps Key Activities Remarks

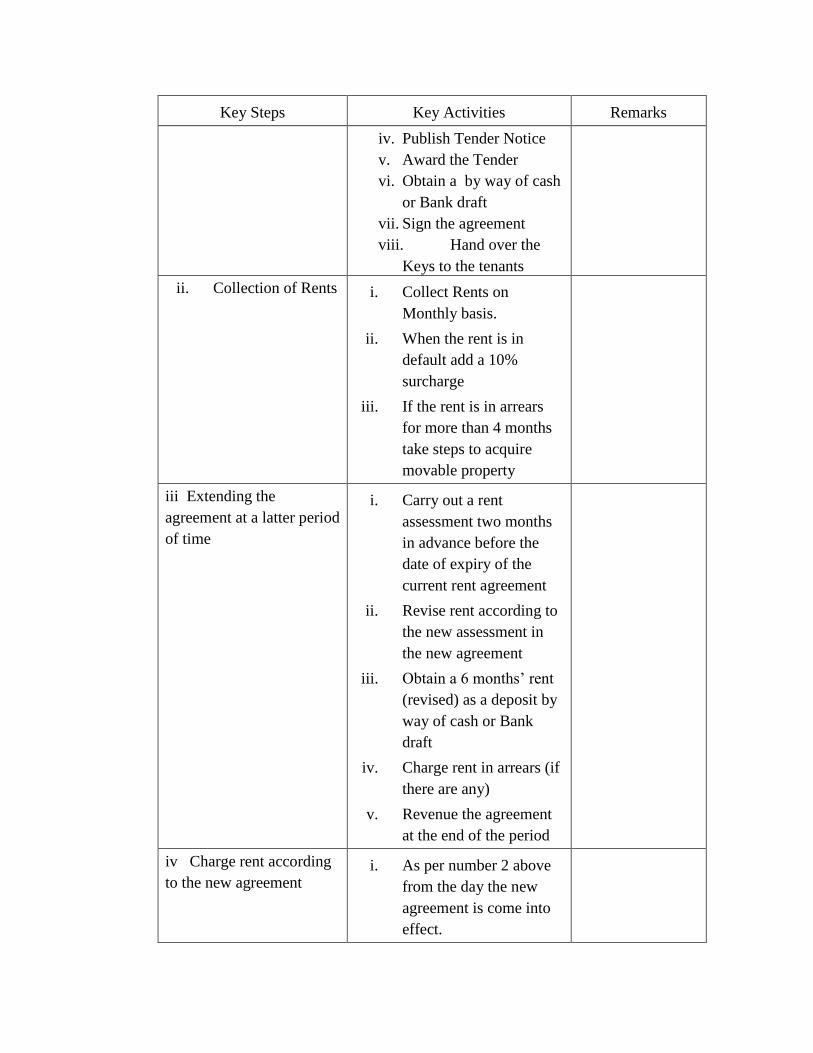

iv. Publish Tender Notice

v. Award the Tender

vi. Obtain a by way of cash

or Bank draft

vii. Sign the agreement

viii. Hand over the

Keys to the tenants

ii. Collection of Rents i. Collect Rents on

Monthly basis.

ii. When the rent is in

default add a 10%

surcharge

iii. If the rent is in arrears

for more than 4 months

take steps to acquire

movable property

iii Extending the

agreement at a latter period

of time

i. Carry out a rent

assessment two months

in advance before the

date of expiry of the

current rent agreement

ii. Revise rent according to

the new assessment in

the new agreement

iii. Obtain a 6 months’ rent

(revised) as a deposit by

way of cash or Bank

draft

iv. Charge rent in arrears (if

there are any)

v. Revenue the agreement

at the end of the period

iv Charge rent according

to the new agreement i. As per number 2 above

from the day the new

agreement is come into

effect.

Key Steps Key Activities Remarks

V Approval of ownership

to operate the Shop as per

agreement.

i. Confirm the identity of

the shop owner once a

month

ii. If the shop is sub-let

notify the owner the

cancellation of

agreement

iii. If the tenant does not

adhered to the notice

take steps to seal the

shop

iv. Follow steps as per

initial renting of shops

when the acquired shops

are rented to new

tenants.

This investigation

will be a duty of

Revenue

Inspector/Revenue

supervisor or if

there is any officer

in charge of

managing the

shops

a. Sources of Income 5 - Renting Market Stalls on Long Term Lease. Municipal Council can generate revenue by constructing Public Market Buildings and

renting market stalls on monthly rental basis. This additional revenue is to be utilized

to provide public utility services for citizens.

b. Legal requirements

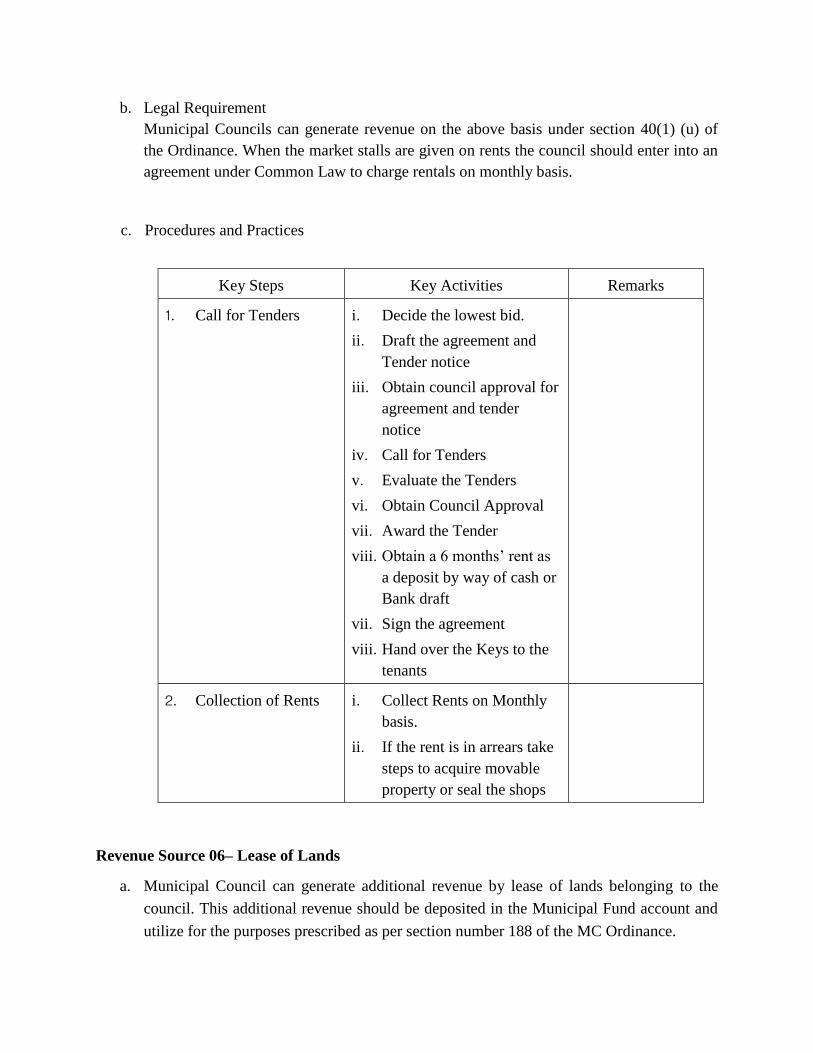

Municipal Councils can generate revenue by renting Market Stalls under section 40(1)

(u) (iv) of the Ordinance. When the market stalls are given on rents the council should

enter into an agreement under Common Law to charge rentals on monthly basis.

c. Procedures and Practices

Key Steps Key Activities Remarks

1. Calling for Tenders at

the initial leasing of

shops,

i' Allocation of Shops

for trading

purposes.

ii' Prepare Tender

Notice and Draft

copy of Agreement

iii' Obtain Council

Approval for Tender

notice and Draft

Agreement

iv' Publish Tender

Notice

v' Award the Tender

vi' Obtain a 6 months’

rent as a deposit by

way of cash or

Bank draft

vii' Sign the agreement

viii' Hand over the Keys

to the tenants

2. Collection of Rents i' Collect Rents on

Monthly basis.

ii' When the rent is in

default add a 10%

surcharge

iii' If the rent is in

arrears for more

than 4 months take

steps to acquire

movable property

3. Extending the

agreement at a latter

period of time

i' Carry out a rent

assessment two

months in advance

before the date of

expiry of the

current rent

agreement

ii' Revise rent

according to the

new assessment in

the new agreement

iii' Obtain a 6 months’

rent (revised) as a

deposit by way of

cash or Bank draft

iv' Charge rent in

arrears (if there are

any)

v' Revenue the

agreement at the

end of the period

4. Charge rent

according to the new

agreement

i' As per number 2

above from the day

the new agreement

is come into effect.

5. Approval of

ownership to operate

the Shop as per

agreement.

i' Confirm the

identity of the shop

owner once a

month

ii' If the shop is sub-

let notify the owner

the cancellation of

agreement

iii' If the tenant does

not adhered to the

notice take steps to

seal the shop

iv' Follow steps as per

initial renting of

shops when the

acquired shops are

rented to new

tenants.

This investigation

will be a duty of

Revenue

Inspector/Revenue

supervisor or if

there is any officer

in charge of

managing the

shops

Source of Income - Renting Market Stalls (Meat Stalls) on Annual Basis (By

Tenders)

a. The Council can generate revenue by constructing Meat Stalls and renting these stalls on

monthly rental basis. This additional revenue is to be utilized to provide public utility

services for citizens.

b. Legal Requirement

Municipal Councils can generate revenue on the above basis under section 40(1) (u) of

the Ordinance. When the market stalls are given on rents the council should enter into an

agreement under Common Law to charge rentals on monthly basis.

c. Procedures and Practices

Key Steps Key Activities Remarks

1' Call for Tenders i' Decide the lowest bid.

ii' Draft the agreement and

Tender notice

iii' Obtain council approval for

agreement and tender

notice

iv' Call for Tenders

v' Evaluate the Tenders

vi' Obtain Council Approval

vii' Award the Tender

viii' Obtain a 6 months’ rent as

a deposit by way of cash or

Bank draft

vii' Sign the agreement

viii' Hand over the Keys to the

tenants

2' Collection of Rents i' Collect Rents on Monthly

basis.

ii' If the rent is in arrears take

steps to acquire movable

property or seal the shops

Revenue Source 06– Lease of Lands

a. Municipal Council can generate additional revenue by lease of lands belonging to the

council. This additional revenue should be deposited in the Municipal Fund account and

utilize for the purposes prescribed as per section number 188 of the MC Ordinance.

b. Legal requirement

MC Ordinance

Section 185 (2) (d)

c. Procedures and Practices

Key Steps Key Activities Remarks

1. Calling for Tenders

at the initial leasing

of shops

i. Allocation of lands

available in the council

area that could be given

on lease ii. Prepare Tender Notice

and Draft copy of

Agreement iii. Obtain Council

Approval for Tender

notice and Draft

Agreement iv. Publish Tender Notice

v. Award the Tender

vi. Obtain a by way of cash

or Bank draft

vii. Sign the agreement and

hand over the tenancy.

2. Collection of Rents i. Collect Rents on

Monthly basis.

ii. When the rent is in

default add a 10%

surcharge

iii. If the rent is in arrears

for more than 4 months

take steps to acquire

movable property

3. Extending the

agreement at a latter

period of time

i. Carry out a rent

assessment two

months in advance

before the date of

expiry of the current

rent agreement

Key Steps Key Activities Remarks

ii. Revise rent

according to the new

assessment in the

new agreement

iii. Obtain a 6 months’

rent (revised) as a

deposit by way of

cash or Bank draft

iv. Charge rent in

arrears (if there are

any)

v. Revenue the

agreement at the end

of the period

4. Charge rent according

to the new agreement

i. As per number 2

above from the day

the new agreement

is come into effect.

5. Approval of ownership

to operate the Shop as

per agreement.

i. Confirm the identity of

the shop owner once a

month

ii. If the shop is sub-let

notify the owner the

cancellation of

agreement

iii. If the tenant does not

adhered to the notice

take steps to seal the

shop

iv. Follow steps as per

initial renting of shops

when the acquired shops

are rented to new

tenants.

This investigation

will be a duty of

Revenue

Inspector/Revenue

supervisor or if

there is any officer

in charge of

managing the

shops

Revenue Source 07– Houses and Official Quarters Rents

a. Municipal Council can generate revenue by renting the houses and official quarters

belonging to the council. Revenue generated through rents should be deposited in the

Municipal Fund Account and utilize in accordance with section 188 of the MC

Ordinance.

b. Legal requirement MC Ordinance

Section 185 (2) (d)

c. Procedures and Practices

Key Steps Key Activities Remarks

1. Identify the

officers who are

entitle to official

quarters

i. Prepare a internal policy

applicable for official

quarters

ii. Inform the occupant that

the council is ready to

handover the official

quarters as per the

council policy.

2. Handing over of

the official

quarters and

charging the

monthly rentals.

i. Enter into a rent

agreement before

tenancy

ii. Handover the

quarters to the

occupant

iii. Charge rents from

the monthly salary of

the officer.

Revenue Source 08– Interest

a. Municipal Councils can invest funds in Banks or Other Financial Institutions and

generate interest on such investments. These interests could be collected on quarterly or

on annual basis. Revenue generated through interest should be deposited in the Municipal

Fund Account and utilize as per the directions given under section 188 of MC Ordinance.

b. Legal requirement MC Ordinance

Section 185 (2) (d)

c. Procedures and Practices

No specific procedure or practice, but will be based on the standard accounting principles

and practices.

Revenue Source 09– Daily/Weekly Fair

a. Municipal Councils may from time to time, as occasions requires, provide places within

the Municipality for the purpose of being used as public markets, and may charge such

rents, tolls and fees as to it may seen fit for use of, or the right to expose goods for sale in,

such markets and for the use of shops stalls sheds, pens, and standing therein. Revenue

generated through interest should be deposited in the Municipal Fund Account and utilize

as per the directions given under the section 188 of the MC Ordinance.

b. Legal requirement MC Ordinance

Section 185 (2) (d)

c. Procedures and Practices

Key Steps Key Activities Remarks

1. Council to decide

the method of

collecting the

revenue from the

daily/weekly fair

i. Council to decide the

policy of charging the

rents i.e. through the

council officers, or

tender and collecting the

lease rents

ii. Decide the rents charged

for shops, stalls, pens

and standing therein.

If the council revenue officers are collecting rents assign them on daily basis to

collect the rents.

2. If tender system is

used call for

tenders

i. Decide the minimum

bid.

Revenue Source 10– Rents derived from letting Play Grounds/Town Hall/Community Halls

a. Municipal Councils may from time to time, as occasions require can hire play grounds,

town halls and community halls for temporary occupancy. Revenue generated through

these processes should be deposited in the Municipal Fund Account and utilize as per the

directions given under the section 188 of the MC Ordinance.

b. Legal requirement MC Ordinance

Section 185 (2) (d)

c. Procedures and Practices

Key Steps Key Activities Remarks

1. Decide the rents

charged.

i. Calculate the rents

based on usage of

water, electricity and

cleaning and

maintenance of the

premises that will be

hired on temporary

basis.

ii. Calculate the

charges on extra

hours for water and

electricity. Consider

the overtime payable

to workers for the

additional hours.

iii. Add extra 5% to the

base rate calculated

on the above and

decide on the rents

chargeable from the

occupants iv. Calculate the extra

hourly charges and

add another 5% to

the base rate for the

extra hour charges.

v. Make a council

decision on the rents

charged based on the

above calculations.

2. Premises given on rent i. Identify an officer in

charge of allocating the

premises.

ii. When the premises are

allocated charge the

rents accordingly

Revenue Source 11– Public Service Charges

a. Municipal Council can generate additional revenue by providing services on a fee basis

to the public. These fees are collected for the services provided at personal levels by the

Council. The fees charged for services such a s clearing of blocked drains and drainage,

removal of branches and other parts of trees cut down on the roads by persons, providing

services of crematoriums, hiring of heavy equipment owned by the council are some of

the examples. Revenue received from such services should be deposited in the Municipal

Fund and utilize according to section 188 of the MC Ordinance.

b. Legal requirement MC Ordinance

Section 185 (2) (d)

c. Procedures and Practices

Key Steps Key Activities Remarks

1. Identify the

services provided

by the council

i. Identify the

machinery/gully

bowsers/crematoriums

that are owned by the

council and the other

series provided.

ii. Calculate the rates

based on the system

provided in section 10

above

Clearing of blocked

drains and drainages,

removal of brancyes

and other parts of

trees cutdown on the

roads by persons

providing services of

crematoriums,

hiring of heavy

equipment owned by

councils etc

2. Service Delivery i. Charge for the services

as per section 10 above

Revenue Source 12, 13, 14, & 15

Grants allocated by decentralized budgets

Grants allocated by Line Ministry

Provincial Council Criteria Based Grants

Criteria Based Grants

a. These funds are received from external sources by the council from time to time for

development activities and improvement of service delivery of the council. Therefore the

council cannot assess or decide in advance the revenue receivable under these sources.

b. Legal requirement

MC Ordinance

Section 185 (2) (g)

c. Procedures and Practices cannot be decided as per the above.

Revenue Source 16 & 17

Staff Salary reimbursements

Members fee reimbursements

a. Municipal Councils receive grants from the Provincial Ministry of Local Government for

reimbursement of salaries and members’ allowances. The percentage of reimbursement

(100% or lesser percentage) and the conditions applicable for reimbursement is decided

by the Provincial Minister from time to time and directions will be given to the Provincial

Commissioners’ of Local Government to act accordingly.

b. Legal requirement MC Ordinance

Section 185 (2) (d)

c. Procedures and Practices

Key Steps Key Activities Remarks

1. Prepare the annual

Budgets and

estimates

i. Identify the cadre and

the Salary payable

together with the

proposed increments for

the budgeted year.

ii. Calculate the amount

payable to the elected

representatives for the

budgeted year

2. Submit the

statements for

reimbursement

i. Calculate the actual

payments on

monthly basis

ii. Submit the statement

to the Provincial

Commissioner of

Local Govt for

reimbursement

Revenue Source 18 - Assessment Rates

a. A certain percentage of the annual value of the lands and buildings situated within

the area of Local Authority is collected as Assessment Rates. This revenue is utilized

to maintain common services delivered to the citizens. The councils may impose a

higher rate on premises used for business or commercial purposes. Council may with

the sanction of the Minister, impose different rates for different areas or parts of the

Municipality according to the services provided by Council for each such area or part.

The council is compelled to provide services even to the unauthorised constructions

and these costs are not being reimbursed by such service recipients as they do not pay

assessment rates. These costs are therefore recovered from the other rate payers. Due

to this reason it can be concluded that there is no uniformity in charging taxes by the

councils and this situation is unavoidable.

As per the powers given under section 230 subsection (1) the Municipal from time to

time so often as it thinks necessary, make and assess, with the sanction of the

Minister, any rate or rates on the annual value of all houses and buildings of every

description and of all lands and tenements whatsoever within the Municipality. Please

refer sections 230-244 of the Municipality Ordinance

The powers to recover the rates and taxes are given under clauses 252 to 264 (a). It

shall be the duty of the Commissioner to issue a warrant signed by him to recover

rates and taxes.

The Assessment rates should be charged annually and council approval should be

obtained prior to charging the annual rates. When the assessment rates are imposed it

is necessary to accept the preceding year assessment to impose the succeeding year

assessment.

b. Legal Requirement

MC Ordinance

Section 230

c. Procedures and Practices

Key Steps Key Activities Remarks

1' Assessment of

Property Tax i' Council decision

ii' Minister’s approval

iii' Assess property

iv' Obtain council approval for

new assessments

v' Decide the new percentage

of increase based on the

new assessment and

expenditure

vi' Issue assessment notices

vii' Call for objections

viii' Review the objections

2' Annual Assessment

Taxes i' Council decisions

ii' Gazette notification

iii' Issue assessment notices

iv' Call for objections

v' Review the objections

3' Collection of

Assessment Taxes i' Payment at the Cashier’s

desk in the Council

ii' Through revenue

inspector/revenue

supervisor

iii' Issue of Warrant of Distress

against defaulters

iv' Acquiring property

v' Sale of Acquired property

vi' Acquire immovable

property

vii' Sale or transfer ownership

of acquired property

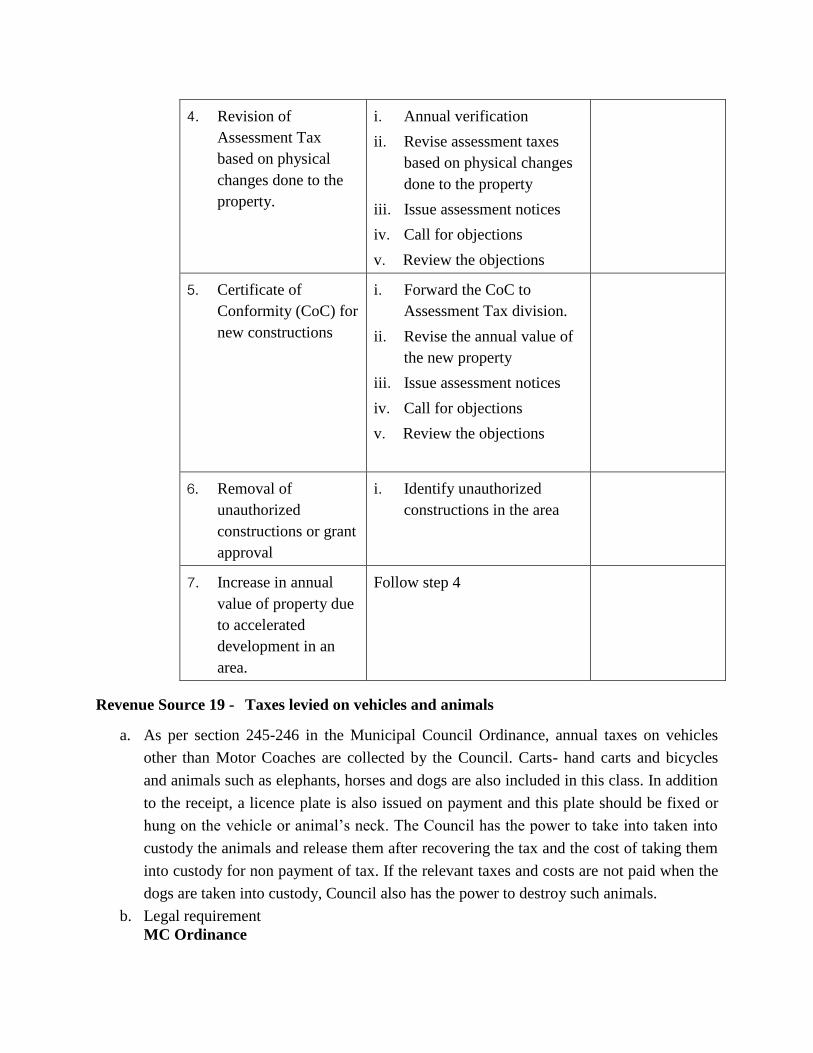

Revenue Source 19 - Taxes levied on vehicles and animals

a. As per section 245-246 in the Municipal Council Ordinance, annual taxes on vehicles

other than Motor Coaches are collected by the Council. Carts- hand carts and bicycles

and animals such as elephants, horses and dogs are also included in this class. In addition

to the receipt, a licence plate is also issued on payment and this plate should be fixed or

hung on the vehicle or animal’s neck. The Council has the power to take into taken into

custody the animals and release them after recovering the tax and the cost of taking them

into custody for non payment of tax. If the relevant taxes and costs are not paid when the

dogs are taken into custody, Council also has the power to destroy such animals.

b. Legal requirement MC Ordinance

4' Revision of

Assessment Tax

based on physical

changes done to the

property.

i' Annual verification

ii' Revise assessment taxes

based on physical changes

done to the property

iii' Issue assessment notices

iv' Call for objections

v' Review the objections

5' Certificate of

Conformity (CoC) for

new constructions

i' Forward the CoC to

Assessment Tax division.

ii' Revise the annual value of

the new property

iii' Issue assessment notices

iv' Call for objections

v' Review the objections

6' Removal of

unauthorized

constructions or grant

approval

i' Identify unauthorized

constructions in the area

7' Increase in annual

value of property due

to accelerated

development in an

area.

Follow step 4

Section 185 (2) (a) and (b)

Section 245 to246

c. Procedures and Practices

Key Steps Key Activities Remarks

Assessment of vehicles

(excluding motor

vehicles) and animals

that are subject to tax

within the council

area

Carryout an annual survey to

assess the vehicles and animals

that are subject to tax

Imposing the tax Prepare a resoulution for

the council

Submit the resolution to

the standing committee

for finance in the council

Submit the resolution

together with the finance

committee report for

council approval

Publish the Gazette

notice

Issue the gazette notice

to the relevant officers in

the council

Collection of tax

Forward the tax notices

to the relevant payers

Collect taxes

Revenue Source 20 - Taxes levied on Business Premises (Trade Tax based on annual value

of the premises

a. Local Authorities have the power to collect an annual tax from industries, trades and

businesses premises within their areas of authority. Such taxes may be collected for the

purposes stated in the by-laws framed under the provisions in the Act and subject to

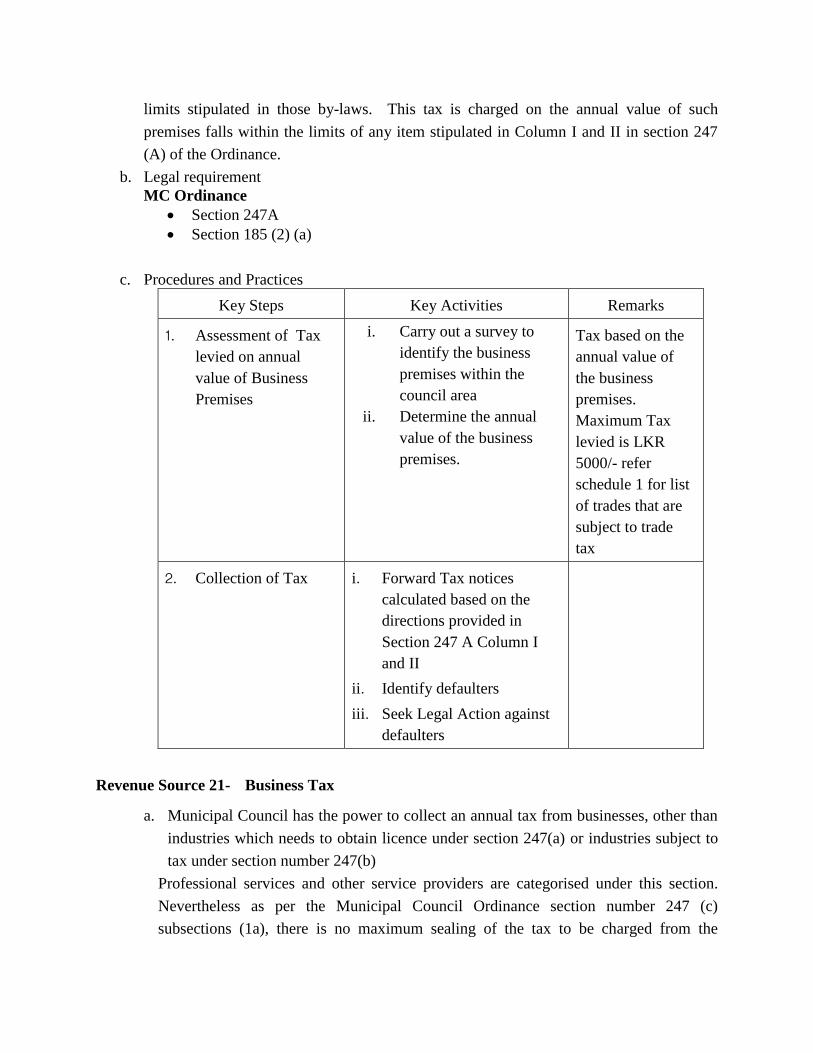

limits stipulated in those by-laws. This tax is charged on the annual value of such

premises falls within the limits of any item stipulated in Column I and II in section 247

(A) of the Ordinance.

b. Legal requirement MC Ordinance

Section 247A

Section 185 (2) (a)

c. Procedures and Practices

Key Steps Key Activities Remarks

1' Assessment of Tax

levied on annual

value of Business

Premises

i. Carry out a survey to

identify the business

premises within the

council area

ii. Determine the annual

value of the business

premises.

Tax based on the

annual value of

the business

premises.

Maximum Tax

levied is LKR

5000/- refer

schedule 1 for list

of trades that are

subject to trade

tax

2' Collection of Tax i' Forward Tax notices

calculated based on the

directions provided in

Section 247 A Column I

and II

ii' Identify defaulters

iii' Seek Legal Action against

defaulters

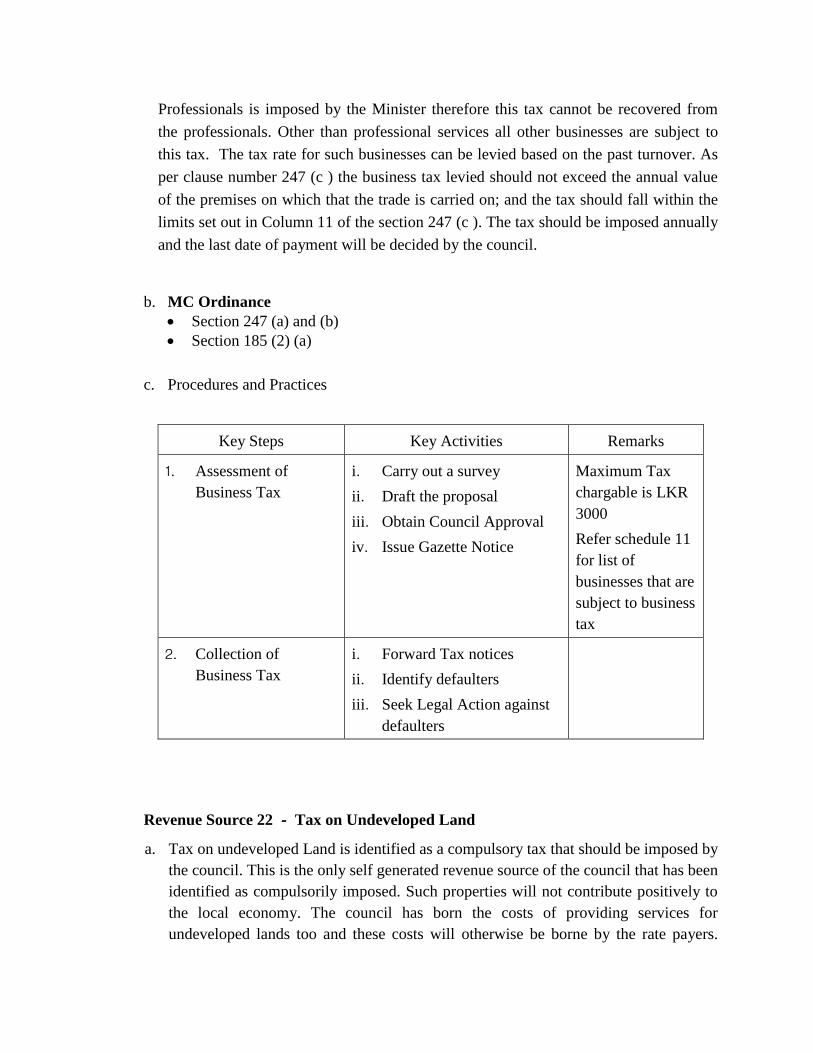

Revenue Source 21- Business Tax

a. Municipal Council has the power to collect an annual tax from businesses, other than

industries which needs to obtain licence under section 247(a) or industries subject to

tax under section number 247(b)

Professional services and other service providers are categorised under this section.

Nevertheless as per the Municipal Council Ordinance section number 247 (c)

subsections (1a), there is no maximum sealing of the tax to be charged from the

Professionals is imposed by the Minister therefore this tax cannot be recovered from

the professionals. Other than professional services all other businesses are subject to

this tax. The tax rate for such businesses can be levied based on the past turnover. As

per clause number 247 (c ) the business tax levied should not exceed the annual value

of the premises on which that the trade is carried on; and the tax should fall within the

limits set out in Column 11 of the section 247 (c ). The tax should be imposed annually

and the last date of payment will be decided by the council.

b. MC Ordinance

Section 247 (a) and (b)

Section 185 (2) (a)

c. Procedures and Practices

Key Steps Key Activities Remarks

1' Assessment of

Business Tax

i' Carry out a survey

ii' Draft the proposal

iii' Obtain Council Approval

iv' Issue Gazette Notice

Maximum Tax

chargable is LKR

3000

Refer schedule 11

for list of

businesses that are

subject to business

tax

2' Collection of

Business Tax i' Forward Tax notices

ii' Identify defaulters

iii' Seek Legal Action against

defaulters

Revenue Source 22 - Tax on Undeveloped Land

a. Tax on undeveloped Land is identified as a compulsory tax that should be imposed by

the council. This is the only self generated revenue source of the council that has been

identified as compulsorily imposed. Such properties will not contribute positively to

the local economy. The council has born the costs of providing services for

undeveloped lands too and these costs will otherwise be borne by the rate payers.

Therefore to minimize the loss to the council tax it is compulsory to impose taxes on

undeveloped lands.

To identify the annual rate to be charged on undeveloped land the council will decide

the proportion of land that the extent of such land which is actually covered by

buildings bears to the total extent of such land, a proportion less than that prescribed

by the council resolution.

b. Legal Requirements

MC Ordinance

Section 247(b)

c. Procedures and Practices

Key Steps Key Activities Remarks

1' Assessment of tax on

undeveloped land i' Carry out a survey

ii' Draft the proposal

iii' Obtain Council Approval

iv' Issue Gazette Notice

2' Collection of tax i' Forward Tax notices

ii' Identify defaulters

iii' Seek legal against

defaulters to recover the

arrears.

Maximum 2% tax

could be levied on

annual value of

bare lands

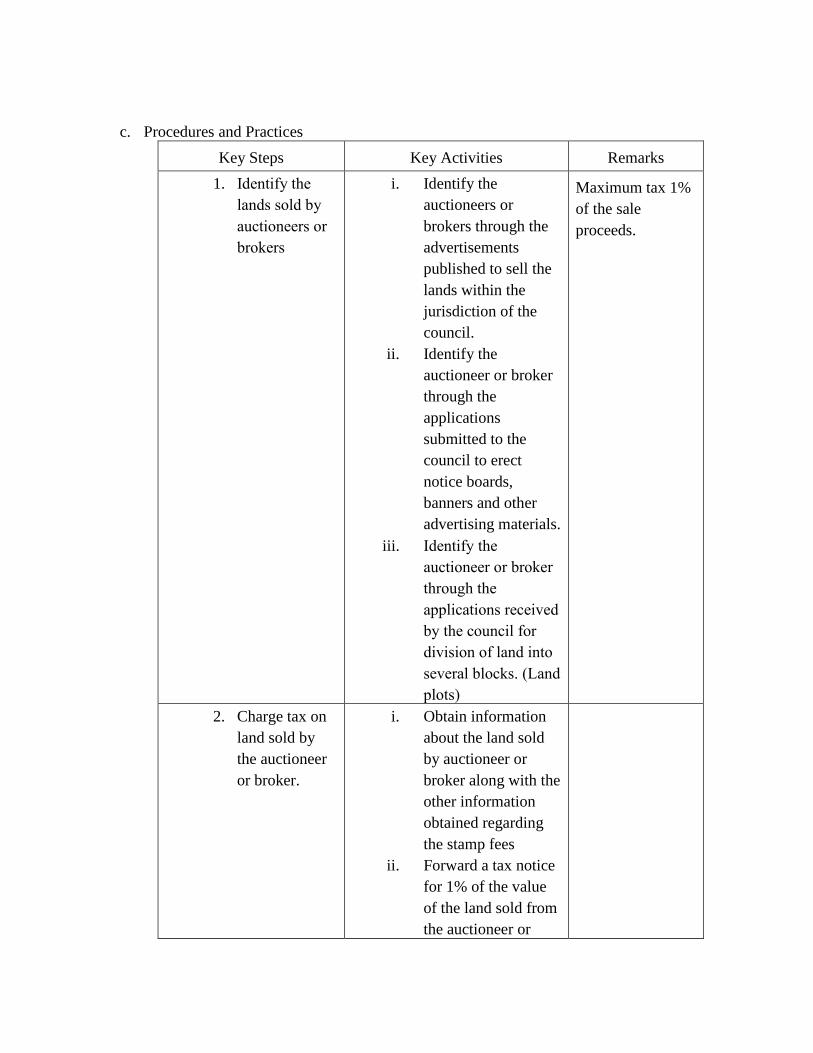

Revenue Source 23 - Taxes levied on Sale of some land plots

a. Local Authorities have the power to collect taxes on any land within the administrative

limits of the sold by public auction or otherwise, by an auctioneer or brokers or his

servant or agent, the vendor or such auctioneer or broker or his servant or agent shall pay

to the Council, from the proceeds of the sale of such land a tax equivalent to 1% of the

amount of such proceeds.

b. Legal requirement MC Ordinance

Section 247 (e)

c. Procedures and Practices

Key Steps Key Activities Remarks

1. Identify the

lands sold by

auctioneers or

brokers

i. Identify the

auctioneers or

brokers through the

advertisements

published to sell the

lands within the

jurisdiction of the

council.

ii. Identify the

auctioneer or broker

through the

applications

submitted to the

council to erect

notice boards,

banners and other

advertising materials.

iii. Identify the

auctioneer or broker

through the

applications received

by the council for

division of land into

several blocks. (Land

plots)

Maximum tax 1%

of the sale

proceeds.

2. Charge tax on

land sold by

the auctioneer

or broker.

i. Obtain information

about the land sold

by auctioneer or

broker along with the

other information

obtained regarding

the stamp fees ii. Forward a tax notice

for 1% of the value

of the land sold from

the auctioneer or

broker.

iii. Inform the

magistrate about

defaluters.,

Revenue Source 24 - Recovery of costs on any warrants issued.

a. Local Authorities are entitled to recover the costs incurred in relation to the warrants

issued by the councils to collect the arrears of assessment rates. This fee should not

exceed the 10% of the value of the rates payable or 15% on the amount of rate due on

bare lands or 20% on the amount of rate due on properties other than bare lands and

residential premises.

b. Legal requirement MC Ordinance

Section 255 (a)

c. Procedures and Practices

Councils can recover this revenue from defaulters of assessment taxes. The Municipal

Commissioner/UC Secretary has to issue the Warrant and based on the amounts in

arrears the revenue will be calculated.

Revenue Source 25 - Charges on seizure and removal of goods seized.

a. Local Authority can recover the costs incurred for seizure and removal of goods seized,

in case such removal takes place, a charge not exceeding five cents for every fifty cents

of rate or tax or rent due

b. Legal requirement MC Ordinance

Section 255 (b)

Revenue Source 26 - Charges on keeping any goods seized in safe custody.

a. Local Authority can recover costs incurred for keeping any goods seized in safe custody

in case of detention, a charge not exceeding Rs.75/- per day

b. Legal requirement MC Ordinance

Section 255 (c)

Revenue Source 27 - When any sales take place of seized movable properties 1% of the

sale value of the movable properties.

a. Local Authority can recover the expense of sale, when any sale takes place a charge bot

exceeding 1% if the sale value of movable properties.

b. Legal requirement MC Ordinance

Section 185 (2) (d)

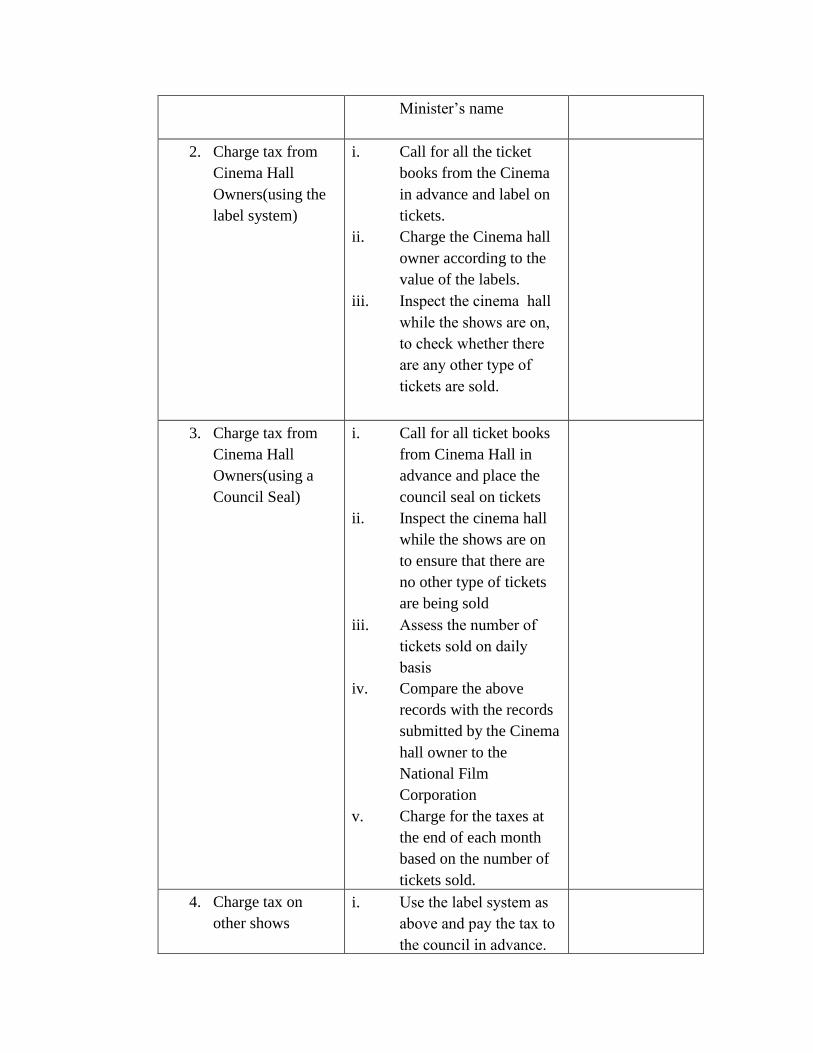

Revenue Source 28 - Entertainment Tax

a. Local Authorities collect these taxes under the provisions of the Entertainment Tax

Ordinance. This tax is imposed according to the value of the tickets issued for entering

the place of entertainment. Generally 10% of the value of tickets issued in cinemas,

theatres, entertainment centres, entertainment programmes or shows organized by

individuals is collected as tax. This tax should be settled within a month from the date of

the programme or the show and failure to do so will result in litigation. Generally for this

type of activities a security deposit will be obtained.

b. Legal requirement For MC & UC

Entertainment Tax Ordinance – Section 2

c. Procedures and Practices

Key Steps Key Activities Remarks

1. Impose

Entertainment tax

i. Council decision on

Entertainment Tax

ii. Obtain approval from

the Provincial Minister

of Local Government

iii. On approval of the

Council decision by the

Provincial Minister,

issue a gazette

notification under the

Minister’s name

2. Charge tax from

Cinema Hall

Owners(using the

label system)

i. Call for all the ticket

books from the Cinema

in advance and label on

tickets.

ii. Charge the Cinema hall

owner according to the

value of the labels.

iii. Inspect the cinema hall

while the shows are on,

to check whether there

are any other type of

tickets are sold.

3. Charge tax from

Cinema Hall

Owners(using a

Council Seal)

i. Call for all ticket books

from Cinema Hall in

advance and place the

council seal on tickets

ii. Inspect the cinema hall

while the shows are on

to ensure that there are

no other type of tickets

are being sold

iii. Assess the number of

tickets sold on daily

basis

iv. Compare the above

records with the records

submitted by the Cinema

hall owner to the

National Film

Corporation

v. Charge for the taxes at

the end of each month

based on the number of

tickets sold.

4. Charge tax on

other shows

i. Use the label system as

above and pay the tax to

the council in advance.

Revenue Source 29 - Charges levied to inspect slaughtered Animals

a. The trade of butcher, had to be carried out only on a licence (annual or temporary) issued

by the Local Authority. The application for Butchers Licence had to specify the premises

where the trade was to be carried out. The procedure to be followed prior to the issue of a

licence is given in section 4 to 7 of the Butchers Ordinance. The Councils are authorised

to charge a levy to inspect the slaughtered animals under section 11 of the Butchers

Ordinance.

b. Legal requirement

For MC & UC

Section 11 of Butchers Ordinance.

Revenue Source 30 – Licensing of Clubs

a. This Law has been enacted to provide for the control of clubs and for matters connected

therewith. In terms of the Section 2 of the Law it is unlawful to run a club without a

licence issued by the Mayor/Chairman of the Local Authority. Under section 4 of this

Law, the Minister is empowered to prescribe in respect of every Local Authority to scale

of fees payable in respect of a license to maintain a club provided however, the fees so

prescribed must not exceed the limits prescribed by the Act.

b. Legal requirement MC & UC

Licensing of Clubs Act No 17 of 1975 section No 04

c. Procedures and Practices

Key Steps Key Activities Remarks

1. Issue of Club

License

i. Manager of the Club

submit an application to

the Council

ii. Obtain certification as

per the requirements of

the Act iii. Publish a notice in the

Gazette stating the

request of license.

iv. If there are no

objections, charge the

relevant fee and issue the

license

Revenue Source 31 Environmental Protection Licence fees

a. The Central Environment Authority has, under the national environmental Act, conferred

on Local Authorities, the powers to deal with minor pollution agents in relation to

environmental protection. The power to issue environmental protection licences has also

been conferred. Minor pollution agents include small scale saw mills, rice mills, stone

crushers, livestock farms, garages, printing press and grinding mills.

b. Legal requirement MC & UC

Section Number 32 of National Environment Authority Act No 26, of 1988 – Please

refer the attached Schedule No 1

Revenue Source 32 - Issue of Licences (Trade Licences)

a. Local Authorities may impose and levy a duty in respect of licences issued by the

council. The duty levied as above in respect of any licences issued by the council

authorizing the use of any premises for any of the purposes described in this

ordinance or in any by-law made there under shall be determined by the Council

according to the annual value of the premises.

b. MC Ordinance

Applicable By-Laws to be read with Section 247 (A) of MC Ordinance – Please refer

Schedule No 111

c. Procedures and Practices

Key Steps Key Activities Remarks

1. Identify the

premises where the

license needs to be

issued.

i. Conduct a survey, in

advance to identify the

premises where the

licenses need to be

issued.

ii. Issue the notices in the

month of December for

the licenses for the

succeeding year.

Maximum Limit

chargable is LKR

5000/-

Refer Schedule

No 111 for the list

of trade activities

where licence

needs to be

obtained from MC

2. Issue of Licenses i. Receive requests for

Licenses

ii. Ensure that the

necessary requirements

are fulfilled to issue the

Licenses

iii. If not, notice to issued to

rectify the problems

iv. Inform the owners when

the License are ready to

be issued

v. Charge the relevant fee

and issue licenses

3. Council to take

Legal action

against defaulters

i. Inform the

Magistrate’s Court

having jurisdiction

over the area in

which the council is

situated.

ii. Recover the penalty

imposed by the

Courts

iii. Inform the occupier

to obtain Licence

immediately

iv. Issue the License

v. If Licenses are not

obtained council to

get a court direction

to wind up the

business

Revenue Source 33-35

Public Slaughter House – Exposure of flesh of Animals

Public Slaughter House- Emergency Permits to transport animals -

Public Slaughter House-Transportation of Meats

a. The trade of butcher had to be carried out only on a licence (annual or temporary) issued

by the Local Authority. The application for Butchers Licence had to specify the premises

where the trade was to be carried out. The procedure to be followed prior to the issue of a

licence is given in section 4 to 7 of the Butchers Ordinance.

Under section 26 to 29 public slaughter house have to be certified as sufficient for the

purpose by the Local Authority to the Provincial Minister who would then issue a notice

proclaiming such slaughter house. Regulations could be made by the Local Authority in

regard to the public slaughter house. The person in charge of public slaughter house

could seize and destroy diseased animals brought to the public slaughter house. Under

Section 13A of Butchers Ordinance no person can sell or expose for sale or cause to be

sold or exposed for sale flesh of any animal at any place other than in a building

constructed in conformity with the plan approved by Provincial Secretary to the Ministry

of Local Govt.

b. Legal requirement MC & UC

If there are slaughter houses within the jurisdiction of the council, the council can

impose the relevant sections as per the Butchers Ordinance.