evolution of cmp and future outlook - nccavs …€¦ · evolution of cmp and future outlook july...

TRANSCRIPT

www.linx-consulting.com

Evolution of CMP and Future Outlook

July 14, 2016Andy Tuan [email protected]

+886 958 111222CMPUG Taiwan Committee Member

www.linx-consulting.com

2

Agenda

1. Introduction to Linx Consulting

2. Where Have We Been and Where are We Going?

3. Industry Evolution

www.linx-consulting.com

3

Introduction to Linx Consulting

www.linx-consulting.com

4

Linx Consulting

1. We help our clients to succeed by creating know ledge and developing unique insights at the intersection of electronic thin film processes and the chemicals industry

2. The know ledge is based on a core understanding of the semiconductor device technology; manufacturing processes and roadmaps; and the structural industry dynamics

3. This know ledge is leveraged to create advanced models, simulations and real-world forecasts

4. Our perspectives are by direct research and leveraging our extensive experience throughout the global industry value chain, including:

• Experience in global electronics and advanced materials and thin film processing industries • Experience in the global chemicals industry• Experience at Device Producers• Experience at OEMs

www.linx-consulting.com

5

Linx Consulting Service Portfolio• Multi-Client Reports

– IC Materials• CMP• Deposition• Patterning• Cleaning• Gases• Bulk Chemicals

– III-Vs, TSV, WLP, Solar

• Proprietary Projects– Market Planning– M & A– Growth and Diversification– Supply Chain Optimization– Technology Commercialization– Strategic Planning– Voice of the Customer

• Econometric Semiconductor Forecast– Financial planning– Sales and Operational planning– Forecasting

Hilltop Economics LLC

• Cost Modeling– Client demand modeling– Product development– Bill of Materials quantification

IC Knowledge, LLC

– Semi– LCD

– Packaging– PV

– Nano Technology– LED/ Compound Semi

www.linx-consulting.com

6

Customer Base in Semiconductors

Finance &Technology

Raws & Chemicals Equipment Services End-users &

Consortia

North America

China

SEA & India

Europe

Japan

Korea

Taiwan

www.linx-consulting.com

7

Where Have We Beenand Where are We Going?

www.linx-consulting.com

8

3,000

2,500

2,000

1,500

1,000

500

75,000

70,000

65,000

60,000

55,000

50,000

45,000

40,000

35,00094 96 98 00 02 04 06 08 10 12 14

Semi MSIWorld Real GDP (Rt Scale)

Million Square Inches Billion 2010 US$

93-15Q495% correlation

MSI Multiple: 2.1X

Silicon Follows GDP Closely

1.0X

2.4X

Source: Hilltop Economics

Macro

www.linx-consulting.com

9

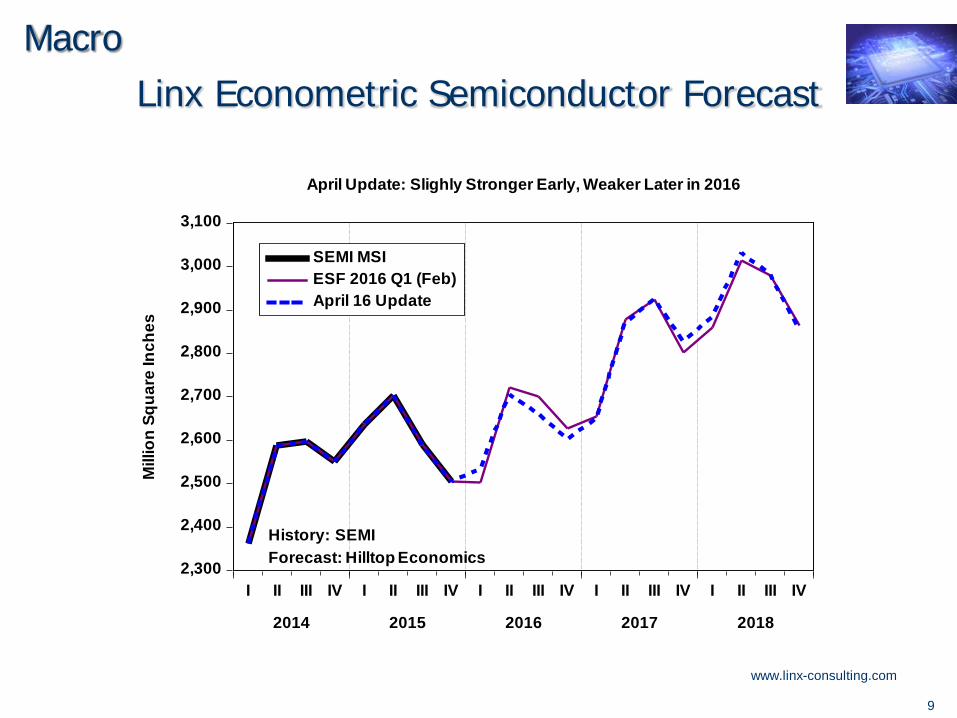

Linx Econometric Semiconductor Forecast

2,300

2,400

2,500

2,600

2,700

2,800

2,900

3,000

3,100

I II III IV I II III IV I II III IV I II III IV I II III IV

2014 2015 2016 2017 2018

SEMI MSIESF 2016 Q1 (Feb)April 16 Update

History: SEMIForecast: Hilltop Economics

April Update: Slighly Stronger Early, Weaker Later in 2016

Mill

ion

Squa

re In

ches

Macro

www.linx-consulting.com

10

Sputter Target Market $M Vs. MSI

7,000

7,500

8,000

8,500

9,000

9,500

10,000

10,500

11,000

$500

$520

$540

$560

$580

$600

$620

$640

$660

2010 2011 2012 2013 2014 2015 2016

Macro

www.linx-consulting.com

11

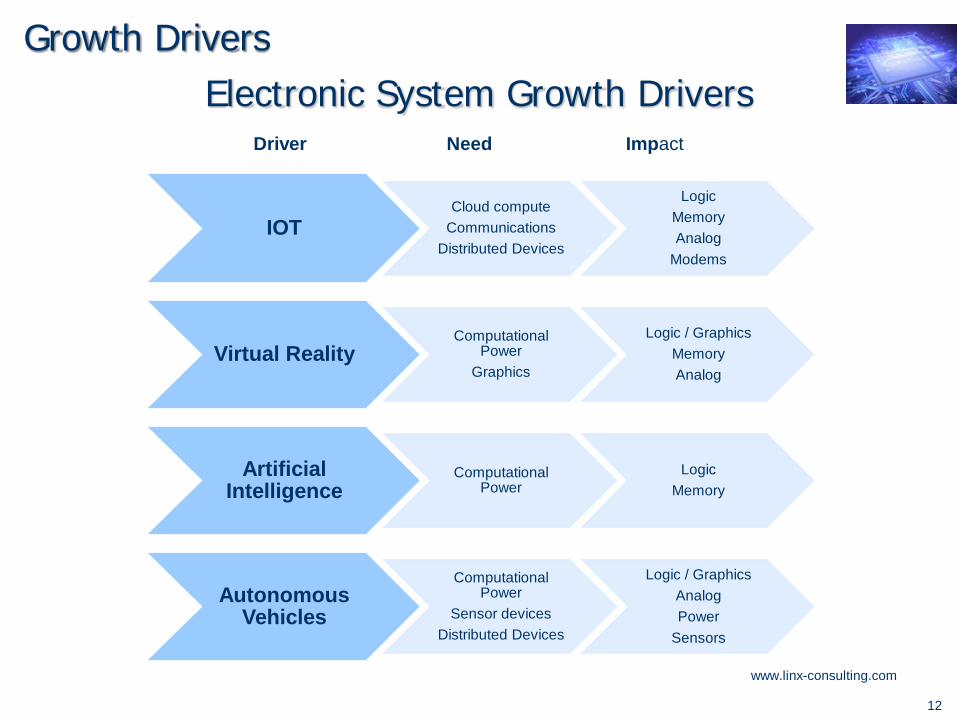

Electronic System Growth DriversGrowth Drivers

Internet of ThingsMuch hyped driver of billions of networked devices generating information for governmental, commercial, consumer, medical, and other information systems

Virtual RealityCreation of virtual displays of real and simulated environments for military, consumer, commercial and other applications, usually through a novel head display

Artificial IntelligenceComputer based intelligent learning systems

Autonomous VehiclesSensor systems supporting vehicle based computer systems offering various degrees of driver assistance including fully autonomous driverless vehicles.

www.linx-consulting.com

12

IOTCloud compute

Communications Distributed Devices

Logic MemoryAnalog

Modems

Virtual RealityComputational

PowerGraphics

Logic / GraphicsMemoryAnalog

Artificial Intelligence

Computational Power

LogicMemory

Autonomous Vehicles

ComputationalPower

Sensor devicesDistributed Devices

Logic / GraphicsAnalogPower

Sensors

Electronic System Growth DriversGrowth Drivers

Driver Need Impact

www.linx-consulting.com

13

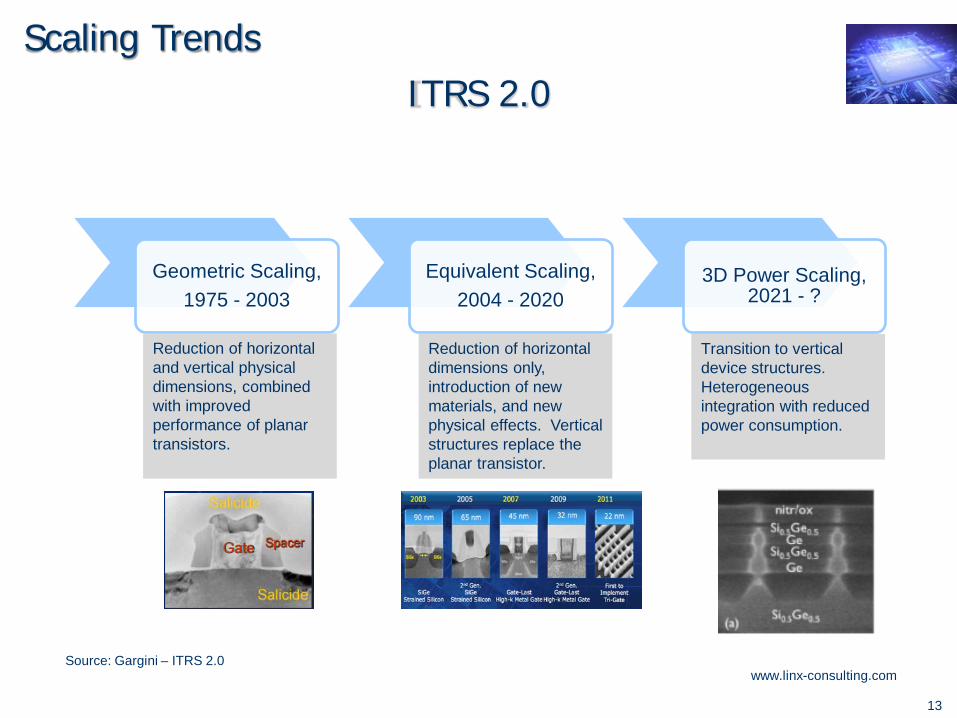

ITRS 2.0

Geometric Scaling,1975 - 2003

Equivalent Scaling,2004 - 2020

3D Power Scaling, 2021 - ?

Reduction of horizontal and vertical physical dimensions, combined with improved performance of planar transistors.

Reduction of horizontal dimensions only, introduction of new materials, and new physical effects. Vertical structures replace the planar transistor.

Transition to vertical device structures. Heterogeneous integration with reduced power consumption.

Source: Gargini – ITRS 2.0

Scaling Trends

www.linx-consulting.com

14

Materials That Enable Moore’s Law

(PM: Patterning Materials)

(IL: InterfaceLayer)sSOI/GeOI

Ge IL III-V ILGaN InSb

InGaAs Ge

STORu

Other PM's EUV

Other PM's EUV

Co Si(C)P

Co Si(C)P

FDSOISiC

FDSOISiC

Air SiCO

Air SiCO

LaO LaOLT SiO LT SiO

SiCN SiCN SiCNTiAlC MG

ZrO Hf(Si)O

AlO

TiAlC MGZrO

Hf(Si)OAlO

TiAlC MGZrO

Hf(Si)OAlO

pSiOC pSiOC pSiOCSOI SOI SOI

SiGe(B)TaO SOG

TaO SOG

SiGe(B)TaO SOG

SiGe(B)TaO SOG

SiOCTa/TaN

Cu SiOF

SiOCTa/TaN

Cu SiOF

SiOCTa/TaN

Cu SiOF

SiOCTa/TaN

Cu SiOF

TiSi PtSi

TiSi PtSi

TiSi PtSi

TiSi PtSi

TiSi PtSi

TiW TiW TiW/TiN TiN TiN TiNWSi, MoSi WSi, W WSi, W W W W

AlBPSG

AlBPSG

AlBPSG

AlBPSG

AlBPSG

AlBPSG

AlBPSG

AlSiO, SiN SiO, SiN SiO, SiN SiO, SiN SiO, SiN SiO, SiN SiO, SiN SiO, SiN

Si Si Si Si Si Si Si Si

1960 1970 1980 1990 2000 2010 2015 2020(*)

(*): Projection

Patterning RelatedBEOLFEOLStarting Materials

Source: ASM

Scaling Trends

www.linx-consulting.com

15

Linx Materials Index

$0.60

$0.65

$0.70

$0.75

$0.80

$0.85

$0.90

$0.95

$1.00

$1.05

$1.10

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

$/sqin Volume slowdownASP decline

Process complexityModest growth Process simplification

Modest growth

Scaling Trends

www.linx-consulting.com

16

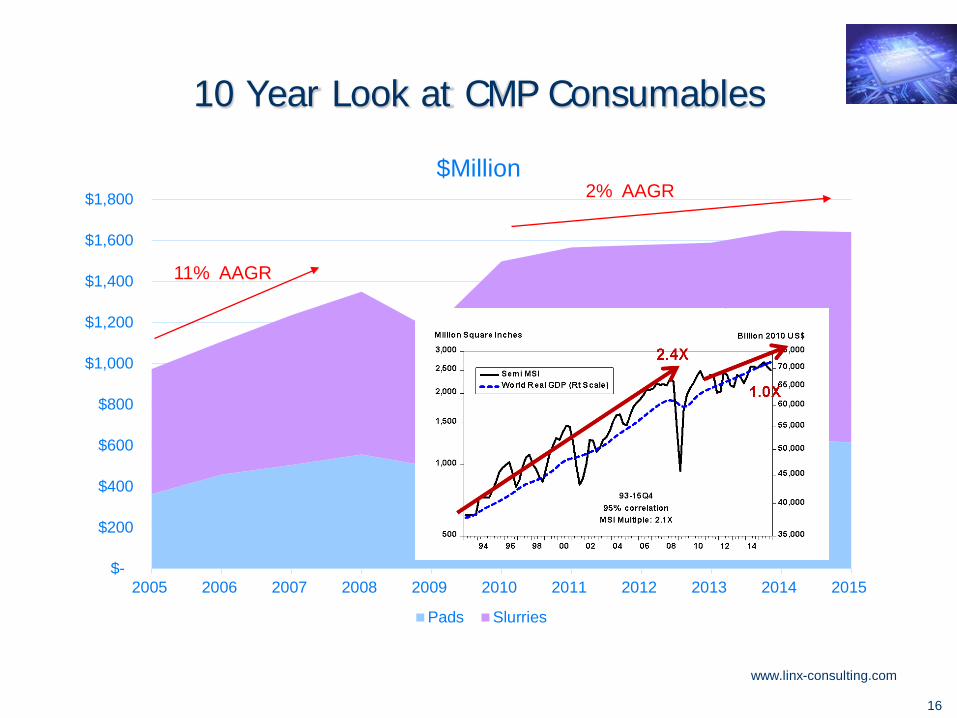

10 Year Look at CMP Consumables

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$Million

Pads Slurries

11% AAGR

2% AAGR

www.linx-consulting.com

17

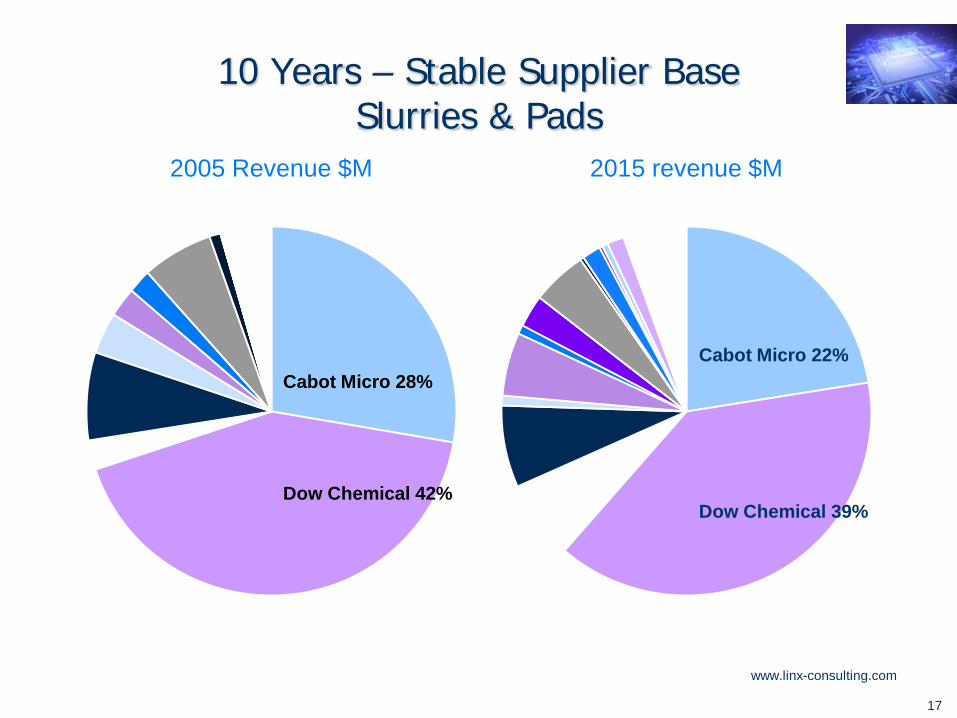

10 Years – Stable Supplier BaseSlurries & Pads

2005 Revenue $M

Cabot Micro 28%

Dow Chemical 42%

2015 revenue $M

Cabot Micro 22%

Dow Chemical 39%

www.linx-consulting.com

18

Industry Evolution

www.linx-consulting.com

19

Defectivity Paradigm Shift at 20nm

1. Pursuit of Moore’s Law is driving ever increasing design innovation, process sensitivity & complexity

2. Paradigm shift in thoughts about what we did not care about earlier in >20nm era & whatwe care to control now!

• Complex Chemistry: Compatibility Issues

• New Defect Sources, increase Defect Sensitivity

3. Metrology techniques of all types are challenged to provide sufficient sensitivity for early detection & prevention

• Supplier Infrastructure Development needed for better defect detection & characterization

• Metrology and Quality Control

4. Proactive engagement and collaboration across the supply chain are essential to HVMreadiness

Source: A. Sengupta, Intel. Semicon West 2015

The Challenge

www.linx-consulting.com

20

Defectivity

• Real-time metrology is practically impossible.• In-line metrology is challenged to measure critical particle sizes below 20nm

– High cost of systems– Off-line analysis to augment particle characterization

• Optical (particle detection) systems such as SP3 and SP5 are identifying new defects– On-wafer metrology has become the only approach able to show defects.– In many cases it is possible to identify the source from on-wafer analysis.– The expectation for particle shedding, and contamination continues to reduce.

• Killer defects, or critical particles are now in the order of 10 or 20 nm.– On-wafer analysis is struggling to define particles sizes or discriminate defects as

residues or discrete solids. – Defect sources vary from chemicals, water, seals, filters, piping etc.

• Equipment suppliers are driving to deliver ultraclean products which are certified with the latest analytical techniques, and targeted at delivering best possible performance.

The Challenge

www.linx-consulting.com

21

Wafer Fab Expectations1. Suppliers should use best practices for control of materials, manufacturing equipment,

and components– Close sub supplier collaboration and integrated quality systems; Vertical integration where

possible– Material and component control is critical

• Material and process control critical• SPC and excursion control is key• Sub-supplier involvement in quality is necessary

2. Advanced statistical process control– Feed forward and feedback SPC– Sophisticated analytical tools– Metrology and analysis gaps, demand collaboration between suppliers and users.

3. Holistic approach to defect control and Design for cost and environmental impact– Collaborative problem-solving helps identify problems quicker, and implement better

solutions – Products and systems need to be optimized for advanced node chemistries and processes

Aqueous and environmentally friendly formulations are preferred– Standardization required to reduce cost

The Challenge

www.linx-consulting.com

22

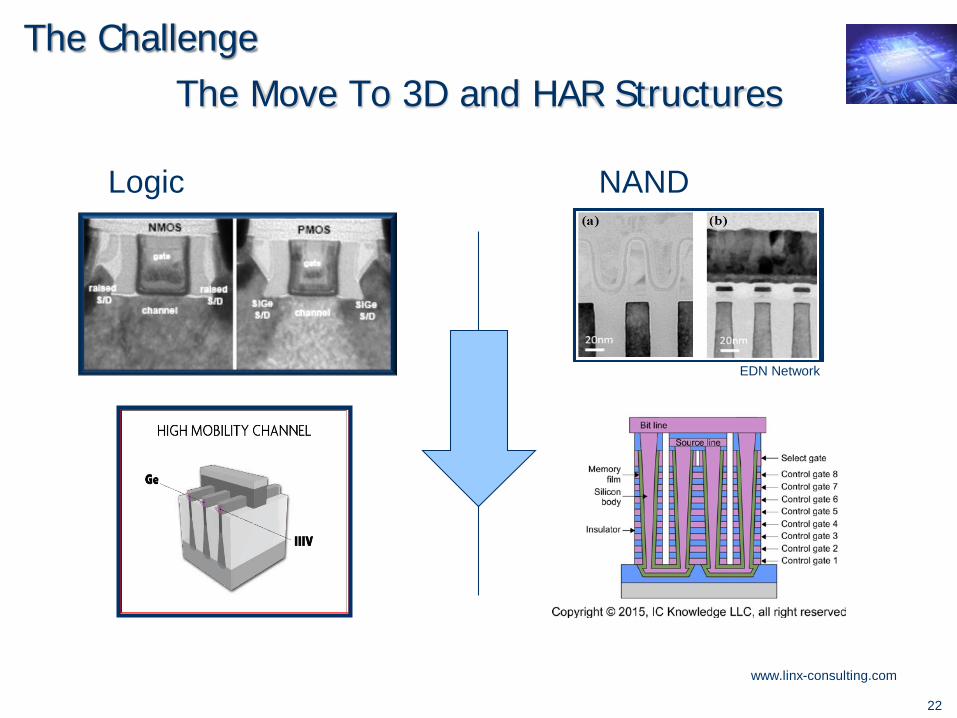

The Move To 3D and HAR Structures

Logic NAND

EDN Network

The Challenge

www.linx-consulting.com

23

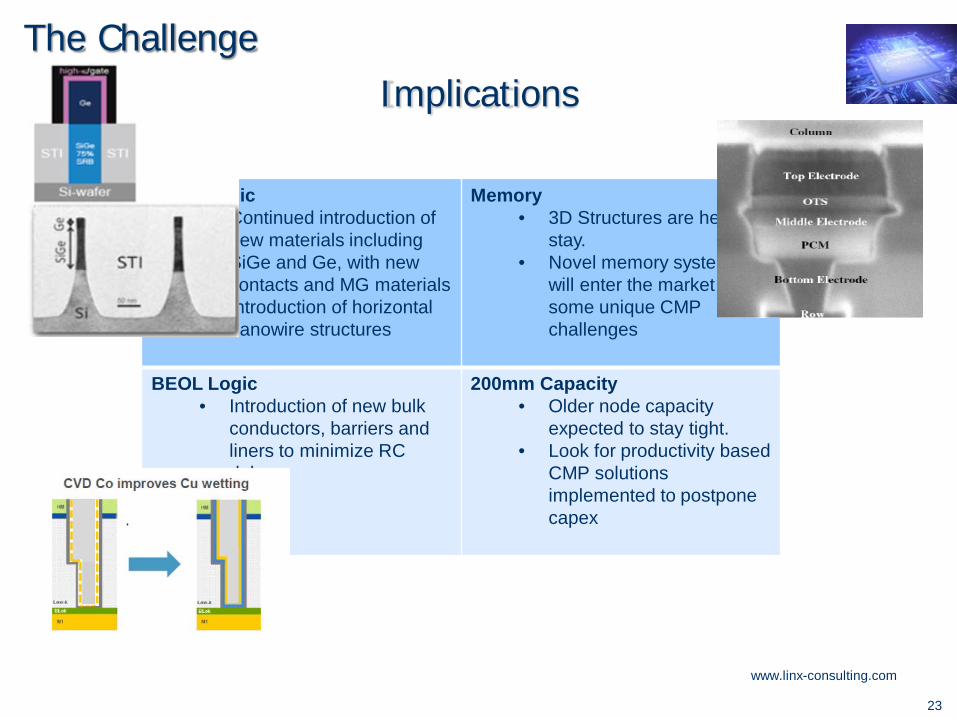

Implications

FEOL Logic• Continued introduction of

new materials including SiGe and Ge, with new contacts and MG materials

• Introduction of horizontal nanowire structures

Memory• 3D Structures are here to

stay.• Novel memory systems

will enter the market with some unique CMP challenges

BEOL Logic• Introduction of new bulk

conductors, barriers and liners to minimize RC delay.

200mm Capacity• Older node capacity

expected to stay tight. • Look for productivity based

CMP solutions implemented to postpone capex

The Challenge

www.linx-consulting.com

24

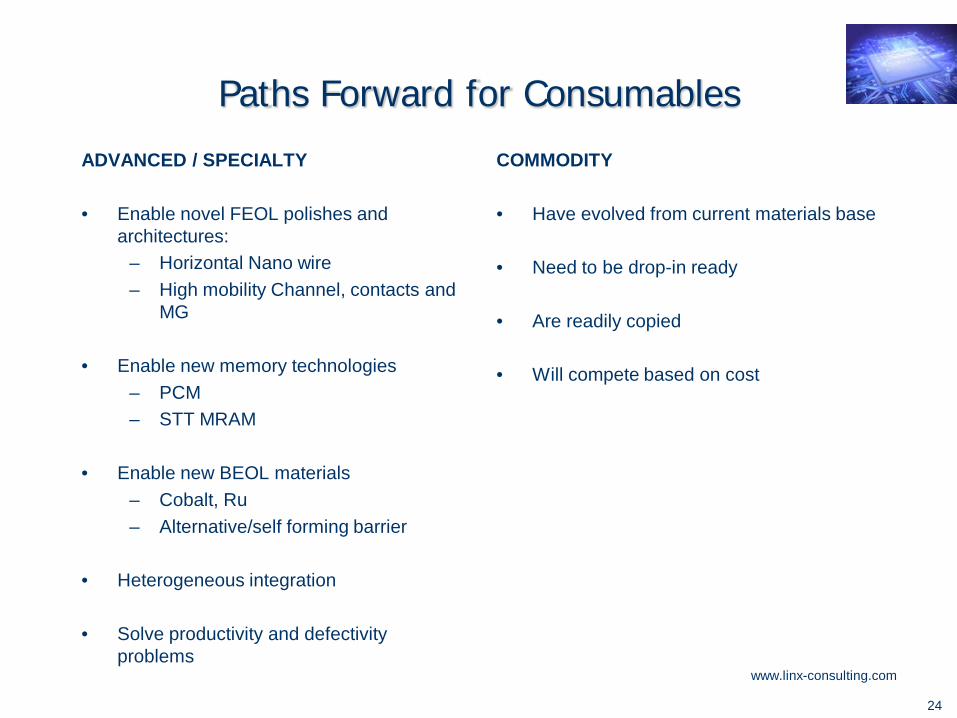

Paths Forward for Consumables

ADVANCED / SPECIALTY

• Enable novel FEOL polishes and architectures:

– Horizontal Nano wire– High mobility Channel, contacts and

MG

• Enable new memory technologies– PCM– STT MRAM

• Enable new BEOL materials– Cobalt, Ru– Alternative/self forming barrier

• Heterogeneous integration

• Solve productivity and defectivity problems

COMMODITY

• Have evolved from current materials base

• Need to be drop-in ready

• Are readily copied

• Will compete based on cost

www.linx-consulting.com

25

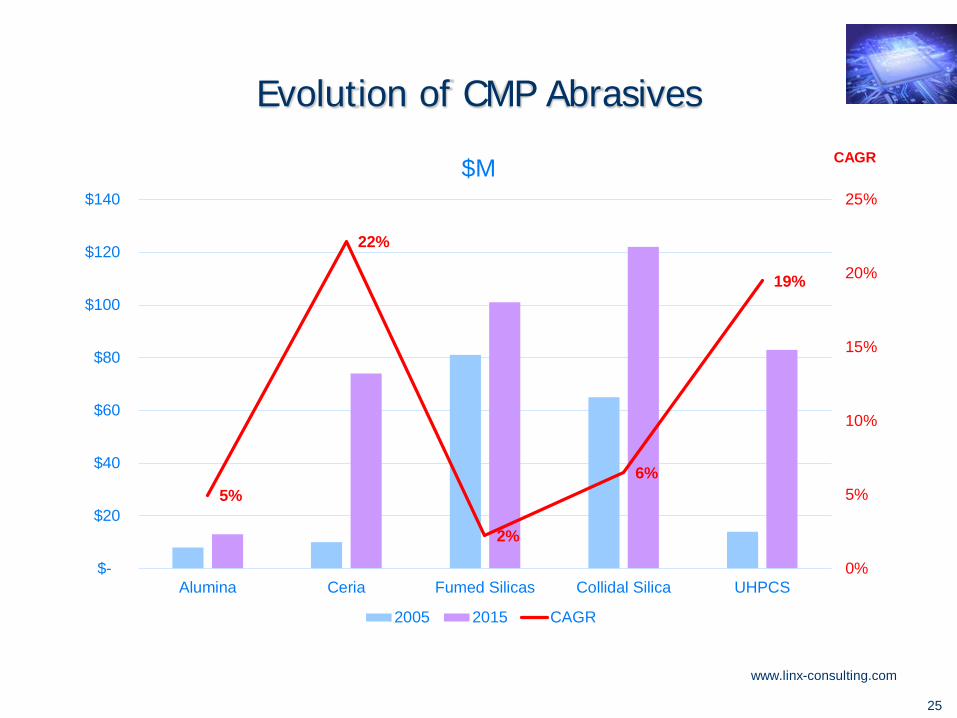

Evolution of CMP Abrasives

5%

22%

2%

6%

19%

0%

5%

10%

15%

20%

25%

$-

$20

$40

$60

$80

$100

$120

$140

Alumina Ceria Fumed Silicas Collidal Silica UHPCS

$M

2005 2015 CAGR

CAGR

www.linx-consulting.com

26

Consolidation Leading to Larger Suppliers

China• Continued acquisition and activity from

multiple companies.• Leveraged government equity positions

to enable significant size acquisitions.

Acquisition Landscape• Tsinghua Unigroup (China): Spreadtrum,

RDA, WD, Powetech…..• Lam Research – KLA/Tencor• Beijing E-Town Investment (China) –

Mattson Technology Materials• KMG - OMG + General Chemical• Entegris - ATMI• Merck - AZ• Merck – Sigma Aldrich & Solmet• Cabot Microelectronics - NexPlanar• Wonik – Nova-Kem • NATA (China) - Kempur • Air Liquide – Air Gas• Air Products – Versum Spinout• SK - OCIM • Dow Chemical – Dow Corning• Dow Chemical - Dupont Specialties Model is still Valued!

www.linx-consulting.com

27

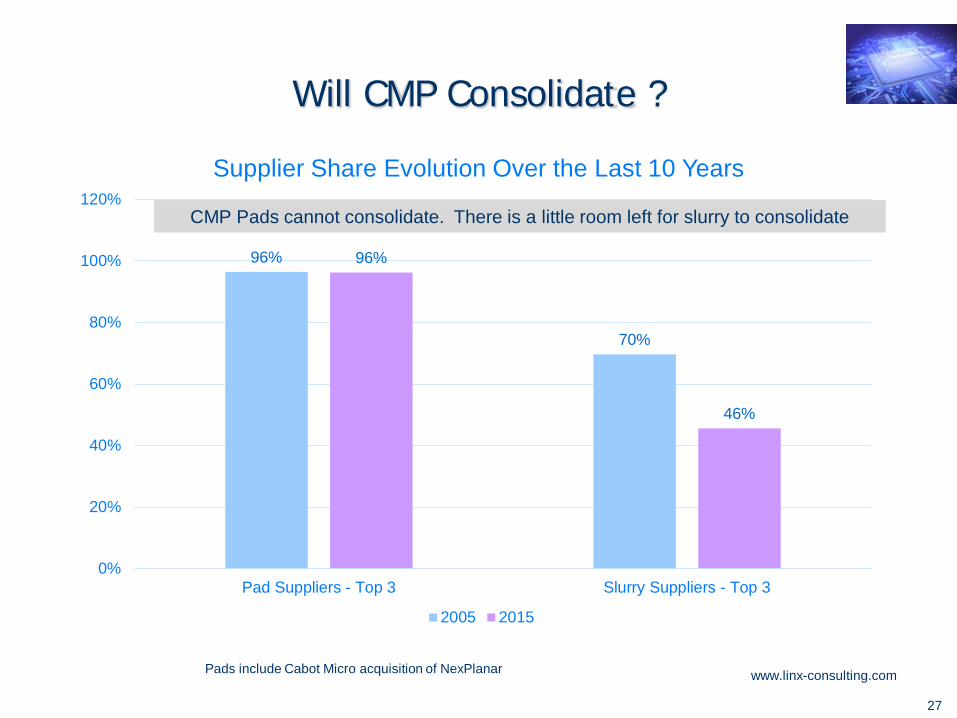

Will CMP Consolidate ?

96%

70%

96%

46%

0%

20%

40%

60%

80%

100%

120%

Pad Suppliers - Top 3 Slurry Suppliers - Top 3

Supplier Share Evolution Over the Last 10 Years

2005 2015

Pads include Cabot Micro acquisition of NexPlanar

CMP Pads cannot consolidate. There is a little room left for slurry to consolidate

www.linx-consulting.com

28

Conclusions

• Drivers for industry growth are changing, but there will continued demand for current device types

• Roadmap trends will drive to 3D device architectures in the medium to long term. System specific hybrid packages, device types, and device architectures will extend the roadmap.

• New device architectures will shift requirements of critical materials for different devices.– Lithography extension is a primary cost driver.– 3D devices will challenge aspect ratios, placing focus on etch and deposition

capabilities.

• The shift from planar scaling to 3D will extend into the packaging realm as some functionality and interconnect is moved into the wafer level package.

• Quality and defectivity requirements continue to be incredibly challenging, and require supply chain engagement.