ev446.eventive.incisivecms.co.ukev446.eventive.incisivecms.co.uk/digital_assets/1820/fic_yearbook_2… ·...

TRANSCRIPT

Fixed Incomeand CreditYearbook

2005The BLOOMBERG PROFESSIONAL® service seamlessly integrates data, news, analytics, multimedia reports and email onto a single platform for fi nancial professionals around the world. In addition, we offer 24-hour, worldwide customer support to all our clients who use the BLOOMBERG PROFESSIONAL service as the defi nitive tool for achieving their goals.

Now, BLOOMBERG ANYWHERESM allows clients to access the BLOOMBERG PROFESSIONAL service from any computer in the world. Keep an eye on your positions, check email and get critical information whenever and wherever you have Internet access.

New York +1 212 318 2000 | Tokyo +81 3 3201 8900 | London +44 20 7330 7500

EVERYTHINGINREACH

©2005 Bloomberg L.P. All rights reserved. 13015939 0105

Cover.50 3/5/05 6:17 PM Page 1

Insidefront Cover 3/4/05 10:56 PM Page a4

001-002 3/4/05 11:43 PM Page 1

2

Contents

Co-publishedfeaturesBloomberg 116

National Australia Bank 119

Grange Securities 122

TD Securities 126

RoundtableTD Securities 26

Allens Arthur Robinson 58

UBS 72

Q&AAllens Arthur Robinson 102

Grange Securities 106

Macquarie Bank 108

Standard & Poor’s 110

TD Securities 112

DirectoryIssuers 152

Investors 159

Intermediaries 168

Professional Services 173

Issuer ProfilesANZ Bank 86

Commonwealth Bank 87

CSR 89

Foster’s Group 90

Macquarie Bank 91

Mayne Group 92

National Australia Bank 93

St.George Bank 94

Sydney Airport 96

Tabcorp 97

Telstra 98

Westfield 99

Westpac 100

Pacific ProspectLevel 25 Chifley Tower2 Chifley SquareSydney NSW 2000AustraliaT 61 2 9251 1820F 61 2 9251 8182E [email protected]:Although every care has been taken to ensure theaccuracy of the information contained within thispublication, neither Pacific Prospect Group Pty. Ltd. nor their employees can be held liable for anyinaccuracies, errors or omissions. Nothing in thispublication should be construed as being FinancialProduct advice. Readers are strongly advised tocontact their professional financial, tax and/or legaladvisers before entering into any transaction orcontract to buy or sell any Financial Products.

Fixed Income and Credit Yearbook 2005ISBN 0-9751366-4-XEdition: 1Publisher: Pacific Prospect Group Pty Ltd

Who’s WhoIssuers 128

Investors 131

Intermediaries 137

Professional Services 147

EditorialForeword 4

Primary Markets 2004 Wrap 5

Fund Managers Outlook for 2005 16

Asian-based Investors 40

Can you Afford to Retire? 52

Primary Markets 68

Growth & Development 82of the Kangaroo Market

Changes to UBS’ 84Australian Bond Indices

001-002 3/4/05 11:43 PM Page 2

4

Despite theundeniable – and ongoing –attractiveness of offshore capital markets, the Australiancorporate bondmarket enjoyedanother record-breaking year in 2004.

The increased competitiveness shown by the Australian market in recent years, in providing funding in sizeable volumes,continued apace in 2004, with heightenedactivity at both ends of the investment-gradespectrum. The strong performance of theKangaroo market boosted total issuancethrough the $40 billion mark for the first time,while at the other end, landmark issues bylower-rated credits showed the market'smaturity and ability to price at globallycompetitive levels.

And market participants expect the lower end of the spectrum to provide plenty ofactivity in 2005, with the recent (effectiveFebruary) expansion of the ratings spectrumof the UBS Credit and Composite Indicesfrom A- to BBB-. While this change is notlarge numerically, it is highly significant in itsramifications for the market – for the simplefact that most Australian companies are BBB-rated.

Inclusion of BBB issuers in the mainbenchmark index assures them of demandfrom Australian institutional investors, whopreviously could not buy their securitiesbecause their investor mandates did not allow them to go outside the index. The ramifications for the market's growth – and diversification – are huge and eagerlyawaited by the market.

However, the question of whether theappetite of local investors springs up quicklyenough, and in large enough mass, to divertAustralian companies from the deep andtempting US markets – for example the US private placement market – is a difficult one. Many market participants are hoping (in terms of the UBS indices) that it will be a case of “If you build it, they will come”,while others worry that issuers will only issuein the local market if they can do so at a costof funding which is competitive compared towhat they could do offshore.

Financial issuers continued to dominate the market, accounting for just over three-quarters of issuance in 2004, which poses a diversification challenge for the market.Many bankers wait to see whether changesto the index will bring an influx of industrialcredits to Australian institutional investors.

Conversely, the continued pull of the USprivate placement and Rule 144A marketsswelled the leakage of Australian issuanceoffshore, and there are no signs that thistraffic is on the wane.

In the structured credit area, record sub-wholesale and retail volumes continue to mask the fact that the participation of domestic wholesale investors, due to mandate restrictions, is limited. However,the ongoing contraction in credit spreadsshould continue to drive investor appetite for structured products.

This yearbook surveys the Australian market in detail. It provides a broad overviewof 2004 from the perspective of investorsand issuers. It contains detailed profiles of some of the more notable transactions of 2004; three roundtables with industryleaders capture the state of play and likelydevelopments for 2005 – in the primarymarkets, credit and structured credit. All sections of the markets are undergoingenormous change, and the Fixed Income & Credit Yearbook represents the mostcomprehensive and up-to-date summary of the market's current thinking and potentialdirections.

Many thanks go to our sponsors, withoutwhom this yearbook would not be possible.They are – lead-sponsor; Bloomberg. AlsoIntermediaries; National Australia Bank, TDSecurities, Fitch Ratings, Grange Securities,Nomura, Standard & Poor's, UBS, MorganStanley, JPMorgan, Westpac InstitutionalBank, Allens Arthur Robinson, BNP Paribas,MBIA, ASX, RBS, Citigroup, MallesonsStephen Jaques, Deutsche Bank, SG,Moodys Investor Service and Reuters.Investors; Macquarie Funds Management,ING Investment Management, QueenslandInvestment Corporation, Principal GlobalInvestors, Absolute Capital, ChallengerFinancial Services Group, SchrodersInvestment Management, Basis Capital andAberdeen Asset Management. And Issuers;Treasury Corporation of New South Wales,Treasury Corporation of Victoria, QueenslandTreasury Corporation, Commonwealth Bankof Australia, National Australia Bank,St.George Bank, Macquarie Bank, ANZ and Westpac Banking Corporation.

Michael StanhopeManaging DirectorPacific ProspectT 61 2 9251 8116E [email protected]

Foreword

004-005 3/4/05 11:46 PM Page 4

Growth sums up Australia's corporatebond market in 2004. In the process of absorbing a record $41 billion of issuance, the market made a stepchange in the pricing, tenor and volumeit offers. It is now globally competitiveand attracting borrowers – domestic and international – that previouslydismissed the market as too small, too hard or too far away.Written by Marion Williams

The market had little choice. It had tobe competitive to attract the issuancerequired to satisfy investor demandamid heavy government and corporatebond maturities, the bulk of which –$15 billion – fell due in the second halfof the year. Australia's institutionalinvestors demonstrated they haveestablished the skills and resources to move beyond their previous comfortzone in terms of ratings and tenors.Intermediaries agree the market ispoised to mature further.

Kangaroos critical to volumeThere is no way that the market would havebroken the $40 billion issuance barrierwithout Kangaroo borrowers, says MarkGarrick, head of primary markets of NationalAustralia Bank's Institutional Markets andServices. According to the bank, Kangarooissuance totalled $20.1 billion in 2004, almost triple the previous year's volume, and it was responsible for 49 per cent of theyear's supply. Kangaroo issuers now make up36 per cent of the corporate bond market'soutstandings, up from 28 per cent at the endof 2003.1

Garrick explains that several factors were at play to attract non-domiciled borrowers to the Australian market:

a) proceeds of Australian dollar issuesswapped into attractively priced US dollar Libor funding

b) with the spread between the governmentbond and interest-rate swap curveshovering around 50 basis points,domestic investors that previouslyshunned AAA Kangaroo bonds becauseof their narrow margins to swap were now keen buyers to take a view on thebond/swap margin. With some AAAKangaroo bonds trading level with swapscompared with semi-government bonds at 25 basis points under swap, the tradewas a no-brainer

c) on 4th March the Reserve Bank of Australia broadened the range of securities it accepts as collateral

for repurchase agreements. This broughtin banks' liquidity books as a new investorbase

d) there were periods when global investorsbought AAA Kangaroo bonds as one of many global “carry trades” to exploitwide interest-rate differentials betweenAustralia and the US and a favourableforecast for the Australian/US dollarexchange rate while taking virtually nocredit risk.

With these four factors interacting, thevolumes issued in the Kangaroo sector put Australia on the radar screen of moreborrowers than ever before.

Market pricing lower-rated credits involume at globally competitive levelsA similar thing was happening at the otherend of the investment-grade rating spectrum.The debuts by Tabcorp Holdings andGoldman Sachs (A+/A3) proved the marketcould offer volume and tenor at competitivemargins. In fact Goldman Sach's $1 billiondebut was one of nine transactions to hit the$1 billion mark during the year. Through thesetransactions four domestic and four offshoreissuers raised $9.345 billion.

Tabcorp, rated BBB+ with a negative ratingoutlook, is one demonstration of theAustralian credit market's maturity and ability to price at globally competitive levels.Via lead manager Westpac Institutional Bank, the gaming group priced $450 million ofseven-year debt at a margin consistent with the pricing on the 10- and 12-year deals

Primary Markets 2004 Wrap

5

004-005 3/4/05 11:46 PM Page 5

C1ear thinking

www.aar.com.au

Complex credit and fi xed income transactions require the

clearest of thinking. That’s why we

are number 1 in the fi eld,

as demonstrated by our involvement in:

Obelisk First 2004-1 CDO Squared CLNs

Westpac Structured Equity Solutions

ABCP FIN46 First-Loss Notes

Tabcorp’s US$700 million US Private Placement

Brambles’ US$425 million US Private Placement

ETSA Utilities’ US$387 million US Private Placement

Transurban’s US$247.5 million + A$72 million US Private Placement

Downer EDI’s US$180 US Private Placement

Coates Hire’s US$160 million US Private Placement

It’s how we point more than

60 of Australia’s,

and 20 of the world’s, top

100 companies

in the right direction.

For more information visit

www.aar.com.au

e

s

w

www.aar.com.au

Clear thinking

8

it subsequently priced in the US privateplacement market. Likewise SPI PowerNetpriced $235 million of seven-year debt whileits A+ rating was on CreditWatch Negative.When National Australia Bank embarked on a massive funding task to boost its capitalratios in the aftermath of its currency optionfiasco, it started its subordinated debtissuance in the Australian market. TheAustralian market effectively set the pricingfor the US dollar and Euro legs that followed.

The acceptance of investment banks as credits is another milestone, says RobVerlander, head of securities origination at Commonwealth Bank. “They providefrequent and liquid deals and they areprofessional borrowers that structuretransactions to meet investor requirements.”He also points to the growing acceptance of different structures such as Rabobank's$500 million perpetual issue that qualifies as Tier 1 capital and Royal Bank of Scotland's$1 billion Lower Tier 2 capital issue of callable10-year debt as signs of the market'smaturity. “When you can't get variations in credit you look for variations on thestructures that are coming. The reality is ifinvestors can pick up any additional spreadon a credit with which they are comfortablethen you can vary the structure.”

Credit intensity to growChanges to the UBS bond indices that

were proposed in July 2004 and becomeeffective in February 2005 will support further development in the credit curve. The Australian benchmark bond index nowincludes credits across the full range ofinvestment-grade ratings. Bankers say thatnot only must investors measured against the index buy into issues rated at the lower-end of investment-grade but those fundmanagers that previously sought tooutperform the index by buying BBB creditswill want to extend along the yield curve inthat part of the rating spectrum. A glimpse of that was seen in the fourth quarter.Previously issuers in the A and BBB ratingbands struggled to get competitive pricingbeyond five years, yet Goldman Sachs, SPIElectricity and Gas Holdings (A-), Tabcorpand SPI PowerNet raised over $1 billion ofseven-year debt in the space of two months.

Intermediaries welcome the index changesbut view the revamp as a validation of whatwas already occurring in the market anyway.Peter Bloomfield, head of corporatesecurities at Westpac Institutional Bank, says local investors are obviously gettingmore aggressive for lower-rated credits andthat has enabled the market to absorb lower-rated credits in greater volume than the past.“Over the years they have become morecomfortable with their ability to make calls on lower-rated credits and to do it in volume.”

The Australian benchmarkbond index now includescredits across the fullrange of investment-graderatings.

Chris Viol, head of credit research atCitigroup Australia, agrees, saying funds are more credit focused and have expandedtheir resources in this area. He notes that theimpending index changes have already had animpact on margins for 10-year subordinatedbank debt, callable after five years, ahead of their inclusion in certain revamped indicesin February. “You saw a real bid for those in the secondary market in the third quarter.”Another development potentially enablinginvestors to better use their credit skills is the launch of the DJ iTraxx credit defaultswap index in July. The 25-name indexincludes seven names that have not issuedlocally. As Citigroup's credit analysts wrote atthe time: “While admittedly credit derivativeshave thus far remained a mostly inter-bankmarket, how long fund mandates can ignoresuch changes remains to be seen.”

The combination of greater credit skills andthe index changes will see increasing depth in the BBB sector over the next one to twoyears, predicts Grant Bush, head of debtcapital markets at Deutsche Bank –Australia/New Zealand. In the past, therelatively short tenors of corporate bonds

have meant that they were buying the paper simply for the running yield. Now that investors have developed credit skills,“you will see them wanting to extend theduration of those investments so they'll get rewarded for the credit skills they havedeveloped. Instead of purely a running yieldargument, they will look to buy for out-performance, credit improvement andappreciation.” So rather than seeking capitalgains through duration views, they will alsolook to do this via credit views. Investorscan't really take a view on a company'smanagement or industry with a three-yearbond because the time frame isn't longenough and the capital appreciation won't be significant on a short-dated security. Thus Bush foresees investors expandingtheir use of credit from merely as a way of maximising spread to also helping tomaximise returns.

Verlander at Commonwealth Bank has similarexpectations and envisages that this will see relatively fewer domestic corporatesmake the trip to the US to undertake privateplacements. “Institutional investors arepricing at globally competitive levels, certainlyin the five- to seven-year part of the curve,and likely out to 10 years. I think you will seepretty big growth – if the yield curve makessense – given the cost of swap lines, upfrontfees and the logistics.” Such a developmentwould be timely. National Australia Bankcalculates that over the next two years 76 per

Primary Markets 2004 Wrap

The combination of greatercredit skills and the indexchanges will see increasingdepth in the BBB sector overthe next one to two years.

Grant BushHead of Debt Capital MarketsDeutsche Bank

Japan remains the mostsignificant international bid for Australian dollarproduct.

James HoustoneHead of Debt Capital MarketsNomura

008 3/4/05 11:49 PM Page 8

Even though listing on ASX

has become second nature, a short

list of the benefits of listing mightn’t

go astray. First, there’s the question

of appeal to investors. They enjoy

exposure to h igher y i e ld and

the potential

f o r g rea t e r

diversification

in a liquid and

t r a n s p a r e n t

marke t . Fo r

issuers, there’s

access to a

broader range of investors with

continuing growth and popularity

of listed Hybrids. Naturally, you

might want to discuss in more

detail why the ASX interest rate

market is the home for Hybrids.

Visit w w w. a s x . c o m . a u / i r m . h t m

or call Bob Biven,

Market Coordinator,

T ra d i n g M a r k e t

Development on (02) 9227 0934

or email [email protected].

OSBORN SOUTHGATE AX481 Australian Stock Exchange Limited ABN 98 008 624 691

Why listing

Hybrids has

become

accepted

wisdom.

AX481 9/19/03 4:01 PM Page 1

10

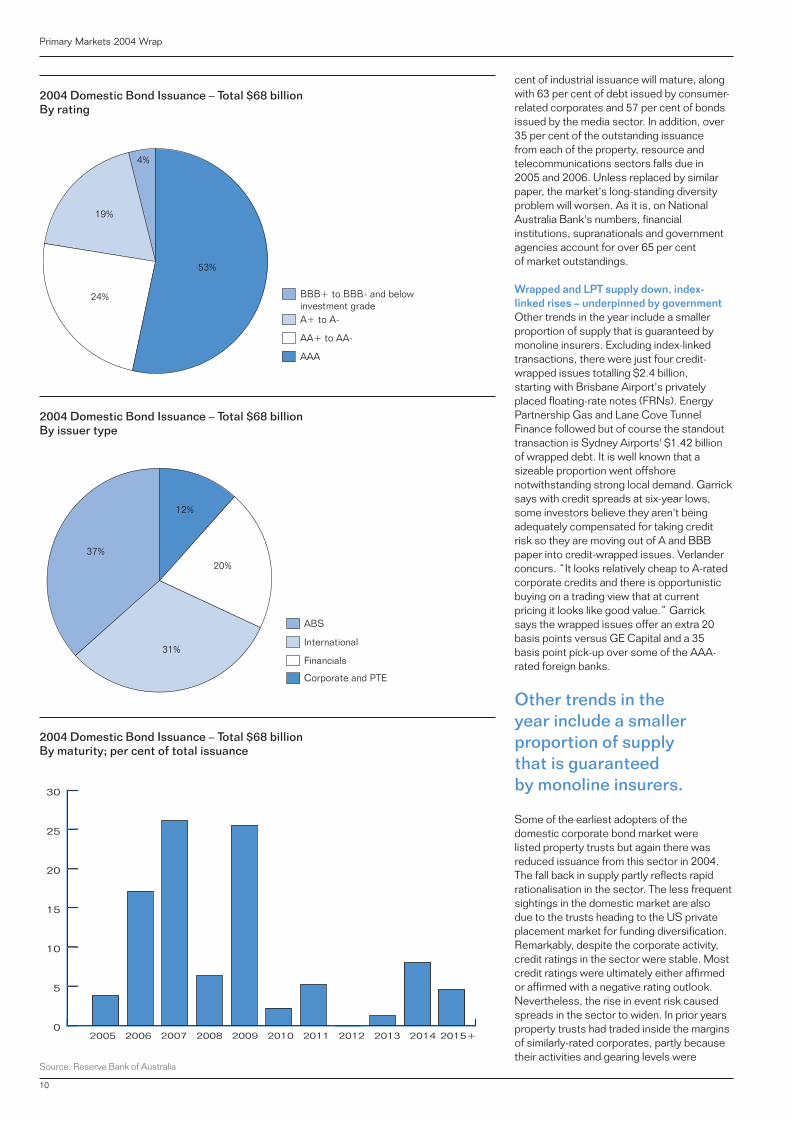

Source: Reserve Bank of Australia

cent of industrial issuance will mature, alongwith 63 per cent of debt issued by consumer-related corporates and 57 per cent of bondsissued by the media sector. In addition, over35 per cent of the outstanding issuance from each of the property, resource andtelecommunications sectors falls due in 2005 and 2006. Unless replaced by similarpaper, the market's long-standing diversityproblem will worsen. As it is, on NationalAustralia Bank's numbers, financialinstitutions, supranationals and governmentagencies account for over 65 per cent of market outstandings.

Wrapped and LPT supply down, index-linked rises – underpinned by government Other trends in the year include a smallerproportion of supply that is guaranteed bymonoline insurers. Excluding index-linkedtransactions, there were just four credit-wrapped issues totalling $2.4 billion, starting with Brisbane Airport's privatelyplaced floating-rate notes (FRNs). EnergyPartnership Gas and Lane Cove TunnelFinance followed but of course the standouttransaction is Sydney Airports' $1.42 billionof wrapped debt. It is well known that asizeable proportion went offshorenotwithstanding strong local demand. Garricksays with credit spreads at six-year lows,some investors believe they aren't beingadequately compensated for taking credit risk so they are moving out of A and BBBpaper into credit-wrapped issues. Verlanderconcurs. “It looks relatively cheap to A-ratedcorporate credits and there is opportunisticbuying on a trading view that at currentpricing it looks like good value.” Garrick says the wrapped issues offer an extra 20basis points versus GE Capital and a 35 basis point pick-up over some of the AAA-rated foreign banks.

Other trends in the year include a smallerproportion of supply that is guaranteed by monoline insurers.

Some of the earliest adopters of thedomestic corporate bond market were listed property trusts but again there wasreduced issuance from this sector in 2004.The fall back in supply partly reflects rapidrationalisation in the sector. The less frequentsightings in the domestic market are also due to the trusts heading to the US privateplacement market for funding diversification.Remarkably, despite the corporate activity,credit ratings in the sector were stable. Mostcredit ratings were ultimately either affirmedor affirmed with a negative rating outlook.Nevertheless, the rise in event risk causedspreads in the sector to widen. In prior yearsproperty trusts had traded inside the marginsof similarly-rated corporates, partly becausetheir activities and gearing levels were

Primary Markets 2004 Wrap

BBB+ to BBB- and below investment gradeA+ to A-

AA+ to AA-

AAA

53%

24%

19%

4%

2004 Domestic Bond Issuance – Total $68 billionBy rating

ABS

20%

12%

37%

31%International

Financials

Corporate and PTE

2004 Domestic Bond Issuance – Total $68 billionBy issuer type

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015+

2004 Domestic Bond Issuance – Total $68 billionBy maturity; per cent of total issuance

010 3/4/05 11:51 PM Page 10

12

restricted by trust deeds. Now however,property companies are trading at marginsfive to 10 basis points higher than 'true'corporates because of the escalation in event risk, says Garrick.

One area of growth that receives littleattention is index-linked debt. AngusCameron, previously division director, debtfinance at Macquarie Bank, says althoughstarting from a low base, issuance is up byone third on 2003. The Lane Cove Tunnel and Sydney Airports' deals were thesegment's main transactions. Both were wellsupported and attracted a diverse range ofinvestors, he adds. “We are alsoexperiencing greater interest in the classfrom offshore investors, contributing to theout performance versus the nominal market.”

The bankers interviewed for this article saythere was little to note in the government and semi-government bond market. Thatsaid, its presence is vital to the continueddevelopment of the non-government sector.“It is predicated on a very deep bond marketand futures market and deep and liquidcurrency and swap markets. Fixed-income isthe last one to develop. You need that entireinfrastructure before you can support volumeissuance at this level,” says Verlander.

Internationalisation of the market –intermediaries and investors follow issuersInternational issuers have been a feature of the bond market for several years now, and as the Kangaroo sector has grown inleaps and bounds, so has the number ofintermediaries. There are now 21 banks in the league tables. The internationalisation of Australia's non-government bond marketextends to the investor base. Granted someof the offshore investor involvement in 2004was cyclical as highly-rated Kangaroo bondswere one of many global “carry trades”favoured by investors around the world,however the participation of Asian investorsis a permanent feature of the landscape.Verlander at Commonwealth Bank saysthese days most transactions are over-subscribed and order books may have morethan 50 accounts. This is a change from thepast when the market was struggling todevelop and cornerstone investors wererequired. “We now tell investors to come in early with their bid so we can give them an appropriate allocation. If people leave ituntil the end they can get disappointed.”

Asian investors important, particularly for bank issuers of EurobondsThe arrival of Asian investors in the Kangaroosector needs to be kept in perspective.James Houstone, head of debt capitalmarkets at Nomura, reminds us that Japanremains the most significant international bidfor Australian dollar product. Japaneseinstitutional investor buying of large liquidlines of semi-government debt promoted tooffshore investors – the so-called global andexchangeable lines issued by QueenslandTreasury Corporation and New South WalesTreasury Corporation, respectively – issupplementing the waves of retail-targetedUridashi bonds. He adds that Asia's bid forAustralian dollar product is tiny comparedwith its bid for securities denominated in USdollars and Euros, thus the relevance of Asianinvestors to the Eurobond programmes ofAustralian borrowers, particularly the majorand regional banks.

Gerard Perrignon, director of debt capitalmarkets at Nomura, sees Westpac BankingCorporation's US$1.5 billion three-year FRN in May as a significant example of anAustralian borrower successfully combiningdemand across the Asian, European and US time zones with one product offering. It is one of the few global issues undertakenby an Australian borrower outside of thesecuritisation sector and it highlights theemerging opportunities available to Australianbanks to raise senior debt in the US market.Houstone says the banks have tended to relyon the Eurobond market for the bulk of theirsenior debt funding and have traditionallytargeted the US market more forsubordinated debt.

US private placements lead leakage offshoreSimon Maidment, head of fixed income

at UBS, says while it has been a good yearfor domestic issuance, the celebrations mustbe kept in the context of still strong growth inAustralian issuance in the Rule 144A andprivate placement markets in the US, as wellas in the EMTN and offshore securitisationmarkets. “There is still leakage of Australianissuers driven by the need for size or need for term or the ability to price credits thatdon't have ratings.” Research by NationalAustralia Bank shows by mid-year, AustraliaInc had already raised more money inoffshore markets than in any year exceptfor 2003 “and that year's total looks likely to be surpassed in the next six months”.2

Speculation that US private placementswould peter out proved incorrect. Around thesame number of Australian issuers tappedthe market as the previous year, but theypriced larger transactions, so producingincreased volume in 2004, says Bloomfield.With the tick-up in Australian merger andacquisition activity and a scant forwardcalendar of US corporate issuers, it is likelythe US private placement market will remainaggressive and continue to get its fair shareof deals, he says.

Outside of the private placement sector, the only Australian corporates to tap the US market via Rule 144A transactions were Foster's Brewing Group and Westfield.According to Simon Rothery, managingdirector of fixed income, currencies andcommodities at Goldman Sachs JBWere,Foster's achieved funding 15 basis pointscheaper than was possible in the domesticmarket, confirming that the US 144A marketremains competitive. Natalie Vanstone, head of debt capital markets at JPMorgan,views the US market as the hottest around.After all where else could an Australiancompany – Westfield – raise US$2.6 billion of debt in one go?

Europe offers greatest diversificationThat may be so but Europe offers unrivalledinvestor diversification through itsfragmented investor base, says Bush atDeutsche Bank. “There is no corporateissuer in Australia that has come close to tapping its full potential investor base in Europe. Mainstream Europe is massive so Europe is a fantastic opportunity forcorporates.”

Like the US where year-to-date corporatesupply has fallen to 28 per cent of totalissuance, corporate bond issuance has fallento 10 per cent of the European market'ssupply, from 15 per cent in 2003, saysVanstone. Therefore the slippage of 'true'corporate supply in the Australian market to around 17 per cent from 28 per cent in theprevious year isn't a local phenomenon but a global one, and nor did it stand in the way of the record $41 billion supply. Corporateliability management is exacerbating thesituation in Europe. Some companies areeither buying back debt or buying it to reissue

Primary Markets 2004 Wrap

There is still leakage of Australian issuers driven by the need for size or need for term or the ability to price credits that don't haveratings.

Simon MaidmentHead of Fixed IncomeUBS

012-014 3/4/05 11:55 PM Page 12

The Fitch Ratings Corporate Group offers a depth of research and analytics that reflectsbroad practical experience and foresight. Focusing our experience on the events thatcause change in the debt markets helps us stay ahead of challenging situations. Bring new products to market. And provide greater accuracy and timeliness in our ratings and research.

Diverse experience. A transparent process. Unparalleled service.All driving the growth of Fitch Ratings.

growthexperiencethrough

Driven to do things better

012-014 3/4/05 11:55 PM Page 13

14

fresh paper because it is more economic. In early December, for example, JPMorganconducted the buyback of €600 million bondsthat InterContinental Hotels had issued only a year earlier because it had a cheaper andmore flexible source of funds provided tothem by the bank market.

If Australian bond investorswant genuine namediversity they will have to compete on price.

Again, in a repeat of the US experience, therewas very little Australian corporate issuanceinto Europe in 2004. Amcor and Telstra'sEuro-denominated bond issues were verywell received, says Vanstone. She adds thatUS and European investors have a very highlevel of comfort with Australian borrowers. In the case of Australian banks, the country'slargest borrowers with annual senior debtfunding requirements of over $10 billion,offshore investors are comfortable with theoperating environment. The banks areperceived as having good quality, low riskassets, and stable strategies andmanagement teams. They therefore get“ticks across the board” as a way to diversifyaway from US and European banks, saysVanstone. She comments that Australian

issuers are very good at being transparent,proactive and maintaining comprehensivewebsites for offshore debt investors.

Despite domestic growth Australian issuersstill reliant on offshore debt marketsMaidment says it is vital they continue to bebecause Australia is reliant on foreign capital.Australian borrowers therefore need to haveclean credits to maintain access to offshorecapital markets. According to the NationalAustralia Bank research cited earlier, in the12 months to March 2004, Australian'scurrent account data reveal gross outflows of $80 billion and a net outflow of $74 billion.That net outflow consisted of $8 billion ofequity and $65 billion of debt. During thattime, Australian entities acquired $15 billionof foreign debt securities. So over the period,foreigners bought around $80 billion of debtsecurities from Australian entities.

Looking forward, the fundamentals look goodfor demand in the domestic market. There isvery little pre-deal switching by investors toaccommodate new supply, there is ongoingdemand to meet the portion of compulsorysuperannuation savings that is directed to thefixed-income portion of balanced funds, andRothery says around $10 billion of couponflows have to be reinvested each year.Furthermore, $12.2 billion of corporate bondsare scheduled to mature in 2005, $700 millionmore than fell due in 2004. Garrick adds thatif the equity market continues to perform as itdoes, fund managers will have to keep sellingequities to rebalance their portfolios so thatthey aren't overweight the sector. That freesup cash for other asset classes. Noting thatcorporate issuance is falling around the worldand stiff competition for assets, Bush says ifAustralian bond investors want genuine namediversity they will have to compete on price.“This isn't a volume market or one offeringdiversification of tenor.”

Vanstone comments that offshore investorsare divided into two camps – the technicaloptimists and the fundamental realists. The optimists believe credit will remain wellbid because corporate balance sheets are in good shape and because of thesupply/demand imbalance in global debtmarkets. The realists are mindful of a rise in shareholder-friendly behaviour such asshare buybacks and the up-tick in mergersand acquisitions. This leads them to questionhow long the current narrow credit marginscan be sustained before investors increaseallocations to other sectors.

1 Australian Credit Markets, National Australia Bank“Maturities in 2005 to add a new dimension?” 14 December 2004

2 Australian Credit Markets 20 July 2004 “FundingAustralia and the basis swap” National Australia Bank

Primary Markets 2004 Wrap

Offshore investors aredivided into two camps –the technical optimists andthe fundamental realists.

Natalie VanstoneHead of Debt Capital MarketsJPMorgan

012-014 3/4/05 11:55 PM Page 14

The consensus among Australian fixedincome fund managers is that 2005should be another year of benign creditconditions. They have identified a fewpotential landmines to monitor but seelittle on the horizon to cause a wholesalerebound in credit margins. Written by Marion Williams

The prolonged credit-friendlyenvironment isn’t necessarily sopositive for fund managers. Forstarters, retail and sub-wholesaleinvestors will continue to investdirectly in the raft of relatively highyielding and complex structuredproducts that investment banks are touting. The banks are devotingincreased resources to theseburgeoning investor segmentshowever some fund managers are hard pressed to find ways toinclude innovative products such as collateralised debt obligations(CDOs) in their clients’ portfolios.That is particularly so when assetconsultants have yet to embracestructured credit and instrumentssuch as non-investment gradedebt/equity hybrid securities. In the meantime, fund managers are listening to what their clients say they want and are trying tostructure new products accordingly.

Fund Managers Outlook for 2005

Another unwanted consequence of thepositive credit environment is that it willremain an issuer’s market. Notwithstandingthe changes to the domestic benchmarkbond index, the offshore debt capital marketsand the local bank loan market will continueto tempt a fair share of Australian corporateborrowers, so depriving local fund managersof the diversification they have craved foryears.

Somewhat ironically, therefore, life might get better for Australia’s fixed income fundmanagers when the inevitable downturn in the credit cycle hits. Local corporateborrowers may then discover the attractionsof their domestic bond market. It could alsobe a wake-up call to retail and sub-wholesaleinvestors that investing in credit is not a one-way bet and is perhaps something better leftto the experts.

A great year for Australia’s credit market – and most markets around the worldUndoubtedly 2004 was a great year forAustralia’s fixed income investors. Despite a rise in corporate activity, there were nomajor credit blow-ups and credit ratingsfinished the year largely unscathed. Creditmargins continued to contract against aglobal backdrop of reasonable economicsettings and corporate profitability. The other factor at work pushing in marginsglobally is too much money chasing too few investments. This is exacerbated by the rise of structured credit products. Thenarrowing in credit margins helped Australianfund managers to post solid returns overthe year.

It was the second consecutive year of recordcorporate bond issuance with over $41 billionof supply absorbed and with new issuers andnew structures arriving ahead of the changesto the benchmark UBS Australian CompositeBond Index in February 2005. Fund managers

applauded Rabobank’s step-up perpetualissue and Tabcorp received accolades for its willingness to test the local market’sability to absorb BBB-rated credit risk inreasonable volume and tenor at margins that are competitive with offshore markets, notably the US private placement market.

The offshore debt capitalmarkets and the local bankloan market will continue to tempt a fair share of Australian corporateborrowers.

Local fund managers were riding a wave that is sweeping across the world. WayneFitzgibbon, head of cash and fixed interest at Macquarie Funds Management, views the global fall in risk premium as the mostfascinating thing about 2004. “Creditspreads have contracted and we’ve seenmost bond markets rally or certainly notrespond as one would have expected to the Fed’s interest rate increases. I think itreally has been a bull market in pretty mucheverything and it is really interesting that wehave seen that reduction in the global riskpremium given the geopolitical picture andthe building economic risk in the worldeconomy.” After all, political risk hasn’tdiminished over the year, the US FederalReserve Bank is still on a path of monetarytightening, oil prices are up sharply, whichapart from anything else has implications for the worsening US current account deficit, and the US federal budget deficit hasincreased massively. All these factors haveimplications for the currency markets yet, asFitzgibbon points out, except for the closingweeks of 2004, it wasn’t a particularly volatileyear in the foreign exchange market.

16

001-039 3/4/05 11:58 PM Page 16

18

Fund Managers Outlook for 2005

While few investors anticipate significantlytighter spreads, they don’t expectfundamentals to deteriorate to the extent that sharply wider margins are warranted.Glenn Feben, Perennial Investment Partners’head of fixed interest, sums up the thoughtsof many fund managers. “We see only a modest and temporary slowing in Australianeconomic activity in the New Year and expecta continuation of the recovery story in bothEurope and North America. In our view, while the rally in credit markets has all butbeen exhausted, the favourable economiclandscape does not threaten any serious sell-off in credit markets.” If credit spreadsweaken in 2005 Feben believes it will bemore a correction from arguably extendedvaluations than as a result of any fundamentaleconomic weakness. Bill Entwistle, head of structured debt investments at AbsoluteCapital, comments there is a strong technicalbid with a wall of money still to flow intocredit.

Beware RMBS and corporates flush with cashThat is not to say that fund managers arecomplacent about credit performance in2005. The two most frequently cited hotspots are cashed-up corporates and theimplications of a hard landing in the propertymarket for the bubble that is residentialmortgage-backed securities (RMBS).

Mark Beardow, manager, credit markets at AMP Capital Investors, says acquisitionrisk is clearly a key event risk for the creditmarket at this point of the cycle. “Well-ratedcompetitors in consolidating industries may

be at risk and also those companies withfinancial positions materially stronger thantheir desired financial policies.” In a similarvein, Craig Vardy, portfolio manager, fixedinterest at Barclays Global Investors, is wary of corporates within sectors that are predisposed to returning capital toshareholders in the current environment.Therefore, rather than sectors wherecompanies are building cash, Beardowfavours those that are still benefiting from the strong economy and repairing balancesheets. He also likes property trusts andsome of the swap proxies. Subordinated debt of regional banks is the pick of GeorgeBoubouras, senior investment manager, fixed income at HSBC Asset Management.“Given the increase in competition in thedomestic bank market from the large globalplayers such as HBOS, HSBC and Citibank,we still view the regionals – includingSt.George Bank, Bank of Queensland and Suncorp – as performing well. It will be the larger players that will initially feel the competition given they have so muchincumbent market share.”

While it isn’t his central case, Rob da Silva,managing director of Principal GlobalInvestors’ asia-pacific fixed income, says a sharp decline in the residentialproperty market will likely have negativecredit consequences for mortgage-backedsecurities and for banks. In his view, non-conforming RMBS could be particularlyaffected because they are a relatively newphenomenon. As such, there is no historyregarding their performance in marketdownturns.

Robert Camilleri, senior manager, credit at Portfolio Partners, is one of several fund managers who is concerned that thecontraction in credit margins has beenfollowed by a loosening of credit standards.He says that when margins on AustralianRMBS reached their peak some three or four years ago the risks seemed muted given there were several mortgage insurers,lending standards were acceptable andproperty values were only just starting toappreciate. Camilleri contrasts that with thecurrent situation of RMBS margins trading at, or in some cases through, historical lows,and effectively there being just one mortgageinsurer. Additionally, “the concept of alending standard has become a myth in aneffort by the mainstream lenders to maintainmarket share in that anyone can walk in offthe street and state their income and borrowmoney. To top it off, the sector has seen the strongest growth for a decade fuelledartificially by government handouts and low interest rates.” He asks why spreadshaven’t widened if the risks have increased.

Relative value key in 2005As Fitzgibbon notes, the sharp fall in creditmargins means running yields are lower andthe probability of margins falling further isalso lower. Future returns are therefore going

to be less than the recent experience. Hesees debt/equity hybrids as most vulnerablebecause these deeply subordinatedsecurities are offering sub-bank bill marginsafter the franking credits are stripped out. “I think we’ll see a lot of investordisappointment with those sorts of fundsgoing forward because historic performancelooked great but the real performance going forward can’t be that great just looking at where spreads have got to.”

Credit spreads have beentrading on technicals, such as CDO issuance and hedging activity, forsome time and the rewardfor risk taken from movingaggressively down thecredit curve is negligible.

Fitzgibbon’s expectation for the creditmarkets in 2005 is “steady as she goes butwith increasing risk.” Beardow is in the samecamp. He expects that returns from the localcredit market won’t be of the same quality as in 2004 and also anticipates a higher ratioof spread wideners to tighteners. “It seemslike relative value will be the key, but at somepoint a less aggressive stance will need to be taken.” Vardy concurs. “One thing we willnot be doing is chasing absolute yield. Creditspreads have been trading on technicals,such as CDO issuance and hedging activity,for some time and the reward for risk takenfrom moving aggressively down the creditcurve is negligible.”

Fitzgibbon expects Macquarie FundsManagement’s focus on relative value will berewarded in 2005 and in the following yearspreceding the inevitable downturn. He says in a bull market, managers that rush out tobuy everything look like geniuses whereasmore circumspect managers like Macquarieunder perform. The opposite applies at theend of the bull phase. “As past experiencehas shown, our approach really substantiallyoutperformed our competitors when we’vehad meltdowns in the past. Not gettingcaught up in bull market frenzies and notgetting caught up chasing paper just for thesake of it always stands you in good stead in the long run.”

How to meet client demand for absolutereturn at the top of the credit cycleFitzgibbon doesn’t envisage a major ruction in credit until perhaps 2008 or 2009. In themeantime fund managers must respond tothe shift towards direct investment by theretail and sub-wholesale sectors. In part thetake-up of instruments such as CDOs anddebt/equity hybrids by non-professionalinvestors is a product of the benign creditenvironment. They are frustrated at the

It will be the larger playersthat will initially feel thecompetition given theyhave so much incumbentmarket share.

George BoubourasSenior Investment Manager, Fixed IncomeHSBC Asset Management

001-039 3/4/05 11:58 PM Page 18

Moodys_HSF05.pdf

Fund Managers Outlook for 2005

relatively low yields offered by traditionalfixed income and, after a sustained bullmarket, many people are tempted to thinkanyone can make money from investing.

In the case of fixed income, Tony Adams,senior portfolio manager, credit funds atColonial First State Investments, says thereis the additional problem that a managed fixedincome fund doesn’t look or feel anything likebuying a fixed income investment. Beingopen-ended, bond funds don’t have a fixedmaturity date. Nor do they have a promisedcoupon rate – the funds can only distributewhatever they receive. In his view, that is why CDOs are proving so popular – it isn’tjust the yield they offer but because they looklike a bond. Rightly or wrongly, because thereis a quoted coupon, retail investors believethat there is more certainty of the return.

To Andrew Canobi, senior credit analyst,fixed income at INVESCO, one criticalchallenge for 2005 is to work through the risk and liquidity issues with investors whoare searching for absolute or minimumreturns in a rising interest rate environment.In some respects there is a chicken-and-eggsituation when trying to include structuredproduct in managed funds. Open-endedfunds have difficulty with the illiquidity of

many structured products but liquidity andprice transparency will remain elusive as longas structured products continue to be held by the retail and sub-wholesale sectors.Beardow expects asset consultants willaccept structured products over time andbelieves those who don’t will come undercompetitive pressure. He adds though that to date the push for structured product hasbeen led by investment banks rather thanfund managers.

Regardless of whether or not assetconsultants come over the line, Derek Tsui,BT Financial Group’s head of credit, says itwill be some time before he is comfortableputting all structured products into his funds.“The ability to manufacture complexsophisticated products has not always beenmatched by the ability to understand andanalyse them. Consequently we haveavoided many of the more esoteric structuressuch as CDO-squared. We may purchasethem in the future but only when we aresufficiently comfortable that we can fullyanalyse the underlying risks.” Similarly, while QIC has a positive disposition towardsstructured credit and high-yield securities, it believes static CDO pools are inherentlyrisky and should be avoided because itsphilosophy is that investing in CDOs requiresprofessional active management. SusanBuckley, QIC’s general manager of globalfixed interest, says the breadth anddevelopment of available credit derivativeinstruments gives active fund managers theability to structure credit transactions such as managed credit-linked notes to deliverhigher returns for clients with lower levels of risk than passive investments in CDOs. In addition to credit default swaps and credit-linked notes, Buckley also favoursincorporating index derivatives such as theDow Jones CDX.

It is not always easy to offer return via high-yield bonds given the illiquidity and verylimited diversification of the Australiandomestic high-yield market. “It may be moreappropriate to consider high yield as a smallcomponent of an otherwise high-grade fundor to think in terms of global high yield,”comments Canobi. In Vardy’s opinion, thereal issue for consultants remains one ofselecting the most appropriate benchmarkagainst which to properly measure the alphaand tracking error being generated bymanagers who provide high-yield fixedincome products.

The search is on for new productsIt is clear that Australia’s fixed income fundmanagers are going to have to do thingsdifferently. Camilleri says Portfolio Partners is focusing on enhanced cash-type products.“With the recent successful marketing ofING Direct and Dragon Direct, we believe the old-style cash management trust is dead.The investor needs a return consummatewith these offerings. The challenge is can

we deliver a better return after fees withoutdelivering substantially more risk to theinvestor.” da Silva at Principal GlobalInvestors views the development of retail and sub-wholesale segments investingdirectly in innovative products as a logicalmarket response to a high level of demandthat presumably was not being metadequately – or perhaps not at the right price– by the managed fund alternatives. “Thechallenge for managed funds is to mount acompetitive response in the form of productsthat deliver the risk/return outcomes that thismarket wants, using distribution models thatare designed to provide pricing that is seenas value for money.”

The challenge for managed funds is to mounta competitive response in the form of products that deliver the risk/returnoutcomes that this marketwants, using distributionmodels that are designedto provide pricing that isseen as value for money.

Thus around half of the fund managers whocontributed to this article are launching newofferings. AMP Capital Investors is receivingencouraging feedback from clients andresearchers on its new retail-focusedEnhanced Yield Fund. In 2005 the group willfine-tune its line up of products and promotethe launch of its new Core Plus StrategiesFund. The fund, which combines Australianbonds and global credit, is co-managed byGoldman Sachs Asset Management.Beardow also expects significant progress in its efforts to include structured products in portfolios for clients.

BT Financial Group’s Enhanced Credit Fundtrades corporate securities, structured creditincluding RMBS and CDOs, hybrids and high-yield bonds. Tsui says the fund activelyseeks returns from multiple strategies ofperformance within a comprehensive riskmanagement framework. Through thisframework various strategies are rigorouslydefined by their underlying risk/return profilesrather than limited by traditional securitymeasures. According to Tsui, this approachgives the fund great flexibility to takeadvantage of various opportunities acrossthe whole market. Citigroup AssetManagement will focus on further developingits alpha transfer product capability. MitchellStack, director and head of fixed income atCitigroup Asset Management, says there willbe particular emphasis on its global capabilityin the high-yield and emerging debt marketsas sources of added value to a core domesticmandate.

20

The additional problem thata managed fixed incomefund doesn’t look or feelanything like buying a fixed income investment.That is why CDOs areproving so popular – it isn’tjust the yield they offer butbecause they look like a bond.

Tony AdamsSenior Portfolio Manager, Credit FundsColonial First State Investments

001-039 3/4/05 11:59 PM Page 20

© 2004 National Australia Bank Limited ABN 12 004 044 937 (12/04)

www.nabmarkets.com

The best bonds are the ones we build

with our clients.

As a leader in the Australian bond market, National Australia Bank has the knowledge, expertise and executional strengthto maximise the success of your next issue. As the winner of insto's 2004 Vanilla Bond House of the Year*, our innovativeapproach to understanding the needs of our clients has enabled us to put together some of the best regarded bond dealsof the past year. So if you’re looking for proven performance and distribution capability, talk to us today.

Morgan Stanley

A$355m5 Year Kangaroo IssueJoint Lead Manager

Merrill Lynch & Co Inc

A$160m & A$415m5 & 10 Year Kangaroo IssueJoint Lead Manager

Bank of AmericaCorporation

A$350m5 & 7 Year Kangaroo IssueJoint Lead Manager

ING Bank (Australia)Limited

A$680m5 Year Fixed/Floating Rate MTN Issue Joint Lead Manager

SPI Australia Finance Pty Ltd

A$170m & A$235m 4 & 7 Year MTN Issue Joint Lead Manager

Mitsubishi DevelopmentPty Ltd

A$150m3 Year Fixed Rate MTN IssueSole Lead Manager

Rentenbank

A$200m5 Year Fungible Kangaroo IssueJoint Lead Manager

BOS International(Australia) Limited

A$560m5 Year Fixed/Floating Rate MTN Issue Joint Lead Manager

CSR Limited

A$200m5 Year Fixed Rate MTN Issue Joint Lead Manager

Smorgon Steel GroupLimited

US$80mSenior Notes due 2011/14Joint Agent

General Property Trust

A$250m18 Month Callable FRN IssueSole Lead Manager

SPI Electricity & GasAustralia Pty Ltd

A$350m4 & 7 Year MTN IssueJoint Lead Manager

Telstra CorporationLimited

A$500m10 Year Fixed Rate MTN IssueJoint Lead Manager

HSBC Bank AustraliaLimited

A$150m5 Year Floating Rate MTN Issue Joint Lead Manager

SNS Bank N.V.

A$550m3 & 5 Year Kangaroo IssueJoint Lead Manager

Coates Hire Limited

US$160mSenior Notes due 2011/14/16Joint Agent

* Source: insto's 6th Annual Distinction Awards - December 2004.These announcements appear as a matter of record only.

Australia Post

A$230m3 Year Fixed Rate MTN IssueSole Lead Manager

C+Fi Tombstone Ad_F21_12 22/12/04 4:59 PM Page 1

22

Fund Managers Outlook for 2005

Macquarie Funds Management is enjoyingsuccess from its entry into the hedge fundbusiness. Having started with an activecurrency product, the group will look toexpand the range of hedge fund products in 2005. It is also developing its competency in credit management and over the comingyear will be adopting a number of differentstyles, moving into higher risk products and looking at mixing and matching activemanagement and credit portfolios with someother investment styles. Additionally, thegroup is working on alpha transfer products and Fitzgibbon says its currency hedgingsolutions business for superannuation funds is proving very popular.

The lack of diversificationin the domestic corporatebond market continues to be a major challenge for local fund managers.

Amid rising allocations to overseas equities,the hedging solutions business has arisenfrom equity managers’ growing awarenessthat the perceived wisdom that currencydoesn’t matter in the long run is misplaced. “I think it has just focused people’s minds on the impact that currency fluctuations canhave on the overall return in their funds. Withcompetition increasing between super funds,and further intensifying with the choice-of-fund, I think a lot of superannuation fundsdon’t want to be in the position where theycome up with very well thought out strategiesand well thought out portfolio structures fortheir members but forget to think about thecurrency hedging and end up being blown outof the water by having the wrong amount ofhedge or none at all.”

Merrill Lynch Investment Managers isharnessing its global credit expertise to offershort duration credit products such as the MLDiversified Credit Fund and the ML MonthlyIncome Fund. Both access global creditexposures that are swapped into floating-rateAustralian dollars. Stephen Miller, managingdirector of fixed interest and cash at MerrillLynch Investment Managers, says theMonthly Income Fund lends itself to theincome-motivated investors in the sub-wholesale market. “We believe investing for income will be a growing market trend and one that is substantially concentrated in the sub-wholesale part of the market.Accordingly, much of the work we have donein the product space and in terms of businessstrategy is focused on this part of the market.Distributional strategies will also be animportant ingredient in the success ofmanagers engaging this market.”

To da Silva, one of the highlights of 2004 wasthe launch of the Principal Global StrategicIncome Fund. It is a low duration, low volatility

fixed income fund that targets high-incomeopportunities around the globe. Theinvestment objective is to achieve, beforefees, a total return for investors of three per cent per annum in excess of the UBSBank Bill Index when measured over rollingthree-year periods. According to da Silva,performance has been strong and the initialresponse and interest has been veryencouraging.

Adams at Colonial First State Investmentssays it is all well and good to launch newproducts but fund managers must be mindfulof cannabilising their existing offerings. “We have ‘X’ amount of product but we can only get ‘Y’ amount of shelf space fromanyone, whether it is from a planning group or an asset consultant. We have to targetwhat product we offer and we have to focuson what can meet our clients’ objectives andgive them the best value. It is a major productissue.”

Domestic diversification remains difficultIn the meantime, the lack of diversification in the domestic corporate bond marketcontinues to be a major challenge for localfund managers. There are several reasonswhy “true corporates” are still a minority inAustralia’s domestic corporate bond market.The average rating of rated corporateAustralia is in the range of A- to BBB, a partof the rating spectrum that the local markethas been slow to embrace. That was partlybecause the benchmark index cut off at A-.As such, even securities rated A- struggled to attract investors because fund managersdidn’t want to be forced sellers in the event of a credit downgrade. Additionally, the localbank loan market and offshore bond marketshave considerable appetite – at verycompetitive margins – for corporates in thisrating group. Another consideration is thatfund managers and asset consultants aremindful that portfolio diversification becomesincreasingly important further down theratings ladder. In an economy as small asAustralia, accessing a sufficiently diverserange of companies in the lower investment-grade and non-investment grade rating bandsis always going to be difficult. Of course thisproblem isn’t confined to the bond market –banks and financial institutions account foraround a third of the local share market’scapitalisation.

Fund managers therefore don’t view thebroadening of the benchmark index inFebruary 2005 to capture BBB credits as the panacea for the market’s diversificationproblems. Canobi at INVESCO says theindex change will have little impact on the market’s dynamics until there is a greatdeal more issuance by lower-rated credits,something which is unlikely to happen quickly.“Issuance by lesser-rated companies will only be encouraged if fund managers,consultants and end-investors are willing to put more risk into portfolios, price it

appropriately and commit the necessaryresources to understand and manage therisks adequately.”

Boubouras at HSBC Asset Managementcomments that private placements in theBBB category have not always presented the required liquidity in the past. The entry of index managers to a new part of the creditcurve will therefore benefit issuers andinvestors alike because of the improvedliquidity. Principal Global Investors’ da Silvasays while the broader index will provide a deeper investor base for BBB-rated issues at the margin, the change itself won’t automatically lead to more corporateissuance. “The domestic corporate bondmarket will still have to compete with sharppricing from bank loans and with the deeperoffshore markets, in particular US privateplacements, which a number of well-knownlocal companies have tapped this year.”Buckley notes that several Australian bluechip companies such as PBL and Fairfax havetheir only domestically issued bonds maturingin the next 12 months. “It is imperative to the development of the Australian creditmarket that such issuers refinance their debtdomestically and that new issuers are alsoattracted to the market,” she says.

Fund managers are taking a number of different pathsto deal with the limiteddomestic diversificationopportunities.

Fund managers are taking a number ofdifferent paths to deal with the limiteddomestic diversification opportunities. Some,such as Macquarie Funds Management, are outsourcing global credit. That way theycan offer co-mingled Australian and globalcredit product. Likewise, QIC uses a blend of internal and external management in itsDiversified Fixed Interest Fund that includes a global credit component and AMP haslinked-up with Goldman Sachs AssetManagement for its Core Plus StrategiesFund. Others are using their group’s globalcredit expertise to access diversificationopportunities through alpha transferproducts. Merrill Lynch InvestmentManagers’ process embraces the concept of non-benchmark foreign-sourced credit and sovereign securities in its portfolios. “The beta is defined by thebenchmark, the alpha is anywhere that youcan see to extract it,” says Miller. In the caseof QIC, Buckley says that structured productwill be a focus in 2005 as a way to continue to diversify exposures via the creditderivative market and that the group is givingattention to the use of credit default swaps in domestic credit funds. “The developmentof the credit default swap market will presentopportunities in 2005. These products

001-039 3/4/05 11:59 PM Page 22

Whose vision can help you navigatethrough complex markets?To crack the fixed income market in today’s conditions, you need global power.Nomura is the debt adviser of choice for some of the worlds largest investors,offering deep market knowledge and technical expertise. With global connections,Nomura’s skill set covers international markets and currencies – offering an enviablecombination of liquidity and capital commitment with a focus on fixed income.

For more information, visit www.nomura.com or contact:

Flow Sales Structured Product SalesJames Hayes Leo D’AndretiHead of Fixed Income Sales DirectorFixed Income Sales, Australia Structured Products Sales, AustraliaTel: + 61 2 9321 3704 Tel: + 61 2 9321 3703

David Rockliff Gavan LynnExecutive Associate DirectorFixed Income Sales, Australia Structured Products Sales, Australia Tel: + 61 2 9321 3701 Tel: + 61 2 9321 3707

NOMURA ICEBREAKER AD 16/12/04 4:07 PM Page 1

Fund Managers Outlook for 2005

provide the opportunity to gain exposure toless liquid securities and issuers not includedin the index.”

Diversification no less a problem in CDO collateralEntwistle at Absolute Capital believes thelack of diversification in the Australian marketextends to the CDO sphere. He says thatrecent history has shown that lower volatilityclasses of collateral such as bank loans andasset-backed securities (ABS) are better and more reliable sources of income streamthan high-yield and investment-grade bonds.

Bank loans are generally senior obligations of corporations secured by the workingcapital assets of the company, are floating-rate in nature, have relatively high recoveryrates as a result of the security package and they have low price and default volatility.Likewise, the mezzanine tranches of ABS are mostly floating-rate and have significantlevels of structural subordination that alsoresult in relatively low price and defaultvolatility. Entwistle contrasts this with high-yield and investment-grade bonds. Theseforms of collateral have fixed-rate coupons,are unsecured obligations, require an interestrate hedge at the special purpose vehiclelevel and are inherently high in terms of price and default volatility. Event risk isanother major component of investment-grade corporate credit that impacts theperformance of CDOs. Therefore inherentlylower expected loss features of this collateralare at odds with unexpected credit eventsbecause of the amount of structural leverageapplied to these transactions, he says.

I don’t think you canmaintain that cycle for a long time withoutsomething nasty happening.

Noting that CDO performance is stronglylinked to the performance of underlyingcollateral, Entwistle says collateralised loanobligations (CLOs) have the best historicalperformance at all levels of debt and equity,while CDOs backed by high-yield andinvestment-grade bonds have the worstperformance. He thinks the point aboutcollateral is important because the vastmajority of structured credit products offeredto Australia’s retail and middle market isCDOs backed by investment-gradecorporate credit. To Entwistle the implicationsare obvious. “Investors are generally notgetting access to the most suitable collateraltypes. Only investors taking advantage of themanaged funds approach to credit have thatluxury.”

Active/passive debate reopens andpotential for increased government supplyFor Feben at Perennial Investment Partnersthe challenge for 2005 is to think creatively

about ways to enhance returns while stillremaining true to the general notion of fixedinterest being the “defensive” asset class.He views the reopening of the debateregarding active versus passive fixed interestmanagement in Australia as one of thehighlights of 2004. “We think this is a veryimportant discussion and think it will againoccupy the minds of many investors in theyear ahead as we all confront the reality oflower nominal returns and the continuedstructural transition of the Australian fixedinterest market from government-guaranteeddebt to corporate debt.”

Only four or five years ago there were projections of budget surpluses thatwere going to be used to pay down the socialsecurity deficit.

That said, in the years ahead, Fitzgibbon at Macquarie Funds Management seespotential for a “massive” increase inissuance from the federal and stategovernments. He believes their underlyingbudgetary positions have deteriorateddramatically in the last five years although this hasn’t become obvious yet amid 14years of unbroken economic growth, lowunemployment, and with property priceskeeping state government coffers healthy via stamp duty. Furthermore, spending oninfrastructure has been constrained and thiswill have to be reversed at some point giventhe growing negative noise surrounding thelikes of trains and hospitals in New SouthWales.

As well as this pressure to increasespending, Fitzgibbon sees pressure comingon the revenue side once the property marketand broader economy cools. “If at somestage the unrelenting boom in the Australianeconomy ends I think people will be verysurprised by how dramatically budgetarysituations will deteriorate.” He has seenresearch that points to new (federal)government bond supply of $100 billion to $120 billion over a three- or four-yearperiod in the event of a recession.

He says the recent experience of the US is instructive. Only four or five years agothere were projections of budget surplusesthat were going to be used to pay down thesocial security deficit. Contrast that with thecurrent US budgetary situation. “Admittedlythere are special factors with the militaryspend but the pace of decline in the USbudget has been breathtaking and the realityis there’s no reason it won’t be just asbreathtaking here if you have the combinationof political pressures on the expenditure sideand the fact that the revenue base of mostgovernments is grossly inflated by the stateof the economy.”

Eyes on CDOs when credit cycle turns downAgain looking far beyond 2005, anothercommon theme is how CDOs will performwhen the credit cycle turns down. Entwistlesays the cycle-low credit spreads haveimplications for investors, particularly instructured credit where investors are taking a levered credit position. “Tighter creditspreads have driven structural innovation inthe search for maintaining yield in structuredcredit. That has been at some cost in termsof additional complexity and higher risk forthe less savvy investor.” He points to thesynthetic CDO-squared market where hesays the economics of these transactions are driven by only 10 to 20 per cent of thecollateral with the remaining 80 to 90 per centcontributing nothing in terms of economicsexcept portfolio diversity. When the creditmarkets experience some stress Entwistlepredicts the more levered structures willinvariably be the ones to be impacted first.“Under this scenario, the concept of a barbellapproach to credit will have true meaning to the participants who have the biggestinformation disadvantage – that being retailand middle-market investors.”

Adams at Colonial First State Investmentssays the ramifications of stress in a particularindustry segment back through the CDOswith their leverage and the debt hedging willbe phenomenal. “It has to be when you leversomething that hard. When it works, it worksreally well. When it doesn’t, it blows.” Hiscolleague, Philip Preston, senior manager of credit at Colonial First State Investments,says now that pricing has come down, thenext thing that has inevitably happened in thebenign credit environment is that structuresand credit standards are really starting tochange for the worse. “I don’t think you canmaintain that cycle for a long time withoutsomething nasty happening.” TonyFitzGerald, Colonial First State Investments’head of credit funds, adds: “It is just like themid-1990s again. Spreads and structuresdeteriorate in some belief that the creditcycle has gone away but guess what – ithadn’t. We are already seeing corporatesstart to support shareholder returns withspecial dividends and other shareholder-friendly activity. These are the first steps to increased leverage and a return to thereality that if you own a five-year bond, a lot can change in that time.”

Vardy at Barclays Global Investorscomments it may not be all bad for fixedincome managers. “If we were to see severalcorporate failures or big-name ratingmigrations there could be a shift backtowards more conservative and transparentcredit strategies. That would present anopportunity for us.”

24

001-039 3/4/05 11:59 PM Page 24

Morgan Stanley and One Client At A Time are service marks of Morgan Stanley Dean Witter & Co. © 2005 Morgan Stanley.

Morgan_MSC-025_A4Size_Hires.pdf

26

Roundtable – TD Securities

Pashley: 2004 fixed income, I think a numberof things have taken people by surprise. In preparation for today I thought it wasworthwhile to collate some of the thoughtsfund managers put to us in early January.Each year we try to get a theme from the fund managers we speak to, to get a handleon where TD can position itself in relation to offering product, outlining our stanceregarding the economic backdrop and our view on rates.

Here are some of their comments:

“Credit spreads were way too tight in January, so it was a bit crazy to overweight them.”

”If you're not short directionally, you're crazy because rates are going higher.”

“Why on earth would you be holding longbonds right now with a yield curve this flat?”

“Honestly there's absolutely no reason tohold Australia at 200 basis points over theUS – see you later at 400 basis points.”

Here we are in December, 12 months on, and using the Lehman credit index as abenchmark, the credit spread is 14 basispoints tighter than when we started. We'vegot 3-year bond yields 50 basis points lowerthan they were in January when thosecomments were made and the 10-year bondyields 70 basis points lower than they were in January. Furthermore, the yield curve is 20basis points flatter. The Aussie/US spread is now 50 basis points tighter.

With this is mind, I then stepped back andlooked at the general performance of theactive fixed income funds within Australia. I was surprised to see (basis October data)there weren't too many domestic funds that were far away from benchmark. What I wanted to do as an icebreaker today is work

Chairman:

Chris PashleyManaging Director, Capital Market SalesTD Securities

Participants:

James WrightHead of Fixed IncomeING Investment Management

Stephen KnightGeneral Manager, Treasury & Deputy Chief ExecutiveNSW Treasury Corporation

Michael HallVice President & DirectorCapital Market Sales TD Securities

Lindsay SkardoonDirectorSpectrum Asset Management

Julian FoxallPortfolio ManagerPIMCO

Roundtable

Stuart GrayCredit AnalystDeutsche Asset Management

Rob da SilvaManaging Director, Asia-Pacific Fixed IncomePrincipal Global Investors

Stephen MillerManaging Director, Fixed Interest and CashMerrill Lynch Investment Managers

Michael KorberCredit SpecialistPerpetual Investments

Louis DavisHead of Financial Institutions Credit ResearchNational Australia Bank

Ross BoltonPortfolio Manager, Fixed InterestState Street Global Advisors

Primary Markets ForecastIn a roundtable discussion sponsored by TD Securities a group of leading fund managersexplain how they ended 2004 with very good returns despite starting with positions based on expectations that turned out to be misplaced.

They see little reason for credit spreads to widen noticeably in 2005 except for specific namesso for the most part credit will continue to be source of alpha for fixed income fund managers.Nor do they anticipate that the changes to the domestic benchmark bond index will make agreat difference. For the foreseeable future the credit market will therefore remain one of short-duration and high credit quality that lacks diversification of issuers.

Another challenge that fund managers face is the investment banks' move into the sub-wholesale market to exploit the shift to direct investment. That is particularly so when yields arelow, when the bull run in credit hasn't allowed fund managers to show their value, when fundmanagers are paid to outperform an index rather than to provide a specified absolute return andgiven there are so many mouths to feed between the end investor and the fund manager.

For further information, please contact TD Securities on:

Chris PashleyManaging Director, Capital Market SalesT 61 2 9619 8866E [email protected]

Michael HallVice President & DirectorCapital Market Sales T 61 2 9619 8866E [email protected]

001-039 3/5/05 12:00 AM Page 26

Roundtable – TD Securities

our way around the table and hear commentsfrom each of you as to whether or not I gotthe themes correct at the beginning of theyear, or whether I was just being spun a story.Alternatively whether or not people were very quick to realise that those main themesweren't going to play out and were able torecoup some of the clear losses that wouldhave been made by that initial strategy and if so, how that came about.

Foxall: I'm the Portfolio Manager at PIMCOhere in Sydney. Out of the Sydney office welook after our Australian portfolios. As well as global portfolios even though they'redirectly managed out of California. I don'tthink our position at the beginning of this year was much different from what Chrissaid. Certainly we thought credit spreadswere too tight, and we had concerns that with the maturities that were coming up inSeptember and October there might be somedifficulties. However obviously they weren't a concern as the year went through. In termsof overall yields we expected yields to gohigher through the year and I suppose for thefirst half of the year they did do that but thenin the second half things turned around. Asfar as the Reserve Bank was concerned wewere thinking they were going to raise ratesat some stage through the year but in nohurry to do so.

In terms of how we positioned ourselvesthrough the year, our ability to put globaltrades in our portfolios has helped us thisyear. I would say through the year we'vetaken advantage of the spreads, not so muchin credit but in terms of swaps. We've had a curve position which is relatively neutral and that's not done us too much harm andwe've also had global positions on whichhave helped us perform through the year. So at the end of the year our performancehas turned out to be pretty good.

Skardoon: We run an absolute return fundand we specialise in credit. We're probablygoing to be the standout here in that weprobably disagreed with everything that wassaid. We certainly thought that credit couldcome in. The reason for that, if you look atcredit over the last 15 years, particularly inthe US, credit spreads were still trading wellabove average. Therefore despite the fact it had contracted quite a bit, we saw therecould still be a lot of contraction comingthrough.

The other thing we thought of at the time wasthere was a war that was being funded. If youlook at the amount of money that was beingpumped into the US economy, if it wasn't upand running hard and fast by December lastyear then there was something inherentlywrong. You could see that if you went to aPolo store in New York where normally theywere 15 deep, you could walk in there andwade up to the counter without having to get in front of anyone. The same anecdotalevidence is here in Australia as well. If youweren't a Harvey Norman then generally

most retailers are struggling, particularly in the clothing and shoe side. They willcontinue to struggle, even more so givencompetitive pressures coming out of China.Therefore we thought if you looked at the market generally there was a lot ofopportunity there for credit not to weakensignificantly as it was unlikely that rates were to rise.

We didn't see a case for interest rates to rise.In fact we probably would have been arguinginterest rates should have been falling, but having said that, the way the ReserveBank of Australia (RBA) has handled interest rate policy this year or monetary policy, it has done a fair job. If you're looking downthe credit curve or further out on the track,credit now seems to be trading well throughits mean (average). Certainly credit is trading through it's mean and then standarddeviation, whether you look at cross-overs, B indices, European high yield, US high yield,they're certainly trading lower now. If you lookat BB indices they're trading-lower as well.About the only thing that doesn't seem to betrading too far out of norm is the BBB area.Therefore if credit spreads could contract anyfurther I'd probably be long the BBB sector. It is certainly an area in Australia that seemsto have well and truly forgotten but you'regoing to have to be very careful on who youpick – the free lunch is no longer there in thelong-term.

Knight: Steve Knight of NSW TreasuryCorporation (TCorp). On the fundsmanagement side of our business, we manage about $15 billion of assets onbehalf of our clients. Our clients are basicallyall state government entities. The money we manage is split pretty evenly betweenfunds that are outsourced, where we act as a manager of managers with the fundsallocated across the asset sectors, and about$8 billion in funds that we manage in-house in cash and fixed income mandates. Typicallywe tend to be at the very conservative end of the credit spectrum which really reflectsthe nature of the clients' requirements or the liabilities that we are managing against, so we have very little credit in those funds or in their benchmarks. We have tailoredbenchmarks for each of those funds, and wetend to be investors in the supranational areaand in the higher grade part of the spectrum.