european diesel locomotive and railcar market: strategic analysis of rail alternative powertrain...

TRANSCRIPT

European Diesel Locomotive And Railcar

Market: Strategic Analysis Of Rail Alternative Powertrain Technologies

© 2011 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

M6DB-18

February 2011

2M6DB-18

Disclaimer

Frost & Sullivan takes no responsibility for any incorrect information supplied to us by manufacturers or users.

Quantitative market information is based primarily on interviews and therefore is subject to fluctuation.

Frost & Sullivan research services are limited publications containing valuable market information provided to

a select group of customers in response to orders. Our customers acknowledge when ordering that Frost &

Sullivan research services are for our customers’ internal use and not for general publication or disclosure to

third parties.

No part of this research service may be given, lent, resold or disclosed to non-customers without written

permission.

Furthermore, no part may be reproduced, stored in a retrieval system or transmitted in any form or by any

means, electronic, mechanical, photocopying, recording or otherwise, without the permission of the publisher.

For information regarding permission, write:

Frost & Sullivan

4 Grosvenor Gardens

Sullivan House

London SW1W 0DH

United Kingdom

3M6DB-18

Certificate

We hereby certify that the views expressed in this research service accurately reflect our views based

on primary and secondary research with industry participants, industry experts, end users, regulatory

organisations, financial and investment community and other related sources.

In addition to the above, our robust in-house forecast and benchmarking models along with the Frost

& Sullivan Decision Support Databases have been instrumental in the completion and publishing of

this research service.

We also certify that no part of our analyst compensation was, is or will be, directly or indirectly, related

to the specific recommendations or view expressed in this research service.

4M64A-18

45

46

Emission Norms and Regulations

Rail Contribution to NOX and Particulate Matter Emissions

CO2 Emissions as per mode of transport

3

37

38

39

40

41

42

43

Introduction to European Diesel Locomotive and Railcar

Overview of European Rail Traffic

Segmentation of Diesel Locomotives and Railcars

Present Infrastructure

Passenger Demand

Utilization of Rail Infrastructure

Investment in Rail Infrastructure

Investment Patterns in Transport Infrastructure

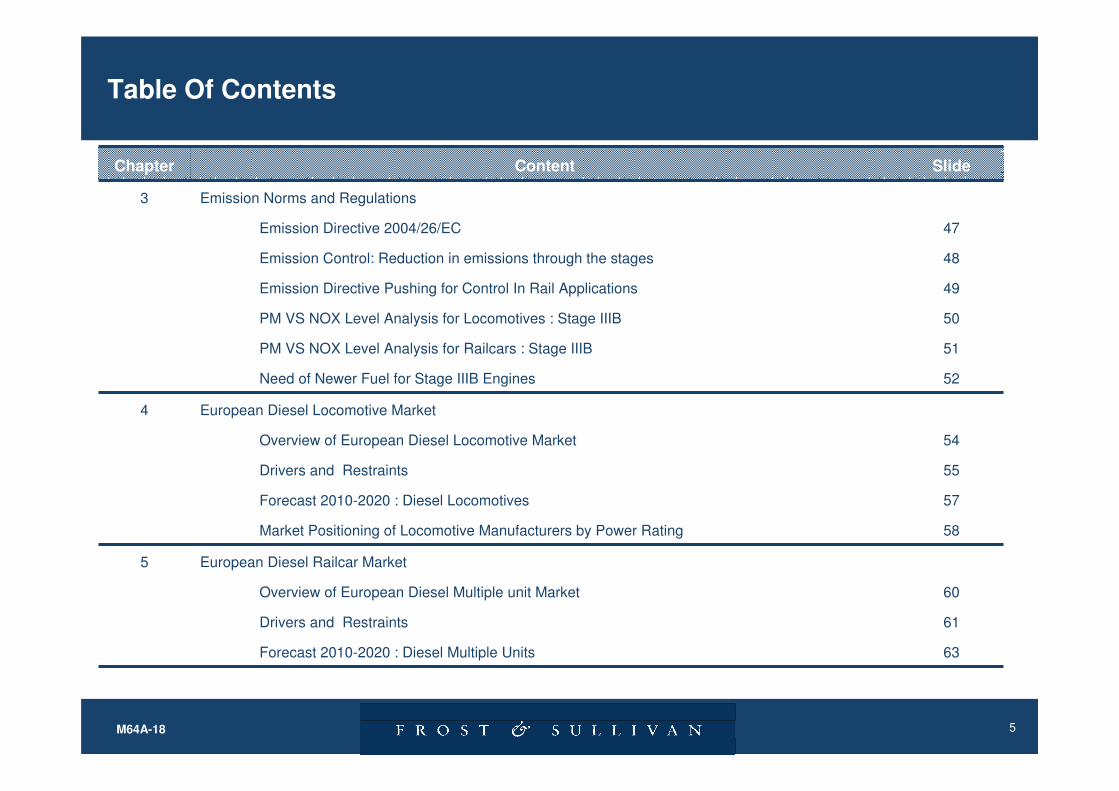

2

SlideContentChapter

27Executive Summary1

19

20

22

25

Geographic Definitions and Research Timeline

Definitions

List of Units, Abbreviations and Acronyms

List of Industry participants

Table Of Contents

5M64A-18

47

48

49

50

51

52

Emission Norms and Regulations

Emission Directive 2004/26/EC

Emission Control: Reduction in emissions through the stages

Emission Directive Pushing for Control In Rail Applications

PM VS NOX Level Analysis for Locomotives : Stage IIIB

PM VS NOX Level Analysis for Railcars : Stage IIIB

Need of Newer Fuel for Stage IIIB Engines

3

60

61

63

European Diesel Railcar Market

Overview of European Diesel Multiple unit Market

Drivers and Restraints

Forecast 2010-2020 : Diesel Multiple Units

5

SlideContentChapter

54

55

57

58

European Diesel Locomotive Market

Overview of European Diesel Locomotive Market

Drivers and Restraints

Forecast 2010-2020 : Diesel Locomotives

Market Positioning of Locomotive Manufacturers by Power Rating

4

Table Of Contents

6M64A-18

80

81

82

83

84

Boosting Technologies

Introduction to Boosting

Variable Geometry Turbochargers

Product Attractiveness and Penetration: Variable Geometry Turbochargers

Forecast 2010-2020 : Variable Geometry Turbochargers in Diesel Locomotives

Forecast 2010-2020 : Variable Geometry Turbochargers in Diesel Multiple Units

8

64

European Diesel Railcar Market

Market Positioning of Locomotive Manufacturers by Power Rating

5

65Diesel Locomotive and Railcar Market Challenges6

SlideContentChapter

74

75

76

77

78

Modern Direct Injection Technologies

Introduction to Injection Technologies

Impact of Common Rail on Emissions

Product Attractiveness and Penetration: Common Rail

Forecast 2010-2020 : Modern Injection Technologies in Diesel Locomotives

Forecast 2010-2020 : Modern Injection Technologies in Diesel Multiple Units

7

Table Of Contents

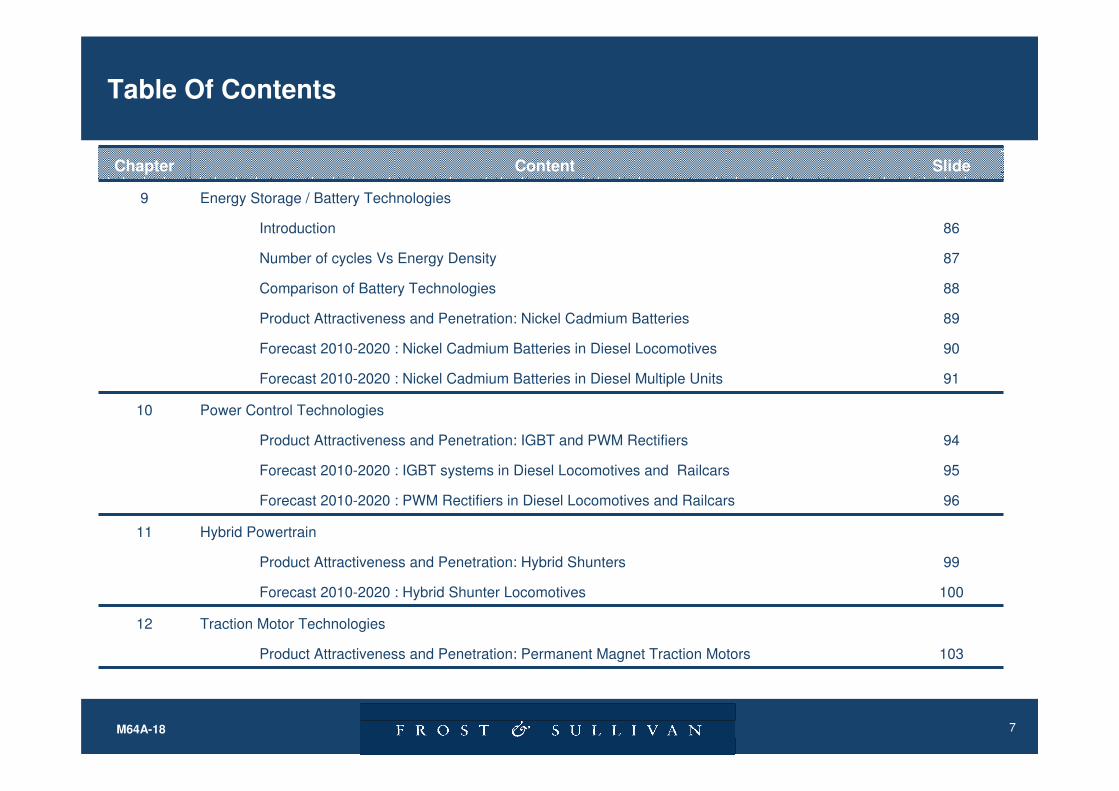

7M64A-18

86

87

88

89

90

91

Energy Storage / Battery Technologies

Introduction

Number of cycles Vs Energy Density

Comparison of Battery Technologies

Product Attractiveness and Penetration: Nickel Cadmium Batteries

Forecast 2010-2020 : Nickel Cadmium Batteries in Diesel Locomotives

Forecast 2010-2020 : Nickel Cadmium Batteries in Diesel Multiple Units

9

94

95

96

Power Control Technologies

Product Attractiveness and Penetration: IGBT and PWM Rectifiers

Forecast 2010-2020 : IGBT systems in Diesel Locomotives and Railcars

Forecast 2010-2020 : PWM Rectifiers in Diesel Locomotives and Railcars

10

103

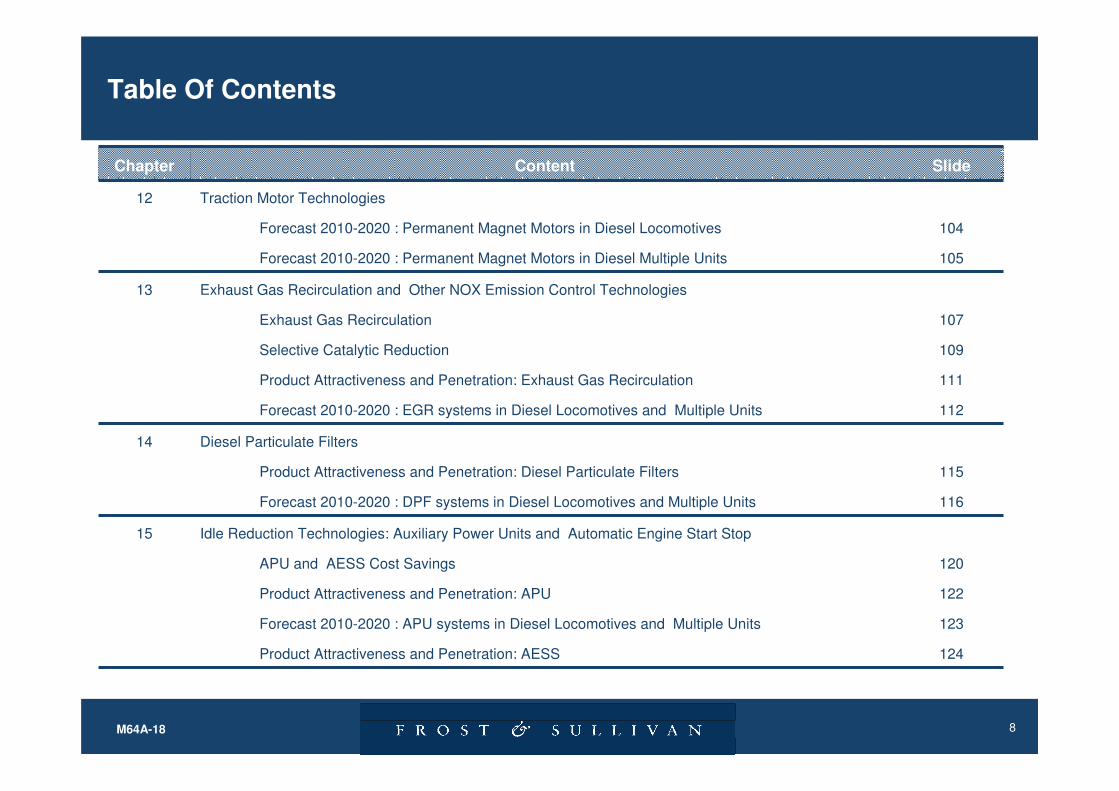

Traction Motor Technologies

Product Attractiveness and Penetration: Permanent Magnet Traction Motors

12

99

100

Hybrid Powertrain

Product Attractiveness and Penetration: Hybrid Shunters

Forecast 2010-2020 : Hybrid Shunter Locomotives

11

SlideContentChapter

Table Of Contents

8M64A-18

104

105

Traction Motor Technologies

Forecast 2010-2020 : Permanent Magnet Motors in Diesel Locomotives

Forecast 2010-2020 : Permanent Magnet Motors in Diesel Multiple Units

12

107

109

111

112

Exhaust Gas Recirculation and Other NOX Emission Control Technologies

Exhaust Gas Recirculation

Selective Catalytic Reduction

Product Attractiveness and Penetration: Exhaust Gas Recirculation

Forecast 2010-2020 : EGR systems in Diesel Locomotives and Multiple Units

13

120

122

123

124

Idle Reduction Technologies: Auxiliary Power Units and Automatic Engine Start Stop

APU and AESS Cost Savings

Product Attractiveness and Penetration: APU

Forecast 2010-2020 : APU systems in Diesel Locomotives and Multiple Units

Product Attractiveness and Penetration: AESS

15

115

116

Diesel Particulate Filters

Product Attractiveness and Penetration: Diesel Particulate Filters

Forecast 2010-2020 : DPF systems in Diesel Locomotives and Multiple Units

14

SlideContentChapter

Table Of Contents

9M64A-18

132About Frost & Sullivan17

125

Idle Reduction Technologies: Auxiliary Power Units and Automatic Engine Start Stop

Forecast 2010-2020 : AESS systems in Diesel Locomotives and Multiple Units

15

127

130

Conclusion and Recommendations

Snapshot and Overview of Forecasts

Key Trends, Observations and Strategic Recommendations

16

SlideContentChapter

Table Of Contents

10M64A-18

107Diesel Powertrain Market : After Exhaust NOX Reduction (Europe), 201013

120Diesel Powertrain Market: Cost Analysis with Break Even Time For APU & AESS Systems (Europe), 201015

114Diesel Powertrain Market: Effectiveness of the Diesel Oxidation Catalyst in Removing Emissions (Europe), 2010-202014

88Diesel Powertrain Market : Benchmarking of Key Battery Technologies (Europe), 20109

63Railcar Market: Diesel Multiple Unit Forecast (Europe), 2010 5

57Locomotive Market: Diesel Locomotive Forecast (Europe), 2010-20204

47

47

50

51

52

Locomotive & Railcar Market: Emission Standards for Engines 130KW ≤ Power ≤ 560KW in g/kWh (Europe), 2010

Locomotive & Railcar Market: Emission Standards for Engines of Locomotives & Railcars in g/kWh (Europe), 2010

Locomotive & Railcar Market: PM Vs NOX for Stage III B Locomotives (Europe) 2010

Locomotive & Railcar Market: PM Vs NOX for Stage IIIB Railcars (Europe) 2010

Locomotive & Railcar Market: Stage IIIB Fuel Specifications (Europe) 2010

3

SlideContentChapter

38Rail Market: Segmentation & Number of Diesel Locomotives & Railcars by Engine Size (Europe), 2010 2

29Locomotive & Railcar Market: Number of Diesel Locomotives & Railcars Nearing Retirement Age (Europe), 20101

List of Figures

11M64A-18

37

38

39

40

41

42

43

Rail Market : Passenger and Freight Traffic (Europe), 2010

Rail Market: Segmentation of Diesel Locomotives & Railcars by Application (Europe), 2010

Rail Market: Total Length of Railway Network & Electrification (Europe), 2010

Rail Market: Passenger Demand for Rail (Europe), 2010

Rail Market: Utilization of Rail Infrastructure for Freight Transport (Europe), 2010

Rail Market: Investment in transport infrastructure (Europe), 2010

Rail Market: Investment in Transportation Infrastructure in Billion Euros (Europe), 2000-2008

2

SlideContentChapter

27

27

28

29

30

31

32

33

33

34

35

Locomotive Market & Railcar : Regional Split of Diesel Locomotives in Key Countries (Europe), 2010

Locomotive Market & Railcar : Regional Split of Diesel Multiple Units in Key Countries (Europe), 2010

Locomotive & Railcar Market: Overview of fleet installed in key countries (Europe), 2010

Locomotive & Railcar Market: Number of Diesel Locomotives & Railcars Nearing Retirement Age (Europe), 2010

Locomotive & Railcar Market: Total Diesel Locomotive Requirement (Europe), 2010-2020

Locomotive & Railcar Market: Total Diesel Railcar Requirement (Europe), 2010-2020

Locomotive & Railcar Market: Technology Roadmap (Europe), 2010-2020

Locomotive & Railcar Market : Penetration of APU Systems in Diesel Locomotives & Railcars (Europe), 2010-2020

Locomotive & Railcar Market : Comparison of Key Battery Technologies (Europe), 2010

Locomotive & Railcar Market : Technology Impact Vs Implementation (Europe), 2010-2020

Locomotive & Railcar Market : Key Findings (Europe), 2010

1

List of Charts

12M64A-18

60

60

61

62

63

64

Railcar Market: Regional Split of Diesel Multiple Units in Key Countries (Europe), 2010

Railcar Market: Overview of Diesel Multiple Unit Fleets Installed (Europe), 2010

Railcar Market : Key Market Drivers (Europe), 2010-2020

Railcar : Key Market Restraints (Europe), 2010-2020

Railcar Market: Diesel Multiple Unit Forecast (Europe), 2010

Railcar Market: Market Positioning of Railcar Manufacturers by Power Rating (Europe), 2010

5

54

54

55

56

57

58

Locomotive Market: Regional Split of Diesel Locomotives in Key Countries (Europe), 2010

Locomotive Market: Overview of Diesel Locomotive Fleets Installed (Europe), 2010

Locomotive Market : Key Market Drivers (Europe), 2010-2020

Locomotive Market : Key Market Restraints (Europe), 2010-2020

Locomotive Market: Diesel Locomotive Forecast (Europe), 2010-2020

Locomotive Market: Market Positioning of Locomotive Manufacturers by Power Rating (Europe), 2010

4

45

46

48

49

50

51

Locomotive & Railcar Market : Oxides of Nitrogen, Sulfur and Particulate Matter Emission by Sector (Europe), 2010

Locomotive & Railcar Market: Specific CO2 emissions per tonne-km and per mode of transport, (Europe) 1995 - 2009

Locomotive & Railcar Market: Reduction in Emissions for Engines 130KW ≤ Power ≤ 560KW in g/kWh(Europe),2010

Locomotive & Railcar Market: Emissions for Engines in Rail Application - Stage IIIA & IIIB (Europe), 2010

Locomotive & Railcar Market: PM Vs NOX for Stage III B Locomotives (Europe) 2010

Locomotive & Railcar Market: PM Vs NOX for Stage IIIB Railcars (Europe) 2010

3

SlideContentChapter

List of Charts

13M64A-18

77Diesel Powertrain Market: Forecast of Common Rail, Electronic Injectors & Engine management Systems in Diesel

Locomotives (Europe), 2010-2020

76Diesel Powertrain Market : Penetration of Common Rail, Electronic Injectors & Engine management Systems in

Diesel Locomotives (Europe), 2010-2020

74Diesel Powertrain Market : Drivers & Restraints for New Engine Technologies (Europe), 2010-2020

75Diesel Powertrain Market : Impact of Common Rail, Electronic Injectors & Engine Management Systems on NOX &

PM Emissions for Diesel Locomotives & Railcars (Europe), 2010-2020

76Diesel Powertrain Market :Product Attractiveness of Common Rail, Electronic Injectors & Engine management

Systems (Europe), 2010-2020

74Diesel Powertrain Market : Key Engine Technologies (Europe), 2010-20207

66

67

68

69

70

71

72

72

Locomotive & Railcar Market : Identification of Market Challenges (Europe), 2010

Locomotive & Railcar Market : Identifying Market Size (Europe), 2010

Locomotive & Railcar Market : Challenge Faced by Electrification (Europe), 2010

Locomotive & Railcar Market : Challenge of implementing New Technologies (Europe), 2010

Locomotive & Railcar Market : Challenge of Meeting Emission Norms (Europe), 2010

Locomotive & Railcar Market: OPEC Basket Prices of Diesel (Europe), 2010

Locomotive & Railcar Market: Country wise Comparison of Diesel Prices (Europe), 2010

Locomotive & Railcar Market: Diesel Consumption by Industry (Europe), 2010

6

SlideContentChapter

List of Charts

14M64A-18

89Diesel Powertrain Market : Penetration of Nickel Cadmium Battery Systems in Diesel Locomotives & Railcars

(Europe), 2010-2020

82Diesel Powertrain Market : Penetration of Variable Geometry Turbochargers in Diesel Locomotives & Railcars

(Europe), 2010-2020

83

84

Diesel Powertrain Market: Forecast of Variable Geometry Turbochargers in Diesel Locomotives (Europe), 2010-2020

Diesel Powertrain Market: Forecast of Variable Geometry Turbochargers in Diesel Multiple Units (Europe), 2010-2020

78Diesel Powertrain Market: Forecast of Common Rail, Electronic Injectors & Engine management Systems in Diesel

Multiple Units (Europe), 2010-2020

7

86

86

87

88

89

Diesel Powertrain Market: Drivers & Restraints for Implementing New Batteries (Europe), 2010

Diesel Powertrain Market : Key Battery Technologies (Europe), 2010-2020

Diesel Powertrain Market : Comparison of Key Battery Technologies (Europe), 2010

Diesel Powertrain Market : Benchmarking of Key Battery Technologies (Europe), 2010

Diesel Powertrain Market :Product Attractiveness of Nickel Cadmium Battery Systems (Europe), 2010-2020

9

80

81

81

82

82

Diesel Powertrain Market : Key Boosting Technologies (Europe), 2010-2020

Diesel Powertrain Market: Advantages of Variable Geometry Turbochargers (Europe), 2010

Diesel Powertrain Market: Drivers for Implementing Turbochargers (Europe), 2010

Diesel Powertrain Market: Variable Geometry Turbocharger (Europe), 2010

Diesel Powertrain Market :Product Attractiveness of Variable Geometry Turbochargers (Europe), 2010-2020

8

SlideContentChapter

List of Charts

15M64A-18

95

95

96

96

Diesel Powertrain Market: Forecast of IGBT Systems in Diesel Locomotives (Europe), 2010-2020

Diesel Powertrain Market: Forecast of IGBT Systems in Diesel Multiple Units (Europe), 2010-2020

Diesel Powertrain Market: Forecast of PWM Rectifier Systems in Diesel Multiple Units (Europe), 2010-2020

Diesel Powertrain Market: Forecast of PWM Rectifier Systems in Diesel Multiple Units (Europe), 2010-2020

94Diesel Powertrain Market : Penetration of IGBT & PWM Rectifier Systems in Diesel Locomotives & Railcars (Europe),

2010-2020

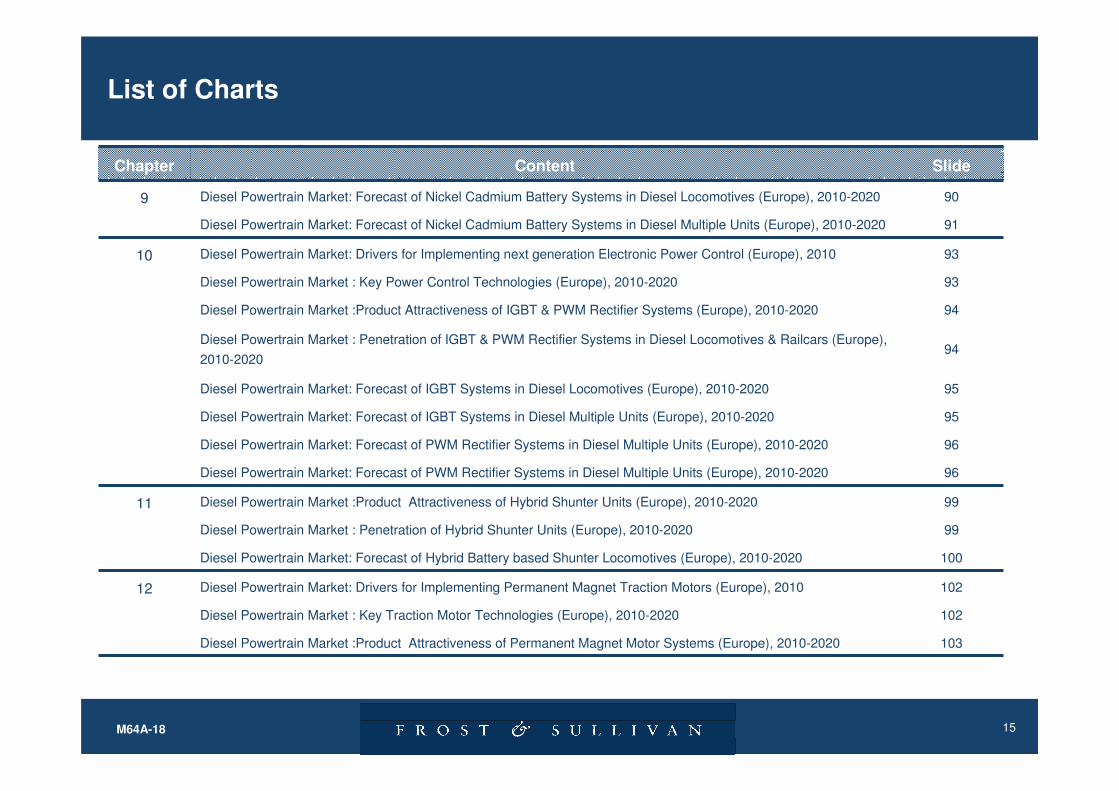

90

91

Diesel Powertrain Market: Forecast of Nickel Cadmium Battery Systems in Diesel Locomotives (Europe), 2010-2020

Diesel Powertrain Market: Forecast of Nickel Cadmium Battery Systems in Diesel Multiple Units (Europe), 2010-2020

9

102

102

103

Diesel Powertrain Market: Drivers for Implementing Permanent Magnet Traction Motors (Europe), 2010

Diesel Powertrain Market : Key Traction Motor Technologies (Europe), 2010-2020

Diesel Powertrain Market :Product Attractiveness of Permanent Magnet Motor Systems (Europe), 2010-2020

12

99

99

100

Diesel Powertrain Market :Product Attractiveness of Hybrid Shunter Units (Europe), 2010-2020

Diesel Powertrain Market : Penetration of Hybrid Shunter Units (Europe), 2010-2020

Diesel Powertrain Market: Forecast of Hybrid Battery based Shunter Locomotives (Europe), 2010-2020

11

93

93

94

Diesel Powertrain Market: Drivers for Implementing next generation Electronic Power Control (Europe), 2010

Diesel Powertrain Market : Key Power Control Technologies (Europe), 2010-2020

Diesel Powertrain Market :Product Attractiveness of IGBT & PWM Rectifier Systems (Europe), 2010-2020

10

SlideContentChapter

List of Charts

16M64A-18

115Diesel Powertrain Market :Product Attractiveness of Diesel Particulate Filters (Europe), 2010-202014

112Diesel Powertrain Market: Forecast of Exhaust Gas Recirculation Systems in Diesel Multiple Units (Europe), 2010-

2020

112Diesel Powertrain Market: Forecast of Exhaust Gas Recirculation Systems in Diesel Locomotives (Europe), 2010-

2020

111Diesel Powertrain Market : Penetration of Exhaust Gas Recirculation Systems in Diesel Locomotives & Railcars

(Europe), 2010-2020

104Diesel Powertrain Market: Forecast of Permanent Magnet Motor Systems in Diesel Locomotives (Europe), 2010-2020

103Diesel Powertrain Market : Penetration of Permanent Magnet Motor Systems in Diesel Locomotives & Railcars

(Europe), 2010-2020

12

115Diesel Powertrain Market : Penetration of Diesel Particulate Filters in Diesel Locomotives & Railcars (Europe), 2010-

2020

109

109

110

111

Diesel Powertrain Market : Selective Catalytic Reduction (Europe), 2010-2020

Diesel Powertrain Market : Advantages and Disadvantages of Selective Catalytic Reduction (Europe), 2010-2020

Diesel Powertrain Market : Exhaust Gas Recirculation Mechanism of action (Europe), 2010-2020

Diesel Powertrain Market :Product Attractiveness of Exhaust Gas Recirculation Systems (Europe), 2010-2020

13

105Diesel Powertrain Market: Forecast of Permanent Magnet Motor Systems in Diesel Multiple Units (Europe), 2010-

2020

SlideContentChapter

List of Charts

17M64A-18

124Diesel Powertrain Market : Penetration of Automatic Engine Start Stop Systems in Diesel Locomotives & Railcars

(Europe), 2010-2020

123

123

124

Diesel Powertrain Market: Forecast of Auxiliary Power Units in Diesel Locomotives (Europe), 2010-2020

Diesel Powertrain Market: Forecast of Auxiliary Power Units in Diesel Multiple Units (Europe), 2010-2020

Diesel Powertrain Market :Product Attractiveness of Automatic Engine Start Stop Systems (Europe), 2010-2020

122Diesel Powertrain Market : Penetration of Auxiliary Power Units in Diesel Locomotives & Railcars (Europe), 2010-

2020

118

119

119

120

121

122

Diesel Powertrain Market: Calculation of Fuel savings by Auxiliary Power Units (Europe), 2010

Diesel Powertrain Market: Drivers for Implementing APU / AESS Systems (Europe), 2010

Diesel Powertrain Market : Key Engine Idle Reduction Technologies (Europe), 2010-2020

Diesel Powertrain Market: Cost Analysis with Break Even Time For APU & AESS Systems (Europe), 2010

Diesel Powertrain Market: Comparison Between APU, AESS & Hybrid Locomotives (Europe), 2010

Diesel Powertrain Market :Product Attractiveness of Auxiliary Power Units (Europe), 2010-2020

15

116

116

Diesel Powertrain Market: Forecast of Diesel Particulate Filters in Diesel Locomotives (Europe), 2010-2020

Diesel Powertrain Market: Forecast of Diesel Particulate Filters in Diesel Multiple Units (Europe), 2010-2020

14

127Diesel Powertrain Market : Snapshot of Diesel Locomotives & Multiple Units (Sales) Forecast (Europe), 2010 – 202016

125Diesel Powertrain Market: Forecast of Automatic Engine Start Stop Systems in Diesel Locomotives (Europe), 2010-

2020

SlideContentChapter

List of Charts

18M64A-18

128

129

130

131

Diesel Powertrain Market: Forecast of Alternate Powertrain Technologies in Diesel Locomotives (Europe), 2010-2020

Diesel Powertrain Market: Forecast of Alternate Powertrain Technologies in Diesel Multiple Units (Europe),2010-2020

Diesel Powertrain Market: Trends and Performance Indicators (Europe),2010-2020

Diesel Powertrain Market: Recommendations for Locomotive & Railcar Manufacturers (Europe),2010-2020

16

SlideContentChapter

List of Charts

19M6DB-18

���� Objectives of the studyThis study aims to identify and analyze:

•Diesel Locomotive & Railcar Market in key European States•Country Focus: France, Germany, Italy, Spain and United

Kingdom•Segment the Locomotives Market and identify the Market Size

•Forecast Locomotive requirements by different segment

•Analyze emission regulations•Provide an in-depth insight into powertrain technologies used

and considered for future emission compliance•Identify complimentary technologies that help reduce emissions

and save fuel and benchmark their potentials

•Provide key finding and recommendation for the various participants in the supply chain.

Short TermShort Term Medium TermMedium Term Long TermLong Term

2010 2011 2012 2013 2014 2015 2016 2020

ForecastPeriod

ForecastPeriod

Time

Line

Time

Line

Geographic RegionsGeographic Regions

Base Year

Base Year

Geographic Definitions and Research Timeline

2017 2018 20192018

Study and analysis is focused in France, Germany, Italy, Spain and United Kingdom

20M6DB-18

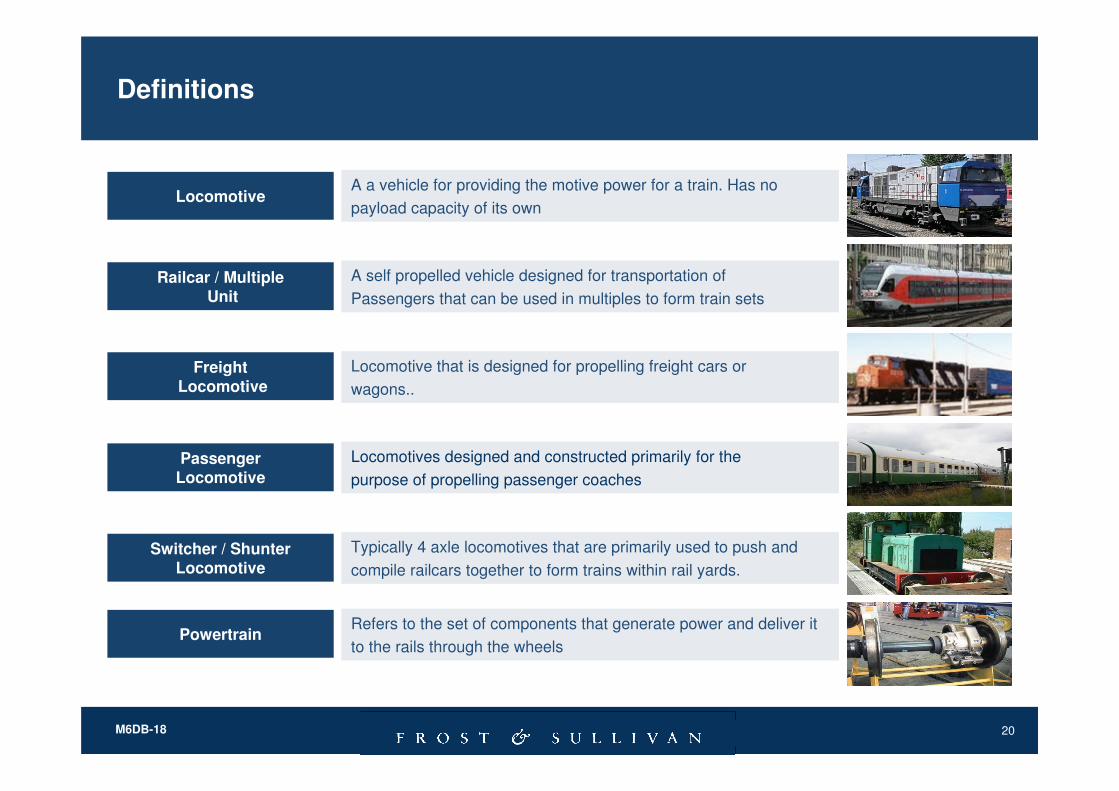

Definitions

Locomotive that is designed for propelling freight cars or

wagons..

Locomotives designed and constructed primarily for the

purpose of propelling passenger coaches

Freight

Locomotive

Passenger

Locomotive

A a vehicle for providing the motive power for a train. Has no

payload capacity of its ownLocomotive

A self propelled vehicle designed for transportation of

Passengers that can be used in multiples to form train sets

Railcar / Multiple

Unit

Typically 4 axle locomotives that are primarily used to push and

compile railcars together to form trains within rail yards.

Switcher / Shunter

Locomotive

Refers to the set of components that generate power and deliver it

to the rails through the wheelsPowertrain

21M6DB-18

Definitions

Supplies electric energy to locomotives and multiple units so that they can operate without the need of an engine

Electrification

22M6DB-18

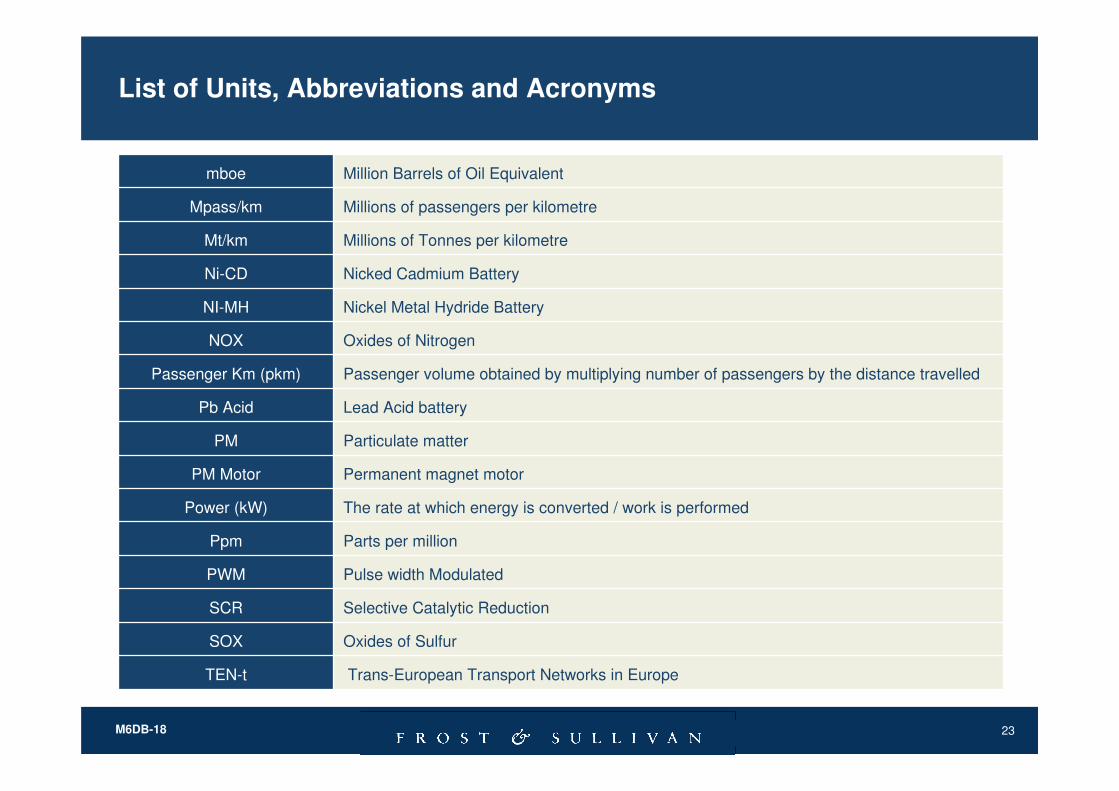

List of Units, Abbreviations and Acronyms

Lithium Ion BatteryLi-ion

Insulated Gate Bipolar TransistorIGBT

Heating, Ventilating and Air conditioningHVAC

HydrocarbonsHC

The amount of pollutant exhausted in grams per kilowatt per hour by the engineG/kWh

Fixed Geometry TurbochargerFGT

European UnionEU

European Rail Traffic Management systemERTMS

Electric Multiple UnitEMU

Exhaust Gas RecirculationEGR

Diesel Particulate FiltersDPF

Diesel Multiple UnitDMU

Carbon monoxideCO

Compound annual growth rateCAGR

Auxiliary power unitAPU

23M6DB-18

List of Units, Abbreviations and Acronyms

Lead Acid batteryPb Acid

Trans-European Transport Networks in EuropeTEN-t

Oxides of SulfurSOX

Selective Catalytic ReductionSCR

Pulse width ModulatedPWM

Parts per millionPpm

The rate at which energy is converted / work is performedPower (kW)

Permanent magnet motorPM Motor

Particulate matterPM

Passenger volume obtained by multiplying number of passengers by the distance travelledPassenger Km (pkm)

Oxides of NitrogenNOX

Nickel Metal Hydride BatteryNI-MH

Nicked Cadmium BatteryNi-CD

Millions of Tonnes per kilometreMt/km

Millions of passengers per kilometreMpass/km

Million Barrels of Oil Equivalentmboe

24M6DB-18

List of Units, Abbreviations and Acronyms

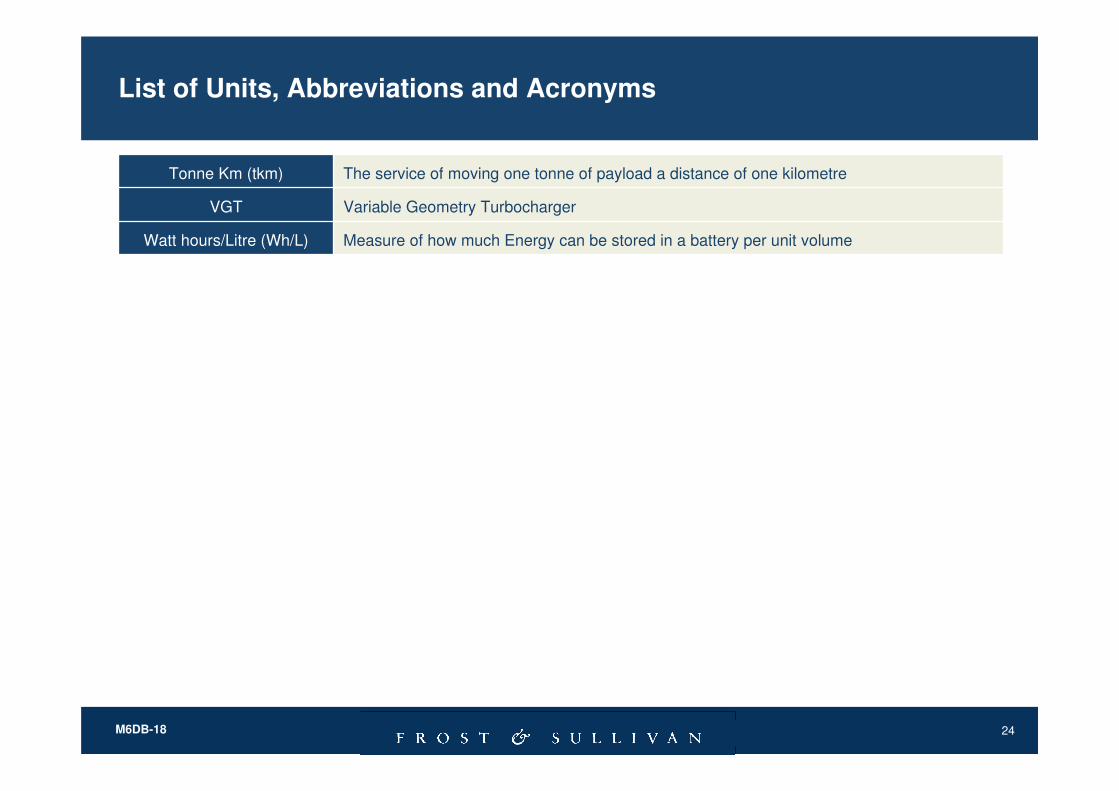

The service of moving one tonne of payload a distance of one kilometreTonne Km (tkm)

Variable Geometry TurbochargerVGT

Measure of how much Energy can be stored in a battery per unit volumeWatt hours/Litre (Wh/L)

25

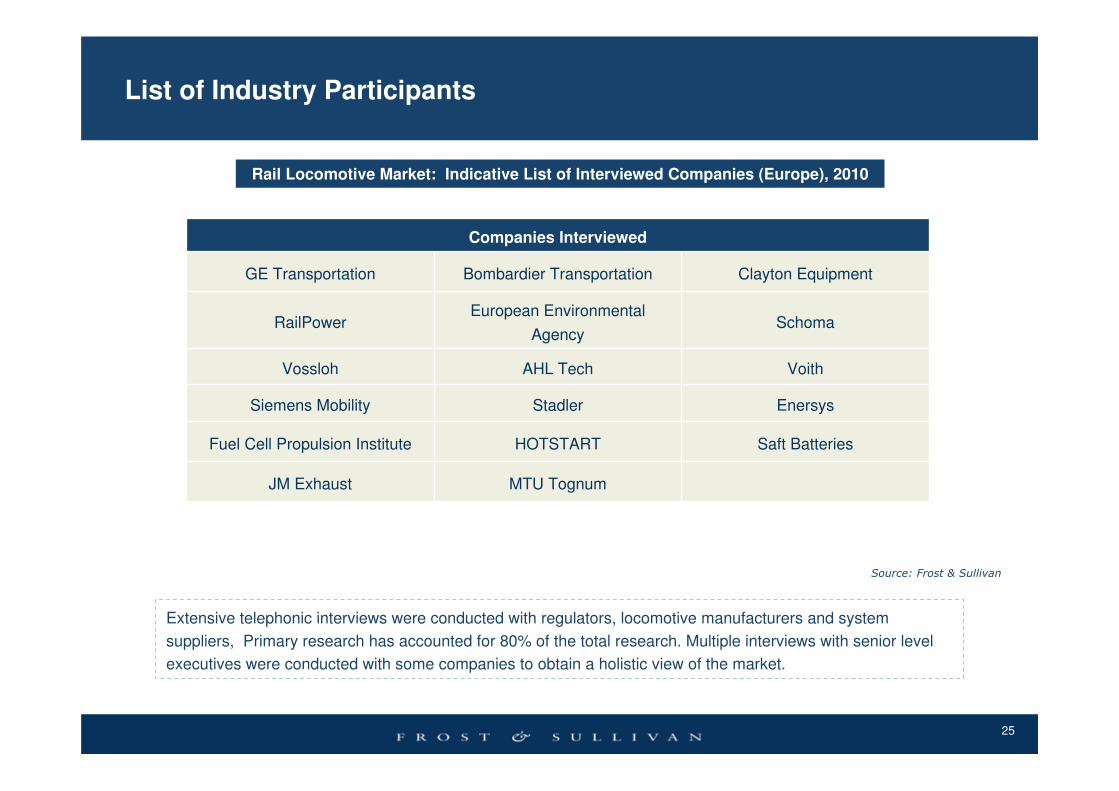

Extensive telephonic interviews were conducted with regulators, locomotive manufacturers and system

suppliers, Primary research has accounted for 80% of the total research. Multiple interviews with senior level

executives were conducted with some companies to obtain a holistic view of the market.

List of Industry Participants

Source: Frost & Sullivan

Rail Locomotive Market: Indicative List of Interviewed Companies (Europe), 2010

Saft Batteries

Enersys

Voith

Schoma

Clayton Equipment

HOTSTARTFuel Cell Propulsion Institute

AHL TechVossloh

StadlerSiemens Mobility

MTU TognumJM Exhaust

Companies Interviewed

European Environmental

AgencyRailPower

Bombardier TransportationGE Transportation

26

Chapter 1: Executive Summary

2727

UK

18%

Germany

41%

France

14%

Spain

8%

Italy

19%UK

Germany

Spain

Italy

France

Overview of European Rail Market: Snapshot of Diesel Locomotive and

Railcar Fleets

4%

Locomotive Market & Railcar : Regional Split of Diesel Multiple Units in Key Countries (Europe), 2010

UK

8%

Germany

31%

France

34%

Spain

8%

Italy

19%

UK

Germany

Spain

Italy

France

Locomotive Market & Railcar : Regional Split of Diesel Locomotives in Key Countries (Europe), 2010

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan

UK, France, Italy

set to become big

markets

Total Volume:

9172 Locomotives

Total Volume:

6149 DMUs

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan

• Germany and France are the biggest diesel

locomotive markets. Together they have a combined share of 65% with 6198 locomotives

• UK has the smallest locomotive fleet, but it is expected to have the highest freight traffic growth rate.

• Aging fleet and increased traffic to boost locomotive sales with a CAGR of 4.13%

• Germany is the largest markets for diesel railcars and

will continue to be the biggest consumer for new railcars through to 2020.

• Dual mode railcars are set to become a major trend as the percentage of electrified lines is steadily increasing

across countries.

2828

Total

Diesel Locomotives

Diesel Multiple Units

Defining the Universe: France and Germany together constitute 61% of

the overall diesel locomotive and railcar market

8751

3280

831

France

3216

553 355

Spain

4574

969 1150

United Kingdom

6554

1765

1264

Italy

25772918

Germany

13613

Europe(Estimate)

103051

2571717568

Locomotive & Railcar Market: Overview of fleet installed in key countries (Europe), 2010

United Kingdom has a mandate pushing

for more electrification which is expected

to result in shift of numbers from diesel to

electric locomotives by 2020

Higher

electrification

levels on

passenger

routes has

dampened

DMU

presence

Germany is the biggest market

for diesel locomotives with Power

> 2000 kW

Despite high

electrification levels,

DMUs are still used to

service low traffic

routes

For immediate

interoperability

purposes Spain is

expected to procure

more diesel

locomotives by

2020.

Note: All figures are rounded; the base year is 2010. Source:

Frost & SullivanTotal= Diesel + Electric units (locomotives & railcars)

2929

Locomotive fleet Age Analysis: 10298 Locomotives & 1860 Railcars likely

to be replaced starting 2015

24%6%

6%

2327

5501

1548

424 498202 289930

160 279

0

2000

4000

6000

France Germany Italy Spain United Kingdom

Num

ber

of

Units

Locmotives (Age >30) Railcars (Age >25)

Locomotive & Railcar Market: Number of Diesel Locomotives & Railcars Nearing Retirement Age (Europe), 2010

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan

129

220

2061

810

2200

Power

Rating

(kW)

43748Y7400SNCF

37434Y 8000SNCFFrance

39840218DB Regio

40847290DB

Schenker

70938232DB

SchenkerGermany

Number

of Units

Average

AgeClassOperatorCountry

• France and Germany will be the biggest and first

market to pursue replacements

Key identified operators with massive locomotive

replacement potential

• The Average age of all diesel locomotive fleets in

countries listed below is 36.69 years.

• The Average age of all diesel railcar fleets in

countries listed below is 26.93 years.

3030

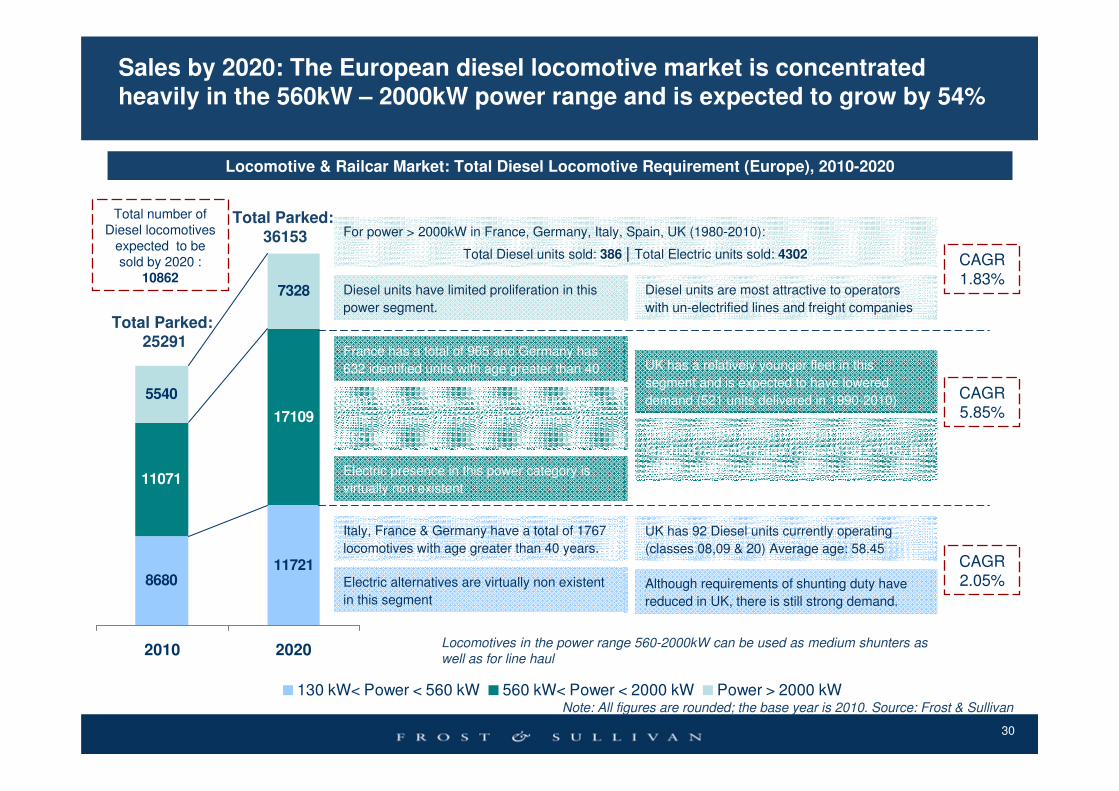

130 kW< Power < 560 kW 560 kW< Power < 2000 kW Power > 2000 kW

868011721

11071

17109

5540

7328

2010 2020

Locomotive & Railcar Market: Total Diesel Locomotive Requirement (Europe), 2010-2020

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan

Sales by 2020: The European diesel locomotive market is concentrated

heavily in the 560kW – 2000kW power range and is expected to grow by 54%

Total Parked:25291

Total Parked:

36153

Total number of Diesel locomotives

expected to be sold by 2020 :

10862

France has a total of 965 and Germany has

632 identified units with age greater than 40

Italy, France & Germany have a total of 1767

locomotives with age greater than 40 years.

Electric alternatives are virtually non existent

in this segment

UK has 92 Diesel units currently operating

(classes 08,09 & 20) Average age: 58.45

CAGR

1.83%

Although requirements of shunting duty have

reduced in UK, there is still strong demand.

CAGR 2.05%

CAGR

5.85%2000-2010 saw massive orders in UK for 221

units, in France for 315 and in Germany for

265 units.

UK has a relatively younger fleet in this

segment and is expected to have lowered

demand (521 units delivered in 1990-2010)

France has 498 diesel units that have are

reaching retirement age ( classes BB 67400, BB

66000, BB 67200 and BB 69200 )Electric presence in this power category is

virtually non existent

For power > 2000kW in France, Germany, Italy, Spain, UK (1980-2010):

Total Diesel units sold: 386 | Total Electric units sold: 4302

Diesel units have limited proliferation in this

power segment.

Diesel units are most attractive to operators

with un-electrified lines and freight companies

Locomotives in the power range 560-2000kW can be used as medium shunters as well as for line haul

3131

130 kW< Power < 560 kW 560 kW< Power < 2000 kW Power > 2000 kW

11917

17329

5440

9306

149

185

2010 2020

Locomotive & Railcar Market: Total Diesel Railcar Requirement (Europe), 2010-2020

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan

Sales by 2020: The European diesel railcar market is concentrated heavily in

the 130kW – 560kW power range and is expected to grow by 45%

Total Parked:

17506

Total Parked:

26820Total number of

DMUs expected to be sold by 2020 :

9314

Germany & UK have had a combined delivery

of 1719 DMUs in 1990-2010

This segment is largest market for the DMUs

Factors with biggest impact:

•Lower cost of utilizing infrastructure

•Ease of adaptability to demand

•Funding aid for municipalities from government

for the move towards mass transportation

CAGR

7.65%

CAGR

9.73%

This is the fastest growing DMU segment.

Power 130 -2000 kW : By 2020, 717 units are

expected to reach retirement age

Factors with biggest impact:

•Increased connectivity

•Passenger volumes

•Increased government interest

Diesel Multiple Units are virtually non

existent in this category

For this category in France, Germany, Italy, Spain, UK (1980-2010):

Total DMUs sold: 1823 | Total EMUs: 4805

For this category in France, Germany, Italy, Spain, UK (1980-2010):

Total DMUs sold: 3168 | Total EMUs: 780

Italy, Germany & Spain took deliveries of 1553

EMUs in 2000-2010

As railcars have power generated from multiple sources, the power range 130-560kW is more attractive for light to medium density passenger loads

32M6DB-18

European Locomotive & Railcar Technology Roadmap 2010-2025: Powertrain

Downsizing, Transmission Automation and Digitized Controls Emerging as the Key

R&D Focal Points

2005 2010 2015 2020 2025

Regenerative BrakingDynamic Braking

Lead Acid Batteries

Idle Reduction

Energy recovery

Energy Storage

Lo

co

mo

tiv

e

Syste

ms

Lo

co

mo

tiv

e

En

gin

es

Alt

ern

ate

Fu

els

Automatic Start Stop Systems Auxiliary Power Systems

Ultra capacitors

Exhaust Gas Utilization

Electronic Power Control

Fuel Injection & Advanced Combustion

Intercoolers & Turbochargers Advanced Variable Geometry Turbochargers

Exhaust After Treatment

PWM RectifiersAdaptive Control

Common Rail Direct Ignition

Variable Valve TimingHomogeneous Charge Compression Ignition

Exhaust Gas Recirculation

Diesel Oxidation Catalyst + Diesel Particulate FiltersSelective Catalytic Reduction

Hydrogen Fuel Cell

Hybrid Locomotive

Hydrogen Fuel Cell Hybrid

Lead acid battery Mild Hybrid Locomotive

Lithium Ion / Nickel Cadmium

Full Hybrid – Li-ion Battery electric locomotive

Traction Motors AC Induction AC Permanent Magnet

IGBT Control

. S

ou

rce

: F

rost &

Su

llivan

Locomotive & Railcar Market: Technology Roadmap (Europe), 2010-2020

3333

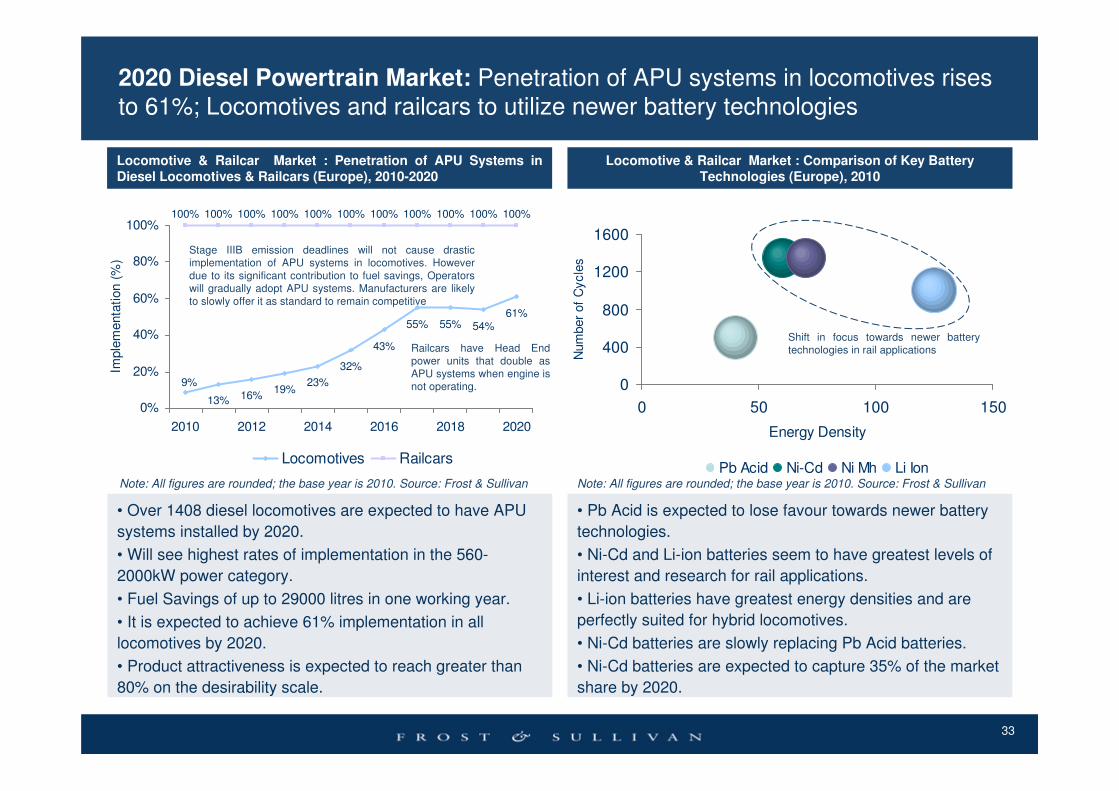

2020 Diesel Powertrain Market: Penetration of APU systems in locomotives rises

to 61%; Locomotives and railcars to utilize newer battery technologies

Locomotive & Railcar Market : Comparison of Key Battery Technologies (Europe), 2010

19%23%

32%

43%

55% 55% 54%61%

100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

13%

9%16%

100%

0%

20%

40%

60%

80%

100%

2010 2012 2014 2016 2018 2020

Imple

menta

tion (

%)

Locomotives Railcars

Locomotive & Railcar Market : Penetration of APU Systems in Diesel Locomotives & Railcars (Europe), 2010-2020

• Over 1408 diesel locomotives are expected to have APU

systems installed by 2020.

• Will see highest rates of implementation in the 560-

2000kW power category.

• Fuel Savings of up to 29000 litres in one working year.

• It is expected to achieve 61% implementation in all

locomotives by 2020.

• Product attractiveness is expected to reach greater than

80% on the desirability scale.

• Pb Acid is expected to lose favour towards newer battery

technologies.

• Ni-Cd and Li-ion batteries seem to have greatest levels of

interest and research for rail applications.

• Li-ion batteries have greatest energy densities and are

perfectly suited for hybrid locomotives.

• Ni-Cd batteries are slowly replacing Pb Acid batteries.

• Ni-Cd batteries are expected to capture 35% of the market

share by 2020.

0

400

800

1200

1600

0 50 100 150

Energy Density

Num

ber

of

Cycle

s

Pb Acid Ni-Cd Ni Mh Li IonNote: All figures are rounded; the base year is 2010. Source: Frost & Sullivan Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan

Stage IIIB emission deadlines will not cause drastic

implementation of APU systems in locomotives. However

due to its significant contribution to fuel savings, Operators

will gradually adopt APU systems. Manufacturers are likely

to slowly offer it as standard to remain competitive

Railcars have Head End

power units that double as

APU systems when engine is

not operating.

Shift in focus towards newer battery

technologies in rail applications

34M6DB-18

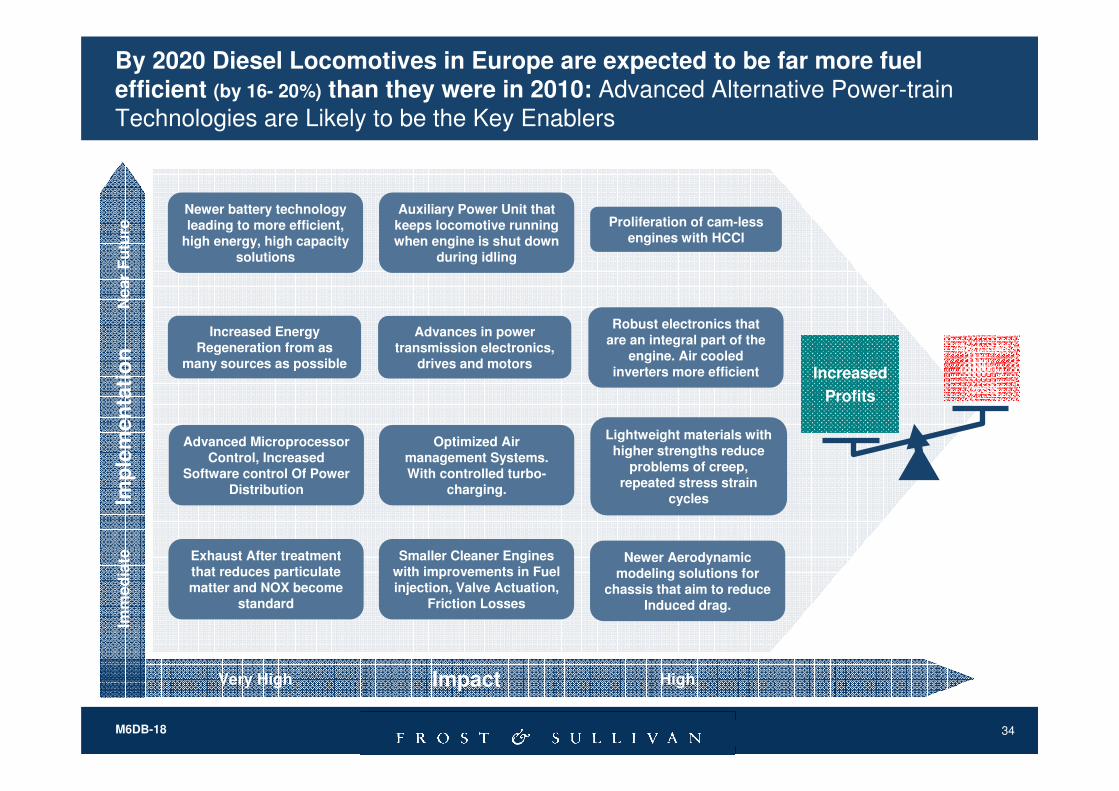

By 2020 Diesel Locomotives in Europe are expected to be far more fuel

efficient (by 16- 20%) than they were in 2010: Advanced Alternative Power-train

Technologies are Likely to be the Key Enablers

Advanced Microprocessor Control, Increased

Software control Of Power Distribution

Auxiliary Power Unit that keeps locomotive running when engine is shut down

during idling

Smaller Cleaner Engines with improvements in Fuel injection, Valve Actuation,

Friction Losses

Newer battery technology leading to more efficient,

high energy, high capacity solutions

Advances in power transmission electronics,

drives and motors

Lightweight materials with higher strengths reduce

problems of creep, repeated stress strain

cycles

Newer Aerodynamic modeling solutions for

chassis that aim to reduce Induced drag.

Exhaust After treatment that reduces particulate matter and NOX become

standard

Robust electronics that are an integral part of the

engine. Air cooled inverters more efficient

Optimized Air management Systems. With controlled turbo-

charging.

Proliferation of cam-less engines with HCCI

Very High Impact High

Imm

ed

iate

Imp

lem

en

tati

on

Near

Fu

ture

Increased Energy Regeneration from as

many sources as possibleReduced

running

costsIncreased

Profits

3535

Key Takeaways : Europe Diesel Powertrain Markets

Alternate fuels and Fuel cell

technologies still in research phase.

Strong demand for passenger rail cars : 3247 Units expected to be

delivered by 2020

Diesel Locomotive Market in the

560-2,000 kW range expected to

grow at 5.85% CAGR

Battery based hybrid locomotives

ideal for shunter / switcher applications. Expected to be gain

prominence by 2020

Locomotive & Railcar Market : Key Findings (Europe), 2010

Source: Frost & Sullivan

Low Sulfur diesel is to become standard supply

By 2020, Battery technologies like

Li-ion are expected to have

increased presence and be economically feasible. Current

generation NiCD set to replace lead acid

10,298 Locomotives & 1,860 Railcars likely to be replaced starting 2015

OEMs to expand portfolio to have

presence in all power segments

Permanent magnet traction motors to have tremendous market

penetration from current levels, 2% to 27% by 2020

Variable geometry turbochargers

likely to have 100% implementation in all railcars by 2020

A total of 7313 units (both diesel locomotives and railcars) are

expected to utilise at least one form

of idle reduction (example APU)

Common rail injection systems to

become standard for all diesel powertrains

Key Findings

36

Chapter 12: Traction Motor Technologies

3737

Traction Motors:

AC motors with permanent magnets

Diesel Powertrain Market : Key Traction Motor

Technologies (Europe), 2010-2020

Permanent Magnet Motor

Three Phase Asynchronous Motor

Three phase asynchronous motors have seen increased

market presence in the last 10 years as they have

greater efficiency and very efficient at brake energy recovery.

Conventionally used for wind turbines, permanent

magnet motors are seeing increased usage in rail applications.

Larger portion of braking can

be done electrically

Diesel Powertrain Market: Drivers for Implementing

Permanent Magnet Traction Motors (Europe), 2010

Drivers

Reduced volume &

weight

Optimized energy

efficiency

Permanent Magnet Motor: Bombardier Mitrac

•Reduced energy consumption

•Less requirements for motor cooling

•Higher performance

Source: Frost & Sullivan

Source: Frost & SullivanSource: Bombardier

3838

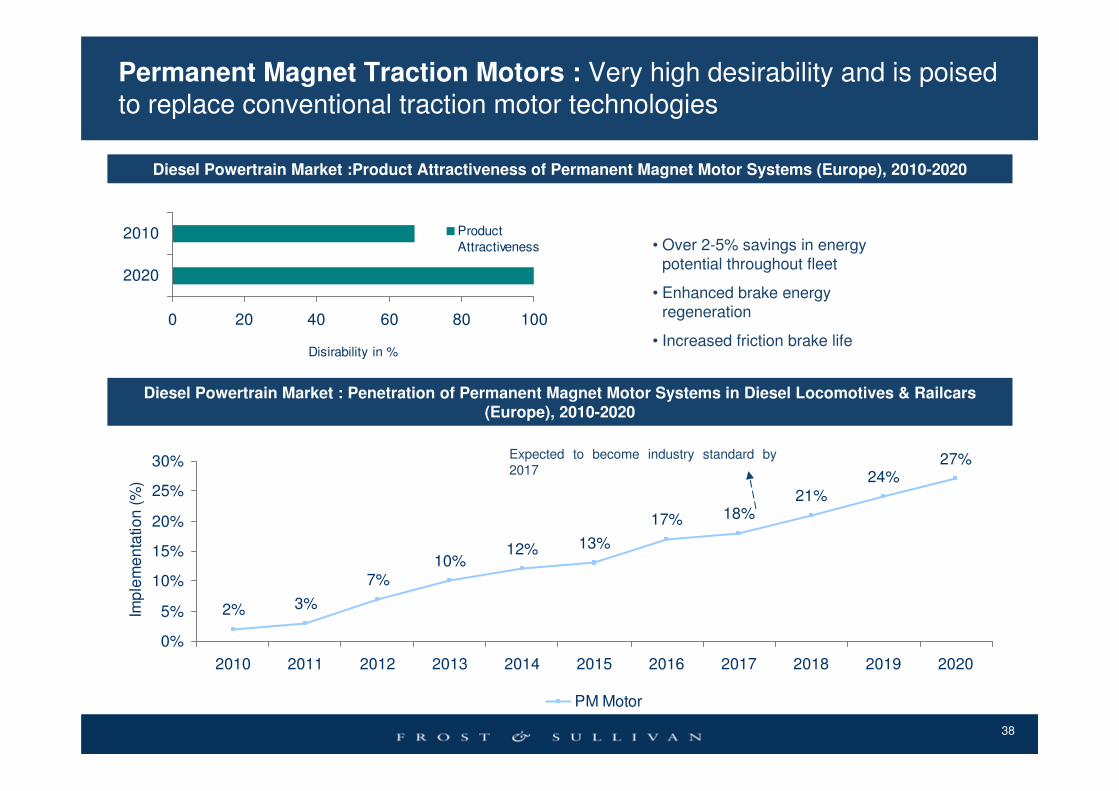

Permanent Magnet Traction Motors : Very high desirability and is poised

to replace conventional traction motor technologies

10%12% 13%

17% 18%21%

24%27%

3%2%

7%

0%

5%

10%

15%

20%

25%

30%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Imp

lem

en

tatio

n (

%)

PM Motor

Diesel Powertrain Market : Penetration of Permanent Magnet Motor Systems in Diesel Locomotives & Railcars

(Europe), 2010-2020

Diesel Powertrain Market :Product Attractiveness of Permanent Magnet Motor Systems (Europe), 2010-2020

• Over 2-5% savings in energy potential throughout fleet

• Enhanced brake energy regeneration

• Increased friction brake life

0 20 40 60 80 100

2020

2010

Disirability in %

Product

Attractiveness

Expected to become industry standard by 2017

3939

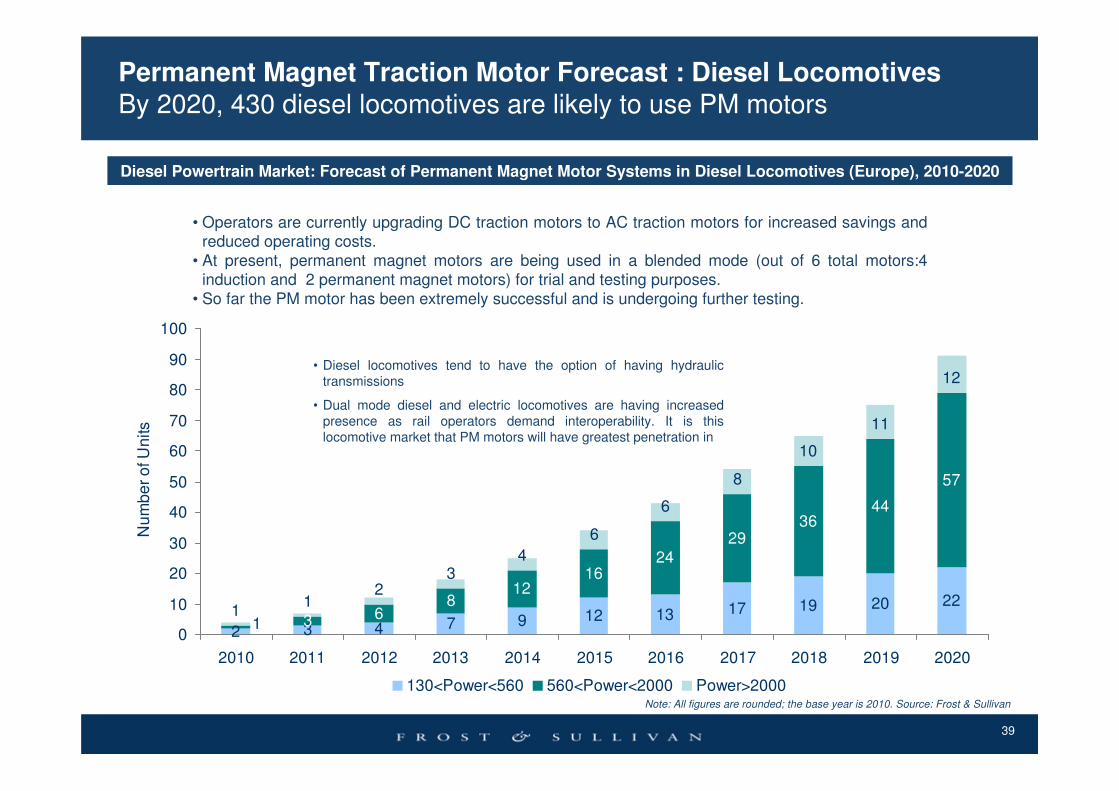

Permanent Magnet Traction Motor Forecast : Diesel Locomotives

By 2020, 430 diesel locomotives are likely to use PM motors

2 3 4 7 9 12 13 17 19 20 22

3 68

1216

2429

3644

57

23

4

6

6

8

10

11

12

1

11

0

10

20

30

40

50

60

70

80

90

100

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Nu

mb

er

of U

nits

130<Power<560 560<Power<2000 Power>2000

Diesel Powertrain Market: Forecast of Permanent Magnet Motor Systems in Diesel Locomotives (Europe), 2010-2020

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan

• Operators are currently upgrading DC traction motors to AC traction motors for increased savings and reduced operating costs.

• At present, permanent magnet motors are being used in a blended mode (out of 6 total motors:4 induction and 2 permanent magnet motors) for trial and testing purposes.

• So far the PM motor has been extremely successful and is undergoing further testing.

• Diesel locomotives tend to have the option of having hydraulic transmissions

• Dual mode diesel and electric locomotives are having increased presence as rail operators demand interoperability. It is this locomotive market that PM motors will have greatest penetration in

4040

Permanent Magnet Traction Motor Forecast : Diesel Railcars

By 2020, 517 diesel multiple units are likely to use PM motors

Diesel Powertrain Market: Forecast of Permanent Magnet Motor Systems in Diesel Multiple Units (Europe), 2010-2020

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan

2 410 14 18 22

31 3645

5565

813

17

2126

35

39

48

4

1 20

20

40

60

80

100

120

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Nu

mb

er

of U

nits

130<Power<560 560<Power<2000

• PM motors have greatest significance for railcars : increased motor life, reduced railcar weight and availability of torque in a wide speed range

• Reduction in size of up to 25% coupled with quiet vibration free operation makes it ideal for multiple unit applications.

• Demand in 2010 is at 1% of total traction motor market. PM motors have high efficiencies and are expected to have tremendous penetration of 27% by start of 2017.

• After which PM motors are expected to become industry standard

41

Chapter 17: About Frost & Sullivan

4242

Who is Frost & Sullivan

• The Growth Consulting Company

• Founded in 1961, Frost & Sullivan has over 45 years of assisting clients with their decision-making

and growth issues

• Over 1,700 Growth Consultants and Industry Analysts across 32 global locations.

• Over 10,000 clients worldwide - emerging companies, the global 1000 and the investment

community.

• Developers of the Growth Excellence Matrix – industry leading growth positioning tool for

corporate executives.

• Developers of T.E.A.M. Methodology, proprietary process to ensure that clients receive a 360o

perspective of technology, markets and growth opportunities.

• Three core services: Growth Partnership Services, Growth Consulting and Career Best

Practices.

4343

What Makes Us Unique

• Exclusively Focused on Growth

Global thought leader exclusively focused on

addressing client growth strategies and plans –

Team actively engaged in researching and

developing of growth models that enable clients

to achieve aggressive growth objectives.

• Industry Breadth

Cover the broad spectrum of industries and

technologies to provide clients with the ability to

look outside the box and discover new and

innovative ideas.

• Global Perspective

32 global offices ensure that clients receive a

global coverage/perspective based on regional

expertise.

• 360o

Perspective

Proprietary T.E.A.M.TM

Methodology integrates

all 6 critical research methodologies to

significantly enhance the accuracy of decision

making and lower the risk of implementing

growth strategies.

• Growth Monitoring

Continuously monitor changing technology,

markets and economics and proactively address

clients growth initiatives and position.

• Trusted Partner

Working closely with client Growth Teams –

helping them generate new growth initiatives

and leverage all of

Frost & Sullivan assets to accelerate their

growth.

4444

T.E.A.M. Methodology

• Frost & Sullivan’s proprietary T.E.A.M. methodology, ensures that clients have complete “360

Degree Perspective” from which to drive decision-making. Technical, Econometric, Application, and

Market information ensures that clients have a comprehensive view of industries, markets and

technology.

Technical Real-time intelligence on technology, including emerging technologies, new R&D breakthroughs,

technology forecasting, impact analysis, groundbreaking research, and licensing opportunities.

Econometric In-depth qualitative and quantitative research focused on timely and critical global, regional, and

country specific trends, including the political, demographic, and socioeconomic landscapes.

Application Insightful strategies, networking opportunities, and best practices that can be applied for enhanced

market growth; interactions between the client, peers, and Frost & Sullivan representatives that

result in added value and effectiveness.

Market Global and regional market analysis, including drivers and restraints, market trends, regulatory

changes, competitive insights, growth forecasts, industry challenges, strategic recommendations,

and end-user perspectives.

4545

Global Perspective

• 1,700 staff across every major market worldwide

• Over 10,000 clients worldwide from emerging to global 1000 companies