estate planning: top seven tools to know

TRANSCRIPT

2019 Edition

Estate Planning: Top Seven Tools to Know

All Courses. All Formats. All Year.

LawPracticeCLEUnlimited

ABOUT USLawPracticeCLE is a national continuing legal education company designed to provide education on current, trending

issues in the legal world to judges, attorneys, paralegals, and other interested business professionals. New to the playing �eld, LawPracticeCLE is a major contender with its o�erings of Live Webinars, On-Demand Videos, and In-per-son Seminars. LawPracticeCLE believes in quality education, exceptional customer service, long-lasting relationships,

and networking beyond the classroom. We cater to the needs of three divisions within the legal realm: pre-law and law students, paralegals and other support sta�, and attorneys.

If you are interested in teaching for LawPracticeCLE, we want to hear from you! Please email our Directior of Operations at [email protected] with your information. Be advised when speaking for LawPracticeCLE, we require you to provide the bellow items related to your course:

WHY WORK WITH US?At LawPracticeCLE, we partner with experienced attorneys and legal professionals from all over the country to bring hot topics and current content that are relevant in legal practice. We are always looking to welcome dynamic and accomplished lawyers to share their knowledge!

As a LawPracticeCLE speaker, you receive a variety of bene�ts. In addition to CLE teaching credit attorneys earn for presenting, our presenters also receive complimentary tuition on LawPracticeCLE’s entire library of webinars and self-study courses.

LawPracticeCLE also a�ords expert professors unparalleled exposure on a national stage in addition to being featured in our Speakers catalog with your name, headshot, biography, and link back to your personal website. Many of our courses accrue thousands of views, giving our speakers the chance to network with attorneys across the country. We also o�er a host of ways for our team of speakers to promote their programs, including highlight clips, emails, and much more!

1. A Course Description2. 3-4 Learning Objectives or Key Topics3. A Detailed Agenda4. A Comprehensive PowerPoint Presentation

CONTACT US

941-584-9833 www.lawpracticecle.com 11161 E State Road 70 #110-213Lakewood Ranch, FL 34202

LAWPRACTICECLE UNLIMITEDLawPracticeCLE Unlimited is an elite program allowing attorneys and legal professionals unlimited access to all Law-PracticeCLE live and on-demand courses for an entire year.

LawPracticeCLE provides twenty new continuing legal education courses each month that will not only appeal to your liking, but it will also meet your State Bar requirement.

Top attorneys and judges from all over the country partner with us to provide a wide variety of course topics from basic to advanced. Whether you are a paralegal or an experienced attorney, you can expect to grow from the wealth of knowledge our speakers provide.

ACCREDITATIONLawPracticeCLE will seek approval of any CLE program where the registering attorney is primarily licensed and a singlealternate state. The application is submitted at the time an attorney registers for a course, therefore approval may not be received at the time of broadcasting. In the event a course is denied credit, a full refund or credit for another Law-PracticeCLE course will be provided.

LawPracticeCLE does not seek approval in Illinois or Virginia, however the necessary documentation to seek CLE creditin such states will be provided to the registrant upon request.

ADVERTISING WITH LAWPRACTICECLEAt LawPracticeCLE, we not only believe in quality education, but providing as many tools as possible to increasesuccess. LawPracticeCLE has several advertising options to meet your needs. For advertising and co-sponsorshipinformation, please contact the Director of Operations, Jennifer L. Hamm, [email protected].

CHECK US OUT ON SOCIAL MEDIAFacebook: www.facebook.com/LawPracticeCLE

Linkedln: www.linkedin.com/company/lawpracticecle

lnstagram: www.instagram.com/lawpracticecle

Twitter: www.twitter.com/LawPracticeCLE

COURSE CATEGORIESA View From The BenchAnimal LawBankruptcy LawBusiness LawCannabis LawConstruction LawCriminal LawCybersecurity LawEducation LawEmployment LawEntertainment Law

Estate PlanningEthics, Bias, and ProfessionalismFamily LawFederal LawFood and Beverage LawGun LawHealth LawImmigration LawIntellectual Property LawInsurance LawNonpro�t Law

Paralegal StudiesPersonal Injury LawPractice Management & Trial PrepReal Estate LawReligious LawSocial Security LawSpecialized TopicsTax LawTechnology LawTransportation LawTribal Law More Coming Soon ...

Estate Planning:Top 7 Tools to Know

Elaine T. Yandrisevits, J.D., LL.M. (Taxation)LawPracticeCLE

131 West State Street, Doylestown, PA | 215.230.7500 | www.ammlaw.com

THE ESTATE PLAN

Antheil Maslow & MacMinn, LLP

What are the Goals of Estate Planning?

• Preserve family values and wealth• Prevent payment of excessive taxes• Disposition of assets

– A child with disabilities? A minor? A child with spending problems?

• Liquidity– If assets all illiquid, no ability to pay tax

• Flexibility– Is plan flexible enough to address changing estate tax

laws or the family needs?

Antheil Maslow & MacMinn, LLP

Legal Terms

• Decedent: Person who died• Testator: Person who makes a Will• Laws of Intestacy: Laws that control how property will pass if a

person dies without a Will• Executor: Person who is responsible for opening an estate at the

county Register of Wills, gathering the assets of the estate, paying any taxes, and distributing the property

• Trustee: Person who manages and invests money that is held in Trust for a beneficiary

• Beneficiary: A person who will receive assets from an estate or trust

• Guardian: A person who, after a legal proceeding, has the authority to make decisions on behalf of someone else, typically a minor or person who has intellectual disabilities

Antheil Maslow & MacMinn, LLP

Fundamental Documents

• Will• Trust(s)• Power of Attorney• Living Will

Antheil Maslow & MacMinn, LLP

Benefits of Executing a Will

• Avoid intestacy laws• Choose the executor of your estate• Name a guardian and create a trust for minor

children• Create a trust for a child with special needs• Direct specific personal property to a specific

person• Avoid payment of excessive taxes

Antheil Maslow & MacMinn, LLP

TOOL #1:METHODS OF AVOIDING PROBATE

Antheil Maslow & MacMinn, LLP

Probate vs. Nonprobate Property

• The Will only controls the disposition of probate assets– Assets owned by the decedent as an individual

that do not include a beneficiary designation• Individually-owned bank accounts• Individually-owned real estate• Vehicles• Tangible personal property• Jointly-owned property owned as Tenants-in-Common

Antheil Maslow & MacMinn, LLP

Probate vs. Nonprobate Property

• Nonprobate property will pass to the surviving joint owner or the named beneficiary, regardless of the terms of the Will– IRAs, 401Ks, 403(b)s, other retirement assets– Life insurance– Jointly-owned bank accounts– Jointly-owned real estate owned as Tenants by the

Entireties or Joint with Right of Survivorship

Antheil Maslow & MacMinn, LLP

Methods of Avoiding Probate

• Revocable Trust and Pour Over Will• Jointly-Titled Assets with Right of Survivorship • Transfer on Death Accounts

Antheil Maslow & MacMinn, LLP

Revocable Trust and Pour Over Will

• Revocable Trust is a “Will Substitute” that functions with a Pour Over Will to transfer property.

• Property titled to a Revocable Trust during life is nonprobate property. – If property is not titled to Revocable Trust during life, it is

probate property. • Pour Over Will directs that any probate property is

distributed to Revocable Trust.– Executor must be appointed to distribute property to

Revocable Trust. • Revocable Trust does not avoid estate or inheritance

taxes.

Antheil Maslow & MacMinn, LLP

Revocable Trust and Pour Over Will

• I give the rest, residue and remainder of my estate, real and personal ("my Residuary Estate"), to the then serving Trustee of the John Doe Revocable Trust (sometimes referred to as "the Trust" or "the Trust Agreement"), that I have signed before signing this Will, to be disposed of as provided in the Trust Agreement, including any amendments to it signed before today, today or after today. If this gift is ineffective but the terms of the Trust may be incorporated into this Will or otherwise carried out under this Will, then (i) I hereby appoint the Trustee under the Trust Agreement to be Trustee under this Will; (ii) I incorporate the provisions of the Trust Agreement into this Will; (iii) I give my Residuary Estate to the Trustee under this Will; and (iv) I direct that my Residuary Estate shall be disposed of in the manner provided in the Trust Agreement but with the trusts thereby set forth treated as trusts under this Will.

Antheil Maslow & MacMinn, LLP

Revocable Trust and Pour Over Will

• Revocable Trust and Pour Over Will structure is useful when: – Probate process is particularly expensive/difficult– Testator owns out-of-state real property– Testator has significant nonprobate assets that will

pass by beneficiary designations– Testator may want to begin titling assets into

Revocable Trust during life for asset management purposes

Antheil Maslow & MacMinn, LLP

Jointly-Titled Assets with Right of Survivorship

• Pass automatically to the surviving joint owner(s) by operation of law

• Jointly-titled assets do not avoid estate or inheritance taxes– Taxed on the proportion attributable to the

deceased joint owner• Need to ensure that clients that jointly-title

assets do not inadvertently change estate plan– Consider using Power of Attorney

Antheil Maslow & MacMinn, LLP

Jointly-Titled Assets with Right of Survivorship

• Mother executes a Will that divides her residuary estate among her three Children. At the time of her death, Mother owns a house, a savings account, and a checking account. Several years before her death, Mother added Eldest Child to the savings account and checking account so that Eldest Child could pay bills for Mother from these accounts; she did not add her other two Children to these accounts.

Antheil Maslow & MacMinn, LLP

Jointly-Titled Assets with Right of Survivorship

• Since the house remained titled solely in Mother’s name, it is the only asset that will be distributed according to the terms of Mother’s Will.

• Eldest Child will receive full ownership of the savings and checking accounts, plus one-third of the value of the house.

• The other two Children will receive the remaining two-thirds of the house only.

Antheil Maslow & MacMinn, LLP

Transfer on Death (TOD) Accounts

• Accounts transfer to named beneficiaries by operation of law at the death of primary account owner

• Typically handled and completed by bank or other financial institution

• Do not avoid estate or inheritance taxes

Antheil Maslow & MacMinn, LLP

FEDERAL ESTATE TAX

Antheil Maslow & MacMinn, LLP

Federal Estate Tax

• Tax on the gross value of the decedent’s estate at the time of death.

• Federal Estate Tax Return must be filed when:– The decedent is a citizen of the United States.– The decedent is a foreign citizen owning property

located in the United States.

• Maximum tax rate: 40%

Antheil Maslow & MacMinn, LLP

Property Subject to Estate Tax

• All worldwide property. • Nonprobate property – IRAs, 401Ks, etc.• Jointly-owned property is taxed on the

proportion of the decedent’s interest in the property.– Real property owned as tenants by the entireties is

subject to federal estate tax at one-half (1/2) of the date of death value.

• Life insurance.• Property subject to a power of appointment.

Antheil Maslow & MacMinn, LLP

Federal Estate and Gift Tax Lifetime Exemption

• If a decedent’s taxable estate and lifetime gifts do not exceed the exclusion amount for the year of death, no federal estate tax will be due.

• 2019 Exemption – $11.4 million

Antheil Maslow & MacMinn, LLP

Federal Estate and Gift Tax Lifetime Exemption

• The exemption is indexed for inflation and has increased every year since 2011.

• 2019 -- $11.4 million– 2018 -- $11.18 million– 2017 -- $5.49 million

• Tax Cuts and Jobs Act of 2017 – Exemption is scheduled to be reduced to $5 million (adjusted for inflation) effective January 1, 2026

Antheil Maslow & MacMinn, LLP

Federal Estate and Gift Tax Lifetime Exemption

Antheil Maslow & MacMinn, LLP

Source: https://www.taxpolicycenter.org/briefing-book/how-many-people-pay-estate-tax

TOOL #2:PORTABILITY

Antheil Maslow & MacMinn, LLP

Portability

• 26 U.S. Code § 2010(c)(5)(A)• Created by the Tax Relief, Unemployment

Insurance Reauthorization, and Job Creation Act of 2010 and made permanent by the American Taxpayer Relief Act of 2013.

• Deceased Spouse’s Unused Exemption (DSUE)– Allows for a surviving spouse to preserve the

“unused” portion of the deceased spouse’s Lifetime Exemption.

Antheil Maslow & MacMinn, LLP

Portability

• Effectively allows a married couple to pass assets totaling $22.8 million free of Federal Estate Tax (2019)

Antheil Maslow & MacMinn, LLP

Portability

• To elect portability, the personal representative must timely file a Federal Estate Tax Return.

• If the decedent was married at the time of death, portability is automatically applied on the Form 706.– If the surviving spouse does not want portability, the

personal representative must affirmatively opt out. • In cases of multiple marriages and remarriages,

the surviving spouse may only use the DSUE of his or her most recently-deceased spouse.

Antheil Maslow & MacMinn, LLP

Portability

Antheil Maslow & MacMinn, LLP

TOOL #3:MARITAL DEDUCTION

Antheil Maslow & MacMinn, LLP

Marital Deduction

• The value of assets passing to the surviving spouse at the first spouse’s death is deducted from the gross taxable estate if the assets pass in a qualifying manner

• Unlimited in value • Assets will be subject to tax at the surviving

spouse’s death.

Antheil Maslow & MacMinn, LLP

Marital Deduction

• “In a qualifying manner” – preserves the property in a manner that provides for the application of tax at the death of the surviving spouse:– Outright– In a qualifying trust

Antheil Maslow & MacMinn, LLP

TOOL #4:CREDIT SHELTER/MARITAL DEDUCTION TRUSTS

Antheil Maslow & MacMinn, LLP

Credit Shelter Trust

• Allows spouses to utilize their individual Federal Estate Tax Exemption– Assets in individual names – Surviving spouse typically is the beneficiary of the

Trust during lifetime– Residue flows to children or other designated

beneficiaries• Sometimes also called a “Family Trust”• Typically utilizes a formula clause

Antheil Maslow & MacMinn, LLP

Credit Shelter Trust

• Allowable Terms:– Income to Surviving Spouse – Surviving Spouse can have absolute right to withdraw

5% of principal or $5,000 annually – Trustee can distribute principal for Health, Education,

Maintenance or Support (HEMS)– Trustee can distribute principal in his discretion – Surviving Spouse can have right to compel required

minimum distributions from IRA/Retirement accounts payable to Credit Shelter Trust

– Surviving Spouse can have a testamentary power of appointment

Antheil Maslow & MacMinn, LLP

Marital Deduction Trust

• Shields assets in excess of the Federal Estate Tax Exemption passing to the surviving spouse from Federal Estate Tax

• Assets will qualify for the Marital Deduction and be included in the estate of the surviving spouse

• Sometimes called a “Marital Trust”

Antheil Maslow & MacMinn, LLP

Qualified Terminable Interest Property (QTIP)

• Qualifies for Marital Deduction– Surviving Spouse must receive all income for life– Trust cannot direct assets to anyone other than

Surviving Spouse

• Irrevocable election made on Estate Tax Return• QTIP property will be taxed at Surviving Spouse’s

death • Used when decedent wants to control where

assets go after Surviving Spouse’s death

Antheil Maslow & MacMinn, LLP

Formula Gift

Antheil Maslow & MacMinn, LLP

Residue into Marital Trust

Antheil Maslow & MacMinn, LLP

TOOL #5:DISCLAIMER TRUSTS

Antheil Maslow & MacMinn, LLP

Disclaimer Trusts

• Permits post-death tax planning by use of a qualified disclaimer of the decedent’s property by the surviving spouse to preserve the surviving spouse’s Federal Estate Tax Exemption

• Disclaimer Trust operates largely like a Credit Shelter Trust

Antheil Maslow & MacMinn, LLP

Disclaimer Trusts

• Elements of a valid disclaimer:– Irrevocable and unqualified refusal to accept an interest in

the property– In writing– Received by the person transferring the interest, or his/her

legal representative, within nine (9) months after the date upon which the interest is created

– Disclaimant cannot accept the disclaimed interest or any of its benefits

– Care must be taken to not inadvertently accept assets by managing accounts or investments.

– Interest must pass without any direction on part of the disclaimant

Antheil Maslow & MacMinn, LLP

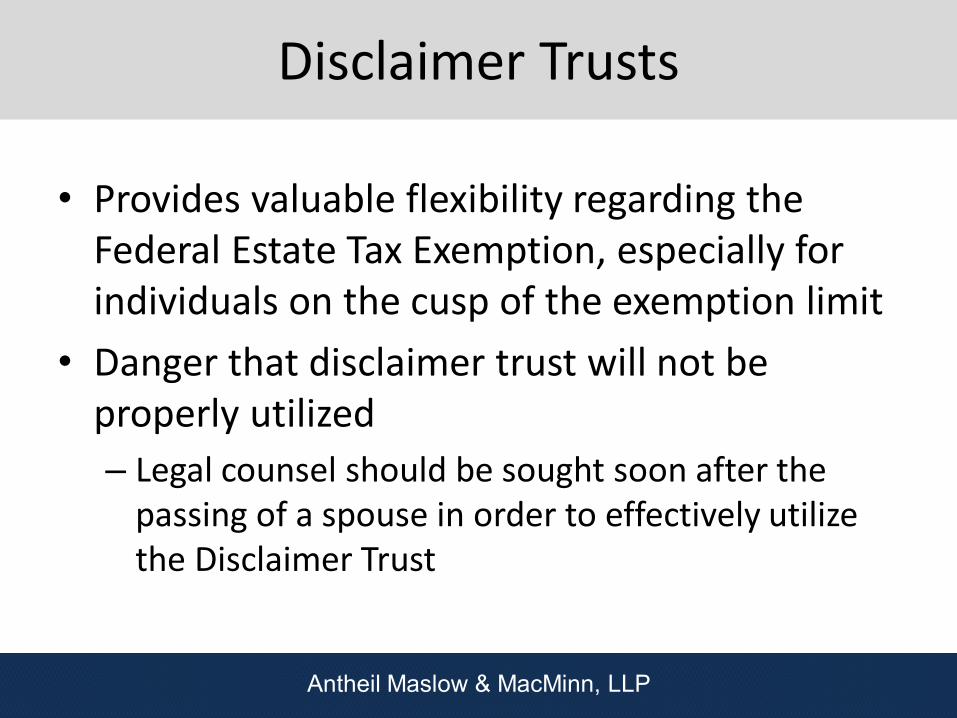

Disclaimer Trusts

• Provides valuable flexibility regarding the Federal Estate Tax Exemption, especially for individuals on the cusp of the exemption limit

• Danger that disclaimer trust will not be properly utilized– Legal counsel should be sought soon after the

passing of a spouse in order to effectively utilize the Disclaimer Trust

Antheil Maslow & MacMinn, LLP

Disclaimer Trusts

Antheil Maslow & MacMinn, LLP

TOOL #6:MINORS’ TRUSTS

Antheil Maslow & MacMinn, LLP

Minors’ Trusts

• Provides a mechanism to maintain resources by a Trustee on behalf of minor children until they reach a certain age, designated by the Testator, at which time full access to the funds will be provided

Antheil Maslow & MacMinn, LLP

Minors’ Trusts

Antheil Maslow & MacMinn, LLP

Minors’ Trusts

• Typically health, education, maintenance, and support (HEMS) standard

• Avoids young beneficiary without financial savvy from receiving funds outright

• Can last as long as testator wants– Indefinitely– A certain age– Payable in stages

Antheil Maslow & MacMinn, LLP

Minors’ Trusts

Antheil Maslow & MacMinn, LLP

Minors’ Trusts

• Could be a single/”one-pot” trust– If a single trust, typically lasts until youngest

beneficiary attains a certain age, then divided into separate shares

– Requires guidance for trustee for distributions to older beneficiaries – example, graduate education

– Would still want separate trust feature for qualified plans

Antheil Maslow & MacMinn, LLP

TOOL #7:SPECIAL NEEDS TRUSTS

Antheil Maslow & MacMinn, LLP

Special Needs Trusts

• Allows an individual with disabilities to benefit from the resources of a Trust while continuing to receive essential public benefits, most notably Medicaid, Supplemental Security Income, and Mental Health/Intellectual Disability benefits

Antheil Maslow & MacMinn, LLP

Definition of Disabled

• An adult is considered to be disabled by the Social Security Administration when:– He or she is unable to engage in any substantial

gainful activity – By reason of any medically determinable physical

or mental impairment – Which can be expected to result in death or which

has lasted or can be expected to last for a continuous period of not less than twelve (12) months.

Antheil Maslow & MacMinn, LLP

Public Benefits

• Resource- and income-dependent:– Programs have strict limits on the amount and type of

funds an individual can own (resources) or earn (income) in order to be financially eligible for the program.

• Examples:– Supplemental Security Income (SSI)

• Individual resource limit: $2,000.00• Couple resource limit: $3,000.00

– Medicaid/Medical Assistance/Waiver programs• Resource limit varies by program

– Food Stamps

Antheil Maslow & MacMinn, LLP

Special Needs Trusts

• Any funds held in a Special Needs Trust do not count as resources for purposes of determining eligibility for public benefits.

• Trust is designed to supplement, not supplant, the beneficiary’s public benefits.

• Trustee has the unfettered discretion in making all distributions from the Trust.

Antheil Maslow & MacMinn, LLP

Third Party Funded SNTs

• Holds funds that belonged to anyone except the beneficiary.

• Typically created as part of an estate plan. • No payback to state Medicaid agency

Antheil Maslow & MacMinn, LLP

Third Party Funded SNTs

• The estate planning documents must include a specific intent by the testator for the funds to be held in a Special Needs Trust. – Example: “I leave the entire residue of my estate

to the Third Party Funded Special Needs Trust for the benefit of my daughter, Jane Smith.”

Antheil Maslow & MacMinn, LLP

If There is no Third Party Funded SNT…

• If the estate planning documents do not include a specific intent that the funds for an individual with disabilities be held by a Third Party Funded Special Needs Trust or in cases of intestacy, the funds must be:– Held by a Self Funded Special Needs Trust;– Held by a Pooled Special Needs Trust;– Held by an ABLE Account; or – Spent down.

Antheil Maslow & MacMinn, LLP

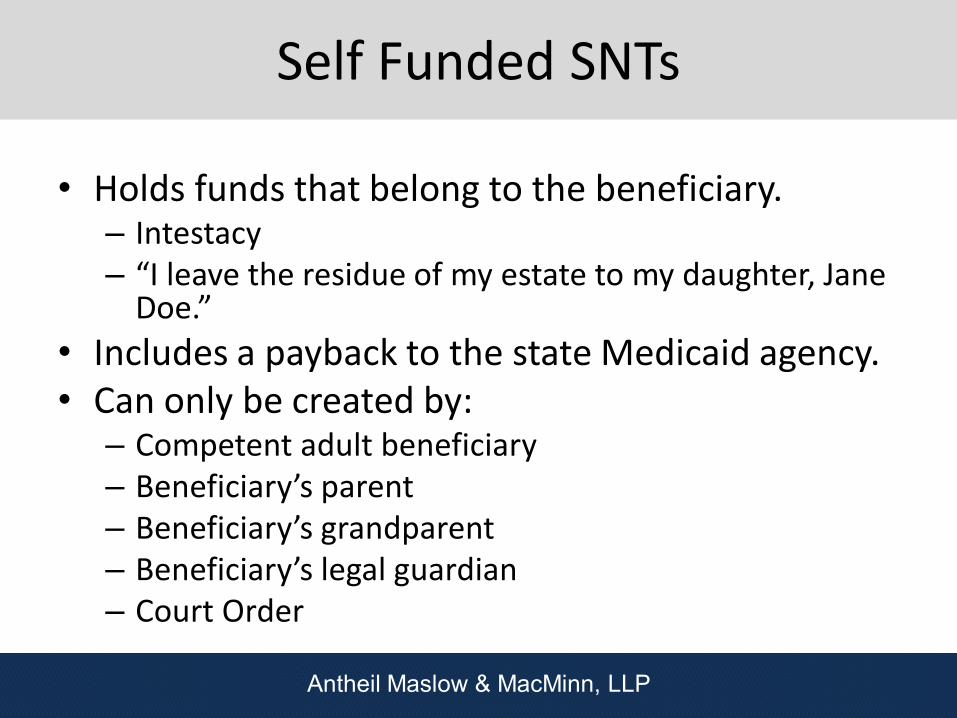

Self Funded SNTs

• Holds funds that belong to the beneficiary.– Intestacy– “I leave the residue of my estate to my daughter, Jane

Doe.”• Includes a payback to the state Medicaid agency. • Can only be created by:

– Competent adult beneficiary– Beneficiary’s parent– Beneficiary’s grandparent– Beneficiary’s legal guardian– Court Order

Antheil Maslow & MacMinn, LLP

131 West State Street, Doylestown, PA | 215.230.7500 | www.ammlaw.com

Estate Planning & Administration | Tax Law Employment | Business/Corporate | Real Estate

Family Law | Litigation |Nonprofits | Personal Injury