esource potential and implications of ^ minera

TRANSCRIPT

esource Potential and Implications of

^ Mineral Development - i n the

South Pacific Papua New Guinea

East-West Center Resource Systems

Institute Summaries of the Papers Presented at the

Conference Held at

Arovo Island Papua New Guinea

September 1981 Commonwealth

Secretariat

r~x~~| EAST-WEST CENTER I n A ^ I H o n o l u l u - Hawaii

Resource Potential and Implications of Mineral Development

in the South Pacific

Summaries of the Papers Presented at the Conference held at Arovo Island, Papua New Guinea

September 11-15, 1981

East-West Resource Systems Institute East-West Center

1777 East-West Road Honolulu, Hawaii 96848

August 1982

[

ACKNOWLEDGEMENTS

It is my pleasure to acknowledge the support of our cosponsors, the Papua New Guinea government and the Commonwealth Secretariat, in organizing and assisting in funding the Arovo Island conference. Within these organizations, Nigel Agonia and Pat Loseby in Port Moresby and Peter Freeman and Michael Faber in London were particularly valuable for their organizational assistance. O f the many participants in the conference, I especially thank The Honorable Wiwa Korowi, Papua New Guinea Minister for Minerals and Energy, and The Honorable Thomas Ruben Seru, Vanuatu Minister of Lands, for taking time out of their busy schedules to attend the sessions. The executives of Broken H i l l Proprietary, Conzinc Riotinto of Australia, and Bougainville Copper shared their time and insights with us, and I greatly appreciate their participation. The courtesy extended by the management of Bougainville Copper Ltd. with respect to the tour of the Bougainville operations deserves a special note of appreciation.

The staff in the Raw Materials Program did a commendable job in putting together the conference and summary report. Research fellows Sam Pintz and Ron Richmond capably handled the conference, and the conscientious note-taking and editorial skills of Jean Brady and Annabelle Lee enabled us to produce this summary report. The logistical support of our program secretary, Lillian Shimoda, was invaluable to the smooth running of the conference and to the preparation of this report.

To all these people and organizations, I express my most sincere appreciation.

Charles J . Johnson Leader Raw Materials Program

u

CONTENTS

Acknowledgements ii Foreword v Opening Address by The Honorable Wiwa Korowi vii

Part I: Geology and Economics Geology, Tectonics, and Mineral Potential of the

Southwest Pacific (R. N . Richmond) 1 Regional Geological Mapping and Mineral Exploration

Activity in Papua New Guinea (K. W. Doble) 5 The Economic Geology of the Solomon Islands

(F. I. Coulson) 6 Economic Minerals in Vanuatu—Known and Potential

Resources (A. Macfarlane a n d j . Carney) 8 Minerals Development Policy and Resource

Classification: Fiji Case Study (D. Greenbaum and H . Plummer) 11

Economics of South Pacific Minerals Development (C.J .Johnson) 13

Perceptions of Risk in Petroleum Exploration (P. Freeman) 19

Part II: Legal Issues Minerals Legislation: The Relevant Legislative

Questions and Options (D. C . Frecker) 21 Petroleum: Current Legal Issues—The Challenge of

Choice for Non-Oil-Producing Developing Countries (C. W . Dundas) 23

Some Issues for Governments When Formulating Mineral Agreements (S. McGil l ) 24

Part III: The Implementation Context: Internal and External Influences Implementation Issues in Mineral and Petroleum Agreements (S. Pintz) 28

Pan gun a Mine, Bougainville Island: The 1980 Land Compensation Agreement (N. Agonia) 29

iii

Mineral Processing in the Pacific Island Countries: Problems and Opportunities (S. A . Zorn) 31

Future Supplies of Petroleum: Implications for the Asia-Pacific Region (F. Fesharaki) 33

Appendices Appendix A . Workshop Agenda 36 Appendix B. List of Participants 38

List of Tables 1. Prices required to induce commercial development of mines in the South

Pacific 2. Company internal rate of return and government share of project net cash

flow

3. Proposed timetable for mining agreements in Papua New Guinea

List of Figures 1. Metallogenesis at mid-ocean ridge, trench, and island-arc areas 2. Mineral occurrences in Papua New Guinea 3. Geologic map and mineral occurrences of Vanuatu 4. Fiji 's mineral resources classification system 5. a) Cumulative value of minerals production by country within the region

b) Cumulative value of minerals production in the region by.commodity 6. Copper-gold ore grades to produce specified recoverable metal values per

tonne of ore

iv

4

FOREWORD

Since 1979 the Resource Systems Institute's (RSI) Raw Materials Program has given increased attention to policy issues associated with mineral development projects in Asian and Pacific developing countries. This focus led to the convening of a mineral policies conference attended by mineral experts from 14 nations to discuss major policy issues associated with large mining projects. The increased attention to mineral policy issues has been accompanied by the articulation of a new set of interrelated research areas. These areas include: 1) the role of mineral assessment in national planning, 2) case studies in mineral policy, 3) arrangements between governments and transnational companies, and 4) economics of mineral development.

Following the 1980 Mineral Policies Conference, officials of several Pacific island nations suggested that the Raw Materials Program address the special problems of minerals development in their region. In response to these suggestions, the Raw Materials group initiated a three-phase study program which culminated in a conference held on Arovo Island, Papua New Guinea in September 1981. In the first phase of the program, program leader Charles Johnson visited several Pacific nations to collect firsthand information pertaining to the region's minerals potential and mineral development problems. Fi j i , Papua New Guinea, Vanuatu, and the Solomon Islands were selected for special attention in a regional conference. The second phase involved the recruitment of two research fellows with policy experience in the South Pacific. Ronald Richmond, former director of the Fi j i Mineral Resources Department, and Sam Pintz, former assistant secretary of the Papua New Guinea Ministry for Minerals and Energy, joined the program and began to plan the Arovo conference.

From its inception it was realized that, while previous regional conferences had dealt with various tax and fiscal aspects of mining and petroleum production, there was only limited information available on other dimensions of mining development. Four topics of special interest to Pacific nations were selected for discussion at the conference, including 1) geology, 2) resource economics, 3) legislation and investor agreements, and 4) internal and external considerations in implementing major projects. In light of the national policy implications of the issues to be considered, ministers as well as civil servants were invited to the conference, and, in fact, ministers led the delegations from Papua New Guinea and Vanuatu. Papua New Guinea agreed to host the meetings and the Commonwealth Secretariat in London joined as the third sponsor.

The Bougainville Province of Papua New Guinea was selected as the venue

v

for the meetings as it provided participants with the opportunity not only to visit the massive Bougainville copper mine (one of the world's largest copper projects), but also to have firsthand discussions with local leaders about the implications of mineral development for local people. To further expand conference perspectives, executives of the two largest mining companies currently active in the region—Conzinc Riotinto of Australia ( C R A ) and Broken Hi l l Proprietary (BHP)—were invited to present their views regarding private sector investment criteria and concerns. |

Seminars such as the Arovo Island conference represent RSI's ongoing attempts to meet the needs of resource policymakers in the Asia-Pacific region. The conference was conceived at the initiative of the participants and directed toward topics of special interest within a particular region. It was undertaken with two joint sponsors (the Papua New Guinea government and the Commonwealth Secretariat), and included the active participation of private sector executives in order to provide participants with a broader range of policy viewpoints. Participants were given the opportunity to form firsthand impressions of modern mining projects and to discuss the environmental and cultural disruptions that can result from such development. We at the East-West Center hope that seminars conducted at the practical level of policymaking, augmented by the overview of experienced international specialists and academics, can make an important contribution to the long-term development needs of countries in the Asia-Pacific region. '

Harrison Brown Director Resource Systems Institute

I

vi

OPENING ADDRESS by The Honorable Wiwa Korowi Minister for Minerals and Energy

Papua New Guinea

On behalf of my government, the East-West Center, and the Commonwealth Secretariat, I would like to welcome you to this conference on the "Resource Potential and Implications of Mineral Development in the South Pacif ic ." Over the next few days we will be discussing a wide range of topics which may fundamentally affect the development prospects of our island nations.

I realize that our nations are at very different places in the development of their mineral resources. Historically, mining has taken place in all our countries but with the exception of Fiji 's Emperor mine and our own Bougainville and Ok Tedi projects, mining is not a major economic activity in our region. However, in looking over some of the geological and economic assessments for this conference, it is equally clear that mining may very soon assume a new importance to our economies. We in Papua New Guinea believe that our region has the potential to be of major importance in the production and processing of minerals. This assessment certainly appears to be supported by the conclusions of our colleagues at the East-West Center. Similarly, our region is rapidly becoming a target for petroleum exploration. Needless to say, oil and minerals have the potential to completely transform the economic development of our nations and to rapidly increase the living standards of our people, but unplanned development of our resources can cause great havoc with our small economies with the result that a potential blessing is transformed into a curse.

As Melanesians we share a common culture and a common view toward the resources that nature has bestowed on us. As ministers and public servants, we have the responsibility to our citizens to see that these natural resources are wisely developed in ways that will bring the greatest good to the largest number of our people. In undertaking this public stewardship we must walk a narrow path between many conflicting concerns and objectives. We inevitably will be forced to deal with outsiders who neither understand our culture nor are sensitive to our environment. We must bring this understanding to those who come to develop our resources or we will violate the stewardship with which the public has entrusted us. We must find wise, long-term policies that are sufficiently attractive to foreign investors while protecting the interests of our nations.

vn

The first step in the formulation of wise policies is to understand clearly the problems that must be faced. When I was originally discussing this conference with M r . Pintz, I insisted that we should consider the real policy questions associated with mineral development and not let our conference become bogged down in abstract or academic questions. We must leave this conference with practical policy information and references that we can take back to our respective governments and translate into action.

In considering what topics should be discussed, our primary concern was to find areas that had not been discussed in previous international forums while focusing on those subjects that reflect the particular situation of our region. As you all know, the present Papua New Guinea government is a vocal supporter of regional approaches to Pacific problems. We must begin to think of our natural resources as a common endowment which God has given to Pacific people. To this end, we must look to these concerns and attitudes that are common to Pacific people and exchange information and experiences so that our region can prosper and advance.

It has always been clear that, even where common cultural and environmental attitudes exist, different nations may select different policy options to achieve their objectives. This is right and natural, and I deeply believe that solutions that work in Papua New Guinea may not be entirely appropriate for our Fi j i or Vanuatu brothers. Each nation must find its own path . . . its own policies . . . its own solutions. Thus, in the topics we will be considering over the next few days, each delegate should consider how each policy issue can be met within the particular political and social situation of his nation. There are no universally "right" or "perfect" solutions to these policy questions, and we must understand this from the outset. The most we can hope for is to achieve policies that are consistent with our national aspirations and that are consciously taken—not imposed by events! Beyond this, we can only trust that traditional Melanesian good sense and flexibility will give us the wisdom to adapt our policies to changing circumstances.

To provide the conference with the widest spectrum of views, we have invited a wide spectrum of participants to present papers. First, of course, we turned to the sponsoring organizations to tap their considerable expertise. From Honolulu, the East-West Center agreed to contribute the geological experience and the economic and negotiating skills to help us to better understand our mineral potential and the economic implications of development. From London, our old friends at the Commonwealth Secretariat have flown half-way around the world to discuss petroleum development and law. And for Papua New Guinea's part, we have arranged for our justice department to speak on agreements and regulations and for my departmental secretary, M r . Agonia, to talk on land acquisition and compensation.

In addition to contributions from the sponsoring organizations, we have been quite fortunate in being able to arrange for several outside speakers. First, two mining companies currently active in the Pacific—BHP and C R A —have graciously agreed to send senior executives to provide us with some insight into the motives and objectives of multinational mining companies. Also

viii

from the private sector, we have arranged for a representative of a Sydney law firm to speak to us about legislative questions related to mining.

I am particularly pleased that we have been able to invite several participants who, because of their past involvement or specialized knowledge, have particular insight into the difficulties and problems associated with mineral and petroleum development. First, we are fortunate to have available to the conference the premier of the North Solomons province, who has been an instrumental figure in ensuring that the social and cultural issues associated with mine development have been prominently discussed at both the national and provincial levels. In addition, we welcome the North Solomons provincial planner who, as much as any man in the province, has had firsthand experience at meshing the day-to-day activities of the Bougainville mine with other socioeconomic policies. In an entirely different area, a consultant to the United Nations in New York has prepared an exhaustive study of mineral processing, and a petroleum economist at the East-West Center has prepared a summary of the energy and petroleum outlook for South Pacific countries.

As you can see, we have cast our net far and wide to bring together this group of people to share their specialized knowledge and insights with us. I hope all the preparations that have gone into the conference will yield a harvest of stimulating ideas and provocative interchange among us all. In a very real sense this conference will be exactly what we choose to make it, so I hope that we can all feel free to exchange our ideas openly and without reservation and, in so doing, come to a better understanding of the problems and promises that mineral development may hold for our nations.

Finally, I would like to recognize the special contributions that our joint sponsors, the East-West Center and the Commonwealth Secretariat, have made in making the conference possible. Not only have these organizations contributed financially and administratively to this meeting, but, of equal importance, their sympathy with our needs and concerns is clear evidence that the poorer nations of the Third World have allies in the developed countries who are willing to build bridges of support and understanding.

Thank you.

IX

Part I Geology and Economics

In its initial sessions, the conference dealt with the regional geology of the South Pacific island nations and with the economics of mining projects that could occur within these geologic settings. The opening paper by Ronald Richmond provides an overview of the geology of the region and of the relationship between metallogenesis and plate tectonics. Richmond combines these concepts to explain where economic mineral deposits occur or may occur in the southwest Pacific. In turn, the chief geologists of Papua New Guinea, (Kerry Doble), the Solomon Islands (Frank Coulson), Fiji (Howard Plum-mer), and Vanuatu (Alexander Macfarlane) presented papers containing detailed information on the geology and mineral potential of their respective countries. The last two papers in these initial sessions dealt with 1) the economics of developing various mineral resources in the region (Charles Johnson), and 2) the perception of risk in petroleum exploration combined with a comparison of alternative taxation regimes (Peter Freeman).

Given the substantial potential for finding commercial mineral deposits in the southwest Pacific, the session concluded that additional efforts should be made by the governments in the region both in exploration and in ensuring that modern, effective minerals legislation is developed among all four nations. Such legislation should encourage active minerals exploration while ensuring that the governments receive maximum benefit as a result of the development of their minerals potential.

Geology, Tectonics, and Mineral Potential of the Southwest Pacific (R. N . Richmond)

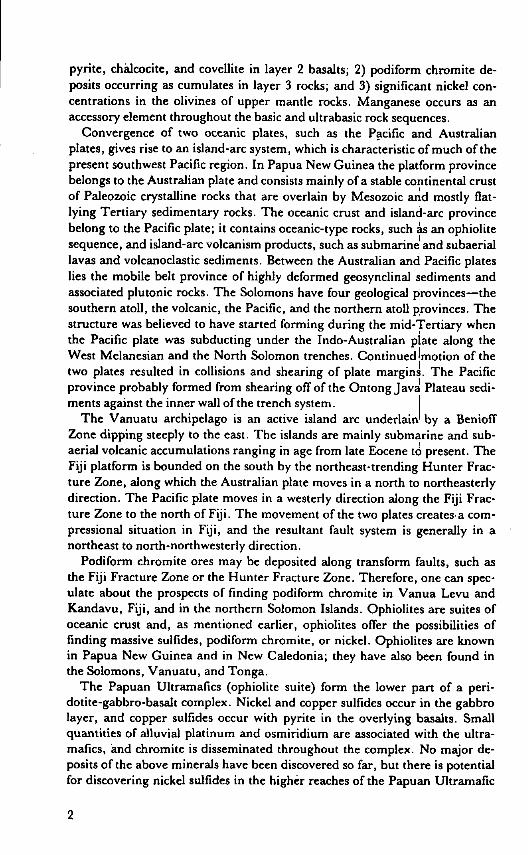

Many writers have proposed a connection between plate tectonics and the genesis of mineral ores and hydrocarbons (see Figure 1). For example, at the rifts along mid-ocean ridge crests, metalliferous sediments enriched in manganese, iron, nickel, copper, zinc, cobalt, and lead are deposited. These massive sulfide deposits are somewhat similar to ophiolite massive deposits on land. Within igneous rocks of layers 1,2, and 3 of the oceanic crust and the underlying mantle, metal-bearing assemblages may occur, such as: 1) massive sulfide deposits containing mostly pyrite but also some copper sulfides such as chalco-

1

pyrite, chalcocite, and covellite in layer 2 basalts; 2) podiform chromite deposits occurring as cumulates in layer 3 rocks; and 3) significant nickel concentrations in the olivines of upper mande rocks. Manganese occurs as an accessory element throughout the basic and ultrabasic rock sequences.

Convergence of two oceanic plates, such as the Pacific and Australian plates, gives rise to an island-arc system, which is characteristic of much of the present southwest Pacific region. In Papua New Guinea the platform province belongs to the Australian plate and consists mainly of a stable continental crust of Paleozoic crystalline rocks that are overlain by Mesozoic and mostly flat-lying Tertiary sedimentary rocks. The oceanic crust and island-arc province belong to the Pacific plate; it contains oceanic-type rocks, such as an ophiolite sequence, and island-arc volcanism products, such as submarine and subaerial lavas and volcanoclastic sediments. Between the Australian and Pacific plates lies the mobile belt province of highly deformed geosynclinal sediments and associated plutonic rocks. The Solomons have four geological provinces—the southern atoll, the volcanic, the Pacific, and the northern atoll provinces. The structure was believed to have started forming during the mid-Tertiary when the Pacific plate was subducting under the Indo-Australian plate along the West Melanesian and the North Solomon trenches. Continued Imotion of the two plates resulted in collisions and shearing of plate margins. The Pacific province probably formed from shearing off of the Ontong Java Plateau sediments against the inner wall of the trench system.

The Vanuatu archipelago is an active island arc underlain by a Benioff Zone dipping steeply to the east. The islands are mainly submarine and sub-aerial volcanic accumulations ranging in age from late Eocene to present. The Fiji platform is bounded on the south by the northeast-trending Hunter Fracture Zone, along which the Australian plate moves in a north to northeasterly direction. The Pacific plate moves in a westerly direction along the Fi j i Fracture Zone to the north of Fi j i . The movement of the two plates creates a com-pressional situation in Fi j i , and the resultant fault system is generally in a northeast to north-northwesterly direction.

Podiform chromite ores may be deposited along transform faults, such as the Fiji Fracture Zone or the Hunter Fracture Zone. Therefore, one can speculate about the prospects of finding podiform chromite in Vanua Levu and Kandavu, Fi j i , and in the northern Solomon Islands. Ophiolites are suites of oceanic crust and, as mentioned earlier, ophiolites offer the possibilities of finding massive sulfides, podiform chromite, or nickel. Ophiolites are known in Papua New Guinea and in New Caledonia; they have also been found in the Solomons, Vanuatu, and Tonga.

The Papuan Ultramafics (ophiolite suite) form the lower part of a peri-dotite-gabbro-basalt complex. Nickel and copper sulfides occur in the gabbro layer, and copper sulfides occur with pyrite in the overlying basalts. Small quantities of alluvial platinum and osmiridium are associated with the ultramafics, and chromite is disseminated throughout the complex. No major deposits of the above minerals have been discovered so far, but there is potential for discovering nickel sulfides in the higher reaches of the Papuan Ultramafic

2

MID-OCEAN RIDCE

(metal-rich exhalations; massive sulfide deposits)

TRENCH

(melange)

ISLAND A R C

(volcanics)

massive sulfides, podiform chromites

Kuroko-type Cu ores

mineralized 'copper porphyries

•50 km

0 ^

OO

LEGEND

oceanic lithosphere: basalt and gabbro

island arc volcanics

oceanic sediments (layer 1), metal-rich hori; at base ; fore-arc basin sediments

subduction melange: pillow lavas, basalts, glaucophane schists, and ultrabasic intrusives with chromite, nickel, asbestos, and ophiolites.

massive sulphides porphyries

granodiorites

fluids and light fractions from crust , melange, and mantle, partial melting "~'

\ ^ of the lithosphere,

150 km

Figure 1. Metallogenesis at mid-ocean ridge, trench, and island-arc areas.

Belt and for discovering more concentrated chromites and platinum minerals deposits in the area.

A number of pyrite-rich ophiolitic rocks (in the ultrabasic massifs) have been located in the Solomons. Other ophiolitic deposits include chromite sands on San Jorge beaches, pyritic copper on Santa Isabel, and some pyrites and chalcopyrites on Choiseul Island. Further exploration may lead to discoveries of other ophiolite-associated minerals, such as nickel sulfides and later-ites, chromite, pyrite-chalcopyrite, and platinum minerals.

On Vanuatu the ultrabasics are only exposed on Pentecost Island. Nickel only occurs in the soil profile, and minor amounts of cobalt, iron, chromium, and pyrite-chalcopyrite are present. A more comprehensive search for copper and nickel mineralization needs to be made on Pentecost and Maewo.

Perhaps the best known correlation between metallogenesis and plate tectonics involves porphyry copper deposits. These ores consist of zoned deposits of disseminated copper and/or molybdenum sulfides with associated hydro-thermally altered host rock. They typically occur with calc-alkaline rocks, such as andesites and diorites, and are closely tied with active or recently active sub-duction zones in the Pacific, Caribbean, and Alpine orogenic belts. Porphyry copper deposits are known at Bougainville and Ok Tedi in Papua New Guinea, in Guadalcanal, the Solomons, Namosi, Fi j i , and may well occur elsewhere in the southwest Pacific.

The southwest Pacific island arcs have gone through a number of changes in location through rotation, migration, back-arc spreading, and flipping of sub-duction directions. Therefore, it is necessary to determine the position of the island arc relative to the trench in order to determine whether porphyry copper mineralization fluids came up at the same time as calc-alkaline magma-tism occurred. There also appears to be a close space-time relationship between porphyry copper deposits, manganese ore deposits, and subduction zones. The manganese deposit at Forari on Efate Island probably formed from seawater leaching of the manganese from submarine andesitic pyroclastic sediments.

Most of the world's largest hydrocarbon fields seem to occur along plate margins. For the convergent margins of the southwest Pacific, the best potential areas would be the thrust-fault basins under continental slopes of island arcs adjacent to deep ocean trenches, and the block-fault basins in the marginal seas areas. Block-fault basins in the Asia-Pacific region generally occur on the landward side of andesitic volcanoes. Such basins could occur in Bligh Water, Fi j i , the Central Basin in Vanuatu, the Central Trough in the Solomons, and the Cape Vogel and New Ireland Basins in Papua New Guinea. Thrust-fault trends in continental margins are prospective for oil and gas accumulations because convergence between oceanic lithosphere and continental lithosphere can result in the thermal generation of hydrocarbons in sediments due to the rapid burial associated with subduction. Potential areas for such basins are the eastern Philippines, the southern margins of Indonesia, New Britain, and the Solomons. The Marianas, Vanuatu, Kermadecs, and Tonga should also have similar potential.

4

The evolution and advancement of plate tectonics theory has brought about new ideas concerning the reasons for metallogenesis around the world. As previously discussed, the potential for finding valuable mineral resources in the southwest Pacific is very high. The exploration interest is now strong in the region and will increase in the future. In order to ensure that the countries remain attractive for exploration and that mining companies come in on a platform of mutual respect and understanding of the host country's laws and customs, it is essential that the current mapping programs in these islands be continued until all the islands have been completed. The mapping programs are extremely useful for mining companies and also for regional urban and rural planning within the countries. Governments may also need to conduct geochemical sampling programs and perhaps some limited drilling on and publication of prospective areas to attract private companies to explore them. The establishment of a firm policy is no longer a disincentive to mineral exploration; companies prefer to see that a government's policies are stable and that they will be able to get a fair chance at achieving a reasonable return on their investment.

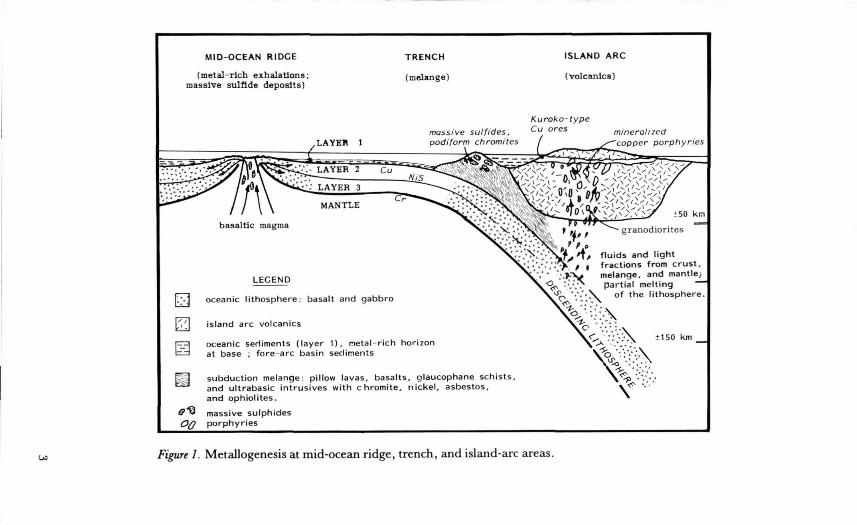

Regional Geological Mapping and Mineral Exploration Activity in Papua New Guinea (K. W. Doble)

The 1:250,000 geological map series covering Papua New Guinea is nearly complete. Al l the mainland sheets except for five in the southwest (areas where there are virtually no outcrops) are available either as preliminary editions (uncolored) or first editions (colored). First editions are also available for the main islands: Bougainville, New Britain, New Ireland, and Manus. A 1:100,000 mapping program was started in 1976 but may cease in 1982 unless arrangements can be made for technical aid.

Mineral exploration is fairly active despite a Prospecting Authority (PA) application moratorium since late 1980. Currently, there are 41 PAs in force throughout the country that cover an area of 41,500 square kilometers (sq km) (slightly less than 10 percent of the total land area), with an additional 27 PA applications outstanding. This is still far less than the peak in 1971 when there were 158 PAs that covered an area of more than 250,000 square kilometers. Mineral exploration in Papua New Guinea tends to be the domain of the large transnational miners such as Esso Papua New Guinea Inc., C R A Exploration Pty. Ltd. , and Goldfields Exploration Pty. Ltd. ; together these companies hold approximately 93 percent of the total land area under prospecting authority. National participation in the mining sector is limited to small-scale alluvial mining, which is reserved for national miners.

Although hampered by the current moratorium on PA applications, the 1980s should be an eventful period for Papua New Guinea's mineral sector. Construction of key infrastructure and the mine at Ok Tedi will begin soon. The mine is to be developed in stages with gold production commencing in 1984, copper concentrate production in 1989, and molybdenum concentrate production subsequent to that. The orebody at Porgera is estimated to have 50 million tonnes of 3 grams per tonne of gold. Negotiations between govern-

5

ment and the mining consortium early in 1982 are expected to set up a timetable for a full feasibility study and eventual mine development. Other prospective deposits (see Figure 2) are the chromite-lateritic nickel/cobalt deposit at Ramu, the porphyry copper-gold and massive sulphides deposit at Frieda, a porphyry copper deposit at Yandera, and the alluvial chromite deposits in onshore and nearshore beach sands at Morobe.

The Economic Geology of the Solomon Islands (F. Coulson) The Solomons form a primary fractured arc of seven major island groups

that form an en echelon double chain extending from Bougainville to San Cristobal. A discontinuous series of trenches flank both sides of the arc. The geology can be described in terms of three structural/stratigraphic elements:

• a basement of upraised ocean floor basalts and cognate intrusions of do-lerite and gabbro, with ultramafic bodies in axial regions. Except for Malaita, the basalts are fractured and variously metamorphosed to am-phibolite facies.

• a sedimentary cover, predominantly of greywacke and associated types, but with extensive Miocene and Pliocene reef development. Volcani-clastic sediments predominate from Pliocene times. This cover lies un-conformably on the basement and is up to 5,000 meters thick.

• calc-alkaJine volcanics forming andesitic cones and volcanic lithosomes and which attain their maximum development in New Georgia during Plio-Pleistocene times. Intrusive subvolcanic stocks occur on Guadalcanal and New Georgia.

Mineral occurrences form three broad categories by age and association: • Oceanic Basalt Association This comprises all occurrences within the pre-

Oligocene basement. It includes small veins and stockworks of copper sulphides found on most islands and Cyprus-type occurrences (Florida Islands). Manganese oxides form exhalative volcanogenic deposits (Florida, Santa Isabel). Gold occurs in the Guadalcanal gabbro and derived gravels where nuggets up to 16 grams are recorded. Gabbros on Santa Isabel contain pyrrhotite and copper and nickel sulphides. Nickel silicates, asbestos, and chromite occur in the ultramafic rocks including known reserves of 24 million tons of 1.3 percent nickel on Santa Isabel.

• Calc-Alkaline Association The andesitic volcanic and parent dioritic stocks of Guadalcanal and New Georgia contain several porphyry copper-type deposits including known reserves of 50 million tons of 0.2 percent copper at Koloula, Guadalcanal. Low-grade disseminations of copper sulphide occur in andesites and volcanic porphyries in these regions together with rare native copper and copper carbonates. Gold occurs at Gold Ridge, Guadalcanal, as a low-grade epithermal deposit where fracture fillings reveal gold contents in excess of 5-10 parts per million.

• Residual Deposits Included are important trihydrate bauxite deposits on Rennell and Waghena (55 million tons at 47-48 percent AI2O3,) which contain low silica, high phosphorus, organic carbon, and moisture. These deposits were brought to the mining feasibility stage in 1978 until the depressed alumina market terminated the project. Nickeliferous lat-

6

Figure 2. Mineral occurrences in Papua New Guinea.

erite caps most of the ultramafic rocks in the Solomons with large tonnages reported from Santa Isabel and San Jorge. Magnetite- and i l -menite-rich beach sands occur on most islands and the beach sands on San Jorge are also chromite-rich. Alluvial gold from the Gold Ridge areas of Guadalcanal is panned by local landowners who produced some 45,000 grams of gold in 1980. Up to 10.7 cubic meters of gold-bearing gravels are estimated to occur in this region, but gold values are erratic.

Hydrocarbons are not recorded in the Solomon Islands, but thick sedimentary accumulations offshore and the occurrence of buried Miocene reefs indicate some potential in the shallow shelf areas.

The tempo of mineral exploration in the Solomon Islands depends to a large extent upon the mineral investment climate in Australia. The 1960s and early 1970s represented a period of relatively intense prospecting; much of this was at the reconnaissance level although a few prospects were examined in some detail. Since that time, the tempo of prospecting activity has remained low.

The government's policy is to encourage mineral prospecting through a program of regional geological mapping and reconnaissance stream sediment geochemistry, and by the maintenance of geological information and advisory systems. The mining law vests minerals in the state and provides for the issue of a variety of prospecting and mining tenements.

Economic Minerals in Vanuatu—Known and Potential Resources (A. Macfarlane and J . Carney)

The Vanuatu archipelago, the subaerial expression of a northwest-southeast ridge of 200 kilometers average width, is bordered by the New Hebrides Trench to the west, and by the North Fiji Basin to the east (see Figure 3). The volcanics range in age from upper Oligocene to Recent and can be assigned to four separate provinces on the basis of age and composition: the western belt, the eastern belt, the central chain, and the marginal province. The western belt (Santo, MaJekula, and the Torres Islands) is an accumulation of submarine lavas and derived volcaniclastics of upper Oligocene to early middle Miocene age. Sedimentation of calcilutites, calcarenites, and mudstone/sandstone sequences followed in the Pliocene and Pleistocene. The oldest rocks in the eastern belt (Maewo and Pentecost) are terrigenous sediments and volcaniclastics that accumulated in the lower to early middle Miocene. Globigerina ooze and upper Miocene to lower Pliocene extrusions of submarine lavas were successively deposited. In the Pliocene major tectonism resulted in westerly tilting, anticlinal arching of the belt, and emplacement of an "ocean ridge-type" ophiolite complex. The central chain islands are a series of upper Pliocene to Recent volcanoes of mainly basic lavas. The marginal province is a volcanic belt of Plio-Pleistocene age. It is subaerially exposed on Futuna Island-

Given the present stat>: of geologic knowledge in Vanuatu, the mineral resources can be assigned to six categories: 1) sedimentary associations, 2) in-

8

9

dustrial raw materials, 3) geothermal energy, 4) porphyry-type mineral associations, 5) ophiolite associations, and 6) offshore minerals. The first three types are known resources in that they have already been evaluated. The latter three are potential resources as they are still in the process of evaluation.

Manganese (Mn) at Forari Mine on the east coast of Efate was, until recently, the only mineral exported from Vanuatu. The deposit occurs as a to-dorokite and is of supergene origin, derived by leaching during weathering of the Pliocene acid tuffs in the interior of Efate. Opencast mining began in 1962 and peaked in 1965 with production that year of 71,401 tonnes. Production gradually declined since then, and the mine has been nonoperational since November 1978 due to low world prices and increasing extraction costs. Other substantial manganese deposits occur on Erromango. The northwest deposit occurs as concentrations within lagoonal sediments and contains an estimated 600,000 to 1,800,000 tonnes at 35 percent M n . The southwest deposit occurs within clay deposits on a Pleistocene terrace. Reserves are estimated at 9.6 million tonnes at 8 percent M n .

Industrial raw materials minerals include heavy mineral sands, limestones, and pozzolan. Black sands on several of the islands contain appreciable amounts of magnetite, derived from the erosion of volcanic rocks. Significant deposits occur in southwest Efate, east Erromango, and south Santo with 173,000, 128,000, and 1,151,000 tonnes of magnetite, respectively. Limestones occur on many of the islands; some are chemically very pure and may be suitable for metallurgical purposes. At present, however, they are utilized only as a source of road dressing and building aggregate. Pliocene tuffs and breccias on Efate and Pleistocene to Recent andesitic pyroclastics on Tanna are known to have good pozzolanic properties.

Vanua Lava, Efate, and Tanna are the principal islands that have geothermal energy potential. The most extensive geothermal feature, "Frenchman's Solfataras," covers an area of about 5 square kilometers of the flanks of M t . Soretimeat on Vanua Lava. On Efate, the main concentrations of thermal springs are at Takara on the northeast coast and within the Teuma Graben in the center of the island. Hot springs, geysers, and fumaroles occur along a recently active fault which forms the western shore of Port Resolution in southeast Tanna.

The western belt islands of Santo and Malekula are part of a chain of Mio cene calc-alkaline volcanics. This feature is known to contain large porphyry copper deposits, for example, such as Bougainville in Papua New Guinea and Namosi in Fi j i . Sulphide mineralization (90 percent pyrite, 10 percent chalco-pyrite) is confined to basaltic, andesitic, and dioritic intrusions that were em-placed in early Miocene volcanics. Three types of mineralization can be recognized—disseminated, vein, and skarn mineralization. Geochemical surveys by mining companies during 1968-1975 have failed to locate major near-surface orebodies of economic potential.

Copper and iron sulphides have been found associated with ophiolite suites; the pre-middle Miocene ophiolites occur in south Pentecost. Offshore minerals include hydrocarbons, metalliferous muds, and precious coral. Explora-

10

tion for offshore minerals is very much at the reconnaissance stage and is being carried out as part of a United Nations Development Program (UNDP) funded regional project on behalf of C C O P / S O P A C member countries.

The mining legislation currently in operation in Vanuatu was enacted in 1957. A l l minerals defined therein are vested in the state; the definition does not include industrial minerals, geothermal energy, or offshore minerals. It is the intention of the government to bring the present regulation up to date with more modern legislation that will cover all areas of mineral exploitation both on land and offshore.

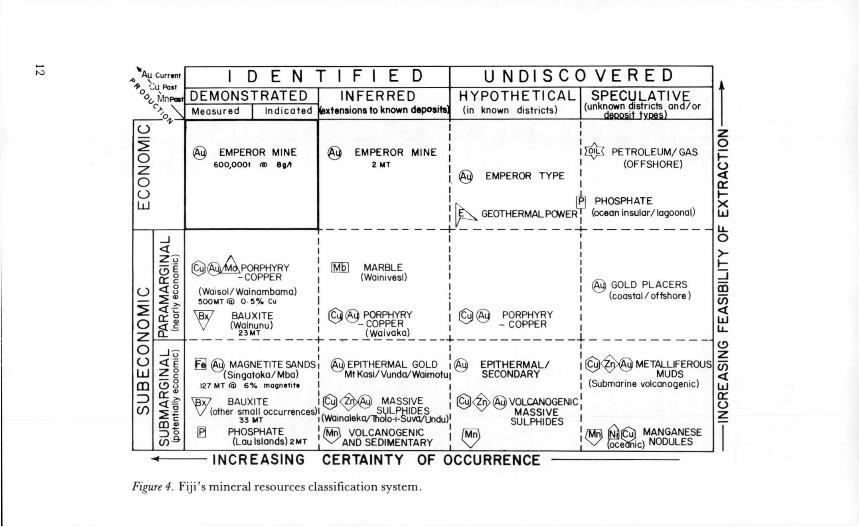

Minerals Development Policy and Resource Classification: Fiji Case Study (D. Greenbaum and H . G . Plummer) Mineral Resources. Fiji has a history of mineral exploration extending back to the last century. Mining for gold, manganese, and base metals has taken place. A summary of Fiji 's mineral resource potential is shown in Figure 4, which is an adaptation of the McKelvey box classification.

The Emperor Gold Mine at Vatukoula is the country's only operating mine with demonstrated economic reserves of about 600,000 tonnes at an average grade of about 8 grams of gold per tonne. In addition, approximately 500,000 tonnes will be available upon eventual mine closure. Inferred extensions of Emperor-type mineralization may exist in the mine environs. Other epithermal gold occurrences have been explored in recent years, corresponding to various entries on Figure 4 under inferred and hypothetical submarginal deposits.

Apart from precious metals, Fiji possesses deposits of both porphyry copper and volcanogenic massive sulphides. The principal porphyry deposit occurs at Waisoi Creek where the indicated resource is 475 million tonnes of 0.48 percent copper ore, plus recoverable gold and molybdenum. Prefeasibility investigations have shown that this deposit is paramarginal at the present low copper price. Other porphyry deposits in the area are poorly known but may be regarded as inferred paramarginal resources.

Various other subeconomic mineral resources are shown in Figure 4. These include deposits of bauxite (demonstrated paramarginal and submarginal), magnetite sands (demonstrated submarginal), massive sulphides (inferred and hypothetical submarginal), and marble (inferred paramarginal). Speculative and hypothetical resources include offshore petroleum/gas, geothermal power, gold placers, metalliferous muds, and manganese nodules. Development Policy. For smaller less developed countries (LDCs) such as Fi j i , the considerable financial risks associated with mineral exploration, and the lack of technical expertise, finance, and possibly access to markets needed to develop a mineral discovery, make it both necessary and desirable to encourage the early involvement of mining companies. Therefore, policies should seek to promote private sector interest by providing a suitable climate for exploration and investment. A fair return to investors should be offered in return for the early and efficient development of the country's mineral resources.

O f fundamental importance in stimulating company interest is a data base of essential geological information. This should at least include regional and

11

Au Current 0 s

°o MnpRM

o

o

UJ

o

O z

o

o

UJ m

3 (/)

81 < S I*

< E

c5 8

P CD ® 3 ° c75^

I D E N T I F I E D D E M O N S T R A T E D Measured Indicated

I N F E R R E D Intensions to known deposits]

EMPEROR MINE 600,0001 <2D QqA

U N D I S C O V E R E D H Y P O T H E T I C A L (in known districts)

S P E C U L A T I V E (unknown districts and/or

deposit ty.ftaai

@ EMPEROR MINE 2 MT

PORPHYRY COPPER

(Waisoi/Wainambama) 500MT © o 5% Cu

BAUXITE (Wainunu)

2 3 M T

g @ MAGNETITE SANDS (Singatoka/Mba)

127 MT (a) 6Vo magnttitt

BAUXITE (other small occurrences)

33 MT

@ PHOSPHATE (Lau Islands) 2 M T

(MS MARBLE (Wainivesi)

(Cul (ftu) PORPHYRY COPPER (Waivaka)

ku) EPITHERMAL GOLD Mt Kasi/Vunda/Waimotu

Au) MASSIVE SULPHIDES

(Wainaleka/ThoTo-i-Suva/undu) (Mn) VOLCANOGENIC ^ A N D SEDIMENTARY

EMPEROR TYPE

GEOTHERMALPOWER

PORPHYRY - COPPER

(Au) EPITHERMAL/ ^ SECONDARY

£u)<£n> (fch VOLCANOGENIC ^ MASSIVE

SULPHIDES (Mn

^ P E T R O L E U M / G A S (OFFSHORE)

PHOSPHATE (ocean insular/ lagoonal)

@ GOLD P L A C E R S (coastal/offshore)

[CuJ<Zri><Au) METALLIFEROUS MUDS

(Submarine volcanogenic)

/Mn} M ^ U ] MANGANESE V Seafic) NODULES

INCREASING CERTAINTY OF OCCURRENCE

Figure 4. Fiji's mineral resources classification system

detailed geological maps and accompanying bulletins, and should ideally aim to include reports on geochemical, geophysical, and mineralization studies. In Fi j i , 1:50,000 geological maps and reports are available for most areas, as well as 1:250,000 metallogenic maps and the results of a regional stream sediment and an aeromagnetic survey. Fiji has also built up an economic geology data bank containing roughly 450 volumes of company reports and other information covering past exploration work. This data is fully catalogued and indexed and is available for open-file reference at the Mineral Resources Department.

Once private sector mineral exploration proceeds, it is essential to obtain full information on the work done. Whereas any one survey may fail in its primary goal of discovering economic mineralization, the eventual discovery of an orebody may depend on the successive exploration programs of several companies, each building upon the results of previous work. In Fiji all prospecting licences require the submission of an annual geotechnical report containing full details of work done and results achieved. This data is used to monitor and guide ongoing exploration programs, and eventually may be added to the government open-file data bank if and when the licence is terminated. The data storage/retrieval system used need not be complex: all too often elaborate systems created by expatriates become obsolete after these staff members leave.

Beyond the need to provide basic geological information, private sector interest is encouraged by political stability, a realistic fiscal/tax regime, well-informed and aware decision makers, and an up-to-date legislative framework operated by an adequately staffed and efficient administration capable of timely response. In essence, investors need to feel confident that the circumstances and attitudes of a country are such that it would be worthwhile to develop a mineral deposit if one is discovered.

Despite such generalizations, the success or otherwise of a minerals policy ultimately can only be judged in regard to a host of local factors relating to an individual country's particular aims and aspirations, including alternative development opportunities. This fact should be borne in mind by smaller L D C s when receiving advice from outside advisors.

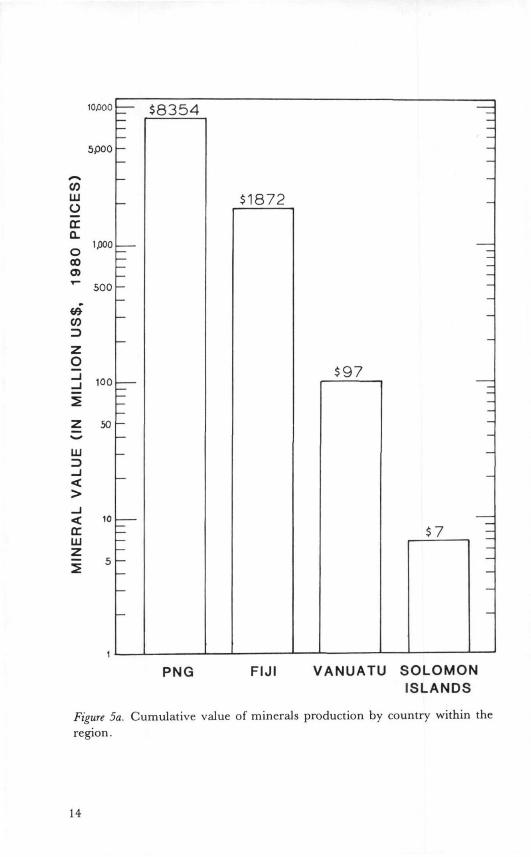

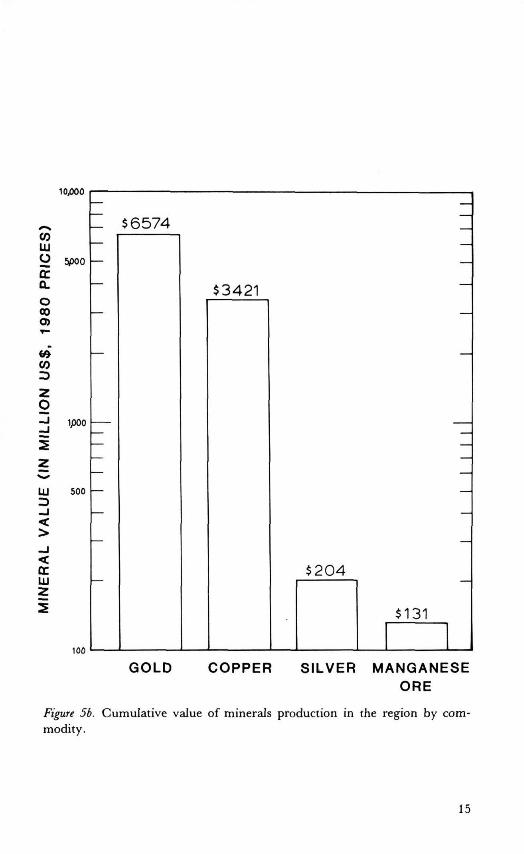

Economics of South Pacific Minerals Development (C. J . Johnson) The geology and geologic history of Fi j i , Papua New Guinea, the Solomon

Islands, and Vanuatu (hereafter referred to as the region) is conducive to the formation of major commercial mineral deposits, including bauxite, copper, nickel, gold, chromite, and possibly petroleum, as well as a number of minerals of lesser importance such as magnetite sands, manganese, and phosphate. The goal of the paper is to provide an indication of the size and relative economics of various mineral resource developments that are taking place or may take place in the region. This information may be particularly useful to government decision makers who must establish mineral policies and develop long-term strategies to ensure that their nation receives the maximum benefits from the development of its mineral resource potential.

To date, commercial production of copper, gold, silver, and manganese has

13

10.000

5p00

CD LU o E CL O CO

CD CD ZD

1JD00

500

50 h-

LLI ZD _ l < >

< LU

— $ 8 3 5 4

$ 1 8 7 2

$ 9 7

10

5h-

$ 7

1 4 1 — •

PNG FIJI VANUATU SOLOMON ISLANDS

Figure 5a. Cumulative value of minerals production by country within the region.

14

10,000

2 5poo

L $ 6 5 7 4

ipoo

LU 500

100

$ 3 4 2 1

$ 2 0 4

$ 1 3 1

GOLD COPPER SILVER MANGANESE ORE

Figure 5b. Cumulative value of minerals production in the region by commodity.

15

produced a cumulative value at 1980 prices of approximately 10 U.S . billion dollars, or roughly one-third of the value of recoverable metals in known commercial mineral deposits in the region. Figure 5a shows the total cumulative value to 1980 of all metal commodity production by country, and Figure 5b shows the cumulative value by metal commodity.

Papua New Guinea accounted for about 81 percent of the value of production at 1980 prices, followed by Fiji with 18 percent, Vanuatu with 1 percent, and the Solomon Islands with about 0.1 percent. Ranking production by commodity at 1980 prices as shown in Figure 5b places gold in first place with about 64 percent, followed by copper with 33 percent, silver with 2 percent, and manganese with 1 percent. Had historical prices been used, the prominent position of gold would be substantially reduced.

Al l four South Pacific countries have potential for commercial deposits. Table 1 shows the estimated prices required to induce development of large mines in the South Pacific at 1980 prices. Although the figures are rough and represent a hypothetical mine, they indicate that commercial investments in large copper, nickel, or aluminum operations are unlikely unless there are substantial increases in metal prices. The price situation in early 1982 was even worse than in 1980.

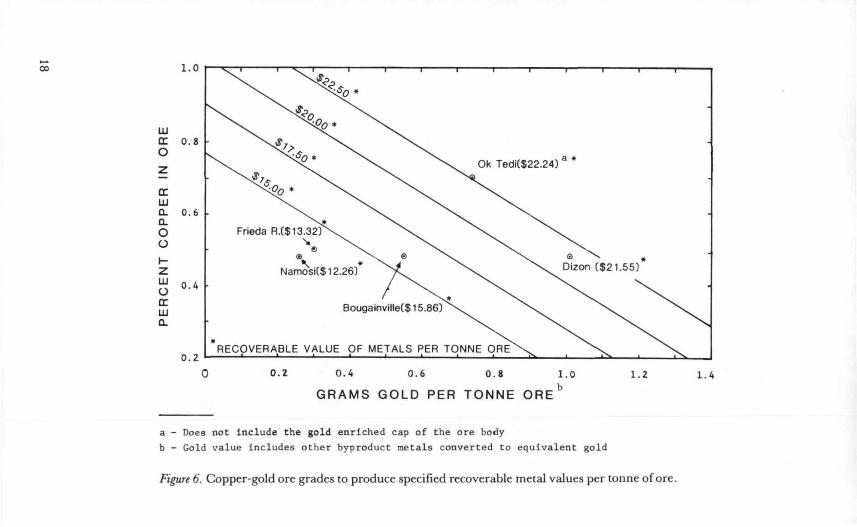

At present prices the most likely commercial metal deposit is a copper porphyry rich in byproducts (usually gold in the South Pacific). Figure 6 illustrates the combination of copper and gold grades that are required to produce a viable deposit—assuming economic viability will be achieved for ores having a recoverable metal value of US$15.00, US$17.50, US$20.00, or US$22.50 per tonne ore. Plotted in Figure 6 are the reported average metal values of four copper porphyries from the South Pacific, plus the Dizon mine in the Philippines. Today, a porphyry ore must have a recoverable metal value of approximately $20.00 per tonne to warrant serious consideration for commercial de-

Metal

Copper 1

Nickel 3

Aluminum 3

Table 1 Prices Required to Induce Commercial

Development of Mines in the South Pacific

USS/pound in 1980 prices (excluding byproduct

credits)

1.45

6.05

0.90

US$/pound in 1980 prices (including byproduct

credits)

1.20

5.25

0.90

Estimated 1980 prices

in US$/pound

0.99

3.00

0.72

'Copper from a large porphyry, assume an average of $0.25 in byproduct metals. 2Nickel from a laterite deposit, assume an average of $ 1.20 in cobalt byproducts. 3AJuminum price includes mining, refining, and smelting with no byproduct credits.

16

velopment. Typical copper porphyries in the South Pacific have a grade of about 0.5 percent copper; therefore, to produce a $20.00 per tonne ore in Figure 6 it is necessary to have 0.8 to 0.9 grams of gold per tonne.

Papua New Guinea, with 90 percent of the land area, more than 80 percent of the minerals production, and probably the majority of the remaining minerals potential in the region, continues to receive most of the region's private sector exploration activity. The current state of relatively low exploration interest in the Solomon Islands and Vanuatu is probably due to a combination of factors, including a general downturn in exploration activity in developing countries, lack of past exploration success, and uncertainty about the terms for development of commercial discoveries. The potential for commercial mineral deposits is reasonably good; however, government assistance in a number of areas is important to increase the chances of commercial discoveries and developments that are compatible with long-term economic development goals.

The following recommendations are suggested: • High priority should be given to private sector petroleum exploration

even though the chances-of discovery are considered relatively low in Fi j i , the Solomon Islands, and Vanuatu. The potential remains largely untested. However, companies are willing to explore, and a commercial discovery could generate government revenue equal to a large copper mine.

• A shift in government attention to greater emphasis on economic geology activities appears warranted. Work is needed to better understand the regional distribution and geologic associations of copper, gold-silver, molybdenum, nickel, and cobalt. Regional comparisons should extend at least to the four countries and perhaps to Indonesia and the Philippines.

• Although low-cost energy is not a panacea for the region's mineral development problems, it can act as a catalyst to attract interest in possible minerals development and processing in the region. Each government's long-range energy strategy should include assessment of the potential of tow-cost energy.

• Small-scale mining activities present special problems needing government assistance. A technical and economic review of the small-scale mining potential and problems should receive medium priority.

• Clues to the next commercial mineral discovery in each of the South Pacific countries are probably already sitting in government files. With respect to most developing countries, only a small percentage of the geologic information collected is effectively used. Put another way, our geologic archives probably already contain information that will guide geologists to the ore deposits that will be explored in the foreseeable future. Therefore, a review of data collection, analysis, and storage activities is warranted to ensure that valuable information is not being overlooked.

• There appear to be many similarities in problems among the four South Pacific countries reviewed here. Al l governments must deal with similar economic geology problems, some of the same companies, data han-

17

G R A M S G O L D P E R T O N N E O R E b

a - Does not i n c l u d e the gold e n r i c h e d cap of the ore body b - Gold v a l u e i n c l u d e s o t h e r byproduct metals c o n v e r t e d t o e q u i v a l e n t g o l d

Figure 6. Copper-gold ore grades to produce specified recoverable metal values per tonne of ore.

dling, problems of ineffective legislation and regulations, problems of small mines, and the problems associated with conflicts between mining interests and traditional attitudes of the people toward their land. Working together, the four governments should be in a stronger position to define the problems and find workable solutions. It is worth considering the establishment of a formal cooperative network for mineral policy and analysis among the four countries. This might lead to the future establishment of, say, a South Pacific Regional Center for M i n erals Policy, Data Collection, and Analysis. A regional focus on mineral problems and the sharing of the cost of experienced expertise might benefit all countries and facilitate more efficient management of the region's mineral resources.

Perceptions of Risk in Petroleum Exploration (P. Freeman) The purpose of this paper is to assist those governments that are facing for

the first time the problems of establishing policies and negotiating agreements to govern the exploration and production activities of petroleum companies. The objective of such policies and negotiations is to secure substantial commitment of corporate funds for exploration while, at the same time, ensuring that corporate returns in the event of success represent no more than a fair reward for the risks taken.

The concept of fairness employed is not a moral one but rests on the assumption that investors will only commit funds if they expect to be better off by doing so. A framework of analysis is constructed in which the investor's expectation is defined in relation to expected internal rates of return.

The paper traces the typical development of a company's interest in a new exploration area from its origins in geological evaluation, through a general consideration of the business environment, to a detailed assessment of the balance between the risks and the potential rewards associated with an exploration program.

On the government's side, the paper considers some of the key questions in the formulation of policy such as state participation (How much? On what terms?); the typical elements of a financial regime (land rental, royalty, income tax, special profits taxes, cost recovery, and profit-sharing provisions); and the structure of agreements to govern petroleum exploration and production activities (production-sharing agreements and tax-based concession agreements). The functions of individual policy components and the interrelationships between them are considered first in general qualitative terms and second in specific quantitative terms by reference to some hypothetical but detailed calculations.

The calculations illustrate the case of a negotiation between a company and a government, utilizing the framework for risk analysis previously established. Hypothetical (but reasonable) parameters are attached to the specification of the target discoveries and to the subjectively-judged probabilities of discovering them. The evaluation of each target discovery is given for each of three different forms of a production-sharing agreement that could emerge from a negotiating process. The results derived from making each discovery are then

19

combined with the possibility of an abortive exploration program in order to calculate expected risk-adjusted rates of return under each form of the production-sharing agreement.

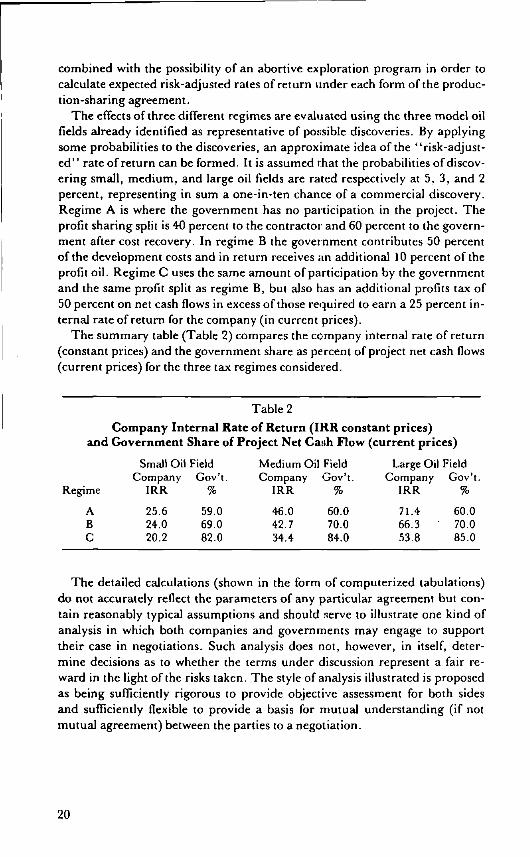

The effects of three different regimes are evaluated using the three model oil fields already identified as representative of possible discoveries. By applying some probabilities to the discoveries, an approximate idea of the "risk-adjusted" rate of return can be formed. It is assumed that the probabilities of discovering small, medium, and large oil fields are rated respectively at 5, 3, and 2 percent, representing in sum a one-in-ten chance of a commercial discovery. Regime A is where the government has no participation in the project. The profit sharing split is 40 percent to the contractor and 60 percent to the government after cost recovery. In regime B the government contributes 50 percent of the development costs and in return receives an additional 10 percent of the profit oil . Regime C uses the same amount of participation by the government and the same profit split as regime B, but also has an additional profns tax of 50 percent on net cash flows in excess of those required to earn a 25 percent internal rate of return for the company (in current prices).

The summary table (Table 2) compares the company internal rate of return (constant prices) and the government share as percent of project net cash flows (current prices) for the three tax regimes considered.

Table 2 Company Internal Rate of Return (IRR constant prices)

and Government Share of Project Net Cash Flow (current prices)

Small Oil Field Medium Oil Field Large Oil Field Company Gov't. Company Gov't. Company Gov't.

ime IRR % IRR % IRR %

A 25.6 59.0 46.0 60.0 71.4 60.0 B 24.0 69.0 42.7 70.0 66.3 • 70.0 C 20.2 82.0 34.4 84.0 53.8 85.0

The detailed calculations (shown in the form of computerized tabulations) do not accurately reflect the parameters of any particular agreement but contain reasonably typical assumptions and should serve to illustrate one kind of analysis in which both companies and governments may engage to support their case in negotiations. Such analysis does not, however, in itself, determine decisions as to whether the terms under discussion represent a fair reward in the light of the risks taken. The style of analysis illustrated is proposed as being sufficiently rigorous to provide objective assessment for both sides and sufficiently flexible to provide a basis for mutual understanding (if not mutual agreement) between the parties to a negotiation.

20

Part II Legal Issues

In its second series of meetings, the conference examined various legal issues associated with mining and petroleum development. David Frecker, a private Australian solicitor, and Carl Dundas of the Commonwealth Secretariat, outlined the policy questions to be addressed in modern mining legislation. In addition to suggesting particular legislative problem areas, the speakers noted a range of solutions adopted in other developing countries. In their presentations, both Frecker and Dundas suggested that while modern legislation is generally directed at a common set of problems, each nation must choose those provisions that best express national attitudes toward resource development. Thus, while a set of model questions was presented to guide legislative draftsmen, no single set of provisions is universally applicable to Pacific countries.

Stuart McGi l l of the Papua New Guinea Department of Justice described the major elements in investor agreements. McGi l l outlined the interaction between a general legislative framework set out in relevant statutes (e.g., on taxation, mining, land, and labor) and negotiated arrangements between the investor and host government that reflect the character of individual projects.

Minerals Legislation: The Relevant Legislative Questions and Options (D. C . Frecker)

Minerals legislation is a compromise between competing interests; in particular the people who wish to explore for and develop mineral resources, the owners of the mineral resource, the owners of the land on which the minerals are located, and the state or government as guardian of the public and national interest. The scope of such legislation is principally determined by the term "minerals"; minerals are commonly dealt with separately from petroleum. In order to provide a separate licensing regime for certain types of substances, separate definitions may also be included of building minerals and industrial minerals.

Modern minerals legislation in a developing country should be based on the principle that the state owns the minerals in the ground, and that the minerals should be developed in the national interest and for the well-being of the peo-

21

pie. The state, as owner of the minerals, should provide a licensing system permitting and controlling access to those minerals by using minerals legislation. A three-tiered licensing system is recommended under which there would be the following:

1. reconnaissance licences permitting exploration for minerals using remote-sensing techniques and surface geology over a wide area,

2. prospecting or exploration licences granted over a much smaller area allowing the licensee to carry out specific exploration work, and

3. mining licences allowing the licensee to mine and remove the minerals found in an identified ore body.

Building various elements into the minerals legislation and administration of a country may enable the government to exercise proper control over exploration and ensure that active exploration programs are carried out. Some of these elements include the area and the term of licences, work programs and minimum expenditure requirements, auction or bidding systems, and reporting requirements.

Mining companies want assurances that they will continue to have rights over an area where they do exploration work and discover minerals or identify an orebody, whereas governments want maximum discretion to ensure that their resources are being investigated and developed in the most expeditious and economic manner. These interests are diametrically opposed and minerals legislation must provide for a compromise. This becomes critical at four points:

• upon application for renewal of an exploration or prospecting licence, • at the point of transition from an exploration or prospecting licence to a

mining licence, • upon application for the renewal of a mining licence, and • in circumstances in which there has been a breach of the conditions of

the licence that may lead to suspension or cancellation.

Minerals legislation usually provides that any assignments or dealings in l i cences are subject to approval of the minister or other issuing authority. This is an important control for a government but should be exercised judiciously so as not to become an unnecessary impediment upon normal commercial transactions. Companies often need to deal with exploration and mining rights as they endeavor to match their commitments with their financial resources. The best way for a government to keep track of such dealings is for the legislation to provide for registration of such rights and interests therein.

The purposes of exploration and development of mineral resources inevitably conflict with the rights of landowners. Each country must determine the extent to which one is allowed to prevail over the other, especially in the matters of compensation for landowners and occupiers, compulsory acquisition of land for mining purposes, and the restoration of land after mining ceases.

The following financial provisions are usually found in minerals legislation: • fees charged to persons applying for or holding licences,

22 '

• royalties payable to governments on mineral resources extracted from its territory, and

• surface rent or occupation fees (which are not generally recommended).

Many of the issues and solutions covered by petroleum legislation are similar to those in mining legislation, but there are a few significant differences. Petroleum is a mobile material that can be recovered without large excavations or other vast disruptions of the environment, and so, land and property rights are not major issues. The high value of petroleum makes it important for governments to facilitate its rapid development, and thus greater incentives and better security of tenure are offered to licensees. The economic evaluation of a petroleum potential is easier to determine than a hardrock mineral potential. Thus, development licences can have fairly fixed development periods.

Petroleum: Current Legal Issues—The Challenge of Choice for Non-Oil-Producing Developing Countries (C. W . Dundas)

The dramatic escalation in oil prices in recent years has caused many non-oil-producing developing countries to reassess the development strategy for their petroleum potential. In this regard, it is important for such developing countries to create a realistic legal environment that will serve to protect their interest, while at the same time placing no undue fetters on the investment needed to carry out exploration programs. Many developing countries have found it necessary to undertake the task of designing a suitable legislative framework within which proper petroleum exploration activities can take place. The non-oil-producing developing countries should be made, aware of the policy options that are possible in the area of legislative framework for petroleum development.

There are three popular approaches available to non-oil-producing developing countries wishing to introduce an operational legislative scheme to regulate their petroleum exploration activities. Petroleum legislation may be designed to provide a mere framework, to cover all possible contingencies and details that arise in the course of exploration or production, or to stipulate the provisions governing the majority of issues but may leave a few important ones for settlement by negotiation. Practice has shown, though, that contractual arrangements are more frequently used as the legal vehicle for the creation of the legal relationship between the investor (oil company) and host country. For those non-oil-producing developing countries that do not have the expertise or experience to conduct keenly-contested negotiations, a carefully designed legislative scheme will undoubtedly improve their ability to conclude more favorable contractual arrangements for themselves with oil companies.

There are several contractual forms presently available to a developing country that desires to conclude a petroleum agreement with an oil company. Many of these forms of petroleum agreements have emerged from a gradual process of improvement through the efforts of the developing countries in or-

23

der to provide better terms and conditions for themselves. Viewed in an historical perspective of the concessional arrangements that dominated the oil industry until about two decades ago, the current popular forms of petroleum agreements are aimed at improving the general position of the host country. These contractual forms include the production-sharing contracts, service contracts, and joint venture arrangements. The effectiveness of a petroleum agreement depends largely on such issues as the following: duration of the agreement and size of area covered thereunder, allocation of blocks for exploration and development, exploration strategies, determination of commercial discoveries, information access and confidentiality, host country participation and role in management and control, access to petroleum by the oil companies, choice of law and settlement of disputes, natural gas development, training and employment, and territorial jurisdiction questions.

An acceptable solution can be found to the problem of designing a petroleum agreement that takes adequate account of the interests of and risks assumed by the oil company, while at the same time preserving for the non-oil-producing host country the enjoyment of fair financial returns in the event of a commercial discovery of petroleum. In addition, the new contractual forms of petroleum agreements are capable of housing various legal devices that enhance the stability of the legal and economic relationship created between the oil company and the host country.

Non-oil-producing developing countries have a relatively wide choice of policy options for legislative designs and forms of contractual agreements. The practice of some oil companies, however, tends to suggest that some of these countries could have their options arbitrarily affected in an adverse manner by being given too high a rating on the political risk chart as perceived by the companies concerned.

Some Issues for Governments When Formulating Mineral Agreements (S. McGil l )

The actual form of the agreement, whether it be a concession agreement, a production-sharing agreement, a service agreement, or a development agreement, should not be overemphasized, as aspects of these formats can be included in any agreement. In particular, the stance that a government takes on several legal-economic issues within the agreement has as much or more influence on the nature of the agreement. These issues need to be considered by governments and are addressed in this paper in the following order: agreements as acts of parliament; issues of timing; equity and risk exposure; infrastructure arrangements; currency availability undertakings; and termination, force majeure, and arbitration.

Agreements as Acts of Parliament Mining companies want agreements enacted in order to create a legal enclave for themselves. The advantage of enactment for a government is that it is not necessary to review other, possibly inappropriate, laws, although this can lead to a lack of uniformity between projects and the general law. The best solution is to update laws particularly relevant to

24

major projects and to keep agreements to a minimum on such issues. When agreements are enacted, attention should be paid to avoiding legal conflicts that arise if the agreement purports to fetter an executive discretion as to whether a right should be granted. Also, preventions should be taken regarding any suggestion that future governments cannot change an agreement (bilaterally or otherwise) due to entrenchment by a so-called "manner and form" provision in the statute.

Issues of Timing The chronological structure of a mineral agreement should reflect the various decision points for each of the parties and the things to be done at, and between, each such turning point. The parties usually decide to enter an agreement after prefeasibility studies in order that governments can have some assurance of, and control over, work done, while allowing companies to obtain some rights to develop the potential project. This is thus the point at which the clock starts running, and thereafter time periods should be practical and relative to the weight of the matters being considered, while being sufficiently demanding to ensure that the respective organizations implement the project with a minimum of delay. A suggested timetable that has been devised for the Papua New Guinea standard mining agreement is set out in Table 3.

Equity and Risk Exposure In discussions of the advantages and disadvantages of equity participation, little attention has been paid to the problem of minimizing risk exposure and the bearing this can have on whether or not to be an equity participant. As well as providing equity funds, a government will normally be required to provide loan support and appropriate contributions to any overrun financing. This is usually embodied in a shareholder's agreement, which means a government may have the unpalatable option of either making infinite financial contributions or facing a penalizing equity dilution. The ideal solution to this problem is to provide in the development agreement

Table 3 Proposed Timetable for Mining Agreements

in Papua New Guinea

Consecutive Time Periods Process

2-5 years Feasibility 'study and presentation of proposals and land applications by developers

4 months Consideration of proposals and their approval by the government

6 months Submission of financing and marketing strategy 2 months Approval of such strategies and government's election

regarding equity 2 months Creation of mining organization 6 months Grant of land

25

that all loan support is to be met by the developers. Overrun Finance above the financing plan limit shall also be the responsibility of the developers, with any additional equity being provided as nonvoting redeemable preference shares.

Infrastructure Arrangements Given that mining agreements now provide that developers construct all necessary infrastructure at their own expense, care must be taken to define when and where that responsibility ends so as to avoid the government having to meet hidden costs. In order to avoid later recriminations, socioeconomic services that are likely to be provided to the local people by the developers should also clearly be the developer's responsibility. Where priority use of infrastructure is granted to the developers, they should be required to provide sufficient capacity to ensure that they have no de facto exclusive use of such infrastructure. Bearing in mind that there are some advantages for the project when the government provides some infrastructure f i nance, any such provision should be via a user charge agreement. Such an agreement was used to fund the construction of the access road to the Ok Tedi project in Papua New Guinea. Lastly, third parties using a project's infrastructure should not be required by existing developers to contribute to initial capital costs so as to allow an advantage to other, possibly subeconomic projects.

Currency Availability Undertakings In order to retain autonomy with respect to fiscal and monetary policies, government should not grant developers an automatic right of capital remittance. Nevertheless, recent research indicates that many governments have already compromised themselves on this issue. A suggested position is that rights only be granted to allow foreign currency from export sales to meet payments with respect to dividends, current goods, and services and loan repayments. Fall-back positions on capital remittance include allowing the creation of a foreign currency account within the country and allowing capital repatriation at a steady rate over a long period.

Termination, Force Majeure, and Arbitration A qualification upon the normal termination provisions (by default, the project: becomes the property of the government) is to agree that a receiver and manager have the opportunity to either restore project cash flow or sell it as a going concern. Such a provision enhances the prospect of obtaining project financing. Finally, arbitration is not cheaper or quicker than litigation, although it is confidential and experts can be utilized. The International Centre for the Settlement of Investment Disputes (ICSID) and the United Nations Commission on International Trade Law ( U N C I T R A L ) rules appear to offer the best avenue of arbitration to governments.

26

Part III The Implementation Context:

Internal and External Influences

In the concluding sessions of the conference, discussion focused on the evolution of projects through the exploration, feasibility, construction, and operational stages and described how external factors such as investor perceptions and the world energy outlook might influence project decisions. Emphasis was placed on the changing nature of policy concerns and investment priorities and on the manner in which early feasibility assumptions and interpretations changed as projects moved toward commercial production.

The opening presentation by Sam Pintz examined environmental, technical policy, and manpower questions within the context of the Bougainville and Ok Tedi projects in Papua New Guinea. Nigel Agonia then described the arrangements necessary to acquire land for mining purposes in Papua New Guinea and suggested various compensation schemes that had been negotiated with landowners. Following Agonia's presentation, the premier of Bougainville province, together with Agonia and other members of the provincial government, participated in a panel discussion on the social impact of mining and the reaction of local residents to development of the Bougainville copper mine. These discussions provided conference participants with useful insights into the differences in perception between the national and provincial governments, and how these differences might be resolved.