equity instruments & markets

TRANSCRIPT

Equity Instruments & Markets B40.3331

Valuation Project

Date due: December 13, 2004

Summary Recommendations

Company Price DCF Valuation Relative Valuation Option EVA in RecommendationModel Used Value Multiple Used Value Valuation last year

Pixar 83.98$ FCFF2 78.11$ PEG 91.35$ N/A $204,600 HoldCitigroup 45.91$ DDM3 59.90$ PBV 75.92$ N/A $12,169,000,000 BuySycamore 3.88$ FCFFGen 3.62$ VBV 11.06$ N/A -$207,061,474 SellR io Tinto 40.08$ FCFF2 39.08$ PE 45.20$ N/A $1,316,000,000 Buy

Swatch (bearer) SFr. 163.00 FCFE2 SFr. 177.90 VS SFr. 102.10 N/A $63,800,000 BuySwatch (reg.) SFr. 33.20 FCFE2 SFr. 35.60 VS SFr. 20.40 N/A $63,800,000 Buy

Group Members:

Stefan Fischer (suf200) Espen Stokke (es1446) Ronny Fluegge (rf829)

David Gowans (djg291) Adam Qaiser (aaq207)

Background Information The Swatch Group is a Swiss company that, together with its subsidiaries, is engaged in the

manufacture of watches, movements and components and other products. The company offers

watches in all price and market categories. It manufactures mechanical and quartz movements

and a range of components, including ruby, sapphire and other components. In addition, the

company produces and markets jewelry under the DYB brand name, as well as manufactures

microchips, quartz resonators and other electronic systems, and operates boutiques and shops.

1. Discounted Cash Flow Valuation

NOTE: ANY VALUES STATED ARE ALWAYS IN MILLION CHF (Swiss francs),

UNLESS IT IS A PER SHARE VALUE

Model 2-stage FCFE Model

Rationale Dividends≠FCFE, relative stable D/E ratio, currently high g

- Market value of D/E relatively stable during last five years around 6% with

long term goal of management to increase it to 7% (interview in Swiss

newspaper article)

- Currently high growth in emerging markets (especially Asia)

FCFE Taking 12-month trailing data to calculate normalized FCFE

2003 2004H 2003H Trailing 12-month data

Total Revenue 3'873.0 2'111.0 1'906.0 4'078.0

Cost of Revenue 739.0 n/a n/a n/a

Gross Profit 3'134.0 n/a n/a n/a

Selling/General/Admin. Expenses 1'262.0 n/a n/a n/a

Depreciation/Amortization 216.0 110.0 105.0 221.0

Other Operating Expenses 1'062.0 n/a n/a n/a

Total Operating Expense 3'279.0 1'763.0 1'682.0 3'360.0

Operating Income 594.0 348.0 224.0 718.0

Interest Expense 1.0 0.0 0.0 1.0

Income Before Tax 593.0 348.0 224.0 717.0

Income Tax 96.0 48.0 38.0 106.0

Income After Tax 497.0 300.0 186.0 611.0

Minority Interest 5.0 3.0 2.0 6.0

Net Income 492.0 297.0 184.0 605.0

Income Statement

- Assuming Debt/Equity ratio of 7% translating into 6.5% Debt ratio (DR)

- Capex of 113% of Depreciation

Growth Assuming a further high growth period over next 10 years

- Payout ratio has been an average of 14% over last three years; steadily

increasing – assuming further increase to 20%

- Average ROE over last three years 14.4% - quite stable

- (1-Payout ratio) x ROE = Retention ratio x ROE = growth rate

- Assuming stable growth after 10 years assuming market growth, therefore

using risk free rate

- Further assuming no change in FCF, but sharp increase in payout ratio

Beta Swatch is officially in Retail-Jewelry Sector

- however Swatch also produces electronics, therefore taking 50% of each

unlevered average sector beta from Europe

- Marginal tax rate depends on cantons (state) in Switzerland – average in

West Switzerland (headquarters of Swatch) accumulates to 16%

- Debt/Equity ratio of 7%

Risk Premium Sales all around the world

- Taking geographic sales data as a proxy for country risk premium

- Adjusting weights for future shifts in sales – expecting more sales in Asia

Valuation Valuing shares as of today

- Calculating value as of beginning 2005 and then discounting another

month

Shares Swatch has bearer and registered shares outstanding

- Calculating percentage using book issuance values

Conclusion I find both Swatch stocks as being undervalued and would recommend

to buy shares

2. Value relative to the comparables

Comparables Swatch is in Retail Jewelry and Electronics sector

- I tried to find as many companies with similar product lines as swatch

excluding companies from the Retail Jewelry sector and adding from

Electronics sector

Multiple EV / Sales

- Comparables have all very different financial leverage – some using no

debt at all

- Comparables are all retailers

- Multiple lets adjust for brand name

Simple Average EV / Sales = 1.2

Swatch Group has multiple = 2.3

Looking at those facts Swatch seems to be far overvalued. However, this

multiple those not account for any margin differences due to strong brand

names. Swatch’s product (including the brand name Swatch itself) have a high

name recognition among customers and most products are well-known for

their quality. Therefore, it will be very easy for Swatch to charge a premium for

their name. Most of the comparables do not possess such an asset. Further,

Swatch does not bear the full risk of being a luxury retailer. Swatch is less

exposed to this cyclical market and therefore receives a higher Enterprise

Value compared to some of the comparables.

Regression EV/Sales explained with After-tax Margin and Debt-ratio

EV/Sales (Regression) still lower than actual multiple translating into a share

price of Sfr. 20.40 / 102.10. This can be interpreted that Swatch might be

overvalued compared to the sector. However, it shows that partly a higher

after-tax margin keeps the multiple higher than for the comparables what

probably is attributed to the strong brand name. Further, the risk for the

different companies have not been fully included in the regression, because

financial risk is only a part risk and does not reflect operating risks.

3. Value relative to the market

Swiss Market Swiss Market has many special characteristics (e.g. low interest rates)

- I decided to run a market regression with the 60 largest market cap stocks

in the Swiss market (SWX respectively Virt-X)

- Bloomberg tickers: Regression:

EV/Sales = 0.25 + 0.47(After-tax Margin) + 10.52 (DR) Regression Last price

(0.22) (0.76) (1.59) Reg. share 20.4 33.20

R2 = 0.75 Bear. share 102.1 163.00

EV/Sales (Regression) 1.64

EV/Sales (Actual) 2.30

Regression shows that Swatch is undervalued compared to the overall Swiss

market.

4. Value Enhancement Strategies / EVA

EVA Calculation was done for the same comparable firms as the relative valuation was done. Spread Cost of Debt Riskfree Rate Beta RP Cost of Equity DR WACC ROI CI EVA EVA-Spread

0.85% 6% 4.8% 0.37 6.4% 7.2% 22.8% 7% 6.3% 77.5 -0.4 -0.56%

0.35% 5% 4.8% 2.17 6.4% 18.8% 0.5% 19% 63.0% 623.9 276.3 44.29%

0.50% 5% 4.8% 1.19 6.4% 12.5% 3.9% 12% 15.8% 60.9 2.2 3.67%

0.35% 9% 8.4% 0.67 6.4% 12.7% 2.3% 13% 4.1% 1591.4 -136.0 -8.55%

0.35% 5% 4.8% 0.88 6.4% 10.5% 8.0% 10% 15.3% 156074.0 8170.7 5.24%

0.35% 9% 8.4% 0.67 6.4% 12.7% 7.6% 12% 7.1% 705.0 -37.3 -5.29%

4.00% 12% 8.4% 0.75 6.4% 13.2% 37.2% 13% 4.4% 2111.4 -180.5 -8.55%

0.35% 5% 4.8% 0.58 6.4% 8.6% 5.5% 8% 0.0% 9859.0 -827.7 -8.40%

0.70% 6% 4.8% 0.49 6.4% 8.0% 18.0% 8% 13.7% 90.2 5.6 6.15%

0.35% 9% 8.4% 0.66 6.4% 12.7% 5.2% 12% 12.6% 529.1 0.6 0.11%

0.35% 5% 4.8% 0.93 6.4% 10.8% 0.0% 11% 7.7% 24265.0 -754.4 -3.11%

0.35% 5% 4.8% 0.58 6.4% 8.5% 0.0% 9% 1.2% 18591.0 -1365.2 -7.34%

0.85% 6% 4.8% 0.88 6.4% 10.5% 58.6% 8% 8.4% 140218.0 955.1 0.68%

0.35% 5% 4.8% 1.36 6.4% 13.6% 10.1% 13% 17.8% 3310.0 168.2 5.08%

0.35% 9% 8.4% 0.73 6.4% 13.1% 18.6% 12% 22.6% 73.2 7.5 10.30%

0.35% 5% 4.8% 1.36 6.4% 13.6% 5.9% 13% 15.0% 3310.0 63.8 1.93%

1.00% 9% 8.4% 0.00 6.4% 8.4% 0.0% 8% 15.9% 148.0 11.1 7.53%

8.00% 16% 8.4% 1.17 6.4% 15.9% 47.8% 16% 6.7% 5272.1 -495.9 -9.41%

Avg 7.31% 6.21% 0.86 0.06 11.7% 14.0% 11.3% 13.2% 20383.87 325.76 1.88%

Median 5.60% 4.82% 0.74 6.4% 12.6% 6.7% 12.2% 10.5% 1851.41 1.42 0.40%

Calculations Following assumptions and calculations were made (marked stock=Swatch):

- in order to be able to compare Swatch values where not taken from DCF

valuation since no adjustments have made for the other comparables

either

- the cost of debt was calculated by using synthetical rating for coverage

ratios and using the risk-free rate appropriate to the company

EV/Sales = 0.25 + 22.472 (After-tax Margin) + 5.449 (DR) + 0.019 (RR)

(0.634) (2.613) (1.405) (0.093)

R2 = 0.62

EV/Sales (Regression) 3.22

EV/Sales (Actual) 2.30

Regression Last price

Reg. share 40.1 33.2

Bear. share 200.5 163.0

ABBN VX Equity EMSN VX Equity MC SW Equity SGKN SW Equity

ADEN VX Equity GALN SW Equity NAAN SW Equity SGSN VX Equity

AT/N SW Equity GEBN SW Equity NESN VX Equity SIGN SW Equity

ATLN SW Equity GIVN VX Equity NOBE SW Equity SIK SW Equity

BAER VX Equity HEPN SW Equity NOVN VX Equity SLHN VX Equity

BALN VX Equity HOLN VX Equity PARG SW Equity STMN SW Equity

BARN SW Equity KNIN SW Equity PHBN SW Equity SUN VX Equity

BCVN SW Equity KUD VX Equity PSPN SW Equity SYNN VX Equity

BEKN SW Equity KUNN SW Equity RIEN SW Equity SYST SW Equity

BKWN SW Equity LISN SW Equity ROG VX Equity UBSN VX Equity

CHRN SW Equity LLB SW Equity RUKN VX Equity UHR VX Equity

CIBN VX Equity LOGN SW Equity SCHN SW Equity UNAX VX Equity

CLN VX Equity LONN VX Equity SCI SW Equity VATN SW Equity

CSGN VX Equity LUKN SW Equity SCMN VX Equity VONN SW Equity

EGL SW Equity MASN SW Equity SEO VX Equity ZURN VX Equity

- the cost of equity was calculated assuming all businesses have same risk

premium since most operate world wide (therefore using risk premium

from DCF valuation of Swatch) and using provided Beta

- DR=Debt ratio, shows how different those companies are leveraged

Conclusion In absolute terms Swatch has been below the average, but above the median.

Relative comparision of the EVA-spread shows that Swatch has been very

well performing comparing to comparables (ignoring the outliner which has a

huge ROI for some reason).

Enhancements Swatch should surely use more leverage financing since it is still very

conservative with its debt ratio. Debt seems to be very cheap, provides tax

shelters, and the beta will in reality not go up as fast to compensate additional

risk. Therefore, WACC will come down and the EVA-spread can be increased.

5. Final Recommendation The DCF valuation and the regression with the Swiss market came to the conclusion that Swatch

is undervalued while the valuation relative to comparables has shown that Swatch is overvalued.

How can that be?

In my opinion, this seems to be very logical. The business of Swatch is cyclical. The last

recession is still not entirely over. Companies that sell luxury goods are therefore in general

undervalued, because not all investors are convinced that the economy will pick up again. Swatch

is in comparison with its peer less undervalued. However, looking at the overall market or at the

fundamental value (DCF) of Swatch, it is clearly undervalued. With the economy swinging back

and its growth rate, Swatch is worth more.

The stock is a BUY.

Sycamore Networks Valuation

Company Sycamore Networks, Inc. Symbol SCMR Sector Telecommunications Equipment Type negative earnings company DCF Valuation ModelFCFF, projections based on revenue Relative Valuation Value to Book Capital Special features Firm has no debt but $1bn in cash/ equivalents from the IPO

in boom times, therefore there is no risk of distress DCF Valuation Sycamore Networks manufactures switches for telecom carriers and is a young company, founded during the Hi-Tech boom at the end of the 90’s. The valuation model is based on revenue growth projections at a compounded rate of 15% for the next 10 years, which is around the expected growth of the telecommunications equipment sector. The firm’s revenues grew by 16% last year after suffering from large losses due to the earlier market crash. The management has taken heavy restructuring measures, cutting costs through lay offs and abandoning unprofitable product lines, leaving the firm very focused with a mature and competitive product line. Together with the rebounding market that translates into better operating margins and potential for initially better Sales/Capital ratios (please refer to the summary sheet in Appendix I). Within the sector analysts rank Sycamore Networks at number 7 and it seems optimistic but reasonable to expect it to grow with the industry. Sycamore has no debt and operating leases are not substantial, hence WACC equals the Cost of Equity with 16.34%. The Risk Premium is a weighted average according to the revenues in different countries. The calculated share price of $3.62 from the DCF valuation is close to the actual current price of $3.88. Sycamore appears slightly overvalued but one could argue that the difference is within the range of acceptable variation. More importantly, the market and the results of the DCF valuation agree that Sycamore’s value is dominated by its cash and marketable securities assets. The pure cash assets divided by number of shares yield a price of $3.54. The reason for this is that if the current market projections for telecommunications equipment are realistic then Sycamore cannot create much value itself relative to the amount of capital it holds. Hence it is not expected to produce a good Return on Capital any time soon. A great upside potential for the telecommunication market is not expected by us and the downside risk is that Sycamore keeps on burning cash which it could maintain for a long time. Based on that conclusion and the calculation results the recommendation tends to ‘sell’.

Relative Valuation Multiple: Value to Book Capital Sector: Telecommunications Equipment Number of comparable firms: 127 (source: compfirm.xls) Sycamore has negative earnings, even a negative EBITDA. Therefore, many multiples do not apply. Moreover, the whole sector is in trouble with most other firms losing money as well, yielding regressions with questionable explanatory power. The multiple that gave the best results is Value to Book Value of Capital. However, Sycamore appears undervalued by the factor of 4 (with an actual V/BV ratio of 1.05), which is unrealistic. The regression results are shown in Appendix II, showing a qualitative contradiction with a ROC that has a negative impact (other multiples and regressions were even worse). Interestingly, if one biases the sample by restricting it to the 45 positive earnings firms only, Sycamore should trade at 65% of its book value (Appendix II A). Given the analyst’s forecast of -8% revenues for the next five years that actually seems more realistic. But again revenues have a negative impact in the regression with is contradictory and does not yield a meaningful result if expected revenues are increased. The market regression (US) giving a V/BV ratio of 3 still translates into a share price of $11.06 as opposed to the current $3.88. A subjective valuation compared to the sector average of 6.9 also does not provide any justifiable basis for some story. The recommendation is therefore to ignore relative valuation results. EVA calculation The numbers used in the calculation are in million US$: Return On Capital

After Tax Op Income

EBIT(1-t) -59.2827

Depreciation 9.618

-49.6647

Book Value of Capital 962.989

ROC -5.16%

Cost of Capital 16.34%

EVA -207.061

Telecom Equipment Sector

ROC - WACC 4.88%

comparative EVA 46.994

The EVA for Sycamore in the most recent year is a negative $200 million compared with a positive EVA of $47 million that it should have produced with a sector average for Return on Capital and Cost of Capital. These results are consistent with Sycamore’s negative earnings. Summary Sycamore has a lot of Capital but the market does not present enough opportunities to invest it. Due to the current negative earnings Sycamore is reluctant to give cash back to shareholders and even thinks about using it for acquisitions. However, it is unclear whether a reasonable opportunity might come up. Since there is no debt Sycamore will definitely survive the negative earnings period but we do not expect it to produce a good Return on Capital in the future. It was not appropriate to carry out an option valuation on this firm since the firm has no debt and therefore does not have a default option to put the assets of the firm to debt-holders. Based on the DCF valuation the recommendation remains ‘sell’.

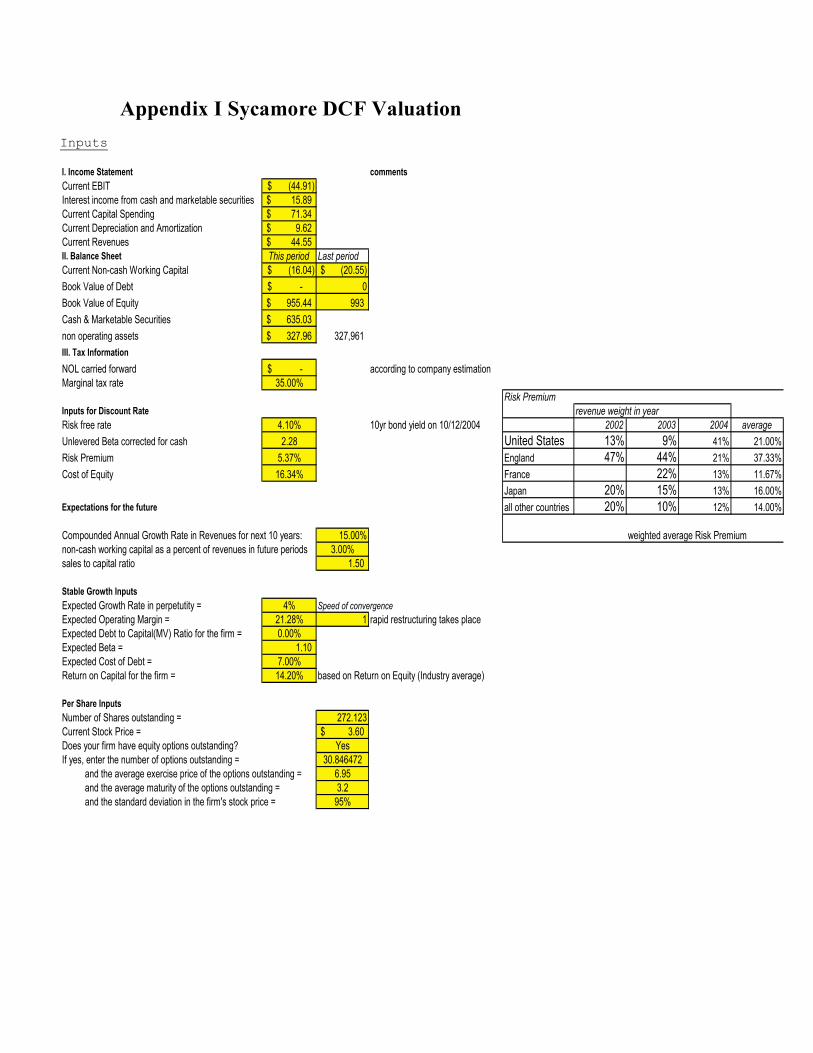

Appendix I Sycamore DCF Valuation Inputs

I. Income Statement comments

Current EBIT (44.91)$ Interest income from cash and marketable securities 15.89$ Current Capital Spending 71.34$ Current Depreciation and Amortization 9.62$ Current Revenues 44.55$ II. Balance Sheet This period Last period

Current Non-cash Working Capital (16.04)$ (20.55)$

Book Value of Debt -$ 0

Book Value of Equity 955.44$ 993

Cash & Marketable Securities 635.03$

non operating assets 327.96$ 327,961

III. Tax Information

NOL carried forward -$ according to company estimationMarginal tax rate 35.00%

Risk Premium

Inputs for Discount Rate revenue weight in year

Risk free rate 4.10% 10yr bond yield on 10/12/2004 2002 2003 2004 average

Unlevered Beta corrected for cash 2.28 United States 13% 9% 41% 21.00%

Risk Premium 5.37% England 47% 44% 21% 37.33%

Cost of Equity 16.34% France 22% 13% 11.67%

Japan 20% 15% 13% 16.00%

Expectations for the future all other countries 20% 10% 12% 14.00%

Compounded Annual Growth Rate in Revenues for next 10 years: 15.00% weighted average Risk Premiumnon-cash working capital as a percent of revenues in future periods 3.00%sales to capital ratio 1.50

Stable Growth Inputs

Expected Growth Rate in perpetutity = 4% Speed of convergence

Expected Operating Margin = 21.28% 1 rapid restructuring takes placeExpected Debt to Capital(MV) Ratio for the firm = 0.00%Expected Beta = 1.10 Expected Cost of Debt = 7.00%Return on Capital for the firm = 14.20% based on Return on Equity (Industry average)

Per Share Inputs

Number of Shares outstanding = 272.123Current Stock Price = 3.60$ Does your firm have equity options outstanding? YesIf yes, enter the number of options outstanding = 30.846472 and the average exercise price of the options outstanding = 6.95 and the average maturity of the options outstanding = 3.2 and the standard deviation in the firm's stock price = 95%

Valuation Summary

Sycamore Networks

The Valuation

PV of FCFF during high growth phase = (27)$ PV of Terminal Value = 83$ Value of Operating Assets of the firm = 56$ Value of Cash & Non-operating assets= 962.99$ Value of Equity = 1,019$ - Value of Equity Options = 33$ Value of Equity in Common Stock = 985$ Treasury Stock ApproachValue of Equity per share = 3.62$ 4.07$

Revenues $53 $64 $77 $92 $111 $129 $144 $158 $171 $181 $189EBIT -$30 -$11 $2 $11 $18 $24 $29 $33 $36 $38 $40EBIT(1-t) -$30 -$11 $2 $11 $18 $19 $19 $21 $23 $25 $26 - Reinvestment $6 $7 $9 $10 $12 $12 $10 $10 $8 $7 $7FCFF -$36 -$18 -$7 $0 $6 $8 $9 $12 $15 $18 $19

Detailed Calculations

Base 1 2 3 4 5 6 7 8 9 10 Terminal YearRevenue Growth Rate 20.00% 20.00% 20.00% 20.00% 20.00% 16.00% 12.00% 10.00% 8.00% 6.00% 4.10%

Revenues $44.547 $53.456 $64.148 $76.977 $92.373 $110.847 $128.583 $144.013 $158.414 $171.087 $181.352 $188.788

Operating Margin -133.08% -55.90% -17.31% 1.99% 11.64% 16.46% 18.87% 20.08% 20.68% 20.98% 21.13% 21.28%EBIT -$59.283 -$29.881 -$11.102 $1.530 $10.748 $18.245 $24.265 $28.913 $32.760 $35.897 $38.324 $40.180Taxes $0.000 $0.000 $0.000 $0.000 $0.000 $0.000 $4.831 $10.120 $11.466 $12.564 $13.413 $14.063EBIT(1-t) -$59.283 -$29.881 -$11.102 $1.530 $10.748 $18.245 $19.434 $18.794 $21.294 $23.333 $24.910 $26.117 + Depreciation $9.618 $11.542 $13.850 $16.066 $17.994 $19.793 $21.377 $22.659 $23.588 $24.555 $25.562 $26.610 - Capital Expenditures $71.341 $17.214 $20.657 $24.234 $27.796 $31.555 $32.668 $32.483 $32.757 $32.624 $32.098 $33.744 - Chg WC $4.505 $0.267 $0.321 $0.385 $0.462 $0.554 $0.532 $0.463 $0.432 $0.380 $0.308 $0.223FCFF -$125.511 -$35.821 -$18.230 -$7.023 $0.484 $5.928 $7.610 $8.507 $11.693 $14.884 $18.067 $18.760NOL $0.000 $29.881 $40.983 $39.453 $28.705 $10.461 $0.000 $0.000 $0.000 $0.000 $0.000 $0.000Terminal Value $317.736

Cost of Capital Calculations

Tax Rate 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 19.91% 35.00% 35.00% 35.00% 35.00% 35.00%Debt Ratio 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Beta 2.28 2.28 2.28 2.28 2.28 2.28 2.04 1.81 1.57 1.34 1.10 1.10 Cost of Equity 16.34% 16.34% 16.34% 16.34% 16.34% 16.34% 15.08% 13.81% 12.54% 11.27% 10.00% 10.00%Cost of Capital 16.34% 16.34% 16.34% 16.34% 16.34% 16.34% 15.08% 13.81% 12.54% 11.27% 10.00% 10.00%

Summary Output

Appendix II Sycamore Regression Results of multiple regression for Value/BV of Capital

Summary measures

Multiple R 0.5694

R-Square 0.3242

Adj R-Square 0.1975

StErr of Est 6.1879

ANOVA Table

Source df SS MS F p-value

Explained 3 293.8922 97.9641 2.5585 0.0915

Unexplained 16 612.6365 38.2898

Regression coefficients

Coefficient Std Err t-value p-value Lower limit Upper limit

Constant 5.8474 2.4783 2.3594 0.0313 0.5936 11.1012

ROC -7.2771 3.0945 -2.3516 0.0318 -13.8372 -0.7171

Expected Growth in Revenues: next 5 years 26.0711 16.2601 1.6034 0.1284 -8.3989 60.5410

Market Debt to Capital -16.4406 12.8402 -1.2804 0.2187 -43.6606 10.7793 Sycamore Value/BV of Capital ROC Expected Growth in Revenues: next 5 years Market Debt to Capital

1.05 -4.53% -8.00% 0.00%

expected V/BV from sector

regression 4.09

expected V/BV from market

regression: 3.04

average V/BV in sector 6.89

Appendix II A: Sample of positive earnings firms Results of multiple regression for Value/BV of Capital

Summary measures

Multiple R 0.8453

R-Square 0.7145

Adj R-Square 0.6366

StErr of Est 3.3789

ANOVA Table

Source df SS MS F p-value

Explained 3 314.2392 104.7464 9.1747 0.0025

Unexplained 11 125.5850 11.4168

Regression coefficients

Coefficient Std Err t-value p-value Lower limit Upper limit

Constant 1.3709 1.6581 0.8268 0.4259 -2.2785 5.0203

ROC 28.4040 6.3706 4.4586 0.0010 14.3823 42.4256

Expected Growth in Revenues: next 5 years -7.0592 12.6620 -0.5575 0.5883 -34.9281 20.8097

Market Debt to Capital 4.3825 11.8829 0.3688 0.7193 -21.7717 30.5366 SCMR expected V/BV = 0.65

PIXAR VALUATION Background Pixar was formed in 1986 and is a leading digital animation studio. The Company’s objective is “to create, develop and produce computer-animated feature films with heartwarming stories and memorable characters that appeal to audiences of all ages.” To date, the company has created and produced six full-length animated feature films: Toy Story, A Bug's Life, Toy Story 2, Monsters, Inc., Finding Nemo, and The Incredibles, which were marketed and distributed by The Walt Disney Company. The first five films are among the top eleven grossing animated films of all time, with combined worldwide box office receipts of more than $2.5 billion. The company is expected to continue growing during the next couple of years. Valuation Methodology.

• Pixar will be valued in US dollars using a 2-stage Free Cash Flow to Firm (FCFF) model. • The calculation will be performed using nominal values and rates.

Risk Free Rate The current yield on the 10 year US Treasury bond is 3.98%. This is the risk free rate used in calculating the cost of equity. Risk Premium Pixar operates in the US, and the geometric average of risk premium in the US from 1928 to 2003 is 4.82%. Market and Book Value of Equity and Debt Equity The book value of equity was given in the Pixar financial statements as $1 119 million. The market value of equity December 10 2004 was $4 779 million (56.901 million shares outstanding; stock price: $83.98). Debt Interest expenses 2,647

Average maturity for the debt 5

Pre-tax cost of debt 4.33%

Present value of annuity 11,676

Book value of debt 61,133

Present value of the book value of the debt 49,457

Estimated market value of conventional debt 61,133

Debt value of opearting leases 1,325

Market value of outstanding debt 62,458 The estimated market values of debt and equity gives Pixar a debt/equity ratio of 1.31% ($4779/$62.458). Compared to the industry average of 20.86%, Pixar is moderately levered.

Beta Calculation The beta of Pixar was estimated by analyzing betas of comparable firms. Pixar’s operations in the computer software industry were treated separately from the main operations in the entertainment industry. First, unlevered betas corrected for cash were calculated. Second, estimated enterprise values were used at weights in order to find Pixar’s total unlevered beta. The unlevered beta is estimated to be 1.107. Levered and unlevered betas by

industry

Average

Beta

Market D/E

Ratio Tax Rate

Unlevered

Beta

Cash/Firm

Value

Corrected

for cash

Entertainment 1.27 26.37% 17.16% 1.04 3.80% 1.08

Computer softw are 1.83 3.58% 9.95% 1.77 13.09% 2.04

Pixar competes in two industries Revenues EV / Sales

Enterprise

Value

Firm Value

Porportion

Unlevered

Beta

Entertainment 316,566 2.82 892,716 97.1% 1.08

Computer softw are 7,537 3.52 26,530 2.9% 2.04

Pixar 919,246 100% 1.107

Using the market values of debt and equity, Pixar’s levered beta is 1.117: Unlevered beta 1.107

Marginal tax rate 35%

Equity, market value 4,853,204

Debt, market value 62,458

Levered beta 1.117 Cost of Equity Pixar’s cost of equity is simply calculated using the risk free rate of 3.98%, the risk premium of 4.82% and the bottom-up levered beta of 1.117. Using the CAPM formula the Cost of Equity for Pixar is 9.28%. Cost of Debt Given Pixar’s conservative leverage, the company default spread is almost insignificant. Also, there is no country default risk. EBT 269,915

Interest expenses 2,647

EBIT 272,562

Operating lease expense 846

Interest expense 2,647

Interest coverage ratio 78.27

Riskfree rate 3.98%

Country default spread 0%

Company default spread (2004) 0.35%

Pre-tax cost of debt 4.33%

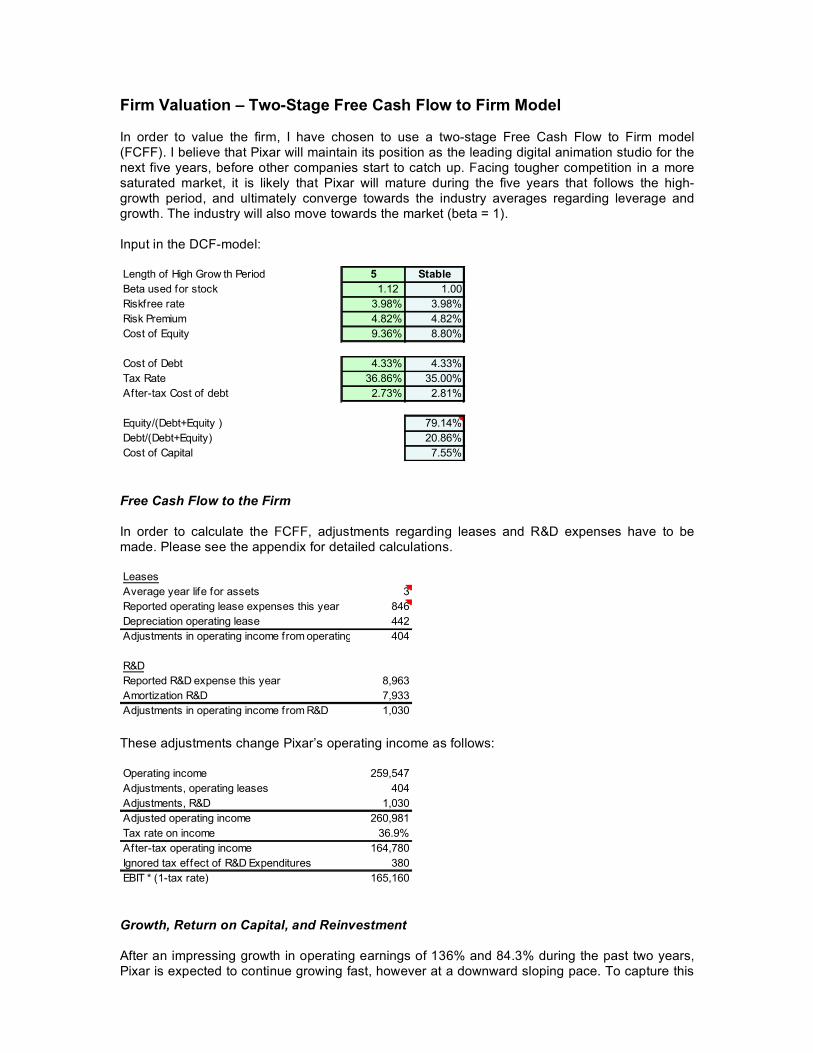

Firm Valuation – Two-Stage Free Cash Flow to Firm Model In order to value the firm, I have chosen to use a two-stage Free Cash Flow to Firm model (FCFF). I believe that Pixar will maintain its position as the leading digital animation studio for the next five years, before other companies start to catch up. Facing tougher competition in a more saturated market, it is likely that Pixar will mature during the five years that follows the high-growth period, and ultimately converge towards the industry averages regarding leverage and growth. The industry will also move towards the market (beta = 1). Input in the DCF-model: Length of High Grow th Period 5 Stable

Beta used for stock 1.12 1.00

Riskfree rate 3.98% 3.98%

Risk Premium 4.82% 4.82%

Cost of Equity 9.36% 8.80%

Cost of Debt 4.33% 4.33%

Tax Rate 36.86% 35.00%

After-tax Cost of debt 2.73% 2.81%

Equity/(Debt+Equity ) 79.14%

Debt/(Debt+Equity) 20.86%

Cost of Capital 7.55% Free Cash Flow to the Firm In order to calculate the FCFF, adjustments regarding leases and R&D expenses have to be made. Please see the appendix for detailed calculations. Leases

Average year life for assets 3

Reported operating lease expenses this year 846

Depreciation operating lease 442

Adjustments in operating income from operating leases 404

R&D

Reported R&D expense this year 8,963

Amortization R&D 7,933

Adjustments in operating income from R&D 1,030 These adjustments change Pixar’s operating income as follows: Operating income 259,547

Adjustments, operating leases 404

Adjustments, R&D 1,030

Adjusted operating income 260,981

Tax rate on income 36.9%

After-tax operating income 164,780

Ignored tax effect of R&D Expenditures 380

EBIT * (1-tax rate) 165,160 Growth, Return on Capital, and Reinvestment After an impressing growth in operating earnings of 136% and 84.3% during the past two years, Pixar is expected to continue growing fast, however at a downward sloping pace. To capture this

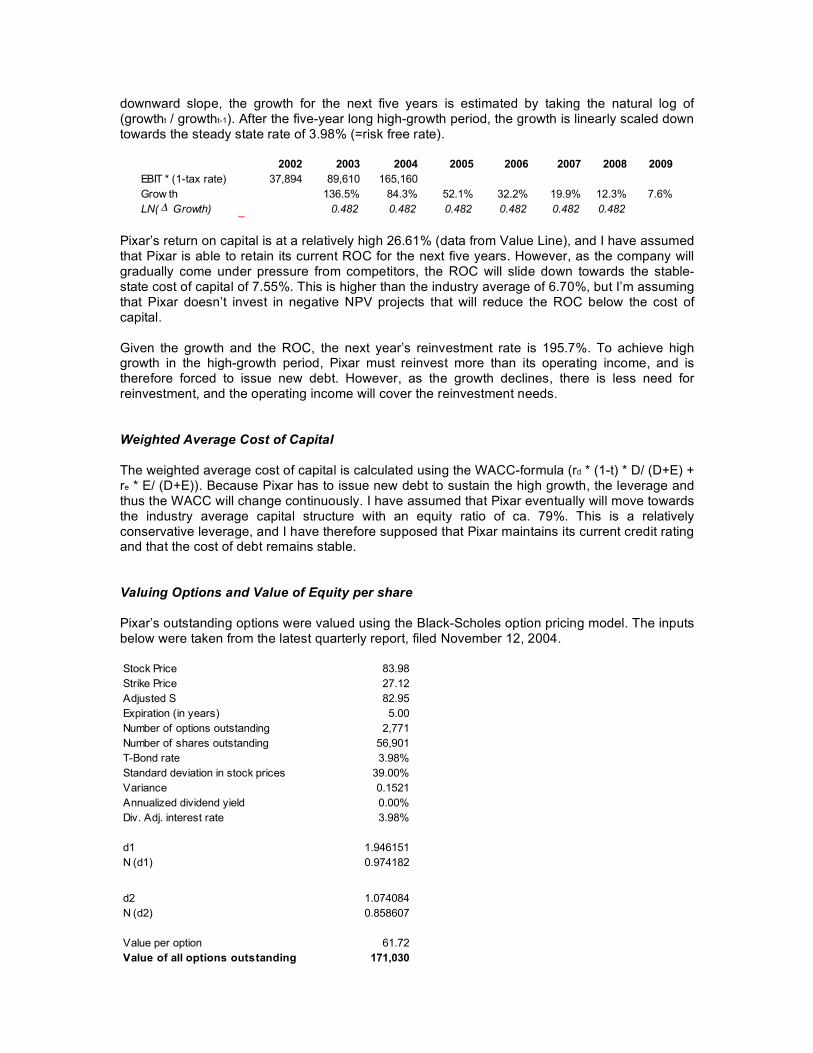

downward slope, the growth for the next five years is estimated by taking the natural log of (growtht / growtht-1). After the five-year long high-growth period, the growth is linearly scaled down towards the steady state rate of 3.98% (=risk free rate).

2002 2003 2004 2005 2006 2007 2008 2009

EBIT * (1-tax rate) 37,894 89,610 165,160

Grow th 136.5% 84.3% 52.1% 32.2% 19.9% 12.3% 7.6%

LN( ! Growth) 0.482 0.482 0.482 0.482 0.482 0.482 Pixar’s return on capital is at a relatively high 26.61% (data from Value Line), and I have assumed that Pixar is able to retain its current ROC for the next five years. However, as the company will gradually come under pressure from competitors, the ROC will slide down towards the stable-state cost of capital of 7.55%. This is higher than the industry average of 6.70%, but I’m assuming that Pixar doesn’t invest in negative NPV projects that will reduce the ROC below the cost of capital. Given the growth and the ROC, the next year’s reinvestment rate is 195.7%. To achieve high growth in the high-growth period, Pixar must reinvest more than its operating income, and is therefore forced to issue new debt. However, as the growth declines, there is less need for reinvestment, and the operating income will cover the reinvestment needs. Weighted Average Cost of Capital The weighted average cost of capital is calculated using the WACC-formula (rd * (1-t) * D/ (D+E) + re * E/ (D+E)). Because Pixar has to issue new debt to sustain the high growth, the leverage and thus the WACC will change continuously. I have assumed that Pixar eventually will move towards the industry average capital structure with an equity ratio of ca. 79%. This is a relatively conservative leverage, and I have therefore supposed that Pixar maintains its current credit rating and that the cost of debt remains stable. Valuing Options and Value of Equity per share Pixar’s outstanding options were valued using the Black-Scholes option pricing model. The inputs below were taken from the latest quarterly report, filed November 12, 2004. Stock Price 83.98

Strike Price 27.12

Adjusted S 82.95

Expiration (in years) 5.00

Number of options outstanding 2,771

Number of shares outstanding 56,901

T-Bond rate 3.98%

Standard deviation in stock prices 39.00%

Variance 0.1521

Annualized dividend yield 0.00%

Div. Adj. interest rate 3.98%

d1 1.946151

N (d1) 0.974182

d2 1.074084

N (d2) 0.858607

Value per option 61.72

Value of all options outstanding 171,030

The value of all options outstanding will be subtracted from the equity, reducing the equity claims on the firm and thus the share price. Estimating the Market Value of Equity per Share The DCF-valuation below indicates that Pixar is slightly overvalued. Length of High Grow th Period 5 Stable

Beta used for stock 1.12 1.00

Riskf ree rate 3.98% 3.98%

Risk Premium 4.82% 4.82%

Cost of Equity 9.36% 8.80%

Cost of Debt 4.33% 4.33%

Tax Rate 36.86% 35.00%

Af ter-tax Cost of debt 2.73% 2.81%

Equity/(Debt+Equity ) 79.14%

Debt/(Debt+Equity) 20.86%

Cost of Capital 7.55%

Grow th Rate 52.06% 3.98%

Return on Capital 7.55%

Reinvestment Rate 52.71%

Current 1 2 3 4 5 6 7 8 9 10 Terminal

Expected Growth Rate 52.1% 32.2% 19.9% 12.3% 7.6% 6.9% 6.1% 5.4% 4.7% 3.98% 3.98%

Return on Capital 26.61% 26.6% 26.6% 26.6% 26.6% 26.6% 22.8% 19.0% 15.2% 11.4% 7.55% 7.55%

Reinvestment Rate 195.7% 120.8% 74.6% 46.1% 28.5% 30.1% 32.3% 35.7% 41.4% 52.71% 52.71%

EBIT * (1 - tax rate) 165,160 251,147 331,900 397,828 446,645 480,486 513,434 544,949 574,478 601,474 625,413 650,304

Reinvestment 491,381 401,056 296,971 205,972 136,811 154,435 176,175 205,140 248,752 329,637 342,757

Free Cash Flow to Firm -240,234 -69,155 100,856 240,673 343,675 358,999 368,774 369,338 352,722 295,776 8,611,976

Equity 4,778,546 4,778,546 4,778,546 4,778,546 4,778,546 4,778,546 4,637,996 4,497,445 4,356,895 4,216,345 4,075,795 4,075,795

Debt 62,458 302,693 371,848 371,848 371,848 371,848 512,398 652,948 793,499 934,049 1,074,599 1,074,599

Equity/(Equity+Debt) 98.7% 94.0% 92.8% 92.8% 92.8% 92.8% 90.1% 87.3% 84.6% 81.9% 79.1% 79.14%

Cost of Capital 9.28% 8.97% 8.88% 8.88% 8.88% 8.88% 8.60% 8.33% 8.06% 7.80% 7.55% 7.55%

Cumulated Cost of Capital 108.97% 118.65% 129.19% 140.67% 153.17% 166.35% 180.20% 194.73% 209.93% 225.78% 242.83%

Present Value -220,463 -58,285 78,067 171,092 224,379 215,816 204,645 189,664 168,020 131,001 3,546,506

Percentage of value of operating assets -4.7% -1.3% 1.7% 3.7% 4.8% 4.6% 4.4% 4.1% 3.6% 2.8% 76.26%

Present Value of FCFF in high grow th phase 1,103,937

Present Value of Terminal Value of Firm 3,546,506

Value of operating assets of the f irm 4,650,443

Value of Cash, Marketable Securities & Non-operating assets 27,545

Value of Firm 4,677,988

Market Value of outstanding debt 62,458

Market Value of Equity 4,615,530

Value of Equity in Options 171,030

Value of Equity in Common Stock 4,444,500

Market Value of Equity/share 78.11

Price per share in the market 83.98

Recommendation SELL! Recommendation: SELL!! Relative Valuation Pixar is a high-growth company, and I have therefore chosen the PEG-ratio for the relative valuation. Independent variables The sample contains 25 firms, and three independent variables have been used in the regression. Given the relatively small sample, one could argue that the regression shouldn’t contain more than two independent variables (maximum one for every 10 stocks in the sample). However, the model’s explanatory power is increased when including three independent variables.

• FCFE/Net Income. The FCFE has been calculated as follows: FCFE = (FCFF - EBIT(1-t)) * (1-d) + Net Income

• LN (Expected growth in earnings per share for the next five years). I have used the natural log to achieve linearity between the PEG and Expected growth in EPS.

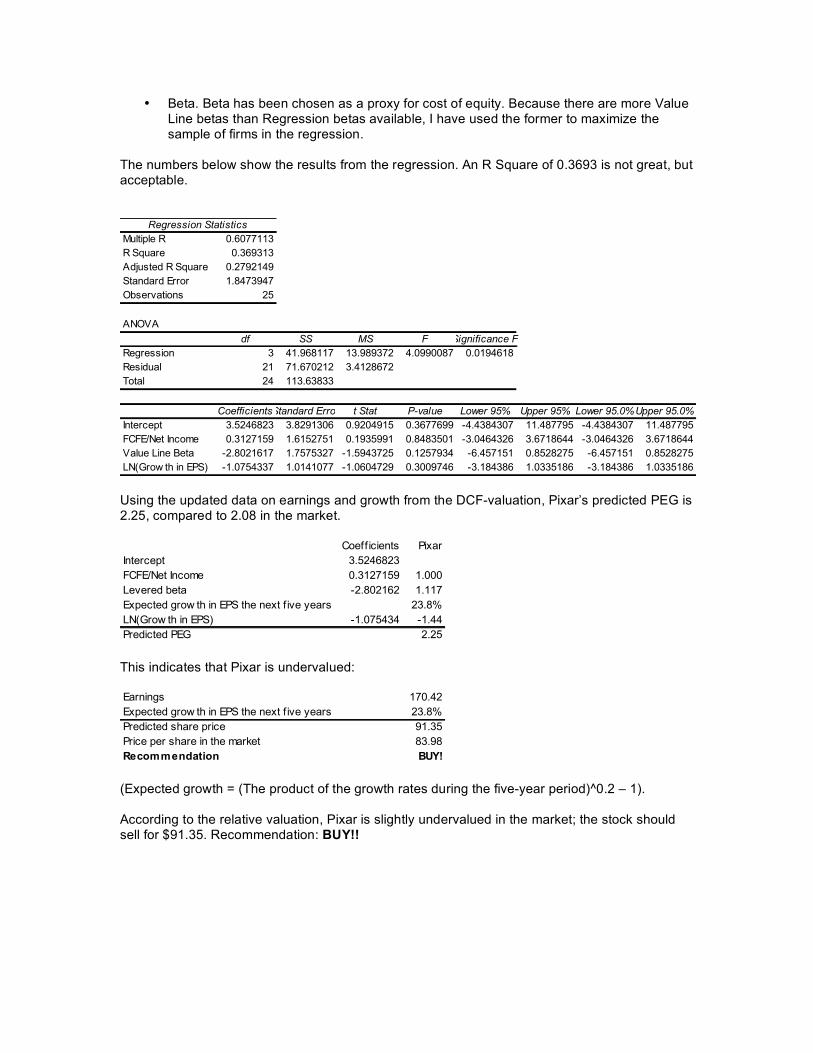

• Beta. Beta has been chosen as a proxy for cost of equity. Because there are more Value Line betas than Regression betas available, I have used the former to maximize the sample of firms in the regression.

The numbers below show the results from the regression. An R Square of 0.3693 is not great, but acceptable.

Regression Statistics

Multiple R 0.6077113

R Square 0.369313

Adjusted R Square 0.2792149

Standard Error 1.8473947

Observations 25

ANOVA

df SS MS F Significance F

Regression 3 41.968117 13.989372 4.0990087 0.0194618

Residual 21 71.670212 3.4128672

Total 24 113.63833

CoefficientsStandard Error t Stat P-value Lower 95% Upper 95% Lower 95.0%Upper 95.0%

Intercept 3.5246823 3.8291306 0.9204915 0.3677699 -4.4384307 11.487795 -4.4384307 11.487795

FCFE/Net Income 0.3127159 1.6152751 0.1935991 0.8483501 -3.0464326 3.6718644 -3.0464326 3.6718644

Value Line Beta -2.8021617 1.7575327 -1.5943725 0.1257934 -6.457151 0.8528275 -6.457151 0.8528275

LN(Grow th in EPS) -1.0754337 1.0141077 -1.0604729 0.3009746 -3.184386 1.0335186 -3.184386 1.0335186

Using the updated data on earnings and growth from the DCF-valuation, Pixar’s predicted PEG is 2.25, compared to 2.08 in the market.

Coefficients Pixar

Intercept 3.5246823

FCFE/Net Income 0.3127159 1.000

Levered beta -2.802162 1.117

Expected grow th in EPS the next f ive years 23.8%

LN(Grow th in EPS) -1.075434 -1.44

Predicted PEG 2.25

This indicates that Pixar is undervalued:

Earnings 170.42

Expected grow th in EPS the next f ive years 23.8%

Predicted share price 91.35

Price per share in the market 83.98

Recommendation BUY!

(Expected growth = (The product of the growth rates during the five-year period)^0.2 – 1). According to the relative valuation, Pixar is slightly undervalued in the market; the stock should sell for $91.35. Recommendation: BUY!!

Value Enhancement The analysis below shows that Pixar are investing in good projects Return on capital 26.61%

Cost of capital 9.28%

Spread 17.33%

Book value of capital 1,180,484

Economic value added 204,600 Compared to the Entertainment industry, the impression of Pixar as a well-managed firm is fortified: Entertainment Industry

Return on capital 6.70%

Cost of capital 8.92%

Spread -2.22% Where Pixar’s current ROC is 17.33% above its cost of capital, the entertainment industry is on average loosing money on its investments; the ROC is 2.22% below the cost of capital. Conclusion The results from the DCF valuation demonstrate that the market overvalues Pixar with ca. $4 per share, or about 7.5%. On the other hand, the relative valuation indicates that Pixar is undervalued by about $7.4 (8.8%). The Value Enhancement analysis suggests that Pixar invests in great projects and creates much more value than the entertainment industry on average. So, which conclusion should be drawn from these ambiguous results? Even though the relative valuation and the EVA-analysis propose a BUY-recommendation, I’m not completely convinced. All of Pixar’s six films have been big blockbusters, but it is unlikely that the future will bring the same impressing amount of home runs. Today, animation films are regarded as something new and exiting. However, I don’t think this will be the case in a few years, and Pixar’s movies will probably face stiffer competition both from other animation films and from “normal” movies. On the other hand, I don’t think the results from the DCF valuation are strong enough to recommend “SELL.” To sum up, my recommendation is HOLD.

Appendix

Future minimum lease payments PV at 6%

2004 882 845

2005 314 288

2006 93 82

2007 74 62

After 2007 58 47

Debt value of leases 1,325

Conventional debt 61,133

Debt value of opearting leases 1,325

Debt outstanding at Pixar 62,458

Convert operating leases into debt

Assumed life of R&D 3

Year

R&D

expense

Amort.

this year

2004 15,095 1.00 15,095

2003 8,963 0.67 5,975 2,988

2002 8,497 0.33 2,832 2,832

2001 6,339 0.00 0 2,113

Total 23,903 7,933

Tax effect on R&D expensing 380

Capitalize R&D expenditures

Unamortized protion