environment and theoretical structure of financial accounting chapter 1 (self-study)

TRANSCRIPT

Environment and Theoretical Structure of

Financial Accounting

Chapter 1(SELF-STUDY)

Learning Objectives

1. Describe the function and primary focus of financial accounting. Pg. 4.2. Explain the difference between cash and accrual accounting. Pg. 6.3. Define generally accepted accounting principles (GAAP) and discuss the historical development of accounting standards. Pg. 8.4. Explain why the establishment of accounting standards is characterized as a political process. Pg. 13.5. Explain factors that encourage high quality financial reporting. Pg. 15.6. Explain the purpose of the FASB’s conceptual framework. Pg. 19.

GO TO NEXT PAGE

Learning Objectives

7. Identify the objective and qualitative characteristics of financial reporting information, and the elements of financial statements. Pg. 21.8. Describe the four basic assumptions underlying GAAP. Pg. 25.9. Describe the Recognition, Measurement and Disclosure Concepts that guide accounting practice. Pg. 27.10. Contrast a revenue/expense and an asset/liability approach to standard setting. Pg. 33.11. Describe the primary differences between US GAAP and IFRS with respect to the development of Accounting standards. Pg. 15 and 21.

Financial Accounting Environment

Profit-orientedcompanies

Not-for-profitentities

Households

Providers ofFinancial

InformationExternal

User Groups

Investors

Creditors

Employees

Labor unions

Customers

Suppliers

Governmentagencies

Financialintermediaries

Relevant

FinancialInformation

Financial Accounting EnvironmentRelevant financial information is provided primarily through

financial statements and related disclosure notes. The following financial statements are the most frequently provided.

1. Balance Sheet2. Income Statement3. Statement of Cash Flows4. Statement of Shareholders’ Equity

Starting in 2012, companies must either provide a Statement of Other Comprehensive Income immediately following the Income Statement, or present a Combined Statement of Comprehensive Income that includes the information normally contained in both the Income Statement and the Statement of Other Comprehensive Income.

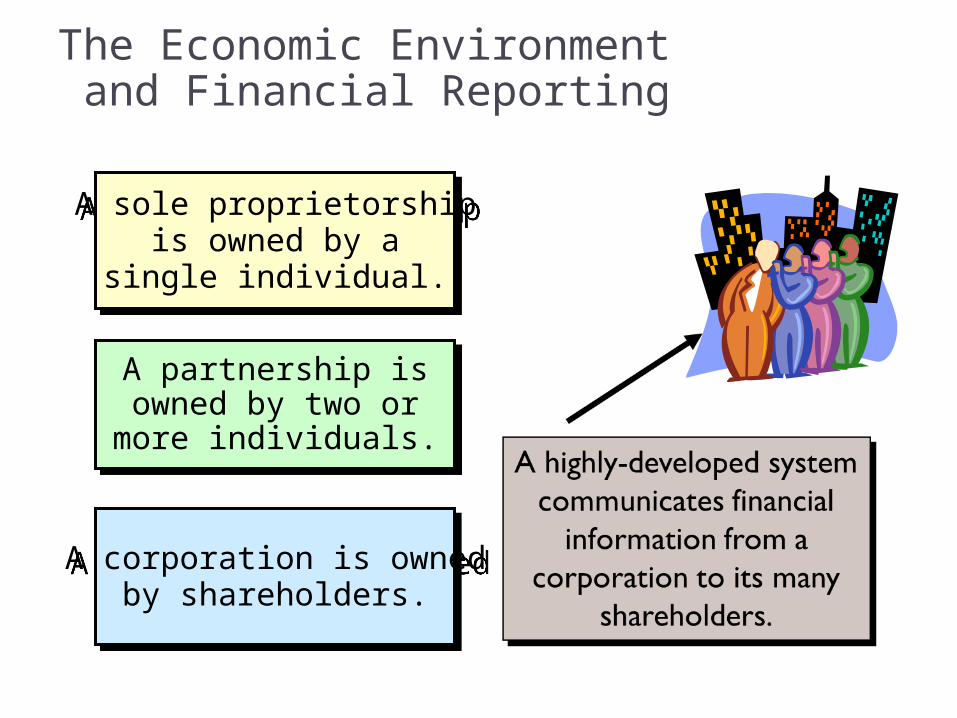

The Economic Environment and Financial Reporting

A sole proprietorshipis owned by a

single individual.

A sole proprietorshipis owned by a

single individual.

A partnership isowned by two ormore individuals.

A partnership isowned by two ormore individuals.

A corporation is ownedby shareholders.

A corporation is ownedby shareholders.

Investment-Credit Decisions ─ A Cash Flow Perspective

Shareholders Receive

Cash

1. Dividends2. Sale of Stock

Creditors Receive

Cash

1. Interest2. Repayment of

Principle

Accounting information should help investors and creditors evaluate the amount, timing, and uncertainty of the enterprise’s future cash flows.

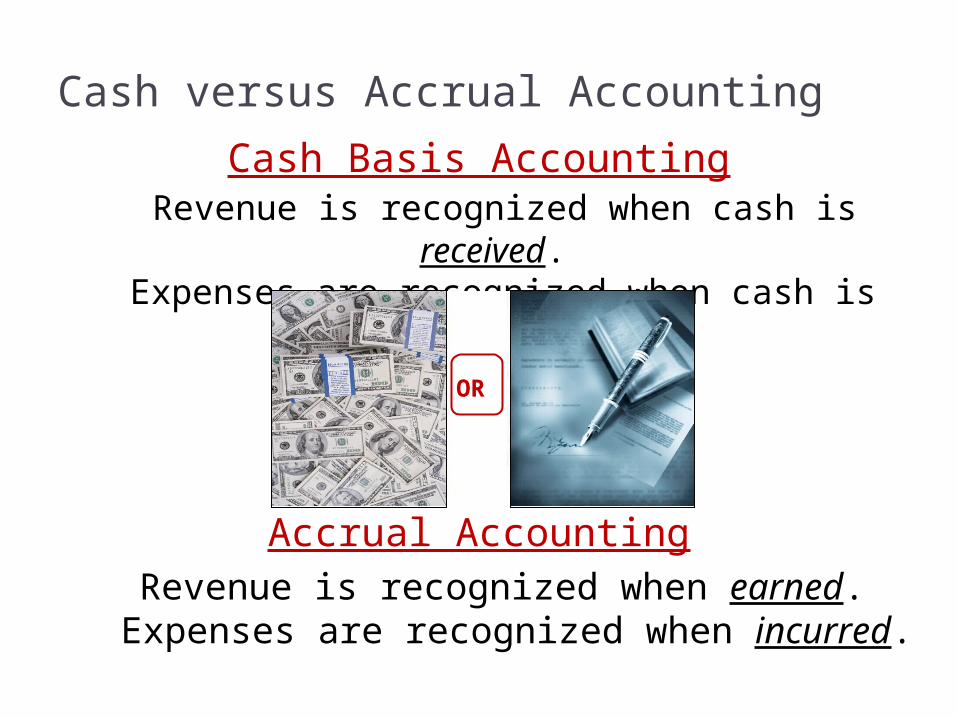

Cash versus Accrual Accounting

Cash Basis Accounting Revenue is recognized when cash is received. Expenses are recognized when cash is paid.

OROROR

OR

Accrual AccountingRevenue is recognized when earned.

Expenses are recognized when incurred.

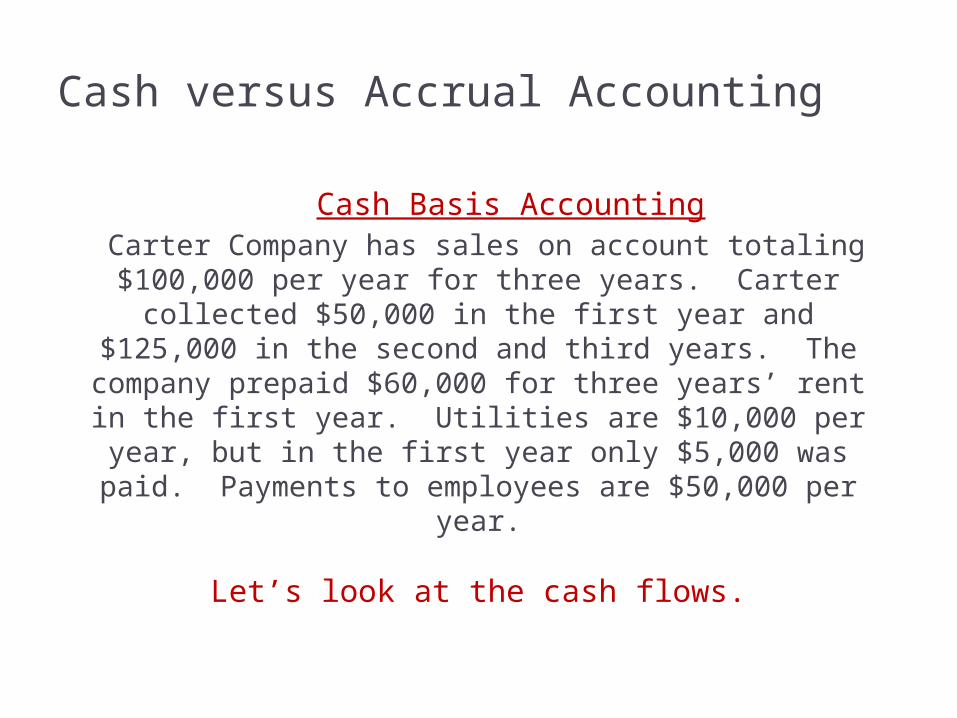

Cash versus Accrual Accounting

Cash Basis Accounting Carter Company has sales on account totaling

$100,000 per year for three years. Carter collected $50,000 in the first year and $125,000 in the second and third years. The company prepaid

$60,000 for three years’ rent in the first year. Utilities are $10,000 per year, but in the first year

only $5,000 was paid. Payments to employees are $50,000 per year.

Let’s look at the cash flows.

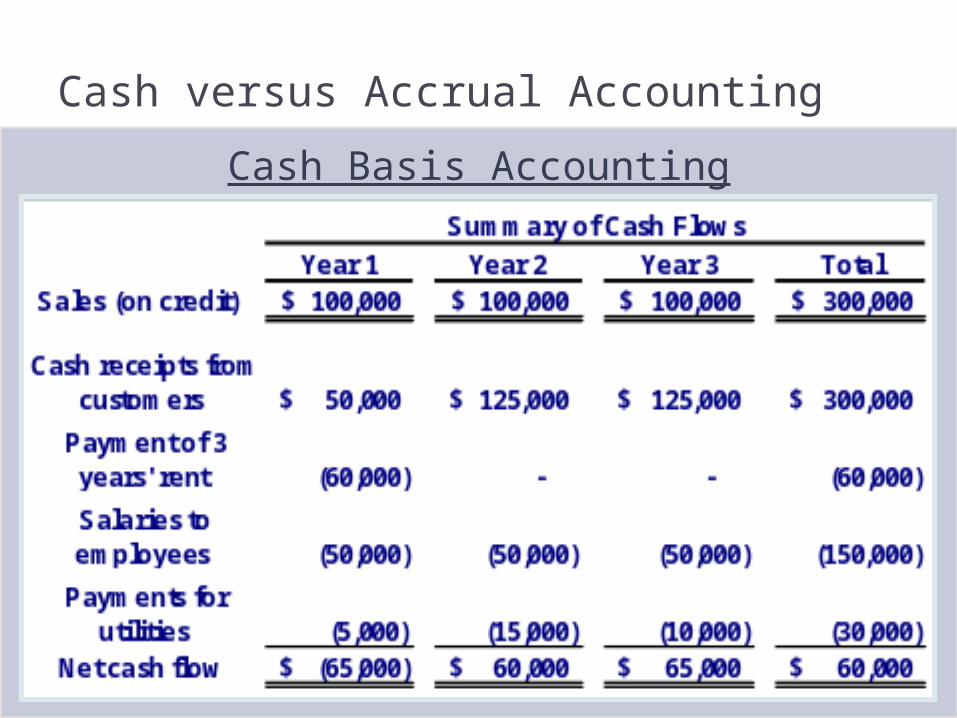

Cash versus Accrual Accounting

Cash Basis Accounting

Cash versus Accrual Accounting

Cash Basis Accounting

Cash flows in any one year may notbe a predictor of future cash flows.

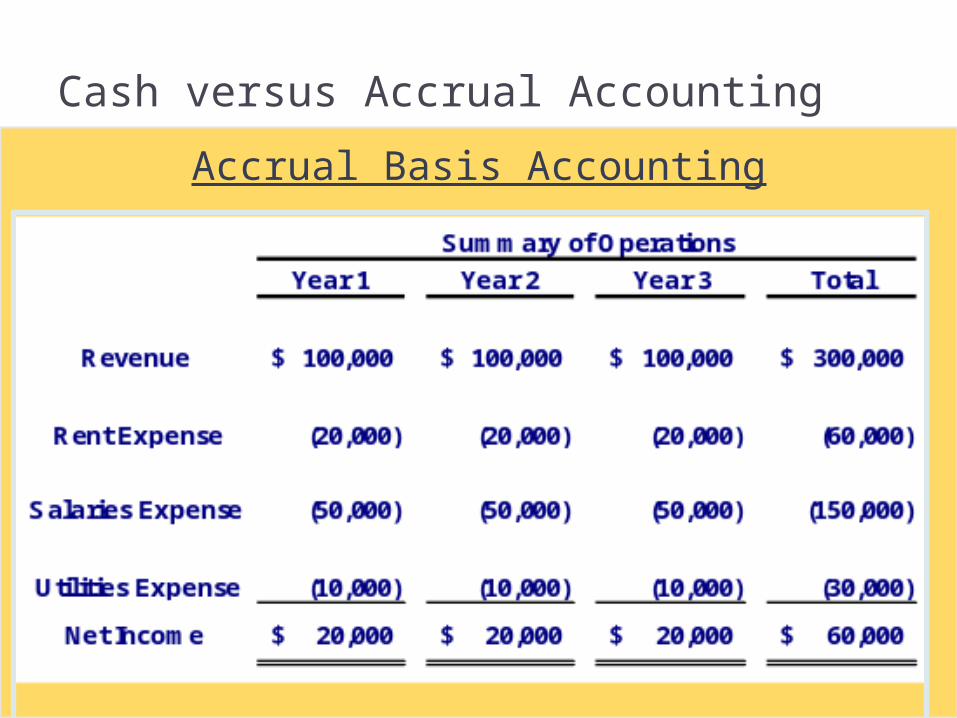

Cash versus Accrual Accounting

Accrual Basis Accounting

Cash versus Accrual Accounting

Accrual Basis Accounting

Net Income is considered a better indicator of future cash flows.

The Development of Financial Accounting and Reporting Standards

Concepts, principles, and

proceduresdeveloped to meet the

needs of external users (GAAP).

Historical Perspective and Standards

Current U. S. Standard Setting

Supported by the Financial Accounting Foundation

Seven full-time, independent voting members

Members not required to be CPAs

Financial Accounting Standards Board

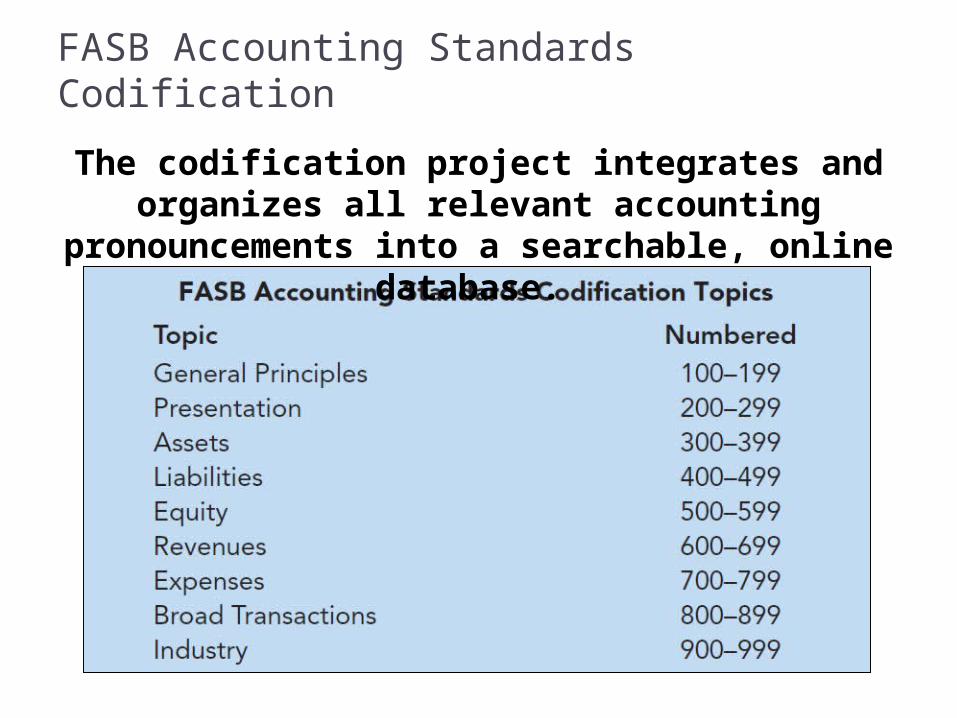

FASB Accounting Standards Codification

The codification project integrates and organizes all relevant accounting

pronouncements into a searchable, online database.

International Standard Setting

The main objective of the International Accounting Standards Board (IASB) is to develop a single set of high quality,

understandable, and enforceable global accounting standards to help participants in the world’s capital

markets and other users make economic decisions.

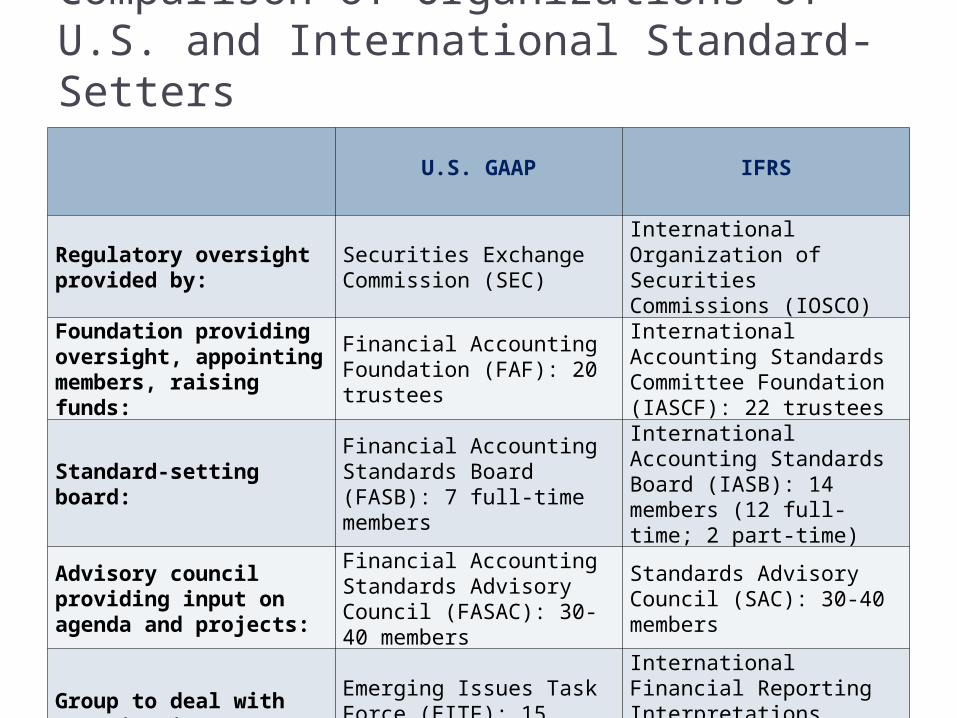

Comparison of Organizations of U.S. and International Standard-Setters

U.S. GAAP IFRS

Regulatory oversight provided by:

Securities Exchange Commission (SEC)

International Organization of Securities Commissions (IOSCO)

Foundation providing oversight, appointing members, raising funds:

Financial Accounting Foundation (FAF): 20 trustees

International Accounting Standards Committee Foundation (IASCF): 22 trustees

Standard-setting board:

Financial Accounting Standards Board (FASB): 7 full-time members

International Accounting Standards Board (IASB): 14 members (12 full-time; 2 part-time)

Advisory council providing input on agenda and projects:

Financial Accounting Standards Advisory Council (FASAC): 30-40 members

Standards Advisory Council (SAC): 30-40 members

Group to deal with emerging issues:

Emerging Issues Task Force (EITF): 15 members

International Financial Reporting Interpretations Committee (IFRIC): 14 members

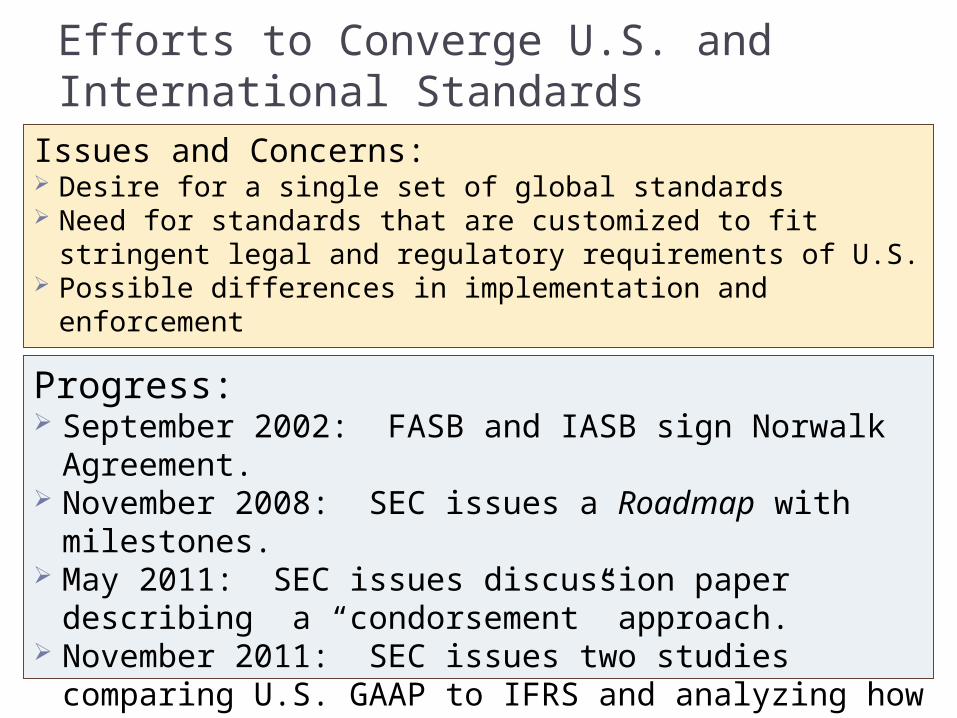

Efforts to Converge U.S. and International Standards

Issues and Concerns: Desire for a single set of global standards Need for standards that are customized to fit stringent

legal and regulatory requirements of U.S. Possible differences in implementation and enforcement

Progress: September 2002: FASB and IASB sign Norwalk

Agreement. November 2008: SEC issues a Roadmap with

milestones. May 2011: SEC issues discussion paper describing a

“condorsement” approach. November 2011: SEC issues two studies comparing

U.S. GAAP to IFRS and analyzing how IFRS are applied globally.

December 2011: SEC postpones final determination until 2012.

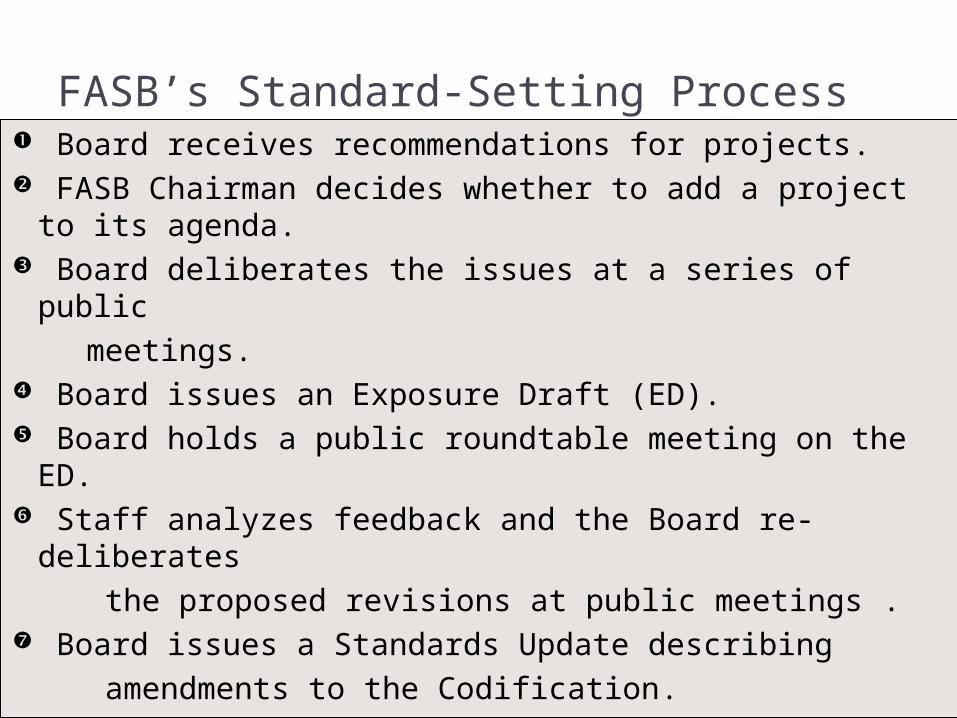

FASB’s Standard-Setting Process Board receives recommendations for projects. FASB Chairman decides whether to add a project to

its agenda. Board deliberates the issues at a series of public meetings. Board issues an Exposure Draft (ED). Board holds a public roundtable meeting on the

ED. Staff analyzes feedback and the Board re-

deliberates the proposed revisions at public meetings . Board issues a Standards Update describing amendments to the Codification.

Role of the Auditor

Auditors serve as independent intermediaries to help ensure that

management has appropriately applied U.S. GAAP in preparing the company’s financial statements.

Financial Reporting Reform

As a result of numerous financial scandals, Congress passed the Public Public

Company Accounting Reform and Company Accounting Reform and Investor Protection Act of 2002Investor Protection Act of 2002,

(Sarbanes-Oxley Act). The goal was to restore credibility and investor

confidence in the financial reporting process.

As a result of numerous financial scandals, Congress passed the Public Public

Company Accounting Reform and Company Accounting Reform and Investor Protection Act of 2002Investor Protection Act of 2002,

(Sarbanes-Oxley Act). The goal was to restore credibility and investor

confidence in the financial reporting process.

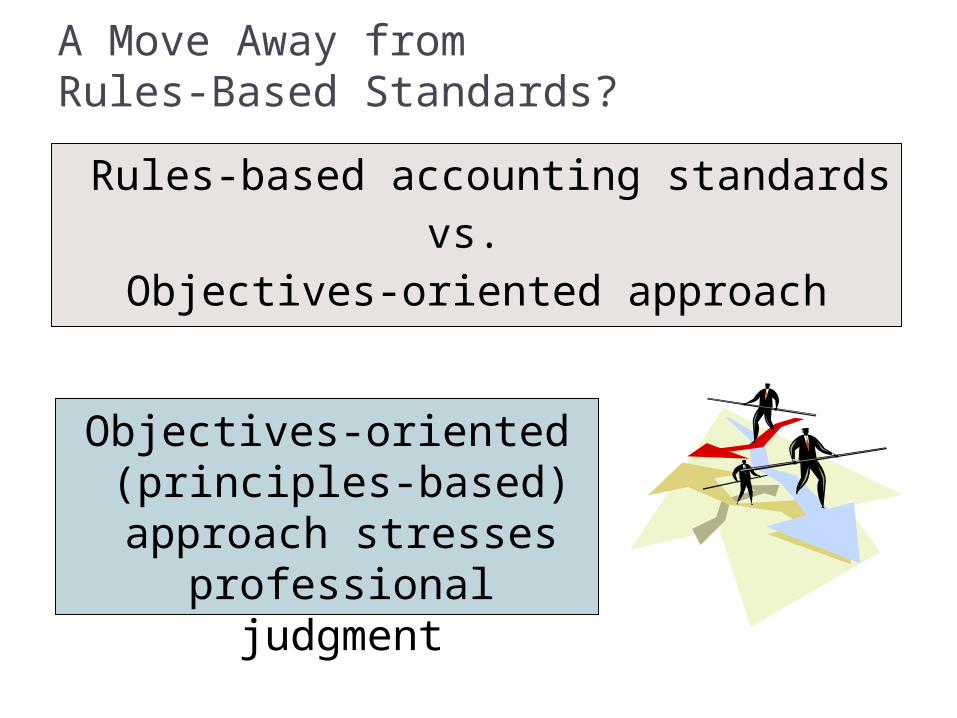

A Move Away from Rules-Based Standards?

Rules-based accounting standards vs.

Objectives-oriented approach

Objectives-oriented (principles-based) approach stresses

professional judgment

Ethics in Accounting

Code of Ethics: Provides guidance and rules to help accounting professionals perform

their professional responsibilities in an ethical manner.

Analytical Model for Ethical Decisions Determine the facts of the situation. Identify the ethical issue and the stakeholders. Identify the values related to the situation. Specify the alternative courses of action. Evaluate the courses of action. Identify the consequences of each course of

action. Make your decision and take any indicated action.

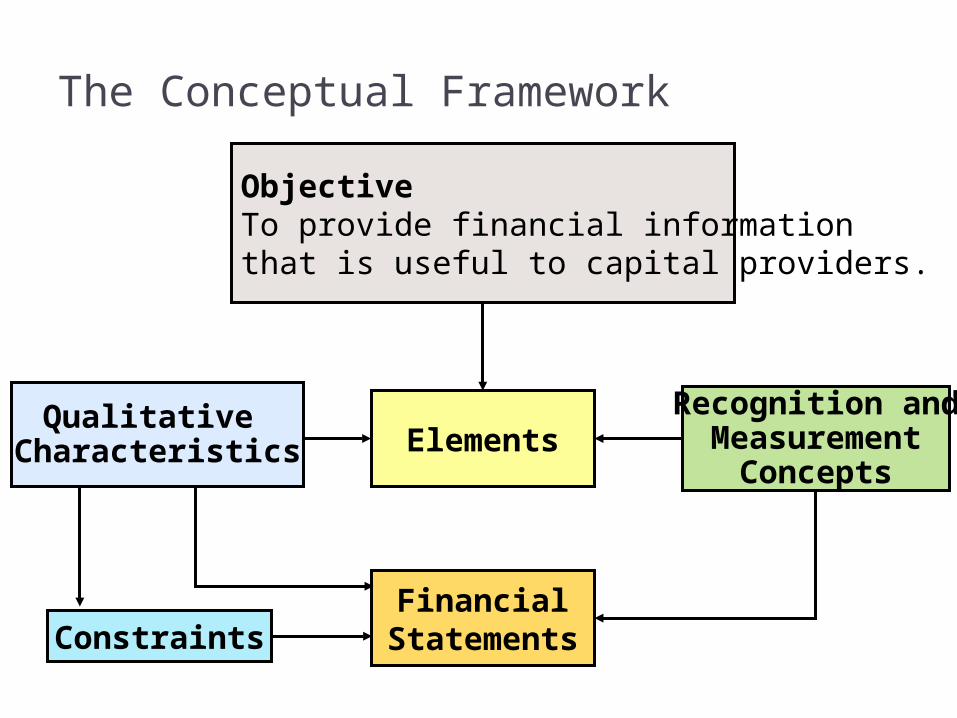

The Conceptual Framework

The Conceptual Framework has been described as an “Accounting Constitution.” It provides the

underlying foundation for accounting standards.

FASB Conceptual Framework(Statements of Financial Accounting Concepts)

Objectives of Financial Reporting (SFAC 1, replaced by SFAC 8)Qualitative Characteristics (SFAC 2, replaced by SFAC 8)Elements of Financial Statements (SFAC 3, replaced by SFAC 6)Recognition and Measurement (SFAC 5 and SFAC 7)

ObjectiveTo provide financial information that is useful to capital providers.

ElementsRecognition and

MeasurementConcepts

ConstraintsFinancial

Statements

The Conceptual Framework

Qualitative Characteristics

NeutralityCompletenessFree from

errorPredictive

valueMateriality

Relevance Faithful representation

Qualitative Characteristics ofAccounting Information

Comparability(Consistency)

UnderstandabilityVerifiability Timeliness

Decision usefulness

Confirmatory value

Key Constraint

CostEffectiveness

CostEffectiveness

Benefits

Costs

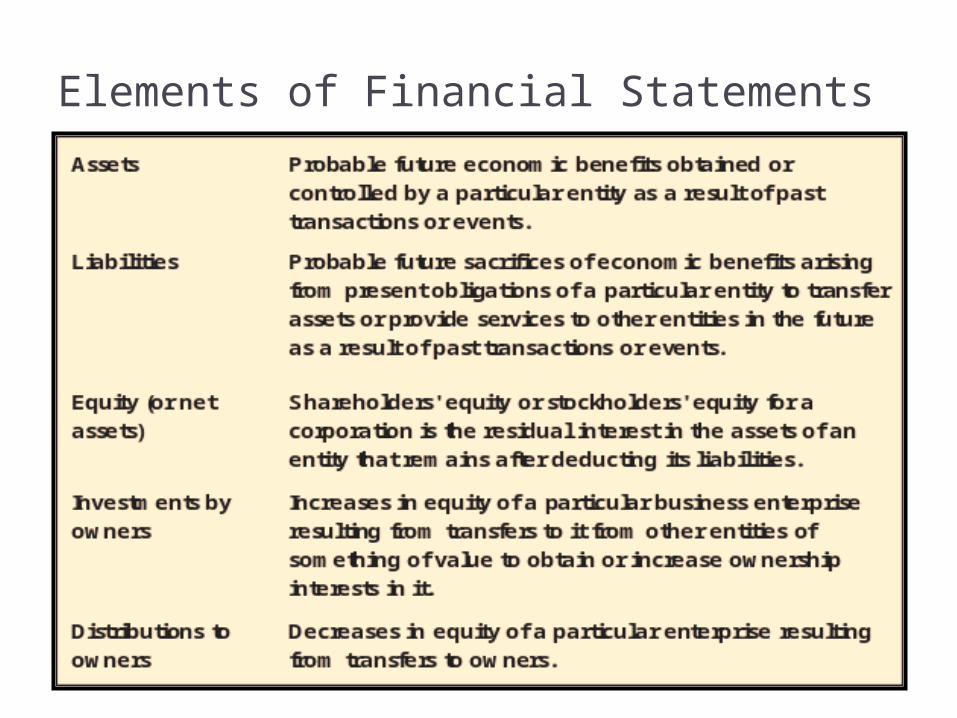

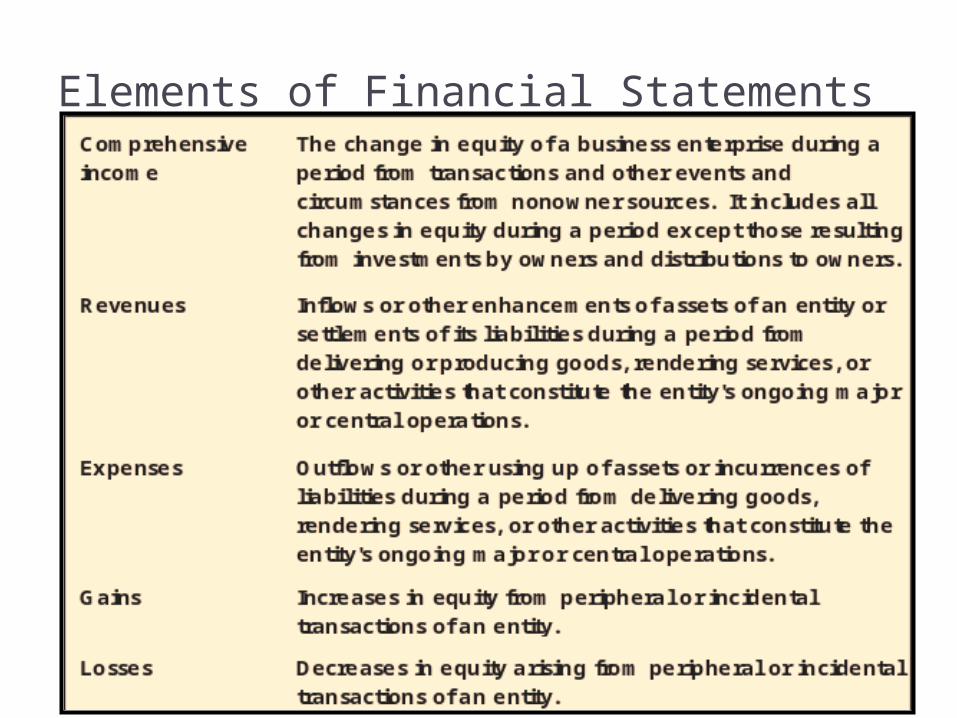

Elements of Financial Statements

Elements of Financial Statements

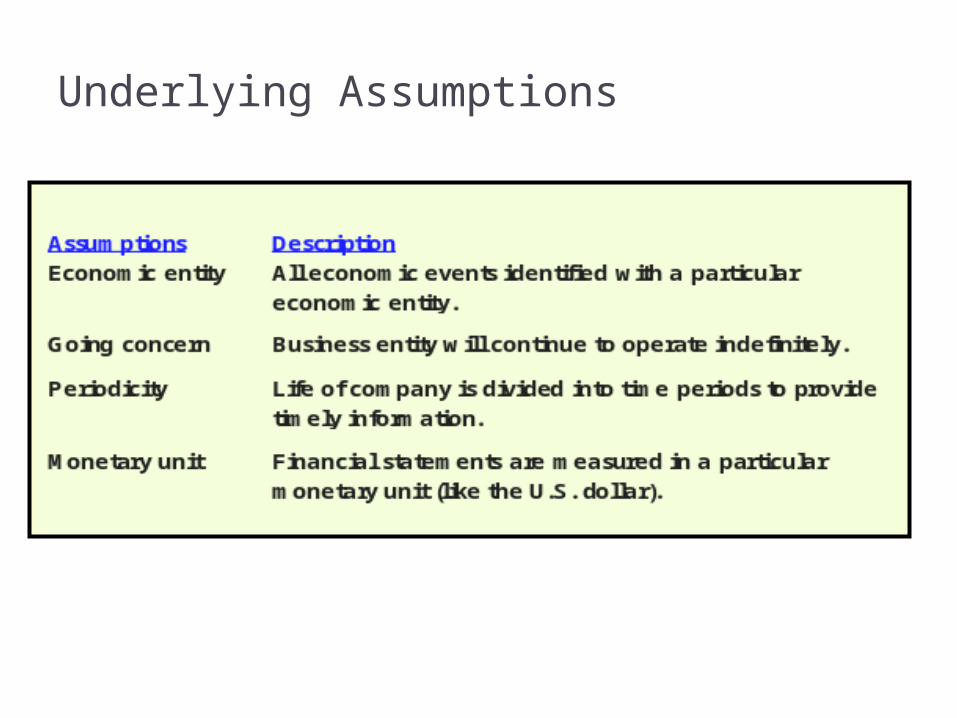

Underlying Assumptions

Recognition, Measurement and Disclosure Concepts

RecognitionProcess of admitting

information into the basic financial statements

Criteria:1. Definition2. Measurability3. Relevance4. Reliability

Measurement Process of associating

numerical amounts with the elements.

Measurement Attributes:

1. Historical cost2. Net realizable

value3. Current cost4. Present value of

future cash flows5. Fair value

Disclosure Process of including

additional supplemental information.

Examples:1. Parenthetical

amounts2. Notes to FS3. Supplemental FS

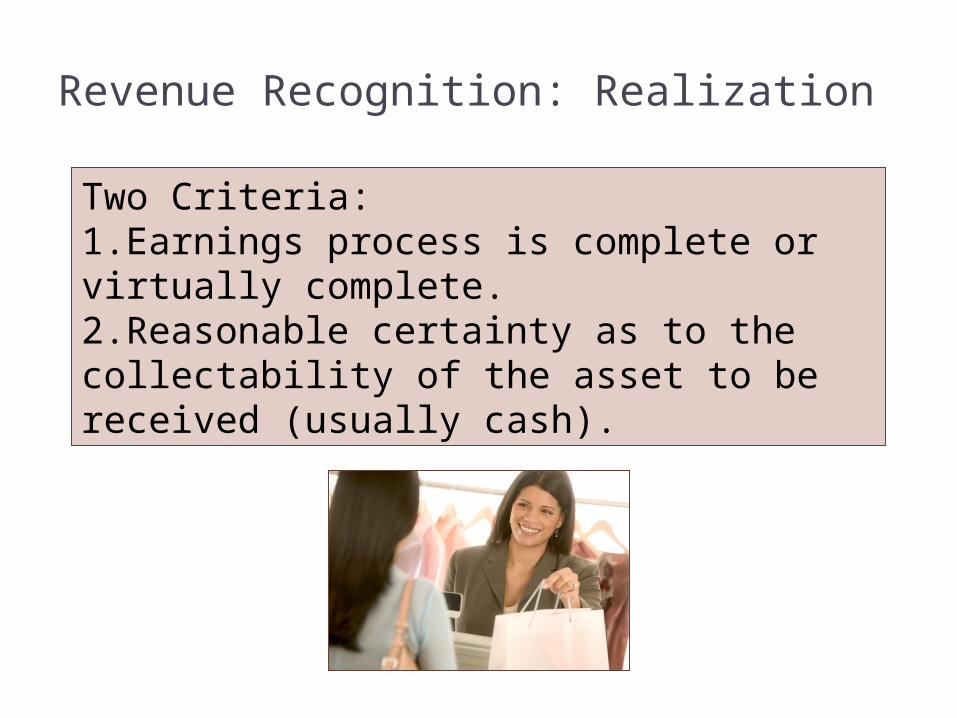

Revenue Recognition: Realization

Two Criteria:1.Earnings process is complete or virtually complete.2.Reasonable certainty as to the collectability of the asset to be received (usually cash).

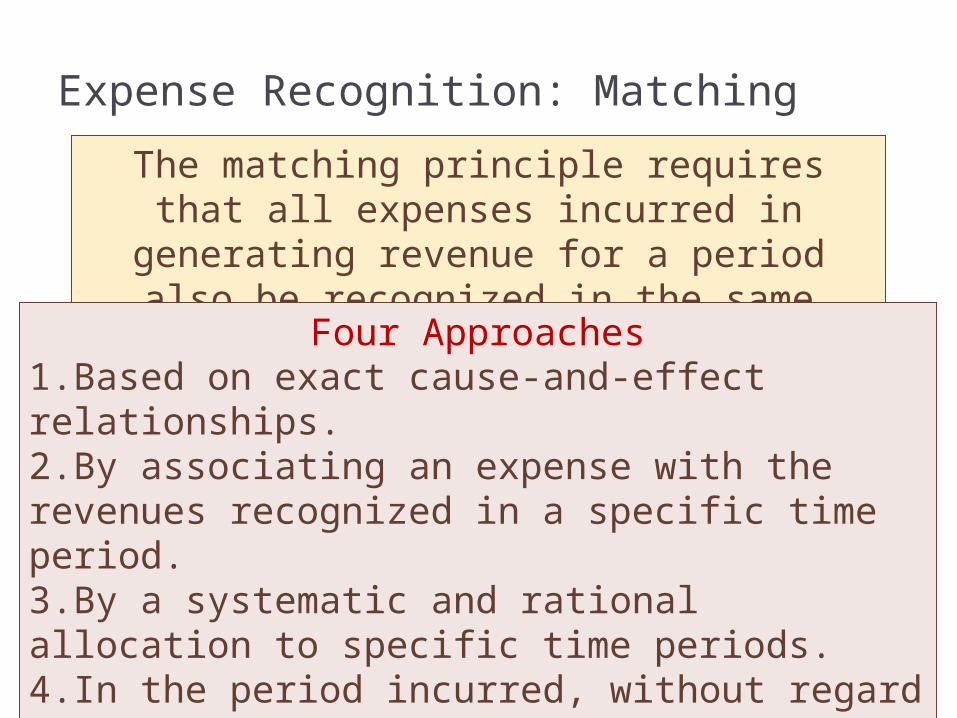

Expense Recognition: Matching

The matching principle requires that all expenses incurred in generating revenue for a period also be recognized in the same period.

Four Approaches1.Based on exact cause-and-effect relationships.2.By associating an expense with the revenues recognized in a specific time period.3.By a systematic and rational allocation to specific time periods.4.In the period incurred, without regard to related revenues.

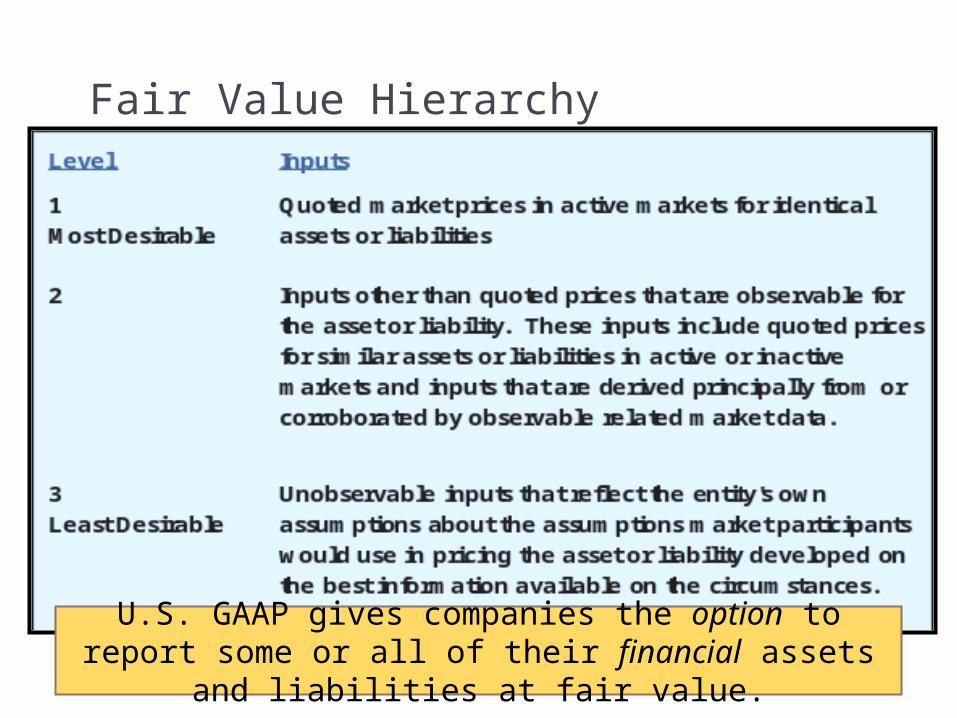

Fair Value Hierarchy

U.S. GAAP gives companies the option to report some or all of their financial assets and liabilities at

fair value.

Evolving U.S. GAAP

U.S. GAAP has been evolving from an emphasis on revenues and expenses to an emphasis on

assets and liabilities.Revenue/Expense Approach: Emphasize principles for recognizing revenues and expenses, with some

assets and liabilities recognized as necessary to make the balance sheet reconcile with the income

statement.Asset/Liability Approach: Emphasize principles for

recognizing assets and liabilities first, and then recognize and measure the revenues, expenses,

gains, and losses needed to account for the changes in assets and

liabilities from the previous measurement date.

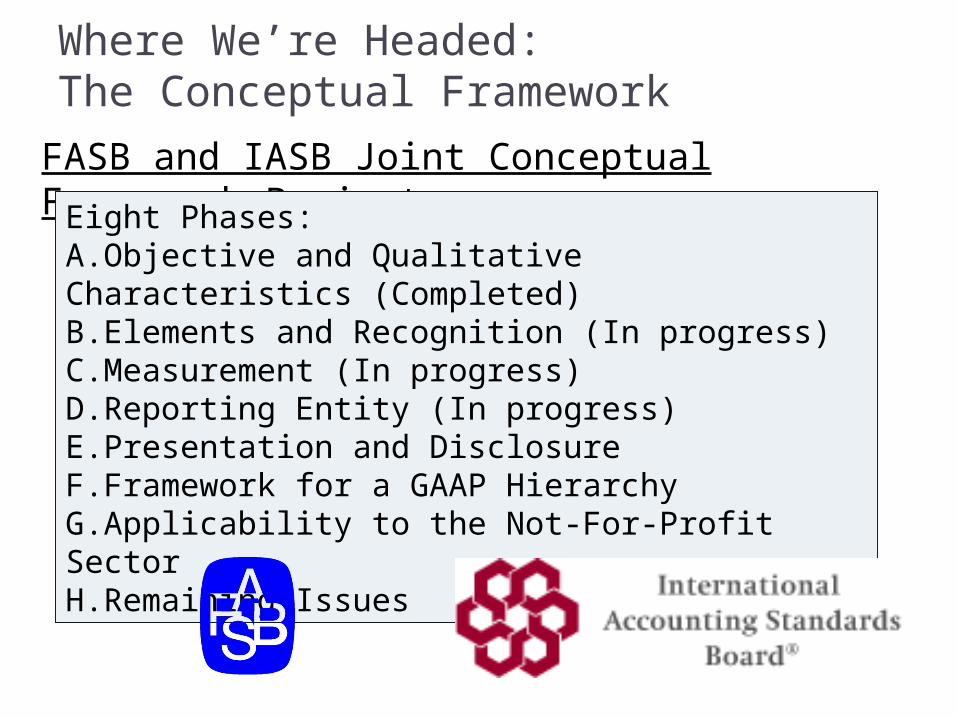

Where We’re Headed:The Conceptual Framework

FASB and IASB Joint Conceptual Framework Project

Eight Phases:A.Objective and Qualitative Characteristics (Completed)B.Elements and Recognition (In progress)C.Measurement (In progress)D.Reporting Entity (In progress)E.Presentation and DisclosureF.Framework for a GAAP HierarchyG.Applicability to the Not-For-Profit SectorH.Remaining Issues

End of Chapter 1