enterprise and household demand for financial services 0 nairobi, may 15-17, 2006 world bank seminar...

TRANSCRIPT

Enterprise and Household Demand for Financial Services 1Nairobi, May 15-17, 2006

World Bank Seminar on Financial Stability and Development

ENTERPRISE AND HOUSEHOLD DEMAND FOR FINANCIAL

SERVICES

Yira MascaróSenior Financial Economist

World Bank

Enterprise and Household Demand for Financial Services 2Nairobi, May 15-17, 2006

Structure Of Presentation

I. Importance of demand side analysis: completing the picture

Financial stability Financial development

II. Understanding the demand for financial services Characteristics of households and firms Using available data Accounting and auditing standards

Enterprise and Household Demand for Financial Services 3Nairobi, May 15-17, 2006

Structure Of Presentation

III. Assessing the financial health of firms Recent trends Performance: financial ratio analysis International benchmarking

IV. Legal and institutional constraints Existing infrastructure Legal and institutional aspects Other aspects

V. Concluding remarks

Enterprise and Household Demand for Financial Services 4Nairobi, May 15-17, 2006

1. Financial stability• Large exposures of financial institutions to:

– groups of troubled debtors (e.g., after crisis)

– systemic exposures to a few large debtors

– dollar liabilities of debtors in non-tradable sectors» indirect exchange rate effect

– Worrisome sectoral concentrations and trends» e.g., tourism, construction

– Related lending » Masked interrelations between economic and financial groups

I. Importance of demand side analysis: completing the picture

Enterprise and Household Demand for Financial Services 5Nairobi, May 15-17, 2006

I. Importance of demand side analysis: completing the picture

1. Financial stability• Large exposures to deposit runs:

– Deposit concentration in a few large accounts– Political and social instability

• Stress testing (bank and corporate)– Shocks

» oil prices» “sudden stop” of capital flows; Foreign credit lines of banks» natural disasters

– Scenario analysis» E.g., deteriorating portfolio

Enterprise and Household Demand for Financial Services 6Nairobi, May 15-17, 2006

I. Importance of demand side analysis: completing the picture

Bolivia: Deposit trends 2001-2005;

Source: Superintendency of banks and financial Institutions (SBEF)

2508

2,464

25052601 2452

2372

2,305

2626

3124

2455

2725

2613

2384

2755

2200

2300

2400

2500

2600

2700

2800

2900

3000

3100

3200

De

c-0

1

Ma

r-0

2

Ju

n-0

2

Se

p-0

2

De

c-0

2

Ma

r-0

3

Ju

n-0

3

Se

p-0

3

De

c-0

3

Ma

r-0

4

Ju

n-0

4

Se

p-0

4

De

c-0

4

Ma

r-0

5

Ju

n-0

5

Se

p-0

5

Bancos: Evolución de las Obligaciones con el Público*Del 31/12/2001 al 30/09/2005

(en millones de $us)

Enterprise and Household Demand for Financial Services 7Nairobi, May 15-17, 2006

2. Financial development • Lending and savings trends

– e.g., credit crunches: demand or supply driven (econometric analysis)– Outreach

• Interest rates and spreads

• Unmet needs of households and firms (data limitations)

• Opportunities for improving existing products and developing new ones

• Legal, regulatory and institutional constraints

I. Importance of demand side analysis: completing the picture

Enterprise and Household Demand for Financial Services 8Nairobi, May 15-17, 2006

1. Characteristics of households and firms• Households:

– Saving patterns, special characteristics » Income levels, concentration of wealth» Education, language, religion

– Assess needs for new and improved financial products » savings vehicles» payment of basic services and taxes» pension services» housing and insurance needs» consumption etc.

II. Understanding the demand for financial services

Enterprise and Household Demand for Financial Services 9Nairobi, May 15-17, 2006

1. Characteristics of households and firms

• Firms: – Structure and characteristics

» Distribution by size» Extent of informality» Growing patterns (by economic sectors and size)» Common features by size (e.g. microenterprises- collateral substititution)

– Vulnerabilities to shocks

» Natural disasters (e.g., hurricanes, earthquakes)» Economic shocks (oil price)

II. Understanding the demand for financial services

Enterprise and Household Demand for Financial Services 10Nairobi, May 15-17, 2006

1. Characteristics of households and firms• Firms:

– Trends of lending by economic sectors and geography

– Financing sources : formal or informal» Financial institutions (banks, NBFIs, moneylenders)» Foreign financing» Suppliers and trade credit» Internal resources» Family and friends

– Residual effects from recent crises» Over-leveraged» Excess of fixed assets (collateral for debt)» illiquid

II. Understanding the demand for financial services

Enterprise and Household Demand for Financial Services 11Nairobi, May 15-17, 2006

2. Using available data (limitations)

• Firms: – Public data

» listed firms, bankscope, bloomberg, chambers of commerce» ICAs (e.g., financing structure of firms) » Moodys, S&Ps

– Superintendencies» credit registries, large debtor analysis (supervisory reports)

– Tax authority, central banks» Labor claims, foreign credit lines

II. Understanding the demand for financial services

Enterprise and Household Demand for Financial Services 12Nairobi, May 15-17, 2006

Sample ICA data on financing of firms: Kenya

Enterprise and Household Demand for Financial Services 13Nairobi, May 15-17, 2006

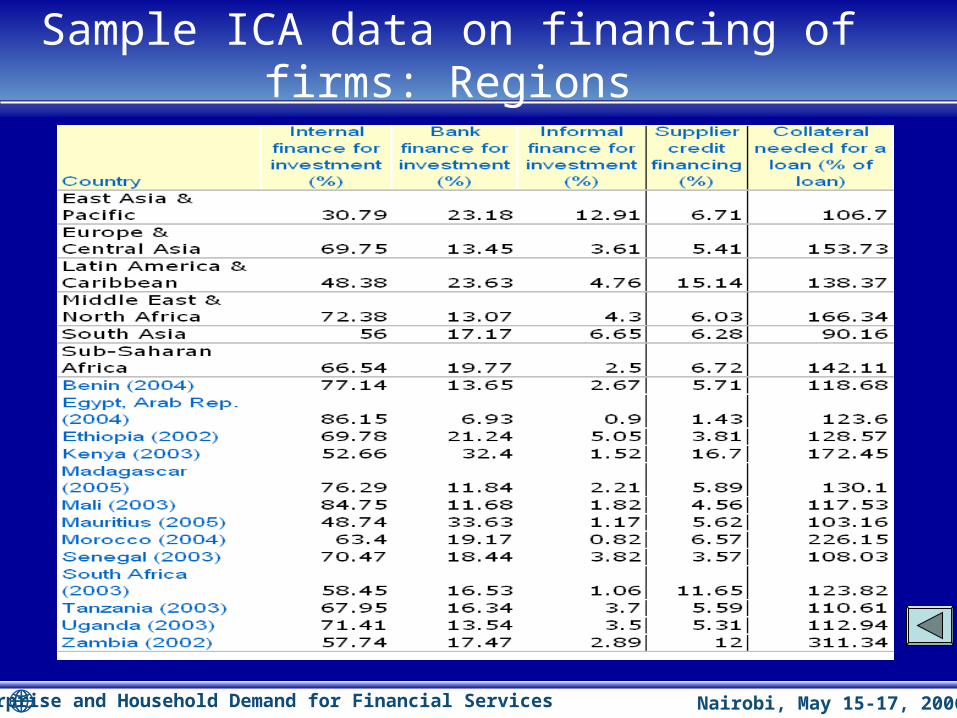

Sample ICA data on financing of firms: Regions

Enterprise and Household Demand for Financial Services 14Nairobi, May 15-17, 2006

3. Accounting and auditing standards• Transparency and availability of information

– Tax considerations

• Comparability of data across firms

• Quality of financial statements – Reporting requirements

II. Understanding the demand for financial services

Enterprise and Household Demand for Financial Services 15Nairobi, May 15-17, 2006

1. Recent trends• Concentration of debtors:

– By financial intermediary; – by quality of loans (NPLs by sectors);– Over-indebtedness

2. Performance: Financial ratio analysis• Leverage

– debt to equity, long-term debt to equity, long-term financial liabilities to equity

• Interest coverage– EBITDA to interest charges, EBITDA to (interest charges plus current portion

of long-term debt)

III. Assessing the financial health of firms

Enterprise and Household Demand for Financial Services 16Nairobi, May 15-17, 2006

• Current exposures – current assets to current liabilities

• Efficiency– operating and administrative costs to operating revenues, net margin

• Leverage– net income to sales, net income to equity

• Leverage– foreign currency debt to total debt

3. International benchmarking• Peer countries• Peer firms (by size, degree of financial development)

III. Assessing the financial health of firms

Enterprise and Household Demand for Financial Services 17Nairobi, May 15-17, 2006

1. Existing infrastructure• Credit bureaus and informational frameworks

• Payments systems – Small value; large transactions

• Titling and registries – quality

– speed

IV. Assessing legal and institutional constraints

Enterprise and Household Demand for Financial Services 18Nairobi, May 15-17, 2006

2. Legal and institutional aspects• Collateral and framework for execution• Framework for corporate restructuring and insolvency• Accounting and auditing standards; reporting standards• Credit culture• Capacity to systematically evaluate firms

2. Other aspects• Political and economic environment

– investment climate, business environment (e.g. doing business)

• physical infrastructure– Roads, ATMs, branches

IV. Assessing legal and institutional constraints

Enterprise and Household Demand for Financial Services 19Nairobi, May 15-17, 2006

• Important issues related to financial stability to better assess extent of exposures and mitigate effects

• Complement supply side analysis to enable deepening of financial markets and broadening of financial services

• Key aspects related to:– Unveiling exposures and analyzing worrisome trends

– Systematic analysis of firms’ health to assess large bank exposures

– Differentiation of agents by size, sectors, and characteristics to address specific demand needs

– Data constraints

– Supporting infrastructure, legal and institutional frameworks

– Lending booms- adequate measure of risks

V. Concluding remarks