engineering economics topics on pe exams

TRANSCRIPT

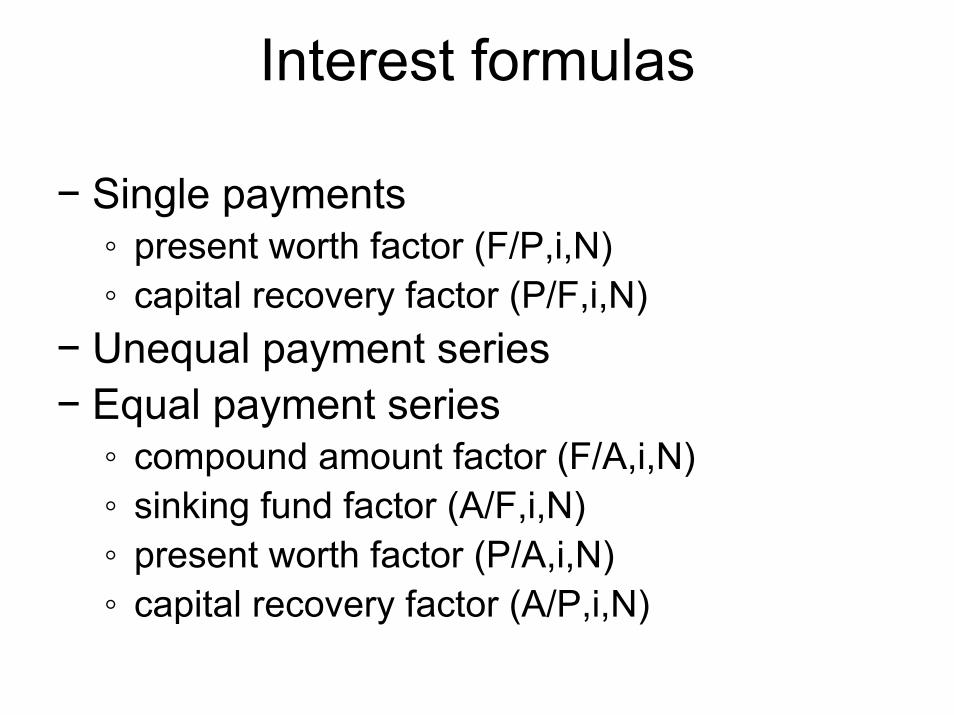

Interest formulas

− Single payments◦ present worth factor (F/P,i,N)◦ capital recovery factor (P/F,i,N)

− Unequal payment series− Equal payment series

◦ compound amount factor (F/A,i,N)◦ sinking fund factor (A/F,i,N)◦ present worth factor (P/A,i,N)◦ capital recovery factor (A/P,i,N)

Engineering economics topics on PE exams

− Annual cost− Breakeven analysis− Cost-benefit analysis− Future worth or value− Present worth− Valuation and depreciation

Retirement planning

A 21-year old inherits $100,000 from a distant relative who has deceased. She decides to spend some and invest the rest immediately in order to retire at 65 with a $1,000,000 savings account. At 8% interest compounded annually, how much must be invested?

Solution

$1,000,000 = P (1+0.08)44

P = $1,000,000/29.56 = $33,834

$100,000 - $33,834 = $66,166

Multiple payments

How much do you need to deposit today (P) to withdraw $25,000 at n=1, $3,000 at n = 2, and $5,000 at n =4, if your account earns 10% annual interest?

0

1 2 3 4

$25,000

$3,000 $5,000

P

Set up spreadsheet solution

Uneven payment series

$25,000

0

1 2 3 4

$5,000

P

$3,000

$25,000

$3,000

0

1 2 3 4

P1

0 0

1 2 3 4

P2

1 2 3 4

$5,000

P4

+ +

2 $3,000( / ,10%,2)$2,479

P P F==

4 $5,000( / ,10%,4)$3,415

P P F==

1 $25,000( / ,10%,1)$22,727

P P F==

P = P1 + P2 + P3 = $28,622

CheckBeginning balance

Interest earned

Payment Ending balance

n = 0 0 0 +28,622 28,622

n = 3 4,133 413 0 4,546

n = 1 28,622 2,862 -25,000 6,484

n = 2 6,484 649 -3,000 4,133

n = 4 4,546 455 -5,000 1

Rounding errorIt should be “0.”

College fund

Suppose you make an annual contribution of $100 each year to a college education fund for a niece. She is 4 years old now, and you will start next year and make the last deposit when she is 18. The fund is a money market account earning 6.5%/year. What will it be worth immediately after the last deposit?

Set up spreadsheet solution

Age nbeginning balance deposit interest

ending balance

4 0 0.00 0 0.00 0.005 1 0.00 100 0.00 100.006 2 100.00 100 6.50 206.507 3 206.50 100 13.42 319.928 4 319.92 100 20.79 440.729 5 440.72 100 28.65 569.36

10 6 569.36 100 37.01 706.3711 7 706.37 100 45.91 852.2912 8 852.29 100 55.40 1007.6913 9 1007.69 100 65.50 1173.1914 10 1173.19 100 76.26 1349.4415 11 1349.44 100 87.71 1537.1616 12 1537.16 100 99.92 1737.0717 13 1737.07 100 112.91 1949.9818 14 1949.98 100 126.75 2176.73

Equal payment series

0 1 2 N

0 1 2 N

A A A

F

P

0 N

Equal payment series – compound amount factor

0 1 2 N

0 1 2 NA A A

F

F

0 1 2N

A A A

Compound amount factor

0 1 2 N 0 1 2 N

A A A

F

A(1+i)N-1

A(1+i)N-2

F = A(1 + i)N-1 + A(1 + i)N-2 + ⋅⋅⋅ + A

Compound amount factorF = A(1 + i)N-1 + A(1 + i)N-2 + ⋅⋅⋅ + A

multiply by (1 + i):

F(1 + i) = A(1 + i)N + A(1 + i)N-1 + ⋅⋅⋅ + A(1 + i)

subtract:

F(1 + i) – F = A(1 + i)N – A

rearrange:

F = A(1 + i)N – 1

iFi = A(1 + i)N – A

Equal payment series compound amount factor(future value of an annuity)

0 1 2 3

F

A

F A ii

A F A i N

N

=+ −

=

( )

( / , , )

1 1N

Example• Given: A = $5,000, N = 5 years, and i = 6%• Find: F• Solution: F = $5,000(F/A,6%,5) = $28,185.46

Validation

nbeginning

balance deposit interestending balance

0 0.00 0 0.00 0.001 0.00 5000 0.00 5000.002 5000.00 5000 300.00 10300.003 10300.00 5000 618.00 15918.004 15918.00 5000 955.08 21873.085 21873.08 5000 1312.38 28185.46

Finding an annuity value(sinking fund factor)

0 1 2 3

A = ?

F

A F ii

F A F i N

N=+ −

=( )( / , , )1 1

N

Example:• Given: F = $5,000, N = 5 years, and i = 7%• Find: A• Solution: A = $5,000(A/F,7%,5) = $869.50

Equal payment series(uniform series)

Find the future worth of the following cash flow, assuming interest rate i.

0 1 2 3 4 N-3 N-2 N-1 N

$A $A $A $A $A $A $A $A

Custodial account

Suppose you decide to open a custodial account for your niece, who was born today. The minimum deposit is $100 on opening the account today, and you will put in $100 each year up to and including her 18th birthday. What is the account worth when it is turned over to the child at age 18? You expect to earn 10% interest per year.

Custodial account cash flow0 1 2 …

18$100 …

0 1 2 …(1 ) 1NiF Ai

⎡ ⎤+ −= ⎢ ⎥

⎣ ⎦ 18$100 …

18(1.10) 1$100 $4559.920.10

F⎡ ⎤−

= =⎢ ⎥⎣ ⎦

Custodial account cash flow

0 1 2 … 18

$100 …0 1 2 … 18

$100 …

Custodial account cash flow

0 1 2 … 18

$100 …0 1 2 … 19

$100 …-1 0 1 … 18

$100 …

Sinking fundYou are saving up money to make a 20% down

payment on a $100,000 house when you graduate in 4 years. You plan to invest $A at the end of each summer in a money market account earning 6.5%/year. Find A.

Sinking fundYou are saving up money to make a 20% down

payment on a $100,000 house when you graduate in 4 years. You plan to invest $A at the end of each summer in a money market account earning 6.5%/year. Find A.

F = A(1 + i)N – 1

i= A

(1 + 0.065)4 – 10.065

= $100,000

4.41 A = $100,000

A = $100,000/4.41 = $22,690

Annuity factor(capital recovery factor)

You want to obtain a loan of $20,000 to buy a used car. You will pay off the loan in yearly payments over the next 5 years. The salesman quotes a 6% annual interest rate and yearly payments of $4,878. Is $4,878 an accurate payment for this loan?

Annuity factor(equal series capital recovery factor)

F = A(1 + i)N – 1

i

A = F(1 + i)N – 1

i= P (1 + i)N

i(1 + i)N – 1

i (1 + i)N

A = P(1 + i)N – 1

A = P(A/P,i,N)

Annuity factor(capital recovery factor)

You want to obtain a loan of $20,000 to buy a used car. You will pay off the loan in yearly payments over the next 5 years. The salesman quotes a 6% annual interest rate and yearly payments of $4,878. Is $4,878 an accurate payment for this loan?

i (1 + i)N

A = P(1 + i)N – 1

0.06 (1 + 0.06)5

(1 + 0.06)5 - 1= $20,000

0.237 x $20,000 = $4,748

Deferred payments

Suppose you get a student loan for $8,000, and your payments are deferred until after you graduate, 2 years from now. Then, you will make 15 yearly payments (starting 2 years from now). What are your payments? The interest rate is 8%/year.

Deferred payments

Suppose you get a student loan for $8,000, and your payments are deferred until after you graduate, 2 years from now. Then, you will make 15 yearly payments (starting 2 years from now). What are your payments? The interest rate is 8%/year.

i (1 + i)N

A = P(1 + i)N – 1

0.08 (1 + 0.08)15

(1 + 0.08)15 - 1= $8,000

0.1168 x $8,000 = $934

Capital recovery factor (annuity factor)

Present worthYour father is about to get downsized out of his position. He has been

with the previous company through 3 previous mergers, and is disgusted with that nature of the business. He is considering retiring rather than seeking a new job. What would his retirement savings have to be worth today in order to withdraw $50,000/year for thenext 15 years? He expects to invest conservatively, earning 5% per year during his retirement years.

Present worthYour father is about to get downsized out of his position. He has been

with the previous company through 3 previous mergers, and is disgusted with that nature of the business. He is considering retiring rather than seeking a new job. What would his retirement savings have to be worth today in order to withdraw $50,000/year for thenext 15 years? He expects to invest conservatively, earning 5% per year during his retirement years.

(1 + 0.05)15 - 1(1 + i)N - 1P = A

i (1 + i)N= $50,000

0.05 (1 + 0.05)15

10.38 x $50,000 = $519,000

Present worth factor

Example: early savings plan – 8% interest

0 1 2 3 4 5 6 7 8 9 10 11 12

Option 2: Deferred Savings Plan

$2,000

0 1 2 3 4 5 6 7 8 9 10

44

Option 1: Early Savings Plan

$2,000

?

?

44

Option 1 – early savings plan

0 1 2 3 4 5 6 7 8 9 10

44

Option 1: Early Savings Plan

$2,000

?

F10 = $2,000 (F/A,8%,10) = $28,973

F44 = $28,973 (F/P,8%,34) = $396,645

Age 6531

Option 2: Deferred Savings Plan

0 11 12

44

Option 2: Deferred Savings Plan

$2,000

?

F44 = $2,000 (F/A,8%,10) = $317,233

At what interest rate would these two options be equivalent?

44

44

Option 1:$2,000( / , ,10)( / , ,34)

Option 2:$2,000( / . ,34)

Option 1 = Option 2$2,000( / , ,10)( / , ,34) $2,000( / . ,34)Solve for

F F A i F P i

F F A i

F A i F P i F A ii

=

=

=

123456789

101112131415161718192021224041424344454647

A B C D E F

Year Option 1 Option 201 (2,000)$ 2 (2,000)$ Interest rate 0.083 (2,000)$ 4 (2,000)$ FV of Option 1 396,645.95$ 5 (2,000)$ 6 (2,000)$ FV of Option 2 317,253.34$ 7 (2,000)$ 8 (2,000)$ Target cell 79,392.61$ 9 (2,000)$

10 (2,000)$ 11 (2,000)$ 12 (2,000)$ 13 (2,000)$ 14 (2,000)$ 15 (2,000)$ 16 (2,000)$ 17 (2,000)$ 18 (2,000)$ 19 (2,000)$ 37 (2,000)$ 38 (2,000)$ 39 (2,000)$ 40 (2,000)$ 41 (2,000)$ 42 (2,000)$ 43 (2,000)$ 44 (2,000)$

Using excel’s goal seek function

Result