energy efficiency trends and policies in spain · energy efficiency trends and policies in ... time...

TRANSCRIPT

Energy Efficiency Trends and Policies in SPAIN 1

Energy Efficiency Trends and Policies in SPAIN

National Report for the ODYSSEE-MURE Project

Planning and Studies Department

Madrid, 30th September 2015

Energy Efficiency Trends and Policies in SPAIN 2

Energy Efficiency Trends and Policies in SPAIN 3

Contacts:

Pilar de Arriba Segurado IDAE C/Madera, 8 28004 – Madrid - Spain Tel.: +34.914.564.900/ Fax: +34.915.230.414 E-Mail: [email protected] www.idae.es Jesús Pedro García Montes IDAE C/Madera, 8 28004 – Madrid - Spain Tel.: +34.914.564.900 / Fax: +34.915.230.414 E-Mail: [email protected] www.idae.es Carlos García Barquero IDAE C/Madera, 8 28004 – Madrid - Spain Tel.: +34.914.564.900 / Fax: +34.915.230.414 E-Mail: [email protected] www.idae.es

The sole responsibility for the content of this publication lies with the authors. It does not necessarily reflect the opinion of the European Communities. The European Commission is not responsible for any use that may be made of the information contained therein.

Energy Efficiency Trends and Policies in SPAIN 4

Energy Efficiency Trends and Policies in SPAIN 5

TABLE OF CONTENT

LIST OF FIGURES ............................................................................................................................................... 6

LIST OF TABLES ................................................................................................................................................. 8

0. EXECUTIVE SUMMARY ................................................................................................................................ 9

1. ECONOMIC AND ENERGY EFFICIENCY CONTEXT ........................................................................................ 12

1.1. ECONOMIC CONTEXT ........................................................................................................................ 12

1.2. TOTAL ENERGY CONSUMPTION AND INTENSITIES ............................................................................ 14

1.2.1.ENERGY CONSUMPTION TRENDS: BY FUEL AND BY SECTOR .................................................... 14

1.2.2.OVERALL TRENDS IN ENERGY INTENSITY .................................................................................. 17

1.3. ENERGY EFFICIENCY POLICY BACKGROUND ...................................................................................... 22

2. ENERGY EFFICIENCY IN BUILDINGS............................................................................................................ 27

2.1. ENERGY EFFICIENCY TRENDS ............................................................................................................. 27

2.1.1.THE HOUSEHOLD SECTOR ........................................................................................................ 28

2.1.2.THE SERVICES SECTOR .............................................................................................................. 34

2.2. ENERGY EFFICIENCY POLICIES ........................................................................................................... 38

2.2.1 THE HOUSEHOLD SECTOR ......................................................................................................... 41

2.2.2 THE SERVICES SECTOR .............................................................................................................. 41

3. ENERGY EFFIENCY IN TRANSPORT ............................................................................................................. 46

3.1. ENERGY EFFICIENCY TRENDS ............................................................................................................. 46

3.2. ENERGY EFFICIENCY POLICIES ........................................................................................................... 53

4. ENERGY EFFICIENCY IN INDUSTRY ............................................................................................................. 61

4.1. ENERGY EFFICIENCY TRENDS ............................................................................................................. 61

4.2. ENERGY EFFICIENCY POLICIES ........................................................................................................... 67

Energy Efficiency Trends and Policies in SPAIN 6

LIST OF FIGURES

Figure 1.1: Evolution of GDP in Spain and EMU .................................................................................................... 12

Figure 1.2: Macro-Economic Developments in Spain ........................................................................................... 13

Figure 1.3: Evolution of Primary Energy Consumption by sources in Spain, 2000-2013 ...................................... 14

Figure 1.4: Trends of Domestic Energy Production and Degree of Self Supply, 2000-2013 ................................. 15

Figure 1.5: Trends of Final Energy Consumption by Sources, 2000-2013 ............................................................. 15

Figure 1.6: Trends of Final Energy Demand by Sectors, 2000-2013...................................................................... 16

Figure 1.7: GDP Structure Trends by Sectors ........................................................................................................ 16

Figure 1.8: Trends of Primary Energy Intensity in Spain and EU, 2000-2013 ........................................................ 17

Figure 1.9: Impact of Energy Supply Structure on the Transformation System/Primary Intensity ....................... 18

Figure 1.10: Trends of Primary Energy Intensity at Purchasing Power Parities .................................................... 18

Figure 1.11: Trends of Primary and Final Intensities in Spain ............................................................................... 19

Figure 1.12: Trends of Final Energy Intensity in Spain and EU, 2000-2013 ........................................................... 19

Figure 1.13: Trends of Final Energy Intensity at purchasing power parities ......................................................... 20

Figure 1.14: Trends of Final Energy Intensity at Constant Structure, 2000-2013 ................................................. 20

Figure 1.15: Trends of Final Energy Intensity in Spain: Global and by Sectors, 2000-2013 .................................. 21

Figure 1.16: Energy Efficiency Progress by Sectors in Spain ................................................................................. 21

Figure 1.17: Time Distribution of the Accumulated Final Saving Energy Objective .............................................. 24

Figure 1.18: Distribution of the Final Energy Saving Objective (571 ktoe/year) by Sectors. ................................ 24

Figure 2.1: Share of Buildings in Final Energy Consumption in Spain, 2000-2013 ................................................ 27

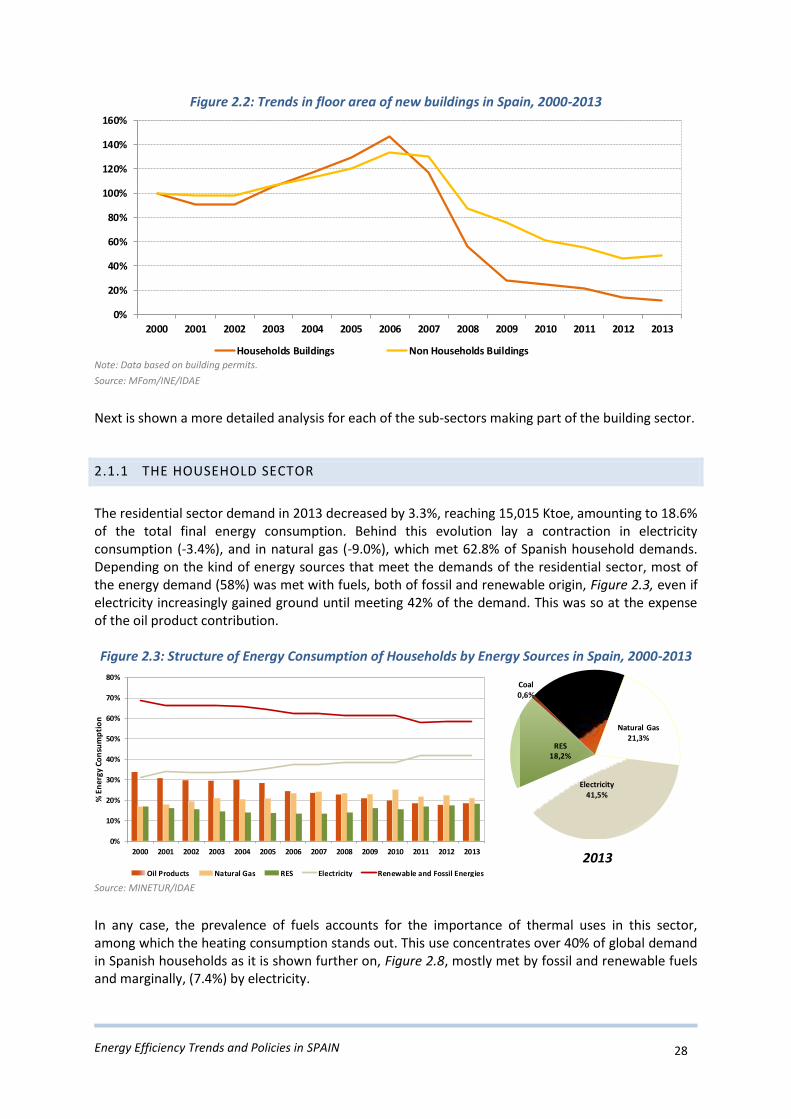

Figure 2.2: Trends in floor area of new buildings in Spain, 2000-2013 ................................................................. 28

Figure 2.3: Structure of Energy Consumption of Households by Energy Sources in Spain, 2000-2013 ................ 28

Figure 2.4: Trends of Income and Energy Consumption per Dwelling in Spain, 2000-2013 ................................. 29

Figure 2.5: Main Indicators of the Household Sector in Spain, 2000-2013........................................................... 30

Figure 2.6: Trends in Electricity Consumption per Dwelling in Spain and EU, 2000-2013 .................................... 30

Figure 2.7: Trends of Energy Intensity in the Household Sector in Spain and EU, 2000-2013 .............................. 31

Figure 2.8: Breakdown of the Energy Consumption by Uses in the Household sector in Spain and EU ............... 32

Figure 2.9: Energy Efficiency Progress in Households in Spain ............................................................................. 32

Energy Efficiency Trends and Policies in SPAIN 7

Figure 2.10: Decomposition of Household’s Energy Consumption Variation ....................................................... 33

Figure 2.11: Main Indicators in the Services Sector in Spain, 2000-2013 ............................................................. 34

Figure 2.12: Trends of Energy Intensity of the Services Sector in Spain and EU, 2000-2013................................ 35

Figure 2.13: Relevance and Structure of the Electricity Consumption in the Services Sector .............................. 35

Figure 2.14: Trends of Energy Intensity in the Services Sector by sub sectors in Spain, 2000-2013 .................... 36

Figure 2.15: Trends of Electricity Intensity of the Services Sector in Spain and EU, 2000-2013 ........................... 36

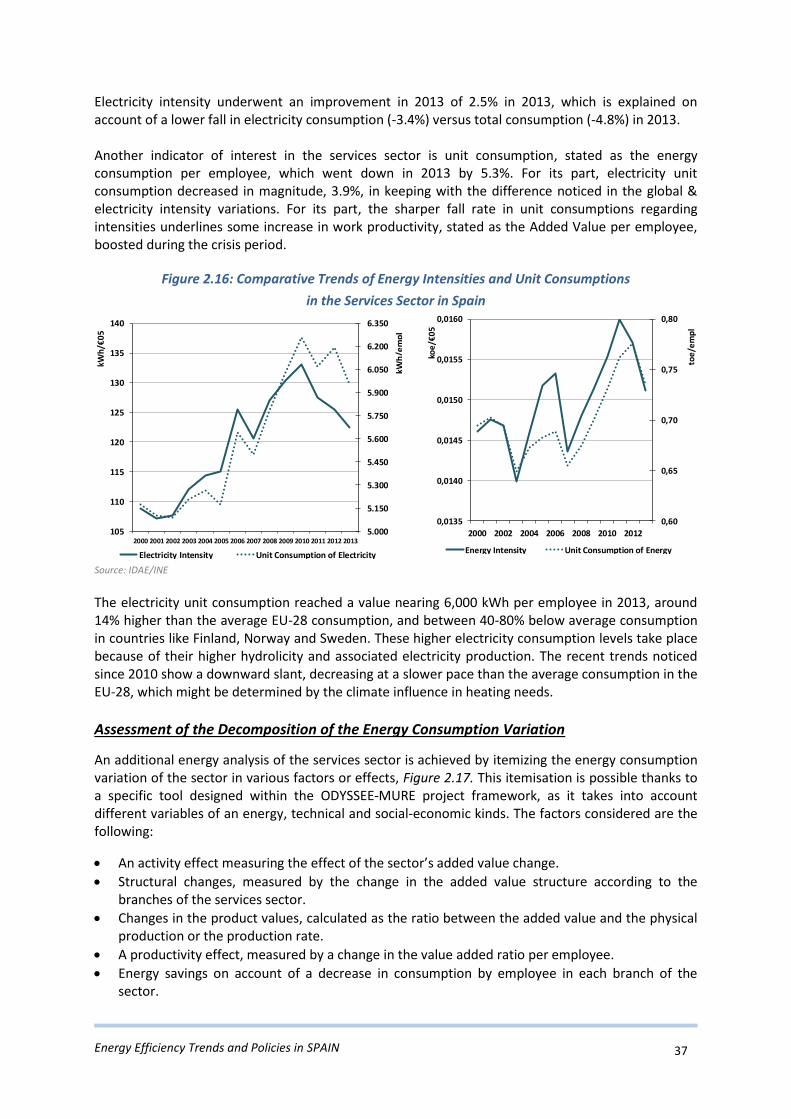

Figure 2.16: Comparative Trends of Energy Intensities and Unit Consumptions ................................................. 37

Figure 2.17: Itemization of Services’ Energy Consumption Variation ................................................................... 38

Figure 2.18: Development of Energy Efficiency Measures by type over time in the Residential Sector .............. 43

Figure 2.19: Development of Energy Efficiency Measures by type over time in the Services Sector ................... 43

Figure 2.20: Semi-quantitative Impact Evaluation in Buildings ............................................................................ 44

Figure 3.1: Trends of Traffic of Goods and Passengers in Spain, 2000-2013 ........................................................ 46

Figure 3.2: Trends of Energy Consumption by Transport Modes in Spain, 2000-2013 ......................................... 47

Figure 3.3: Variation of Energy Consumption by Transport Modes in Spain and the EU ..................................... 47

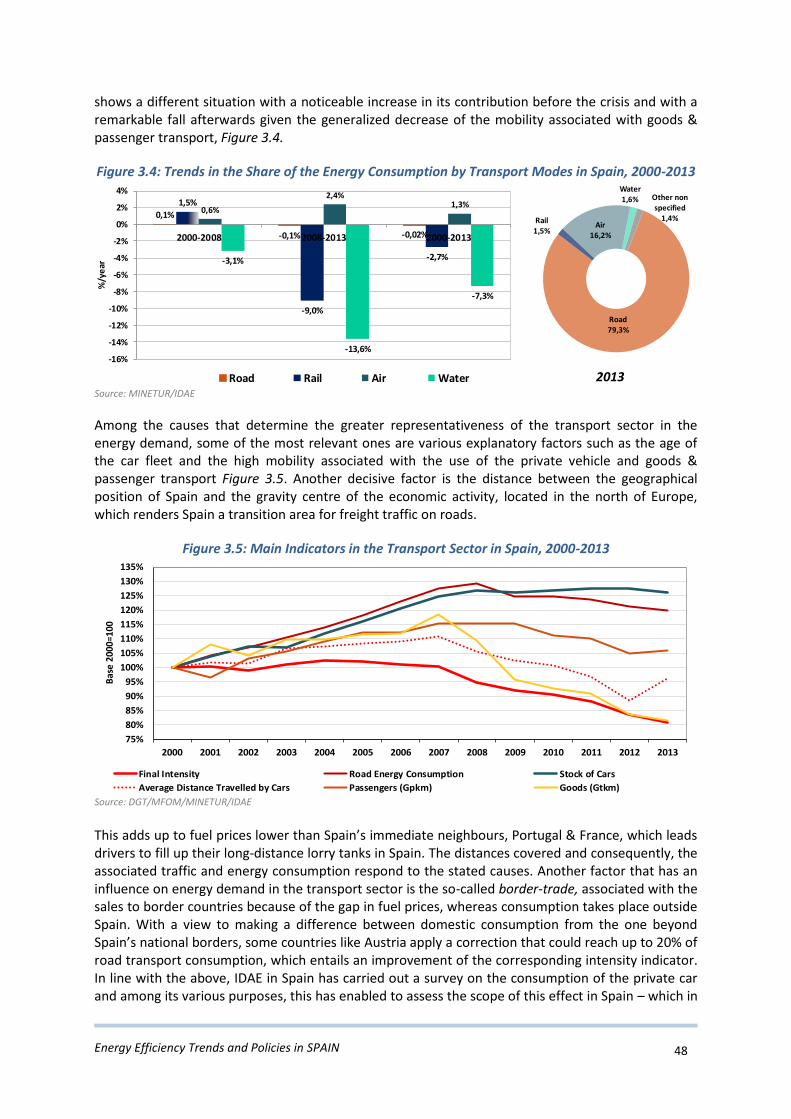

Figure 3.4: Trends in the Share of the Energy Consumption by Transport Modes in Spain, 2000-2013 .............. 48

Figure 3.5: Main Indicators in the Transport Sector in Spain, 2000-2013 ............................................................ 48

Figure 3.6: Energy Consumption in Goods and Passenger Transport in Spain, 2013 ........................................... 49

Figure 3.7: Energy Consumption in Road Transport by Types of Vehicle in Spain, 2013 ...................................... 49

Figure 3.8: Car Ownership in Spain and the EU .................................................................................................... 50

Figure 3.9: Trends of Unit Consumption and Average Annual Distance Travelled ............................................... 50

Figure 3.10: Trends in the Specific Consumption of New Cars in Spain ................................................................ 51

Figure 3.11: Trends of Energy Intensity in Transport Sector in Spain and EU, 2000-2013 ................................... 51

Figure 3.12: Energy Efficiency Progress in Transport in Spain .............................................................................. 52

Figure 3.13: Decomposition of Transport’s Energy Consumption Variation......................................................... 53

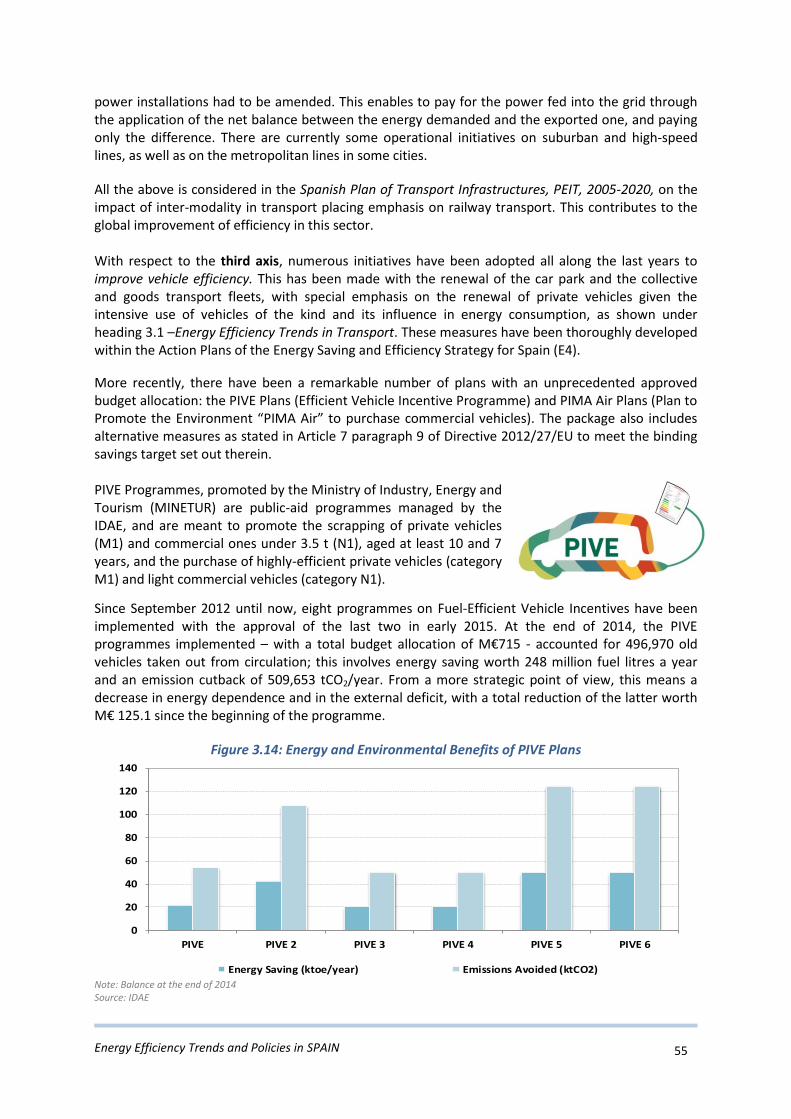

Figure 3.14: Energy and Environmental Benefits of PIVE Plans ............................................................................ 55

Figure 3.15: Development of Energy Efficiency Measures by type over time in the Transport Sector ................ 58

Figure 3.16: Semi-quantitative Impact Evaluation in Transport ........................................................................... 59

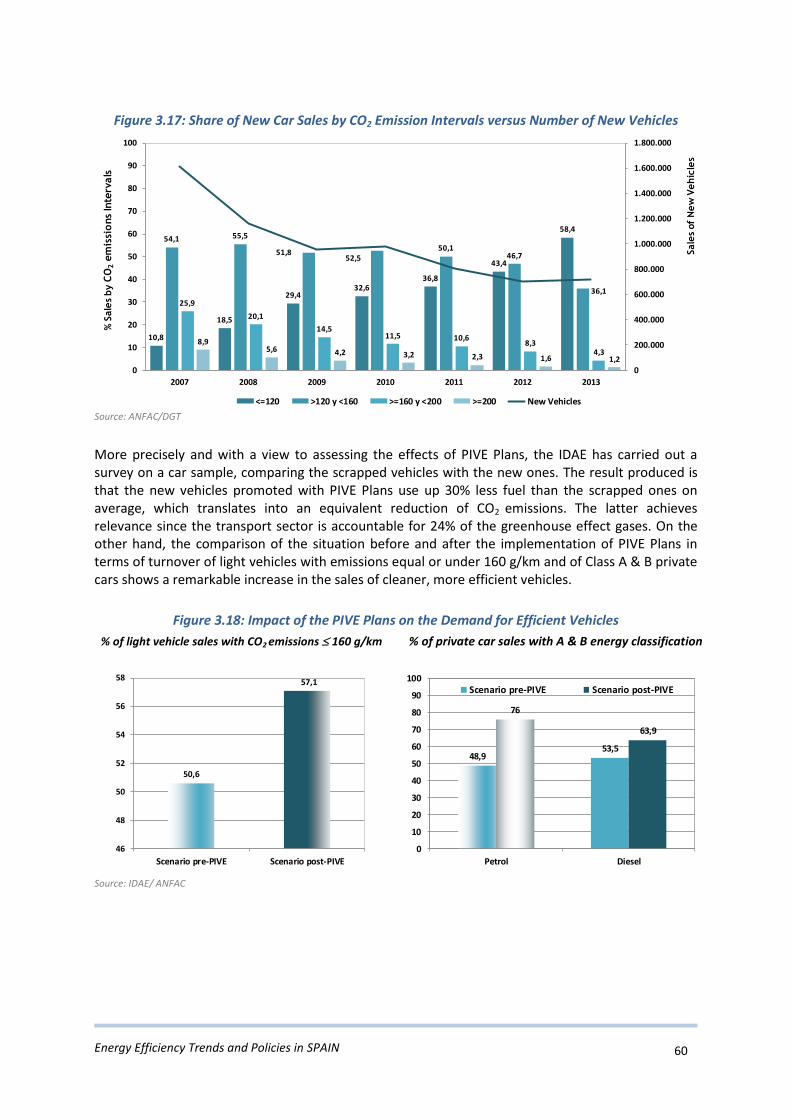

Figure 3.17: Share of New Car Sales by CO2 Emission Intervals versus Number of New Vehicles ........................ 60

Energy Efficiency Trends and Policies in SPAIN 8

Figure 3.18: Impact of the PIVE Plans on the Demand for Efficient Vehicles ....................................................... 60

Figure 4.1: Energy-Economic Characterization of the Industry Sector by branches in 2013 ................................ 61

Figure 4.2: Trends of Energy Intensity in Manufacturing Industry in Spain and EU, 2000-2013 .......................... 62

Figure 4.3: Changes in the Added Value Structure in Manufacturing Industry .................................................... 62

Figure 4.4: Trends of Energy Intensity in Industry Sector in Spain and EU, 2000-2013 ........................................ 63

Figure 4.5: Trends of Energy Intensity and Consumption in Intensive Industry Branches, 2000-2013 ................ 63

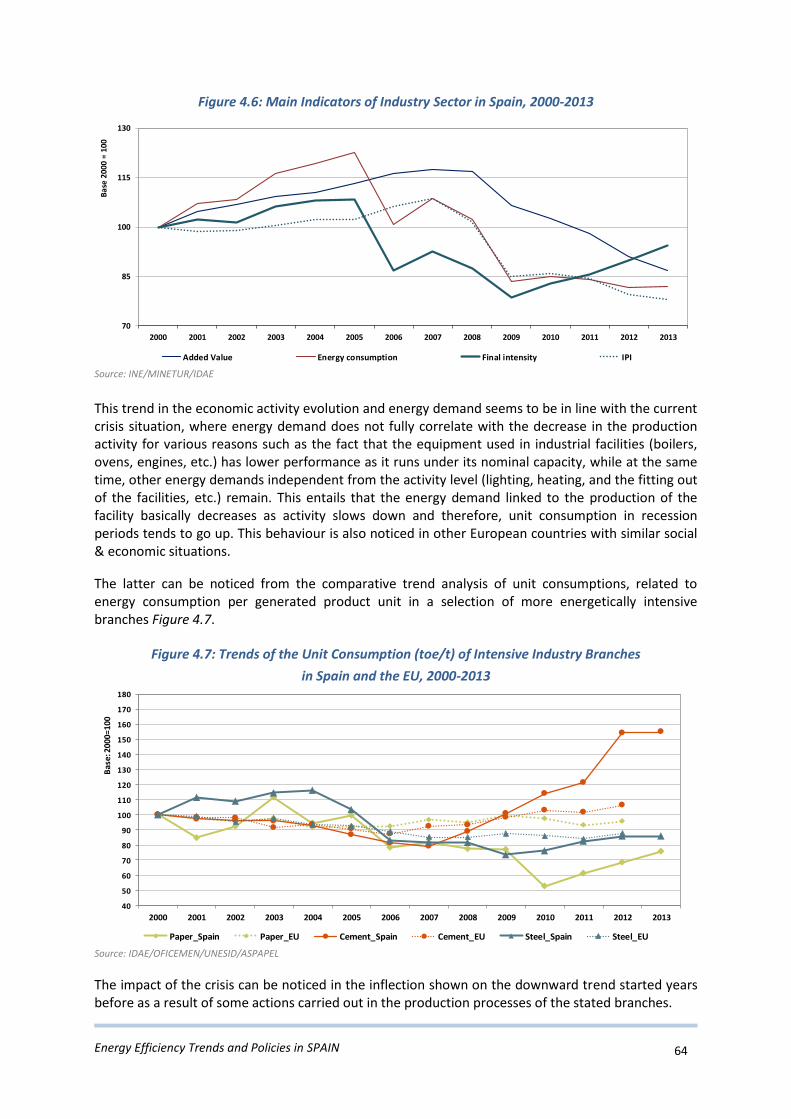

Figure 4.6: Main Indicators of Industry Sector in Spain, 2000-2013 ..................................................................... 64

Figure 4.7: Trends of the Unit Consumption (toe/t) of Intensive Industry Branches ........................................... 64

Figure 4.8: Effect of the Electrification in Industry in Spain .................................................................................. 65

Figure 4.9: Energy Efficiency Progress in Manufacturing Industry by Branches in Spain ..................................... 66

Figure 4.10: Decomposition of Industry’s Energy Consumption Variation ........................................................... 67

Figure 4.11: Development of Energy Efficiency Measures by type over time in the Industry Sector ................... 69

Figure 4.12: Semi-quantitative Impact Evaluation in Industry .............................................................................. 70

LIST OF TABLES

Table 1.1: Indicative Primary Energy Consumption Objective (ktoe) By Energy Sources ..................................... 23

Table 1.2: Indicative Final Energy Consumption Objective (ktoe) By Energy Sources .......................................... 23

Table 1.3: Final and Primary Energy Savings ......................................................................................................... 26

Table 2.1 : Ongoing Energy Efficiency Measures in Building Sector ..................................................................... 45

Table 3.1 : On going Energy Efficiency Measures in Transport Sector .................................................................. 59

Energy Efficiency Trends and Policies in SPAIN 9

0. EXECUTIVE SUMMARY

This report introduces Spanish national case for the Intelligent Energy Europe project “Monitoring of energy efficiency in the EU (ODYSSEE MURE 2012)”. It is divided into four chapters, introducing the most recent efficiency trends, both at general and sectoral level, as well as a general overview of the policies and efficiency measures applied in the last years. Chapter 1 accounts for a general context addressing the economic and energy situation in Spain, as well as the policies in force concerning energy planning, and more specifically, in terms of energy efficiency. Chapters 2, 3 and 4 focus on the building, transport and industry sector, respectively. The building sector analyses the situation within the residential and the tertiary sectors. Each chapter is divided into two parts: the first one accounts for an analysis of the energy efficiency trends in each sector, and the second illustrates the most relevant energy efficiency actions, particularly, the most recent ones. Energy supply in Spain has evolved in the last years towards a more diversified, balanced structure with the growing contribution of renewable energies and natural gas. This came along with an upward trend in energy demand during the first half of the former decade, and with the ensuing turning point from 2007 on. Since then, the situation has been on the wane, which has mainly contributed to a fall in the demand of oil and coal products. This trend became more dramatic from 2008 onwards under the effects of the economic crisis, which has been constraining since then the trends noticed in demand, both in terms of primary and final energy. Nevertheless, from the second half of 2013 on, a fledgling recovery scenario has been consolidating for Spanish economy. In this context, primary and final energy demand in 2013 recorded a decrease of 6.8% and 2.6%, respectively. The sharper fall of demand in primary energy responded to a greater contribution of renewable energies in the electric generation system, and particularly, in hydro energy with an increase of 79% in its production. The primary and final energy intensity followed the demand trend, showing a change in trend from 2004 till the beginning of the crisis in 2008 with a somewhat disruption in its evolution. In 2013 and in the stated context, primary and final energy intensity recorded improvements of 5.7% and 3.5% respectively as a result of the difference in the evolution of energy demands and of the Gross Domestic Product (GDP) (-1.2%) with regard to the former year. Various factors explain the improvement noticed in both indicators, such as the effects associated with electricity generation technologies based on renewable energies and natural gas; to structural and activity changes, enhanced by the current economic scenario, as well as to the impact of energy efficiency policies. The whole has had a repercussion on a moderate evolution of energy intensities. At final use sector level, some stabilization can be noticed in the consumption’s sector structure, with the transport sector ahead of it with nearly 40% of the total consumption, followed by the industrial sector with 25.7% of demand. The industrial sector keeps accounting for a progressive recoil which is at loggerheads with the growing role that the residential, services and agriculture sectors have been reaching - grouped under the category of “Various Uses” – and which at present accounts for 33.9% of demand. As for the energy intensities of the various sectors, the influence of the transport sector in global intensity stands out given its weight in the demand structure. To a lesser extent, the industrial sector is less affected, with a more volatile behaviour from the beginning of the crisis; and the residential sector. Virtually all the sectors with the exception of industry have shown an improvement trend

Energy Efficiency Trends and Policies in SPAIN 10

regarding their intensities. The residential sector in 2013 improved its intensity by 4.2%. The effects of a somewhat contention of demand, linked to households and motivated by the current economic scenario, overlapped those linked to the technological improvements in electric appliance equipment and household thermal installations. The favourable impact of legislative advances in the field of building also adds up to the above. The tertiary sector in 2013 underwent an improvement of its energy intensity of 3.8%. The evolution of intensity largely responds to the demand’s structure, highly represented in electric consumption. This explains the different behaviour of electric intensity, which has been rating over the EU-28 average in the last years in contrast with global intensity. In the last three years, both global and electric intensity revealed a downward trend possibly associated with the increase of electricity prices which has taken place since 2008. In the transport sector, energy intensity has maintained a downward trend since year 2004, reinforced by the current economic situation. This is one of the issues that have led to lower mobility associated with passenger and freight traffic. This situation prevailed in 2013 with a recorded decrease of 3.0% in the associated intensity. The industrial sector as a whole has recorded a deterioration of the intensity in recent years, coinciding with the beginning of the crisis. The manufacturing industry, for its part, has shown a downward trend since 2004, which seems to continue after the beginning of the crisis, even if with slight fluctuations. In 2013 the intensities of the global and the manufacturing industry increased by 5.2% and 3.2% respectively. In general terms, the change of the economic scenario has been affecting many a branch of industry, leading to certain uncoupling between the evolutions of the economic activity and of energy demand, which penalised the corresponding intensities. Among other factors, this responds to the fact that the used equipment runs under its nominal capacity affecting its performance. On the other hand, the more dramatic worsening of global industry is slightly linked to the recent evolution of the building sector, very much affected by the change in the economic situation.

According to the global energy efficiency index (ODEX)1, more appropriate for the analysis of energy efficiency, Spain accounts for a continued progress in energy efficiency in the period analysed from 2000 to 2013, and which counts on the contribution of all the sectors, namely the contribution of transport and industry sectors, with annual average improvement of 1%.

Spain has been doing its best for years to improve energy efficiency, taking into account the EU guidelines in force in the field of energy efficiency. This becomes evident in numerous actions, a large part of which are available on the MURE Database (www.mure2.com).

On a general level, one of the milestones is the recent approval of the National Action Plan on Energy Efficiency 2014-2020, in accordance with the requirements set out by Directive 2012/27/EU of the

1The ODEX index has been developed under the ODYSSEE project so as to have better understanding of energy efficiency progress, regardless of factors unrelated to efficiency. The results of the analysis based on this index can be contrasted with those obtained on the basis of energy intensities since the latter consider the influence of factors other than efficiency; this explains possible differences at sector-level analysis.

Energy Efficiency Trends and Policies in SPAIN 11

European Parliament and the Council, and the third (NEEAP3), in accordance with the provisions of article 14 of Directive 2006/32/EC, of 5 April 2006, on energy end-use efficiency and energy services. This plan is a continuation of previous plans approved within the framework of the Energy Saving and Efficiency Strategy for Spain 2004-2012 (E4) and the subsequent Action Plan 2011-2020 (NEEAP2). The Action Plan 2014-2020 considers a series of instruments and measures to meet the energy objectives assumed by Spain in relation to Articles 3 and 7 of the said Directive. As for the implementation of the second of these objectives, Law 18/2014, of 15 October, approving urgent measures for growth, competitiveness and efficiency, creates a national system of energy efficiency obligations as well as a national fund meant to finance energy efficiency mechanisms for economic, financial, technical assistance, training, information and other measures that help increase energy efficiency in the different sectors of final energy consumption. At sectoral level, the relevant ones are the transport and building sectors for being the recipients of the larger number of measures, consistent with the EU guidelines in force on energy efficiency. Regarding the transport sector, the most relevant measures aim at renewing the car fleet, particularly PIVE Plans and PIMA Air Plans, and at boosting electric mobility through initiatives such as the MOVELE Programme. Regarding the building sector, apart from the legislative progress compliant with Directive 2010/31/EU on the energy efficiency of buildings, there are a large number of actions aimed at the energy rehabilitation of buildings, focussing on public buildings given their exemplary role. Further details of the measures currently applied in the different sectors are available in Chapters 2, 3 and 4.

Energy Efficiency Trends and Policies in SPAIN 12

1. ECONOMIC AND ENERGY EFFICIENCY CONTEXT

1.1. ECONOMIC CONTEXT

The change in the economic situation, whose effects started becoming evident in Spain from the third term 2008 onwards, involves a large number of challenges for the consolidation of the recovery and the setting up of a new growth path on the basis of stability. A new scenario with a fledgling recovery of Spanish economy consolidated from the second half 2013, and therefore, it overcame the recession that had started two years earlier in the third term. The GDP has shown positive, if somewhat moderate, quarter-on-quarter growth rates, joined to a modest net job creation. A growth in consumption, investment in capital goods and an increase in employment have boosted a new recovery phase in economy. Nonetheless and despite the improvement slant all along the fiscal year, the GDP decreased by 1.2% in 2013, partly as a result of the bandwagon effect stemming from a dramatic decrease of activity in late 2012. From an expenditure point of view, national demand in 2013 went back to 2.7%, even if the contraction pace slowed down all along the year. For its part, net foreign demand contributed to the GDP growth for the sixth year. The foreign sector’s positive contribution is a reflection of the exports strength, which increased by 4.9% in 2013, whereas goods & services imports accounted for a slight advance (0.4%) after a two-year slump in a context of improvement in final demand. The increase in goods exports was largely due to the beginning of an investment cycle, which demanded the purchase of capital goods, many of which are not manufactured in Spain. For its part, export growth was motivated both by capital goods and tourist service exports in an exceptionally good year, which reached historic peaks both at income levels for this item and foreign tourist visits (60.7 million). The increase in exports, along with a decrease in the energy deficit favoured by the lower price of crude oil, contributed to the improvement of the trade deficit. Behind the positive evolution of the foreign demand lies the recovery of the world trade, as well as new gains in competitiveness. Both the Euro zone and the Economic Monetary Union (EMU) have taken part in the economic recovery, having registered positive GDP term-on-term growth rates from the second term 2013, Figure 1.1.

Figure 1.1: Evolution of GDP in Spain and EMU

Note: GDP in current prices

Source: OECD/INE

In a nutshell, the benchmarking of Spanish economy and of the main economies of the Spanish milieu accounts for some parallelism. Recently, this greater convergence has been constrained by the

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2007-Q1 2007-Q4 2008-Q3 2009-Q2 2010-Q1 2010-Q4 2011-Q3 2012-Q2 2013-Q1 2013-Q4

Inte

r-a

nn

ua

l gro

wth

Euro zone Spain

Energy Efficiency Trends and Policies in SPAIN 13

drive of international trade recorded in the second semester of 2013, as well as by the fiscal consolidation and structural reform processes registered in a large number of the surrounding countries. Among the private components of domestic expenditure, investment in capital goods shows an earlier recovery from the very beginning of the year; household consumption also joined this trend from the second term onwards. Household consumption accounts for recovery signs in the second half of 2013, after two years’ slum, especially dramatic at the end of 2012 given the impact of a set of measures for fiscal consolidation that affected household incomes. This consumption recovery has taken place in a slowing-down of the disposable income and of a more favourable evolution of the wealth financial household component. As for the public components of expenditure, subject to an adjustment process stated in 2012, its negative contribution to the activity decreased within a context of relaxation of fiscal requirements in mid-year. From the point of view of offer, the decreases in the added value of the various production branches in the annual average were lower in 2013 than in the previous year, and the best performance all along the fiscal year became evident in small upturns in industry and in market services from the third term on. The sector’s evolution was not homogeneous, so much so that the improvement concentrated, above all, on the more dependent branches of foreign demand.

Figure 1.2: Macro-Economic Developments in Spain

Source: INE/IDAE

The good performance of the automotive sector, whose production was favoured by foreign demand and the positive impact of the various governmental plans to boost car purchase, stands out among the manufacturing industry branches. Moreover, the thrust of the latter branch has brought about the advance of specific automotive industries, such as rubber or plastic products. In like manner stands out the positive performance of sectors as the textile and others of high-technological content. Among the market services, the most outstanding performance recorded was the one of the branches linked to tourism and transport. On the other hand, trade stepped back somehow dramatically, as a result of the weak domestic demand. Finally, construction became again the sector with the greatest regression, in accordance with the dramatic contraction of demand, both public and private. This latter sector had been the driving force of Spanish economy for over a decade, and consequently, its decline worsened the effect of the crisis on the national economy.

60%

70%

80%

90%

100%

110%

120%

130%

140%

150%

160%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Bas

e 2

00

0=1

00

GDP (€05) VA_Services (€05) VA_Construction (€05)

VA_Agriculture (€05) VA_Manufacturing Industry (€05) Private Consumption (€05)

Energy Efficiency Trends and Policies in SPAIN 14

1.2. TOTAL ENERGY CONSUMPTION AND INTENSITIES

1.2.1. ENERGY CONSUMPTION TRENDS: BY FUEL AND BY SECTOR

The primary energy consumption in Spain has evolved in recent years towards a more diversified, balanced structure, with greater contribution of renewable energy and natural gas sources, Figure 1.3. This has come along an upward trend in energy demand, which shows a turning point for year 2007. From then on, a decreasing path took place, which essentially involved a slump in the demand of oil and coal products. This trend became worse from year 2008 under the effects of the economic crisis, whose greater impact took place in 2009 with a regression in the demand of primary energy of 8.6%. Later on, a period of greater stability opened up, with a downward trend for 2009-2012, and a reduction in consumption in 2013 of 6.8% as compared to the previous year, standing at 120,447 ktoe.

Figure 1.3: Evolution of Primary Energy Consumption by sources in Spain, 2000-2013

Note: Non- renewable wastes included in petrol; *small Hydro in Hydraulic

Source: MINETUR/IDAE

This last reduction resulted from the decrease in the demand of all conventional energy sources, specifically of coal (-26.4%), nuclear power (-7.7%), natural gas (-8.7%) and oil (-5.0%) - the latter two ones being accountable for 66.4% of demand. Renewable energies, with an increase of 8.0%, partially compensated a fall in the demand of conventional sources. In 2013 within renewable energies is to be highlighted an increase of 79% in hydro contribution, resulting from the greater availability of water resources in contrast with previous years’ trends. Solar and wind energy also stand out, with respective increases of 11.2% and 9%. The evolution of biomass, biogas and biofuels was not that favourable, recording regression in their corresponding demands – particularly remarkable in the case of biofuels with a slump of 57.3% in demand. Globally, the evolution of renewable energies in 2013 involved an improvement on meeting the primary energy demand, reaching 14.4% versus 12.4% of the previous year. The autochthonous production potential from the various energy sources, along with an evolution in the structure of energy supply towards greater diversification, Figure 1.4, points to a capacity of self-supply. National energy dependence has reached at present 71.4%, nearly 20 percentage points over the European average. Despite this, the evolution of renewable energies since year 2005 is a remarkable fact, featured by their progressive introduction in the energy system, which has led to an autochthonous production, similar or even higher than the nuclear one. This translated into a somehow better energy self-supply, which amounted to 28.6% in 2013.

0

15.000

30.000

45.000

60.000

75.000

90.000

105.000

120.000

135.000

150.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Kto

e

Electrical Balance Other RES Hydraulics* Nuclear Natural Gas Coal Oil

Energy Efficiency Trends and Policies in SPAIN 15

Figure 1.4: Trends of Domestic Energy Production and Degree of Self Supply, 2000-2013

2013

Note: Non-renewable waste included in petrol

Source: MINETUR/IDAE

The analysis of the evolution of final energy demand by sources, Figure 1.5, shows a profile similar to the primary energy one, accounting for the same peculiarities in their global evolution. In 2013 and under the effects of the crisis, final energy consumption – non-energy uses excluded – recorded a fall of 2.6%, finally standing at 80,836 ktoe. This evolution represents a deceleration in the rate of decrease with respect to the previous year, when demand fell by 4%.

Figure 1.5: Trends of Final Energy Consumption by Sources, 2000-2013

2013 Note: Non-energy uses excluded

Source: MINETUR/IDAE

The 2013 situation basically responds to the lower demand associated with oil products (-2.2%) and electricity (-3.4%), who jointly represent 73% of the global final energy demand. The transport and industry sectors are behind this evolution, given the weight of these two energy sources in the said sectors and their sensitivity on facing the current crisis. Renewable energies, for their part, have seen their demand reduced by 16% in terms of final energy. This fact is essentially due to the evolution undergone by biofuels (-57.3%) and, to a lesser extent, to the fall in the demand of biogas (-15.1%), associated with a lower use of co-generation plants running on biogas. As whole, renewable energies in 2013 have involved meeting a 6.5% global energy demand, a lower contribution than the previous year’s, put at 13.7%. Biomass, with an increase of 5.3% in demand, remains the most representative renewable resource of final use, which reached 77.1% of the renewable energy contribution to final energy demand.

20%

21%

22%

23%

24%

25%

26%

27%

28%

29%

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

De

gre

e o

f Se

lf S

up

ply

(%)

Kto

e

Oil Natural Gas Coal RES Nuclear Degree of self supply

Coal5,1%

Oil1,5%

Natural Gas0,1%

Nuclear42,9%

RES50,3%

Geotermia

0

15.000

30.000

45.000

60.000

75.000

90.000

105.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Kto

e

Electricity RES Natural Gas Coal Oil Products

Coal1,9%

Oil Products48,8%

Natural Gas17,9%

Electricity24,7%

RES6,7%

Energy Efficiency Trends and Policies in SPAIN 16

Considering the final energy demand by sectors, some stabilization in the consumption sectoral structure is noticed, placing the transport sector at the head with nearly 40% of total consumption, Figure 1.6. The former is followed by the industrial sector, with 25.7% of the demand, with a downward trend in its relative weight on demand, compensated by the whole of the sectors grouped under the category of “Miscellaneous Uses”2. This category is gaining ground, and has now overcome the industry one from the year 2006, meeting at present as much as 33.9% of demand.

Figure 1.6: Trends of Final Energy Demand by Sectors, 2000-2013

2013 Note: Non-energy uses excluded

Source: MINETUR/IDAE

This relative loss of weight of the industry sector in the global energy demand goes along with a cutback in its contribution to the GPD within the context of a progressive switch to the services sector in Spanish economy.

Finally, at a comparative level, among the EU-28 countries, Spain holds the fifth position in terms of primary and final energy consumption, occupying a more distant position concerning per capita consumption – precisely, 19th position.

Figure 1.7: GDP Structure Trends by Sectors

2000

2008

2013

Source: INE/IDAE

2 The “Miscellaneous Uses” sector includes the residential, services, agriculture and other sectors.

0

15.000

30.000

45.000

60.000

75.000

90.000

105.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

kto

e

Transport Industria Households Services Agriculture&Fisheries Other

Industria 25,7%

Transport 39,4%

Households

18,6%

Services 11,8%

Agriculture

&Fisheries 3,5%

Otros 1,0%

Agriculture 3,6%

Energy Branches

2,2%

Manuf. Industry

15,7%

Construc. 10,6%

Services 58,3%

Taxes 9,6%

Agriculture 2,7%

Energy Branches

2,5%

Manuf. Industry

13,6%

Construc. 9,8%

Services 61,8%

Taxes 9,7%

Agriculture 3,1%

Energy Branches

2,9%

Manuf. Industry

12,1%

Construc. 5,7%

Services 67,4%

Taxes 8,8%

Energy Efficiency Trends and Policies in SPAIN 17

1.2.2. OVERALL TRENDS IN ENERGY INTENSITY

The evolution of the primary energy intensity indicator in Spain shows a profile compliant with the primary energy demand, and displays a trend change from 2004 until the beginning of the crisis in 2008; from then on, its evolution accounts for some kind of imbalance. As it happened with other neighbouring countries, the crisis had an impact on economy, leading to a disruption in the energy intensity evolution – largely due to the effects bound to structural and activity changes – which, in general terms, intensified the downward trend in energy demand and its associated intensity. Prior to the current crisis, there was a sustained improvement in primary energy intensity, bringing closer the trends of the national and European indicators, even with a higher record of the national indicator than its average EU counterpart. This convergence in the trends of both indicators still remains. During the period 2004-2012, there was an annual average improvement of 1.96% in Spain, slightly higher than the corresponding EU average (1.90%), Figure 1.8.

Figure 1.8: Trends of Primary Energy Intensity in Spain and EU, 2000-2013

Source: EnR/IDAE

There are miscellaneous factors behind the improvement noticed in the domestic indicator, among which, the favourable effect stemming from electric generation technologies based on renewable energies and natural gas (co-generation and combined cycles). Thus, the improvement in the transformation performance of these technologies and energy sources, along with the positive effect of a decentralised generation linked to co-generation and renewable energies had an impact on the improvement in the energy efficiency of the transformation system, Figure 1.9. This effect is joined by the one derived from structural changes in the Spanish economy, somehow prior to and independent from the crisis, as well as by the impact of the energy efficiency policies. All of it has a bearing on the moderate evolution of the primary energy intensity. In this context, in 2013 there was an improvement of 5.7% in primary energy intensity as a result of the differential evolution in primary energy demand (-6.8%) and of the Gross Domestic Product (GDP) (-1.2%) as compared to the previous year. This improvement is in line with the upturn noticed in hydro production in 2013, representing an improvement in the transformation system performance as compared to the previous year when lower water resources made it necessary to start running coal-based power plants. This effect is enhanced by the lower demand brought about by a decrease in the activity and production of final use sectors, largely as a result of the economic crisis.

0,075

0,090

0,105

0,120

0,135

0,150

0,165

0,180

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

koe

/€05

EU-28 France Alemania Italy Spain UK Ireland Portugal

Energy Efficiency Trends and Policies in SPAIN 18

Figure 1.9: Impact of Energy Supply Structure on the Transformation System/Primary Intensity

Source: MINETUR/IDAE

An additional analysis has been made on the basis of the intensity adjusted for purchasing power parity, Figure 1.10. This kind of adjustment enables a more realistic benchmarking of intensities at international level, given that it introduces a correction on the differences between countries in terms of prices and purchase power. This enables a vertical shift of the rated currents, improving the relative position of countries with a lower GDP. In the case of Spain, the adjusted intensity maintains the former profile, even if it improves its position as it has increased its distance with the EU average in its favour.

Figure 1.10: Trends of Primary Energy Intensity at Purchasing Power Parities

in Spain and EU, 2000-2013

UE28 = Reference; Source: ODYSSEE/IDAE

The decreasing evolution of final energy demand at a faster slump pace than the economy’s productivity led to a fall of 3.5% in final energy intensity. The most dramatic primary intensity fall as compared to the final one is due to the greater contribution of renewable energies in the electric generation system, and particularly, of hydro power with an increase in production of 79%.

70%

73%

76%

79%

82%

85%

88%

91%

94%

97%

100%

103%

106%

109%

112%

115%

118%

121%

124%

127%

130%

-75%

-55%

-35%

-15%

5%

25%

45%

65%

85%

105%

125%

145%

165%

185%

205%

225%

245%

265%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Co

ntr

ibu

tio

n t

o P

rim

ary

Ene

rgy

De

man

d(%

)2

00

0=1

00

RES Natural Gas Oil Coal Nuclear Transformation System Eff. Primary Intensity

Pri

mar

y En

erg

y In

ten

sity

/Tr

ansf

orm

atio

n S

yste

m E

ffic

ien

cy (%

)2

00

0=1

00

0,075

0,090

0,105

0,120

0,135

0,150

0,165

0,180

0,195

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

koe/

€05p

EU-28 France Germany Italy Spain UK Ireland Portugal

Energy Efficiency Trends and Policies in SPAIN 19

Figure 1.11: Trends of Primary and Final Intensities in Spain

Source: IDAE

The drop noticed in final intensity is in line with the structural and activity effects of the crisis on the economic activity, and therefore, on the relevant demand of final energy. A benchmarking of this indicator regarding Spain’s surrounding countries, Figure 1.12, shows a convergence from year 2004 as it happens with the primary energy indicator. The evolution since then and until year 2009 accounts for a parallelism between the national and the EU indicators at an annual improvement pace higher than in the case of the national indicator. In recent years and under the impact of the crisis on both indicators, an improvement of the national annual average in Spain of 2.4% can be noticed for the period 2004-2012, above the 1.8% rate recorded for the whole of the EU in the said period.

Figure 1.12: Trends of Final Energy Intensity in Spain and EU, 2000-2013

Note: Non-energy uses excluded Source: ODYSSEE/IDAE

The analysis of the final intensity indicator adjusted for purchasing power parity, Figure 1.13, provides similar conclusions and improves the domestic position with respect to the European average in an analogous way, as shown on Figure 1.10, corresponding to the same adjustment on primary energy intensity.

60%

65%

70%

75%

80%

85%

90%

95%

100%

105%

110%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

20

00

=10

0

Primary Intensity (Kep/€2005) Final Intensity (Koe/€2005)

0,060

0,075

0,090

0,105

0,120

0,135

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

koe/

€05

EU-28 France Germany Italy Spain UK Ireland Portugal

Energy Efficiency Trends and Policies in SPAIN 20

Figure 1.13: Trends of Final Energy Intensity at purchasing power parities

in Spain and EU, 2000-2013

Note: Non-energy uses excluded

Source: ODYSSEE/IDAE

The aforementioned structural effect is made evident from the evolution benchmarking of the real final energy intensity and the corresponding one to the constant structure of year 2005, Figure 1.14. As it can be noticed, the structural effect was predominant from year 2008 while in the previous period other factors were more predominant, such as the ones linked to technological improvements and efficiency policies.

Figure 1.14: Trends of Final Energy Intensity at Constant Structure, 2000-2013

Notes: Intensities with climate correction; Non-energy uses excluded Source: IDAE/ODYSSEE

The comparison of the evolution in relative terms of final energy intensities at sectoral and global level, Figure 1.15, accounts for a differentiation of the trends followed by the final use sectors in the various analysis periods. The global intensity shows the transport sector influence, given the weight of this sector in the demand structure. To a lesser extent are affected the industry sector, with a more volatile performance from the beginning of the crisis, and the residential sector, which encompasses Spanish households, and whose energy demand shows a somewhat contention.

0,060

0,075

0,090

0,105

0,120

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

koe

/€0

5p

EU-28 France Germany Italy Spain UK Ireland Portugal

0,080

0,083

0,086

0,089

0,092

0,095

0,098

0,101

0,104

0,107

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

ko

e/€

05

Final Intensity at Constant Structure Final Intensity

Structural Effect

-0,67%

-1,09%

-0,58%

-2,25%

-1,85%

-3,18%-3,40%

-3,10%

-2,80%

-2,50%

-2,20%

-1,90%

-1,60%

-1,30%

-1,00%

-0,70%

-0,40%

-0,10%

2004-2013 2008-2013 2004-2008

An

nu

al A

vera

ge V

aria

tio

n (%

/yea

r)

Structural Effect Real Variation

Energy Efficiency Trends and Policies in SPAIN 21

Figure 1.15: Trends of Final Energy Intensity in Spain: Global and by Sectors, 2000-2013

Note: Non-energy uses excluded

Source: MINETUR/IDAE

Assessment of Energy Efficiency through ODEX

Energy intensity is usually used to value the energy efficiency trends at global and sectoral level. Nonetheless, the evolution of the final energy intensity can be due to different factors away from energy efficiency as, for example, the structural changes of economy, changes in lifestyle, etc.; these factors should be strictly separated so as to have a better understanding of the energy efficiency progress. To this end, an alternative indicator has been developed, the ODEX index, which happens to be more appropriated. This index allows a better analysis of efficiency for each sector, combining the trends of indicators for each sub-group or each final use. In compliance with this index, Figure 1.16, Spain accounts for a continuous energy efficiency progress in the analysed period 2000-2013, where all the sectors take part. In this framework stand out the transport and industry sectors, with annual average improvements of 1%. This is coherent with the contents in Figure 1.15.

Figure 1.16: Energy Efficiency Progress by Sectors in Spain

Note: The progress of the ODEX index in the household sector is underestimated because of the lack of detailed information on the energy consumption of the stock of electrical household appliances

Source: IDAE/ ODYSSEE

70%

80%

90%

100%

110%

120%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Bas

e 2

00

0=1

00

Final Intensity Industry Transport Services Households

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

FinalIntensity

Industry Transport Services Households

Bas

e 2

00

4=1

00

2004 2009 2013

80

85

90

95

100

105

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Bas

e 2

00

0=1

00

Global ODEX Industry Transport Households

Energy Efficiency Trends and Policies in SPAIN 22

1.3. ENERGY EFFICIENCY POLICY BACKGROUND

Currently in Spain stand out two remarkable planning tools that define the priorities in energy policy matters for the 2020 horizon: the Action Plan on Energy Saving and Efficiency 2014-2020 and the Renewable Energies Plan 2011-2020. They are meant to carry out a transition towards a more sustainable energy model where autochthonous renewable energies take up greater relevance at the time of meeting a more moderate energy demand, thanks to the implementation of energy saving and efficiency policies.

In the area of renewable energies, the Renewable Energies Plan (PER) 2011-2020, approved in Cabinet Meeting Agreement of 11 November 2011, establishes the objectives complying with Directive 2009/28/EC of the European Parliament and the Council, of 23 April 2009, on the promotion of the use of energy from renewable sources. The PER 2011-2020 includes a package with over 80 measures to meet the EU requirements, reaching the national objectives by 2020 established in the Plan, and which will represent, according to the methodology of the above Directive, a renewable energy consumption rate of 20.8% on the gross final energy consumption, as well as a final consumption rate of the former of 11.3% over the transport energy consumption.

Concerning the energy efficiency area, the Action Plan on Energy Saving and Efficiency 2014-2020 means to respond to the obligation set forth by Directive 2012/27/EU of the European Parliament and of the Council, of 25 October 2012 on energy efficiency (EED), according to which all State Members of the European Union are demanded to submit national Action Plans on energy efficiency - the first of which should be by 30 April 2014 at the latest, and then, every three years.

This Action Plan makes up the first Action Plan within the framework of Directive 2012/27/EU and the third one (NEEAP3), in compliance with the provisions of article 14 of Directive 2006/32/EC on energy end-use efficiency and energy services. This Plan gives continuity to the former plans approved within the framework of the Energy Saving and Efficiency Strategy for Spain 2004-2012 (E4), as well as further Action Plan 2011-2020 (NEEAP2).

The approval of the DEE has entailed the adoption on the part of all the State Members of two energy saving and efficiency objectives: the first one, indicative and set up by each State Member, in compliance with article 3 of the said Directive, and the second, binding and calculated in compliance with its article 7.

With regards to the indicative objective and taking into account the evolution of the macroeconomic scenario, Spain has submitted to the European Commission a new energy consumption objective in 2020, equivalent to 110.9 Mtoe in terms of primary energy: this entails a reduction in consumption of primary energy of 42.8 Mtoe in the trend scenario. This consumption objective is coherent with the one set up by the EU for the 2020 horizon — 1, 474 Mtoe of primary energy.

Once included non-energy consumptions, the primary energy consumption objective for 2020 is put at 125.280 Mtoe. Table 1.1 accounts for the estimated primary energy balance until 2020. The envisaged situation highlights an increase in the contribution of renewable energies and natural gas to meet the demand, at the expense oil-derivative product consumption, essentially as a result of the foreseen cutback on petrol and fuel oil for transport.

Energy Efficiency Trends and Policies in SPAIN 23

Table 1.1: Indicative Primary Energy Consumption Objective (ktoe) By Energy Sources

2020

Coal 13,652

Oil 46,026

Natural Gas 30,276

Nuclear 15,549

Renewable Energies 20,406

Non Renewable Wastes 319

Electricity Balance (Imp.-Exp.) -946 TOTAL 125,280

TOTAL Non-energy uses excluded 119,893

Source: MINETUR

As for final energy, Table 1.2, consumption estimates point to an increase in the relevance electric power and renewable energies consumption, and to a decrease in the relevance of oil products. The total final energy for energy uses in 2020 is estimated at 80.1 Mtoe.

Table 1.2: Indicative Final Energy Consumption Objective (ktoe) By Energy Sources

2020

Coal 1,753

Oil Products 33,771

Natural Gas 15,710

Electricity 2,.928

Renewable Energies 6,977

TOTAL 80,139

Note: Non-energy uses excluded

Source: EnR/IDAE

The consumption estimates of both primary and final energy consumption by 2020 may be revised to be adapted to other macroeconomic scenarios that may be officially adopted by Spain on the occasion of the next annual report, and have to be submitted before the end of April 2015 in compliance with article 3 of Directive 2012/27/EU. As regards the second objective, article 7 of the EED compels every Member State to reach a binding saving objective of accumulated final energy for the period 2014-2020. According to this, Spain has set up a saving objective of 15,979 ktoe between 2014 and 2020, the equivalent to an annual saving objective of 571 ktoe – assuming a linear distribution all along the engagement period. The achievement of the said saving objective requires high investments of both a public and private kind in actions, basically, to renew equipment and processes in the industrial sector, heating installations and heating & cooling and lighting installations in the building sector (either residential or tertiary use) or renew the building envelope, as well as in measures to make a more efficient use of means of transport. As for the implementation of this objective, Law 18/2014, of 15 October, approving urgent measures for growth, competitiveness and efficiency, creates a national system of energy efficiency obligations as well as a national fund meant to finance energy efficiency mechanisms for economic, financial, technical assistance, training, information and other measures that help increase energy efficiency in the different sectors of final energy consumption. Moreover, the implementation of other alternative measures allowed by the Directive is envisaged:

Energy Efficiency Trends and Policies in SPAIN 24

measures of a fiscal, regulatory, training kind, as well as communication campaigns, etc.

Figure 1.17: Time Distribution of the Accumulated Final Saving Energy Objective

Source: IDAE

As regards the sectoral distribution of the final energy annual saving objective (571 ktoe/year), Figure 1.18, the industry sector stands out with 54.6% of the saving objective. The most relevant measure is the adoption of the best available technologies for equipment and processes, and to a lesser extent, the introduction of energy management systems.

Figure 1.18: Distribution of the Final Energy Saving Objective (571 ktoe/year) by Sectors.

Source: IDAE

25.3% of the saving objective will be reached thanks to measures in the transport sector, namely, measures for modal change, sustainable urban mobility actions, and workplace travel plans, followed by those promoting a more efficient use of the means of transport. Given their special features, the energy efficiency improvement measures for vehicles will be carried out through specific

571 571 571 571 571 571 571

3995

571 571 571 571 571 571

3424

571 571 571 571 571

2853

571 571 571 571

2283

571 571 571

1712

571 571

1141

571

571

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

2014 2015 2016 2017 2018 2019 2020 2014-2020

kto

e

3.9953.424

2.8532.283

1.7121.141

571

Total Accumulated Saving 2014-2020 : 15,979 ktoe

Industry54,6%

Transport25,3%

Buildings&Equipment15,3% Public Services

2,2%

Agriculture1,7%

Communication1,1%

Energy Efficiency Trends and Policies in SPAIN 25

programmes. The Building and Equipment sector account for 15.3% of the saving objective. These savings may come from the energy rehabilitation of the existing building thermal envelope; from the energy efficiency improvement of the heating thermal installations, heating & cooling and sanitary hot water, lighting, lifts and other transport systems, as well as electric installation, and from the rehabilitation of existing buildings with high energy qualification. Other measures to improve the efficiency of commercial refrigeration installations and data process centre installations are included. Last, the installation of intelligent systems and the renewal of the electric appliance stock are considered. This distribution only states the savings in the building and equipment sector, promoted by the system of energy efficiency obligations. 2.2% of the objective will be reached thanks to the measures in the Public Services sector. The most relevant measures are those linked to the renewal of street lighting and to a lesser extent, those linked to energy efficiency improvement in water treatment, supply, sewage-water treatment and desalination installations. 1.7% of the objective will be reached with measures in the Agriculture & Fishing sector, above all due to the energy efficiency improvement in farming holdings and in the use of farming machinery. Additionally stands out the “Spanish Strategy for Energy Rehabilitation in the Building Sector”, within the framework of this Action Plan in the field of building, drafted by the Ministry of Development in compliance with article 4 of the EED. It is a long-term strategy that will be updated every three years, and whose aim is to mobilise investments for renewing residential and business buildings so as to achieve better energy performance in the building stock. This Strategy delves into the reforms already started in the years 2012 and 2013, which materialized in the approval and enforcement of Law 8/2013 of 26 June, on urban rehabilitation, regeneration and renewal; and of Royal Decree 233/2013 of 5 April, approving the State Plan to promote house renting, building rehabilitation and urban regeneration and renewal for the period 2013-2016. This Strategy describes its main objectives, defines the various strategic scenarios and relates the measures that will be necessary to have them implemented, among which: those of a regulatory kind; of administrative kind; financial; information and communication ones; and last, the measures for enterprises to develop business strategies in the sector aimed at rehabilitation and energy efficiency. On the other hand, also in the building sector and in compliance with article 4 of the DEE, an energy renewal objective is introduced for 3% of the building surface of the State General Administration (AGE). To this end was made an inventory of buildings belonging to the State General Administration, the equivalent to 1,763 buildings with a surface over 11.2 million square metres, as well as the development of a Computer Platform of Energy and Heritage Management (PIGEP). In the new macroeconomic scenario, the improvement of the final intensity of the 2020 horizon is estimated as an average in the year-on-year 1.60% since 2013, calculated on the indicator including the non-energy uses. In terms of primary energy, the intensity indicator will be presumably reduced to a year-on-year 1.14% between 2013 and 2020. The improvement envisaged in the final and

Energy Efficiency Trends and Policies in SPAIN 26

primary intensity indicators guarantees savings3 equivalent to 22.5% in 2020, in terms of final energy, and to 18.6% that same year, in terms of primary energy.

Table 1.3: Final and Primary Energy Savings

2020

Final Energy Consumption Total Energy Uses (ktoe) 80,139

Final Energy Intensity (ktoe/M€ 2005) 0.078

Final Energy Savings Base 2007 (ktoe) 23,306

(%) 22.5%

Primary Energy Consumption Total Energy Uses (ktoe) 119,893

Primary Energy Intensity (ktoe/M€ 2005) 0.116

Primary Energy Savings Base 2007 (ktoe) 27,315

(%) 18.6%

Source: IDAE

All the above is completed with the Planning in the Electricity and Gas Sectors 2008-2016, whose main aim is to guarantee the security and quality of energy supply in the mid and long term. Currently a new planning process for the electricity transport networks is open thanks to Order IET/2598/2012, of 29 de November, which opens up a procedure to carry out development proposals for the transport network for electric energy. The new planning will finally span the period 2015-2020.

3 Savings are calculated as a product of the difference between the value of the indicator in the corresponding year and the value of the indicator in the year 2007; and the said difference is to be multiplied by the Gross Domestic Product of the year for which savings are to be determined, stated in constant Euros of year 2005.

Energy Efficiency Trends and Policies in SPAIN 27

2. ENERGY EFFICIENCY IN BUILDINGS

2.1. ENERGY EFFICIENCY TRENDS

The building sector in Spain is attaining more and more weight in the global energy demand, Figure 2.1, as opposed to the backward movement noticed in the industry sector. In the last years, energy consumption in buildings has maintained a downward pattern, as it happens in neighbouring countries. In 2013 energy consumption in buildings accounted for 30.4% of total final energy consumption, and 64.6% of electricity consumption. All the above contrasts with the representativeness of the whole of the EU-28 buildings in total (40.3%) and electricity consumption (59.8%), with a remarkable greater weight of the electricity consumption in Spain.

Figure 2.1: Share of Buildings in Final Energy Consumption in Spain, 2000-2013

Source :IDAE

The average consumption per capita in buildings in Spain is 0.54 toe, approximately 60% of the average consumption of the EU countries. Part of this difference is explained by Spain’s more favourable climate conditions. According to the information available from the Ministry of Development, the estimated total surface of buildings exceeds 5,000 million m2. Approximately 62% of the entire built-up surface corresponds to buildings in the residential sector. In like manner and in accordance with the information from the housing census published by the Spanish National Institute for Statistics (INE), about 60% of the residential buildings are block-building dwellings. There has been a continuous decrease in the new building pace in the last years, particularly sharp in the cases of the residential sector buildings. This has a bearing on the energy demand of the whole of the buildings by also limiting the favourable impact associated with the new building regulation. Considering the useful floor area of both kinds of buildings, a new average consumption per m2 of 142 kWh was attained in 2013, 32% less than the average consumption of buildings in the EU-28.

0

5.000

10.000

15.000

20.000

25.000

30.000

0%

5%

10%

15%

20%

25%

30%

35%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Co

nsu

mp

tio

n (k

toe

)

% O

vera

ll C

on

sum

pti

on

Services Households % Industry Consumption % Buildings Consumption

Energy Efficiency Trends and Policies in SPAIN 28

Figure 2.2: Trends in floor area of new buildings in Spain, 2000-2013

Note: Data based on building permits. Source: MFom/INE/IDAE

Next is shown a more detailed analysis for each of the sub-sectors making part of the building sector.

2.1.1 THE HOUSEHOLD SECTOR

The residential sector demand in 2013 decreased by 3.3%, reaching 15,015 Ktoe, amounting to 18.6% of the total final energy consumption. Behind this evolution lay a contraction in electricity consumption (-3.4%), and in natural gas (-9.0%), which met 62.8% of Spanish household demands. Depending on the kind of energy sources that meet the demands of the residential sector, most of the energy demand (58%) was met with fuels, both of fossil and renewable origin, Figure 2.3, even if electricity increasingly gained ground until meeting 42% of the demand. This was so at the expense of the oil product contribution. Figure 2.3: Structure of Energy Consumption of Households by Energy Sources in Spain, 2000-2013

2013

Source: MINETUR/IDAE

In any case, the prevalence of fuels accounts for the importance of thermal uses in this sector, among which the heating consumption stands out. This use concentrates over 40% of global demand in Spanish households as it is shown further on, Figure 2.8, mostly met by fossil and renewable fuels and marginally, (7.4%) by electricity.

0%

20%

40%

60%

80%

100%

120%

140%

160%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Households Buildings Non Households Buildings

0%

10%

20%

30%

40%

50%

60%

70%

80%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

% E

ne

rgy

Co

nsu

mp

tio

n

Oil Products Natural Gas RES Electricity Renewable and Fossil Energies

Coal

Oil Products

Natural Gas

Electricity

RES

Carbón

Gas Natural

Coal0,6%

Oil Products18,4%

Natural Gas21,3%

Electricity41,5%

RES18,2%

Energy Efficiency Trends and Policies in SPAIN 29

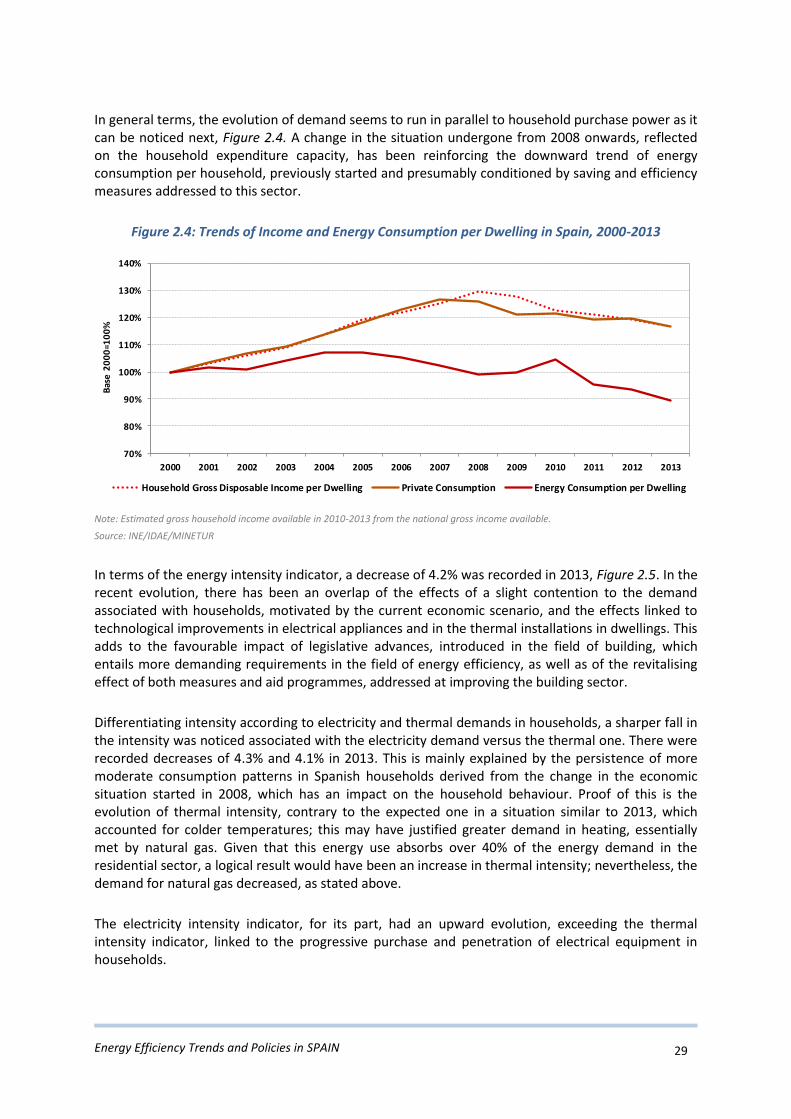

In general terms, the evolution of demand seems to run in parallel to household purchase power as it can be noticed next, Figure 2.4. A change in the situation undergone from 2008 onwards, reflected on the household expenditure capacity, has been reinforcing the downward trend of energy consumption per household, previously started and presumably conditioned by saving and efficiency measures addressed to this sector.

Figure 2.4: Trends of Income and Energy Consumption per Dwelling in Spain, 2000-2013

Note: Estimated gross household income available in 2010-2013 from the national gross income available.

Source: INE/IDAE/MINETUR

In terms of the energy intensity indicator, a decrease of 4.2% was recorded in 2013, Figure 2.5. In the recent evolution, there has been an overlap of the effects of a slight contention to the demand associated with households, motivated by the current economic scenario, and the effects linked to technological improvements in electrical appliances and in the thermal installations in dwellings. This adds to the favourable impact of legislative advances, introduced in the field of building, which entails more demanding requirements in the field of energy efficiency, as well as of the revitalising effect of both measures and aid programmes, addressed at improving the building sector.

Differentiating intensity according to electricity and thermal demands in households, a sharper fall in the intensity was noticed associated with the electricity demand versus the thermal one. There were recorded decreases of 4.3% and 4.1% in 2013. This is mainly explained by the persistence of more moderate consumption patterns in Spanish households derived from the change in the economic situation started in 2008, which has an impact on the household behaviour. Proof of this is the evolution of thermal intensity, contrary to the expected one in a situation similar to 2013, which accounted for colder temperatures; this may have justified greater demand in heating, essentially met by natural gas. Given that this energy use absorbs over 40% of the energy demand in the residential sector, a logical result would have been an increase in thermal intensity; nevertheless, the demand for natural gas decreased, as stated above.

The electricity intensity indicator, for its part, had an upward evolution, exceeding the thermal intensity indicator, linked to the progressive purchase and penetration of electrical equipment in households.

70%

80%

90%

100%

110%

120%

130%

140%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Bas

e 2

00

0=1

00

%

Household Gross Disposable Income per Dwelling Private Consumption Energy Consumption per Dwelling

Energy Efficiency Trends and Policies in SPAIN 30

Figure 2.5: Main Indicators of the Household Sector in Spain, 2000-2013

Source: INE/MINETUR/IDAE

Nevertheless, from the year 2004 onwards a change in the behaviour trend for both indicators is noticed, even recording an almost sustained decrease. In like manner, a difference in the evolution pace for both indicators can be observed, as well as greater lessening in the case of electricity intensity. This seems to be in line with some sort of saturation of the electrical appliance equipment in households, as well as with the efficiency improvements associated with the electrical appliance equipment and lighting. As regards the latter, it is important to stand out the comparison at European level of the average electricity consumption per household, linked to the penetration of electrical appliances in Spanish households. A progressive convergence between Spain and the EU average can be noticed, Figure 2.6; therefore, all along the last two decades, average electricity consumption in Spanish households increased in progressive convergence with the average consumption of the EU until reaching the same consumption level in 2005. Further on, some stabilization with a downward trend was recorded, as it happened with the EU countries. This can be partially explained in both cases by much more conservative behavior patterns brought about by the crisis. This upturn noticed in 2011 in the relation between the average Spanish electricity consumption and the European one seems to respond to the difference in the rate of fall of both, somehow more dramatic in the whole of EU households.

Figure 2.6: Trends in Electricity Consumption per Dwelling in Spain and EU, 2000-2013

Source: IDAE/MINETUR/EnR

70

80

90

100

110

120

130

140

150

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Ba

se 2

00

0=

10

0

Total Intensity (toe/dw) Thermal Intensity (toe/dw) Electricity Intensity (kWh/dw) Nº Dwellings Degree-Day

75%

80%

85%

90%

95%

100%

105%

110%

115%

1.500

2.000

2.500

3.000

3.500

4.000

4.500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

% S

pai

n/E

U-2

8

EU-28 Spain %Spain/EU-28

Energy Efficiency Trends and Policies in SPAIN 31

As mentioned earlier, the drop in consumption can be partly explained as a saturation of the level of electrical household appliances of Spanish households; this would add up to a renewal of the existing equipment, both of electrical appliances and lighting with more efficient ones. This leads to a reduction in the electricity consumption associated with lighting and the electrical appliances stock as a result of a technological improvement. Proof of it are the recorded trends in the sales of new electrical appliances, with a growing quota for more efficient equipment, more and more present in Spanish households as it can be gathered from the information available in various market surveys.

Finally, the evolution of the energy intensity in the residential sector at EU-28 country level must be highlighted, considering to this end a climate correction with a view to adjusting the variations impact between winters. Benchmarking, Figure 2.7, enables to notice a difference of around 40% between the national indicator and its European counterpart. In like manner, the evolution of this indicator in countries like Italy, Greece and Portugal seems to confirm the climate influence.

Figure 2.7: Trends of Energy Intensity in the Household Sector in Spain and EU, 2000-2013

Note: Intensity with climate correction

Source: EnR/IDAE/INE

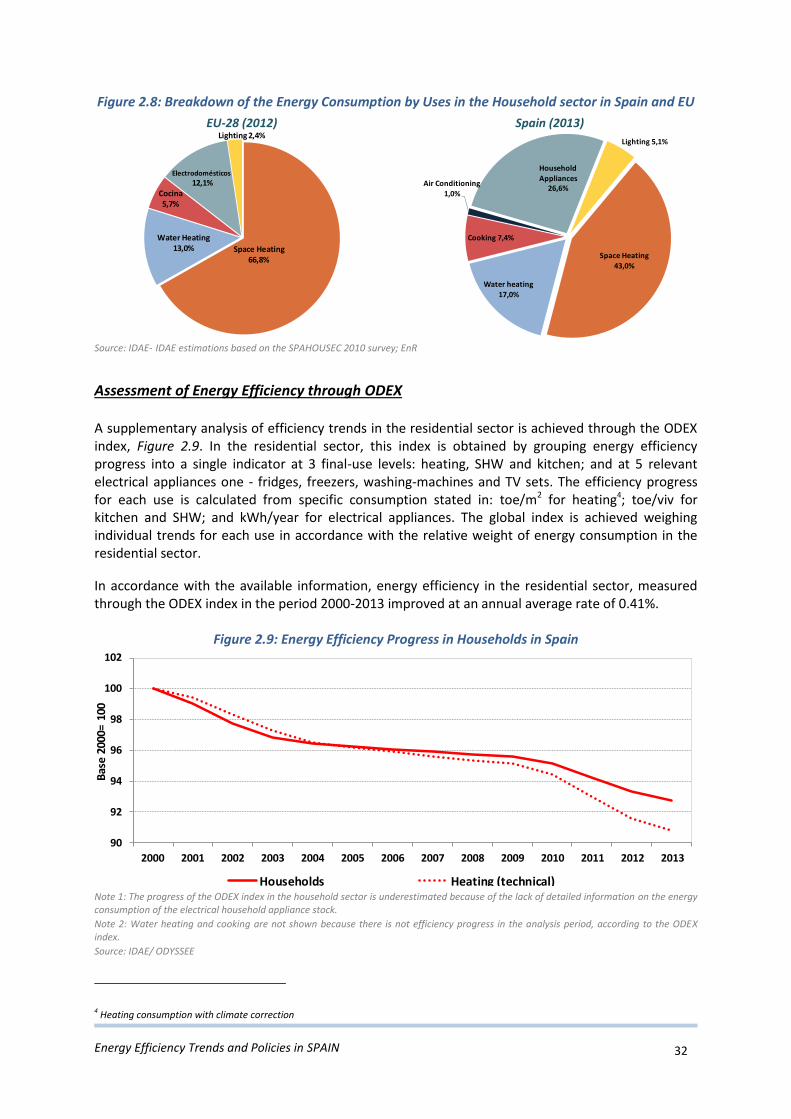

The milder climatology of South-Eastern countries accounts for a lower use of heating, whose demand ranges from 43% in Spain to 67% in the whole of the EU-28, Figure 2.8. Consequently, the weight difference in terms of heating largely determines energy intensity in the residential sector. As for the rest of household uses, the following position is held by the electrical household appliances, with approximately one fourth of total consumption and fridges at the forefront of consuming equipment: it accounts for 31% of electrical appliances consumption and 19% of total electricity consumption. The last position is occupied by air-conditioning systems with 1% of total consumption, and even if as this is a seasonal service, its demand concentrates on a short period of time and can involve demand peaks difficult to manage.

0,65

0,80

0,95

1,10

1,25

1,40

1,55

1,70

1,85

2,00

2,15

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

toe

/dw

UE-28 France Germany Italy Spain UK Greece Ireland Portugal

Energy Efficiency Trends and Policies in SPAIN 32

Figure 2.8: Breakdown of the Energy Consumption by Uses in the Household sector in Spain and EU

EU-28 (2012) Spain (2013)

Source: IDAE- IDAE estimations based on the SPAHOUSEC 2010 survey; EnR

Assessment of Energy Efficiency through ODEX

A supplementary analysis of efficiency trends in the residential sector is achieved through the ODEX index, Figure 2.9. In the residential sector, this index is obtained by grouping energy efficiency progress into a single indicator at 3 final-use levels: heating, SHW and kitchen; and at 5 relevant electrical appliances one - fridges, freezers, washing-machines and TV sets. The efficiency progress for each use is calculated from specific consumption stated in: toe/m2 for heating4; toe/viv for kitchen and SHW; and kWh/year for electrical appliances. The global index is achieved weighing individual trends for each use in accordance with the relative weight of energy consumption in the residential sector.

In accordance with the available information, energy efficiency in the residential sector, measured through the ODEX index in the period 2000-2013 improved at an annual average rate of 0.41%.

Figure 2.9: Energy Efficiency Progress in Households in Spain

Note 1: The progress of the ODEX index in the household sector is underestimated because of the lack of detailed information on the energy consumption of the electrical household appliance stock.

Note 2: Water heating and cooking are not shown because there is not efficiency progress in the analysis period, according to the ODEX index.

Source: IDAE/ ODYSSEE

4 Heating consumption with climate correction

Space Heating 66,8%

Water Heating 13,0%

Cocina 5,7%

Electrodomésticos

12,1%

Lighting 2,4%

Space Heating

43,0%

Water heating 17,0%

Cooking 7,4%

Air Conditioning 1,0%

Household Appliances

26,6%

Lighting 5,1%

90

92

94

96

98

100

102

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Bas

e 2

000=

100

Households Heating (technical)

Energy Efficiency Trends and Policies in SPAIN 33

This improvement moderated in the period after 2008, coinciding with the beginning of the crisis, and which limited the favourable impact associated with energy efficiency standards in terms of equipment and building. This issue involved a slowing-down in the pace of the existing dwelling rehabilitation and of penetration of the new ones, Figure 2.2, as well as of more efficient equipment, not only in Spain but also in surrounding countries. Therefore, a new contrast becomes evident between the former average improvement prior to the crisis of 0.49%/year, and the further improvement of 0.28%/year. Most of these improvements go for heating, whose relevance in consumption largely determines the global progress of efficiency in the sector. In the former order of magnitude, a progress on energy efficiency is presumed within the electrical appliances stock, given the market trends and the purchase patterns of household equipment. Nevertheless, the lack of information available in this sense limits the assessment of this effect through the ODEX index.

Assessment of the Decomposition of the Energy Consumption Variation