employment tax laws version 08.a lausd small business boot camp

TRANSCRIPT

Employment Tax Laws

Version 08.a

LAUSD Small Business Boot Camp

Presenters

IRS

Anthony SykesAnthony SykesIRS Presenter

EDD

Jimmy WongJimmy WongTaxpayer Education and Assistance Taxpayer Assistance Center:1-888-745-3886

Agenda

• Employee vs. Independent Contractor

• Reporting Requirements for Independent Contractors

• Employer Responsibilities

• Reporting and Deposit Requirements

Employee vs.Employee vs.Independent ContractorIndependent Contractor

Independent Contractor:

An individual who performs services for you, but for whom you control only the result of the work.

Employee:

An individual who performs services for you and is subject to your control regarding what will be done AND how it will be done.

Employee vs. Independent Contractor

Types of Workers

• Employees

– Common law

– Statutory• Corporate officer

• Unlicensed construction contractor (state)

• Independent contractors

Common Law Employment

• Common law evolved slowly over the years based on court decisions on individual cases.

• Common law rules of employment are the total of all court decisions on employment.

Common Law Employment (continued)

Person who hires an individual to perform services has the right to control the manner and means of performing those services,

whether exercised or not.

The right to discharge a worker at will and without cause is strong evidence

of right to control.

What Can Happen If I Misclassify My Workers?

• Costly audits by the IRS, the EDD, and the Dept. of Industrial Relations due to:

– Worker claims for injury/unemployment.

– Worker informants.

– Competitor informants.

• Additional taxes, penalties, and interest.

• Revocation of state/local licenses.

Voluntary Classification Settlement Program

• Optional program to reclassify workers

• Applies to future tax periods

• Must meet eligibility requirements

• Apply by filing Form 8952

• Must enter into a closing agreement

• Business and Specialty Tax Hotline 800-829-4933

• Visit IRS.gov

– Click on “Businesses” tab, “Employment Taxes” in the left navigation

– Search Keyword “worker classification”

• Worker classification resource handout

Resources

• Pub 1779, Independent Contractor or Employee

• Pub 15 (Circular E), Employer’s Tax Guide

• Pub 15-A, Employer’s Supplemental Tax Guide

• Form SS – 8, Determination of Worker Status

Resources (continued)

• DE 44, California Employer’s Guide

• DE 231, Information Sheet - Employment

• DE 38, Employment Determination Guide

• DE 1870, Determination of Employment Work Status

Resources (continued)

• Employment Status Course www.edd.ca.gov/Payroll_Taxes/Web_Based_Seminars.htm

• Employee or Independent Contractor Tax Seminar www.edd.ca.gov/Payroll_Tax_Seminars/

• EDD Payroll Tax Forms and Publications www.edd.ca.gov/Payroll_Taxes/Forms_and_Publications.htm

Resources (continued)

Reporting Requirements Reporting Requirements for for

Independent ContractorsIndependent Contractors

Form W-9, Request for Taxpayer Identification and Certification

• Reports:

–Payee’s correct name

–Payee’s Taxpayer Identification number

Backup Withholding Requirements

• Withhold 28 percent of income if:– Payee does not provide TIN– Payee provides incorrect TIN– IRS notifies payer of incorrect TIN

• Withholding time frames– begin with first payment over $600– until payee provides correct TIN

TIN Matching Program

• Benefits:– Match payee name with Form W-9 – Match TIN with IRS records– Decrease backup withholding and

penalty notices– Reduce the error rate in TIN validation

• e-services verification available

California Backup Withholding Requirements

• If required to remit federal backup withholding to IRS, withhold 7 percent of income.

• Remit to Franchise Tax Board: www.ftb.ca.gov/individuals/WSC/Backup_Withholding.shtml

Reporting Independent Contractors to EDD

DE 542, Report of Independent Contractor(s)

– $600 or more for services in a calendar year.

– Applies to services provided by sole proprietor.

Form 1099-MISC Filing Requirement

• Report payments of $600 or more paid in the course of your trade or business to non-employees annually.

• Report payments of at least $10 in royalties or broker payments in lieu of dividends or tax-exempt interest.

• Provide required copies timely to:

– Payees by January 31

– IRS by last day of February

• Exception awareness

Potential Penalties

• Failure to file correct information returns by due date

• Trust fund– imposed when taxes withheld are not

sent to IRS– 100% of taxes, for taxes not sent to IRS– potential backup withholding for payer

• Form 945 to IRS, due January 31

• Form 1099-MISC to:–Independent contractor, due January

31–IRS, due last day of February

• Form 1096 (with Forms 1099) to IRS, due last day of February

NOTE: Obtain Form W-9 from independentcontractor prior to first payment.

Federal Forms and Due Dates

Employer Employer ResponsibilitiesResponsibilities

Employer’s Federal Requirements

• Obtain Federal Employer Identification Number with Form SS-4

• Complete federal forms– W-4, Employee’s Withholding

Allowance Certificate– Form I-9, Employment Eligibility

Verification

• Notify IRS of address change

• Obtain a Workers’ Compensation Insurance policy.

www.dir.ca.gov/dwc www.statefundca.com

• Apply for state employer account number.

DE 1, Registration Form for Commercial Employers

Employer’s State Requirements

When Hiring New Employees

• Obtain DE 4, Employee’s Withholding Allowance Certificate, if status/allowances claimed differ from Form W-4.

• Submit DE 34, Report of New Employee(s).

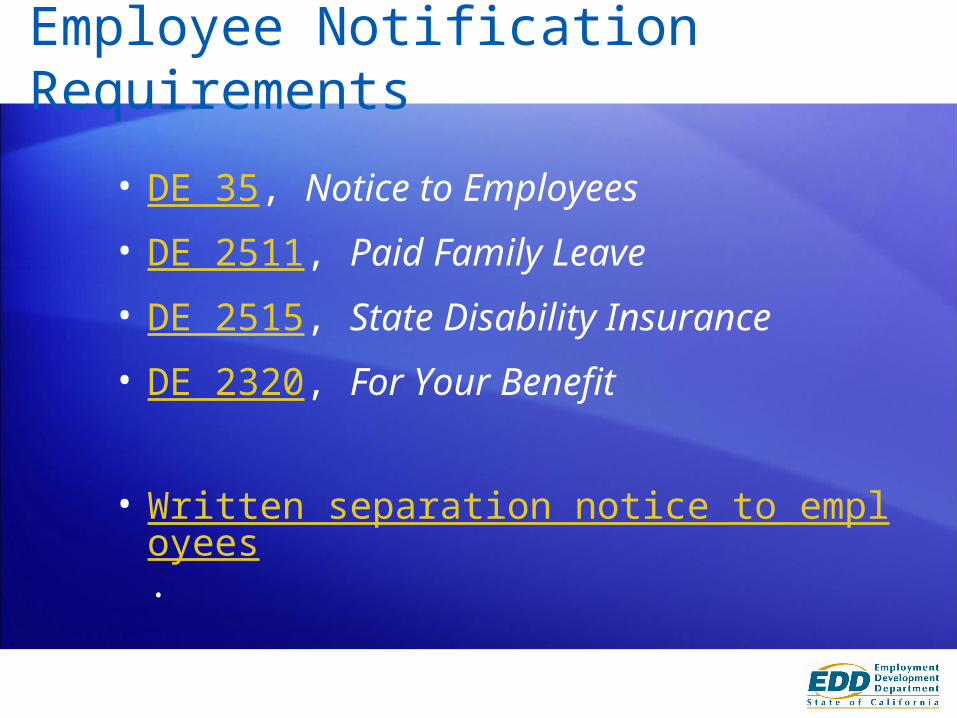

Employee Notification Requirements

• DE 35, Notice to Employees

• DE 2511, Paid Family Leave

• DE 2515, State Disability Insurance

• DE 2320, For Your Benefit

• Written separation notice to employees.

Posting Requirements

Generally, federal and state laws require that employers post complete, up-to-date versions of labor notices and other required posters.

Current posting requirements are available at: www.taxes.ca.gov/Payroll_Tax/postingreqbus.shtml

Recordkeeping

• Maintain wage, earning, deduction, and withholding records on employees.

• Provide earning statements to each employee, each payday.

• Retain employee records and returns for at least four years.

Reporting and Reporting and Depositing RequirementsDepositing Requirements

Employer pays:

• FUTA: 0.6% for the first $7,000 paid to each employee as wages during the year

• FICA Social Security: 6.2% on first $117,000 (wage base limit)

• FICA Medicare: 1.45% on all wages

2014 Federal Payroll Taxes

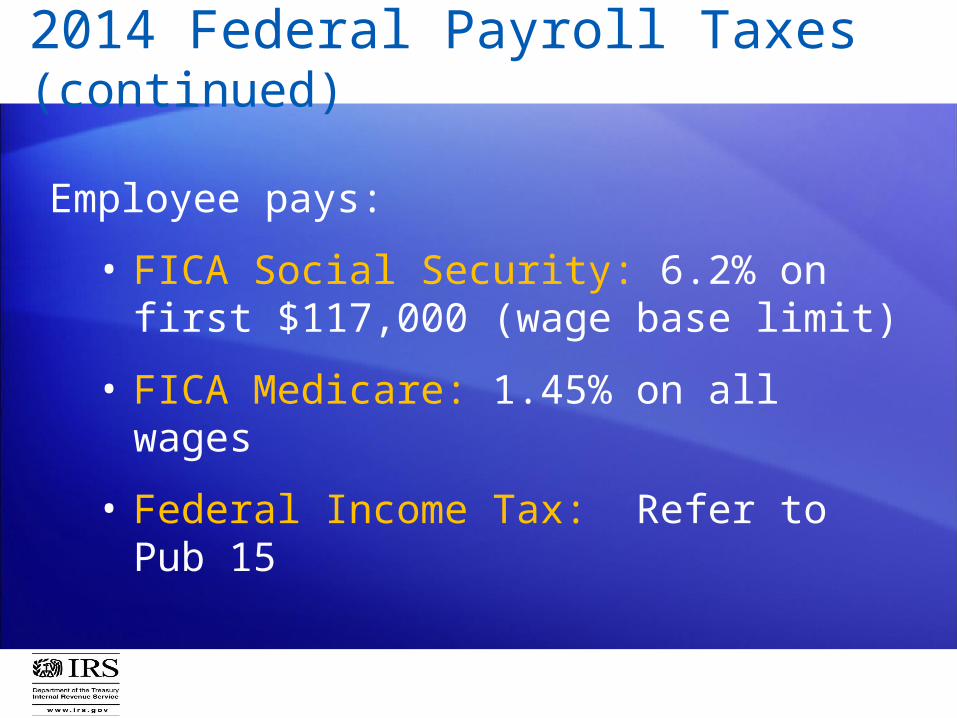

Employee pays:

• FICA Social Security: 6.2% on first $117,000 (wage base limit)

• FICA Medicare: 1.45% on all wages

• Federal Income Tax: Refer to Pub 15

2014 Federal Payroll Taxes (continued)

2014 State Payroll Taxes

STATEUI

Unemployment Insurance

ETT Employment Training Tax

SDI State Disability

Insurance

PIT Personal Income Tax

(State Income Tax)

Employer pays 3.4% 0.1%

Employee pays 1.0% Refer to DE 44

Wage Limit $7,000 $7,000 $101,636 None

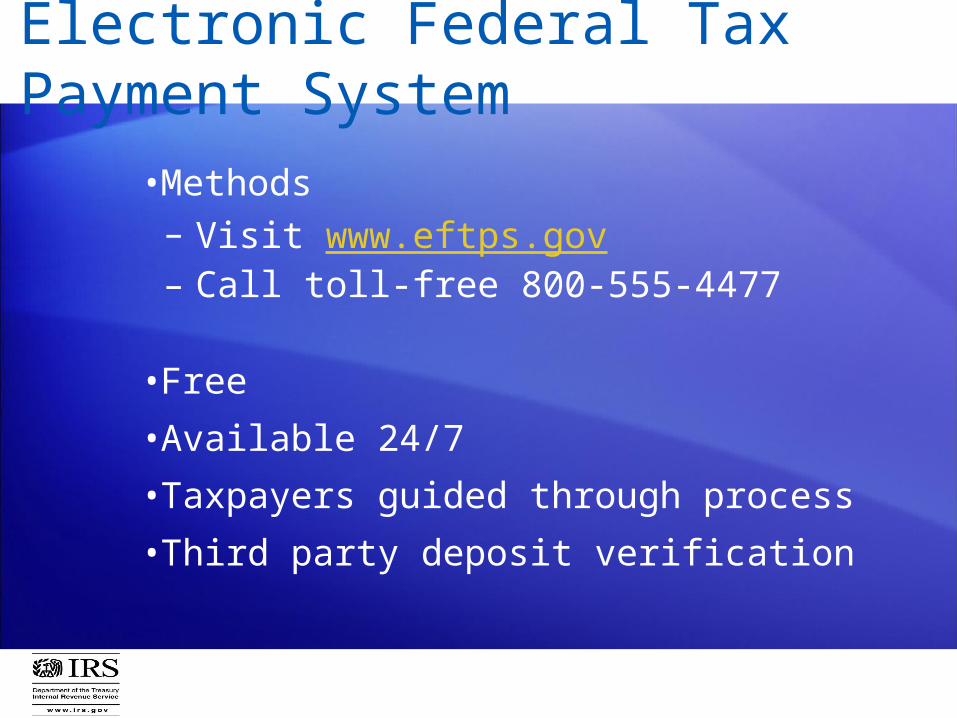

Electronic Federal Tax Payment System

•Methods– Visit www.eftps.gov– Call toll-free 800-555-4477

•Free

•Available 24/7

•Taxpayers guided through process

•Third party deposit verification

State Electronic Filing and Payment Methods

e-Services for Business

• Fast, easy, and secure ways to manage your payroll taxes online.

• View and edit your returns/reports prior to submission.

• Available 24 hours a day, 7 days a week.

State Payroll Tax Deposit Methods

• DE 88, Payroll Tax Deposit

• Electronic Funds Transfer

• Credit Card (Telephone or Internet)

State Payroll Tax Reporting Forms

DE 88, Payroll Tax Deposit

DE 9, Quarterly Contribution Return and Report of Wages

DE 9C, Quarterly Contribution Return and Report of Wages (Continuation)

Forms and Due Dates

State Period Due by

DE 9

DE 9C

1st Quarter April 30

Jan., Feb., March

DE 9

DE 9C

2nd QuarterJuly 31

Apr., May, June

DE 9

DE 9C

3rd QuarterOctober 31

July, Aug., Sep.

DE 9

DE 9C

4th QuarterJanuary 31

Oct., Nov., Dec.

Federal Payroll Tax Reporting Forms

• Form 941, Employer’s Quarterly Federal Tax Return

• Form 940, Employer’s Annual Federal Unemployment (FUTA) Tax Return

– Schedule A, Multi-State Employer and Credit Reduction Information Return

• Form 944, Employer’s Annual Federal Tax Return

Federal Payroll Tax Reporting Forms(continued)

• Form W-2, Wage and Tax Statement

• Form W-3, Transmittal of Wage and Tax Statements

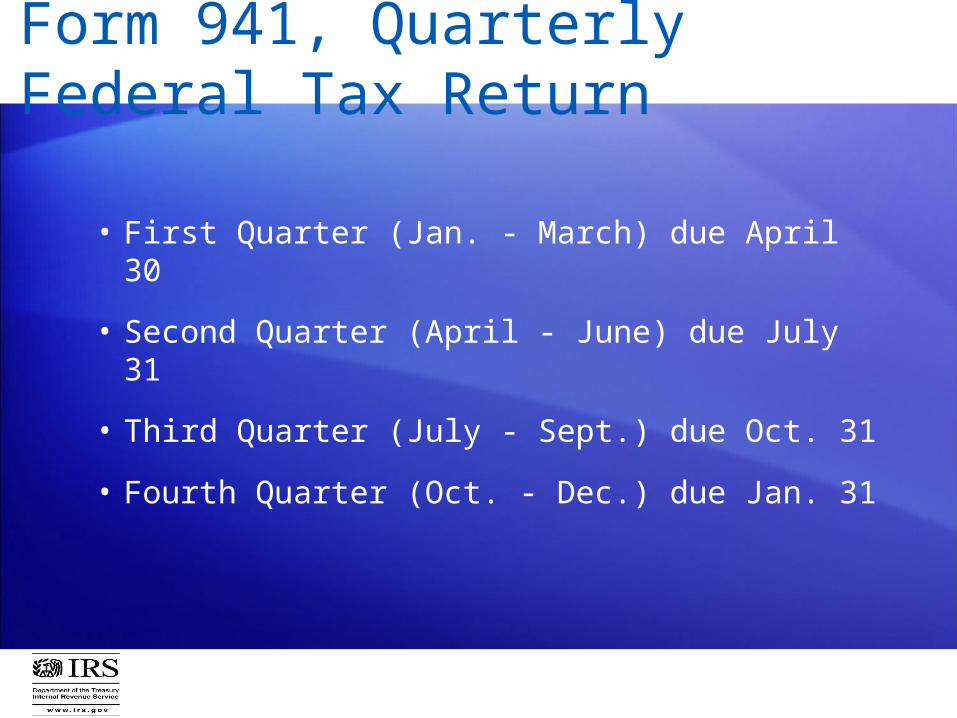

Form 941, Quarterly Federal Tax Return

• First Quarter (Jan. - March) due April 30

• Second Quarter (April - June) due July 31

• Third Quarter (July - Sept.) due Oct. 31

• Fourth Quarter (Oct. - Dec.) due Jan. 31

Penalty and Interest Prevention

• Classify workers properly.

• File all documents and returns timely.

• Make all payments timely and in full.

• Use electronic filing and payment methods to reduce errors.

• Respond timely to all correspondence.

California Tax Service Center

Thank You!Thank You!Questions?Questions?