empea industry statistics q2 2015_official member

TRANSCRIPT

INDUSTRY STATISTICS Q2 2015

Emerging Markets Private Capital

Fundraising & Investment Analysis

2 | EMPEA

Announcements & AcknowledgementsImportant Update to EMPEA’s Research MethodologyPlease note that this release incorporates several changes to EMPEA's research methodology. Unless otherwise specified, EMPEA's data and statistics now include expanded coverage of private infrastructure and real assets and private credit funds, in addition to previously reported private equity activity.

For more information, please see our full Research Methodology here: http://empea.org/research/data-and-statistics/data-methodology

Terms of UseAll material and underlying data contained within this presentation are the intellectual property of EMPEA. Any reference to the material must be properly cited with notation attributing EMPEA as the source.

Contact UsFor additional information, inquiries, or questions, please contact us at [email protected] or call +1.202.333.8171 ext. 224.

AcknowledgmentsEMPEA would like to acknowledge the information provided by Asociación Mexicana de Capital Privado (AMEXCAP), Associação Brasileira de Private Venture Capital (ABVCAP), Association Marocaine des Investisseurs en Capital (AMIC), Czech Private Equity & Venture Capital Association (CVCA), Hong Kong Venture Capital & Private Equity Association (HKVCA) and Latin American Private Equity & Venture Capital Association (LAVCA). We thank these Industry Partners for their support.

3 | EMPEA

Table of Contents

• Overview of EM Private Capital• Global Private Equity• EM Private Capital: Fundraising• EM Private Capital: Investment• Cambridge Associates Private Equity & Venture

Capital Fund Performance

Note: “Private Capital” includes private equity, private credit, private infrastructure and real assets.

4 | EMPEA

Accessing EMPEA’s Quarterly Data

• For in-depth look at the data behind the charts in this presentation, EMPEA Members have exclusive access to:– Right click on the chart, and click “Edit Data” to view the full

table(s), or– Visit empea.org for the accompanying Excel data pack.

• EMPEA Members may also contact us to request a custom cut of the data via HelpDesk.

• For additional information, inquiries or questions, please contact us at [email protected] or call +1.202.333.8171 ext. 224.

5 | EMPEA

Overview of EM Private CapitalEmerging Markets │ Q2 2015 Industry Statistics

6 | EMPEA

Overall EM Fundraising & Investment

2011 2012 2013 2014 1H 2015$0

$20

$40

$60

48 4744

51

19

3128 28

36

14

Funds Raised Capital Invested

US

$ B

illio

ns

Data as of 30 June 2015. Published 5 August 2015.

Note: Includes private equity, private credit, private infrastructure and real assets.

Funds Raised

Capital Invested

$0

$5

$10

$15

$20

14 13

4.3

0.9

Private Equity

Infrastructure & Real Assets

Private Credit

US

$ B

illio

ns

1H 2015

19

14

7 | EMPEA

EM Fundraising by Asset Class

2011 2012 2013 2014 1H 20150%

20%

40%

60%

80%

100%

90% 86%79% 85%

72%

6% 9%12%

9%23%

5% 8% 6% 5%

Private Equity Infrastructure & Real Assets Private Credit

% o

f T

ota

l Ca

pit

al R

ais

ed

Data as of 30 June 2015. Published 5 August 2015.

Note: Includes private equity, private credit, private infrastructure and real assets.

8 | EMPEA

EM Investment by Asset Class

2011 2012 2013 2014 1H 20150%

20%

40%

60%

80%

100%

95% 96% 94% 91% 91%

4%4% 7%5%

Private Equity Infrastructure & Real Assets Private Credit

% o

f T

ota

l Ca

pit

al I

nv

es

ted

Data as of 30 June 2015. Published 5 August 2015.

Note: Includes private equity, private credit, private infrastructure and real assets.

9 | EMPEA

Global Private EquityEmerging Markets │ Q2 2015 Industry Statistics

10 | EMPEA

EM PE as % of Global PE Fundraising

2011 2012 2013 2014 1H 2015$0

$100

$200

$300

$400

0%

5%

10%

15%

20%19%

18%

10%

13%

11%

Developed Asia (JANZ) United States Western Europe Emerging Markets EM Fundraising as % of Global Total

US

$ B

illio

ns E

M a

s %

of G

lob

al

Sources: Developed Asia - Asia Private Equity Review, U.S. – PitchBook, Western Europe – EVCA, EM – EMPEA

Data as of 30 June 2015. Published 5 August 2015.

Note: Only includes private equity.

11 | EMPEA

EM PE as % of Global PE Investment

Sources: Developed Asia - Asia Private Equity Review, U.S. – PitchBook, Western Europe – EVCA, EM – EMPEA

Data as of 30 June 2015. Published 5 August 2015.

2011 2012 2013 2014 1H 2015$0

$100

$200

$300

$400

0%

5%

10%10% 10% 10% 10%

8%

Developed Asia (JANZ) United States Western Europe Emerging Markets EM Investment as % of Global Total

US

$ B

illio

ns E

M a

s %

of G

lob

al

Note: Only includes private equity.

12 | EMPEA

Global PE Penetration

Israel United States

United Kingdom

India South Korea

China Brazil Japan SSA* South Africa

Poland MENA** Turkey Russia0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

1.47

1.09

0.93

0.190.23

0.080.13

0.040.11

0.050.09

0.010.05

0.01

1.65

1.46

0.79

0.20 0.19 0.15 0.13 0.13 0.11 0.100.04

0.01 0.02 0.004

2013

2014

PE

Inv

es

tme

nt/

GD

P (

%)

Data as of 30 June 2015. Published 5 August 2015.

Sources:• Emerging Markets – EMPEA• United Kingdom – Centre for Management Buy-Out Research• United States – PitchBook• Israel – Israel Venture Capital Research Center• Japan – Asia Private Equity Review• All GDP data – International Monetary Fund

*Sub-Saharan Africa; **Middle East & North Africa

Note: Only includes private equity.

13 | EMPEA

EM PE Fundraising & Investment as % of Global PE

2011 2012 2013 2014 1H 20150%

5%

10%

15%

20% 19%18%

10%

13%

11%

10% 10% 10% 10%

8%

EM PE Fundraising EM PE Investment

% o

f G

lob

al T

ota

l

Data as of 30 June 2015. Published 5 August 2015.

Note: Only includes private equity.

14 | EMPEA

EM Private Capital: FundraisingEmerging Markets │ Q2 2015 Industry Statistics

15 | EMPEA

Overall EM Fundraising

2011 2012 2013 2014 1H 2015$0

$20

$40

$60

$80

0

50

100

150

200

250

48 4744

51

19

228236

220 223

100

Total Capital Raised (US$B) No. of Funds

US

$ B

illio

ns

No

. of F

un

ds

Data as of 30 June 2015. Published 5 August 2015.

Note: Includes private equity, private credit, private infrastructure and real assets.

16 | EMPEA

EM Fundraising by Region

2011 2012 2013 2014 1H 20150%

20%

40%

60%

80%

100%

70%61%

67% 62% 64%

4%11% 4%

19%13% 13% 19%

15%

4%

5% 9% 15%8% 12%

4%

Emerging Asia CEE & CIS Latin America MENA Sub-Saharan Africa Multi-Region

% o

f T

ota

l Ca

pit

al R

ais

ed

Data as of 30 June 2015. Published 5 August 2015.

Note: Includes private equity, private credit, private infrastructure and real assets.

17 | EMPEA

EM Fundraising by Strategy

2011 2012 2013 2014 1H 20150%

20%

40%

60%

80%

100%

22%

41%32% 36%

24%

51%

38%

42% 35%

35%

17% 7%5% 14%

14%

5% 7%11%

8%

18%

5% 8% 6% 5%5%

Buyout Growth Venture Capital Infrastructure Real Assets Private Credit

% o

f T

ota

l Ca

pit

al R

ais

ed

Data as of 30 June 2015. Published 5 August 2015.

Note: Includes private equity, private credit, private infrastructure and real assets.

18 | EMPEA

EM Fund Size Distribution

2011 2012 2013 2014 1H 20150%

20%

40%

60%

80%

100%

38%49% 44%

33%39%

22%

21% 26%

31% 22%

21%

16% 12%

12% 19%

10%8% 11%

14% 11%

9% 7% 6% 10% 9%

<US$100m US$100m-US$249m US$250m-US$499m US$500m-US$999m >US$1 billion

% o

f T

ota

l No

. of

Fu

nd

s

Data as of 30 June 2015. Published 5 August 2015.

Note: Based on total capital raised by funds reaching a final close in the designated year.

Note: Includes private equity, private credit, private infrastructure and real assets.

19 | EMPEA

EM Median Fund Size by Asset Class

Data as of 30 June 2015. Published 5 August 2015.

2011 2012 2013 2014 1H 2015$0

$100

$200

$300

$400

152

84104

150

113

356

167

220

119

274

111

256

175

136

NS

155

100

127146 154

Private Equity Infrastructure & Real AssetsPrivate Credit All Asset Classes

US

$ M

illio

ns

Note: NS = Not Significant.

Note: Includes private equity, private credit, private infrastructure and real assets.

20 | EMPEA

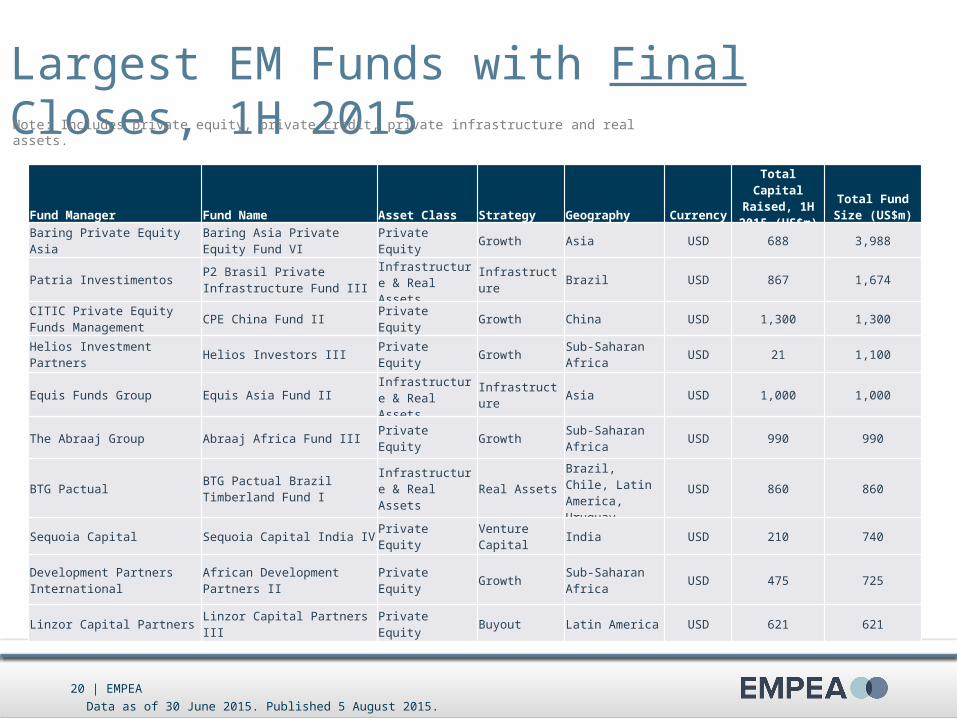

Largest EM Funds with Final Closes, 1H 2015

Data as of 30 June 2015. Published 5 August 2015.

Fund Manager Fund Name Asset Class Strategy Geography Currency

Total Capital Raised, 1H

2015 (US$m)Total Fund Size

(US$m)

Baring Private Equity AsiaBaring Asia Private Equity Fund VI

Private Equity Growth Asia USD 688 3,988

Patria InvestimentosP2 Brasil Private Infrastructure Fund III

Infrastructure & Real Assets

Infrastructure Brazil USD 867 1,674

CITIC Private Equity Funds Management

CPE China Fund II Private Equity Growth China USD 1,300 1,300

Helios Investment Partners Helios Investors III Private Equity GrowthSub-Saharan Africa

USD 21 1,100

Equis Funds Group Equis Asia Fund IIInfrastructure & Real Assets

Infrastructure Asia USD 1,000 1,000

The Abraaj Group Abraaj Africa Fund III Private Equity GrowthSub-Saharan Africa

USD 990 990

BTG PactualBTG Pactual Brazil Timberland Fund I

Infrastructure & Real Assets

Real AssetsBrazil, Chile, Latin America, Uruguay

USD 860 860

Sequoia Capital Sequoia Capital India IV Private Equity Venture Capital India USD 210 740

Development Partners International

African Development Partners II Private Equity GrowthSub-Saharan Africa

USD 475 725

Linzor Capital Partners Linzor Capital Partners III Private Equity Buyout Latin America USD 621 621

Note: Includes private equity, private credit, private infrastructure and real assets.

21 | EMPEA

Largest EM Funds with Closes, 1H 2015

Data as of 30 June 2015. Published 5 August 2015.

*Fundraising as of 30 June 2015.

Fund Manager Fund Name Asset Class Strategy Geography Currency

Total Capital Raised, 1H

2015 (US$m)Total Fund Size

(US$m)

Baring Private Equity AsiaBaring Asia Private Equity Fund VI

Private Equity Growth Asia USD 688 3,988

RRJ Capital RRJ Capital Master Fund III* Private Equity BuyoutAsia, China, Southeast Asia

USD 2,600 2,600

Patria InvestimentosP2 Brasil Private Infrastructure Fund III

Infrastructure & Real Assets

Infrastructure Brazil USD 867 1,674

CITIC Private Equity Funds Management

CPE China Fund II Private Equity Growth China USD 1,300 1,300

Helios Investment Partners Helios Investors III Private Equity GrowthSub-Saharan Africa

USD 21 1,100

Equis Funds Group Equis Asia Fund IIInfrastructure & Real Assets

Infrastructure Asia USD 1,000 1,000

The Abraaj Group Abraaj Africa Fund III Private Equity GrowthSub-Saharan Africa

USD 990 990

BTG PactualBTG Pactual Brazil Timberland Fund I

Infrastructure & Real Assets

Real AssetsBrazil, Chile, Latin America, Uruguay

USD 860 860

Sequoia Capital Sequoia Capital India IV Private Equity Venture Capital India USD 210 740

Development Partners International

African Development Partners II Private Equity GrowthSub-Saharan Africa

USD 475 725

Note: Includes private equity, private credit, private infrastructure and real assets.

22 | EMPEA

EM Private Capital: InvestmentEmerging Markets │ Q2 2015 Industry Statistics

23 | EMPEA

Overall EM Investment

2011 2012 2013 2014 1H 2015$0

$10

$20

$30

$40

$50

0

500

1,000

1,500

3128 28

36

14

1,081 1,0631,128

1,391

738

Total Capital Invested (US$B) No. of Deals

US

$ B

illio

ns

No

. of D

ea

ls

Data as of 30 June 2015. Published 5 August 2015.

Note: Includes private equity, private credit, private infrastructure and real assets.

24 | EMPEA

EM Investment by Quarter

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q22012 2013 2014 2015

$0

$5

$10

$15

$20

0

100

200

300

400

6.4

9.5

6.1

3.7

7.15.8

10.9

7.4

9.1

11.4

8.5

6.0

8.4

266286

209

284

251266

327347

327

365352 345

393

Total Capital Invested (US$B) No. of Deals

US

$ B

illio

ns N

o. o

f De

als

Data as of 30 June 2015. Published 5 August 2015.

Note: Includes private equity, private credit, private infrastructure and real assets.

25 | EMPEA

EM Investment by Region

2011 2012 2013 2014 1H 20150%

20%

40%

60%

80%

100%

69%58%

66%74% 78%

11%

9%8%

5%5%

14%

22%18%

14% 11%

5% 4% 7% 6% 4%7%

Emerging Asia CEE & CIS Latin America MENA Sub-Saharan Africa

% o

f T

ota

l Ca

pit

al I

nv

es

ted

Data as of 30 June 2015. Published 5 August 2015.

Note: Includes private equity, private credit, private infrastructure and real assets.

26 | EMPEA

EM Investment by Sector

2011 2012 2013 2014 1H 20150%

20%

40%

60%

80%

100%

30% 29% 27%32% 35%

15% 18%17%

16%16%

11% 10% 13%

15%15%

13% 14% 14%

11%10%9% 10% 11%

10%11%7%

9% 8%7%

6%5%

TelecommunicationsUtilitiesBasic MaterialsOil & GasHealth CareFinancialsConsumer GoodsTechnologyIndustrialsConsumer Services

% o

f N

o. o

f D

ea

ls

Data as of 30 June 2015. Published 5 August 2015.

FTSE ICB Industry†

† The Industry Classification Benchmark (“ICB”) is owned by FTSE International Limited (“FTSE”). “FTSE®” is a trademark of the London Stock Exchange Group companies and is used by FTSE under license. FTSE does not accept any liability to any person for any loss or damage arising out of any error or omission in the ICB.

Note: Includes private equity, private credit, private infrastructure and real assets.

27 | EMPEA

EM Investment by Stage

Data as of 30 June 2015. Published 5 August 2015.

2011 2012 2013 2014 1H 20150%

20%

40%

60%

80%

100%

46% 43%33% 26% 26%

10% 12%12%

10%

33% 35%44% 54% 64%

9% 9% 7%Mezzanine

Debt

PIPE

Venture Capital

Buyout

Growth

% o

f N

o. o

f D

ea

ls

2011 2012 2013 2014 1H 20150%

20%

40%

60%

80%

100%

44% 51%33% 37% 41%

26%24%

41% 30%10%

12% 8% 10% 19%31%

18% 17% 12% 9% 15%Mezzanine

Debt

PIPE

Venture Capital

Buyout

Growth% o

f C

ap

ita

l In

ve

ste

d

Note: Includes private equity, private credit, private infrastructure and real assets.

28 | EMPEA

EM Investment Size Distribution

2011 2012 2013 2014 1H 20150%

20%

40%

60%

80%

100%

38%47% 50% 46% 51%

26%20%

24% 28%26%

15%15%

10% 9% 7%10% 8% 7% 7% 6%

9% 8% 7% 7% 9%

300+

100-299

50-99

25-49

10-24

<10

% o

f N

o. o

f D

ea

ls

Data as of 30 June 2015. Published 5 August 2015.

US$m

Note: Includes private equity, private credit, private infrastructure and real assets.

29 | EMPEA

EM Median Deal Size by Region

Emerging Asia CEE & CIS Latin America MENA Sub-Saharan Africa

$0

$10

$20

$30

15

6

23

5

8

10

13

25

9

5

10

6

15

5

6

10

4

11

6

1010

7 7

2

9

2011 2012 2013 2014 1H 2015

US

$ M

illio

ns

Data as of 30 June 2015. Published 5 August 2015.

Note: Includes private equity, private credit, private infrastructure and real assets.

30 | EMPEA

EM Median Deal Size by Asset Class

2011 2012 2013 2014 1H 2015$0

$20

$40

$60

$80

$100

1410 9 10 9

90

58

75

85

75

1711

1518

141410 10 10 10

Private Equity Infrastructure & Real Assets Private Credit All Asset Classes

US

$ M

illio

ns

Data as of 30 June 2015. Published 5 August 2015.

Note: Includes private equity, private credit, private infrastructure and real assets.

31 | EMPEA

EM Median Deal Size by Investment Stage

Buyout Growth PIPE Venture CapitalDebt & Mezzanine$0

$20

$40

$60

$80

$100

65

16

30

6

17

35

17

26

4

11

72

1518

4

15

98

15 15

5

18

85

1621

6

14

2011 2012 2013 2014 1H 2015

US

$ M

illio

ns

Data as of 30 June 2015. Published 5 August 2015.

*“Private Capital” includes private equity, private credit, infrastructure and real assets.

Note: Includes private equity, private credit, private infrastructure and real assets.

32 | EMPEA

Largest Known EM InvestmentsLargest Known Investments in Emerging Asia, 1H 2015

Data as of 30 June 2015. Published 5 August 2015.

Fund Manager, Co-investors Company Name Country ICB Sector† Asset ClassInvestment Type

Investment Amount (US$m)

Investment Date

Shikumen Capital Management (SCM), CDH Investments, China International Capital Corp (CICC)

Shanghai Lujiazui International Financial Asset Exchange (Lufax)

China Financial Services Private Equity Growth 483 Mar-15

The Carlyle GroupAsia Satellite Telecommunications Holdings (AsiaSat)

ChinaTechnology Hardware & Equipment

Private Equity PIPE 461 May-15

CITIC Private Equity Funds Management

Jin Cai Holdings China General Industrials Private Equity PIPE 407 May-15

KKR Fujian Sunner Development China Food Producers Private Equity PIPE 400 May-15

Silver Lake Qunar.com China Travel & Leisure Private Equity PIPE 330 Jun-15

Cybernaut (China) InvestmentChongqing Zhubajie Network (Zhubajie.com)

ChinaSoftware & Computer Services

Private Equity Growth 258 Jun-15

DST Global, Accel Partners, Tiger Global Management

ANI Technologies (Ola) (Formerly Olacabs)

India Travel & Leisure Private EquityVenture Capital

252 Apr-15

RRJ CapitalShanghai Yupei Company (China Logistics)

China Industrial Transportation Private Equity Growth 250 Jun-15

RRJ Capital Shanghai Bright Holstan China Food Producers Private Equity Growth 244 Jan-15

† The Industry Classification Benchmark (“ICB”) is owned by FTSE International Limited (“FTSE”). “FTSE®” is a trademark of the London Stock Exchange Group companies and is used by FTSE under license. FTSE does not accept any liability to any person for any loss or damage arising out of any error or omission in the ICB.

Note: Includes private equity, private credit, private infrastructure and real assets.

33 | EMPEA

Data as of 30 June 2015. Published 5 August 2015.

Largest Known Investments ex-Emerging Asia, 1H 2015

Fund Manager, Co-investors Company Name Country ICB Sector† Asset ClassInvestment Type

Investment Amount (US$m)

Investment Date

The Carlyle Group Rede D’Or Sao Luiz BrazilHealth Care Equipment & Services

Private Equity Growth 592 Apr-15

Advent International Allied BrazilTechnology Hardware & Equipment

Private Equity Buyout 373 Feb-15

Apollo Global Management Nova KBM Slovenia Banks Private Equity Buyout 224 Jun-15

Actis Lekela PowerSouth Africa

ElectricityInfrastructure & Real Assets

Growth 220 Feb-15

Mid Europa Partners Danube Foods Group Serbia Food Producers Private Equity Buyout 192 Apr-15

The Abraaj GroupNorth Africa Hospital Holdings Group (NAHHG)

North Africa

Health Care Equipment & Services

Private Equity Growth 145 Mar-15

Ethos Private Equity

Nampak's Tissue, Corrugated and Sacks Division (Neopack and TwinSaver)

South Africa

Household Goods & Home Construction

Private Equity Buyout 133 Apr-15

Patria Investimentos Hidrovias do Brasil Brazil Industrial TransportationInfrastructure & Real Assets

Growth 100 May-15

Helios Investment Partners Africa Oil Corp Kenya Oil & Gas Producers Private Equity Growth 100 May-15

The Abraaj Group Hepsiburada Turkey General Retailers Private Equity Growth 100 Feb-15

Largest Known EM InvestmentsNote: Includes private equity, private credit, private infrastructure and real assets.

† The Industry Classification Benchmark (“ICB”) is owned by FTSE International Limited (“FTSE”). “FTSE®” is a trademark of the London Stock Exchange Group companies and is used by FTSE under license. FTSE does not accept any liability to any person for any loss or damage arising out of any error or omission in the ICB.

34 | EMPEA

Most Active Dealmakers

Fund Manager(s) No. of Deals

Sequoia Capital 56

Matrix Partners 34

IDG Capital Partners (IDGVC) 24

SAIF Partners 24

Tiger Global Management 24

500 Startups 21

East Ventures 20

Accel Partners 14

Lightspeed Venture Partners 14

Morningside Ventures 12

Most Active VC Dealmakers, 1H 2015

Data as of 30 June 2015. Published 5 August 2015.

Fund Manager(s) No. of Deals

Aavishkaar Venture Management 8

Investisseurs et Partenaires (I&P) 8

Sequoia Capital 8

Mezzanine Capital Partners 6

RRJ Capital 5

Advent International, Canbank Venture Capital, CDH Investments, Creador, IDG Capital Partners (IDGVC), KKR, Matrix Partners, The Abraaj Group, TPG, Warburg Pincus

4

Most Active Private Capital (ex. VC) Dealmakers, 1H 2015

Note: “VC” includes seed, early-stage and late-stage transactions.

Note: “Private Capital (ex. VC)” includes private equity growth and buyout, private infrastructure and private credit investments.

Note: Includes private equity, private credit, private infrastructure and real assets.

35 | EMPEA

Cambridge Associates Private Equity & Venture Capital Fund Performance

Emerging Markets │ Q2 2015 Industry Statistics

36 | EMPEA

Global PE & VC Fund Performance

Comparative End-to-End Returns by Region (as of 31 March 2015)

Source: Cambridge Associates LLC Proprietary Index: pooled end-to-end returns, net of fees, expenses and carried interest.

Notes: The index is an end-to-end calculation based on data compiled from 553 global emerging markets private equity and venture capital funds (includes funds investing primarily in Africa, Asia/Pacific–Emerging, Europe–Emerging, Latin America & Caribbean and Middle East–Emerging) including fully liquidated partnerships, formed between 1986 and 2014. The Asia Emerging Markets Index consists of 309 funds, the Europe Emerging Markets Index consists of 61 funds, the Latin America & Caribbean Index consists of 52 funds and the Africa Index consists of 49 funds. Please note that the Global Emerging Markets Index contains 82 funds that do not fall into these specific regions stated above. A Middle East index is not calculated because of insufficient sample size.

Data as of 31 March 2015.

Index One Year Three Year Five Year Ten YearEmerging Markets PE & VC 14.83 11.81 11.94 12.09Emerging Asia PE & VC 23.94 16.39 15.17 14.39CEE & Russia PE & VC -20.29 -2.09 4.35 6.71Latin America & Caribbean PE & VC 0.09 0.04 2.34 9.74Africa PE & VC 0.24 5.99 5.86 7.22MSCI Emerging Markets 0.79 0.67 2.08 8.82US VC 20.21 17.81 16.83 10.82US PE 10.66 14.50 15.43 12.98Western Europe VC 1.53 13.53 12.66 7.09Western Europe PE -4.28 -5.73 8.03 10.64S&P 500 12.73 16.11 14.47 8.01

37 | EMPEA

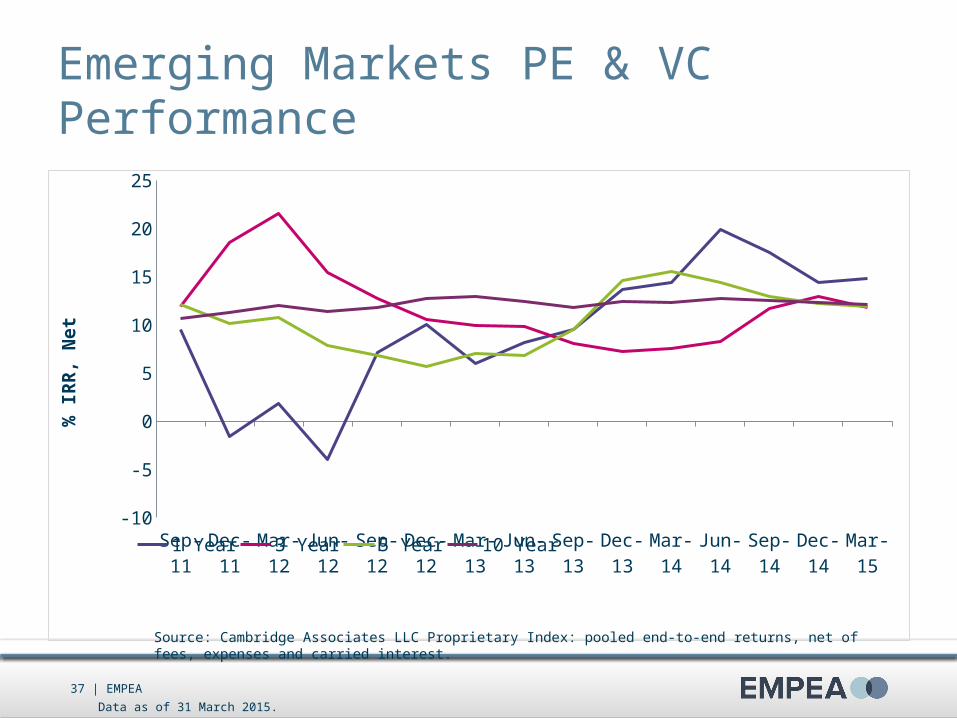

Emerging Markets PE & VC Performance

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Mar-13

Jun-13

Sep-13

Dec-13

Mar-14

Jun-14

Sep-14

Dec-14

Mar-15

-10

-5

0

5

10

15

20

25

1 Year 3 Year 5 Year 10 Year

% IR

R, N

et

Data as of 31 March 2015.

Source: Cambridge Associates LLC Proprietary Index: pooled end-to-end returns, net of fees, expenses and carried interest.

38 | EMPEA

Emerging Asia PE & VC Performance

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Mar-13

Jun-13

Sep-13

Dec-13

Mar-14

Jun-14

Sep-14

Dec-14

Mar-15

-10

-5

0

5

10

15

20

25

30

1 Year 3 Year 5 Year 10 Year

% IR

R, N

et

Data as of 31 March 2015.

Source: Cambridge Associates LLC Proprietary Index: pooled end-to-end returns, net of fees, expenses and carried interest.

39 | EMPEA

Central & Eastern Europe* PE & VC Performance

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Mar-13

Jun-13

Sep-13

Dec-13

Mar-14

Jun-14

Sep-14

Dec-14

Mar-15

-25

-20

-15

-10

-5

0

5

10

15

20

25

1 Year 3 Year 5 Year 10 Year

% IR

R, N

et

Data as of 31 March 2015.

Source: Cambridge Associates LLC Proprietary Index: pooled end-to-end returns, net of fees, expenses and carried interest.

*The Central & Eastern Europe PE Index includes Russia.

40 | EMPEA

Latin America & Caribbean PE & VC Performance

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Mar-13

Jun-13

Sep-13

Dec-13

Mar-14

Jun-14

Sep-14

Dec-14

Mar-15

-15

-10

-5

0

5

10

15

20

25

1 Year 3 Year 5 Year 10 Year

% IR

R, N

et

Data as of 31 March 2015.

Source: Cambridge Associates LLC Proprietary Index: pooled end-to-end returns, net of fees, expenses and carried interest.

41 | EMPEA

Africa PE & VC Performance

Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15-5

0

5

10

15

20

1 Year 3 Year 5 Year 10 Year

% IR

R, N

et

Data as of 31 March 2015.

Source: Cambridge Associates LLC Proprietary Index: pooled end-to-end returns, net of fees, expenses and carried interest.

42 | EMPEA

EMPEA’s industry data and statistics provide an overview of fundraising, investment and exit activity among private alternative asset managers active in the emerging markets of Africa, Asia, Europe, Latin America and the Middle East. Unless stated otherwise, the information presented in EMPEA reports and data products is drawn from EMPEA’s proprietary research database, FundLink, and is based on data obtained from surveys of industry participants, direct communications with fund managers, press releases, trade publications and exchanges with regional and local venture capital associations. Fundraising, investment and exit amounts in EMPEA reports have been confirmed wherever possible directly by fund managers. EMPEA updates historical data on a quarterly basis as new data from fund managers and other sources is compiled in FundLink. Any discrepancies between the aggregate statistics published by EMPEA and the constituent data on individual funds and transactions included in tables and raw data files can be attributed to confidential information that has been omitted from public reporting.

EMPEA’s reporting covers activity by long-term, private, direct investment funds, backed by institutional investors, across the following three asset classes: private equity, private infrastructure and real assets and private credit—collectively “private funds” or “private capital”. EMPEA data and statistics exclude activity from real estate funds, fund of funds, secondaries funds, traditional investment holding companies, corporate strategic investors, government-owned or managed entities and captive investment vehicles, as well as funds investing primarily in publicly-traded equity or debt securities.

Funds: Reported fundraising totals reflect only official closes (interim and/or final) as reported in primary and secondary sources or directly by fund managers. Capital commitments accruing prior to or between official closes are not included in reporting.

Investments: EMPEA classifies investments into one of three asset classes—private equity, private infrastructure and real assets or private credit—and into one of the following deal types: buyout, growth, venture capital, PIPE, mezzanine or debt. Venture capital includes seed, early-stage and late-stage investments. When determining how an investment should be classified, EMPEA takes into account the typical investment strategy of the fund manager(s) involved, the type of security acquired, the reported round number or type of transaction, the development stage of the company at the time of investment, the company’s business model and the type of product or service that the company provides. Secondary investments (both traditional and direct) are excluded from reporting. In addition, wherever possible, bank (acquisition) financing and co-investment from excluded entities (mentioned in the first section of this note) are excluded from reported investment values, both to ensure continuity across regions and to provide a more accurate picture of the scale and pace of capital deployment by the funds that are the primary focus of EMPEA’s research.

Geographies: EMPEA data and statistics are compiled based on the “market” approach. Fundraising activity is categorized based on the countries, sub-regions or regions in which fund

managers intend to invest, while investment activity is categorized based on the country headquarters of investee companies. For companies registered in offshore financial centers or developed markets, but operating exclusively or predominately in emerging markets, investment activity is categorized based on the geographic footprint of the operations of investee companies. In the case of global or multi-regional funds, only those funds investing primarily in emerging markets are included in fundraising totals (e.g., pan-Asia funds with a significant portion of capital intended for investment in China and India). Country-dedicated fundraising data and statistics reflect only those funds with a single-country strategy or mandate. Target allocations to individual markets within a broader global or regional fund are not attributed to single-country fundraising totals.

Regions in this report are defined as: • Emerging Asia: Asia Pacific, excluding Japan, Australia and New Zealand. • Central and Eastern Europe (CEE) and Commonwealth of Independent States (CIS): European Union accession countries (2004), Southeastern Europe (excluding Greece) and Turkey, as well as Russia and other CIS countries.• Latin America: Mexico, Central and South America and the Caribbean (excluding Puerto Rico and other overseas territories and departments).• Middle East and North Africa (MENA): Gulf Cooperation Council (GCC), Afghanistan, Iran, Iraq, Jordan, Lebanon, Pakistan, Palestinian Territories, Syria and Yemen, as well as North Africa (Algeria, Egypt, Libya, Morocco, Sudan and Tunisia).• Sub-Saharan Africa: Africa, excluding North Africa as defined above.

Sectors: EMPEA’s fund and company sector classifications are based on the Industry Classification Benchmark (ICB), which is owned by FTSE International Limited (FTSE). FTSE® is a trademark of the London Stock Exchange Group companies and is used by FTSE under license. FTSE does not accept any liability to any person for any loss or damage arising out of any error or omission in the ICB.

Additional Notes: Abbreviations commonly used in EMPEA reports:EM – Emerging marketsPE – Private equityVC – Venture capitalGP – General partner (fund manager)LP – Limited partner (fund investor) In some exhibits in EMPEA publications, percentage labels may not sum to 100% due to rounding. In all tables in which it appears, “N/A” denotes a confidential or otherwise undisclosed value.

EMPEA Research Methodology

43 | EMPEA

EMPEA is the global industry association for private capital in emerging markets. We are an independent non-profit organization. We have over 300 member firms, comprising institutional investors, fund managers and industry advisors, who together manage more than US$1 trillion of assets and have offices in more than 100 countries across the globe. Our members share EMPEA’s belief that private capital is a highly suited investment strategy in emerging markets, delivering attractive long-term investment returns and promoting the sustainable growth of companies and economies. We support our members through global authoritative intelligence, conferences, networking, education and advocacy.

Robert W. van Zwieten │ President & Chief Executive Officer

Shannon Stroud │ VP, Programs & Business Development

Randy Mitchell │ VP, Strategic Engagement

Ann Marie Plubell │ VP, Regulatory Affairs

Holly Radel │ Senior Director, Marketing & Communications

Nadiya Satyamurthy │ Senior Director, Consulting Services

Kyoko Terada │ Senior Director, Membership & Industry Partners

Mike Casey │ Senior Director, Consulting Services

Phillip Reid │ Chief Financial Officer

Maryam Haque │ Senior Director, Research

Kim Bennett │ Senior Manager, Programs & Events

Emily Sandhaus │ Senior Manager, Programs & Business Development

Jeff Schlapinski │ Manager, Research

Cassie Hodges │ Associate, Marketing & Communications

Abigail Beach │ Associate, Strategic Engagement

Molly Brister │ Senior Research Analyst

Brady Jewett │ Research Analyst

Luke Moderhack │ Research Analyst

Rae Winborn │ Research Analyst

Sara Cousins │ Member Services Coordinator

Leela Vosko │ Member Services Coordinator

Michele Rucker │ Marketing & Communications Coordinator

Michael Barth │ Senior Advisor

David Creighton │ Senior Advisor

Pat Dinneen │ Senior Advisor

Sanjiv Kapur │ Senior Advisor

Jamil Kassum │ Senior Advisor

Peter Tropper │ Senior Advisor

Kelly Williams│ Senior Advisor

1077 30th Street NW • Suite 100 • Washington, DC 20007 USAPhone: +1.202.333.8171 • Fax: +1.202.333.3162 • Web: empea.org

About EMPEA