el paso independent school district annual financial …

TRANSCRIPT

EL PASO INDEPENDENT SCHOOL DISTRICT

ANNUAL FINANCIAL AND COMPLIANCE REPORTS

FOR THE YEAR ENDED JUNE 30, 2015

EL PASO INDEPENDENT SCHOOL DISTRICTAnnual Financial and Compliance Reports

For the Year Ended June 30, 2015

Table of ContentsPage Exhibit

Certificate of Board . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1Directory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

FINANCIAL SECTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Independent Auditor's Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7Management’s Discussion and Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Basic Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27Government-wide Financial Statements:

Statement of Net Position . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29 A-1Statement of Activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30 B-1

Governmental Fund Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33Balance Sheet - Governmental Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34 C-1Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Position . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35 C-2Statement of Revenues, Expenditures and Changes in Fund Balance - Governmental Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36 C-3Reconciliation of the Governmental Funds Statement of Revenues, Expenditures, and Changes in Fund Balances to the Statement of Activities . . . . . . . . . . . . . . . . . . . . . . . . . 37 C-4

Proprietary Fund Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39Statement of Net Position . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40 D-1Statement of Revenues, Expenses, and Changes in Fund Net Position . . . . . . . . . . . . . . . . . . . . . 41 D-2Statement of Cash Flows . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42 D-3

Fiduciary Fund Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43Statement of Fiduciary Net Position . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44 E-1Statement of Changes in Fiduciary Fund Net Position . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45 E-2

Notes to the Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46Required Supplementary Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

Statement of Revenues, Expenditures, and Changes in Fund Balance Budget and Actual - General Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94 G-1Schedule of the District’s Proportionate Share of the Net Pension Liability - Teacher Retirement System . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95 G-2Schedule of District Contributions - Teacher Retirement System . . . . . . . . . . . . . . . . . . . . . . . . . 96 G-3Notes to Required Supplement Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

Supplementary Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99Nonmajor Governmental Funds

Combining Balance Sheet - Nonmajor Governmental Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100 H-1Combining Statement of Revenues, Expenditures, and Changes in Fund Balances - Nonmajor Governmental Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106 H-2

Internal Service FundsCombining Statement of Net Position - Internal Service Funds . . . . . . . . . . . . . . . . . . . . . . . . . . 112 H-3Combining Statement of Revenues, Expenses, and Changes in Fund Net Position - Internal Service Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 113 H-4Combining Statement of Cash Flows - Internal Service Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . 114 H-5

Agency FundStatement of Changes in Assets and Liabilities - Agency Fund . . . . . . . . . . . . . . . . . . . . . . . . . . 115 H-6

EL PASO INDEPENDENT SCHOOL DISTRICT

Table of Contents (Continued)

Page Exhibit

Other Information - Required TEA Schedules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 117Schedule of Delinquent Taxes Receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 118 J-1Schedule of Revenues, Expenditures, and Changes in Fund Balance Budget and Actual - Child Nutrition Program . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120 J-2Schedule of Revenues, Expenditures, and Changes in Fund Balance Budget and Actual - Debt Service Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121 J-3

FEDERAL AWARDS SECTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123Independent Auditor’s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards . . . . . . . . . . . . . . . . . . . . . . . 125Independent Auditor’s Report on Compliance for Each Major Program and on Internal Control Over Compliance Required by OMB Circular A-133 . . . . . . . . . . . . . . . . 127Schedule of Findings and Questioned Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129Schedule of Status of Prior Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131Schedule of Expenditures of Federal Awards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132 K-1Notes on Accounting Policies for Federal Awards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 135

EI Paso Independent School District Name of School District

CERTIFICATE OF BOARD

El Paso County County

071902 Co. -Dis!. Number

We, the undersigned, certify that the attached annual tlnancial and compliance reports of the above named

school district were reviewed and / approved ___ disapproved for the year ended June 30, 2015,

at a meeting of the Board of Trustees of snch school district on the IT" day of November 2015.

Si nature of Board Secretary Signature of Board President

If the Board of Trustees disapproves of the independent auditor's repOlt, the reason(s) for disapproving it is(are): (attach list as necessary)

This page is left blank intentionally.

2

EL PASO INDEPENDENT SCHOOL DISTRICT

DIRECTORY

BOARD OF TRUSTEES

Dori FenenbockPresident

Al VelardeVice-President

Trent HatchSecretary

Bob GeskeMember

Susie ByrdMember

Diane DyeMember

Chuck TaylorMember

ADMINISTRATION

Juan CabreraSuperintendent

3

This page is left blank intentionally.

4

FINANCIAL SECTION

5

This page is left blank intentionally.

6

600 SUNLAND PARK, 6-300 EL PASO, TX 79912

P 915 356-3700 F 915356-3779 W GRP-CPACOM

To the Board of Trustees

INDEPENDENT AUDITOR'S REPORT

EI Paso Independent School District

Report on the Financial Statements

GRP GIBSON RUDDOCK PATTERSON LLC certified public accountants

We have audited the accompanying financial statements of the governmental activities, each major fund, and the aggregate remaining fund information ofEI Paso Independent School District as of and for the year ended June 30, 2015, and the related notes to the financial statements, which collectively comprise the EI Paso Independent School District's basic financial statements as listed in the table of contents.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting pol icies used and the reasonableness of sign ificant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

7

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respectivefinancial position of the governmental activities, each major fund, and the aggregate remaining fundinformation of El Paso Independent School District, as of June 30, 2015, and the respective changes infinancial position, and, where applicable, cash flows, thereof for the year then ended in accordance withaccounting principles generally accepted in the United States of America.

Emphasis of Matter

Change in Accounting Principle

As described in Note I to the financial statements, in 2015 El Paso Independent School District adopted newaccounting guidance, GASB Statement no. 68, Accounting and Financial Reporting for Pensions - andamendment of GASB Statement No. 27. and GASB Statement No. 71, Pension Transition for ContributionsMade Subsequent to the Measurement Date - an amendment of GASB Statement No. 68. Our opinion is notmodified with respect to this matter.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’sdiscussion and analysis, budgetary comparison, and pension information on pages 11 through 26 and 93through 97 be presented to supplement the basic financial statements. Such information, although not a partof the basic financial statements, is required by the Governmental Accounting Standards Board, whoconsiders it to be an essential part of financial reporting for placing the basic financial statements in anappropriate operational, economic, or historical context. We have applied certain limited procedures to therequired supplementary information in accordance with auditing standards generally accepted in the UnitedStates of America, which consisted of inquiries of management about the methods of preparing theinformation and comparing the information for consistency with management’s responses to our inquiries,the basic financial statements, and other knowledge we obtained during our audit of the basic financialstatements. We do not express an opinion or provide any assurance on the information because the limitedprocedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Supplementary and Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectivelycomprise the El Paso Independent School District’s basic financial statements. The combining and individualnonmajor fund financial statements and the required TEA schedules are presented for purposes of additionalanalysis and are not a required part of the basic financial statements. The schedule of expenditures of federalawards is presented for purposes of additional analysis as required by the U.S. Office of Management andBudget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, and is also nota required part of the basic financial statements.

8

The combining and individual nonmajor fund financial statements and the schedule of expenditures of federalawards are the responsibility of management and were derived from and relate directly to the underlyingaccounting and other records used to prepare the basic financial statements. Such information has beensubjected to the auditing procedures applied in the audit of the basic financial statements and certainadditional procedures, including comparing and reconciling such information directly to the underlyingaccounting and other records used to prepare the basic financial statements or to the basic financial statementsthemselves, and other additional procedures in accordance with auditing standards generally accepted in theUnited States of America. In our opinion, the combining and individual nonmajor fund financial statementsand the schedule of expenditures of federal awards are fairly stated in all material respects in relation to thebasic financial statements as a whole.

The required TEA schedules have not been subjected to the auditing procedures applied in the audit of thebasic financial statements and, accordingly, we do not express an opinion or provide any assurance on them.

Other Reporting Required by Government Audit Standards

In accordance with Government Auditing Standards, we have also issued our report dated November 12,2015, on our consideration of the El Paso Independent School District’s internal control over financialreporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grantagreements and other matters. The purpose of that report is to describe the scope of our testing of internalcontrol over financial reporting and compliance and the results of that testing, and not to provide an opinionon internal control over financial reporting or on compliance. That report is an integral part of an auditperformed in accordance with Government Auditing Standards in considering the El Paso Independent SchoolDistrict’s internal control over financial reporting and compliance.

Gibson, Ruddock, Patterson LLCEl Paso, TexasNovember 12, 2015

9

This page is left blank intentionally.

10

MANAGEMENT’S DISCUSSION AND ANALYSIS

11

12

Our discussion and analysis of the El Paso Independent School District’s (the “District”) financial performance provides an overview of the District’s financial activities for the fiscal year ended June 30, 2015. It should be read in conjunction with the basic financial statements, which follow this section. The Management’s Discussion and Analysis is a combination of both government-wide financial statements and fund financial statements. FINANCIAL HIGHLIGHTS The District’s change in net position from normal operations was an increase of $18.8 million. Total net position of the District decreased from $329.9 million in fiscal year 2014 to $275.1 million at year-end 2015. The decrease was due to the new GASB 68 reporting requirement for TRS pension contributions, which resulted in a prior period adjustment of $73.6 million. Due to the GASB adjustment, the ending net position decreased $54.8 million from the prior year. Of this total amount, unrestricted assets decreased by $58.8 million from $92.6 million to $33.8 million. Total revenues increased $11.7 million from $609 million in fiscal year 2014, to $620.7 million in fiscal year 2015. Total expenses increased $9 million, from $592.9 million to $601.9 million.

The District implemented GASB Statement No. 68, Accounting and Financial Reporting for Pensions (“GASB 68”), which establishes accounting and financial reporting standards for school districts to report their portion of the unfunded liability or overfunded asset pension of the Teacher Retirement System of Texas pension plan. The District’s financial statements as of June 30, 2015 are presented in accordance with the guidance provided by this Statement.

The District’s governmental funds financial statements reported a combined ending fund balance in fiscal year 2015 of $219.2 million. The combined ending fund balance of the District decreased $13.7 million from $232.9 million in fiscal year 2014. Of this total amount, $1.5 million is Nonspendable, $115 million is Restricted, $8.1 million is Assigned, and $94.6 million is Unassigned in the General Fund and is available for spending at the District’s discretion. The 2008 Bond Capital Projects fund balance is $73.2 million and includes expenditures of $11.5 million at June 30, 2015.

Several projects were completed during fiscal year 2015. The Reconstruction of Logan Elementary School, located at Fort Bliss, Texas was completed. The project was funded through a Grant from the Department of Defense – Office of Economic Adjustment. Funds from the 2008 Bond Capital Projects fund were utilized for the required local match of $3.3 million. The Grant funded $11.8 million for a total cost of $15.1 million. This is the first Grant of its kind awarded by the Department of Defense. The Reconstruction of Hart Elementary School was also completed during the fiscal year 2015 for $12.1 million and was fully funded by the 2008 Bond Capital Projects fund. There are two classroom additions nearing completion at Milam Elementary School and Chapin High School, both located at Fort Bliss, Texas.

The term for the Bond Committee members ended in May 2015 and the Committee ceased to exist. The Facilities and Construction Department is working to complete all reallocated projects currently in progress in the 2008 Bond Capital Projects fund.

MANAGEMENT’S DISCUSSION AND ANALYSIS

13

ACADEMIC HIGHLIGHTS The El Paso Independent School District (EPISD) exceeded performance requirements on state standards (Target Scores) in all four Indexes on the Texas State Accountability System during the 2015 fiscal year. The Student Achievement Index earned 14 points above the target score of 60. Student Progress Index earned 17 points above the target score of 20. Closing Performance Gap Index exceeded the target score of 28 by 13 points and the Post-Secondary Readiness Index exceeded the target score of 57 by 19 points. When comparing EPISD to the State’s overall performance, EPISD was above the State in Student Achievement by three points, but below the State in Closing Performance Gap and the Post-Secondary Readiness by one point.

The following graph indicates the District’s standing in relation to the State’s overall performance: Distinction designations in academic subjects and areas such as top 25% student progress, top 25% closing performance gaps, and post-secondary readiness were awarded to numerous campuses across the district. Fifty-five EPISD campuses received distinction designations, 37 elementary, 9 middle schools (including MacArthur Elementary-Intermediate), and 9 high schools. There were 42 campuses that received academic distinction designations, 29 in Reading/ELA, 11 in Math, 27 in Science, and 8 in Social Studies. Twenty-nine campuses received a Top 25% Student Progress Distinction, 40 campuses received a Top 25% Closing Performance Gaps Distinction, and 31 campuses received a Post-Secondary Readiness Distinction. Three high schools received all seven distinctions, El Paso, Silva Health Magnet, and Transmountain Early College. Wiggs Middle School was the only middle school that received all seven distinctions. There were eight elementary campuses that received all five distinctions, Coldwell, Lamar, Collins, Cielo Vista, Mitzi Bond, Nixon, Green, and Guerrero.

14

Government-Wide Financial Statements All of the District’s services are reported in the government-wide financial statements (refer to Exhibits A-1 and B-1), including instruction, student support services, student transportation, general administration, school leadership, facilities acquisition and construction and food services. Property taxes, state and federal aid, and investment earnings finance most of the activities. Additionally, all capital and debt financing activities are reported on these statements. The government-wide financial statements are designed to provide readers a broad overview of the District’s finances, in a manner similar to a private-sector business. The statement of net position presents information on all of the District’s assets and liabilities, with the difference between the two reported as net position. Over time, increases or decreases in the net position may serve as a useful indicator of whether the District’s financial position is improving or deteriorating. The statement of activities details how the District’s net position changed during the most recent fiscal year. All changes in the net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Therefore, revenues and expenses are reported in this statement for some items that will only result in cash flows in future fiscal periods (e.g., uncollected taxes and earned but unused sick leave). Both the government-wide financial statements distinguish functions of the District that are principally supported by taxes and intergovernmental revenues (governmental activities), as opposed to business-type activities that are intended to recover all, or a significant portion, of their costs through user fees and charges. Figure A-1 summarizes the major features of the District’s financial statements and the types of information they contain. Figure A-1: Figure A-1 Major Features of the District’s Government‐Wide and Fund Financial Statements

Fund Statements

Type of Statements Government‐Wide Governmental Funds Proprietary Funds Fiduciary Funds

Scope Entire Agency’s Government (except fiduciary funds) and the Agency’s component units

The activities of the District that are not proprietary or fiduciary

Activities the District operates similar to private business

Instances in which the District is the trustee or agent for someone else’s resources

Required financial statements

Statement of net position Balance Sheet Statement of net position Statement of fiduciary position

Statement of activities Statement of revenues, expenditures, & changes in fund balance

Statement of revenues, expenses and changes in fund net position

Statement of changes in fiduciary net position

Statement of cash flows

Accounting basis and measurement focus

Accrual accounting and economic resources focus

Modified accrual accounting and current financial resources focus

Accrual accounting and economic resources focus

Accrual accounting and economic resources focus

Type of asset/liability information

All assets, deferred outflows and liabilities, deferred inflows both financial and capital, short‐term and long‐term

Only assets, deferred outflows, expected to be used up and liabilities, deferred inflows, that come due during the year or soon thereafter; no capital assets included

All assets, deferred outflows and liabilities, deferred inflows, both financial and capital, and short‐term and long‐term

All assets and liabilities, both short‐term and long‐term; the Agency’s funds do not currently contain capital assets, although they can

Type of inflow/outflow information

All revenues and expenses during the year, regardless of when cash is received or paid

Revenues for which cash is received during or soon after the end of the year; expenditures when goods or services have been received and payment is due during the year or soon thereafter

All revenues and expenses during year, regardless of when cash is received or paid

All revenues and expenses during year, regardless of when cash is received or paid

15

OVERVIEW OF THE FINANCIAL STATEMENTS This discussion and analysis is intended to serve as an introduction to the District’s basic financial statements. The District’s basic financial statements are comprised of three components: 1) government-wide financial statements, 2) fund financial statements, and 3) notes to the basic financial statements. This is illustrated in Figure A-2 below. This report also contains required supplementary information, other supplementary information, and TEA required schedules, in addition to the basic financial statements themselves. Fund Financial Statements The District uses fund accounting to keep track of specific sources of funding and spending for particular purposes. The fund financial statements provide additional detailed information about the District’s most significant funds, not the District as a whole. Funds are accounting devices that the District uses to keep track of specific sources of funding and spending for particular purposes:

Some fund designations are required by state law and by bond covenants. The District establishes other funds to control and manage money for particular purposes, or to

show that it is properly using certain grants.

All of the funds of the District can be divided into three categories: governmental funds, proprietary funds, and fiduciary funds.

Figure A‐2. The figure shows how the required parts of this

annual report are arranged and related to one another.

16

Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. Most of the District’s activities are included in governmental funds using modified accrual accounting. The focus is on 1) how cash and other financial assets can readily be converted to cash flow in and out, and 2) the balances left at year-end that are available. However, unlike the government-wide financial statements, governmental fund financial statements provide a detailed short-term view that helps determine whether there are more or fewer financial resources that can be spent in the near future to finance the District’s programs. Proprietary funds are used to account for operations that are financed similar to those found in the private sector. These funds provide both long and short-term financial information. The District maintains a type of proprietary fund called an Internal Service Fund. The District uses Internal Service Funds to account for its Workers’ Compensation, Health Care Clinic, and Print Shop programs. These funds employ the full accrual method. Fiduciary funds are used to account for assets held by the District, in a trustee capacity or as an agent, for individuals, private organizations and/or other funds. No fiduciary funds are used as clearing accounts to distribute financial resources to other funds. The District is responsible for ensuring that the assets reported in these funds are used for their intended purposes. The District uses Fiduciary funds to account for student activity funds and scholarships. All of the District’s fiduciary activities are reported in a separate statement of fiduciary net position, statement of changes in fiduciary net position, and the statement of changes in assets and liabilities. We exclude these activities from the District’s government-wide financial statements, because the District cannot use these assets to finance its operations.

Notes to the Basic Financial Statements

The notes to the basic financial statements provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements.

Other Information

In addition to the basic financial statements and accompanying notes, this report also presents certain required supplementary information that further explains and supports the information in the financial statements. Immediately following the required supplementary information, combining statements are included for the non-major funds, the internal service funds, and the fiduciary funds. In addition, this report also includes the required TEA schedules.

17

GOVERNMENT-WIDE FINANCIAL ANALYSIS

Statement of Net Position

As noted earlier, the net position may serve over time as a useful indicator of the District’s financial position. The District’s total net position was approximately $275.1 million at June 30, 2015. The District’s governmental activities net position decreased by $54.8 million.

Table I El Paso Independent School District

Statement of Net Position (in millions of dollars)

Governmental Activities Percentage2015 2014 Variance Change

Current and other assets 312.1 333.0 (20.9) (6.3%)Capital and Non-Current Assets 570.9 562.7 8.2 1.5%

Total Assets 883.0 895.7 (12.7) (1.4%)

Deferred Charge for Refunding 20.8 3.9 16.9 433.3% Deferred Outflow Related to TRS 14.4 0 14.4 N/A Total Deferred Outflows of Resources 35.2 3.9 31.3 802.6%

Current Liabilities 103.8 103.1 0.7 0.7%Non-Current Liabilities 519.7 466.6 53.1 11.4%

Total Liabilities 623.5 569.7 53.8 9.4% Deferred Inflow Related to TRS 19.6 0.00 19.6 N/A Total Deferred Inflows of Resources 19.6 0.00 19.6

Net Position: Net Investment in Capital Assets 204.4 188.7 15.7 8.3%

Restricted 36.9 48.6 (11.7) (24.1%)

Unrestricted 33.8 92.6 (58.8) (63.5%)

Total Net Position 275.1 329.9 (54.8) (16.6%)

Statement of Activities

Revenues

The District’s total revenues were $620.7 million. A significant portion, approximately 44 percent, of the District’s revenue comes from state aid-formula grants. Operating and capital grants and contributions provided revenue of 24 percent, 31 percent comes from property taxes, while only 1 percent relates to charges for services and local miscellaneous sources.

Funding for governmental activities is by specific program revenue or through general revenues such as, property taxes and investment earnings. The following is a summary of the governmental activities:

The cost of all governmental activities this year was $601.9 million.

Program revenues directly attributable to specific activities funded some of the governmental activities. These program revenues amounted to $156.8 million.

18

The remaining cost of governmental activities, not directly funded by program revenues, was $445 million of which $192.2 million was funded by property taxes, and $270.1 million was funded by state aid – not restricted to specific programs.

Expenses

The District’s total expenses were $601.9 million. The largest portion, $372.5 million or approximately 62 percent, was spent on instruction and instructional related services. Meanwhile, expenses for instructional leadership and school administration were only 7 percent; 8 percent for guidance, social work, health and transportation, while only 2 percent relates to general administration.

19

Investment in capital assets (e.g. land, buildings, furniture, and equipment), less any related debt used to acquire those assets that is still outstanding is $204.4 million. The District uses these capital assets to provide services to students; consequently, these assets are not available for future spending. Although the District’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. An additional portion of the District’s net position of $36.9 million represents resources that are subject to external restrictions on how they may be used. The remaining balance of the unrestricted net position of $33.8 million may be used to meet the District’s ongoing obligations. Changes in Net Position The net position of the District’s governmental activities decreased by 16.6%, or $54.8 million. The total net position of the District was impacted by the following activities:

A prior period adjustment of $73.6 million was required due to the implementation of GASB Statement No. 68, Accounting and Financial Reporting for Pensions, which establishes accounting and financial reporting standards for school districts to report their portion of the unfunded liability or overfunded asset pension of the Teacher Retirement System of Texas pension.

Property Tax Revenue increased $1 million due to increases in the appraised property values. Appraised values for fiscal year 2015 increased by $74.7 million over 2014.

State Aid-Formula Grants increased by $3.2 million. This was due to an increase of $99 in the adjusted allotment per student in the State Foundation Formula.

Charges for Services decreased $1.6 million primarily due to the participation in the Community Eligibility Provision (CEP) program that allowed qualified schools to provide free meals to students.

Operating grants and contributions increased $13.5 million primarily due to an increase in Instructional Materials Allotment of $2.1 million, an increase in the Child Nutrition Program of $4.5 million, an increase in Title I funds of $5 million, a decrease in Title II funds of $3.3 million, an increase of SHARS Medicare cost reimbursement revenue of $2.1 million and the one-time state contribution of $3.8 million for the TRS Non-OASDI fee.

Capital grants and contributions decreased $3.6 million due to the completion of the reconstruction of Logan Elementary School, mostly funded by the Department of Defense.

Instructional expenses increased $2.5 million primarily due to an increase in expenditures for the Power Up Districtwide Initiative of $4.2 million; an increase in textbook purchases of $1.5 million; an increase in instructional supplies of $1.1 million; an increase in the new TRS Non-OASDI contributions of $2.7 million, a decrease in salaries of $3.5 million due to declining student enrollment; and a decrease in the TRS On-Behalf of $1.5 million. There were no contributions made during fiscal year 2015 for Workers Compensation which accounts for a decrease of $1.8 million.

Instructional resources and media resources increased $1.1 million due to additional library reading material purchases.

20

School Leadership increased by approximately $900 thousand due to an increase in TRS Active Care enrollment, new TRS Non-OASDI charge, and an increase in support salaries.

Food services expenditures increased $4.6 million due to the completion of middle and high school cafeteria remodels and the purchase of security cameras and kitchen equipment.

Debt Service expenditures increased by $1.4 million due to the costs for the issuance of Series 2015 and Series 2015A bonds.

Table II El Paso Independent School District

Statement of Activities (in millions of dollars)

Governmental Activities Percentage2015 2014 Variance Change

Revenues Program Revenues Charges for Services 6.6 8.2 (1.6) (19.5%) Operating Grants and Contributions 148.4 134.9 13.5 10.0% Capital Grants and Contributions 1.8 5.4 (3.6) (66.7%) Sub-Total 156.8 148.5 8.3 5.6% General Revenues Property Taxes 192.2 191.3 0.9 0.5% State Aid-Formula Grants 270.1 266.9 3.2 1.2% Investment Earnings 0.5 0.5 0.0 0.0% Miscellaneous 1.6 1.8 (0.2) (11.1%) Special Item - Loss on Disposal of Asset (0.5) 0.0 (0.5) N/A Sub-Total 463.9 460.5 3.4 0.7%Total Revenues 620.7 609.0 11.7 1.9%

Expenses Instruction and Instructional Related 372.5 369.3 3.2 0.9% Instructional Leadership/School Administration 42.8 42.3 0.5 1.2% Guidance, Social Work, Health, Transportation 46.6 47.0 (0.4) (0.9%) Food Services 34.6 29.9 4.7 15.7% Extracurricular Activities 12.0 11.4 0.6 5.3% General Administration 10.8 10.5 0.3 2.9% Plant Maintenance, Security & Data Processing 60.6 61.7 (1.1) (1.8%) Community Services 1.5 1.4 0.1 7.1% Debt Service 17.7 16.3 1.4 8.6% Capital Outlay 0.5 0.7 (0.2) (28.6%) Other Intergovernmental Charges 2.3 2.4 (0.1) (4.2%)Total Expenses 601.9 592.9 9.0 1.5%Increase in Net Position 18.8 16.1 2.7 16.8%

Beginning Net Position 329.9 317.2 12.7 4.0%Prior Period Adjustment (73.6) (3.4) (70.2) 2064.7%Ending Net Position 275.1 329.9 (54.8) (16.6%)

21

DEBT ADMINISTRATION AND CAPITAL ASSETS Long-Term Debt At year-end, the District had $455.6 million in total long term debt outstanding versus $466.5 million at the end of 2015. The District issued the $78,740,000 Unlimited Tax Refunding Bonds, Series 2015 to refund $84,280,000 of the Series 2007 Bonds. The District also issued $104,555,000 Unlimited Tax Refunding Bonds, Series 2015A to refund $108,375,000 of the Series 2008 Bonds. The two bond refundings resulted in $21.5 million of debt service savings over the next 18 years. The present value savings of both issues was $15.6 million.

The net change of bonded debt was $32.6 million, to bring the year-end balance to $365.8 million. The District also made a $3 million principal payment on the 2004B variable rate bonds. This reduced the outstanding balance on the variable rate bonds to $29.7 million.

In the General Fund, the District used $3,345,957 to pay off the balance of the Loan Star loan. The early payoff resulted in interest savings of $338,472 over the next 6 years. Other long term obligations include accrued sick leave of $11.5 million, capital leases of $3.5 million, and the Qualified School Construction Maintenance Tax Notes (QSCMTN) of $15.3 million. The District has established a Sinking Fund and has entered into a Repurchase Investment Agreement to pay off the QSCMTN at maturity, on February 15, 2025. The sinking fund has a year-end balance of $4.5 million.

The District has aggressively managed its debt by competitive bidding to obtain the best interest rates available and by refinancing existing debt for lower rates when in the best interest of the District. The efficient management of budgets and Fund Balance has provided an adequate cash flow so that at no time has the District been short of cash when needed. No investment has been sold before its scheduled maturity date. More detailed information about the District’s long-term liabilities is presented in Note IV.J through Note IV.Q of the Financial Statements.

Bond Ratings The District’s bonds presently carry an ‘AAA’ rating with both Fitch Ratings and Standard & Poor’s. This long-term rating reflects the guaranty provided by the Texas Permanent School Fund. The underlying rating, reflecting the credit quality before considerations of the guaranty is AA by Fitch and AA- by S&P. Both ratings were affirmed in December 2014, with a stable outlook.

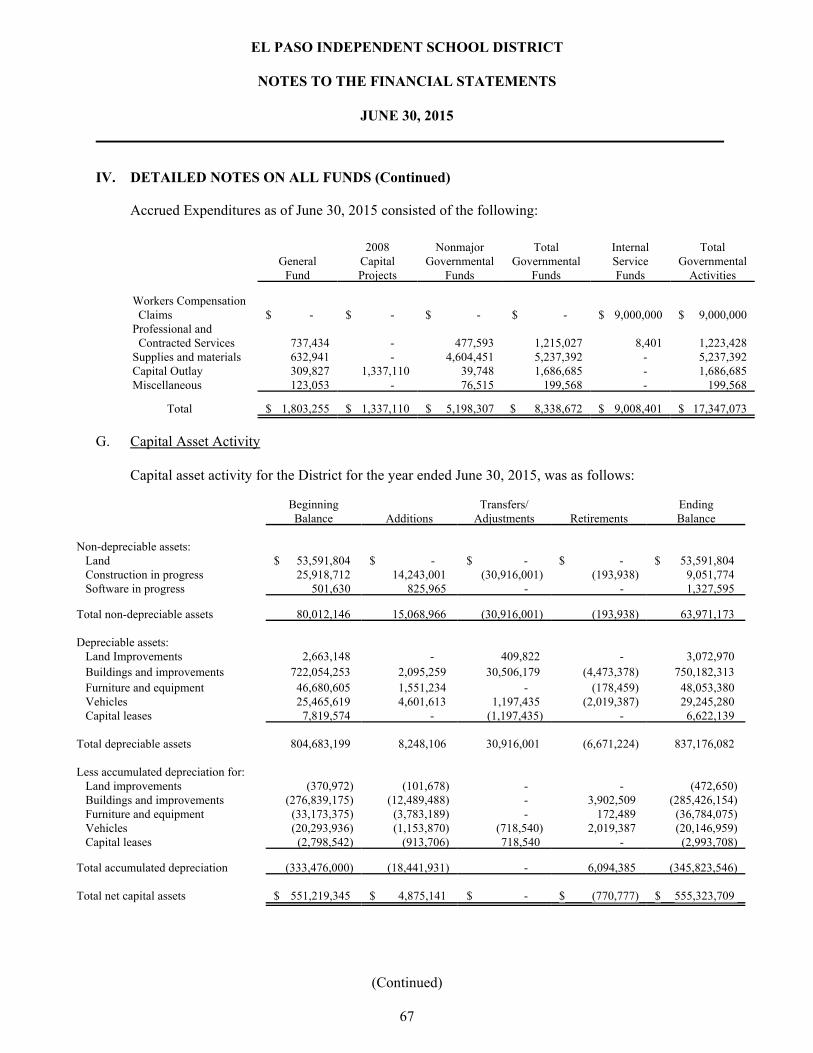

Capital Assets The District has invested $555.3 million, net of depreciation, in a broad range of capital assets including land, buildings and improvements, furniture and equipment and vehicles. This amount represents a net increase (including additions, deductions, and depreciation) of $4.1 million over the past year. Fiscal year 2015 major completed projects include (in millions):

Logan Elementary School Reconstruction $15.1 Hart Elementary School Reconstruction 12.1 Franklin High School Athletic Upgrades 2.2 District-wide Critical Roofing 1.0 Richardson Middle School HVAC Replacement .7 Austin High School Computer labs & Gym upgrades .6 Nixon Elementary School Classroom addition .5 TOTAL MAJOR COMPLETED PROJECTS $32.2

22

Additional detailed information about the District’s capital assets activity is presented in Note IV.G of the Notes to the Financial Statements.

FINANCIAL ANALYSIS OF DISTRICT’S FUNDS

Governmental Funds

The District’s accounting records, for general governmental operations, are maintained on a modified accrual basis as prescribed by the Financial Accountability System Resource Guide, Texas Education Agency, with the revenues being recorded when available and measureable to finance expenditures of the fiscal period. Expenditures are recorded and the fund liabilities are incurred when services or goods are received. The general governmental operations include the following major funds: General Fund and 2008 Capital Projects Fund.

The District has established fund balance categories of nonspendable, restricted, committed, assigned and unassigned. A more detailed explanation about the District’s Fund Balance can be found in Note I.E. 21 and Note IV.X to the financial statements.

The District’s total governmental fund revenues were $620.8 million, compared to $611.2 million in the prior year. Federal Program Revenues increased by $6.3 million. State aid and grants increased by $5.7 million. Local revenues decreased $2.6 million. The Maintenance and Operations tax rate remained at $1.04 (the mandated compressed rate under House Bill 1 of $1.00 plus 4 cents authorized by the Board of Trustees).

The District’s total governmental fund expenditures for fiscal 2015 amounted to $631.2 million compared to $631.5 million in 2014. Instruction, Instructional Resources, and Instructional Staff Development expenses increased by $4.4 million. Transportation increased by $2.2 million, Food Service increased by $7.2 million, and Maintenance decreased approximately $1.3 million. The principal on the debt service cost increased $5.1 million. Facilities, Acquisition and Construction expenses, decreased $13.6 million.

Table III El Paso Independent School District

The District's Capital Assets (in millions of dollars)

Governmental Activities Percentage2015 2014 Variance Change

Land 53.6 53.6 0.0 0.0% Land Improvements 3.1 2.7 0.4 14.8% Buildings & Improvements 750.2 722.1 28.1 3.9% Furniture, Equipment & Vehicles 77.2 72.1 5.1 7.2% Capital Leases 6.6 7.8 (1.2) (15.4%)Construction/Software in Progress 10.4 26.4 (16.0) (60.6%)

Totals at Historical Cost 901.1 884.7 16.4 1.9%

Total Accumulated Depreciation (345.8) (333.5) (12.3) 3.7%

Net Capital Assets 555.3 551.2 4.1 0.7%

23

The governmental funds reported a combined fund balance of $219.2 million, a decrease of $13.7 million. The net decrease of the combined fund balances was comprised of a fund balance increase in the General Fund of $5.8 million, a decrease of $11.4 million in 2008 Capital Projects Fund, and a decrease in the non-major governmental funds of approximately $8.1 million. The General Fund is the primary operating fund of the District. The General Fund balance increased by $5.8 million during the fiscal year to $107.5 million. Revenues came in at approximately 2% higher than budgeted, primarily due to greater tax collections, higher average daily attendance from originally budgeted, and an increase in SHARS/Medicaid and Impact Aid revenue. A portion of the General Fund balance is Nonspendable and held as inventories. This amount is $1.5 million. Another portion, $3.4 million, is Restricted and therefore, is legally segregated for a specific future use. It is restricted by TEA for use by the High School Allotment, Career and Technology Education, and State Compensatory Education. Another portion of the General Fund balance is classified as Assigned, which indicates tentative plans for financial resource utilization in a future period. The District assigned a total of $8.1 million of fund balance. The General Fund total fund balance of $107.5 million is equivalent to approximately 22.9% of expenditures and 73.4 days of operational expenditures in the unassigned fund balance. The unassigned fund balance of $94.6 million, minimizes the likelihood that the District would be required to enter the short-term debt market to pay for current operating expenditures. The fund balance in the Debt Service Fund is $26.6 million, down from $30.6 at year-end 2014. This decrease is mainly due to less State revenue received due to the decline in the number of students. During fiscal year ending June 30, 2015, the District made a $3 million principal payment on the Series 2004B variable bonds. The Interest and Sinking tax rate for fiscal year 2015 remained at the 2014 level of $0.1950. Proprietary Funds The Proprietary Funds are those funds, which are primarily self-supporting. The District maintains three Proprietary Funds, which are the Internal Service Funds. These funds are the Print Shop, the Workers’ Compensation Fund, and the Health Care Clinic Program Fund. The Print Shop, had an operating loss of $37,102 for the current fiscal year ending 2015. There was also a loss in the prior year, of $161,702. The fund closed the year with a positive total net position balance of $230,026. The District reduced staff in the Print Shop during 2015. The Workers’ Compensation Fund experienced a loss of $3,515,658 for the year ending June 30, 2015. The net position ended at $4,445,502. The large deficit was because the District did not contribute to the fund during the 2014-15 fiscal year. The fund also has $9 million in funds to support the claims liability. The District felt that there were sufficient funds on hand to reduce the net position without adversely effecting future fund operations. The Health Care Clinic Program had a loss of $82,819 for the current fiscal year. During the year, the fund received funding at $8 per participant in the TRS Active Care program. It has an ending net position balance of $380,063.

Fiduciary Funds

Fiduciary Funds (trust and agency funds) are used to account for assets held by a government, in a trustee capacity or as an agent, for individuals, private organizations, other governmental units, and/or other funds. The District accounts for student activity funds that are received and held by a school as agency funds. These funds have no equity and do not include revenues or expenditures of the District. The District accounts for scholarship funds in a trust fund.

24

General Fund - Fund Balances

Days of Operational Expenditures in the Unassigned Fund Balance 2008 2009 2010 2011 2012 2013 2014 2015 40.5 32.2 31.9 64.8 68.1 68.7 40.9 73.4

Percentage of Total Fund Balance to GF Expenditures 2008 2009 2010 2011 2012 2013 2014 2015

14.8% 10.3% 12.4% 21.2% 22.1% 22.4% 21.6% 22.9%

25

General Fund Current Year Budgetary Highlights

Over the course of the year, the District revised its budget several times. Expenditures were increased by $11.4 million. The increase in expenditures was primarily attributed to increases in Function 11 – Instructional in the amount of $3.5 million for the purchase of classroom laptops and student calculators, Function 51 – Facilities, Maintenance and Operations in the amount of $400 thousand for the maintenance of campus buildings and grounds, and Function 81 – Facilities Acquisition and Construction in the amount of $2.5 million of roll-forward funds for ongoing projects and $600 thousand for costs associated with the relocation of a data center. Furthermore, the expenditure budget was increased for purchase orders rolled forward from prior year in the amount of $6.1 million. The roll-forward consisted of High School Allotment funding in the amount of $2.9 million for personnel costs and instructional supplies, $2.3 million from the Food Service Fund for operational and equipment costs, and an aggregate $863 thousand from General Fund for encumbrances from various departments, to include Athletics, Fine Arts, Technology Services, and Instructional Departments. Additionally, the budget was increased under Other Financing Sources classification due to the payoff of the Loan Star loan in the amount of the $3.3 million.

Total actual revenues were 2% greater than budgeted revenues. The final budgeted amount for revenues was $470.6 million, and actual revenues totaled $480.2 million. Actual local revenues exceeded budget by $1.1 million. This was due to tax collections exceeding the budget. The reason for higher tax collections was because the taxable levy billed exceeded the certified levy. State revenue exceeded budget by $4.8 million. This was primarily due to ADA coming in at 397 students above projection. Special Education also had higher student counts than the prior year. The new Food Service Community Eligibility Provision program has increased the number of free and reduced students. This has increased our allotment for State Compensatory Education. Actual federal revenues exceeded budget by $3.7 million. This was due to SHARS/Medicaid and Impact Aid revenue exceeding budget, by $1.7 and $1.5 million.

Actual expenditures were $20 million less than the appropriated budget amounts. These positive variances occurred in several areas: Instruction - $6.3 million, the variance was mainly due to equipment that was not received prior to the fiscal year end; to include technology, athletic, and fine arts equipment. The area of facilities maintenance and operations - $6.4 million was attributed to cost savings mainly due to utility costs savings and an increase in E-rate reimbursements and credits. The facilities acquisition and construction area had unspent construction funds totaling $1.5 million which were rolled forward to next fiscal year to complete various projects. Lastly, guidance, counseling and evaluation services had a remaining budget balance of $1.5 million mainly due to vacant personnel positions. Overall, the District experienced savings due to less expenditures, personnel cost savings due to vacancies across functions, and projections of a higher enrollment number for health insurance due to mandatory provisions. However, two areas reported negative variances – these were the areas of social work services ($64) thousand and student (pupil) transportation ($647) thousand. The variance in the social work services area resulted when the Focus on Children and Families Intervention Specialists were reclassified from an external funding source to better align the funding with the intent of the position role. The budgetary shortfall in student (pupil) transportation occurred due to an error in the system upload of personnel budget.

Staffing is budgeted at one hundred percent of actual salary. Budget amounts for vacant positions are monitored to ensure that only limited revisions are allowed for departments. Schools have a flexible revision policy for non-payroll budgets, but cannot transfer excess salary budgets to be used for non-salary purposes. In most cases, unspent payroll dollars are taken back to the fund balance.

26

ECONOMIC FACTORS AND NEXT YEAR’S BUDGETS AND RATES

The District’s elected and appointed officials considered many factors when setting the fiscal year 2016 budget and tax rates. Appraised values used for the 2016 budget preparation decreased by $221 million, or 1.41% less than 2015. The change is due to an increase in the homestead exemption from $15 thousand to $25 thousand. The increase in the exemption occurred with the passage of a state constitutional amendment on November 3, 2015. The loss in local revenue will be offset by increased state funding. In addition, the state funding adjusted allotment increased by $110.

On August 22, 2015, the District held a successful Tax Ratification Election which resulted in a 3 cent increase to the M&O rate. The additional 3 cents will increase the 2016 state funding by $13.8 million. The District’s 2015-16 tax rates are $1.07 for Maintenance and Operations and $.1650 for Interest and Sinking. The District’s 2016 refined average daily attendance was budgeted at 55,204 students. This is a decrease of 984 from the final 2014-15 ADA of 56,188. The District’s Board of Trustees adopted a balanced budget for fiscal year 2015-16. Both revenues and expenditures were budgeted at $490.9 million. CONTACTING THE DISTRICT’S FINANCIAL MANAGEMENT

This financial report is designed to provide our citizens, taxpayers, customers, investors and creditors with a general overview of the District’s finances, and to show the District’s accountability for the funding it receives. The administration believes that the El Paso Independent School District has sound financial practices. The District has financial challenges ahead such as, completing bond construction on time and within budget, increasing salaries to a competitive level, while increasing the Unassigned Fund Balance. The District is moving in the right direction both financially and educationally.

Many thanks are owed to teachers, campus administrators, support staff, the District’s elected and appointed officials, volunteers, and central office administrators, whose purpose is to direct the resources of the District to educate our children. In many cases, these individuals have been asked to make sacrifices to assist the District in achieving its current financial position.

If you have questions about this report or need additional financial information, please contact Maria D. Pineda, Executive Director, Financial Services at (915) 230-2145, or Art Martin, Interim Chief Financial Officer, Business Services at (915) 230-2801, or by mail at El Paso Independent School District, 6531 Boeing Drive, El Paso, Texas, 79925. The El Paso Independent School District does not discriminate in its educational programs or employment practices on the basis of race, color, creed, age, gender, religion, national origin, marital status, ancestry, citizenship, military status, mental or physical disability, gender stereotyping and perceived gender, or on any other basis prohibited by law. Inquiries concerning the application of Titles VI, VII, IX, and Section 504 may be referred to the District compliance officer, Patricia Cortez, at 230‐2033; Section 504 inquiries regarding students may be referred to Verna Ball at 230‐2829. El Distrito Escolar Independiente de El Paso no discrimina en los programas de educación o en prácticas de empleo usando el criterio de raza, color, credo, edad, genero, religión, origen nacional, estado civil, ascendencia, ciudadanía, estado militar, discapacidad física o mental, estereotipo genero o generoidad percibida, u otra práctica prohibida por la ley. Preguntas acerca de la aplicación del título VI, VII o IX, y la Sección 504 pueden ser referidas al oficial del distrito, Patricia Cortez al 230‐2033; preguntas sobre 504 tocante a estudiantes pueden ser referidas a Verna Ball al 230‐2829.

BASIC FINANCIAL STATEMENTS

27

This page is left blank intentionally.

28

EXHIBIT A-1EL PASO INDEPENDENT SCHOOL DISTRICT

STATEMENT OF NET POSITIONJUNE 30, 2015

Control

Data

Codes

Governmental

Activities

Primary Government

ASSETS185,515,496 Cash and Cash Equivalents $1110

4,939,734 Current Investments1120

13,861,785 Property Taxes Receivable (Delinquent)1220

(7,162,000)Allowance for Uncollectible Taxes1230

112,839,279 Due from Other Governments1240

111,135 Accrued Interest1250

433,913 Other Receivables, net1290

1,476,908 Inventories1300

235,780 Prepayments1410

Capital Assets:

56,192,124 Land and Land Improvements, Net1510

464,756,159 Buildings, Net1520

20,367,626 Furniture and Equipment, Net1530

3,628,431 Leased Property Under Capital Leases, Net1550

10,379,369 Construction and Software in Progress1580

60,228 Restricted Assets1800

15,362,594 Long Term Investments1990

Total Assets1000 882,998,561

DEFERRED OUTFLOWS OF RESOURCES20,801,124 Deferred Charge for Refunding1701

14,440,449 Deferred Outflow Related to TRS1705

Total Deferred Outflows of Resources1700 35,241,573

LIABILITIES3,133,657 Accounts Payable2110

5,759,905 Interest Payable2140

6,433,486 Payroll Deductions & Withholdings2150

52,742,305 Accrued Wages Payable2160

12,737 Due to Other Governments2180

17,347,073 Accrued Expenses2200

18,291,720 Unearned Revenue2300

Noncurrent Liabilities

23,524,796 Due Within One Year2501

432,063,846 Due in More Than One Year2502

64,148,427 Net Pension Liability (District's Share)2540

Total Liabilities2000 623,457,952

DEFERRED INFLOWS OF RESOURCES19,623,194 Deferred Inflow Related to TRS2605

Total Deferred Inflows of Resources2600 19,623,194

NET POSITION204,394,860 Net Investment in Capital Assets3200

7,107,674 Restricted for Federal and State Programs3820

21,778,229 Restricted for Debt Service3850

8,086,401 Restricted for Other Purposes3890

33,791,824 Unrestricted3900

Total Net Position3000 275,158,988 $

29The notes to the financial statements are an integral part of this statement.

EL PASO INDEPENDENT SCHOOL DISTRICTSTATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2015

Control

Data

CodesExpenses Services

Charges for

Contributions

Grants and

Operating

Program Revenues

1 43

Primary Government:

GOVERNMENTAL ACTIVITIES:838,748 342,470,623 72,091,638 Instruction $ $ $11

- 11,273,339 1,364,036 Instructional Resources and Media Services12

89,726 18,654,734 8,135,200 Curriculum and Staff Development13

22,432 4,396,206 1,768,061 Instructional Leadership21

33,647 38,471,312 3,466,019 School Leadership23

56,079 22,380,233 6,936,538 Guidance, Counseling and Evaluation Services31

- 4,182,973 786,727 Social Work Services32

- 7,076,101 10,610,739 Health Services33

149,746 13,086,695 1,114,614 Student (Pupil) Transportation34

3,437,243 34,571,954 28,791,696 Food Services35

1,374,738 11,989,018 466,691 Extracurricular Activities36

549,572 10,801,379 1,579,958 General Administration41

91,498 49,610,698 3,489,067 Facilities Maintenance and Operations51

- 5,720,221 440,656 Security and Monitoring Services52

- 5,250,456 213,968 Data Processing Services53

- 1,462,588 1,360,662 Community Services61

- 15,832,910 5,791,913 Debt Service - Interest on Long Term Debt72

- 1,872,908 - Debt Service - Bond Issuance Cost and Fees73

- 462,639 3,230 Capital Outlay81

- 2,348,227 - Other Intergovernmental Charges99

[TP] TOTAL PRIMARY GOVERNMENT: 601,915,214 6,643,429 148,411,413 $ $ $

DataControlCodes

General Revenues:Taxes:

Property Taxes, Levied for General PurposesMT

Property Taxes, Levied for Debt ServiceDT

State Aid - Formula GrantsSF

Investment EarningsIE

Miscellaneous Local and Intermediate RevenueMI

Special Item - Loss on Disposal of AssetsS2

Total General Revenues and Special ItemsTR

Net Position - Beginning

Change in Net Position

Net Position - Ending

Prior Period Adjustment Required by GASB 68

CN

NB

PA

NE

30

The notes to the financial statements are an integral part of this statement.

EXHIBIT B-1

Net (Expense) Revenue and

Activities

Governmental

Contributions

Grants and

Capital

5

Primary Government

6

Changes in Net Position

(269,540,237)$ - $

(9,909,303) - (10,429,808) -

(2,605,713) - (34,971,646) - (15,387,616) - (3,396,246) - 3,534,638 -

(11,822,335) - (2,343,015) -

(10,147,589) -

(8,671,849) - (46,030,133) - (5,279,565) - (5,036,488) -

(101,926) - (10,040,997) - (1,872,908) - 1,353,619 1,813,028

(2,348,227) -

(445,047,344)1,813,028 $

161,542,945 30,733,241

270,032,641 462,759

1,581,098 (476,580)

463,876,104

18,828,760

329,942,806

275,158,988 $

(73,612,578)

31

This page is left blank intentionally.

32

GOVERNMENTAL FUND FINANCIAL STATEMENTS

33

EXHIBIT C-1EL PASO INDEPENDENT SCHOOL DISTRICT

BALANCE SHEET

GOVERNMENTAL FUNDS

JUNE 30, 2015

Control

Data

Codes

General

Fund Projects

Capital

2008

Funds

Other

Funds

Governmental

Total

ASSETS65,140,042 81,073,136 27,043,285 173,256,463 Cash and Cash Equivalents $ $ $ $1110

- 4,939,734 - 4,939,734 Investments - Current1120

- 11,828,367 2,033,418 13,861,785 Property Taxes - Delinquent1220

- (6,110,000) (1,052,000) (7,162,000)Allowance for Uncollectible Taxes (Credit)1230

- 91,293,342 21,545,937 112,839,279 Receivables from Other Governments1240

16,081 21,136 72,347 109,564 Accrued Interest1250

2,552,947 13,139,438 11,970,479 27,662,864 Due from Other Funds1260

- 396,876 37,037 433,913 Other Receivables1290

- 1,475,114 1,794 1,476,908 Inventories1300

- - 60,228 60,228 Restricted Assets1800

6,847,016 - 6,109,030 12,956,046 Long Term Investments1900

Total Assets1000 198,057,143 74,556,086 67,821,555 340,434,784 $ $ $ $

LIABILITIES - 2,653,447 287,919 2,941,366 Accounts Payable $ $ $ $2110

- 6,433,486 - 6,433,486 Payroll Deductions and Withholdings Payable2150

- 44,622,166 8,118,694 52,740,860 Accrued Wages Payable2160

- 14,691,253 12,492,282 27,183,535 Due to Other Funds2170

- 754 11,983 12,737 Due to Other Governments2180

1,337,110 1,803,255 5,198,307 8,338,672 Accrued Expenditures2200

- 15,764,360 2,527,360 18,291,720 Unearned Revenues2300

Total Liabilities2000 85,968,721 1,337,110 28,636,545 115,942,376

DEFERRED INFLOWS OF RESOURCES - 4,551,692 763,476 5,315,168 Unavailable Revenue - Property Taxes2601

Total Deferred Inflows of Resources2600 4,551,692 - 763,476 5,315,168

FUND BALANCESNonspendable Fund Balance:

- 1,475,114 - 1,475,114 Inventories3410

Restricted Fund Balance:

- - 7,107,674 7,107,674 Federal or State Funds Grant Restriction3450

73,218,976 - - 73,218,976 Capital Acquisition and Contractual Obligation3470

- - 26,644,278 26,644,278 Retirement of Long-Term Debt3480

- 3,416,819 4,669,582 8,086,401 Other Restricted Fund Balance3490

Assigned Fund Balance: - 1,981,987 - 1,981,987 Construction3550

- 6,097,930 - 6,097,930 Other Assigned Fund Balance3590

- 94,564,880 - 94,564,880 Unassigned Fund Balance3600

Total Fund Balances3000 107,536,730 73,218,976 38,421,534 219,177,240

Total Liabilities, Deferred Inflows & Fund Balances4000 198,057,143 74,556,086 67,821,555 340,434,784 $ $ $ $

34

The notes to the financial statements are an integral part of this statement.

EXHIBIT C-2EL PASO INDEPENDENT SCHOOL DISTRICT

RECONCILIATION OF THE GOVERNMENTAL FUNDS BALANCE SHEET TO THESTATEMENT OF NET POSITION

JUNE 30, 2015

219,177,240 $Total Fund Balances - Governmental Funds

5,055,591 1 The District uses internal service funds to charge the costs of certain activities, such as self-insurance and printing, to appropriate functions in other funds. The assets and liabilities of the internal service funds are included in governmental activities in the statement of net position. The net effect of this consolidation is to increase net position.

81,827,874 2 Capital assets used in governmental activities are not financial resources and therefore are not reported in governmental funds. At the beginning of the year, the cost of these assets was $884,695,345 and the accumulated depreciation was ($333,476,000). In addition, long-term liabilities, including bonds payable, are not due and payable in the current period, and, therefore are not reported as liabilities in the funds. The net effect of including the beginning balances for capital assets (net of depreciation) and long-term debt in the governmental activities is to increase net position.

48,581,618 3 Current year capital outlays and long-term debt principal payments are expenditures in the fund financial statements, but they should be shown as increases in capital assets and reductions in long-term debt in the government-wide financial statements. The net effect of including the 2015 capital outlays and debt principal payments is to increase net position.

(69,331,172)4 Included in the items related to debt is the recognition of the District's proportionate share of the net pension liability required by GASB 68 in the amount of $64,148,427, a Deferred Resource Inflow related to TRS in the amount of $19,623,194 and a Deferred Resource Outflow related to TRS in the amount of $14,440,449. This amounted to a decrease in Net Position in the amount of $69,331,172.

(18,419,368)5 The 2015 depreciation expense increases accumulated depreciation. The net effect of the current year's depreciation is to decrease net position.

8,267,205 6 Various other reclassifications and eliminations are necessary to convert from the modified accrual basis of accounting to accrual basis of accounting. These include recognizing unavailable revenue from property taxes as revenue, reclassifying the proceeds of bond sales as an increase in bonds payable, and recognizing the liabilities associated with maturing long-term debt and interest. The net effect of these reclassifications and recognitions is to increase net position.

275,158,988 $19 Net Position of Governmental Activities

35

The notes to the financial statements are an integral part of this statement.

EXHIBIT C-3EL PASO INDEPENDENT SCHOOL DISTRICT

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCE

GOVERNMENTAL FUNDS

FOR THE YEAR ENDED JUNE 30, 2015

Control

Data

Codes

General

Fund Projects

Capital

2008

Funds

Other

Funds

Governmental

Total

REVENUES:133,151 167,039,171 35,060,206 202,232,528 Total Local and Intermediate Sources $ $ $ $5700

- 296,684,012 12,750,700 309,434,712 State Program Revenues5800 - 16,472,761 92,620,269 109,093,030 Federal Program Revenues5900

Total Revenues5020 480,195,944 133,151 140,431,175 620,760,270

EXPENDITURES:Current:

- 282,592,973 47,674,216 330,267,189 Instruction0011 - 9,991,184 848,861 10,840,045 Instructional Resources and Media Services0012 - 10,716,866 7,742,853 18,459,719 Curriculum and Instructional Staff Development0013 - 2,691,994 1,638,533 4,330,527 Instructional Leadership0021 - 35,886,086 902,060 36,788,146 School Leadership0023 - 15,795,544 6,311,113 22,106,657 Guidance, Counseling and Evaluation Services0031 - 3,467,017 647,143 4,114,160 Social Work Services0032 - 6,297,203 478,293 6,775,496 Health Services0033 - 16,026,451 387,798 16,414,249 Student (Pupil) Transportation0034 - - 37,267,243 37,267,243 Food Services0035 - 11,661,237 - 11,661,237 Extracurricular Activities0036 - 9,872,121 - 9,872,121 General Administration0041

505,420 46,641,001 1,623,902 48,770,323 Facilit ies Maintenance and Operations0051 - 5,506,309 102,063 5,608,372 Security and Monitoring Services0052

783,734 5,418,684 - 6,202,418 Data Processing Services0053 - 125,833 1,355,565 1,481,398 Community Services0061

Debt Service: - 2,399,992 23,220,000 25,619,992 Principal on Long Term Debt0071 - 446,759 15,456,349 15,903,108 Interest on Long Term Debt0072 - 661 1,872,247 1,872,908 Bond Issuance Cost and Fees0073

Capital Outlay:10,250,912 2,445,580 1,813,028 14,509,520 Facilit ies Acquisition and Construction0081

Intergovernmental: - 2,348,227 - 2,348,227 Other Intergovernmental Charges0099

Total Expenditures6030 470,331,722 11,540,066 149,341,267 631,213,055

1100 Excess (Deficiency) of Revenues Over (Under)

Expenditures9,864,222 (11,406,915) (8,910,092) (10,452,785)

OTHER FINANCING SOURCES (USES): - - 183,295,000 183,295,000 Capital Related Debt Issued (Regular Bonds)7911 - - 684,059 684,059 Transfers In7915 - - 33,808,270 33,808,270 Premium or Discount on Issuance of Bonds7916 - (684,059) - (684,059)Transfers Out (Use)8911 - (3,345,957) (217,043,789) (220,389,746)Other (Uses)8949

Total Other Financing Sources (Uses) 7080 (4,030,016) - 743,540 (3,286,476)

1200 Net Change in Fund Balances 5,834,206 (11,406,915) (8,166,552) (13,739,261)

0100 Fund Balance - July 1 (Beginning) 101,702,524 84,625,891 46,588,086 232,916,501

3000 Fund Balance - June 30 (Ending) $ 107,536,730 $ 73,218,976 $ 38,421,534 $ 219,177,240

36The notes to the financial statements are an integral part of this statement.

EXHIBIT C-4EL PASO INDEPENDENT SCHOOL DISTRICT

RECONCILIATION OF THE GOVERNMENTAL FUNDS STATEMENT OF REVENUES, EXPENDITURES,AND CHANGES IN FUND BALANCES TO THE STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2015

(13,739,261)$Total Net Change in Fund Balances - Governmental Funds

(3,635,579)The District uses internal service funds to charge the costs of certain activities, such as self-insurance and printing, to appropriate functions in other funds. The net loss of internal service funds are reported with governmental activities. The net effect of this consolidation is to decrease net position.

48,581,618 Current year capital outlays and long-term debt principal payments are expenditures in the fund financial statements, but they should be shown as increases in capital assets and reductions in long-term debt in the government-wide financial statements. The net effectof removing the 2015 capital outlays and debt principal payments is to increase net position.

(18,419,368)Depreciation is not recognized as an expense in governmental funds since it does not require the use of current financial resources. The net effect of the current year's depreciation is to decrease net position.

1,759,944 Various other reclassifications and eliminations are necessary to convert from the modified accrual basis of accounting to accrual basis of accounting. These include recognizing unavailable revenue from property taxes as revenue, adjusting current year revenue to show the revenue earned from the current year's tax levy, reclassifying the proceeds of bond sales, and recognizing the liabilities associated with maturing long-term debt and interest. The net effect of these reclassifications and recognitions is to increasenet position.

4,281,406 The implementation of GASB 68 required that certain expenditures be de-expended and recorded as deferred resource outflows. The contributions made after the measurement date of 8/31/2014 caused the change in the ending net position to increase in the amount of $9,278,654. Contributions made before the measurement date but during the 2015 FY were also de-expended and recorded as a reduction in the net pension liability for the District. This also caused an increase in the change in net position in the amount of $932,140. The District recorded its proportionate share of the pension expense during the measurement period as part of the net pension liability. The amounts expensed for FY 2015 were $9,964,913 for pension expense columns 6 - 12 from TRS data and the amounts de-expended for the net deferred resource inflow recognized by TRS in the measurement period were $4,035,525. This caused a net decrease in the change in net position of $5,929,388. The impact of all of these is to increase the change in net positionby $4,281,406.

18,828,760 $ Change in Net Position of Governmental Activities

37

The notes to the financial statements are an integral part of this statement.

This page is left blank intentionally.

38

PROPRIETARY FUND FINANCIAL STATEMENTS

39

EXHIBIT D-1EL PASO INDEPENDENT SCHOOL DISTRICT

STATEMENT OF NET POSITIONPROPRIETARY FUNDS

JUNE 30, 2015

Total

Internal

Service Funds

Governmental

Activities -

ASSETSCurrent Assets:

12,259,033 Cash and Cash Equivalents $

1,571 Accrued Interest

167,827 Due from Other Funds

12,428,431 Total Current Assets

Noncurrent Assets:Capital Assets:

368,294 Furniture and Equipment

(298,389)Depreciation on Furniture and Equipment

2,406,548 Long Term Investments

2,476,453 Total Noncurrent Assets

Total Assets 14,904,884

LIABILITIES

Current Liabilities:

192,291 Accounts Payable

1,445 Accrued Wages Payable647,156 Due to Other Funds

9,008,401 Accrued Expenses

Total Liabilities 9,849,293

NET POSITION

69,905 Net Investment in Capital Assets

4,985,686 Unrestricted Net Position

Total Net Position 5,055,591 $

40

The notes to the financial statements are an integral part of this statement.

EXHIBIT D-2EL PASO INDEPENDENT SCHOOL DISTRICT

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN FUND NET POSITION

PROPRIETARY FUNDS

FOR THE YEAR ENDED JUNE 30, 2015

Total

Internal

Service Funds

Governmental

Activities -

OPERATING REVENUES:

1,456,643 Local and Intermediate Sources $

Total Operating Revenues 1,456,643

OPERATING EXPENSES:

3,893,056 Payroll Costs

994,233 Professional and Contracted Services

136,052 Supplies and Materials

59,133 Other Operating Costs

22,563 Depreciation Expense

Total Operating Expenses 5,105,037

Operating Income (Loss) (3,648,394)

NONOPERATING REVENUES (EXPENSES):

12,815 Earnings from Temporary Deposits & Investments

Total Nonoperating Revenues (Expenses) 12,815

Change in Net Position

Total Net Position - July 1 (Beginning)

Total Net Position - June 30 (Ending)

(3,635,579)

8,691,170

$ 5,055,591

41

The notes to the financial statements are an integral part of this statement.

EXHIBIT D-3EL PASO INDEPENDENT SCHOOL DISTRICT

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED JUNE 30, 2015PROPRIETARY FUNDS

Total

Internal

Service Funds

Governmental

Activities -

Cash Flows from Operating Activities:

25,294 Cash Received from User Charges $

1,575,960 Cash Received from Assessments - Other Funds(1,086,798)Cash Payments to Employees for Services(2,211,850)Cash Payments for Insurance Claims

(938,377)Cash Payments for Suppliers(59,133)Cash Payments for Other Operating Expenses

(2,694,904)Net Cash Used for OperatingActivities

Cash Flows from Investing Activities:

(12,036,518)Purchase of Investment Securities12,522,917 Proceeds from Sale & Maturities of Securities

21,786 Interest and Dividends on Investments

508,185 Net Cash Provided by InvestingActivities

Net Decrease in Cash and Cash Equivalents (2,186,719)

Cash and Cash Equivalents at Beginning of Year 14,445,752

Cash and Cash Equivalents at End of Year 12,259,033 $

Operating Income (Loss):$

Reconciliation of Operating Income (Loss) to Net Cash

Used for Operating Activities:(3,648,394)

to Net Cash Used for Operating Activities:Adjustments to Reconcile Operating Income

22,563 Depreciation

Assets and Liabilities:Effect of Increases and Decreases in Current

161,999 Decrease (increase) in Due from Other Funds127,107 Increase (decrease) in Accounts Payable

(195)Increase (decrease) in Accrued Wages Payable1,854 Increase (decrease) in Accrued Expenses

640,162 Increase (decrease) in Due to Other FundsNet Cash Used for OperatingActivities (2,694,904)$

42

The notes to the financial statements are an integral part of this statement.

FIDUCIARY FUND FINANCIAL STATEMENTS

43

EXHIBIT E-1EL PASO INDEPENDENT SCHOOL DISTRICTSTATEMENT OF FIDUCIARY NET POSITION

FIDUCIARY FUNDSJUNE 30, 2015

Private

Purpose

Trust Fund Fund

Agency

ASSETS

2,295,929 - Cash and Cash Equivalents $ $

- 190,364 Restricted Assets

Total Assets 190,364 2,295,929 $

LIABILITIES

2,295,929 - Due to Student Groups $

Total Liabilities - 2,295,929 $

NET POSITION

190,364 Restricted for Scholarships

Total Net Position 190,364 $

44

The notes to the financial statements are an integral part of this statement.

EXHIBIT E-2EL PASO INDEPENDENT SCHOOL DISTRICT

STATEMENT OF CHANGES IN FIDUCIARY FUND NET POSITIONFIDUCIARY FUNDS

FOR THE YEAR ENDED JUNE 30, 2015

Private

Purpose

Trust Fund

ADDITIONS:

1,259 Local and Intermediate Sources $

Total Additions 1,259

DEDUCTIONS:

8,303 Other Operating Costs

Total Deductions 8,303

Change in Net Position

Total Net Position - July 1 (Beginning)

Total Net Position - June 30 (Ending)

(7,044)

197,408

$ 190,364

45

The notes to the financial statements are an integral part of this statement.

EL PASO INDEPENDENT SCHOOL DISTRICT

NOTES TO THE FINANCIAL STATEMENTS

JUNE 30, 2015

I. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES