egypt s atural gas arket overview - unece

TRANSCRIPT

EGYPT’SNATURAL GAS

MARKET OVERVIEW

2

Egypt’s Gas Industry Milestones

1st gasDiscovery

1967 1976 1981 1992 1996 2003 2012

1st

Industrialcustomer

1st

Residentialcustomer

1st CNG Vehicle

Private LDC

1st Gas Export

1st FSRUTender

2015

1st LNG import

GasRegulator

2017

3

0102030405060708090

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

BCM/yr

Nooros Fields West Delta Deep Marine West Nile Delta Project

Zohr Total production

Historical and Forecast Gas Production (by area)

4

Zohr Gas Discovery

• The Largest gas discovery in the Mediterranean.• One of the largest gas discoveries in The World.• 30+ TCF of GAS in place• 1.5km water depth , 100 km2 acreage, 220km from shore• Significant potential in adjacent Blocks

5

A 500 mmcfd capacity Floating Storage andRegasification Unit (FSRU) was installedat the Port of Sokhna on the Red Sea and multi-year deals have been concluded with LNG

sellers.A second FSRU, with a capacity of 750 mmcfd,was commissioned in November 2015 alongsidethe first at Sokhna

In August 2015, Eni announced the Zohrdiscovery, a new play opening find with anestimated 21.5tcf of recoverable gas reserves.With a fast track development planned, Zohr willhelp to reduce the need for costlier LNG imports.This new source of gas will help Egypt to lower itscost of supply and, if followed by furtherdiscoveries, could see Egypt return to a period ofenergy self sufficiency

Source: Woodmac – Seek Permission, OIES

61.3 63 61.9 5748.5 44 41.6 47 46 45.1

36.128.9 23.9 18 14.7 12

0.3 0.4

515.3

23.6 39.443.7 48

49.348.3

45.5

3.610.3

10

10.3

2.82.8

-10.4 -9.4 -7.7 -3.7 -1.4 -0.8 -0.7 -0.7 -0.7 -0.7 -2.9-4.8 -8.7 -10.1 -11.5

Production online in 2015

New gas production (2015)

LNG imports

LNG exports

Gas balance (BCM)

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Due to the ongoing energy shortageEgypt began importing LNG in 2015

LNG imports act as bridge for next upstream production

6

Egypt as the new Energy Hub in the Mediterranean

• Major recent huge gas discoveries (Zohr)

• Oil & Gas infrastructure (LNG Facilities, Pipelines)

• Centered looking in the middle of resource-rich countries and major energy

consumers, as well as availability of major Int. Maritime Trade lines.

EMG P/L

FAJR P/L

Damietta LNG

Idku LNG

East Gas P/LAQABAFSRU

FSRU

ZOHR

7

Source: World Steel Association, BP Statistical Review, GIIGNL LNG Reports

Steel production Ktn/yr

Gas production

LNG imports

0

10

20

30

40

50

60

70

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

LNG helps growth in the Egyptian steel industry

Gas & LNGimports (BCM)

Steel production‘000tn/yr

LNG imports enablesteel plants to continue

to operate

Rapidly deployed FSRUs importLNG until new fields were inproduction

This allowed $457mn steel tobe exported, using idlecapacity, keeping the lights onwith significant financial andenvironmental saving vsalternative fuels

with greater than anticipateddemand led to costly fuel and power shortages in Egypt

Falling domestic production

Gas fuels economic growth

8

Gas Usages

Gas GridLocal Distribution

Gas Delivery

Fertilizers

Industry

CNG

Domestic

Power

Gas Value Chain in Egypt

9

Natural Gas Supply vs. Demand vs. Consumption

Going forward, Egypt will witness a growth in natural gas production from “supergiant” Zohr. Producing currently 0.349 BCF per day, to reach 1 BCF per day in June and 2.7 BCF by end of 2019.

Additionally importation through gas el sharq will start beginning of 2019.

Egypt consumption of Natural gas is increasing by higher rate than worldwide consumption Despitethe drop of production in the last four years, turning Egypt from being a gas exporter to gas importerWith the new discovery of Zohr, net gas imports are expected to be covered by local production.

10

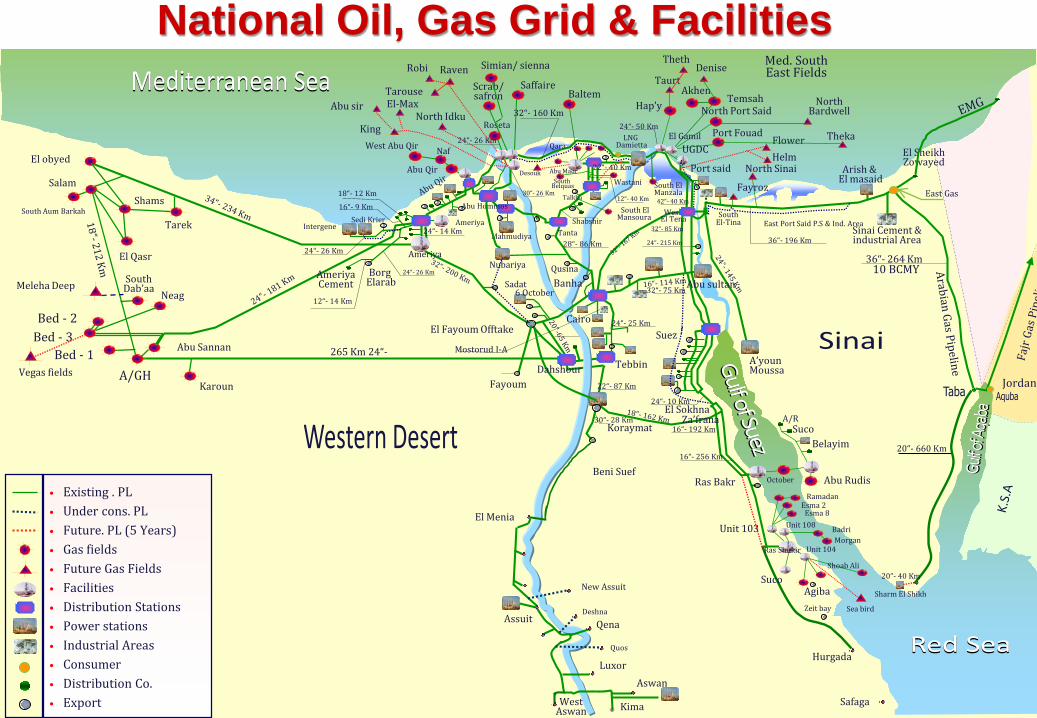

Abu sir

West Abu Qir

North Idku

RavenScrab/safron

LNGDamietta

Arish &El masaid

Baltem

Port said

Hap’y

Theka

North Bardwell

Akhen

Naf

Roseta

El Sheikh Zowayed

East Port Said P.S & Ind. Area

East Gas

Flower

North SinaiHelm

Temsah

Talkha

Shabshir

Abu MadiAbu Qir

Abu Hommos South El Mansoura

Mahmudiya

Qara

Tanta

SouthBelquas

Abu sultan6 October

QusinaBanhaSadat

Suez

A’youn Moussa

Mostorud I-ATebbin

Koraymat

Ras BakrBeni Suef

Za’frana

October

Unit 103El Menia

Assuit

Unit 104

Unit 108

Zeit bay

Abu Rudis

Morgan

Ramadan

Esma 8

AgibaSea bird

Shoab Ali

Badri

Esma 2

Sinai Cement & industrial Area

Sedi Krier

Ameriya

King

El-Max

Intergene

BorgElarab

Ameriya Cement

12“- 14 Km

El obyed

Salam

South Aum Barkah

El Qasr

Tarek

Bed - 2

Abu Sannan

South Dab’aaMeleha Deep

Bed - 3Bed - 1 265 Km 24“-

Qena

LuxorAswan

Kima

Hurgada

Safaga

Cairo

Neag

A/GHKaroun

SouthEl-Tina

WestEl Tena

Jordan

DeniseTaurt

El GamilUGDC

South El Manzala

Shams

Saffaire

Simian/ sienna

Fayroz

Robi

Tarouse

Theth Med. South East Fields

Vegas fields

Desouk

A/RSuco

Belayim

Wastani

Fayoum

El Sokhna

• Existing . PL• Under cons. PL• Future. PL (5 Years)• Gas fields• Future Gas Fields• Facilities• Distribution Stations• Power stations• Industrial Areas• Consumer• Distribution Co.• Export

Ameriya

24“- 26 Km

18“- 12 Km

16“- 9 Km

24“- 26 Km

24“- 26 Km

32“- 160 Km

24“- 14 Km

30“- 26 Km

22“- 87 Km

24“- 25 Km

32“- 75 Km

24“- 215 Km

32“- 85 Km

28“- 86 Km

42“- 40 Km

30“- 28 Km

16“- 256 Km

16“- 192 Km

24“- 10 Km

22“- 40 Km

24“- 50 Km

36“- 196 Km

36“- 264 Km10 BCMY

20“- 660 Km

20“- 40 Km

12“- 40 Km

National Oil, Gas Grid & Facilities

Dahshour

Nubariya

North Port Said

Port Fouad

Sharm El Shikh

Suco

West Aswan

Ras Shukir

El Fayoum Offtake

Deshna

Quos

New Assuit

11

Natural Gas Consumption in numbers (till June 2018)

Source: EGAS annual report 2018

» 58 Power Generation plants

» 14 Local Distribution companies

» More than 2,491 Industrial Consumer

» 415 brick kilns

» 8.8 Million Residential Customer

» More than 18,776 Commercial customer

» 7486 Bakeries

» 243,688 vehicles converted to CNG

» More than 70 conversion centers

» 187 CNG stations

12

Gas to end users

• FactoriesMedium Heavy

- Chemical - Steel- Paint - Cement- Textile - Fertilizer- Food

Fuels substitution & conversionWater heating Space heating

Cooking Steam Generation

Furnaces Manufacturing Process Heat

Refrigeration Gas-fired Air-conditioning

Natural gas will replace:

• Diesel for water and central heating

• LPG for heating and cooking

• Fuel oil and diesel for industrial applications

• Gasoline in cars

Residential

Commercial

Industrial

• Apartments• Houses• Villas

• Hospitals• Schools and Universities• Offices• Restaurants• Bakeries etc.

13

Development of the Egyptian Gas Distribution Sector

14

Gas Distribution – Deregulation Development

The Main National Grid / Trunk line is constructed & Operated by GASCO (on behalf of EGAS)Everything down stream of the Pressure Reduction Station is within the cost of the LDC connection rate. Payments made “per converted customer”

15

From ONE state monopoly …

… to 9 private sectors & 5 state-owned LDCs/EPCs

Development of the Egyptian Gas Distribution Sector

Off Take

P.R.SRegulator

Regulator

Typical Downstream Gas Network

Ongoing Distribution Activities8.8 Million customers connected

Over 1 bn $ of Foreign & Local investment

16 Egyptian Governorates covered by Gas networks

600 MM $ /Year Saved in subsidies

Enhanced HSE Standards

Introducing new technologies

Attracting the Multi-Nationals

Social Investment – Jobs/Employment - Environmental

Provide a better quality of life for Egypt’s citizens

16

Well developed gas grid;

The end consumer price and margin areregulated;

Conversion is undertaken only by the CNGcompanies;

Local codes in place governing all technicaland HSE aspects;

Conversion loans were offered through CNGcompanies till mid. 2003, now throughcommercial banks;

The Government is the sole supplier of thegas, and the sole owner of the supply gridnationwide

Compressed Natural Gas “CNG” Business Model

17

Deregulation Development – Egypt’s CNG Market

Phase I1992 - 1996

Phase II1996 - 2002

Phase III2002 - now

Pilot Project National Project Expansion

2 Pilot ProjectsWith the assistance

Of 2 IOCs

Monopoly2 State-Owned(JV with IOCs)

4 Private “NGVs”

(Local & Int.)

18

Market based Incentives: CNG Smart Card

18

Mechanism

Financing 100% of cost of conversion throughcommercial lending on a debit card to bepresented at fueling stations by convertedvehicles’ drivers

Increase

No. of Vehicles Converted

19

Gas Sector Governance

• The new Gas Law, paves the way for a substantial reform of the gas sector.• The law mandates the creation of a new independent gas regulator.• Offering an opportunity to the private sector to enter and compete in wholesale

downstream market segments, the existing shadow regulator finalized the gas transmission codes, gas transmission tariff, which will be published soon.

The Egyptian Government has approved a new Gas Law.

20

Lessons from Egypt - Making it work Supply and infrastructure

Role of private sector

Support from international institutions

Full involvement of investors & distribution companies Capital intensive industry Slow but steady returns Involvement in the whole supply chain Consumer education

Commitment from international institutions Financing collective infrastructures Support for micro-credits Exchange of good practices

Regulations developing adequate framework using experience from well established and

structured market opting for a cylinder deposit system banning cross-filling establishing a licensing system

21

Access for poorer classes and implication of taxes developing an efficient network financing solutions such as micro-credit eliminate taxation of LPG and cylinders (import duties and VAT) harmonizing the tax system (in case partial taxation is maintained)

Support from governments Stability of the political and legal systems Rules governing trade and investment Regulations concerning industry operating and safety standards Involvement in fair tax / duty treatment

Awareness & Consumer’s Adherence Openness to change

education campaigns(schools, associations, role of village heads)- safety- applications

advertising campaigns by marketers

Lessons from Egypt - Making it work

22

Enablers•Strong multilateral support, FDI•Subsidy regime (initially)•Clear cost recovery model for LDCs•Free trade zones

Blockers•Cost recovery mechanism for upstream, power sector•Subsidy regime (later)•Regulatory environment•Customer payback•Security of supply for large industry•Connection fees•Monopsony buyer

Opportunities•Regional gas hub•Modernisation programme (subsidy phase out)•Regulatory reforms and capacity building (direct sales)•Efficiency opportunities

Policy enablers, blockers and opportunities

23

THANK YOU

2 Simon Bolivar Sq, Garden City , 8th floor

Tel: (202) 2796 1494 Fax: (202) 27962821www.taqa.com.eg