dr. singh cbn msmedf presentation

TRANSCRIPT

MSME Financing in India

MSME Development Fund workshop -

Organized by Central Bank of Nigeria/ Bankers Committee

March 18-20, 2015

Dr. Kamakhya Nr. Singh

+234 (0)706 636 8219

Outline of the Presentation• State of the Indian Economy

• Definition of MSMEs in India

• Role of MSMEs

• Challenges Faced by MSMEs

• Financing needs of MSMEs – Demand and Supply

• What has been done?

– Making the environment for MSMEs more enabling through improving

• Legal and Regulatory Framework

• Government Support

• Financial Infrastructure Support

– Schemes of financing MSMEs by Government of India

• What more can be done?

– Make the environment in which MSMEs operate more support-worthy through• enabling infrastructure

• liquidity management

• and risk management

2

State of the Indian Economy

• Comparison of economic performance across different countries for the

year 2014-15, shows the emergence of India among the few large

economies with propitious economic outlook, amidst the mood of

pessimism and uncertainties that engulf a number of advanced and

emerging economies.

• Brighter prospects in India owe mainly to the fact that the economy stands

largely relieved of the vulnerabilities associated with an economic

slowdown, persistent inflation, elevated fiscal deficit, slackening domestic

demand, external account imbalances, and oscillating value of its currency.

(Source: The Economic Survey, 2014-15, Ministry of Finance, Government of India)

2

MSMEs – driver of growth

SMEs play a vital role for the growth of Indian

economy by contributing:

• 45% of the industrial output,

• 40% of exports,

• 42 million in employment,

• creating one million jobs every year and

• producing more than 8000 quality products for the

Indian and international markets(http://www.smechamberofindia.com/rol_of_sme_sector.aspx)

2

MSMEs – driver of growth, contd..

The picture becomes more holistic with the

inclusion of microenterprises.• There are 36.1 million (MSMEs) which contribute 37.5 per

cent of the country’s GDP playing a critical role in boosting

industrial growth and economic development (Economic

Survey, 2014-15)

• Although 94 percent of MSMEs are unregistered1*, the

contribution of the sector to India’s GDP has been growing

consistently at 11.5 percent a year, which is higher than the

overall GDP growth rate of India (IFC report, 2013)(1*) Unregistered Enterprises: MSMEs that do not file business information with District Industry Centers (DICs) of the State/

Union Territory; The data on enterprise output performance is not adequately tracked by the government agencies

2

Definitions of Micro, Small &

Medium Enterprises

In accordance with the provision of Micro, Small

& Medium Enterprises Development (MSMED)

Act, 2006 the Micro, Small and Medium

Enterprises (MSME) are classified in two Classes:

(a) Manufacturing Enterprises

(b) Service Enterprises

2

Manufacturing and Service

Enterprises• Manufacturing Enterprises are those enterprises which are

engaged in the manufacture or production of goods pertaining to any

industry specified in the first schedule to the industries (Development and

regulation) Act, 1951) or employing plant and machinery in the process of

value addition to the final product having a distinct name or character or

use. The Manufacturing Enterprises are defined in terms of investment in

Plant & Machinery.

• Service Enterprises are those enterprises that are engaged in

providing or rendering of services and are defined in terms of investment

in equipment.

2

Investment Limit for MSMEs

The limit for investment in plant and machinery / equipment for manufacturing /

service enterprises, as notified, vide S.O. 1642(E) dtd.29-09-2006 are as under:

2

Manufacturing Sector

Enterprises Investment in plant & machinery ‘@ 1 USD = 60 Rupees

Micro Enterprises Does not exceed twenty five lakh rupees < 41667

Small Enterprises More than twenty five lakh rupees but does

not exceed five crore rupees

41667-833333

Medium Enterprises More than five crore rupees but does not

exceed ten crore rupees

833333-1666667

Service Sector

Enterprises Investment in equipments

Micro Enterprises Does not exceed ten lakh rupees: < 16667

Small Enterprises More than ten lakh rupees but does not

exceed two crore rupees

16667-333333

Medium Enterprises More than two crore rupees but does not

exceed five core rupees

333333-833333

Sub-segments of the Manufacturing and

Services Sectors

Source: MSME Census

2

Stakeholders

2

Stake in the

Development of

MSMEs

Regulators/

Government Social Groups/

Environmental

Groups and

Public in general

Communities,

where MSME

operates

Business Partners,

suppliers, vendors

Employees

and

Promoters

Lenders and

Investors

Clients/

Customers

Industry

peers

Given the significant role played by MSMEs in economy and society, it’s important for all the

stakeholders of MSME development to help the MSMEs meet the challenges faced by them.

Distribution of Enterprises in the MSME Sector

and Prevalent Ownership Structures

2

Percentage (%) represent the distribution of MSMEs on the bases of ownership structure

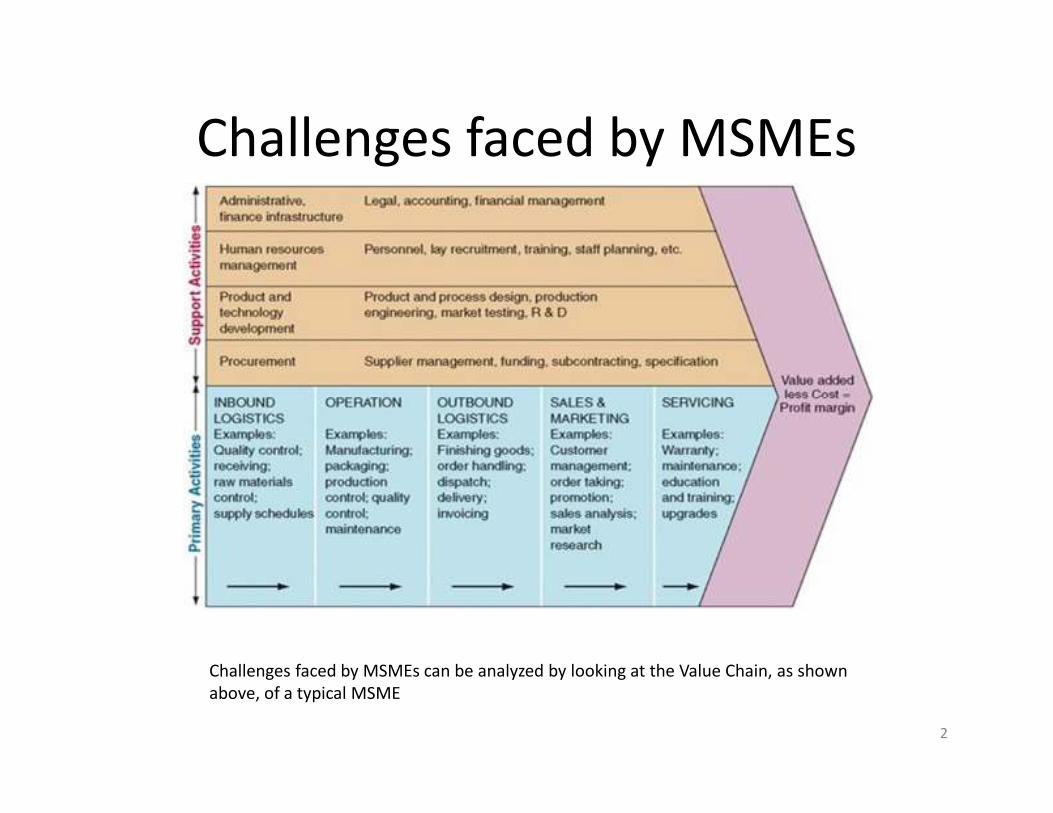

Challenges faced by MSMEs

2

Challenges faced by MSMEs can be analyzed by looking at the Value Chain, as shown

above, of a typical MSME

Challenges faced by MSMEs

Value Chain analysis on the previous slide shows the major

challenges faced by MSMEs. These challenges are related with:

Inputs:

• Raw material – quantity, quality, price

• Technology

• Management skills

• Human Resources

• Finance

Output:

• Quality of product

• Marketing of finished product – market linkages

2

Challenges faced by MSMEs

While poor infrastructure, lack of other inputs and inadequate

market linkages are key factors that have constrained growth of

the sector, it is the lack of adequate and timely access to finance

that has been the one of the biggest challenges.

The financing needs of the sector depend on the size of

operation, industry, customer segment, and stage of

development.

Financial institutions have limited their exposure to the sector

due to a higher risk perception and limited access of MSMEs to

immovable collateral.2

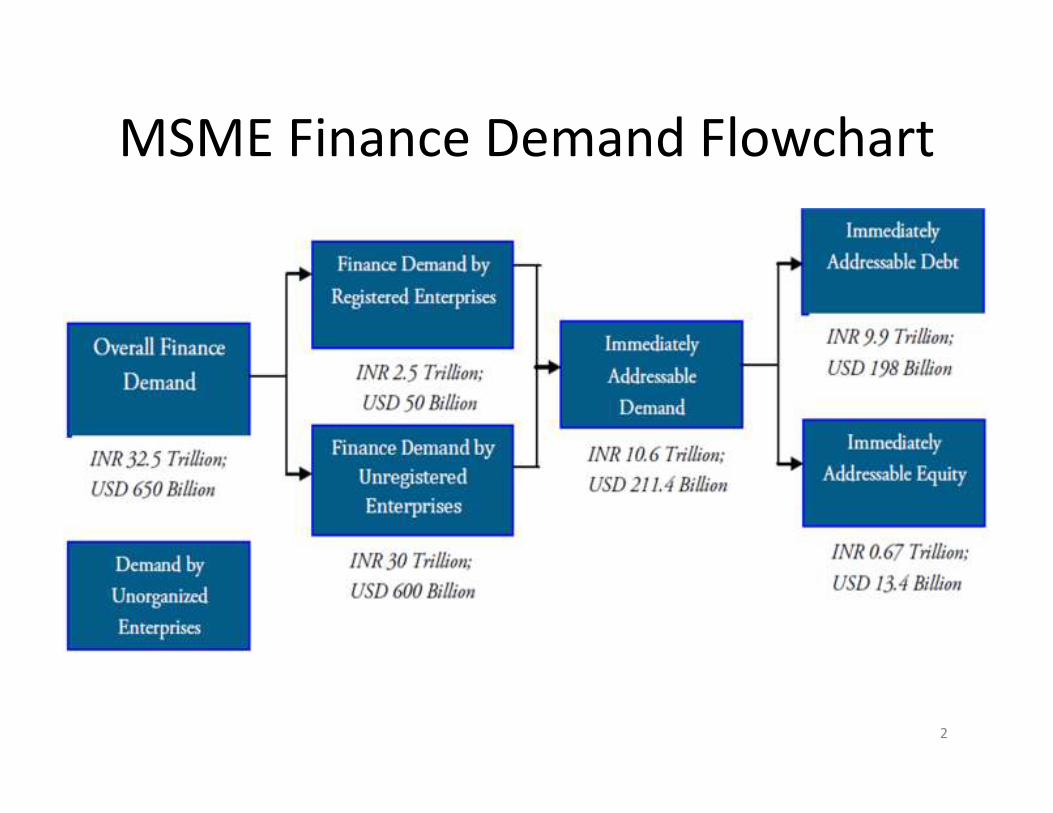

Sources of finance

Broadly, of the overall finance demand of INR

32.5 trillion($650 billion) (as estimated by IFC report, 2013)

- 78 percent, or INR 25.5 trillion ($510 billion) is either

self-financed or from informal sources

- 22 percent or INR 7 trillion ($140 billion) of the total

MSME financing is from formal sources

2

Sources of finance, contd…

Within the formal financial sector

- Banks account for nearly 85 percent of debt supply to the

MSME sector, with Scheduled Commercial Banks comprising

INR 5.9 Trillion (USD 118 Billion).

- Non-Banking Finance Companies and smaller banks such as

Regional Rural Banks (RRBs), Urban Cooperative Banks (UCBs)

and government financial institutions (including State

Financial Corporation and State Industrial Development

Corporations) constitute the rest of the formal MSME debt

flow.

2

MSME Finance Demand Flowchart

2

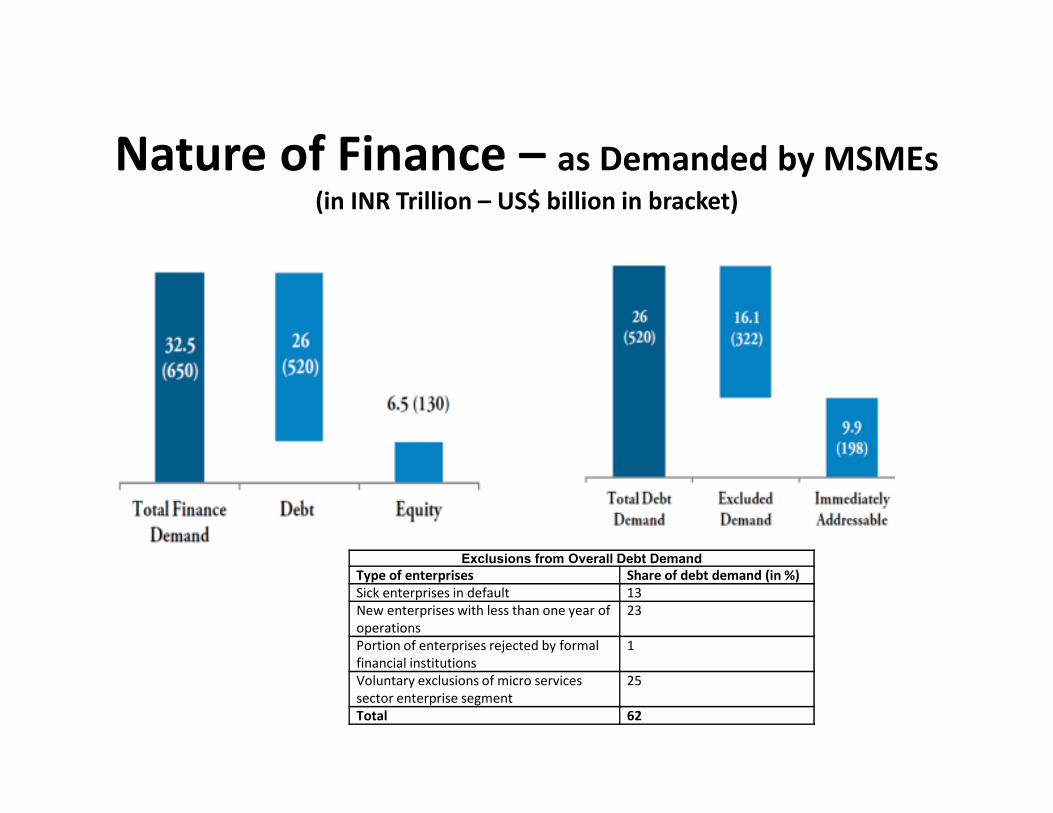

Nature of Finance – as Demanded by MSMEs(in INR Trillion – US$ billion in bracket)

Exclusions from Overall Debt Demand

Type of enterprises Share of debt demand (in %)

Sick enterprises in default 13

New enterprises with less than one year of

operations

23

Portion of enterprises rejected by formal

financial institutions

1

Voluntary exclusions of micro services

sector enterprise segment

25

Total 62

Overall Finance Gap in MSME Sector(In INR trillion* – figure in brackets is in US$ billion)

2

What has the Government done ?

Enabling Environment for Growth of Finance

in the MSME Sector

• MSMEs function in a highly competitive environment and

require an enabling environment to sustain growth.

• Well - rounded fiscal support, a strong policy framework, and

incentives promoting innovation by financial institutions can

significantly increase the penetration of formal financial

services to the MSME sector.

• The three main pillars around which the government has

worked for creating enabling environment for MSMEs are:

(a) legal and regulatory framework

(b) government support

(c) financial infrastructure support.

2

Pillars of the enabling environment(Schematic diagram of Key Elements of the Enabling Environment)

Source: IFC-Intellecap Analysis

2

MSME Schemes (Government of India, 2015)

Various Ministries of Government of India have a

number of schemes for the development, promotion

and finance of MSMEs.

Providing financial infrastructure support to MSMEs is

one of the most important means of development and

growth of those MSMEs.

Details of the schemes (exisiting in the first quarter of

2015) for promoting the development and growth of

MSMEs can be found at –

http://msme.gov.in/web/portal/Scheme-Msme.aspx

2

MSME Schemes (Government of India, 2015)

A few of the schemes promoted by Ministry Of MSMEs are as under:• Development Commissioner (DC-MSME) Schemes

1. Credit Guarantee 2. Credit Linked Capital Subsidy for Technologny Upgradation

3. ISO 9000/ISO 14001 Certification Reimbursement 4. Micro & Small Enterprises Cluster Development

Programme

5. Micro Finance Programme 6. MSME Market Development Assistance (MDA)

• NSIC Schemes

1. Performance and Credit Rating 2. Bank Credit Facilitation

3. Raw Material Assistance 4. Single Point Registration

5. Infomediary Services 6. Marketing Intelligence Services Lease

7. Bill Discounting

• ARI Division Scheme

1. Prime Minister Employment Generation Programme (PMEGP)

2. Janshree Bima Yojana for Khadi Artisans 3. Market Development Assistance (MDA)

4. R&D Activities of Coir Board Under Central Sector Plan of Science & Technology (S&T)

5. Rejuvenation, Modernisation and Technology Upgradation of Coir Industry (REMOT)

6. CSS of Export Market Promotion

2

MSME Schemes (Government of India, 2015)

A few of the schemes promoted by Ministry Of Finance are as under:

• SIDBI Schemes

1. Growth Capital and Equity Assistance 2. Refinance for Small Road Transport Operators

3. General Refinance (GR) 4. Refinance for Textile Industry under Technology Upgradation Fund

5. Acquisition of ISO Series Certification by MSE Units 6. Composite Loan

7. Single Window (SW) 8. Rehabilitation of Sick Industrial Units 9. Development of Industrial Infrastructure for

MSME Sector 10. Integrated Infrastructural Development (IID) 11. Bills Re-Discounting Equipment

12. Bills Re-Discounting-Equipment(Inland Supply Bills) 13. Direct Finance (Project Finance, Equipment Finance,

etc.)

• NABARD Schemes

1. Producers Organisations Development Fund 2. Dairy Venture Capital Fund

3. Establishing “Poultry Estates” and Mother Units for Rural Backyard Poultry

4. Establishment/Modernisation of Rural Slaughter Houses

5. Commercial Production Units of Organic Inputs 6. Poultry Venture Capital Fund

2

Way Forward…

• It’s not only the Ministry of MSME and Ministry of Finance

that have the schemes for the development, promotion and

finance of MSMEs

• Others such as Ministry of Agriculture, Ministry of Commerce

and Industry, Ministry of Communication and IT, Ministry of

Food Processing Industries, Ministry of Rural Development,

Ministry of Science and Technology, Ministry of Textile, etc.

also have targeted schemes for MSMEs.

• Stakeholders need to be doing more so that the financial

access for MSMEs becomes better, more efficient and less

costly,

2

Potential interventions to increase

access to Finance for the MSMEs

Given the significance of MSME sector, there is still requirement

for additional intervention to be made and action to be taken for

unleashing the full potential of the MSME sector.

Potential interventions that can be undertaken to expand the

access to MSME finance in India are:

• enabling infrastructure

• liquidity management

• and risk management

2

Potential interventions contd..-

Enabling infrastructure

• Encourage securitization of trade-receivables in the sector

through conducive legal infrastructure.

• Promote institutions to syndicate finance and provide advisory

support to MSMEs in rural and semi-urban areas.

• Incentivize formation of new MSME-specific venture funds by

allowing existing government equity funds to make anchor

investment in venture funds.

2

Potential interventions contd..-

Liquidity management

• Improve debt access to non-banking finance companies

focused on these enterprises and provide regulatory incentives

for participation in the sector.

• Develop an IT-enabled platform to track MSME receivables to

facilitate securitization of these trade receivables, or

alternatively expand the scope of SIDBI and NSE’s IT-platform

NTREES to facilitate securitization.

• Provide credit guarantee support for MSME finance to non-

banking finance companies.

2

Potential interventions contd..-

Risk management

• Develop a better understanding of financing patterns of service

enterprises in the sector.

• Expand the scope of the sector’s credit information bureau to

collate and process important transaction data, including utility

bill payment.

• Strengthen the recently established collateral registry and

create stronger linkages with other financial infrastructure.

• Facilitate greater debt access to non-banking finance

companies.

2

30

Thank you!Dr. Kamakhya Nr. Singh

CFO, LAPO MF Bank

Project Manager, UNDP (AMSCO)

http://ng.linkedin.com/in/kamakhyasingh/

This presentation has, apart from using various secondary sources, also used the paper “Micro, Small and

Medium Enterprise Finance in India: prepared by IFC in association with the Government of Japan in 2012.