dr. edward altman nyu stern school of business defaulted bond & bank loan markets and outlook...

TRANSCRIPT

Dr. Edward AltmanNYU Stern School of Business

Defaulted Bond & Bank Loan Markets and Outlook

Investing in Distressed CompaniesGFA SeminarNYU Stern School of BusinessMarch 29, 2004

2004YTD $856,000 $3,540 0.4142003 $825,000 $38,451 4.661

Par Value Par Value DefaultYear Outstandinga Defaults Rates (%)

2002 $757,000 $96,855 12.7952001 $649,000 $63,609 9.8012000 $597,200 $30,295 5.0731999 $567,400 $23,532 4.1471998 $465,500 $7,464 1.6031997 $335,400 $4,200 1.2521996 $271,000 $3,336 1.2311995 $240,000 $4,551 1.8961994 $235,000 $3,418 1.4541993 $206,907 $2,287 1.1051992 $163,000 $5,545 3.4021991 $183,600 $18,862 10.2731990 $181,000 $18,354 10.1401989 $189,258 $8,110 4.2851988 $148,187 $3,944 2.6621987 $129,557 $7,486 5.7781986 $90,243 $3,156 3.4971985 $58,088 $992 1.7081984 $40,939 $344 0.8401983 $27,492 $301 1.0951982 $18,109 $577 3.1861981 $17,115 $27 0.158

a As of mid-yearb Weighted by par value of amount outstanding for each year.

Source: Author’s compilation and Salomon Smith Barney

Straight Bonds Only Excluding Defaulted Issues From Par Value Outstanding, 1971 – 2004YTD (US$ millions)

Historical Default Rates

Par Value Par Value DefaultYear Outstandinga Defaults Rates (%)

1980 $14,935 $224 1.5001979 $10,356 $20 0.1931978 $8,946 $119 1.3301977 $8,157 $381 4.6711976 $7,735 $30 0.3881975 $7,471 $204 2.7311974 $10,894 $123 1.1291973 $7,824 $49 0.6261972 $6,928 $193 2.7861971 $6,602 $82 1.242

Standard Deviation (%)

Arithmetic Average Default Rate1971 to 2003 3.292% 3.161%1978 to 2003 3.656% 3.394%1985 to 2003 4.567% 3.515%Weighted Average Default Rateb

1971 to 2003 5.352%1978 to 2003 5.382%1985 to 2003 5.474%Median Annual Default Rate1971 to 2003 1.896%

QUARTERLY DEFAULT RATE AND FOUR QUARTER MOVING AVERAGE

1992 –2003

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Qua

rter

ly D

efau

lt R

ate

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

4-Q

uart

er M

ovin

g A

vera

ge

Quarterly

Moving

Historical Default Rates

Number of Filings and Pre-petition Liabilities of Public Companies

1989- 2004 YTD

200395 filings and pre-petition liabilities of

$110.4 billion

Note: Minimum $100 million in liabilitiesSource: NYU Salomon Center Bankruptcy Filings Database

Filings for Chapter 11

$0

$50

$100

$150

$200

$250

$300

$350

$400

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

$ B

illio

n

0

40

80

120

160

200

Pre- Petition Liabilities, in $ billions (left axis)

Number of Filings (right axis)

March 200415 filings and pre-petition liabilities of

$9.1 billion

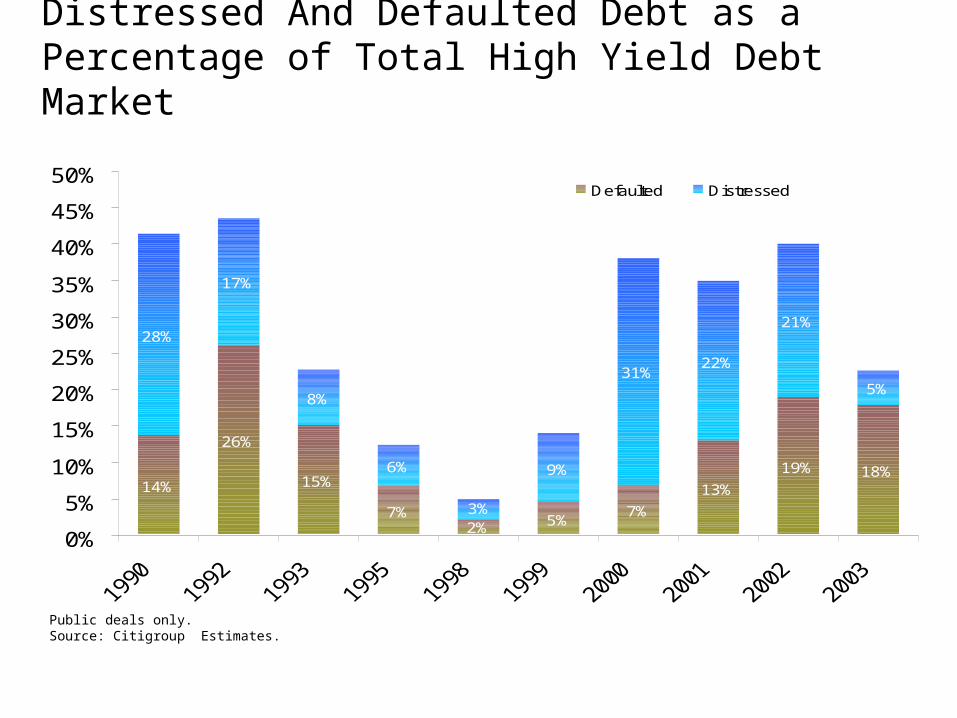

Public deals only. Source: Citigroup Estimates.

14%

26%

15%

7%5%

7%

13%

19% 18%

28%

17%

8%

6% 9%

31%22%

21%

5%

2%3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%Defaulted Distressed

Distressed And Defaulted Debt as a Percentage of Total High Yield Debt Market

(1) Calculated using: (2002 defaulted population) + (2003 defaults) - (2003 Emergences)

(2) For 12/31/02 and 12/31/03, we use a private/public ratio of 1.40.

Source: Edward Altman, NYU Salomon Center, Stern School of Business

Face Value Market Value12/31/02 12/31/03 12/31/02 xFV 12/31/03 xFV

Public DebtDefaulted 187.7$ 193.6$ (1) 37.5$ 0.20 87.1$ 0.45

Distressed 204.7$ 50.5$ (2) 102.4$ 0.50 32.8$ 0.65

Total Public 392.5$ 244.1$ 139.9$ 119.9$

Private DebtDefaulted 262.8$ 271.0$ (3) 157.7$ 0.60 189.7$ (2) 0.70

Distressed 286.6$ 70.7$ (3) 215.0$ 0.75 60.1$ (2) 0.85

Total Private 549.5$ 341.7$ 372.7$ 249.8$

Total Public and Private 941.9$ 585.8$ 512.6$ 369.8$

Estimated Face And Market ValuesOf Defaulted And Distressed Debt

Source: E. Altman, NYU Salomon Center .

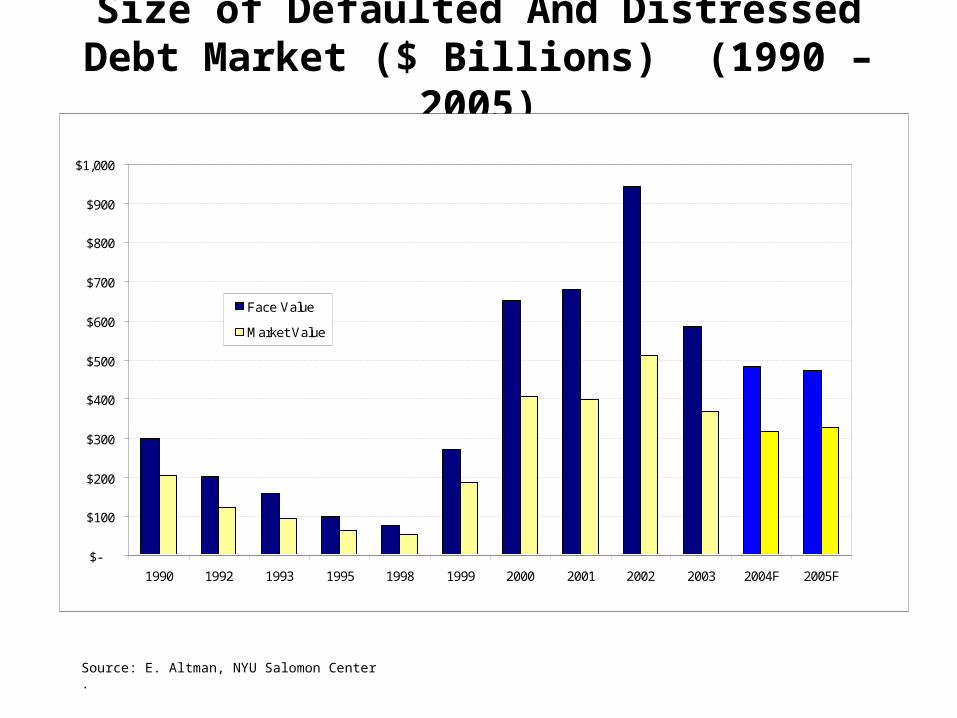

9/15/2002

$-

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1990 1992 1993 1995 1998 1999 2000 2001 2002 2003

Face Value

Market Value

Size of Defaulted And Distressed Debt Market ($ Billions) (1990 – 2003)

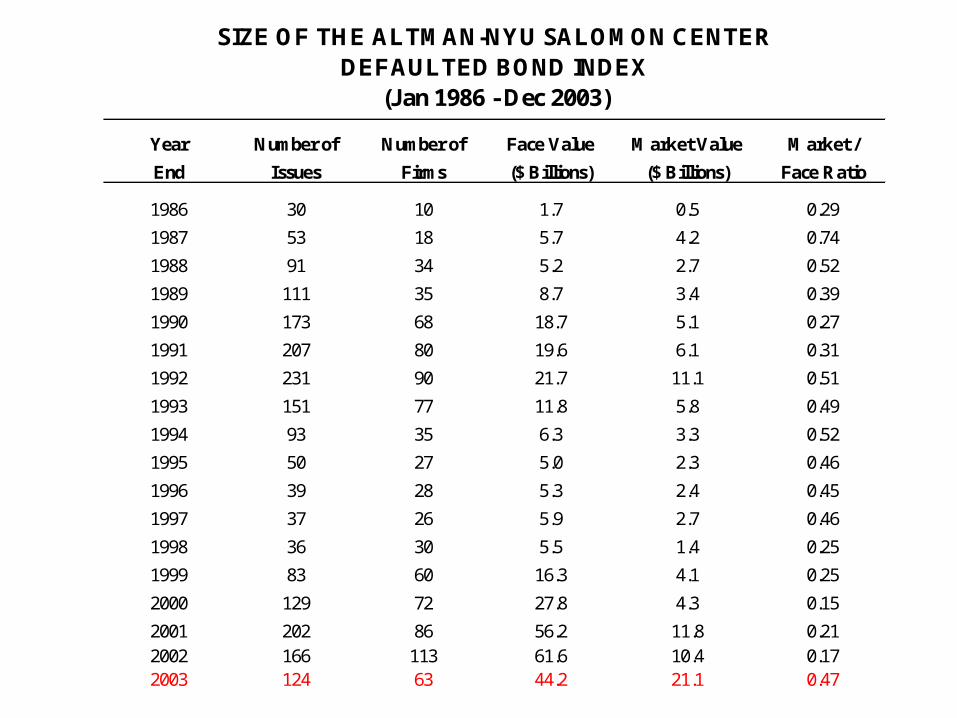

SIZE OF THE ALTMAN-NYU SALOMON CENTERDEFAULTED BOND INDEX

(Jan 1986 - Dec 2003)

Year Number of Number of Face Value Market Value Market /

End Issues Firms ($ Billions) ($ Billions) Face Ratio

1986 30 10 1.7 0.5 0.29

1987 53 18 5.7 4.2 0.74

1988 91 34 5.2 2.7 0.52

1989 111 35 8.7 3.4 0.39

1990 173 68 18.7 5.1 0.27

1991 207 80 19.6 6.1 0.31

1992 231 90 21.7 11.1 0.51

1993 151 77 11.8 5.8 0.49

1994 93 35 6.3 3.3 0.52

1995 50 27 5.0 2.3 0.46

1996 39 28 5.3 2.4 0.45

1997 37 26 5.9 2.7 0.46

1998 36 30 5.5 1.4 0.25

1999 83 60 16.3 4.1 0.25

2000 129 72 27.8 4.3 0.15

2001 202 86 56.2 11.8 0.212002 166 113 61.6 10.4 0.172003 124 63 44.2 21.1 0.47

Defaulted Debt Indexes:Market-to-Face Value Ratio

(Annual 1986 –2003)

Source: Altman-NYU Salomon Center Defaulted Debt Indexes

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Loans

Bonds

YearAltman-NYU Salomon Center

Defaulted Bond Index S&P 500 Stock IndexCitigroup High Yield Loan

Index

1987 37.85% 5.26% 4.67%1988 26.49% 16.61% 13.47%1989 -22.78% 31.68% 2.75%1990 -17.08% -3.12% -7.04%1991 43.11% 30.48% 39.93%1992 15.39% 7.62% 17.86%1993 27.91% 10.08% 17.36%1994 6.66% 1.32% -1.25%1995 11.26% 37.56% 19.71%1996 10.21% 22.96% 11.29%1997 -1.58% 34.36% 13.18%1998 -26.91% 28.58% 3.60%1999 11.34% 20.98% 1.74%2000 -33.09% -9.11% -5.68%2001 17.47% -11.87% 5.44%2002 -5.98% -22.08% -1.53%2003 84.87% 28.70% 30.62%

1987 - 2003 ArithmeticAverage (Annual) Rate 10.89% 13.53% 9.77%

Standard Deviation 29.13% 18.04% 12.65%

1987 - 2003 Compounded 7.42% 12.09% 9.12%Average (Annual) Rate

1987 - 2003 ArithmeticAverage (Monthly) Rate 0.70% 1.06% 0.75%

Standard Deviation 4.41% 4.59% 2.16%

1987 - 2003 Compounded 0.64% 1.02% 0.78%Average (Monthly) Rate

(1987 -2003)

ALTMAN-NYU SALOMON CENTERDEFAULTED BOND INDEX

COMPARISON OF RETURNS

Distressed Debt Managers 2003Ares Corporate Opportunities Fund HBV/Mellon PPM America

Ashmore Asian Recovery Highland Capital Quadrangle Group LLC

Avenue Capital Partners JLL Partners Questor ManagementBay Harbour Advisors KD Distressed Capital Resolution Partners

Bennett Management Company King Street Advisors Restoration Capital Management

Black Diamond KPS Special Stuations Fund Satellite

Blackstone Alternative Asset Mgmt. KS Distressed Debt Schultze Asset Management

Canyon Capital Litespeed Partners Scott 's Cove Capital

Cardinal Capital Lampe Conway Silverpoint CapitalCargill Leucadia National Corporations Stanfield Capital ManagementCarl Marks LongAcre Capital Partners Stark Investments

Carlyle Strategic Partners Longroad Asset Management Strategic Value Partners

Cerebrus Partners Levco Debt Opportunities Sunrise Capital Partners

Citadel Investments Marathon Capital LLC TA Mckay & Co.

Concordia Advisors MatlinPatterson Global Advisors Third Avenue Value Fund

Contrarian Capital MD Sass Corporate Resurgence Triage Capital

Cypress Management MHR Trilogy Capital

Davidson Kempner MJ Whitman Mgmt Co. Trust Company of the West

DDJ Capital Management Moore Asian Recovery Fund Turnberry Capital

Durham (Delaware Bay) Murray Capital Varde Partners, Inc.

Epic Asset Management MW Post Wellspring Capital Partners

Farallon Partners New Generation Advisers Wexford Capital

Franklin Mutual Recovery Oakhill Wayland Fund

Golden Tree LLC Oaktree Capital Whippoorwill Associates, Inc.

Gramercy Capital Och Ziff Friedheim William E. Simon & Sons

Greenwich Street Capital Owl Creek Capital W.R. Ross & Co.

Pequot Capital York Capital

Investment Styles in Distressed Debt Investing

Forecasting Defaults and the Default Rate

Forecasting Defaults and the Default Rate

MODEL DRIVERS

• Mortality Rate Estimates: 1971 - 2003= f {bond rating, age, redemptions, defaults}

• Historical New Issuance over last 10 years by credit quality• Bond-ratings • Z-score Bond-equivalent ratings

New Defaults and Default Rate in 2004

• Estimate high yield market growth in 2004

New Defaults and Default Rate in 2005

Z’’ Score Model for Manufacturers, Non-Manufacturer Industrials, & Emerging

Market CreditsZ’’ = 3.25 + 6.56X1 + 3.26X2 + 6.72X3 + 1.05X4

X1 = Current Assets - Current Liabilities

Total Assets

X2 = Retained Earnings

Total Assets

X3 = Earnings Before Interest and Taxes

Total Assets

X4 = Book Value of Equity Z’’ > 2.60 - “Safe” Zone

Total Liabilities 1.1 < Z’’ < 2.60 - “Grey” Zone

Z ” < 1.1 - “Distress” Zone

US Bond Rating Equivalent Based on Adjusted Z” Score Model

US Equivalent Rating Average Z” Score Sample Size

AAA 8.15 8AA+ 7.6 -AA 7.3 18AA- 7 15A+ 6.85 24A 6.65 42A- 6.4 38

BBB+ 6.25 38BBB 5.85 59BBB- 5.65 52BB+ 5.25 34BB 4.95 25BB- 4.75 65B+ 4.5 78B 4.15 115B- 3.75 95

CCC+ 3.2 23CCC 2.5 10CCC- 1.75 6

D 0 14

Z’’ = 3.25 + 6.56X1 + 3.26X2 + 6.72X3 + 1.05X4

Forecasted High Yield Market Size, Defaults and Default Rates for 2004

and 2005

High Default DefaultYield Market Rate Amount

($ Billion) (%) ($ Billions)

2004 $946.5 3.50% $33.10

2005 $1,041.0 4.10% $42.70

Face Value Market Value

12/31/04 12/31/05 12/31/04 xFV 12/31/05 xFVPublic Debt

Defaulted 151.3$ 119.0$ (1) 72.6$ 0.48 59.5$ 0.50

Distressed 49.7$ 78.0$ (2) 32.3$ 0.65 50.7$ 0.65

Total Public 201.0$ 197.0$ 104.9$ 110.2$

Private Debt

Defaulted 211.8$ 166.6$ (3) 154.6$ 0.73 125.0$ 0.75

Distressed 69.6$ 109.2$ (3) 59.1$ 0.85 92.8$ 0.85

Total Private 281.4$ 275.9$ 213.8$ 217.8$

Total Public and Private 482.4$ 472.9$ 318.7$ 328.0$

Forecasted Face and Market Values of Defaulted and Distressed Debt 2004 –

2005 (US$billions)

(1) Calculated using: (2003 defaulted population) + (2004 defaults) - (2005 Emergences), same for 2005

(2) Based on 5.0% of size of high yield market (in 2004, $994 billion); 7.5% of market in 2005 ($1,041 billion)

(3) For 12/31/04 and 12/31/05, we use a private/public ratio of 1.40.

Source: Edward Altman, NYU Salomon Center, Stern School of Business

Source: E. Altman, NYU Salomon Center .

Size of Defaulted And Distressed Debt Market ($ Billions) (1990 – 2005)

$-

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1990 1992 1993 1995 1998 1999 2000 2001 2002 2003 2004F 2005F

Face Value

Market Value