dr. abd elrahman elzahi saaid ali economist islamic research and training institute, a member of idb...

TRANSCRIPT

Global Experience for Sukuk Issuance

Dr. Abd elrahman Elzahi Saaid AliEconomist

Islamic Research and Training Institute, a Member of IDB Group

Since the end of the last century, Islamic finance has become a continuing growing industry.

The market consensus is that Islamic finance has a bright future, owing to:

Favorable demographics and Rising incomes in Muslim communities

Leading banks are buying sukuk and forming subsidiaries specifically to conduct Islamic finance

Laws have been enacted in non-Muslim financial centers

Introduction

Generally, Sukuk are asset-backed, stable income, tradable and Shari’ah compatible trust certificates.

The primary condition of issuance of Sukuk is the existence of assets on the balance sheet of the entity which wants to mobilize the financial resources.

The identification of suitable assets is the first step in the process of issuing Sukuk certificates.

Shari’ah considerations dictate that the pool of assets should not solely be comprised of debts

Sukuk

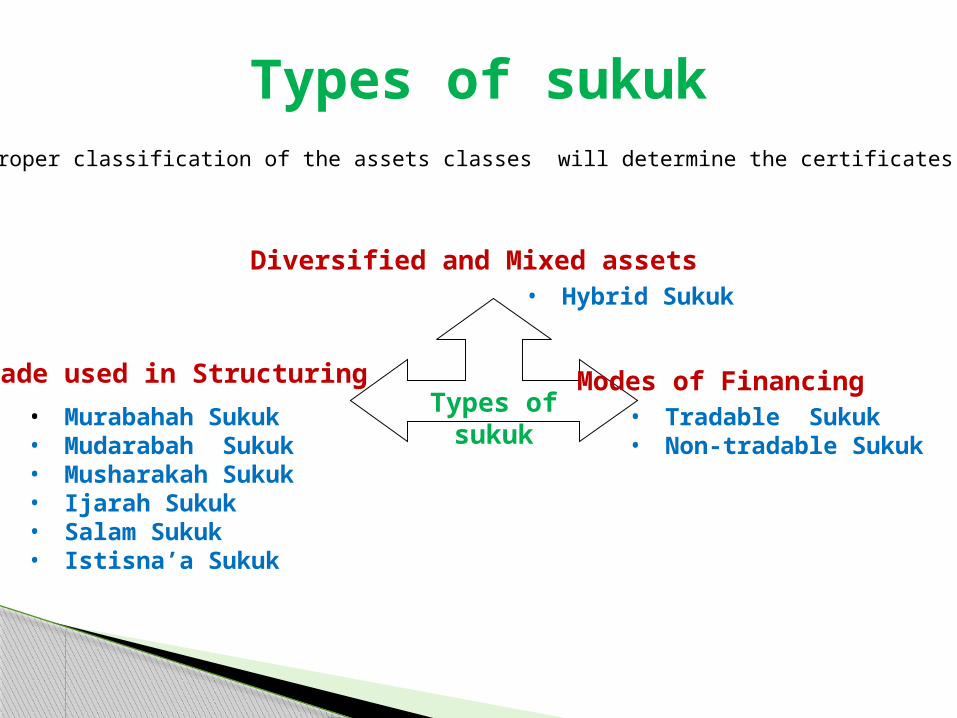

Types of sukuk

Types of sukuk

Modes of Financing Trade used in Structuring

• Tradable Sukuk• Non-tradable Sukuk

Diversified and Mixed assets• Hybrid Sukuk

• Murabahah Sukuk• Mudarabah Sukuk• Musharakah Sukuk• Ijarah Sukuk• Salam Sukuk• Istisna’a Sukuk

The proper classification of the assets classes will determine the certificates issued

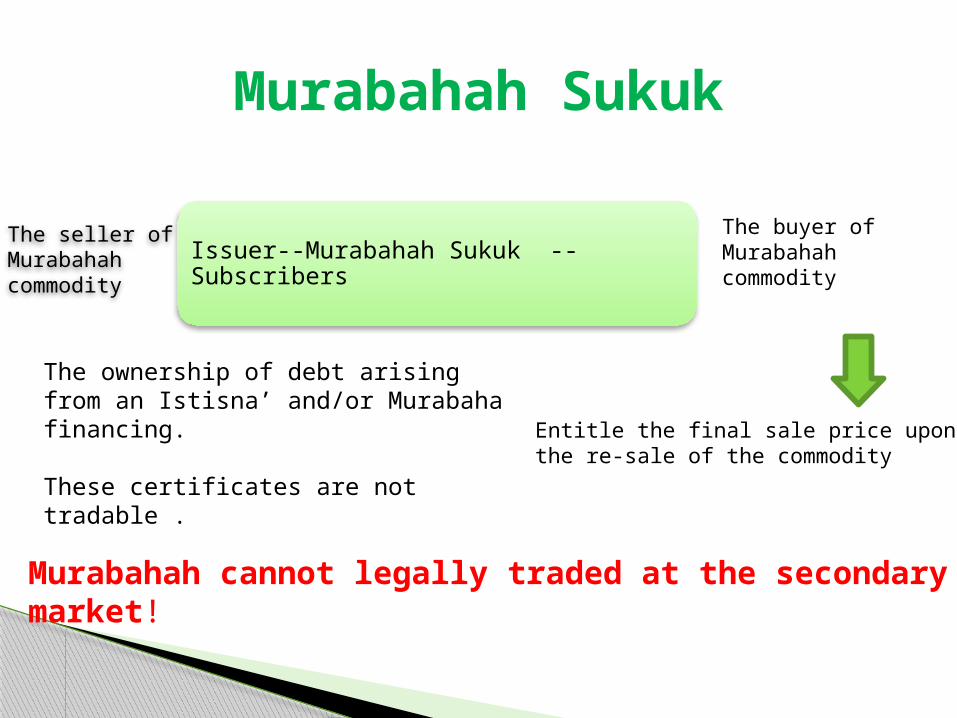

Murabahah Sukuk

Issuer--Murabahah Sukuk --SubscribersThe seller of Murabahahcommodity

The buyer of Murabahahcommodity

Entitle the final sale price upon the re-sale of the commodity

Murabahah cannot legally traded at the secondary market!

The ownership of debt arising from an Istisna’ and/or Murabaha financing.

These certificates are not tradable .

Mudarabah Sukuk

Issuer---Mudarabah Sukuk ---Holders

Rabb al-mal • Suppliers of

capital• Owns shares

in MD equity• transfer the

ownership

MudaribNo guarantee For the funds?capital or profit

Its an investment sukuk /common ownership

Certificates of permanent ownership in a company and businesses without control and management rights

Musharakah Sukuk

Issuer--- Musharakah Sukuk ---Holders

investment sukuk ownership of MSH. equity

holders of sukuk :• Committee• Shared investment

decisions

• Certificates of permanent ownership in a company and businesses with control and management rights

• SPV can purchased or construct Musharakah Assets or construct by the issuing entity

• MSH. Sukuk are negotiable instruments that can be bought and sold in the secondary MRTS.

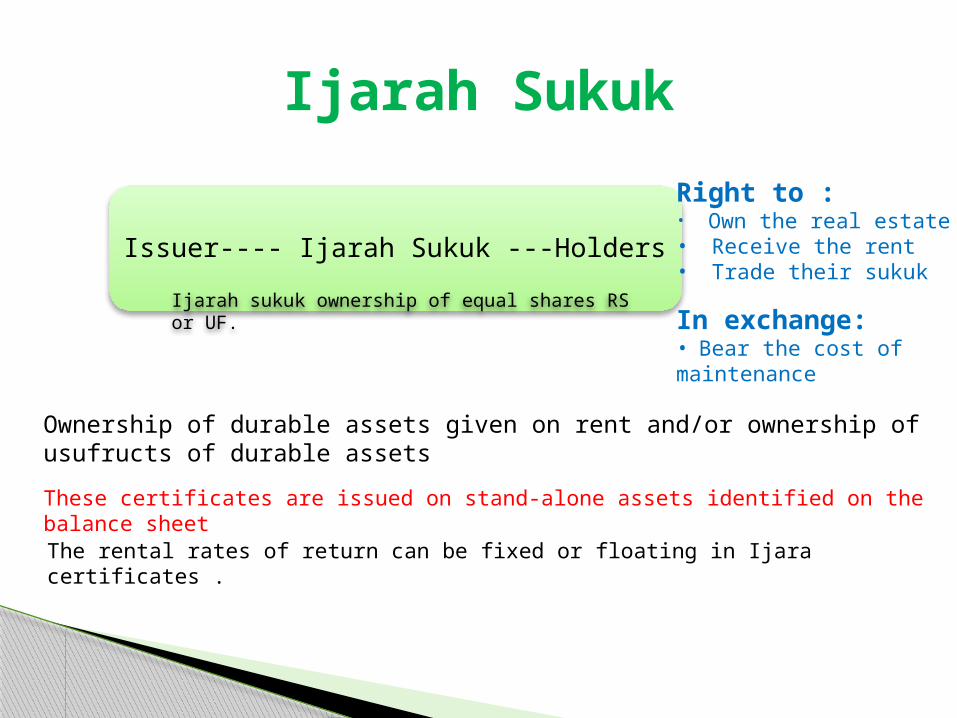

Ijarah Sukuk

Issuer---- Ijarah Sukuk ---Holders

Ijarah sukuk ownership of equal shares RS or UF.

Right to :• Own the real estate• Receive the rent• Trade their sukuk

In exchange:• Bear the cost of maintenance

The rental rates of return can be fixed or floating in Ijara certificates .

These certificates are issued on stand-alone assets identified on the balance sheet

Ownership of durable assets given on rent and/or ownership of usufructs of durable assets

Salam Sukuk

issuer---- Salam Sukuk ---holders

Sukuk of equal value for mobilizing S. Capital

The issuer is the seller of Salam goods

The holders are the buyer of the goods

They are entitle to:• Sale the price of the

certificates• Or sale price of the Salam

goods

• Investors pay in advance funds to the SPV in return for a promise to deliver a commodity in Future.

• In salam, funds are paid in advance and the commodity becomes debt. It can also be in the form of certificates representing the debt. These certificates are non-tradable.

Istisna’a Sukuk

Issuer---- Istisna’a ---Holders Certificates of equal value issued to mobilized

fund for production of goods products

Owned the productsThe issuers ManufacturersThe subscribers are the buyers Of the intended products

• The funds realized from the subscription are the cost of the product

• Shari'ah prohibit these sukuk certificates to be traded in the secondary markets

The ownership of debt arising from an Istisna’

The underlying pool of assets can comprise of Istisna’, Murabahah receivables as well as Ijarah

However, still at least 51 percent of the pool must comprise of Ijarah assets

having a portfolio of assets comprising of different classes allows for a greater mobilization of funds

Hybrid/Pooled Sukuk

The development Islamic financial Institutions

The need for capital market instruments The legitimization of the concepts of

sukuk in 1988 Why sukuk are important? Islamic Issuers and Investors and

conventional securities.

The global Market for Sukuk

The global Market for Sukuk

Pioneer Sukuk Issuers: Malaysian, Shell (1990), Sudan Government (2000)

Sukuk become global from 2001:

• USA issued Sukuk al Ijarah of US 100 Million (5 year tenor)

• Central Bank of Bahrain issued Sukuk Al Salam

• After that Sukuk issued in various jurisdictions:

• Malaysia, UAE, KSA, Indonesia, Qatar, Pakistan; bruin, Singapore, Kuwait.

Total Global Sukuk Issuance for the Period 1st Jan 2001 – 31st Dec

2010

November 2011 witnessed a record number of sukuk issues totaling USD 8.86 billion globally

a global level corporate level Major announcements of new sukuk

Global sukuk Development in 2011

2011 is the best year in terms of sukuk issuance, with USD 79.5 billion

The global sukuk market has reached a record level of USD 180 billion.

Market dominated by sovereign issuers and financial institutions

The sukuk industry benefited from the Eurozone debt crisis.

More conventional issuers will join the club of sukuk issuers.

Standardization of the rules governing the structures and the market.

The industry continues to suffer from the effects of double taxation

Many countries are opening up Islamic banking on their territories

Short-term sukuk issue is on the rise.

New structures, such as Wakala

Sukuk Trends in 2011onwards

Islamic Interbank Benchmark Rate

Islamic Benchmark for Pricing Credit Instruments

Regulatory Developments

Thanks