January 2013

The outlook for the oil storage industry

Introduction

Charles Smissaert

General Manager

Botlek Tank Terminal

Rotterdam

Contents:

The outlook for the oil storage industry

1. Introduction Botlek Tank Terminal

2. Trends in the Oil products Market

3. Tank storage market (ARA)

4. Conclusion and future trends

Introduction BTT

Previously named Maas Silo

Storage of grains & vegetable oils

Decrease of grain handling activities

Repositioning needed

Introduction BTT

Development of state-of-the-art tank terminal

Phase 1 – 200.000 cbm started-up in 2011

Phase 2 in development (start up from Q4 2014)

Key markets:

Gasoline and Gasoline components

Middle distillates and jetfuel

Bio Fuels

Edible Oils

Petrochemicals

December 2009

September 2010

August 2011

February 2012

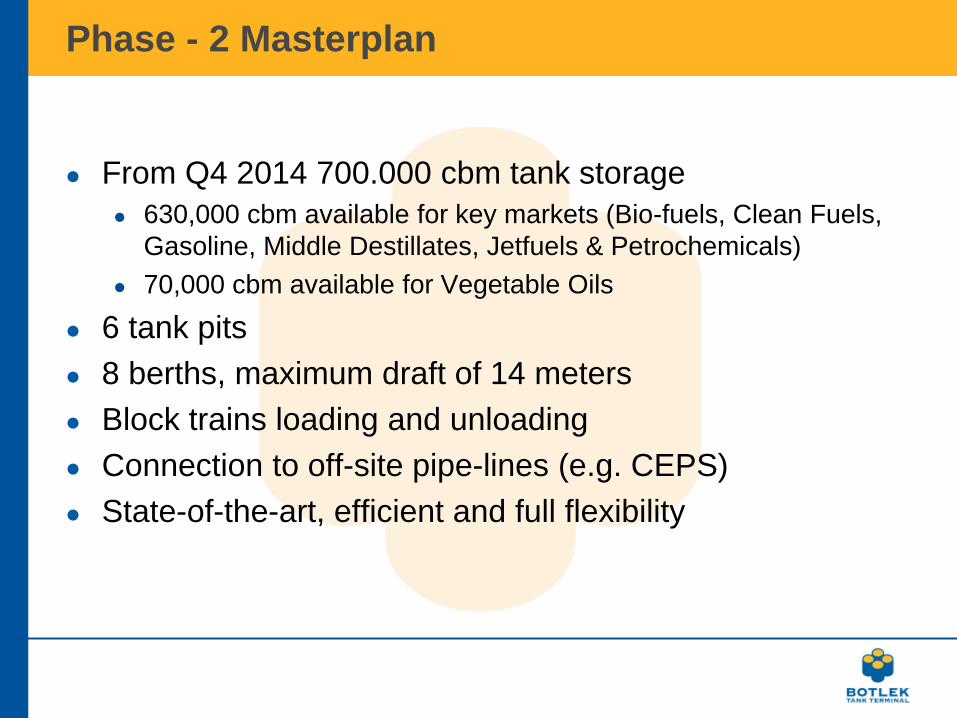

Phase - 2 Masterplan

From Q4 2014 700.000 cbm tank storage

630,000 cbm available for key markets (Bio-fuels, Clean Fuels,

Gasoline, Middle Destillates, Jetfuels & Petrochemicals)

70,000 cbm available for Vegetable Oils

6 tank pits

8 berths, maximum draft of 14 meters

Block trains loading and unloading

Connection to off-site pipe-lines (e.g. CEPS)

State-of-the-art, efficient and full flexibility

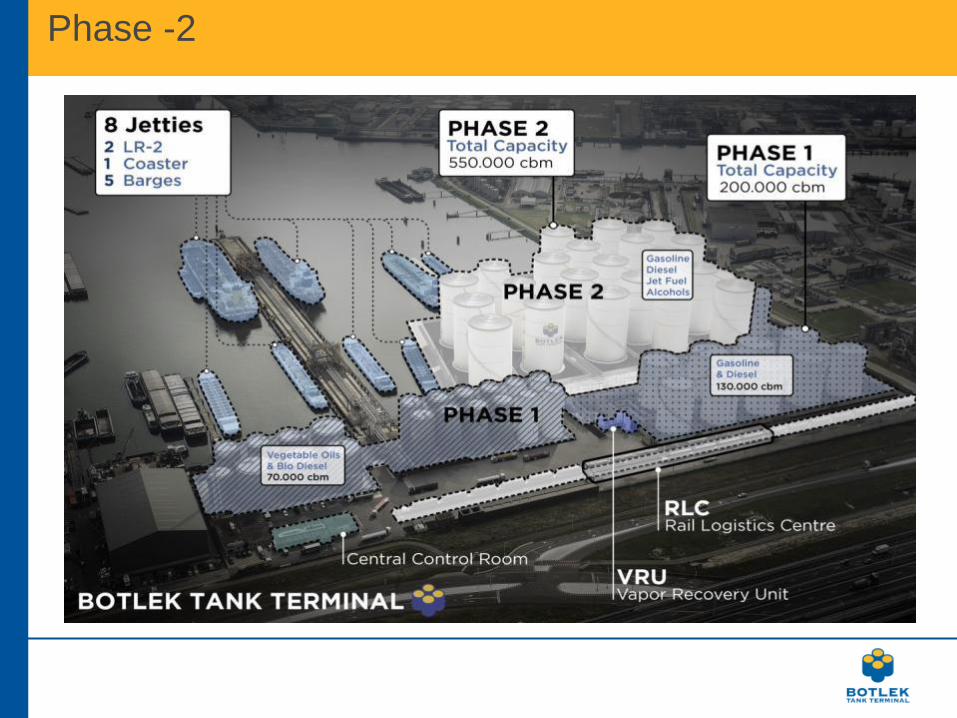

Phase -2

Phase -2

Contents:

The outlook for the oil storage industry

1. Introduction Botlek Tank Terminal

2. Trends in the Oil products Market

3. Tank storage market (ARA)

4. Conclusion and future trends

Worldwide trade flows - Exports

Globalization of fuels production:

strong growth in trade of oil products

Source: calculations EUR, based on Unctad, Worldbank and Eurostat.

Price corrections: oils by average crude, all products by EU inflation

0

50

100

150

200

250

300

350

400

Exports 1995-2011 (index, price corrected)

Nl all export

NL Oilproducts

WRLD all export

WRLD Crude

WRLD Oilproducts

Source: calculations EUR, based on Unctad, Worldbank and Eurostat.

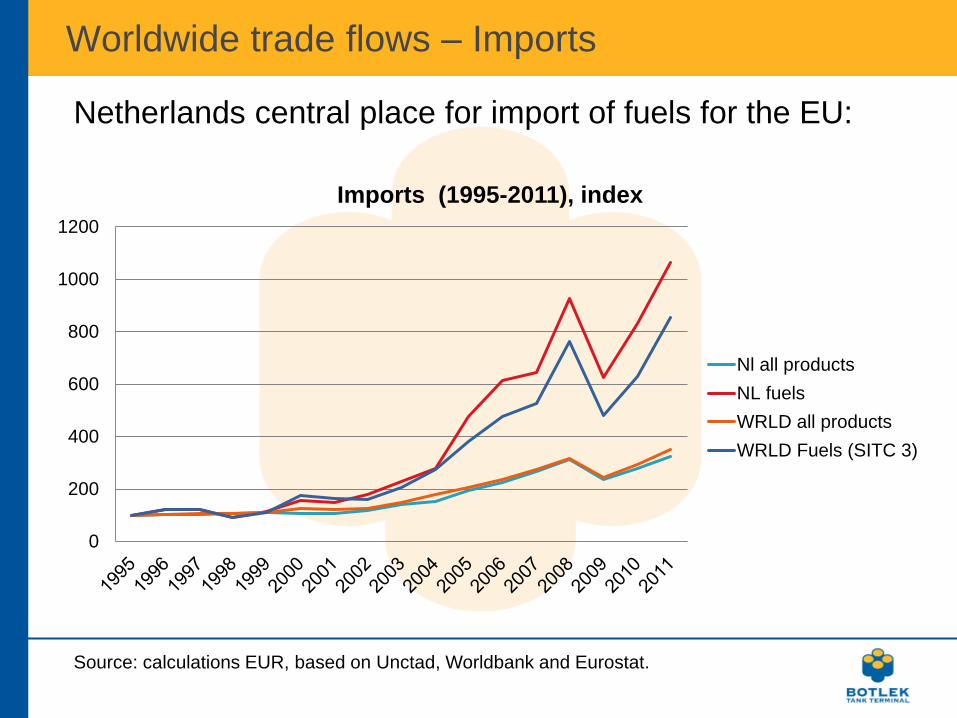

Worldwide trade flows – Imports

0

200

400

600

800

1000

1200

Imports (1995-2011), index

Nl all products

NL fuels

WRLD all products

WRLD Fuels (SITC 3)

Netherlands central place for import of fuels for the EU:

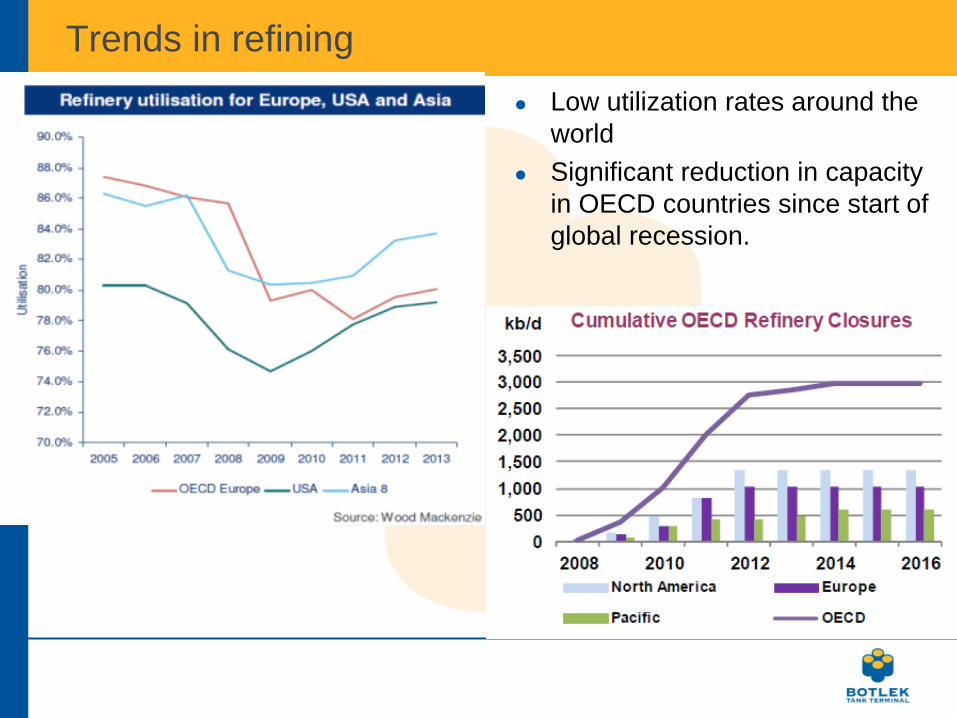

Trends in refining

Low utilization rates around the

world

Significant reduction in capacity

in OECD countries since start of

global recession.

Mid-term Trends in the EU Oil products Market

Gasoline Diesel/Jet

EU-position LONG SHORT

Refinery closures in EU decrease Increase

Biofuel (Ethanol /Diesel) Increase Decrease

Bunker market - Increase

USA More export to USA Less export to EU

Russia More export to EU More export EU

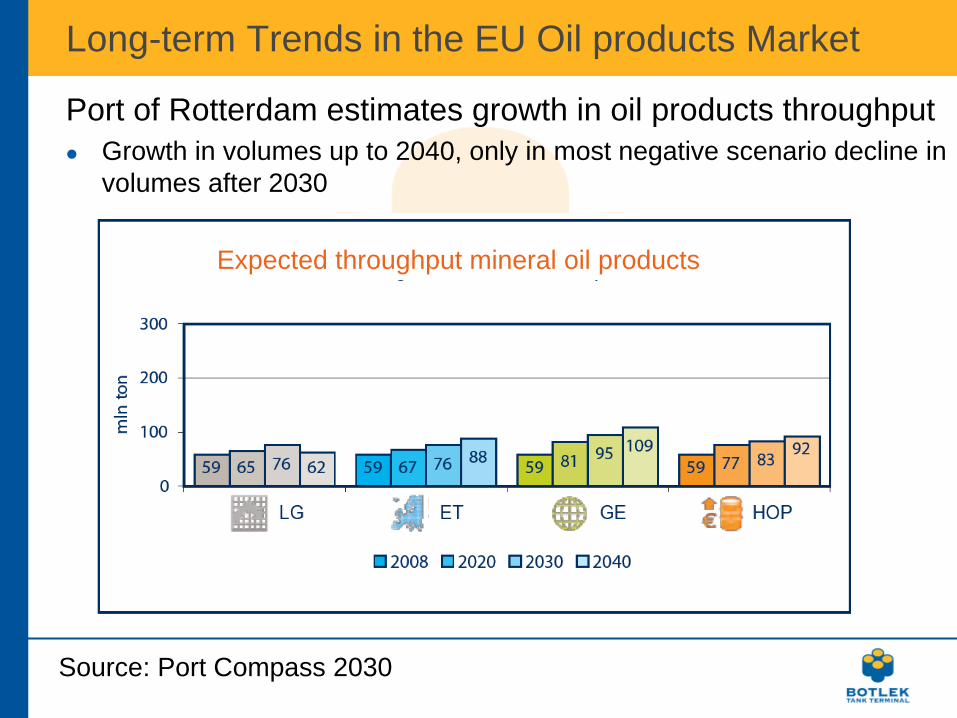

Long-term Trends in the EU Oil products Market

Port of Rotterdam estimates growth in oil products throughput

Growth in volumes up to 2040, only in most negative scenario decline in

volumes after 2030

Expected throughput mineral oil products

Source: Port Compass 2030

Contents:

The outlook for the oil storage industry

1. Introduction Botlek Tank Terminal

2. Trends in the Oil products Market

3. Tank storage market (ARA)

4. Conclusion and future trends

Oil products in the ARA-range

Quarterly throughput of refined oil products (x1000 tonnes) Source: Eurostat / EUR

0

5000

10000

15000

20000

2500020

00Q

1

20

00Q

3

20

01Q

1

20

01Q

3

20

02Q

1

20

02Q

3

20

03Q

1

20

03Q

3

20

04Q

1

20

04Q

3

20

05Q

1

20

05Q

3

20

06Q

1

20

06Q

3

20

07Q

1

20

07Q

3

20

08Q

1

20

08Q

3

20

09Q

1

20

09Q

3

20

10Q

1

20

10Q

3

20

11Q

1

20

11Q

3

20

12Q

1

x1

00

0 t

on

ne

s

Throughput of refined oil products ARA-range

Amsterdam refined oil products

Rotterdam refined oil products

Terneuzen refined oil products

Vlissingen refined oil products

Antwerp refined oil products

Ghent refined oil products

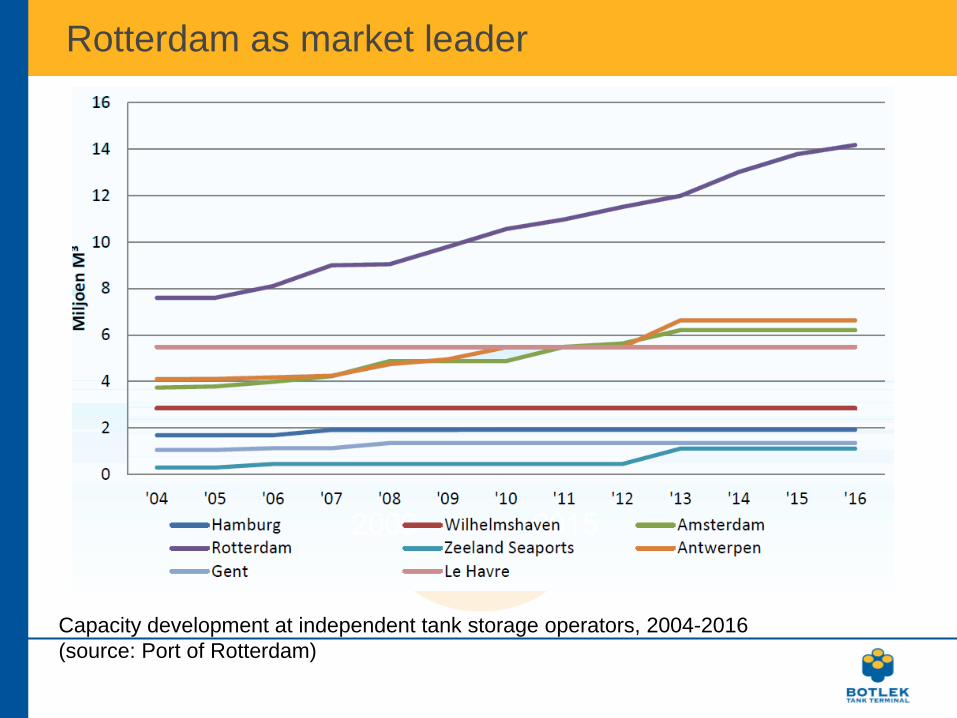

Rotterdam as market leader

Capacity development at independent tank storage operators, 2004-2016

(source: Port of Rotterdam)

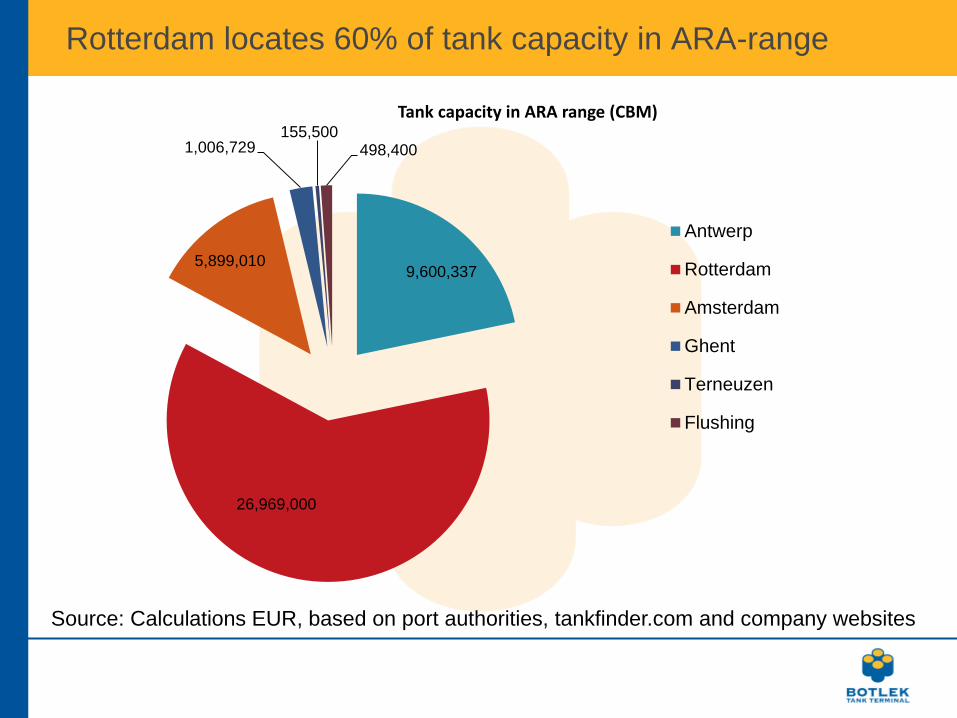

Rotterdam locates 60% of tank capacity in ARA-range

Source: Calculations EUR, based on port authorities, tankfinder.com and company websites

9,600,337

26,969,000

5,899,010

1,006,729 155,500

498,400

Tank capacity in ARA range (CBM)

Antwerp

Rotterdam

Amsterdam

Ghent

Terneuzen

Flushing

Only 20% of tank capacity in Rotterdam is independent

storage for oil products.

Source: EUR calculations based on Port Authorities of ARA ports and individual company information

12,385,000

800,000

4,500,000

5,884,000

2,300,000

200,000 900,000

Capacity in Rotterdam (CBM, 2011)

Crude oil at refineries

Crude oil, independent

Oil products at refinery

Oil products independent

Chemicals, independent

Veg oil at refineries

Veg oil independent

Oil product

usage

Fuel trading

Crude

extraction

Fuel

production

Storage

Storage

Storage

Storage is essential in the

fuel supply chain.

Most storage in seaports.

Ever present demand for

storage because of trading

and speculation on oil

price

Cargo transfers before

final consumption have

increased from 3 times up

to 10 times.

Trade and storage

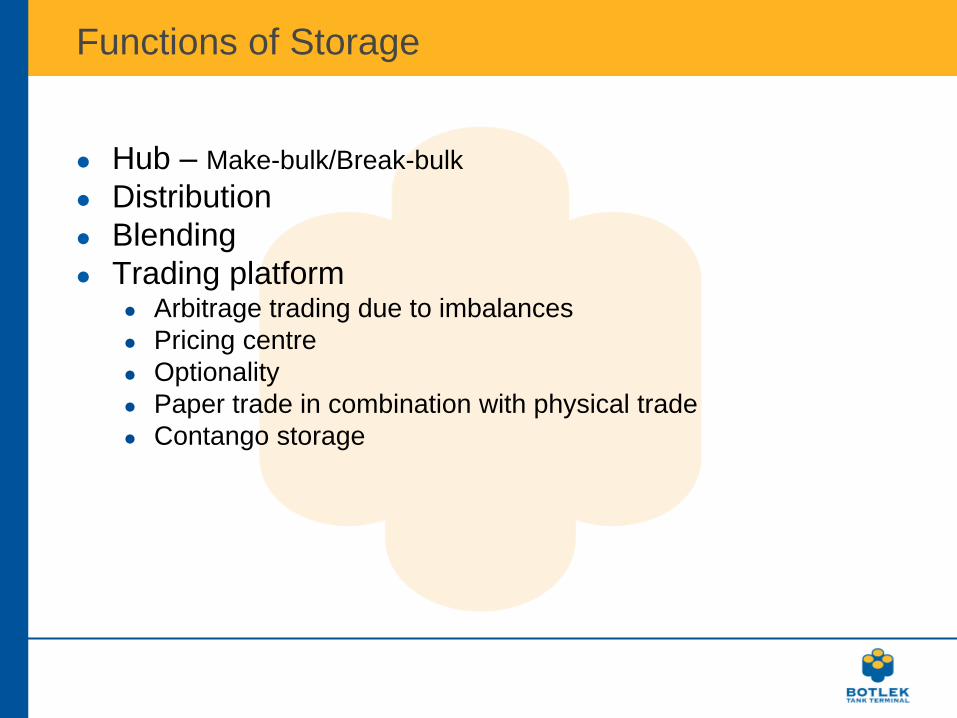

Functions of Storage

Hub – Make-bulk/Break-bulk

Distribution

Blending

Trading platform Arbitrage trading due to imbalances

Pricing centre

Optionality

Paper trade in combination with physical trade

Contango storage

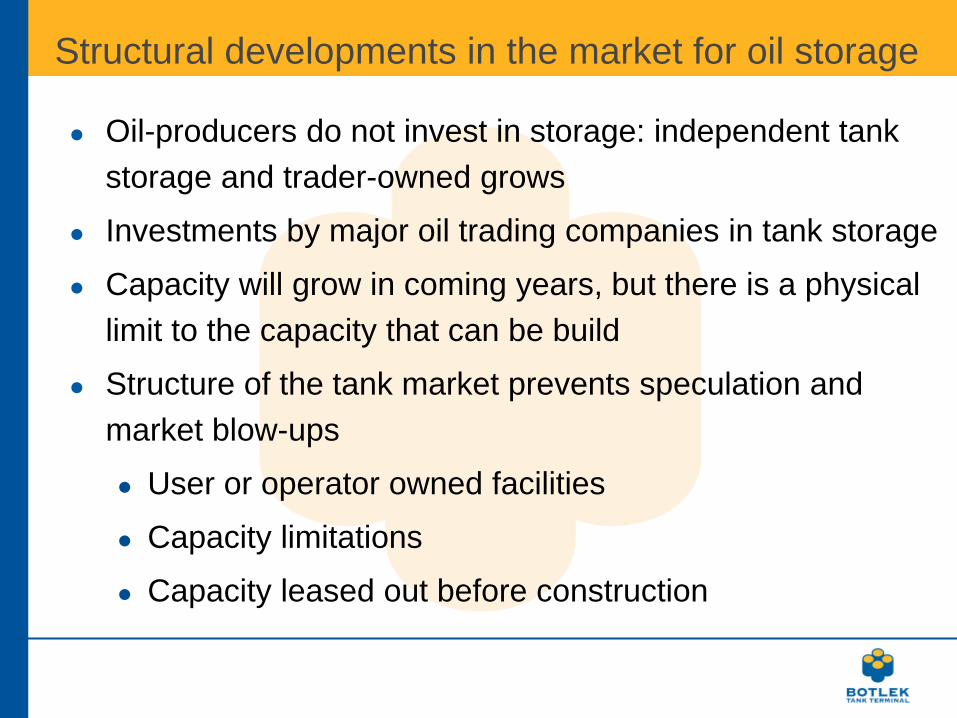

Structural developments in the market for oil storage

Oil-producers do not invest in storage: independent tank

storage and trader-owned grows

Investments by major oil trading companies in tank storage

Capacity will grow in coming years, but there is a physical

limit to the capacity that can be build

Structure of the tank market prevents speculation and

market blow-ups

User or operator owned facilities

Capacity limitations

Capacity leased out before construction

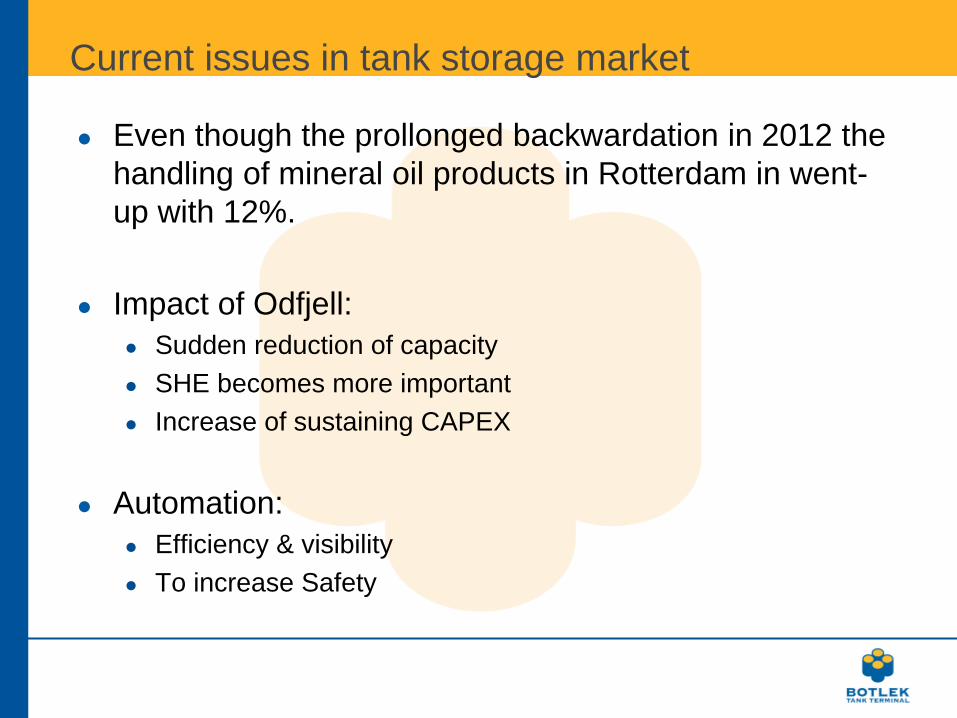

Current issues in tank storage market

Even though the prollonged backwardation in 2012 the

handling of mineral oil products in Rotterdam in went-

up with 12%.

Impact of Odfjell:

Sudden reduction of capacity

SHE becomes more important

Increase of sustaining CAPEX

Automation:

Efficiency & visibility

To increase Safety

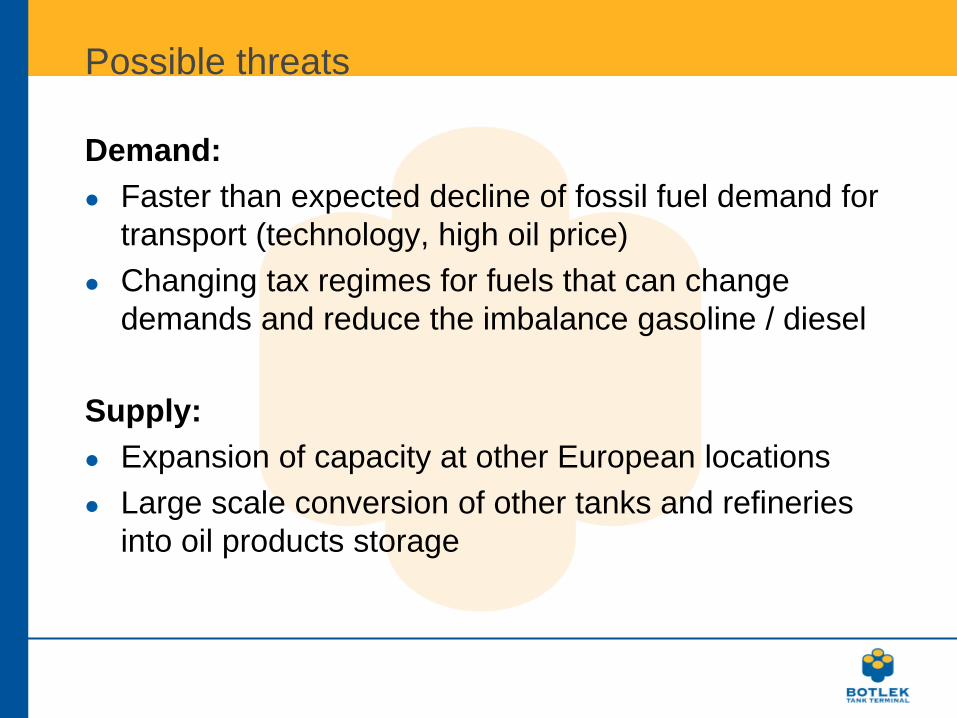

Possible threats

Demand:

Faster than expected decline of fossil fuel demand for

transport (technology, high oil price)

Changing tax regimes for fuels that can change

demands and reduce the imbalance gasoline / diesel

Supply:

Expansion of capacity at other European locations

Large scale conversion of other tanks and refineries

into oil products storage

Contents:

The outlook for the oil storage industry

1. Introduction Botlek Tank Terminal

2. Trends in the Oil products Market

3. Tank storage market (ARA)

4. Conclusion and future trends

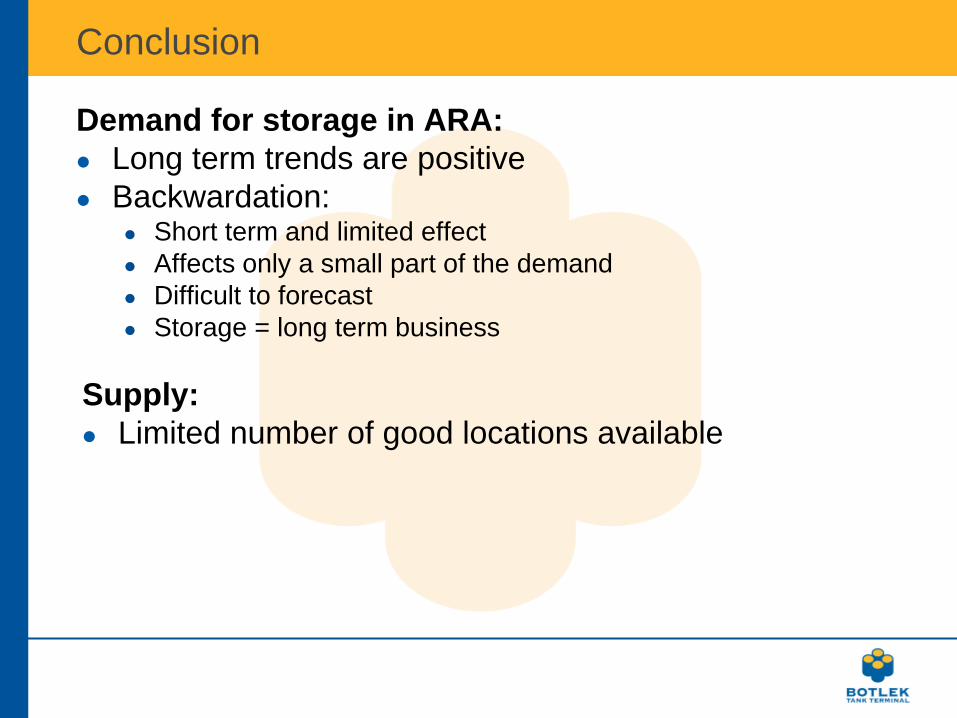

Conclusion

Demand for storage in ARA:

Long term trends are positive

Backwardation: Short term and limited effect

Affects only a small part of the demand

Difficult to forecast

Storage = long term business

Supply:

Limited number of good locations available

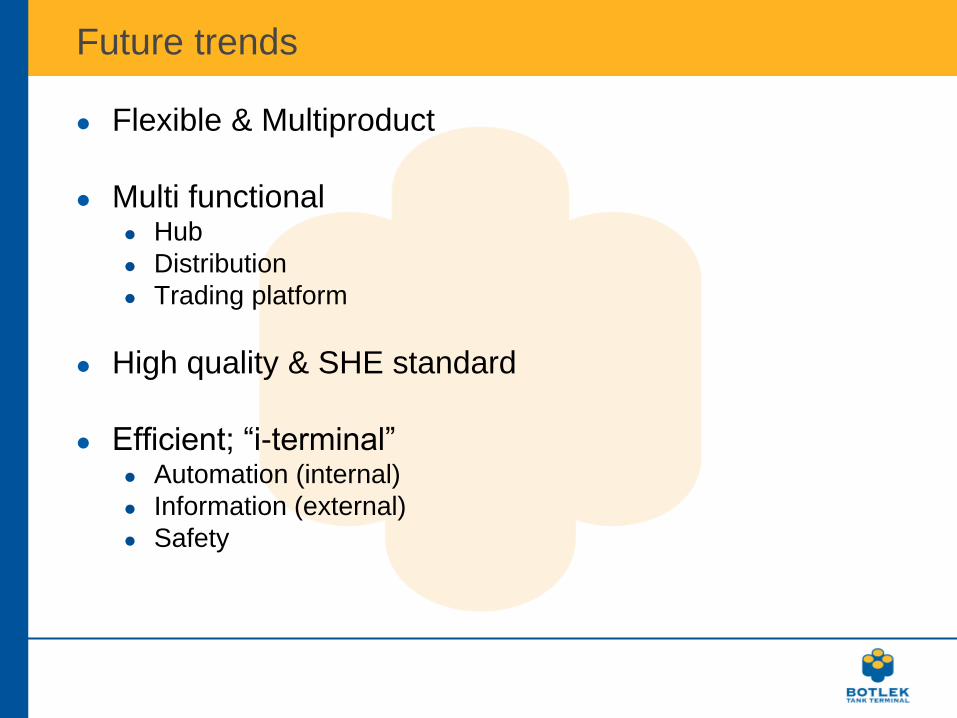

Future trends

Flexible & Multiproduct

Multi functional Hub

Distribution

Trading platform

High quality & SHE standard

Efficient; “i-terminal” Automation (internal)

Information (external)

Safety

Thank you

Questions ?