1

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY

USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT

POLICY

Date:

GAIN Report Number:

Approved By:

Prepared By:

Report Highlights:

FAS/Moscow forecasts Russia’s 2017 production of three major crops (sunflowerseed, soybeans, and rapeseed)

at 15.3 million metric tons (MMT), a 2 percent increase over last year. Sunflowerseed is forecast to increase 1.3

percent to 11.0 MMT and soybeans are forecast to increase 2 percent to 3.2 MMT respectively. The increase in

sunflowerseed is primarily due to an increase in yields, while the increase in soybean production is due to an

increase in area. Production of rapeseed is forecast to increase 10 percent to 1.1 MMT, due to an increased share

of high yielding winter rapeseed in the total rapeseed crop. Area sown to these three major crops is forecast to

remain almost the same, but sunflowerseed area will decrease slightly and soybean area will increase.

FAS/Moscow forecasts Russia’s imports of these three crops at approximately 2.2 MMT, including 2.1 MMT of

soybeans. Exports are forecast at 0.67 MMT, including 0.4 MMT of soybeans, 0.2 MMT of sunflowerseed, and

0.07 MMT of rapeseed. Russia’s total crush for the three major oilseed crops is forecast to increase from

estimated 15.39 MMT in MY 2016/17 to 15.8 MMT, including 10.4 MMT of sunflowerseed, 4.35 MMT of

soybeans and 1.05 MMT of rapeseed. Production of oilseed meal is forecast to increase from estimated 8.13

MMT in MY 2016/17 to 8.29 MMT in MY 2017/18. Production of vegetable oil is forecast to increase from

5.36 MMT in MY 2016/17 to 5.49 MMT in MY 2017/18.

FAS/Moscow Staff

Robin Gray

Annual 2017

Oilseeds and Products Annual

Russian Federation

RS1714

3/16/2017

Required Report - public distribution

2

General Information

NOTE: USDA unofficial data excludes Crimean production and exports. However, as of June

2014, Russian official statistics (ROSSTAT) began incorporating Crimean production and trade

data into their official estimates. Where possible, data reported by FAS Moscow is exclusive of

information attributable to Crimea.

Table of Contents OILSEEDS ...................................................................................................................................... 3

Production ................................................................................................................................... 3

Results of 2016 crop ............................................................................................................. 11 Consumption: ............................................................................................................................ 17 Trade: ........................................................................................................................................ 21

Stocks ........................................................................................................................................ 25 Policy ........................................................................................................................................ 26

Marketing .................................................................................................................................. 27 PSD Tables for Oilseeds ........................................................................................................... 30

MEALS ......................................................................................................................................... 32 Production ................................................................................................................................. 32 Feed Consumption .................................................................................................................... 33

Trade ......................................................................................................................................... 36 Stocks ........................................................................................................................................ 39

PSD Tables for Meal ................................................................................................................. 40

OILS .............................................................................................................................................. 41

Production ................................................................................................................................. 41 Consumption ............................................................................................................................. 42

Trade ......................................................................................................................................... 43 Stocks ........................................................................................................................................ 46 PSD Tables for Oils .................................................................................................................. 46

3

OILSEEDS Commodities:

- Sunflowerseed

- Soybean

- Rapeseed

- Peanuts

NOTE: From 2016, the Russian State Statistical Service (Rosstat) began publishing data on

production of oilseeds in clean weight. Before 2015, Rosstat did not calculate clean weight for

oilseeds. In 2017, all Rosstat data for oilseeds are in clean weight, and Rosstat also re-calculated

previous crops from bunker to clean weight for the last 7 years. Thus, all oilseed production data

in this report are in clean weight.

Production

FAS/Moscow forecasts Russia’s 2017 production for the three major Russian oilseed crops

(sunflowerseed, soybeans, and rapeseed) at 15.3 million metric tons (MMT), a two percent increase

from the crop last year. This forecast includes 11.0 MMT of sunflowerseed, a one percent increase from

last year, 3.2 MMT of soybeans, a 2 percent increase from last year, and 1.1 MMT of rapeseed, a 10

percent increase from last year. The forecast summary for MY 2017/18 is provided below in Table 1.

In the last five years Russia has also increased production of niche oilseed crops, such as oil flax,

Camelina, and safflower. In 2016, the total crop of these three oilseeds reached 1 MMT, and

FAS/Moscow forecasts the same volume of production for these three crops in 2017. Thus, Russia’s

total production of oilseeds in MY 2017/18 may reach 16.3 MMT.

Table 1. Consolidated PSD Forecast for Major Oilseeds for MY 2017/18, Thousand Metric Tons

(TMT), 1,000 HA Post MY 2017/18 Sunflowerseed Soybeans Rapeseed Peanuts TOTAL

Area Planted 7,400 2,300 1,000 0 10,700

Area Harvested 7,150 2,200 910 0 10,260

Beginning Stocks 353 131 33 5 522

Production 11,000 3,200 1,100 0 15,300

MY Imports 50 2,100 60 145 2,355

MY Imp. from U.S. 0 300 0 0 300

MY Imp. from EU 0 0 0 0 0

Total Supply 11,403 5,431 1,193 150 18,177

MY Exports 200 400 70 0 670

MY Exp. to EU 10 0 5 0 15

Crush 10,400 4,350 1,050 0 15,800

Food Use Dom. Cons. 220 0 0 145 365

Feed Waste Dom. Cons. 300 550 25 0 875

Total Dom. Cons. 10,920 4,900 1,075 145 17,040

Ending Stocks 283 131 48 5 467

Total Distribution 11,403 5,431 1,193 150 18,177

Note: The above table is composed of PSD forecast for each crop, despite differing marketing years.

The marketing year for sunflowerseed and soybeans is September – August. The marketing year for

rapeseed is July – June.

4

FAS/Moscow’s forecast for production is based on the assumption that weather in 2017 will be normal,

area sown to oilseeds will remain almost the same, and yields of the major oilseed crops will remain

low1. Oilseeds in Russia compete for fertile soil and climate-friendly regions with grains, sugar beets,

and other crops. Therefore, a significant increase in the area sown to oilseed crops is not possible. The

financial situation for most Russian farmers remains poor, and they cannot afford significant

investments in new expensive agro-technologies (i.e. Clearfield technology for sunflowerseed), which

would improve yields and made crop production less dependent on weather and pests. Almost all

oilseeds in Russia are sown in the spring. Area sown to winter oilseeds (winter rapeseed and false flax

(Camelina) is small and comprises approximately 2.5 percent of all area sown to oilseeds. In fall 2016,

farmers planted 301.0 thousand hectares (THA) to winter oilseeds (compared to 317.6 THA in fall

2015), of which area sown to winter rapeseed was 181.5 THA, or 20 percent of the total forecast

rapeseed planted area in MY 2017/18. The other 119.5 THA of winter oilseeds were sown to false flax

(Camelina)2

Sunflowerseed

Given normal weather conditions, FAS/Moscow forecast sunflowerseed production at 11.0 MMT. This

forecast is based on an assumption that the average yield for sunflowerseed (in clean weight) will be, in

accordance with the trend line, at approximately 1.54 MT/HA (compared with 1.51 MT/HA in 2016).

FAS/Moscow forecasts that sunflowerseed planted area will be 7.4 million hectares, and harvested area

will be 7.15 million hectares, almost the same as in 2016. In MY 2016/17, sunflowerseed was harvested

from 7.2 million hectares. The FAS/Moscow forecast assumes that, as happened in the previous years,

farmers will commit more area to sunflowerseed than the Ministry of Agriculture recommends and/or

plans.

1 In the United States the average yield of soybeans is 3.2 MT/HA, the average yield of canola (spring rapeseed) is 2.0

MT/HA, and the average yield of sunflowerseed is approximately 1.8 MT/HA. The average sunflowerseed yield in the EU-28

is 2.0 MT/HA. 2 Source: Ministry of Agriculture of the Russian Federation: http://www.mcx.ru/documents/document/show/37808.htm

5

Source: FAS/Moscow based on Rosstat data.

The Ministry of Agriculture and provincial authorities are trying to convince farmers to decrease area

planted to sunflowerseed, and the Ministry of Agriculture forecasts that in 2017 farmers will plant 7.17

million hectares to sunflowerseed, or 0.33 million hectares less than in 2016 (7.5 million hectares).

Sunflowerseed, more than any other crop, exhausts the soil. Moreover, if sunflowerseed is sown in

consecutive seasons, the risks are very high that the next crop will be damaged by pests that remain in

the soil. In particular the parasite weed sunflower broomrape – Orobanche cumanaache sps., also called

“zarazikha.” Zarazikha affects the root of the sunflowerseed plant and kills the plant. This parasite

weed has spread in Russia and may kill up to 100 percent of the crop in the field. Only farmers that can

afford investments in high-quality pest-resistant seeds, herbicides and other chemicals, and follow exact

agronomic practices are able to successfully plant sunflowerseed season after season and maintain good

yields. However, most farmers that sow sunflowerseed cannot afford such expenses. Despite the threat

of losing the crop, and recommendations of provincial and federal authorities, most farmers make their

planting decisions based on returns. If they can get profit even with low yields, they will continue

planting sunflowerseed despite all recommendations. So far, a stable demand for sunflowerseed in the

domestic market has kept the average returns from selling sunflowerseed higher than returns from

selling most other crops. As a result, farmers have planted more area to sunflowerseed than the federal

and provincial authorities recommended.

In 2016, the price of sunflowerseed remained stable, but at the beginning of 2017 sunflowerseed prices

began to decrease. This trend may decrease the incentive for farmers to sow sunflowerseed (see

paragraph Marketing of OILSEED section of this report.) However, the demand from crushers is high

due to new capacity put into operation. The demand from traders has also increased due a lower export

duty. Sunflowerseed still remains one of the most profitable crops for farmers. This factor favors

forecast stability for the 2017 sunflowerseed sown area projections, despite recommendations from the

6

Ministry of Agriculture and local authorities. However, at the time of this report, sunflowerseed sowing

has not yet started in Russia.

Soybeans

FAS/Moscow forecasts that Russian area sown to soybeans will continue grow and may reach 2.3

million hectares (slightly higher than the Ministry of Agriculture plans of 2.25 million hectares). This

will result in a total of 2.2 million hectares of harvested area. However, yield progress is not forecast.

Based on the trend line, the average yield of soybeans will be at best, 1.45 MT/HA. Given normal

weather conditions, FAS/Moscow forecasts the soybean crop in MY 2017/18 at 3.2 MMT, three percent

higher than in 2016.

Source: Source: FAS/Moscow based on Rosstat data.

The Russian Ministry of Agriculture forecasts that area sown to soybeans will increase by 79.0 THA

from last year, and will reach 2.26 million hectares. Since demand for domestic soybeans is increasing

in Russia, these forecasts seem feasible.

Rapeseed

FAS/Moscow forecasts that the MY 2017/18 rapeseed crop will recover to 1.1 MMT, a ten percent

increase y-o-y. This forecast is based on the assumption that the area sown to winter rapeseed will

increase slightly. Given normal weather conditions and the increase in winter rapeseed, total rapeseed

production will increase. Note, yields for winter rapeseed are 70-80 percent higher on average than

spring rapeseed yields.

7

Source

: Source: FAS/Moscow based on Rosstat data.

The Russian Ministry of Agriculture reports that the winter 2017 rapeseed crop was planted on 0.18

million hectares, and spring rapeseed will be planted on 0.87 million hectares.

Table 2. Russian Ministry of Agriculture’s Forecast for Planting of Oilseeds, THA.

Crops 2016

(spring data)

2017

(forecast) 2017 in % to 2016

2017 +/ -

to 2016

All oilseed crops sown area 12,170.7 11,744.8 96.5 -425.9

- Sunflowerseed 7,498.8 7,171.4 95.6 -327.3

- Soybeans 2,184.8 2,263.8 103.6 79.0

- Rapeseed 995.1 1,053.9 105.9 58.8

- Oil (crown) flax 709.2 662.3 93.4 -47.0

- Mustard 180.6 169.5 93.9 -11.1

- False flax (Camelina) 141.3 112.9 79.9 -28.4

- Other 460.9 311.0 67.5 -149.9

Source: Ministry of Agriculture

Inputs:

There are no significant changes in the supply of inputs for production of oilseeds in Russia.

Fertilizer and chemicals

The Ministry of Agriculture reports that as of February 2017, there were higher stocks of mineral

fertilizer than last year: 450,100 metric tons (MT) (in active ingredient), 149,900 MT more than last

8

year3. However, there are no data on the share of fertilizer that is used for spring sowing of oilseeds,

and since oilseeds are sown later than grains and many other crops, the fertilizer supply is not so

important for oilseed producers.

There are no official data on supply and use of chemicals in oilseed production, although herbicides and

pesticides are very important for oilseed crop protection. Crop producers’ incomes in 2016/17

decreased compared to 2015/16. Thus, they are likely to cut purchase of expensive inputs, including

chemicals.

Planting seeds

Supply and quality of planting seeds is a critical factor for oilseeds production in Russia. In 2015,

Russia adopted federal programs aimed at supporting the development of breeding and selection of

planting seeds for the improvement of production of some crops and substitution of imports of planting

seeds. According to the Russian Ministry of Agriculture, in 2016, Russian farmers (including so called

peasant farms) planted 34.65 TMT of planting seeds of sunflowerseed, 245.59 TMT of planting seeds of

soybeans, and 7.1 TMT of planting seeds of spring rapeseed (Table 3). The total cost of all these

planting seeds was over 25 million Rubles4 ($390,625).

Table 3. Ministry of Agriculture’s Estimate of Volume of Planted Seeds of Major Oilseeds in 2016

Crops Area,

THA

Planted

seeds,

TMT

Availability,

percent

Price of

1 MT,

thousand

Rub.

Value of sown

seeds, thousand

Rub. 2016 2015

Sunflowerseed 7,498.8 34.65 98.5 98.9 383.2 13,277.9

Soybeans 2,184.7 245.59 108.8 105.7 43.2 10,609.5

Rapeseed,

spring

893.3 7.1 83.5 86.7 172.9 1,227.6

Source: Ministry of Agriculture

The Ministry of Agriculture estimates the “need” for planting seeds for the 2017 crop as 35.1 TMT of

sunflowerseed, 243.4 TMT of soybeans, and 7.5 TMT of spring rapeseed (Table 4). However,

according to reported sources, by the end of January 2017, Russian farmers had only 38.2 percent of

planting seeds of sunflowerseed, 98.3 percent of soybeans, and 54.7 percent of planting seeds of

rapeseed. Since oilseed planting starts later than planting of many other crops, farmers purchase oilseed

planting seeds later. The availability of seed at the end of January was higher in 2017 than in 2016.

Table 4. Ministry of Agriculture’s Estimate of “Need” for Planting Seeds for Major Oilseeds for 2017

Spring Sowing (as of January 25, 2017)

Need,

TMT

Availability,

TMT

Incl.

imported,

TMT

Availability,

percent

Quality*,

percent

2017 2016

Sunflowerseed 35.1 13.4 0.1 38.2 33.3 91.2

3 http://www.mcx.ru/news/news/show/58274.355.htm

4 Russian Ruble exchange rate in 2016 was volatile, but for reference, in this report FAS/Moscow assumes the exchange rate

at 64 Rubles per $1.

9

Soybeans 243.4 239.3 0.0 98.3 94.8 86.3

Rapeseed,

spring

7.5 4.1 0.0 54.7 59.0 39.6

*Quality means that seeds meet their specifications

Source: Ministry of Agriculture

Farmers usually purchase imported planting seeds in spring, before sowing, and the share of imported

planting seeds remain high. According to the Ministry of Agriculture, in 2016 the share of imported

seeds in 2016 varied from 21.6 percent for soybeans to 53.6 percent for sunflowerseed (Table 5).

Table 5. Origin of Planting Seeds of Oilseeds, 2016, TMT

Imported Domestic, registered Non-registered

Sunflowerseed 53.6 37.5 8.9

Soybeans 21.6 58.1 20.3

Rapeseed, spring 30.0 40.4 29.5

Rapeseed, winter 49.7 31.0 19.3

Source: Ministry of Agriculture

Only large agroholdings can afford imported, high-yield hybrids or varieties, and proper chemicals. The

majority of farmers use domestically registered and even non-registered seeds. Thus, the difference in

yields may vary for sunflowerseed from less than 1 MT per HA to more than 2 MT per HA.

Breeding and Selection of Domestic Planting Seeds5

Sunfloweseed

Sunflowerseed is the main oilseed crop in Russia, and provides for the major supply of vegetable oils.

The federal government supports substitution of imports of these planting seeds. The R&D Institute

Named after Pustovoitov in Krasnodar Kray, and the R&D Institute of Agriculture of the South-East (in

Saratov Oblast), as well as several private seed-selection companies are involved in selection of

domestic sunflowerseed varieties and hybrids. So far, almost 54 percent of planting seeds of

sunflowerseed in Russia are varieties and hybrids of foreign selection, and most of these seeds are

imported.

According to industry analysts, the price of foreign planting seeds may be three, even four times higher

than the price of domestic seeds. The State Seeds Register has four varieties and 48 sunflowerseed

hybrids, including 15 of Russian origin. Russian specialists consider that there are enough hybrids of

domestic selection that can replace imported sunflowerseed in two years. However, there is a shortage

of planting material for multiplication and commercial production. When domestic hybrids of

sunflowerseed are compared with imported, then under normal growing conditions, domestic seeds are

on par with imported. But the situation changes when the soil preparation and cultivation practices

improve, then imported hybrids produce much higher yields. According to specialists from the Institute

of Pustovoitov, given that half of the 7.5 million hectares sown to sunflowerseed in Russia have

unfavorable soil and cultivation practices, domestic varieties and hybrids may even be better than

foreign: “Foreign hybrids were created especially for high crop culture, for yields at 4-4.5 MT per HA.

5 Source: http://www.agroinvestor.ru/technologies/article/25823-ukhod-ot-semennoy-zavisimosti/ (in Russian)

10

Considering that in our country sunflowerseed are often sown in not the best regions, i.e., in Saratov

oblast, where the potential yields cannot be higher than 2-3 MT per HA, there is no big difference

between domestic and foreign hibrids.”

The Russian government is subsidizing the selection of planting seeds for sunflowerseed. The 2017

federal budget envisages 91.3 million Rubles (($1.4 million) in subsidies for compensation of 20 percent

of the cost of production of planting seeds for sunflowerseed. These subsidies are part of the so called

per hectare “decoupled support” program, and rates for subsidies are calculated per hectare: 33,000

Rubles ($516) for parent forms of sunflowerseed hybrids, 8,700 Rubles ($136) for the first generation of

hybrids, and 32,600 Rubles ($509) for original seeds of varieties of sunflowerseed, and 9,000 Rubles

($141) for elite seeds of varieties of sunflowerseed.6

Industry analysts consider the threat of the parasite plant called Orobanche Cumana as the major threat

for an increase in sunflowerseed production in Russia. This parasite weed affects the roots of

sunflowerseed and can destroy up to 100 percent of the crop. The main way to combat this plague is

either to use an eight to 10-years crop rotation schedule, (crops such as corn, millet, and sorghum do not

allow the seeds of the parasite to survive) or to use special practices called Clearfield based on special

hybrids, herbicides, and strict agronomic practices.

Soybeans

Russia increased development of soybean varieties. Russian breeders have oriented their research

towards resistance to weather and the climate peculiarities of the different Russian regions. This factor,

so called “regionalization” of planting seeds is praised even by foreign companies that sell imported

seeds. Additionally, Russian varieties are less expensive than imported. Thus, the price of soybean

planting seeds of Russian selection is about 40,000 Rubles ($625) per 1 MT, while the first reproduction

of imported soybean planting seeds is over 80,000 Rubles ($1,250) per 1 MT.

According to industry, Russian varieties comprise 83 percent of used soybean planting seeds. Soybean

seed breeding orients towards the following: a decrease of the vegetation period (early varieties),

stability of yields, improvements of biochemical and technological characteristics of soybeans,

resistance to dangerous pathogens, resistance to drought, frost, hail damage, waterlogging, soil salinity

and soil acidity. According to the Russian Soy Union, over 130 soybean varieties are registered in

Russia, including over 100 Russian varieties. There are several soy-breeding centers in Russia,

including in Amur Oblast (All-Russian R&D Institute of Soybeans), in Krasnodar Kray (Research

Institute named after Pustovoitov), and the Center “Soybean Complex”. The price for good Russian

varieties (first reproduction) is approximately 60,000 Rubles ($938) per 1 MT. This is almost two times

lower than the price of imported varieties. However, agronomists report that yields and protein content

of local varieties are lower than yields and protein content of registered imported varieties. Russian

varieties are “extensive,” and may even be damaged by intensive technologies (“super-nutrition may

lead to lodging”). There are two criteria for the measurement of protein content: raw protein and protein

calculated in over-dry matter (DM). The second characteristic determines the quality of soybeans and

determines the price. According to the General Director of the Russian Division of the Canadian

company “Semans Prograin” (the company sells and produces in Russia some Canadian varieties of

soybeans), in 2016 the soybean price differences for different protein levels varied significantly. The

price of soybeans with a protein DM of 27 percent was 19,000 Rubles ($297), while the price of

6 Source: Ministry of Agriculture

11

soybeans with a protein DM over 38 percent was 28,000 Rubles ($438). However, farmers that plant

soybeans for commercial purposes first consider the total expenses per hectare and the consistency of

the crop: foreign varieties may have higher yields (up to 1 MT per hectare), but harvest season for some

foreign varieties is mid-October or even end of October. Given the fall climate in European Russia, a

later harvest may result in the complete loss of crop, or at least, interfere in the harvesting of other crops.

Finance

There are no data on the financing of Russian agriculture by crops. The decoupled support of

agriculture is based on sown area, and this support is small. To some extent agricultural producers may

rely on interest rate subsidies. In 2017, the new mechanism for interest rate subsidies became available.

The government will subsidize the banks directly, and the banks will provide credits to farmers at the

five percent interest rate. Previously, farmers had to obtain loans at commercial interest rates and were

later reimbursed by the state. As of the end of January 2017, the Ministry of Agriculture signed

agreements on the new scheme of government interest rate subsidies with six banks: Rosselkhozbank,

Alfa-Bank, Promsvyazbank, Bank VTB, Sberbank, and Gazprombank, and was going to sign

agreements with UniKreditbank, Bank “Otkrytie”, RosBank, and Raiphizenbank.7 However, industry

analysts report of significant delays in financing with this scheme.

Results of 2016 crop

In 2016, Rosstat continued reporting oilseed crops in clean weight, and results of oilseed production in

2016, by crops, are provided in the table below:

Table 6. Results of 2016 Oilseed Crop

2009 2010 2011 2012 2013 2014 2015 2016

Planted Area, 1,000 hectares

Sunflowerseed 6,19

6

7,15

4

7,614 6,529 7,271 6,823 6,922 7,481

Soybeans 875 1,20

6

1,229 1,481 1,532 2,002 2,123 2,228

Rapeseed 688 856 893 1,191 1,326 1,174 1,014 978

- winter 178 218 175 105 239 261 138 96

- spring 511 638 718 1,085 1,087 913 876 881

Mustard 101 110 134 118 154 182 188 173

Oil flax (Crown

flax)

146 267 500 618 478 488 628 683

False flax

(Camelina)

182 268 207 142

Safflower 16 89 123 292 445

Other 15 24 76 135 30 17 20 21

Total 8,02

0

9,61

6

10,44

7

10,08

7

11,06

0

11,07

6

11,393.

1

12,151.

0

Production, 1,000 MT

Sunflowerseed 6,01 4,97 9,062 7,495 9,842 8,374 9,173 10,858

7 http://www.mcx.ru/news/news/show_print/58309.355.htm

12

5 9

Soybeans 873 1,13

3

1,641 1,683 1,517 2,362 2,707 3,135

Rapeseed 605 608 956 945 1,259 1,324 1,001 997

- winter 308 395 304 166 407 460 255 163

- spring 359 275 752 869 987 990 747 834

Mustard 24 36 88 42 55 99 64 68

Oil flax (Crown

flax)

94 173 464 361 320 379 502 634

False flax

(Camelina)

0 0 0 0 128 156 90 79

Safflower 8 45 87 154 286

Other 3 10 53 67 21 13 11 11

Total 8,18

6

7,45

7

13,11

5

11,31

3

14,15

1

13,70

7

13,702 16,067

Yields per harvested area, 1hectares

Sunflowerseed 1.15 0.96 1.34 1.30 1.55 1.40 1.42 1.51

Soybeans 1.11 1.09 1.48 1.31 1.36 1.36 1.30 1.48

Rapeseed 1.20 1.10 1.26 1.06 1.25 1.39 1.12 1.11

- winter 1.82 1.90 1.77 1.68 1.73 1.81 1.93 1.82

- spring 0.93 0.68 1.13 0.99 1.13 1.25 0.98 1.02

Mustard 0.47 0.48 0.80 0.54 0.50 0.67 0.49 0.55

Oil flax (Crown

flax)

0.88 0.86 1.04 0.69 0.78 0.93 0.85 0.97

False flax

(Camelina)

0.61 0.78 0.66 0.57 0.60

Safflower 0.62 0.64 0.76 0.64 0.67

Source: Rosstat, except Crimea. Original Rosstat data includes Crimea. In 2016, Crimea produced 191

TMT of oilseeds, including 152 TMT of sunflowerseed, 0.72 TMT of soybeans, 1.74 TMT of rapeseed

(primarily spring), 5.5 TMT of mustard seed, 30.4 TMT of oil flax and 0.1 TMT of other oilseeds

(safflower).

Area sown to all oilseeds (three major crops and other crops, such as Oil flax, Camelina and Safflower)

in Russia has grown steadily since 2000 from 5.5 million hectares in 2000 to 8.02 million hectares in

2009, and to 12.15 million hectares in 2016. This includes the area sown to sunflowerseed that

increased from 4.6 million hectares in 2000 to 6.20 million hectares in 2009 and to 7.48 million hectares

in 2016. However, the share of area sown with sunflowerseed, as a percentage of total area sown to

oilseeds, decreased. At the same time, the share of soybeans, rapeseed and other oilseed crops increased

(Chart 4). Nevertheless, sunflowerseed still dominates total oilseed production. However, because

sunflowerseed yields are heavily dependent on weather, production fluctuations are significant (Chart

5).

13

Source: Rosstat

Source: Rosstat.

Sunflowerseed

Sunflowerseed still remains among the most profitable crops in Russia. In MY 2016/17, the price of

sunflowerseed began to decrease despite high demand from crushers. However, industry analysts report

that relative to other crops, the margin of sunflowerseed produccers is higher than the margin of grain

producers. In 2016, production of sunflowerseed increased in all federal districts except the Central

Federal District. The increase in production was primarily due to favorable weather and slightly

improved yields.

14

Source: Rosstat

In 2016, the Volga Valley Federal District became the leader in production of sunflowerseed, with 3.6

MMT crop (30 percent or almost 0.84 MMT’s increase y-o-y). Production there increased primarily due

to increased sown area, while the average yield still remained low, approximately 1.1 MT per 1 HA

(only 5 percent higher than in 2015). The Southern Federal District followed in sunflowerseed

production of over 3.2 MMT (22 percent or 0.59 MMT increase y-o-y). Production in the Southern

Federal District increased primarily due to increased yields from the average 1.65 MT/HA in 2015 to

1.93 MT/HA in 2016, or by 17 percent. Yields increased practically in all sunflowerseed producing

oblasts of the Southern Federal District, but the variation in yields was significant: from 1.43 MT/HA in

Volgograd oblast to 2.53 MT/HA in Krasnodar Kray. Sunfloweseed production in the Central Federal

District, the last year leader, decreased from 2.82 MMT in 2015 to 2.68 MMT in 2016, primarily due to

decreased area sown to sunflowerseed, although average sunflowerseed yields remained among the

highest in Russia: 2.16 MT/HA in 2016 compared with 2.15 MT/HA in 2015. Bryansk and Belgorod

oblast were the leaders in the yields with 2.86 MT/HA and 2.64 MT/HA respectively.

Chart 7. Location of Sunflowerseed Production in Russia in 2015

15

Over 1.0 MMT (Dark Red)

- Rostov Oblast - 1.26 MMT (0.83 MMT in 2015)

- Saratov Oblast – 1.29 MMT (1.0 MMT in 2015)

- Krasnodar Kray – 1.07 MMT (1.02 MMT in 2015)

From 0.5 to 1.0 MMT (Red)

- Voronezh Oblast – 0.92 MMT (1.0 MMT in 2015)

- Volgograd Oblast – 0.81 MMT (0.73 MMT in 2015)

- Samara Oblast – 0.71 MMT (0.54 MMT in 2015)

- Orenburg Oblast – 0.66 MMT 9 0.53 MMT in 2015)

- Tambov Oblast – 0.57 MMT (0.74 MMT in 2015)

- Stavropol Kray – 0.54 MMT (0.39 MMT in 2015)

From 0.3 to 0.5 MMT (Light Red)

- Altay Kray – 0.50 MMT (0.36 MMT in 2015)

- Belgorod Oblast – 0.37 MMT (0.32 MMT in 2015)

- Penza Oblast – 0.34 MMT (0.26 MMT in 2015)

- Kursk Oblast – 0.31 MMT (0.27 MMT in 2015)

- Ulyanovsk Oblast – 0.26 MMT (0.17 MMT in 2015)

- Bashkortostan Republic – 0.22 MMT (0.24 MMT in 2015)

Source: FAS/Moscow based on Rosstat data for 2016 crop.

Soybeans

In 2016, soybean area increased by 100 THA to 2.2 million hectares, average soybean yield also

increased by almost 0.2 MT/HA, and reached 1.48 MT/HA. The 2016 Russian soybean crop reached an

historic high of 3.1 MMT (2.7 MMT in 2015), and the increase was due to increased crop in European

Russia due to an increased area and favorable-for yield weather. The Far East Federal District still

remains the leader in soybean production with 1.3 MMT crop (1.4 MMT in 2015), but its share

decreased from 52 percent in 2015 to 42 percent in 2016. The Central Federal District is the second

16

largest producer of soybeans with over 1.2 MMT crop (0.8 MMT in 2015). According to industry

analysts, the volume of soybean production in the Russian Far Eastern and its location distinguishes it

from the Russian European market. Given the location, soybeans produced in the Far East are either

exported to China or sold to crushers located in the Far East or Siberia. High soybean prices in the Far

East and the high cost of transporting soybeans from the Far East to Central European Russia make

soybeans from the Far East more expensive for processors than either soybeans from European Russia

or even imported soybeans. Export duties on soybeans were lifted on September 1, 2015. Soybean

exports to China have increased, and soybean production in the Far East remains profitable.

Source: Rosstat

Chart 9. Location of Soybean Production in Russia in 2016

17

Over 0.5 MMT (Dark Green)

- Amur Oblast – 0.92 (1.00 MMT in 2015)

From 0.2 to 0.5 MMT (Green)

- Belgorod Oblast – 0.48 MMT (0.32 MMT in 2015)

- Krasnodar Kray – 0.32 MMT (0.25 MMT in 2015)

- Kursk Oblast – 0.29 MMT (0.17 MMT in 2015)

- Primorskiy Kray – 0.28 MMT (0.26 MMT in 2015)

From 0.1 to 0.2 MMT (Light Green)

- Voronezh Oblast – 0.11 MMT (0.09 MMT in 2015)

Source: FAS/Moscow based on Rosstat data for 2016 crop.

Consumption:

Since the early 2000’s, Russian oilseeds consumption has steadily increased due to the growing demand

for protein feeds, such as meal, cake and, in the last 2-3 years, whole-fat feeds (semi-processed

soybeans). Although, vegetable oil still remains a major product of the Russian oilseeds industry.

FAS/Moscow forecasts that Russia’s domestic consumption of the three major oilseeds in MY 2017/18

will reach 16.90 MMT, a 2.5 percent increase compared with MY 2016/17 domestic consumption of

16.48 MMT. The domestic consumption total includes 10.92 MMT of sunflowerseed (2.4 percent

increase from last year), all due to increased crush from 10.10 MMT that FAS/Moscow estimated for

MY 2016/17 to 10.40 MMT. Food use domestic consumption will remain at the same level as last year:

0.22 MMT, but feed waste will decrease from 0.34 MMT to 0.3 MT due to increased crushers’ demand.

Consumption of soybeans will increase from 4.8 MMT in MY 2016/17 to 4.9 MMT in MY 2017/18, and

this will include crush of 4.35 MMT and direct feeds use of 0.55 MMT of beans (whole and semi-

crushed beans). Soybean crush and direct use are forecast to increase from last year by 50 TMT each.

18

Domestic consumption of rapeseed is forecast to increase from MY 2016/17 by 35 TMT to 1.08 in MY

2017/18.

Source: IKAR: http://soyanews.info/news/u_mezov_snova_defitsit_syrya.html and Rosstat

Estimates of total crushing capacity of Russia vary from 18 MMT to 21 MMT. According to the

Russian Union of Oils and Fats Producers and some industry analysts, Russia’s total capacity for

crushing oilseeds in 2016 was 18.0 MMT. Other analysts estimate Russia’s total crushing capacity at

20-21 MMT.8 The difference depends on the inclusion or exclusion of small crushing operations at

farms. Additionally, some analysts consider that due to the technological necessity to keep some

facilities inactive, Russia’s actual capacity to crush oilseeds is 18 MMT. However, even the minimum

estimate of 18 MMT exceeds Russia’s production of oilseeds by 12 percent.

There is no official information on the specification of oilseed crushing capacity. Most crushers work

with sunflowerseed, but many of the modern plants built in the last five years in European Russia can

switch between crushing sunflowerseed and rapeseed, and some have the ability to crush soybeans. The

Institute of Agricultural Marketing (IKAR) estimates the 2016/17 oilseeds crushing capacity in the

sunflowerseed producing regions at 18.76, that is 36 percent more than the sunflowerseed production in

these regions.

Some industry analysts separate crushing plants for sunflowerseed and rapeseed versus plants that can

crush soybeans. The actively working capacity of sunflowerseed and rapeseed plants (without small

crushers at farms) is estimated at 14.7 MMT, and the capacity of soybean crushing plants at 5.7 MMT.

The specialized soybean crushing plants are located in the North-West of Russia (Kaliningrad oblast),

8 http://www.agroinvestor.ru/analytics/news/25433-urozhay-maslichnykh-priblizilsya-k-16-mln-tonn/

19

and work primarily with imported soybeans, and in the Far East. In 2016/17 soybean crushing capacity

also increased in the Central FD (Belgorod Oblast).

In all of the sunflowerseed and rapeseed producing regions production has lagged behind the quickly

growing crushing capacity. According to IKAR, in MY 2016/17 crushing capacity in the South of

Russia (Southern and North Caucasus federal districts) approached 7 MMT, while the total production

of oilseeds in this region was 4 MMT, including 3.9 MMT of sunflowerseed. In the Center of European

Russia crushing capacity is also estimated at 7 MMT, and production of all oilseeds was 3.38 MMT,

including 2.7 MMT of sunflowerseed. In the Volga Valley FD crushing capacity was 4.2 MMT, and

production of oilseeds (all sunflowerseed) was 3.6 MMT. Even in Siberia and Ural crushing capacity

(616 TMT) exceeded production of sunflowerseed, which was 588 TMT.9

According to IKAR, 60 percent of crushing capacity in Russia is held by the top ten oilseeds crushing

holdings.10

The crushing capacity of these ten companies is estimated at approximately 12.9 MMT a

year.11

Companies included in this top ten list are:

- “Yug Rusi” – 2,700 TMT. The leader in terms of crushing capacity is the holding “Yug Rusi”

with nine plants in several different Russian provinces, mostly in the Central FD and in

Krasnodar Kray;

- “Sodrugestvo” – 2,688 TMT. “Sodruzhestvo,” is the largest processor of soybeans. In 2015/16,

three Sodruzhestvo plants processed 2.27 MMT of soybeans and 0.267 MMT of rapeseed. (One

facility crushed 0.62 MMT of soybeans a year, the second crushed 0.5 MMT of soybeans and

0.369 MMT of rapeseed a year, and the third crushed 1.67 MMT of soybeans a year. In

2015/2016 and in the first half of MY 2016/17, the plants worked at almost 100 percent capacity.

Sodruzhestvo’s oilseeds raw materials sourced domestically are seven percent for soybeans and

85 percent of rapeseed;

- “Efko” – 1,900 TMT capacity of all plants, of which 0.825 MMT are produced at plants that are

owned by Efko, including a sunflowerseed curshing facility in Belgorod (0.61 MMT a year) and

a sunflowerseed and rapeseed crushing facility in Taman (Krasnodar Kray) that can process

214,500 MT of sunflowerseed and rapeseed per year, mostly for export. Additionally, the Efko

company has developed a strategic business on processing with the “Alekseevskiy” soy complex,

the biggest soybean crusher in the Central FD with a capacity of 0.66 MMT per year;

- “Solnechnye Produkty” holding (in the group Bukyet) – 1,400 TMT a year. Solnechnye

Produkty’s crushing capacity is split between two enterprises in Saratov Oblast and one in

Krasnodar Kray;

- “Kazan Oils and Fats Combine” – 1,000 TMT capacity for crushing rapeseed and sunflowerseed.

Kazan Oils and Fats Comgine produces approximately 0.45 MMT vegetable oil and

approximately 380,000 of meal;

- “Sigma” holding company – 760 TMT. “Sigma” has two plants in Bashkortostan – one

modernized plans will process 345 TMT a year and another new plant will start working at full

capacity of 415 TMT in 2017;

- “Aston” – 750 TMT, located in Rostov oblast;

- “Nizhegorodskiy MEZ” – 600 TMT. Nizhegorodskiy MEZ’s crushing is split between two

plants, one in Orenburg Oblast and one in Volgograd Oblast;

9 Source: IKAR

10 http://www.efko.ru/press-centr/smi/10755/

11 http://www.efko.ru/press-centr/smi/10755/

20

- “Bunge, CIS”, in Voronezh Oblast – process 560 TMT of sunflowerseed per year; and

- “RusAgro Group” – 547 TMT. Rusagro has two oilseeds crushing enterprises: 410 TMT a year

of sunflowerseed in Samara Oblast and 137 TMT of soybeans a year in Primorskiy Kray

(Russian Far East)/

Some industry analysts consider that the rapid growth of crushing capacity in some provinces stimulated

production of oilseeds in Russia. Thus, according to some industry analysts, from 2015 through 2016

production of sunflowerseed increased in Belgorod Oblast from 157 TMT to 321 TMT, and production

of soybeans from 78 TMT to 320 TMT. This increase is primarily due to the development of two Yug

Rusi sunflowerseed crushing plants, one soybean complex and Efko’s sunflowerseed crushing plant.

In MY 2017/18, industry analysts forecast that two other plants (Cargill in Volgograd Oblast and plant

owned by the company Chernozemye” in Lipetsk Oblast) may increase Russia’s crushing capacity by

another 1 MT.

Industry analysts, consider that the margins are higher in those companies, which invest/contract

production of sunflowerseed, although this situation is not typical for oilseed crushing companies in

other countries.

Food Use Consumption:

Oilseed market analysts report that consumers’ interest in confectionary–type sunflowerseed and in

sunflowerseed with high oleic content is increasing. However, there are no data on production and

consumption of these products, and the share of confectionary type of sunflowerseed is less than one

percent of sunflowerseed production.

According to industry analysts, production of highly oleic sunflowerseed (with high content of Omega 3

acid) is also not significant, and area sown to this type of sunflowerseed is less than one percent of

sunflowerseed area. Crushers’ demand for this sunflowerseed is small because Russian consumers still

cannot afford to pay bonus prices for high oleic oil. Russian consumer interest in “healthy food”

increased in 2013-2014. However, in the last two years, along with the decline of average incomes of

Russian consumers, preferences have reverted to lower priced vegetable oil from “healthy” vegetable

oil.

Feed, Seed, Waste Consumption:

Livestock and poultry producers increased consumption of semi- and whole fat oilseeds in feeds.

However, there are no official data on such consumption.

Soybeans

According to Russian officials12

, Russia still does not produce enough soybeans to meet the demand of

the livestock and poultry industries, and up to 43% of soybeans are imported.13

Development of the

Russian poultry and livestock industries still depends, to a large extent, on imported protein ingredients,

vitamins, and additives. Soybean meal comprises a significant portion of protein feeds. According to

industry sources, in production of broilers, feeds comprise 70 percent of the cost of production.

12

Reports at the “Where the Margin Is” conference 13

http://kvedomosti.ru/news/rossiya-importiruet-43-soi.html

21

Soybean meal comprises approximately 20 percent of the volume of feeds for broilers, but in terms of

value, according to the Vice President of the International Program of Development of Poultry

Production,14

the value of soybean meal is equal to the value of the other 80 percent of feeds. Thus,

soybean meal accounts for approximately 35 percent of the cost of production of broilers.

Global production and supply of soybeans has been growing during the last five years, and despite the

strong and growing global demand, soybean prices in U.S. Dollars, have been stable. However, Ruble

volatility in 2014-2016 increased the cost of imported soybeans and soybean meal, which may result in

an increased cost of broiler production, which might not be balanced by the decreasing prices for the

grain component of feeds.

Trade:

Russian trade in oilseeds in MY 2017/18 will be influenced by several factors:

- Domestic production of oilseeds. Crushing capacity in Russia already exceeds oilseeds

production. Given that the high domestic demand for oilseeds is based on demand of large agro-

holding companies, crushers and feed consumers, domestic demand will prevail over other

factors that stimulate exports of raw oilseeds.

- Decreased export duties on sunflowerseed, rapeseed and zero export duty on soybeans could

stimulate exports of these oilseeds;

- Volatility of Russian Ruble. In MYs 2015/16 and the first half of MY 2016/17, Ruble volatility

was a very important factor that significantly influenced trade: a weak Ruble increases the

incentive to export seeds, while a stronger Ruble increases incentives to sell seeds domestically.

However, there is no direct correlation: the domestic demand for vegetable oil has almost

reached the ceiling (see Oils section), and crushers are trying to increase exports of vegetable oil.

A weak Ruble facilitates this goal. In the beginning of CY 2017, the Russian Ruble has

stabilized. There are economic symptoms that indicate that this stability may last through the

end of MY 2016/17, and possibly into MY 2017/18; and

- Increased domestic competition for oilseeds. In order to keep their margins high, domestic

crushers, wherever possible, try to decrease their purchase prices for sunflowerseed. In turn,

farmers try to increase their sales of sunflowerseed directly to exporters.

Thus, incentives for exports of sunflowerseed and rapeseed will not be high. However, given the

decreased export duties on sunflowerseed and rapeseed, exports may grow slightly. Exports of soybeans

from the Far East will continue to increase because of high demand from China. Moreover, crushing

capacity in the Russian Far East is still lower than production, and new facilities in Amur Oblast and in

Primorskiy Kray may not start working at full capacity in MY 2017/18.

FAS/Moscow forecasts Russia’s total exports of the three major oilseeds at 0.67 MMT, 20 percent up y-

o-y, and these exports will include 0.2 MMT of sunflowerseed and 0.4 MMT of soybeans. Russia will

also continue exports of niche crops, such as oil flax, Camelina and safflower, and exports of these crops

may add another 0.6-0.7 MMT to Russia’s oilseeds exports in MY 2017/18. Imports of oilseeds is

forecast to grow by 0.1 MMT to 2.36 MMT due to the forecast restoration of soybean imports from

estimated 2.0 MMT in MY 2016/17 to 2.1 MMT in MY 2017/18.

14

http://kvedomosti.ru/news/rossiya-importiruet-43-soi.html

22

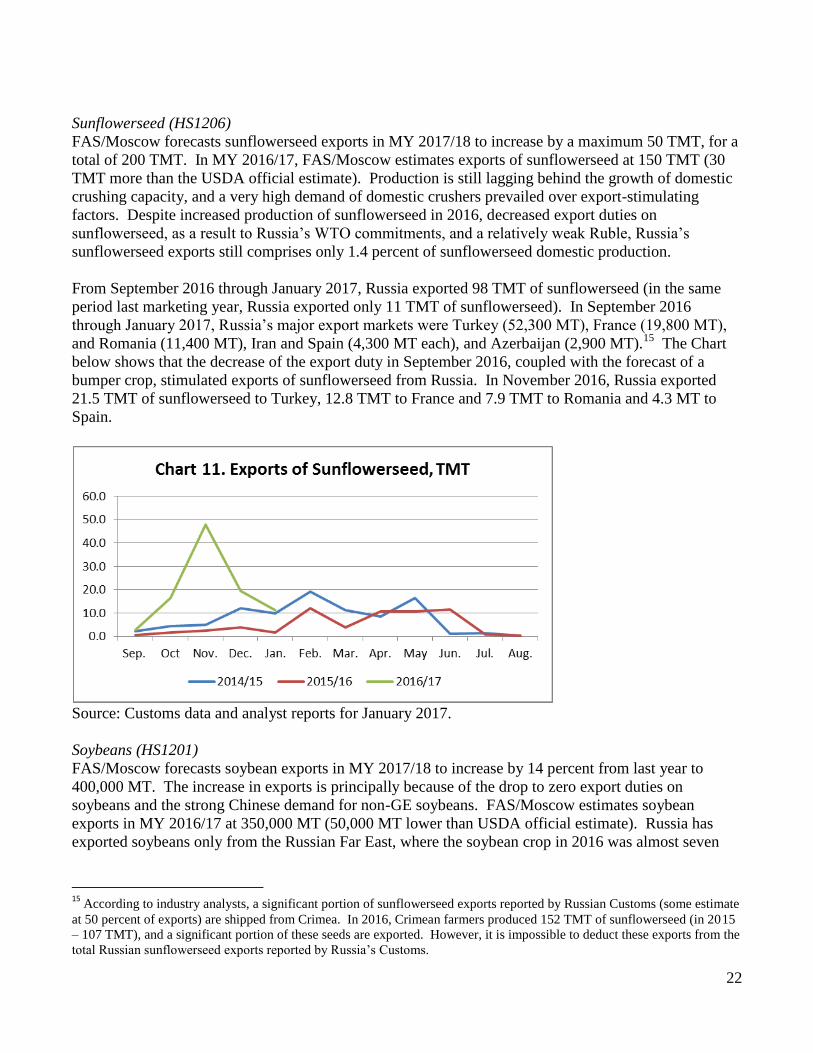

Sunflowerseed (HS1206)

FAS/Moscow forecasts sunflowerseed exports in MY 2017/18 to increase by a maximum 50 TMT, for a

total of 200 TMT. In MY 2016/17, FAS/Moscow estimates exports of sunflowerseed at 150 TMT (30

TMT more than the USDA official estimate). Production is still lagging behind the growth of domestic

crushing capacity, and a very high demand of domestic crushers prevailed over export-stimulating

factors. Despite increased production of sunflowerseed in 2016, decreased export duties on

sunflowerseed, as a result to Russia’s WTO commitments, and a relatively weak Ruble, Russia’s

sunflowerseed exports still comprises only 1.4 percent of sunflowerseed domestic production.

From September 2016 through January 2017, Russia exported 98 TMT of sunflowerseed (in the same

period last marketing year, Russia exported only 11 TMT of sunflowerseed). In September 2016

through January 2017, Russia’s major export markets were Turkey (52,300 MT), France (19,800 MT),

and Romania (11,400 MT), Iran and Spain (4,300 MT each), and Azerbaijan (2,900 MT).15

The Chart

below shows that the decrease of the export duty in September 2016, coupled with the forecast of a

bumper crop, stimulated exports of sunflowerseed from Russia. In November 2016, Russia exported

21.5 TMT of sunflowerseed to Turkey, 12.8 TMT to France and 7.9 TMT to Romania and 4.3 MT to

Spain.

Source: Customs data and analyst reports for January 2017.

Soybeans (HS1201)

FAS/Moscow forecasts soybean exports in MY 2017/18 to increase by 14 percent from last year to

400,000 MT. The increase in exports is principally because of the drop to zero export duties on

soybeans and the strong Chinese demand for non-GE soybeans. FAS/Moscow estimates soybean

exports in MY 2016/17 at 350,000 MT (50,000 MT lower than USDA official estimate). Russia has

exported soybeans only from the Russian Far East, where the soybean crop in 2016 was almost seven

15

According to industry analysts, a significant portion of sunflowerseed exports reported by Russian Customs (some estimate

at 50 percent of exports) are shipped from Crimea. In 2016, Crimean farmers produced 152 TMT of sunflowerseed (in 2015

– 107 TMT), and a significant portion of these seeds are exported. However, it is impossible to deduct these exports from the

total Russian sunflowerseed exports reported by Russia’s Customs.

23

percent lower y-o-y. Moreover, Russia has increased crush capacity in the Far East, and domestic

demand for soybeans there increased.

From September 2016 through January 2017, Russia exported 147,000 MT of soybeans compared with

208,100 MT in the same period y-o-y. In marketing year 2015/16, Russia exported 97 percent of

soybeans to China. In the first five months of MT 2016/17 Russia’s exports to China comprised only 84

percent (124,000 TMT), 10,000 MT were exported to the U.S., 8,900 MT were shipped to Iran, 2,100

MT were shipped to Azerbaijan, and 1,000 MT were shipped to South Korea. Small shipments to

several other countries account for the remaining 1,000 MT. Russia has not cultivated GE crops before

2016, and in mid-2016 cultivation of GE crops was officially banned. Thus, soybeans of Russian origin

are non-GE.

Domestic demand for soybeans remains strong due to stable demand from the poultry and swine

industries and a growth in domestic soybean crushing facilities. This demand is filled primarily by

soybeans that are produced in European Russia and by imported soybeans. Delivery of soybeans from

the Far East to European Russia, where Russian poultry and livestock industries are concentrated, is too

expensive. A good soybean crop in European Russia, stabilization (no increase) of development in the

Russian poultry and swine industries, trend in large livestock and poultry agro-holdings to increase

production of their own feeds, a big feed grains crop in 2016, coupled with the weak Ruble in the first

half of 2016/17 have created natural grounds for a slowdown in imports of soybeans in MY 2016/17.

SPS protective measures by the Russian authorities16

and strengthened control over imported GE crops,

specifically soybeans, also played an important role in curbing soybean imports to Russia in MY

2016/17. For these reasons, FAS/Moscow lowered its estimate of soybean imports in MY 2016/17 to

2.0 MMT compared with the official USDA estimate at 2.1 MMT, and forecast only a small increase in

imports to 2.1 MMT in MY 2017/18.

From September 2016 through January 2017, Russia imported 864.4 TMT17

of soybeans, including

435.4 TMT from Paraguay, 274.2 TMT from Brazil, 78.5 TMT from Croatia, 29.8 TMT from Canada,

and the other approximately 46.5 MMT were imported primarily from Argentina and Uruguay.18

Soybean imports from the U.S. have been banned since March 2016.

16

Russia Restricts Imports of US Corn and Soybeans_2-17-2016.pdf 17

Estimate of imports of soybeans is based on data from GTA in September – December 2016 and data from industry sources

for January 2017. 18

GTA and analysts’ statistical data on imports of soybeans from Argentina and Uruguay differ. Thus, GTA reports of

imports from Argentina, and does not report on imports from Uruguay, while analysts report on imports from Uruguay and

do not report on imports from Argentina.

24

Source: Customs data and analyst reports for January 2017.

Rapeseed (HS1205)

FAS/Moscow estimates exports of rapeseed in MY 2016/17 at 60 TMT. From July 2016 through

January 2017, Russia exported only 56.4 TMT of rapeseed. The main destinations were China (22.2

TMT) and Mongolia (8.4 TMT). Exports to Latvia, Germany, Lithuania and several other countries in

these months were less than 2 TMT each. At the same time Russia imported 53.2 TMT of rapeseed,

primarily from Kazakhstan. Russia also exported almost 140 TMT of rapeseed oil. Thus, the low

export duty did not appear to influence exports. Domestic crushing capacity continues to grow, and

exports of rapeseed oil are forecast to grow faster than exports of seed. FAS/Moscow forecasts exports

of rapeseed in MY 2017/18 at 70 TMT, due to increased production.

Linseed Crops for Oil (Crown Flax, Camelina) and Safflower (HS numbers 1204 and 1207)

Exports of linseed crops for oil were fanned in 2015/16 and 206/17 by the devaluation of the Ruble and

zero export duties on these niche crops. In 2016/17, traders continued developing foreign markets for

these crops, and exports of these crops in July 2016 through January 2017 reached 578 TMT (compared

with 420 TMT in the same period y-o-y). FAS/Moscow estimates exports of these crops in MY 2016/17

at over 850 TMT. Thus, exports of niche crops are much bigger than exports of both sunflowerseed and

rapeseed. Most of these niche crops are exported to Turkey, and to various EU countries, such as

Belgium, Latvia, and Poland. In MY 2016/17, Russia also started exporting these niche crops to China

and Vietnam.

25

Source: FAS/Moscow based on Customs and Rosstat data.

Peanuts

FAS/Moscow forecasts that imports of peanuts will remain at the same level in MY 2017/18 as in MY

2016/17 – 140 TMT. FAS/Moscow estimates peanut imports in MY 2016/17, 15 TMT lower than the

official USDA estimate.

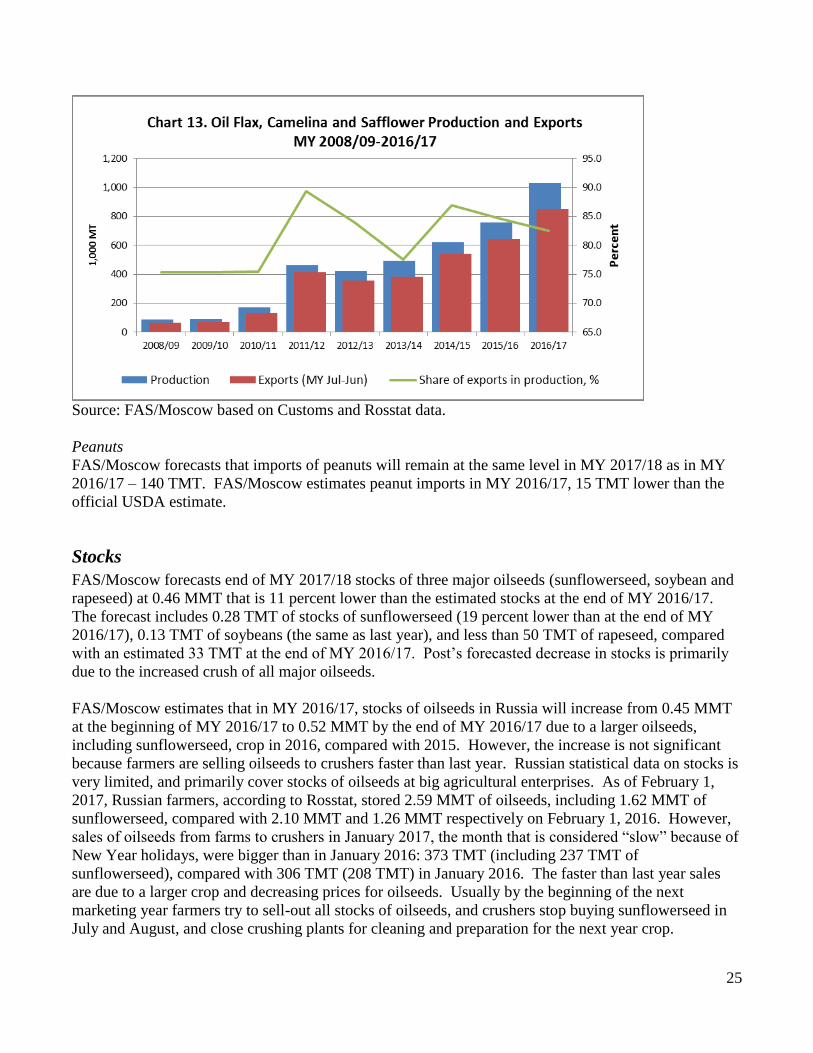

Stocks

FAS/Moscow forecasts end of MY 2017/18 stocks of three major oilseeds (sunflowerseed, soybean and

rapeseed) at 0.46 MMT that is 11 percent lower than the estimated stocks at the end of MY 2016/17.

The forecast includes 0.28 TMT of stocks of sunflowerseed (19 percent lower than at the end of MY

2016/17), 0.13 TMT of soybeans (the same as last year), and less than 50 TMT of rapeseed, compared

with an estimated 33 TMT at the end of MY 2016/17. Post’s forecasted decrease in stocks is primarily

due to the increased crush of all major oilseeds.

FAS/Moscow estimates that in MY 2016/17, stocks of oilseeds in Russia will increase from 0.45 MMT

at the beginning of MY 2016/17 to 0.52 MMT by the end of MY 2016/17 due to a larger oilseeds,

including sunflowerseed, crop in 2016, compared with 2015. However, the increase is not significant

because farmers are selling oilseeds to crushers faster than last year. Russian statistical data on stocks is

very limited, and primarily cover stocks of oilseeds at big agricultural enterprises. As of February 1,

2017, Russian farmers, according to Rosstat, stored 2.59 MMT of oilseeds, including 1.62 MMT of

sunflowerseed, compared with 2.10 MMT and 1.26 MMT respectively on February 1, 2016. However,

sales of oilseeds from farms to crushers in January 2017, the month that is considered “slow” because of

New Year holidays, were bigger than in January 2016: 373 TMT (including 237 TMT of

sunflowerseed), compared with 306 TMT (208 TMT) in January 2016. The faster than last year sales

are due to a larger crop and decreasing prices for oilseeds. Usually by the beginning of the next

marketing year farmers try to sell-out all stocks of oilseeds, and crushers stop buying sunflowerseed in

July and August, and close crushing plants for cleaning and preparation for the next year crop.

26

Policy

Russia’s WTO commitments (eliminating or decreasing export duties on oilseeds) have been gradually

implemented after the first year of Russia’s WTO membership (August 2012). The table below shows

the final export duties at the end of the transition period and export duties as of March 2017, the fourth

year of implementation of WTO commitments (Table 7). FAS/Moscow reported on the last changes to

export duties of sunflowerseed in a GAIN report.19

Table 7. Russia’s WTO Commitments:

HS

No

Name of

Product

Export

duty

before

WTO

accessi

on

Target

export

duty

Transition

al Period

Export

duty

from

Septemb

er 2013

through

August

2014

Export

duty

from

Septemb

er 2014

through

August

2015

Export

duty

beginnin

g

Septemb

er 2015

Export

duty

beginnin

g

Septemb

er 2016

120

1

Soybean 20

percent,

but not

less

than 35

Euro

per 1

MT

0 3 years 13.33

percent,

but not

less than

23.33

Euro per

1 MT

6.67

percent,

but not

less than

11.67

Euro per

1 MT

0 None

120

5

Rapeseed 20

percent,

but not

less

than 35

Euro

per 1

MT

6.5

percen

t, but

not

less

than

11.4

Euro

per 1

MT

3 years 15

percent,

but not

less than

27.13

Euro per

1 MT

11

percent,

but not

less than

19.26

Euro per

1 MT

6.5

percent,

but not

less than

11.4

Euro per

1 MT

6.5

percent,

but not

less than

11.4

Euro per

1 MT

120

6

Sunflowerse

ed

20

percent,

but not

less

than 30

Euro

per 1

MT

6.5

percen

t, but

not

less

than

9.75

Euro

per 1

MT

4 years 16.62

percent,

but not

less than

24.94

Euro per

1 MT

13.24

percent,

but not

less than

19.88

Euro per

1 MT

9.88

percent,

but not

less than

14.81

Euro per

1 MT

6.5

percent,

but not

less than

9.75

Euro per

1 MT

19

Russian Agricultural Policy and Situation Bi-Weekly Update_9-16-2016.pdf

27

120

7

50

Mustard

seed

10

percent,

but not

less

than 25

Euro

per 1

MT

0 1 year 0 None None None

Source: Russian Customs

Russia supports programs of selection and breeding of planting seeds of sunflowerseed and soybeans

(see section Planting Seeds, above). These subsidies are relatively small, and the results are not

expected in MY 2017/18.

Marketing

Prices of major oilseeds in MY 2016/17 are influenced by four factors: volume of production, crushers

demand, export demand and Ruble exchange rate. Sunflowerseed prices in Rubles have been declining

due to the bumper crop. By March 10, 2017 prices had declined nearly 30 percent (in Rubles) from July

2017 prices. Rapeseed prices were more stable, and were supported by lower than last year crop. By

March 10, 2017, rapeseed prices even increased by three percent from the beginning of July 2016.

Soybean prices peaked in August 2016 and then declined as sharply as they had peaked, to the level of

May 2016. Since that sharp decline, they have continued declining at a slow pace. By March 3, 2017,

the level of soybean prices in the domestic market was 16 percent lower than in July 2016. The peak in

soybean prices in August was caused by both uncertainty about the soybean crop in European Russia

and the VPSS’s measures that threatened to curb imports of soybeans. A good soybean crop in

European Russia, coupled with Russia’s bumper crop of feed quality grain, and continuation of imports

of soybeans, have stabilized and then decreased soybean prices. However, according to industry

analysts, domestic production of all oilseeds still remains profitable despite the decreased prices due to

the following factors:

- Increased Russian crushing capacity has increased domestic demand for raw materials;

- The step-by-step decrease in export duties on sunflowerseed, rapeseed and zero export duty on

soybeans (Table 7), along with the weak Ruble in MY 2015/16 created incentives for exports of

oilseeds from Russia.

In fall 2016, the Ruble exchange rate stabilized, and this lowered the incentive to export oilseeds. It also

contributed to a decline in the domestic prices for oilseeds. According to industry analysts, the margin

of oilseed producers decreased in MY 2016/17, but this margin is still higher than the margins seen in

grain production, and still favors oilseed producers. According to analysis of IKAR, the “net margin”

(in Rubles per hectare) from the production of sunflowerseed in the South of European Russia decreased

from approximately 42,000 Rubles ($656) per hectare in MY 2015/16 to approximately 32,000 Rubles

($500) per hectare in MY 2016/17. However, this margin was still higher than the margin from

production of wheat, barley and corn in the South. In Central European Russia the margin from

production of sunflowerseed also decreased y-o-y, but was higher than the margin from production of all

other crops, such as wheat, barley, corn, soybeans, and sugar beets. The net margin: from production of

soybeans in the South was almost the same as last year, approximately 19,000 Rubles ($267) per

28

hectare, and was the third lowest margin (only margins from production of barley and corn were lower).

In Central European Russia the margin from production of soybeans was over 31,000 Rubles, higher

than in 2015/16, and soybeans were the second most profitable crop after sunflowerseed in this region20

.

On the other hand, for processors, stable procurement prices along with the decreasing demand for

vegetable oils in the foreign markets, and decreasing prices for these products both in Rubles and in U.S.

Dollars, will decrease processors’ returns.

Source: ProZerno

20

Source: Presentation of IKAR at the Conference “Where the Margin Is” in February 2017:

http://www.ikar.ru/lenta/603.html

29

Source: ProZerno

Source: ProZerno

30

Source: ProZerno

PSD Tables for Oilseeds

Oilseed, Sunflowerseed 2015/2016 2016/2017 2017/2018 Market Begin Year Sep 2015 Sep 2016 Sep 2017

Russia USDA Official New Post USDA Official New Post USDA Official New Post

Area Planted 0 6921 0 7481 0 7400

Area Harvested 6454 6454 6962 7191 0 7150

Beginning Stocks 135 135 255 255 0 353

Production 9173 9173 10536 10858 0 11000

MY Imports 121 121 50 50 0 50

MY Imp. from U.S. 0 0 0 0 0 0

MY Imp. from EU 0 0 0 0 0 0

Total Supply 9429 9429 10841 11163 0 11403

MY Exports 104 104 120 150 0 200

MY Exp. to EU 10 10 10 10 0 10

Crush 8550 8550 9850 10100 0 10400

Food Use Dom. Cons. 220 220 220 220 0 220

Feed Waste Dom. Cons. 300 300 300 340 0 300

Total Dom. Cons. 9070 9070 10370 10660 0 10920

Ending Stocks 255 255 351 353 0 283

Total Distribution 9429 9429 10841 11163 0 11403

(1000 HA) ,(1000 MT)

Oilseed, Soybean 2015/2016 2016/2017 2017/2018 Market Begin Year Sep 2015 Sep 2016 Sep 2017

Russia USDA Official New Post USDA Official New Post USDA Official New Post

Area Planted 2000 2000 2200 2228 0 2300

Area Harvested 2082 2082 2094 2118 0 2200

Beginning Stocks 109 109 146 146 0 131

31

Production 2707 2707 3099 3135 0 3200

MY Imports 2336 2336 2100 2000 0 2100

MY Imp. from U.S. 486 350 300 0 0 300

MY Imp. from EU 0 0 0 0 0 0

Total Supply 5152 5152 5345 5281 0 5431

MY Exports 456 456 400 350 0 400

MY Exp. to EU 0 0 0 0 0 0

Crush 4050 4050 4300 4300 0 4350

Food Use Dom. Cons. 0 0 0 0 0 0

Feed Waste Dom. Cons. 500 500 500 500 0 550

Total Dom. Cons. 4550 4550 4800 4800 0 4900

Ending Stocks 146 146 145 131 0 131

Total Distribution 5152 5152 5345 5281 0 5431

(1000 HA) ,(1000 MT)

Oilseed, Rapeseed 2015/2016 2016/2017 2017/2018 Market Begin Year Jul 2015 Jul 2016 Jul 2017

Russia USDA Official New Post USDA Official New Post USDA Official New Post

Area Planted 925 925 950 978 0 1000

Area Harvested 897 897 915 898 0 910

Beginning Stocks 57 57 51 51 0 33

Production 1001 1001 997 997 0 1100

MY Imports 40 40 70 60 0 60

MY Imp. from U.S. 0 0 0 0 0 0

MY Imp. from EU 3 3 0 0 0 0

Total Supply 1098 1098 1118 1108 0 1193

MY Exports 32 32 50 60 0 70

MY Exp. to EU 5 5 5 5 0 5

Crush 990 990 990 990 0 1050

Food Use Dom. Cons. 0 0 0 0 0 0

Feed Waste Dom. Cons. 25 25 25 25 0 25

Total Dom. Cons. 1015 1015 1015 1015 0 1075

Ending Stocks 51 51 53 33 0 48

Total Distribution 1098 1098 1118 1108 0 1193

(1000 HA) ,(1000 MT)

Oilseed, Peanut 2015/2016 2016/2017 2017/2018 Market Begin Year Oct 2015 Oct 2016 Oct 2017

Russia USDA Official New Post USDA Official New Post USDA Official New Post

Area Planted 0 0 0 0 0 0

Area Harvested 0 0 0 0 0 0

Beginning Stocks 4 4 5 5 0 5

Production 0 0 0 0 0 0

MY Imports 156 156 160 140 0 145

MY Imp. from U.S. 2 2 2 2 0 0

MY Imp. from EU 0 0 0 0 0 0

Total Supply 160 160 165 145 0 150

MY Exports 0 0 0 0 0 0

MY Exp. to EU 0 0 0 0 0 0

Crush 0 0 0 0 0 0

Food Use Dom. Cons. 155 155 160 140 0 145

Feed Waste Dom. Cons. 0 0 0 0 0 0

Total Dom. Cons. 155 155 160 140 0 145

Ending Stocks 5 5 5 5 0 5

Total Distribution 160 160 165 145 0 150

32

(1000 HA) ,(1000 MT)

MEALS - Meal, Sunflowerseed

- Meal, Soybean

- Meal, Rapeseed

- Meal, fish

Production

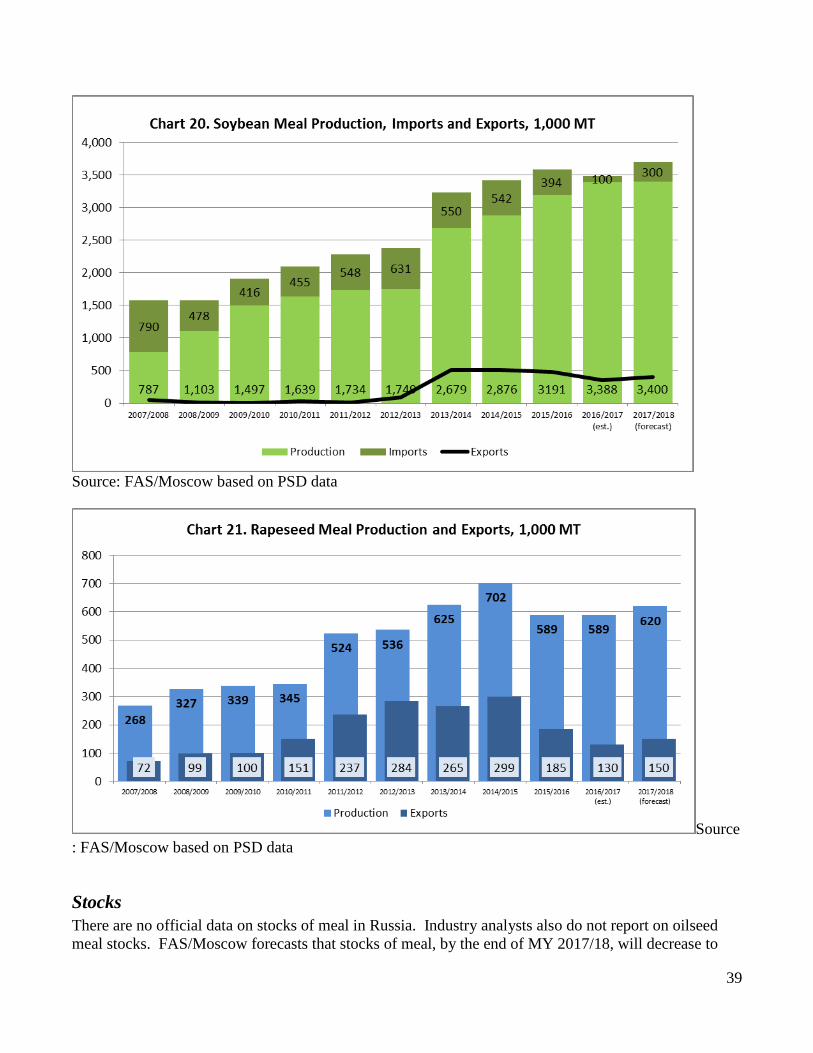

FAS/Moscow forecasts total crush of the three major oilseed crops at 15.8 MMT in MY 2017/18, which

is a 2.7 percent increase from the estimated 15.39 MMT in MY 2016/17. The factors that will motivate

the further increase (although slow) in the crushing and production of meal are the following:

- Crushing capacity in Russia continues to increase (see Consumption paragraphs in the OILSEED

sector of the report);

- Domestic demand in protein feeds remains strong; and

- Problems with imports of soybean meal may continue in MY 2017/18.

FAS/Moscow’s forecast for MY 2017/18 includes crush of 10.4 MMT for sunflowerseed (10.1 MMT in

MY 2016/17), 4.35 MMT for soybeans (4.3 MMT in MY 2016/17), and 1.05 MMT for rapeseed (0.99

MMT in MY 2016/17). Russia’s total domestic production of the three major oilseed meals will

increase to 8.29 MMT in MY 2017/18 (estimate for MY 2016/17 is 8.13 MMT), including 4.27 MMT

of sunflowerseed meal (4.15 MMT in MY 2016/17), 3.4 MMT of soybean meal (3.39 MMT in MY

2016/17), and 0.62 MMT of rapeseed meal (0.59 MMT in MY 2016/17).

Table 8. Russia: Consolidated PSD Forecast for Major Meals for MY 2017/18, TMT

POST MY 2017/18 Sunflowerseed Soybean Rapeseed Fish Meal TOTAL

Crush 10,400 4,350 1,050 570 16,370

Extr. Rate, 999.9999 0.411 0.782 0.591 0.263

Beginning Stocks 294 65 10 4 373

Production 4,270 3,400 620 150 8,440

MY Imports 5 300 10 20 335

MY Imp. from U.S. 0 10 0 0 10

MY Imp. from EU 5 150 0 0 155

Total Supply 4,569 3,765 640 174 9,148

MY Exports 1,700 400 150 50 2,300

MY Exp. to EU 800 100 150 0 1,050

Industrial Dom. Cons. 0 0 0 0 0

Food Use Dom. Cons. 0 0 0 0 0

Feed Waste Dom. Cons. 2,600 3,300 480 120 6,500

Total Dom. Cons. 2,600 3,300 480 120 6,500

Ending Stocks 269 65 10 4 348

33

Total Distribution 4,569 3,765 640 174 9,148

Note: The above table is composed of PSD forecast for each meal despite differing marketing years.

Russia produces and trades fish meal as well, although Russia’s production of fish meal is small.

FAS/Moscow estimates domestic production of fish meal in MY 2016/17 at 145,000 MT, imports at

20,000 MT, and exports at 55,000 MT. These estimates are the same as USDA’s estimates. Fish meal

production, imports and exports have been stagnating over the last several years. There are almost no

reliable statists on production of fish meal in Russia. The demand in fish meal has been growing in

Russia along with attempts to develop the domestic aquaculture industry based on feeding fish meal.

However, statistical data on fish catch and exports are not reliable, because significant volumes of fish

are shipped abroad and are not reported. Thus, FAS/Moscow forecasts a slight increase in production of

fish meal in MY 2017/18 to 150,000 MT. Imports are forecast to remain the same as in MY 2016/17,

while exports are forecast to increase to 60,000 MT.

Feed Consumption

FAS/Moscow forecasts Feed Waste Domestic Consumption of oilseed meals at 6.38 MMT in MY

2017/18, compared to the FAS/Moscow estimate of 6.14 MMT in MY 2016/17, and USDA’s estimate

of oilseed meal consumption in MY 2016/17 at 6.32 MMT. The difference between the Post estimate

and the USDA estimate is due to the adjustment to the imports of soybean meal. FAS/Moscow’s

estimates of soybean meal imports are based on Customs data for the period from September 2016 to

January 2017, and estimates for the MY 2016/17 are 100,000 MT compared with the USDA’s estimate

of 450,000 MT.

Chart 18 shows the change in the domestic consumption of major meals in Russia in the last ten years

and the forecast for MY 2017/18. The data are in actual volumes for different meals.

34

Source

: FAS/Moscow based on PSD data

Table 9 presents the aggregated view on feed consumption in Russia in MY 2015/16, MY 2016/17

(estimate) and forecast for MY 2017/18 in soybean meal equivalent (SME). The estimates and forecasts

are based on the assumption that Feed Domestic Consumption category equals the Feed Waste Domestic

Consumption. Data for grains consumption (Feed and Residual) are for marketing years 2015/16 and

2016/17, because FAS/Moscow’s forecast for grains for MY 2017/17 will be available only in April

2017.

Table 9. Russia: Domestic Feeds Consumption in MYs 2015/16, 2016/17, and Forecast for 2017/18,

TMT, Actual and in Soybean Meal Equivalent Feeds Domestic Consumption (actual) Feeds Domestic

Consumption in SME

MY

2015/16

MY

2016/

17

(est)

MY

2017/18

(forecast)

MY

2015

/16

MY

2016

/17

(est)

MY

2017/

18

(forec

ast)

Soybe

an

Meal

Conve

rsion

Factor

Meals

Sunflowersee

d Meal

2,250 2,510 2,600 2,12

4

2,37

0

2,455 0.944

2

Soybean

Meal

3,150 3,150 3,300 3,15

0

3,15

0

3,300 1.000

0

Rapeseed

Meal

420 480 480 299 342 342 0.711

5

35

Fish Meal 90 110 120 130 159 173 1.445

0

TOTAL 5,70

3

6,02

0

6,270

Seeds

Sunflowerse

ed

300 340 300 156 177 156 0.519

3

Soybeans 500 500 550 400 400 440 0.800

0

Rapeseed 25 25 25 10 10 10 0.409

1

TOTAL 566 587 606

Grain

Corn 7,800 8,100 1,28

4

1,33

3

0.164

6

Wheat 14,00

0

16,00

0

3,17

9

3,63

4

0.227

1

Barley 8,900 9,200 2,13

2

2,20

4

0.239

6

Rye 225 300 56 75 0.250

0

Oats 3,000 3,050 875 890 0.291

7

Millet 320 330 73 76 0.229

2

TOTAL 7,60

0

8,21

2

FAS/Moscow estimates that consumption of meal in SME in Russia increased in MY 2016/17, and

forecasts that this consumption will continue growing in 2017/18. Consumption of grain, as a source of

energy also increased. However, there are no official data on the balance between protein meal and

energy in feeding different types of animal and livestock. According to the recent FAS/Moscow report

on poultry production,21

on average, Russian poultry producers in 2015 and 2016 increased the portion

of grain in mixed feeds. However, leaders in the poultry industry continue using feeds according to the

best feeding practices, but most of them have their own feed mills and produce feeds from raw materials

that they grow themselves. According to Rosstat, 14 MMT of compound feeds were produced

specifically for the poultry industry in 2015, and the lion’s share, approximately 10 MMT, were

produced by companies from the list of the top 20 broiler producers.

There are no official data on the average composition of feeds for different industries. In 2016,

development of the poultry industry slowed and consumer demand for poultry stabilized. For some

poultry producers, the price of ingredients became the major factor in choosing feeding formulas. In

MY 2015/16 and 2016/17, the supply of fodder grains increased and prices decreased. However, the

21

https://gain.fas.usda.gov/Recent%20GAIN%20Publications/Poultry%20and%20Products%20Semi-

annual_Moscow_Russian%20Federation_2-16-2017.pdf

36

expenses for other ingredients, such as soy, vitamins and minerals, as well as the cost of production of

compound feeds may increase in MY 2017/18, and poultry producers may continue using more grain in

feeds than required by optimal feeding formulas.

Some big Russian meat companies that have poultry, swine and cattle operations support development

of domestic production of feed ingredients. Thus, two lysine plants were recently opened in Belgorod22

and in Volgograd.23

The two new plants have enough capacity to cover the needs of the whole broiler

industry.24

According to industry contacts however, problems with the quality of lysine from one of the

new plants reportedly hurt the performance of its clients in the first half of 2016. Regardless of this

hurdle, if production costs of compound feeds grow due to prices of imported ingredients, the

expectation for 2017 is that low prices for local grain, oilseeds and other ingredients can improve

margins for some poultry producers.

The absence of highly efficient competitors in the market allows local companies to maintain a

relatively high ratio of low priced domestic forage grains in feeds, even at the expense of operational

efficiency. The average feed conversion ratio (FCR), 1.85-1.87,25

allows the domestic industry to win

market share over current importers. As internal competition becomes more intensive, broiler

companies that have a feed production component in their business structure (so called “vertically