Q2 Special Guest Contributor: David Arthur, Brookfield Asset Management

The Preqin Quarterly Update

Insight on the quarter from the leading provider of alternative assets data

alternative assets. intelligent data.

Private Equity

Plus, Special Guest Contributor: Clay Deniger, Capstone Partners

Q2 2013 JULY 2013

Content Includes....

FundraisingWe review the latest fundraising figures, including funds which exceeded their target size and the largest funds closed in the

quarter.

InvestorsWe look at investor appetite for private equity and the challenges investors are currently facing.

Buyout DealsWe analyze private equity buyout deals and exits in Q2 2013 and look at the largest deals in the quarter.

Venture Capital DealsWe examine venture capital deal activity in Q2 2013 by value, region and stage.

PerformanceWe provide the latest private equity performance data, including dry powder figures, IRRs and the PrEQIn Private Equity Quarterly Index.

SecondariesWe take a look at which institutions are looking to buy and sell fund interests on the secondary market.

2

The Preqin Quarterly Update: Private Equity, Q2 2013

© 2013 Preqin Ltd. / www.preqin.com

Download the data pack at:www.preqin.com/quarterlyupdate

All rights reserved. The entire contents of The Preqin Quarterly Update: Private Equity, Q2 2013 are the Copyright of Preqin Ltd. No part of this publication or any information contained in it may be copied, transmitted by any electronic means, or stored in any electronic or other data storage medium, or printed or published in any document, report or publication, without the express prior written approval of Preqin Ltd. The information presented in The Preqin Quarterly Update: Private Equity, Q2 2013 is for information purposes only and does not constitute and should not be construed as a solicitation or other offer, or recommendation to acquire or dispose of any investment or to engage in any other transaction, or as advice of any nature whatsoever. If the reader seeks advice rather than information then he should seek an independent fi nancial advisor and hereby agrees that he will not hold Preqin Ltd. responsible in law or equity for any decisions of whatever nature the reader makes or refrains from making following its use of The Preqin Quarterly Update: Private Equity, Q2 2013.

While reasonable efforts have been made to obtain information from sources that are believed to be accurate, and to confi rm the accuracy of such information wherever possible, Preqin Ltd. does not make any representation or warrantythat the information or opinions contained in The Preqin Quarterly Update: Private Equity, Q2 2013 are accurate, reliable, up-to-date or complete.

Although every reasonable effort has been made to ensure the accuracy of this publication Preqin Ltd. does not accept any responsibility for any errors or omissions within The Preqin Quarterly Update: Private Equity, Q2 2013 or for any expense or other loss alleged to have arisen in any way with a reader’s use of this publication.

Contents

Foreword

Q2 2013 was the strongest private equity fundraising quarter since Q4 2008, with an aggregate $124bn raised by 164 funds that held a fi nal close in the quarter. However, the actual number of funds closed in Q2 is the lowest quarterly number since 2005, which demonstrates that investors are committing capital to the more established fund managers that are raising larger funds. Investors have been active during H1 2013, with 57% of investors interviewed by Preqin indicating that they have already made new commitments to private equity funds so far in 2013, while a signifi cant 85% of LPs plan to increase or maintain their allocation to the asset class over the longer term.

Over H1 2013, the value of dry powder held by private equity funds increased to $991bn, following a decrease over 2012. Long-term performance continues to attract LPs to the asset class; private equity horizon IRR data shows that over the longer horizon periods of three, fi ve and 10 years, private equity outperforms the S&P 500, MSCI Europe and MSCI Emerging Markets Indices.

Private equity-backed buyout deal fl ow was down in the second quarter, with 622 deals announced globally totalling $62bn, compared to 678 deals in Q1 2013 valued at $86bn; however, there was an increase in the number and aggregate value of private equity-backed buyout exits compared to the previous quarter. Q2 2013 saw one of the highest quarterly aggregate exit values since 2006, with an aggregate value of $93bn. Venture capital fi nancings were at a high level, with 1,330 fi nancings announced globally at an aggregate $10.6bn, which is the highest quarterly value of fi nancings since Q2 2012.

Preqin’s Private Equity Online services generate the data points behind these reports, offering a wealth of individual fi rm and fund-level data, which is gathered through Preqin’s direct contact with industry professionals from across the globe. We hope you fi nd this report useful, and welcome any feedback you may have. For more information, please visit www.preqin.com or contact [email protected].

Interview with Clay Deniger - Capstone Partners

Fundraising in Q2 2013

p3.

p5.

Institutional Investors in Private Equity p7.

Buyout Deals p8.

Venture Capital Deals p9.

Fund Performance

Secondaries

p10.

p11.

2013 Preqin Investor Network Global Alternatives Report

The 2013 Preqin Investor Network Global Alternatives Report is the most comprehensive review of the alternatives industry aimed exclusively at institutional investors ever undertaken. The report covers a wide range of topics, including asset allocation, fund selection and due diligence.

The 105-page 2013 Preqin Investor Network Global Alternatives Report is freely accessible on Preqin’s website.

To download a digital copy of the Report, please visit:

www.preqin.com/PIN2013

3

The Preqin Quarterly Update: Private Equity, Q2 2013

© 2013 Preqin Ltd. / www.preqin.com

Download the data pack at:www.preqin.com/quarterlyupdate

Interview with Clay Deniger

Capstone Partners

What is your current perspective on the fundraising environment?

The fundraising market remains diffi cult, and I think for the near term it will continue to present challenges. There was a tremendous bottleneck of 2005, 2006 and 2007 vintage funds that otherwise would have been back in the market, but took longer to right their portfolios coming out of the fi nancial crisis. So 2012 was a particularly heavy re-up year, which has lightened in 2013. We would expect 2014 to be similar in terms of normalized re-up levels, which is obviously good news for GPs who should fi nd themselves in a less crowded market relative to 2012. That said, it remains tough and today we consistently see binary outcomes in the fundraising world. It is a tale of two timelines. Those GPs who are highly sought after, who have a compelling story, and who can generate momentum in their fundraising early, tend to be in market for three to six months. Those GPs who have to fi ght harder and scratch and claw to generate momentum fi nd themselves in market for 12-18 months or longer. This clearly puts focus and importance on coming to market at the right time with a clear strategy and portfolios in the best shape possible for generating fundraising momentum.

The fi rst half of 2013 has produced good fundraising numbers. Do you expect that to continue throughout the rest of the year?

We expect 2013 to be a strong year and even to carry over into 2014, which is positive news for those managers currently fundraising. While we expect the fl ow of dollars and commitments to be strong through the end of the year, many of those Q3/Q4 commitments are already spoken for today in re-ups or soft circles. A GP needs to keep that in mind when thinking about chasing commitments in the second half of this year or any calendar year.

What strategies are LPs viewing most favourably at present?

In general, LP portfolios in the US and Europe are mature and stable and not many LPs are looking to dramatically change how their portfolios are constructed, so it is much more about fi ne-tuning around the edges. Within the category of fi ne-tuning, we are seeing a few things. While large cap buyouts will always be a critical part of any portfolio, there is a general move of some dollars (or Euros) out of large cap and mega buyouts and into the middle market based on the belief that more ineffi ciencies exist at the smaller end of the buyout world. Geographically, for North American investors, we are seeing an opportunistic move into Europe, both through equity and credit strategies. In recent years, North American LPs have been largely on the sidelines in relation to Europe, waiting for things to settle a bit and to develop

their own strategies around playing the macro challenges in Europe. We are seeing the interest in European funds materialize into commitments this year and expect that trend to continue.

How do LPs view the asset class compared to prior years?

LPs’ macro view of the asset class largely comes from the success of the underlying portfolios and sponsors that they manage. The fact that GPs are returning capital means we are seeing more investments go cash-to-cash and LP commitments are being returned. LPs are enjoying gains on those commitments, which then primes the pump for them to make new commitments this year and in coming years. The liquidity that exists, particularly from North American managers, is helping to support continued enthusiasm for the asset class.

Competition for LP commitments is still tough. What is critical for a GP to do to be successful? The prerequisites for successful fundraising remain the same: strong and experienced teams; a repeatable, sustainable strategy; and a well-articulated, underlying track record that demonstrates successful execution of that strategy – in this respect, fundraising is no different than in prior years. We advise clients that the most important thing in driving a successful fundraise outside of these prerequisites is giving LPs a reason to act. Their allocations are so tight and their calendars so full that unless they have a reason to focus on the underwriting of your fund, as a GP, you just won’t be able to grab the mindshare that is required to obtain commitments. For the most successful GPs, that call to action comes from scarcity value and momentum during a fundraise. This is certainly the best case for a GP - having an LP focus on your fund because they run the risk of missing it. For many other managers that have some of the prerequisites but perhaps not the necessary momentum, we increasingly see the need to offer LPs a special reason to act. Whether that is preferred economics for committing early in a fundraise or access to co-investments on a reduced or no fee basis, offering motivation beyond the typical fundraising tools is an important part of what a GP needs to do to generate momentum that is essential to drive successful closes.

What do fi rst-time managers without a track record need to do to be successful in fundraising?

Without a track record, we advise GPs to fi nd some other connection point with an LP that makes them comfortable that a strategy will be successful. That connection usually comes from the manager’s existing relationships, whatever those may be - whether they are friends and family or investors that backed them at a previous fi rm. Both cold starts and developing new

4

The Preqin Quarterly Update: Private Equity, Q2 2013

© 2013 Preqin Ltd. / www.preqin.com

Download the data pack at:www.preqin.com/quarterlyupdate

relationships without a track record are extremely diffi cult to accomplish. Getting the backing of previous investors and close relationships or investing in deals with other managers to build out a track record is critical, so that when you do come to market you have a track record that offers some level of proof of concept for the stated strategy.

What benefi t have you seen in GPs informally talking to LPs between fundraises?

We regularly advocate to GPs that marketing between funds is no longer an option; it really is a prerequisite. Back to the crowded nature of an LP’s portfolio and the pressure on re-ups, if the only time you are having discussions with LPs is when you are asking for new commitments or attending an AGM, you have missed the opportunity to deepen the relationship and increase the likelihood of a re-up or new commitment. Re-ups are not automatic as they once were, so taking the time to both nurture existing LP relationships and advance discussions with targeted new LPs between fundraises is a critical function. This is true not just for large fi rms with IR departments but also for mid-market fi rms and for smaller funds as well. For some smaller funds it can be even more important, as they may have a less prominent position in the investor’s portfolio, so deepening existing LP relationships is particularly crucial. We also encourage GPs to see priority prospective investors several times a year to ensure they are on forward investment calendars so that the LP is tracking the sponsor as much as the sponsor is tracking the LP.

Has the way GPs communicate with LPs changed overall recently?

Yes, I think GPs are getting the message. They recognize that they need to nurture their investor base and give them the same focus and commitment as they do to deal sourcing. Both sides of the business are critical for their ongoing success. You cannot just focus on systematically making investments; you also need to be systematic about ensuring sources of capital are available for the long term, which means treating LPs like partners and communicating regularly.

Do you see any change in terms and conditions?

I wouldn’t say we have seen bright lines or binary changes in terms and conditions. Generally, we have seen downward pressure on fees particularly in the larger cap funds, which is translated as direct pressure on management fees. In smaller funds, fee pressure may be refl ected in LPs looking for alternative ways to deploy lower cost capital, as in reduced or no fee co-investments. Regarding specifi c terms, there remains pressure on deal-by-deal carry and transaction fees in particular, but I would characterize it as pressure, as opposed to “we will or will not support this type of fee structure.” Investors recognize that, even in this market, top GPs are rewarded with premium terms and those that drive scarcity value in a fundraising process continue to command premium fees. Those GPs who must fi ght harder to generate momentum fi nd themselves in a weaker negotiating position and can end up with terms that are less aggressive, particularly in those two areas - the sharing of transaction fees and deal-by-deal carry.

What impact are you seeing on the implementation of the AIFMD?

The main theme today on AIFMD is uncertainty. As the July 22nd deadline approaches, it is still unclear how offshore funds will be able to market to the bulk of European LPs. The cleanest answer is to work hard to close prospective European investors prior to July 22nd, but that advice only applies to cases where an investor is already in advanced diligence. For the broader universe post July 22nd, we advise GPs to be extremely careful and to work closely with counsel, based on the belief that the additional clarifi cation and regulatory infrastructure will start to unfold in the coming months.

Thank you for your time.

Clay Deniger is responsible for North American Operations including project management, transaction structuring, and fi rm operations.

Prior to Capstone, Clay was founder and CEO of Substrate Technologies, Inc. (STI), a venture-backed semiconductor component supplier. At STI, Clay raised capital from strategic and institutional investors on three continents, and ultimately deployed the proceeds for construction of a dedicated manufacturing facility in Shenzhen, China. In 2003, Clay negotiated the sale of STI to a group of China-based investors.

Prior to STI, Clay was founder and CEO of Customer Survey Technologies (CST) a boutique technology research fi rm operating in North America and Europe. Clay raised CST’s critical capital through strategic investors and foreign government backed fi nancings in the US and Europe. In 1998, he sold CST to a domestic competitor.

Clay has written extensively on the subject of technology and tech industry investment. He is a Magna Cum Laude graduate of Hamilton College.

www.capstonepartnerslp.com

5

The Preqin Quarterly Update: Private Equity, Q2 2013

© 2013 Preqin Ltd. / www.preqin.com

Download the data pack at:www.preqin.com/quarterlyupdate

Fundraising in Q2 2013

Fig. 1: Quarterly Global Private Equity Fundraising, Q1 2008 -

Q2 2013

Source: Preqin Funds in Market

307

375

288

438

205203185

328

182

223

189

314

214

253

195

319

211242

206

263

182164173

212

128

171

7895

5984 77 66

79 66 7795

6192 79 91 83

10680

124

0

50

100

150

200

250

300

350

400

450

500

Q1 Q2 Q3 Q4 Q1Q2 Q3 Q4Q1 Q2Q3 Q4 Q1Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2008 2009 2010 2011 2012 2013

No. of FundsClosed

AggregateCapitalRaised ($bn)

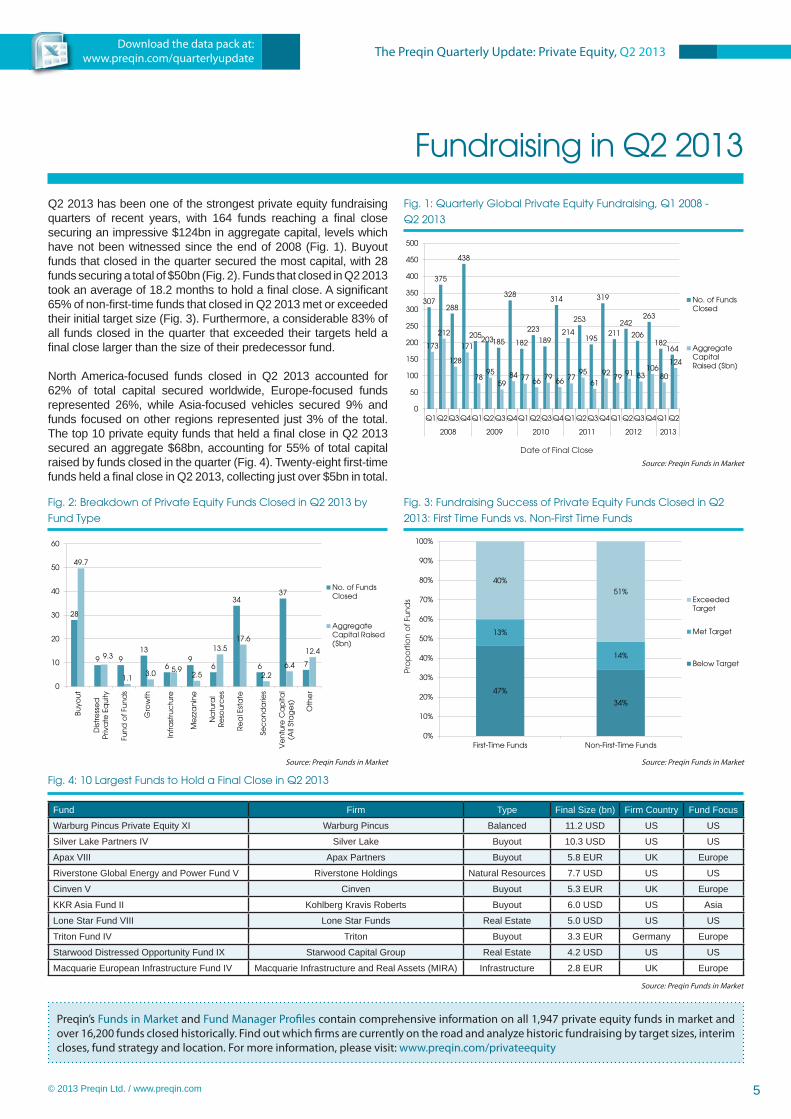

Q2 2013 has been one of the strongest private equity fundraising quarters of recent years, with 164 funds reaching a fi nal close securing an impressive $124bn in aggregate capital, levels which have not been witnessed since the end of 2008 (Fig. 1). Buyout funds that closed in the quarter secured the most capital, with 28 funds securing a total of $50bn (Fig. 2). Funds that closed in Q2 2013 took an average of 18.2 months to hold a fi nal close. A signifi cant 65% of non-fi rst-time funds that closed in Q2 2013 met or exceeded their initial target size (Fig. 3). Furthermore, a considerable 83% of all funds closed in the quarter that exceeded their targets held a fi nal close larger than the size of their predecessor fund.

North America-focused funds closed in Q2 2013 accounted for 62% of total capital secured worldwide, Europe-focused funds represented 26%, while Asia-focused vehicles secured 9% and funds focused on other regions represented just 3% of the total. The top 10 private equity funds that held a fi nal close in Q2 2013 secured an aggregate $68bn, accounting for 55% of total capital raised by funds closed in the quarter (Fig. 4). Twenty-eight fi rst-time funds held a fi nal close in Q2 2013, collecting just over $5bn in total.

Fig. 2: Breakdown of Private Equity Funds Closed in Q2 2013 by

Fund Type

Source: Preqin Funds in Market

28

9 913

69

6

34

6

37

7

49.7

9.3

1.13.0 5.9

2.5

13.517.6

2.26.4

12.4

0

10

20

30

40

50

60

Buyo

ut

Dis

tre

sse

dP

riva

te E

qu

ity

Fun

d o

f Fu

nd

s

Gro

wth

Infr

ast

ruc

ture

Me

zza

nin

e

Na

tura

lR

eso

urc

es

Re

al E

sta

te

Sec

on

da

ries

Ve

ntu

re C

ap

ital

(All

Sta

ge

s)

Oth

er

No. of FundsClosed

AggregateCapital Raised($bn)

Fig. 3: Fundraising Success of Private Equity Funds Closed in Q2

2013: First Time Funds vs. Non-First Time Funds

Source: Preqin Funds in Market

47%

34%

13%

14%

40%

51%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

First-Time Funds Non-First-Time Funds

ExceededTarget

Met Target

Below Target

Date of Final Close

Pro

po

rtio

n o

f Fu

nd

s

Fig. 4: 10 Largest Funds to Hold a Final Close in Q2 2013

Fund Firm Type Final Size (bn) Firm Country Fund Focus

Warburg Pincus Private Equity XI Warburg Pincus Balanced 11.2 USD US US

Silver Lake Partners IV Silver Lake Buyout 10.3 USD US US

Apax VIII Apax Partners Buyout 5.8 EUR UK Europe

Riverstone Global Energy and Power Fund V Riverstone Holdings Natural Resources 7.7 USD US US

Cinven V Cinven Buyout 5.3 EUR UK Europe

KKR Asia Fund II Kohlberg Kravis Roberts Buyout 6.0 USD US Asia

Lone Star Fund VIII Lone Star Funds Real Estate 5.0 USD US US

Triton Fund IV Triton Buyout 3.3 EUR Germany Europe

Starwood Distressed Opportunity Fund IX Starwood Capital Group Real Estate 4.2 USD US US

Macquarie European Infrastructure Fund IV Macquarie Infrastructure and Real Assets (MIRA) Infrastructure 2.8 EUR UK Europe

Source: Preqin Funds in Market

Preqin’s Funds in Market and Fund Manager Profi les contain comprehensive information on all 1,947 private equity funds in market and over 16,200 funds closed historically. Find out which fi rms are currently on the road and analyze historic fundraising by target sizes, interim closes, fund strategy and location. For more information, please visit: www.preqin.com/privateequity

7

The Preqin Quarterly Update: Private Equity, Q2 2013

© 2013 Preqin Ltd. / www.preqin.com

Download the data pack at:www.preqin.com/quarterlyupdate

Institutional Investors in Private Equity

Fig. 1: Proportion of LPs That Have Made New Private Equity

Commitments So Far in 2013

Source: Preqin Investor Interviews, June 2013

57%

43%Made NewPrivate EquityCommitments SoFar in 2013

Not Made NewCommitments SoFar in 2013

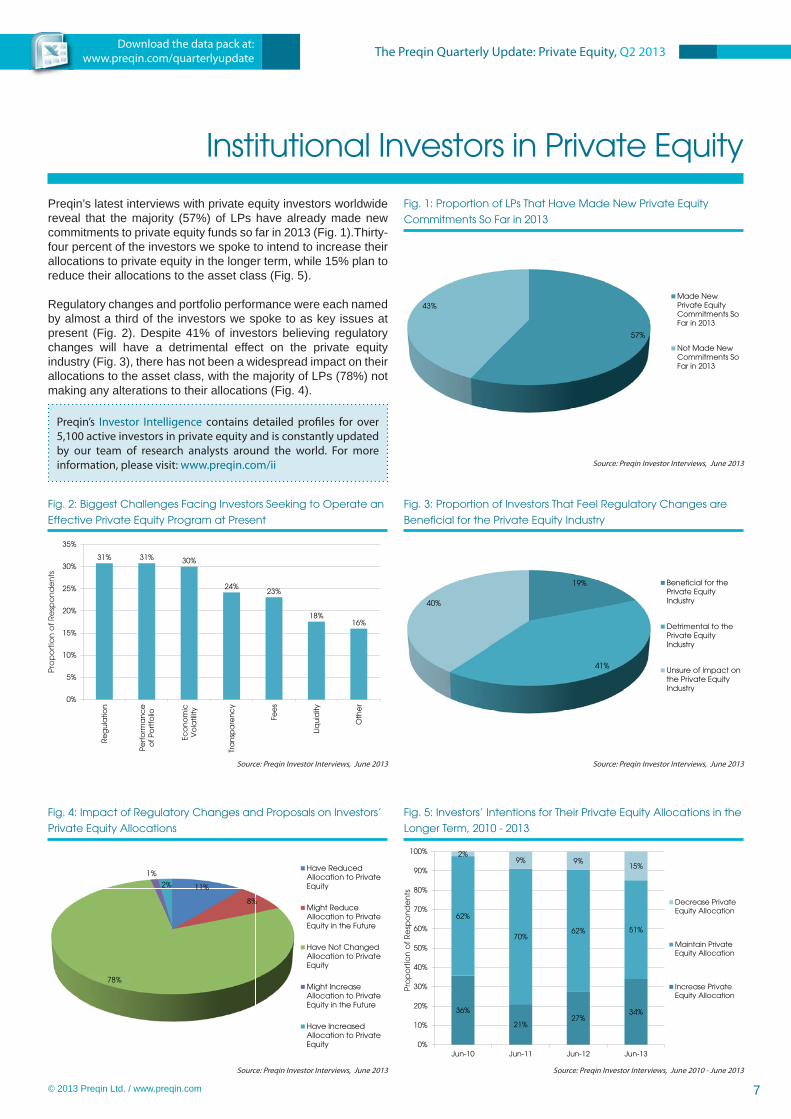

Preqin’s latest interviews with private equity investors worldwide reveal that the majority (57%) of LPs have already made new commitments to private equity funds so far in 2013 (Fig. 1).Thirty-four percent of the investors we spoke to intend to increase their allocations to private equity in the longer term, while 15% plan to reduce their allocations to the asset class (Fig. 5).

Regulatory changes and portfolio performance were each named by almost a third of the investors we spoke to as key issues at present (Fig. 2). Despite 41% of investors believing regulatory changes will have a detrimental effect on the private equity industry (Fig. 3), there has not been a widespread impact on their allocations to the asset class, with the majority of LPs (78%) not making any alterations to their allocations (Fig. 4).

Fig. 2: Biggest Challenges Facing Investors Seeking to Operate an

Effective Private Equity Program at Present

Source: Preqin Investor Interviews, June 2013

31% 31% 30%

24%23%

18%16%

0%

5%

10%

15%

20%

25%

30%

35%

Re

gu

latio

n

Pe

rfo

rma

nc

eo

f P

ort

folio

Eco

no

mic

Vo

latil

ity

Tra

nsp

are

nc

y

Fee

s

Liq

uid

ity

Oth

er

Fig. 3: Proportion of Investors That Feel Regulatory Changes are

Beneficial for the Private Equity Industry

Source: Preqin Investor Interviews, June 2013

19%

41%

40%

Beneficial for thePrivate EquityIndustry

Detrimental to thePrivate EquityIndustry

Unsure of Impact onthe Private EquityIndustry

Pro

po

rtio

n o

f R

esp

on

de

nts

Fig. 4: Impact of Regulatory Changes and Proposals on Investors’

Private Equity Allocations

Source: Preqin Investor Interviews, June 2013

11%

8%

78%

1%

2%

Have ReducedAllocation to PrivateEquity

Might ReduceAllocation to PrivateEquity in the Future

Have Not ChangedAllocation to PrivateEquity

Might IncreaseAllocation to PrivateEquity in the Future

Have IncreasedAllocation to PrivateEquity

Fig. 5: Investors’ Intentions for Their Private Equity Allocations in the

Longer Term, 2010 - 2013

Source: Preqin Investor Interviews, June 2010 - June 2013

36%

21%27%

34%

62%

70%62% 51%

2%9% 9%

15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jun-10 Jun-11 Jun-12 Jun-13

Decrease PrivateEquity Allocation

Maintain PrivateEquity Allocation

Increase PrivateEquity Allocation

Preqin’s Investor Intelligence contains detailed profi les for over 5,100 active investors in private equity and is constantly updated by our team of research analysts around the world. For more information, please visit: www.preqin.com/ii

Pro

po

rtio

n o

f R

esp

on

de

nts

8

The Preqin Quarterly Update: Private Equity, Q2 2013

© 2013 Preqin Ltd. / www.preqin.com

Download the data pack at:www.preqin.com/quarterlyupdate

Buyout Deals

Fig. 1: Quarterly Number and Aggregate Value of Private Equity-

Backed Buyout Deals Globally, Q1 2006 - Q2 2013

Source: Preqin Buyout Deals Analyst

0

50

100

150

200

250

300

0

200

400

600

800

1,000

1,200

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

2006 2007 2008 2009 2010 2011 2012 2013

No. of Deals Aggregate Deal Value ($bn)

A total of 622 private equity-backed buyout deals were announced globally in Q2 2013, with an aggregate value of $62bn (Fig. 1). This represents a 28% decrease from the $86bn witnessed during Q1 2013. North American deals accounted for 46% of aggregate deal value in Q2 2013, while European deals accounted for 47% (Fig. 2). The largest deal announced in the quarter was the $6.9bn privatization of BMC Software (Fig. 4).

Three-hundred and thirty private equity-backed buyout exits were announced during Q2 2013, with an aggregate value of $93bn; this represents an 86% increase in the aggregate value of exits compared to Q1 2013 (Fig. 3). Q2 2013 witnessed one of the highest quarterly aggregate exit values in the period since 2006, second only to Q2 2011 where 364 exits were valued at $128bn.

No

. of

De

als

Fig. 2: Quarterly Aggregate Value of Private Equity-Backed Buyout

Deals by Region, Q1 2008 - Q2 2013

Source: Preqin Buyout Deals Analyst

0

10

20

30

40

50

60

70

80

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2008 2009 2010 2011 2012 2013

North America Europe Asia Rest of World

Fig. 3: Global Number of Private Equity-Backed Buyout Exits by

Type and Aggregate Exit Value, Q1 2006 - Q2 2013

Source: Preqin Buyout Deals Analyst

0

20

40

60

80

100

120

140

0

50

100

150

200

250

300

350

400

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

2006 2007 2008 2009 2010 2011 2012 2013

IPO Restructuring Sale to GP Trade Sale Aggregate Exit Value ($bn)

Ag

gre

ga

te D

ea

l Va

lue

($b

n)

Ag

gre

ga

te D

ea

l Va

lue

($bn

)

No

. of

Exits

Ag

gre

ga

te Exit V

alu

e ($b

n)

Fig. 4: 10 Largest Private Equity-Backed Buyout Deals Announced in Q2 2013

Firm Deal Date Investment Type

Deal Size (mn) Deal Status Investors Bought From/Exiting Company Location Primary

Industry

BMC Software May-13 Public To Private 6,900 USD Announced Bain Capital, GIC Special Investments, Golden

Gate Capital, Insight Venture Partners - US Software

Springer SBM Jun-13 Buyout 3,300 EUR Announced BC Partners EQT Partners, Government of Singapore Investment Corporation (GIC) Germany Publishing

ista Apr-13 Buyout 3,100 EUR Announced CVC Capital Partners Charterhouse Capital Partners Germany Energy

CeramTec GmbH Jun-13 Buyout 1,490 EUR Announced Cinven Rockwood Holdings Germany Manufacturing

Vue Entertainment Jun-13 Buyout 935 GBP Announced Alberta Investment Management Corporation, OMERS Private Equity Doughty Hanson & Co UK Entertainment

CSC ServiceWorks Inc. May-13 Merger 1,440 USD Announced AIR-Serv Holding, LLC., Coinmach, Pamplona

Capital Management - US Industrial

Befesa Medio Ambiente Apr-13 Buyout 1,075 EUR Announced Triton Abengoa, Qualitas Equity Partners Spain Environmental

Services

Allfl ex May-13 Buyout 1,300 USD Announced BC Partners Electra Partners, Intermediate Capital Group France Manufacturing

National Financial Partners Corp. Apr-13 Public To

Private 1,300 USD Completed Madison Dearborn Partners - US Financial Services

PRA International Jun-13 Buyout 1,300 USD Announced Kohlberg Kravis Roberts Caisse de depot et placement du Quebec, Genstar Capital Partners US Medical

Technologies

Source: Preqin Buyout Deals Analyst

Analyze over 30,000 private equity buyout deals globally using Preqin’s Buyout Deals Analyst. For more information, please visit: www.preqin.com/buyoutdeals

9

The Preqin Quarterly Update: Private Equity, Q2 2013

© 2013 Preqin Ltd. / www.preqin.com

Download the data pack at:www.preqin.com/quarterlyupdate

Venture Capital Deals

Fig. 1: Number and Aggregate Value of Venture Capital Deals

Globally, Q1 2008 – Q2 2013

Source: Preqin Venture Deals Analyst

0

2

4

6

8

10

12

14

16

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2008 2009 2010 2011 2012 2013

No. of Deals Aggregate Deal Value ($bn)

Q2 2013 saw 1,330 venture capital fi nancings announced globally, valued at an aggregate $10.6bn, which represents the highest quarterly aggregate value since Q2 2012 (Fig. 1). North America saw the highest number of venture capital deals announced, with 815 fi nancings in Q2 2013 (Fig. 2). The number of fi nancings in China fell to its lowest level in the period since 2008, with just 22 deals in the quarter. The $170mn fi nancing of internet company, Fanatics Inc., was the largest venture capital deal completed in Q2 2013 (Fig. 4).

The proportion of Angel/seed deals, Series A and Series B in Q2 2013 increased compared to last quarter (Fig. 3). Series A deals saw the most signifi cant increase, accounting for 17% of all venture capital deals in the quarter, up from 13% in Q1 2013.

No

. of

De

als

Fig. 2: Number of Venture Capital Deals by Region, Q1 2008 – Q2

2013

Source: Preqin Venture Deals Analyst

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2008 2009 2010 2011 2012 2013

North America Europe China India Israel Other

Fig. 3: Proportion of Number of Venture Capital Deals by Stage,

Q2 2013

Source: Preqin Venture Deals Analyst

6%1%

2%1%

20%

17%

10%4%

3%

34%

3%

Add-on and Other

Grant

GrowthCapital/Expansion

PIPE

Angel/Seed

Series A/Round 1

Series B/Round 2

Series C/Round 3

Series D/Round 4and LaterUnspecified Round

Venture Debt

No

. of

De

als

Ag

gre

ga

te D

ea

l Va

lue

($bn

)

Fig. 4: 10 Largest Venture Capital Deals in Q2 2013

Portfolio Company Name

Deal Date Stage Deal Size

(mn) Investors Primary Industry Location

Fanatics, Inc. Jun-13 Unspecifi ed Round 170 USD Alibaba Group, Temasek Holdings Internet US

Fab.com Jun-13 Series D/Round 4 150 USDAndreessen Horowitz, Atomico, DOCOMO Capital, ITOCHU

Corporation, Menlo Ventures, Pinnacle Ventures, RTP Ventures, Tencent

Internet US

Intrexon Corporation May-13 Series F/Round 6 150 USD Third Security Biotechnology US

Lamoda Jun-13 Unspecifi ed Round 130 USD Access Industries, Summit Partners, Tengelmann Group Internet Russia

Bloom Energy May-13 Series G/Round 7 130 USD Credit Suisse Clean Technology US

ShanghaiMed Healthcare, Inc. Apr-13 Growth Capital/Expansion 100 USD Goldman Sachs Merchant Banking Division, Government of

Singapore Investment Corporation (GIC) Healthcare China

Lazada Jun-13 Unspecifi ed Round 100 USD Holtzbrinck Ventures, Kinnevik, Summit Partners, Tengelmann Group, Verlinvest Internet Indonesia

Zalora May-13 Unspecifi ed Round 100 USD Kinnevik, Rocket Internet, Summit Partners, Tengelmann Group, Verlinvest Internet Singapore

Acumen Brands, Inc. Apr-13 Growth Capital/Expansion 83 USD General Atlantic Internet US

Hyperoptic May-13 Unspecifi ed Round 50 GBP Quantum Strategic Partners Ltd. Telecoms UK

Source: Preqin Venture Deals Analyst

Examine details for over 44,000 venture capital deals globally using Preqin’s Venture Deals Analyst. For more information, please visit: www.preqin.com/vcdeals

10

The Preqin Quarterly Update: Private Equity, Q2 2013

© 2013 Preqin Ltd. / www.preqin.com

Download the data pack at:www.preqin.com/quarterlyupdate

Fund Performance

Fig. 1: Private Equity Dry Powder by Fund Type, 2003 - 2013

Source: Preqin Performance Analyst

0

200

400

600

800

1,000

1,200

De

c-0

3

De

c-0

4

De

c-0

5

De

c-0

6

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

Jul-1

3

Buyout

DistressedPrivate Equity

Growth

Mezzanine

Real Estate

Venture Capital

Other

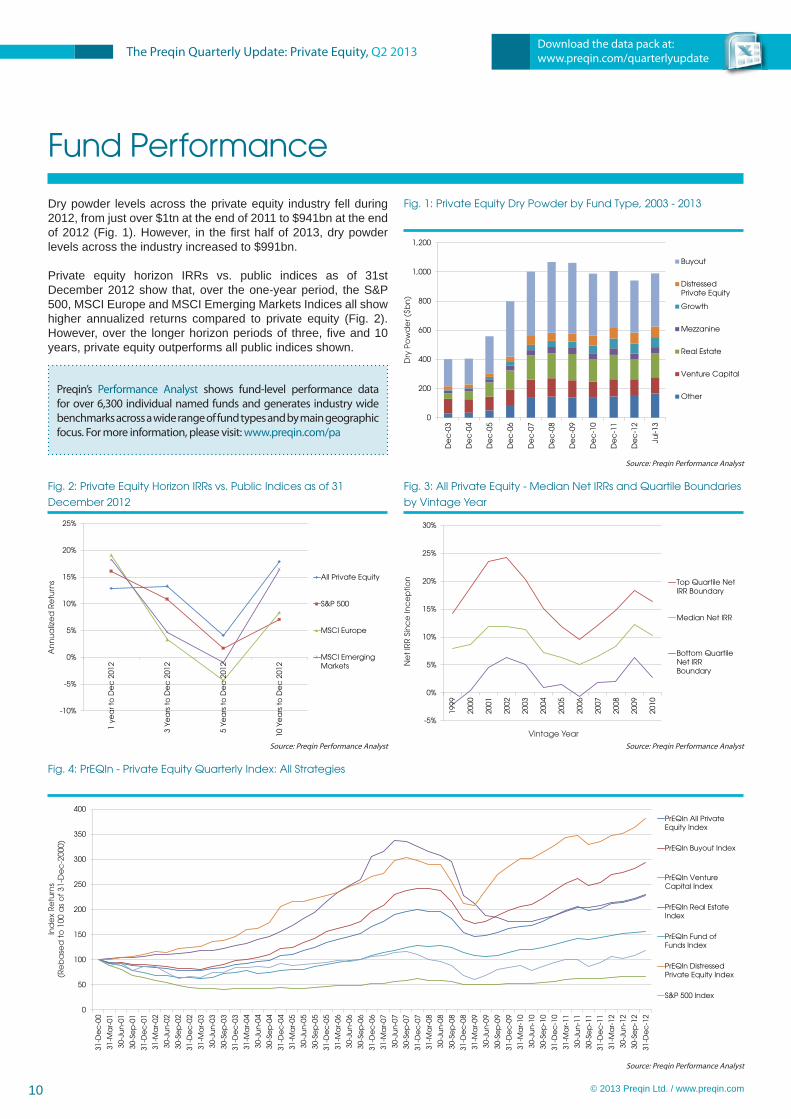

Dry powder levels across the private equity industry fell during 2012, from just over $1tn at the end of 2011 to $941bn at the end of 2012 (Fig. 1). However, in the fi rst half of 2013, dry powder levels across the industry increased to $991bn.

Private equity horizon IRRs vs. public indices as of 31st December 2012 show that, over the one-year period, the S&P 500, MSCI Europe and MSCI Emerging Markets Indices all show higher annualized returns compared to private equity (Fig. 2). However, over the longer horizon periods of three, fi ve and 10 years, private equity outperforms all public indices shown.

Preqin’s Performance Analyst shows fund-level performance data for over 6,300 individual named funds and generates industry wide benchmarks across a wide range of fund types and by main geographic focus. For more information, please visit: www.preqin.com/pa

Dry

Po

wd

er (

$bn

)

Fig. 2: Private Equity Horizon IRRs vs. Public Indices as of 31

December 2012

Source: Preqin Performance Analyst

-10%

-5%

0%

5%

10%

15%

20%

25%

1 ye

ar t

o D

ec

201

2

3 Ye

ars

to

De

c 2

012

5 Ye

ars

to

De

c 2

012

10 Y

ea

rs t

o D

ec

201

2

All Private Equity

S&P 500

MSCI Europe

MSCI EmergingMarkets

Fig. 3: All Private Equity - Median Net IRRs and Quartile Boundaries

by Vintage Year

Source: Preqin Performance Analyst

-5%

0%

5%

10%

15%

20%

25%

30%

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Top Quartile NetIRR Boundary

Median Net IRR

Bottom QuartileNet IRRBoundary

An

nu

aliz

ed

Re

turn

s

Ne

t IR

R S

inc

e In

ce

ptio

n

Vintage Year

Fig. 4: PrEQIn - Private Equity Quarterly Index: All Strategies

Source: Preqin Performance Analyst

0

50

100

150

200

250

300

350

400

31-D

ec

-00

31-M

ar-

01

30-J

un

-01

30-S

ep

-01

31-D

ec

-01

31-M

ar-

02

30-J

un

-02

30-S

ep

-02

31-D

ec

-02

31-M

ar-

03

30-J

un

-03

30-S

ep

-03

31-D

ec

-03

31-M

ar-

04

30-J

un

-04

30-S

ep

-04

31-D

ec

-04

31-M

ar-

05

30-J

un

-05

30-S

ep

-05

31-D

ec

-05

31-M

ar-

06

30-J

un

-06

30-S

ep

-06

31-D

ec

-06

31-M

ar-

07

30-J

un

-07

30-S

ep

-07

31-D

ec

-07

31-M

ar-

08

30-J

un

-08

30-S

ep

-08

31-D

ec

-08

31-M

ar-

09

30-J

un

-09

30-S

ep

-09

31-D

ec

-09

31-M

ar-

10

30-J

un

-10

30-S

ep

-10

31-D

ec

-10

31-M

ar-

11

30-J

un

-11

30-S

ep

-11

31-D

ec

-11

31-M

ar-

12

30-J

un

-12

30-S

ep

-12

31-D

ec

-12

PrEQIn All PrivateEquity Index

PrEQIn Buyout Index

PrEQIn VentureCapital Index

PrEQIn Real EstateIndex

PrEQIn Fund ofFunds Index

PrEQIn DistressedPrivate Equity Index

S&P 500 Index

Ind

ex

Re

turn

s(R

eb

ase

d t

o 1

00 a

s o

f 31

-De

c-2

000)

11

The Preqin Quarterly Update: Private Equity, Q2 2013

© 2013 Preqin Ltd. / www.preqin.com

Download the data pack at:www.preqin.com/quarterlyupdate

Secondaries

Fig. 1: Likelihood of Investors Purchasing Private Equity Fund

Interests on the Secondary Market over the Next 24 Months

Source: Preqin Secondary Market Monitor

2%

7%

16%

75%

Highly Likely

Opportunistic

Possible

Unlikely

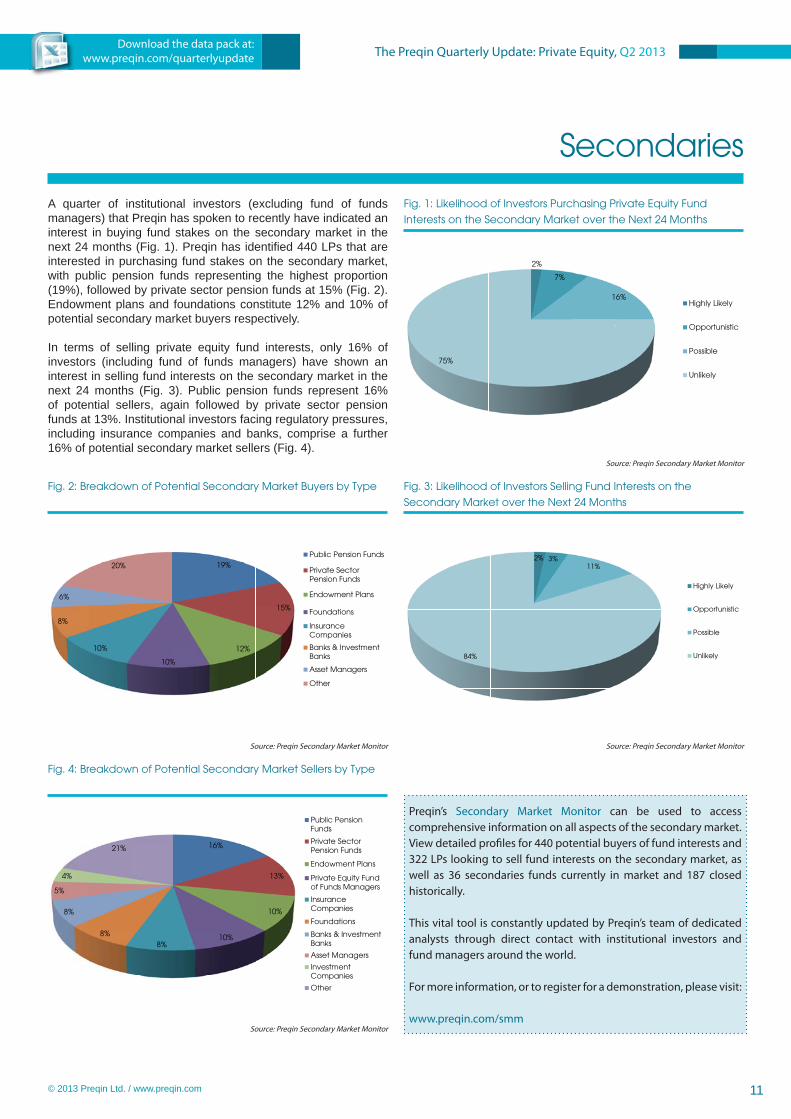

A quarter of institutional investors (excluding fund of funds managers) that Preqin has spoken to recently have indicated an interest in buying fund stakes on the secondary market in the next 24 months (Fig. 1). Preqin has identifi ed 440 LPs that are interested in purchasing fund stakes on the secondary market, with public pension funds representing the highest proportion (19%), followed by private sector pension funds at 15% (Fig. 2). Endowment plans and foundations constitute 12% and 10% of potential secondary market buyers respectively.

In terms of selling private equity fund interests, only 16% of investors (including fund of funds managers) have shown an interest in selling fund interests on the secondary market in the next 24 months (Fig. 3). Public pension funds represent 16% of potential sellers, again followed by private sector pension funds at 13%. Institutional investors facing regulatory pressures, including insurance companies and banks, comprise a further 16% of potential secondary market sellers (Fig. 4).

Fig. 2: Breakdown of Potential Secondary Market Buyers by Type

Source: Preqin Secondary Market Monitor

19%

15%

12%

10%

10%

8%

6%

20%

Public Pension Funds

Private SectorPension Funds

Endowment Plans

Foundations

InsuranceCompanies

Banks & InvestmentBanks

Asset Managers

Other

Fig. 3: Likelihood of Investors Selling Fund Interests on the

Secondary Market over the Next 24 Months

Source: Preqin Secondary Market Monitor

2% 3%11%

84%

Highly Likely

Opportunistic

Possible

Unlikely

Preqin’s Secondary Market Monitor can be used to access comprehensive information on all aspects of the secondary market. View detailed profi les for 440 potential buyers of fund interests and 322 LPs looking to sell fund interests on the secondary market, as well as 36 secondaries funds currently in market and 187 closed historically.

This vital tool is constantly updated by Preqin’s team of dedicated analysts through direct contact with institutional investors and fund managers around the world.

For more information, or to register for a demonstration, please visit:

www.preqin.com/smm

Fig. 4: Breakdown of Potential Secondary Market Sellers by Type

Source: Preqin Secondary Market Monitor

16%

13%

10%

10%8%

8%

8%

5%

4%

21%

Public PensionFunds

Private SectorPension Funds

Endowment Plans

Private Equity Fundof Funds Managers

InsuranceCompanies

Foundations

Banks & InvestmentBanks

Asset Managers

InvestmentCompanies

Other

The Preqin Quarterly Update:Private Equity, Q2 2013

alternative assets. intelligent data.

Preqin Private Equity Online

With global coverage and detailed information on all aspects of the private equity asset class, Preqin’s industry-leading Private Equity Online services keep you up to date on all the latest developments in the private equity universe.

Source new investors for funds and co-investments

Find the most relevant investors, with access to detailed profi les for over 5,100 institutional investors actively investing in private equity, including future fund searches and mandates, direct contact information and sample investments.

Identify potential investment opportunities

View in-depth profi les for over 1,900 unlisted private equity funds currently in the market, including information on investment strategy, geographic focus, key fundraising data, service providers used and sample investors.

Find active fund managers in private equity

Search for fi rms actively targeting private equity investments. View information on key contacts, fi rm fundraising and performance history, and applied strategies of the fi rm when investing in portfolio companies and assets.

Analyze the latest private equity fundraising activity

See which fi rms are currently on the road raising a private equity fund and which will be coming to market soon. Analyze fundraising over time by fund strategy, property type and location.

Benchmark performance

Identify which fund managers have the best track records, with performance benchmarks for private equity funds and performance details for over 6,300 individual named funds.

Examine fund terms

Use our unique Fund Terms Calculator to model fee changes and see: what are the typical terms that a private equity fund charges? What are the implications of making changes to different fees? How do these fees vary between fund types and geographies?

If you want any further information, or would like to apply for a demo of our

products, please contact us:

New York:

One Grand Central Place60 E 42nd Street

Suite 2544, New YorkNY 10165

Tel: +1 212 350 0100Fax: +1 440 445 9595

London:

Equitable House47 King William Street

LondonEC4R 9AF

Tel: +44 (0)20 7645 8888Fax: +44 (0)87 0330 5892

Singapore:

One Finlayson Green, #11-02 Singapore 049246

Tel: +65 6305 2200Fax: +65 6491 5365

San Francisco:

580 California StreetSuite 1638, San Francisco

CA 94104

Tel: +1 415 635 3580Fax: +1 440 445 9595

Email: [email protected]: www.preqin.com

Find out how Preqin’s range of products and services can help you:

www.preqin.com/privateequity