1

Leading voice of the Financial Industry

MAURITIUS

FINANCIAL SECTOR OVERVIEW

2

Table of Contents

Title Page………………………………………………………………………………………….1

Table of Contents…………………………………………………………………………………2

List of Figures…………………………………………………………………………………….4

List of Tables……………………………………………………………………………………...5

1.0 Country Profile…………………………………………………………………………...6

2.0 Executive Summary……………………………………………………………………...7

3.0 Domestic Economy……………………………………………………………………...10

3.1 Output and Inflation…………………………………………………………....10

3.2 Investment and Savings………………………………………………………...11

3.3 Fiscal Policy……………………………………………………………………..13

3.4 Interest Rate Policy…………………………..…………………………………13

3.5 Domestic Stock Market……………………………………..………………….13

3.6 Exchange Rate…………………………………….…………………………….15

4.0 Overview of the Financial System of Mauritius……….……………………………...17

5.0 Banking Sector………………………………………………………………….………21

5.1 Evolution of the Banking Sector…………………………………….…………21

5.2 Financial Stability………………………………………………………………22

5.3 Performance of the Banking Sector……………………………………….…..26

5.4 Financial Soundness Indicators………………………………………….……28

6.0 The Non-Bank Financial Sector……………………………………………….………33

6.1 Financial Services Commission……………………………………..…………33

6.2 Securities Exchanges……………………………………………………………34

6.2.1 Stock Exchange of Mauritius Ltd………………………………………35

6.2.2 Bourse Africa Ltd…………………………………………….…………37

6.2.3 Investment Funds and Intermediaries…………………………………37

6.3 Insurance……………………………………………………………..…………39

6.4 Pensions…………………………………………………………………………40

6.5 Global Business Companies……………………………………………………41

6.6 Other Non Bank Financial Institutions………………………………….……43

3

6.7 The Supervisory and Regulatory Framework………………………..………44

6.7.1 Prudential supervision………………………………………….………44

6.7.2 Regulation of conduct……………………………………….…….……45

7.0 A SWOT Analysis of the Financial Services Industry of Mauritius…………………48

8.0 Mauritius International Financial Centre…………………………………….………52

9.0 The financial services sector: increasing value added to become a regional financial

center…………………………………………………………………………….………54

10.0 Financial Stability………………………………………………………………………56

4

LIST OF FIGURES

Figure 1: Mauritius: Gross Fixed Capital Formation, Investment as a % &ICOR………..12

Figure 2: SEMDEX and SEM-7 Indices…………………………………………………..14

Figure 3: Transactions by Foreign Investors on the SEM…………………………………14

Figure 4: Evolution of NEER, REER, MERI1 and MERI2 Indices……………………….15

Figure 5: Exchange Rate Movements……………………………………………………...16

Figure 6: Distribution of Banks’ Advances and Assets……………………………………28

Figure 7: Return on Assets of the Banking Sector…………………………………………29

Figure 8: Return on Equity of the Banking Sector…………………………………………29

Figure 9: Tier 1 Capital Ratio………………………………………………………………30

Figure 10: Non –Performing Loans of Banks……………………………………………….31

Figure 11: Non- Performing Loans and Coverage Ratio…………………………………….32

5

LIST OF TABLES

Table 1: Saving –Investment Balance…………………………………………………..11

Table 2: Figures for Market Caps and SEMDEX………………………………………36

Table 3: Trends in General Insurance Business………………………………………...39

Table 4: Private pension industry at a glance…………………………………………...41

6

1.0 Country Profile

Quick Facts

Capital Port Louis

Official Language None

Government Type Republic

Population 1,261,208

Currency Mauritian Rupee (MUR)

Total Area 2,040 Square Kilometers

787 Square miles

GDP $ 12.6 billion 2014

GDP Growth 3.6% 2014

Inflation 3.2%

Language English, French, Hindi, Urdu, Chinese

7

2.0 Executive Summary

Mauritius has established itself as one of the leading economic reformers in Africa, successfully

transitioning from a Low Income into an upper Middle Income Country (MIC). Strong institutions

in a politically stable and thriving business environment and effective use of trade preferences

particularly with Europe and India have been instrumental in driving growth and facilitating an

impressive economic diversification. At independence the small island economy was completely

dependent on sugar. It has since diversified into tourism, textiles, financial services, and

Information and Communication Technology (ICT). A generous social welfare system has been

used to distribute proceeds from high economic growth rates. Less than 1% of the population is

classified as poor. Mauritius is now positioning itself for another important transition. The

Government has announced an ambitious agenda: to transform Mauritius into a High Income

Country (HIC) on the basis of growth that is sustainably generated and equitably distributed by

2025.

The economy has avoided recession during the global economic downturn thanks to the

Government of Mauritius (GoM)’ bold policy response measures. Nonetheless growth has slowed

down from an average of 4.8% during 2003-2007 to 3.9% during 2008-2012. Unemployment has

also slowly increased especially among less skilled youth and women. The GoM is aware that if it

is to achieve a HIC status, it must urgently propel the country back onto a high growth path. The

biggest challenge for Mauritius is to enhance its competitiveness to sustainably move up the value

chain. Small and isolated, Mauritius is highly open and vulnerable to changes in the environment

and climate. With trade accounting for about 120.5% of GDP, the GoM would like to deepen its

participation in cross-border value chains to sustainably drive growth. However, remaining

infrastructure deficiencies and an emerging skills mismatch driven by underlying structural

bottlenecks in the education system are impacting on the quality of its human capital, productivity

and innovation capacity.

Close public-private partnerships facilitated private sector-led growth in a stable macroeconomic

and institutional environment. The government implemented an active industrial policy to support

private sector competitiveness while exploiting global trade niches created by preferential access

arrangements. As a result, savings were high and reinvested in diversifying the economy. Starting

8

as a mono-cropped, inward-looking economy, Mauritius moved toward an export oriented and

diversified economy producing textiles, tourism, financial and ICT services.

However, the country’s economic model has been showing signs of distress, associated with the

loss of preferential trade access, negative terms of trade and growing international competition in

low cost industries. The country’s GDP growth has slowed, employment creation remains subpar,

and growing inequality is slowly eroding the standard of living for the poor and the most

vulnerable. As a result, the middle class has shrunk during the last five years, and some are

vulnerable to falling back into poverty.

Regarding the Mauritian banking and financial systems, it remained well-capitalised and sound.

The 2014 IMF Mauritius Article IV Report found that the Mauritian banking system is healthy and

resilient to a range of shocks to their credit portfolios. Banks are well capitalised, with 17% of

Regulatory Tier I capital to risk-weighted assets, well above the proposed Basel III requirements.

The capital adequacy ratio (CAR) has increased following the global financial crisis and stood at

16.5% as of September 2014, well above the regulatory minimum of 10%. Based on BoM

estimates, the aggregate CAR could absorb losses of up to 15% of the current balance sheet of

banks. Also, the overall liquidity ratio rose from 17% end-2012 to 20% in June 2014, but has not

fully recovered to the level of 2008 and 2009.

Furthermore, the return-on-equity (ROE) declined to 19.7% by mid 2014, compared with a ROE

of 20.3% recorded a year earlier, reflecting a decline of bank earnings and profitability. Total credit

has continued to trend upwards but the quality of assets held by the banks, particularly in the

construction and tourism sectors, has deteriorated, leading to a slight rise in the non-performing

loan (NPL) ratio to 3.9%, but this ratio remains relatively low by international comparisons. The

GCR 2014-15 highlighted the country’s financial market deepening on the back of improved

access to the different modes of financing and financial services. The country ranked 26th

worldwide in terms of financial sector depth. Commercial banks continue to be the most dominant

player in the Mauritian financial services sector, with assets amounting to MUR 1 125 billion or

278% of GDP. However, alternative sources of finance, such as the Stock Exchange of Mauritius

9

(SEM), are increasing their presence on their financial stage, itself an indicator of financial depth

and efficiency.

Lastly, we can say that Mauritius is often cited as a success story and has performed exceptionally well in

many corners. The financial services sector is one of them and is now a major pillar of the economy. Today,

when Mauritius stands at crossroads, the domain of financial services has the potential to continue

performing miracles for our small island nation. To make this possible, government and stakeholders have

been active in looking at strategies to boost the financial services sector and create opportunities for

employment. In terms of global ranking, Mauritius is a reference in the African region whereby it

is ranked 1st in the African region and 29th overall in the World Bank Doing Business Survey 2015.

Also, Mauritius was ranked 1st in the Mo Ibrahim Index 2014 for good governance and by Forbes

Survey of Best Countries for Business 2014 in Africa.

10

3.0 Domestic Economy

During 2014, the Mauritian economy performed relatively well in terms of output growth and

inflation and is benefitting from low international oil prices during 2015. Low international oil

prices are likely to have beneficial effects on economic growth, inflation, and the balance of

payments. To date, the monetary policy stance has remained accommodative with economic

growth still below potential and inflation low by historical standards. Fiscal policy was broadly

conservative in 2014, with the overall budget deficit equivalent to around 3.2 per cent of GDP -

remaining along past trends.

3.1 Output and Inflation

Latest national accounts estimates show that Mauritius registered a commendable annual growth

rate of 3.5 per cent in 2014. Economic growth stemmed mainly from the positive contribution to

growth by a number of sectors, including, “financial and insurance activities” (0.5 percentage

point), “manufacturing” and “wholesale and retail trade” (0.4 percentage point each); and

“information and communication”, “public administration”, “human health and social work

activities”, and “professional, scientific and technical activities” (0.3 percentage point each). The

construction sector, however, contributed negatively to growth for a fourth consecutive year. On

the demand side, strong growth of net exports and final consumption expenditure offset a

contraction of gross domestic fixed capital formation (GDFCF).

For 2015, Bank of Mauritius staff expected a marginal acceleration of economic growth supported

by low international oil prices. Falling international oil prices in 2014 have been passed through

to domestic customers and are likely to raise growth in private consumption, commerce and trade-

related activities. The contraction of the construction sector may also be contained, following a 4-

year cumulative retrenchment of more than 20 per cent, although risks remain given the debt

overhang confronting leading local corporations that may hamper investment growth.

Y-o-y overall inflation fell by 4.9 percentage points, from 5.1 per cent to 0.2 per cent over the year

to December 2014, along with a fall in food and energy inflation. Concurrently, CORE2 inflation,

which excludes food, beverages, tobacco, mortgage interest payments, energy prices and

administered prices, fell from 3.4 per cent to 2.1 per cent during the same period. Headline inflation

11

(i.e., a 12-month moving average of overall inflation) was relatively flat throughout 2014,

remaining at 3.2 per cent by December 2014.

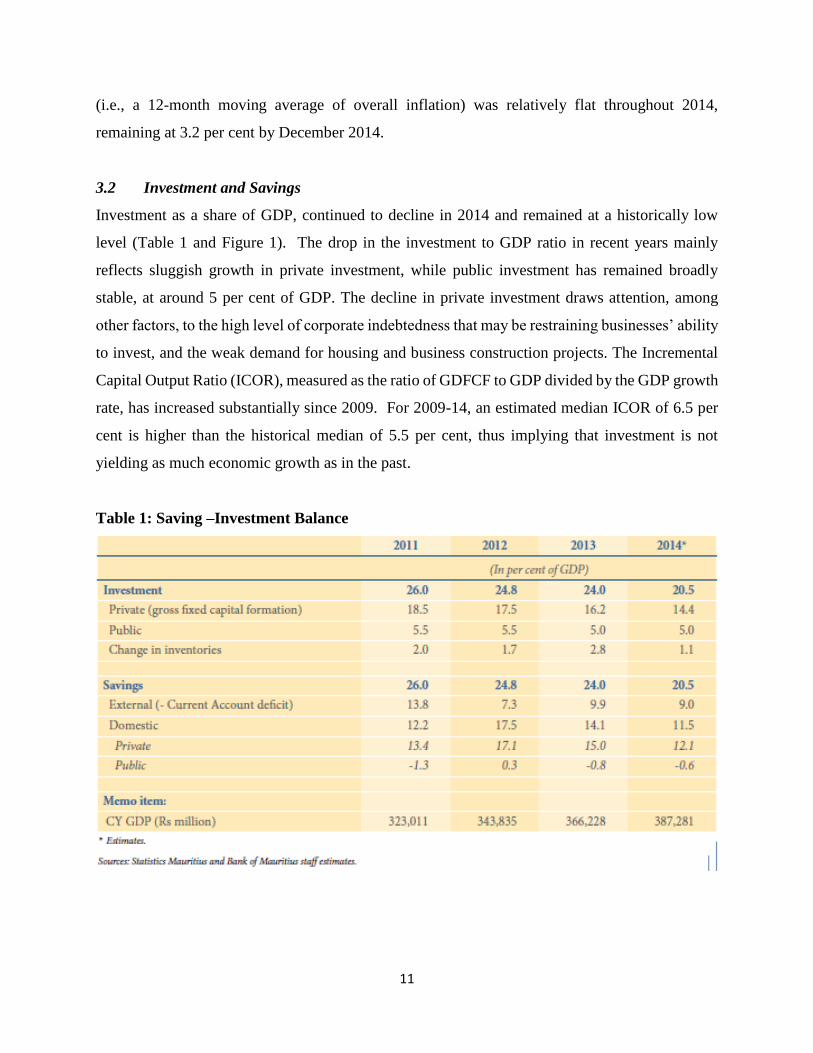

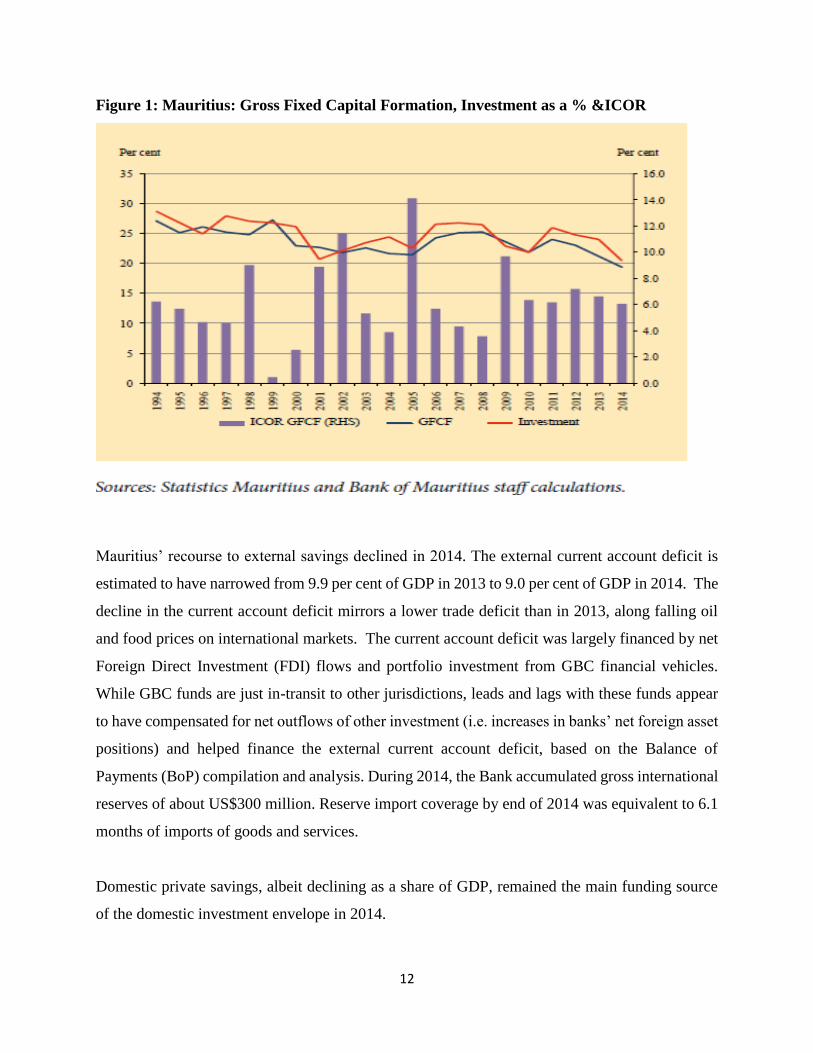

3.2 Investment and Savings

Investment as a share of GDP, continued to decline in 2014 and remained at a historically low

level (Table 1 and Figure 1). The drop in the investment to GDP ratio in recent years mainly

reflects sluggish growth in private investment, while public investment has remained broadly

stable, at around 5 per cent of GDP. The decline in private investment draws attention, among

other factors, to the high level of corporate indebtedness that may be restraining businesses’ ability

to invest, and the weak demand for housing and business construction projects. The Incremental

Capital Output Ratio (ICOR), measured as the ratio of GDFCF to GDP divided by the GDP growth

rate, has increased substantially since 2009. For 2009-14, an estimated median ICOR of 6.5 per

cent is higher than the historical median of 5.5 per cent, thus implying that investment is not

yielding as much economic growth as in the past.

Table 1: Saving –Investment Balance

12

Figure 1: Mauritius: Gross Fixed Capital Formation, Investment as a % &ICOR

Mauritius’ recourse to external savings declined in 2014. The external current account deficit is

estimated to have narrowed from 9.9 per cent of GDP in 2013 to 9.0 per cent of GDP in 2014. The

decline in the current account deficit mirrors a lower trade deficit than in 2013, along falling oil

and food prices on international markets. The current account deficit was largely financed by net

Foreign Direct Investment (FDI) flows and portfolio investment from GBC financial vehicles.

While GBC funds are just in-transit to other jurisdictions, leads and lags with these funds appear

to have compensated for net outflows of other investment (i.e. increases in banks’ net foreign asset

positions) and helped finance the external current account deficit, based on the Balance of

Payments (BoP) compilation and analysis. During 2014, the Bank accumulated gross international

reserves of about US$300 million. Reserve import coverage by end of 2014 was equivalent to 6.1

months of imports of goods and services.

Domestic private savings, albeit declining as a share of GDP, remained the main funding source

of the domestic investment envelope in 2014.

13

3.3 Fiscal Policy

During 2014, the Government continued to adopt a prudent macroeconomic management of its

fiscal policies, with the overall fiscal deficit declining over the first three quarters of the year.

Information through November 2014, confirms the ongoing decline in the overall deficit. On this

path, the overall fiscal deficit is expected to be broadly on target - at 3.2 per cent of GDP - by close

of the year. The primary deficit, which excludes interest payments from the overall fiscal deficit,

is also expected to maintain a declining trend in the fourth quarter of 2014. The budget deficit is

expected to be financed by domestic sources, mostly banks and non-banks, and by foreign sources.

3.4 Interest Rate Policy

During 2014, the Monetary Policy Committee kept the Key Repo Rate unchanged at 4.65 per cent

against the backdrop of weak global growth and contained domestic inflationary pressures. The

protracted period of low interest rates was broadly translated into low deposit and lending nominal

interest rates. This led to a relatively low borrowing cost, with a return on bank deposits close to

zero or negative in real terms.

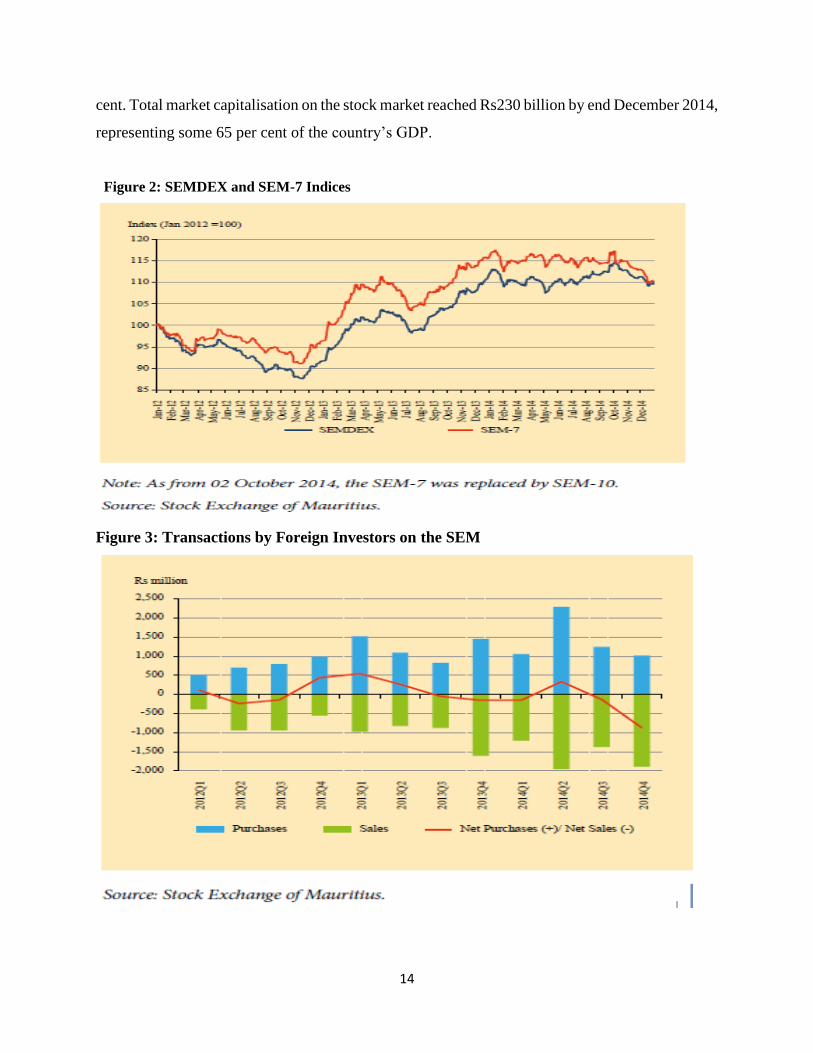

3.5 Domestic Stock Market

During 2014, the aggregate stock market index (SEMDEX) and that comprising the seven largest

companies listed in the stock exchange (SEM-7) remained near historical highs reached in late

2013 (Figure 2). During 2013, both indices increased on average by 20 per cent, while in 2014,

the SEM-7 declined by 4.4 per cent between end December 2013 and end December 2014. The

SEMDEX registered some gains (3.3 per cent q-o-q) during the 2014Q3, but ended up the year at

relatively the same level as of end-December 2013. The decline in the SEM-7 index happened

mainly in the last quarter of 2014, mirroring Moody’s downgrade of MCB and SBM in late

October 2014, on account of material declines in their capitalisation following completion of the

group restructuring, in addition to the disappointing financial results of the largest hotelier, New

Mauritius Hotels (NMH) as at September 2014.

Foreign investors were net sellers of domestic stocks during 2014, with net outflows of Rs824.5

million compared with net inflows of Rs603.6 million in 2013 (Figure 3). As at end-December

2014, the market was trading at a Price Earning (PE) ratio of 9.9 and a dividend yield of 2.99 per

14

cent. Total market capitalisation on the stock market reached Rs230 billion by end December 2014,

representing some 65 per cent of the country’s GDP.

Figure 2: SEMDEX and SEM-7 Indices

Figure 3: Transactions by Foreign Investors on the SEM

15

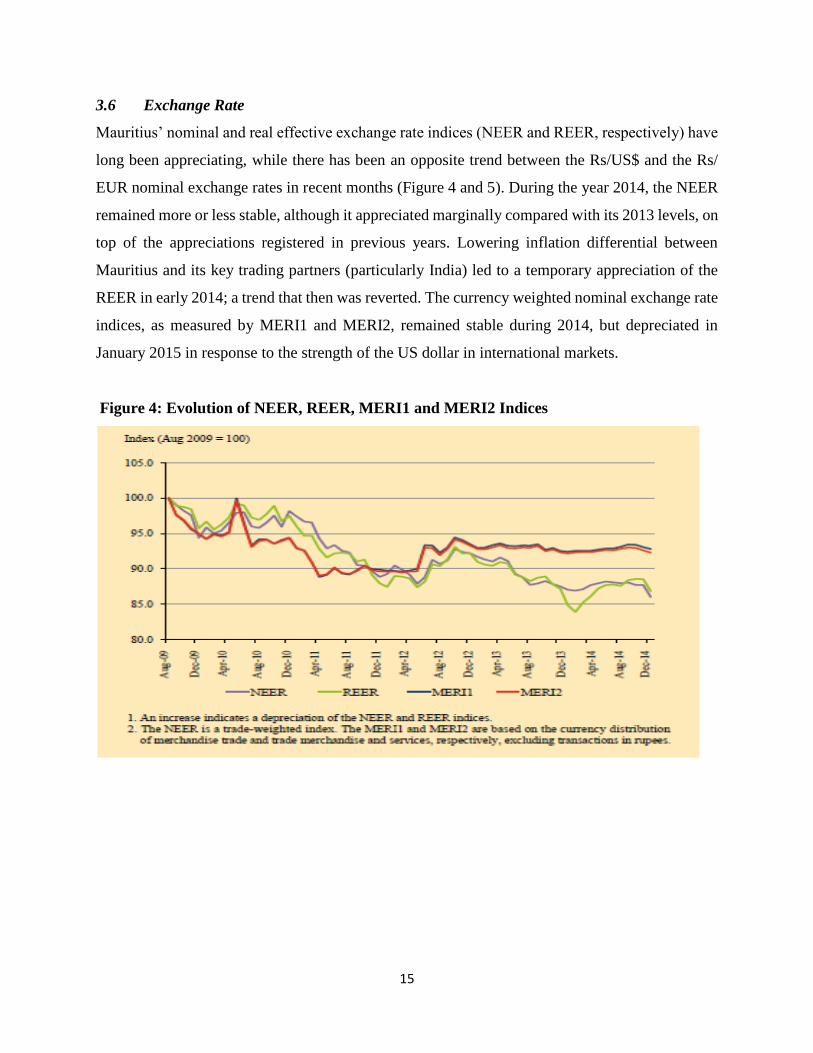

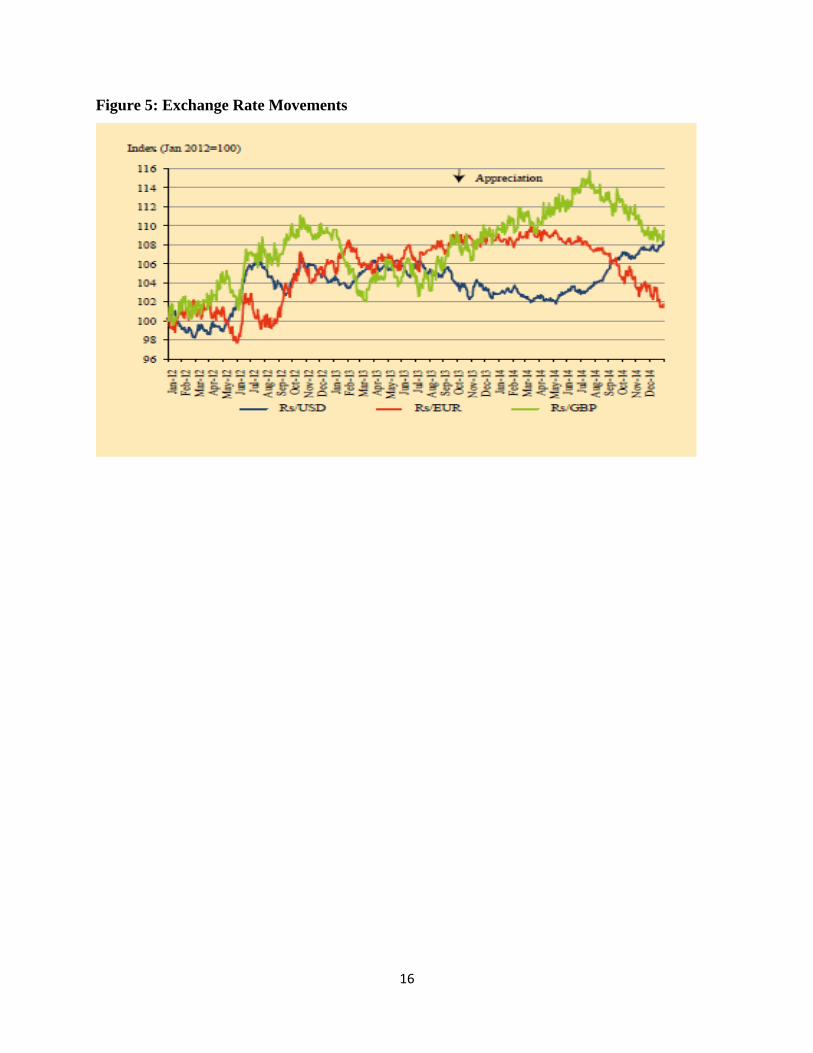

3.6 Exchange Rate

Mauritius’ nominal and real effective exchange rate indices (NEER and REER, respectively) have

long been appreciating, while there has been an opposite trend between the Rs/US$ and the Rs/

EUR nominal exchange rates in recent months (Figure 4 and 5). During the year 2014, the NEER

remained more or less stable, although it appreciated marginally compared with its 2013 levels, on

top of the appreciations registered in previous years. Lowering inflation differential between

Mauritius and its key trading partners (particularly India) led to a temporary appreciation of the

REER in early 2014; a trend that then was reverted. The currency weighted nominal exchange rate

indices, as measured by MERI1 and MERI2, remained stable during 2014, but depreciated in

January 2015 in response to the strength of the US dollar in international markets.

Figure 4: Evolution of NEER, REER, MERI1 and MERI2 Indices

16

Figure 5: Exchange Rate Movements

17

4.0 Overview of the Financial system of Mauritius

Mauritius is a small island which has witnessed a relentless struggle to achieve an ‘outward looking

strategy’ in the course of its economic development. Its economic history reflects different levels

of progression (ThinkQuest, 2001). Since independence the Mauritian economy has experienced

outstanding transformations. Moving from a mono- agricultural industry (sugar) to a service

industry; from high unemployment to low unemployment, Mauritius enjoyed a rapid growth and

a substantial diversification.

The financial system of the economy has evolved considerably over time. Initially the financial

system consisted mainly of banking sector with two main banks namely Mauritius Commercial

Bank and State Bank of Mauritius. However, as pointed out by Thinkquest (2001), the need for

non-bank financial institutions was being felt and in the late 1970s and early 1980s, there was an

increase in the number of insurance companies and other financial institutions. Thus, the structure

of the financial system started to experience some changes; the economy was witnessing a real

boom with the setting up of non-bank financial institutions. According to FSC (2008) and BOM,

since the mid 1980’s, financial activities in Mauritius have experienced a gradual shift away from

the dominance of banks and insurance companies.

A number of non-bank financial institutions have emerged to play a vital role in mobilizing

savings, stimulating investments and providing financial support to other productive economic

sectors. The responsibility to regulate bank and non-bank activities falls on different regulators. In

this regard, the regulatory approach has been product based, such as for banking and insurance.

As from the beginning of the 1990’s, the economy began to face new challenges: in particular,

increased wage and price pressures threatened the economy’s competitiveness in export markets.

With the economy at near full employment, the strategy was to regain the competitive edge through

enhanced labour productivity and export diversification.

In this respect, new investments was required to substitute existing technologies for more capital

intensive ones, as well as investments in new product lines. Ultimately, the then Government

decided to transform the economy into a ‘center for offshore banking and financial services’. The

Banking Act was revised in 1988, providing inter alia for the licensing of offshore banks and the

18

Stock Exchange was set up in 1989. Steps were also taken to prepare legislation for the

authorization of non-bank offshore companies .Hence, it was of utmost importance that the level

of domestic savings is increased and the allocation of investable funds be further improved (BOM,

annual report). Between 1990 and 2000, the combined contribution of the three main sectors of

the economy, namely Agriculture, Manufacturing and Tourism to GDP went down from 38.9% to

35.9%. It was expected that their share would continue to decline whereas that of the other services

sector would increase. The need for diversification was thus felt. Thus, proper macroeconomic

policies was put in place to diversify the economy’s export and productive bases. The offshore

financial services were developed as the fourth pillar of the economy contributing to the creating

of high value-added jobs (IMF, 2003). With the aim to diversify the economy, the Mauritius

Offshore Business Activities Authority {MOBAA} Act was endorsed in 1992 and the Freeport

was established in the same year, thereby emphasizing the external sources on which further

financial sector development would be based, in the context of global financial sector

liberalization.

Due to its competitive economy and good economic performance, the island can be classified as a

middle-income country. The current financial services include payment services, credit services,

asset accumulation, protection and real estate. In addition, corporate finance, risk management and

financial data processing are other types of financial services being provided to the business sector.

It is foreseen on present trends that these services could potentially be provided by new entrants

on the market in competition with the existing ones. For instance, payment services could in future

be provided not only by banks, but also by software companies, telecom companies and money-

changers. The range of services provided by financial institutions has also been growing in past

years. In the insurance sector, in addition to the traditional life and non-life insurance products,

companies also provide asset accumulation, reinsurance, consultancy services, risk assessment and

claim settlement services.

In the banking sector, the scope of services has widened to include asset accumulation ,

participation in issues of securities, settlement and clearing services, provision and transfer of

financial information, custodial services and financial data processing (FSC, 2008; BOM,

Thinkquest, 2001). Hence, according to the IMF report 2008, Mauritius had a ‘relatively large and

19

well-developed financial system’. The basic financial sector infrastructure was modern and

efficient, and the financial services were easily accessible with more than one bank account per

capita. However, despite after the two decades of solid growth, Mauritius’s economy has slowed

down as a result of ‘a terms of trade (TOT) deterioration’.

This may be due to the expiration of the Multi-fibre Agreement1, and the decrease in price of sugar

export for the period 2006-2010 to the European Union’s, and rise in oil prices. They, along with

high fiscal deficits and slow changes in consumption, have increased the current account deficit

and external vulnerability.

In 2001, Mauritius established a steering committee which recognized that the Mauritian financial

services industry has the potential to develop into a viable and dynamic sector capable of

generating a large number of high value-added jobs. As a means to unlock this potential, the

Committee recommended a unified approach to the regulation and the supervision of the financial

services industry. It therefore recommended the setting up of a Financial Services Commission, of

which the Bank of Mauritius shall be the anchor, to which will be entrusted the task of bringing

under a common roof the supervision of the insurance, securities market and offshore sector

activities in a bid to bring about integrated financial services supervision in a phased manner.

The Financial Services Commission (FSC) operates under the Financial Services Act 2007. It was

established as the supervisory body for the global business and the non-bank financial services

sector. Its main duties are to license, regulate, monitor and supervise the conduct of business

activities. The FSC’s remit includes those of the earlier regulatory bodies namely: securities (Stock

Exchange Commission), insurance (Insurance Division of the Ministry of Economic Development,

Financial Services and Corporate Affairs) and global business (Mauritius Offshore Business

Activities Authority’. The main aim of the FSC is to foster the development of the economic

environment, ensure the stability, fairness, efficiency and transparency of financial institutions and

capital markets in Mauritius. This will help to maintain the integrity of the island as a sound and

competitive International Financial Centre of repute. The non-bank financial institutions focus in

using specialize financial agreement such as ‘financial leasing, securitised lending, and financial

derivatives’ and providing loans to particular types of borrowers. Hence, their tasks are to channel

20

funds from lenders to borrowers. To achieve this, they accept long-term or specialized types of

deposits and by gaining liabilities on their own account ‘through the issuing of bills, bonds or other

securities’. With a view to ensuring that FSC operates efficiently and effectively, emphasis is laid

on the flexibility of its internal organizational structure. A project-based approach to all major

initiatives has been adopted. In order to ensure the effective and timely implementation of these

initiatives, cross-functional teams have been constituted to work on the projects. The FSC is

committed to giving all members of staff opportunities to contribute and add value to the various

initiatives (FSC).

21

5.0 Banking Sector

5.1 Evolution of the Banking Sector

The Bank of Mauritius was established in 1966 under the Bank of Mauritius Act. It is headed by

a Governor, who is also the Chairman of the Board of Directors. The Governor is appointed by the

Prime Minister as the principal representative of the Bank and is responsible for the general

supervision of the Bank. The Managing Director, who is also appointed by the Prime Minister, is

responsible for the day- to-day management of the Bank’s affairs and business.

The Bank of Mauritius, established under the Bank of Mauritius Ordinance 1966, started its

operations on 14 August 1967. In 1971, the Bank’s headquarters building was completed at Sir

William Newton Street and was inaugurated in 1972. The establishment of the Bank of Mauritius

marked the beginning of a new phase in the monetary history of Mauritius. The Bank was vested

with ‘the sole right to issue legal tender currency in the country and was charged with the

responsibility of maintaining the internal and external value of the currency and its international

convertibility’.

As per section 4 of the Bank of Mauritius Act 2004, the primary object of the Bank is to maintain

price stability and to promote orderly and balanced economic development. Other objectives of

the Bank are (a) to regulate credit and currency in the best interests of the economic development

of Mauritius; (b) to ensure the stability and soundness of the financial system of Mauritius; and (c)

to act as the central bank for Mauritius.

To fulfil its mandate, the Bank performs a number of core functions that include (a) conducting

monetary policy and managing the exchange rate of the rupee, taking into account the orderly and

balanced economic development of Mauritius; (b) regulating and supervising financial institutions

carrying on activities in, or from within, Mauritius; (c) managing, in collaboration with other

relevant supervisory and regulatory bodies, the clearing, payment and settlement systems of

Mauritius; (d) collecting, compiling and disseminating, on a timely basis, monetary and related

financial statistics; and (e) managing the foreign exchange reserves of Mauritius.

22

The Bank also formulates and implements appropriate policies to promote economic growth while

taking into account global and regional developments, the domestic real economy and the financial

sector. In addition, the Bank constantly monitors factors that may impact negatively on the

financial soundness of institutions falling under its purview. It is further necessary for the Bank to

safeguard the rights and interests of depositors and creditors of financial institutions.

Further, right from its primary responsibility of issuing currency notes, the role of the Bank has

evolved with time as its mandate broadens and deepens in spheres such as repressing improper

practices through market intelligence and investigations, promoting regional cooperation, and

contributing to enhance financial literary. With a view to fostering the sustained growth of the

banking sector, and as custodian for the welfare of bank customers, the Bank launched the Banking

Your Future campaign by advocating for reforms that will bring fairer deals between stakeholders

and improve the bank-customer relationship. By improving its channel of communication through

forward guidance and being more transparent, the Bank is making further headway towards

building an inclusive and modern banking sector.

5.2 Financial Stability

The domestic financial system remains sound and resilient. Despite the still challenging economic

environment, banks in Mauritius remained broadly profitable and well capitalised, albeit

confronting excess liquidity. Banks continued to operate with ample funding from domestic and

international sources. Deposits from customers rather than short-term wholesale funding remained

the main source of banks’ funding. Excess liquidity increased and remained significantly high in

the domestic money market on account of part of the foreign exchange interventions that were not

sterilised, foreign financing of the budget deficit, and low private sector credit growth. Excess

liquidity has exerted downward pressures on interbank rates and led to concerns about the

effectiveness of monetary policy transmission mechanism.

In regards to credit expansion, though they have slowed down, the high growth rates recorded in

the past few years have led to an accumulation of debt in household and corporate sectors posing

challenges to banks. In the household sector, a shift from housing to consumption loans has

23

warranted greater vigilance amid signs of lower growth in household disposable income and

eventual increase in nominal interest rate.

As far as the Non-bank deposit-taking institutions are concerned they are performing well and are

adequately capitalised. According to the Financial Services Commission, the insurance sector

recorded a sound performance with improving profitability. The interlinkages between banks and

insurance companies were not considered as significant and contagion risks are deemed to be

moderate.

The banking sector remained generally sound and profitable during 2013-14, although challenges

remain in terms of credit concentration risk, increasing non-performing loans (albeit from a low

base), and still high but declining return to asset and return to equity ratios.

The Bank of Mauritius issued a number of new guidelines and reviewed existing ones with a view

to enhancing the financial soundness of financial institutions falling under its purview:

Guideline on Scope of Application of Basel III and Eligible Capital

In response to shortcomings identified during the global financial crisis 2008-09, the Basel

Committee on Banking Supervision (BCBS) introduced a number of fundamental reforms to the

international regulatory framework, commonly known as Basel III. The reforms aim at

strengthening global capital and liquidity rules, while improving the ability of the banking sector

to absorb shocks arising from financial stress. Banks are expected to become more resilient,

thereby reducing spillover risks from the financial sector to the real economy.

In line with the objective of the Basel III reform package, the Bank issued a Consultation Paper on

the Implementation of Basel III in Mauritius in October 2012, which was followed by a draft

Guideline on Scope of Application of Basel III and Eligible Capital in May 2013. Following

consultation with the industry, the guideline was finalised and came into effect on 1 July 2014.

Through transitional arrangements to be phased in until 1 January 2019, the guideline aims at

raising the quality of capital, with strong focus laid on common equity. During the transitional

24

period, the banking sector is expected to meet the higher capital standards through reasonable

earnings retention and capital raising exercise.

The guideline also introduces a Capital Conservation Buffer (CCB), designed to ensure that banks

build up capital buffers to be drawn down if losses are incurred during a period of stress.

Guideline for dealing with Domestic-Systemically Important Banks

Large and complex banks can have systemic impact on the domestic economy because of their

size, interconnectedness, complexity and lack of substitutability. In this context, the BCBS had, in

November 2011, issued rules on the methodology for assessing Global Systemically Important

Banks (G-SIBs) and their loss absorbency requirements.

Based on the recommendations of the BCBS, the Bank has issued a Guideline for dealing with

Domestic-Systemically Important Banks (D-SIBs) that came into effect on 30 June 2014. The

guideline sets out the assessment methodology to be applied by the Bank for classifying an

institution as being systemically important. In order to identify D-SIBs, five equally-weighted

parameters have been identified namely (1) size; (2) interconnectedness; (3) substitutability/

financial institution infrastructure; (4) structure and complexity; and (5) large exposures. The D-

SIB framework focuses on the impact that the failure of large banks will have on the domestic

economy. Based on the importance of the D-SIB, a capital surcharge will be applied to the bank

and calibrated accordingly.

Guideline on Credit Concentration Risk

This guideline was reviewed to prescribe new regulatory credit concentration limits, and which

came into effect as from 1 January 2014. For banks, other than subsidiaries and branches of foreign

banks, aggregate large credit exposure to all customers and groups of closely-related customers,

denominated in Mauritian Rupee and currencies other than the Rupee, shall not exceed 600 per

cent of the bank’s capital base, or the group’s capital base. For subsidiaries and branches of

foreign-owned banks, the aggregate large credit exposures denominated in Mauritian Rupee, to all

customers and groups of closely-related customers, shall not exceed 600 per cent of the bank’s

capital base.

25

Concurrently, the aggregate large credit exposures of NBDTIs to all customers and groups of

closely-related customers shall not exceed 600 per cent of the institution’s capital base. With effect

as from 1 January 2015, the abovementioned limit of 600 per cent will be reduced further to 400

per cent. On 26 November 2013, a new section on sectoral concentration was introduced following

the implementation of macroprudential measures issued by the Bank in October 2013.

Guideline on Standardised Approach to Credit Risk

The guideline was reviewed to incorporate new risk weights prescribed by the macroprudential

measures in respect of claims secured by residential property and commercial real estate for

construction purposes in Mauritius.

Guideline on Complaints Handling Procedures

Following an amendment brought to the Banking Act 2004, a Guideline on Complaints Handling

Procedures was issued by the Bank that came into effect on 1 November 2013. Banks were

henceforth required to appoint a Complaints Officer to handle complaints and grievances from

their customers, and to report information thereof to the Bank on a quarterly basis.

Guideline on Disclosure of Information to Guarantors

Effective as from 1 January 2014, a Guideline on Disclosure of Information to Guarantors was

issued by the Bank that prescribed the instances for issuing statements of accounts in written or

electronic form to guarantors of credit facilities.

Guideline on Agent Banking

In accordance with Section 7(7B) of the Banking Act 2004, the Bank issued a Guideline on Agent

Banking which sets the criteria to be observed by a bank when outsourcing its activities to service

providers or an agent. The guideline also provides minimum standards and requirements for agent

banking operations.

Guideline on Fit and Proper Person Criteria and Fit and Proper Person Questionnaire

The Guideline was reviewed in June 2014, calling for additional information to facilitate the

process for assessing the independence, fitness and probity of senior officers, directors and

26

shareholders who exercise significant influence, and for determining any conflict of interest in the

exercise of their functions. The Questionnaire was also revised to simplify the reporting of

information on shareholding structure of financial institutions.

Guideline on Transactions or Conditions respecting Well-being of a Financial Institution

Reportable by the External Auditor to the Bank of Mauritius.

The guideline was reviewed in February 2014 to incorporate, inter alia, three new sections dealing

with major conflict among directors and dissension among shareholders, aggressive strategies

detrimental to the interest of depositors and financial institutions, and risks associated with

complex group structures and overseas operations.

Guideline on Control of Advertisement

The guideline was amended in March 2014, stipulating that advertisement that invites deposits in

foreign currency should not be made through billboards.

Guideline on Maintenance of Accounting and Other Records and Internal Control Systems

This guideline was issued in November 2013 and superseded the Guidance Notes on General

Principles for Maintenance of Accounting and Other Records and Internal Control Systems.

5.3 Performance of the Banking Sector

Banking sector assets grew by 8.5 per cent at end-September 2014 compared with an increase of

10.9 per cent in the corresponding period in 2013, with most of the increase reflecting growth in

foreign assets of subsidiaries of foreign-owned banks and that of domestic-owned banks. Total

assets held by branches of foreign-owned banks contracted by 6.2 per cent, although their

contribution to overall trends was rather small given the size of their balance sheet. The growth

in banks’ foreign assets, particularly those of domestically-owned banks, reflects ventures by local

banks in India and frontier markets in Africa with concomitant increases in credit and market risk.

Banks’ role as financial intermediaries in the domestic economy is being curtailed by the trends in

growth of households and corporate bank credit. The growth of banks’ claims on the private sector

(including households and corporations) has been declining and may have become negative in

27

recent months. Banks’ net foreign asset positions remain sizeable, while banks’ claims on the

Government and the central bank have generally registered positive growth in recent years. Gross

foreign asset positions averaged US$25 billion during 2010-14, with a net value of about US$10

billion. Banks’ claims on Government refer mainly to holdings of Government securities, while

banks’ claims on the central bank are cash reserve requirements with the monetary authority and

holdings of BoM securities.

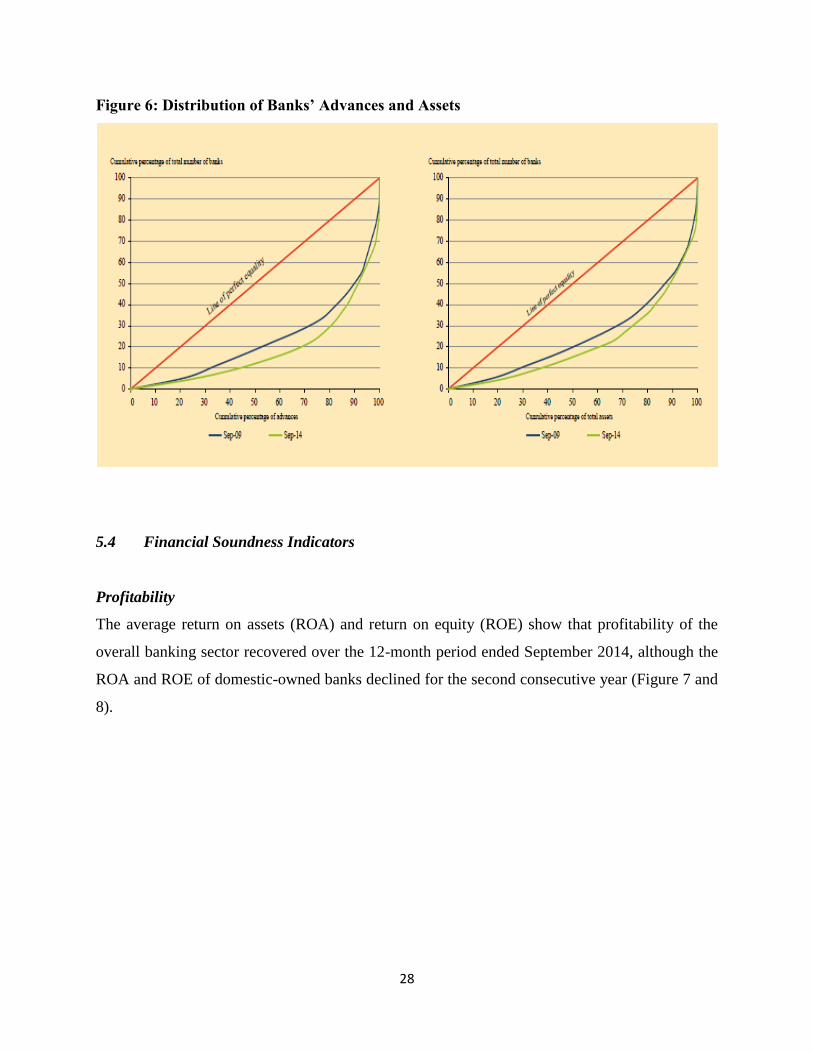

Market Concentration

The domestic banking sector is characterised by a high degree of market concentration. The four

largest banks held 56.5 per cent of total banking assets while the corresponding Herfindahl

Hirschman Index (HHI) stood at 1073 as at end September 2014. The degree of concentration in

the banking industry is further depicted in the Lorenz Curve (Figure 6). Over the past five years

ended September 2014, the market share of advances by four banks has increased from 57.0 per

cent to 65.0 per cent, which points to a more unequal distribution of bank assets. However,

notwithstanding the level of concentration of bank assets, smaller banks have increased their

visibility lately through assertive publicity campaigns to attract new customers. This may

eventually lead to a decline in market concentration, with increased competition in the banking

sector.

28

Figure 6: Distribution of Banks’ Advances and Assets

5.4 Financial Soundness Indicators

Profitability

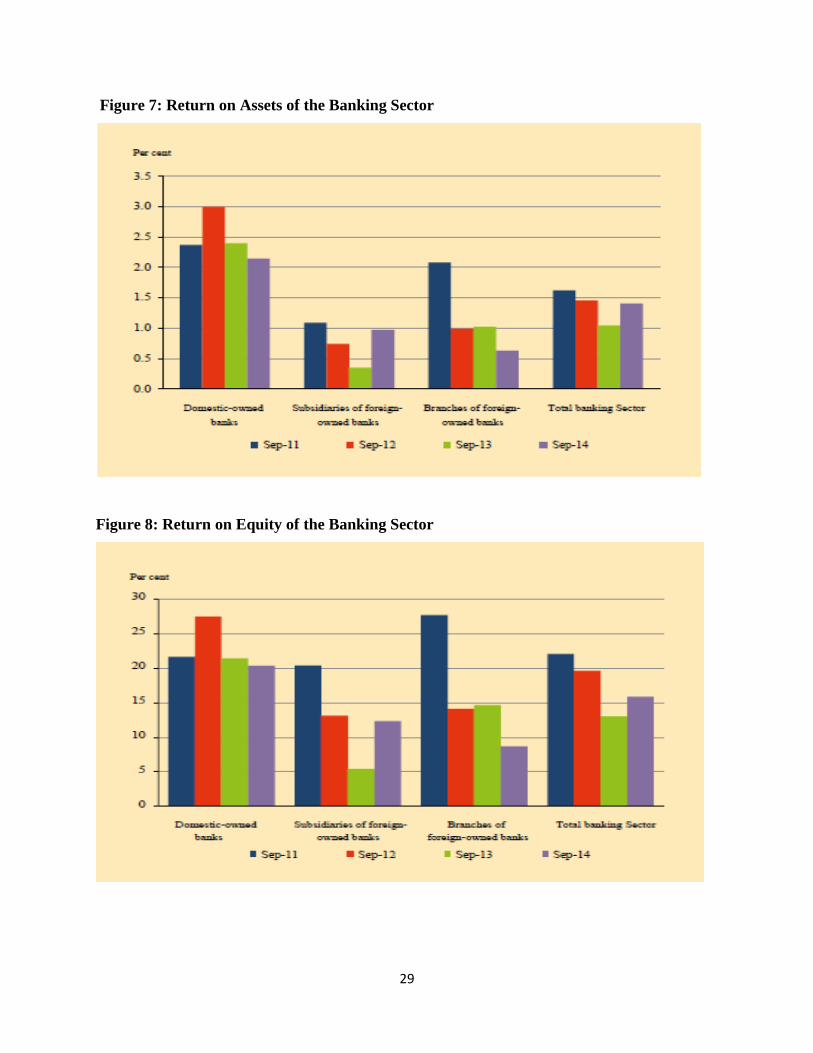

The average return on assets (ROA) and return on equity (ROE) show that profitability of the

overall banking sector recovered over the 12-month period ended September 2014, although the

ROA and ROE of domestic-owned banks declined for the second consecutive year (Figure 7 and

8).

29

Figure 7: Return on Assets of the Banking Sector

Figure 8: Return on Equity of the Banking Sector

30

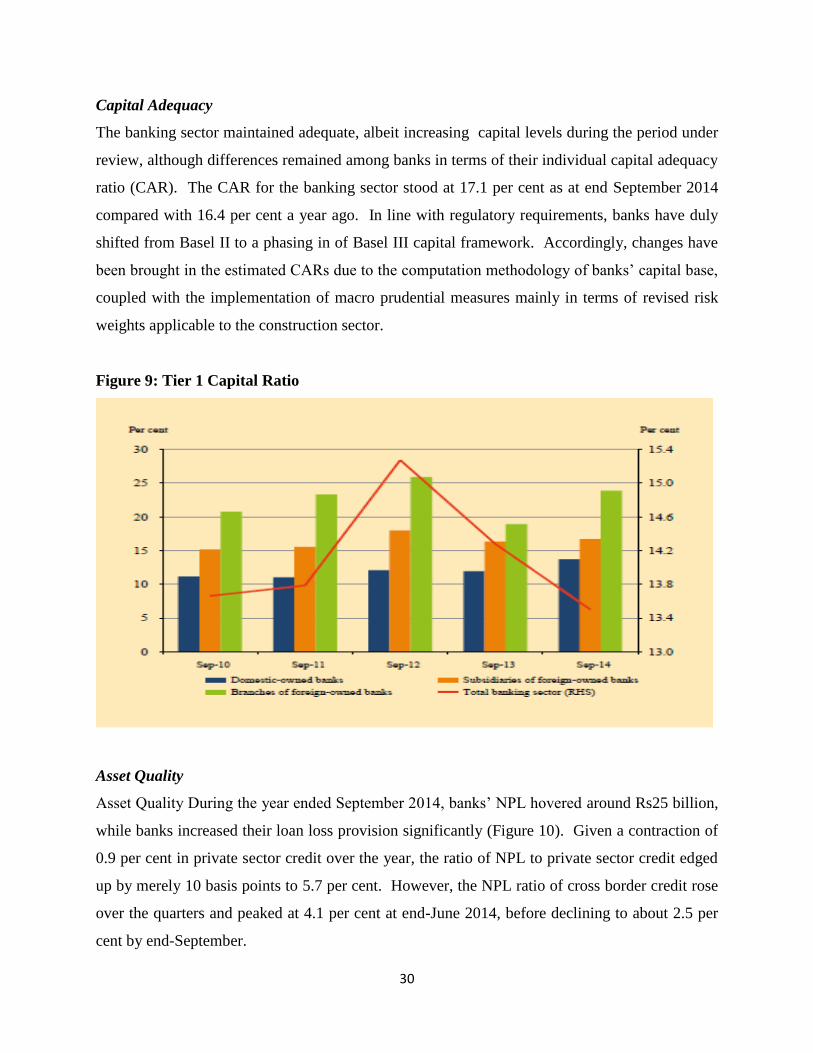

Capital Adequacy

The banking sector maintained adequate, albeit increasing capital levels during the period under

review, although differences remained among banks in terms of their individual capital adequacy

ratio (CAR). The CAR for the banking sector stood at 17.1 per cent as at end September 2014

compared with 16.4 per cent a year ago. In line with regulatory requirements, banks have duly

shifted from Basel II to a phasing in of Basel III capital framework. Accordingly, changes have

been brought in the estimated CARs due to the computation methodology of banks’ capital base,

coupled with the implementation of macro prudential measures mainly in terms of revised risk

weights applicable to the construction sector.

Figure 9: Tier 1 Capital Ratio

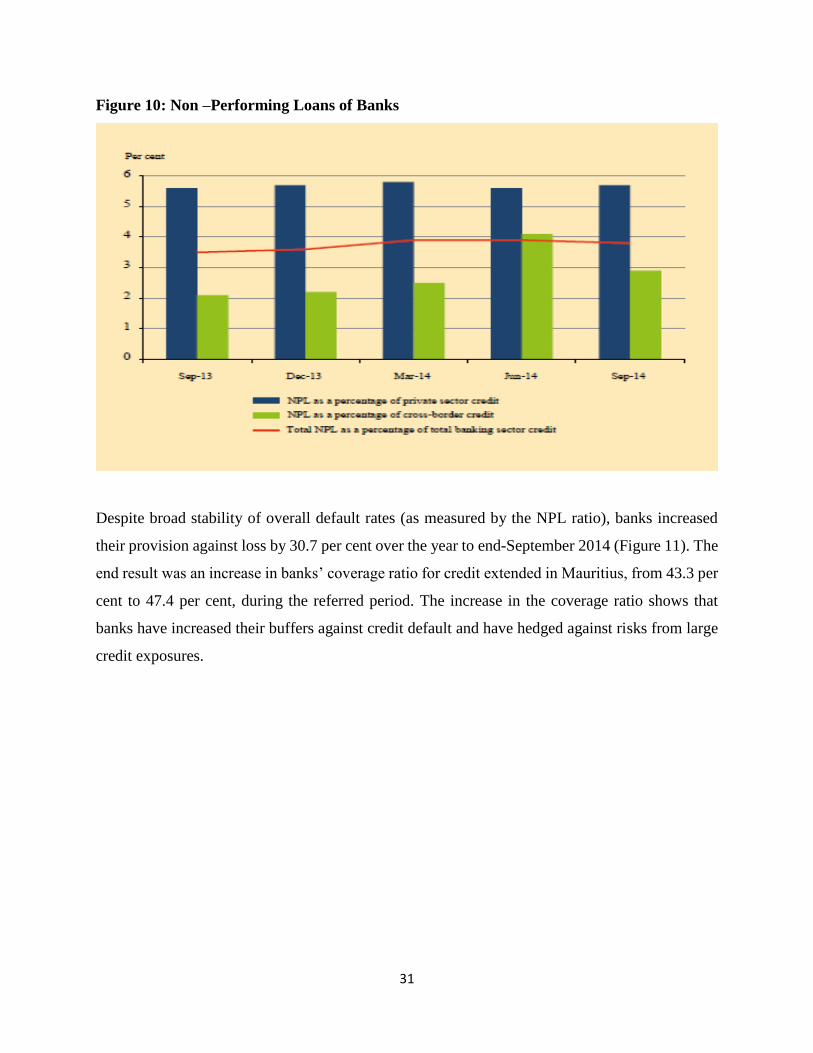

Asset Quality

Asset Quality During the year ended September 2014, banks’ NPL hovered around Rs25 billion,

while banks increased their loan loss provision significantly (Figure 10). Given a contraction of

0.9 per cent in private sector credit over the year, the ratio of NPL to private sector credit edged

up by merely 10 basis points to 5.7 per cent. However, the NPL ratio of cross border credit rose

over the quarters and peaked at 4.1 per cent at end-June 2014, before declining to about 2.5 per

cent by end-September.

31

Figure 10: Non –Performing Loans of Banks

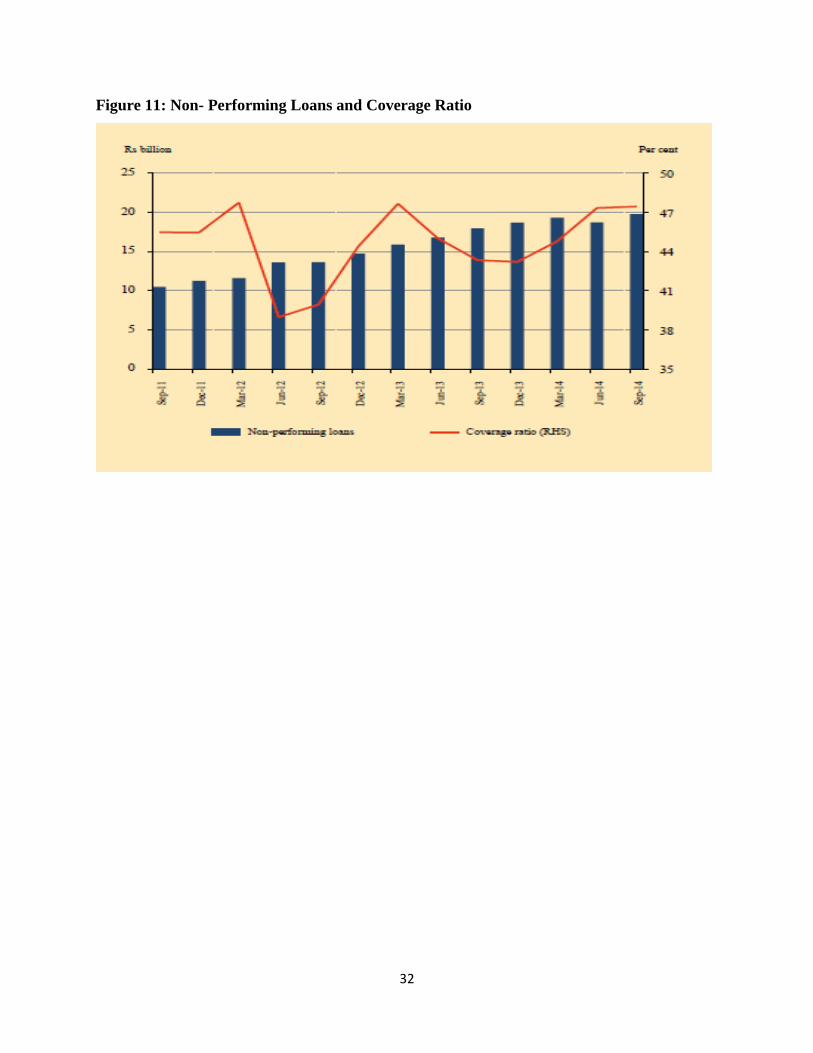

Despite broad stability of overall default rates (as measured by the NPL ratio), banks increased

their provision against loss by 30.7 per cent over the year to end-September 2014 (Figure 11). The

end result was an increase in banks’ coverage ratio for credit extended in Mauritius, from 43.3 per

cent to 47.4 per cent, during the referred period. The increase in the coverage ratio shows that

banks have increased their buffers against credit default and have hedged against risks from large

credit exposures.

32

Figure 11: Non- Performing Loans and Coverage Ratio

33

6.0 The Non-Bank Financial Sector

6.1 Financial Services Commission

The Financial Services Commission, Mauritius (FSC Mauritius) was established in 2001 and is

the integrated regulator for the financial services other than banking and the global business

sectors. The FSC Mauritius operates under the Financial Services Act 2007 (‘FSA’), the Securities

Act 2005 (‘SA’), the Insurance Act 2005 (‘IA’) and the Private Pension Schemes Act 2012

(‘PPSA’). The FSC Mauritius licenses, regulates, monitors and supervises the conduct of business

activities in the non-banking financial services and the global business sectors.

In carrying its mission, the FSC aims to:

- promote the development, fairness, efficiency and transparency of financial institutions

and capital markets in Mauritius

- suppress crime and malpractices so as to provide protection to members of the public

investing in non-bank financial products

- ensure the soundness and stability of the financial system in Mauritius for the benefit of

the economy.

The FSC is also committed to the sustained development of Mauritius as a sound and competitive

international financial services centre.

The Key Objectives of the FSC Mauritius are to:

Ensure orderly administration of the financial services and global business activities;

Ensure sound conduct of business in the financial services and global business sectors;

Elaborate policies which are directed to ensuring fairness, efficiency and transparency of

financial and capital markets in Mauritius; and

Study new avenues for development in the financial services sector, to respond to new

challenges and to take full advantage of new opportunities for achieving economic

sustainability and job creation.

34

The FSC regulates non-bank financial institutions whose roles are to channel funds from lenders

to borrowers by accepting long-term or specialized types of deposits and by incurring liabilities on

their own account through the issuing of bills, bonds or other securities. Such institutions often

specialize in lending to particular types of borrowers and in using specialized financial

arrangements such as financial leasing, securitised lending, and financial derivatives.

6.2 Securities Exchanges

The Securities market is a key to efficient capital formation and allocation in any economy. Dearth

of resources in growing sectors can hamper economic growth. Through stock markets,

governments and industry are able to raise long-term capital for financing new projects, and

expanding and modernizing industrial and commercial concerns.

As per the Securities Act 2005, the FSC is the regulator of the non-bank financial markets in

Mauritius which comprises Securities Exchanges, clearing and settlement facilities and securities

trading systems on the one hand and Collective Investment Schemes and intermediaries on the

other.

Therefore, as the regulator of the securities markets, the FSC strives to:

Foster fair, efficient, transparent and informed markets for securities in Mauritius;

Monitor and regulate the operations of securities exchanges and the activities of persons providing

clearing and settlement services and trading systems for securities;

Suppress and prevent financial crimes and illegal practices;

Regulate the disclosure of information by persons issuing securities and by reporting issuers to

securities holders and to the public;

Cooperate and collaborate with domestic and international organisations, law enforcement,

supervisory and regulatory bodies; and

Reinforce the protection of investors in Mauritius from unfair, improper and fraudulent practices.

There are two licensed Securities Exchanges in Mauritius : the Stock Exchange of Mauritius Ltd

(SEM) and the Bourse Africa Ltd.

35

6.2.1 Stock Exchange of Mauritius Ltd

SEM, one of the leading exchanges in Africa operates a fully automated stock market infrastructure

from trading to settlement which is in line with international standards. This system has

revolutionised trading practices in Mauritius and empowered investors to benefit from real time

trading.

SEM has gained international recognition by achieving membership status to the World Federation

of Exchanges since 2005 and has gone live on the Bloomberg index since 2009.

It operates two markets in the equity segment: the Official Market - meant for larger companies,

consisting of some 40 listed companies and the Development and Enterprise Mauritius (DEM)

catering for medium and small enterprises which comprises some 50 companies. The listed

companies span over the various sectors of the economy such as banks, insurance and other

finance, commerce, sugar, industry, investments and transport.

With the lifting of the Exchange Control in 1994, foreign investors can also trade on the SEM.

The Central Depository & Settlement Co Ltd(CDS) is a subsidiary of the SEM and is operational

since 1997. CDS was established to provide centralised depository, clearing and settlement

services for the Mauritian equity and debt markets. It complies with the international standards

(Group of 30 Recommendations; Core Principles for Systemically Important Payment

Systems/International Organisation of Securities Commission - CPSS/IOSCO Recommendations)

on depository, clearing and settlement systems. Trades are settled within a rolling T+3 settlement

cycle on a strict Delivery versus Payment (DvP) basis.

The SEM was characterised by a continuous upbeat path for the year 2013. Both Markets under

the SEM namely the Official Market and the Development & Enterprise Market, performed well

during the year. This could be attributed to a combination of a profit-motivated investor base with

good fundamentals, corporate restructuring and reported earnings results of some stocks. This

trend was also mirrored on the part of foreign investors who showed an appetite for Mauritian

securities. As such, a net amount of MUR 547.2 million was injected into the market. The initiative

36

of reducing brokerage fees on turnaround trades was another factor accounting for further trading

on the platform.

SEM currently lists, trades and settles equity and debt products in USD, Euro, GBP, ZAR and

MUR.

As part of its internationalisation programme, SEM provides a value-chain of products to promote

an attractive listing, trading and capital-raising platform which includes products and services for

Global funds, Global Business Companies, Mining and Mineral companies, specialist-debt

products, Depositary receipts among others. In 2013, the introduction of Exchange Traded Funds

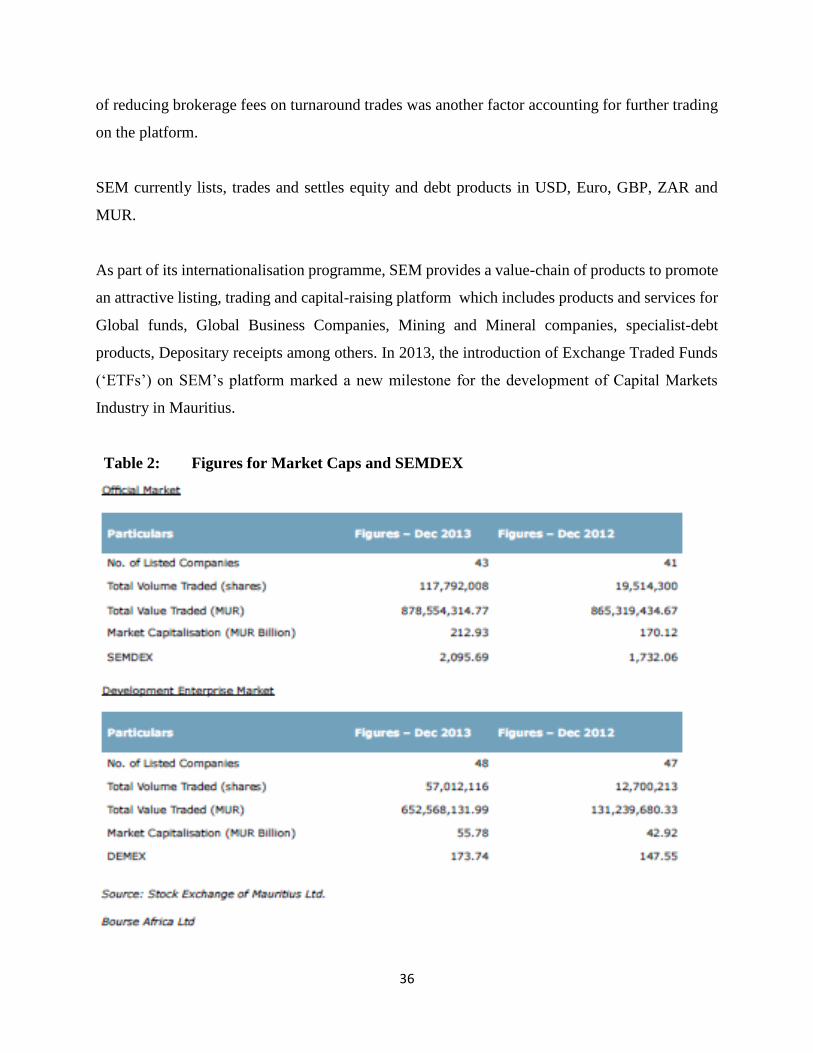

(‘ETFs’) on SEM’s platform marked a new milestone for the development of Capital Markets

Industry in Mauritius.

Table 2: Figures for Market Caps and SEMDEX

37

6.2.2 Bourse Africa Ltd

The Bourse Africa Ltd was launched in October 2010 and is promoted by the Financial

Technologies Group of India. It is licensed as an international multi-class exchange which offers

and trades in three segments namely, the Commodity Derivatives Segment, the Currency

Derivatives Segment, and the Equity Segment. For the Commodity Derivatives Segment, three

contracts namely in gold, silver and Crude Oil (WTI) are offered while for the Currency

Derivatives Segment, five currency pairs are traded namely EUR/USD, GBP/USD, JPY/USD,

USD/MUR, ZAR/ USD.

The Bourse Africa Ltd is the first exchange to offer derivative products in Mauritius. It has a state-

of-the-art trading platform with clearing and settlement systems, providing access to several of the

world's fastest growing economies.

The licensing of the Bourse Africa Ltd by the FSC was a major milestone in the development of

the capital markets industry in Mauritius. Bourse Africa Ltd promotes Mauritius as a financial hub

as it helps the investment community to hedge price risk movements in international markets and

provides an opportunity for investors to capitalise on arbitrage opportunities.

For the year 2013, the performance of BAL was relatively positive with total turnover varying

between USD 300 million and USD 700 million, the highest turnover being recorded in May 2013.

The greatest total volume traded was in December with 144,284 lots traded.

6.2.3 Investment Funds and Intermediaries

Investment Funds and their Intermediaries (CIS Managers, CIS Administrators and Custodians)

are regulated by the FSC under the Securities Act 2005 and the Securities (Collective Investment

Schemes and Closed-End Funds) Regulations 2008, which provide for a consolidated regulatory

and supervisory framework.

38

In line with the International Organisation of Securities Commissions (IOSCO) Principles, the

FSC aims at:

Setting standards for the governance, organisation and operational conduct of those who wish to

market or operate a fund;

Providing a legal framework governing the legal form and structure of funds;

Ensuring that sufficient disclosures and information are provided for investors to evaluate the

suitability of an investment;

Regulating fund intermediaries; and

Protecting the best interest of investors and the financial market.

Investment Funds

Under the Securities (Collective Investment Schemes and Closed-end Funds) Regulations 2008

(the CIS Regulations), investors have the possibility to select the type of Investment Funds,

whether Collective Investment Schemes (CIS) or Closed-end Funds (CEF), that best suits their

profile, risk tolerance and return objective.

In May 2013, the FSC Mauritius became signatory to the Memorandum of Understanding (‘MoU’)

with the European Securities Markets Authority (more specifically Economic Area Member

States). The MoU relates to the supervision of hedge funds, private equity and real estate funds

under the Alternative Investment Fund Managers’ Directive. This agreement enables Mauritius-

licensed funds to continue to market in Europe under the private placement regimes of EU Member

States after the introduction of the EU AIFMD in July 2013.

Further, the FSC Mauritius issued the Financial Services (Special Purpose Funds) Rules 2013.

Special Purpose Fund was introduced in the Income Tax Act further to amendments brought about

by the Finance (Miscellaneous Provisions) Act 2012. These Rules allow both foreign and local

investors investing outside and within Mauritius to benefit of tax exemption, subject to applicable

terms and conditions.

39

6.3 Insurance

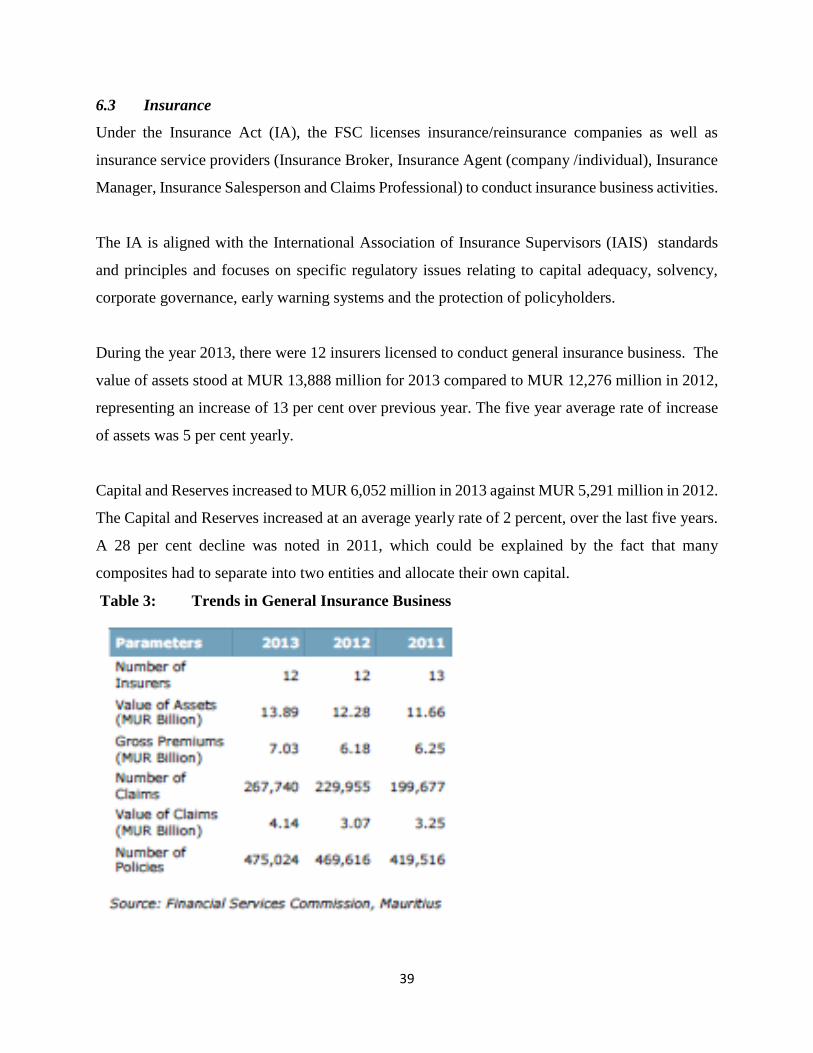

Under the Insurance Act (IA), the FSC licenses insurance/reinsurance companies as well as

insurance service providers (Insurance Broker, Insurance Agent (company /individual), Insurance

Manager, Insurance Salesperson and Claims Professional) to conduct insurance business activities.

The IA is aligned with the International Association of Insurance Supervisors (IAIS) standards

and principles and focuses on specific regulatory issues relating to capital adequacy, solvency,

corporate governance, early warning systems and the protection of policyholders.

During the year 2013, there were 12 insurers licensed to conduct general insurance business. The

value of assets stood at MUR 13,888 million for 2013 compared to MUR 12,276 million in 2012,

representing an increase of 13 per cent over previous year. The five year average rate of increase

of assets was 5 per cent yearly.

Capital and Reserves increased to MUR 6,052 million in 2013 against MUR 5,291 million in 2012.

The Capital and Reserves increased at an average yearly rate of 2 percent, over the last five years.

A 28 per cent decline was noted in 2011, which could be explained by the fact that many

composites had to separate into two entities and allocate their own capital.

Table 3: Trends in General Insurance Business

40

6.4 Pensions

Mauritius has a long tradition of voluntary private pension provisions. The majority of these

provisions are catered through defined benefit (DB) and defined contribution (DC) schemes

established by private companies to provide pensions for their employees. These private pension

schemes constitute the lifelong savings of individuals including those who may not be conversant

with the financial services. As such, it is extremely important for such pension schemes to be well

regulated and supervised in order to ensure their reliability as well as to safeguard the best interests

of beneficiaries.

As from 1 November 2012, the Private Pension Schemes Act 2012 ('PPSA') had come into force.

The PPSA provides for a comprehensive and modern regulatory and supervisory framework for

the operation of private pension schemes. The FSC ensure that private pension schemes comply

with provisions of the PPSA with a view to maintaining a fair, safe, stable and efficient private

pension industry in Mauritius

Under the PPSA, the FSC Mauritius is the authority which:

a) licenses and authorises private pension schemes;

b) enforces compliance with prudential requirements;

c) applies the fit and proper requirements to persons constituting the governing body of private

pension schemes; and

d) intervenes in the event of misconduct of a licensed or authorized private pension scheme.

The Private Pension Schemes Act is in line with the standards of international organisations such

the IOPS (International Organisation of Pension Supervisors) and the OECD (Organisation for

Economic Co-operation and Development).

As at date, five FSC Rules under the PPSA have been issued by FSC Mauritius. The regulatory

and supervisory framework for the private pensions industry is being further consolidated with the

drafting of other FSC Rules under the same Act.

41

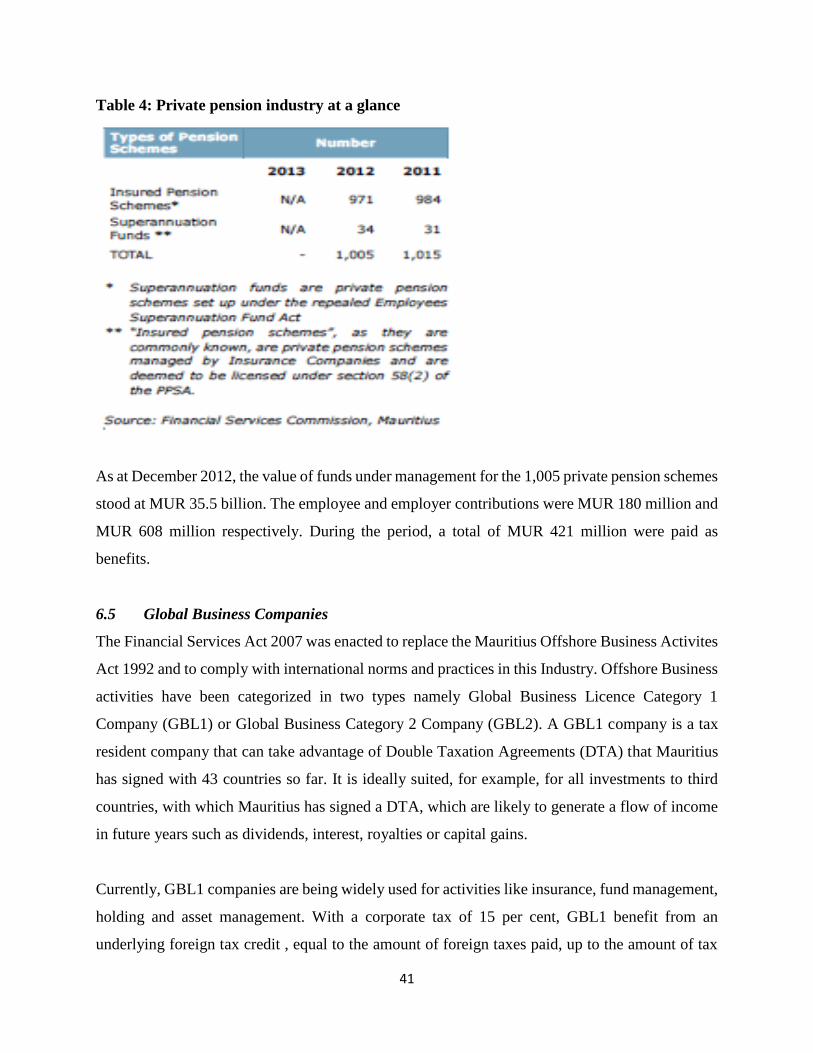

Table 4: Private pension industry at a glance

As at December 2012, the value of funds under management for the 1,005 private pension schemes

stood at MUR 35.5 billion. The employee and employer contributions were MUR 180 million and

MUR 608 million respectively. During the period, a total of MUR 421 million were paid as

benefits.

6.5 Global Business Companies

The Financial Services Act 2007 was enacted to replace the Mauritius Offshore Business Activites

Act 1992 and to comply with international norms and practices in this Industry. Offshore Business

activities have been categorized in two types namely Global Business Licence Category 1

Company (GBL1) or Global Business Category 2 Company (GBL2). A GBL1 company is a tax

resident company that can take advantage of Double Taxation Agreements (DTA) that Mauritius

has signed with 43 countries so far. It is ideally suited, for example, for all investments to third

countries, with which Mauritius has signed a DTA, which are likely to generate a flow of income

in future years such as dividends, interest, royalties or capital gains.

Currently, GBL1 companies are being widely used for activities like insurance, fund management,

holding and asset management. With a corporate tax of 15 per cent, GBL1 benefit from an

underlying foreign tax credit , equal to the amount of foreign taxes paid, up to the amount of tax

42

due in Mauritius. In the absence of proof, the amount of foreign tax paid is presumed to be 80

percent of the Mauritius tax. The effective tax rate can thereby be reduced to a maximum of three

per cent. It is worth highlighting that there is no capital gains tax, nor withholding tax on dividends

and interest paid to non-residents.

GBL1 companies satisfy international standards in terms of transparency and substance

requirements. Yearly audited financial statements have to be filed with the authorities. The board

of directors should comprise of at least two directors who are resident in Mauritius and the GBL1

is required to have its principal bank account in Mauritius. In addition to these conditions, as from

1 January 2015, additional substance requirements have come into force. A GBL1 needs to satisfy

at least one of the following conditions: the GBL1 has office premises in Mauritius; or the the

GBL1 employs or shall employ at least one full time employee resident in Mauritius; or the

constitution of the GBL1 provides for all disputes arising out of the constitution to be resolved by

way of arbitration in Mauritius ;or the shares of the GBL1 are listed on a Mauritius Stock exchange

; or the GBL1 has incurred yearly expenditure in Mauritius that can reasonably be expected from

a similar corporation controlled and managed from Mauritius.

On the other hand, GBL2 companies are international companies which are not subject to taxation

in Mauritius. They are mainly used for trading purposes, invoicing, international contracts or

holding of assets. With a simple administration and low cost of setting up and operation , GBL2

offer a wide range of flexibility. They do not have access to DTA and do not need to satisfy any

specific conditions as required for GBL1. However, full disclosure is required for the identity of

the ultimate beneficial owner and an annual financial summary should also be filed with the

authorities.

The Global Business sector has been growing in momentum during the year 2013 despite the

aftermath of the financial and Euro Zone crisis coupled with perceived uncertainties prevailing on

the outcome of the Technical Joint Working Group in the re-negotiation of the Double Taxation

Avoidance Agreement between India and Mauritius. In an effort to curtail the downside effects of

the foregoing, the FSC Mauritius and the Board of Investment worked together on making the

43

Mauritius jurisdiction the preferred financial hub for investment in Africa, in line with the Africa

Strategy set by Government.

Further to government policy of consolidating the position of Mauritius IFC as a jurisdiction of

substance and sound repute, discussions with relevant stakeholders were held prior to amendments

being brought to the Guide to Global Business. Existing GBC1s had to comply with these new

requirements by 01 January 2015.

Market Trends

During the year 2013, 77 audited financial statements for Management Companies (‘MC’) and

Corporate Trustees (‘CT’) were received and reviewed.

The total Income, as per the 77 audited financial statements received, amounts to USD 77.5 million

and profit before tax amounts to USD 23.2 million. The corresponding figures for the same

population of 77 Management Companies for the year 2012 was USD 73.9 million for total income

and USD 21.2 million for profits before tax.

6.6 Other Non Bank Financial Institutions (Second schedule of the FSA)

Section 14 of the FSA requires any entity / person carrying out any financial services activities to

be a licensee of the FSC Mauritius. While most of the financial services activities fall under

relevant Acts as prescribed in the First Schedule of the FSA, there are other financial business

activities mentioned in the Second Schedule of the FSA which include

Assets Management

Credit Finance

Custodian Services (non-CIS)

Distribution of Financial Products

Factoring

Leasing

Pension Scheme Administrator

Registrar and Transfer Agent

Treasury Management

Credit Rating Agencies/Rating Agencies

44

Global headquarters administration

Global treasury activities

Representative Office (for financial services provided by a person established in a foreign

jurisdiction)

Actuarial services

Payment intermediary services

6.7 The Supervisory and Regulatory Framework

The FSC regularly reinforces its supervisory framework in response to international challenges in

order to promote robust regulation of its licensees, safeguard public interest, foster investors'

confidence and ensure more effective enforcement.

The over-arching aims of the FSC's supervisory framework include:

Ensuring that licensed entities are compliant with its legislative framework and are

financially sound;

Identifying licensees engaged in activities that are unlawful or contrary to public interest

for appropriate enforcement action;

Fostering public and investor confidence in the financial system; and

Maintaining the good repute of Mauritius as an International Financial Centre.

The FSC's supervisory framework is based on prudential supervision as well as the conduct of

business. While prudential supervision ensures the safety and soundness of institutions with a

focus on risk, capital and liquidity, regulation of conduct focuses on how consumers are impacted

by the actions of financial institutions. As an integrated regulator, the FSC delivers by maintaining

a stable equilibrium of conduct and prudential supervision.

6.7.1 Prudential supervision

The purpose of prudential supervision is to ensure the financial soundness of financial

undertakings and to contribute to the stability of the financial sector. There are two ways in which

prudential supervision is carried out: at micro level and at macro level.

45

At micro level, individual firms must prudentially manage their own risks, and financial

supervisors must prudently manage the risks posed by the financial system to society. Macro-

prudential supervision is the oversight that focuses on the stability of a financial system as a whole,

rather than on its components. The need for macro-prudential regulation of the system arises

because the actions of individual companies acting prudently within guidelines may collectively

result in the instability of a financial system.

Macro-prudential supervision in conjunction with micro-prudential supervision are sufficient

working instruments for stemming systemic crisis through early detection of vulnerabilities and

threats with appropriate policy responses to pre-empt the occurrence of systemic crisis.

6.7.2 Regulation of conduct

Market conduct regulation ensures that markets function well and continue to provide the services

expected of these infrastructures in an orderly manner. The focus is on protecting customers who

buy financial products or otherwise entrust funds to financial institutions. Such regulation provides

consumer protection by addressing the unequal position of financial institutions relative to their

customers. The most vulnerable customers are retail clients who often lack the sophistication and

information necessary to protect themselves from fraud, market abuse or ill-informed advice and

rely on financial institutions and their representatives to look after their interests.

As an integrated regulator for the non-banking financial services and global business sectors, one

of their core functions, as defined in the FSA, includes licensing, monitoring and regulating the

conduct of business activities in these sectors.

The licensing stage is the first limb in the supervisory process of the FSC Mauritius and has an

important role in establishing high regulatory standards at the outset.

In the chain of operations, FSC Mauritius performs a pre-surveillance function at licensing stage

and conducts a screening role so as to enable the Commission to reinforce its core duties of

ensuring a sound and stable market from both prudential and conduct perspectives.

46

The Surveillance process at the Commission is twofold such that licensees are assessed both

through desk monitoring and on-site inspections which enable the Commission to gain an

understanding of the level of risks posed by the licensees to the jurisdiction.

Apart from protecting consumers, the market conduct regulator is required to promote confidence

in the financial system and ensure financial services institutions and markets function well and to

high ethical and professional standards.

The FSC carries out pre-surveillance at the stage of licensing to ensure only qualified licensees

operate with the Mauritius IFC. Applicants have to demonstrate financial soundness, governance

and potential for good market conduct before being licensed. Once licensed, licensees come under

the continuous surveillance and monitoring by the FSC and are expected to comply with the

prevailing legal framework at all times and to meet all the licensing conditions and licensing

requirements. Constant monitoring and surveillance entails ensuring the licensees comply with

legislations at all times which is verified through off-site supervision and on-site inspections.

In order to ensure appropriate allocation of limited supervisory resources in accordance with the

level of risk, the FSC used a Risk-Based Supervision (RBS) Framework. The relevancy of the

framework is regularly assessed and over the years, the RBS Framework has evolved to reflect

most of the major developments in the market.

The following parameters are used to measure the riskiness posed to the system by the licensee:

Corporate Governance;

Prudential Procedures;

Financial performance;

Risk-to-Objectives Matrix;

Risk Profile;

System; and

Market Conduct Procedures.

47

The risk score based of the parameters assists in planning and scheduling on-site inspections on

the one hand and focusing off-site monitoring resources towards licensees with a higher risk profile

on the other hand.

48

7.0 A SWOT Analysis of the Financial Services Industry of Mauritius.

This section considers the strengths, weaknesses, opportunities and threats relating to the financial

sector of Mauritius.

Strengths

(1) Mauritius has well-established and fairly well developed banking and insurance sectors with

a few prominent and professionally managed domestic companies.

(2) The enviable democratic history of the country, underpinned by the rule of law formulated by

an elected legislature, and administered by an independent judiciary with the ultimate appellant

body being the Queen’s Privy Council, is a unique asset and provides essential comfort to investors

and economic operators.

(3) Commercial, civil and criminal law codes are well developed and are, by and large, based on

and inspired from the French code and English law; this has ensured clarity in, and acceptance of,

the outcome of the litigation process, which is often an essential recourse in the resolution of

complex claims.

(4) It has a strong banking regulator, the Bank of Mauritius. The payment system operates on a

real time basis (RTGS) through the Mauritius Automated Clearing and Settlement System

(MACSS) and is linked to an efficient and reliable international payment system infrastructure, i.e

SWIFT.

Weaknesses

(1) The operation of too many small players may become the source of systemic risk. In the

insurance sector, for example, the presence of some marginal, undercapitalized, illiquid and poorly

staffed companies operating at the fringe of the market, and, writing mostly motor insurance at

uneconomic terms, may be viewed as a source of risk. Most of them would not have the capital

resources to invest in technology and risk management processes to stay competitive.

(2) The dominant position of a handful of players inhibits competition and innovation. There is

no innovation in terms of products and business models. Other than the secondary securities market

developed by the Bank of Mauritius, there is barely significant secondary market trading in stocks

and shares.

49

(3) The failure of three insurance companies, transacting primarily motor insurance business, in

the last decade may have shaken public confidence in the insurance sector, and, has raised

questions about the effectiveness of insurance supervision.

(4) Inadequate supply of skilled manpower having international exposure could be one of the

reasons for the observed insufficient innovation in the provision of financial services. The industry

has no institutional set-up for the continuing training and upgrading of skills of its human

resources. There is no defined policy to encourage the employment of foreign skilled manpower

in new areas such as assets securitization and financial engineering.

(5) The money and capital markets are prone to malfunctioning. Poor disclosure practices by

companies hinder the proper evaluation of business and credit risk. In the present circumstances,

there is a risk that some areas may not develop the required scope to remain in business or to have

a meaningful market presence. This leads to potential errors and inherent weaknesses in the pricing

of financial assets such as equities, insurance policies, debentures and bank loans. In addition, with

the exception of the banking sector, there is a lack of risk management culture across the financial

services industry. The end result could be a misallocation of capital that would in the long run

weaken the financial position of some financial institutions operating in Mauritius and, hence, the

entire system. A revamping of the stock market as well as the development of an active and vibrant

debt market is urgently needed.

(6) The pace of economic development of the countries forming part of the region surrounding

Mauritius is comparatively slow. These countries are not attracting significant foreign investment,

equity or debt. Hence, Mauritius is prevented from effectively playing the role of the regional

financial center to channel funds to these countries.

Opportunities

(1) Mauritius can focus at becoming a financial centre meeting specific needs of companies world-

wide. In addition, some of the domestic players can potentially become important players in the

region after some consolidation among themselves.

(2) As the population of Mauritius embraces the global trend by shifting from savers into

becoming investors, deposit-taking institutions, banks and non-banks, will lose their share of

deposits. These deposits will flow into investment products. Therein lays both an opportunity for

50

and a threat to the domestic financial services industry. It would be an opportunity if the domestic

financial institutions would be innovative enough to offer investment products that would meet

the needs of domestic investors. It would be a threat if domestic consumers do not find the right

investment products in the domestic market and hence invest their savings with financial

institutions operating in foreign jurisdictions. This move from savings to investment has already

started. There has recently taken place, for instance, a net outflow of funds from Mauritius by local

investors that has affected the liquidity of the foreign exchange market, thus exposing its

insufficient depth and resilience.

(3) Fund management is one of the fastest growth segments of the financial services industry

worldwide in the context of globalization. Capital will flow to areas and countries that would

provide superior returns on capital for a given level of risks. At the same time, asset managers

want to manage funds invested in a particular market or country in or near that market or country.

The trend to shift out of saving accounts with banks into investment products will accelerate in

countries surrounding Mauritius and create opportunities if Mauritius inspires the necessary

investor confidence and has the appropriate products to offer by revamping its financial sector.

Threats

(1) The main threat is the inability of the industry to adapt to and embrace the globalization trend.

The existing dominant players in each segment could become complacent and satisfied with their

market positions. Satisfied with their inward-looking status quo and with no challenge from