John FeliceJohn FeliceVice President Manufacturing, Technology & Global EnterpriseChrysler Corporation LLC

Vice President Manufacturing, Technology & Global EnterpriseChrysler Corporation LLC

C H R Y S L E R G R O U P

Chrysler Group’s Flexible Manufacturing Strategy

May 17, 2007

John Felice

Vice President – Manufacturing, Technology & Global Enterprise

Chrysler Group

C H R Y S L E R G R O U P

Market and Competitive Challenges

Tough Competition

Government Regulation

Consumer Demand

SupplyChain

C H R Y S L E R G R O U P

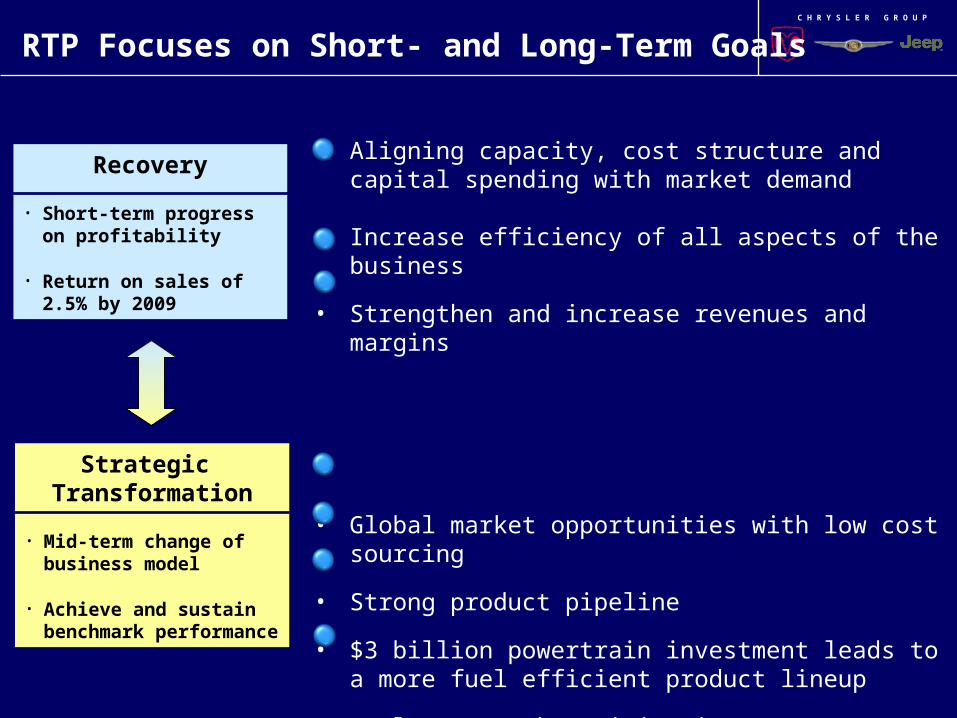

• Aligning capacity, cost structure and capital spending with market demand

Increase efficiency of all aspects of the business

• Strengthen and increase revenues and margins

• Global market opportunities with low cost sourcing

• Strong product pipeline

• $3 billion powertrain investment leads to a more fuel efficient product lineup

• Dealer network optimization

Recovery

• Short-term progress on profitability

• Return on sales of 2.5% by 2009

Strategic Transformation

• Mid-term change of business model

• Achieve and sustain benchmark performance

RTP Focuses on Short- and Long-Term Goals

C H R Y S L E R G R O U P

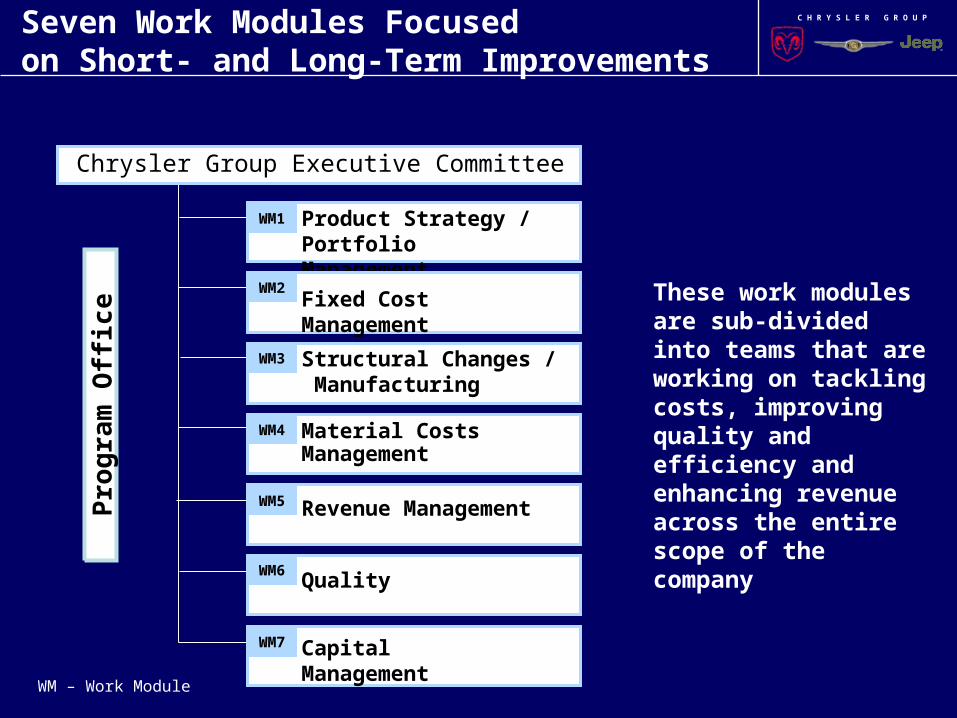

WM1 Product Strategy / Portfolio Management

Capital ManagementWM7

Fixed Cost ManagementWM2

Structural Changes / Manufacturing

WM3

Material Costs Management

WM4

Revenue ManagementWM5

QualityWM6

Chrysler Group Executive Committee

WM – Work Module

Seven Work Modules Focusedon Short- and Long-Term Improvements

These work modules are sub-divided into teams that are working on tackling costs, improving quality and efficiency and enhancing revenue across the entire scope of the company

Pro

gra

m O

ffic

e

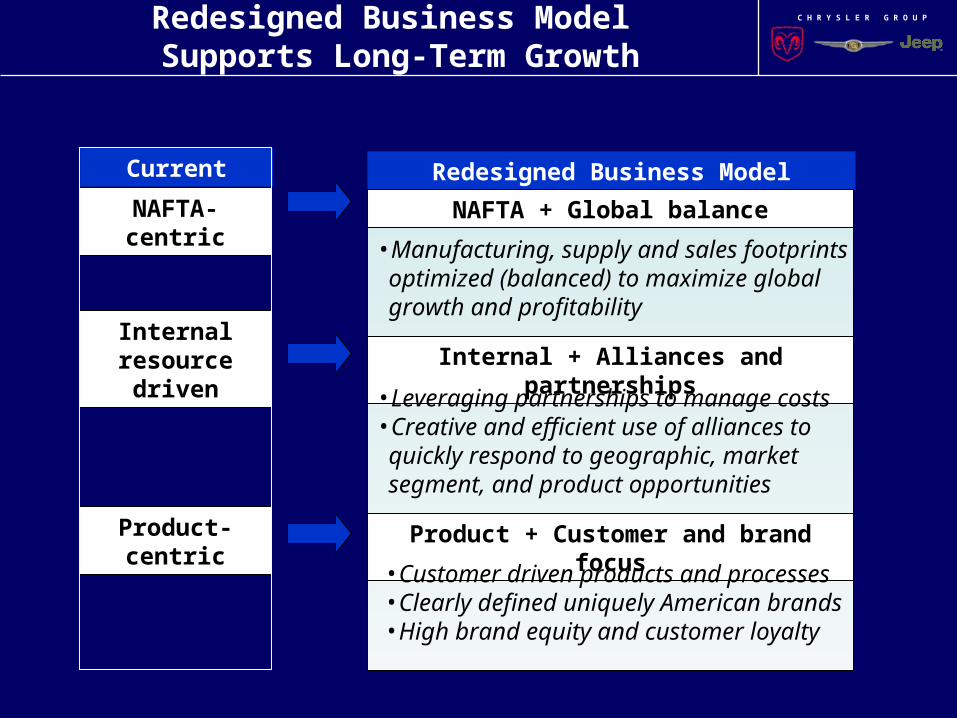

C H R Y S L E R G R O U PRedesigned Business Model Supports Long-Term Growth

Current Redesigned Business Model

Product-centric

Product + Customer and brand focus

NAFTA-centric NAFTA + Global balance

Internal resource

drivenInternal + Alliances and partnerships

• Customer driven products and processes • Clearly defined uniquely American brands• High brand equity and customer loyalty

• Manufacturing, supply and sales footprints optimized (balanced) to maximize global growth and profitability

• Leveraging partnerships to manage costs• Creative and efficient use of alliances to quickly respond to geographic, market segment, and product opportunities

C H R Y S L E R G R O U P

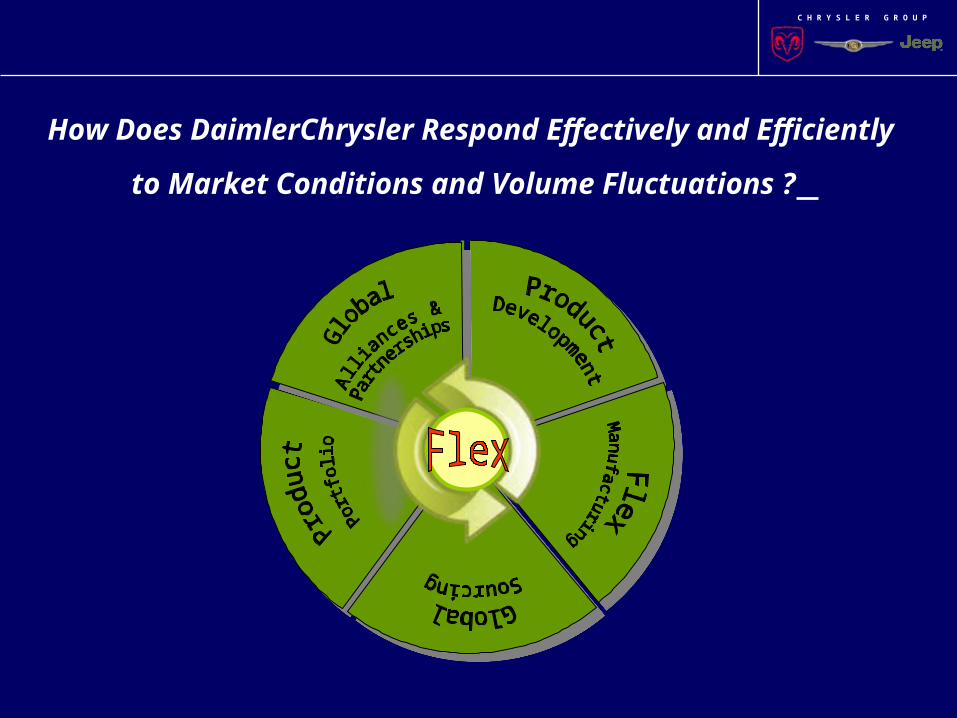

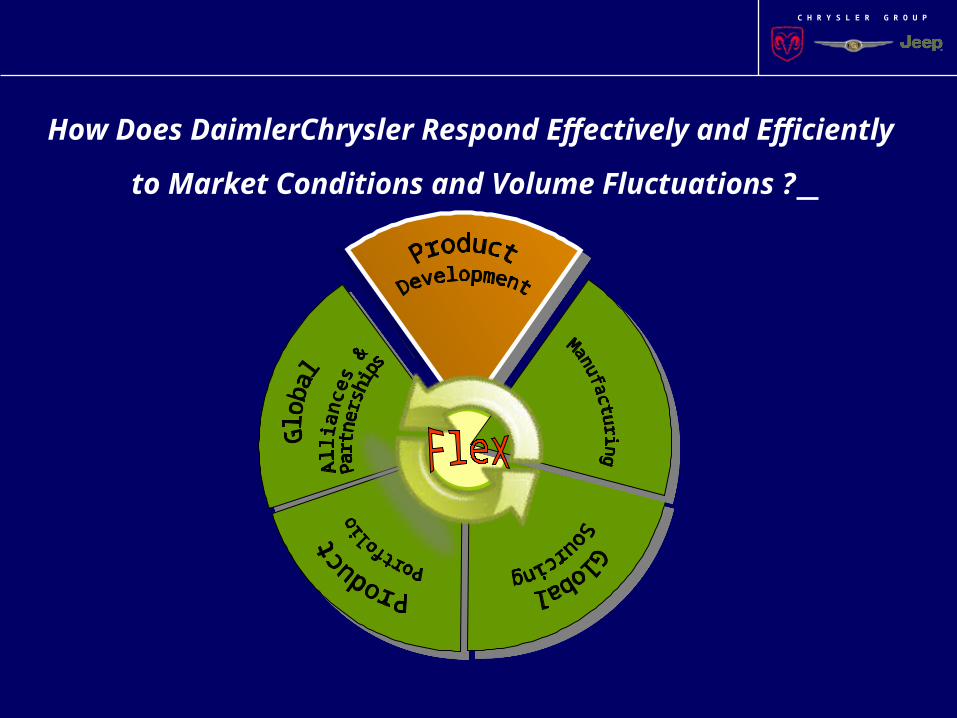

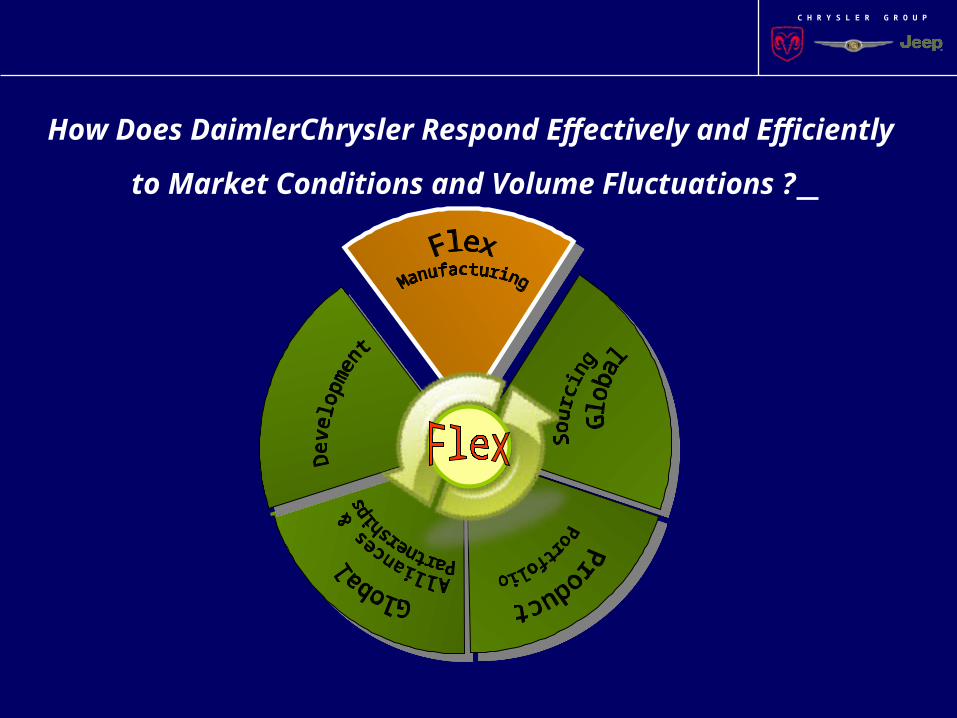

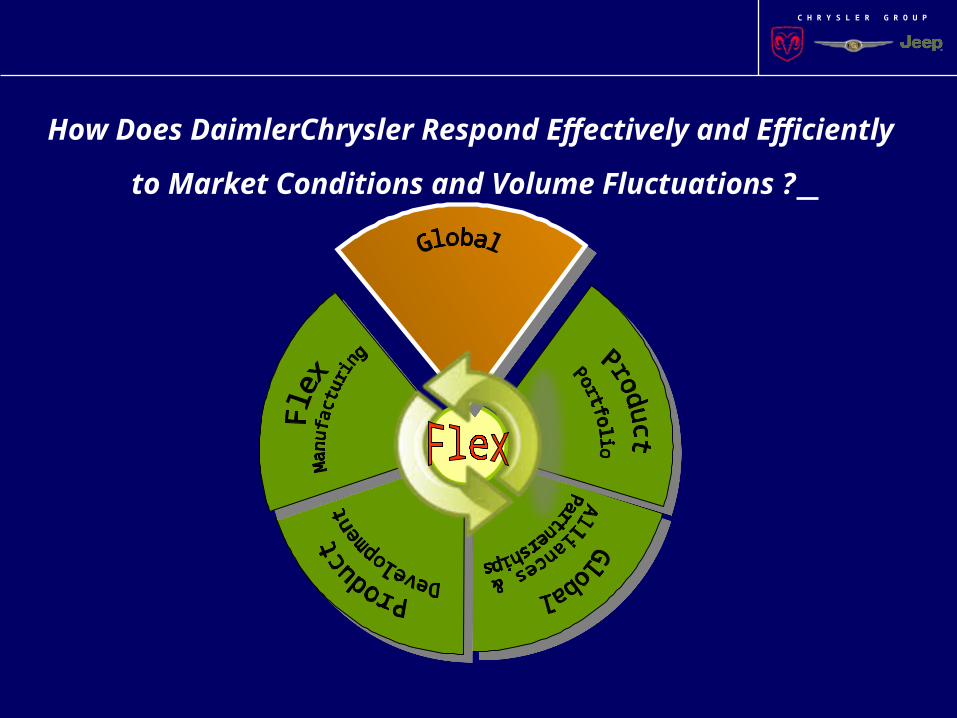

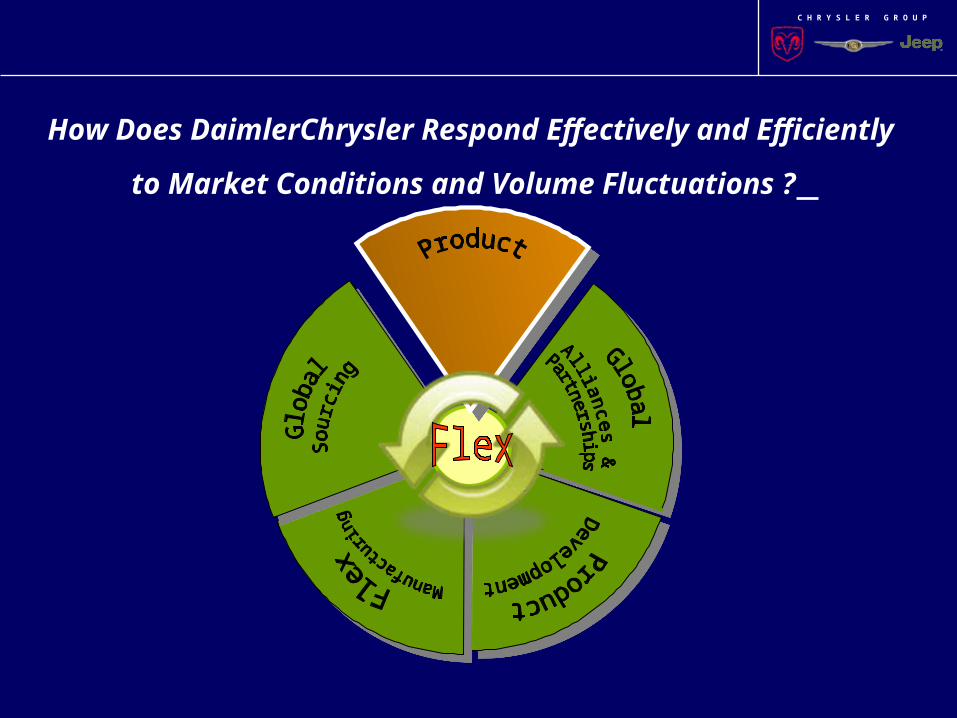

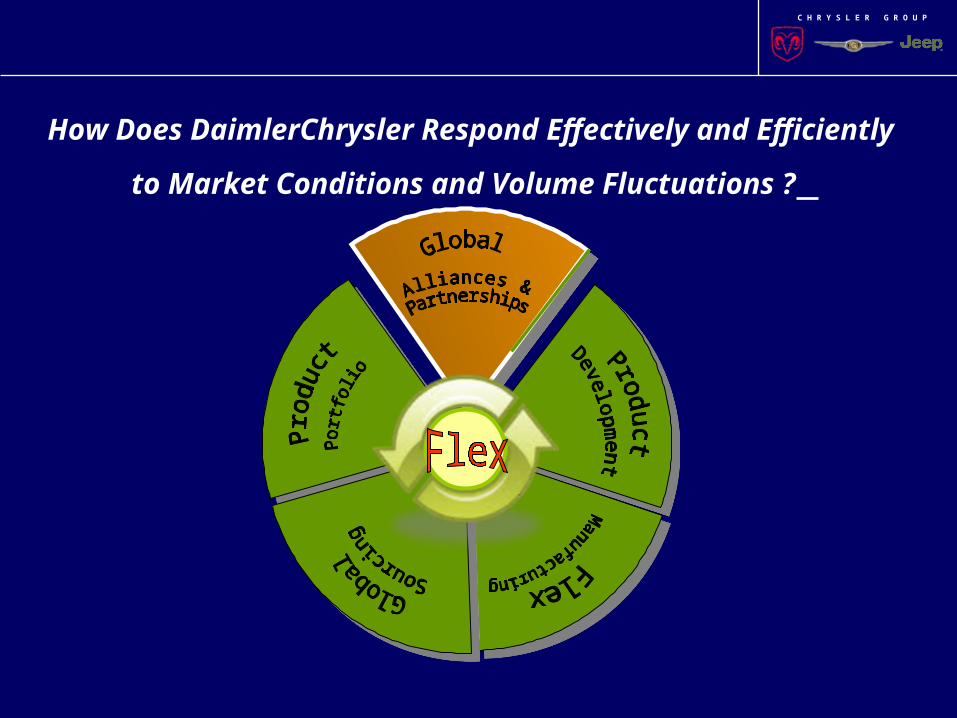

How Does DaimlerChrysler Respond Effectively and Efficiently

to Market Conditions and Volume Fluctuations ?

C H R Y S L E R G R O U P

Flex Target State

FLEX OPPORTUNITIES KEY QUESTIONS

How do you develop an optimum number of

quality products efficiently?

How do you best use the existing asset base to

build products in response to market demand

swings quickly?

How do you globally leverage the best cost-

saving sourcing opportunities through volume

bundling and commonization?

How do you offer consumer-driven product

lines that can achieve geographic and market

segment opportunities?

How do you achieve better global balance and

leverage partnerships to manage cost and seize

growth opportunities?

Product Development

Flex Manufacturing

Global Sourcing

Product Portfolio

Global Alliances & Partnerships

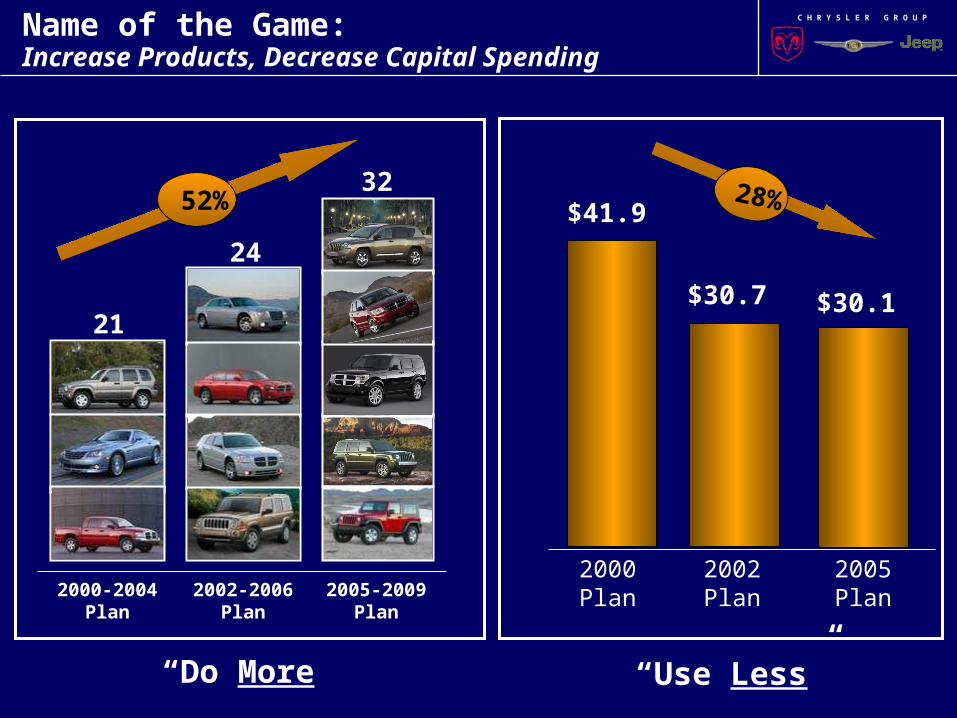

C H R Y S L E R G R O U PName of the Game: Increase Products, Decrease Capital Spending

$41.9

$30.7 $30.1

2000Plan

2002Plan

2005Plan

28%

“Do More” “Use Less”

2000-2004Plan

2002-2006Plan

2005-2009Plan

21

24

32 52%

C H R Y S L E R G R O U P

How Does DaimlerChrysler Respond Effectively and Efficiently

to Market Conditions and Volume Fluctuations ?

C H R Y S L E R G R O U P

C H R Y S L E R G R O U P

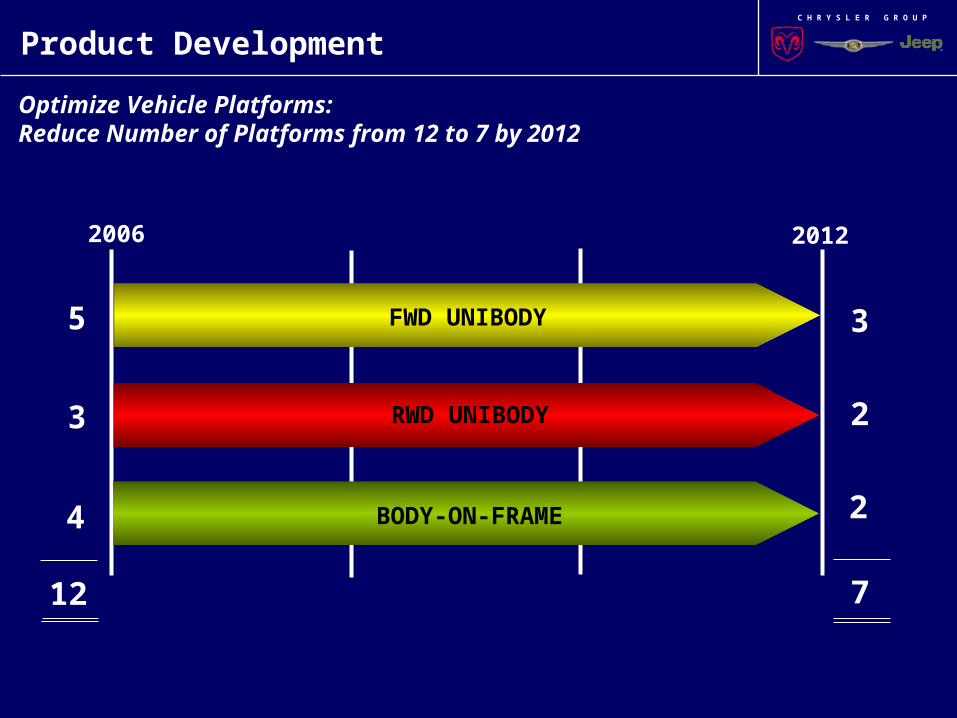

Product Development

3

2

2

2006 2012

712

RWD UNIBODY3

FWD UNIBODY5

BODY-ON-FRAME4

Optimize Vehicle Platforms:Reduce Number of Platforms from 12 to 7 by 2012

C H R Y S L E R G R O U P

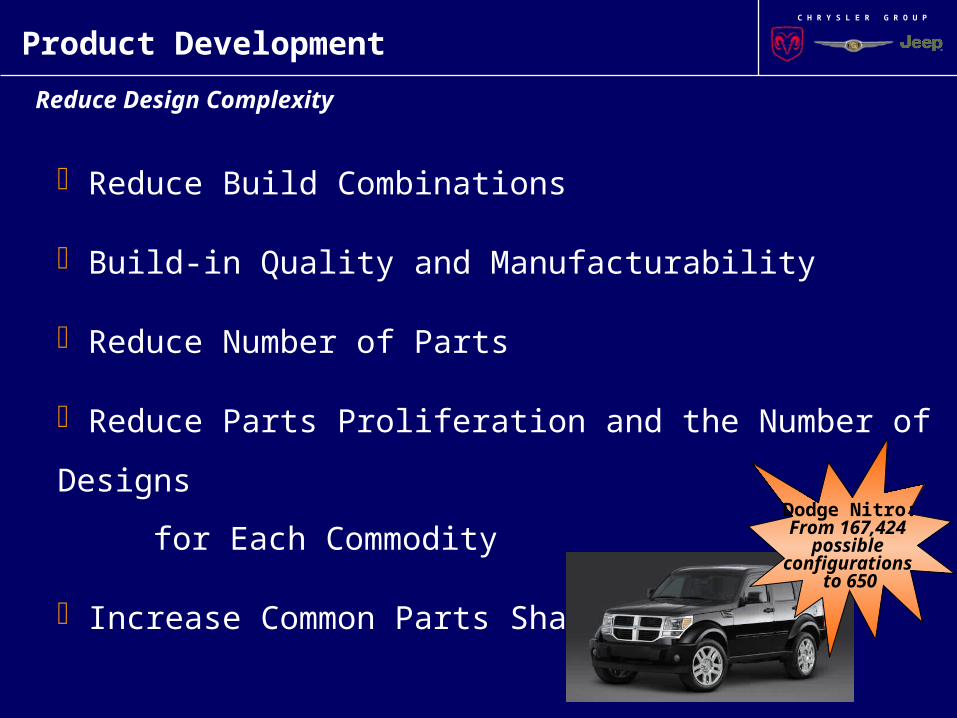

Reduce Build Combinations

Build-in Quality and Manufacturability

Reduce Number of Parts

Reduce Parts Proliferation and the Number of Designs

for Each Commodity

Increase Common Parts Sharing

Product Development

Reduce Design Complexity

Dodge Nitro:From 167,424

possible configurations

to 650

C H R Y S L E R G R O U P

How Does DaimlerChrysler Respond Effectively and Efficiently

to Market Conditions and Volume Fluctuations ?

C H R Y S L E R G R O U P

Body-on-frame Arch

Model

Model

Model

Model

Model

Model

Model

Model

Model

Unibody Arch #1

Model

Unibody Arch #2

Model

Model

Model

Model

Model

Model

Model

Model

Model

Model

Model

Model

Model

Model

Model

Model

Model

Model

Other Arch

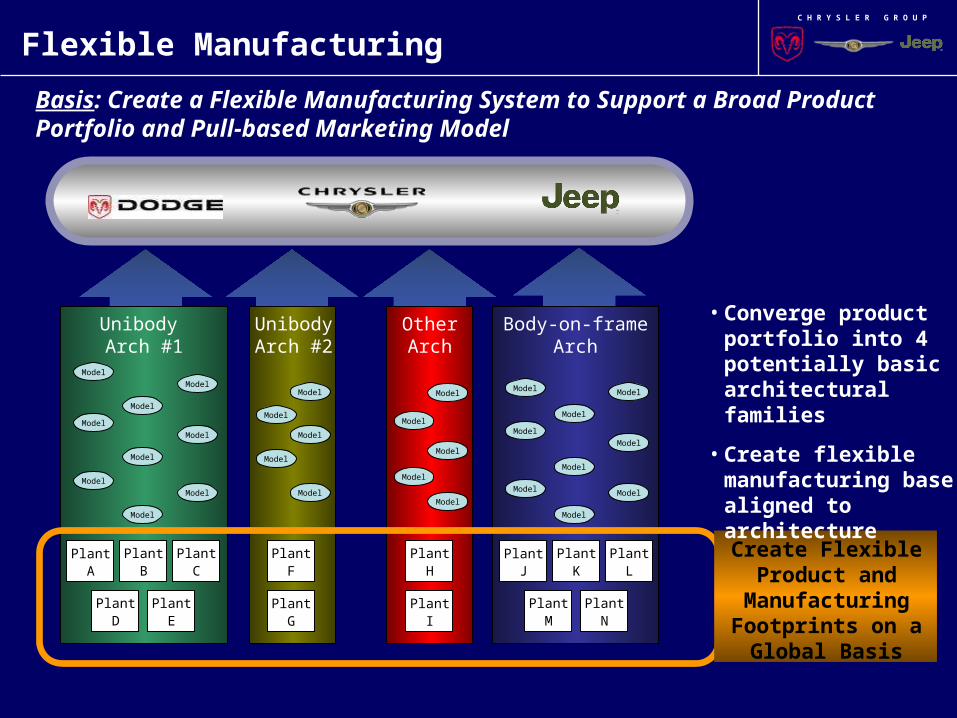

Flexible Manufacturing

Basis: Create a Flexible Manufacturing System to Support a Broad Product Portfolio and Pull-based Marketing Model

Create FlexibleProduct and

Manufacturing Footprints on a

Global Basis

• Converge product portfolio into 4 potentially basic architectural families

• Create flexible manufacturing base aligned to architecture

PlantA

PlantB

PlantC

PlantD

PlantE

PlantF

PlantG

PlantH

PlantI

PlantJ

PlantK

PlantL

PlantM

PlantN

C H R Y S L E R G R O U P

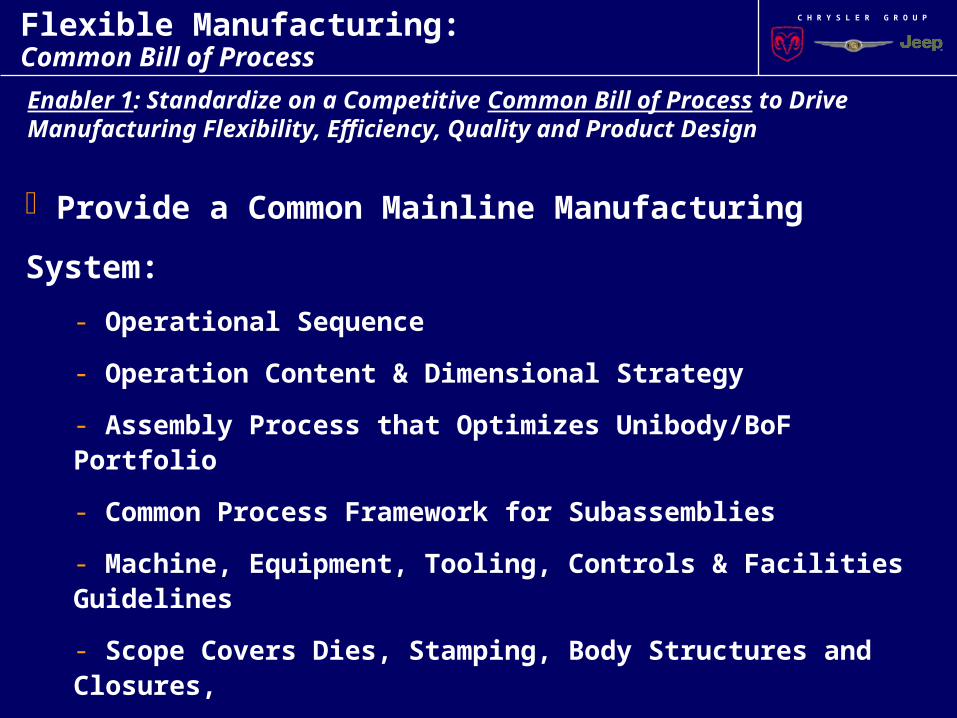

Enabler 1: Standardize on a Competitive Common Bill of Process to Drive Manufacturing Flexibility, Efficiency, Quality and Product Design

Provide a Common Mainline Manufacturing System:

- Operational Sequence

- Operation Content & Dimensional Strategy

- Assembly Process that Optimizes Unibody/BoF Portfolio

- Common Process Framework for Subassemblies

- Machine, Equipment, Tooling, Controls & Facilities Guidelines

- Scope Covers Dies, Stamping, Body Structures and Closures,

Paint, Trim, Chassis, Final, Powertrain, etc.

- Catalog of Technology

Flexible Manufacturing: Common Bill of Process

C H R Y S L E R G R O U P

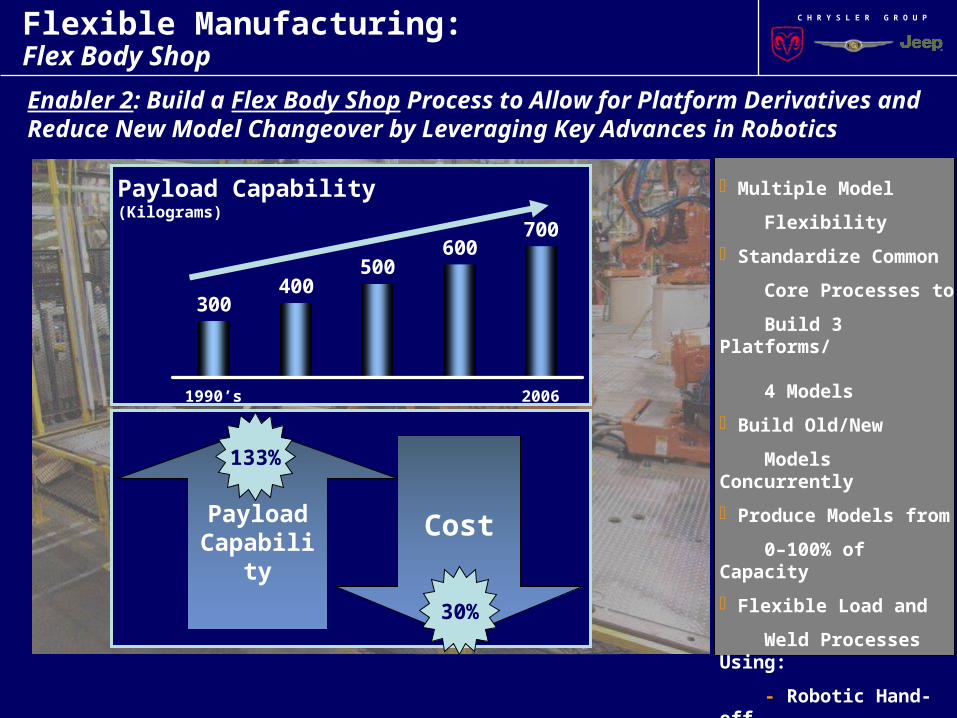

Enabler 2: Build a Flex Body Shop Process to Allow for Platform Derivatives and Reduce New Model Changeover by Leveraging Key Advances in Robotics

Key Developments

in Robotics:

- More Payload

range

- More powerful

Controllers

- Reduced Cost

300400

500600

700

Payload Capability(Kilograms)

1990’s 2006

PayloadCapability

Cost

30%

Multiple Model

Flexibility

Standardize Common

Core Processes to

Build 3 Platforms/ 4 Models

Build Old/New

Models Concurrently

Produce Models from

0–100% of Capacity

Flexible Load and

Weld Processes Using:

- Robotic Hand-off

- Geo End-effectors

133%

Flexible Manufacturing: Flex Body Shop

C H R Y S L E R G R O U P

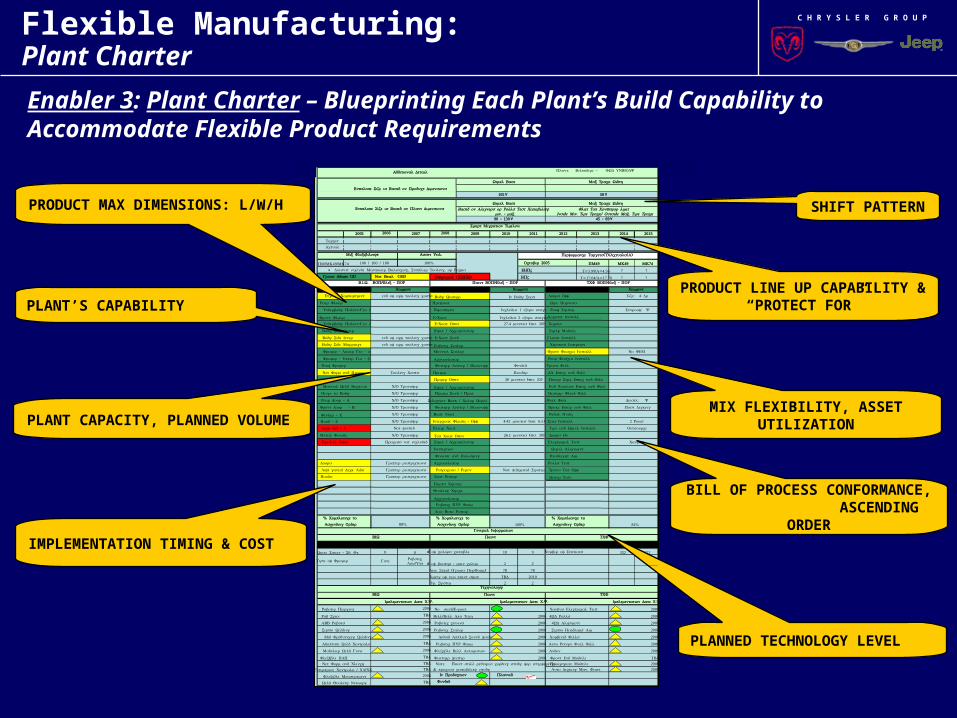

Enabler 3: Plant Charter – Blueprinting Each Plant’s Build Capability to Accommodate Flexible Product Requirements

IMPLEMENTATION TIMING & COST

PRODUCT MAX DIMENSIONS: L/W/H

PLANT CAPACITY, PLANNED VOLUME

PLANT’S CAPABILITY

SHIFT PATTERN

PRODUCT LINE UP CAPABILITY & “PROTECT FOR”

BILL OF PROCESS CONFORMANCE,

ASCENDING ORDER

PLANNED TECHNOLOGY LEVEL

MIX FLEXIBILITY, ASSET UTILIZATION

Flexible Manufacturing: Plant Charter

C H R Y S L E R G R O U P

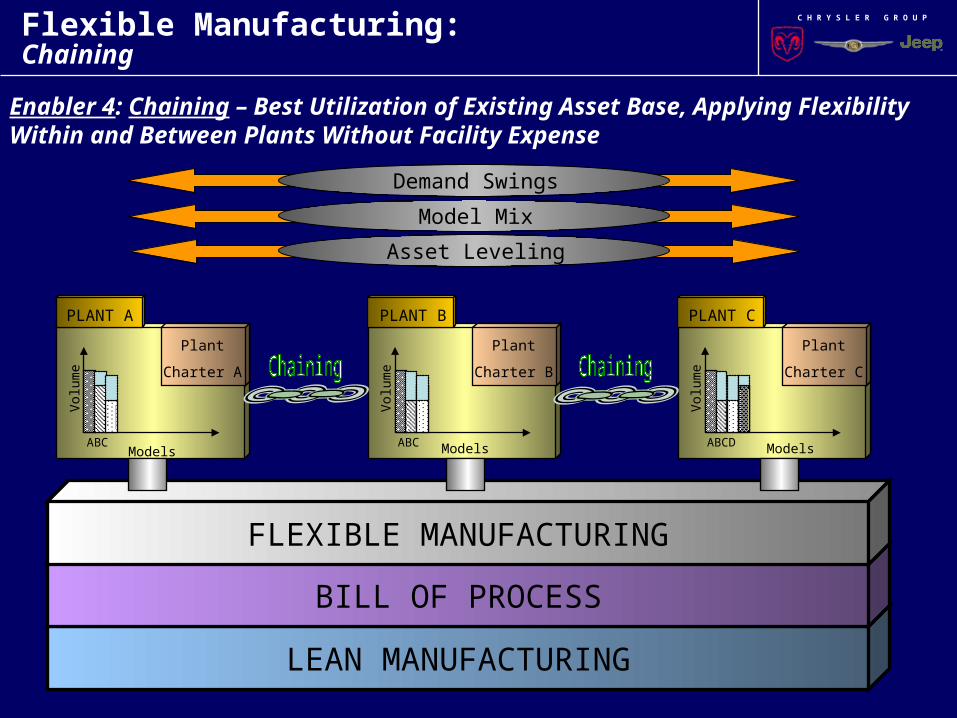

Enabler 4: Chaining – Best Utilization of Existing Asset Base, Applying FlexibilityWithin and Between Plants Without Facility Expense

LEAN MANUFACTURING

BILL OF PROCESS

FLEXIBLE MANUFACTURING

Plant

Charter A

Models

Vol

ume

PLANT A

Plant

Charter B

Models

Vol

ume

PLANT B

ABC

Plant

Charter C

Models

Vol

ume

PLANT C

ABC ABCD

Demand Swings

Model Mix

Asset Leveling

Flexible Manufacturing: Chaining

C H R Y S L E R G R O U P

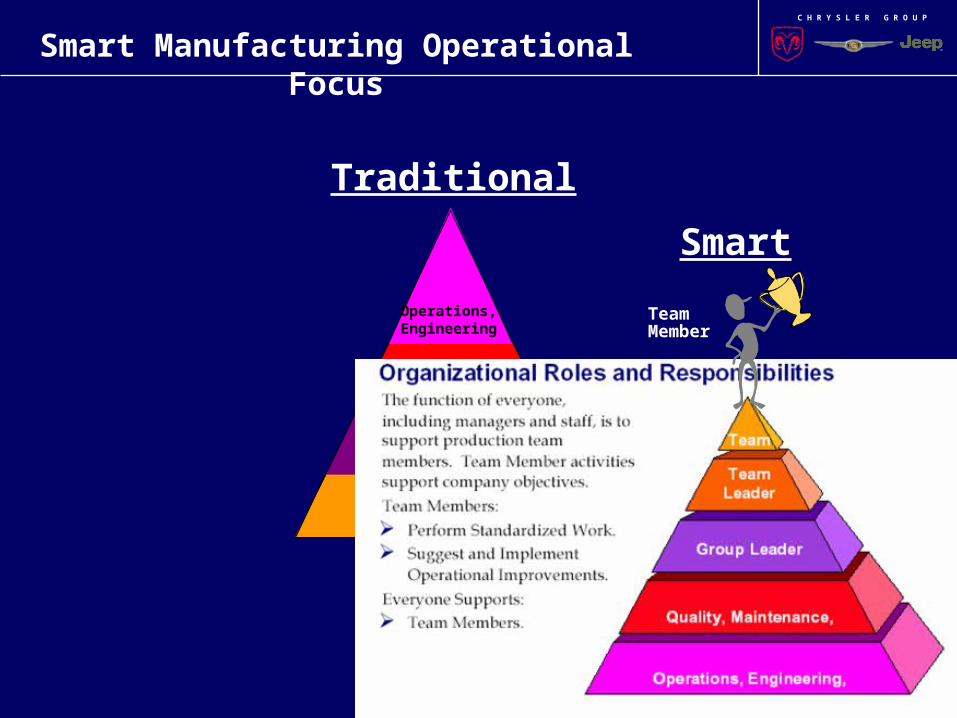

C H R Y S L E R G R O U P

Operators

Supervisors

Support Functions:Quality, Maintenance,

PC

Operations, Engineering

Smart Manufacturing Operational Focus

Traditional

Smart

TeamMember

C H R Y S L E R G R O U P

How Does DaimlerChrysler Respond Effectively and Efficiently

to Market Conditions and Volume Fluctuations ?

C H R Y S L E R G R O U P

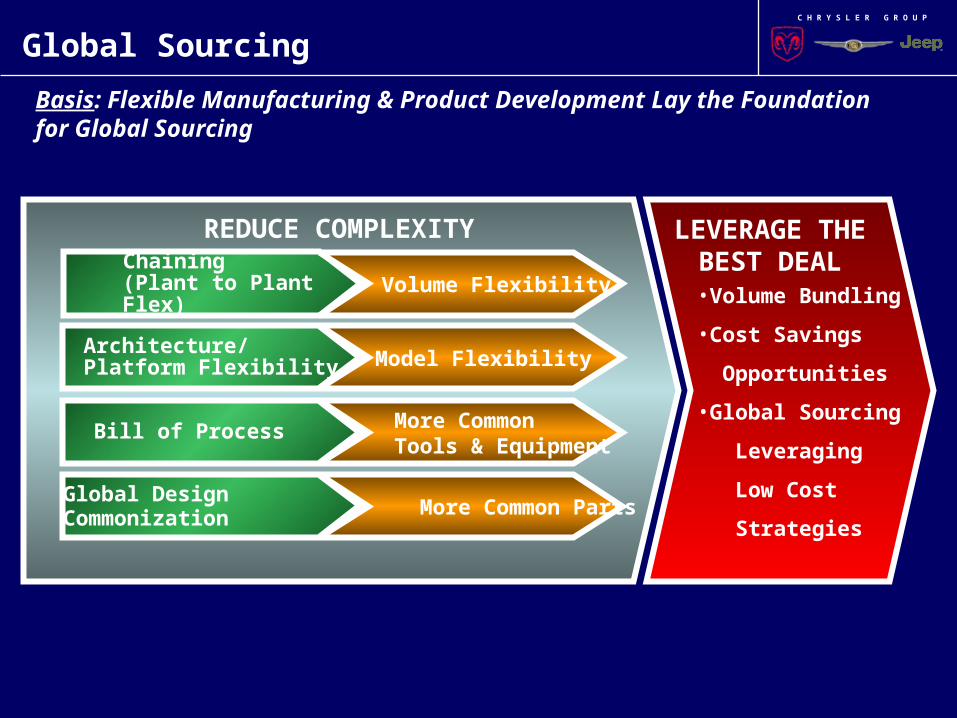

Global Sourcing

Basis: Flexible Manufacturing & Product Development Lay the Foundationfor Global Sourcing

• Volume Bundling

• Cost Savings

Opportunities

• Global Sourcing

Leveraging

Low Cost

Strategies

Chaining (Plant to Plant Flex) Volume Flexibility

Architecture/ Platform Flexibility Model Flexibility

Bill of Process More Common Tools & Equipment

Global Design Commonization More Common Parts

REDUCE COMPLEXITY LEVERAGE THE BEST DEAL

C H R Y S L E R G R O U P

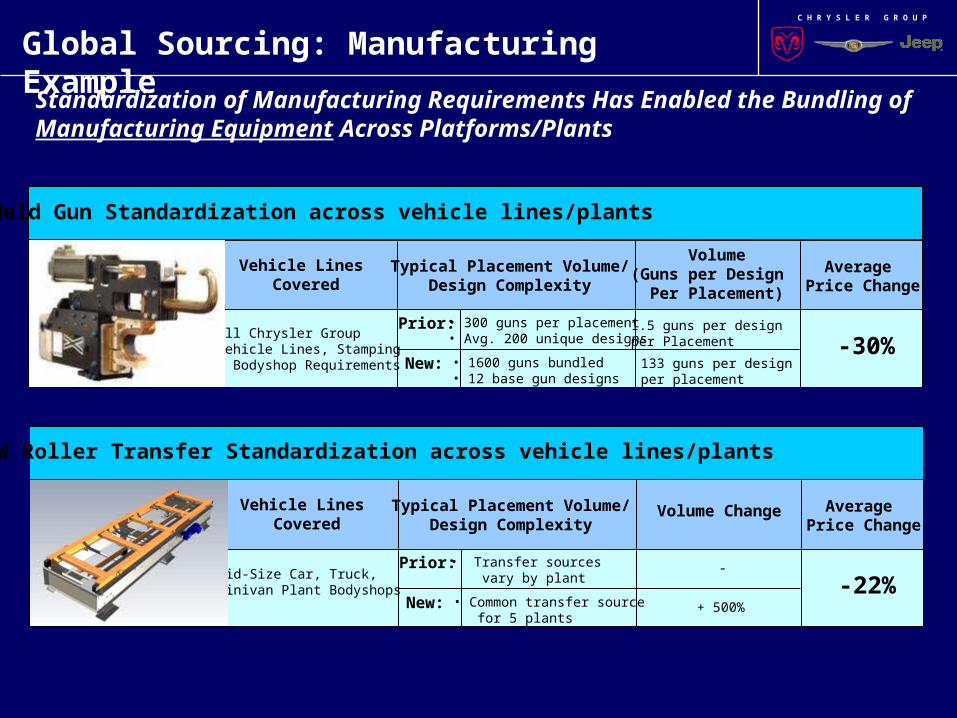

Global Sourcing: Manufacturing Example

Standardization of Manufacturing Requirements Has Enabled the Bundling of Manufacturing Equipment Across Platforms/Plants

BIW Roller Transfer Standardization across vehicle lines/plants

Vehicle Lines Covered

Typical Placement Volume/Design Complexity

Prior:

New:

• Transfer sources vary by plant

• Common transfer source for 5 plants

Mid-Size Car, Truck,Minivan Plant Bodyshops

Volume Change Average Price Change

+ 500%-22%

-

Weld Gun Standardization across vehicle lines/plants

Vehicle Lines Covered

Typical Placement Volume/Design Complexity

Prior:

New:

• 300 guns per placement• Avg. 200 unique designs

• 1600 guns bundled• 12 base gun designs

All Chrysler Group Vehicle Lines, Stamping & Bodyshop Requirements

Volume(Guns per Design

Per Placement)

Average Price Change

133 guns per designper placement

-30%1.5 guns per design per Placement

C H R Y S L E R G R O U P

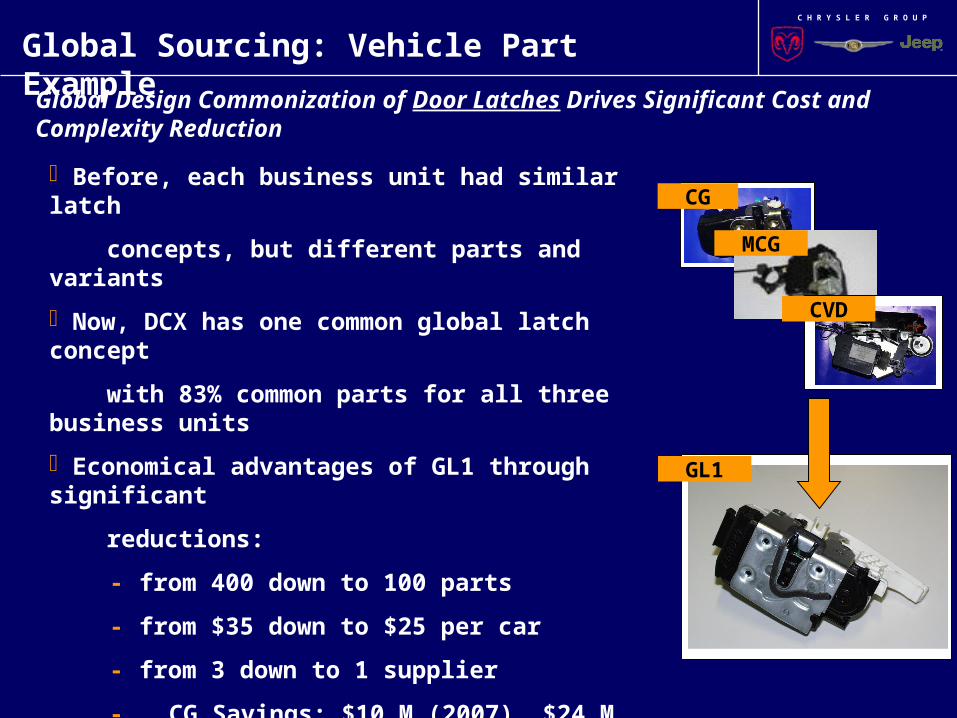

Global Sourcing: Vehicle Part Example

Global Design Commonization of Door Latches Drives Significant Cost and Complexity Reduction

Before, each business unit had similar latch

concepts, but different parts and variants

Now, DCX has one common global latch concept

with 83% common parts for all three business units

Economical advantages of GL1 through significant

reductions:

- from 400 down to 100 parts

- from $35 down to $25 per car

- from 3 down to 1 supplier

- CG Savings: $10 M (2007), $24 M (2009)

All new CG, MCG and CVD-Van models will be

equipped with GL1 by 2010; CG launch with Dodge

Caliber

CVD

MCG

CG

GL1

C H R Y S L E R G R O U P

How Does DaimlerChrysler Respond Effectively and Efficiently

to Market Conditions and Volume Fluctuations ?

C H R Y S L E R G R O U P

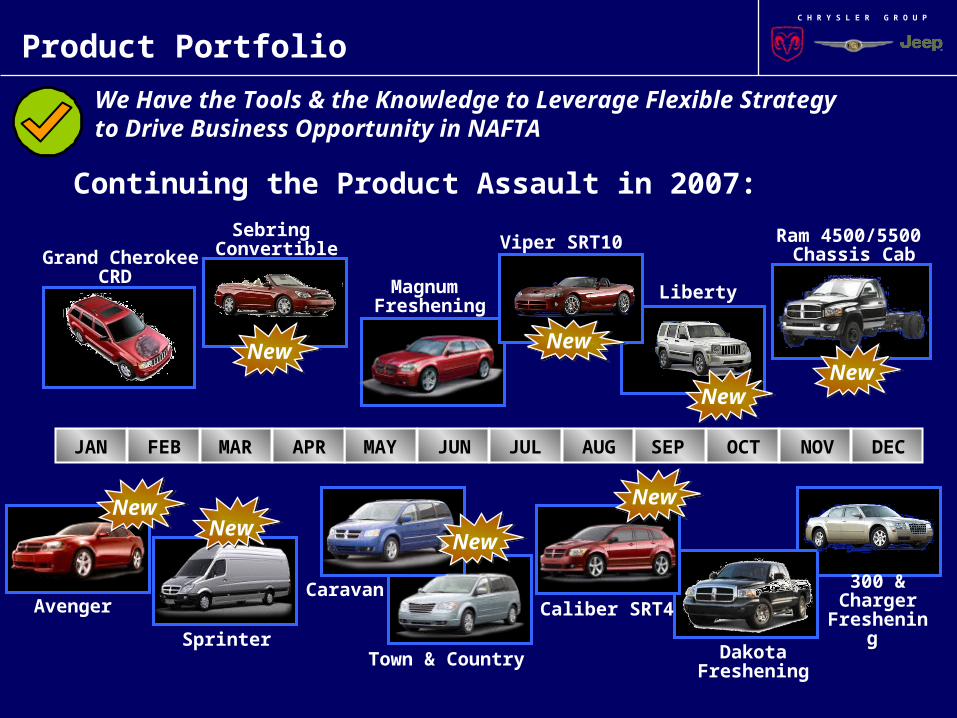

Product Portfolio

We Have the Tools & the Knowledge to Leverage Flexible Strategy to Drive Business Opportunity in NAFTA

Avenger

Grand CherokeeCRD Magnum

Freshening

Sebring Convertible

Liberty

Ram 4500/5500 Chassis Cab

DakotaFreshening

Viper SRT10

SprinterTown & Country

Caravan Caliber SRT4

300 & Charger

Freshening

JAN FEB MAY JUNAPR JUL AUGMAR OCT DECNOVSEP

New

New

NewNew

New

New

New

New

Continuing the Product Assault in 2007:

C H R Y S L E R G R O U P

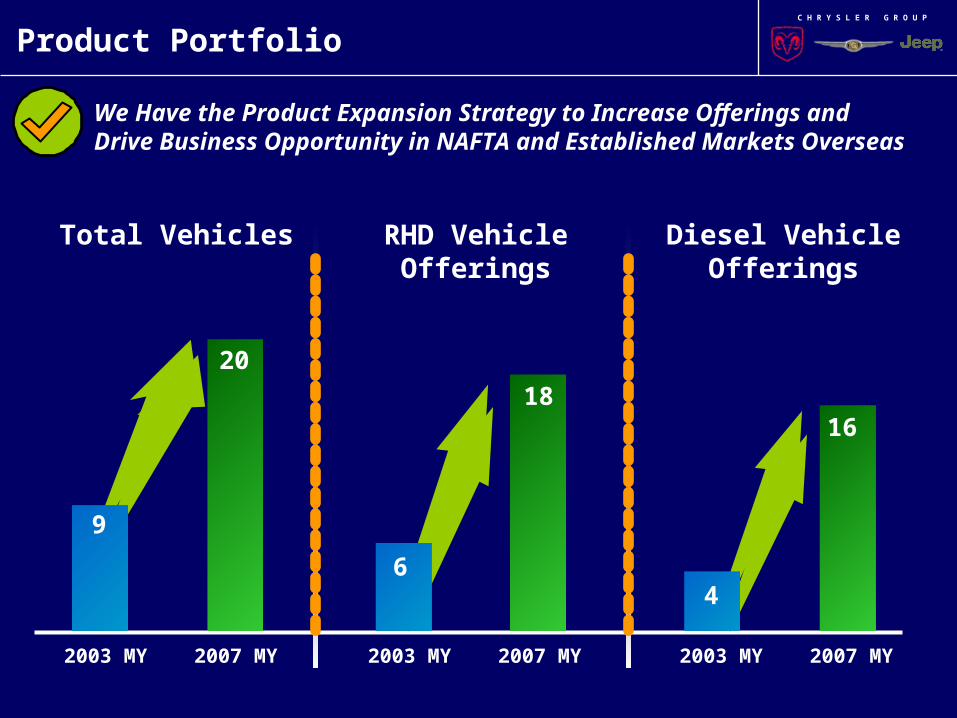

2003 MY 2007 MY 2003 MY 2007 MY 2003 MY 2007 MY

Total Vehicles RHD VehicleOfferings

Diesel VehicleOfferings

20

6

18

4

16

9

Product Portfolio

We Have the Product Expansion Strategy to Increase Offerings and Drive Business Opportunity in NAFTA and Established Markets Overseas

C H R Y S L E R G R O U P

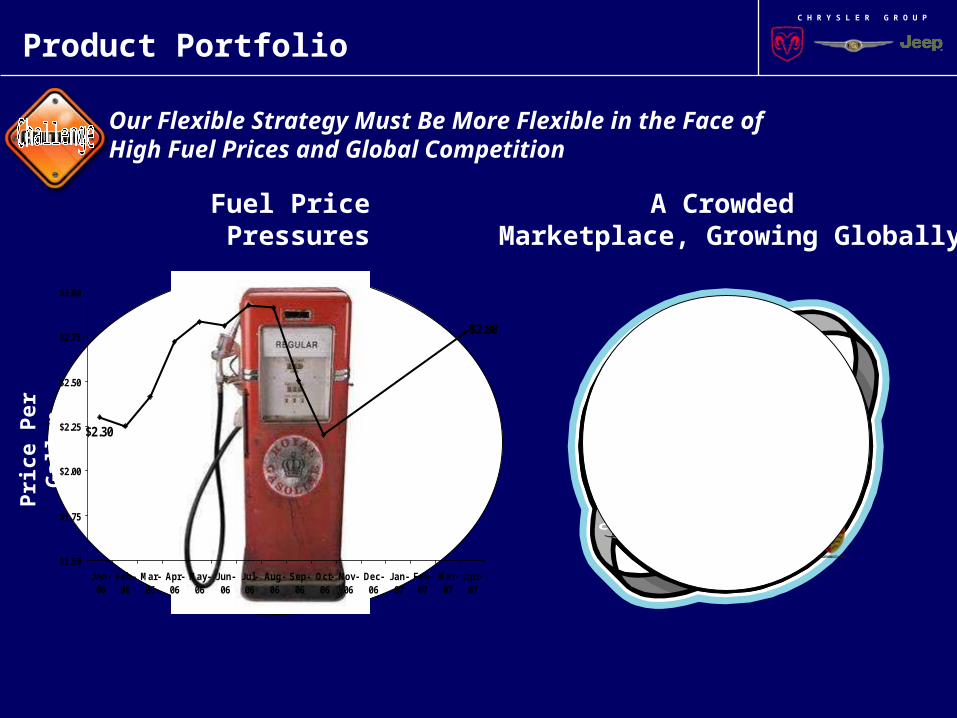

Product Portfolio

Fuel Price Pressures

Pri

ce P

er G

allo

n

A Crowded Marketplace, Growing Globally

$2.80

$2.30

$1.50

$1.75

$2.00

$2.25

$2.50

$2.75

$3.00

Jan-06

Feb-06

Mar-06

Apr-06

May-06

Jun-06

Jul-06

Aug-06

Sep-06

Oct-06

Nov-06

Dec-06

Jan-07

Feb-07

Mar-07

Apr-07

Our Flexible Strategy Must Be More Flexible in the Face of High Fuel Prices and Global Competition

C H R Y S L E R G R O U P

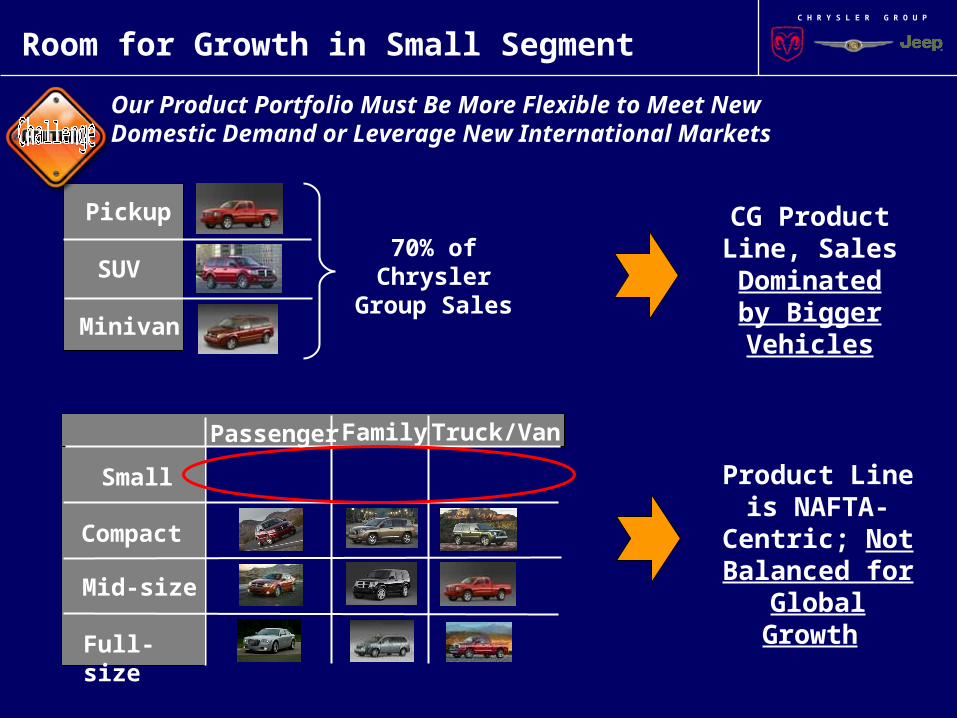

Room for Growth in Small Segment

Pickup

SUV

Minivan

70% of Chrysler Group

Sales

CG Product Line, Sales

Dominated by Bigger

Vehicles

Product Line is NAFTA-

Centric; Not Balanced for

Global Growth

Small

Compact

Mid-size

Full-size

Passenger Family Truck/Van

Our Product Portfolio Must Be More Flexible to Meet New Domestic Demand or Leverage New International Markets

C H R Y S L E R G R O U P

Product Portfolio

Our Strategy:Global Balance

Defend/grow NAFTA CG strongholds

Add new non-NAFTA vehicle programs crucial to

global expansion

Leverage 3rd party alliances to cost-effectively

access regional products/markets

$5+ billion additional purchasing to low cost

sources – balance supplier footprint

C H R Y S L E R G R O U P

How Does DaimlerChrysler Respond Effectively and Efficiently

to Market Conditions and Volume Fluctuations ?

C H R Y S L E R G R O U P

Select Regional Expansion

Global Alliances & Partnerships

Leveraging partnerships for growth and to manage costs Creative, efficient use of alliances to leverage geographic/market segment/product opportunity

Strong NAFTA Position

Small Vehicle B Segment Chery Motors, China

Manufacturing (300C, Jeep) Magna, Austria

Retail Network Marketing Hyundai in Mexico

Internal Manufacturing Minivan Assembly for VW

Diesel BlueTec Engine Cummins, MCG

Focused Alliances GEMA World Engine (HMC, MMC)

Hybrid GM, BMW

C H R Y S L E R G R O U P

Chrysler Group’s Flexible Manufacturing Strategy

May 17, 2007

John Felice

Vice President – Manufacturing, Technology & Global Enterprise

Chrysler Group