Fixed Income Securities

Dr. Rong ChenThe Department of

FinanceXiamen University

Fixed income ?

Fixed cash flow / interest rate sensitiveMajor types— traditional fixed-income securities—Interest rate derivatives—Bonds with embedded options

Copyright © Rong Chen, 2007, Finance Department, XMU 2

SyllabusPart I basic knowledge: Fixed-income instruments, prices and yieldsPart II Term structure: Empirical properties and classical theories of the term structure & Deriving the zero-coupon yield curvePart III Hedging interest-rate risk with duration, convexity and other waysPart IV Investment strategies: passive, active and performance measurement.

Part V: Interest rate swaps, forwards and futuresPart VI: Dynamic term structure modelingPart VII: Interest-rate derivativesPart VIII: Securitization

Copyright © Rong Chen, 2007, Finance Department, XMU 3

ReferenceLionel Martellini, Philippe Priaulet, Stephane Priaulet, 2003, Fixed-income securities: valuation, risk management and portfolio strategies, Wiley.Suresh M. Sundaresan, 1997, Fixed income markets and their derivatives, South-Western College PublishingJohn Hull, 2006, options, futures and other derivatives, Prentice HallMoorad Choudhry, 2005, Fixed-income securities and derivatives handbook, BloombergBond markets, analysis and strategies, Frank J. Fabozzi ,4th edition, NJ :Prentice Hall,2000 固定收益证券 , ( 美 ) 布鲁斯 ·塔克曼 (Bruce Tuckman) 著 , 黄嘉斌译;北京:宇航出版社, 1999固定收益证券:对利率风险进行定价和套期保值的动态方法 , 李奥奈尔 ·马特里尼 , 菲利普 ·普里奥兰德著;肖军译 , 北京:机械工业出版社, 2002谢剑平, 2003 , 固定收益证券:投资与创新,人民大学出版社薛立言 刘亚秋, 2006 , 债券市场,东华书局林清泉, 2005 ,固定收益证券 , 武汉大学出版社姚长辉 , 2006 ,固定收益证券 : 定价与利率风险管理 , 北京大学出版社

Copyright © Rong Chen, 2007, Finance Department, XMU 4

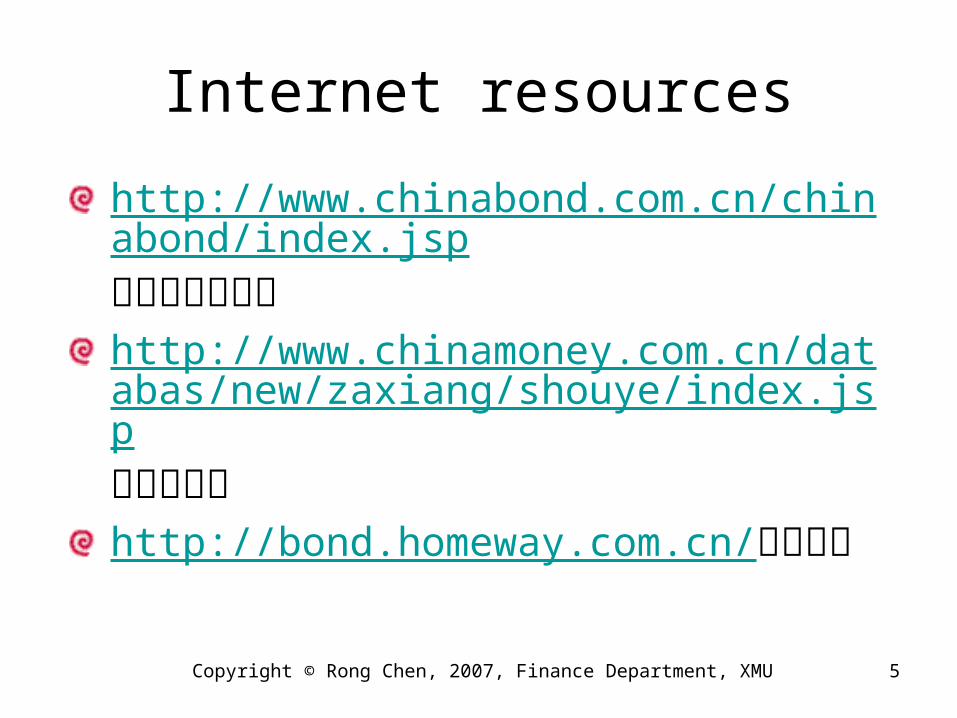

Internet resources

http://www.chinabond.com.cn/chinabond/index.jsp中国债券信息网http://www.chinamoney.com.cn/databas/new/zaxiang/shouye/index.jsp中国货币网http://bond.homeway.com.cn/和讯债券

Copyright © Rong Chen, 2007, Finance Department, XMU 5

Chapter 1

Introduction

MAJOR CHARACTERISTICS

1.1

Issuers

the issuer’s name

the issuer’s type

the issuer’s domicile

Copyright © Rong Chen, 2007, Finance Department, XMU 8

Time

The maturity date Short/ medium/ long term/ ConsolsCallable, puttable….

—The issuance date—the interest accrual date—the settlement date—Day-count conventions

Copyright © Rong Chen, 2007, Finance Department, XMU 9

Face value

—par amount/ nominal amount/ principal amount

—The total issued amount—The outstanding amount—The minimum amount and minimum

increment that can be purchased—The redemption value—The issuance price—Currency denomination

Copyright © Rong Chen, 2007, Finance Department, XMU 10

Interest rate

Interest rates— The coupon type ( zero, fixed, floating,

multicoupon, step-up coupon…)—The coupon rate —The coupon frequency

Mortgage/ government guarantee…The rating (Moody’s and S&P)

Copyright © Rong Chen, 2007, Finance Department, XMU 11

Other characteristics

Amortization Feature

Embedded options

Issuance market (Domestic , Eurodollar…)

Copyright © Rong Chen, 2007, Finance Department, XMU 12

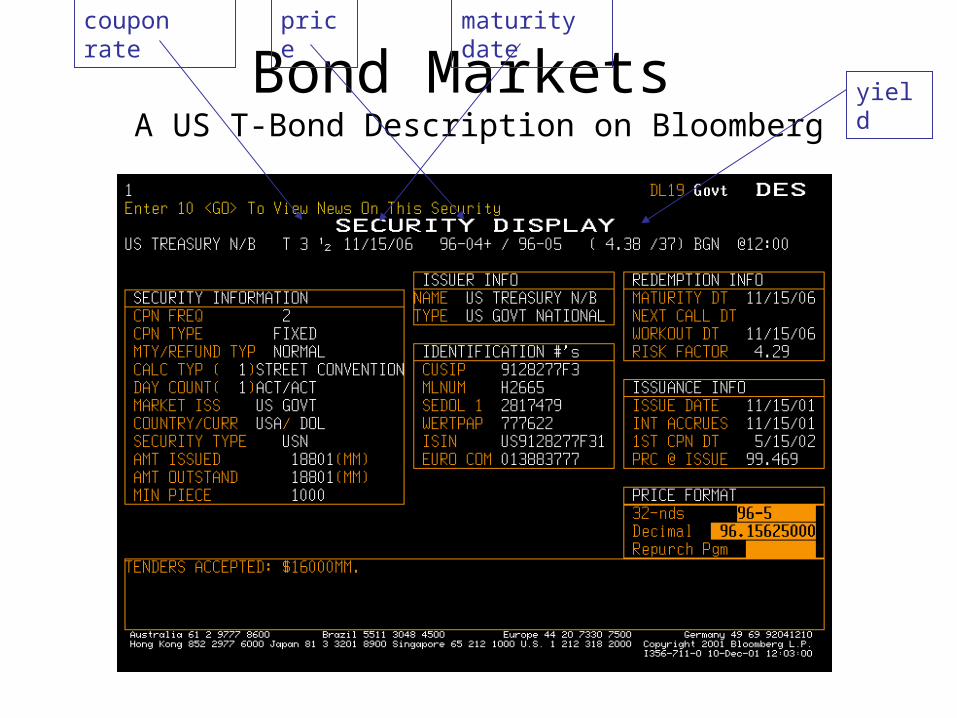

Bond Markets A US T-Bond Description on Bloomberg

yield

price coupon rate

maturity date

TYPES OF FIXED INCOME SECURITIES

1.2

BONDS1.2.1

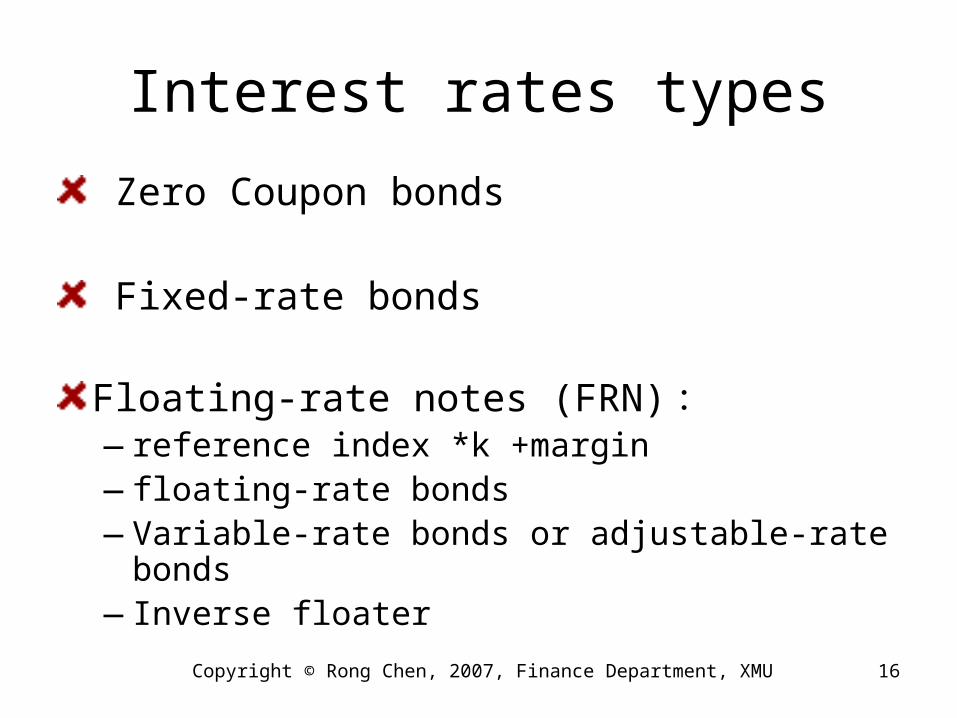

Interest rates types

Zero Coupon bonds

Fixed-rate bonds

Floating-rate notes (FRN) :—reference index *k +margin—floating-rate bonds—Variable-rate bonds or adjustable-rate

bonds—Inverse floater

Copyright © Rong Chen, 2007, Finance Department, XMU 16

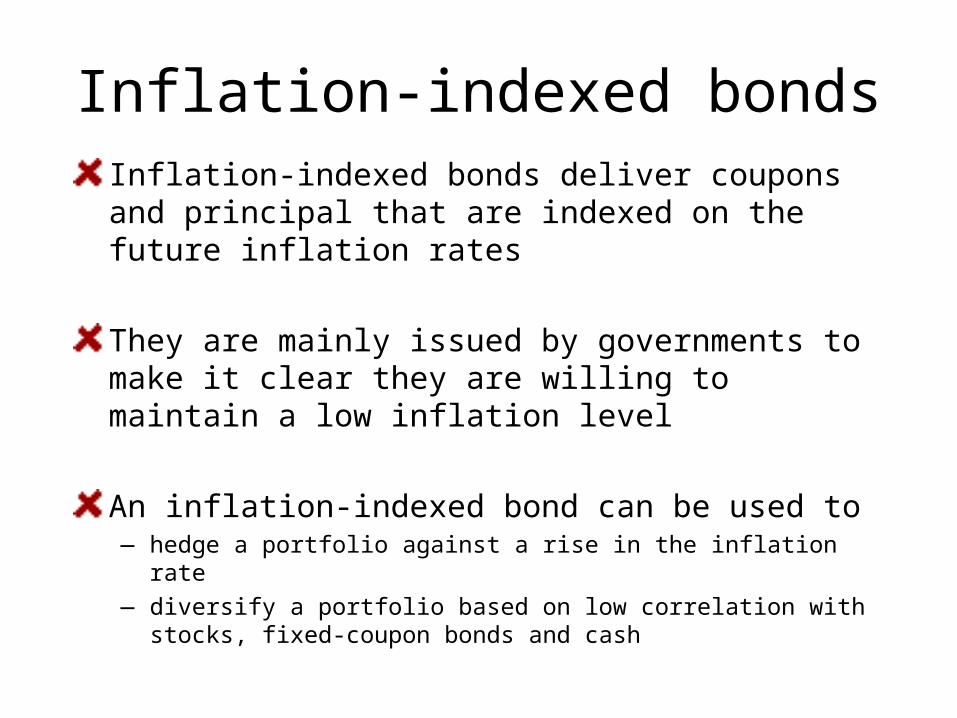

Inflation-indexed bondsInflation-indexed bonds deliver coupons and principal that are indexed on the future inflation rates

They are mainly issued by governments to make it clear they are willing to maintain a low inflation level

An inflation-indexed bond can be used to — hedge a portfolio against a rise in the inflation rate— diversify a portfolio based on low correlation with stocks,

fixed-coupon bonds and cash

Strips

Initially created by investment banks( trademark zeros)

Coupons are detached and principal and coupons sold individually

—It used to imply a tax break—Not anymore, the law has changed—Even after the law changed, great success

The government has its own program

Copyright © Rong Chen, 2007, Finance Department, XMU 18

Issuer’s types

US Treasury

—T-Bill (maturity < 1 year)—T-Notes (maturity 2, 3, 5, 7 and 10 year) —T-Bonds (>10 years)

Municipalities

Corporations

International Governments and CorporationsCopyright © Rong Chen, 2007, Finance Department, XMU 19

Government SecuritiesTreasury Bills

—Pure discount securities placed through auction—Maturity 13, 26 and 52 weeks

Treasury Notes and Bonds

—Half coupon paid semi-annually—Maturity 2, 3, 5, 7, 10 (notes) and 30 years

(bonds)—Sold in denominations of $1,000—Bonds may be callable or term securities—Bullet bonds/ amortization—Nominal coupon-bearing securities/ inflation-

linkedCopyright © Rong Chen, 2007, Finance Department, XMU 20

Government Securities

—Full faith and credit of the US government

—The most active, liquid and efficient market

—On-the-run/off-the-run

—2 year/5 year/10year/30 year : benchmark securities, market indicator, overliquid

Copyright © Rong Chen, 2007, Finance Department, XMU 21

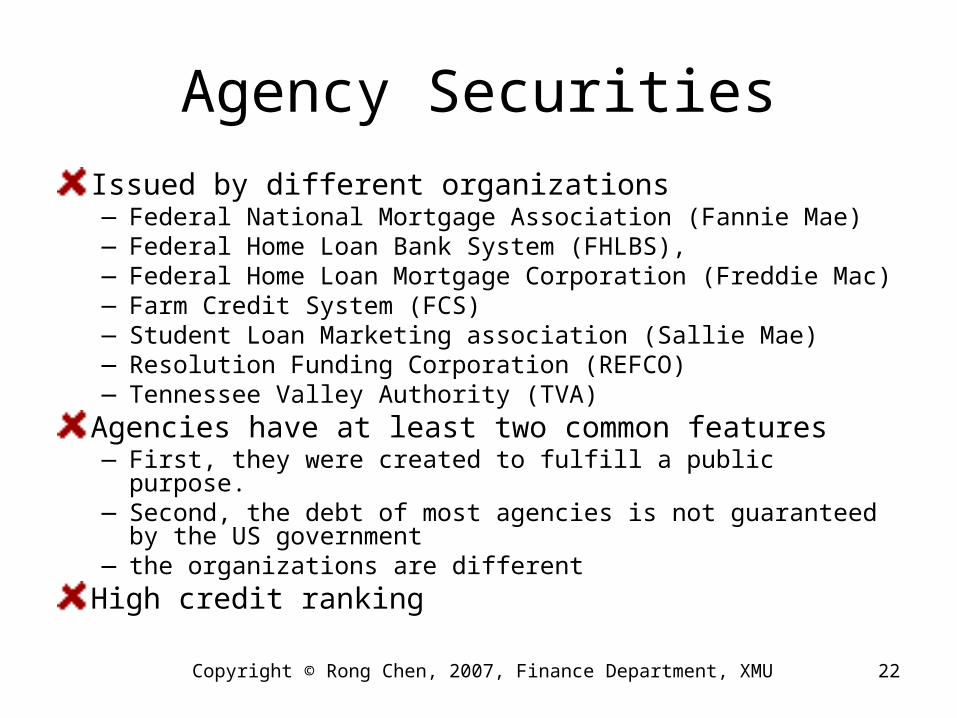

Agency SecuritiesIssued by different organizations—Federal National Mortgage Association (Fannie Mae)—Federal Home Loan Bank System (FHLBS),—Federal Home Loan Mortgage Corporation (Freddie Mac) —Farm Credit System (FCS)—Student Loan Marketing association (Sallie Mae) —Resolution Funding Corporation (REFCO)—Tennessee Valley Authority (TVA)

Agencies have at least two common features—First, they were created to fulfill a public purpose.—Second, the debt of most agencies is not guaranteed by

the US government—the organizations are different

High credit ranking

Copyright © Rong Chen, 2007, Finance Department, XMU 22

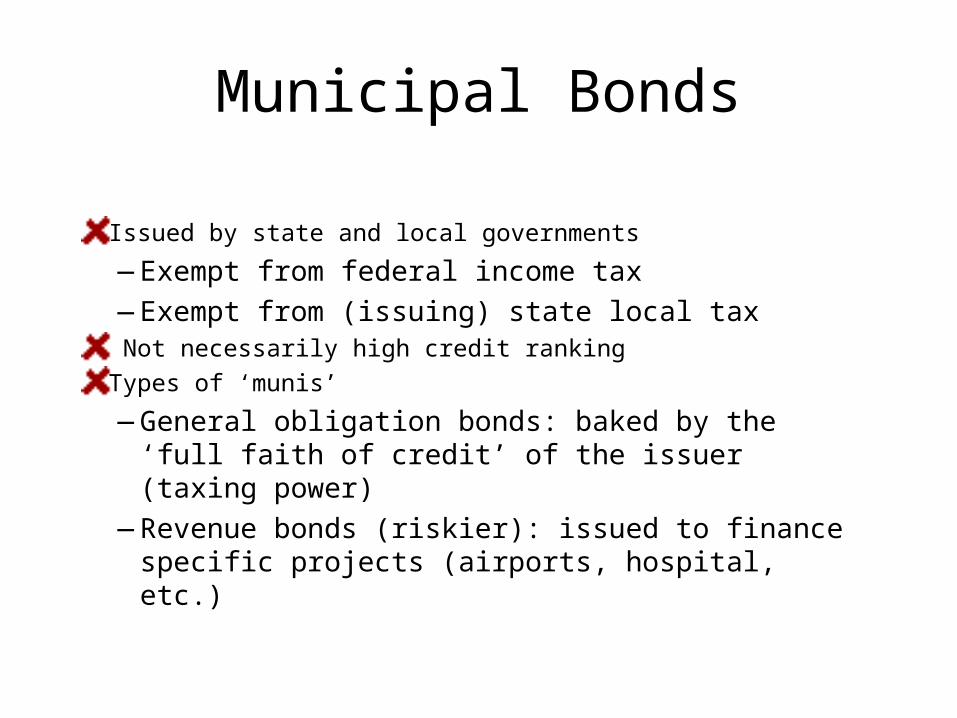

Municipal Bonds

Issued by state and local governments

—Exempt from federal income tax—Exempt from (issuing) state local tax

Not necessarily high credit rankingTypes of ‘munis’

—General obligation bonds: baked by the ‘full faith of credit’ of the issuer (taxing power)

—Revenue bonds (riskier): issued to finance specific projects (airports, hospital, etc.)

Municipal Bonds

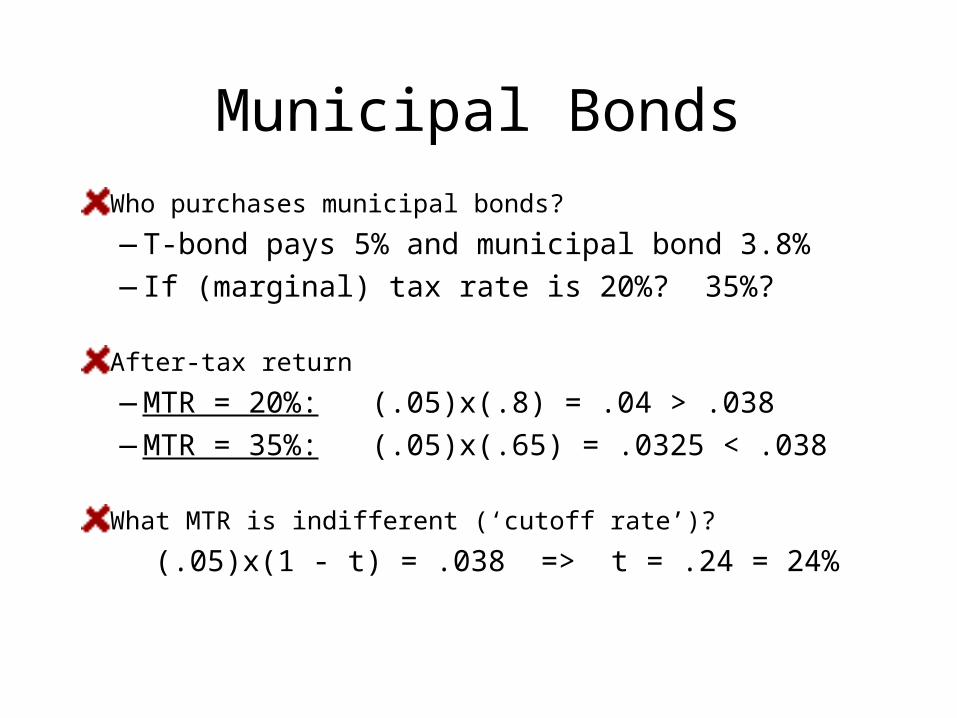

Who purchases municipal bonds?

—T-bond pays 5% and municipal bond 3.8%—If (marginal) tax rate is 20%? 35%?

After-tax return

—MTR = 20%: (.05)x(.8) = .04 > .038—MTR = 35%: (.05)x(.65) = .0325 < .038

What MTR is indifferent (‘cutoff rate’)?

(.05)x(1 - t) = .038 => t = .24 = 24%

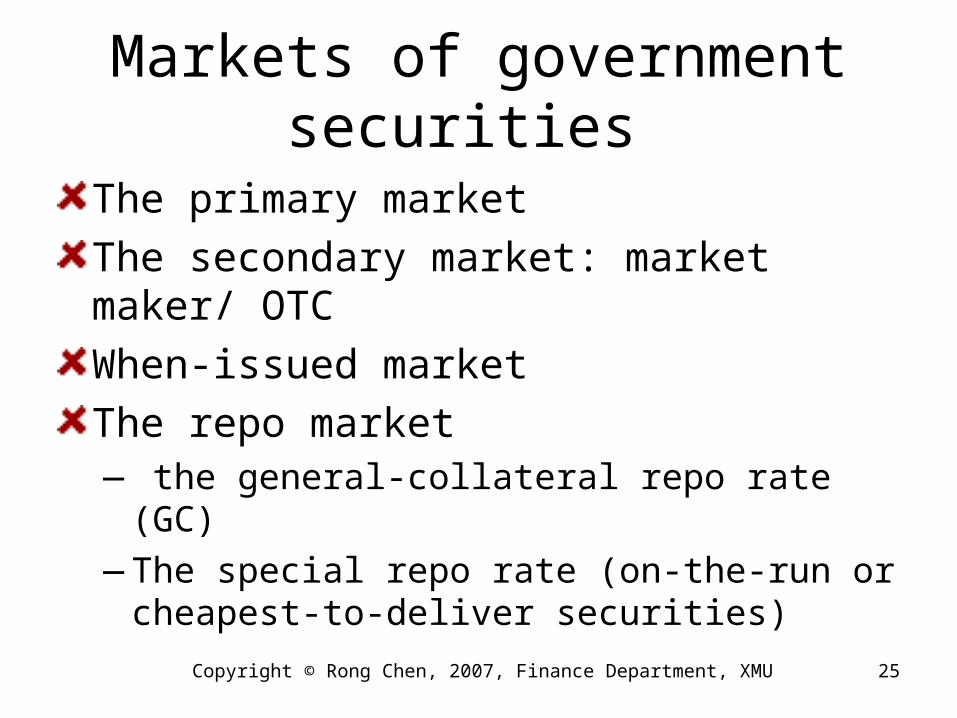

Markets of government securities

The primary marketThe secondary market: market maker/ OTCWhen-issued marketThe repo market— the general-collateral repo rate (GC)—The special repo rate (on-the-run or

cheapest-to-deliver securities)

Copyright © Rong Chen, 2007, Finance Department, XMU 25

Corporate bondsBonds issued by a corporation Typically pay semi-annual coupons3 Sources of Risk

— Interest Rate Risk— Default Risk— Liquidity Risk

Bond indenture contracts stipulate collateral and specify termsDifferent “seniority” classes— Secured Bonds— Subordinated debentures— Debentures

Preferred stocks— ‘Promises’ fixed dividend = coupon rate — Cannot force bankruptcy if no dividend paid

Corporate bonds

Standard & Poor, Moody’s and other firms score ‘the probability of continued & uninterrupted streams of interest & principal payments to investors’

Classes of grades

—Moody’s Investment Grades: Aaa,Aa,A,Baa—Moody’s Speculative Grades: Ba, B, Caa,

Ca, C—Moody’s Default Class: D

Are ratings agencies better able to discern default risk or simply react to events?

Corporate bonds

Lower liquidityCredit marketDefault or credit risk— Bankruptcy, recovery rate—Reorganization—Negotiation between shareholders and

creditors: a package of cash and newly issued securities

Copyright © Rong Chen, 2007, Finance Department, XMU 28

MONEY MARKET INSTUMENTS

1.2.2

Money Markets Instruments

Markets for short term debt

Highly marketable (liquid)

Low risk

Very large denominations

MM mutual funds accessible

Very sensitive to the central bank’s policy — open market operations— key interest rate

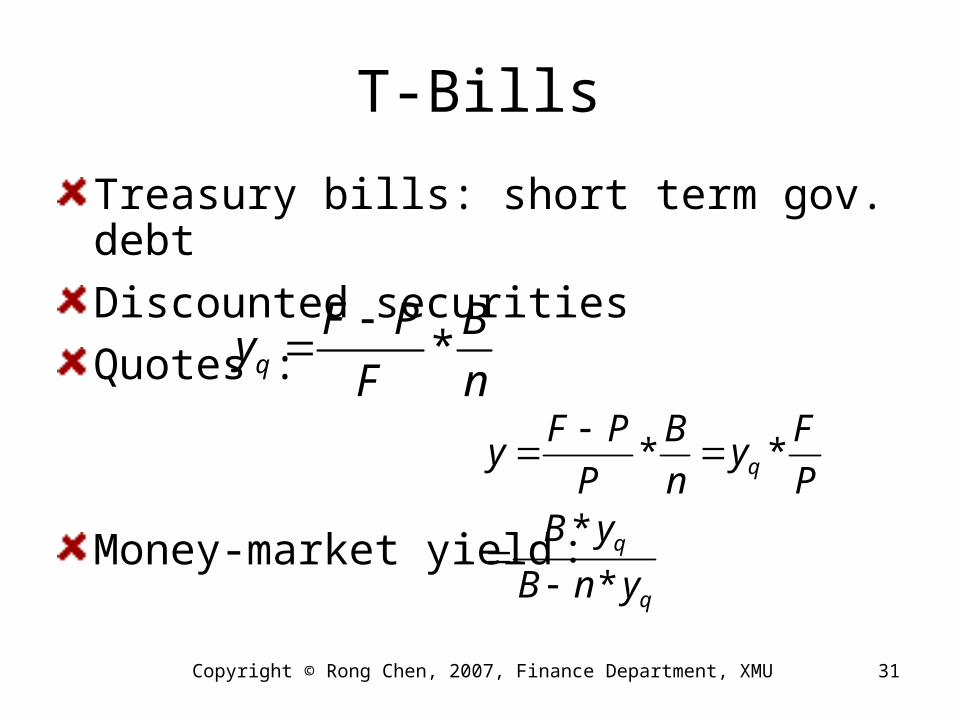

T-Bills

Treasury bills: short term gov. debt

Discounted securitiesQuotes :

Money-market yield :

Copyright © Rong Chen, 2007, Finance Department, XMU 31

*q

F P By

F n

* *

*

*

q

q

q

F P B Fy y

P n PB y

B n y

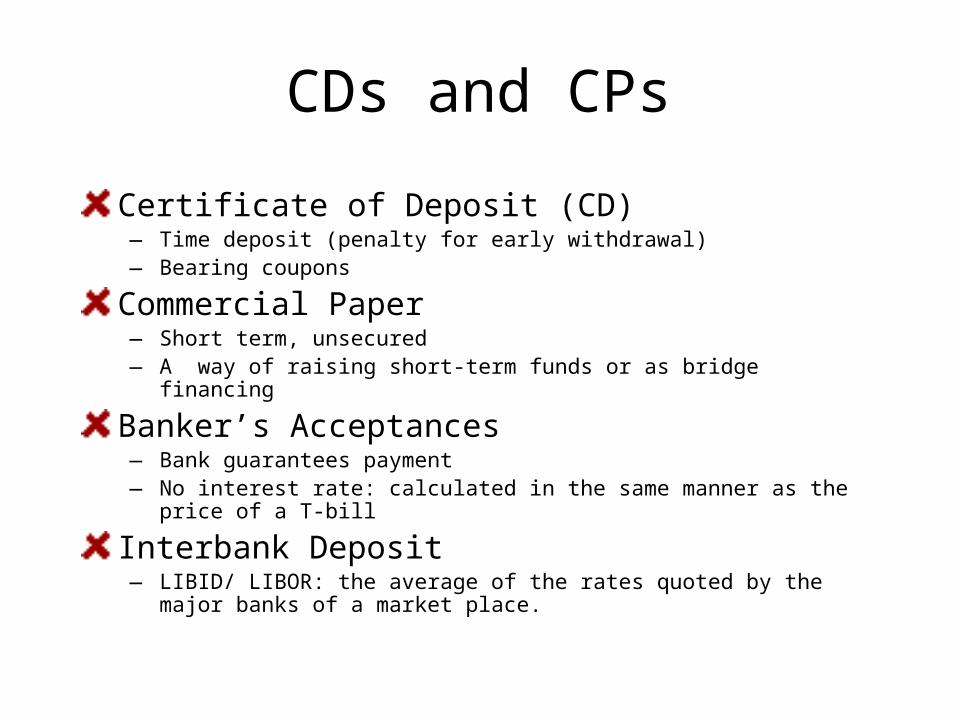

CDs and CPs

Certificate of Deposit (CD)— Time deposit (penalty for early withdrawal)— Bearing coupons

Commercial Paper— Short term, unsecured— A way of raising short-term funds or as bridge financing

Banker’s Acceptances— Bank guarantees payment— No interest rate: calculated in the same manner as the price of a

T-bill

Interbank Deposit— LIBID/ LIBOR: the average of the rates quoted by the major banks

of a market place.

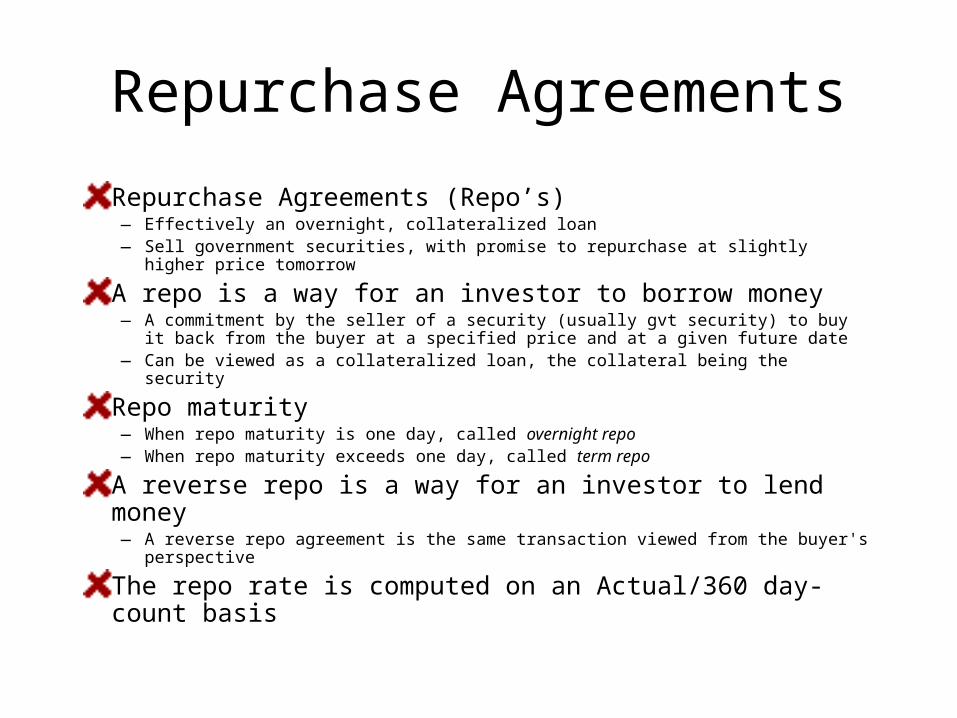

Repurchase Agreements

Repurchase Agreements (Repo’s)— Effectively an overnight, collateralized loan— Sell government securities, with promise to repurchase at slightly higher

price tomorrow

A repo is a way for an investor to borrow money— A commitment by the seller of a security (usually gvt security) to buy it back

from the buyer at a specified price and at a given future date— Can be viewed as a collateralized loan, the collateral being the security

Repo maturity— When repo maturity is one day, called overnight repo— When repo maturity exceeds one day, called term repo

A reverse repo is a way for an investor to lend money— A reverse repo agreement is the same transaction viewed from the buyer's

perspective

The repo rate is computed on an Actual/360 day-count basis

An exampleA German investor needs money—He lends € 1 million …—… of the 10-year Bund benchmark bond (i.e., the Bund 5%

07/04/2011 with a quoted price of 104.11, on 10/29/2001) …—… over 1 month at a repo rate of 4%—There is 160 days' accrued interest as of the starting date of the

transaction

Cash payments—At the beginning of the transaction, investor receives an amount

of cash equal to the gross price of the bond times the nominal of the loan, that is

(104.11+5x160/360)x1,000,000/100= € 1,063,322

—At the end of the transaction, in order to repurchase the securities he will pay the amount of cash borrowed plus the repo interest due over the period, that is

1,063,322 + 1,063,322 x 4 x 30/360= € 1,066,866

Types of repos

Repo and reverse repo

general repo and special repo

Copyright © Rong Chen, 2007, Finance Department, XMU 35

OTHER FIXED-INCOME SECURITIES

1.2.3

Other Fixed-Income Securities

Swaps (Chapter 10)Futures and forwards (Chapter 11)Bonds with embedded options (Chapter 14)Swaptions (Chapter 15)Caps, floors, collars (Chapter 15)Exotic options (Chapter 16)Credit derivatives (Chapter 16)Mortgage-Backed Securities (Chapter 17)etc…

Questions

The structure and development of Chinese bonds markets?

Copyright © Rong Chen, 2007, Finance Department, XMU 38