Financing transport capacity in the United States

Is experience elsewhere useful?

Presentation to Minnesota Agri-growth CouncilMinneapolis, MNMarch 21, 2002

Louis S. ThompsonRailways AdviserThe World Bankhttp://www.worldbank.org/transport/rl_over.htm

Freight demand growth in the U.S.

Demand has grown steadily for truck and railThe relationship of transportation demand to GDP is strong, but a chicken and egg issueLimited potential for modal shiftsLimited effect of electronic data versus freight movement

Ton-Km in the U.S. by mode(000,000 Ton-Km)

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

29 34 39 44 49 54 59 64 69 74 79 84 89 94 99

Rail Truck

Lakes Canals

Pipelines Air

Freight modal shares in the U.S.(% T-Km)

0

10

20

30

40

50

60

50 55 60 65 70 75 80 85 90 95

Rail Truck Lakes Rivers Pipelines Air

Deregulation

U.S. transportation capacity history -- railroads

Rail (responding to market incentives)? Early growth, then decline? Post –Staggers deregulation, reducing capacity,

increasing demand and density.? Dramatic productivity growth, decline in tariffs

Capacity is becoming stretched

Km of Rail Line in the US

0

50000

100000

150000

200000

250000

300000

350000

400000

1820 1840 1860 1880 1900 1920 1940 1960 1980 2000

Class I Railroads

Local Railroads

Regional Railroads

Employees of US railroads

0

500000

1000000

1500000

2000000

2500000

1915 1920 1925 1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Class I Railroads

In 1998 Regional Railroads had 10,995 employees and Local Railroads had 11,741 employees

Productivity in U.S. railroads:Index: 1982=100

0

50

100150

200

250

300350

400

450

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Labor(Ton-km/employee)

Wagons(Ton-km/ton of wagon capacity)

Locomotives:(Ton-km/horsepower)

US rail freight revenue(US cents/ton-km)

0

0.5

1

1.5

2

2.5

3

3.5

1970 1975 1980 1985 1990 1995 2000

Constant 1988 dollars

Current dollars

Source: AAR Handbooks of Railroad facts, various years

1997 U.S. rail traffic

Top 12 commodities, 86 % of ton-miles

00.5

11.5

22.5

33.5

44.5

Coal

Farm

Prod

ucts

Food

Metallic O

res

Lu

mb

er/ Wood

Non

metallic

Min

erals

Prim

ary Metals

Clay, C

oncrete

Petroleu

m/C

oalP

rod

Pu

lp, P

aper

Ch

emicals

Tran

sportation

Eq

pt

Revenue/Ton-MileRevenue/Variable Cost

10.0

Average

Average

Ton-Mi/Mi on U.S. Class I Railroads

2,0003,0004,0005,0006,0007,0008,0009,000

10,00011,00012,000

1950 1960 1970 1980 1990 2000

AmtrakEstablished

Deregulation

Average U.S. freight train speed (mph)

1516171819202122232425

1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

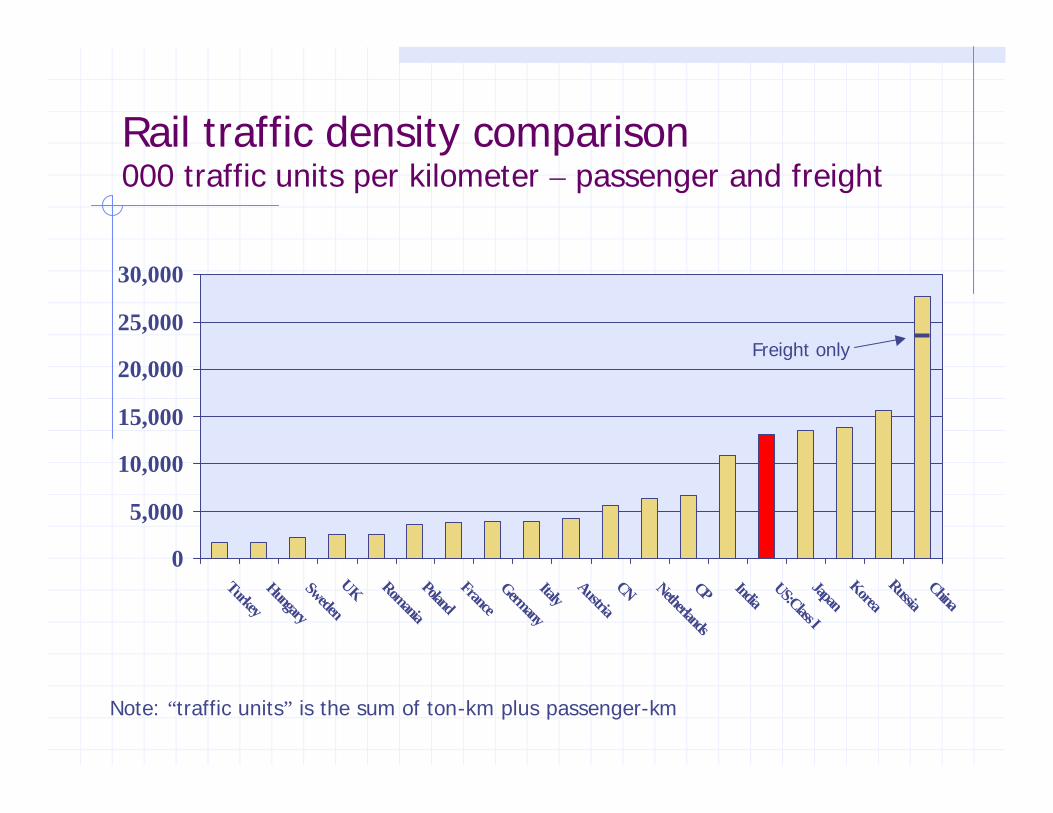

U.S. rail freight line traffic density -- 1995

Rail traffic density comparison000 traffic units per kilometer – passenger and freight

0

5,000

10,000

15,000

20,000

25,000

30,000

Turkey

Hungary

Sweden

UK Romania

Poland France

Germany

Italy Austria

CN Netherlands

CP India US:Class I

JapanKorea

Russia China

Freight only

Note: “traffic units” is the sum of ton-km plus passenger-km

Labor productivity 1999 and compared with 1988

0

2000

4000

6000

8000

10000

12000

14000

Macedonia

Croatia Bulgaria Hungary Cz+Slvk Rom

ania TurkeySlovenia Poland

Armenia

LithuaniaUkraineBelarusLatviaKazakhstanRussiaEstonia

US:Amtrak

Austria Italy France G

ermany*

Finland Canada:CN US: Cl I Frt

0

50

100

150

200

250

TU/Emp

Ratio 99/88 %

Output (000 TU)/Employee

Ratio of:99 output/employee to88 output/employee %

CEE CIS EUR/NA

Source: World Bank Railway Database

U.S. transport capacity: roads and highways

Roads: (the U.S. built them and the traffic came even faster)? Lane-mile capacity growth? More rapid traffic increases (auto and bus vs.

truck)? The urban/rural balance

Result: increasing congestion

Lane-miles of major highways in the U.S.

100,000200,000300,000400,000500,000600,000700,000800,000900,000

1,000,0001,100,0001,200,0001,300,000

1980 1985 1990 1995 2000

InterstatesOther ArterialsTotal

Source: National Transportation Statistics 2000

Interstate Highways mileage

0

5000

1000015000

20000

25000

3000035000

40000

45000

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Highway traffic density in the U.S.Index: 1980=100

90100110120130140150160170180190

1980 1985 1990 1995

Urban InterstateUrban ArterialsRural InterstateRural Arterials

(Vehicle Miles Traveled/Lane-Mile) index

Source: National Transportation Statistics 2000

Urban highway congestion

0.6

0.7

0.8

0.9

1

1.1

1.2

1982 1984 1986 1988 1990 1992 1994 1996

Minneapolis/St Paul

Average for all 68 cities

Congestion Index:>1.0 = “undesirable”

68 cities total. 50 largest plus 18 selected by States.5 congested in 1982, 40 congested in 1997

Source: National Transportation Statistics 2000

Financing issues: past and future

How the U.S. financed transport capacity in the pastTransport financing in U.S. compared with elsewhereThe various degrees of cross subsidy

Balance of U.S. transportation spending in 1998

-120,000

-100,000

-80,000

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

80,000

Ch

arg

es

Sp

end

ing

Net

Ch

arg

es

Sp

end

ing

Net

Ch

arg

es

Sp

end

ing

Net

Ch

arg

es

Sp

end

ing

Net

Ch

arg

es

Sp

end

ing

Net

StateFederal

Highways

Air

Transit

Water

Rail

Average highway user charge revenue: U.K. compared to U.S.(US cents per vehicle mile)

05

101520253035404550

Auto Light trucks Heavy trucks

UKUS

Source: Sansom, Nash, Mackie, et al, “Surface Transport Costs and Charges, Great Britain, 1998And, Addendum to the 1997 Federal Highway Cost Allocation Study, May, 2000

Ratio of highway user charge revenue to fully allocated infrastructure costs

050

100150200250300350400450

Auto Light trucks Heavy trucks

UK

US

Source: Sansom, Nash, Mackie, et al, “Surface Transport Costs and Charges, Great Britain, 1998And, Addendum to the 1997 Federal Highway Cost Allocation Study, May, 2000

Financing capacity in the future:barriers

What can the U.S. afford?? Railroads? Highways

Getting prices right, for capacity and for environmental effectsFunding and administrative barriers (FAA and air traffic control, Corps of Engineers, funding fences)A better public/private balance? Public investment in private rail infrastructure?? Private investment in highway infrastructure?

New technology (road pricing, intelligent vehicles, rail signaling and electrification): does or can it promote efficiency and increase capacity?

GDP/Capita 1999 (US$ at PPP)

0

5000

10000

15000

20000

25000

30000

35000

India

China

Rom

aniaB

razil

Russia

Mexico

Poland

Spain

Ireland

Italy

Sweden

UK Finland

France

Germ

anyN

etherlandsC

anada

Japan

Belgium

Denm

ark

Norw

ayUS

Source: WDR 2000/2001, pg 274/275

Class I railroad investment in track as % of total investment

3035404550556065707580

1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998

Accounting Change

Rate of Return in U.S. Railroads()

-2

0

2

4

6

8

10

12

14

1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Net Railway Operating Income as % of Asset Value

Net income as % of shareholder equity

One approach to relieving urban congestion

Average U.S. freight tariffsIndex: 1990 = 100

0

20

40

60

80

100

120

140

1950 1960 1970 1980 1990 2000

RailLTL truckTL truckBargeProd.Price

Deregulation

Gasoline and diesel fuel prices (US $/gallon) 1998

00.5

11.5

22.5

33.5

44.5

5

Saudi Arabia

Untaxed

Russia

India

China

US A

verageM

exico

Brazil

Canada

Rom

ania

Poland

Germ

any

Japan

Spain

France

Finland

Netherlands

Sweden

Belgium

Denm

ark

Italy

Ireland

Norw

ay

UK

Gasoline (super)Diesel

Source: Fuel Prices and Taxation, GTZ, May 1999

Ratio of highway user charge revenue to marginal transport costs in the U.K. and U.S.

0102030405060708090

Auto Light trucks Heavy trucks

UK

US

Source: Sansom, Nash, Mackie, et al, “Surface Transport Costs and Charges, Great Britain, 1998And, Addendum to the 1997 Federal Highway Cost Allocation Study, May, 2000

Percent of marginal costs attributable to congestion

0102030405060708090

Auto Light trucks Heavy trucks

UK

US

Source: Sansom, Nash, Mackie, et al, “Surface Transport Costs and Charges, Great Britain, 1998And, Addendum to the 1997 Federal Highway Cost Allocation Study, May, 2000