Download - BRITISH SKY BROADCASTING GROUP PLC - BSkyB

All figures and growth rates quoted above are based on adjusted results 1

BRITISH SKY BROADCASTING GROUP PLC

Results for the twelve months ended 30 June 2013

RECORD RESULTS. STRONG PLANS FOR 2013/14

Adjusted results Reported results

Twelve months to 30 June 2012/13 2011/12 Variance 2012/13 2011/12 Variance

Revenue £7,235m £6,791m +7% £7,235m £6,791m +7%

EBITDA £1,692m £1,567m +8% £1,669m £1,587m +5%

Operating profit £1,330m £1,223m +9% £1,291m £1,243m +4%

Earnings per share (basic) 60.0p 50.8p +18% 60.7p 52.6p +15%

Record financial and operational performance on the back of strong demand

Paid-for subscription product growth of 3.3 million to a total of 31.6 million

Revenue of £7,235 million, up 7%

EBITDA of £1,692 million, up 8% and operating profit of £1,330 million, up 9%

Basic earnings per share of 60.0p, up 18%

Free cash flow in excess of £1 billion

ARPU of £577, up £29 year on year

New services resonating strongly with customers

170% growth in internet-connected Sky+HD boxes to 2.7 million

19% increase in Sky Go users to 3.3 million

Fivefold increase in On Demand downloads

200% growth in Sky Store video rentals

Strong set of plans for 2013/14

Extending leadership in core areas:

o New slate of original British drama and outstanding year for Sky Sports

o Offer best quality and value in broadband

o Build advantage in customer service

Investing to accelerate growth and returns from new services:

o Accelerate roll-out of connected boxes

o Extend leadership in mobile video

o Build market-leading on demand service

o Volume-driven impact of £60 million to £70 million expected on operating profit in

2013/14 with rapid returns from accelerated take-up and usage of new services

Growing returns to shareholders

18% increase in full year dividend to 30.0p per share, ninth consecutive year of growth

£500 million capital return to shareholders via share buy-back

2

Jeremy Darroch, Chief Executive, commented:

“We have had another very good year of growth, with revenues up 7%, operating profit up 9% and

earnings per share up 18%. The strength of our financial performance is a result of our successful

transition to more broadly-based growth and sustained investment to create a better service and

wider range of products for customers.

“On the back of this performance, we are increasing returns to shareholders with the ninth

consecutive rise in the ordinary dividend and we intend to seek approval for a further £500 million

of share repurchases.

“Over the course of the year, we added more than three million new paid-for subscription products.

We finished the year strongly with 11% organic growth in product sales for the fourth quarter,

reflecting good demand in all areas. It was a particularly significant quarter for home

communications as good organic growth, combined with the consolidation of the consumer

broadband and fixed-line telephony business acquired from O2, delivered well over a million

product additions.

“In our television business, there has been an excellent response from customers to our new

services. We’ve seen an explosion in on-demand and mobile viewing as more people connect their

Sky boxes to broadband and watch TV on laptops and mobile devices with Sky Go. Sky Go Extra, our

new subscription service, has already attracted more than 150,000 customers in just five months.

Customers tell us they get huge value from these services. The benefits to our business are equally

strong through take-up of higher-tier packages, expanded revenue opportunities and improved

customer satisfaction. We see an exciting opportunity for future growth in this area and we intend

to increase investment over the next year to accelerate growth and returns from these new

services.

“We expect the consumer environment to remain challenging over the coming twelve months.

Against that backdrop, we have a strong set of plans that will extend our leadership in core areas –

on screen, in home communications and in front-line service delivery; accelerate growth in new

services; and improve efficiency to build a bigger, more profitable business for shareholders.”

3

Results highlights

Customer Metrics (unaudited)

Consolidated for the acquisition of O2’s consumer broadband and fixed-line telephony business

As at

30-Jun-13

As at

30-Jun-12

Annual

growth

Quarterly

Growth to

30-Jun-13

Paid-for subscription products (‘000s) 31,634 28,365 +3,269 +1,406

TV 10,422 10,288 +134 +34

HD 4,786 4,343 +443 +117

Multiroom 2,489 2,402 +87 +13

Sky Go Extra 166 - +166 +122

Broadband 4,906 4,001 +905 +519

Telephony 4,501 3,768 +733 +293

Line rental 4,364 3,563 +801 +308

Paid-for products per retail customer 2.8 2.7

New connected TV services (‘000s)

Internet-connected Sky+HD boxes 2,709 995 +1,714 +425

Sky Go unique users 3,257 2,740 +517 -5

Other metrics

Total customers (‘000s) 14,830 14,278 +552 +217

Retail customers 11,153 10,606 +547 +341

Wholesale customers (4)

3,677 3,672 +5 -124

ARPU (2) (5)

£577 £548 +£29

Triple-play(5)

35% 32% +3%

Churn (2)

(5)

10.9% 9.9% +1.0%

Additional KPI summary tables containing further detailed disclosure, including the effect of the O2

consolidation in the fourth quarter may be found at Schedules 1 and 2.

Business Performance (1)

(unaudited) 12 months to

30-Jun-13

12 months to

30-Jun-12

Movement

Revenue £7,235m £6,791m +7%

Adjusted EBITDA £1,692m £1,567m +8%

% Adjusted EBITDA profit margin 23.4% 23.1% +30bps

Adjusted operating profit £1,330m £1,223m +9%

Adjusted profit before tax £1,264m £1,148m +10%

Adjusted basic earnings per share (3)

60.0p 50.8p +18%

Adjusted free cash flow £1,028m £910m +13%

Net debt as at the end of the period £1,183m £876m

1 A reconciliation of adjusted operating profit, adjusted EBITDA and adjusted PBT to reported measures as well as cash generated from

operations to adjusted free cash flow and net debt is set out in Appendix 2. 2

Quarterly annualised. 3 Adjusted basic EPS is calculated from adjusted profit for the period. A reconciliation of reported profit to adjusted profit is set out in

note 6 to the consolidated financial information. 4

Wholesale customers taking at least one paid for Sky channel. The customer numbers are as reported to us at May 2013. 5

Other metrics to include O2 broadband and fixed-line telephony customers from Q1 2013/14 onwards.

4

SUMMARY OF OPERATIONAL AND FINANCIAL PERFORMANCE

We delivered a very strong performance for the year with good operating growth translating

into another record set of financial results. A 7% increase in revenues, combined with a

continued focus on cost efficiency, led to an 8% increase in adjusted EBITDA and an 18%

growth in adjusted basic earnings per share to 60.0p, more than double the level of five

years ago. The full year dividend of 30.0 pence per share is 18% higher year on year, the ninth

consecutive year of growth.

Our successful transition to more broadly-based growth, combined with the acquisition of

O2’s consumer broadband and fixed-line telephony business (“O2”), delivered an increase of

1.4 million subscription products in the fourth quarter. We grew subscription products by

700,000 organically, with a further 706,000 as a result of the acquisition of the O2 business.

In all, we added 3.3 million subscription products over the year to reach 31.6 million, more

than double the level of five years ago. Customers now take an average of 2.8 paid-for

products from Sky.

We closed the quarter with 11.2 million retail customers, an increase of 341,000 in the

quarter. Of these, after reflecting overlap of the two customer bases, 290,000 joined Sky

through our purchase of the O2 business.

ARPU continued to rise to £577, up £29 on last year. Quarterly annualised churn was 10.9%.

We saw good growth in the quarter across all products adding another 117,000 HD

customers and 122,000 Sky Go Extra customers. In all, Sky Go Extra, our new paid-for mobile

TV service, had a total of 166,000 paying customers at year end, just five months after

launch. The transactional element of NOW TV, the sports day pass, got off to a good start as

more than 50,000 individual users purchased day passes in the first three months. We

continue to roll-out NOW TV across multiple platforms having launched on PS3, and this

week concluded an exclusive agreement with LG by which they will make NOW TV available

on their Smart TVs.

Home communications also had a very good quarter on the back of our broadband value

campaign. Before accounting for the acquisition of O2, we added 119,000 customers in

broadband, 140,000 in telephony and 155,000 in line rental. The acquisition of O2 added a

further 400,000 broadband subscribers and 153,000 each of telephony and line rental. In

all, 35% of our customer base now take all three of TV, broadband and telephony from Sky,

up from 32% last year.

STRONG SET OF PLANS FOR 2013/14

We enter the new financial year in a strong position to continue to grow our business and

create value. Our plan for 2013/14 will focus on two broad areas: firstly, extending leadership

in our core areas of strength, on screen, in home communications and in our front-line

customer service delivery; and secondly, accelerating the take-up and usage of new services

where we are already seeing a very strong response from customers.

5

Products

Our focus on providing customers with more ways to watch TV is delivering good results with

strong momentum in the take-up and usage of our connected TV services.

More than 2.7 million customers, one quarter of our TV base, have now connected their

Sky+HD boxes to broadband, a rise of 170% on last year. Combined with an expanded range

of content available on demand, this led to a fivefold increase in the number of average

weekly On Demand downloads over the year. Meanwhile, our mobile video service Sky Go

continues to perform well with quarterly users up 19% to 3.3 million, 166,000 of whom are

now paying £5 a month for our new subscription service Sky Go Extra. Our transactional

movie rental service, Sky Store, also grew strongly, with the number of films rented up

threefold on last year.

With the momentum that we have established, we will push harder in 2013/14 to bring

forward both growth and returns for the business.

There are three key elements to our plan: first, we will step up the roll-out of connected

boxes across our base by offering a low-cost wireless connector to customers that have a

Sky+HD box but haven’t yet connected it to broadband. We will also launch a new WiFi-

enabled Sky+HD box as standard from September, rolling it out to targeted groups of

customers who don’t yet have Sky+HD boxes. This acceleration of our connected Sky+HD

platform will open up access to the full range of On Demand services, increasing the value we

deliver to customers and providing an important platform from which to grow new revenue

streams.

Additionally, we plan to extend our reach into new segments of the market with the launch

of a NOW TV IP streaming box. This will be available from today for just £9.99 and will provide

an attractive new way for customers to access our content via NOW TV.

Second, we are going to extend the leadership that we have established in mobile TV with

Sky Go. We will add more than ten new channels to the service next year and continue to

improve functionality. On the back of this, we will increase our marketing to drive greater

usage and upsell to our new subscription service Sky Go Extra. For £5 a month, this lets

customers register up to four devices per account and download movies and TV shows to

watch offline.

Third, we are going to enhance our market-leading on demand service. We plan to add more

than 20 new channels to our Catch Up TV service and develop the quality of our Box Sets,

increasing the hours of content available by around 50% in the next year. Both initiatives are

aimed at driving on-demand usage and reinforcing our platform superiority. We will

monetise this usage with the new Entertainment Extra+ bundle. In addition, we will expand

Sky Store, our movie rental service offering customers the choice of thousands of

blockbuster movies.

6

Investment in these three areas will enable us to meet the growing customer demand for

new services and drive greater returns from increased take-up of higher-tier packages;

higher transactional revenues; increased penetration of NOW TV; and higher levels of

customer satisfaction and advocacy.

Overall, we expect accelerating the take-up and usage of new services to have an impact of

between £60 million and £70 million on operating profit in 2013/14. The majority of the

investment will be in hardware and largely volume-driven. We expect the aggregate effect of

investment and higher revenue to be broadly neutral in 2014/15 and to increase our profits

in 2015/16 and thereafter.

Content

In 2013/14, we will continue to improve the quality of our on-screen offering building on the

progress we have made in the past year.

In sport, the summer got off to a great start with the Lions Tour to Australia attracting

record audiences for Rugby Union on Sky, with figures for the Test series up 85% on 2009.

Meanwhile, coverage of the Ashes started well this month, with the average audience to the

first test up almost 20% on the last English Ashes series. The coverage benefited from

having its own channel for the first time following the temporary rebrand of Sky Sports 2 HD

as Sky Sports Ashes HD.

We continue to expand the breadth of our offering in sport having secured a number of key

rights agreements in the year. These include live rights to all Home Nations and Republic of

Ireland qualification matches for UEFA Euro 2016 and 2018 FIFA World Cup and a new three-

year broadcasting agreement with the Football League. Starting in August 2015, this will give

us 148 live games each season from the Football League, Capital One Cup and Johnstone’s

Paint Trophy.

Elsewhere, we have continued to strengthen our entertainment offering with a good

response from customers. An Idiot Abroad 3 on Sky 1 delivered the highest weekly audience

ever in the channel’s history, taking account of live, On Demand and time-shifted viewing. US

acquisitions also performed strongly across the portfolio. Arrow on Sky 1 was the most

successful US drama in pay TV history averaging 1.5 million viewers per episode; The

Following was the highest-rating series ever on Sky Atlantic; while Elementary has become

the highest-rating series ever on Sky Living. Meanwhile, season 3 of Game of Thrones broke

new records for On Demand viewing across all platforms including more than 1 million On

Demand downloads through the set-top box and 2.3 million views over Sky Go.

In all, the number of entertainment shows attracting an audience of more than 1 million rose

200% in the last two years to 122.

Looking ahead, we are taking our next big step in original British content this year with a big

step up in commissioned drama across the portfolio. We currently have close to 90 hours in

production with highlights including The Tunnel, a ten-part crime drama, based on the

format of The Bridge and co-produced with Canal+ and Fleming, a new four-part drama

about the life of the celebrated James Bond creator, Ian Fleming.

7

Service

In an environment where customers are taking a broader set of products and services from

us, customer service is an increasingly important differentiator. Sky has consistently been

top of Ofcom’s Customer Satisfaction survey in all three categories of TV, broadband and

telephony.

We know that efficient service is better service. We aim to achieve further improvements in

service quality this year by rolling out our ‘One Service’ pilot. We have been testing One

Service for a number of months with the aim of providing customers with a more joined-up

service experience. As part of this, we are bringing around 700 engineers from our outsource

partner AVC in house in October to help achieve better coordination between the customer

call centres and engineers in the field. Results from the pilot have been excellent with first-

time resolution scores up 10% and our net promoter score, a key measure of customer

advocacy, three times higher than previously.

BROADER CONTRIBUTION

Our partnership with British Cycling delivered further success this month with Chris

Froome's victory in the Tour de France, the 100th anniversary year of the event and the

second consecutive win for Team Sky. This is a great success story for British sport that we

hope will deliver another boost to grassroots cycling and inspire even more people to get

out and ride their bikes.

This year marked the tenth anniversary of Sky Sports Living for Sport, our programme to

help the confidence and life skills of young people using the power of sport. During the

quarter, we reached our target of one third of all UK secondary schools participating in the

scheme. With 1,500 schools now taking part, we have doubled the size of the initiative in the

past year, growing it tenfold in the last four years. In May, we expanded the programme to

Ireland where we aim to engage a third of all schools within three years. Additionally, we

announced a long-term partnership with David Beckham who will support the Sky Sports

Living For Sport programme as a Sky ambassador.

In the arts, our second Sky Arts Ignition project, where we collaborate with major arts

organisations and artists to create new works, opened at the V&A in London. Memory Palace

opened in June, the result of a collaboration between Sky Arts and the V&A to bring an

original work of fiction by Hari Kunzru, Memory Palace, to life.

DETAILED FINANCIAL PERFORMANCE

Unless otherwise stated, all figures and growth rates included below exclude exceptional

items. Adjusting items are detailed on page 10 and in Appendix 2.

As we consistently executed our strategy throughout the year, we delivered excellent

growth in each of revenue, EBITDA, earnings and free cash flow. For the twelve months ended

30 June 2013, revenue growth of 7% combined with our continued focus on operating

efficiency to deliver growth in profit before tax of 10% and earnings per share of 60.0p, up

18%.

8

Revenue

Group revenue increased by 7% to £7,235 million (2012: £6,791 million), with good growth in

both retail and wholesale operations and improvement in the more cyclical operations in

advertising and Sky Business (pubs and clubs).

Retail subscription revenue grew by 6% to £5,951 million (2012: £5,593 million), reflecting

continued product and customer growth and the benefit of the price rise which came into

effect in September 2012. Sky Business returned to growth in the second half to achieve

revenue growth of 1% for the full year.

We delivered a strong performance in wholesale subscription revenue which increased by

13% to £396 million (2012: £351 million). Although the volume of wholesale subscribers was

flat year on year, we continue to benefit from greater take-up of Sky premium channels on

other platforms.

Advertising revenue was flat year on year at £440 million (2012: £440 million), despite the

impact of the Olympics in our first quarter. Sky Media gained market share across the year

to reach 22.2%, with the majority of this growth underpinned by increased ratings for our

media partner channels with whom we share revenue upside. AdSmart, our tailored

advertising product, is on track to launch this summer with good interest from potential

advertisers.

Installation, hardware and service revenue of £87 million was lower year on year (2012: £98

million) driven by improved product reliability, an increased number of customer self-

installations, and higher right-first-time engineer visits.

Other revenue increased by 17% to £361 million (2012: £309 million) due to continued strong

performance from Sky Bet which saw an increase in unique users in the year, and growth in

international programme sales due to more original commissions.

Direct Costs

Programming costs increased by 8% to £2,486 million (2012: £2,298 million) in line with our

expectations. Sports accounted for the majority of the absolute increase due to the

inclusion of Formula 1, Ryder Cup and Lions costs not in the prior year. Movie costs increased

and included investment in expanded rights agreements to support new product offerings

such as Sky Go Extra and NOW TV. Entertainment costs saw the largest percentage increase

(+15% year on year) as we continued to invest in new and exclusive UK-commissioned

content across our channel portfolio.

Our work on network efficiency within our communications operations resulted in excellent

operating leverage in direct network costs, up only 6% to £715 million (2012: £676 million)

despite a 15% increase in organic home communications product volumes.

9

Other Operating Costs

We continued to focus on costs and once again delivered a strong performance, with other

operating costs reducing as a percentage of sales by 80 basis points. Within other operating

costs, every cost line reduced as a percentage of sales year on year, continuing our approach

of seeking efficiency in our cost base to improve margins and reinvestment where

customers see value.

Marketing costs of £1,116 million (2012: £1,064 million) reduced by 30 basis points as a

percentage of sales. Lower cost route-to-market sales and lower acquisition volumes helped

to offset additional advertising spend to support the launch of NOW TV and a national

broadband campaign which included the launch of fibre in the second half of the year.

Subscriber management and supply chain costs were up 4% at £647 million (2012: £621

million) driven largely by higher volume of set-top box sales to Sky Italia and our own higher

broadband volumes.

Transmission, technology and fixed network costs increased by a net 2% to £401 million

(2012: £395 million) due to the increased transmission of additional content from the

Formula 1 channel, Sky Go, NOW TV and On Demand largely offset by continued efficiencies.

Administration costs were up 5% at £540 million (2012: £514 million) reflecting the biennial

phasing of our share incentive plans. Excluding this, administration expenses would have

been flat on last year.

Profits and Earnings

EBITDA of £1,692 million was up strongly at 8%. Depreciation and amortisation of £362

million increased 5% year on year, largely due to new products being depreciated for the first

time and a higher proportion of intangible capital expenditure on assets with shorter

economic lives. Operating profit of £1,330 million was up 9%.

Profit before tax was £1,264 million (2012: £1,148 million), which included the Group’s share of

joint ventures and associates’ profits of £37 million (2012: £32 million) and a net interest

charge of £103 million (2012: £107 million). Taxation for the period was £295 million (2012:

£273 million). Our adjusted effective tax rate was 23% (2012: 24%), benefiting from the

reduction in the rate of UK corporation tax on 1 April 2012 from 26% to 24% and 1 April 2013

to 23%.

Profit after tax for the year was £969 million (2012: £875 million), generating earnings per

share of 60.0 pence (2012: 50.8 pence). Over the year the weighted average number of

shares excluding those held by the Employee Share Ownership Plan (‘ESOP’) for the

settlement of employee share awards was 1,614 million (2012: 1,721 million). The number of

shares, excluding the ESOP shares, at the end of the year was 1,573 million (2012: 1,658

million).

10

Adjusting Items

Reported profit after tax of £979 million (2012: £906 million) includes a net exceptional gain

of £10 million. In addition to the gain of £26 million recognised in previous quarters, we

incurred a £15 million charge related to the acquisition of O2’s consumer broadband and

fixed-line telephony business, and £33 million from a corporate efficiency programme

including the redundancy of approximately 250 head office employees. Other adjusting

items were a £23 million gain relating to mark to market values of derivative financial

instruments and a £17 million gain relating to the tax exceptionals and the tax effect on all

adjusting items. Full details of all of these items are set out in Appendix 2.

Cash Flow & Financial Position

Adjusted free cash flow was 13% higher at £1,028 million (2012: £910 million) reflecting

strong growth in adjusted EBITDA, a positive working capital movement, lower interest and

capital expenditure.

Capital expenditure of £454 million (2012: £457 million) was slightly lower than last year.

Phasing of spend throughout the year picked up in the fourth quarter as we started the

construction of a new building on our main site and commenced the integration of O2

broadband customers.

Net debt increased to £1,183 million (2012: £876 million) primarily as a result of the share

buy-back and dividend growth. Gross debt was £2,593 million, with £1,410 million of cash and

equivalents at 30 June 2013. The Group’s liquidity and headroom remain comfortable.

Uses of Capital and Distributions to Shareholders

Our policy on use of capital continues to focus on four consistent areas: organic growth,

regular dividends, acquisitions and share repurchases. We are a growth company and our

first priority is investing in areas in which we see the opportunity to add revenues and grow

earnings. Today's investment of around £60 million to £70 million in organic growth during

2013/14 is a good example of such an opportunity.

At the same time, we understand the value our shareholders place on a growing regular

return and have once again increased our ordinary dividend in line with earnings growth,

maintaining a sector-leading payout ratio of fifty per cent. The Directors’ proposed final

dividend of 19.0 pence per share takes the total dividend payable in respect of the financial

year to 30.0 pence per share, an increase of 18% over prior year and almost double the level

of six years ago. We have shown through our past successful investments in both

Broadband and HD that our financial flexibility enables us to balance both investment in

growth and cash returns to shareholders. Consequently, looking to the year ahead we

anticipate continued growth in the ordinary dividend.

The ex-dividend date will be 13 November 2013 and, subject to shareholder approval at the

Annual General Meeting to be held on 22 November 2013, the final dividend of 19.0 pence will

be paid on 6 December 2013 to shareholders appearing on the register at the close of

business on 15 November 2013.

11

Finally, we will continue to look to deploy our balance sheet strength in a disciplined way to

enhance returns for shareholders via acquisitions, should attractive opportunities present

themselves, or share repurchases. To this end, we intend to seek shareholder approval at

the Company's AGM for a further £500 million of share repurchases.

As with the current share repurchase programme, we have entered into an agreement with

Twenty-First Century Fox, Inc. (formerly known as News Corporation) (and others) under

which, following any market purchases of shares by the Company, Twenty-First Century Fox,

Inc. will sell to the Company sufficient shares to maintain its percentage shareholding at the

same level as applied prior to those market purchases, ensuring that there will be no change

in Twenty-First Century Fox, Inc.’s economic or voting interests in the Company as a result of

the share buy-back programme. The agreement is conditional on the appropriate

shareholder approvals being granted.

12

Schedule 1 – KPI Summary

All figures (000) FY10/11 FY11/12 FY12/13

unless stated

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Total paid-for

subscription products 25,375 26,058 26,830 27,734 28,365 28,898 29,513 30,228 31,634

TV 10,187 10,213 10,253 10,268 10,288 10,308 10,358 10,388 10,422

Sky+HD 3,822 3,925 4,063 4,222 4,343 4,468 4,561 4,669 4,786

Multiroom 2,250 2,295 2,350 2,378 2,402 2,423 2,467 2,476 2,489

Sky Go Extra - - - - - - - 44 166

Broadband 3,335 3,485 3,651 3,863 4,001 4,103 4,235 4,387 4,906

Telephony 3,101 3,248 3,407 3,627 3,768 3,888 4,022 4,208 4,501

Line Rental 2,680 2,892 3,106 3,376 3,563 3,708 3,870 4,056 4,364

New connected TV

services - 1,829 2,549 3,211 3,735 4,023 4,781 5,546 5,966

Connected HD boxes - 204 442 604 995 1,255 1,715 2,284 2,709

Sky Go unique users - 1,625 2,107 2,607 2,740 2,768 3,066 3,262 3,257

Total products and

services 25,375 27,887 29,379 30,945 32,100 32,921 34,294 35,774 37,600

Other metrics:

Retail customers 10,294 10,371 10,471 10,549 10,606 10,654 10,742 10,812 11,153

Wholesale customers 3,522 3,569 3,629 3,657 3,672 3,714 3,751 3,801 3,677

Total customers 13,816 13,940 14,100 14,206 14,278 14,368 14,493 14,613 14,830

ARPU (£) £538 £535 £544 £546 £548 £550 £568 £576 £577

Triple-play % 27% 28% 29% 31% 32% 33% 33% 34% 35%

Churn 10.4% 11.1% 9.6% 10.1% 9.9% 10.9% 10.3% 10.8% 10.9%

Fixed Network Metrics

On-net base 3,045 3,205 3,403 3,636 3,778 3,882 4,031 4,190 4,696

MPF base 1,686 1,869 2,146 2,423 2,588 2,762 2,926 3,159 3,359

SMPF base 1,359 1,336 1,257 1,213 1,190 1,120 1,105 1,031 1,337

MPF % 55% 58% 63% 67% 69% 71% 73% 75% 72%

SMPF % 45% 42% 37% 33% 31% 29% 27% 25% 28%

Off-net base 290 280 248 227 223 221 204 197 210

Total Broadband 3,335 3,485 3,651 3,863 4,001 4,103 4,235 4,387 4,906

On-net % 91% 92% 93% 94% 94% 95% 95% 96% 96%

Total no. of LLU

exchanges 1,577 1,732 1,907 1,964 1,965 2,036 2,108 2,202 2,323

13

Schedule 2 – Impact of O2 consumer broadband and fixed-line telephony acquisition

All figures (000) FY12/13

unless stated

Q4

opening

Q4 organic

growth

Q4 acquired

growth (O2)

Q4

closing

Total paid-for subscription products 30,228 700 706 31,634

TV 10,388 34 10,422

Sky+HD 4,669 117 - 4,786

Multiroom 2,476 13 - 2,489

Sky Go Extra 44 122 - 166

Broadband 4,387 119 400 4,906

Telephony 4,208 140 153 4,501

Line Rental 4,056 155 153 4,364

New connected TV services 5,546 420 - 5,966

Connected HD boxes 2,284 425 - 2,709

Sky Go unique users 3,262 -5 - 3,257

Total products and services 35,774 1,120 706 37,600

Customers

Retail customers 10,812 51 290 11,153

Wholesale customers 3,801 -124 - 3,677

Total customers 14,613 -73 290 14,830

14

Enquiries:

Analysts/Investors:

Edward Steel Tel: 020 7032 2093

Lang Messer Tel: 020 7032 2657

E-mail: [email protected]

Press:

Alice Macandrew Tel: 020 7705 3000

Stephen Gaynor Tel: 020 7705 3000

E-mail: [email protected]

There will be a presentation for analysts and investors at 9.00 a.m (BST) at Allen & Overy,

One Bishops Square, London, E1 6AD. CEO, Jeremy Darroch and CFO, Andrew Griffith, will

present. Participants should register by contacting Camilla Regan on +44 20 7251 3801 or at

There will be a separate conference call for US analysts and investors at 10.00 a.m. (EDT). To

register for this please contact Dana Diver at Taylor Rafferty on +1 212 889 4350.

Alternatively you may register online by using the following link

http://invite.taylor-rafferty.com/_bskyb/2013Q2CC/Default.htm .

A live webcast of the UK and US call will be available to analysts and investors via the BSkyB

website at http://www.sky.com/corporate. Replays will be subsequently available.

15

Use of measures not defined under IFRS

This press release contains certain information on the Group’s financial position, results and cash flows that have been derived

from measures calculated in accordance with IFRS. This information should not be read in isolation from the related IFRS

measures.

Forward looking statements

This document contains certain forward looking statements with respect to the Group’s financial condition, results of

operations and business and management’s strategy, plans and objectives for the Group. These statements include, without

limitation, those that express forecasts, expectations and projections, such as forecasts, expectations and projections in

relation to new products and services, the potential for growth of free-to-air and pay television, fixed-line telephony,

broadband and bandwidth requirements, advertising growth, DTH and OTT customer growth, Multiroom, On Demand, NOW TV,

Sky Go, Sky Go Extra, Sky+HD and other services, revenue, administration costs and other costs, advertising growth, churn,

profit, cash flow, product penetration, our broadband network footprint, content, wholesale, marketing and capital

expenditure and proposals for returning capital to shareholders.

Although the Company believes that the expectations reflected in such forward looking statements are reasonable, these

statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which

are beyond our control, are difficult to predict and could cause actual results to differ materially from those expressed or

implied or forecast in the forward looking statements. Information on the significant risks and uncertainties are described in

the "Principal risks and uncertainties" section of Sky's Annual Report for the full year ended 30 June 2012 (as updated in Sky’s

results for the six months ended 31 December 2012). Copies of the Annual Report and 31 December 2012 results are available

from the British Sky Broadcasting Group plc web page at www.sky.com/corporate.

All forward looking statements in this document are based on information known to the Group on the date hereof. The Group

undertakes no obligation publicly to update or revise any forward looking statements, whether as a result of new information,

future events or otherwise.

Glossary of Terms

A glossary of terms is included within the Annual Report and on our corporate investor relations web page at

http://corporate.sky.com/investors/glossary .

16

Appendix 1 – Consolidated Financial Information

Consolidated Income Statement for the year ended 30 June 2013

2013 2012

Notes £m £m

Revenue 2 7,235 6,791

Operating expense 3 (5,944) (5,548)

EBITDA 1,669 1,587

Depreciation and amortisation (378) (344)

Operating profit 1,291 1,243

Share of results of joint ventures and associates 11 46 39

Investment income 4 28 18

Finance costs 4 (108) (111)

Profit before tax 1,257 1,189

Taxation 5 (278) (283)

Profit for the year attributable to equity shareholders of the parent company 979 906

Earnings per share from profit for the year (in pence)

Basic 6 60.7p 52.6p

Diluted 6 59.7p 52.2p

Adjusted earnings per share from adjusted profit for the year (in pence)

Basic 6 60.0p 50.8p

Diluted 6 59.1p 50.4p

Consolidated Statement of Comprehensive Income for the year ended 30 June 2013

2013 2012

£m £m

Profit for the year attributable to equity shareholders of the parent company 979 906

Other comprehensive income

Amounts recognised directly in equity

Exchange differences on translation of foreign operations - 2

Gain on revaluation of available-for-sale investments 186 8

(Loss) gain on cash flow hedges (27) 99

Tax on cash flow hedges 7 (23)

166 86

Amounts reclassified and reported in the income statement

Loss on cash flow hedges (48) (29)

Tax on cash flow hedges 11 7

(37) (22)

Other comprehensive income for the year (net of tax) 129 64

Total comprehensive income for the year attributable to equity shareholders of the parent company 1,108 970

17

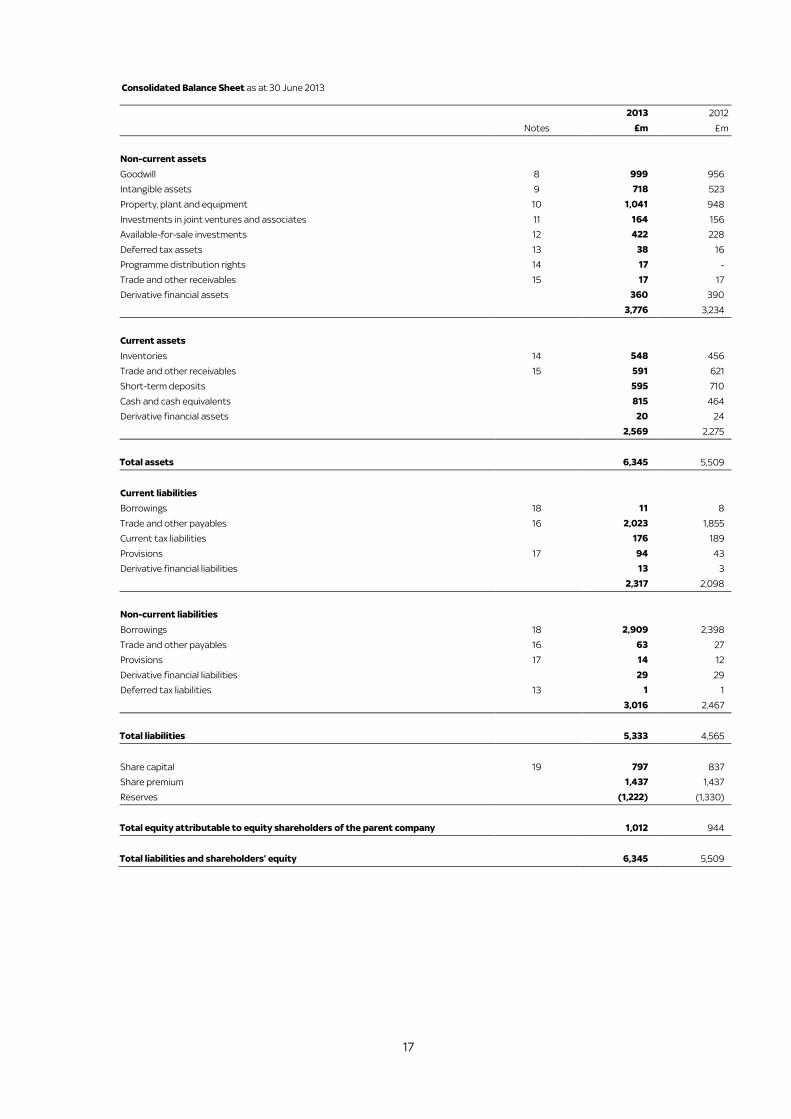

Consolidated Balance Sheet as at 30 June 2013

2013 2012

Notes £m £m

Non-current assets

Goodwill 8 999 956

Intangible assets 9 718 523

Property, plant and equipment 10 1,041 948

Investments in joint ventures and associates 11 164 156

Available-for-sale investments 12 422 228

Deferred tax assets 13 38 16

Programme distribution rights 14 17 -

Trade and other receivables 15 17 17

Derivative financial assets 360 390

3,776 3,234

Current assets

Inventories 14 548 456

Trade and other receivables 15 591 621

Short-term deposits 595 710

Cash and cash equivalents 815 464

Derivative financial assets 20 24

2,569 2,275

Total assets 6,345 5,509

Current liabilities

Borrowings 18 11 8

Trade and other payables 16 2,023 1,855

Current tax liabilities 176 189

Provisions 17 94 43

Derivative financial liabilities 13 3

2,317 2,098

Non-current liabilities

Borrowings 18 2,909 2,398

Trade and other payables 16 63 27

Provisions 17 14 12

Derivative financial liabilities 29 29

Deferred tax liabilities 13 1 1

3,016 2,467

Total liabilities 5,333 4,565

Share capital 19 797 837

Share premium 1,437 1,437

Reserves (1,222) (1,330)

Total equity attributable to equity shareholders of the parent company 1,012 944

Total liabilities and shareholders’ equity 6,345 5,509

18

Consolidated Cash Flow Statement for the year ended 30 June 2013

2013 2012

Notes £m £m

Cash flows from operating activities

Cash generated from operations 21 1,877 1,737

Interest received 29 17

Taxation paid (300) (254)

Net cash from operating activities 1,606 1,500

Cash flows from investing activities

Dividends received from joint ventures and associates 43 39

Net funding to joint ventures and associates (4) (6)

Proceeds on disposal of an investment 4 -

Purchase of property, plant and equipment (203) (228)

Purchase of intangible assets (251) (229)

Purchase of subsidiaries (net of cash and cash equivalents purchased) (197) (15)

Purchase of available-for-sale investments (9) (5)

Decrease (increase) in short-term deposits 115 (280)

Net cash used in investing activities (502) (724)

Cash flows from financing activities

Net proceeds from borrowings 498 -

Repayment of obligations under finance leases (1) (1)

Proceeds from disposal of shares in Employee Share Ownership Plan (“ESOP”) 15 10

Purchase of own shares for ESOP (69) (161)

Purchase of own shares for cancellation (627) (546)

Interest paid (128) (125)

Dividends paid to shareholders (441) (410)

Net cash used in financing activities (753) (1,233)

Net increase (decrease) in cash and cash equivalents 351 (457)

Cash and cash equivalents at the beginning of the year 464 921

Cash and cash equivalents at the end of the year 815 464

19

Consolidated Statement of Changes in Equity for the year ended 30 June 2013

Share capital

Share premium

ESOP reserve

Hedging reserve

Available- for-sale reserve

Other reserves

Retained earnings

Total shareholders’

equity

£m £m £m £m £m £m £m £m

At 1 July 2011 876 1,437 (107) 14 157 358 (1,700) 1,035

Profit for the year - - - - - - 906 906

Exchange differences on translation of foreign operations

- - - - - 2 - 2

Revaluation of available-for-sale investments - - - - 8 - - 8

Recognition and transfer of cash flow hedges - - - 70 - - - 70

Tax on items taken directly to equity - - - (16) - - - (16)

Total comprehensive income for the year - - - 54 8 2 906 970

Share-based payment - - (5) - - - (80) (85)

Tax on items taken directly to equity - - - - - - (10) (10)

Share buy-back programme (see note 20):

- Purchase of own shares for cancellation (39) - - - - 39 (546) (546)

- Financial liability for close period purchases - - - - - - (10) (10)

Dividends - - - - - - (410) (410)

At 30 June 2012 837 1,437 (112) 68 165 399 (1,850) 944

Profit for the year - - - - - - 979 979

Revaluation of available-for-sale investments - - - - 186 - - 186

Recognition and transfer of cash flow hedges - - - (75) - - - (75)

Tax on items taken directly to equity - - - 18 - - - 18

Total comprehensive income for the year - - - (57) 186 - 979 1,108

Share-based payment - - (35) - - - 61 26

Tax on items taken directly to equity - - - - - - 8 8

Share buy-back programme (see note 20):

- Purchase of own shares for cancellation (40) - - - - 40 (617) (617)

- Financial liability for close period purchases - - - - - - (16) (16)

Dividends - - - - - - (441) (441)

At 30 June 2013 797 1,437 (147) 11 351 439 (1,876) 1,012

20

Notes to the consolidated financial statements

1 Basis of Preparation

The financial information set out in this preliminary announcement does not constitute statutory financial statements for the years ended

30 June 2013 or 2012, for the purpose of the Companies Act 2006, but is derived from those financial statements. Statutory financial

statements for 2013, on which the Group’s auditors have given an unqualified report which does not contain statements under s. 498(2) or

(3) of the Companies Act 2006, will be filed with the Registrar of Companies by 31 December 2013. Statutory financial statements for 2012

have been filed with the Registrar of Companies. The Group’s auditors have reported on those accounts; their reports were unqualified and

did not contain statements under s. 498(2) or (3) of the Companies Act 2006.

Whilst the financial information included in this press release has been prepared in accordance with International Financial Reporting

Standards (“IFRS”) as adopted for use in the European Union and as issued by the International Accounting Standards Board, this

announcement does not itself contain sufficient information to comply with IFRS. The accounting policies applied in preparing this financial

information are consistent with the Group’s financial statements for the year ended 30 June 2012 except in relation to the mandatory

adoption of new accounting standards and revisions and amendments to existing accounting standards, none of which had any significant

impact on the Group’s results or financial position.

The Group maintains a 52 or 53 week fiscal year ending on the Sunday nearest to 30 June in each year. In fiscal year 2013, this date was 30

June 2013, this being a 52 week year (fiscal year 2012: 1 July 2012, 52 week year). For convenience purposes, the Group continues to date its

consolidated financial statements as at 30 June and to refer to the accounting period as a “year” for reporting purposes.

2 Revenue

2013 2012

£m £m

Retail subscription 5,951 5,593

Wholesale subscription 396 351

Advertising 440 440

Installation, hardware and service 87 98

Other 361 309

7,235 6,791

3 Operating expense

2013 2012

£m £m

Programming 2,487 2,298

Direct networks 686 676

Marketing 1,117 1,064

Subscriber management and supply chain 673 621

Transmission, technology and fixed networks 405 395

Administration

576 494

5,944 5,548

21

4 Investment income and finance costs

2013 2012

£m £m

Investment income

Interest on cash, cash equivalents and short-term deposits 9 14

Dividends received from available-for-sale investments 19 4

28 18

2013 2012

£m £m

Finance costs

– Interest payable and similar charges

£743 million/£750 million Revolving Credit Facilities (“RCF”) (i)

(2) (8)

Guaranteed Notes (122) (115)

Finance lease interest (7) (7)

(131) (130)

– Other finance income (expense)

Remeasurement of borrowings and borrowings-related derivative financial instruments(ii)

22 20

Remeasurement of other derivative financial instruments (ii)

(1) -

(Loss) gain arising on derivatives in a designated fair value hedge accounting relationship (34) 47

Gain (loss) arising on adjustment for hedged item in a designated fair value hedge

accounting relationship 36 (48)

23 19

(108) (111)

(i) Included in RCF costs for the year ended 30 June 2012 is a write-off of £5 million relating to the facility fee on the £750 million RCF

which has now been replaced with the £743 million RCF.

(ii) Not qualifying for hedge accounting.

5 Taxation

Taxation recognised in the income statement

2013 2012

£m £m

Current tax expense

Current year 332 303

Adjustment in respect of prior years (44) (33)

Total current tax charge 288 270

Deferred tax expense

Origination and reversal of temporary differences (20) 6

Adjustment in respect of prior years 10 7

Total deferred tax (credit) charge (10) 13

Taxation 278 283

Taxation relates to a £275 million UK corporation tax charge (2012: £280 million) and £3 million overseas corporation tax charge (2012: £3

million).

22

6 Earnings per share

The weighted average number of shares for the year was:

2013 2012

Millions of shares Millions of shares

Ordinary shares 1,633 1,731

ESOP trust ordinary shares (19) (10)

Basic shares 1,614 1,721

Dilutive ordinary shares from share options 26 16

Diluted shares 1,640 1,737

The calculation of diluted earnings per share excludes no share options (2012: less than 1 million) which could potentially dilute earnings per

share in the future, but which have been excluded from the calculation of diluted earnings per share as they are anti-dilutive in the year.

Basic and diluted earnings per share are calculated by dividing the profit for the year into the weighted average number of shares for the

year. In order to provide a measure of underlying performance, management have chosen to present an adjusted profit for the year which

excludes items that may distort comparability. Such items arise from events or transactions that fall within the ordinary activities of the

Group but which management believes should be separately identified to help explain underlying performance.

2013 2012

£m £m

Reconciliation from profit for the year to adjusted profit for the year

Profit for the year 979 906

Credit received following final settlement of disputes with a former manufacturer of set-

top boxes (33) -

Costs relating to a corporate efficiency programme 33 -

Credit received following an Ofcom determination (32) -

Costs relating to one-off upgrade of set-top boxes 31 -

Costs relating to programme to offer wireless connectors to selected Sky Movies

customers 25 -

Cost relating to the acquisition and integration of the O2 consumer broadband and fixed-

line telephony business 15 -

Net recovery of costs in relation to News Corporation (subsequently renamed Twenty-

First Century Fox, Inc.) proposal - (31)

Costs relating to a restructuring exercise - 11

RCF fee write-off (see note 4) - 5

Remeasurement of all derivative financial instruments not qualifying for hedge accounting

and hedge ineffectiveness (see note 4) (23) (19)

Profit on disposal of joint venture (see note 11) (9) (7)

Tax adjusting items and the tax effect of above items (17) 10

Adjusted profit for the year 969 875

7 Dividends

2013 2012

£m £m

Dividends declared and paid during the year

2011 Final dividend paid: 14.54p per ordinary share - 253

2012 Interim dividend paid: 9.20p per ordinary share - 157

2012 Final dividend paid: 16.20p per ordinary share 265 -

2013 Interim dividend paid: 11.00p per ordinary share 176 -

441 410

The 2013 final dividend proposed is 19.0 pence per ordinary share being £299 million. The dividend was not declared at the balance

sheet date and is therefore not recognised as a liability as at 30 June 2013.

23

8 Goodwill

2013 2012

£m £m

Carrying value 999 956

During the year, the Group completed the acquisition of the O2 consumer broadband and fixed-line telephony business which resulted

in additional goodwill of £49 million.

9 Intangible assets

Internally

generated

intangible

assets

Software

development

(external) and

software

licences

Customer

contracts

and related

customer

relationships

Other

intangible

assets

Internally

generated

intangible

assets not

yet available

for use

Acquired

intangible

assets not

yet

available

for use Total

£m £m £m £m £m £m £m

Cost

At 1 July 2012 252 427 60 224 54 103 1,120

Additions from

business combinations - - 137 2 - - 139

Additions 102 45 - 66 25 20 258

Disposals (15) (6) - - (2) (7) (30)

Transfers 47 59 - - (47) (59) -

At 30 June 2013 386 525 197 292 30 57 1,487

Amortisation

At 1 July 2012 122 308 9 158 - - 597

Amortisation 72 55 7 57 - - 191

Disposals (15) (6) - - (2) (7) (30)

Impairments 2 - - - 2 7 11

At 30 June 2013 181 357 16 215 - - 769

Carrying amounts

At 1 July 2012 130 119 51 66 54 103 523

At 30 June 2013 205 168 181 77 30 57 718

In order to improve the presentation of the Group’s intangible assets “Customer contracts and related customer relationships” have been

disaggregated from the “Other intangible assets” category and “Software licences” have been aggregated with the “Software development

(external)” category. The prior year categories have been re-presented accordingly.

24

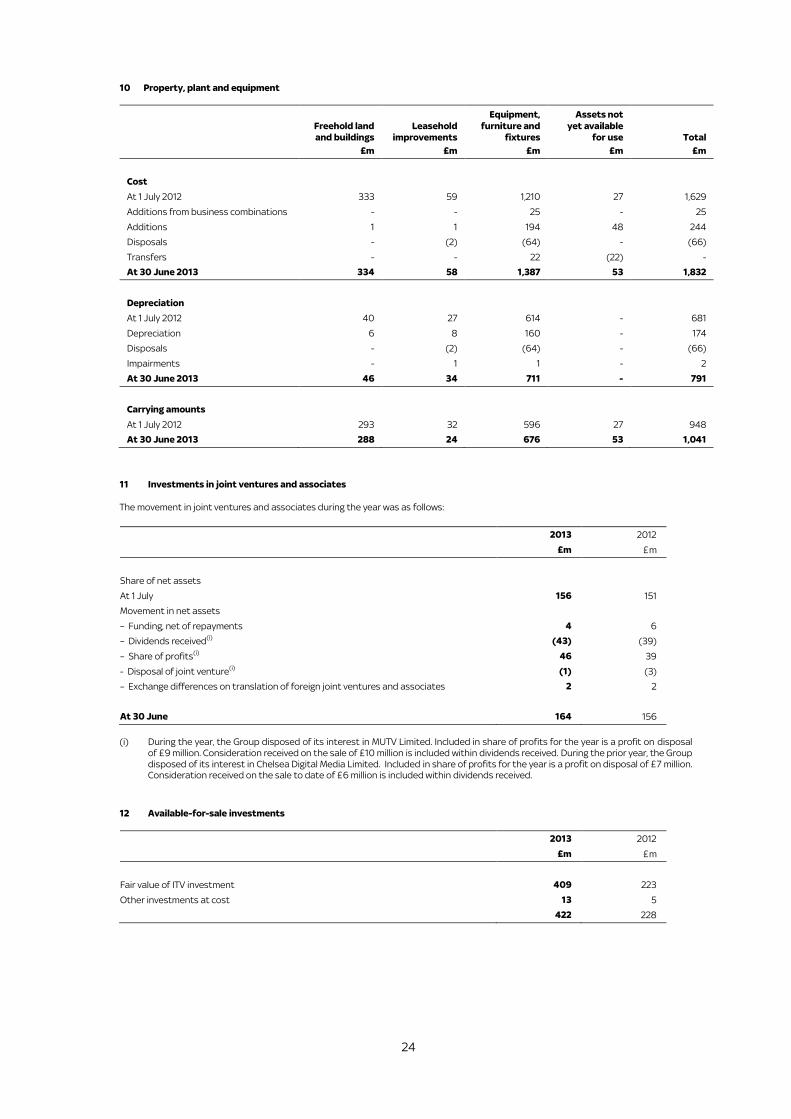

10 Property, plant and equipment

Freehold land

and buildings

Leasehold

improvements

Equipment,

furniture and

fixtures

Assets not

yet available

for use Total

£m £m £m £m £m

Cost

At 1 July 2012 333 59 1,210 27 1,629

Additions from business combinations - - 25 - 25

Additions 1 1 194 48 244

Disposals - (2) (64) - (66)

Transfers - - 22 (22) -

At 30 June 2013 334 58 1,387 53 1,832

Depreciation

At 1 July 2012 40 27 614 - 681

Depreciation 6 8 160 - 174

Disposals - (2) (64) - (66)

Impairments - 1 1 - 2

At 30 June 2013 46 34 711 - 791

Carrying amounts

At 1 July 2012 293 32 596 27 948

At 30 June 2013 288 24 676 53 1,041

11 Investments in joint ventures and associates

The movement in joint ventures and associates during the year was as follows:

2013 2012

£m £m

Share of net assets

At 1 July 156 151

Movement in net assets

– Funding, net of repayments 4 6

– Dividends received(i)

(43) (39)

– Share of profits(i)

46 39

- Disposal of joint venture(i)

(1) (3)

– Exchange differences on translation of foreign joint ventures and associates 2 2

At 30 June 164 156

(i) During the year, the Group disposed of its interest in MUTV Limited. Included in share of profits for the year is a profit on disposal

of £9 million. Consideration received on the sale of £10 million is included within dividends received. During the prior year, the Group

disposed of its interest in Chelsea Digital Media Limited. Included in share of profits for the year is a profit on disposal of £7 million.

Consideration received on the sale to date of £6 million is included within dividends received.

12 Available-for-sale investments

2013 2012

£m £m

Fair value of ITV investment 409 223

Other investments at cost 13 5

422 228

25

13 Deferred tax

Recognised deferred tax assets (liabilities)

Accelerated tax

depreciation

Tax losses

Short-term

temporary

differences

Share-based

payments

temporary

differences

Financial

instruments

temporary

differences

Total

£m £m £m £m £m £m

At 1 July 2012 12 1 6 26 (30) 15

(Charge) credit to income (2) (1) - 18 (5) 10

Credit to equity - - - 6 18 24

Acquisition of subsidiaries (12) - - - - (12)

Effect of change in tax rate

- Income 1 - (1) (1) 1 -

At 30 June 2013 (1) - 5 49 (16) 37

14 Inventories

2013 2012

£m £m

Television programme rights 470 379

Set-top boxes and related equipment 70 69

Other inventories 8 8

Current inventory 548 456

Non-current programme distribution rights 17 -

Total inventory 565 456

15 Trade and other receivables

2013 2012

£m £m

Net trade receivables 74 81

Amounts receivable from joint ventures and associates 8 8

Amounts receivable from other related parties 7 12

Prepayments 309 294

Accrued income 162 155

VAT 1 1

Other 30 70

Current trade and other receivables 591 621

Prepayments 6 7

Other receivables 11 10

Non-current trade and other receivables 17 17

Total trade and other receivables 608 638

26

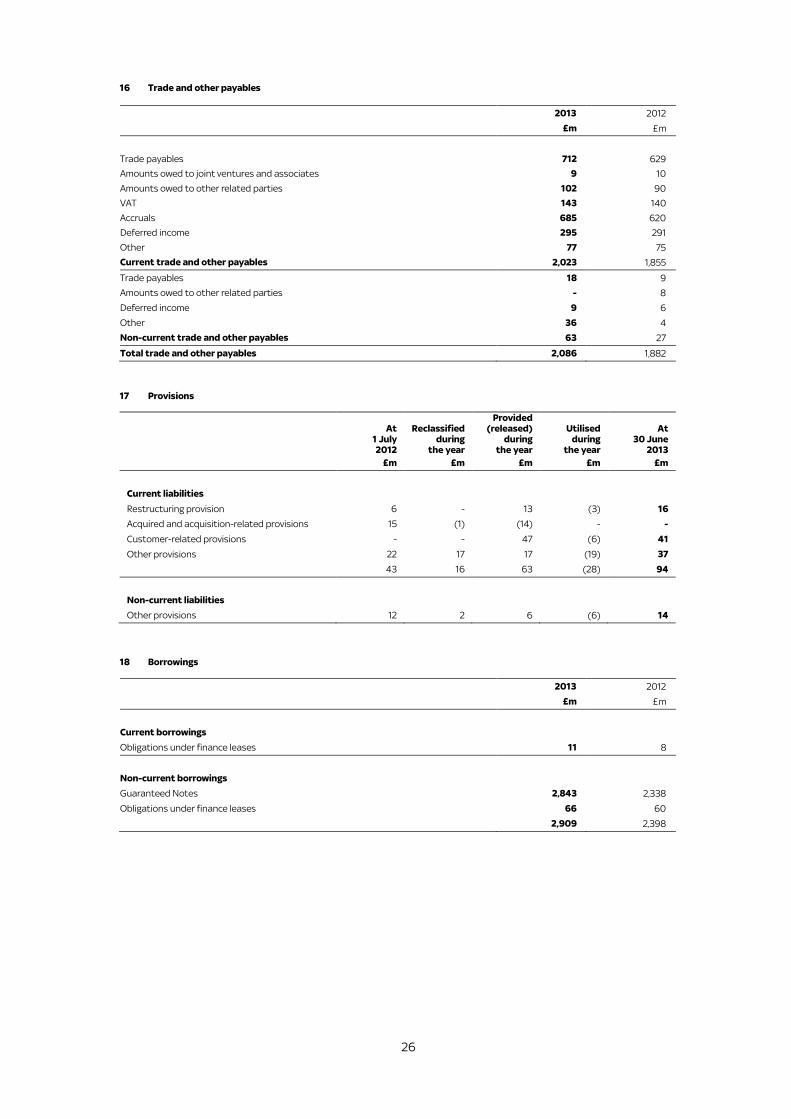

16 Trade and other payables

2013 2012

£m £m

Trade payables 712 629

Amounts owed to joint ventures and associates 9 10

Amounts owed to other related parties 102 90

VAT 143 140

Accruals 685 620

Deferred income 295 291

Other 77 75

Current trade and other payables 2,023 1,855

Trade payables 18 9

Amounts owed to other related parties - 8

Deferred income 9 6

Other 36 4

Non-current trade and other payables 63 27

Total trade and other payables 2,086 1,882

17 Provisions

At 1 July 2012

Reclassified during

the year

Provided (released)

during the year

Utilised during

the year

At 30 June

2013

£m £m £m £m £m

Current liabilities

Restructuring provision 6 - 13 (3) 16

Acquired and acquisition-related provisions 15 (1) (14) - -

Customer-related provisions - - 47 (6) 41

Other provisions 22 17 17 (19) 37

43 16 63 (28) 94

Non-current liabilities

Other provisions 12 2 6 (6) 14

18 Borrowings

2013 2012

£m £m

Current borrowings

Obligations under finance leases 11 8

Non-current borrowings

Guaranteed Notes 2,843 2,338

Obligations under finance leases 66 60

2,909 2,398

27

19 Share capital

2013 2012

£m £m

Allotted, called-up and fully paid shares of 50p

1,593,905,182 (2012: 1,674,454,881) 797 837

20 Shareholders’ equity Purchase of own equity shares for cancellation

On 29 November 2011, at the Company’s AGM, the Company was granted the authority to return £750 million of capital to shareholders via

a share buy-back programme. This authority was subject to an agreement between the Company and Twenty-First Century Fox, Inc.

(formerly known as News Corporation) (and others) dated 28 July 2011 whereby following any market purchases of shares by the Company,

Twenty-First Century Fox, Inc. would sell to the Company sufficient shares to maintain its percentage shareholding at the same level as

applied prior to those market purchases. The price payable to Twenty-First Century Fox, Inc. would be the price payable by the Company in

respect of the relevant market purchases (the “2011 Share Buy-back Agreement”).

At the Company’s AGM on 1 November 2012, the Company was granted the authority to return a further £500 million of capital to

shareholders via a share buy-back programme. This authority was subject to an agreement between the Company and Twenty-First

Century Fox, Inc. (and others) dated 28 July 2012 on substantially the same terms as the 2011 Share Buy-back Agreement.

During the year, the Company purchased, and subsequently cancelled, 80,549,699 ordinary shares at an average price of £7.75 per share,

with a nominal value of £40 million, for a consideration of £627 million. Consideration included stamp duty and commission of £3 million.

This represents 5% of called-up share capital at the beginning of the period. Of these purchases, the Company purchased, and

subsequently cancelled, 31,525,314 ordinary shares from Twenty-First Century Fox, Inc. at an average price of £7.75 per share, with a nominal

value of £16 million, for a consideration of £245 million. Consideration included stamp duty of £1 million.

During the prior year, the Company purchased, and subsequently cancelled, 78,387,718 ordinary shares at an average price of £6.92 per

share, with a nominal value of £39 million, for a total consideration of £546 million. Consideration included stamp duty and commission of

£3 million. This represented 4% of called-up share capital at the beginning of the period. Of these purchases, the Company purchased, and

subsequently cancelled, 30,679,157 ordinary shares from Twenty-First Century Fox, Inc. at an average price of £6.92 per share, with a

nominal value of £15 million, for a consideration of £213 million. Consideration included stamp duty of £1 million.

21 Notes to the Consolidated Cash Flow Statement

Reconciliation of profit before tax to cash generated from operations

2013 2012

£m £m

Profit before tax 1,257 1,189

Depreciation and impairment of property, plant and equipment 176 179

Amortisation and impairment of intangible assets 202 165

Share-based payment expense 80 66

Net finance costs 80 93

Share of results of joint ventures and associates (46) (39)

1,749 1,653

Decrease (increase) in trade and other receivables 35 (32)

Increase in inventories (93) (81)

Increase in trade and other payables 136 175

Increase in provisions 52 25

Decrease in derivative financial instruments (2) (3)

Cash generated from operations 1,877 1,737

22 Events after the reporting period

On 25 July 2013, the Board agreed to seek the necessary approvals to return a further £500 million of capital to shareholders via a share

buy-back programme. Shareholder approvals will be sought at the Company’s AGM on 22 November 2013. The Company has entered into an

agreement with Twenty-First Century Fox, Inc. (formerly known as News Corporation) (and others) under which, following any market

purchases of shares by the Company, Twenty-First Century Fox, Inc. will sell to the Company sufficient shares to maintain its percentage

shareholding at the same level as applied prior to those market purchases. The price payable to Twenty-First Century Fox, Inc. will be the

price payable by the Company in respect of the relevant market purchases. The agreement is conditional on the appropriate shareholder

approvals being granted. The effect of the agreement is to provide that there will be no change in Twenty-First Century Fox, Inc.’s economic

or voting interests in the Company as a result of the share buy-back programme.

28

Appendix 2 – Non-GAAP measures

Reconciliation of cash generated from operations to adjusted free cash flow

for the year ended 30 June 2013

2013 2012

Note £m £m

Cash generated from operations 21 1,877 1,737

Interest received 29 17

Taxation paid (300) (254)

Dividends received from joint ventures and associates 43 39

Net funding to joint ventures and associates (4) (6)

Purchase of property, plant and equipment (203) (228)

Purchase of intangible assets (251) (229)

Interest paid (128) (125)

Free cash flow 1,063 951

Receipt following final settlement of disputes with a former manufacturer of set-top boxes(i)

(10) -

Cash paid relating to a corporate efficiency programme 4 -

Receipt following an Ofcom determination(i)

(28) -

Cash paid relating to one-off upgrade of set-top boxes(i)

7 -

Cash paid relating to programme to offer wireless connectors to selected Sky Movies

customers(i)

1 -

Cash paid relating to the acquisition and integration of the O2 consumer broadband and

fixed-line telephony business 4 -

Net recovery of costs in relation to News Corporation (subsequently renamed Twenty-First

Century Fox, Inc.) proposal(i)

- (13)

Cash paid relating to a restructuring exercise - 3

Recovery of import duty on set-top boxes(i)

- (25)

Receipt on disposal of joint venture(i)

(13) (6)

Adjusted free cash flow 1,028 910

(i) Net of applicable corporation tax.

Net debt

2013 2012

£m £m

Current borrowings 11 8

Non-current borrowings 2,909 2,398

Borrowings-related derivative financial instruments (327) (356)

Gross debt 2,593 2,050

Cash and cash equivalents (815) (464)

Short-term deposits (595) (710)

Net debt 1,183 876

29

Consolidated Income Statement - reconciliation of reported and adjusted numbers

Notes: explanation of adjusting items for the year ended 30 June 2013

A. Costs of £1 million relating to a corporate efficiency programme.

B. Credit of £32 million relating to a credit note received following an Ofcom determination and costs of £3 million relating to the acquisition and

integration of the O2 consumer broadband and fixed-line telephony business.

C. Costs of £1 million relating to a corporate efficiency programme.

D. Credit of £33 million relating to the final settlement of disputes with a former manufacturer of set-top boxes (net of associated costs and including

an impairment of £6 million in relation to associated intangible assets), costs of £31 million relating to one-off upgrade of set-top boxes, costs of

£25 million relating to a programme to offer wireless connectors to selected Sky Movies customers, costs of £2 million relating to the acquisition

and integration of the O2 consumer broadband and fixed-line telephony business and costs of £1 million relating to a corporate efficiency

programme.

E. Costs of £1 million relating to a corporate efficiency programme, significantly an impairment of associated intangible and tangible assets, and £3

million relating to the acquisition and integration of the O2 consumer broadband and fixed-line telephony business.

F. Costs of £29 million relating to a corporate efficiency programme, primarily redundancy costs and including an impairment of £5 million in relation

to associated intangible and tangible assets, and £7 million relating to the acquisition and integration of the O2 consumer broadband and fixed-

line telephony business, including amortisation of £4 million in relation to associated intangible assets.

G. Profit on disposal of the Group’s interest in MUTV Limited.

H. Remeasurement of all derivative financial instruments not qualifying for hedge accounting and hedge ineffectiveness.

I. Tax adjusting items and the tax effect of above items.

Notes: explanation of adjusting items for the year ended 30 June 2012

F. Credit of £31 million relating to the News Corporation (subsequently renamed Twenty-First Century Fox, Inc.) proposal in 2011 consisting of costs

incurred offset by the receipt of the break fee and restructuring costs of £11 million, which comprise severance payments relating to approximately

35 senior roles as part of a restructuring initiative to improve operational efficiency.

G. Profit on disposal of the Group’s interest in Chelsea Digital Media Limited.

H. A write-off of £5 million relating to the facility fee on the £750 million RCF which has now been replaced with the £743 million RCF and the

remeasurement of all derivative financial instruments not qualifying for hedge accounting and hedge ineffectiveness (credit of £19 million).

I. Tax effect of adjusting items.

2013 2012

Reported

Adjusting

Items Adjusted Reported

Adjusting

Items Adjusted

Notes £m £m £m £m £m £m

Revenue

Retail subscription 5,951 - 5,951 5,593 - 5,593

Wholesale subscription 396 - 396 351 - 351

Advertising 440 - 440 440 - 440

Installation, hardware and

service 87 - 87 98 - 98

Other 361 - 361 309 - 309

7,235 - 7,235 6,791 - 6,791

Operating expense

Programming A (2,487) 1 (2,486) (2,298) - (2,298)

Direct networks B (686) (29) (715) (676) - (676)

Marketing C (1,117) 1 (1,116) (1,064) - (1,064)

Subscriber management and

supply chain

D (673) 26 (647) (621) - (621)

Transmission, technology and

fixed networks E (405) 4 (401) (395) - (395)

Administration

F (576) 36 (540) (494) (20) (514)

(5,944) 39 (5,905) (5,548) (20) (5,568)

EBITDA 1,669 23 1,692 1,587 (20) 1,567

Operating profit 1,291 39 1,330 1,243 (20) 1,223

Share of results of joint ventures

and associates G 46 (9) 37 39 (7) 32

Investment income 28 - 28 18 - 18

Finance costs H (108) (23) (131) (111) (14) (125)

Profit before tax 1,257 7 1,264 1,189 (41) 1,148

Taxation I (278) (17) (295) (283) 10 (273)

Profit for the year 979 (10) 969 906 (31) 875

Earnings per share (basic) 60.7p (0.7)p 60.0p 52.6p (1.8)p 50.8p