british sky broadcasting group plc -...

TRANSCRIPT

1

BRITISH SKY BROADCASTING GROUP PLC

Unaudited results for the nine months ended 31 March 2014

Adjusted results1

Nine months to 31 March 2014 2013 Variance

Revenue1 £5,666m £5,313m +6.6%

EBITDA £1,223m £1,253m (2.4%)

Operating profit £910m £994m (8.5%)

Earnings per share (basic) 42.2p 43.7p (3.4%)

Strong quarter of growth

764,000 new paid-for subscription products in Q3: 2.4 million in year to date

74,000 net new TV customers, more than double growth in Q3 last year

Connected TV services ahead of plan and delivering clear benefits

Almost 50% of TV customers now connected

On Demand usage tripled year on year

3.7 million Sky Go unique users, up 13% year on year

Financial performance on track

Adjusted revenue1 of £5,666 million, up 7%

Adjusted EBITDA of £1,223 million, down 2%

Jeremy Darroch, Chief Executive, commented:

“We have had a strong third quarter and continued to grow at an accelerated rate as customers

respond to the quality and breadth of our offering. Nine months into our plans for the year, we

have added almost a third more new paid-for subscription products than in the same period

last year.

“Our investment in connected TV services is delivering results. Almost 50% of Sky homes are

now connected and this is transforming their viewing experience: connected customers are

watching more TV, they’re more loyal and they’re more likely to recommend Sky. Our expanded

Box Sets service has been particularly popular with a fourfold increase in viewing of top titles

like 24 and Game of Thrones.

“We are making good progress in developing new revenue streams. Our targeted advertising

service, AdSmart, is attracting many new advertisers to Sky while our new Buy & Keep service in

Sky Store opens up the DVD purchase marketplace for the first time.

“We’ve also made further strides to increase the range and quality of content across our

platforms. Our new original dramas are working well; we’ve agreed 17 new sports rights deals

since January; struck major new partnerships with HBO and ITV; and we’ve announced today the

renewal of our movie output deal with Paramount giving us exclusive UK pay TV rights to hit

titles like Noah and Anchorman 2. These continue to make Sky the number one destination for

customers who want the best choice of TV.

1 Adjusted revenue as presented here is from recurring activities. It excludes revenues earned from the discontinued retailing of the ESPN channel in

the current and prior periods. The current period includes the consolidation of revenues from the acquired O2 broadband and fixed line telephony

business (the “Acquired O2 Business”)

2

“All this has enabled us to continue to deliver strong rates of top-line growth. Revenues

increased by 7% in the first nine months compared with the same period last year. And, in a year

of investment, adjusted EBITDA of £1.2 billion is a good result. We’re now more than three

quarters of the way through our plan for the year and are on track to deliver returns in line with

our expectations.”

Results Highlights

Customer Metrics (unaudited)

As at

31-Mar-14

As at

31-Mar-13

Annual

Growth

Quarterly

Growth to

31-Mar-14

Total paid-for products (‘000s) 34,071 30,228 +3,843 +764

TV 10,610 10,388 +222 +74

HD 5,113 4,669 +444 +108

Multiscreen 2,540 2,476 +64 +12

Sky Go Extra 927 44 +883 +284

Broadband 5,197 4,387 +810 +70

Telephony 4,895 4,208 +687 +103

Line rental 4,789 4,056 +733 +113

Paid-for products per retail customer 3.0 2.8 +0.2 +0.1

New connected TV services (‘000s)

Internet-connected Sky+HD boxes 4,952 2,284 +2,668 +600

Sky Go unique users 3,678 3,262 +416 +364

Total Customers (‘000s) 15,022 14,613 +409 +68

Retail Customers 11,420 10,812 +608 +90

Wholesale Customers (1)

3,602 3,801 -199 -22

ARPU (2)

£571 £567 +£4 +£1

Triple-play 37% 34% +3% +1%

Churn (3)

10.9% 10.8% +0.1% +0.1%

An additional KPI summary table containing further detailed disclosure can be found in Schedule 1.

_________ 1 Wholesale customers taking at least one paid for Sky channel. The customer numbers are as reported to us at February 2014.

2

Quarterly annualised. Excluding revenues earned from retailing the ESPN channel.

3 Quarterly annualised.

A reconciliation of adjusted EBITDA and adjusted operating profit to statutory measures is set out in Appendix 2. Adjusted basic

earnings per share are calculated from adjusted profit for the period. A reconciliation of statutory profit to adjusted profit is set

out in note 3 to the consolidated financial information.

3

Operational Performance

The business performed strongly in the nine months to the end of March, demonstrating once

again the benefits of our broad-based approach to growth. Despite continuing pressures on

household budgets, we grew our revenues by 7% over the period with good levels of demand

across the board. In all, we added 2.4 million new paid-for subscription products in the nine

months since 30 June 2013, 31% more than the same period last year, taking our total product

base past 34 million.

Our main focus in Q3 was a continued push on our connected homes strategy, responding to

strong demand and enabling more customers to enjoy the full benefits of the Sky service. This

helped deliver a particularly strong performance in TV, with growth across all TV subscription

products in the quarter more than double that of the prior year. In Q3, we added 74,000 net

new TV customers and 108,000 net new HD customers. We also added 284,000 new Sky Go

Extra customers, an area where we continue to see excellent growth potential with around 5

million households now registered to use Sky Go. The success of our expanded TV Box Sets

offering drove a significant proportion of the upgrades to HD, as well as delivering even more

value for existing customers.

In home communications, we added 70,000 net new broadband products in the three months

to 31 March. This reflects the focus of our marketing in the quarter on growing TV products and

driving take up of connected TV services among our existing customer base, as well as slightly

higher levels of churn from the acquired O2 broadband base as we complete the migration of

the remaining customers. This had an estimated impact of between 20,000 and 30,000. At the

end of the third quarter, 37% of our customers took all three of TV, broadband and telephony

from Sky, up 3 percentage points on the prior year, extending our lead as the UK’s favourite

triple-play provider.

ARPU increased by a further £4 to £571 on the prior year while churn remained stable at 10.9%.

We closed the quarter with 11.4 million retail customers, an increase of 90,000 in the quarter.

Content

We had a big quarter for UK produced content with double the number of hours of first-run

commissioned drama and comedy compared to the same period last year. New dramas like the

The Smoke and Fleming worked well as did returning commissions like Stella and Moone Boy.

In Sport, we built on the strong first half as Sky Sports achieved its highest share of viewing for

seven years. Average audiences for the Premier League are up 7% year on year and 49 of the top

50 most watched matches in the season so far have been on Sky Sports. At the same time, we

recorded our three biggest Sky Go audiences ever in the quarter, led by a peak of 379,000 Sky

Go viewers for February’s fixture between Manchester City and Chelsea.

We have also continued to strengthen the breadth and quality of our sports offering. Away from

football, audiences to the start of the Super League season were up almost 30%. We have

agreed 17 sports rights deals so far this year including the US Masters, IPL cricket and European

rugby.

4

In addition, we have announced today the renewal of our movie output deal with Paramount

giving us exclusive rights across all platforms to blockbusters like Noah and Anchorman 2. This

means we've secured new deals with five of the six major studios in the last two years. We have

also signed a new deal with Fox to ensure that Sky1 remains the exclusive home for first-run

Simpsons through to 2016.

Connected TV Services

We’ve made further strong progress with our investment to drive take up of connected TV

services. We connected a further 600,000 Sky+HD boxes in the quarter to take the connected

base to 5 million, nearly half of all Sky TV homes. We also added more On Demand content, with

a particular focus on building our Box Sets offering where we’ve more than doubled the hours of

quality titles available in the past nine months, including hit series such as Sopranos and 24.

As a result, consumption of On Demand content continued to grow rapidly: weekly downloads in

the third quarter were three times higher than a year ago, equating to each connected

household downloading on average three pieces of content a week. On Demand viewing now

accounts for more than 5% of viewing in connected Sky homes. To put this in context, this

means that On Demand is equivalent to the third most popular linear channel in those homes. A

surge in demand for our expanded Box Sets offering accounted for much of this increase – in

March, Game of Thrones Series 1-3 became our most downloaded box set ever.

We took another big step forward in our connected TV offering in March with the launch of a

new home page for our electronic programming guide. This showcases the full range of

programming available to customers up front for the first time, including On Demand content

such as Sky Store, Box Sets and Catch Up.

The growth in reach and usage of our connected box platform is enabling us to open up

additional sources of revenue growth with the roll out of new services. Customer rentals via Sky

Store in the third quarter were up over 100% versus the prior year benefitting from greater

awareness of the service, repeat usage from existing customers and availability of strong titles

such as Captain Phillips and Gravity. We have built on the early success of Sky Store rentals with

the launch in April of our new 'Buy & Keep' service which targets the much larger DVD purchase

marketplace.

A second new service, Sky AdSmart, launched in January. This is improving effectiveness for our

existing advertiser clients and attracting new advertisers to TV by giving them the ability, for

the first time, to run targeted campaigns across Sky and third party channels. To date, of the

100 advertisers that have run AdSmart campaigns, half are new to Sky and around 20% had

never previously advertised on TV.

We have also struck a new deal with Sony to make Sky Go and NOW TV available on

Playstation®4 (PS4) from this summer.

5

Financial performance

We delivered a good financial performance for the nine months to 31 March 2014. Adjusted

revenue growth was 7% and this, together with continued discipline on costs, allowed us to

deliver adjusted EBITDA of £1,223 million, down only 2.4%, despite our connected services

investment and the uplift in Premier League amortisation. Adjusted basic earnings per share

were 42.2 pence, in line with our expectations. Unless otherwise stated, all figures and growth

rates below exclude adjusting items.

Revenue increased by 7% to £5,666 million (2013: £5,313 million) with continued strong growth in

both our retail and commercial businesses.

Retail subscription revenue grew by 7% to £4,655 million (2013: £4,354 million) after adjusting

for £6 million of ESPN revenue (2013: £68 million), reflecting the continued product and

customer growth, price rises and strong growth in transactional revenues.

Our commercial businesses performed well. Advertising revenue was up 8% to £354 million

(2013: £327 million) through a combination of market growth, share gains through our

consolidation of two small houses in this financial year and a contribution for the first time of

AdSmart. The one area of slower growth was wholesale subscription revenue which increased by

2% to £301 million (2013: £295 million) as renewed carriage agreements and price increases were

partially offset by lower customer volumes on third party platforms.

Other revenue increased by 10% to £295 million (2013: £269 million). A continued strong

performance from Sky Bet was partially offset by the absence of one time sublicence revenue of

£8 million from England away qualifiers included in the prior period.

Growth in the cost base - held in aggregate to just 5% excluding the £173 million one-time step

up in Premier League amortisation - was driven by the enhanced rate of growth in product and

customer volumes, the first time consolidation of the acquired O2 business and the investment

in our connected home strategy.

We were pleased with the progress we continue to make on operating efficiency; both in our

volume facing activities, typically reported within subscriber management and supply chain

costs; and in our overhead and administration costs with each of these cost categories for the

period growing at below the rate of revenue.

Depreciation and amortisation was up 21% to £313 million (2013: £259 million) due to the

integration of the Acquired O2 Business, depreciable kit installed in more exchanges, network

upgrades carried out across the year and a higher fixed asset base as we begin to depreciate

the development costs of recently launched products such as NOW TV and AdSmart.

Adjusted EBITDA of £1,223 million and operating profit for the period of £910 million were both in

line with our expectations. After tax of £183 million and interest of £94 million – reflecting a full

nine months of interest for the first time on the November 2022 bond – earnings per share were

42.2 pence.

Net debt at 31 March 2014 was £1,543 million. The number of votable shares in issue at 31 March

2014 was 1,574 million.

6

CORPORATE

Pay TV Case

In February, the Court of Appeal (CoA) upheld BT's appeal against the Competition Appeal

Tribunal’s (CAT) August 2012 judgment in relation to the imposition by Ofcom of Wholesale

Must Offer (WMO) obligations on Sky in respect of Sky Sports 1 and 2.

The CoA remitted the case back to the CAT for further consideration.

Ofcom review of WMO obligations

On 16 April, Ofcom announced a review of the WMO obligations imposed on Sky in relation to Sky

Sports 1 and 2. Ofcom has noted that there have been a number of sector developments since

2010, which will need to be considered as part of its review. As yet Ofcom has not published any

further details of its review.

7

Enquiries:

Analysts/Investors:

Edward Steel Tel: 020 7032 2093

Lang Messer Tel: 020 7032 2657

E-mail: [email protected]

Press:

Alice Macandrew Tel: 020 7032 4256

Robin Tozer Tel: 020 7032 0620

E-mail: [email protected]

A conference call for UK and European analysts and investors will be held at 8.30 a.m. (BST)

today. Participants must register by contacting Felicity Marshall on +44 20 7251 3801 or at

There will be a separate conference call for US analysts and investors at 10.00 a.m. (EDT) today.

Details of this call have been sent to US institutions and can be obtained from Dana Diver at

Taylor Rafferty on +1 212 889 4350. Alternatively you may register online at: http://invite.taylor-

rafferty.com/_bskyb/2013Q2CC/Default.htm.

The live conference calls of the UK and US calls will be available to analysts and investors via the

BSkyB website at http://www.sky.com/corporate. Replays will be subsequently available.

8

Schedule 1 – KPI Summary

All figures (000) FY11/12 FY12/13 FY13/14

unless stated Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Total paid-for subscription

products 27,734 28,365 28,898 29,513 30,228 31,634 32,434 33,307 34,071

TV 10,268 10,288 10,308 10,358 10,388 10,422 10,459 10,536 10,610

Sky+ HD 4,222 4,343 4,468 4,561 4,669 4,786 4,893 5,005 5,113

Multiscreen 2,378 2,402 2,423 2,467 2,476 2,489 2,503 2,528 2,540

Sky Go Extra - - - - 44 166 385 643 927

Broadband 3,863 4,001 4,103 4,235 4,387 4,906 5,017 5,127 5,197

Telephony 3,627 3,768 3,888 4,022 4,208 4,501 4,652 4,792 4,895

Line Rental 3,376 3,563 3,708 3,870 4,056 4,364 4,525 4,676 4,789

New connected TV services 3,211 3,735 4,023 4,781 5,546 5,966 6,642 7,666 8,630

Connected HD boxes 604 995 1,255 1,715 2,284 2,709 3,351 4,352 4,952

Sky Go unique users 2,607 2,740 2,768 3,066 3,262 3,257 3,291 3,314 3,678

Total products and services 30,945 32,100 32,921 34,294 35,774 37,600 39,076 40,973 42,701

Other metrics:

Retail customers 10,549 10,606 10,654 10,742 10,812 11,153 11,224 11,330 11,420

Wholesale customers 3,657 3,672 3,714 3,751 3,801 3,677 3,617 3,624 3,602

Total customers 14,206 14,278 14,368 14,493 14,613 14,830 14,841 14,954 15,022

ARPU (£)1 £538 £541 £542 £558 £567 £569 £559 £570 £571

Triple-play % 31% 32% 33% 33% 34% 35% 36% 36% 37%

Churn 10.1% 9.9% 10.9% 10.3% 10.8% 10.9% 11.0% 10.8% 10.9%

Fixed Network Metrics

On-net base 3,636 3,778 3,882 4,031 4,190 4,696

4,826 4,921 4,992

MPF base 2,423 2,588 2,762 2,926 3,159 3,359 3,504 3,659 3,831

SMPF base 1,213 1,190 1,120 1,105 1,031 1,337 1,322 1,262 1,161

MPF % 67% 69% 71% 73% 75% 72% 73% 74% 77%

SMPF % 33% 31% 29% 27% 25% 28% 27% 26% 23%

Off-net base 227 223 221 204 197 210 191 206 205

Total Broadband 3,863 4,001 4,103 4,235 4,387 4,906 5,017 5,127 5,197

On-net % 94% 94% 95% 95% 96% 96% 96% 96% 96%

Total no. of LLU exchanges 1,964 1,965 2,036 2,108 2,202 2,323 2,354 2,355 2,355

1 Calculations have been restated to exclude revenue earned from retailing the ESPN channel.

9

Use of measures not defined under IFRS

This press release contains certain information on the Group’s financial position, results and cash flows that have been derived from

measures calculated in accordance with IFRS. This information should not be read in isolation from the related IFRS measures.

Forward looking statements

This document contains certain forward looking statements with respect to the Group’s financial condition, results of operations

and business, and our strategy, plans and objectives for the Group. These statements include, without limitation, those that express

forecasts, expectations and projections, such as forecasts, expectations and projections in relation to new products and services,

the potential for growth of free-to-air and pay television, fixed line telephony, broadband and bandwidth requirements, advertising

growth, DTH and OTT customer growth, Multiscreen, On Demand, NOW TV, Sky Go, Sky Go Extra, Sky+, Sky+HD and other services

penetration, revenue, administration costs and other costs, advertising growth, churn, profit, cash flow, products and our

broadband network footprint, content, wholesale, marketing and capital expenditure and proposals for returning capital to

shareholders.

Although the Company believes that the expectations reflected in such forward looking statements are reasonable, these

statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are

beyond our control, are difficult to predict and could cause actual results to differ materially from those expressed or implied or

forecast in the forward looking statements. Information on the significant risks and uncertainties are described in the “Principal

risks and uncertainties” section of Sky’s Annual Report for the full year ended 30 June 2013 (as updated in Sky’s results for the six

months ended 31 December 2013). Copies of the Annual Report and 31 December 2013 results are available from the British Sky

Broadcasting Group plc web page at www.sky.com/corporate.

All forward looking statements in this document are based on information known to the Group on the date hereof. The Group

undertakes no obligation publicly to update or revise any forward looking statements, whether as a result of new information,

future events or otherwise.

Glossary of Terms

A glossary of terms is included within the Annual Report and on our corporate investor relations web page at

http://corporate.sky.com/investors/glossary. Copies of the Annual Report are available from the British Sky Broadcasting Group plc

web page at www.sky.com/corporate and in hard copy from the Company Secretary, British Sky Broadcasting Group plc, Grant Way,

Isleworth, Middlesex TW7 5QD.

10

Appendix 1 - Consolidated Financial Information

Consolidated Income Statement for the nine months ended 31 March 2014

2013/14 2012/13

Nine months Nine months

ended ended

31 March 31 March

£m £m

Notes (unaudited) (unaudited)

Revenue 1 5,672 5,381

Operating expense 2 (4,809) (4,374)

EBITDA 1,193 1,272

Depreciation and amortisation (330) (265)

Operating profit 863 1,007

Share of results of joint ventures and associates 28 37

Investment income 6 9

Finance costs (104) (87)

Profit before tax 793 966

Taxation (170) (230)

Profit for the period 623 736

Earnings per share from profit for the period (in pence)

Basic 39.8p 45.3p

Diluted 39.5p 44.9p

Adjusted earnings per share from adjusted profit for the period (in pence)

Basic 3 42.2p 43.7p

Diluted 3 41.9p 43.3p

11

Notes:

1 Revenue

2013/14 2012/13

Nine months Nine months

ended ended

31 March 31 March

£m £m

(unaudited) (unaudited)

Retail subscription 4,661 4,422

Wholesale subscription 301 295

Advertising 354 327

Installation, hardware and service 61 68

Other 295 269

5,672 5,381

2 Operating expense

2013/14 2012/13

Nine months Nine months

ended ended

31 March 31 March

£m £m

(unaudited) (unaudited)

Programming 2,000 1,860

Direct networks 630 497

Marketing 901 818

Subscriber management and supply chain 522 512

Transmission, technology and fixed networks 341 295

Administration 415 392

4,809 4,374

3 Earnings per share

The weighted average number of shares for the period was:

2013/14

Nine months

ended

31 March

Millions of shares

2012/13

Nine months

ended

31 March

Millions of shares

Ordinary shares 1,586 1,642

ESOP trust ordinary shares (19) (18)

Basic shares 1,567 1,624

Dilutive ordinary shares from share options 9 14

Diluted shares 1,576 1,638

Basic and diluted earnings per share are calculated by dividing profit for the period into the weighted average number of shares

for the period. In order to provide a measure of underlying performance, management have chosen to present an adjusted

profit for the period which excludes items that may distort comparability. Such items arise from events or transactions that fall

within the ordinary activities of the Group but which management believes should be separately identified to help explain

underlying performance.

12

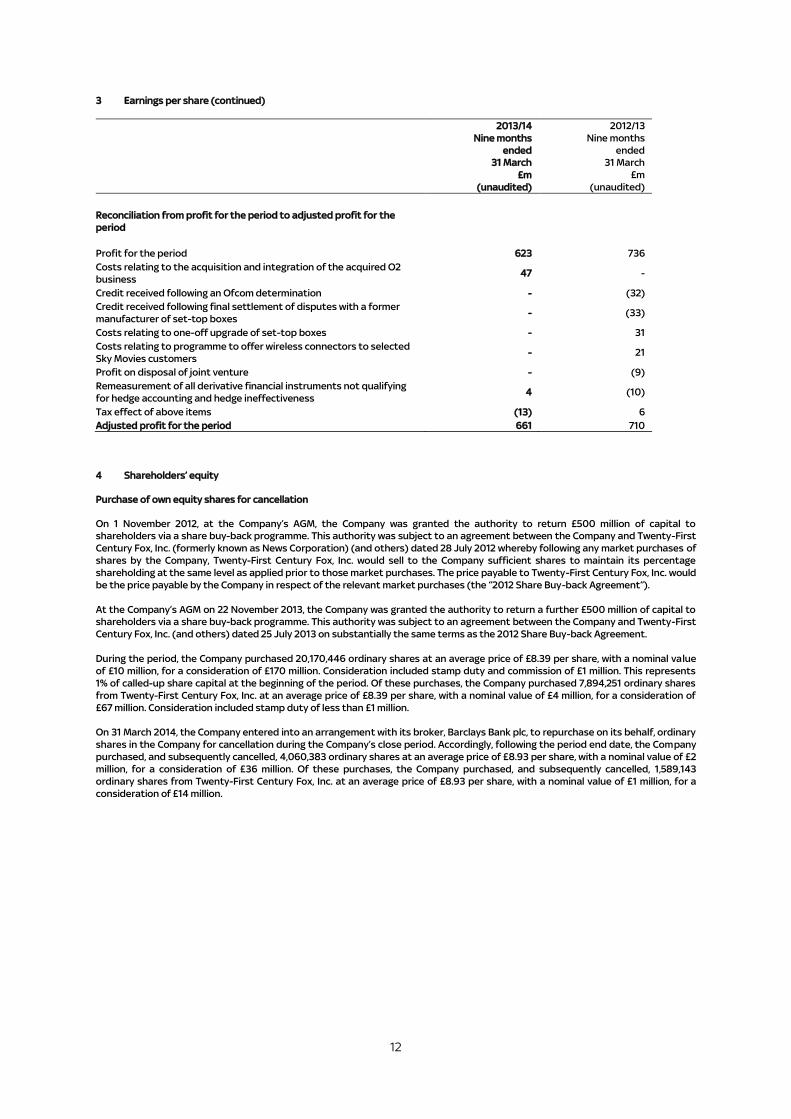

3 Earnings per share (continued)

2013/14

Nine months

ended

31 March

£m

(unaudited)

2012/13

Nine months

ended

31 March

£m

(unaudited)

Reconciliation from profit for the period to adjusted profit for the

period

Profit for the period 623 736

Costs relating to the acquisition and integration of the acquired O2

business 47 -

Credit received following an Ofcom determination - (32)

Credit received following final settlement of disputes with a former

manufacturer of set-top boxes - (33)

Costs relating to one-off upgrade of set-top boxes - 31

Costs relating to programme to offer wireless connectors to selected

Sky Movies customers - 21

Profit on disposal of joint venture - (9)

Remeasurement of all derivative financial instruments not qualifying

for hedge accounting and hedge ineffectiveness 4 (10)

Tax effect of above items (13) 6

Adjusted profit for the period 661 710

4 Shareholders’ equity

Purchase of own equity shares for cancellation

On 1 November 2012, at the Company’s AGM, the Company was granted the authority to return £500 million of capital to

shareholders via a share buy-back programme. This authority was subject to an agreement between the Company and Twenty-First

Century Fox, Inc. (formerly known as News Corporation) (and others) dated 28 July 2012 whereby following any market purchases of

shares by the Company, Twenty-First Century Fox, Inc. would sell to the Company sufficient shares to maintain its percentage

shareholding at the same level as applied prior to those market purchases. The price payable to Twenty-First Century Fox, Inc. would

be the price payable by the Company in respect of the relevant market purchases (the “2012 Share Buy-back Agreement”).

At the Company’s AGM on 22 November 2013, the Company was granted the authority to return a further £500 million of capital to

shareholders via a share buy-back programme. This authority was subject to an agreement between the Company and Twenty-First

Century Fox, Inc. (and others) dated 25 July 2013 on substantially the same terms as the 2012 Share Buy-back Agreement.

During the period, the Company purchased 20,170,446 ordinary shares at an average price of £8.39 per share, with a nominal value

of £10 million, for a consideration of £170 million. Consideration included stamp duty and commission of £1 million. This represents

1% of called-up share capital at the beginning of the period. Of these purchases, the Company purchased 7,894,251 ordinary shares

from Twenty-First Century Fox, Inc. at an average price of £8.39 per share, with a nominal value of £4 million, for a consideration of

£67 million. Consideration included stamp duty of less than £1 million.

On 31 March 2014, the Company entered into an arrangement with its broker, Barclays Bank plc, to repurchase on its behalf, ordinary

shares in the Company for cancellation during the Company’s close period. Accordingly, following the period end date, the Company

purchased, and subsequently cancelled, 4,060,383 ordinary shares at an average price of £8.93 per share, with a nominal value of £2

million, for a consideration of £36 million. Of these purchases, the Company purchased, and subsequently cancelled, 1,589,143

ordinary shares from Twenty-First Century Fox, Inc. at an average price of £8.93 per share, with a nominal value of £1 million, for a

consideration of £14 million.

13

Appendix 2 – Non-GAAP measures

Consolidated Income Statement - reconciliation of statutory and adjusted numbers

Notes: explanation of adjusting items for the period ended 31 March 2014

A. Costs of £47 million relating to the acquisition and integration of the Acquired O2 Business, including amortisation of £17

million in relation to acquired intangible assets.

D. Remeasurement of all derivative financial instruments not qualifying for hedge accounting and hedge ineffectiveness.

E. Tax effect of adjusting items.

Notes: explanation of adjusting items for the period ended 31 March 2013

A. A credit of £32 million in relation to a credit note received following an Ofcom determination.

B. A credit of £33 million relating to the final settlement of disputes with a former manufacturer of set-top boxes (net of

associated costs), costs of £31 million relating to one-off upgrade of set-top boxes, and costs of £21 million relating to

programme to offer wireless connectors to selected Sky Movies customers. Included within this adjusting item is an

impairment of £6 million in relation to associated intangible assets.

C. Profit on disposal of the Group’s interest in MUTV Limited.

D. Remeasurement of all derivative financial instruments not qualifying for hedge accounting and hedge ineffectiveness.

E. Tax effect of adjusting items.

2013/14 2012/13

Statutory

Adjusting

Items Adjusted Statutory

Adjusting

Items Adjusted

Notes £m £m £m £m £m £m

Revenue

Retail subscription 4,661 - 4,661 4,422 - 4,422

Wholesale subscription 301 - 301 295 - 295

Advertising 354 - 354 327 - 327

Installation, hardware and

service 61 - 61 68 - 68

Other 295 - 295 269 - 269

5,672 - 5,672 5,381 - 5,381

Operating expense

Programming (2,000) - (2,000) (1,860) - (1,860)

Direct networks A (630) 19 (611) (497) (32) (529)

Marketing A (901) 1 (900) (818) - (818)

Subscriber management and

supply chain

A,B (522) 2 (520) (512) 19 (493)

Transmission, technology and

fixed networks A (341) 7 (334) (295) - (295)

Administration

A (415) 18 (397) (392) - (392)

(4,809) 47 (4,762) (4,374) (13) (4,387)

EBITDA 1,193 30 1,223 1,272 (19) 1,253

Operating profit 863 47 910 1,007 (13) 994

Share of results of joint

ventures and associates C 28 - 28 37 (9) 28

Investment income 6 - 6 9 - 9

Finance costs D (104) 4 (100) (87) (10) (97)

Profit before tax 793 51 844 966 (32) 934

Taxation E (170) (13) (183) (230) 6 (224)

Profit for the period 623 38 661 736 (26) 710

Earnings per share (basic) 39.8p 2.4p 42.2p 45.3p (1.6)p 43.7p