dodd-frank chapter x: the consumer financial protection...

TRANSCRIPT

Dodd-Frank Chapter X: The Consumer Financial Protection Bureau

Lewis S. Wiener March 23, 2011

Association of Corporate Counsel (ACC) Financial Services Committee Legal Quick Hit

©2011 Sutherland Asbill & Brennan LLP 2

The Consumer Financial Protection Bureau (CFPB)

• Created by Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act, Pub. L. No. 111-203, 124 Stat. 1376 (2010).

• The CFPB is scheduled to assume its powers as an independent bureau within the Federal Reserve System on July 21, 2011 (the “Transfer Date”).

• Prior to confirmation of a Director, the CFPB’s authority is limited.

• Initial budget equal to 10% of the Federal Reserve System’s 2009 operating expenses (increasing to 12% in 2013) - $370 - $540 million outside of the appropriations process.

• Additional appropriation of up to $200 million authorized (Dodd-Frank Act §1017).

©2011 Sutherland Asbill & Brennan LLP 3

Mission and Scope

• OBJECTIVES – The Bureau is authorized to exercise its authorities under federal consumer financial law for the purposes of ensuring that, with respect to consumer financial products and services:

1. Consumers are provided with timely and understandable information to make responsible decisions about financial transactions;

2. Consumers are protected from unfair, deceptive, or abusive acts and practices and from discrimination;

3. Outdated, unnecessary, or unduly burdensome regulations are regularly identified and addressed in order to reduce unwarranted regulatory burdens;

4. Federal consumer financial law is enforced consistently, without regard to the status of a person as a depository institution, in order to promote fair competition; and

5. Markets for consumer financial products and services operate transparently and efficiently to facilitate access and innovation.

(Dodd-Frank Act §1021(b))

©2011 Sutherland Asbill & Brennan LLP 4

Mission and Scope

• Regulated entities: § Large depositories (more than $10 billion in assets); § Lenders and loan servicers, including payday lenders, mortgage-

related businesses, and private student loan providers; § Loan acquirers, purchasers, sellers, and brokers; § Sellers, providers, and issuers of stored value instruments; § Those engaged in check cashing, collecting, and guaranty

services; § Payment processors; § Providers of credit counseling, debt management, and debt

settlement services; § Consumer reporting services; and § Debt collectors. (Dodd-Frank Act §1024)

©2011 Sutherland Asbill & Brennan LLP 5

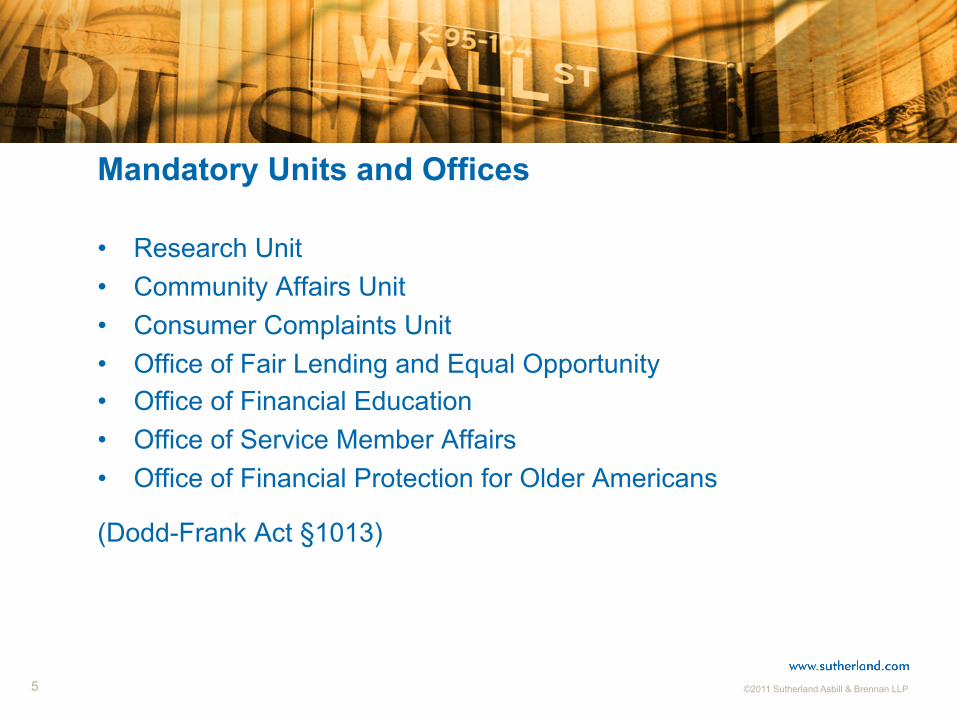

Mandatory Units and Offices

• Research Unit • Community Affairs Unit • Consumer Complaints Unit • Office of Fair Lending and Equal Opportunity • Office of Financial Education • Office of Service Member Affairs • Office of Financial Protection for Older Americans

(Dodd-Frank Act §1013)

©2011 Sutherland Asbill & Brennan LLP 6

Limitations on Authority

• Prior to the confirmation of a Director, the CFPB may not exercise its organic authority to:

§ Prohibit unfair, deceptive or abusive acts or practices; § Prescribe disclosure rules or require model disclosure forms; § Prescribe rules relating to the filing of reports for the purpose of

determining whether a nondepository institution should be supervised by the CFPB;

§ Supervise nondepository institutions. • After the Transfer Date, but before the confirmation of a Director,

the CFPB may exercise only those authorities transferred to it from other agencies, including the authority to prescribe all rules under the enumerated federal consumer laws.

(Dodd-Frank Act §1066)

©2011 Sutherland Asbill & Brennan LLP 7

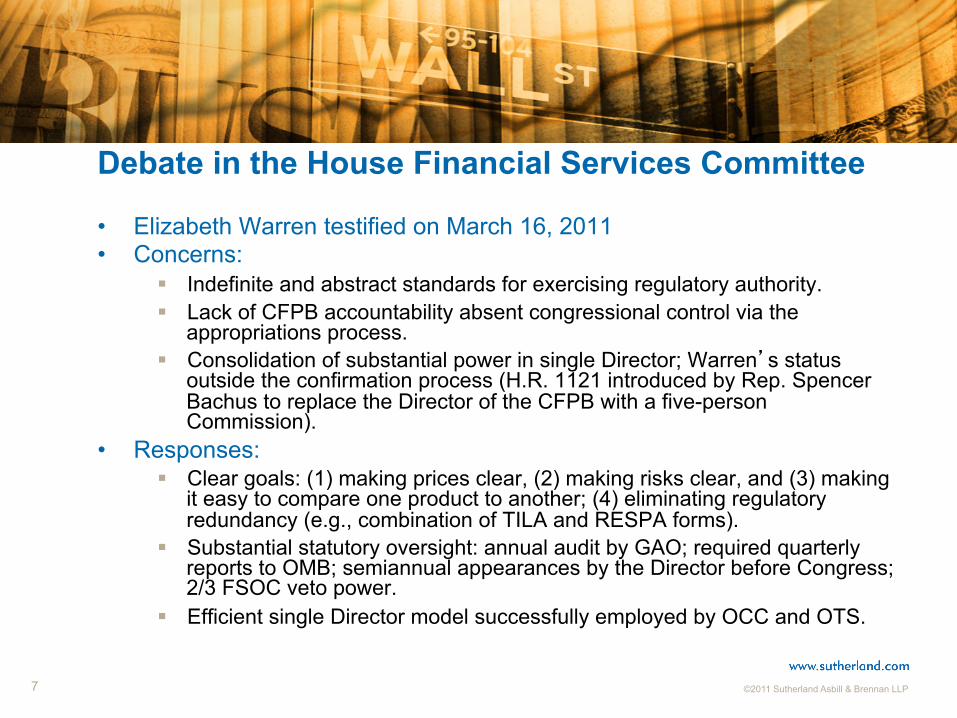

Debate in the House Financial Services Committee

• Elizabeth Warren testified on March 16, 2011 • Concerns:

§ Indefinite and abstract standards for exercising regulatory authority. § Lack of CFPB accountability absent congressional control via the

appropriations process. § Consolidation of substantial power in single Director; Warren’s status

outside the confirmation process (H.R. 1121 introduced by Rep. Spencer Bachus to replace the Director of the CFPB with a five-person Commission).

• Responses: § Clear goals: (1) making prices clear, (2) making risks clear, and (3) making

it easy to compare one product to another; (4) eliminating regulatory redundancy (e.g., combination of TILA and RESPA forms).

§ Substantial statutory oversight: annual audit by GAO; required quarterly reports to OMB; semiannual appearances by the Director before Congress; 2/3 FSOC veto power.

§ Efficient single Director model successfully employed by OCC and OTS.

©2011 Sutherland Asbill & Brennan LLP 8

Lewis S. Wiener Partner 202.383.0140 [email protected]

Lew Wiener, a member of Sutherland’s Litigation Practice Group and chair of the firm’s Financial Services Litigation Team, focuses his practice on all aspects of commercial litigation including financial service, consumer finance, tax litigation, and class action defense. He also represents clients in eminent domain/inverse condemnation and land-use litigation before state and federal trial and appellate courts. Prior to joining Sutherland, Lew served as a trial lawyer with the U.S. Department of Justice where he was twice recognized by the Attorney General for special achievement in the handling of significant litigation matters on behalf of the United States. While at the Department of Justice, Lew was lead government counsel in one of the largest class actions ever filed against the United States.

©2011 Sutherland Asbill & Brennan LLP 9

SUTHERLAND’S FINANCIAL SERVICES PRACTICE More than 150 Sutherland attorneys devote their practice to achieving business objectives and solving complex problems for clients in the financial services industry. Our team has deep industry knowledge and regulatory experience and includes former senior attorneys

of the U.S. Securities and Exchange Commission (SEC), Financial Industry Regulatory Authority (FINRA) and Department of Justice (DOJ). This experience, coupled with the

firm’s philosophy of handling cases with the right number of lawyers and emphasizing responsiveness and accessibility, enables the firm to provide creative and effective legal solutions to its financial services clients.