wrio june 2014

TRANSCRIPT

The World Rubber Industry Outlook

Review and Prospects to 2023

June 2014

International Rubber Study Group

Table of Contents

Foreword i

Assumptions and Scenarios ii

Executive Summary 1

1 The Economy 5

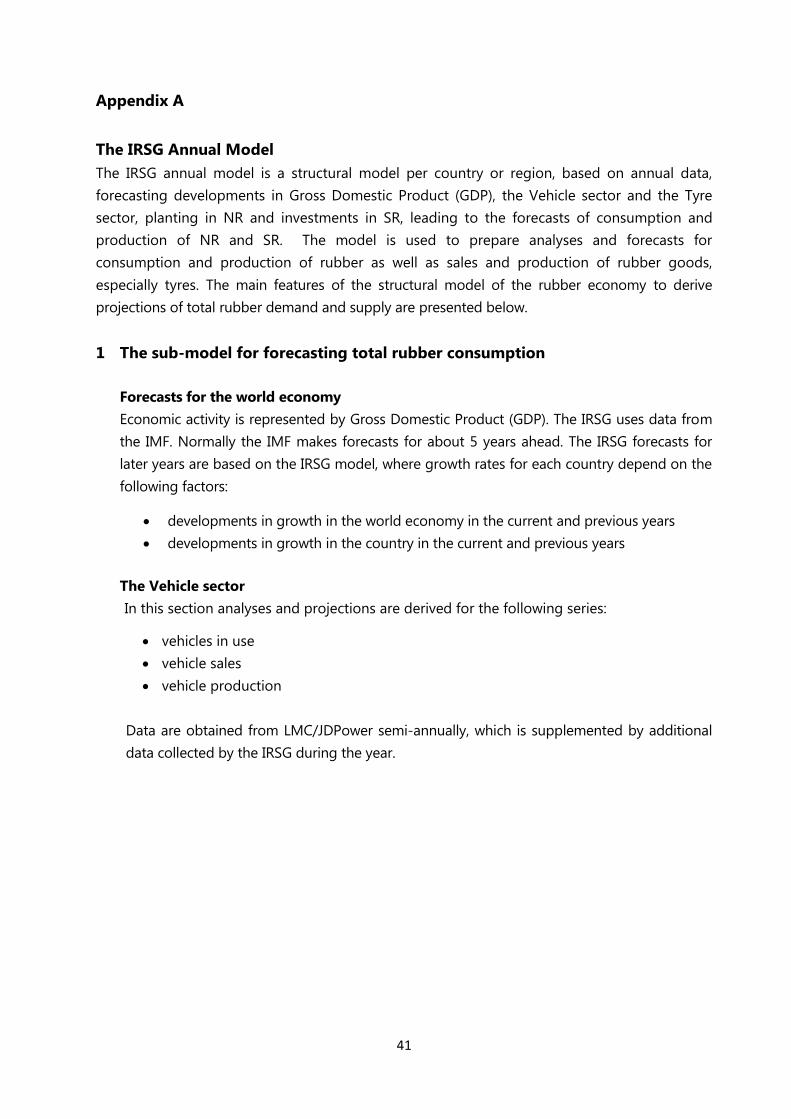

2 The Vehicle Sector 6

3 The Tyre Sector 8

4 Rubber Consumption 9

5 Normal Production of Natural Rubber 16

6 Supply-Demand Interaction and Price Formation 22

7 Production of Natural Rubber 25

8 Consumption of Natural Rubber and Synthetic Rubber 27

Appendix A Summary Description of the IRSG Modelling System 40

© Copyright : The International Rubber Study Group. All rights reserved. No part of this

publication may be reprinted or reproduced, stored in a retrieval system or transmitted in any

form or by any means, electronic, photocopy, recording or otherwise without the prior written

permission of the publisher.

i

Foreword

The International Rubber Study Group (IRSG) was established in 1944 as the only

intergovernmental organization that brought the world‟s rubber producing and consuming

stakeholders together. The IRSG is the forum for the discussion of matters affecting the

supply and demand for natural as well as synthetic rubber.

The IRSG is the authoritative source of statistical data and analysis for all aspects of the

rubber industry, including production, consumption and trade in rubber as well as rubber

products. The seminal purpose of the IRSG Secretariat is to prepare current estimates and

analyse future supply and demand trends, while undertaking statistical and economic studies

on specific aspects of the industry so as to continually improve its value-added service to

stakeholders.

As part of its work program, the Secretariat prepares long-term forecasts for the world

rubber industry using its Modelling System. It is an integrated, layered model that starts

with the economy, working its way up through the vehicle and tyre sectors before finally

arriving at the rubber demand and production.

The operation of the Modelling System is guided by two principles: keep it simple and

delegate to experts where possible. In regards to the second principle, the Modelling

System sources and uses the following data from third party:

Economic outlook

Vehicle data

Tyre data

Oil price outlook

The use of the third-party sourced data is not entirely wholesale. It is in some cases used

only as a guide. This is to ensure operational independence, especially in regards to carrying

out studies on alternative scenarios.

Details on the specific use of the third-party sourced are found in the respective chapters.

ii

Assumptions, Scenarios, Data Sources and Methodology

Assumptions

A number of key assumptions run through the June 2014 World Rubber Industry Outlook

(WRIO):

There is a significant build-up of pent-up demand from two sources: lower than

expected growth in 2012 and the remnant from the sharp fall in consumption during

2008-2009. The average world total rubber consumption growth rate was 3.7% for 1961-

2007, which came down to 2.7% for 2008-2013. The assumption of build-up of pent-up

demand will run through from the vehicle sector to the rubber sector. The pent-up

demand will be released at an accelerating rate from 2014 onwards reaching the peak in

2016, released by the accelerating world economic growth rate.

The long maturity period of rubber trees (5-7 years) means that new natural rubber

(NR) supply potential for the entire forecast period has largely been decided. As such,

the NR supply potential (normal production) will continue to increase in 2014-2023,

based on trees already planted.

There is flexibility within the NR supply and it is expected to remain throughout the

forecast period. The rubber tree is a perennial crop that is harvested throughout the

year and its tapping intensity to some extent can be altered in both directions. The price

of NR dictates how much focus on tapping is given by smallholders plus the amount of

fertilisers and stimulants used.

Scenarios

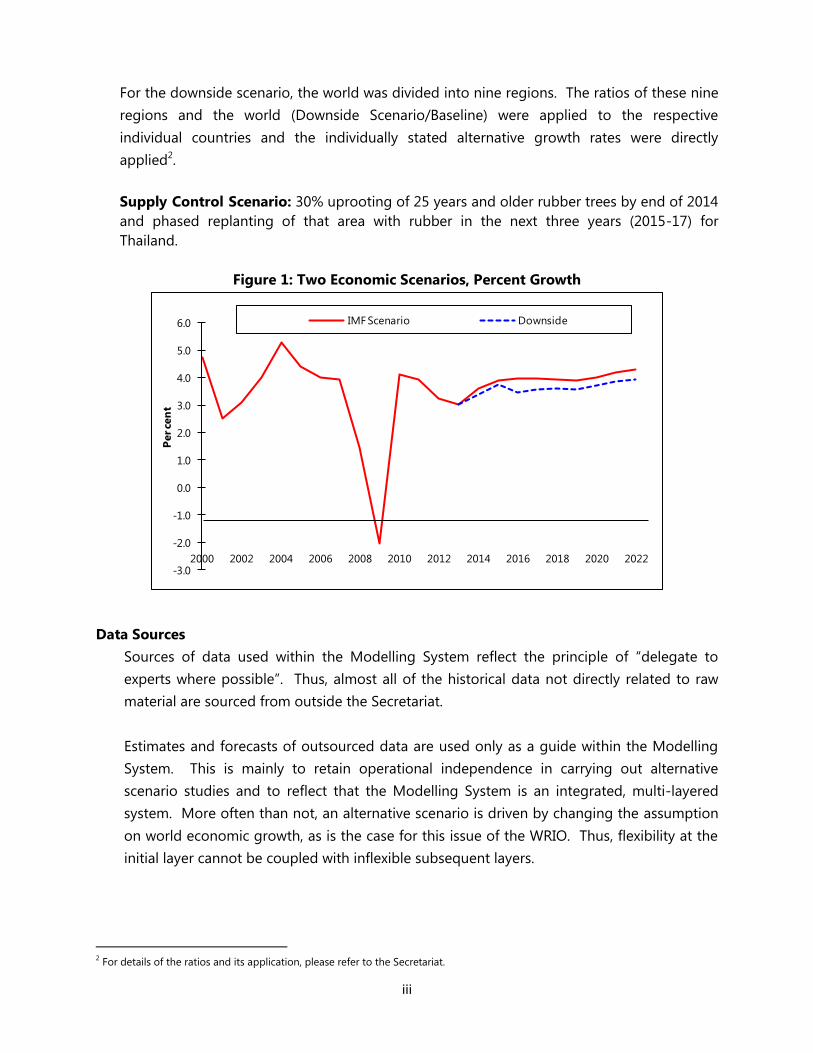

There are two economic and one supply control scenarios for the June 2014 WRIO.

Economic - IMF Scenario

This is work developed from using the comprehensive world economic outlook of the

International Monetary Fund (IMF). The data were extracted from the latest World Economic

Outlook (WEO), which was released in April 2014.

Economic - Downside Scenario

This is work developed using data from the April 2014 WEO‟s scenario works1. Two were

developed and for the June 2014 WRIO, the second, downside scenarios is being used:

weaker-than-baseline investment growth in G20 emerging market economies leads to the

world economy growing by on average around 0.3% below the baseline for 2014-15.

1For further information, refer to the IMF http://www.imf.org/external/pubs/ft/weo/2014/01/pdf/c1.pdf,

iii

For the downside scenario, the world was divided into nine regions. The ratios of these nine

regions and the world (Downside Scenario/Baseline) were applied to the respective

individual countries and the individually stated alternative growth rates were directly

applied2.

Supply Control Scenario: 30% uprooting of 25 years and older rubber trees by end of 2014

and phased replanting of that area with rubber in the next three years (2015-17) for

Thailand.

Figure 1: Two Economic Scenarios, Percent Growth

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Per ce

nt

IMF Scenario Downside

Data Sources

Sources of data used within the Modelling System reflect the principle of “delegate to

experts where possible”. Thus, almost all of the historical data not directly related to raw

material are sourced from outside the Secretariat.

Estimates and forecasts of outsourced data are used only as a guide within the Modelling

System. This is mainly to retain operational independence in carrying out alternative

scenario studies and to reflect that the Modelling System is an integrated, multi-layered

system. More often than not, an alternative scenario is driven by changing the assumption

on world economic growth, as is the case for this issue of the WRIO. Thus, flexibility at the

initial layer cannot be coupled with inflexible subsequent layers.

2 For details of the ratios and its application, please refer to the Secretariat.

iv

Economics

Historical and forecast economic growth rates of the world and individual countries/regions

up to and including 2019 were taken from the April 2014 World Economic Outlook (WEO)

of the IMF. Thereafter, the data are the output of the Secretariat‟s Modelling System.

Vehicles

Historical vehicle data (in use, sales and production) of the world and individual

countries/regions for 2000-2013 were taken from the May 2014 World Tyre Forecast Service

(WTFS) of LMC International. The historic data were wholly accepted and used in the

Modelling System exclusively, except for Canada, France and the USA.

Tyres

Historical tyre data (in use, sales and production) of the world and individual

countries/regions for 2000-2012 were taken from the May 2014 World Tyre Forecast Service

(WTFS) of LMC International. The historic data were wholly accepted and used in the

Modelling System.

Rubber

All rubber data (consumption, production, NR planted area, NR planting and NR replanting)

are sourced entirely within the Secretariat. Planting data and future planting assumptions

were updated and reviewed based on the annual survey as well as through discussions with

stakeholders.

Oil and rubber prices

Oil prices are sourced entirely from the Energy Information Agency (EIA). The short-term

outlook (2014-2015) was taken from the “Short-Term Energy Outlook” released on 10 June

2014, and the long-term outlook was taken from the “Annual Energy Outlook”, released on

7 May 2014.

Forecasts of natural and synthetic rubber prices are made by the Secretariat‟s Modelling

System.

Methodology – Tyre and Tyre Products Rubber Consumption

The calculation of total rubber consumption by the tyre sector is derived by multiplying the

number of tyres produced by the rubber weight of tyre. This calculation is carried for the three

main categories of automobile tyres:

Passenger car tyres (PCT) * Rubber weight = Total rubber consumption of PCT

Light commercial vehicle tyres (LCVT) * Rubber weight = Total rubber consumption of

LCVT

v

Medium/heavy vehicle tyres (MHCVT) * Rubber weight = Total rubber consumption of

MHCVT

Rubber weight of the three tyre types are estimated through surveys of the major tyre

manufacturers, which are intermittently reassessed by benchmarking against the following

parameters:

Average total weight of tyres – gathered via the national tyre manufacturers‟ associations

or trade data

Reverse engineered data

First-tier suppliers estimates

Publicly available and quoted data

There are, however, more than the three types of tyres produced in the world:

Aircraft tyres

Tow wheeled vehicle tyres: bicycle and motorcycle tyres

Off-the-road tyres: mining vehicle tyre, solid tyres (fork-lift trucks, supermarket trolleys,

buggies etc) and others

Others

These are aggregated into a category called Other Tyres, and its total rubber consumption

calculated as a remainder of the total rubber consumption of the total tyre sector and the

combined total rubber consumption of the three main categories of tyres. The total rubber

consumption of the Other Tyres category is calculated in this way due to:

Lack of production data of these tyre types

Lack of rubber weight data of these tyre types

To follow the first guiding principle in running the Modelling System – keep it simple

In practice, there are a number of challenges in correctly deriving the total rubber

consumption of the tyre sector, and the success of it depends upon the followings:

Assumption that the production data of the three main tyre types are correct

Availability of rubber weight of the three main tyre types for all producing countries

Assumption that rubber weights are correct

Availability of total rubber consumption of the total tyre sector

Only a limited number of countries report total rubber consumption data for the total tyre

sector and these countries include USA, Brazil, Japan, Germany, France, Italy, Spain, India,

Indonesia, Thailand, Malaysia, Korea and Taiwan, China. Already implied, the total rubber

consumption of the Other Tyres can only be derived in the presence of reported total rubber

consumption for the total tyre sector. In the absence of such data, the total rubber

consumption of the tyre sector is estimated using information from its most-like neighbour.

vi

The ranges of rubber weight used for the three main categories of automobile tyre are:

Rubber weight of PCT will range between 3.4-6.2kg

Rubber weight of LCVT will range between 5.3-13.1kg

Rubber weight of MHCVT will range between 20.7-40.4kg

Methodology – Natural and Synthetic Rubber Consumptions

Splitting the total rubber consumption by the Tyre sector into Natural rubber (NR)/Synthetic

Rubber (SR) is calculated by multiplying the total rubber consumption of the four tyre types by

its respective NR ratios.

The respective NR ratios of the four tyre types are estimated through surveys of the major tyre

manufacturers, which are intermittently reassessed through benchmarking against the

following parameters:

Reverse engineered data

First-tier suppliers estimates

Publicly available and quoted data

The NR ratios vary according to each country/regional location, and in most cases will

reflect:

Producer status, identifying the individual country as either a NR or SR producer. Thus,

country such as India (NR producer) has relatively higher NR ratios, while Russia (SR

producer) has relatively lower NR ratios.

Technology employed in the manufacture in tyres and local legislation.

Introduction of international company into a domestic company dominated country,

changing the NR/SR mix to that of the international norm.

Due to sensitivity surrounding the NR ratios, it will not explicitly be mentioned within this

report. Following the above statement, it is implicit that the SR consumption of the Tyre and

Tyre Products are calculated as a remainder of total rubber consumption of the Tyre and

Tyre Products following discovery of its NR consumption.

Methodology – Non-Tyre and Non-Tyre Products Rubber Consumption

Total rubber consumption of the Non-Tyre and Non-Tyre Products is calculated as a

remainder of total rubber consumption and total rubber consumption of the Tyre and Tyre

Products. This methodology is used because the Non-Tyre and Non-Tyre Products are too

fragmented for individual data collection and analysis. Thus, for historic data, the accuracy of

information pertaining to the Non-Tyre and Non-Tyre Products is contingent upon the

accuracy of the total rubber consumption and the total rubber consumption of the tyre

sector. For the outlook, it is directly linked to economic growth, with the individual country

vii

rubber consumption a function of its respective economic performance and consumption

trend.

Methodology – Normal Production

The combination of new planting, replanting, total area, yield and technical progress will

lead to projections of „normal production‟. The analysis incorporates the Vintage approach,

which is a model to analyse the effects of planting decisions in a positive or negative

direction on production potential. In this connection, the term vintage is defined as the area

planted in a certain year. Such a vintage is followed over time, when part of it will be

discarded because the land is used for other purposes or for replanting with the same crop.

Detailed modelling analyses using the Vintage approach have been done for eleven

countries: Thailand, Indonesia, Malaysia, India, Vietnam, China, Sri Lanka, Cambodia,

Philippines, Myanmar and Laos.

For further details on the Vintage approach, please contact the Secretariat.

1

Executive Summary

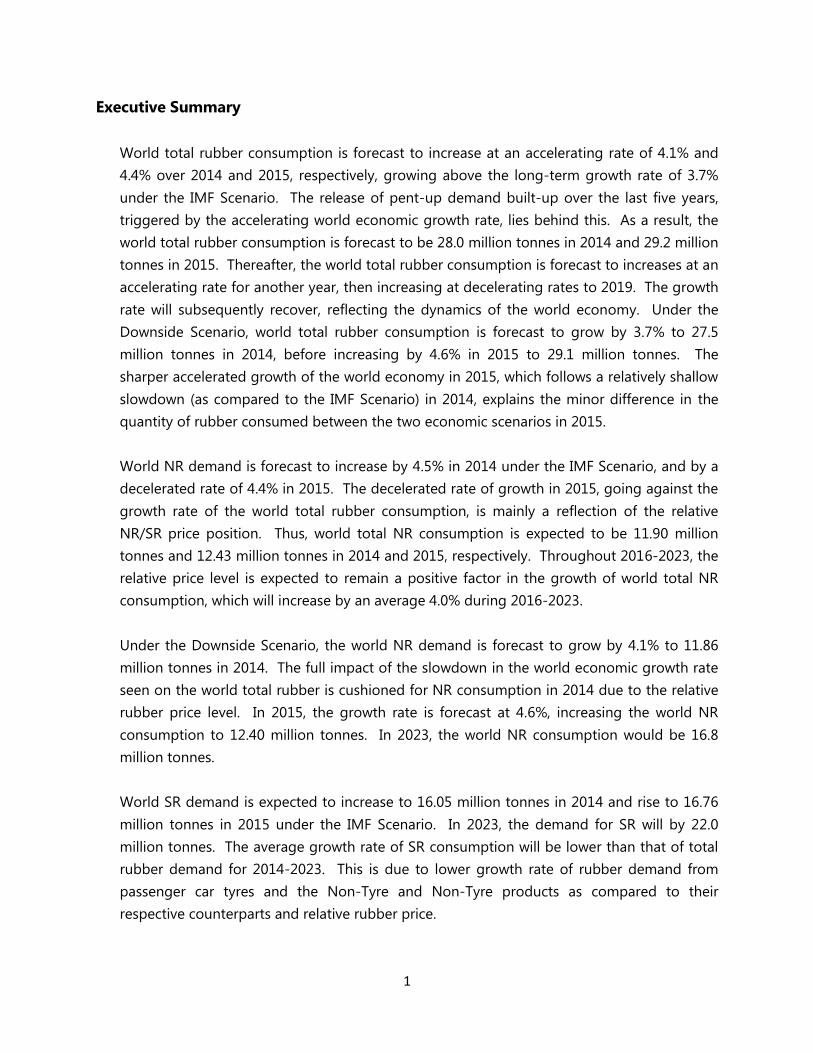

World total rubber consumption is forecast to increase at an accelerating rate of 4.1% and

4.4% over 2014 and 2015, respectively, growing above the long-term growth rate of 3.7%

under the IMF Scenario. The release of pent-up demand built-up over the last five years,

triggered by the accelerating world economic growth rate, lies behind this. As a result, the

world total rubber consumption is forecast to be 28.0 million tonnes in 2014 and 29.2 million

tonnes in 2015. Thereafter, the world total rubber consumption is forecast to increases at an

accelerating rate for another year, then increasing at decelerating rates to 2019. The growth

rate will subsequently recover, reflecting the dynamics of the world economy. Under the

Downside Scenario, world total rubber consumption is forecast to grow by 3.7% to 27.5

million tonnes in 2014, before increasing by 4.6% in 2015 to 29.1 million tonnes. The

sharper accelerated growth of the world economy in 2015, which follows a relatively shallow

slowdown (as compared to the IMF Scenario) in 2014, explains the minor difference in the

quantity of rubber consumed between the two economic scenarios in 2015.

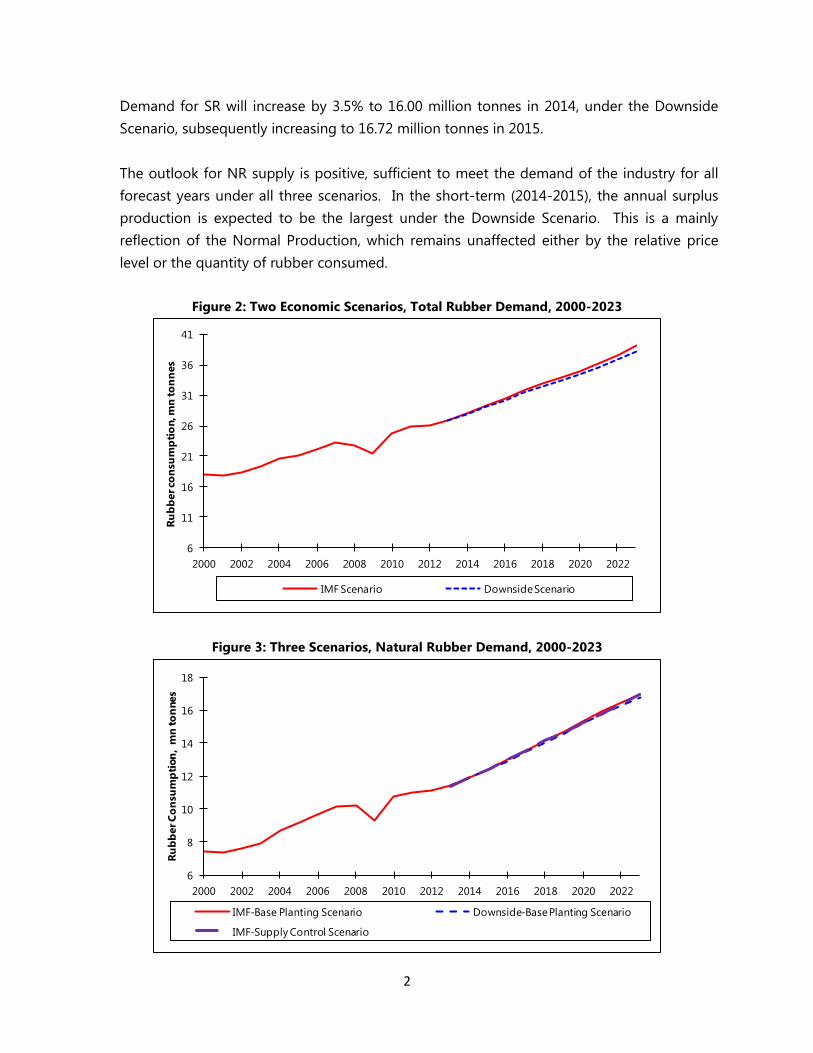

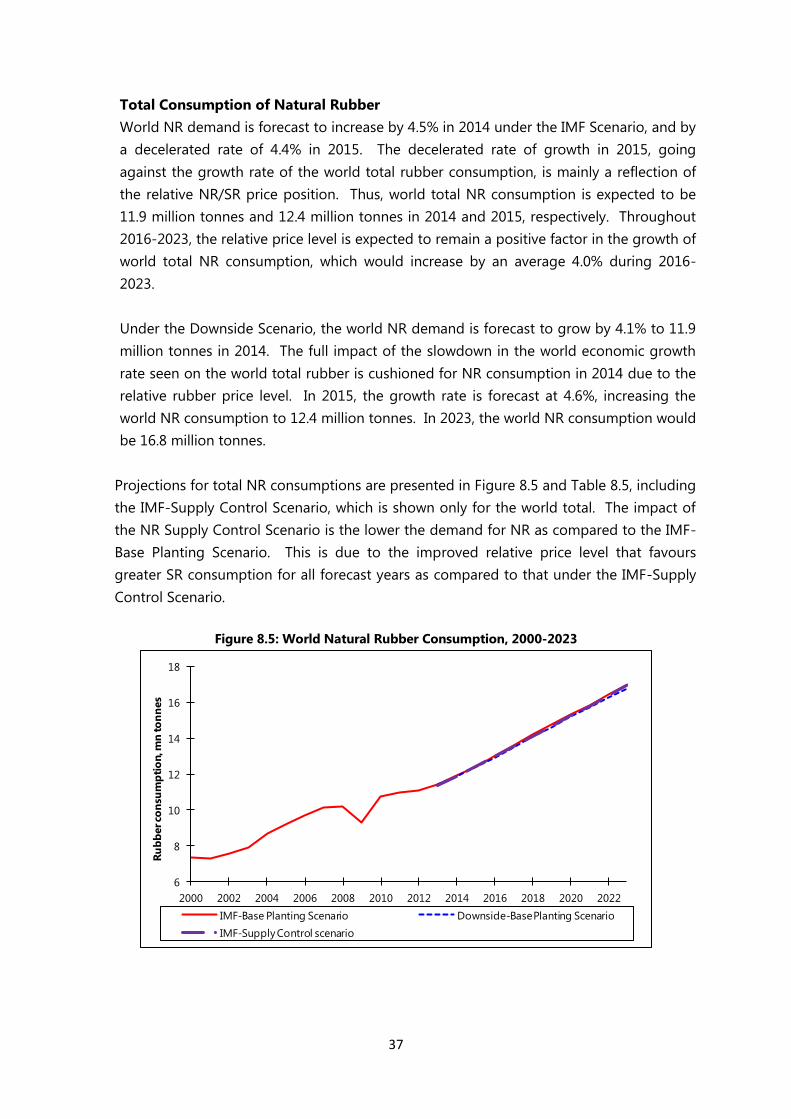

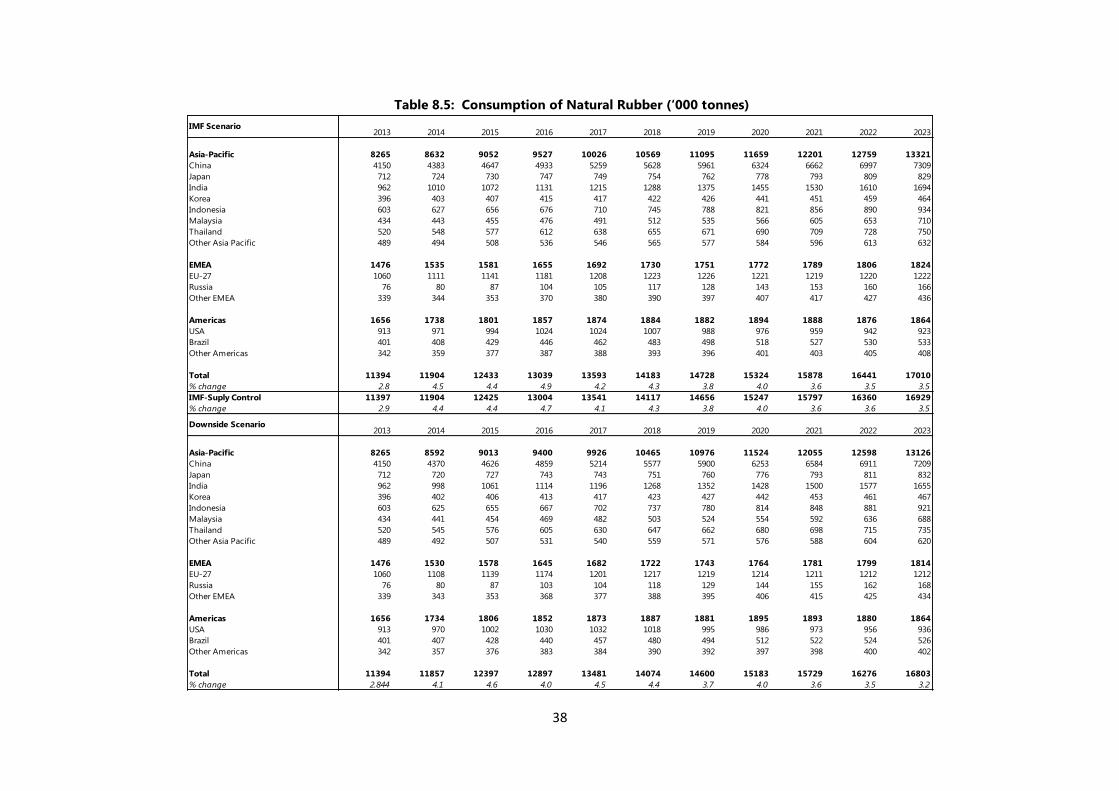

World NR demand is forecast to increase by 4.5% in 2014 under the IMF Scenario, and by a

decelerated rate of 4.4% in 2015. The decelerated rate of growth in 2015, going against the

growth rate of the world total rubber consumption, is mainly a reflection of the relative

NR/SR price position. Thus, world total NR consumption is expected to be 11.90 million

tonnes and 12.43 million tonnes in 2014 and 2015, respectively. Throughout 2016-2023, the

relative price level is expected to remain a positive factor in the growth of world total NR

consumption, which will increase by an average 4.0% during 2016-2023.

Under the Downside Scenario, the world NR demand is forecast to grow by 4.1% to 11.86

million tonnes in 2014. The full impact of the slowdown in the world economic growth rate

seen on the world total rubber is cushioned for NR consumption in 2014 due to the relative

rubber price level. In 2015, the growth rate is forecast at 4.6%, increasing the world NR

consumption to 12.40 million tonnes. In 2023, the world NR consumption would be 16.8

million tonnes.

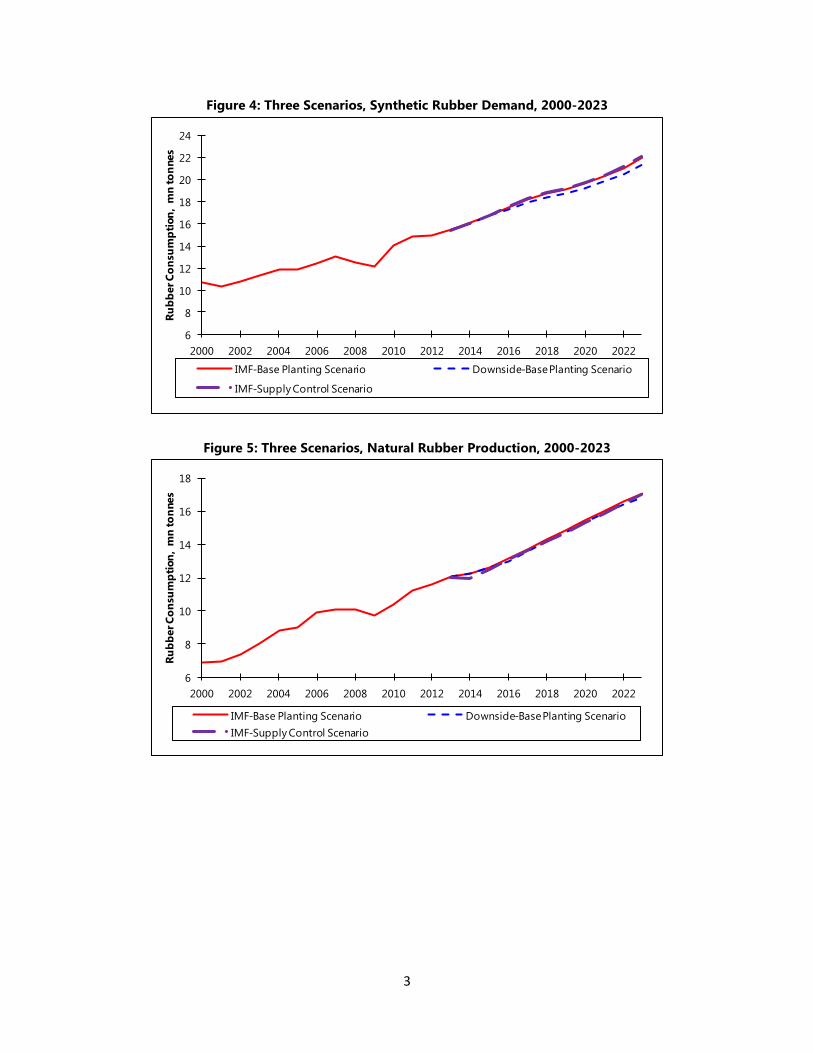

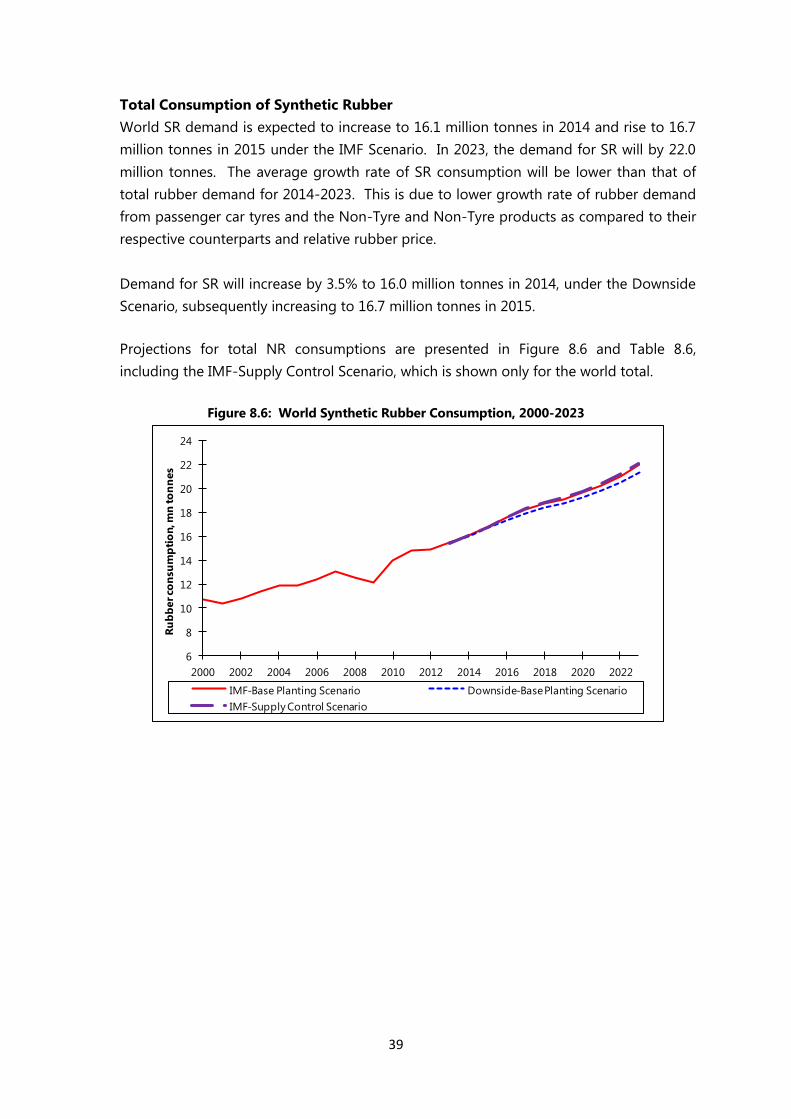

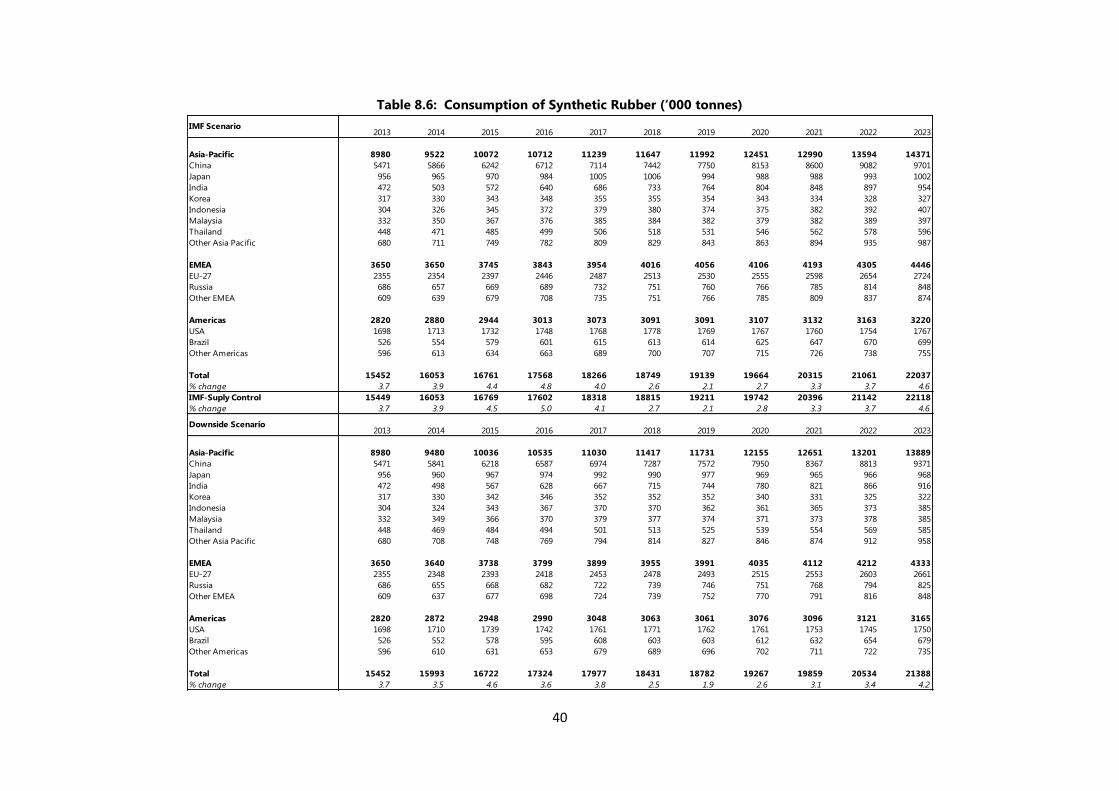

World SR demand is expected to increase to 16.05 million tonnes in 2014 and rise to 16.76

million tonnes in 2015 under the IMF Scenario. In 2023, the demand for SR will by 22.0

million tonnes. The average growth rate of SR consumption will be lower than that of total

rubber demand for 2014-2023. This is due to lower growth rate of rubber demand from

passenger car tyres and the Non-Tyre and Non-Tyre products as compared to their

respective counterparts and relative rubber price.

2

Demand for SR will increase by 3.5% to 16.00 million tonnes in 2014, under the Downside

Scenario, subsequently increasing to 16.72 million tonnes in 2015.

The outlook for NR supply is positive, sufficient to meet the demand of the industry for all

forecast years under all three scenarios. In the short-term (2014-2015), the annual surplus

production is expected to be the largest under the Downside Scenario. This is a mainly

reflection of the Normal Production, which remains unaffected either by the relative price

level or the quantity of rubber consumed.

Figure 2: Two Economic Scenarios, Total Rubber Demand, 2000-2023

6

11

16

21

26

31

36

41

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Ru

bb

er co

nsu

mp

tio

n, m

n to

nn

es

IMF Scenario Downside Scenario

Figure 3: Three Scenarios, Natural Rubber Demand, 2000-2023

6

8

10

12

14

16

18

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Ru

bb

er C

on

sum

pti

on

, m

n to

nnes

IMF-Base Planting Scenario Downside-Base Planting Scenario

IMF-Supply Control Scenario

3

Figure 4: Three Scenarios, Synthetic Rubber Demand, 2000-2023

6

8

10

12

14

16

18

20

22

24

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Ru

bb

er C

on

sum

pti

on

, m

n to

nnes

IMF-Base Planting Scenario Downside-Base Planting Scenario

IMF-Supply Control Scenario

Figure 5: Three Scenarios, Natural Rubber Production, 2000-2023

6

8

10

12

14

16

18

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Ru

bb

er C

on

sum

pti

on

, m

n to

nnes

IMF-Base Planting Scenario Downside-Base Planting Scenario

IMF-Supply Control Scenario

4

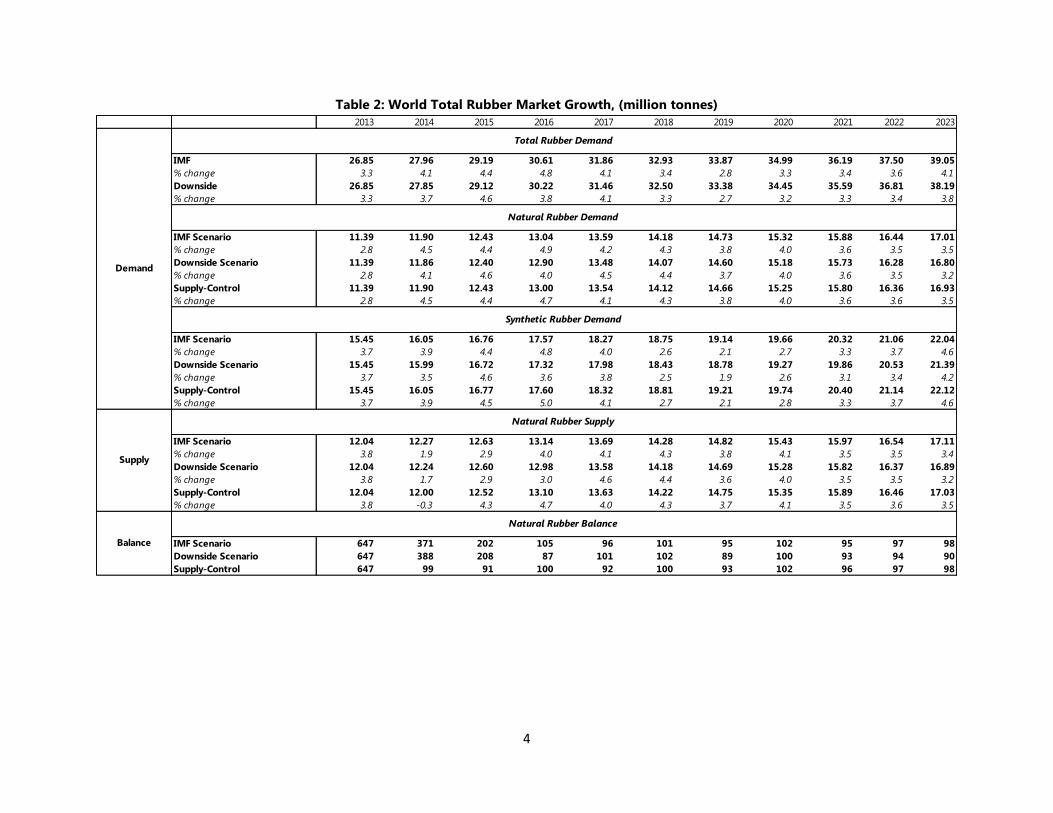

Table 2: World Total Rubber Market Growth, (million tonnes)

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

IMF 26.85 27.96 29.19 30.61 31.86 32.93 33.87 34.99 36.19 37.50 39.05

% change 3.3 4.1 4.4 4.8 4.1 3.4 2.8 3.3 3.4 3.6 4.1

Downside 26.85 27.85 29.12 30.22 31.46 32.50 33.38 34.45 35.59 36.81 38.19

% change 3.3 3.7 4.6 3.8 4.1 3.3 2.7 3.2 3.3 3.4 3.8

IMF Scenario 11.39 11.90 12.43 13.04 13.59 14.18 14.73 15.32 15.88 16.44 17.01

% change 2.8 4.5 4.4 4.9 4.2 4.3 3.8 4.0 3.6 3.5 3.5

Downside Scenario 11.39 11.86 12.40 12.90 13.48 14.07 14.60 15.18 15.73 16.28 16.80

% change 2.8 4.1 4.6 4.0 4.5 4.4 3.7 4.0 3.6 3.5 3.2

Supply-Control 11.39 11.90 12.43 13.00 13.54 14.12 14.66 15.25 15.80 16.36 16.93

% change 2.8 4.5 4.4 4.7 4.1 4.3 3.8 4.0 3.6 3.6 3.5

IMF Scenario 15.45 16.05 16.76 17.57 18.27 18.75 19.14 19.66 20.32 21.06 22.04

% change 3.7 3.9 4.4 4.8 4.0 2.6 2.1 2.7 3.3 3.7 4.6

Downside Scenario 15.45 15.99 16.72 17.32 17.98 18.43 18.78 19.27 19.86 20.53 21.39

% change 3.7 3.5 4.6 3.6 3.8 2.5 1.9 2.6 3.1 3.4 4.2

Supply-Control 15.45 16.05 16.77 17.60 18.32 18.81 19.21 19.74 20.40 21.14 22.12

% change 3.7 3.9 4.5 5.0 4.1 2.7 2.1 2.8 3.3 3.7 4.6

IMF Scenario 12.04 12.27 12.63 13.14 13.69 14.28 14.82 15.43 15.97 16.54 17.11

% change 3.8 1.9 2.9 4.0 4.1 4.3 3.8 4.1 3.5 3.5 3.4

Downside Scenario 12.04 12.24 12.60 12.98 13.58 14.18 14.69 15.28 15.82 16.37 16.89

% change 3.8 1.7 2.9 3.0 4.6 4.4 3.6 4.0 3.5 3.5 3.2

Supply-Control 12.04 12.00 12.52 13.10 13.63 14.22 14.75 15.35 15.89 16.46 17.03

% change 3.8 -0.3 4.3 4.7 4.0 4.3 3.7 4.1 3.5 3.6 3.5

IMF Scenario 647 371 202 105 96 101 95 102 95 97 98

Downside Scenario 647 388 208 87 101 102 89 100 93 94 90

Supply-Control 647 99 91 100 92 100 93 102 96 97 98

Demand

Total Rubber Demand

Natural Rubber Demand

Synthetic Rubber Demand

Natural Rubber Supply

Natural Rubber Balance

Supply

Balance

5

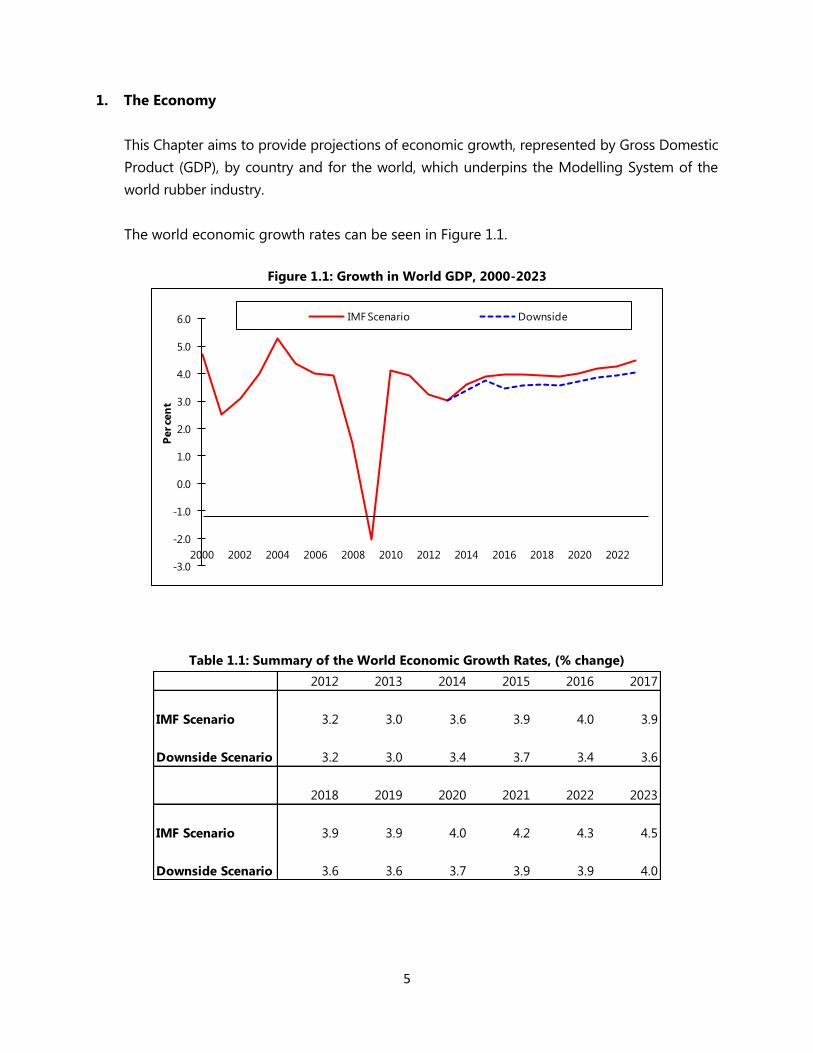

1. The Economy

This Chapter aims to provide projections of economic growth, represented by Gross Domestic

Product (GDP), by country and for the world, which underpins the Modelling System of the

world rubber industry.

The world economic growth rates can be seen in Figure 1.1.

Figure 1.1: Growth in World GDP, 2000-2023

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Per ce

nt

IMF Scenario Downside

Table 1.1: Summary of the World Economic Growth Rates, (% change)

2012 2013 2014 2015 2016 2017

IMF Scenario 3.2 3.0 3.6 3.9 4.0 3.9

Downside Scenario 3.2 3.0 3.4 3.7 3.4 3.6

2018 2019 2020 2021 2022 2023

IMF Scenario 3.9 3.9 4.0 4.2 4.3 4.5

Downside Scenario 3.6 3.6 3.7 3.9 3.9 4.0

6

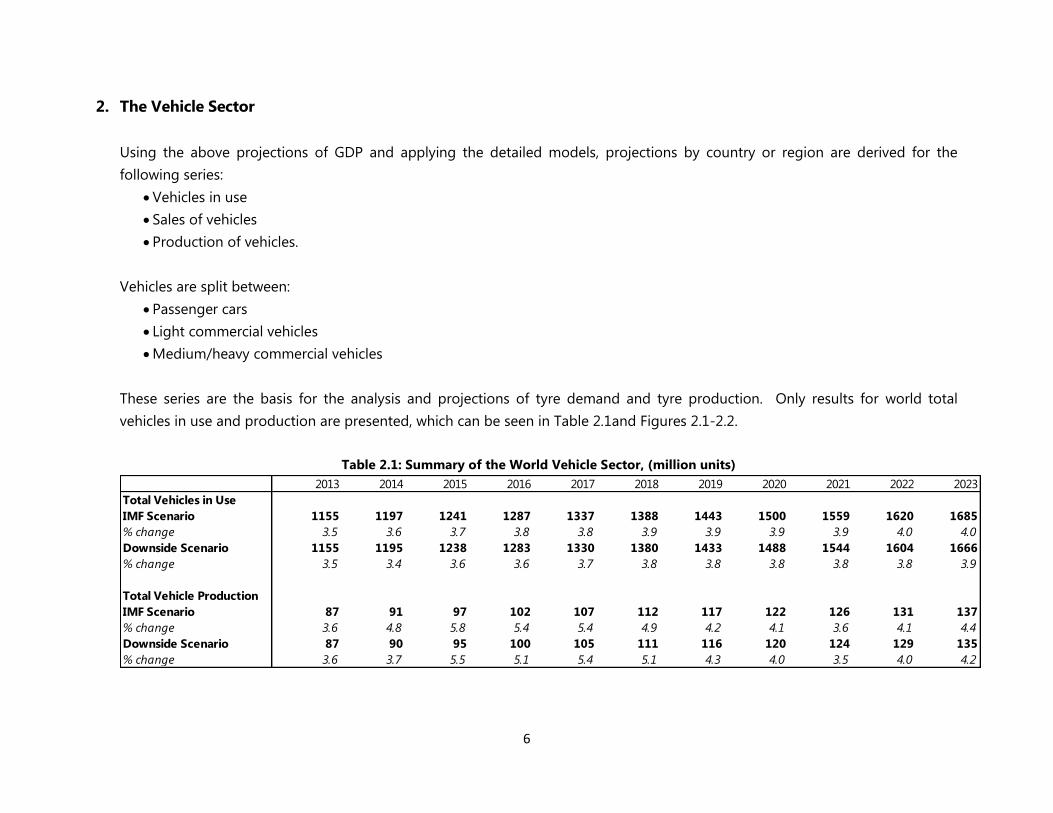

2. The Vehicle Sector

Using the above projections of GDP and applying the detailed models, projections by country or region are derived for the

following series:

Vehicles in use

Sales of vehicles

Production of vehicles.

Vehicles are split between:

Passenger cars

Light commercial vehicles

Medium/heavy commercial vehicles

These series are the basis for the analysis and projections of tyre demand and tyre production. Only results for world total

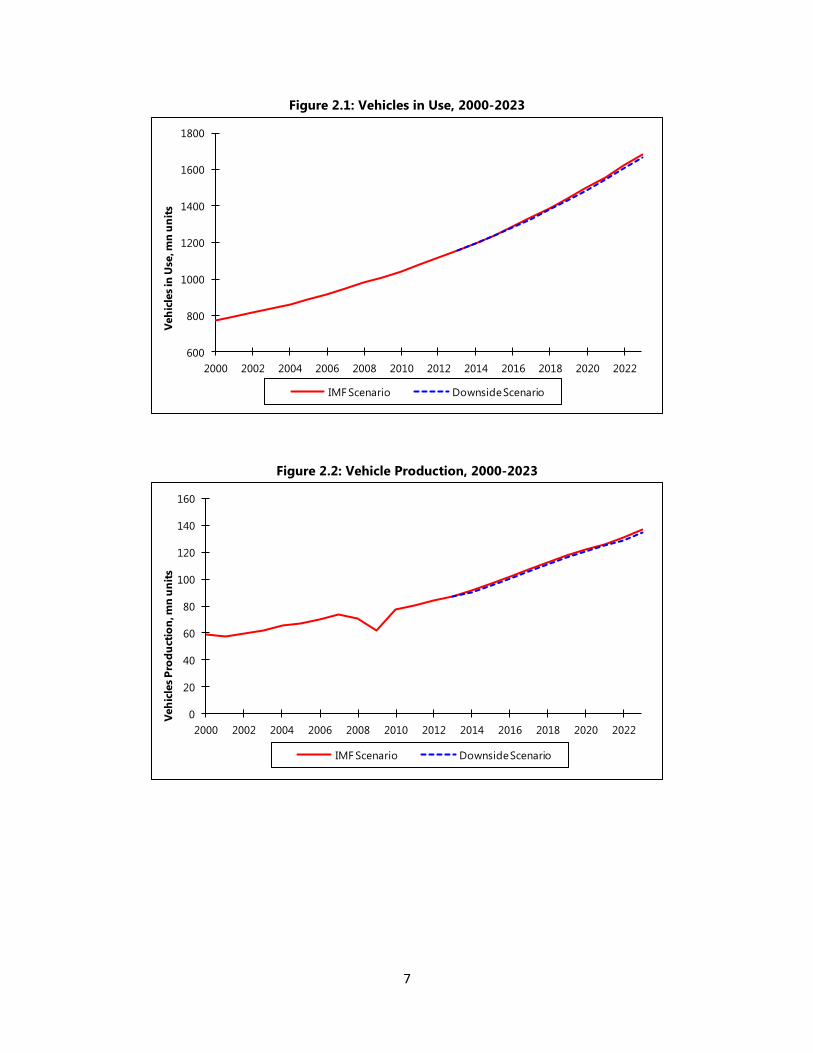

vehicles in use and production are presented, which can be seen in Table 2.1and Figures 2.1-2.2.

Table 2.1: Summary of the World Vehicle Sector, (million units)

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Total Vehicles in Use

IMF Scenario 1155 1197 1241 1287 1337 1388 1443 1500 1559 1620 1685

% change 3.5 3.6 3.7 3.8 3.8 3.9 3.9 3.9 3.9 4.0 4.0

Downside Scenario 1155 1195 1238 1283 1330 1380 1433 1488 1544 1604 1666

% change 3.5 3.4 3.6 3.6 3.7 3.8 3.8 3.8 3.8 3.8 3.9

Total Vehicle Production

IMF Scenario 87 91 97 102 107 112 117 122 126 131 137

% change 3.6 4.8 5.8 5.4 5.4 4.9 4.2 4.1 3.6 4.1 4.4

Downside Scenario 87 90 95 100 105 111 116 120 124 129 135

% change 3.6 3.7 5.5 5.1 5.4 5.1 4.3 4.0 3.5 4.0 4.2

7

Figure 2.1: Vehicles in Use, 2000-2023

600

800

1000

1200

1400

1600

1800

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Veh

icle

s in

Use

, mn

un

its

IMF Scenario Downside Scenario

Figure 2.2: Vehicle Production, 2000-2023

0

20

40

60

80

100

120

140

160

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Veh

icle

s P

rod

uct

ion

, mn

un

its

IMF Scenario Downside Scenario

8

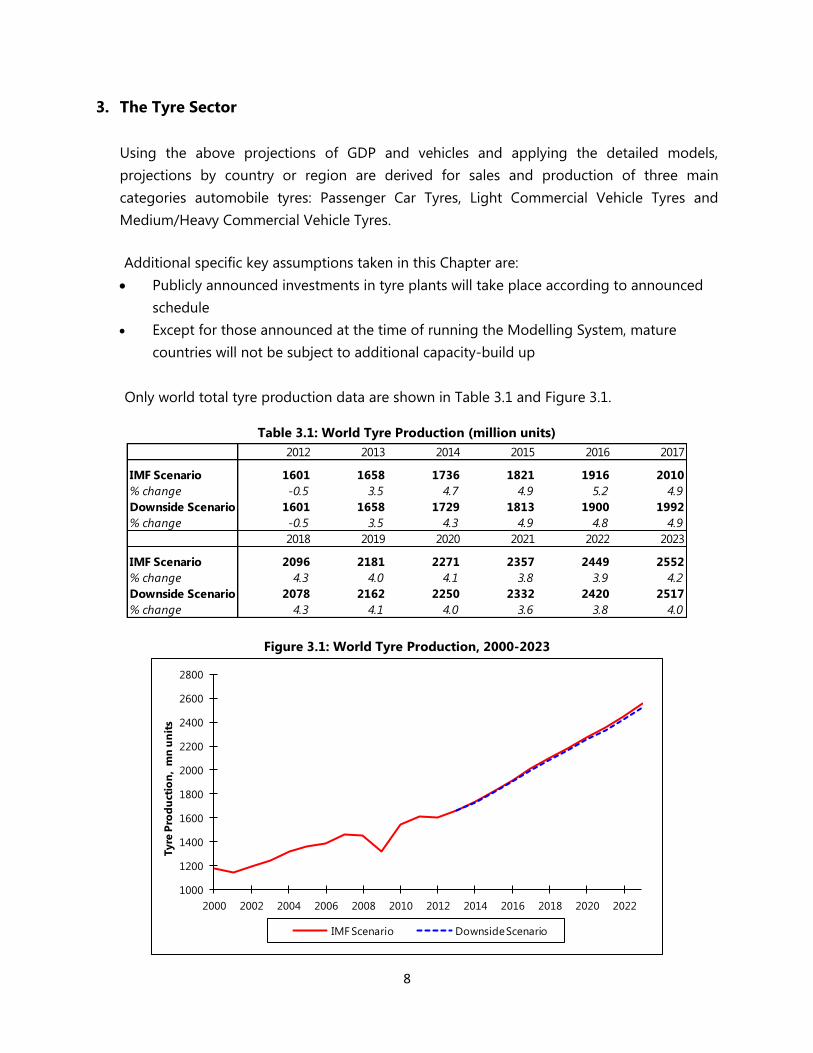

3. The Tyre Sector

Using the above projections of GDP and vehicles and applying the detailed models,

projections by country or region are derived for sales and production of three main

categories automobile tyres: Passenger Car Tyres, Light Commercial Vehicle Tyres and

Medium/Heavy Commercial Vehicle Tyres.

Additional specific key assumptions taken in this Chapter are:

Publicly announced investments in tyre plants will take place according to announced

schedule

Except for those announced at the time of running the Modelling System, mature

countries will not be subject to additional capacity-build up

Only world total tyre production data are shown in Table 3.1 and Figure 3.1.

Table 3.1: World Tyre Production (million units)

2012 2013 2014 2015 2016 2017

IMF Scenario 1601 1658 1736 1821 1916 2010

% change -0.5 3.5 4.7 4.9 5.2 4.9

Downside Scenario 1601 1658 1729 1813 1900 1992

% change -0.5 3.5 4.3 4.9 4.8 4.9

2018 2019 2020 2021 2022 2023

IMF Scenario 2096 2181 2271 2357 2449 2552

% change 4.3 4.0 4.1 3.8 3.9 4.2

Downside Scenario 2078 2162 2250 2332 2420 2517

% change 4.3 4.1 4.0 3.6 3.8 4.0

Figure 3.1: World Tyre Production, 2000-2023

1000

1200

1400

1600

1800

2000

2200

2400

2600

2800

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tyre

Pro

du

ctio

n,

mn

un

its

IMF Scenario Downside Scenario

9

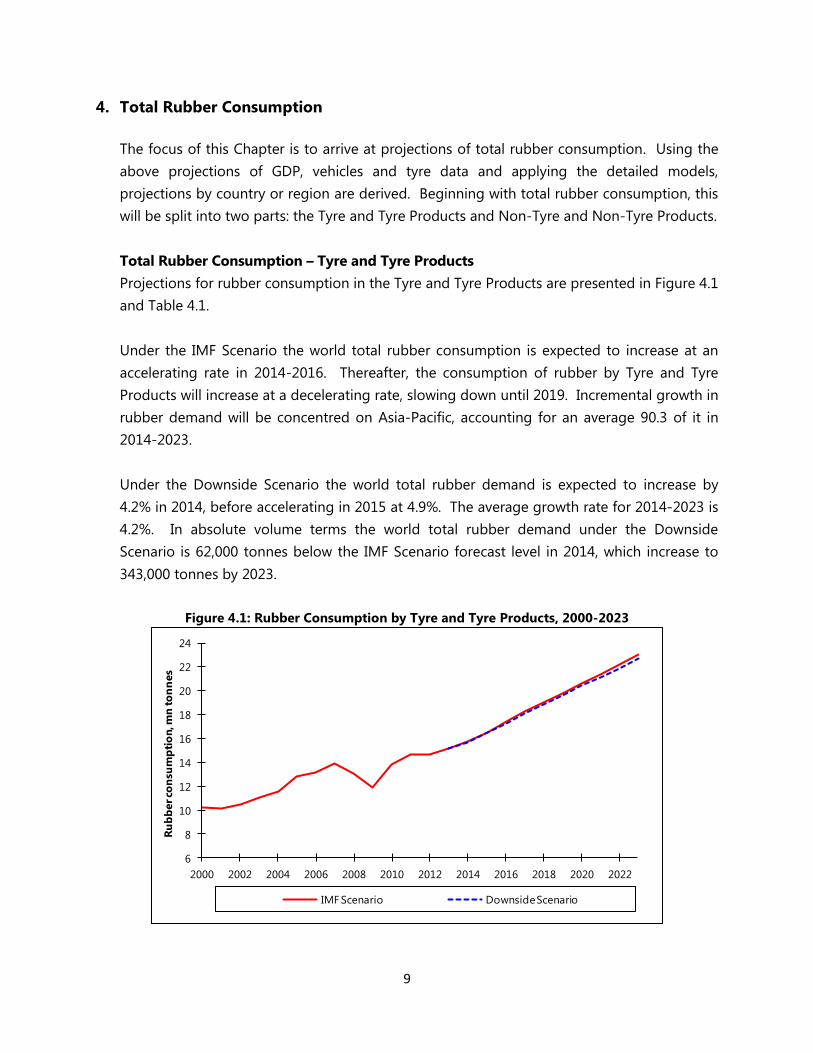

4. Total Rubber Consumption

The focus of this Chapter is to arrive at projections of total rubber consumption. Using the

above projections of GDP, vehicles and tyre data and applying the detailed models,

projections by country or region are derived. Beginning with total rubber consumption, this

will be split into two parts: the Tyre and Tyre Products and Non-Tyre and Non-Tyre Products.

Total Rubber Consumption – Tyre and Tyre Products

Projections for rubber consumption in the Tyre and Tyre Products are presented in Figure 4.1

and Table 4.1.

Under the IMF Scenario the world total rubber consumption is expected to increase at an

accelerating rate in 2014-2016. Thereafter, the consumption of rubber by Tyre and Tyre

Products will increase at a decelerating rate, slowing down until 2019. Incremental growth in

rubber demand will be concentred on Asia-Pacific, accounting for an average 90.3 of it in

2014-2023.

Under the Downside Scenario the world total rubber demand is expected to increase by

4.2% in 2014, before accelerating in 2015 at 4.9%. The average growth rate for 2014-2023 is

4.2%. In absolute volume terms the world total rubber demand under the Downside

Scenario is 62,000 tonnes below the IMF Scenario forecast level in 2014, which increase to

343,000 tonnes by 2023.

Figure 4.1: Rubber Consumption by Tyre and Tyre Products, 2000-2023

6

8

10

12

14

16

18

20

22

24

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Ru

bb

er co

nsu

mp

tio

n, m

n to

nn

es

IMF Scenario Downside Scenario

10

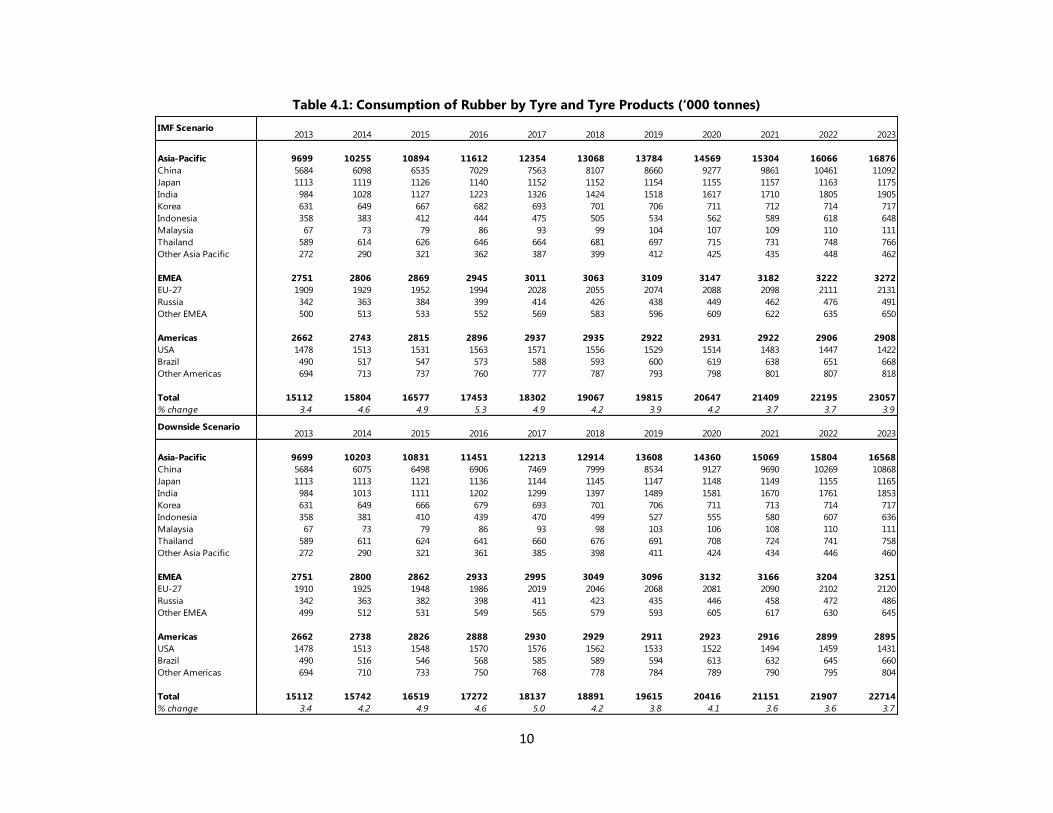

Table 4.1: Consumption of Rubber by Tyre and Tyre Products (‘000 tonnes)

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 9699 10255 10894 11612 12354 13068 13784 14569 15304 16066 16876

China 5684 6098 6535 7029 7563 8107 8660 9277 9861 10461 11092

Japan 1113 1119 1126 1140 1152 1152 1154 1155 1157 1163 1175

India 984 1028 1127 1223 1326 1424 1518 1617 1710 1805 1905

Korea 631 649 667 682 693 701 706 711 712 714 717

Indonesia 358 383 412 444 475 505 534 562 589 618 648

Malaysia 67 73 79 86 93 99 104 107 109 110 111

Thailand 589 614 626 646 664 681 697 715 731 748 766

Other Asia Pacific 272 290 321 362 387 399 412 425 435 448 462

EMEA 2751 2806 2869 2945 3011 3063 3109 3147 3182 3222 3272

EU-27 1909 1929 1952 1994 2028 2055 2074 2088 2098 2111 2131

Russia 342 363 384 399 414 426 438 449 462 476 491

Other EMEA 500 513 533 552 569 583 596 609 622 635 650

Americas 2662 2743 2815 2896 2937 2935 2922 2931 2922 2906 2908

USA 1478 1513 1531 1563 1571 1556 1529 1514 1483 1447 1422

Brazil 490 517 547 573 588 593 600 619 638 651 668

Other Americas 694 713 737 760 777 787 793 798 801 807 818

Total 15112 15804 16577 17453 18302 19067 19815 20647 21409 22195 23057

% change 3.4 4.6 4.9 5.3 4.9 4.2 3.9 4.2 3.7 3.7 3.9

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 9699 10203 10831 11451 12213 12914 13608 14360 15069 15804 16568

China 5684 6075 6498 6906 7469 7999 8534 9127 9690 10269 10868

Japan 1113 1113 1121 1136 1144 1145 1147 1148 1149 1155 1165

India 984 1013 1111 1202 1299 1397 1489 1581 1670 1761 1853

Korea 631 649 666 679 693 701 706 711 713 714 717

Indonesia 358 381 410 439 470 499 527 555 580 607 636

Malaysia 67 73 79 86 93 98 103 106 108 110 111

Thailand 589 611 624 641 660 676 691 708 724 741 758

Other Asia Pacific 272 290 321 361 385 398 411 424 434 446 460

EMEA 2751 2800 2862 2933 2995 3049 3096 3132 3166 3204 3251

EU-27 1910 1925 1948 1986 2019 2046 2068 2081 2090 2102 2120

Russia 342 363 382 398 411 423 435 446 458 472 486

Other EMEA 499 512 531 549 565 579 593 605 617 630 645

Americas 2662 2738 2826 2888 2930 2929 2911 2923 2916 2899 2895

USA 1478 1513 1548 1570 1576 1562 1533 1522 1494 1459 1431

Brazil 490 516 546 568 585 589 594 613 632 645 660

Other Americas 694 710 733 750 768 778 784 789 790 795 804

Total 15112 15742 16519 17272 18137 18891 19615 20416 21151 21907 22714

% change 3.4 4.2 4.9 4.6 5.0 4.2 3.8 4.1 3.6 3.6 3.7

IMF Scenario

Downside Scenario

11

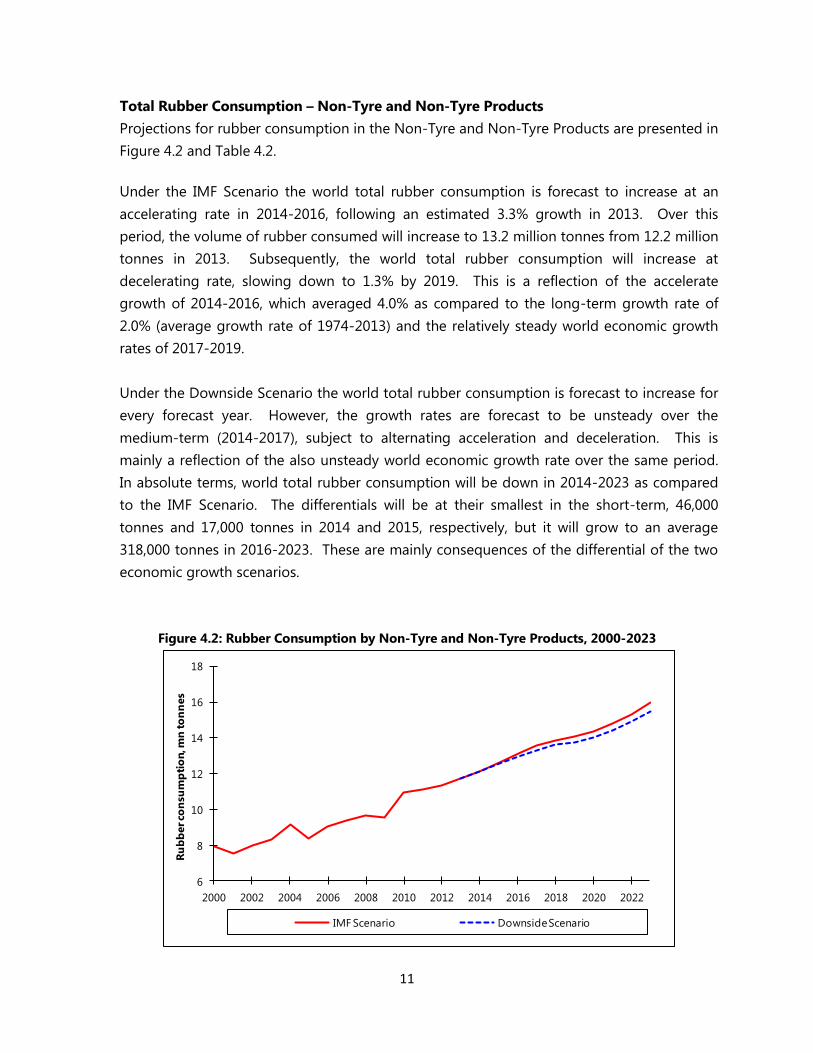

Total Rubber Consumption – Non-Tyre and Non-Tyre Products

Projections for rubber consumption in the Non-Tyre and Non-Tyre Products are presented in

Figure 4.2 and Table 4.2.

Under the IMF Scenario the world total rubber consumption is forecast to increase at an

accelerating rate in 2014-2016, following an estimated 3.3% growth in 2013. Over this

period, the volume of rubber consumed will increase to 13.2 million tonnes from 12.2 million

tonnes in 2013. Subsequently, the world total rubber consumption will increase at

decelerating rate, slowing down to 1.3% by 2019. This is a reflection of the accelerate

growth of 2014-2016, which averaged 4.0% as compared to the long-term growth rate of

2.0% (average growth rate of 1974-2013) and the relatively steady world economic growth

rates of 2017-2019.

Under the Downside Scenario the world total rubber consumption is forecast to increase for

every forecast year. However, the growth rates are forecast to be unsteady over the

medium-term (2014-2017), subject to alternating acceleration and deceleration. This is

mainly a reflection of the also unsteady world economic growth rate over the same period.

In absolute terms, world total rubber consumption will be down in 2014-2023 as compared

to the IMF Scenario. The differentials will be at their smallest in the short-term, 46,000

tonnes and 17,000 tonnes in 2014 and 2015, respectively, but it will grow to an average

318,000 tonnes in 2016-2023. These are mainly consequences of the differential of the two

economic growth scenarios.

Figure 4.2: Rubber Consumption by Non-Tyre and Non-Tyre Products, 2000-2023

6

8

10

12

14

16

18

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Ru

bb

er co

nsu

mp

tio

n, m

n to

nn

es

IMF Scenario Downside Scenario

12

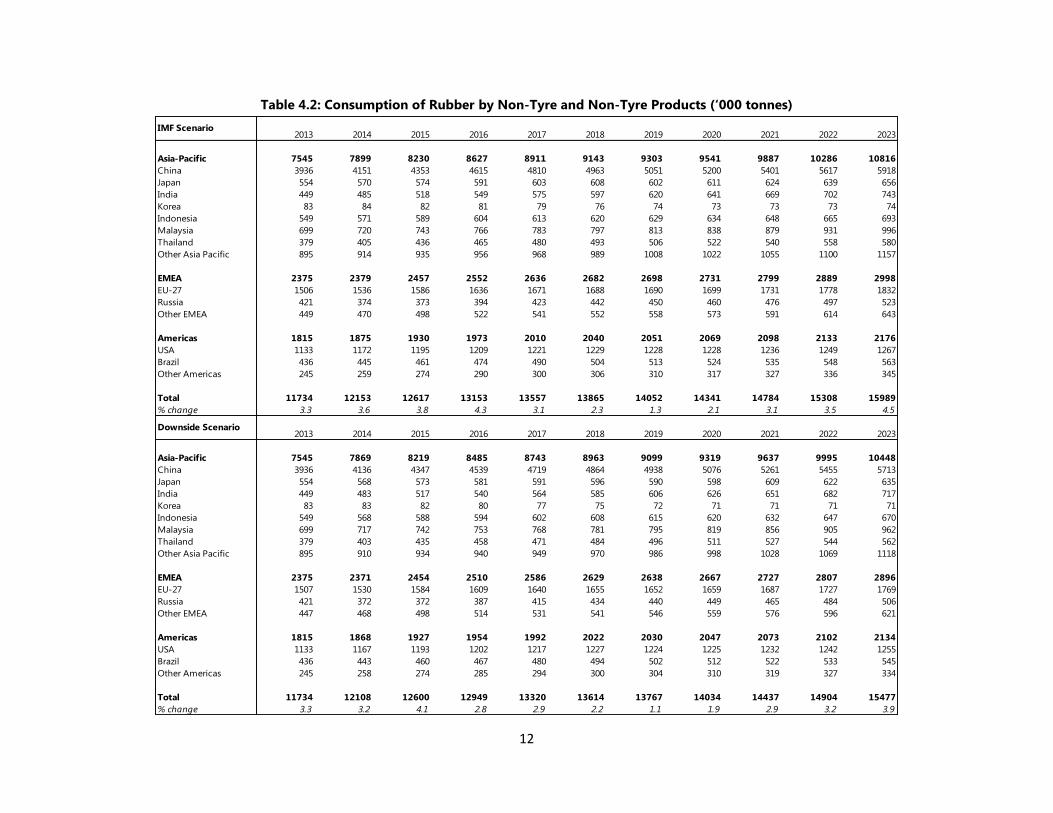

Table 4.2: Consumption of Rubber by Non-Tyre and Non-Tyre Products (‘000 tonnes)

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 7545 7899 8230 8627 8911 9143 9303 9541 9887 10286 10816

China 3936 4151 4353 4615 4810 4963 5051 5200 5401 5617 5918

Japan 554 570 574 591 603 608 602 611 624 639 656

India 449 485 518 549 575 597 620 641 669 702 743

Korea 83 84 82 81 79 76 74 73 73 73 74

Indonesia 549 571 589 604 613 620 629 634 648 665 693

Malaysia 699 720 743 766 783 797 813 838 879 931 996

Thailand 379 405 436 465 480 493 506 522 540 558 580

Other Asia Pacific 895 914 935 956 968 989 1008 1022 1055 1100 1157

EMEA 2375 2379 2457 2552 2636 2682 2698 2731 2799 2889 2998

EU-27 1506 1536 1586 1636 1671 1688 1690 1699 1731 1778 1832

Russia 421 374 373 394 423 442 450 460 476 497 523

Other EMEA 449 470 498 522 541 552 558 573 591 614 643

Americas 1815 1875 1930 1973 2010 2040 2051 2069 2098 2133 2176

USA 1133 1172 1195 1209 1221 1229 1228 1228 1236 1249 1267

Brazil 436 445 461 474 490 504 513 524 535 548 563

Other Americas 245 259 274 290 300 306 310 317 327 336 345

Total 11734 12153 12617 13153 13557 13865 14052 14341 14784 15308 15989

% change 3.3 3.6 3.8 4.3 3.1 2.3 1.3 2.1 3.1 3.5 4.5

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 7545 7869 8219 8485 8743 8963 9099 9319 9637 9995 10448

China 3936 4136 4347 4539 4719 4864 4938 5076 5261 5455 5713

Japan 554 568 573 581 591 596 590 598 609 622 635

India 449 483 517 540 564 585 606 626 651 682 717

Korea 83 83 82 80 77 75 72 71 71 71 71

Indonesia 549 568 588 594 602 608 615 620 632 647 670

Malaysia 699 717 742 753 768 781 795 819 856 905 962

Thailand 379 403 435 458 471 484 496 511 527 544 562

Other Asia Pacific 895 910 934 940 949 970 986 998 1028 1069 1118

EMEA 2375 2371 2454 2510 2586 2629 2638 2667 2727 2807 2896

EU-27 1507 1530 1584 1609 1640 1655 1652 1659 1687 1727 1769

Russia 421 372 372 387 415 434 440 449 465 484 506

Other EMEA 447 468 498 514 531 541 546 559 576 596 621

Americas 1815 1868 1927 1954 1992 2022 2030 2047 2073 2102 2134

USA 1133 1167 1193 1202 1217 1227 1224 1225 1232 1242 1255

Brazil 436 443 460 467 480 494 502 512 522 533 545

Other Americas 245 258 274 285 294 300 304 310 319 327 334

Total 11734 12108 12600 12949 13320 13614 13767 14034 14437 14904 15477

% change 3.3 3.2 4.1 2.8 2.9 2.2 1.1 1.9 2.9 3.2 3.9

IMF Scenario

Downside Scenario

13

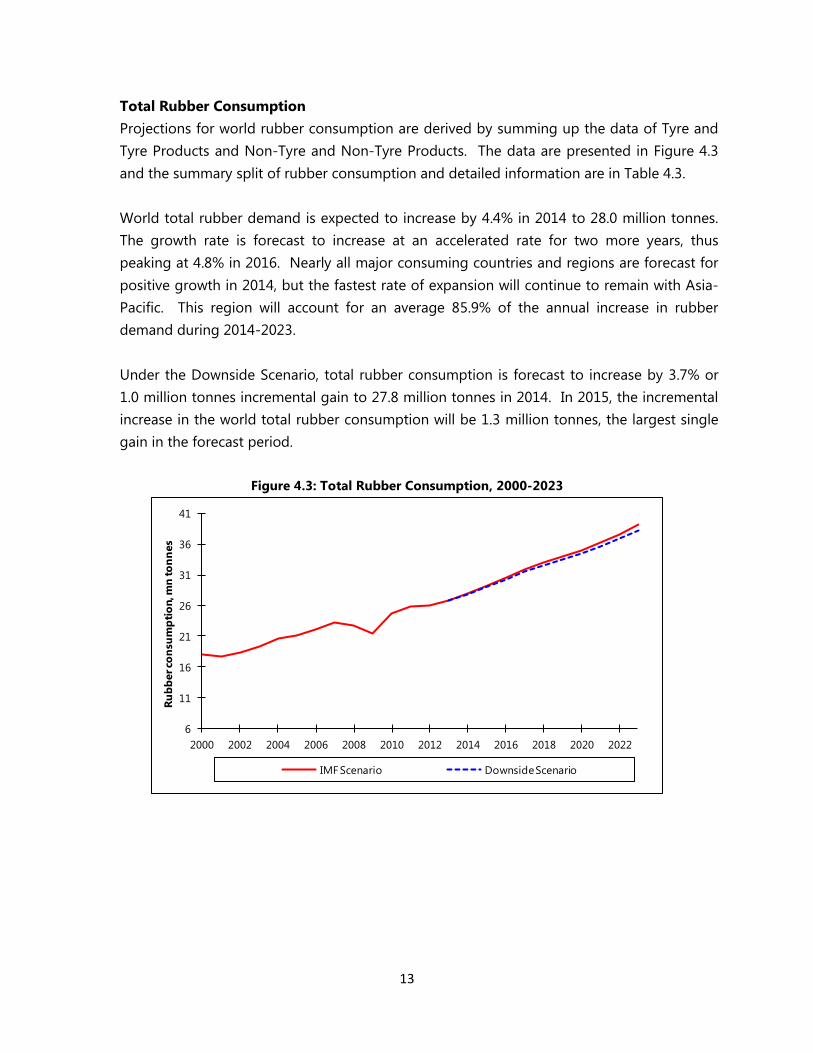

Total Rubber Consumption

Projections for world rubber consumption are derived by summing up the data of Tyre and

Tyre Products and Non-Tyre and Non-Tyre Products. The data are presented in Figure 4.3

and the summary split of rubber consumption and detailed information are in Table 4.3.

World total rubber demand is expected to increase by 4.4% in 2014 to 28.0 million tonnes.

The growth rate is forecast to increase at an accelerated rate for two more years, thus

peaking at 4.8% in 2016. Nearly all major consuming countries and regions are forecast for

positive growth in 2014, but the fastest rate of expansion will continue to remain with Asia-

Pacific. This region will account for an average 85.9% of the annual increase in rubber

demand during 2014-2023.

Under the Downside Scenario, total rubber consumption is forecast to increase by 3.7% or

1.0 million tonnes incremental gain to 27.8 million tonnes in 2014. In 2015, the incremental

increase in the world total rubber consumption will be 1.3 million tonnes, the largest single

gain in the forecast period.

Figure 4.3: Total Rubber Consumption, 2000-2023

6

11

16

21

26

31

36

41

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Ru

bb

er co

nsu

mp

tio

n, m

n to

nn

es

IMF Scenario Downside Scenario

14

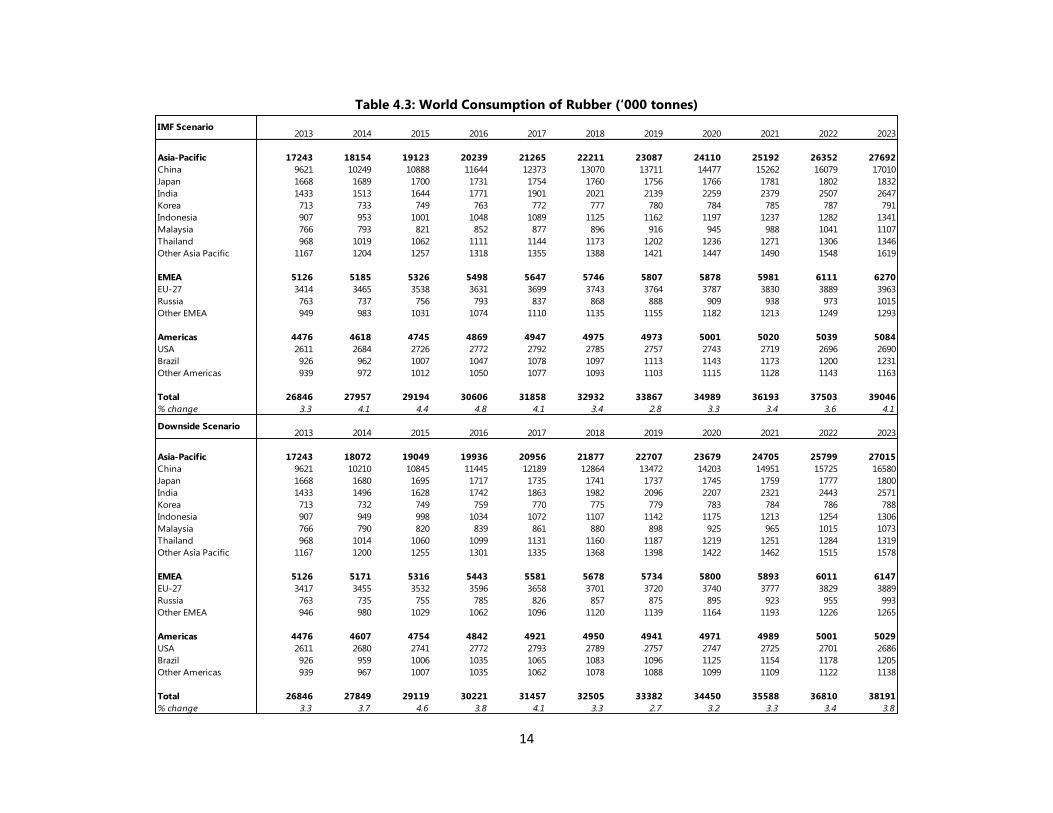

Table 4.3: World Consumption of Rubber (‘000 tonnes)

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 17243 18154 19123 20239 21265 22211 23087 24110 25192 26352 27692

China 9621 10249 10888 11644 12373 13070 13711 14477 15262 16079 17010

Japan 1668 1689 1700 1731 1754 1760 1756 1766 1781 1802 1832

India 1433 1513 1644 1771 1901 2021 2139 2259 2379 2507 2647

Korea 713 733 749 763 772 777 780 784 785 787 791

Indonesia 907 953 1001 1048 1089 1125 1162 1197 1237 1282 1341

Malaysia 766 793 821 852 877 896 916 945 988 1041 1107

Thailand 968 1019 1062 1111 1144 1173 1202 1236 1271 1306 1346

Other Asia Pacific 1167 1204 1257 1318 1355 1388 1421 1447 1490 1548 1619

EMEA 5126 5185 5326 5498 5647 5746 5807 5878 5981 6111 6270

EU-27 3414 3465 3538 3631 3699 3743 3764 3787 3830 3889 3963

Russia 763 737 756 793 837 868 888 909 938 973 1015

Other EMEA 949 983 1031 1074 1110 1135 1155 1182 1213 1249 1293

Americas 4476 4618 4745 4869 4947 4975 4973 5001 5020 5039 5084

USA 2611 2684 2726 2772 2792 2785 2757 2743 2719 2696 2690

Brazil 926 962 1007 1047 1078 1097 1113 1143 1173 1200 1231

Other Americas 939 972 1012 1050 1077 1093 1103 1115 1128 1143 1163

Total 26846 27957 29194 30606 31858 32932 33867 34989 36193 37503 39046

% change 3.3 4.1 4.4 4.8 4.1 3.4 2.8 3.3 3.4 3.6 4.1

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 17243 18072 19049 19936 20956 21877 22707 23679 24705 25799 27015

China 9621 10210 10845 11445 12189 12864 13472 14203 14951 15725 16580

Japan 1668 1680 1695 1717 1735 1741 1737 1745 1759 1777 1800

India 1433 1496 1628 1742 1863 1982 2096 2207 2321 2443 2571

Korea 713 732 749 759 770 775 779 783 784 786 788

Indonesia 907 949 998 1034 1072 1107 1142 1175 1213 1254 1306

Malaysia 766 790 820 839 861 880 898 925 965 1015 1073

Thailand 968 1014 1060 1099 1131 1160 1187 1219 1251 1284 1319

Other Asia Pacific 1167 1200 1255 1301 1335 1368 1398 1422 1462 1515 1578

EMEA 5126 5171 5316 5443 5581 5678 5734 5800 5893 6011 6147

EU-27 3417 3455 3532 3596 3658 3701 3720 3740 3777 3829 3889

Russia 763 735 755 785 826 857 875 895 923 955 993

Other EMEA 946 980 1029 1062 1096 1120 1139 1164 1193 1226 1265

Americas 4476 4607 4754 4842 4921 4950 4941 4971 4989 5001 5029

USA 2611 2680 2741 2772 2793 2789 2757 2747 2725 2701 2686

Brazil 926 959 1006 1035 1065 1083 1096 1125 1154 1178 1205

Other Americas 939 967 1007 1035 1062 1078 1088 1099 1109 1122 1138

Total 26846 27849 29119 30221 31457 32505 33382 34450 35588 36810 38191

% change 3.3 3.7 4.6 3.8 4.1 3.3 2.7 3.2 3.3 3.4 3.8

IMF Scenario

Downside Scenario

15

5 Normal Production of Natural Rubber

New planting and replanting data for natural rubber (NR) for the major countries is being

collected on a continuous basis and the impact on production has been analysed. Using

assumptions on planting policies for the future, the consequences for future NR

production potential have been derived. The analysis makes use of the Vintage approach,

which is a powerful model to analyse the effect of planting decisions on the production

potential for perennial crops. Detailed modelling analyses using the Vintage approach

have been done for eleven countries: Thailand, Indonesia, Malaysia, India, Vietnam, China,

Sri Lanka, Cambodia, Philippines, Myanmar and Laos.

The interaction of supply, demand and prices will be presented in Chapter 6. This will then

lead to projections of natural rubber production in Chapter 7. In this Chapter only

projections of Normal Production are given; these incorporate the latest revisions to

historic planting data and updates on future planting policy information.

Farmers respond to price levels in general and to price changes in particular. The general

assumption is that an increase in price leads to an increment in supply through intensive

tapping while a decrease in price may induce some farmers to tap more intensively to

maintain same level of income. However, a continued price drop can have an effect on

supply through investment decisions. For a crop like natural rubber, low prices may result in

uprooting of trees for the purpose of replanting with natural rubber or with another crop.

The boom and bust cycles of NR prices in the last four years have stimulated farmers to

react to the NR price behaviour in the above mentioned manner. The continued decline in

NR prices during the last two years and a slower than expected recovery in global

demand as well as increased supply has lead to an inventory build up which has created

concerns across the producer community around the world. This continuing bearish

market situation has dampened enthusiasm for some of the new planting projects and

has stimulated discussions on the need for accelerated replanting programmes to control

supply in short-term.

Planting Information: Data Collection and Forecast Assumptions

New planting and replanting data for the major countries are being collected on a

continuous basis and the impact on production has been analysed. Using assumptions on

planting policies for the future, the consequences for future NR production potential have

been derived. The Vintage model approach is used to analyse the effect of planting

decisions on the production potential. Detailed modelling analyses using the Vintage

model approach have been carried out for eleven countries: Thailand, Indonesia, Malaysia,

India, Vietnam, China, Sri Lanka, Cambodia, Philippines, Myanmar and Laos.

16

The interaction of supply, demand and prices will be presented in Chapter 6. This will then

lead to projections of NR production in Chapter 7. In this Chapter only projections of

Normal Production are given; these incorporate the latest revisions to historic planting

data and updates on future planting policy information.

The IRSG Secretariat has validated planting data and reviewed assumptions on the future

planting information across producers in Asia, Africa and Latin America based on the

annual survey conducted in 2014 as well as the latest feedback from stakeholders. The

latest update on planting information covers:

Revisions to the 2012-13 data on total area, new planting and replanting area

across producers.

Revision to Thailand‟s new planting information aligned to the previously

published high planting scenario

Updates to future planting information across other regions and countries.

The future production potential is analysed under a base planting scenario and an

alternative supply control scenario. The alternative supply control scenario premises

accelerated replanting for the largest producer, Thailand and the scenario logic is based

on the following observations:

Additional production capacity from the 2006-09 planted area.

Early opening of the new mature areas compared to the 7 years immaturity period

assumed for traditional rubber growing regions.

Intensive tapping during the high price period (2011-12)

Displacement of migrant tappers back to their counties of origin

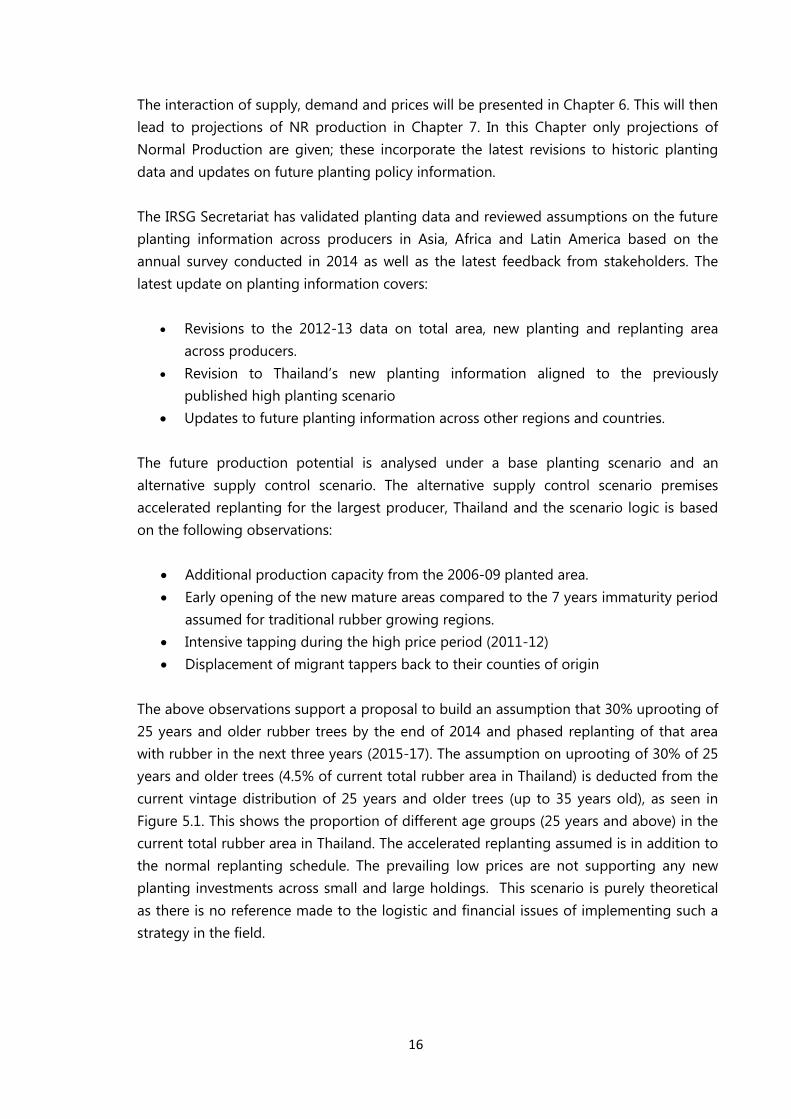

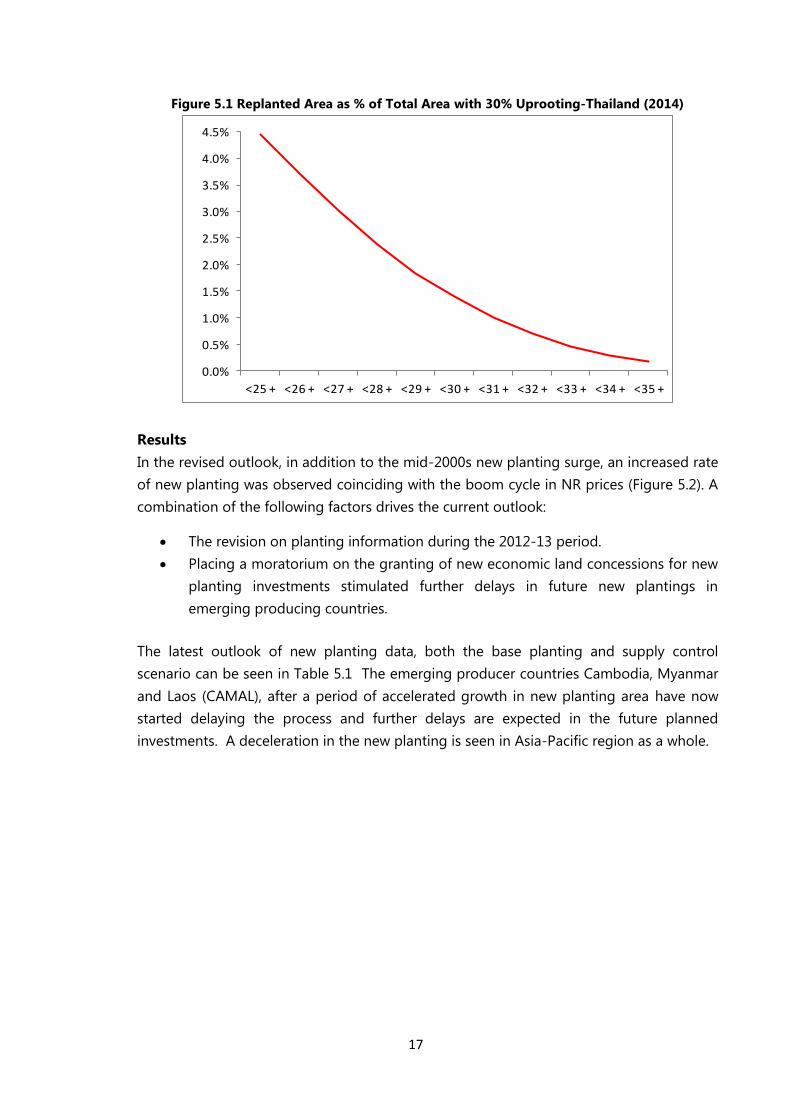

The above observations support a proposal to build an assumption that 30% uprooting of

25 years and older rubber trees by the end of 2014 and phased replanting of that area

with rubber in the next three years (2015-17). The assumption on uprooting of 30% of 25

years and older trees (4.5% of current total rubber area in Thailand) is deducted from the

current vintage distribution of 25 years and older trees (up to 35 years old), as seen in

Figure 5.1. This shows the proportion of different age groups (25 years and above) in the

current total rubber area in Thailand. The accelerated replanting assumed is in addition to

the normal replanting schedule. The prevailing low prices are not supporting any new

planting investments across small and large holdings. This scenario is purely theoretical

as there is no reference made to the logistic and financial issues of implementing such a

strategy in the field.

17

Figure 5.1 Replanted Area as % of Total Area with 30% Uprooting-Thailand (2014)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

<25 + <26 + <27 + <28 + <29 + <30 + <31 + <32 + <33 + <34 + <35 +

Results

In the revised outlook, in addition to the mid-2000s new planting surge, an increased rate

of new planting was observed coinciding with the boom cycle in NR prices (Figure 5.2). A

combination of the following factors drives the current outlook:

The revision on planting information during the 2012-13 period.

Placing a moratorium on the granting of new economic land concessions for new

planting investments stimulated further delays in future new plantings in

emerging producing countries.

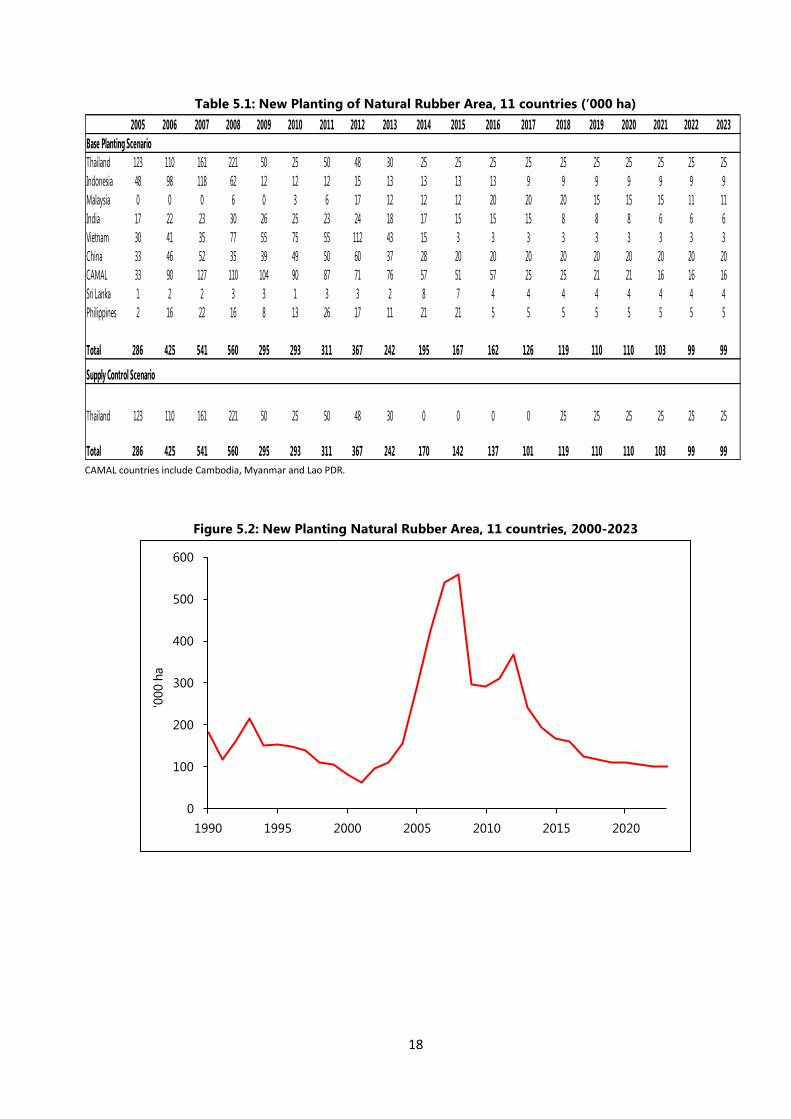

The latest outlook of new planting data, both the base planting and supply control

scenario can be seen in Table 5.1 The emerging producer countries Cambodia, Myanmar

and Laos (CAMAL), after a period of accelerated growth in new planting area have now

started delaying the process and further delays are expected in the future planned

investments. A deceleration in the new planting is seen in Asia-Pacific region as a whole.

18

Table 5.1: New Planting of Natural Rubber Area, 11 countries (‘000 ha)

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Base Planting Scenario

Thailand 123 110 161 221 50 25 50 48 30 25 25 25 25 25 25 25 25 25 25

Indonesia 48 98 118 62 12 12 12 15 13 13 13 13 9 9 9 9 9 9 9

Malaysia 0 0 0 6 0 3 6 17 12 12 12 20 20 20 15 15 15 11 11

India 17 22 23 30 26 25 23 24 18 17 15 15 15 8 8 8 6 6 6

Vietnam 30 41 35 77 55 75 55 112 43 15 3 3 3 3 3 3 3 3 3

China 33 46 52 35 39 49 50 60 37 28 20 20 20 20 20 20 20 20 20

CAMAL 33 90 127 110 104 90 87 71 76 57 51 57 25 25 21 21 16 16 16

Sri Lanka 1 2 2 3 3 1 3 3 2 8 7 4 4 4 4 4 4 4 4

Philippines 2 16 22 16 8 13 26 17 11 21 21 5 5 5 5 5 5 5 5

Total 286 425 541 560 295 293 311 367 242 195 167 162 126 119 110 110 103 99 99

Supply Control Scenario

Thailand 123 110 161 221 50 25 50 48 30 0 0 0 0 25 25 25 25 25 25

Total 286 425 541 560 295 293 311 367 242 170 142 137 101 119 110 110 103 99 99 CAMAL countries include Cambodia, Myanmar and Lao PDR.

Figure 5.2: New Planting Natural Rubber Area, 11 countries, 2000-2023

0

100

200

300

400

500

600

1990 1995 2000 2005 2010 2015 2020

'000 h

a

19

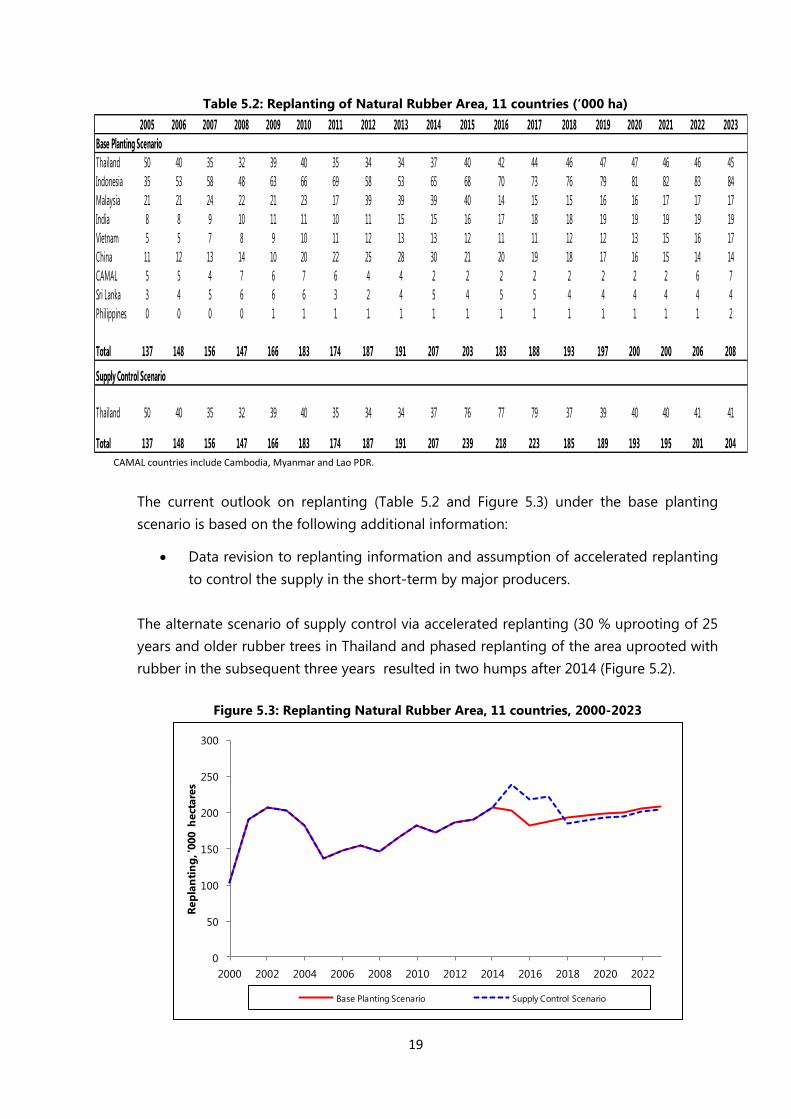

Table 5.2: Replanting of Natural Rubber Area, 11 countries (‘000 ha)

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Base Planting Scenario

Thailand 50 40 35 32 39 40 35 34 34 37 40 42 44 46 47 47 46 46 45

Indonesia 35 53 58 48 63 66 69 58 53 65 68 70 73 76 79 81 82 83 84

Malaysia 21 21 24 22 21 23 17 39 39 39 40 14 15 15 16 16 17 17 17

India 8 8 9 10 11 11 10 11 15 15 16 17 18 18 19 19 19 19 19

Vietnam 5 5 7 8 9 10 11 12 13 13 12 11 11 12 12 13 15 16 17

China 11 12 13 14 10 20 22 25 28 30 21 20 19 18 17 16 15 14 14

CAMAL 5 5 4 7 6 7 6 4 4 2 2 2 2 2 2 2 2 6 7

Sri Lanka 3 4 5 6 6 6 3 2 4 5 4 5 5 4 4 4 4 4 4

Philippines 0 0 0 0 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2

Total 137 148 156 147 166 183 174 187 191 207 203 183 188 193 197 200 200 206 208

Supply Control Scenario

Thailand 50 40 35 32 39 40 35 34 34 37 76 77 79 37 39 40 40 41 41

Total 137 148 156 147 166 183 174 187 191 207 239 218 223 185 189 193 195 201 204 CAMAL countries include Cambodia, Myanmar and Lao PDR.

The current outlook on replanting (Table 5.2 and Figure 5.3) under the base planting

scenario is based on the following additional information:

Data revision to replanting information and assumption of accelerated replanting

to control the supply in the short-term by major producers.

The alternate scenario of supply control via accelerated replanting (30 % uprooting of 25

years and older rubber trees in Thailand and phased replanting of the area uprooted with

rubber in the subsequent three years resulted in two humps after 2014 (Figure 5.2).

Figure 5.3: Replanting Natural Rubber Area, 11 countries, 2000-2023

0

50

100

150

200

250

300

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Rep

lan

tin

g, '

000 h

ect

are

s

Base Planting Scenario Supply Control Scenario

20

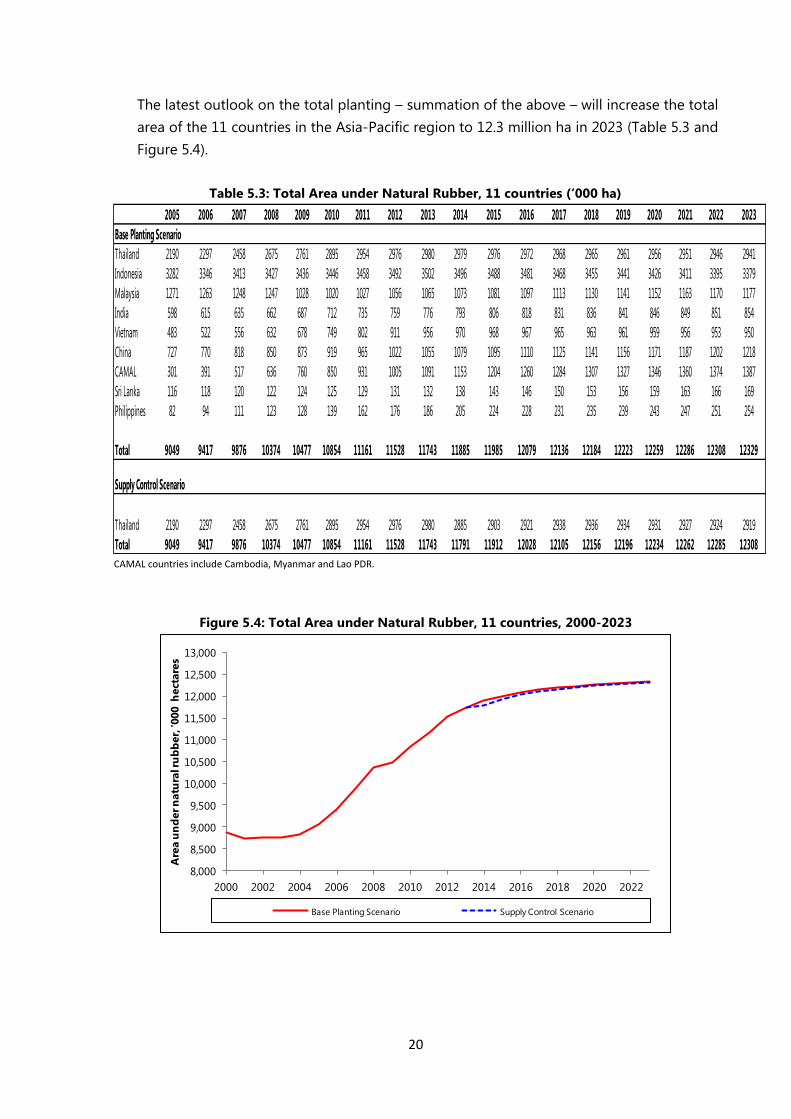

The latest outlook on the total planting – summation of the above – will increase the total

area of the 11 countries in the Asia-Pacific region to 12.3 million ha in 2023 (Table 5.3 and

Figure 5.4).

Table 5.3: Total Area under Natural Rubber, 11 countries (‘000 ha)

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Base Planting Scenario

Thailand 2190 2297 2458 2675 2761 2895 2954 2976 2980 2979 2976 2972 2968 2965 2961 2956 2951 2946 2941

Indonesia 3282 3346 3413 3427 3436 3446 3458 3492 3502 3496 3488 3481 3468 3455 3441 3426 3411 3395 3379

Malaysia 1271 1263 1248 1247 1028 1020 1027 1056 1065 1073 1081 1097 1113 1130 1141 1152 1163 1170 1177

India 598 615 635 662 687 712 735 759 776 793 806 818 831 836 841 846 849 851 854

Vietnam 483 522 556 632 678 749 802 911 956 970 968 967 965 963 961 959 956 953 950

China 727 770 818 850 873 919 965 1022 1055 1079 1095 1110 1125 1141 1156 1171 1187 1202 1218

CAMAL 301 391 517 636 760 850 931 1005 1091 1153 1204 1260 1284 1307 1327 1346 1360 1374 1387

Sri Lanka 116 118 120 122 124 125 129 131 132 138 143 146 150 153 156 159 163 166 169

Philippines 82 94 111 123 128 139 162 176 186 205 224 228 231 235 239 243 247 251 254

Total 9049 9417 9876 10374 10477 10854 11161 11528 11743 11885 11985 12079 12136 12184 12223 12259 12286 12308 12329

Supply Control Scenario

Thailand 2190 2297 2458 2675 2761 2895 2954 2976 2980 2885 2903 2921 2938 2936 2934 2931 2927 2924 2919

Total 9049 9417 9876 10374 10477 10854 11161 11528 11743 11791 11912 12028 12105 12156 12196 12234 12262 12285 12308 CAMAL countries include Cambodia, Myanmar and Lao PDR.

Figure 5.4: Total Area under Natural Rubber, 11 countries, 2000-2023

8,000

8,500

9,000

9,500

10,000

10,500

11,000

11,500

12,000

12,500

13,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Are

a u

nd

er n

atu

ral r

ub

ber,

'000 h

ect

are

s

Base Planting Scenario Supply Control Scenario

21

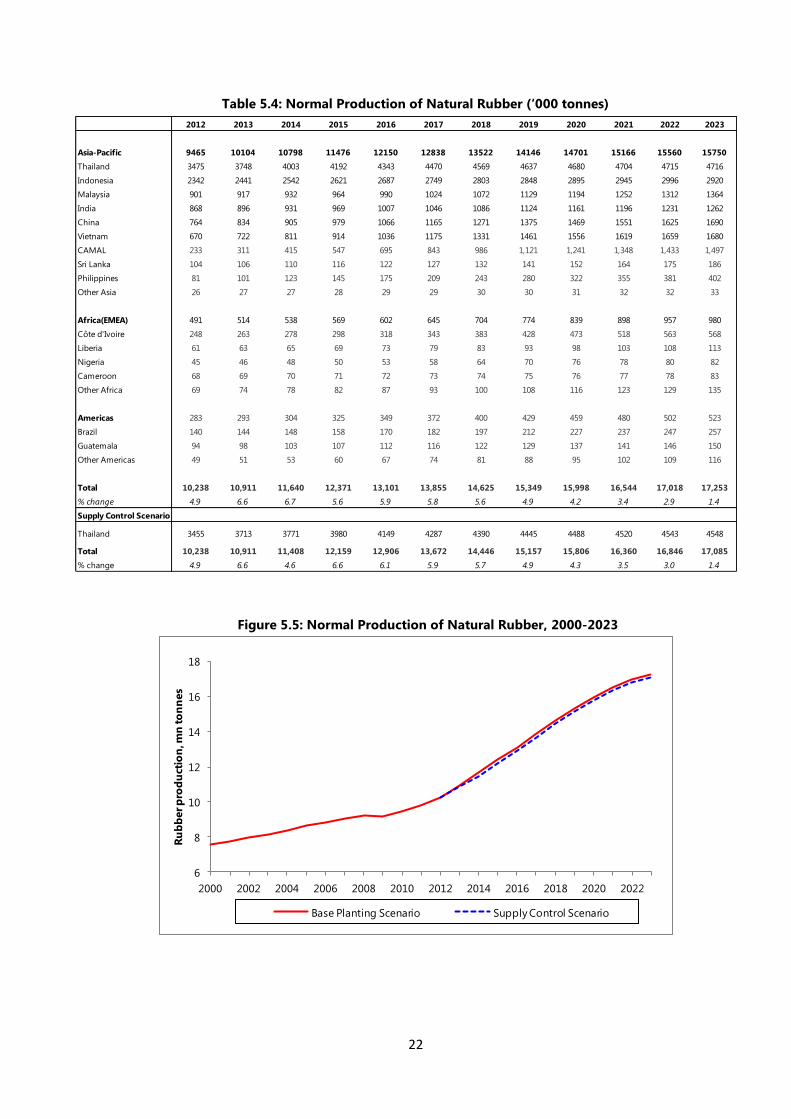

Results – Normal Production

The outlook for the Normal Production has been driven by the following key assumptions

and additional information:

Acceptance of developments in total planting and total area under rubber as

discussed above

The Normal Production data are shown in Table 5.4 and Figure 5.5. Under the base planting

scenario, the Normal Production is expected to increase by 6.6% in 2014, 6.7% in 2015 and by

a further 5.6% in 2016 (Table 5.4). The Normal Production forecast is expected to reach 17.3

million tonnes of NR in 2023.

Under the supply control scenario, via uprooting 30% of 25 years and older trees in 2014 and

replanting that in the subsequent three years, the Normal production forecast is expected to

reach 17.1 million tonnes in 2023.

22

Table 5.4: Normal Production of Natural Rubber (‘000 tonnes)

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 9465 10104 10798 11476 12150 12838 13522 14146 14701 15166 15560 15750

Thailand 3475 3748 4003 4192 4343 4470 4569 4637 4680 4704 4715 4716

Indonesia 2342 2441 2542 2621 2687 2749 2803 2848 2895 2945 2996 2920

Malaysia 901 917 932 964 990 1024 1072 1129 1194 1252 1312 1364

India 868 896 931 969 1007 1046 1086 1124 1161 1196 1231 1262

China 764 834 905 979 1066 1165 1271 1375 1469 1551 1625 1690

Vietnam 670 722 811 914 1036 1175 1331 1461 1556 1619 1659 1680

CAMAL 233 311 415 547 695 843 986 1,121 1,241 1,348 1,433 1,497

Sri Lanka 104 106 110 116 122 127 132 141 152 164 175 186

Philippines 81 101 123 145 175 209 243 280 322 355 381 402

Other Asia 26 27 27 28 29 29 30 30 31 32 32 33

Africa(EMEA) 491 514 538 569 602 645 704 774 839 898 957 980

Côte d'Ivoire 248 263 278 298 318 343 383 428 473 518 563 568

Liberia 61 63 65 69 73 79 83 93 98 103 108 113

Nigeria 45 46 48 50 53 58 64 70 76 78 80 82

Cameroon 68 69 70 71 72 73 74 75 76 77 78 83

Other Africa 69 74 78 82 87 93 100 108 116 123 129 135

Americas 283 293 304 325 349 372 400 429 459 480 502 523

Brazil 140 144 148 158 170 182 197 212 227 237 247 257

Guatemala 94 98 103 107 112 116 122 129 137 141 146 150

Other Americas 49 51 53 60 67 74 81 88 95 102 109 116

Total 10,238 10,911 11,640 12,371 13,101 13,855 14,625 15,349 15,998 16,544 17,018 17,253

% change 4.9 6.6 6.7 5.6 5.9 5.8 5.6 4.9 4.2 3.4 2.9 1.4

Supply Control Scenario

Thailand 3455 3713 3771 3980 4149 4287 4390 4445 4488 4520 4543 4548

Total 10,238 10,911 11,408 12,159 12,906 13,672 14,446 15,157 15,806 16,360 16,846 17,085

% change 4.9 6.6 4.6 6.6 6.1 5.9 5.7 4.9 4.3 3.5 3.0 1.4

Figure 5.5: Normal Production of Natural Rubber, 2000-2023

6

8

10

12

14

16

18

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Ru

bb

er p

rod

uct

ion

, mn

to

nn

es

Base Planting Scenario Supply Control Scenario

23

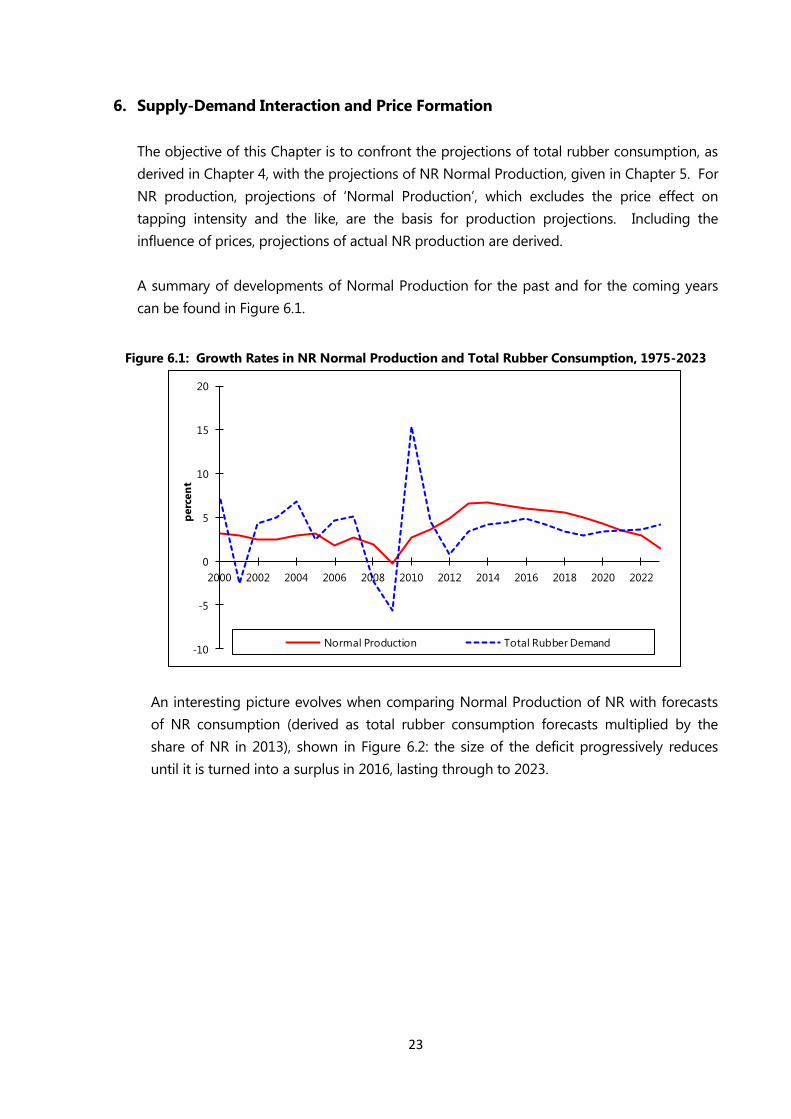

6. Supply-Demand Interaction and Price Formation

The objective of this Chapter is to confront the projections of total rubber consumption, as

derived in Chapter 4, with the projections of NR Normal Production, given in Chapter 5. For

NR production, projections of „Normal Production‟, which excludes the price effect on

tapping intensity and the like, are the basis for production projections. Including the

influence of prices, projections of actual NR production are derived.

A summary of developments of Normal Production for the past and for the coming years

can be found in Figure 6.1.

Figure 6.1: Growth Rates in NR Normal Production and Total Rubber Consumption, 1975-2023

-10

-5

0

5

10

15

20

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

perc

en

t

Normal Production Total Rubber Demand

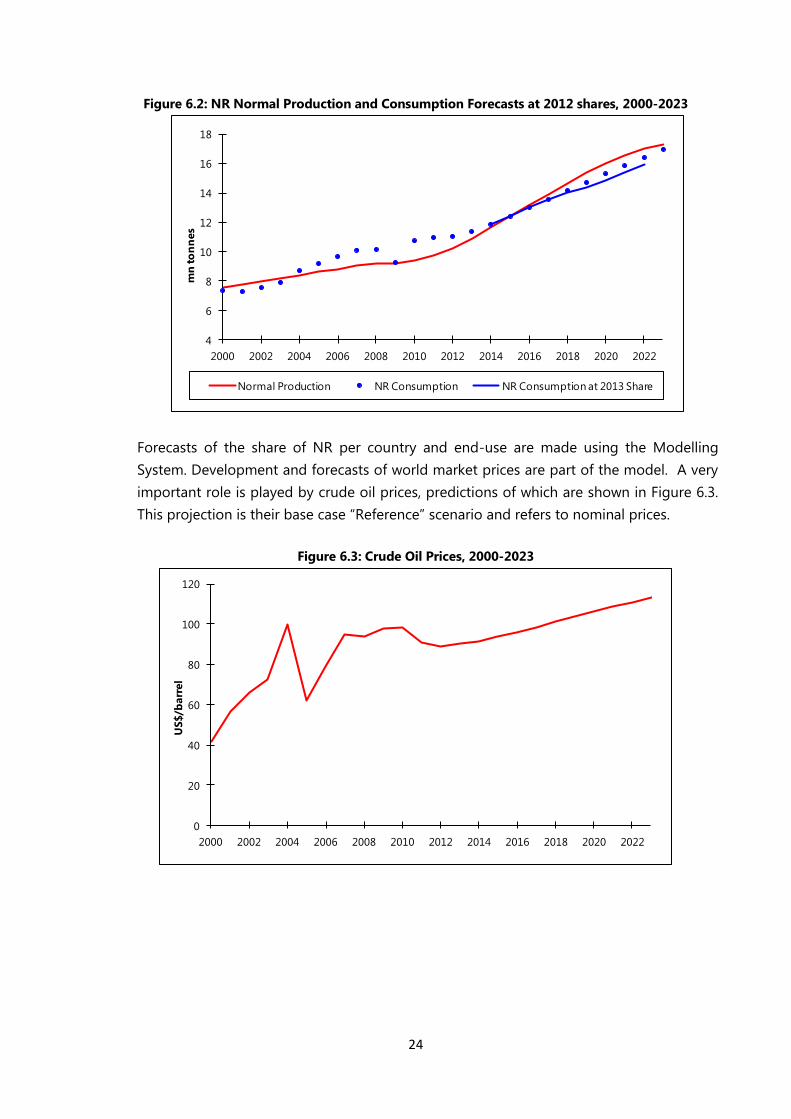

An interesting picture evolves when comparing Normal Production of NR with forecasts

of NR consumption (derived as total rubber consumption forecasts multiplied by the

share of NR in 2013), shown in Figure 6.2: the size of the deficit progressively reduces

until it is turned into a surplus in 2016, lasting through to 2023.

24

Figure 6.2: NR Normal Production and Consumption Forecasts at 2012 shares, 2000-2023

4

6

8

10

12

14

16

18

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

mn

to

nn

es

Normal Production NR Consumption NR Consumption at 2013 Share

Forecasts of the share of NR per country and end-use are made using the Modelling

System. Development and forecasts of world market prices are part of the model. A very

important role is played by crude oil prices, predictions of which are shown in Figure 6.3.

This projection is their base case “Reference” scenario and refers to nominal prices.

Figure 6.3: Crude Oil Prices, 2000-2023

0

20

40

60

80

100

120

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

US$/b

arr

el

25

Prices of feedstocks for SR have historically been closely related to oil prices. Data and

projections for butadiene and styrene are derived, acting as a basis for forecasting the

price of Styrene Butadiene Rubber (SBR), which is the central price component in the

analysis on the SR side. The US export unit value of SBR is used to represent the indirect

price. Projections are derived for the price of SBR partly in interaction with the price of

NR. The NR price is to a large extent determined by the equilibrium between demand

and supply of NR. The IRSG is not allowed to publish absolute price forecasts. The ratio of

the NR price and the SR price has some influence on projections of developments in the

share of NR and SR in total rubber consumption by country and by end-use.

Synthetic Rubber Production

In 2008 the price of SR and its primary feedstock, butadiene, climbed to their historic

highs. While much of the increase in the price was due to the general increase in crude

oil, a significant part could be laid at the door step of decreased availability of C4. While

the global petrochemical industry and specifically the SR production is well served with

surplus butadiene extraction capacity, which is relatively and absolutely increasing, the

supply of available C4 from the cracker is not as the industry switched to lighter

feedstocks.

The pressure on the supply of C4 and subsequently on the supply of butadiene comes

from the fact that it is a by-product of the petrochemical cracking industry, which is driven

by the needs of the polyethylene and polypropylene industries for ethylene and

propylene. In the most recent past, the two most noticeable features of the cracking

industry have been the rise of the Middle East and the rejuvenation of the US cracking

industry based on cheap natural gas. Both regional cracking industries are based on gas

as feedstock, with the US cracking industry using shale gas. This lighter feedstock, whilst

producing more ethylene and propylene, however results in lower C4 output. The US is

structurally short of butadiene and the further move to shale gas would further

exacerbate the butadiene supply position. The significance of the increased Middle East

cracker capacity is that economics and geography could drive some laggard European

crackers to close. Mainly naphtha based, the loss of such Europe based crackers would

add to the diminishing supply of C4 and add to the global reduction in its availability.

While a number of crackers have closed in Europe, none appear as yet to have been

attributed to economic pressure from the gas fed Middle East crackers. Despite this,

many within the industry are of the opinion that European closures are inevitable,

although and the size and the timing it is open to speculation.

The Secretariat still assumes that the SR manufacturers will meet the needs of the

industry, rationally planning future “on-purpose” butadiene investments and as such the

availability of butadiene will remain sufficient to meet future demand.

26

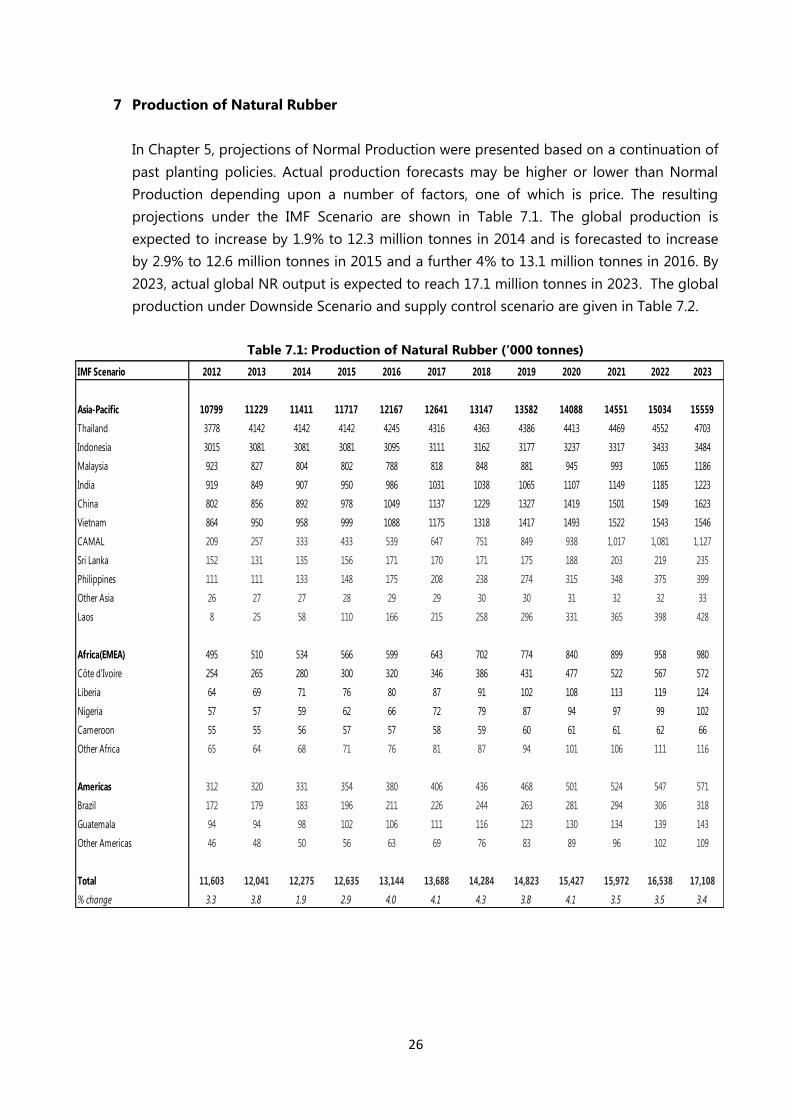

7 Production of Natural Rubber

In Chapter 5, projections of Normal Production were presented based on a continuation of

past planting policies. Actual production forecasts may be higher or lower than Normal

Production depending upon a number of factors, one of which is price. The resulting

projections under the IMF Scenario are shown in Table 7.1. The global production is

expected to increase by 1.9% to 12.3 million tonnes in 2014 and is forecasted to increase

by 2.9% to 12.6 million tonnes in 2015 and a further 4% to 13.1 million tonnes in 2016. By

2023, actual global NR output is expected to reach 17.1 million tonnes in 2023. The global

production under Downside Scenario and supply control scenario are given in Table 7.2.

Table 7.1: Production of Natural Rubber (‘000 tonnes)

IMF Scenario 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 10799 11229 11411 11717 12167 12641 13147 13582 14088 14551 15034 15559

Thailand 3778 4142 4142 4142 4245 4316 4363 4386 4413 4469 4552 4703

Indonesia 3015 3081 3081 3081 3095 3111 3162 3177 3237 3317 3433 3484

Malaysia 923 827 804 802 788 818 848 881 945 993 1065 1186

India 919 849 907 950 986 1031 1038 1065 1107 1149 1185 1223

China 802 856 892 978 1049 1137 1229 1327 1419 1501 1549 1623

Vietnam 864 950 958 999 1088 1175 1318 1417 1493 1522 1543 1546

CAMAL 209 257 333 433 539 647 751 849 938 1,017 1,081 1,127

Sri Lanka 152 131 135 156 171 170 171 175 188 203 219 235

Philippines 111 111 133 148 175 208 238 274 315 348 375 399

Other Asia 26 27 27 28 29 29 30 30 31 32 32 33

Laos 8 25 58 110 166 215 258 296 331 365 398 428

Africa(EMEA) 495 510 534 566 599 643 702 774 840 899 958 980

Côte d'Ivoire 254 265 280 300 320 346 386 431 477 522 567 572

Liberia 64 69 71 76 80 87 91 102 108 113 119 124

Nigeria 57 57 59 62 66 72 79 87 94 97 99 102

Cameroon 55 55 56 57 57 58 59 60 61 61 62 66

Other Africa 65 64 68 71 76 81 87 94 101 106 111 116

Americas 312 320 331 354 380 406 436 468 501 524 547 571

Brazil 172 179 183 196 211 226 244 263 281 294 306 318

Guatemala 94 94 98 102 106 111 116 123 130 134 139 143

Other Americas 46 48 50 56 63 69 76 83 89 96 102 109

Total 11,603 12,041 12,275 12,635 13,144 13,688 14,284 14,823 15,427 15,972 16,538 17,108

% change 3.3 3.8 1.9 2.9 4.0 4.1 4.3 3.8 4.1 3.5 3.5 3.4

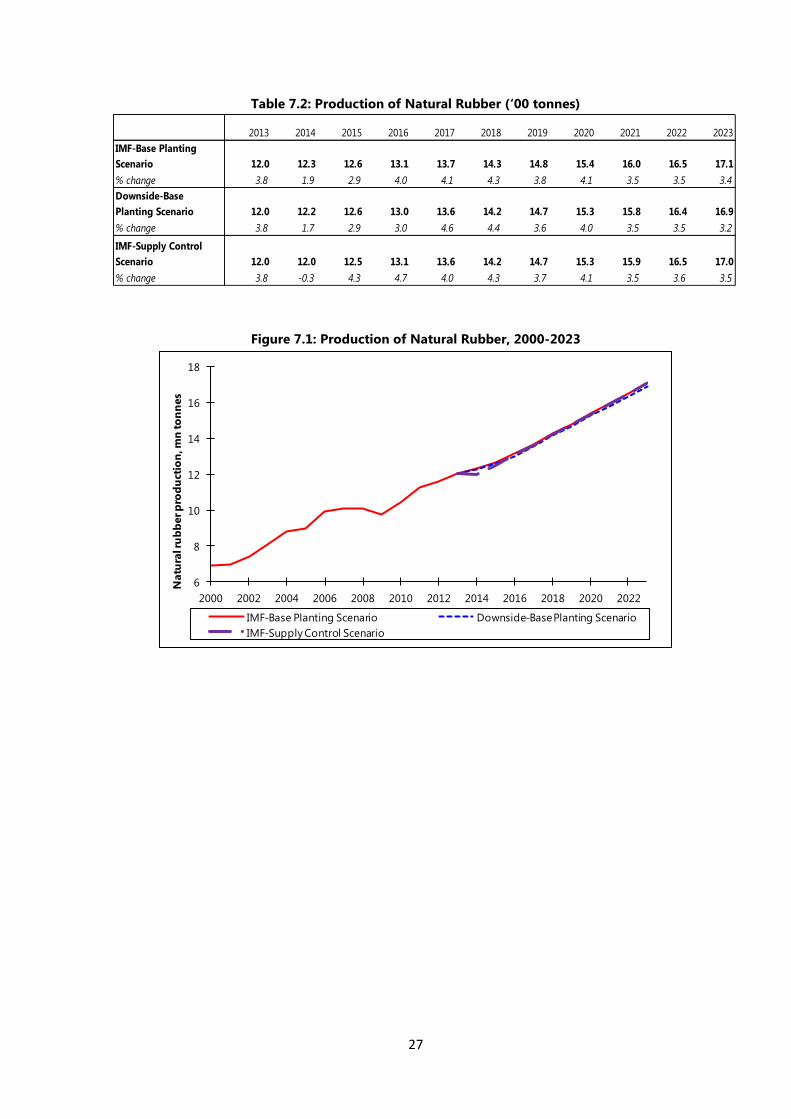

27

Table 7.2: Production of Natural Rubber (‘00 tonnes)

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

IMF-Base Planting

Scenario 12.0 12.3 12.6 13.1 13.7 14.3 14.8 15.4 16.0 16.5 17.1

% change 3.8 1.9 2.9 4.0 4.1 4.3 3.8 4.1 3.5 3.5 3.4

Downside-Base

Planting Scenario 12.0 12.2 12.6 13.0 13.6 14.2 14.7 15.3 15.8 16.4 16.9

% change 3.8 1.7 2.9 3.0 4.6 4.4 3.6 4.0 3.5 3.5 3.2

IMF-Supply Control

Scenario 12.0 12.0 12.5 13.1 13.6 14.2 14.7 15.3 15.9 16.5 17.0

% change 3.8 -0.3 4.3 4.7 4.0 4.3 3.7 4.1 3.5 3.6 3.5

Figure 7.1: Production of Natural Rubber, 2000-2023

6

8

10

12

14

16

18

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Natu

ral r

ub

ber p

rod

uct

ion

, mn

to

nn

es

IMF-Base Planting Scenario Downside-Base Planting Scenario

IMF-Supply Control Scenario

28

8 Consumption of Natural Rubber and Synthetic Rubber

The focus of this Chapter is to present projections of NR and SR consumption for Tyre and

Tyre Products and Non-Tyre and Non-Tyre Products, splitting the total rubber consumption

that was presented in Chapter 4.

In this Chapter, the impact of the third scenario – High Planting – on rubber demand will be

also introduced along side the Downside Scenario. The results of High Planting Scenario will

be confined to the world total.

The High Planting Scenario on rubber demand is limited to a price substitution effect only on

the relative NR-SR demand. Thus, the volume and the growth rate of total rubber will not be

affected. Demand for NR under IMF-High Planting Scenario and Downside-High Planting

Scenario will increase at faster rates than their respective counterparts for nearly all years of

the forecast period. This assessment also applies to the two sub-component NR demands of

Tyre and Tyre Products and Non-Tyre and Non-Tyre Products.

Consumption of Natural Rubber by Tyre and Tyre Products

The outlook for the NR consumption by the Tyre and Tyre Products has been driven by these

following additional, specific key assumptions:

No technology or legislation will be introduced within the 2014-2023 period that

will alter the current NR ratios of its own accord;

Producer status driven NR ratios will not be altered for any country in 2012-2023;

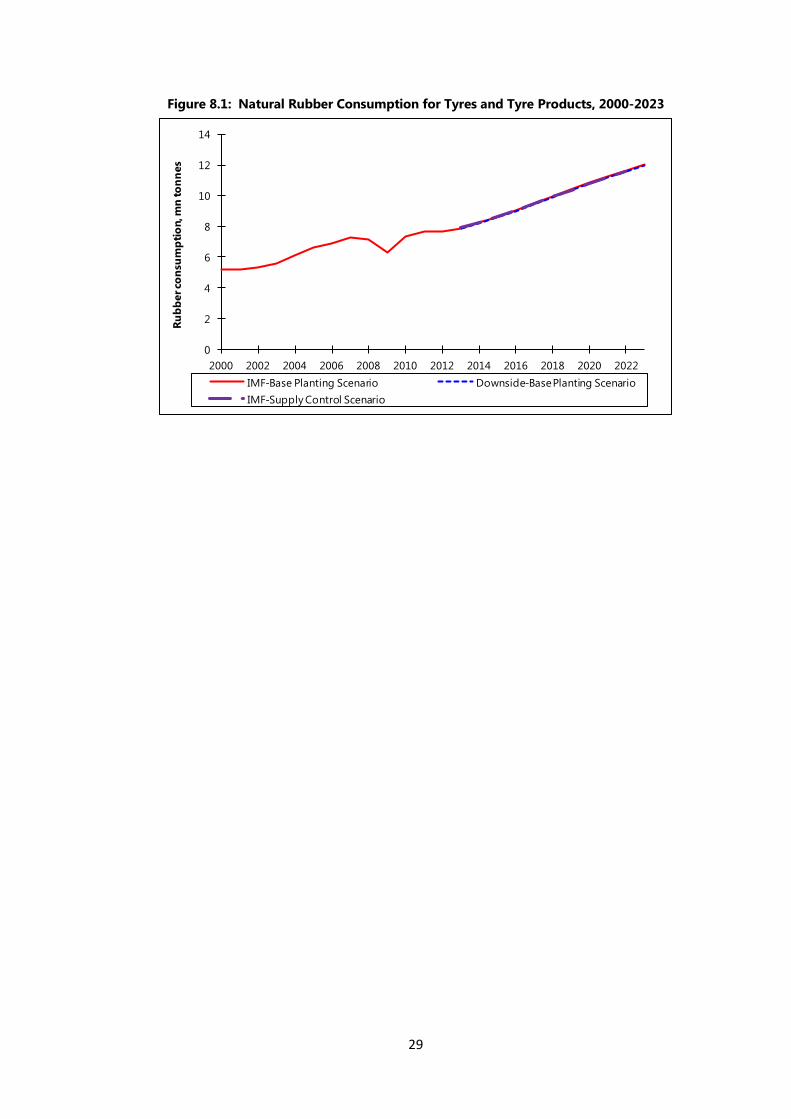

The world NR demand is forecast to increase by 4.5% in 2014 and by 4.7% in 2015, under the

IMF Scenario. The volume of demand will be 8.2 million tonnes and 8.6 million tonnes,

respectively. By 2023, the NR demand is forecast to be 12.0 million tonnes. The forecast

growth rates of NR demand is lower than total rubber demand by Tyre and Tyre Products in

2014-2017. This is due mainly to China and India, which are forecast to reduce their

proportion of NR demand, reflecting the two countries‟ SR capacity build-up.

Under the Downside Scenario, the NR demand is forecast to grow by 4.0% in 2014 and by

4.7% in 2015. The full impact of the slowdown in the global economic growth rate seen on

the global rubber is cushioned for NR demand in 2014 due to the relative rubber price level.

The subsequent recovery in 2014-2018, is forecast to increase at a faster rate than that under

the IMF Scenario due mainly to the deteriorated relative price level.

Projections for NR consumptions by Tyre and Tyre Products are presented in Figure 8.1 and

Table 8.1, including the IMF-Supply Control Scenario, which is shown only for the world total.

29

Figure 8.1: Natural Rubber Consumption for Tyres and Tyre Products, 2000-2023

0

2

4

6

8

10

12

14

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Ru

bb

er co

nsu

mp

tio

n, m

n to

nn

es

IMF-Base Planting Scenario Downside-Base Planting Scenario

IMF-Supply Control Scenario

30

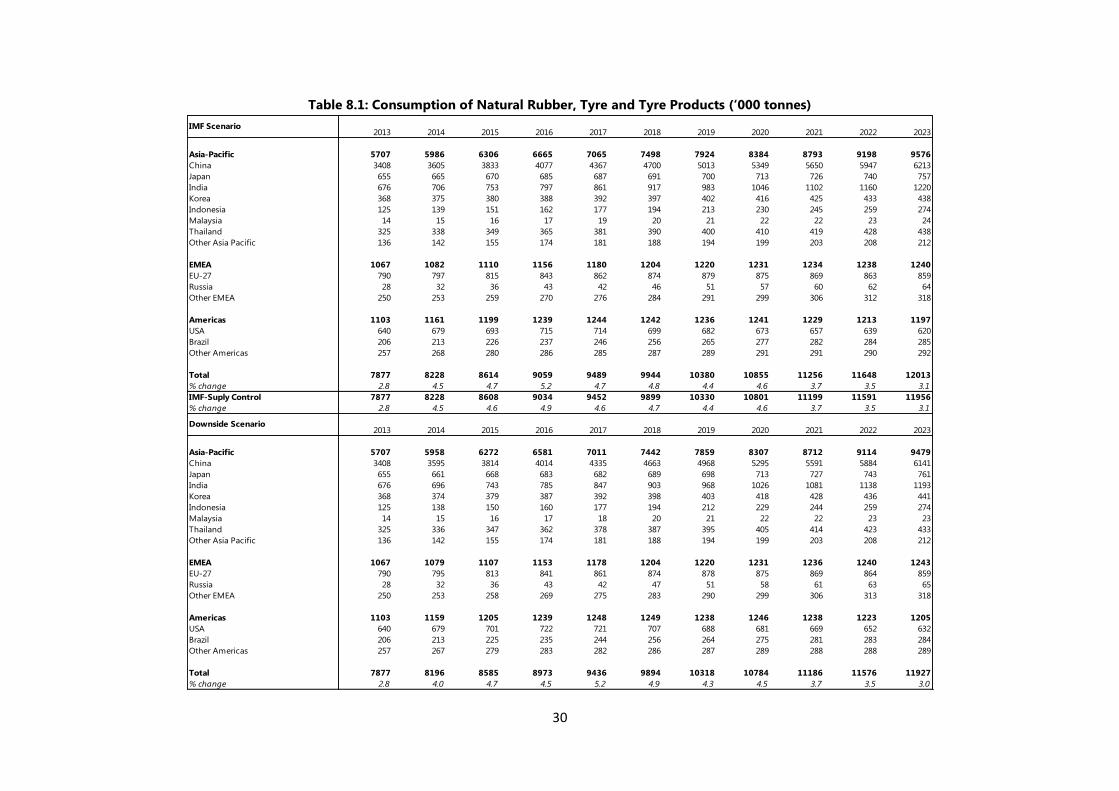

Table 8.1: Consumption of Natural Rubber, Tyre and Tyre Products (‘000 tonnes)

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 5707 5986 6306 6665 7065 7498 7924 8384 8793 9198 9576

China 3408 3605 3833 4077 4367 4700 5013 5349 5650 5947 6213

Japan 655 665 670 685 687 691 700 713 726 740 757

India 676 706 753 797 861 917 983 1046 1102 1160 1220

Korea 368 375 380 388 392 397 402 416 425 433 438

Indonesia 125 139 151 162 177 194 213 230 245 259 274

Malaysia 14 15 16 17 19 20 21 22 22 23 24

Thailand 325 338 349 365 381 390 400 410 419 428 438

Other Asia Pacific 136 142 155 174 181 188 194 199 203 208 212

EMEA 1067 1082 1110 1156 1180 1204 1220 1231 1234 1238 1240

EU-27 790 797 815 843 862 874 879 875 869 863 859

Russia 28 32 36 43 42 46 51 57 60 62 64

Other EMEA 250 253 259 270 276 284 291 299 306 312 318

Americas 1103 1161 1199 1239 1244 1242 1236 1241 1229 1213 1197

USA 640 679 693 715 714 699 682 673 657 639 620

Brazil 206 213 226 237 246 256 265 277 282 284 285

Other Americas 257 268 280 286 285 287 289 291 291 290 292

Total 7877 8228 8614 9059 9489 9944 10380 10855 11256 11648 12013

% change 2.8 4.5 4.7 5.2 4.7 4.8 4.4 4.6 3.7 3.5 3.1

IMF-Suply Control 7877 8228 8608 9034 9452 9899 10330 10801 11199 11591 11956

% change 2.8 4.5 4.6 4.9 4.6 4.7 4.4 4.6 3.7 3.5 3.1

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 5707 5958 6272 6581 7011 7442 7859 8307 8712 9114 9479

China 3408 3595 3814 4014 4335 4663 4968 5295 5591 5884 6141

Japan 655 661 668 683 682 689 698 713 727 743 761

India 676 696 743 785 847 903 968 1026 1081 1138 1193

Korea 368 374 379 387 392 398 403 418 428 436 441

Indonesia 125 138 150 160 177 194 212 229 244 259 274

Malaysia 14 15 16 17 18 20 21 22 22 23 23

Thailand 325 336 347 362 378 387 395 405 414 423 433

Other Asia Pacific 136 142 155 174 181 188 194 199 203 208 212

EMEA 1067 1079 1107 1153 1178 1204 1220 1231 1236 1240 1243

EU-27 790 795 813 841 861 874 878 875 869 864 859

Russia 28 32 36 43 42 47 51 58 61 63 65

Other EMEA 250 253 258 269 275 283 290 299 306 313 318

Americas 1103 1159 1205 1239 1248 1249 1238 1246 1238 1223 1205

USA 640 679 701 722 721 707 688 681 669 652 632

Brazil 206 213 225 235 244 256 264 275 281 283 284

Other Americas 257 267 279 283 282 286 287 289 288 288 289

Total 7877 8196 8585 8973 9436 9894 10318 10784 11186 11576 11927

% change 2.8 4.0 4.7 4.5 5.2 4.9 4.3 4.5 3.7 3.5 3.0

IMF Scenario

Downside Scenario

31

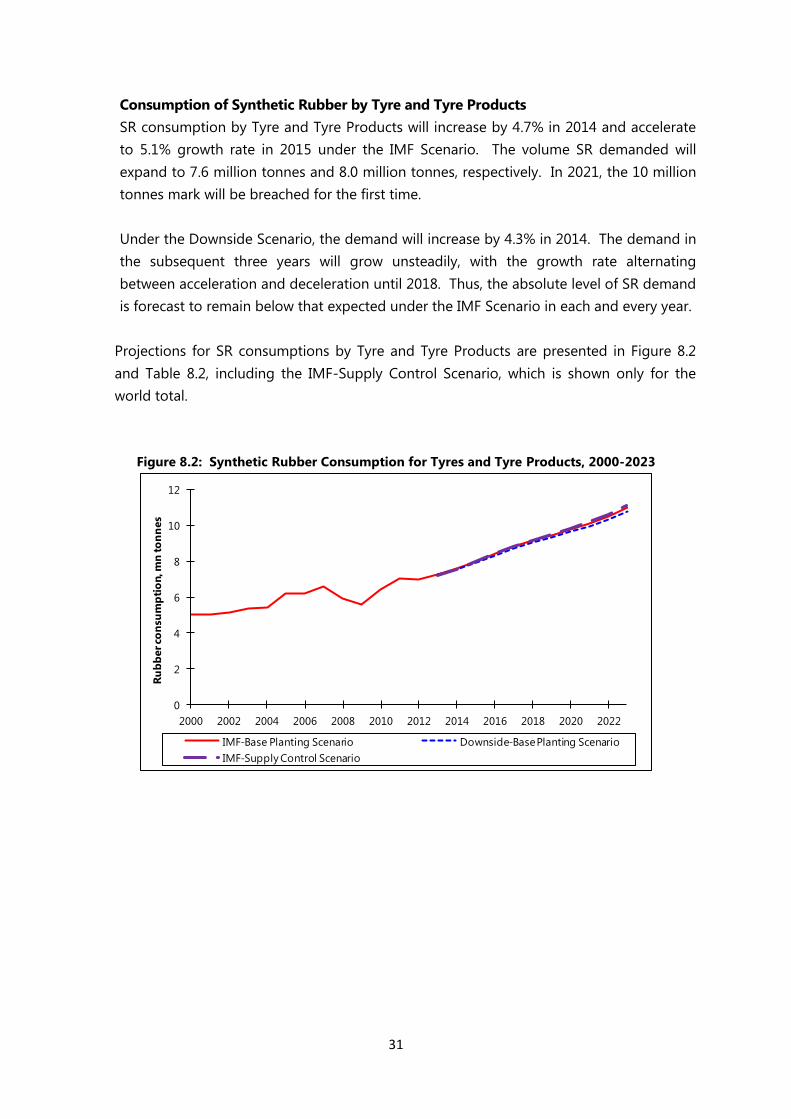

Consumption of Synthetic Rubber by Tyre and Tyre Products

SR consumption by Tyre and Tyre Products will increase by 4.7% in 2014 and accelerate

to 5.1% growth rate in 2015 under the IMF Scenario. The volume SR demanded will

expand to 7.6 million tonnes and 8.0 million tonnes, respectively. In 2021, the 10 million

tonnes mark will be breached for the first time.

Under the Downside Scenario, the demand will increase by 4.3% in 2014. The demand in

the subsequent three years will grow unsteadily, with the growth rate alternating

between acceleration and deceleration until 2018. Thus, the absolute level of SR demand

is forecast to remain below that expected under the IMF Scenario in each and every year.

Projections for SR consumptions by Tyre and Tyre Products are presented in Figure 8.2

and Table 8.2, including the IMF-Supply Control Scenario, which is shown only for the

world total.

Figure 8.2: Synthetic Rubber Consumption for Tyres and Tyre Products, 2000-2023

0

2

4

6

8

10

12

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Ru

bb

er co

nsu

mp

tio

n, m

n to

nn

es

IMF-Base Planting Scenario Downside-Base Planting Scenario

IMF-Supply Control Scenario

32

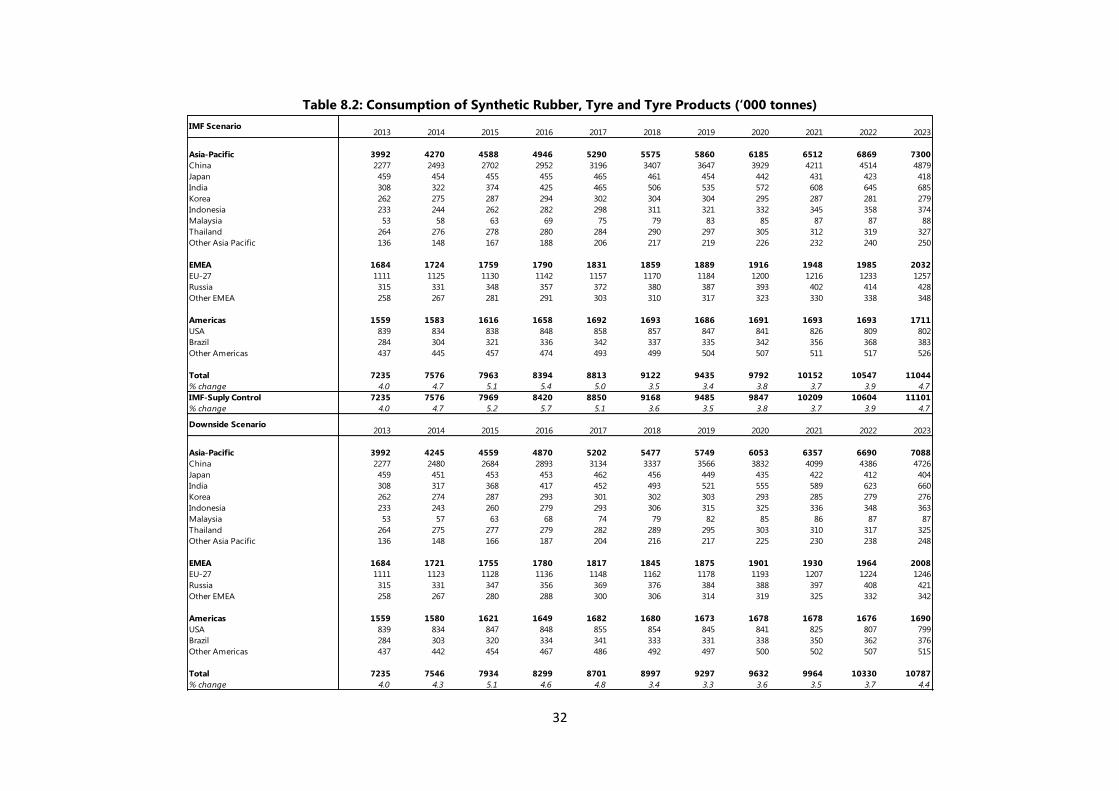

Table 8.2: Consumption of Synthetic Rubber, Tyre and Tyre Products (‘000 tonnes)

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 3992 4270 4588 4946 5290 5575 5860 6185 6512 6869 7300

China 2277 2493 2702 2952 3196 3407 3647 3929 4211 4514 4879

Japan 459 454 455 455 465 461 454 442 431 423 418

India 308 322 374 425 465 506 535 572 608 645 685

Korea 262 275 287 294 302 304 304 295 287 281 279

Indonesia 233 244 262 282 298 311 321 332 345 358 374

Malaysia 53 58 63 69 75 79 83 85 87 87 88

Thailand 264 276 278 280 284 290 297 305 312 319 327

Other Asia Pacific 136 148 167 188 206 217 219 226 232 240 250

EMEA 1684 1724 1759 1790 1831 1859 1889 1916 1948 1985 2032

EU-27 1111 1125 1130 1142 1157 1170 1184 1200 1216 1233 1257

Russia 315 331 348 357 372 380 387 393 402 414 428

Other EMEA 258 267 281 291 303 310 317 323 330 338 348

Americas 1559 1583 1616 1658 1692 1693 1686 1691 1693 1693 1711

USA 839 834 838 848 858 857 847 841 826 809 802

Brazil 284 304 321 336 342 337 335 342 356 368 383

Other Americas 437 445 457 474 493 499 504 507 511 517 526

Total 7235 7576 7963 8394 8813 9122 9435 9792 10152 10547 11044

% change 4.0 4.7 5.1 5.4 5.0 3.5 3.4 3.8 3.7 3.9 4.7

IMF-Suply Control 7235 7576 7969 8420 8850 9168 9485 9847 10209 10604 11101

% change 4.0 4.7 5.2 5.7 5.1 3.6 3.5 3.8 3.7 3.9 4.7

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 3992 4245 4559 4870 5202 5477 5749 6053 6357 6690 7088

China 2277 2480 2684 2893 3134 3337 3566 3832 4099 4386 4726

Japan 459 451 453 453 462 456 449 435 422 412 404

India 308 317 368 417 452 493 521 555 589 623 660

Korea 262 274 287 293 301 302 303 293 285 279 276

Indonesia 233 243 260 279 293 306 315 325 336 348 363

Malaysia 53 57 63 68 74 79 82 85 86 87 87

Thailand 264 275 277 279 282 289 295 303 310 317 325

Other Asia Pacific 136 148 166 187 204 216 217 225 230 238 248

EMEA 1684 1721 1755 1780 1817 1845 1875 1901 1930 1964 2008

EU-27 1111 1123 1128 1136 1148 1162 1178 1193 1207 1224 1246

Russia 315 331 347 356 369 376 384 388 397 408 421

Other EMEA 258 267 280 288 300 306 314 319 325 332 342

Americas 1559 1580 1621 1649 1682 1680 1673 1678 1678 1676 1690

USA 839 834 847 848 855 854 845 841 825 807 799

Brazil 284 303 320 334 341 333 331 338 350 362 376

Other Americas 437 442 454 467 486 492 497 500 502 507 515

Total 7235 7546 7934 8299 8701 8997 9297 9632 9964 10330 10787

% change 4.0 4.3 5.1 4.6 4.8 3.4 3.3 3.6 3.5 3.7 4.4

IMF Scenario

Downside Scenario

33

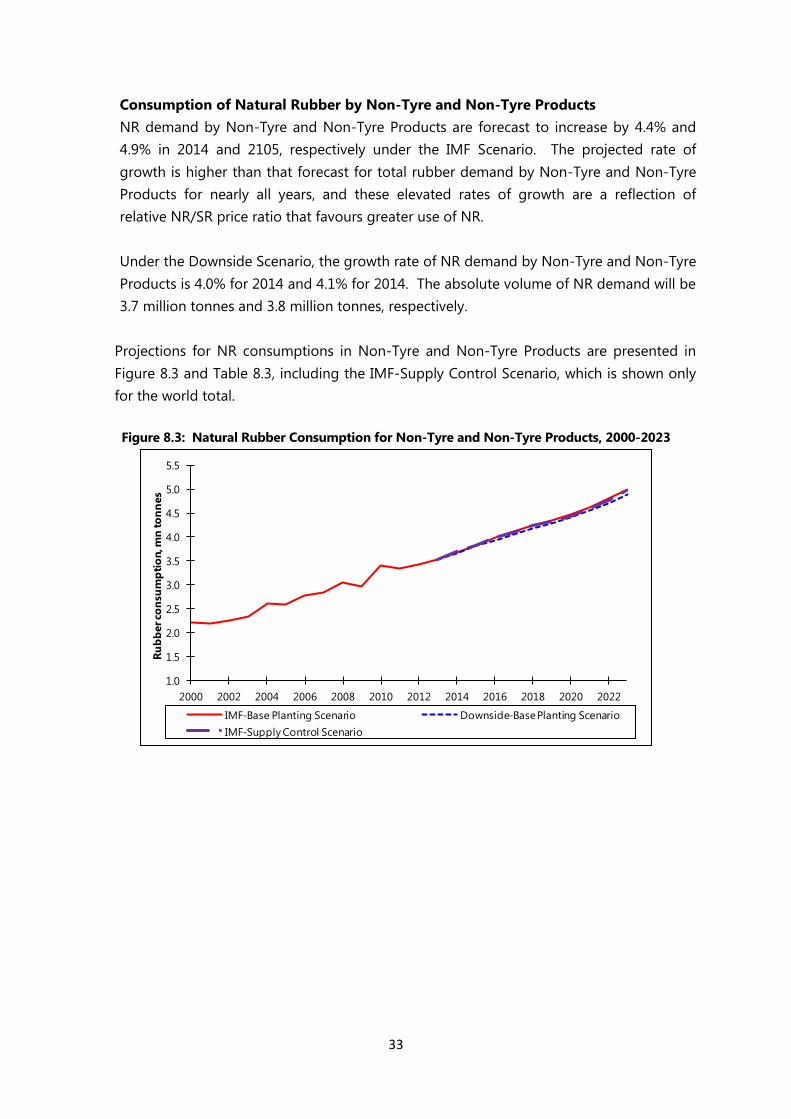

Consumption of Natural Rubber by Non-Tyre and Non-Tyre Products

NR demand by Non-Tyre and Non-Tyre Products are forecast to increase by 4.4% and

4.9% in 2014 and 2105, respectively under the IMF Scenario. The projected rate of

growth is higher than that forecast for total rubber demand by Non-Tyre and Non-Tyre

Products for nearly all years, and these elevated rates of growth are a reflection of

relative NR/SR price ratio that favours greater use of NR.

Under the Downside Scenario, the growth rate of NR demand by Non-Tyre and Non-Tyre

Products is 4.0% for 2014 and 4.1% for 2014. The absolute volume of NR demand will be

3.7 million tonnes and 3.8 million tonnes, respectively.

Projections for NR consumptions in Non-Tyre and Non-Tyre Products are presented in

Figure 8.3 and Table 8.3, including the IMF-Supply Control Scenario, which is shown only

for the world total.

Figure 8.3: Natural Rubber Consumption for Non-Tyre and Non-Tyre Products, 2000-2023

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Ru

bb

er co

nsu

mp

tio

n, m

n to

nn

es

IMF-Base Planting Scenario Downside-Base Planting Scenario

IMF-Supply Control Scenario

34

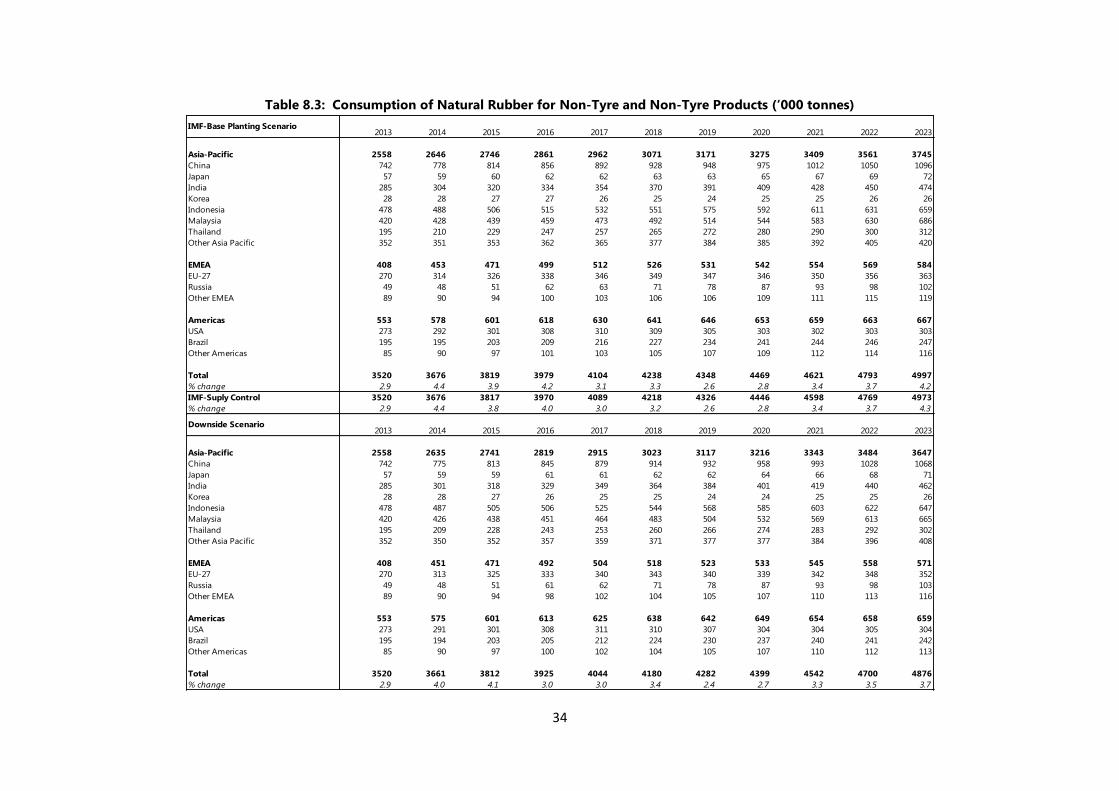

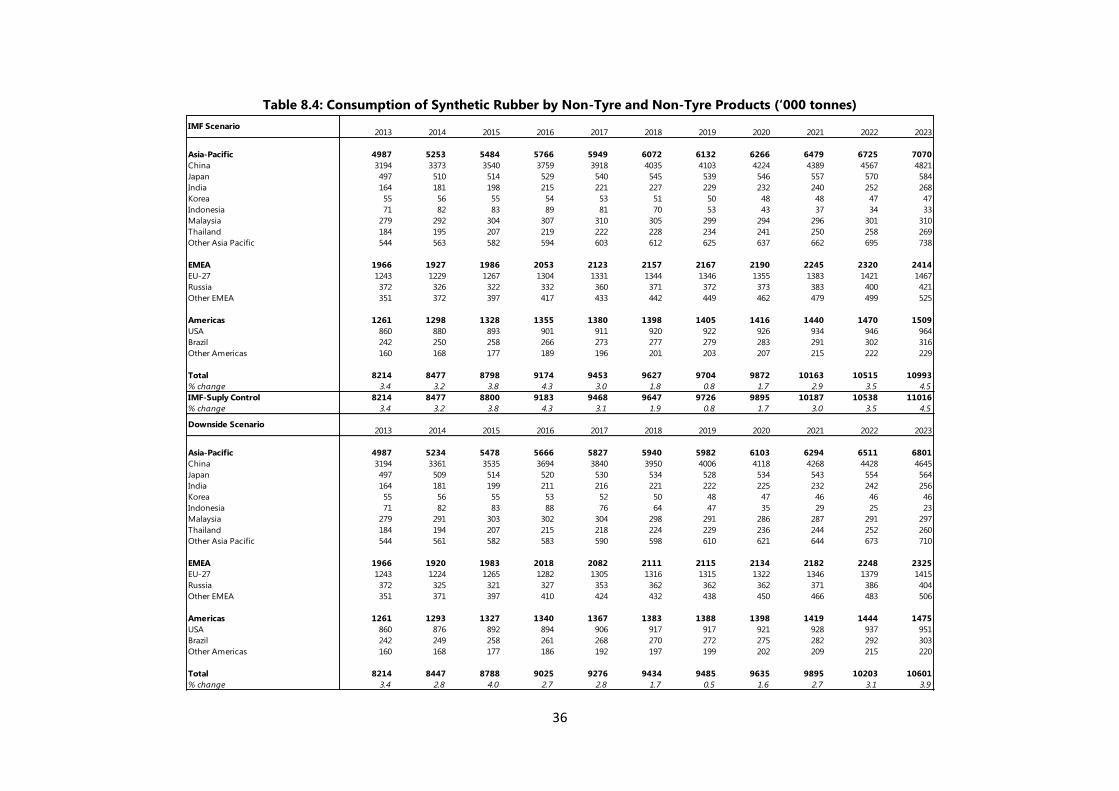

Table 8.3: Consumption of Natural Rubber for Non-Tyre and Non-Tyre Products (‘000 tonnes)

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 2558 2646 2746 2861 2962 3071 3171 3275 3409 3561 3745

China 742 778 814 856 892 928 948 975 1012 1050 1096

Japan 57 59 60 62 62 63 63 65 67 69 72

India 285 304 320 334 354 370 391 409 428 450 474

Korea 28 28 27 27 26 25 24 25 25 26 26

Indonesia 478 488 506 515 532 551 575 592 611 631 659

Malaysia 420 428 439 459 473 492 514 544 583 630 686

Thailand 195 210 229 247 257 265 272 280 290 300 312

Other Asia Pacific 352 351 353 362 365 377 384 385 392 405 420

EMEA 408 453 471 499 512 526 531 542 554 569 584

EU-27 270 314 326 338 346 349 347 346 350 356 363

Russia 49 48 51 62 63 71 78 87 93 98 102

Other EMEA 89 90 94 100 103 106 106 109 111 115 119

Americas 553 578 601 618 630 641 646 653 659 663 667

USA 273 292 301 308 310 309 305 303 302 303 303

Brazil 195 195 203 209 216 227 234 241 244 246 247

Other Americas 85 90 97 101 103 105 107 109 112 114 116

Total 3520 3676 3819 3979 4104 4238 4348 4469 4621 4793 4997

% change 2.9 4.4 3.9 4.2 3.1 3.3 2.6 2.8 3.4 3.7 4.2

IMF-Suply Control 3520 3676 3817 3970 4089 4218 4326 4446 4598 4769 4973

% change 2.9 4.4 3.8 4.0 3.0 3.2 2.6 2.8 3.4 3.7 4.3

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Asia-Pacific 2558 2635 2741 2819 2915 3023 3117 3216 3343 3484 3647

China 742 775 813 845 879 914 932 958 993 1028 1068

Japan 57 59 59 61 61 62 62 64 66 68 71

India 285 301 318 329 349 364 384 401 419 440 462

Korea 28 28 27 26 25 25 24 24 25 25 26

Indonesia 478 487 505 506 525 544 568 585 603 622 647

Malaysia 420 426 438 451 464 483 504 532 569 613 665

Thailand 195 209 228 243 253 260 266 274 283 292 302

Other Asia Pacific 352 350 352 357 359 371 377 377 384 396 408

EMEA 408 451 471 492 504 518 523 533 545 558 571

EU-27 270 313 325 333 340 343 340 339 342 348 352

Russia 49 48 51 61 62 71 78 87 93 98 103

Other EMEA 89 90 94 98 102 104 105 107 110 113 116

Americas 553 575 601 613 625 638 642 649 654 658 659

USA 273 291 301 308 311 310 307 304 304 305 304

Brazil 195 194 203 205 212 224 230 237 240 241 242

Other Americas 85 90 97 100 102 104 105 107 110 112 113

Total 3520 3661 3812 3925 4044 4180 4282 4399 4542 4700 4876

% change 2.9 4.0 4.1 3.0 3.0 3.4 2.4 2.7 3.3 3.5 3.7

IMF-Base Planting Scenario

Downside Scenario

35

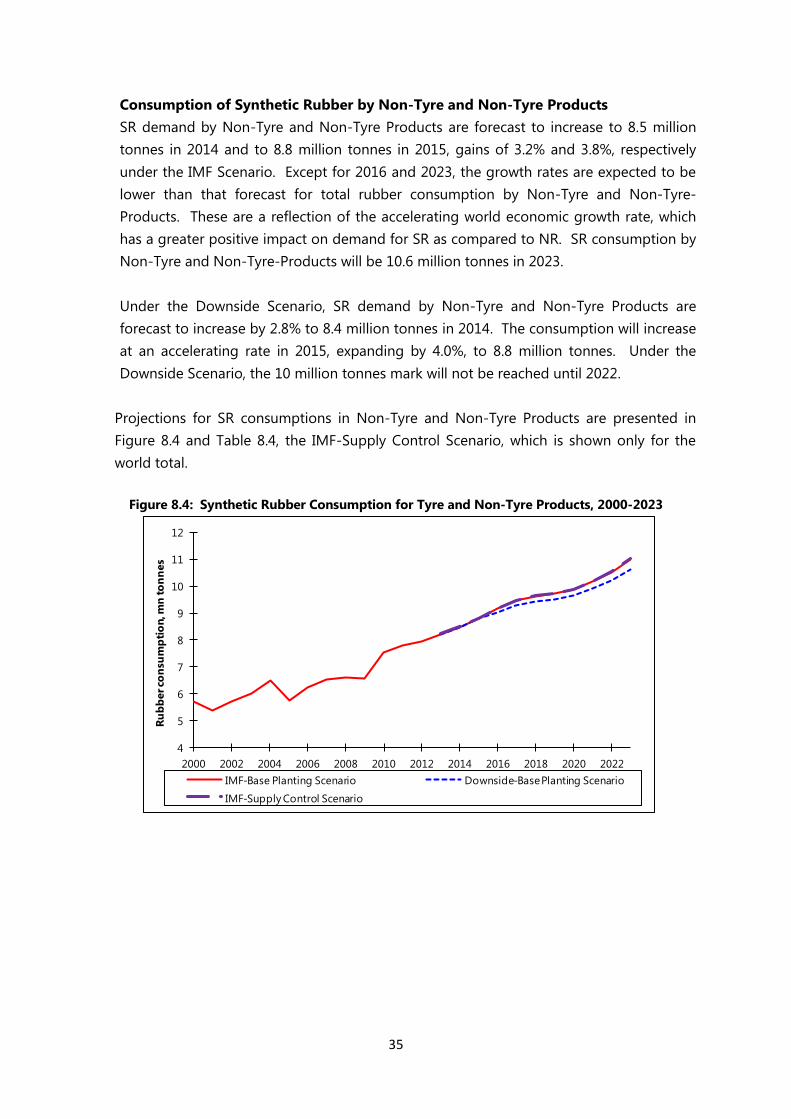

Consumption of Synthetic Rubber by Non-Tyre and Non-Tyre Products

SR demand by Non-Tyre and Non-Tyre Products are forecast to increase to 8.5 million

tonnes in 2014 and to 8.8 million tonnes in 2015, gains of 3.2% and 3.8%, respectively

under the IMF Scenario. Except for 2016 and 2023, the growth rates are expected to be

lower than that forecast for total rubber consumption by Non-Tyre and Non-Tyre-

Products. These are a reflection of the accelerating world economic growth rate, which