why a decision maker may prefer a seemingly unfair gamble

TRANSCRIPT

Decision Sciences Mume 27 Number 2 Spring 19% Printed in the U.S.A.

Why a Decision Maker May Prefer a Seemingly Unfair Gamble Arun J. Prakash, Chun-Hao Chang, and Shahid Hamid College of Business Administration, Florida International University, Miami, FL 33199

Michael W. Smyser College of Business, Southern University, Baton Rouge, LA 70813

ABSTRACT

It is generally believed that risk-averse managers will not accept unfair gambles and therefore may not have the incentive to invest in high-risk projects, products or technology. This paper argues that this is not necessarily so. Rational, risk-averse managers with sufficient preference for positive skewness may undertake projects with payoff distributions that are unfair gambles. Furthermore, the minimum required payoff is shown to be less for managers with preference for positive skewness than otherwise. Thus, a risk-averse manager with preference for positive skewness may accept potentially innovative high-risk projects that are rejected by those without such preference.

Subject Areas: Capital Budgering, Decision Analysk, Risk and Vncertabqy, and Utiw Theory.

INTRODUCTION

Traditional expected utility theorems tell us that a risk-averse person will not accept an unfair game [8] [14] [19]. Therefore, there art concerns that a risk-averse manager may not have sufficient incentive to take bold risks, and occasionally invest in high-risk innovative projects, products, and technology required to remain competitive in the long-run [7] [13]. On the other hand, it is desirable to have risk-averse managers who are not reckless gamblers. Thus, an interesting question arises: under what conditions would the normally prudent and risk-averse managers have the incentive to undertake risky projects that may appear to be unfair gambles, but which may provide a long-term competitive edge?

Expected utility theory cannot explain many of the important decisions made under uncertainty by normally risk-averse individuals, investors, and managers, which appear to be unfair gambles. Numerous examples of such anomalous behavior have been documented [ I ] [ 111 [ 191. For example, individuals simultaneously pur- chase insurance and gamble. The same investors and portfolio managers hedge in some securities and speculate in others. Managers or investors invest in long-shot bets, and they sometimes continue pouring more money into a project after huge losses. Managers undertake conglomerate mergers that appear to have negative

239

240 Seemingly Unfair Gamble

expected excess returns. Risk-averse entrepreneurs and managers often decide to invest in or to market new products, technology or production processes that appear to be unfair gambles. The traditional explanation for these behaviors is that investors and managers overestimate the probability of success, or they get utility from the act of gambling itself [I41 [24]. A more recent, plausible explanation for some of the anomalous behavior is based on the assumption that risk aversion is contextual and differs depending on the situation or on the subjective beliefs in self-competence 111 131 [61[9] [111[131[17] [18] [19].TheprospecttheoryofKahlmanandTravesky [ll], for example, proposes that risk aversion depends on whether the initial situation is favorable or unfavorable. We propose an alternative explanation that assumes individuals have preference for positive skewness and is based on the observation that many decision-making processes involve payoffs that are skewed [2] [4] [5 ] [lo] [21]. We show how a risk-averse manager with sufficient preference for posi- tive skewness may undertake projects with skewed payoff distributions that appear to be unfair gambles. Furthermore, the minimum required payoff is shown to be less for managers with preference for positive skewness than for those with neutral preference for skewness. The implications of these propositions are that managers need not be reckless gamblers, or they need not violate the basic postulates of utility theory in order to occasionally undertake high-risk projects. Rather, if the payoff is skewed, a rational, cautious, and risk-averse manager has the incentive to both gamble and buy insurance, invest in high-risk projects, aggressively develop new products, and adopt new technology required to remain competitive.

We present our arguments in two independent parts. In part one, we develop the general theoretical justifications for the acceptance by risk-averse managers of an unfair gamble with skewed payoff distribution. To provide the theoretical justi- fication, first, the probability distribution is formally introduced and adapted to a variant of the expected utility model of Pratt [16], incorporating both risk aversion and preference for positive skewness in the payoff distribution. To maintain continuity, we then derive the well-known result of necessary conditions for the existence of an acceptable lottery for a risk-averse individual possessing a neutral preference for skewness. Necessary conditions for the existence of an acceptable lottery are then derived for a risk-averse individual with preference for positive skewness. Next, we examine the expected payoff required by a risk-averse individual possessing neutral preference for skewness relative to the expected payoff required by a risk-averse individual possessing preference for positive skewness, and show that the former requires a premium in the expected payoff relative to that required by the latter.

In the second part, an independent example is developed to illustrate the implica- tions of preference for skewness for capital budgeting. A three-moment capital asset pricing model is applied to a hypothetical project to show that the decision making may vastly differ from that of the standard two-moment asset pricing model. Finally, some concluding comments are offered.

CHARACTERIZATION OF THE GAMBLE AND THE EXPECTED UTILITY MODEL

Consider the payoff offered in a lottery. With this gamble (probability distribution), a small probability exists for the individual to win a relatively enormous monetary

Prakash, Chang, Hamid, and Smyser 24 1

prize, so the payoff distribution is clearly nonsymmetric. We examine the general conditions under which a risk-averse individual or manager will willingly accept a nonsymmetric gamble if the decision maker possesses a preference for positive skewness.

For simplicity, the gamble, Z(O,p), considered by the individual is assumed to have a single nonzero payoff of “prize” 8 with known probability p , so that with probability (I-p) the individual expects to receive nothing. Now, consider an indi- vidual endowed with (nonrandom) wealth x and having utility function U(x). We shall assume throughout this paper that the marginal utility of wealth is positive (U(x)O). The individual is confronted with the decision whether or not to accept the gamble ?(8,p), which can be purchased for the price n(a. Following Pratt [ 161, the utility function containing the bid price of the gamble, xb(x,2), is:

Thus, nb(x,?) is the maximum amount the decision maker with wealth x would be willing to pay for gamble Z. Given the distribution of the gamble, the probability distribution of the net payoff of the gamble (defined as the difference between ?and nb(x,Fj), will be:

8 - zbl with probability p -xb, with probability 1 - p .

-. z - n b =

For the probability distribution in (2) the following are obvious:

E(? - nb)3 = p(O - Xb)3 + ( 1 - p)(-nb3

where nb is the Pratt bid price of the gamble defined above. We shall assume that the individual is rational in the sense that when

xb21c(2), the individual would then, and only then, willingly purchase Z(f3,p) for the price of n(a. From (3) it is obvious that a gamble will be unfair if p8<nb; neutral, if p h b ; and fair, if fl>nb.

Expanding the right-hand side of (1) by Taylor’s theorem around x we have:

242 Seemingly Unfair Gamble

and, rearranging terms, we have:

where ml=V'(x)lU'(x), is the measure of absolute risk aversion and v l ( x ) " ( x ) is the elasticity of absolute risk aversion with respect to x. Substituting (3), (4) and ( 5 ) into (7):

In this paper, we determine the bounds on the minimum p, say p*, such that the individual would willingly purchase the gamble z" for the (maximum) price of x ( z w b . Given a specification of U(x) in terms of ml,-, and higher order preferences, proof that p*(O<p<l) exists is equivalent to proving that an individual possessing V(x) as specified would willingly purchase the gamble Y((e,p*) for the maximum price I t ( ? ) q b . TO prove the existence of p*, we assume without loss of generality, that the maximum purchase price of this gamble is one dollar, that is, Itb=l.

Risk Aversion and Neutral Preference for Skewness

Consider a risk-averse (ml<O) individual with neutral preference for skewness (m2=0). The conditions necessary for the existence of p*(o<p*<l) in this case can be obtained by examining a fair gamble.

Lemma 1: For an individual with utility function V(x) characterized by m,<O and m2=0, a necessary and sufficient condition for the existence of p*(o<p*<l) is that @-Itb>o.

Proof: See Appendix A.

Lemma 1 is a restatement of the well-known result that a risk-averse individual possessing neutral preference for skewness requires some compensation for accept- ing any risky gamble, where in this case, compensation arises from the gamble being fair. The following corollary is a direct consequence of Lemma 1 (this result also follows directly from the definition of a fair gamble).

Corollary 1.1: For an individual with V(x) characterized by m,<0 and m+, a necessary condition for p*(Ocp*<l) to exist is that e>n(?). Proof (trivial)

We have used from Lemma 1 the following condition: p8>Itb. Substituting xb=n(z?)=l, p* must then satisfy p * b 1 or p*>l/B. Now, since O<p*<l we have 8> 1 immediately.

Thus, by Corollary 1.1, a risk-averse individual with neutral preference for skewness demands that the prize of the gamble be greater than the cost of the gamble since, otherwise, p*(o<p*<l) no longer exists.

Prakash, Chang, Hamid, and Smyser 243

Risk Aversion and Preference for Positive Skewness In this section, we consider a risk-averse (ml<O) individual with preference for positive skewness (m2>0) and neutral preference for higher moments of the payoff distribution.

Lemma 2: For an individual with U(x) characterized by ml<O, q>o , and &4/h4=0, necessary conditions for the existence of p*(Ckp*cl) in the case of an unfair gamble are:

and

proof: Using (8), the following condition is implied for an unfair gamble:

or, the equivalent condition:

Substituting xb=l and rearranging, we have:

or

provided [.]>0. However, a necessary condition for O<p*<{ .) is that [.]<O, which is a contradiction (note that my3ml<0). Therefore, it must be that [.I&, which now implies the condition:

1 <p* < 1, 1 x- m2 1

O <

244 Seemingly Unfair Gamble

provided [.]<O. To show that p*(O<p*<l) exists we need to prove that m2/3rn1<0 can be chosen such that (.)<1 and [.]<O. Rearranging (.)<1 we have:

In order that [.]<0 we require the condition:

provided b 1 . Comparing (9) and (10) it is obvious that:

0 - 2 82 - 30 + 3’

-(0 - l)-l <

provided 8>1. Therefore (9) implies (10). Thus, by Lemma 2, it is possible that a risk-averse individual would willingly

purchase an actuarially unfavorable gamble provided the individual possesses suf- ficient preference for positive skewness relative to risk aversion. Therefore, an individual who willingly accepts an unfair gamble should not necessarily be regarded as a “risk lover” (ml>O), provided that the individual possesses sufficient preference for positive skewness. We can now state Lemma 3.

Lemma 3: For an individual with U(x) characterized by m,<0, mp0, and d‘u/dr4=0, necessary conditions for the existence of p*(kp*<l) in the case of a fair gamble are:

when

Proof: See Appendix B.

In a similar fashion, we can obtain the necessary condition for the individual to accept a neutral gamble. This is done in Lemma 4.

Lemma 4: For an individual with U(x) characterized by m 1 4 , q>o, and d‘diix4=0, necessary conditions for the existence of p*(o<p*<l) for a neutral gamble are:

Proof: See Appendix C.

Prakash, Chang, Hamid, and Smyser 245

Actuarial Value Premium of the Gamble Resulting from Preference for Positive Skewness Under Risk Aversion A consequence of individual preference for positive skewness (m2>0) is that the required actuarial value of the gamble @8-nb) will be less than the actuarial value required by an individual having neutral preference for skewness (m#), ceteres paribus, as stated in the following lemma.

Lemma 5: If p ; is the minimum p such that q,=(i) for an individual with U(x) characterized by mlcO and m#, andp; is the minimum p such that nb=n(a for an individual with U(x) characterized by ml<O and m 2 S , and dlu/dr4=0, then:

o < @;e-nb) - @;e -nb) c =+=.

Proof Denote p in (A4 in Appendix A) by p l , and p in (C1 in Appendix C) by pz . Subtracting (Cl) from (A4) and rearranging, we have:

Substituting nb-(i)")=l into (11) and rearranging p i and p ; must then satisfy:

or

Clearly p;e-p;e given by (12) is bounded from above when b 1 . From (12) the following relationships are apparent:

w p;[(e - 113 + 11 c 1

provided b1. However, when 8>1, we have p ; satisfying Ocp'cl always, and therefore:

p ; e - p;e > 0.

246 Seemingly Unfair Gamble

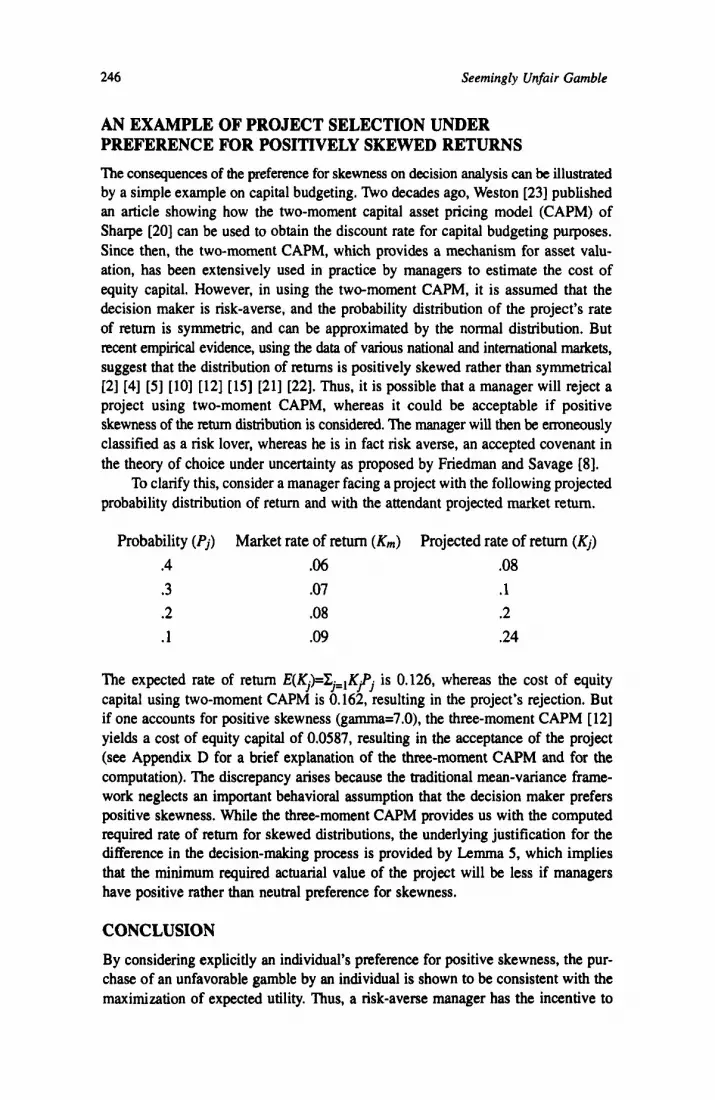

AN EXAMPLE OF PROJECT SELECTION UNDER PREFERENCE FOR POSITIVELY SKEWED RETURNS The consequences of the preference for skewness on decision analysis can be illustrated by a simple example on capital budgeting. nKo decades ago, Weston [23] published an article showing how the two-moment capital asset pricing model (CAPM) of Sharpe [20] can be used to obtain the discount rate for capital budgeting purposes. Since then, the two-moment CAPM, which provides a mechanism for asset valu- ation, has been extensively used in practice by managers to estimate the cost of equity capital. However, in using the two-moment CAPM, it is assumed that the decision maker is risk-averse, and the probability distribution of the project’s rate of return is symmetric, and can be approximated by the normal distribution. But recent empirical evidence, using the data of various national and international markets, suggest that the distribution of returns is positively skewed rather than symmetrical [21 [4] [5] [lo] [12] [15] [21] [22]. Thus, it is possible that a manager will reject a project using two-moment CAPM, whereas it could be acceptable if positive skewness of the return distribution is considered. The manager will then be emneously classified as a risk lover, whereas he is in fact risk averse, an accepted covenant in the theory of choice under uncertainty as proposed by Friedman and Savage [8].

To clarify this, consider a manager facing a project with the following projected probability distribution of return and with the attendant projected market return.

Probability (Pj) Market rate of return (Km) Projected rate of return (Kj) .4 .06 .08 .3 .07 .1 .2 -08 .2 .1 .09 .24

The expected rate of return E(I$)=Cj=lKfj is 0.126, whereas the cost of equity capital using two-moment CAPM is 0.162, resulting in the project’s rejection. But if one accounts for positive skewness (gamma=7.0), the three-moment CAPM [12] yields a cost of equity capital of 0.0587, resulting in the acceptance of the project (see Appendix D for a brief explanation of the three-moment CAPM and for the computation). The discrepancy arises because the traditional mean-variance frame- work neglects an important behavioral assumption that the decision maker prefers positive skewness. While the three-moment CAPM provides us with the computed required rate of retum for skewed distributions, the underlying justification for the difference in the decision-making process is provided by Lemma 5, which implies that the minimum required actuarial value of the project will be less if managers have positive rather than neutral preference for skewness.

CONCLUSION By considering explicitly an individual’s preference for positive skewness, the pur- chase of an unfavorable gamble by an individual is shown to be consistent with the maximization of expected utility. Thus, a risk-averse manager has the incentive to

Prakush, Chang, Hamid, and Smyser 241

accept high-risk but potentially innovative projects required for long-term competitive viability if the returns exhibit skewness. The importance of this result is enhanced because we are able to retain the desirable property that the individual is risk averse. More specifically, our analysis shows that an individual’s level of relative skewness preference to risk aversion, mf3m,, and the payoff, 8, of any single prize gamble determines completely whether some probability, p*(o<p*<l), exists such that this individual would willingly purchase the gamble. This result is unaffected by whether the gamble is fair, neutral, or unfair.

An obvious implication of our theory is that a manager with preference for positive skewness will naturally have a lower minimum required return, or hurdle rate, for any type of project. Thus, even a rational, cautious, and risk-averse manager may have the incentive to invest in high-risk projects with skewed payoffs, and aggressively develop new products, adopt new technology, and consequently become more competitive. Similarly, a rational and risk-averse investor may have the incen- tive to gamble and buy insurance, both hedge and speculate, and is more likely to undertake projects with low or negative ex-ante returns, but with a skewed distri- bution that has the potential to generate a high payoff. [Received: August 28, 1994. Accepted: November 17, 1995.1

REFERENCES

Appleby, L., & Starmer, C. Individual choices under uncertainty: A review of experimental evidence, past and present. In J.D. Hey & P.J. Lambert (Eds.), Surveys in the economics of uncertuinry. Oxford, UK: Basil Blackwell, 1987. Aggarwal, R. Distribution of spot and forward exchange rates: Empirical evidence and investor valuation of skewness and kurtosis. Decision Sciences,

Bromiley, P., & Curley, S. Individual differences in risk taking. In J. Yaks (Ed.), Risk taking behavior. New York: Wiley, 1992, 87-132. Chunhachinda, P., Dandapani, K., Hamid, S., & Rakash, A.J. Efficacy of portfolio performance measures: An evaluation. Quarterly Journal of Business and Economics, 1994,3.?(4), 74-87. Comer, J. Index option pricing: Do investors pay for skewness? Jounuzl of Futures Markets, 1991, ff(1), 1-8. Currim, I.S., & Sarin, R.K. Prospect versus utility. Management Science,

Dickson, P. Toward a general theory of competitive rationality. Journal of Marketing, 1992, 56, 69-83. Friedman, M., & Savage, L.J. The expected-utility hypothesis and the meas- urability of utility. Journul of Political Economy, 1952, 60(6). 463-486. Ghosh, D., & Manash, R.R. Risk attitude, ambiguity intolerance and decision- making: An exploratory investigation. Decision Sciences, 1992,23(2), 43 1-444. Junkus, J.C. Systematic skewness in futures contracts. Journal of Futures Markets, 1991, 1f(1), 9-24. Kahneman, D., & Tversky, A. Prospect theory: An analysis of decision under risk. Econometrica, 1979,47, 263-291.

1990, 2f(3), 588-595.

1989,33( l), 22-41.

248 Seemingly Unfair Gamble

[12] Kraus, A.. & Litzenberger, R.H. Skewness preference and the valuation of risky assets. Journal of Finance, 1976,31(4), 1085-1100.

[ 131 Krueger, N., & Dickson, P.R. How believing in ourselves increases risk taking: Perceived self-efficiency and opportunity recognition. Decision Sciences, 1994, 25(3), 385-401.

[ 141 Layard, P.R., & Walters, A.A. Microeconomic theory. New York McGraw- Hill, 1978.

[15] Prakash, A.J., & Bear, R.M. A simplifying performance measure recognizing skewness. Financial Review, 1986, 21( l), 135-144.

[16] Pratt, J. Risk aversion in the small and in the large. Econometricu, 1964.32,

[17] Salminen, P., & Wallenius, J. Testing prospect theory in a deterministic mul- tiple criteria decision-making environment. Decision Sciences, 1993. 24(2),

[ 181 Schoemaker, P. Are risk-attitudes related across domains and response modes? Management Science, 1990,34(10), 1451-1463.

[19] Schoemaker, P. Experiments on decisions under risk: The expected utility hypothesis. Boston: Martinus Nijhoff Publishing, 1980.

[20] Sharpe, W.F. Capital asset prices: A theory of market equilibrium under con- ditions of risk. Journal of Finance, 1964, 19(3), 425-442.

[21] Singleton, J., & Wingender, J. Skewness persistence in common stock returns. Journal of Financial and Quantitative Analysis, 1986, 13, 335-341.

[22] Stephens, A., & ProRtt, D. Performance measurement when return distribu- tions are nonsystematic. Quarterly Journal of Business and Economics, 1991,

[23] Weston, J.E Investment decisions using the capital asset pricing model. F i m i a l

[24] Yaari, M.E. Convexity in the theory of choice under risk. Quarterly Journal

122-1 36.

279-294.

30(4), 23-41.

Management, 2(1). 25-33.

of Economics, 1975, 300, 278-290.

Prakash, Chang, Hamid, and Smyser 249

APPENDIX A

Proof of Lemma 1

For a fair gamble p8-z6>0, which implies from (8) that:

because mlcO. Substituting xb=l in (Al) and rearranging, p* must satisfy:

or

or

Thus, no matter what the value of 8, a necessary condition for the existence of p* is that p* is between 0 and 1.

To show that p&xb>O is also a sufficient condition for p* to exist, we consider next the complement to a fair gamble (i.e., unfair and neutral gambles) and show that, in this case, p* does not exist.

For an unfair gamble, by using (8), the following condition must be true:

or the equivalent condition:

since m 1 4 . For an actuarially unfavorable gamble, p* must satisfy (A2); after substituting x6=l, we have:

p*e2 - 2p*e < -1

p* c (28 - e2)-I.

or

(A3)

If p* exists for this unfair gamble it must be less than 1 . From (A3), we have p * < ( 2 0 2 ) - ' . If p'cl, then ( 2 W 2 ) - ' must be less than or equal to 1, or 11(2&e2), or 2&82-110, or #-2e+l5Oo, or (8-1)210, a contradiction. Therefore, p* cannot be less than 1 for unfair gamble.

Consider the same individual faced with the decision to purchase a neutral gamble. For the neutral gamble, we obtain, using (8):

250 Seemingly Unfair Gamble

substituting nb=l into (A4) and rearranging, p* is given by:

However, from the definition of a neutral gamble we have p*8=1, or p*=lA. Sub- stituting 1/8 forp* in (A5), we see that 8=1 and, thus, p*=l. Therefore, for the case of a neutral gamble p*(o<p*<l) does not exist.

APPENDIX B

Proof of Lemma 3 Consider the same individual confronted with a decision to purchase a fair gamble. Using (8), the following condition is implied for a fair gamble:

or, the equivalent condition:

Substituting nb=l into ( B l ) and rearranging,p* must satisfy the following condition:

Equation (B2) is similar to the unfavorable gamble just considered. When [.I*, we havep* greater than some negative number, thus satisfying o<p*<l. For [.]>O, from (10) it is required that:

provided 8>1. When [.]<O, we have p* less than some positive number, thus satis- fying O<p*<l. For [.]cO, it is required that:

given that 8>1. For the special case when [.]a, then m#rnl=(&2y(&3e+3). We have, after substituting for m#ml in (B2) and rearranging:

Prakash, Chang, Hamid, and Smyser

e2 - 48 + 5 e2 - 38 + 3 '

2p*e(e - 2) > -

25 1

(B3)

From (B3) we see that Ocp*<1 is satisfied when b 2 .

APPENDIX C

Proof of Lemma 4

Consider the same individual confronted with a decision to purchase a neutral gamble. Using (8) again, we have for a neutral gamble:

or, after rearranging:

Substituting xb=l, p* is given by:

"22 $(e2 - 28) + I + [p*(e3 - 3e2 + 38) - 11 - = 0. 3ml

However, from the definition of an actuarially neutral gamble, E(Z-xb)=p*8=1. Substituting p*&l into the expression above and simplifying:

which will be less than 0, as required for mf3m1, provided 8>2.

APPENDIX D

Application to Capital Budgeting Let Kp K,, and K j represent, respectively, 1 plus the rate of return on the riskless asset, the market, and a risky security j . If the returns are asymmetrically distributed, following Kraus and Litzenberger [ 111 and Prakash and Bear [ 141, in equilibrium, the three-moment CAPM is:

252

where

Seemingly Urlfair Gamble

is the systematic risk of the asset,

is the asset's systematic coskewness with the market K,,

The quantities b , /o i and b2/Mi are known, respectively, as market prices of risk associated with systematic risk and systematic coskewness. For our example, E(K,)=0.07, E(Kj)=0.126, 0~=0.0001, Kf is assumed to be 0.05, Cov(q,K,)= 0.00056, P,=5.6,1=7.0, b1=0.001402, and b2=0.00012. Thus, the cost of equity capi- tal (minimum expected required rate of return) using the two-moment CAPM is:

' he cost of equity capital using the three-moment CAPM is:

Since E(Kj)cE(q)**, the use of two-moment CAPM results in the rejection of the project. However, since E(5)>E(Kj)*, the use of three-moment CAPM leads to project's acceptance.

Arun Prakash is a professor and chairman of the Finance Department at Florida International University. He received his M.S. in statistics and M.B.A. from the University of California-Berkeley, and his Ph.D. from the University of Oregon. His current research interests include portfolio theory, performance measures, international equity markets, impact of options, fixed income securities, financial policies, risk and utility theory, and statistical models in finance. He has pub- lished in many journals, most recently in Journal of the Royal Statistical Sociefy, Journal of Business Finance and Accounting, Managerial Decision Economics, Financial Review, International Journal of Finance, and Quarterly Journal of Business and Economics.

Prakash. Chang, Hamid, and Smyser 253

Chun-Hao Chang is an associate professor of finance at Florida International University. He received his Ph.D. from Northwestern University. His recent publications have appeared in International Economic Review Southern Econommic Journal, Journal of Financial Research, and Journal of International Accounting, Auditing, and Finance. His research interests are in information economics, game theory, bank regulation, and real estate mortgages.

Shahid Hamid is an associate professor of finance at Florida International University. He received his Ph.D. from the University of Maryland. His recent articles have appeared in Journal of Business Finance and Accounting, Journal of Regional Science, Quarterly Journal of Business and Economics, Applied Economics, and Znternutional Journal of Finance. His current research interests include financial policies of corporations, international portfolio performance, option trading, risk and utility theory, impact of managerial objectives and ownership, interest rate risk, free trade agreements, and productivity and technological change in the banking industry.

Michael Smyser is an assistant professor of finance at Southern University. He received his Ph.D. from Florida International University. He has published in the Journal of Business Finance and Accounting, and Applied Economics. His research interests include fixed income securities, market transaction cost, financial policies, taxes, and risk and utility theory.