vive la resistance: competing logics and the consolidation of u.s. community banking

TRANSCRIPT

VIVE LA RESISTANCE: COMPETING LOGICS AND THECONSOLIDATION OF U.S. COMMUNITY BANKING

CHRISTOPHER MARQUISHarvard University

MICHAEL LOUNSBURYUniversity of Alberta

We investigate how competing logics facilitate resistance to institutional change,focusing on banking professionals’ resistance to large, national banks’ acquisitions ofsmaller, local banks. Acquisitions led to new bank foundings, particularly whenout-of-town banks were the acquirers and a community’s local population of bankprofessionals was large. We argue that the national banks’ efforts to introduce abanking logic emphasizing efficiencies of geographic diversification triggered newforms of professional entrepreneurialism intended to preserve a community logic ofbanking. Contributions to a synthesis of ecological and institutional perspectives andto research on entrepreneurship and resistance to institutional change are discussed.

Over the past few years, institutionalists haveshifted attention away from the study of isomor-phic diffusion to develop more nuanced ap-proaches to the study of organizational variationand change (e.g., Kraatz & Moore, 2002; Leblebici,Salancik, Copay, & King, 1991; Lounsbury, 2001;Maguire, Hardy, & Lawrence, 2004; Marquis,Glynn, & Davis, 2007). Despite this redirection ofscholarly effort, little attention has been paid tohow and under what conditions organizations, pro-fessionals, and other actors resist broader-scale in-stitutional changes, such as those catalyzed by thepassage of regulatory acts (Schneiberg & Bartley,2001). Oliver (1991) argued that resistance is a keybut little understood strategic response to institu-tional pressures and that more research is neededon the processes and mechanisms by which insti-tutional change is contested. Such a focus on resis-tance is important because it can help to revise themore passive conceptualizations of organizationalaction that have dominated institutional theorizing(Hirsch & Lounsbury, 1997) by highlighting the ac-tive role of organizations and other actors in nego-tiating and shaping their environments. In addi-tion, since resistance hinders isomorphism, a focuson resistance will help develop greater insight into

how organizational variety emerges and is sus-tained in organizational fields (Aldrich & Ruef,2006; Davis & Marquis, 2005). In this article, weseek to expand understanding of institutional andcompetitive dynamics by exploring the sources ofactor resistance to change.

Recent work has shown that as fields change,aggrieved actors may be activated to countermobi-lize to protect their jurisdictions and establishedroutines (Davis, McAdam, Scott, & Zald, 2005;Wade, Swaminathan, & Saxon, 1998). Abbott(1988), for instance, showed how the status andscope of professions could be understood by focus-ing on ongoing interprofessional conflicts andresistance over jurisdictional boundaries. In thecontext of markets, firms may compete for jurisdic-tional control by constructing barriers to entry andforging monopolistic and oligopolistic advantage ina particular product-market or geographically de-lineated space (Scherer, 1980). And recently, sev-eral scholars in economic sociology and organiza-tional theory have employed institutional analysisto reveal how the social organization of industriesand fields, including the demographic mix of kindsof organizations, is fundamentally shaped by suchjurisdictional struggles (e.g., Fligstein, 1996, 2001;Haveman & Rao, 1997; Lounsbury, Ventresca, &Hirsch, 2003; Scott, Reuf, Mendel, & Caronna,2000; Thornton & Ocasio, 1999).

A core idea emerging in this literature is theconcept of logic, which generally refers to broadcultural beliefs and rules that structure cognitionand fundamentally shape decision making and ac-tion in a field (e.g., see Thornton, 2002, 2004). AsScott and his coauthors (2000) demonstrated in the

We are particularly grateful to Michael Hitt for hisinsight and support throughout the review process. JerryDavis, Mary Ann Glynn, Mark Mizruchi, Jason Owen-Smith, Don Palmer, and the anonymous reviewers allprovided helpful comments on prior versions of thispaper. We also thank the Division of Research at HarvardBusiness School for funding collection of some of thesedata.

� Academy of Management Journal2007, Vol. 50, No. 4, 799–820.

799

Copyright of the Academy of Management, all rights reserved. Contents may not be copied, emailed, posted to a listserv, or otherwise transmitted without the copyright holder’s expresswritten permission. Users may print, download or email articles for individual use only.

context of U.S. health care, changes in logics overtime go hand-in-hand with changes in field gover-nance arrangements. In a similar vein, Thorntonand Ocasio (1999) showed how a shift from a pro-fessional to a market logic in higher education pub-lishing led to corollary changes in corporate gover-nance practices.

Some scholars have begun to extend this work bydrawing on the competing logic imagery of Fried-land and Alford (1991) to shed light on how mul-tiple kinds of historically rooted belief systems pro-vide the foundation for ongoing conflict andchange (e.g., Fiss & Zajac, 2004; Lounsbury, 2007;Reay & Hinings, 2005; Stryker, 1994). For instance,Fiss and Zajac (2004) examined how different ori-entations toward corporate governance—corporat-ist and shareholder value—led to dramatic shifts inGerman corporations’ use of United States–stylegovernance. Lounsbury (2007) extended this ap-proach by demonstrating how contending logicsfundamentally shape variation in the practices andbehavior of distinct groups of actors; mutual fundsin Boston resisted the efforts of New York funds topush aggressive growth money management strate-gies by maintaining a focus on conservative, long-term investing. Despite this new emphasis on com-peting logics and conflict, there has been noexamination of resistance per se.

In this article, we build on this notion thatlogics can be rooted in geographical differences(Lounsbury, 2007; Marquis et al., 2007), high-lighting how competing logics can provide afoundation for resistance. In doing so, we aim toredirect the study of resistance away from a morenarrow focus on strategic action (e.g., Oliver,1991) to examination of how broader belief sys-tems can shape such dynamics. In particular, wefocus on how community-level actors may oper-ate with a “community” logic of governance in-tended to protect local autonomy in the face ofefforts by nationally oriented outsiders to imposea “national” logic of governance that focusesmore on efficiencies gained by standardizationover multiple geographic regions. For example,many communities have mobilized resources andenergy to prevent mass-market firms such as Wal-Mart or Starbucks from opening stores that mightthreaten long-standing local establishments.Such political protest to prevent entry by na-tional chains into individual communities dem-onstrates a particularly vivid type of resistance,yet resistance can also come in less dramaticforms (Hirschman, 1970). Organizational re-searchers, for instance, have highlighted howconsumers’ expression of preferences and actionsin the marketplace can constitute resistance (Car-

roll & Swaminathan, 2000), as can the actions oflocal professionals whose high level of humanand relational capital (e.g., Hitt, Bierman, Uhlen-bruck, & Shimizu, 2006) enables mobility or theability to create organizational alternatives(Haveman & Cohen, 1994; Schneiberg, 2007).

This tension between community and nationalactors and logics has been particularly important inthe banking industry, dating to the founding of theUnited States and the debate between Thomas Jef-ferson and Alexander Hamilton over the benefitsand drawbacks of a national financial system.Other notable historical episodes of jurisdictionalstruggle in this sector include the “bank wars” ofthe 1830s over Andrew Jackson’s revocation of thecharter of the Second Bank of the United States(Hammond, 1957) and the branch banking debatethat pervaded the U.S. states and the nation formuch of the 20th century. In the 1990s, the passageof a series of federal regulatory changes designed toremove all prior geographic restrictions on bankexpansion led national banks to prey on commu-nity banks as acquisition targets. The rhetoric sur-rounding this national shift emphasized the effi-ciency gains that would result from combining theoperations of existing banks into a smaller numberof large banks and threatened the community ori-entation of many local banking infrastructures.

Economic work on banking suggests that commu-nity stakeholders (e.g., borrowers) are hostile toout-of-town banks (Seelig & Critchfield, 2002), yetthe resistance of local actors to these changes hasnot been systematically explored. Communities or-ganized substantial resistance via community non-profits and groups such as the California Reinvest-ment Committee, which, for instance, protestedCitigroup’s expansion into California in 2002. Theinvading out-of-town banks were portrayed as “si-phoning banks away” (Prial, 2000), and local adscounseled consumers not to “give your money tostrangers” (Allen & Pae, 1991). Although there werea variety of such dramatic examples of politicalprotest, press and banking trade journals also sug-gested that these acquisitions laid the groundworkfor resistance by creating pools of bank executiveswho could found new banks (e.g., Epstein, 1996;Gillam, 1998; Murray, 1998; Zellner, 1998). We ar-gue that these new banks represented not only anew form of economic competition for consolidat-ing banks, but also a kind of countermovement(McAdam, McCarthy, & Zald, 1996) whose agentsaimed to resist the imposition of a national logic ofgovernance upon the local banking infrastructure.

We specifically examine how the acquisition-driven consolidation efforts of national banks facil-itated a form of resistance, namely, the creation of

800 AugustAcademy of Management Journal

competing community banks by professional bank-ers, many of whom had left consolidating banks. Byfocusing on the relationship between organization-al dynamics and professionals, our research ad-dresses a key link between interorganizational pro-cesses and more individual-level “human capital”(e.g., Hitt et al., 2006). In this tradition, Havemanand Cohen (1994) highlighted the importance ofstudying how mergers among California savingsand loans facilitated the mobility of bank execu-tives, although it indirectly led to a decrease inmobility as “vacancy chains” were closed. Con-versely, Stuart and Sorenson (2003) studied howbiotech entrepreneurs emerged following “liquid-ity events” such as acquisitions that weakened fi-nancial bonds between technologists and theirorganizations.

We extend this research by examining how sometypes of acquisitions, conditioned by institutionallogics, may systematically open up entrepreneurialopportunities for professionals (McGrath & Mac-Millan, 2000). We show that consolidation of localbanking markets by community actors does nottrigger the creation of new community banks bylocal professionals but that consolidation promul-gated by large national banks does. This findingsuggests that it is not competitive processes in ageneric sense that enable entrepreneurial action,but particular forms of competitive dynamics re-lated to the clash between community and nationallogics. Thus, sensing “entrepreneurial opportuni-ties” (Sarasvathy, 2001) is not a neutral, objectiveoccurrence but one perhaps embedded in broaderinstitutional dynamics involving competing logics.

By concentrating on the heterogeneous processesby which professionals’ new community bank cre-ation counters consolidation pressures, our ap-proach takes on an ecological flavor. Existing workin this area (e.g., Carroll & Swaminathan, 2000)focuses on long-term industry transitions, but ourfocus on a shorter time frame of dramatic consoli-dation (cf. Stearns & Allan, 1996) and our fine-grained, community-level data allowed us to un-cover the possibility that institutional logics rootedin geographical difference (Lounsbury, 2007; Mar-quis, 2003; Marquis, Glynn, & Davis, 2007) underliesome market activities and shape the ecologicalmix of organizations. Our paper contributes to theunderstanding of resistance by highlighting the in-stitutional contingency of community resistance toregulation-driven consolidation. Given such resis-tance, consolidation processes can yield organiza-tional variation as opposed to homogeneity, whichhas been the trope of institutional theorists for fartoo long.

In the next section, we provide an overview of

the historically rooted tension between communityand national logics in U.S. banking and how thenational banks’ acquisition movement deepenedthis long-standing schism, precipitating entrepre-neurial action by local banking professionals. Wedevelop several hypotheses that we tested in dataon a population of U.S. banking communities from1994 to 2002. We then discuss the implications ofthis research for the study of resistance, entrepre-neurship, and the merging of institutional and eco-logical perspectives.

NATIONAL AND COMMUNITY LOGICS INU.S. BANKING

Whether banks should be controlled by localcommunity or national organizations is one of themost enduring debates of U.S. history. Its roots canbe traced to the core philosophical positions of thetwo major political parties present at the foundingof this republic. The Republicans, led by ThomasJefferson, preferred decentralized political and eco-nomic systems under community control. The ma-jor opposing party, the Federalists, led by Alex-ander Hamilton, favored centralized political andeconomic systems and established early nationalbanks in the United States. Although those on thecentralization side of this debate were able to es-tablish a few early national banks, the country’searliest experience of national banking ended in1836, when Andrew Jackson, expressing warinessof consolidated financial power, vetoed the charterrenewal of the Second Bank of the United States.Stated Jackson, “It is easy to conceive that greatevils to our country and its institutions might flowfrom such a concentration of power of a few menirresponsible to the people” (quoted in Roe,1994: 58).

This tension has remained vivid throughout U.S.banking history and has become embedded incounterposing institutional logics that have in-formed and shaped policy debates to this day. Atthe turn of the 20th century, those who advocatedlocal control were in positions of power. But manyof the larger banks, seeing the advantage of expand-ing beyond their headquarters communities, advo-cated for a relaxation of the laws prohibitingbranching (Collis, 1926; Fischer, 1968). This groupargued that banks with branches were safer becausethey were able to spread credit risk geographically.Organized opposition to branching came fromsmall and medium-sized banks. Echoing Jackson,they capitalized on public fear of consolidated cap-ital, arguing that branching would sever an impor-tant link between local bankers and communityborrowers. Opposition was mounted through the

2007 801Marquis and Lounsbury

agency of trade associations (Ingram & Rao, 2004)organized with the explicit goal of lobbying units ofgovernment. For example, in 1923, the Kansas,Missouri, and Pennsylvania bankers’ associationsall declared themselves opposed to branch bankingand actively worked to prevent the passage of pro-branching legislation (White, 1985), and in 1930,leaders of single-unit banks established the Inde-pendent Bankers Association (Calomiris, 1993),which came to be the primary national trade organ-ization for community and independent banks.

Although the single-unit banks controlled only asmall percentage of overall industry assets, thepublic and legislators often supported their viewbecause of their success in framing the debate as aconflict between community banking and consoli-dated capital. It was believed that communities,individuals, and small businesses would suffer ifbanks were managed by an “agent acting at a dis-tance under delegated authority” (Charles Dawes,comptroller of the currency in 1902, quoted inFischer, 1968: 28) and that banking dominated bylarge banks would break the link between deposi-tors and bank directors (Chapman & Westerfield,1942; Fischer, 1968). There was strong agreementamong community-oriented banking professionals.A mid-1930s survey found 90 percent of Nebraskasingle-unit bank executives to be opposed tobranching (Kuhn, 1968).

Whereas the institutional logic of community bank-ing focused on local control and avoidance of consol-idated financial power, banking professionals fromlarger banks, who were focused on expanding branchnetworks, emphasized a national logic of economicefficiency centered on the assumption that geo-graphic diversification would lead to a more securebanking system. William B. Ridgley, the comptrollerof the currency in 1903, opined as follows: “I believein branch banking. Theoretically, it is the best system,as it is more economical, more efficient, will serve itscustomers better, and the organization can be such asto secure in most respects better management”(quoted in Fischer, 1968: 29). As the 20th centuryunfolded, this logic began gaining more widespreadsupport. By the late 1980s, a majority of U.S. statespermitted out-of-state banks to operate within theirborders. The federal government essentially endedstate restrictions on banking with the passage in 1994of the Riegle-Neal Interstate Banking and BranchingEfficiency Act, which opened the door to a nationalinterstate branching network.1 As the word “effi-

ciency” in the name of the Riegle-Neal act suggests,the explicit goal was to eliminate geographic barriersperceived to impede scale in banking. This deregula-tory period witnessed many mergers and acquisitionsand the rise of a new form of organization, thesuperregional bank.

Despite the growing power of national banks,adherents of the community logic remained activein contesting deregulation and its effects. Bankingprofessionals and community groups protestedmany acquisitions of local firms. As noted, therhetoric was heated, and invading out-of-townbanks were portrayed as establishing foreign “col-onies” (Finkelstein, 2002) and as having “lost theidea of serving the community” (Tripp, 1999). Al-though some lobbied government officials to pre-vent these changes, more often the resistance tookthe form of consumers supporting firms they feltmore authentically tapped their personal values(Tripp, 1999; cf. Carroll & Swaminathan, 2000).This support enabled an explosion of new commu-nity bank foundings at the same time that massivenational consolidation was occurring. Some eco-nomics-based commentators have described theseparallel events as a “paradox” (Moore & Skelton,1998). However, examining consolidation as a pro-cess that brought to the fore longstanding tensionsrooted in community versus national logics mayenable insights into the sources of community re-sistance to the nationalization of banking via thecreation of new community banks.

THEORY AND HYPOTHESES

Our theoretical focus is on the mechanismswhereby professional bankers founded new com-munity-oriented commercial banks amidst regula-tion-triggered efforts to consolidate their industry.Given the importance of this phenomenon, it is nosurprise that financial economists and other bank-ing scholars have posited explanations. After usingthis existing literature to present a hypothesis thathas been dominant in the literature on banking, wedevelop a set of theoretically informed hypothesesgrounded in the growing corpus of work on insti-

1 Large banks heavily lobbied for the 1994 act. NationsBank CEO Hugh McColl theorized that expansion-minded bank-holding companies that owned large banks

headquartered in major cities surrounded by rural areaswere particularly successful lobbyists because the geo-graphic diversity of these heartland banks made it easierfor them to accumulate congressional votes (Kane, 1996).The unsuccessful countermovement originated withsmaller banks represented by the Independent BankersAssociation of America (the national trade organizationfor community and independent banks), the Conferenceof State Bank Supervisors, and other unions of smallerbanks.

802 AugustAcademy of Management Journal

tutional ecology (e.g., Carroll & Swaminathan,2000; Wade, 1998). This work emphasizes bothcompetitive processes and the role of broader insti-tutional processes related to legitimation (e.g.,Baum & Powell, 1995) as well as shifts in logics(e.g., Haveman & Rao, 1997). We extend this liter-ature by examining how competing institutionallogics shape ecological dynamics. In addition, byfocusing on the role of organization-based profes-sionals, we highlight how the human capital offirms can provide a basis for resistance to change.

Bank Acquisitions and Foundings:The Extant Banking Literature

A number of scholars have suggested that routinecompetitive processes might account for a link be-tween mergers and acquisitions and the foundingof new organizations in a given market. For in-stance, existing research on banking suggests thatacquisitions create opportunities for smaller, newerorganizations that target niches at the periphery ofa market. The basic argument is that acquisitionseffect changes in the product offerings of mergedfirms that facilitate start-ups, especially in product-markets that larger firms tend to be less efficient atserving. A presumably larger and more organiza-tionally complex merged bank might, for example,be expected to deemphasize consumer and smallbusiness loans and services inasmuch as theseniches are not as amenable to scale economies ascorporate lending and fee-based services such asinvestment banking (Davis & Mizruchi, 1999).

Supporting this view, Berger, Kashyap, andScalise (1995) found that larger banks devoted lessof their assets to small business lending, and theysuggested that large banks likely reduce small busi-ness lending because it is less efficient. Keeton(1995) found that front-line loan officers in largerorganizations have less discretion, which often de-lays lending decisions for smaller customers. Thedisruption to customers occasioned by consolida-tion affords new banks an opportunity to steal cus-tomers who perceive a reduction in service (Berger,Bonime, Goldberg, & White, 1999). The bottom lineof these economically oriented studies is that theprimary causal mechanism behind bank foundingis perceived market needs. New banks are foundedto serve newly attractive and underserved marketniches left in the wake of mergers.

Hypothesis 1. The more local banks are ac-quired in a community, the greater the found-ing rate of new banks in that community.

An Institutional Ecology Approach

In contradistinction to the existing literature onbank dynamics, an institutionally based ecologicalapproach is sensitive to how both competitive andinstitutional processes influence outcomes of inter-est via a focus on the actions and behaviors ofdifferent kinds of actors and organizational forms.For example, resource partitioning theorists pro-pose a relationship between the consolidation ofmarkets and a proliferation of specialist organiza-tions. They argue that as a market consolidates intolarger competitors, the target markets of those thatfail or are acquired become free, which opens upperipheral resource niches. New specialist organi-zations then fill these emergent resource spaces.The statistical association between generalist con-solidation and specialist proliferation has beendocumented in a number of industries, includingnewspapers (Carroll, 1985), beer brewing (Carroll &Swaminathan, 2000), and winemaking (Swami-nathan, 1995).

Carroll, Dobrev, and Swaminathan (2002) offeredthree different explanations for why resource par-titioning occurs: customization, conspicuous statusconsumption, and anti–mass production culturalsentiment. Customization has been studied in thecontext of audit firms (Boone, Broecheler, & Car-roll, 2000) and it is generally argued that specialistorganizations are able to provide greater personal-ization and customization of products. Also, Car-roll, Dobrev and Swaminathan (2002) wrote thatsometimes product status and conspicuous con-sumption lead to the rise of specialists who canbetter fill a niche—for example, the sustained suc-cess of small boutique auto producers, suchas Porsche and Ferrari.

Closer to the issues of our study on banking con-solidation and resistance is the mechanism of cul-tural sentiment opposing mass production—a re-jection of powerful mainstream producers in favorof craft and specialty products. This mechanismhas been most prolifically explored in the contextof the microbrewing industry, where, Carroll andSwaminathan (2000) argued, beer consumers preferproducts from smaller, independent brewers andlook to an organization’s identity when makingpurchasing decisions. This preference enabled theproliferation of microbreweries, which took on asocial movement–like quality. Supported by exten-sive qualitative analyses of interviews and industryreports, they showed that following the dramaticconsolidation of the postwar brewing industry toonly 43 firms in 1983, consumer pressures for al-ternative products led to an explosion in new brew-ery foundings and the creation of almost 1,500 spe-

2007 803Marquis and Lounsbury

cialist firms by the turn of the 21st century. Thus,increased concentration in a local market may trig-ger a resource partitioning process that enables newspecialist community banks to be created. Hence,

Hypothesis 2. The greater the market concen-tration of a local community, the greater thefounding rate of new banks in that community.

In contrast to the standard resource partitioningapproach, according to which greater concentrationwill leave underserved niches, some ecologistshave drawn on the old industrial organization eco-nomics literature (e.g., Scherer, 1980) to argue thatlarge incumbents may use market power to discour-age entry (Bain, 1956). A number of studies of bank-ing have tested this phenomenon, finding that mar-kets with fewer larger competitors have higherprices, which suggests that the large incumbentfirms can exercise market power (see Berger et al.[1999] for a summary). For instance, Prager andHannan (1998) found that prices for deposit ac-counts increased following merger-driven growth.And Hanweck (1971) showed that new bank forma-tion in 230 cities was negatively related to in-creased market control by large players.

This focus on the negative influences of marketcontrol on foundings provides an interesting coun-terpoint to the resource partitioning arguments pos-ited above. Even though these could be seen asclassic competing hypotheses, since industrial or-ganization economists have typically operation-alized market power with concentration ratios, theorganizational ecology literature suggests a differ-ent operationalization that emphasizes the exis-tence of multiple generalist organizations (e.g., Car-roll & Swaminathan, 2000). This conceptualizationof market power is more of a complement to re-source partitioning and is actually in line with Car-roll’s (1985) original statement, which suggestedthat having multiple strong generalist organizationsin a market discourages entry, because differentia-tion among generalists leads them to focus on “avariety of domains simultaneously” (Carroll, 1985:1266). This is particularly apropos in banking,since large national banks establish themselves onthe basis of their ability to leverage power andexpertise over distinct domains.

In our case, generalist banks with achieved mar-ket power in commercial and real estate businesses(the primary types of banking other than retail)would be able to leverage their greater market reachand profits to discourage retail-oriented start-ups(see also Carroll & Swaminathan [2000] for a simi-lar approach). Thus, our definition of a generalist isa bank engaged in substantial efforts in the majorbanking businesses of retail, commercial, and real

estate. Such banks of broad scope are almost alwaysnationally oriented, since the infrastructures re-quired to support extensive products and services,particularly those serving larger firms, are not eco-nomically practical unless they can be leveragedover multiple markets. Banks with a more commu-nity orientation are typically much smaller andfocused on single market segments. Keeton (2000)suggested that banks with commitments and activ-ities that span a broader array of product offeringswill dissuade banking entrepreneurs from startingsmaller banks for fear of being driven out of busi-ness. So in addition to any effect of market concen-tration resulting from resource partitioning, wemay observe a negative relationship between largegeneralist banks and start-ups. Hence:

Hypothesis 3. The greater the presence of gen-eralist banks in a community, the lower therate of founding of new banks in thatcommunity.

Although organizational demographers havegone far in specifying the rise of specialist organi-zations in consolidating markets, as well as theeffects of powerful generalist organizations, an im-portant question remains: Who are the entrepre-neurs that generate new specialist organizations?Some organizational demographers have begun toexamine this question (e.g., Haveman & Cohen,1994; Stuart & Sorensen, 2003), but more effort isrequired to link organizational processes to themore individual-level processes of entrepreneurswho create organizations. In the context of profes-sional service firms such as banks, professionalsthemselves can often provide key motors forchange and resistance because they have signifi-cant levels of human capital, often backed by spe-cialized education, credentialing, and experientialknowledge (Becker, 1976).

The importance of human capital is evident overa wide range of professional services. For instance,the human capital of lawyers enables law firms toprovide services related to intangible forms ofknowledge and information (e.g., Hitt, Bierman,Shimizu, & Kochhar, 2001; Hitt et al., 2006). In asimilar way, banking professionals design and sellproducts that package intangible qualities of mon-etary flows such as risk (Bernstein, 1996). Suchhuman capital provides a crucial resource that en-ables a firm to attain higher levels of performanceand sustainable competitive advantage (Alvarez &Barney, 2004; Barney, 1991). Further, banking pro-fessionals have significant “relational capital”(Uzzi, 1999), a resource that is developed over timeand is embedded in social relationships (Uzzi,1997). As in the legal profession (Hitt et al., 2006;

804 AugustAcademy of Management Journal

Spar, 1997), this capital is portable, as it frequentlyresides in the relationships that individual bankingprofessionals have with their clients.

In other cases, professionals might become animportant resource for new organizations (e.g., Al-drich & Ruef, 2006; Meyer, 1994; Ruef, 2000).Meyer (1994) described this supply-side processwhereby certain types of actors, particularly in thesciences and professions, occupy institutional rolesthat enable and encourage them to devise and pro-mote new kinds of organizations (Burton, Soren-son, & Beckman, 2002; Freeman, 1986). For exam-ple, a number of highly skilled engineers, who asemployees of Fairchild Semiconductor in the late1950s and 1960s had access to unique knowledgeabout semiconductor innovation and process, ex-ited to found competing firms such as Intel, Ad-vanced Micro Devices, and LSI Logic (Saxenian,1994).

These effects may be expected to be particularlypronounced in banking; professionalism, as Collins(1979) argued, is essential in financial industriesthat rely on credentials to gain and hold the publictrust. Banking executives, an elite subset of bankingprofessionals who are the key actors creating newbanks, are also bound by an extensive body of in-dustry and location-specific regulatory knowledge(Haveman, 1995). Evidence of a profession of bankerincludes professional associations (Lounsbury, 2002)and the American Banker, a daily periodical that hasbeen published since the 1830s, as well as popularbooks such as Martin Mayer’s (1997) The Bankers.Thus, a greater number of bank foundings is likelyin communities in which there is a strong profes-sional presence.

Hypothesis 4. The greater the number of bankprofessionals in a community, the greater thefounding rate of new banks in that community.

However, the actions of entrepreneurs who cre-ate new organizations do not occur in an institu-tional vacuum (Scott, 2001) and, as we have arguedearlier, competing institutional logics have impor-tantly shaped the behavior of actors in the U.S.banking field over a long period of time. In partic-ular, we argue that the geographic locus of actorstied to community and national banking logics maybe important. Thus, although extant explanationsof bank foundings have tended to focus on aggre-gate rates of acquisition, it may be helpful to dis-tinguish between acquisitions that are made bypeer firms within a community, where the result ismaintenance of community-based financial ser-vices and a community logic, and those undertakenby national firms, which lead to the aforemen-tioned siphoning away of banking assets and the

introduction of a national logic. Substantial survey-based and anecdotal data suggest that acquisitionsby national firms generate greater resistance be-cause such banks have fewer ties to local stakehold-ers and make decisions about resource allocationremotely, often without adequate consideration ofthe impact on a local economy.

Researchers in economics have suggested, for ex-ample, that local borrowers are hostile to out-of-market banks (Seelig & Critchfield, 2002), a feelingthat should be reflected in consumers’ reacting neg-atively to having larger, increasingly nonlocalbanks invade their communities. Even if outrighthostility is not observed, there is overwhelmingevidence that people like to bank with local firms,the tradition of local banking being much ingrainedin the U.S. population. For instance, national sur-veys conducted in 1989 (Elliehausen & Wolken,1992) and 1995 (Kwast, Starr-McCluer, & Wolken,1997) showed that households overwhelminglychoose local depository institutions, especially lo-cal commercial banks, when given a choice be-tween local and national banks. As countless pressaccounts following bank mergers have suggested,consumers want a “place where you are known byname and your financial record does not have to bespelled out to a new bank officer every time youwant a transaction” (Nadler, 2001: 38). In general,acquisitions by outsiders can create considerableuncertainty by introducing a new national logicinto a community, opening up opportunities fornew firm creation (e.g., McGrath & Macmillan,2000). Thus, we also expect the effects of out-of-town acquisitions on community bank foundings tobe greater than that of within-community acquisi-tions. Hence,

Hypothesis 5. The greater the number of acqui-sitions by out-of-town banks in a community,the greater the founding rate of new banks inthat community.

Hypothesis 6. Acquisitions by out-of-townbanks in a community will have a greater effecton the founding rate of new banks in that com-munity than acquisitions by local banks.

To more powerfully demonstrate the effects ofcompeting institutional logics, however, it is im-portant to show how they differentially shape be-havior (see Lounsbury, 2007). This goal can be use-fully approached by assessing interactions betweencarriers of logics (e.g., national banks) and actorsdriving change processes of interest (e.g., profes-sionals creating community banks), focusing onhow such actions are institutionally contingent(e.g., Schneiberg & Bartley, 2001; Schneiberg &

2007 805Marquis and Lounsbury

Clemens, 2006). In this case, we expect the effect ofprofessionals to be strongest when communitybanks are acquisition targets of out-of-town, na-tional banks. Put another way, we expect that ac-quisitions made by out-of-town banks will be apositive moderator of the effect of the number ofbanking professionals on new bank foundings. Aswe theorized above, it is these outsider banks thatgenerate substantial resistance in communities byintroducing a national logic. To wit, we expect thatthe existence of a pool of local bank professionalsin concert with acquisitions by outsider banks willmore likely catalyze resistance in the form of newcommunity bank foundings.

This focus on the relationship between profes-sionals and competing logics is particularly illumi-nating in the context of banking. To the extent thata local banking market is subject to acquisitions bynational banks, often headquartered far from thetarget banks, professional autonomy is threatened.In smaller, local banks, major decisions are madelocally, not at a geographically distant headquar-ters. As institutional theorists have documented,professional identity is a significant driver of ac-tion, especially when autonomy is challenged,whether within organizations (e.g., Powell, 1985)or over an entire field or industry (e.g., Scott et al.,2000). Many studies document how professionalsunder threat mobilize to create new or transformexisting organizations (e.g., Brint & Karabel, 1991;DiMaggio, 1991; Kraatz & Zajac, 1996). Brint andKarabel (1991), for instance, explained how earlypresidents of junior colleges, realizing that theywere becoming increasingly locked into lower sta-tus in the academic hierarchy, despite resistancefrom consumers and business, developed an alter-native strategy: to transition from transfer-orientedinstitutions to institutions providing terminal vo-cational education.

Further, although the justification for acquisi-tions and mergers is often staff reduction and reor-ganization (Birch, 1987; Unger, 1986; Walsh, 1988),acquisitions undertaken by outsiders tend to bemore hostile, creating greater dislocation and dis-satisfaction (Newton, 1988). In addition, executiveturnover in an acquisition target is more likelywhen target and acquirer are dissimilar (Hambrick& Cannella, 1993). Focusing more on individuals’financial resources created by “liquidity events,”Stuart and Sorenson (2003) also argued that eventsthat break leaders’ ties to their organization maylead to entrepreneurial action. In the wake of merg-ers, some banking professionals might be forced toleave, and others may exit voluntarily to seek au-tonomy via the creation of new banks (see Buono &Bowditch, 1989). Numerous articles in the business

press and banking trade journals offer anecdotalsupport for the idea that acquisitions of local banksby outsiders lead to a population of bank execu-tives who become activists in reshaping the mix oftheir communities’ banking institutions (e.g., Ep-stein, 1996; Gillam, 1998; Murray, 1998; Zellner,1998).

As noted above, these professionals can tap intothe historic antipathy toward the logic promulgatedby national banks by appealing to consumers andsmall businesses that prefer doing business withcommunity-focused firms. Thus, Moore and Skel-ton’s (1998) “paradoxical” finding that bank merg-ers beget bank foundings might be driven by theunexplored process whereby acquisitions by out-of-town banks precipitate efforts by professionalbankers to create new, community-oriented banks.As press accounts and banking research suggest,efforts to maintain or regain local and professionalidentities as well as to resist efforts of nationalbanks to dominate a community’s banking infra-structure motivate these creations. Thus, the signif-icant dynamic may not be the mere presence ofindividual professionals, or even mere acquisitionsby out-of-town firms, but the interaction betweenthese two forces. Hence,

Hypothesis 7. The greater the interaction be-tween local bank professionals and acquisi-tions by out-of-town banks in a community, thegreater the founding rate of new banks in thatcommunity.

METHODS AND ANALYSES

Sample and Units of Analysis

We examined our hypotheses at the communitylevel of analysis in data from 1994 to 2002. We tookthis approach for two interrelated reasons. First,entrepreneurship is theorized to be a community-level phenomenon, yet little empirical work existson the topic (Romanelli & Schoonhoven, 2001). Anadditional important reason, one that differentiatesbanking from other industries, is that geographiccommunity is traditionally seen as defining themain market for banking services. The years stud-ied, 1994 to 2002, are significant because they en-capsulate the period of full nationalization of U.S.banking triggered by the 1994 Riegle-Neil act andfollowing the banking crisis of the late 1980s andearly 1990s (Federal Deposit Insurance Corpora-tion, 1997).

We defined community in terms of the metropol-itan statistical areas (MSAs) established by the Of-fice of Management and Budget as of June 6, 2003.We included not only units officially designated

806 AugustAcademy of Management Journal

MSAs, but also metropolitan divisions of MSAs(these are similar to the earlier PMSAs; for exam-ple, the Philadelphia MSA has metropolitan divi-sions of both Philadelphia proper and Wilmington,Delaware). As of the date noted above, there were379 of these geographical areas. Examining these379 communities from 1994 to 2002 gave us 3,411community-year observations. As noted, the timeperiod is opportune for this analysis because itbegins with a change in regulation that might havehad an effect on bank foundings and mergers.

The main source of community market data, theFederal Deposit Insurance Corporation’s (FDIC)Summary of Deposits, which began online coveragein 1994 (http://www2.fdic.gov/sdi/main.asp), pro-vides annual branch-level data on all bankingbranches in the United States, an average of morethan 80,000 observations per year. We constructeda branch-level database that contains 751,581 ob-servations for the entire nine-year period. To con-struct our community measures, we aggregatedthese data to the MSA level.

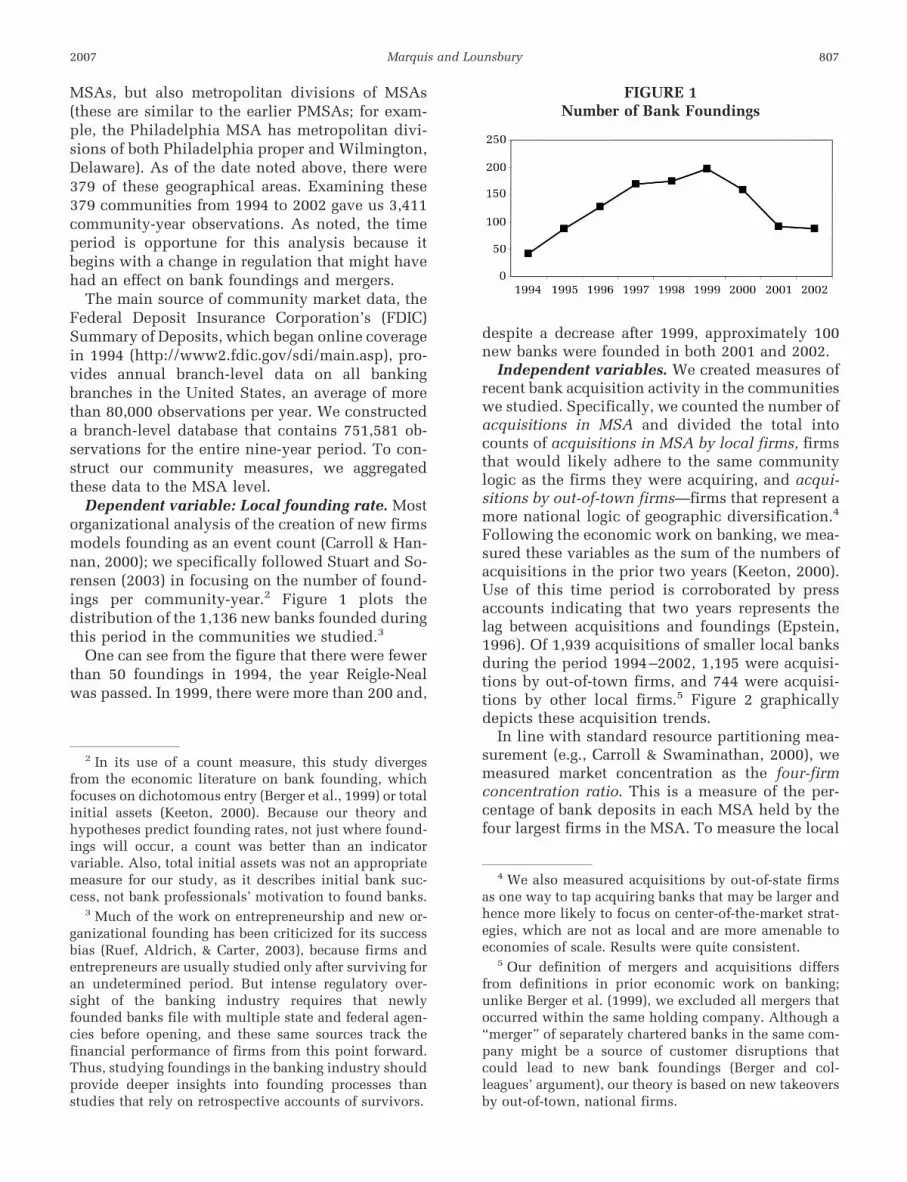

Dependent variable: Local founding rate. Mostorganizational analysis of the creation of new firmsmodels founding as an event count (Carroll & Han-nan, 2000); we specifically followed Stuart and So-rensen (2003) in focusing on the number of found-ings per community-year.2 Figure 1 plots thedistribution of the 1,136 new banks founded duringthis period in the communities we studied.3

One can see from the figure that there were fewerthan 50 foundings in 1994, the year Reigle-Nealwas passed. In 1999, there were more than 200 and,

despite a decrease after 1999, approximately 100new banks were founded in both 2001 and 2002.

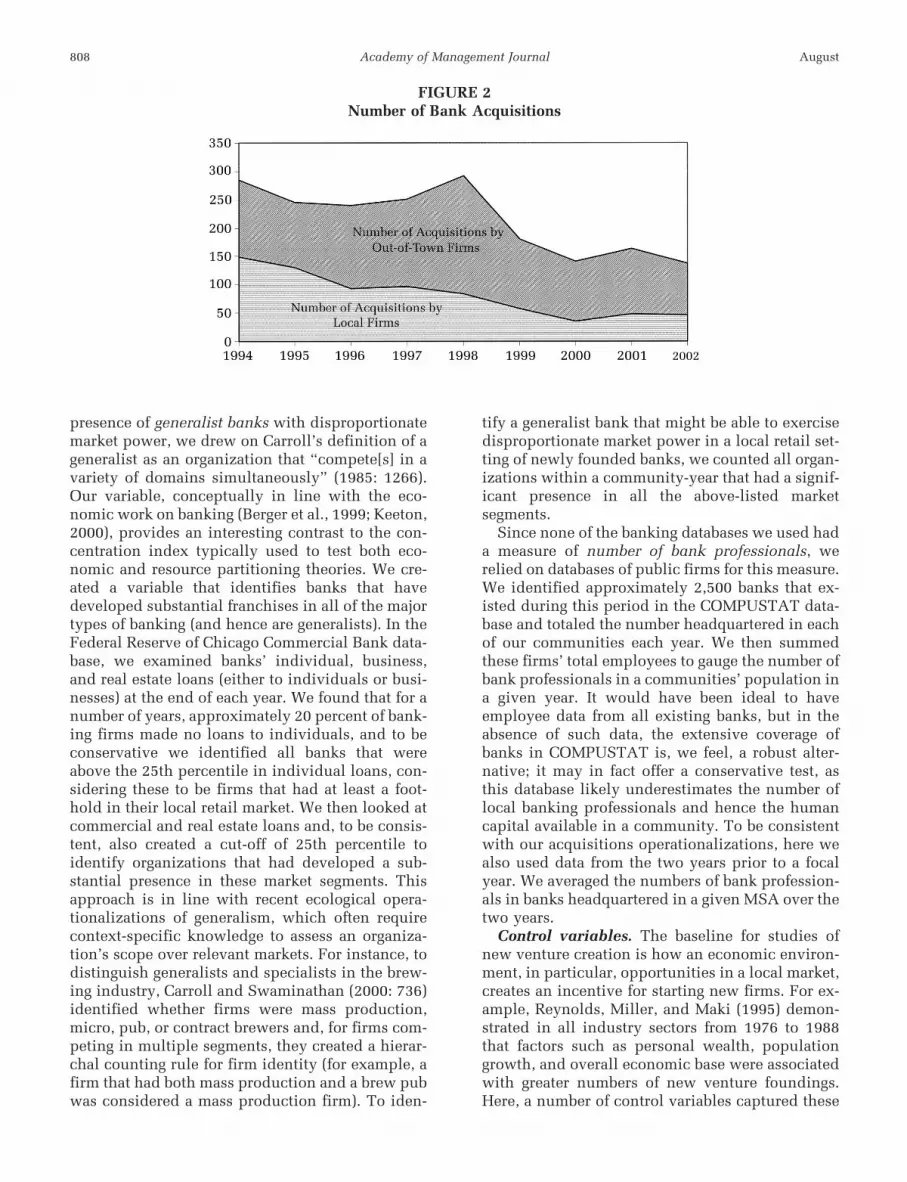

Independent variables. We created measures ofrecent bank acquisition activity in the communitieswe studied. Specifically, we counted the number ofacquisitions in MSA and divided the total intocounts of acquisitions in MSA by local firms, firmsthat would likely adhere to the same communitylogic as the firms they were acquiring, and acqui-sitions by out-of-town firms—firms that represent amore national logic of geographic diversification.4

Following the economic work on banking, we mea-sured these variables as the sum of the numbers ofacquisitions in the prior two years (Keeton, 2000).Use of this time period is corroborated by pressaccounts indicating that two years represents thelag between acquisitions and foundings (Epstein,1996). Of 1,939 acquisitions of smaller local banksduring the period 1994–2002, 1,195 were acquisi-tions by out-of-town firms, and 744 were acquisi-tions by other local firms.5 Figure 2 graphicallydepicts these acquisition trends.

In line with standard resource partitioning mea-surement (e.g., Carroll & Swaminathan, 2000), wemeasured market concentration as the four-firmconcentration ratio. This is a measure of the per-centage of bank deposits in each MSA held by thefour largest firms in the MSA. To measure the local

2 In its use of a count measure, this study divergesfrom the economic literature on bank founding, whichfocuses on dichotomous entry (Berger et al., 1999) or totalinitial assets (Keeton, 2000). Because our theory andhypotheses predict founding rates, not just where found-ings will occur, a count was better than an indicatorvariable. Also, total initial assets was not an appropriatemeasure for our study, as it describes initial bank suc-cess, not bank professionals’ motivation to found banks.

3 Much of the work on entrepreneurship and new or-ganizational founding has been criticized for its successbias (Ruef, Aldrich, & Carter, 2003), because firms andentrepreneurs are usually studied only after surviving foran undetermined period. But intense regulatory over-sight of the banking industry requires that newlyfounded banks file with multiple state and federal agen-cies before opening, and these same sources track thefinancial performance of firms from this point forward.Thus, studying foundings in the banking industry shouldprovide deeper insights into founding processes thanstudies that rely on retrospective accounts of survivors.

4 We also measured acquisitions by out-of-state firmsas one way to tap acquiring banks that may be larger andhence more likely to focus on center-of-the-market strat-egies, which are not as local and are more amenable toeconomies of scale. Results were quite consistent.

5 Our definition of mergers and acquisitions differsfrom definitions in prior economic work on banking;unlike Berger et al. (1999), we excluded all mergers thatoccurred within the same holding company. Although a“merger” of separately chartered banks in the same com-pany might be a source of customer disruptions thatcould lead to new bank foundings (Berger and col-leagues’ argument), our theory is based on new takeoversby out-of-town, national firms.

FIGURE 1Number of Bank Foundings

2007 807Marquis and Lounsbury

presence of generalist banks with disproportionatemarket power, we drew on Carroll’s definition of ageneralist as an organization that “compete[s] in avariety of domains simultaneously” (1985: 1266).Our variable, conceptually in line with the eco-nomic work on banking (Berger et al., 1999; Keeton,2000), provides an interesting contrast to the con-centration index typically used to test both eco-nomic and resource partitioning theories. We cre-ated a variable that identifies banks that havedeveloped substantial franchises in all of the majortypes of banking (and hence are generalists). In theFederal Reserve of Chicago Commercial Bank data-base, we examined banks’ individual, business,and real estate loans (either to individuals or busi-nesses) at the end of each year. We found that for anumber of years, approximately 20 percent of bank-ing firms made no loans to individuals, and to beconservative we identified all banks that wereabove the 25th percentile in individual loans, con-sidering these to be firms that had at least a foot-hold in their local retail market. We then looked atcommercial and real estate loans and, to be consis-tent, also created a cut-off of 25th percentile toidentify organizations that had developed a sub-stantial presence in these market segments. Thisapproach is in line with recent ecological opera-tionalizations of generalism, which often requirecontext-specific knowledge to assess an organiza-tion’s scope over relevant markets. For instance, todistinguish generalists and specialists in the brew-ing industry, Carroll and Swaminathan (2000: 736)identified whether firms were mass production,micro, pub, or contract brewers and, for firms com-peting in multiple segments, they created a hierar-chal counting rule for firm identity (for example, afirm that had both mass production and a brew pubwas considered a mass production firm). To iden-

tify a generalist bank that might be able to exercisedisproportionate market power in a local retail set-ting of newly founded banks, we counted all organ-izations within a community-year that had a signif-icant presence in all the above-listed marketsegments.

Since none of the banking databases we used hada measure of number of bank professionals, werelied on databases of public firms for this measure.We identified approximately 2,500 banks that ex-isted during this period in the COMPUSTAT data-base and totaled the number headquartered in eachof our communities each year. We then summedthese firms’ total employees to gauge the number ofbank professionals in a communities’ population ina given year. It would have been ideal to haveemployee data from all existing banks, but in theabsence of such data, the extensive coverage ofbanks in COMPUSTAT is, we feel, a robust alter-native; it may in fact offer a conservative test, asthis database likely underestimates the number oflocal banking professionals and hence the humancapital available in a community. To be consistentwith our acquisitions operationalizations, here wealso used data from the two years prior to a focalyear. We averaged the numbers of bank profession-als in banks headquartered in a given MSA over thetwo years.

Control variables. The baseline for studies ofnew venture creation is how an economic environ-ment, in particular, opportunities in a local market,creates an incentive for starting new firms. For ex-ample, Reynolds, Miller, and Maki (1995) demon-strated in all industry sectors from 1976 to 1988that factors such as personal wealth, populationgrowth, and overall economic base were associatedwith greater numbers of new venture foundings.Here, a number of control variables captured these

FIGURE 2Number of Bank Acquisitions

808 AugustAcademy of Management Journal

socioeconomic features of our communities. Fromthe U.S. Commerce Department, we obtained foreach of our community-years data on per capitaincome and population growth for the previousyear (thus, lagged one year). From the FDIC Sum-mary of Deposits database, we calculated the levelof local savings (deposits in thousands), an impor-tant measure of banking market attractiveness that,along with the size of a community, influencesbank founding activity (Rose, 1977; Siegfried &Evans, 1994).6 We used FDIC data through June 30for savings, but our dependent variable relies ondata through December 31, so the savings variableis lagged half a year. Since a large number of organ-izations can deplete available resources and de-press new foundings in a niche (Carroll & Hannan,2000), we included a measure of local organization-al density; this was the logarithm of a count, takenfrom the FDIC database, of the number of differentbanking institutions operating branches in a com-munity. To control for the wave of national mergers(Stearns & Allan, 1996), we included the number ofbank mergers that had occurred outside a focalcommunity in the previous two years and also alinear time trend variable (year) to account for thetime elapsed since the Riegle-Neil act.

Statistical Models

We followed Carroll and Swaminathan (2000)and modeled our counts of foundings in each com-munity as a zero-inflated Poisson model (Long,1997).7 This was the most appropriate model for anumber of reasons. First, approximately 84 percentof our community-year observations did not con-tain a founding event, which suggests that differentdynamics underlie the zero and nonzero observa-tions. A zero-inflated model estimates an outcomewith two equations, one predicting the occurrenceof nonzero counts and the other, the count offoundings. In modeling the zeros, we relied on theunderlying economic conditions of the communi-ties, reflected by the variables for populationgrowth and local savings. A Poisson model wasappropriate for the counts in this situation becausethe overdispersion in the data resulted entirely

from the zero observations. When the zero observa-tions were excluded, the mean and standard devi-ation were nearly identical. And a final consider-ation was that not all observations wereindependent, as community-level data were iden-tical for all organizations in each community. Tocorrect for this, we used the cluster subcommand inSTATA to adjust our standard errors to account forthe multiple observations per community.

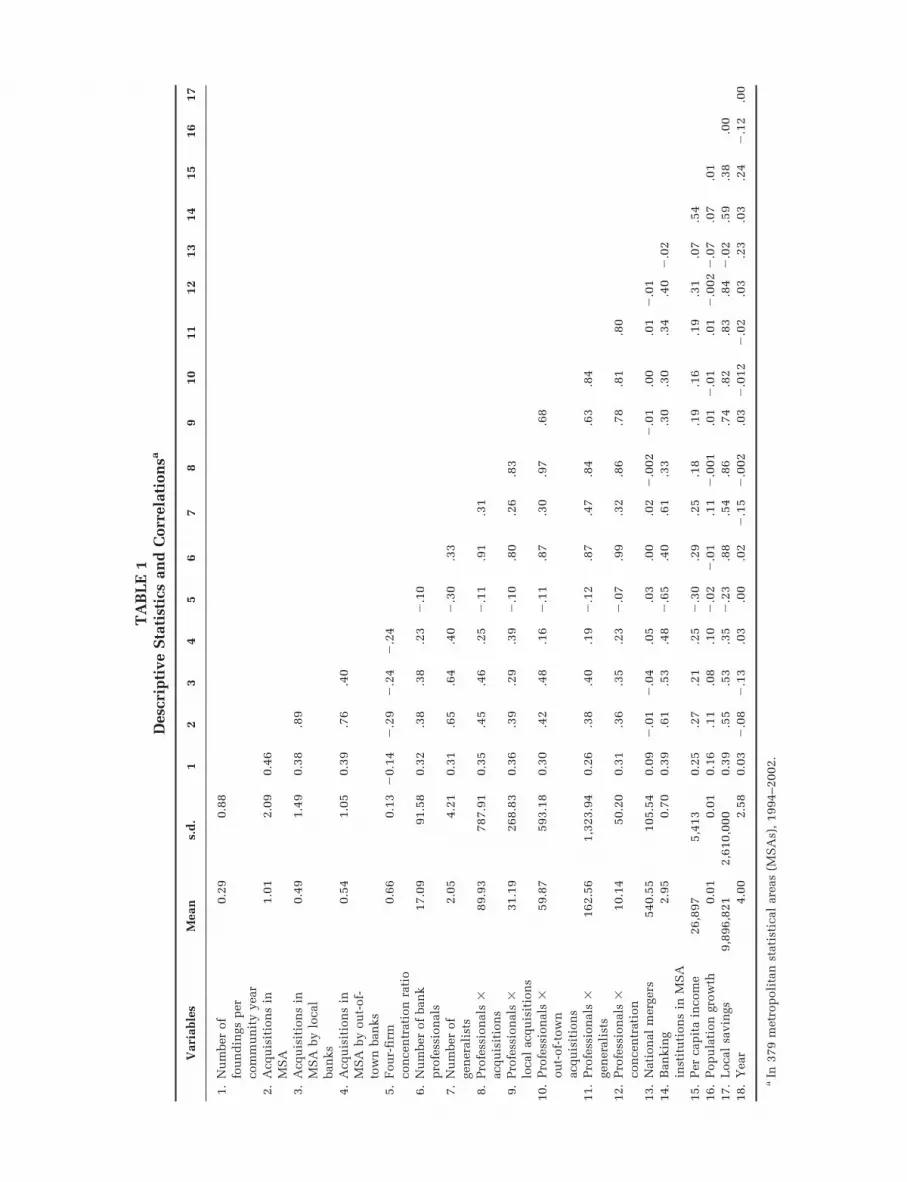

RESULTS

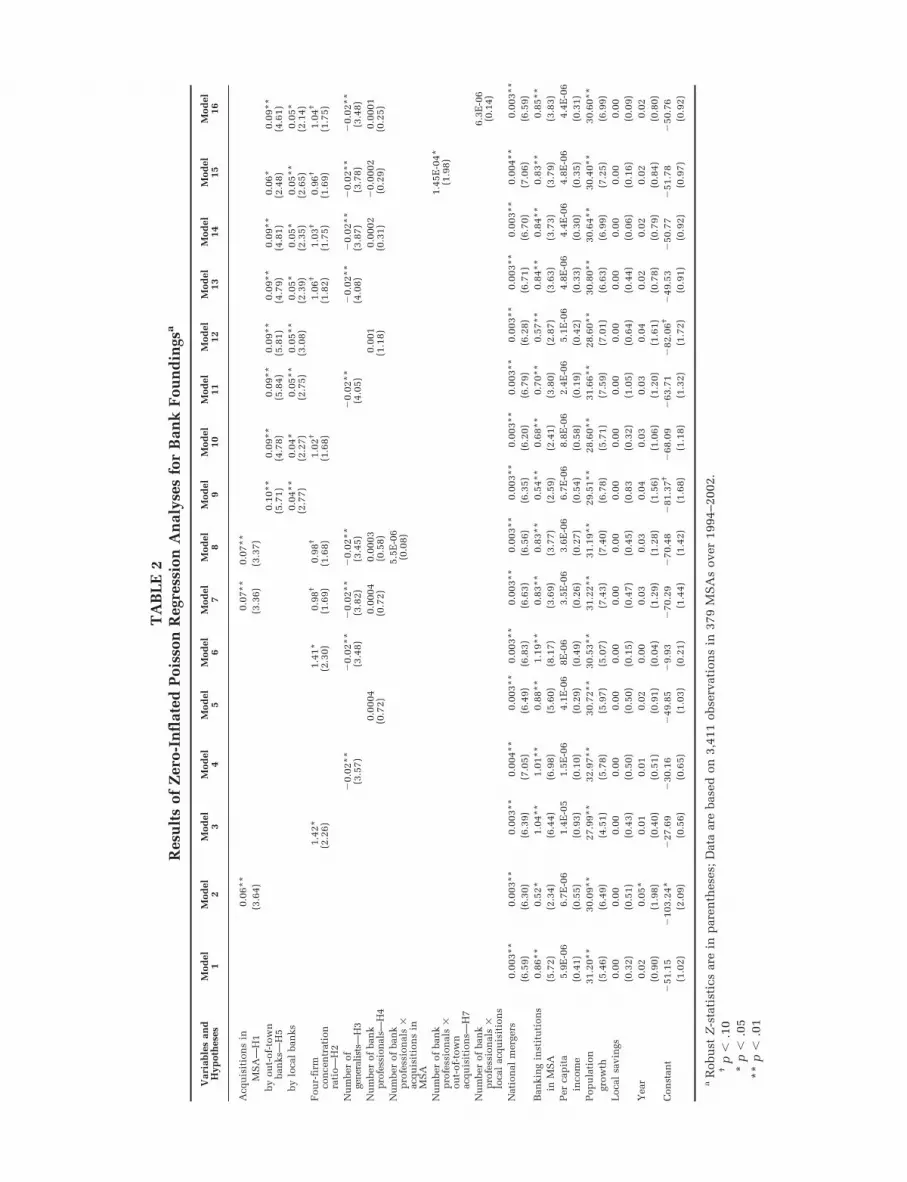

Table 1 presents descriptive statistics and corre-lations, and Table 2 gives the regression equationresults for the 379 communities from 1994 to 2002.In Table 2, we present a number of models forinformational purposes, indicating the associatedhypothesis number next to the appropriate vari-able. In models 1 to 8, we present models with all ofthe hypothesized main effects and the combinedacquisition variable. Models 9 to 16 are modelswith acquisitions decomposed into those by bankslocal to an MSA and those by out-of-town banks.

Model 1 presents only the control variables, andmodels 2 to 5 present this base model and maineffects relating to acquisitions, concentration, bankprofessionals, and generalist organizations. Giventhe close conceptual relationship between concen-tration and generalist organizations, we alsopresent an informational model with those twovariables (model 6). We begin interpreting our find-ings using model 7, the full model with all maineffects. Regarding Hypothesis 1, as predicted on thebasis of the standard explanations in the bankingliterature, the level of acquisitions in the previoustwo years is a strongly significant predictor of num-ber of foundings, which suggests that mergers in alocal environment establish the conditions for sub-sequent bank foundings. The concentration vari-able hypothesized to have a positive effect onfoundings in Hypothesis 2 is positive and statisti-cally significant at the 10 percent level (two-tailedtest) lending support to the standard resource par-titioning hypothesis. Conversely, there is alsostrong support for the dampening effect of powerfulgeneralist organizations in a community on bankfoundings, supporting Hypothesis 3. We considerthe potential sources and implications of these con-trasting findings in our Discussion (below). Theeffect of local bank professionals on foundings isnot statistically significant; hence, Hypothesis 4 isnot supported. As noted, however, because thismeasure underestimates the human capital in acommunity, it is likely a conservative test of ourclaims.

To better test our institutional ecology account

6 This variable is correlated at 0.92 with local popula-tion. Including local population did not change reportedresults, As a further sensitivity test, we also ran analyseson the 88 cities with over one million in population andagain, results are consistent.

7 ZIP command in STATA; we also ran the modelsusing a negative binomial specification with similarresults.

2007 809Marquis and Lounsbury

TA

BL

E1

Des

crip

tive

Sta

tist

ics

and

Cor

rela

tion

sa

Var

iabl

esM

ean

s.d

.1

23

45

67

89

1011

1213

1415

1617

1.N

um

ber

offo

un

din

gsp

erco

mm

un

ity

year

0.29

0.88

2.A

cqu

isit

ion

sin

MS

A1.

012.

090.

46

3.A

cqu

isit

ion

sin

MS

Aby

loca

lba

nks

0.49

1.49

0.38

.89

4.A

cqu

isit

ion

sin

MS

Aby

out-

of-

tow

nba

nks

0.54

1.05

0.39

.76

.40

5.F

our-

firm

con

cen

trat

ion

rati

o0.

660.

13�

0.14

�.2

9�

.24

�.2

4

6.N

um

ber

ofba

nk

pro

fess

ion

als

17.0

991

.58

0.32

.38

.38

.23

�.1

0

7.N

um

ber

ofge

ner

alis

ts2.

054.

210.

31.6

5.6

4.4

0�

.30

.33

8.P

rofe

ssio

nal

s�

acqu

isit

ion

s89

.93

787.

910.

35.4

5.4

6.2

5�

.11

.91

.31

9.P

rofe

ssio

nal

s�

loca

lac

quis

itio

ns

31.1

926

8.83

0.36

.39

.29

.39

�.1

0.8

0.2

6.8

3

10.

Pro

fess

ion

als

�ou

t-of

-tow

nac

quis

itio

ns

59.8

759

3.18

0.30

.42

.48

.16

�.1

1.8

7.3

0.9

7.6

8

11.

Pro

fess

ion

als

�ge

ner

alis

ts16

2.56

1,32

3.94

0.26

.38

.40

.19

�.1

2.8

7.4

7.8

4.6

3.8

4

12.

Pro

fess

ion

als

�co

nce

ntr

atio

n10

.14

50.2

00.

31.3

6.3

5.2

3�

.07

.99

.32

.86

.78

.81

.80

13.

Nat

ion

alm

erge

rs54

0.55

105.

540.

09�

.01

�.0

4.0

5.0

3.0

0.0

2�

.002

�.0

1.0

0.0

1�

.01

14.

Ban

kin

gin

stit

uti

ons

inM

SA

2.95

0.70

0.39

.61

.53

.48

�.6

5.4

0.6

1.3

3.3

0.3

0.3

4.4

0�

.02

15.

Per

cap

ita

inco

me

26,8

975,

413

0.25

.27

.21

.25

�.3

0.2

9.2

5.1

8.1

9.1

6.1

9.3

1.0

7.5

416

.P

opu

lati

ongr

owth

0.01

0.01

0.16

.11

.08

.10

�.0

2�

.01

.11

�.0

01.0

1�

.01

.01

�.0

02�

.07

.07

.01

17.

Loc

alsa

vin

gs9,

896,

821

2,61

0,00

00.

39.5

5.5

3.3

5�

.23

.88

.54

.86

.74

.82

.83

.84

�.0

2.5

9.3

8.0

018

.Y

ear

4.00

2.58

0.03

�.0

8�

.13

.03

.00

.02

�.1

5�

.002

.03

�.0

12�

.02

.03

.23

.03

.24

�.1

2.0

0

aIn

379

met

rop

olit

anst

atis

tica

lar

eas

(MS

As)

,19

94–2

002.

TA

BL

E2

Res

ult

sof

Zer

o-In

flat

edP

oiss

onR

egre

ssio

nA

nal

yses

for

Ban

kF

oun

din

gsa

Var

iabl

esan

dH

ypot

hes

esM

odel

1M

odel

2M

odel

3M

odel

4M

odel

5M

odel

6M

odel

7M

odel

8M

odel

9M

odel

10M

odel

11M

odel

12M

odel

13M

odel

14M

odel

15M

odel

16

Acq

uis

itio

ns

in0.

06**

0.07

**0.

07**

MS

A—

H1

(3.6

4)(3

.36)

(3.3

7)by

out-

of-t

own

ban

ks—

H5

0.10

**(5

.71)

0.09

**(4

.78)

0.09

**(5

.84)

0.09

**(5

.81)

0.09

**(4

.79)

0.09

**(4

.81)

0.06

*(2

.48)

0.09

**(4

.61)

bylo

cal

ban

ks0.

04**

(2.7

7)0.

04*

(2.2

7)0.

05**

(2.7

5)0.

05**

(3.0

8)0.

05*

(2.3

9)0.

05*

(2.3

5)0.

05**

(2.6

5)0.

05*

(2.1

4)F

our-

firm

con

cen

trat

ion

rati

o—H

2

1.42

*(2

.26)

1.41

*(2

.30)

0.98

†

(1.6

9)0.

98†

(1.6

8)1.

02†

(1.6

8)1.

06†

(1.8

2)1.

03†

(1.7

5)0.

96†

(1.6

9)1.

04†

(1.7

5)

Nu

mbe

rof

gene

ralis

ts—

H3

�0.

02**

(3.5

7)�

0.02

**(3

.48)

�0.

02**

(3.8

2)�

0.02

**(3

.45)

�0.

02**

(4.0

5)�

0.02

**(4

.08)

�0.

02**

(3.8

7)�

0.02

**(3

.78)

�0.

02**

(3.4

8)N

um

ber

ofba

nk

pro

fess

ion

als—

H4

0.00

04(0

.72)

0.00

04(0

.72)

0.00

03(0

.58)

0.00

1(1

.18)

0.00

02(0

.31)

�0.

0002

(0.2

9)0.

0001

(0.2

5)N

um

ber

ofba

nk

pro

fess

ion

als

�ac

quis

itio

ns

inM

SA

5.5E

-06

(0.0

8)

Nu

mbe

rof

ban

kp

rofe

ssio

nal

s�

out-

of-t

own

acqu

isit

ion

s—H

7

1.45

E-0

4*(1

.98)

Nu

mbe

rof

ban

kp

rofe

ssio

nal

s�

loca

lac

quis

itio

ns

6.3E

-06

(0.1

4)

Nat

ion

alm

erge

rs0.

003*

*0.

003*

*0.

003*

*0.

004*

*0.

003*

*0.

003*

*0.

003*

*0.

003*

*0.

003*

*0.

003*

*0.

003*

*0.

003*

*0.

003*

*0.

003*

*0.

004*

*0.

003*

*(6

.59)

(6.3

0)(6

.39)

(7.0

5)(6

.49)

(6.8

3)(6

.63)

(6.5

6)(6

.35)

(6.2

0)(6

.79)

(6.2

8)(6

.71)

(6.7

0)(7

.06)

(6.5

9)B

anki

ng

inst

itu

tion

s0.

86**

0.52

*1.

04**

1.01

**0.

88**

1.19

**0.

83**

0.83

**0.

54**

0.68

**0.

70**

0.57

**0.

84**

0.84

**0.

83**

0.85

**in

MS

A(5

.72)

(2.3

4)(6

.44)

(6.9

8)(5

.60)

(8.1

7)(3

.69)

(3.7

7)(2

.59)

(2.4

1)(3

.80)

(2.8

7)(3

.63)

(3.7

3)(3

.79)

(3.8

3)P

erca

pit

a5.

9E-0

66.

7E-0

61.

4E-0

51.

5E-0

64.

1E-0

68E

-06

3.5E

-06

3.6E

-06

6.7E

-06

8.8E

-06

2.4E

-06

5.1E

-06

4.8E

-06

4.4E

-06

4.8E

-06

4.4E

-06

inco

me

(0.4

1)(0

.55)

(0.9

3)(0

.10)

(0.2

9)(0

.49)

(0.2

6)(0

.27)

(0.5

4)(0

.58)

(0.1

9)(0

.42)

(0.3

3)(0

.30)

(0.3

5)(0

.31)

Pop

ula

tion

31.2

0**

30.0

9**

27.9

9**

32.9

7**

30.7

2**

30.5

3**

31.2

2**

31.1

9**

29.5

1**

28.6

0**

31.6

6**

28.6

0**

30.8

0**

30.6

4**

30.4

0**

30.6

0**

grow

th(5

.46)

(6.4

9)(4

.51)

(5.7

8)(5

.97)

(5.0

7)(7

.43)

(7.4

0)(6

.78)

(5.7

1)(7

.59)

(7.0

1)(6

.63)

(6.9

9)(7

.25)

(6.9

9)L

ocal

savi

ngs

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

(0.3

2)(0

.51)

(0.4

3)(0

.50)

(0.5

0)(0

.15)

(0.4

7)(0

.45)

(0.8

3(0

.32)

(1.0

5)(0

.64)

(0.4

4)(0

.06)

(0.1

6)(0

.09)

Yea

r0.

020.

05*

0.01

0.01

0.02

0.00

0.03

0.03

0.04

0.03

0.03

0.04

0.02

0.02

0.02

0.02

(0.9

0)(1

.98)

(0.4

0)(0

.51)

(0.9

1)(0

.04)

(1.2

9)(1

.28)

(1.5

6)(1

.06)

(1.2

0)(1

.61)

(0.7

8)(0

.79)

(0.8

4)(0

.80)

Con

stan

t�

51.1

5�

103.

24*

�27

.69

�30

.16

�49

.85

�9.

93�

70.2

9�

70.4

8�

81.3

7†�

68.0

9�

63.7

1�

82.0

6†�

49.5

3�

50.7

7�

51.7

8�

50.7

6(1

.02)

(2.0

9)(0

.56)

(0.6

5)(1

.03)

(0.2

1)(1

.44)

(1.4

2)(1

.68)

(1.1

8)(1

.32)

(1.7

2)(0

.91)

(0.9

2)(0

.97)

(0.9

2)

aR

obu

stZ

-sta

tist

ics

are

inp

aren

thes

es;

Dat

aar

eba

sed

on3,

411

obse

rvat

ion

sin

379

MS

As

over

1994

–200

2.†

p�

.10

*p

�.0

5**

p�

.01

focused on competing logics, we shifted to a seriesof models embodying a finer-grained conceptual-ization of acquisitions, separating out those madeby firms from outside a focal community. Models 9through 13, which are presented only for informa-tional purposes, show the effects of the main vari-ables of interest when they are included with thetwo types of acquisitions, mirroring the modelsdescribed above. In model 14, we present tests ofHypotheses 5 and 6, which focus on how out-of-town acquisitions are the most important drivers offoundings, not acquisitions more generally. Theout-of-town acquisitions variable is strongly signif-icant, providing support for Hypothesis 5. Note thatlocal acquisitions is also significant, which sug-gests that some of the economics arguments under-lying Hypothesis 1 may hold as well. We are heart-ened by the fact, however, that the coefficient forout-of-town acquisitions is actually much largerthan that for local acquisitions (�2 � 24.45, df � 2,p � .00001), which supports Hypothesis 6. Thus,although the economics explanation of this rela-tionship in terms of market pressure may be par-tially true, our hypotheses and results suggest thatfirms from outside a community face different andmore substantial pressures, likely relating to thehistorically rooted resistance to outsider banks wedescribed earlier.

Model 15 presents our tests of Hypothesis 7, stat-ing that acquisitions made by out-of-town banks area positive moderator of the effect of the number ofbanking professionals on new bank foundings. Aspredicted, this coefficient is positive, supportingHypothesis 7 regarding interaction between num-

ber of bank professionals and community resis-tance. Note the contrast between model 15 andmodels 8 and 16, in which we show the interac-tions between bank professionals and total and lo-cal acquisitions, respectively. Neither is signifi-cant, which suggests that it is not acquisitions perse that are important to understanding communityresistance to national banks, but that—in keepingwith our theory and many anecdotal examples—acquisitions pursued by out-of-town banks are thesalient events that spur action by local profession-als. To aid visualization of this effect, in Figure 3we graph the predicted effects of the banking pro-fessional interaction with out-of-town acquisitionsusing a method from Stewart and Barrick (2000). Inthis graph, we show the effects on number of banksfounded in a community for two levels of out-of-town acquisitions, low (minus one standard devia-tion from the mean) and high (plus one standarddeviation from the mean). We then plotted thenumber of banking foundings regressed on differ-ent levels of local bank professionals. Figure 3shows that the highest level of bank foundings in acommunity occurred when both bank professionalsand out-of-town acquisitions were high. From ouranalyses, we conclude that out-of-town acquisi-tions accentuate the effect of professionals on newbank foundings in communities to a much greaterdegree than acquisitions by local firms.

Results of the control variables are all as wouldbe expected on the basis of the existing banking(e.g., Berger et al., 1999) and entrepreneurship(Reynolds, Miller, & Maki, 1995) literatures. As ex-pected, banks are founded where there is already a

FIGURE 3Effect on New Bank Foundings of the Interaction of the Numbers of

Banking Professionals and Out-of-Town Acquisitions, 1994–2002

812 AugustAcademy of Management Journal

significant banking presence and the population ofbanks is expanding. Further, a variable capturingthe national merger wave (acquisitions from out-side a focal community) was significant, furthersuggesting that the national consolidation spurredthe new bank foundings we observed.

These results as a whole illustrate the complexityof new bank foundings in local communities andprovide substantial support for our perspective onhow competing institutional logics facilitate resis-tance to change. Although existing predictions re-garding competitive processes stemming from eco-nomics in some sense set the baseline for studies ofcommunity bank foundings, our results suggestthat economics does not provide the whole story.Building on the long-standing tension between na-tional and community logics, our results highlighthow this conflict persists and how the context ofcommunity banking remains highly politicized. Lo-cal banking professionals founded new banks inthe wake of out-of town acquisitions and, just asstrenuously, larger national banks strove to main-tain their market power. We discuss implicationsfor theories of institutional change and resistancebelow.

DISCUSSION AND CONCLUSIONS

In this article, we explored how the growingdominance of nationally oriented banks has beenresisted in some U.S. communities. Following legalchanges that allowed and encouraged banks to ex-tend their reaches beyond the states where theirheadquarters were located, acquisitions by banksseeking to expand their domains increased dramat-ically. In some communities, local politicians, cit-izens, activists, and consumers contested this pro-cess, shifting their banking to firms that were moreconsistent with their ideology of and interest inlocally headquartered financial institutions. Empir-ically, we specifically explored how the growth ofbank acquisitions by outsider, national firms fos-tered resistance in the form of new communitybank creation. Focusing on the historically rootedcompeting logics underlying the organization ofU.S. banking enabled us to provide a nuanced ac-count that goes beyond extant explanations of thisphenomenon to illuminate the conditions underwhich professionals in a community can resistbroader consolidation efforts.

Although our evidence supports some generalarguments in the banking literature that bank ac-quisitions can spur new bank creation in a commu-nity (e.g., Berger et al., 1999), this existing explana-tion does not go far enough in specifying andtesting the particular mechanisms through which

and conditions under which acquisitions drivebank foundings. We drew on institutional and eco-logical approaches to organizational analysis—es-pecially on recent efforts to understand how com-peting logics create variation in the practices andbehaviors of distinct groups of actors—to focus at-tention on the dynamics that undergird nationalbank expansion and the countermovement of newcommunity bank creation. We showed that, underconditions of acquisition-driven expansion of na-tional banks, a community’s ability to spawn as acountervailing force new, local banks depended onthe existence of a pool of professional bankers. Weshowed the effect of professionally driven localbank creation to be even greater when acquisitionsin a community were specifically undertaken byout-of-town, national banks. This finding supportsour contention that the creation of new banks incommunities was a form of resistance to the effortsof national banks to control resource allocation de-cisions in those communities.

Contributions to Institutional Ecology

Our findings are of interest to scholars forging aninstitutional ecology approach, especially thosewho focus on resource partitioning and organiza-tional founding processes. An important point ofdeparture from other ecological work that analyzesindustry dynamics and career mobility (Haveman &Cohen, 1994; Stuart & Sorenson, 2003) is that ourmodel focuses on the founding of new firms as aninteraction between local professionals and organ-izational dynamics. Our work extends this streamby emphasizing how competing logics, particularlythose rooted in geographic difference (Lounsbury,2007; Marquis et al., 2007), both influence theseprocesses and offer a more refined understandingof the relationship between acquisitions and found-ings. Although Haveman and Cohen (1994) showedhow mergers among California savings and loansenabled first-order mobility for bank executives,they also posited a second-order effect of blockedmobility. Even though they did not focus on newbank creation, to the extent that acquisitions facil-itate foundings by professionals, mobility may beenhanced both directly and indirectly.

That is, bank creation by professionals exiting anacquired bank may provide a model for other pro-fessionals to follow and create more new banks. Inaddition, new bank creation further increases mo-bility for professionals, opening up possibilities tojoin more independent community-oriented banks;Haveman and Cohen (1994) actually supported thisassociation, showing that many professionals mi-grate to newly founded banks after their current

2007 813Marquis and Lounsbury

banks have been acquired. Further work is neededto specify the conditions under which the indirecteffect of mergers and acquisitions enhances mobil-ity, and such work will require finer-grained dataon individual professionals and their movementsbetween organizations.

An additional distinction between the currentstudy and the ecological literature is that we at-tempted to tease apart the concentration-based ar-guments underlying resource partitioning and themarket power arguments typically made by econo-mists (Amel & Liang, 1997; Scherer, 1980). Nottypically seen as competing approaches, these twoliteratures in fact contain opposite predictions andfindings regarding the effects of market concentra-tion. To that end, we find that both processes existand that some of the divergent findings may relateto measurement issues. Given our results, we deemconcentration, which suggests a crowding of mar-ket niches, to be a better measure of resource par-titioning, but we consider measures such as ours—measures that tap the existence of dominantgeneralist organizations (as distinct from concen-tration)—to be better operationalizations of econo-mists’ market power arguments. Our results suggestthat market power can come from organizationalcharacteristics other than size and that the presenceof powerful generalists and market concentrationcan be distinct phenomena, despite being typicallydiscussed as similar in both of these literatures.Future researchers may want to explore these pro-cesses in more detail.

Although the concentration results are a nice cor-roboration of existing resource partitioning find-ings, we feel our study goes beyond standard re-source partitioning theory in at least a couple ofimportant ways that we hope will aid future schol-ars in that area. First, focusing our analyses on ashort period allowed us to uncover some of thedetailed activity and mechanisms—in this case,competing logics and the human capital of profes-sionals—underlying observed relationships thatthe generally long-term historical perspective ofecologists may mask. Consolidation typically oc-curs in a punctuated fashion (Stearns & Allan,1996), and so looking at periods of intense consol-idation is particularly valuable for testing a theorythat analyses such punctuated processes. Second,we extend the cultural approach to consumptionproffered by Carroll and Swaminathan (2000) toencompass the cultural ideology and motivationsof entrepreneurs, particularly in situations markedby different visions of industry organization(Lounsbury, 2007). Such a direction suggests anopportunity for a more complete engagement be-tween the institutional and ecological literatures

and the scholarship on entrepreneurship (see, e.g.,Aldrich & Ruef, 2006).

Resistance and Institutional Change

Consolidation and concentration may be baselineconditions for studies of new firm creation in theU.S. banking industry, but our results suggest thatunderstanding the opposing logics that have under-girded competition in the history of U.S. bankingprovides additional insight into how the structureof community banking has changed recently. Whenout-of-town banks, carriers of a national logic ofgarnering efficiencies from geographic diversifica-tion, invaded communities by acquiring localfirms, some community members resisted these ef-forts and supported foundings of new firms thatmore authentically tapped their values. Thus, eventhough institutionalists have suggested that profes-sionals can play a key role as institutional entre-preneurs who create and catalyze institutionalchange (e.g., Battilana, 2006; DiMaggio, 1991; Scott,2001), here we emphasize that the actions of suchprofessionals are fundamentally shaped by broaderinstitutional logics.