upper canada insurance

TRANSCRIPT

Executive Summary

Situational Analysis Overview

Upper Canada Insurance (UCI) in Toronto is a subsidiary of The

Bank of Upper Canada (Upper Canada), which is one of the large

financial institutions in Canada. In less than 8 years, Upper

Canada Insurance has developed various products, including

home, auto, travel, health and life insurance. Its life

insurance falls into the category of term-life product, which

is usually sold to parents or a family who has dependent

children. This insurance company has gotten strong financial

support and a stable source of customers from Upper Canada,

which has made it more competitive. However, the life

insurance part has operated at a loss of around $19,310,718

annually because of high wastage. The company’s business

integration specialist, Deborah McDonald, is looking for

solutions to deal with the high wastage from an inefficient

life insurance applicant process.

SWOT Analysis

One of the biggest strengths of UCI is that it can get strong

financial support from Upper Canada, which also guarantees a

stable source of customers. The diversified insurance products

strengthen its competitive advantage as well. Poor customer

1

service and the tedious application process are two main

weaknesses that exist in UCI. The trend of capital

globalization offers the company an opportunity to draw more

customers and make good use of cheaper labor from developing

countries. In addition, the development of technology would

enhance the working efficiency greatly; however, the large

number of competitors has also brought a threat to its

financial success.

Problem Analysis

The high number of applicants withdrawing from the life

insurance application process before completion is the main

problem for UCI. This problem results from a tedious

application process, a lack of communication and poor customer

service.

Alternatives and Decision Criteria

Simplifying the working process, creating an official website

and offering work training for employees are three

alternatives that could address the problems that concern

McDonald. There are three criteria used to assess a

recommendation; it should be quick to implement (within one

months); it should save time processing consumer applications;

2

it should help the company lower the operation cost by

$811,300.

Recommendation

The recommendation is to simplify the working process. This

includes two parts: buying two scanners from Amazon and

setting up appointments for phone interviews where life

insurance advisors (LIA) can complete the initial application

over the phone.

Action Plan

Five critical steps need to be implemented immediately. First,

the company’s buyer should purchase two more scanner machines

online by Nov. 1st. On Nov 2nd, McDonald should modify the

initial application form by adding an additional column for

the appointment date and inform the office manager this

change. On the next day, the office manager will inform all 16

LIA about their duties. The support staff will complete the

installment on Nov 4th. On Nov. 7, the PR manager will be

responsible for contacting the health firm and informing them

about the change to the application form. One of the possible

issues is that the LIA may have complaints about the

additional duty. In this case, the LIA’s morale will decrease.

3

In order to solve this problem, the company could provide more

benefits to the LIA (such as more vacation days or bonuses).

Situation Analysis

Upper Canada Insurance in Toronto (UCI) is a subsidiary of

the Bank of Upper Canada (Upper Canada), which is one of the

large financial institutions in Canada. In less than 8 years,

Upper Canada Insurance has developed various products,

including home, auto, travel, health and life insurance. Its

life insurance falls into the term-life product category.

Upper Canada Insurance has gotten strong financial support and

a stable source of customers from Upper Canada, which has made

it more competitive. However, the life insurance part has

4

operated at a loss of around $19,310,718 annually (see Exhibit

1) because of high wastage. The company’s business integration

specialist, Deborah McDonald, is looking for solutions to deal

with the high wastage from an inefficient life insurance

applicant process.

One of the biggest strengths of Upper Canada Insurance is

that it can get strong financial support from the Bank of

Upper Canada, which also guarantees a stable source of

customers. The tedious application process and poor customer

service are two weaknesses of Upper Canada Insurance. Based on

customer surveys, many clients have not been satisfied with

5

the service that is offered by the company. In addition, it

takes a long time (5-7weeks) to complete the Upper Canada

Insurance application process; hence, the clients have had to

wait for a long time to get a response. A lack of

communication between customers and Upper Canada Insurance has

even made the situation worse.

The continuing trend of consolidation can be an opportunity

for this company. Upper Canada Insurance can increase its

company size, total assets, and competitive advantages through

consolidation. The trend of capital globalization offers the

company an opportunity to draw more customers and make good

6

use of cheaper labor from developing countries. In addition,

the development of technology greatly enhances the work

efficiency. The threat is that the whole insurance industry is

highly competitive. Only five companies in Canada account for

almost three fifths of all premiums. Legislative changes have

also allowed many more banks to easily enter the insurance

industry. Therefore, the number of the insurance companies has

increased a lot. Also, many companies have been competing on

price and selling directly to consumers.

Problem Analysis

The company faces a very serious problem. The wastage rate

7

on life insurance applications is 45 per cent, which is

relatively high compared to the industry average. Its clients

wait for a long time to get a response, causing them to

abandon applications. There are three obvious causes. Firstly,

it takes at least five weeks to complete the application due

to uneven distribution of employees’ duties. Secondly,

although each of the five parts of the application process has

enough employees to finish their tasks, the inefficiency of

some employees leads to the wasting of time. Finally, a lack

of communication and poor customer service results in clients

abandoning the application process. The application process

8

causes a long response time for customers, and it has also

damaged the reputation of the company. In addition, the whole

application process costs UCI about $600 to $700 per

application and total $29243100 (see Exhibit 2). McDonald only

has one month to present her assessment and recommendations.

Therefore, it is urgent for McDonald to solve the problem

quickly.

Alternative Identification

There are three alternatives. The first alternative is to

simplify the working process by adding two additional scanners

on the fourth floor and making an appointment with applicants

9

in advance. The 16 LIA will take only 6.7 hours (see Exhibit

3) for completing their daily work. Assume each LTA will work

8 hours per workday, so there is sufficient time for them to

do the additional tasks. The scanners will cost $1200 in

total. The second alternative is to create an official

website, on which customers can check their application and

address their concerns throughout the process. The company

needs to hire three additional LIA to answer customers’

questions through the website. The cost is $258,240 (see

Exhibit 5). The third alternative is to offer work training

for employees by hiring a trainer who has professional

10

customer service orientation knowledge. This training will be

held every weekend. The company needs to pay the trainer

$2,250 (see Exhibit 6).

Decision Criteria

The first decision is to reduce the application cost by

$811300 (see Exhibit 2). The previous application cost ($600-

700/application) is extremely high. We want to lower that cost

to $450 (see Exhibit 2). The second decision is to reduce the

application process time to two to four weeks. This is a

reasonable time for a normal application process. The last

decision is that the action should have an impact as soon as

11

possible. Specifically, the action should be implemented

within the urgency period, which is one month. Based on Upper

Canada Insurance’s current situation, McDonald only has half

of a month to present her assessment and recommendations.

Beginning on October 19th and ending at the end of the month,

there is only 13 days for McDonald to implement her

recommendation. The next half month will be used to estimate

whether or not the action is helpful. Hence, the criteria for

this decision are really important for the business.

Analysis of Alternatives

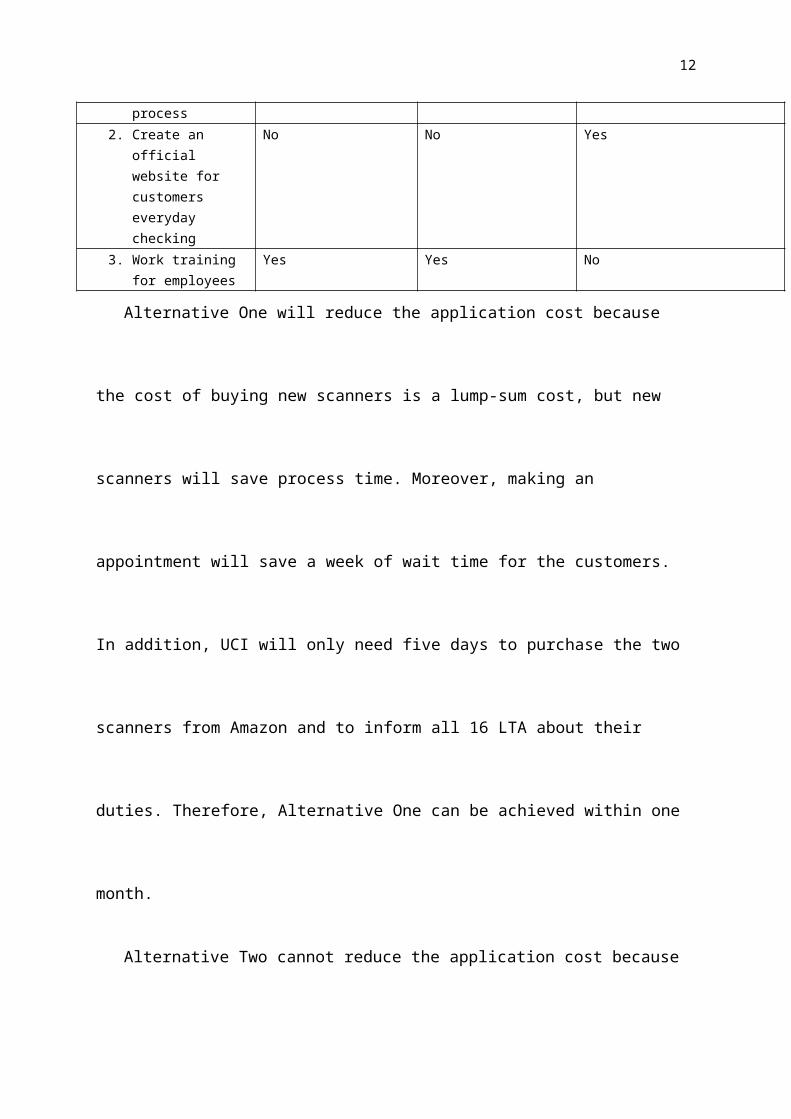

DecisionAlternative

Reduce applicationcost by $811300

Reduce the processtime to2 - 4 weeks

Quick to implement within 1 month

1. Simplify the working

Yes Yes Yes

12

process2. Create an

official website for customers everyday checking

No No Yes

3. Work training for employees

Yes Yes No

Alternative One will reduce the application cost because

the cost of buying new scanners is a lump-sum cost, but new

scanners will save process time. Moreover, making an

appointment will save a week of wait time for the customers.

In addition, UCI will only need five days to purchase the two

scanners from Amazon and to inform all 16 LTA about their

duties. Therefore, Alternative One can be achieved within one

month.

Alternative Two cannot reduce the application cost because

13

the company needs to hire three additional LIA to answer

customers’ questions through the website. The cost is $258,240

(see Exhibit 5). This alternative increases customers’

satisfaction, but it does not reduce process time. In

addition, because the company already has online access, it

will be easy to implement within one month. UCI need to spend

one week to look for LTA from outside of the company; then the

company spend one day to do an interview, and select three

competent LTA through those interviewees.

Alternative Three will reduce the cost because training can

enhance employees’ efficiency at work. The employees will use

14

less time to do more tasks. Therefore, the total process time

can be reduced. If the total process time is decreased, the

total application cost will also be decreased. However,

training will cost half of a month to implement, and McDonald

only has one month to resolve the issue for Upper Canada

Insurance.

Recommendation, Reaction & Results

The recommendation is to simplify the application process

by adding one additional scanner on the fourth floor and

making appointments with customers in advance. LIA will

basically complete their work and transfer a specific

15

interview time to a third party. The new scanner will shorten

the waiting time for coordinators and enhance their efficiency

to some degree. If this recommendation is put into practice,

it will lead to one of these three results: it will complete

entire applications within two to four weeks with a 32%

wastage rate, which is the lower standard; the wastage rate

will decrease to 38%, which is neither good nor bad; the

wastage rate will remain the same or go even higher (see

Exhibit 4). The company will increase the workload for LIA, so

they may complain about a lot of things and do an inefficient

job. This could also lead to increasing complaints from

16

customers. Furthermore, if the new scanners break down,

coordinators will have to go down to the copy center in the

basement, which will waste more of the coordinators time.

These would lead to the worst case scenario.

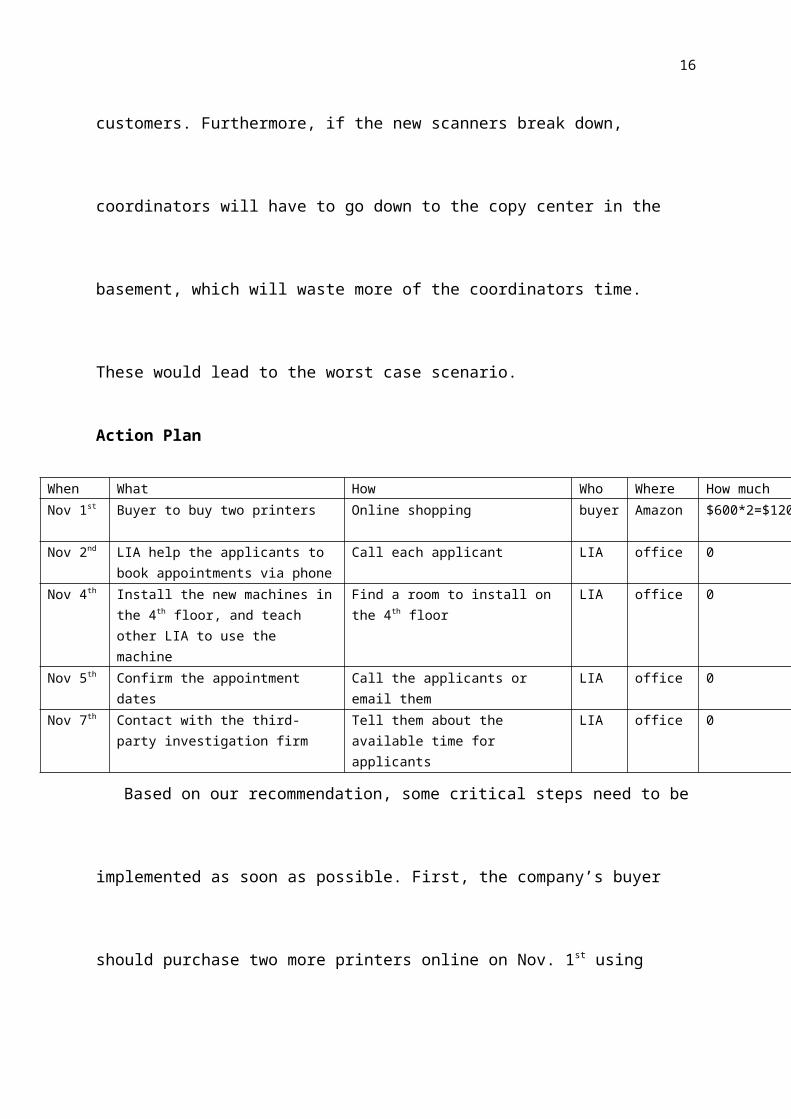

Action Plan

When What How Who Where How muchNov 1st Buyer to buy two printers Online shopping buyer Amazon $600*2=$1200

Nov 2nd LIA help the applicants to book appointments via phone

Call each applicant LIA office 0

Nov 4th Install the new machines inthe 4th floor, and teach other LIA to use the machine

Find a room to install on the 4th floor

LIA office 0

Nov 5th Confirm the appointment dates

Call the applicants or email them

LIA office 0

Nov 7th Contact with the third-party investigation firm

Tell them about the available time for applicants

LIA office 0

Based on our recommendation, some critical steps need to be

implemented as soon as possible. First, the company’s buyer

should purchase two more printers online on Nov. 1st using

17

Amazon, which will cost $1200 ($600/printer). On Nov 2nd, all

16 LIA should make a phone call to book an appointment for a

health investigation firm, a third-party, to speak with the

clients when they complete the initial application.

Consequently, the investigation firm will be able to save at

least one week by reaching the applicant earlier. The next

critical step is to install two new machines on Nov 4th by

choosing two of the LIA who have computer skills to help the

company install them on the fourth floor so that the

coordinators do not need to go to the copy center in the

basement. Furthermore, these two machines will only be used

18

for staff in the fourth floor, so it won’t be that busy. On

Nov 5th, LIA should make a second phone call to remind the

applicants and to confirm their appointment date. On Nov 7th,

LIA should contact the third-party health investigation firm

and inform them about the applicants’ available time.

There are still many problems that may occur during these

steps. The first problem is that LIAs’ morale could decrease

due to them having extra tasks. In order to solve this

problem, the company should provide more benefits for the LIA.

For example, it could provide more annual vacation days or

reimburse part of their personal phone bill.

19

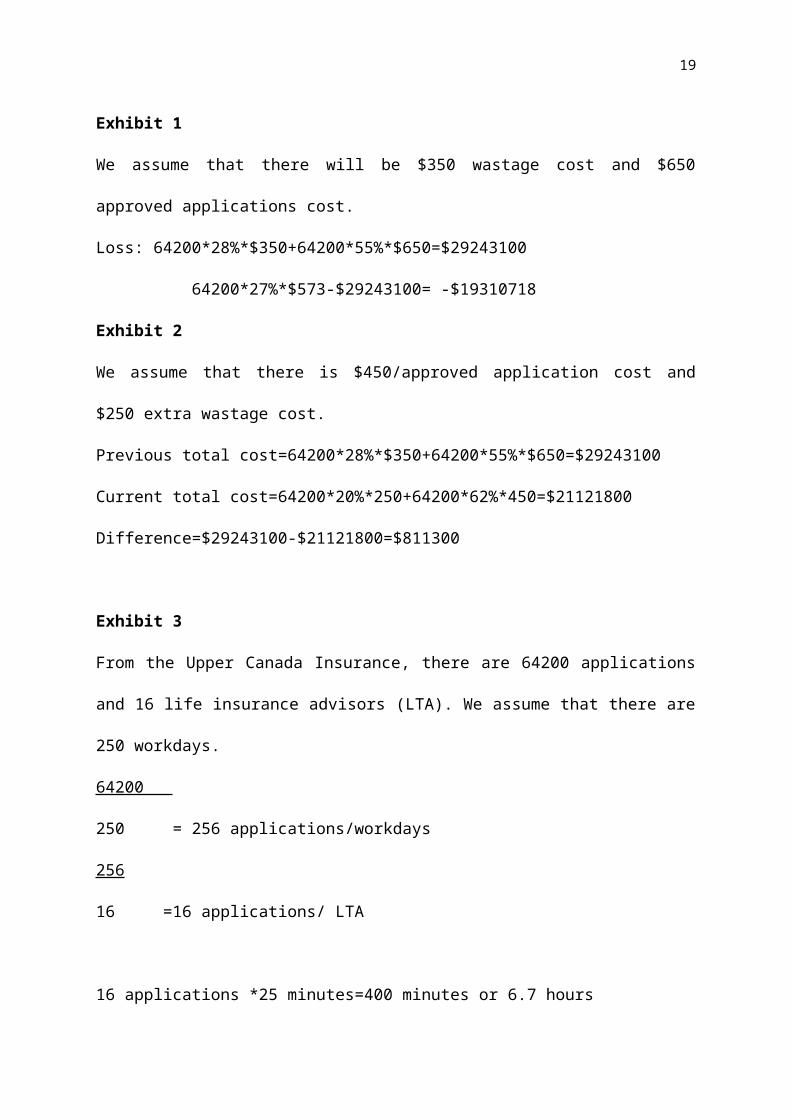

Exhibit 1

We assume that there will be $350 wastage cost and $650

approved applications cost.

Loss: 64200*28%*$350+64200*55%*$650=$29243100

64200*27%*$573-$29243100= -$19310718

Exhibit 2

We assume that there is $450/approved application cost and

$250 extra wastage cost.

Previous total cost=64200*28%*$350+64200*55%*$650=$29243100

Current total cost=64200*20%*250+64200*62%*450=$21121800

Difference=$29243100-$21121800=$811300

Exhibit 3

From the Upper Canada Insurance, there are 64200 applications

and 16 life insurance advisors (LTA). We assume that there are

250 workdays.

64200

250 = 256 applications/workdays

256

16 =16 applications/ LTA

16 applications *25 minutes=400 minutes or 6.7 hours

20

Then LTA will have additional one working hour, so they can

use these working hours to finish more applications.

Exhibit 4

The incomplete rate also will be decreased from 28% to 21%;

then the wastage rate can be increased by 38% and already

decision rate can be increased by 62%.

21% (incompletes) + 1% (not taken) + 16% (decline) =38%

(wastage rate)

100%-38% (wastage rate) = 62% (decision rate)

Exhibit 5

To hire a team of 3 employees who have professional knowledge

about health insurance to check clients’ application process

and give feedback to clients every workday.

We suppose that one year has 269 workdays, and every employee

can work 8hrs per day.

And we pay each employee $40 per hours.

In conclusion, we need to pay the team $258,240 per year.

(269*8*3*$40=$258,240) So, alternative 2 could not reduce

budget

21

Exhibit 6

The training process needs 5 weekends, so it needs 10 days to

complete. Also, the process costs 5 hours per day.

We pay the professional trainer $45 per hour, so we need to

pay $2,250 to the trainer. ($45*5*10=$2250)

In conclusion, alternative 3 could not reduce budget.