updated valuation report - fpts

TRANSCRIPT

UPDATED VALUATION REPORT

www.fpts.com.vn Bloomberg – FPTS <GO> | 1

d

SBT and VNIndex price movements

IMPROVEMENT OF CORE BUSINESS ACTIVITIES,

MAINTAINING THE LEADING POSITION

We conduct the updated valuation of SBT share. By using the

discounted cash flow models, we determine the target price of a

SBT share as 18,650 VND/share, a 22,7% upside from current

price (details). We recommend BUY position for SBT stock for

a medium and long holding period.

We estimate SBT’s revenue in 2020/21F will be about VND

13.184,3 billion (+2.6% yoy). Net profit after tax is estimated at

VND 415.8 billion (+11.8% yoy), equivalent to an EPS of VND

689.2 VND/share (details).

INVESTMENT PROSPECTS

► The sugar industry diverges after the effect of ATIGA,

sugar imported from Thailand surged (details)

By the end of the 2019/20 crop year, the amount of cheap Thai

sugar imported into Vietnam increased by 3.3 times compared

to the previous period, 12.1% higher than the amount of

domestically produced cane sugar, putting great pressure on

Vietnam’s sugar industry.

► SBT continues to maintain the leading position (details)

With the ability to refine raw sugar, high quality products and

distribution system, SBT continues to maintain the leading

position in the domestic sugar market with revenue of more than

VND 12.9 trillion (+21.6% yoy ), consumption volume reached

over 01 million tons (+41% yoy), accounting for nearly 50% of

the domestic sugar market share. The EVFTA, effective from

August 1, 2020, is also expected to provide long-term export

opportunities for SBT (details).

► Operating profits and ability to pay interest improves

(details)

SBT’s profit structure has improved positively. In the second half

of the 2019/20 crop, profit from core businesses increased,

accounting for a large proportion in the structure of profits,

enhancing the firm’s ability to pay interest.

INVESTMENT RISKS

► Risk of weather condition affect sugarcane production

The impact of weather on yield and sugar content of sugarcane

raw material directly affects the production efficiency.

► Risk of domestic sugar price volatility

Due to pressure from cheap imported sugar supply, domestic sugar

price is hard to increase in crop year 2020/21 (details).

THANH THANH CONG – BIEN HOA JSC (HSX: SBT)

AGRICULTURAL INDUSTRY Sep 25th, 2020

Ms. Duong Bich Ngoc

Equity Analyst

Email: [email protected]

Tel: (8424) – 3773 7070 - Ext: 4312

Market Snapshot (25/09/2020)

Current Price (VND/share) 15,200

52-week High (VND/share) 22,100

52-week Low (VND/share) 11,900

Issued Shares (mil shares) 586.7

Outstanding Shares (mil shares) 608.4

30-day Average Volume (shares) 3,249,077

% Foreign Ownership 9.18%

Market capitalization (bil VND) 8,790

LTM P/E trailing (times) 25.3x

LTM EPS trailing (VND/share) 600.5

Business Overview

Company Thanh Thanh Cong – Bien Hoa JSC

Address Tan Hung, Tan Chau, Tay Ninh

Key revenues

Producing and trading sugar products

Key input costs

Raw sugarcane, imported raw sugar

Key strengths

Production scale and technology; Branding and distribution; Diverse and high-end products

Key risks Price volatility of raw sugarcane and sugar

-50%

0%

50%

100%

150% SBT VNI

Approved by

Ms. Nguyen Thi Kim Chi

Deputy Director – Research Department

Current price: 15.200

Target price: 18.650

Upside: +22,7%

RECOMMENDATION

BUY

References: Updated Sugar Industry Report – Sep 2020

SBT Updated Valuation Report Nov 2019

HSX: SBT

www.fpts.com.vn Bloomberg – FPTS <GO> | 2

I. OVERVIEW OF VIETNAM SUGAR INDUSTRY

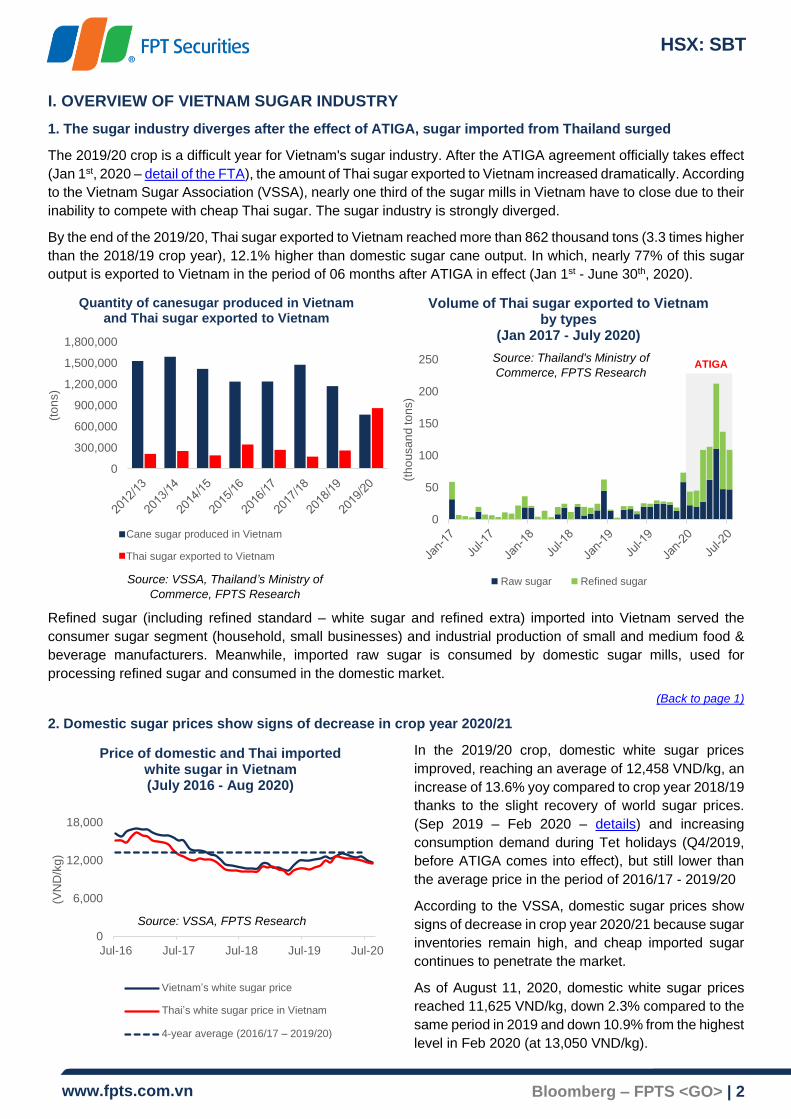

1. The sugar industry diverges after the effect of ATIGA, sugar imported from Thailand surged

The 2019/20 crop is a difficult year for Vietnam's sugar industry. After the ATIGA agreement officially takes effect

(Jan 1st, 2020 – detail of the FTA), the amount of Thai sugar exported to Vietnam increased dramatically. According

to the Vietnam Sugar Association (VSSA), nearly one third of the sugar mills in Vietnam have to close due to their

inability to compete with cheap Thai sugar. The sugar industry is strongly diverged.

By the end of the 2019/20, Thai sugar exported to Vietnam reached more than 862 thousand tons (3.3 times higher

than the 2018/19 crop year), 12.1% higher than domestic sugar cane output. In which, nearly 77% of this sugar

output is exported to Vietnam in the period of 06 months after ATIGA in effect (Jan 1st - June 30th, 2020).

Refined sugar (including refined standard – white sugar and refined extra) imported into Vietnam served the

consumer sugar segment (household, small businesses) and industrial production of small and medium food &

beverage manufacturers. Meanwhile, imported raw sugar is consumed by domestic sugar mills, used for

processing refined sugar and consumed in the domestic market.

(Back to page 1)

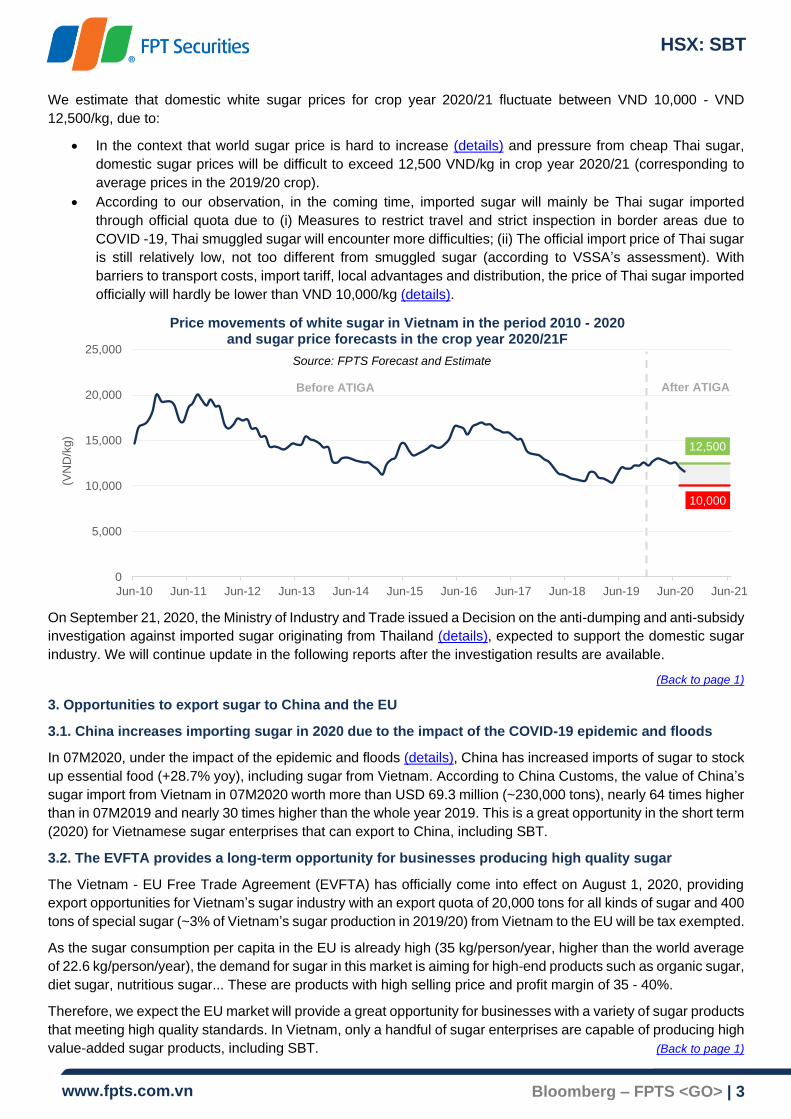

2. Domestic sugar prices show signs of decrease in crop year 2020/21

In the 2019/20 crop, domestic white sugar prices

improved, reaching an average of 12,458 VND/kg, an

increase of 13.6% yoy compared to crop year 2018/19

thanks to the slight recovery of world sugar prices.

(Sep 2019 – Feb 2020 – details) and increasing

consumption demand during Tet holidays (Q4/2019,

before ATIGA comes into effect), but still lower than

the average price in the period of 2016/17 - 2019/20

According to the VSSA, domestic sugar prices show

signs of decrease in crop year 2020/21 because sugar

inventories remain high, and cheap imported sugar

continues to penetrate the market.

As of August 11, 2020, domestic white sugar prices

reached 11,625 VND/kg, down 2.3% compared to the

same period in 2019 and down 10.9% from the highest

level in Feb 2020 (at 13,050 VND/kg).

0

300,000

600,000

900,000

1,200,000

1,500,000

1,800,000

(to

ns)

Quantity of canesugar produced in Vietnam and Thai sugar exported to Vietnam

Đường mía sản xuất trong nước

Đường Thái Lan xuất khẩu sang Việt Nam

0

50

100

150

200

250

(th

ou

sa

nd

to

ns)

Volume of Thai sugar exported to Vietnam by types

(Jan 2017 - July 2020)

Đường thô Đường luyện

Source: Thailand's Ministry of

Commerce, FPTS ResearchATIGA

0

6,000

12,000

18,000

Jul-16 Jul-17 Jul-18 Jul-19 Jul-20

(VN

D/k

g)

Price of domestic and Thai imported white sugar in Vietnam(July 2016 - Aug 2020)

Đường trắng Việt Nam

Đường Thái Lan tại Việt Nam

TB 04 năm (2016/17 - 2019/20)

Source: VSSA, FPTS Research

Source: VSSA, Thailand’s Ministry of

Commerce, FPTS Research

Cane sugar produced in Vietnam

Thai sugar exported to Vietnam

Raw sugar Refined sugar

Vietnam’s white sugar price

Thai’s white sugar price in Vietnam

4-year average (2016/17 – 2019/20)

HSX: SBT

www.fpts.com.vn Bloomberg – FPTS <GO> | 3

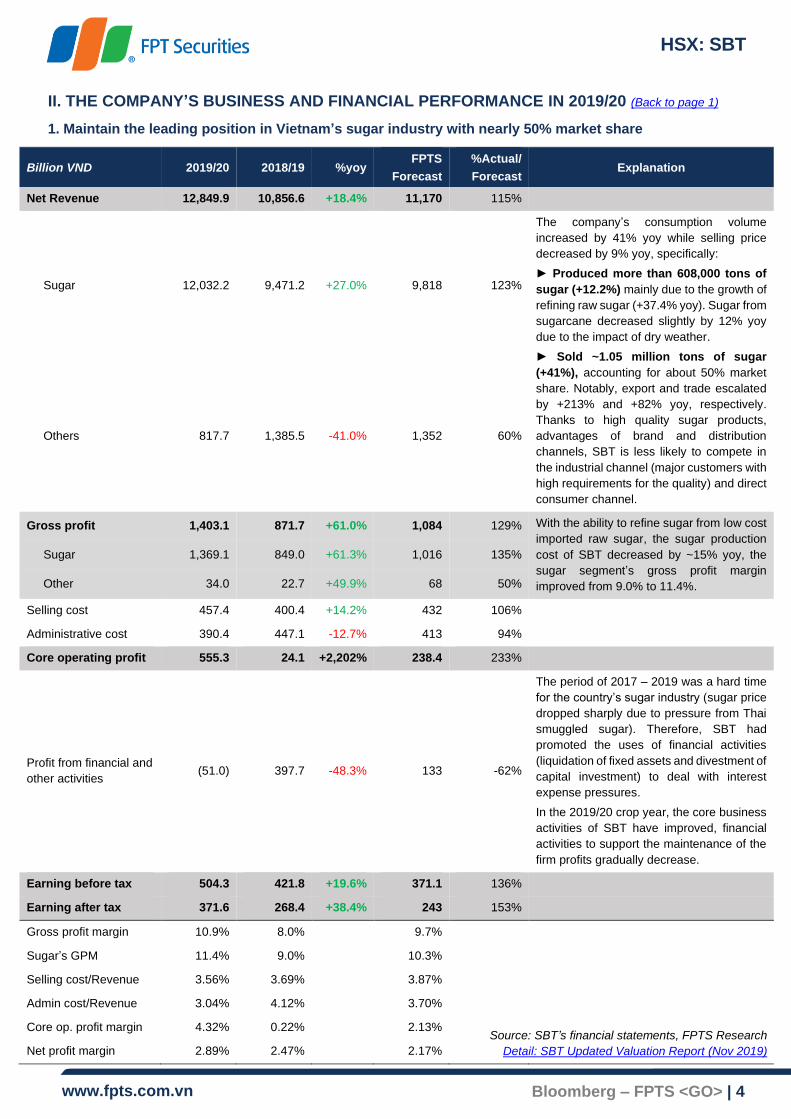

We estimate that domestic white sugar prices for crop year 2020/21 fluctuate between VND 10,000 - VND

12,500/kg, due to:

• In the context that world sugar price is hard to increase (details) and pressure from cheap Thai sugar,

domestic sugar prices will be difficult to exceed 12,500 VND/kg in crop year 2020/21 (corresponding to

average prices in the 2019/20 crop).

• According to our observation, in the coming time, imported sugar will mainly be Thai sugar imported

through official quota due to (i) Measures to restrict travel and strict inspection in border areas due to

COVID -19, Thai smuggled sugar will encounter more difficulties; (ii) The official import price of Thai sugar

is still relatively low, not too different from smuggled sugar (according to VSSA’s assessment). With

barriers to transport costs, import tariff, local advantages and distribution, the price of Thai sugar imported

officially will hardly be lower than VND 10,000/kg (details).

On September 21, 2020, the Ministry of Industry and Trade issued a Decision on the anti-dumping and anti-subsidy

investigation against imported sugar originating from Thailand (details), expected to support the domestic sugar

industry. We will continue update in the following reports after the investigation results are available.

(Back to page 1)

3. Opportunities to export sugar to China and the EU

3.1. China increases importing sugar in 2020 due to the impact of the COVID-19 epidemic and floods

In 07M2020, under the impact of the epidemic and floods (details), China has increased imports of sugar to stock

up essential food (+28.7% yoy), including sugar from Vietnam. According to China Customs, the value of China’s

sugar import from Vietnam in 07M2020 worth more than USD 69.3 million (~230,000 tons), nearly 64 times higher

than in 07M2019 and nearly 30 times higher than the whole year 2019. This is a great opportunity in the short term

(2020) for Vietnamese sugar enterprises that can export to China, including SBT.

3.2. The EVFTA provides a long-term opportunity for businesses producing high quality sugar

The Vietnam - EU Free Trade Agreement (EVFTA) has officially come into effect on August 1, 2020, providing

export opportunities for Vietnam’s sugar industry with an export quota of 20,000 tons for all kinds of sugar and 400

tons of special sugar (~3% of Vietnam’s sugar production in 2019/20) from Vietnam to the EU will be tax exempted.

As the sugar consumption per capita in the EU is already high (35 kg/person/year, higher than the world average

of 22.6 kg/person/year), the demand for sugar in this market is aiming for high-end products such as organic sugar,

diet sugar, nutritious sugar... These are products with high selling price and profit margin of 35 - 40%.

Therefore, we expect the EU market will provide a great opportunity for businesses with a variety of sugar products

that meeting high quality standards. In Vietnam, only a handful of sugar enterprises are capable of producing high

value-added sugar products, including SBT. (Back to page 1)

12,500

10,000

0

5,000

10,000

15,000

20,000

25,000

Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16 Jun-17 Jun-18 Jun-19 Jun-20 Jun-21

(VN

D/k

g)

Price movements of white sugar in Vietnam in the period 2010 - 2020 and sugar price forecasts in the crop year 2020/21F

Before ATIGA After ATIGA

Source: FPTS Forecast and Estimate

HSX: SBT

www.fpts.com.vn Bloomberg – FPTS <GO> | 4

II. THE COMPANY’S BUSINESS AND FINANCIAL PERFORMANCE IN 2019/20 (Back to page 1)

1. Maintain the leading position in Vietnam’s sugar industry with nearly 50% market share

Billion VND 2019/20 2018/19 %yoy FPTS

Forecast

%Actual/

Forecast Explanation

Net Revenue 12,849.9 10,856.6 +18.4% 11,170 115%

Sugar 12,032.2 9,471.2 +27.0% 9,818 123%

The company’s consumption volume

increased by 41% yoy while selling price

decreased by 9% yoy, specifically:

► Produced more than 608,000 tons of

sugar (+12.2%) mainly due to the growth of

refining raw sugar (+37.4% yoy). Sugar from

sugarcane decreased slightly by 12% yoy

due to the impact of dry weather.

► Sold ~1.05 million tons of sugar

(+41%), accounting for about 50% market

share. Notably, export and trade escalated

by +213% and +82% yoy, respectively.

Thanks to high quality sugar products,

advantages of brand and distribution

channels, SBT is less likely to compete in

the industrial channel (major customers with

high requirements for the quality) and direct

consumer channel.

Others 817.7 1,385.5 -41.0% 1,352 60%

Gross profit 1,403.1 871.7 +61.0% 1,084 129% With the ability to refine sugar from low cost

imported raw sugar, the sugar production

cost of SBT decreased by ~15% yoy, the

sugar segment’s gross profit margin

improved from 9.0% to 11.4%.

Sugar 1,369.1 849.0 +61.3% 1,016 135%

Other 34.0 22.7 +49.9% 68 50%

Selling cost 457.4 400.4 +14.2% 432 106%

Administrative cost 390.4 447.1 -12.7% 413 94%

Core operating profit 555.3 24.1 +2,202% 238.4 233%

Profit from financial and

other activities (51.0) 397.7 -48.3% 133 -62%

The period of 2017 – 2019 was a hard time

for the country’s sugar industry (sugar price

dropped sharply due to pressure from Thai

smuggled sugar). Therefore, SBT had

promoted the uses of financial activities

(liquidation of fixed assets and divestment of

capital investment) to deal with interest

expense pressures.

In the 2019/20 crop year, the core business

activities of SBT have improved, financial

activities to support the maintenance of the

firm profits gradually decrease.

Earning before tax 504.3 421.8 +19.6% 371.1 136%

Earning after tax 371.6 268.4 +38.4% 243 153%

Gross profit margin 10.9% 8.0% 9.7%

Sugar’s GPM 11.4% 9.0% 10.3%

Selling cost/Revenue 3.56% 3.69% 3.87%

Admin cost/Revenue 3.04% 4.12% 3.70%

Core op. profit margin 4.32% 0.22% 2.13%

Net profit margin 2.89% 2.47% 2.17% Source: SBT’s financial statements, FPTS Research

Detail: SBT Updated Valuation Report (Nov 2019)

HSX: SBT

www.fpts.com.vn Bloomberg – FPTS <GO> | 5

6.1

1.9 1.5 1.62.5

1.50.8

-0.10.9

-2

0

2

4

6

8

0

2,000

4,000

6,000

8,000

10,000

12,000(t

ime

s)

(bil

VN

D)

Debt structure and SBT's capability of debt repayment

Nợ vay DH (cột trái)

Nợ vay NH (cột trái)

Lợi nhuận HĐKD*/chi phí lãi vay

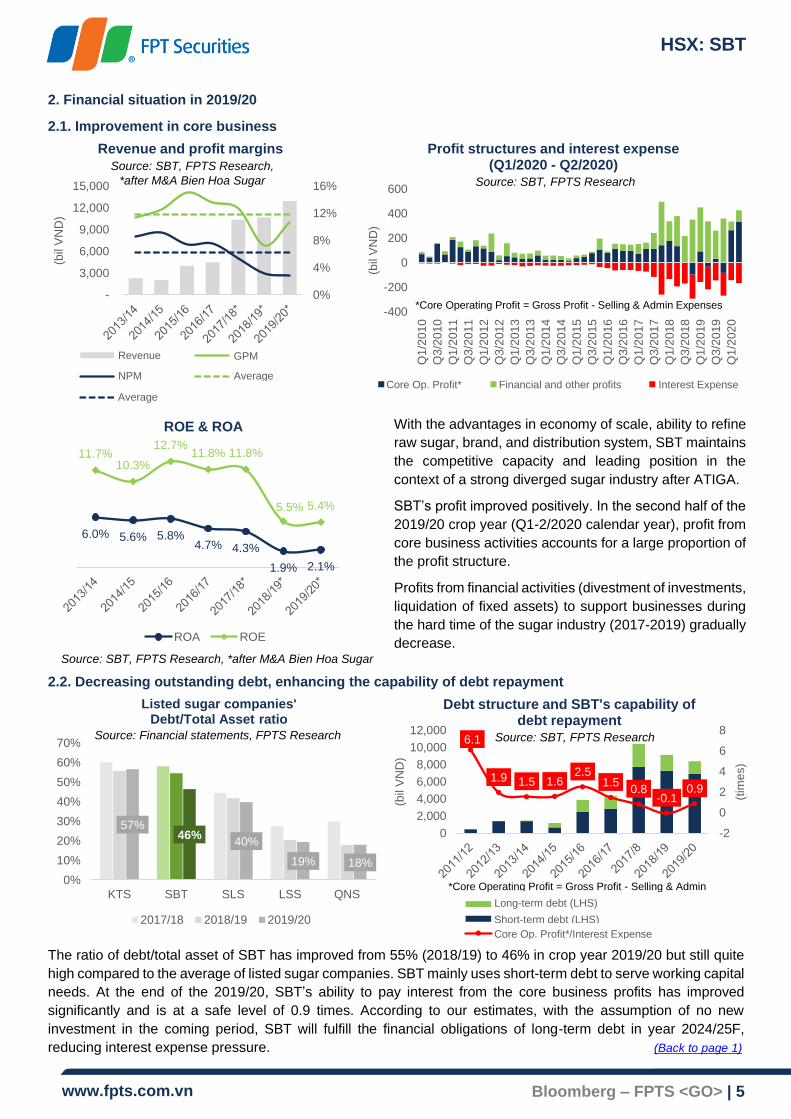

2. Financial situation in 2019/20

2.1. Improvement in core business

2.2. Decreasing outstanding debt, enhancing the capability of debt repayment

The ratio of debt/total asset of SBT has improved from 55% (2018/19) to 46% in crop year 2019/20 but still quite

high compared to the average of listed sugar companies. SBT mainly uses short-term debt to serve working capital

needs. At the end of the 2019/20, SBT’s ability to pay interest from the core business profits has improved

significantly and is at a safe level of 0.9 times. According to our estimates, with the assumption of no new

investment in the coming period, SBT will fulfill the financial obligations of long-term debt in year 2024/25F,

reducing interest expense pressure. (Back to page 1)

Core Op. Profit*/Interest Expense

0%

4%

8%

12%

16%

-

3,000

6,000

9,000

12,000

15,000

(bil

VN

D)

Revenue and profit margins

Doanh thu Tỷ suất LNG

Tỷ suất LNST Trung bình

Trung bình

6.0% 5.6% 5.8%4.7% 4.3%

1.9% 2.1%

11.7%10.3%

12.7%11.8% 11.8%

5.5% 5.4%

ROE & ROA

ROA ROE

Source: SBT, FPTS Research,

*after M&A Bien Hoa Sugar

57%46%

40%

19% 18%

0%

10%

20%

30%

40%

50%

60%

70%

KTS SBT SLS LSS QNS

Listed sugar companies' Debt/Total Asset ratio

2017/18 2018/19 2019/20

With the advantages in economy of scale, ability to refine

raw sugar, brand, and distribution system, SBT maintains

the competitive capacity and leading position in the

context of a strong diverged sugar industry after ATIGA.

SBT’s profit improved positively. In the second half of the

2019/20 crop year (Q1-2/2020 calendar year), profit from

core business activities accounts for a large proportion of

the profit structure.

Profits from financial activities (divestment of investments,

liquidation of fixed assets) to support businesses during

the hard time of the sugar industry (2017-2019) gradually

decrease.

-400

-200

0

200

400

600

Q1

/201

0

Q3

/201

0

Q1

/201

1

Q3

/201

1

Q1

/201

2

Q3

/201

2

Q1

/201

3

Q3

/201

3

Q1

/201

4

Q3

/201

4

Q1

/201

5

Q3

/201

5

Q1

/201

6

Q3

/201

6

Q1

/201

7

Q3

/201

7

Q1

/201

8

Q3

/201

8

Q1

/201

9

Q3

/201

9

Q1

/202

0

(bil

VN

D)

Profit structures and interest expense(Q1/2020 - Q2/2020)

Lợi nhuận HĐKD* Lợi nhuận tài chính & khác Chi phí lãi vay

*Core Operating Profit = Gross Profit - Selling & Admin Expenses

Source: SBT, FPTS Research

*Core Operating Profit = Gross Profit - Selling & Admin

Expenses

Source: SBT, FPTS Research, *after M&A Bien Hoa Sugar

Source: Financial statements, FPTS Research Source: SBT, FPTS Research

Revenue GPM

NPM Average

Average Core Op. Profit* Financial and other profits Interest Expense

Short-term debt (LHS)

Long-term debt (LHS)

HSX: SBT

www.fpts.com.vn Bloomberg – FPTS <GO> | 6

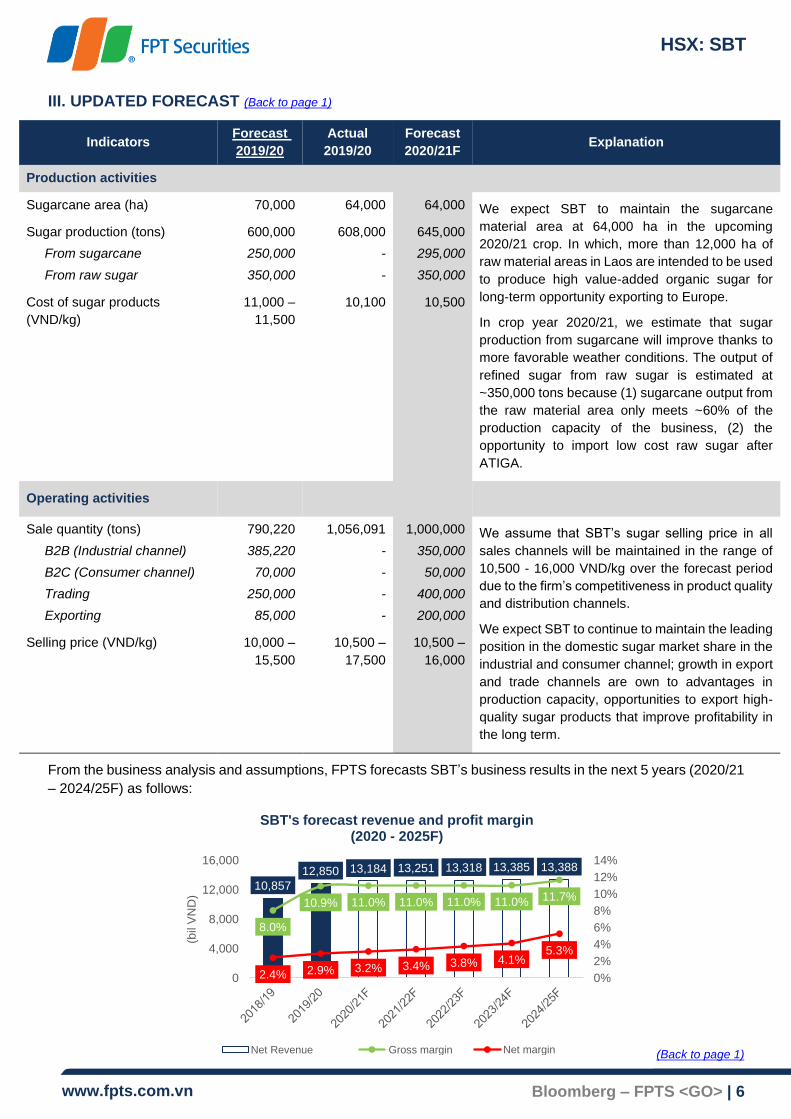

III. UPDATED FORECAST (Back to page 1)

Indicators Forecast

2019/20

Actual

2019/20

Forecast

2020/21F Explanation

Production activities

Sugarcane area (ha) 70,000 64,000 64,000 We expect SBT to maintain the sugarcane

material area at 64,000 ha in the upcoming

2020/21 crop. In which, more than 12,000 ha of

raw material areas in Laos are intended to be used

to produce high value-added organic sugar for

long-term opportunity exporting to Europe.

In crop year 2020/21, we estimate that sugar

production from sugarcane will improve thanks to

more favorable weather conditions. The output of

refined sugar from raw sugar is estimated at

~350,000 tons because (1) sugarcane output from

the raw material area only meets ~60% of the

production capacity of the business, (2) the

opportunity to import low cost raw sugar after

ATIGA.

Sugar production (tons)

From sugarcane

From raw sugar

600,000

250,000

350,000

608,000

-

-

645,000

295,000

350,000

Cost of sugar products

(VND/kg)

11,000 –

11,500

10,100 10,500

Operating activities

Sale quantity (tons)

B2B (Industrial channel)

B2C (Consumer channel)

Trading

Exporting

790,220

385,220

70,000

250,000

85,000

1,056,091

-

-

-

-

1,000,000

350,000

50,000

400,000

200,000

We assume that SBT’s sugar selling price in all

sales channels will be maintained in the range of

10,500 - 16,000 VND/kg over the forecast period

due to the firm’s competitiveness in product quality

and distribution channels.

We expect SBT to continue to maintain the leading

position in the domestic sugar market share in the

industrial and consumer channel; growth in export

and trade channels are own to advantages in

production capacity, opportunities to export high-

quality sugar products that improve profitability in

the long term.

Selling price (VND/kg) 10,000 –

15,500

10,500 –

17,500

10,500 –

16,000

From the business analysis and assumptions, FPTS forecasts SBT’s business results in the next 5 years (2020/21

– 2024/25F) as follows:

(Back to page 1)

10,857

12,850 13,184 13,251 13,318 13,385 13,388

8.0%

10.9% 11.0% 11.0% 11.0% 11.0% 11.7%

2.4% 2.9% 3.2% 3.4% 3.8% 4.1%5.3%

0%

2%

4%

6%

8%

10%

12%

14%

0

4,000

8,000

12,000

16,000

(bil

VN

D)

SBT's forecast revenue and profit margin (2020 - 2025F)

Doanh thu thuần Tỷ suất LNG Tỷ suất LNSTNet Revenue Gross margin Net margin

HSX: SBT

www.fpts.com.vn Bloomberg – FPTS <GO> | 7

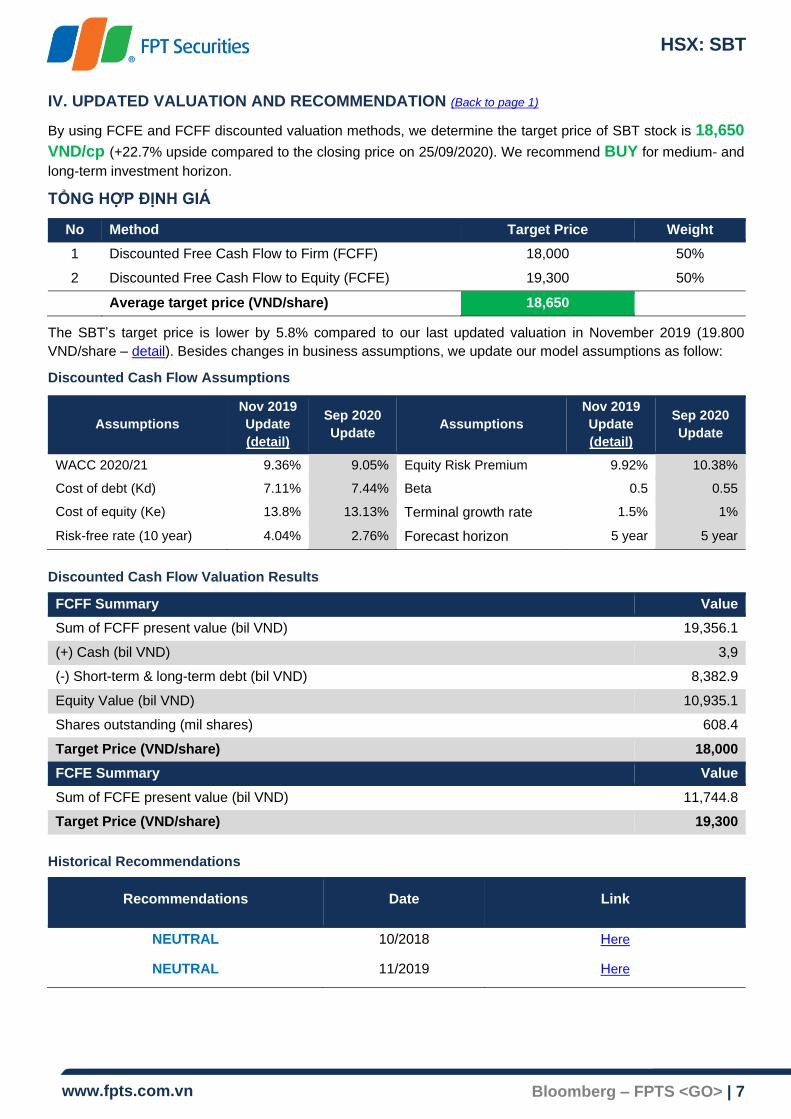

IV. UPDATED VALUATION AND RECOMMENDATION (Back to page 1)

By using FCFE and FCFF discounted valuation methods, we determine the target price of SBT stock is 18,650

VND/cp (+22.7% upside compared to the closing price on 25/09/2020). We recommend BUY for medium- and

long-term investment horizon.

TỔNG HỢP ĐỊNH GIÁ

No Method Target Price Weight

1 Discounted Free Cash Flow to Firm (FCFF) 18,000 50%

2 Discounted Free Cash Flow to Equity (FCFE) 19,300 50%

Average target price (VND/share) 18,650

The SBT’s target price is lower by 5.8% compared to our last updated valuation in November 2019 (19.800

VND/share – detail). Besides changes in business assumptions, we update our model assumptions as follow:

Discounted Cash Flow Assumptions

Assumptions

Nov 2019

Update

(detail)

Sep 2020

Update Assumptions

Nov 2019

Update

(detail)

Sep 2020

Update

WACC 2020/21 9.36% 9.05% Equity Risk Premium 9.92% 10.38%

Cost of debt (Kd) 7.11% 7.44% Beta 0.5 0.55

Cost of equity (Ke) 13.8% 13.13% Terminal growth rate 1.5% 1%

Risk-free rate (10 year) 4.04% 2.76% Forecast horizon 5 year 5 year

Discounted Cash Flow Valuation Results

FCFF Summary Value

Sum of FCFF present value (bil VND) 19,356.1

(+) Cash (bil VND) 3,9

(-) Short-term & long-term debt (bil VND) 8,382.9

Equity Value (bil VND) 10,935.1

Shares outstanding (mil shares) 608.4

Target Price (VND/share) 18,000

FCFE Summary Value

Sum of FCFE present value (bil VND) 11,744.8

Target Price (VND/share) 19,300

Historical Recommendations

Recommendations Date Link

NEUTRAL 10/2018 Here

NEUTRAL 11/2019 Here

HSX: SBT

www.fpts.com.vn Bloomberg – FPTS <GO> | 8

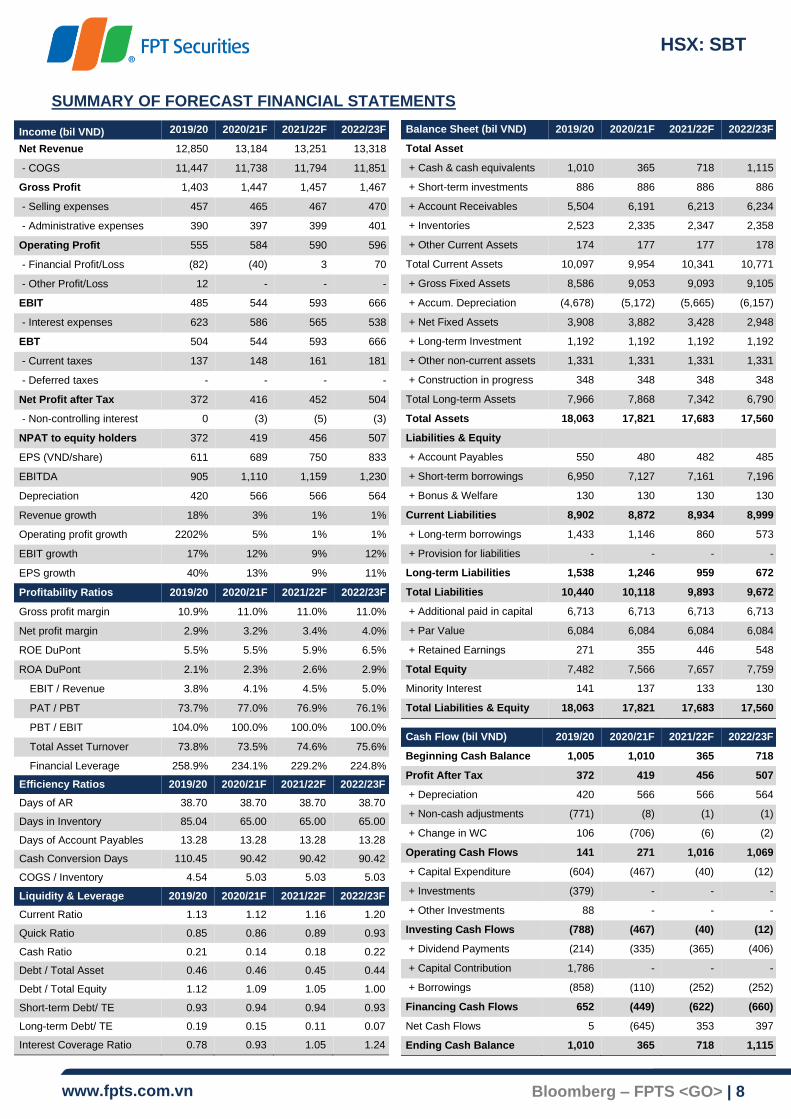

Efficiency Ratios 2019/20 2020/21F 2021/22F 2022/23F

Days of AR 38.70 38.70 38.70 38.70

Days in Inventory 85.04 65.00 65.00 65.00

Days of Account Payables 13.28 13.28 13.28 13.28

Cash Conversion Days 110.45 90.42 90.42 90.42

COGS / Inventory 4.54 5.03 5.03 5.03

Liquidity & Leverage 2019/20 2020/21F 2021/22F 2022/23F

Current Ratio 1.13 1.12 1.16 1.20

Quick Ratio 0.85 0.86 0.89 0.93

Cash Ratio 0.21 0.14 0.18 0.22

Debt / Total Asset 0.46 0.46 0.45 0.44

Debt / Total Equity 1.12 1.09 1.05 1.00

Short-term Debt/ TE 0.93 0.94 0.94 0.93

Long-term Debt/ TE 0.19 0.15 0.11 0.07

Interest Coverage Ratio 0.78 0.93 1.05 1.24

Cash Flow (bil VND) 2019/20 2020/21F 2021/22F 2022/23F

Beginning Cash Balance 1,005 1,010 365 718

Profit After Tax 372 419 456 507

+ Depreciation 420 566 566 564

+ Non-cash adjustments (771) (8) (1) (1)

+ Change in WC 106 (706) (6) (2)

Operating Cash Flows 141 271 1,016 1,069

+ Capital Expenditure (604) (467) (40) (12)

+ Investments (379) - - -

+ Other Investments 88 - - -

Investing Cash Flows (788) (467) (40) (12)

+ Dividend Payments (214) (335) (365) (406)

+ Capital Contribution 1,786 - - -

+ Borrowings (858) (110) (252) (252)

Financing Cash Flows 652 (449) (622) (660)

Net Cash Flows 5 (645) 353 397

Ending Cash Balance 1,010 365 718 1,115

SUMMARY OF FORECAST FINANCIAL STATEMENTS

Income (bil VND) 2019/20 2020/21F 2021/22F 2022/23F

Net Revenue 12,850 13,184 13,251 13,318

- COGS 11,447 11,738 11,794 11,851

Gross Profit 1,403 1,447 1,457 1,467

- Selling expenses 457 465 467 470

- Administrative expenses 390 397 399 401

Operating Profit 555 584 590 596

- Financial Profit/Loss (82) (40) 3 70

- Other Profit/Loss 12 - - -

EBIT 485 544 593 666

- Interest expenses 623 586 565 538

EBT 504 544 593 666

- Current taxes 137 148 161 181

- Deferred taxes - - - -

Net Profit after Tax 372 416 452 504

- Non-controlling interest 0 (3) (5) (3)

NPAT to equity holders 372 419 456 507

EPS (VND/share) 611 689 750 833

EBITDA 905 1,110 1,159 1,230

Depreciation 420 566 566 564

Revenue growth 18% 3% 1% 1%

Operating profit growth 2202% 5% 1% 1%

EBIT growth 17% 12% 9% 12%

EPS growth 40% 13% 9% 11%

Profitability Ratios 2019/20 2020/21F 2021/22F 2022/23F

Gross profit margin 10.9% 11.0% 11.0% 11.0%

Net profit margin 2.9% 3.2% 3.4% 4.0%

ROE DuPont 5.5% 5.5% 5.9% 6.5%

ROA DuPont 2.1% 2.3% 2.6% 2.9%

EBIT / Revenue 3.8% 4.1% 4.5% 5.0%

PAT / PBT 73.7% 77.0% 76.9% 76.1%

PBT / EBIT 104.0% 100.0% 100.0% 100.0%

Total Asset Turnover 73.8% 73.5% 74.6% 75.6%

Financial Leverage 258.9% 234.1% 229.2% 224.8%

Balance Sheet (bil VND) 2019/20 2020/21F 2021/22F 2022/23F

Total Asset

+ Cash & cash equivalents 1,010 365 718 1,115

+ Short-term investments 886 886 886 886

+ Account Receivables 5,504 6,191 6,213 6,234

+ Inventories 2,523 2,335 2,347 2,358

+ Other Current Assets 174 177 177 178

Total Current Assets 10,097 9,954 10,341 10,771

+ Gross Fixed Assets 8,586 9,053 9,093 9,105

+ Accum. Depreciation (4,678) (5,172) (5,665) (6,157)

+ Net Fixed Assets 3,908 3,882 3,428 2,948

+ Long-term Investment 1,192 1,192 1,192 1,192

+ Other non-current assets 1,331 1,331 1,331 1,331

+ Construction in progress 348 348 348 348

Total Long-term Assets 7,966 7,868 7,342 6,790

Total Assets 18,063 17,821 17,683 17,560

Liabilities & Equity

+ Account Payables 550 480 482 485

+ Short-term borrowings 6,950 7,127 7,161 7,196

+ Bonus & Welfare 130 130 130 130

Current Liabilities 8,902 8,872 8,934 8,999

+ Long-term borrowings 1,433 1,146 860 573

+ Provision for liabilities - - - -

Long-term Liabilities 1,538 1,246 959 672

Total Liabilities 10,440 10,118 9,893 9,672

+ Additional paid in capital 6,713 6,713 6,713 6,713

+ Par Value 6,084 6,084 6,084 6,084

+ Retained Earnings 271 355 446 548

Total Equity 7,482 7,566 7,657 7,759

Minority Interest 141 137 133 130

Total Liabilities & Equity 18,063 17,821 17,683 17,560

161 176 190

HSX: SBT

www.fpts.com.vn Bloomberg – FPTS <GO> | 9

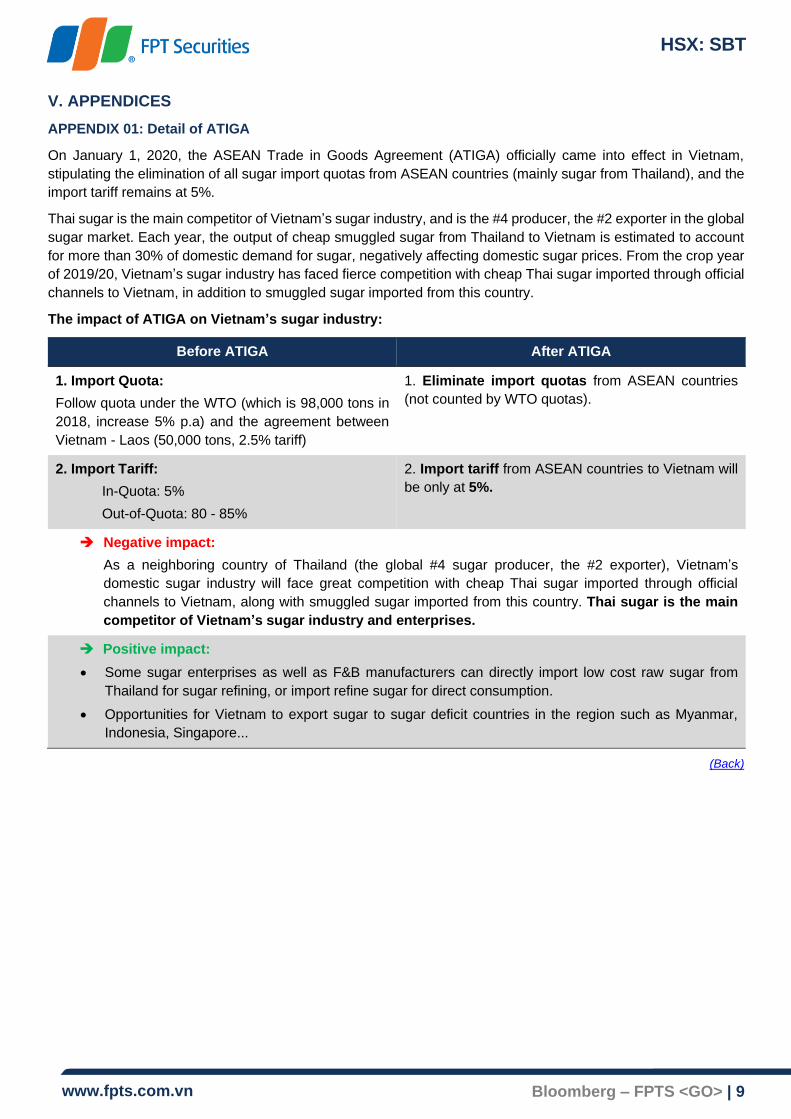

V. APPENDICES

APPENDIX 01: Detail of ATIGA

On January 1, 2020, the ASEAN Trade in Goods Agreement (ATIGA) officially came into effect in Vietnam,

stipulating the elimination of all sugar import quotas from ASEAN countries (mainly sugar from Thailand), and the

import tariff remains at 5%.

Thai sugar is the main competitor of Vietnam’s sugar industry, and is the #4 producer, the #2 exporter in the global

sugar market. Each year, the output of cheap smuggled sugar from Thailand to Vietnam is estimated to account

for more than 30% of domestic demand for sugar, negatively affecting domestic sugar prices. From the crop year

of 2019/20, Vietnam’s sugar industry has faced fierce competition with cheap Thai sugar imported through official

channels to Vietnam, in addition to smuggled sugar imported from this country.

The impact of ATIGA on Vietnam’s sugar industry:

Before ATIGA After ATIGA

1. Import Quota:

Follow quota under the WTO (which is 98,000 tons in

2018, increase 5% p.a) and the agreement between

Vietnam - Laos (50,000 tons, 2.5% tariff)

1. Eliminate import quotas from ASEAN countries

(not counted by WTO quotas).

2. Import Tariff:

In-Quota: 5%

Out-of-Quota: 80 - 85%

2. Import tariff from ASEAN countries to Vietnam will

be only at 5%.

➔ Negative impact:

As a neighboring country of Thailand (the global #4 sugar producer, the #2 exporter), Vietnam’s

domestic sugar industry will face great competition with cheap Thai sugar imported through official

channels to Vietnam, along with smuggled sugar imported from this country. Thai sugar is the main

competitor of Vietnam’s sugar industry and enterprises.

➔ Positive impact:

• Some sugar enterprises as well as F&B manufacturers can directly import low cost raw sugar from

Thailand for sugar refining, or import refine sugar for direct consumption.

• Opportunities for Vietnam to export sugar to sugar deficit countries in the region such as Myanmar,

Indonesia, Singapore...

(Back)

HSX: SBT

www.fpts.com.vn Bloomberg – FPTS <GO> | 10

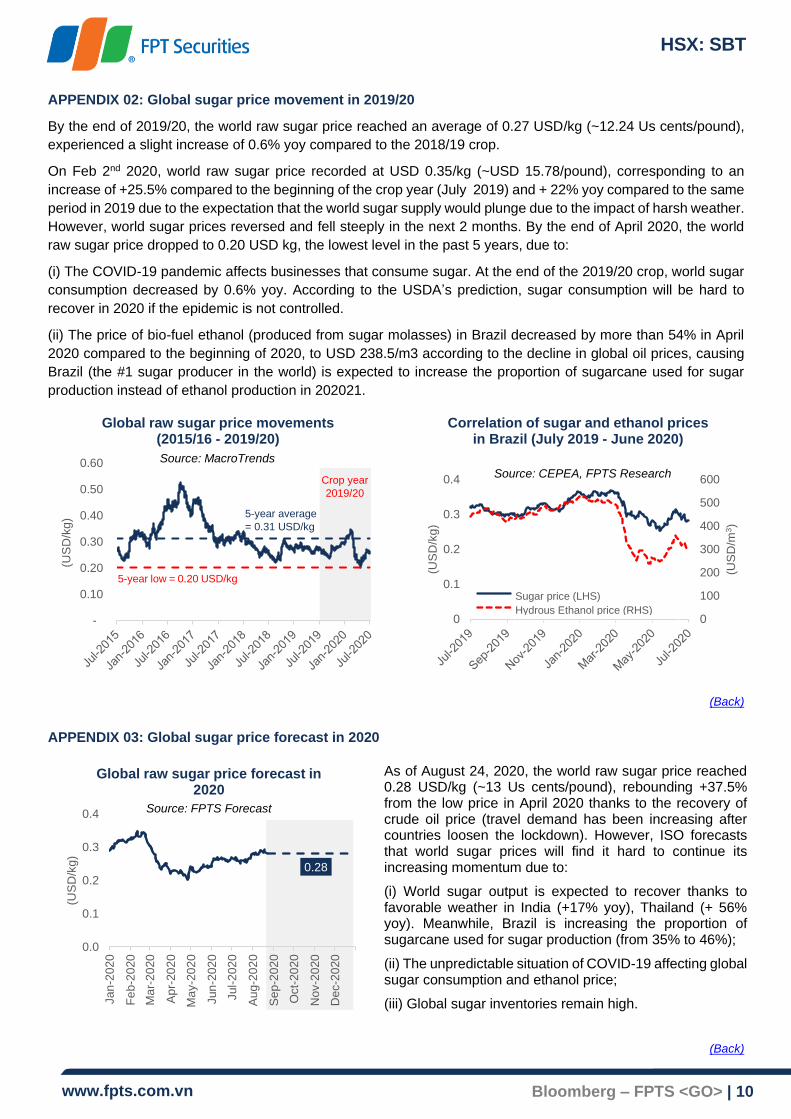

APPENDIX 02: Global sugar price movement in 2019/20

By the end of 2019/20, the world raw sugar price reached an average of 0.27 USD/kg (~12.24 Us cents/pound),

experienced a slight increase of 0.6% yoy compared to the 2018/19 crop.

On Feb 2nd 2020, world raw sugar price recorded at USD 0.35/kg (~USD 15.78/pound), corresponding to an

increase of +25.5% compared to the beginning of the crop year (July 2019) and + 22% yoy compared to the same

period in 2019 due to the expectation that the world sugar supply would plunge due to the impact of harsh weather.

However, world sugar prices reversed and fell steeply in the next 2 months. By the end of April 2020, the world

raw sugar price dropped to 0.20 USD kg, the lowest level in the past 5 years, due to:

(i) The COVID-19 pandemic affects businesses that consume sugar. At the end of the 2019/20 crop, world sugar

consumption decreased by 0.6% yoy. According to the USDA’s prediction, sugar consumption will be hard to

recover in 2020 if the epidemic is not controlled.

(ii) The price of bio-fuel ethanol (produced from sugar molasses) in Brazil decreased by more than 54% in April

2020 compared to the beginning of 2020, to USD 238.5/m3 according to the decline in global oil prices, causing

Brazil (the #1 sugar producer in the world) is expected to increase the proportion of sugarcane used for sugar

production instead of ethanol production in 202021.

(Back)

APPENDIX 03: Global sugar price forecast in 2020

(Back)

0

100

200

300

400

500

600

0

0.1

0.2

0.3

0.4

(US

D/m

3)

(US

D/k

g)

Correlation of sugar and ethanol prices in Brazil (July 2019 - June 2020)

Giá đường (cột trái)Giá hydrous ethanol (cột phải)

Source: CEPEA, FPTS Research

-

0.10

0.20

0.30

0.40

0.50

0.60

(US

D/k

g)

Global raw sugar price movements(2015/16 - 2019/20)

Source: MacroTrends

Crop year 2019/20

5-year average

= 0.31 USD/kg

5-year low = 0.20 USD/kg

0.28

0.0

0.1

0.2

0.3

0.4

Jan

-202

0

Fe

b-2

020

Ma

r-2

020

Ap

r-20

20

Ma

y-2

02

0

Jun

-202

0

Jul-

202

0

Au

g-2

02

0

Se

p-2

02

0

Oct-

20

20

Nov-2

020

Dec-2

020

(US

D/k

g)

Global raw sugar price forecast in 2020

Source: FPTS Forecast

As of August 24, 2020, the world raw sugar price reached 0.28 USD/kg (~13 Us cents/pound), rebounding +37.5% from the low price in April 2020 thanks to the recovery of crude oil price (travel demand has been increasing after countries loosen the lockdown). However, ISO forecasts that world sugar prices will find it hard to continue its increasing momentum due to:

(i) World sugar output is expected to recover thanks to favorable weather in India (+17% yoy), Thailand (+ 56% yoy). Meanwhile, Brazil is increasing the proportion of sugarcane used for sugar production (from 35% to 46%);

(ii) The unpredictable situation of COVID-19 affecting global sugar consumption and ethanol price;

(iii) Global sugar inventories remain high.

Sugar price (LHS)

Hydrous Ethanol price (RHS)

HSX: SBT

www.fpts.com.vn Bloomberg – FPTS <GO> | 11

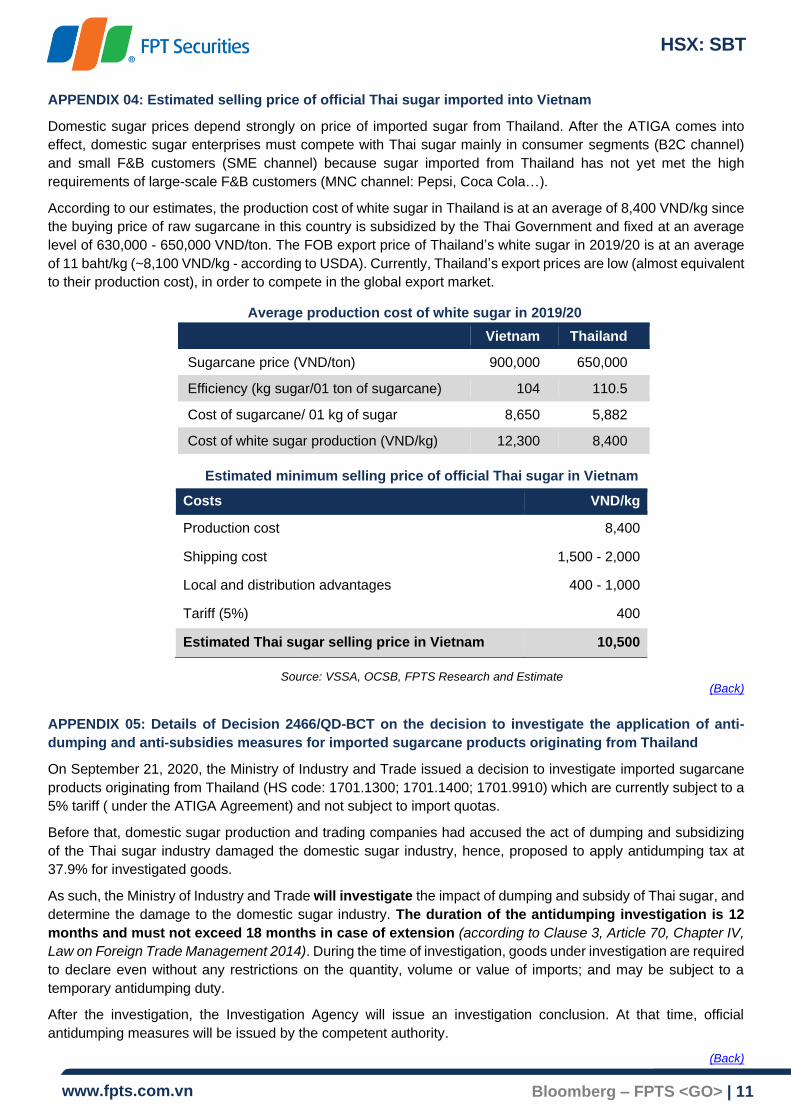

APPENDIX 04: Estimated selling price of official Thai sugar imported into Vietnam

Domestic sugar prices depend strongly on price of imported sugar from Thailand. After the ATIGA comes into

effect, domestic sugar enterprises must compete with Thai sugar mainly in consumer segments (B2C channel)

and small F&B customers (SME channel) because sugar imported from Thailand has not yet met the high

requirements of large-scale F&B customers (MNC channel: Pepsi, Coca Cola…).

According to our estimates, the production cost of white sugar in Thailand is at an average of 8,400 VND/kg since

the buying price of raw sugarcane in this country is subsidized by the Thai Government and fixed at an average

level of 630,000 - 650,000 VND/ton. The FOB export price of Thailand’s white sugar in 2019/20 is at an average

of 11 baht/kg (~8,100 VND/kg - according to USDA). Currently, Thailand’s export prices are low (almost equivalent

to their production cost), in order to compete in the global export market.

(Back)

APPENDIX 05: Details of Decision 2466/QD-BCT on the decision to investigate the application of anti-

dumping and anti-subsidies measures for imported sugarcane products originating from Thailand

On September 21, 2020, the Ministry of Industry and Trade issued a decision to investigate imported sugarcane

products originating from Thailand (HS code: 1701.1300; 1701.1400; 1701.9910) which are currently subject to a

5% tariff ( under the ATIGA Agreement) and not subject to import quotas.

Before that, domestic sugar production and trading companies had accused the act of dumping and subsidizing

of the Thai sugar industry damaged the domestic sugar industry, hence, proposed to apply antidumping tax at

37.9% for investigated goods.

As such, the Ministry of Industry and Trade will investigate the impact of dumping and subsidy of Thai sugar, and

determine the damage to the domestic sugar industry. The duration of the antidumping investigation is 12

months and must not exceed 18 months in case of extension (according to Clause 3, Article 70, Chapter IV,

Law on Foreign Trade Management 2014). During the time of investigation, goods under investigation are required

to declare even without any restrictions on the quantity, volume or value of imports; and may be subject to a

temporary antidumping duty.

After the investigation, the Investigation Agency will issue an investigation conclusion. At that time, official

antidumping measures will be issued by the competent authority.

(Back)

Estimated minimum selling price of official Thai sugar in Vietnam

Costs VND/kg

Production cost 8,400

Shipping cost 1,500 - 2,000

Local and distribution advantages 400 - 1,000

Tariff (5%) 400

Estimated Thai sugar selling price in Vietnam 10,500

Source: VSSA, OCSB, FPTS Research and Estimate

Average production cost of white sugar in 2019/20

Vietnam Thailand

Sugarcane price (VND/ton) 900,000 650,000

Efficiency (kg sugar/01 ton of sugarcane) 104 110.5

Cost of sugarcane/ 01 kg of sugar 8,650 5,882

Cost of white sugar production (VND/kg) 12,300 8,400

HSX: SBT

www.fpts.com.vn Bloomberg – FPTS <GO> | 12

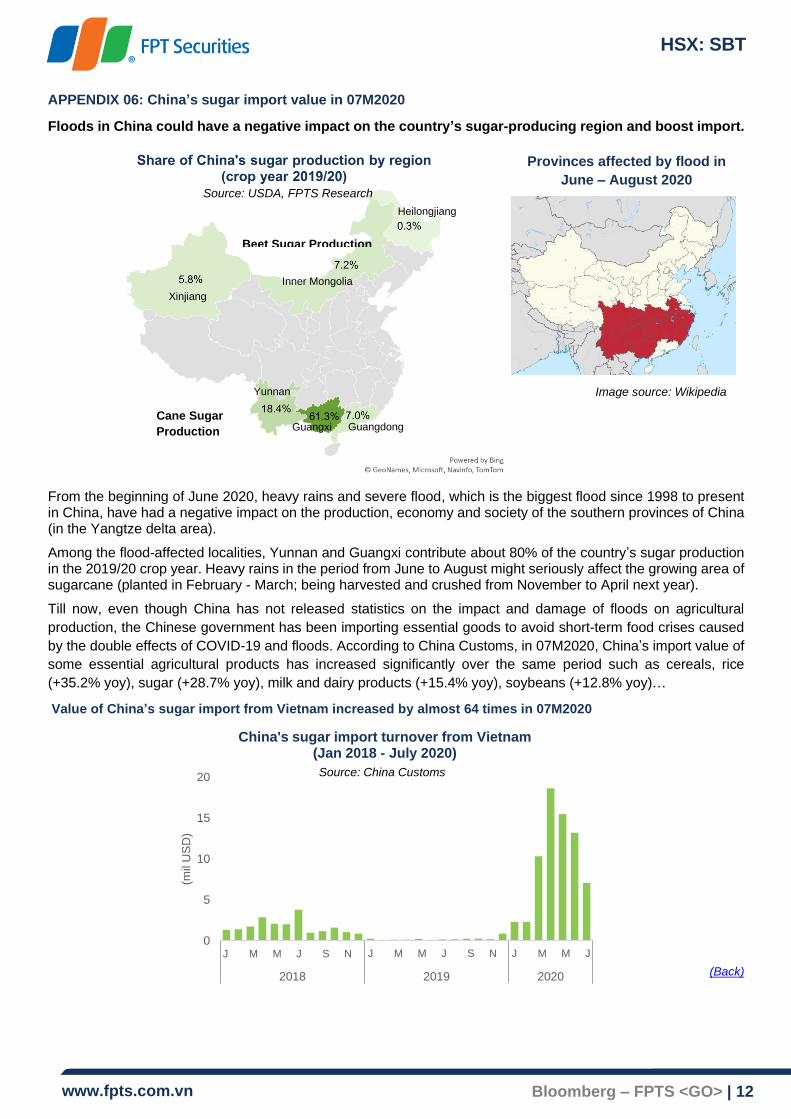

APPENDIX 06: China’s sugar import value in 07M2020

Floods in China could have a negative impact on the country’s sugar-producing region and boost import.

From the beginning of June 2020, heavy rains and severe flood, which is the biggest flood since 1998 to present in China, have had a negative impact on the production, economy and society of the southern provinces of China (in the Yangtze delta area).

Among the flood-affected localities, Yunnan and Guangxi contribute about 80% of the country’s sugar production in the 2019/20 crop year. Heavy rains in the period from June to August might seriously affect the growing area of sugarcane (planted in February - March; being harvested and crushed from November to April next year).

Till now, even though China has not released statistics on the impact and damage of floods on agricultural

production, the Chinese government has been importing essential goods to avoid short-term food crises caused

by the double effects of COVID-19 and floods. According to China Customs, in 07M2020, China’s import value of

some essential agricultural products has increased significantly over the same period such as cereals, rice

(+35.2% yoy), sugar (+28.7% yoy), milk and dairy products (+15.4% yoy), soybeans (+12.8% yoy)…

Value of China’s sugar import from Vietnam increased by almost 64 times in 07M2020

(Back)

Cane Sugar

Production

Beet Sugar Production

Xinjiang

Inner Mongolia

Heilongjiang

Yunnan

Guangxi Guangdong

Provinces affected by flood in

June – August 2020

Image source: Wikipedia

Source: USDA, FPTS Research

0

5

10

15

20

T1 T3 T5 T7 T9 T11 T1 T3 T5 T7 T9 T11 T1 T3 T5 T7

2018 2019 2020

(mil

US

D)

China's sugar import turnover from Vietnam (Jan 2018 - July 2020)

Source: China Customs

J M M J S N J M M J S N J M M J

HSX: SBT

www.fpts.com.vn Bloomberg – FPTS <GO> | 13

Disclaimer

All of information and analysis in this report made by FPTS based on reliable, public and legal sources. Except for

information about FPTS, we do not guarantee about the accuracy and completeness of these information.

Investors who use this report need to note that all of judgements in this report are only subjective opinions of FPTS.

Investors have to take responsibility about their decisions when using this report.

FPTS might make investment decisions based on information in this report or others and do not have any claim on the

legal perspective of given information.

By the time of publishing the report, FPTS holds 31 shares of SBT, the analyst and the approver do not hold any share

of the subject company.

Information related to stocks and industries could be viewed at https://ezsearch.fpts.com.vn or will be

provided upon official request.

© Copyright by FPT Securities 2010

FPT Securities Joint Stock Company

Head Office

No. 52 Lac Long Quan St, Buoi Ward,

Tay Ho District, Hanoi, Vietnam

Tel: (84.24) 3 773 7070 / 271 7171

Fax: (84.24) 3 773 9058

FPT Securities Joint Stock Company

Ho Chi Minh City Office

3rd Floor, Ben Thanh Times Square,

136-138 Le Thi Hong Gam St, D1,

Ho Chi Minh City, Vietnam.

Tel: (84.28) 6 290 8686

Fax: (84.28) 6 291 0607

FPT Securities Joint Stock Company

Da Nang City Office

3rd Floor, Trang Tien Building,

No. 130 Dong Da St, Hai Chau District,

Da Nang City, Vietnam

Tel: (84.23) 6 3553 666

Fax: (84.23) 6 3553 888