understanding the behavior of fdi and its role in capital formation in egypt

TRANSCRIPT

Understanding the Behavior of FDI and Its

Role in Capital Formation in Egypt

By

Ali Massoud, Ph.D.

Visiting scholar at Claremont Graduate University, USA

Associate professor of Economics, Sohag University, Egypt

1

Abstract:This paper attempts to fill the gap in the current

literature that deals with FDI in Egypt. The purpose of

this paper is twofold: to introduce a new

classification of FDI episodes in Egypt during the

period from 1970 to 2012 and to examine the impact of

FDI on capital formation in Egypt during the same

period. The findings of this paper can be summarized as

follows. (1) Out of the eighteen speed up episodes of

FDI, seven episodes were identified as surges. FDI’s

surge episodes were found to be associated with major

economic reforms. (2) Out of the thirteen slow down

episodes of FDI, five episodes were identified as

stops. FDI’s stop episodes were found to be associated

with political turbulences in Egypt and/or in the

region. (3) Over the period from 1977 to 2012, FDI was

found to have insignificant impacts on gross capital

formation in Egypt. However, when I dropped out the

period that witnessed large surges in FDI inflows to

Egypt for purchasing the privatized public firms and

2

estimated the model over the period from 1977 to 2002,

FDI inflows were found to have a positive and

significant impact on gross capital formation.

Understanding the Behavior of FDI and ItsRole in Capital Formation in Egypt

ByAli Massoud, Ph.D

Visiting scholar at Claremont Graduate University, USA

Associate professor of Economics, Sohag University, Egypt

Introduction:

Since the Egyptian authorities implemented what is

known as “Open Door Policy” in October 1974, Egypt

changed its view on foreign direct investment (FDI).3

Thus, the government has given various types of

incentives for foreign investors to invest in Egypt. It

is not difficult to understand why does the Egyptian

government do that? FDI is not only a source of finance

for development in Egypt, but also a mean of

technological transfer as well. Egypt can use FDI in

extracting natural resources. Foreign multinationals

bring in capital, knowledge, and advanced technology.

However, contracts with multinationals have to be

managed in a way that enhances spillover-effects on

other sectors. Moreover, FDI should be encouraged

towards industry and manufacturing activities. Poelhekke

and Ploeg (2010) have argued that FDI that is directed to

the natural resources sector is proven to have less

spillover-effects than FDI that is directed to other

sectors. Tho Nguyen, et al (2011) and De Gregorio (2003) have

reviewed a wide range of literature dealing with the

impact of FDI and natural resources on economic growth.

FDI is found to be more attractive than other forms of

foreign investment because of the following reasons.

(1) FDI is less reversal than other forms of

investment. Capital flows reversals have been proven to

4

be a source of financial crises. Sula (2010) have found

that if capital flow is dominated by private loans and

portfolio flows rather than FDI, it has a high

probability to end with a sudden stop that may lead to

a financial crisis. (2) FDI, if it is associated with

sound policies, has proven to have a stronger impact on

economic growth comparing with other sources of foreign

investment. (3) FDI involves a risk-sharing

relationship with local investors. Such a criterion

does not exist in the formal contractual arrangements

for foreign loans as well as all types of portfolio

investments.

This paper tends to tackle two issues that the current

literatures on FDI inflows to Egypt lack. The first issue is

identifying the behavior of FDI in terms of speed up,

surge, slowdown, and stop episodes. The importance of

that is enhancing policymakers’ understanding of the

behavior of FDI inflows to Egypt and the reasons behind

this behavior. The second issue is investigating the impact

of FDI on capital formation in Egypt over a very long

period of time. The timeframe of the study is from 1970

to 2012. This timeframe covers the period right before

5

the “Open Door Policy” was introduced in Egypt up to

the most recent years. As far as I know, no empirical

studies so far cover this issue over this long

timeframe. The paper proceeds as follows. Section (1)

provides a brief summary of the most related literature

to the topic under investigation. Section (2) analyzes the

distribution of FDI inflows in the whole world and

emphasizes where do developing countries and Egypt

stand in terms of their share of FDI inflows? Section (3)

examines the behavior of FDI inflows to Egypt and

identifies its speed up, surge, slow down, and stop

episodes. Section (4) presents a simple model to estimate

the impact of FDI on gross capital formation in Egypt.

Section (5) emphasizes the conclusion remarks and the

policy implications that come out of this study.

(1) Literature Review:

This section presents an overview of the most related

literature to the two dimensions covered by this paper.

First, how can various episodes of FDI be identified?

Second, what is the impact of FDI on capital formation

in Egypt?

6

Regarding the identification of FDI’s episodes, Calvo, et al. (2004) have

defined a Sudden Stop as a phase that: (1) contains at

least one observation where capital flows fall under

two standard deviations below its sample mean. (2) The

Sudden Stop episode ends when the capital flows exceed

one standard deviation below its sample mean. By using

this technique, they identified the episodes of Sudden

Stops for 32 developed and developing countries. Reinhart

and Reinhart (2008) used two samples of advanced and

emerging countries to catalog capital inflow

“Bonanzas”. The first sample contains 181 countries and

covers the period from 1980 to 2007. The second sample

contains 66 countries and covers the period from 1960

to 2007. They defined a sudden stop as a deterioration

in the current account deficit / GDP ratio that lies

within the threshold of the 20th percentile of the

sample countries. Forbes and Warnock (2011) differentiated

between four episodes of capital flows: Surges, Stops,

Flight, and Retrenchment. They identified the four

episodes using three criteria: “(1) current year-over-year

changes in four-quarter gross capital inflows or outflows is more than two

standard deviations above or below the historic average during at least

one quarter of the episode; (2) the episode is defined as lasting for all7

consecutive quarters for which the year-over-year change in annual gross

capital flow is more than one standard deviation above or below the

historical average; (3) the length of the episode is greater than one

quarter.” (p.9). They used quarterly data on gross capital

flows for a sample of 58 countries over the period from

1980 to 2009 in order to identify the four types of

episodes they cited above. Burger and Ianchovichina (2014)

defined a surge episode of FDI as an increase in the

FDI/GDP ratio in a given year by more than one standard

deviation above its average. A stop episode was defined

in a symmetric way. They also imposed one more

restriction to FDI movements to be considered as a

surge or as a stop. According to this restriction, an

increase/ decrease in FDI/GDP ratio should fall with in

the top 25th percentile of the entire sample. They used

data for 95 developing countries covering the period

from 1990 to 2010 in order to identify FDI surges and

stops episodes using their definition of these episodes

as cited above. They also differentiated between two

types of FDI: Greenfield FDI and Mergers & Acquisitions

FDI.

8

Regarding the impact of FDI on capital formation, Acar, et al (2012)

used a panel data analysis to examine the relationship

between FDI and capital formation in 13 countries

through the MENA region covering the period from 1980

to 2008. They found a negative impact of FDI on capital

formation for the sample countries included in the

model. They concluded that for the 13 countries in the

MENA region, FDI is associated with a reduction in

domestic investment which means that FDI crowds out

domestic investment in this group of countries. Fry (1993)

used a sample of 16 developing countries. He found that

in 11 countries out of them, FDI has been associated

with a reduction in domestic investment. Timmer and Ark

(2002) examined the impact of FDI on capital stock in

Korea and Taiwan. They found a low share of FDI on

capital stock. Hejazi and Pauly (2002) used annual industry-

level data for the period from 1983 to 1995 in order to

examine the impact of FDI on domestic capital formation

in Canada. They found that FDI is a supplement to

domestic capital formation in Canada. Krkoska (2001)

examined the impact of FDI on gross fixed capital

formation in the transition economies in Central and

9

Eastern Europe. He found that FDI has a positive impact

on gross fixed capital formation.

(2) FDI inflows around the world: Where do developing

countries and Egypt stand?

From 1970 to 2012, FDI inflows around the world

accumulated to 21.3 trillion USD. Developed countries

have received 62% of global FDI flows and developing

countries received 34% while the transition economies

only received 4% of the world FDI flows. This means

that developed countries have received the largest

share of global FDI flows among the other groups of

countries while the transitions economies received just

a fraction of global FDI flows. But, how was the

historic trend of the distribution of FDI inflows among

these groups of countries like? To answer this

question, I graphed the distribution of FDI during four

periods of time. These periods are: 1970-19980, 1981-

1990, 1991-2000, and 2001-2012.

During the period from 1970 to 1980, developed

countries received more than 227 billion USD which was

around 77% of the total FDI inflows around the world.

During the same period, developing countries received10

more than 66 billion USD which was around 23% of the

total FDI inflows while transition economies received a

small share of FDI which was 23.6 million USD.

During the period from 1981 to 1990, there was no

substantial change in the distribution of global FDI

inflows among the different groups of countries. Over

this period, developed countries had kept their large

share of FDI and even their share increased by 1% to

get 78% of the global FDI inflows. Developing countries

lost 1% of its share to end up getting 22% of the

global FDI inflows. For the transition economies, they

received only 132 million USD from global FDI inflows

during this period.

To examine the trend of FDI inflows into the main

groups of countries during the period from 1991 to

2000, this section sheds light on the behavior of FDI

to these groups. During this decade, developed

countries had received the largest share of global FDI

inflows. This group received 72% of global FDI inflows.

However, its share declined from 78% during the

previous decade to 72% during the decade under

examination. For developing countries, their share from

11

global FDI inflows during this decade increased to 27%

compared with its share over the previous decade which

was 22%. Also, during this decade, transition economies

share of global FDI increased. This group of countries

received more than 51 billion USD which is much more

than what it had received during the previous period.

The period from 2001-2012 had witnessed a noticeable

change in the distribution of global FDI inflows among

the main groups of countries. During this period,

developed countries received around 8.5 trillion USD in

the form of FDI inflows. Even though the FDI received

by developed countries increased dramatically in

comparison with what this group received in the

previous period, its share declined from 72% to 58%

during the previous period. For developing countries,

FDI inflows increased dramatically during this period

as well. FDI inflows to this group of countries

increased from being around 1.4 trillion USD in the

previous period to be around 5.5 trillion USD in this

period. Moreover, its share of global FDI inflows

increased to be 37% compared with its share in the

previous period which was 27%. For transition

12

economies, they received during this period around

713.4 billion USD compared with what they received

during the previous period which was around 51.1

billion USD. Their share increased as well to reach 5%

from global FDI inflows compared with their share in

the last period which was 1%.

We conclude from the previous analysis that: (1)

developed countries have received the largest share of

global FDI. (2) The last decade has witnessed a sharp

increase in global FDI inflows into all groups of

countries. (3) During the last decade, both developing

countries and transition economies received higher

shares of global FDI inflows than they used to receive

during the previous decades. (5) Global FDI inflows are

moving in favor of developing countries.

To investigate to what extent Egypt has been a

destination for global FDI, I examined the share of

Egypt from global FDI and compared this share with what

developing countries had received from 1970 to 2012.

During the period from 1970 to 1980, Egypt received

around 2.3 billion USD of FDI inflows. In the same

period, developing countries received around 66.713

billion USD. Thus, Egypt’s share of global FDI inflows

overall this decade was 3% of the global FDI that

flowed into developing countries.

Over the period from 1981 to 1990, FDI inflows into

developing countries accumulated to 233.5 billion USA

which more what was received during the previous period

which was around 66.7 billion USD. This means that FDI

growth was 250% between this period and the previous

period. For Egypt, its share from FDI that flowed into

developing countries increased to 4% compared to its

share in the previous period which was 3%. Egypt

received around 8.8 billion USD as FDI inflows during

this period. If we compare this number with what Egypt

received from FDI inflows during the previous period,

we find that FDI inflows into Egypt increased by 283%

and this was more than the increase that happened in

the size of FDI that developing countries received

between the decade under investigation and the previous

decade.

During the period from 1991 to 2000, developing

countries received around 1.4 trillion USD in form of

FDI inflows. This period had witnessed a sharp increase

14

in global FDI inflows to developing countries. What

developing countries received during this period

increased dramatically by 507% of what these countries

received during the previous decade. From the data, we

conclude that this decade witnessed a large surge in

global FDI that flowed into developing countries. The

question now is where did Egypt stand among developing

countries regarding the size of FDI it received during

this period? As figure (8) shows, the answer for this

question is not in favor of Egypt. Egypt’s share from

FDI inflows to developing countries during this decade

declined to be only 1% from being 4% in the previous

decade. Not only did Egypt’s share of FDI inflows to

developing countries decline, but also the size of

these inflows declined during this decade as well. It

declined to be around 8.5 billion USD instead of being

8.8 billion USD during the previous decade. This means

that the size of FDI inflows to Egypt during this

decade declined by 3.4%. But why did Egypt’s position

in terms of what it received of FDI deteriorate during

the decade under investigation? I argue that the main

reason behind this deterioration is the first gulf war

at the beginning of this decade. This argument is15

supported by the noticeable decline in FDI inflows into

Egypt during 1991 and 1992.

The rest of this section is allocated to investigate

where did Egypt stand in terms of the size of FDI it

received during the period from 2000 to 2012? During

this period, FDI inflows to Egypt during the period

under investigation increased dramatically to be around

55.5 billion USD. By comparing this size with the size

of FDI that Egypt received during the previous decade

which was 8.5 billion USD, FDI inflows increased by 553

%. For Egypt, this is just a historical jump in FDI

inflows. But does this mean that Egypt’s position among

developing countries, in terms of FDI inflows that it

received during this period, had changed? During the

period under investigation, developing countries

received around 5.5 trillion USD in forms of FDI

inflow. By comparing this with the size of global FDI

that developing countries received during the previous

period which was around 1.4 trillion USD, I found that

FDI inflows to developing countries grew by a rate of

293%. We conclude from this figure that the sharp

increase in global FDI inflows was not a special case

16

for Egypt, but it was a common phenomenon for

developing countries.

This phenomenon can be attributed to the following

reasons. (1) The decline in the rate of return on

investments in developed countries. (2) The decline in

the global investment risk. (3) The global financial

crisis that started in developed countries between 2007

and 2008 and erupted all over the world afterward. (4)

The development that took place in the financial

markets in developing countries. (5) The accumulation

of human capital in developing countries. (6) The

tendency of developed countries to move some of their

heavy industries to developing countries. (7) During

this period many developing countries speeded up their

economic reform program which encouraged foreigners to

buy domestic assets.

(3) The behavior of FDI inflows into Egypt:

To examine the behavior of FDI inflows to Egypt from

1970 to 2012, I used the following steps. Firstly, I

graphed the data to see how it looks like and to

identify the behavior of FDI inflows to Egypt.

Secondly, I introduced a modification to the approach17

used by Calvo, et al. (2004); and Forbes and Warnock (2011) to

identify capital flows surges and stops. I applied

their technique after the modification to identify

various episodes of FDI inflows. This paper

differentiates among four episodes of FDI as follows:

speed up, slow down, surge, and stop. Using data for

FDI inflows to Egypt during the period under

investigation, I identified the four episodes mentioned

above.

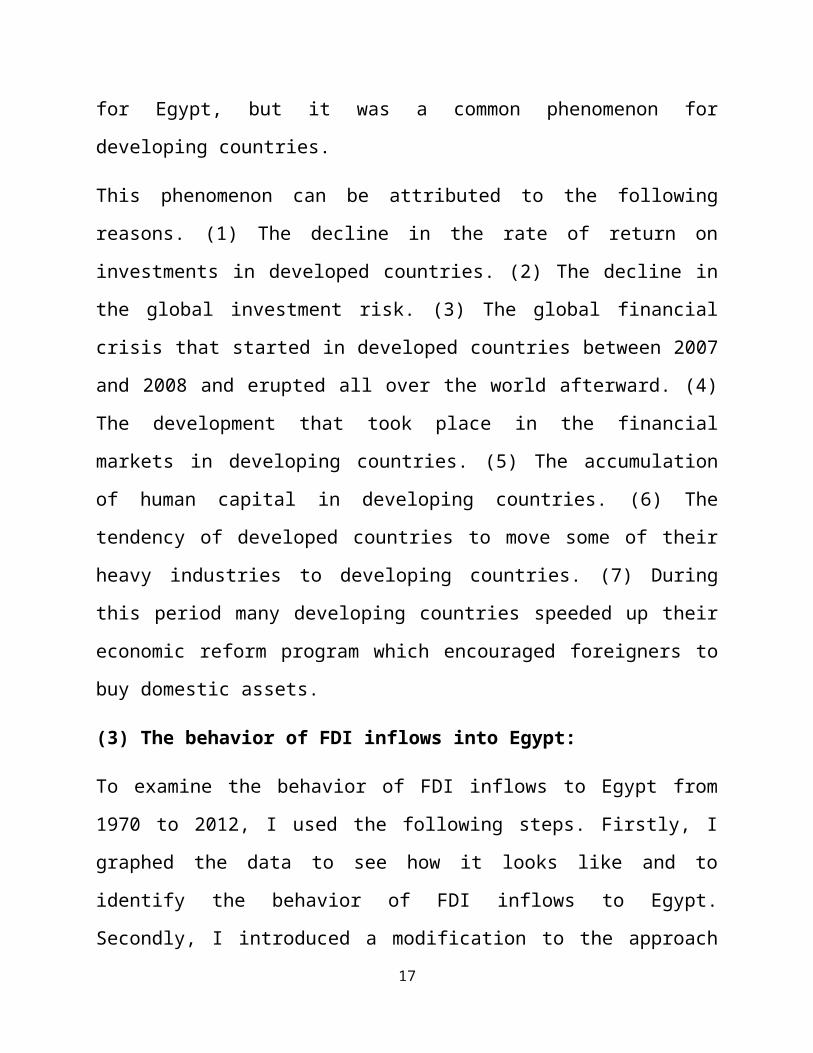

Firstly, what the data on

FDI inflows to Egypt looks

like. Figure (1) shows

that FDI inflows to

Egypt were extremely

low during the first

half of the 1970’s.

However, starting

from 1977 it increased to reach its peak in 1979. This

can be attributed to the economic reforms that the

Egyptian authorities had taken in the second half of

the 1970’s as a part of the “Open Door Policy”. Then,

overall the following years and up until 2004, FDI

18

1970

197419781982

19861990

1994

19982002

2006

2010-5000

0

5000

10000

15000

Figure (1)FDI inflows to Egypt from 1970-2012 millions USD

Year

FDI

infl

ows in

milli

ons

USD

inflows never reached 1.3 billion USD. In 2004, FDI

inflows were about 2.2 billion USD and this was the

first time in the history of FDI inflows to Egypt to

reach the 2 billion USD. Then, the size of FDI inflows

continued to increase to reach its peak in 2007 when it

was about 11.6 billion USD. This sharp increase in FDI

inflows can be attributed to the acceleration of

privatization program during this period. In 2008, FDI

inflows declined by 18% from its level in 2007 to be

around 9.5 billion USD. FDI inflows had continued to

decline over the following years until it crashed

dramatically in 2011 to be (-482.7) million USD. This

means that FDI in 2011 declined by 108% from its size

in 2010.

Secondly, identifying the speed up, slow down, surge, and stop

episodes for FDI inflows.

In this section, I identify the speed up, slow down,

surge, and stop episodes of FDI inflows to Egypt. To

calculate these episodes, I conducted the follow steps.

(1) I calculated the rolling mean for 5-year periods

for FDI inflows from 1970 to 2012. (2) I calculated

the standard deviation from the rolling mean for every19

5-year period. (3) I defined the above episodes as

follows:

“Speed Up”: an increase in FDI inflows in a given

year that is more than one standard deviation

above its 5-year rolling average.

“Slow Down”: a decline in FDI inflows in a given

year that is more than one standard deviation

below its 5-year rolling average.

“Surge”: an increase in FDI inflows in a given

year that is more than one standard deviation

above its 5-year rolling average and this increase

in FDI inflows should fall within the top 25th

percentile of the entire sample.

“Stop”: a decline in FDI inflows in a given year

that is more than one standard deviation below its

5-year rolling average and this decline in FDI

inflows should fall within the top 25th percentile

of the entire sample.

Based on the above methodology, I identified the

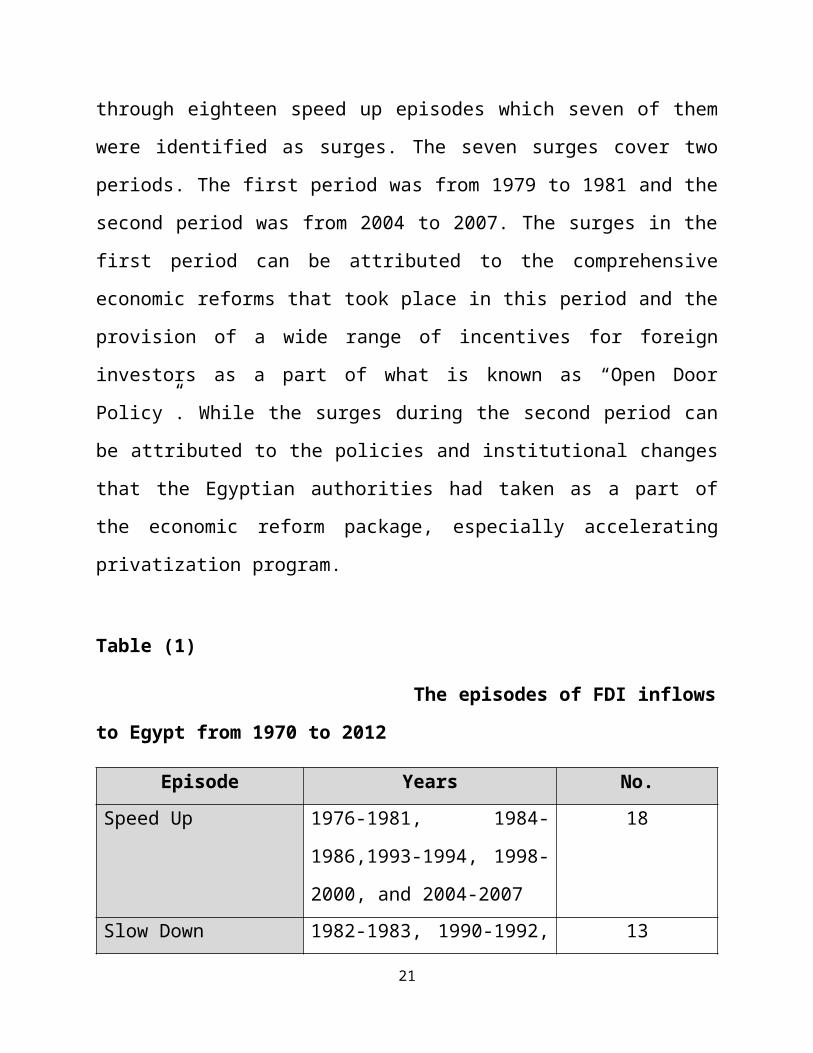

various episodes as defined before. Table (1)

summarizes the identified episodes. As table (1) shows,

over the period from 1970 to 2012, FDI inflows had been

20

through eighteen speed up episodes which seven of them

were identified as surges. The seven surges cover two

periods. The first period was from 1979 to 1981 and the

second period was from 2004 to 2007. The surges in the

first period can be attributed to the comprehensive

economic reforms that took place in this period and the

provision of a wide range of incentives for foreign

investors as a part of what is known as “Open Door

Policy”. While the surges during the second period can

be attributed to the policies and institutional changes

that the Egyptian authorities had taken as a part of

the economic reform package, especially accelerating

privatization program.

Table (1)

The episodes of FDI inflows

to Egypt from 1970 to 2012

Episode Years No.Speed Up 1976-1981, 1984-

1986,1993-1994, 1998-

2000, and 2004-2007

18

Slow Down 1982-1983, 1990-1992, 13

21

1995-1996, 2001-2003,

and 2010-2012Surge 1979-1981 and 2004-

2007

7

Stop 1991-1992 and 2010-

2012

5

The open door Policy that the Egyptian authorities

introduced in October 1974 is considered as a very

important step on the road of economic liberalization

and openness toward the rest of the world. Many laws

and decrees were issued in order to encourage foreign

investments in Egypt. However, the most important law

in this matter is law no. 43 that was issued in 1974

and its modifications afterwards. This law has opened

the Egyptian economy for the Arab and foreign investors

to invest in Egypt in almost all sectors: industry,

mining, land reclamation, transportation, tourism,

agriculture products, housing, banking, and insurance.

This law not only provides protection for foreign

investments in Egypt, but also provides taxes incentive

for them. To liberalize trade, law no. 118 was issued

22

in 1975 to give private sector the right to import and

export, which is very important to FDI inflows.

Moreover, many steps were taken in order to reform

foreign exchange market. For instance, law no. 97

issued in 1976 allowed private banks that have a

foreign share to deal with foreign exchange. All these

steps stimulated foreign investors and multinationals

to think about Egypt as a promising destination which

lead to the capital surge during the late of 1970’s.

One of the main institutional reforms in Egypt that has

been playing a very important role in attracting FDI

inflows to Egypt is the establishment of the General

Authority for Investment and Free Zones in 2004. This

specialized authority has been providing all data and

information that foreign investors need in order to

invest in Egypt. It also markets the investment

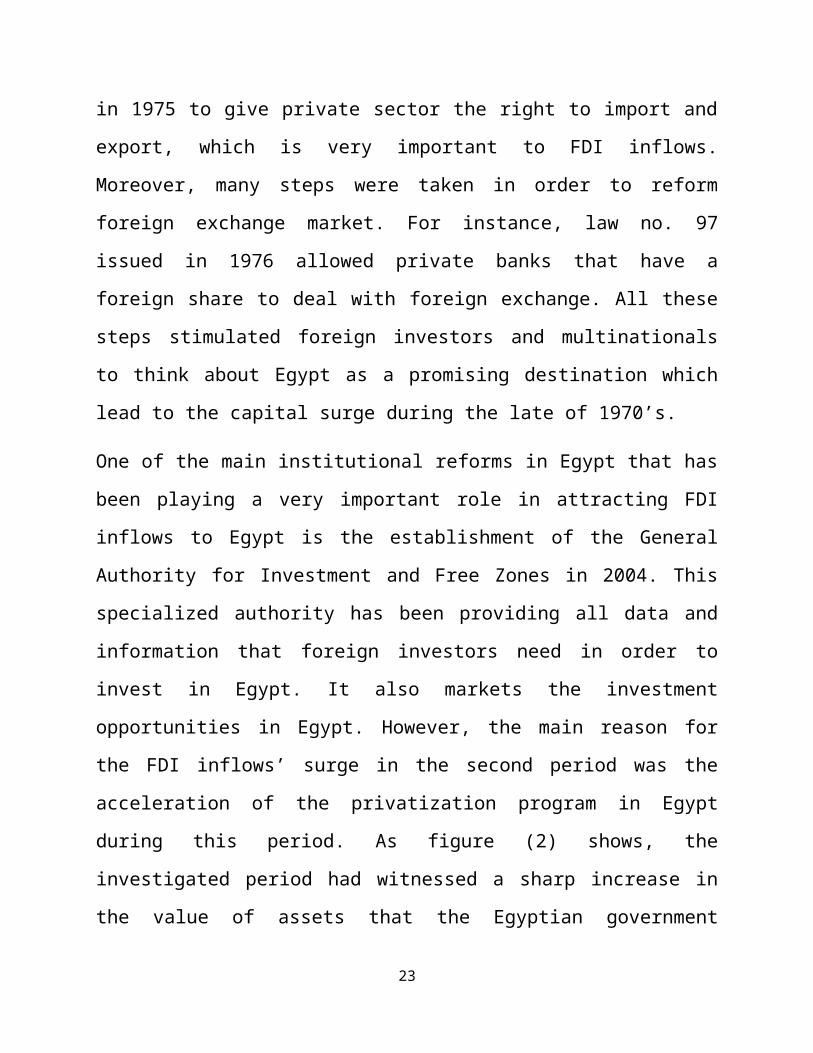

opportunities in Egypt. However, the main reason for

the FDI inflows’ surge in the second period was the

acceleration of the privatization program in Egypt

during this period. As figure (2) shows, the

investigated period had witnessed a sharp increase in

the value of assets that the Egyptian government

23

privatized. Privatization program reached its peak in

2006. During this year, the government privatized a

number of public sector companies that accumulated to

around 2.2 billion USD.

Also table (1) shows that during the investigation

period, FDI inflows had been through thirteen slow down

episodes which five of them were identified as stops.

The five stops cover two periods. The first period was

from 1991-1992 and the second period was from 2010-

2012. The first stop can be attributed to the “First

Gulf War” while the second stop can be attributed to

the political and social unrest as a result of what is

well known as “the 25th of January Revolution”. Even

24

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 20090

2000

4000

6000

8000

Figure (2)Privatization Value from 2000 to 2008 (in millions USD)

Years

mill

ions

USD

though the year of 2010 witnessed a stop episode in FDI

inflow, but this can be attributed to the global

financial crisis from 2007 to 2008. The negative impact

of this crisis on FDI inflows to Egypt had continued

from 2008 to 2010. However, the dramatic decline in FDI

inflows to Egypt happened in 2011.

(4) FDI and Capital Formation:

One of the main reasons for a developing country to

open up its economy for FDI is its willingness to

achieve a higher level of capital formation.

In this section, I used a simple model in order to

examine to what extent FDI has helped Egypt to achieve

a higher level of capital formation. The rest of this

section is allocated for model specification, data

sources, the estimation technique, model testing, and

the estimation results.

Model specification, in order to examine to what extent FDI

has helped Egypt to achieve a higher level of capital

formation, I used the following model.

CF = C + β1TR + β 2CR + β 3 FDI + µ

Where:

25

CF is gross capital formation as a percentage of GDP,

as defined in the World Bank Database (World

Development Indicators). According to the World

Development Indicators database “Gross capital formation

consists of outlays on additions to the fixed assets of the economy plus net

changes in the level of inventories. Fixed assets include land improvements

(fences, ditches, drains, and so on); plant, machinery, and equipment

purchases; and the construction of roads, railways, and the like, including

schools, offices, hospitals, private residential dwellings, and commercial

and industrial buildings. Inventories are stocks of goods held by firms to

meet temporary or unexpected fluctuations in production or sales, and

work in progress. According to the 1993 SNA, net acquisitions of valuables

are also considered capital formation.”

C is a constant term.

TR is trade as a percentage of GDP. Trade as defined

in the World Development Indicators database “is the sum of

exports and imports of goods and services.”

CR is domestic credit to private sector as a percentage

of GDP. As defined in the World Development Indicators

Database, “domestic credit to private sector refers to financial

resources provided to the private sector, such as through loans, purchases

of nonequity securities, and trade credits and other accounts receivable,

26

that establish a claim for repayment. For some countries these claims

include credit to public enterprises.”

FDI is foreign direct investment inflows.

µ is the residuals term.

Data sources, I used two sources of data for the

variables included in the model. For gross capital

formation, trade, and domestic credit to the private

sector, I used World Development Indicator Database

that published by the World Bank. For foreign direct

investment, I used the UNCTAD database. The data in the

model covers the period from 1977 (when FDI starts to

flow into Egypt in a considerable size as a result of

the” Open Door Policy” that had been implemented by the

Egyptian government in October 1974) to 2011, the years

in which the data for all variables was available.

The estimation technique, to conduct a time series analysis,

I used “Least Squares” technique and E-Views

statistical package version 8 in estimating the model’s

parameters and in conducting all the required tests. To

test for structure break, I conducted Chow Breakpoint Test.

The result suggests that there is no structure break in

27

the series of all variables. As stationary is a very

important condition in time series analysis, I tested

for the unit root using Augmented Dickey Fuller Test. The test

shows that all variables have a unit root. To make

variables stationary, I took the first difference for

all variables and then I applied the unit root test

again. The first difference for all variables was found

to be stationary. This means that all variables are

stationary on AR (1). Thus, the first difference was

used for all variables included in the model.

The estimation result, before presenting the result of the

model estimation, it is worth mentioning to report that

I conducted the following tests in order to be sure

that the model is reliable. First, to test for

Heteroskedasticity, I conducted Breusch-Pagan-Godfrey Test.

The result of the test suggests that there is no

Heteroskedasticity problem. Moreover, I conducted White

Test to test for the same problem. The result of White Test

suggests that there is no Hetroskedasticity as well.

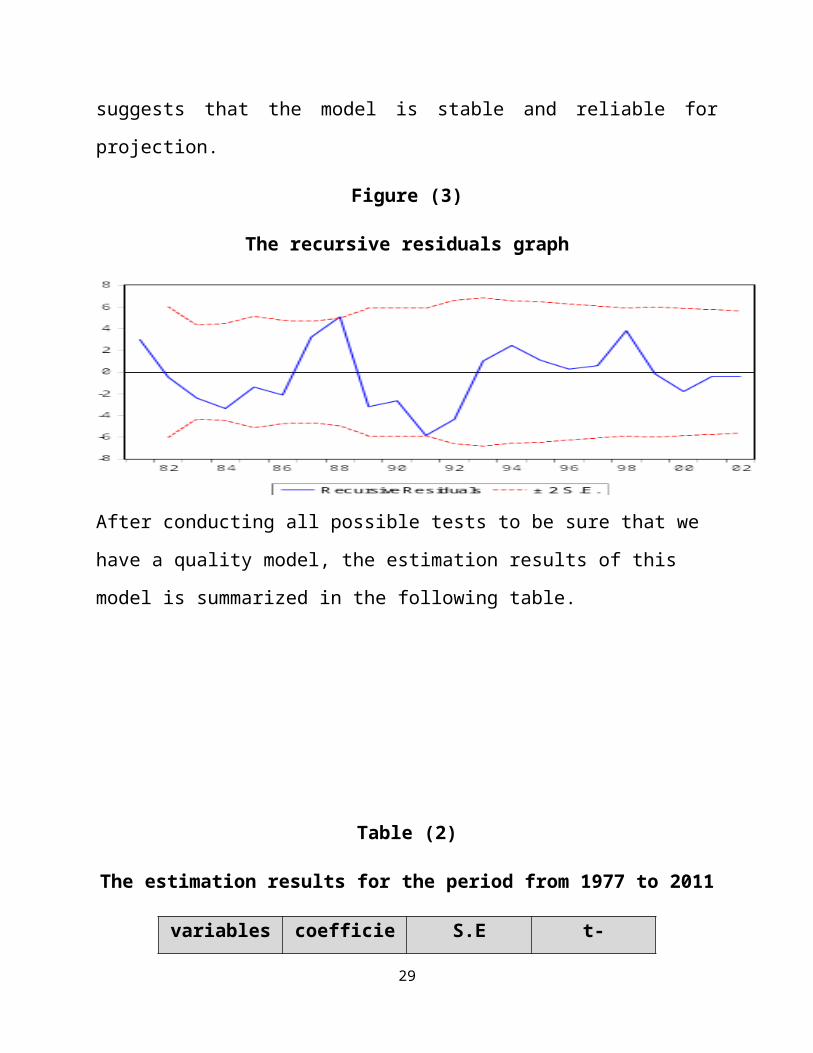

Second, to test for the stability of the model, I used

Recursive Residuals Test. As figure (3) shows, the recursive

residuals are within the intervals of 2 S.E. This

28

suggests that the model is stable and reliable for

projection.

Figure (3)

The recursive residuals graph

After conducting all possible tests to be sure that we

have a quality model, the estimation results of this

model is summarized in the following table.

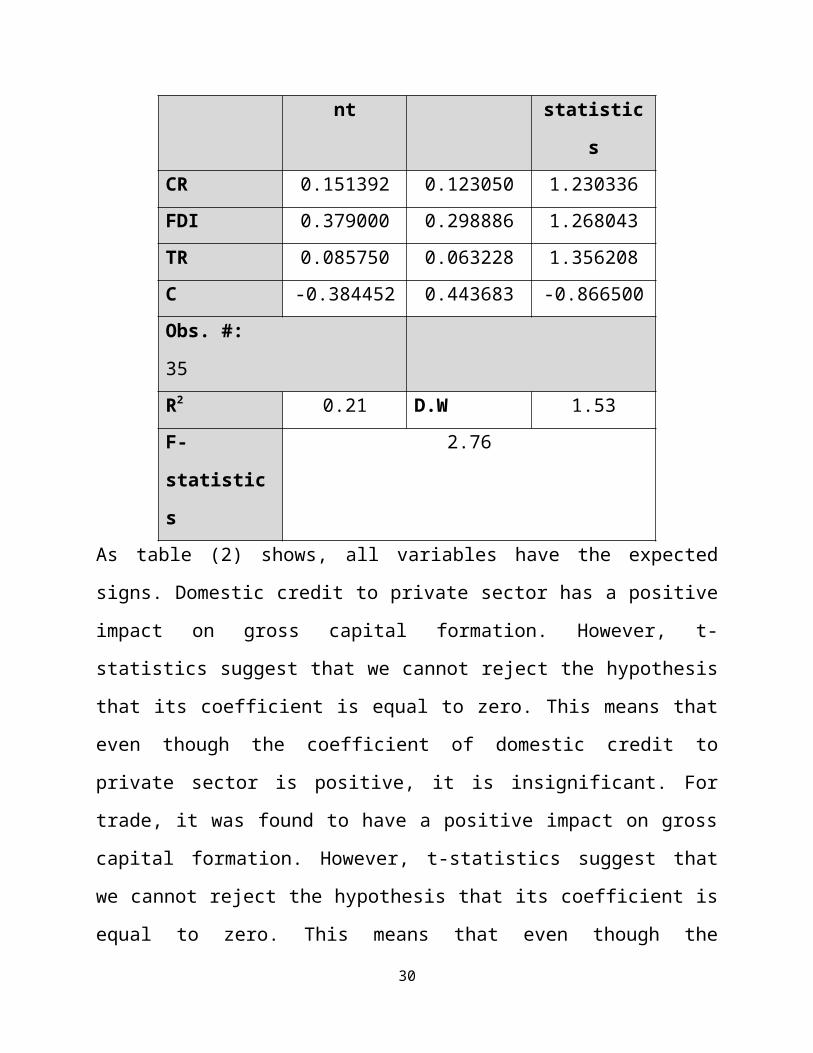

Table (2)

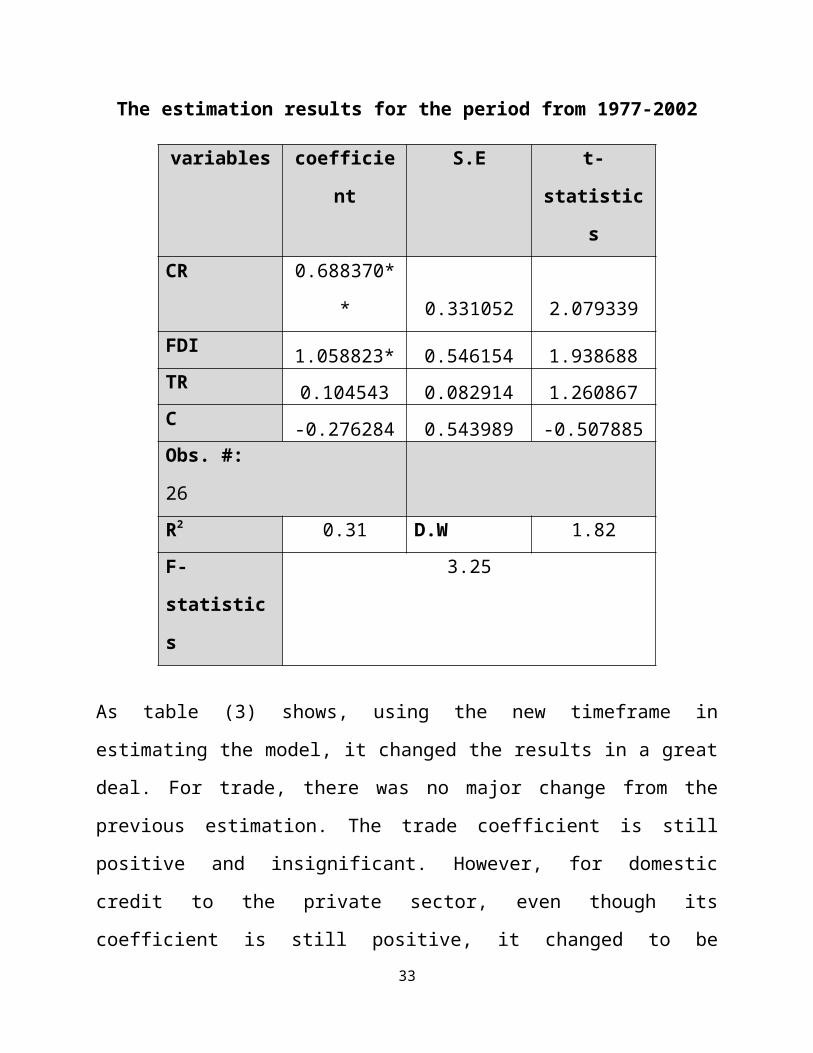

The estimation results for the period from 1977 to 2011

variables coefficie S.E t-

29

nt statistic

sCR 0.151392 0.123050 1.230336FDI 0.379000 0.298886 1.268043TR 0.085750 0.063228 1.356208C -0.384452 0.443683 -0.866500Obs. #:

35R2 0.21 D.W 1.53F-

statistic

s

2.76

As table (2) shows, all variables have the expected

signs. Domestic credit to private sector has a positive

impact on gross capital formation. However, t-

statistics suggest that we cannot reject the hypothesis

that its coefficient is equal to zero. This means that

even though the coefficient of domestic credit to

private sector is positive, it is insignificant. For

trade, it was found to have a positive impact on gross

capital formation. However, t-statistics suggest that

we cannot reject the hypothesis that its coefficient is

equal to zero. This means that even though the

30

coefficient of trade is positive, it is insignificant.

Regarding foreign direct investment, the estimation

results suggest that it has a positive impact on gross

capital formation. However, t-statistics suggest that

we cannot reject the hypothesis that its coefficient is

equal to zero. Thus, we conclude that the coefficient

of foreign direct investments is insignificant. This

means that there is no evidence, based on this model,

that foreign direct investment lead to a higher level

of gross capital formation in Egypt. This result is

consistent with what Timmer and Ark (2002) found. They

found fairly low shares of FDI in the capital stock in

both Korea and Taiwan. Moreover, Acar, et al (2012) found

that FDI has a negative impact on domestic investment

in the MENA region. Fry (193) also found that FDI has a

negative impact on domestic investments. Both the

latter two studies attribute their findings to the

relationship between FDI and local investors. They

argued that FDI has not created business for local

investors, but replaced them instead. Krkoska (2001) found

there is no statistically significant link between FDI

and capital formation in Central and Eastern Europe.

However, it is worth mentioning that Hejazi and Pauly (2002)31

found that FDI is a supplement to Canadian domestic

capital formation. We conclude that the findings from

the model I used go along with most of the other

studies findings. However, the interpretation for why

does the relationship between FDI and gross capital

formation in Egypt during the investigation period is

statistically insignificant? I argue that this result

can be attributed to the fact that a large share of FDI

inflows to Egypt went to the privatized public firms

according to the Egyptian privatization program. To

investigate to what extent this argument is valid, I

run the model by using data covering the period from

1977 to 2002. The new timeframe I used in the model

excluded the period when privatization program was in

its peak which the same period when FDI speeded up very

fast. The results of estimating the model using the new

timeframe is reported in the following table.

Table (3)

32

The estimation results for the period from 1977-2002

variables coefficie

nt

S.E t-

statistic

sCR 0.688370*

* 0.331052 2.079339FDI 1.058823* 0.546154 1.938688TR 0.104543 0.082914 1.260867C -0.276284 0.543989 -0.507885Obs. #:

26R2 0.31 D.W 1.82F-

statistic

s

3.25

As table (3) shows, using the new timeframe in

estimating the model, it changed the results in a great

deal. For trade, there was no major change from the

previous estimation. The trade coefficient is still

positive and insignificant. However, for domestic

credit to the private sector, even though its

coefficient is still positive, it changed to be33

significant at level of 5%. This means that after

excluding the period of the speed up in foreign direct

investments and privatization in Egypt, domestic credit

to the private sector turns to have a statistically

significant impact on capital formation in Egypt.

Regarding foreign direct investment, its coefficient is

still positive. However, this coefficient changed to be

statistically significant at level of 10%. This means

that at a confidence level of 90%, foreign direct

investments have a positive impact on gross capital

formation in Egypt. From the new estimation results, we

conclude that there is an evidence that when a high

percentage of FDI takes the form of merges and

acquisitions, as what happened in the FDI that flowed

to Egypt for purchasing the public sector privatized

firms, FDI turns to have insignificant impact on

capital formation. Rather, it crowds out and replaces

domestic investment. However, when the Greenfield

investment has a high percentage of FDI, we found an

evidence of a positive significant impact of FDI

inflows on capital formation in Egypt.

(5) Conclusion and policy implications:

34

The purpose of this paper is twofold. The first is to

examine the behavior of FDI inflows to Egypt. In doing

so, I introduced a new classification of FDI episodes

as follows: speed up, surge, slow down, and stop. Using

the technique explained in section (3), I identified

eighteen episodes of speed up in FDI inflows. Seven out

of these speed up episodes were identified as surge

episodes. The FDI’s Surge episodes were found to be

associated with introduction of major economic reforms

in Egypt. Also, over the period of the study, I

identified thirteen FDI slow down episodes. Five out of

these slow down episodes identified as stop episodes.

The FDI’s stop episodes were found to be associated

with political turbulences in Egypt or in the Region.

The second purpose of this paper is to estimate the impact

of FDI on capital formation in Egypt. To do so, I used

a time series analysis with a simple model explained in

section (4). The findings of estimating the model over

the period from 1977 to 2011 prove that even though the

coefficient of FDI is positive, it is statistically

insignificant. This means that the model cannot prove

the existence of a positive impact of FDI on capital

35

formation during this period. However, when the model

was estimated using the period from 1977 to 2002, the

FDI coefficient was found to be positive and

statistically significant at level of 10%. This means

that at a confidence level of 90%, foreign direct

investment turns to have a positive impact on gross

capital formation in Egypt. From the new estimation

results, we conclude that there is evidence that when a

high percentage of FDI takes the form of merges and

acquisitions, as what happened in the FDI that flowed

to Egypt for purchase the public sector privatized

firms, FDI is found to have insignificant impact on

capital formation. Rather it crowds out and replaces

domestic investment. However, when the Greenfield

investment has a high percentage of FDI, we found out

evidence of a significant impact of FDI inflows on

capital formation in Egypt.

The main policy implications that emerge from this study can

be summarized as follows. (1) As the development

process in Egypt requires a large size of finance that

it is not available from the domestic sources,

encouraging FDI inflows should be a priority in policy

36

making process in Egypt. (2) As this study shows,

Greenfield FDI has much more impact on capital

formation than mergers & acquisitions FDI. Thus,

Egyptian authorities have to encourage a higher share

of FDI in form of Greenfield investments. As shown in

the literature that has been reviewed in this paper,

FDI that flows into natural resources sector has a weak

spillover effects on other sectors in the economy.

Based on these findings, I encourage the Egyptian

authorities to increase the share of FDI that flows

into industry and other sectors relative to the share

of FDI that flows to natural resources sector.

References:

[1] Acar, S., et al (2012). “The Effect of Foreign

Direct Investment on Domestic Investment: Evidence from

MENA Countries.” European Trade Study Group (ETSG) 14th Annual

Conference.

37

[2] Adhikary, B.K. (2011). “FDI, Trade Openness,

Capital Formation, and Economic Growth in Bangladesh: A

Linkage Analysis.” International Journal for Business and

Management, Vol.6, no.1, pp16-28.

[3] Burger, M. and E. I. Lanchovichina (2014). “Surges

and Stops in FDI Flows to Developing Countries: Does

the Mode of Entry make a Difference?” The World Bank, Policy

Research, Working Paper WPS6771.

[4] Calvo, G.A., et al (2004). “On the Empirics of

Sudden Stops: the Relevance of Balance-Sheet Effects.”

Inter-American Development Bank, Working Paper no.509.

[5] De Gregorio, J. (2003). “The Role of Foreign Direct

Investment and Natural Resources in Economic

Development.” Central Bank of Chile, Working Paper No.196.

[6] Forbes, K.J and F.E.Warnock (2012). “Capital Flow

Waves: Surges, Stops, Flight, and Retrenchment.” Journal

of International Economics, vol.88 (2), pp.235-251.

[7] Fry, M. J. (1993). “Foreign Direct Investment in a

Macroeconomic Framework: Finance, Efficiency,

Incentives, and Distortions.” The World Bank, Policy Research

Working Paper No. WPS1141.

38

[8] Hejazi, W. and P. Pauly (2002). “Foreign Direct

Investment and Domestic Capital Formation.” Industry

Canada Research Program, Working Paper No. 36.

[9] Krkoska, L. (2001). “Foreign Direct Investment

Financing of Capital Formation in Central and Eastern

Europe.” European Bank for Reconstruction and Development, Working

Paper No.67.

[10] Poelhekke, S. and F. v. d. Ploeg (2010). “Do

Natural Resources Attract FDI? Evidence from Non-

Stationary Sector Level Data.” De Nederlandsche Bank, DNB

Working Paper No.266.

[11] Reinhart, C.M. and V.R. Reinhart (2008). “Capital

Flow Bonanzas: an Encompassing View of the Past and

Present.” NBER Working Paper no.14321.

[12] Sula, O. (2010). “Surges and Sudden Stops of

Capital Flows to Emerging Markets.” Open Economies Review

21(4), pp.589-605.

[13] Tho Nguyen, Q., et al (2011). “The Nature and

Growth of Foreign Direct Investment and its Impact in

Vietnam: A National Innovation System Perspective.”

39

Aalborg University, Research Center on Development and International

Relations, Working Paper No.148.

[14] Timmer, M. and B.V. Ark (2002). “Capital Formationand Foreign Direct Investment in Korea and Taiwan:Coping with Diminishing Returns?” in J. Th. Lindblad,ed., Asian Growth and Foreign Capital: Case Studies from Eastern Asia,Aksant, Amsterdam, pp. 59-98.

40