u s. case - shale gas (format)

TRANSCRIPT

SHALE GAS: A glimpse into the Case of the

United States of AmericaScott Nicoll

April 2014

Shale Gas Capacities: The Energy Mix, Transition and

Revolution in the US

Over the last 35 years, the US government has embarked

on several major projects to spur the commercial development

of energy technologies intended to substitute for

conventional energy resources, especially fossil fuels.1

This generalization made here, although correct, was, and

arguably still is today, of little known fact to ordinary

American citizens. Slowly, an alternative energy source,

more specifically shale gas, is entering onto the radar

screen from its previous marginalization. With shale gas

becoming a new ‘blip on the radar’ and garnering more

attention throughout media, magazines, newspapers,

publications and the like, in today’s news, the truth

remains that this energy transition was well under way long

before it reached the headlines. The proceeding section will

stand to outline the energy mix and transition in the US

case that took place after the 1973 global energy crisis.

The energy mix in the US and the transition toward shale gas

production will be discussed to show how the US has become a1 Grossman, Peter Z. U.S. Energy Policy and the Presumption of Market Failure. Cato Journal, Vol. 29, No.2 (Spring/Summer 2009). Cato Institute. March 30, 2014. P.1

2

key player in today’s “shale gas revolution,” or as many

argue, “the shale gas evolution.”

Following the energy crisis of 1973, the stage was set

for the US to seek ways in which to reach energy autarky.

Seeing as at the time, as still today, the US was largely

dependent on oil, the 1973 oil crisis made it that much more

apparent. As a result, President Nixon became the first US

leader to announce a plan, “Project Independence,” that’s

main goal was to put the wheels in motion that would drive

the US to become fully energy independent over decades to

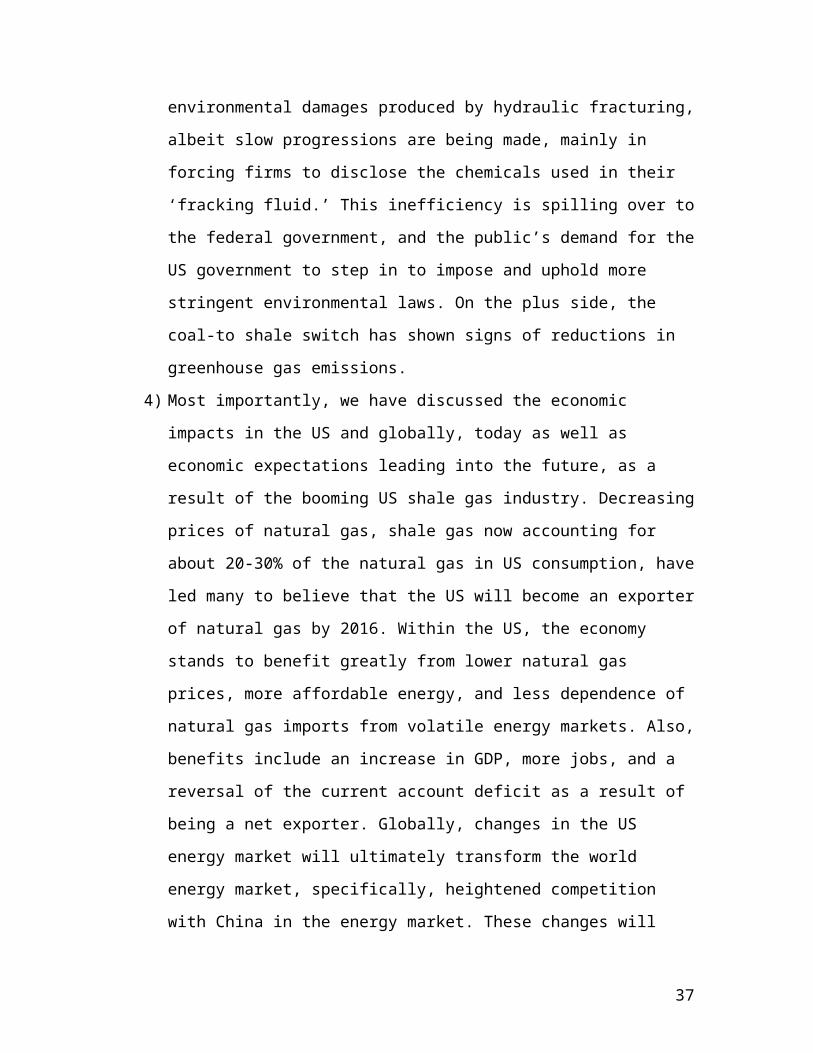

come. Figure 1 depicts the negative impact that the oil

crisis had on the strength of the dollar and overall US

economic growth, thereby ‘shocking’ the US economy as a

whole (see Figure 1). Although Nixon put energy self-

sufficiency on the agenda, it was not until “Ford’s 1975

energy act, plans for energy independence were tied directly

to the development of new, alternative energy technologies.

Under President Carter in particular, the federal government

embarked on highly publicized, heavily funded efforts at

developing new technologies with specific timetables for

commercial entry and, in a few cases, a timetable for mass

market substitution.”2 With the US grappling to level out

the playing field within its domestic economy and between

the OPEC countries throughout the oil shocks of the 1970s, a2 Grossman, Peter Z. U.S. Energy Policy and the Presumption of Market Failure. Cato Journal, Vol. 29, No.2 (Spring/Summer 2009). Cato Institute. March 30, 2014. P.1

3

substantial increase in US energy R&D funding was evident.

During this time, “U.S. federal government spending on key

large scale energy R&D programs was initiated in response to

the oil crisis of the 1970s. Over this period, nearly 24% of

the total federal investment in energy R&D occurred during

the short seven-year span of 1974-1980.”3 The seed of the

shale gas boom was planted in the late 1970s when the US

government decided to fund R&D programs and provide tax

credits (and incentive pricing) for developing

unconventional natural gas in response to the severe natural

gas shortage at the time.4

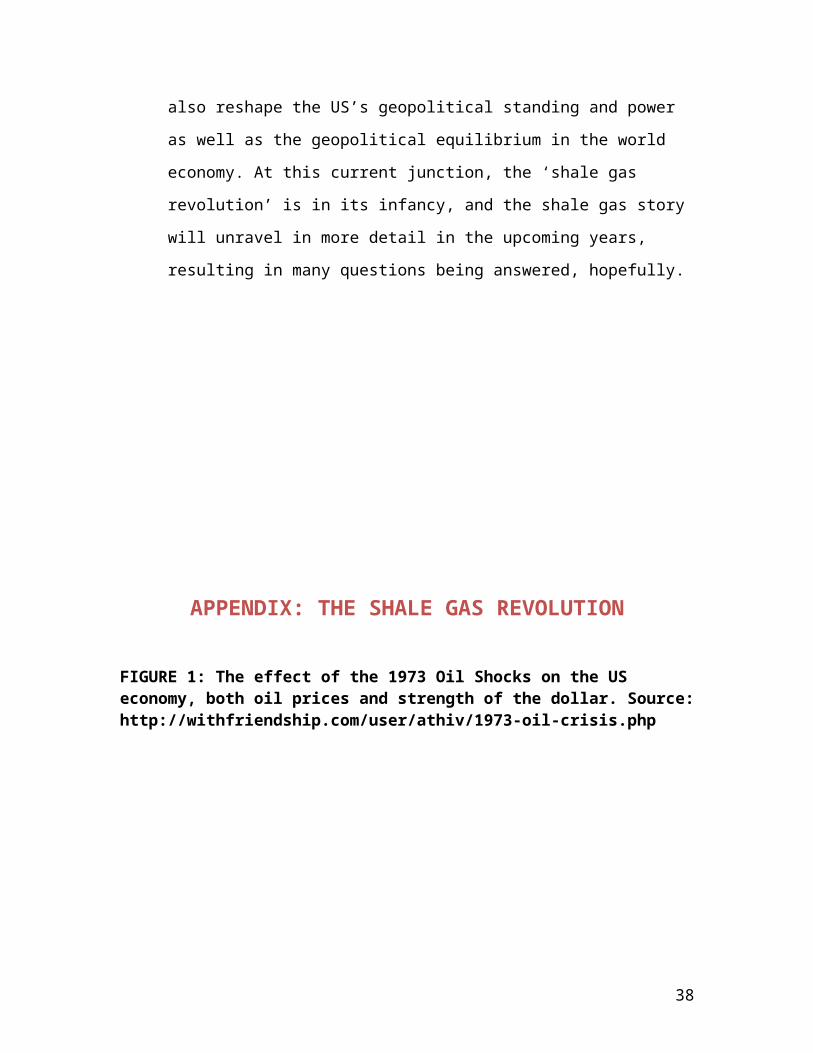

As shown in Figure 2, increases in US government

spending into the R&D energy sector in the 1970s becomes

evident. Another striking fact is that “from 1977-1981,

energy R&D investments briefly rose above 10% of all federal

R&D; however, since the mid-1990s energy R&D has accounted

for only about 1% of all federal R&D investments.”5 Today,

US energy R&D spending is well below its peak in the 1970s,

but US energy R&D levels have been growing in recent years.

A study of funding costs and benefits between 1980 and 2000

noted “more than $9 billion was spent on high visibility

3 Dooley, JJ. U.S. Federal Investments in Energy R&D: 1961-2008. PacificNorthwest National Laboratory. October 2008. P. 24 Krupnick, Alan and Wang, Zhongmin. A Retrospective Review of Shale GasDevelopment in the United States. Resources for the Future. April 2013. P. 35 Dooley, JJ. U.S. Federal Investments in Energy R&D: 1961-2008. PacificNorthwest National Laboratory. October 2008. P. 2

4

alternative energy development projects intended to induce

innovation and overcome perceived market failures; these

produced no quantifiable economic benefit.”6 Many of these

‘alternative energy development projects’ have been centered

around the extensive research and extraction of shale gas,

and more recently, shale ‘tight’ oil. Whether or not these

projects have indeed produced any ‘economic benefits,’ or

even substantial costs, will be discussed later in this

paper. This section is merely meant to discuss the

progressions regarding the rise of shale gas as an

alternative source of energy in the US economy, sparked by

the oil shocks of the 1970s.

The point to be drawn here is that, although shale gas

has been around for decades, and that the US government has

been aware of its existence and investing in its research

and extraction, it was not until recently that shale gas has

become a viable, and realistic option. “George P.

Mitchell is regarded as the father of the shale gas

industry, by making it commercially viable in the Barnett

Shale by getting costs down to $4 per million British

Thermal Units. Mitchell Energy achieved the first economical

shale fracture in 1998 using slick-water fracturing. Since

then, natural gas from shale has been the fastest growing

contributor to total primary energy in the United States” 6 Fri, R. W. (2006) "From Energy Wish Lists to Technological Reality." Issues in Science and Technology. Available at www.issues.org/ 23.1/fri.html.

5

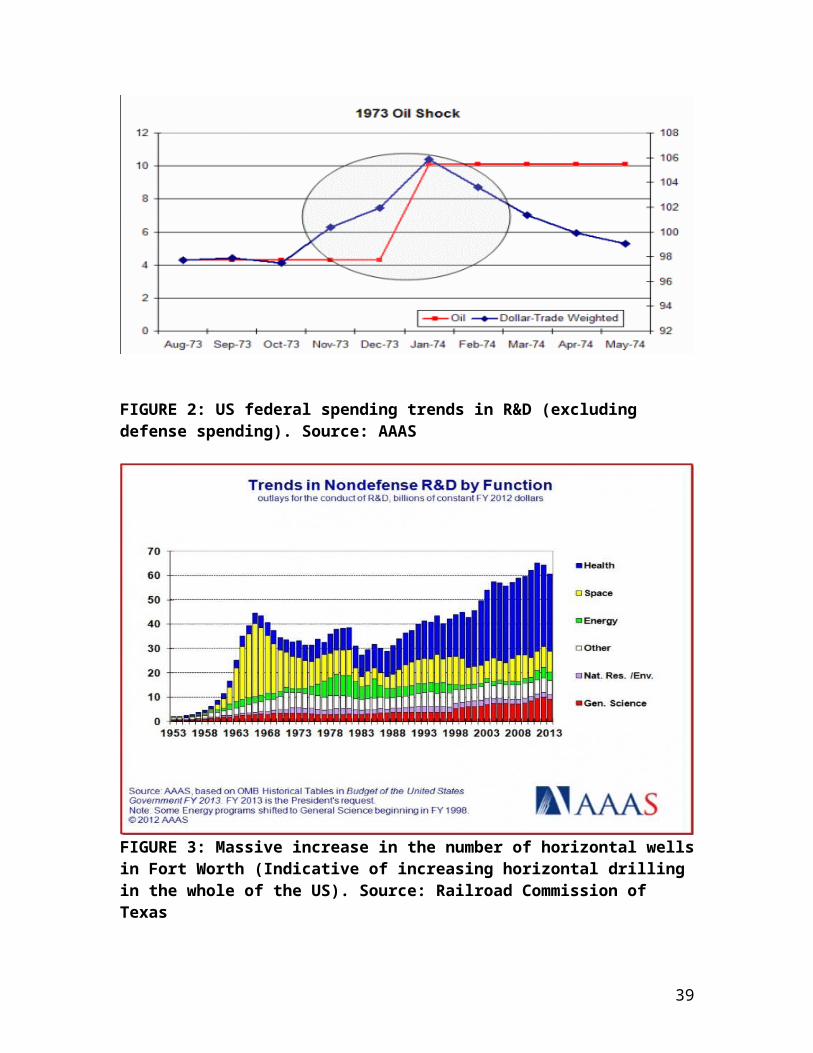

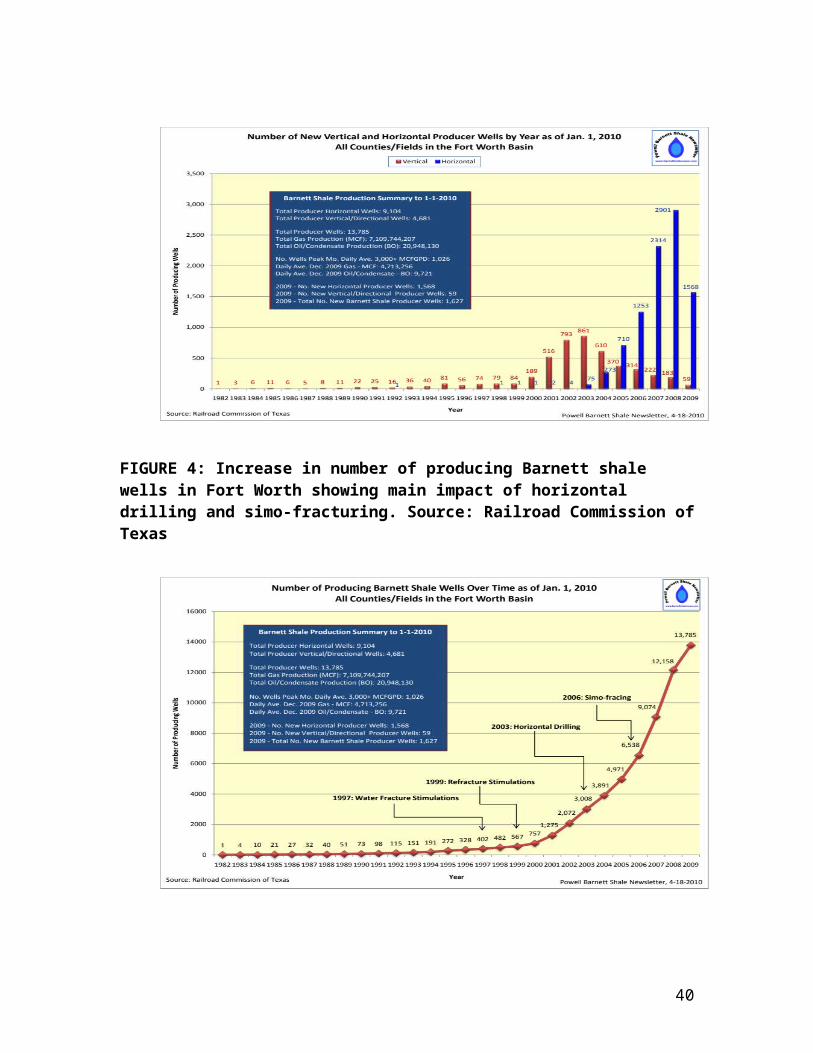

(Shale Gas, Wikipedia, See Figure 3 and 4). This

commercialization of shale gas enabled companies and private

investment sectors to infiltrate the shale gas arena,

therefore leading to its massive expansion over the past

decade. Along with this fact, two other factors allow for

the explanation of the ‘shale gas revolution,” technology

and high prices of natural gas:

Geologists have long been aware of the presence of large amounts of methane in

subterranean shale rock layers. Indeed, much of the conventional gas resources

that have been exploited for well over a century were simply pockets of shale gas

that had over time migrated upward and collected in easily accessible pools

(often associated with far more lucrative pools of petroleum). However, until

recently, shale as a source rock for extracting natural gas was deemed

uneconomical by industry because unlike conventional gas, shale gas was not

collected in pools but rather tightly compressed in the tiny seams within the

dense layer of rock itself. The roots of the recent revolution are twofold. The first

is technological: by combining innovations in horizontal drilling with the high-

pressure injection of a cocktail of water, chemicals, and sand into the horizontal

layer of shale at regular intervals thereby creating larger fissures (“hydraulic

fracturing” or “fracking”), the industry was able to recover large volumes of

methane at an acceptable cost. Second, the sustained relatively high price of

natural gas sent—and in markets outside North America, continues to send—

market signals to industry that there was money to be made by applying these

technologies on a widespread basis7 (Refer to Figure 5).

7 Boersma, T., and Johnson, C. (2012). The Shale Gas Revolution: US and EU Policy and Research Agendas. Review of Policy Research 29(4): 570-576.

6

Culminating from Nixon’s initial views held in “Project

Independence,” in the 1970s for implementing programs

“needed to stimulate domestic production” (Nixon 1974), came

the seed for the ‘shale gas revolution.’ America’s

dependence on expensive foreign oil, shaken by the

instability of oil producing countries, and the arduous

nature of oil markets, sparked the tinder wood that was the

US’s desire to be energy independent. These infant programs

and “the severe natural gas shortage led to the passage of

the Natural Gas Policy Act of 1978 (NGPA), which required

phased removal of wellhead price controls and provided

incentive pricing for developing new natural gas, including

natural gas from unconventional sources. The natural gas

shortage also led federal agencies to establish R&D programs

on unconventional natural gas.8 Coupled with these R&D

programs came an influx in government policies, which were

justified in that private companies, at the time, lacked the

proper incentive for risky R&D investments, more

specifically, investments in extracting unconventional

natural gas and the necessary technologies required to do

so. In referring to one of the most fundamental concepts in

economics, the Law of Supply, one of the essential ways to

increase the supply of any good, is through technological

advancement. In the early 21st century, the technology

necessary for the extraction of shale gas came to form:8 Krupnick, Alan and Wang, Zhongmin. A Retrospective Review of Shale GasDevelopment in the United States. Resources for the Future. April 2013. P. 7

7

A number of factors converged in the early 2000s to make it profitable for firms

to produce large quantities of shale gas, but the most important factor was

technology innovation, which took a long time to develop and ultimately made it

cost-effective to produce shale gas… some of the key technology innovations

resulted from government research and development (R&D) programs and

private entrepreneurship that aimed to develop unconventional natural gas (e.g.,

shale gas, coalbed methane, and tight gas), but some of the key technologies

(e.g., horizontal drilling and three-dimensional [3-D] seismic imaging) were

largely developed by the oil industry to explore and produce oil instead of

unconventional natural gas.9

The final step to take in this section of the energy

transition to shale gas in the US is to depict its standing

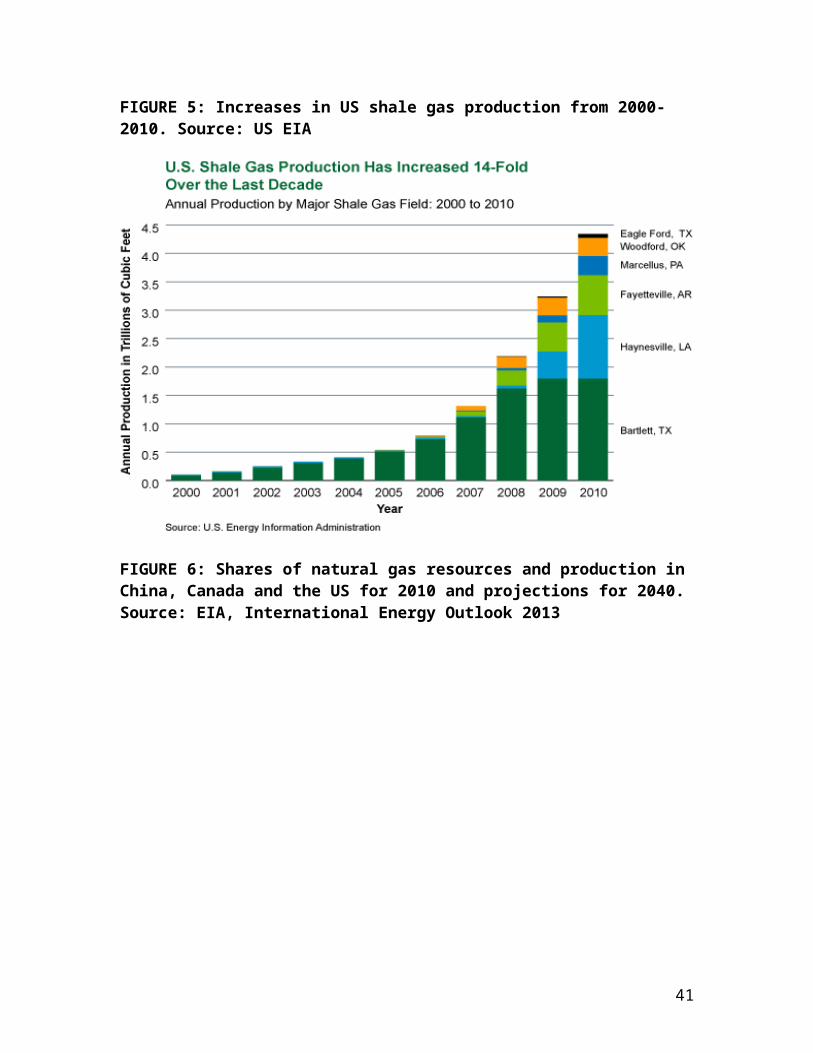

today and projections for the future. As is clearly seen in

Figure 6, from an EIA International Energy Outlook 2013

report, the importance of shale gas and tight gas are on the

rise, and there are major expectations for the rise to

continue well into the future. It becomes evident that the

projected energy mix in the US‘s future expectations, show a

major shift toward shale gas and tight gas. “The EIA expects

the United States to become a net exporter of LNG in

2016...By 2010 shale gas constituted 23% of US gas

production, a significant change from the previous year,

during which shale gas constituted only 14% of the total

9 Krupnick, Alan and Wang, Zhongmin. A Retrospective Review of Shale GasDevelopment in the United States. Resources for the Future. April 2013. P. 3

8

country’s gas production”10 The US Energy Information

Administrations’ Annual Energy Outlook 2013 has projected a

44% increase in US natural gas production by 2040, mainly

due to the surge in shale gas production. Another decisive

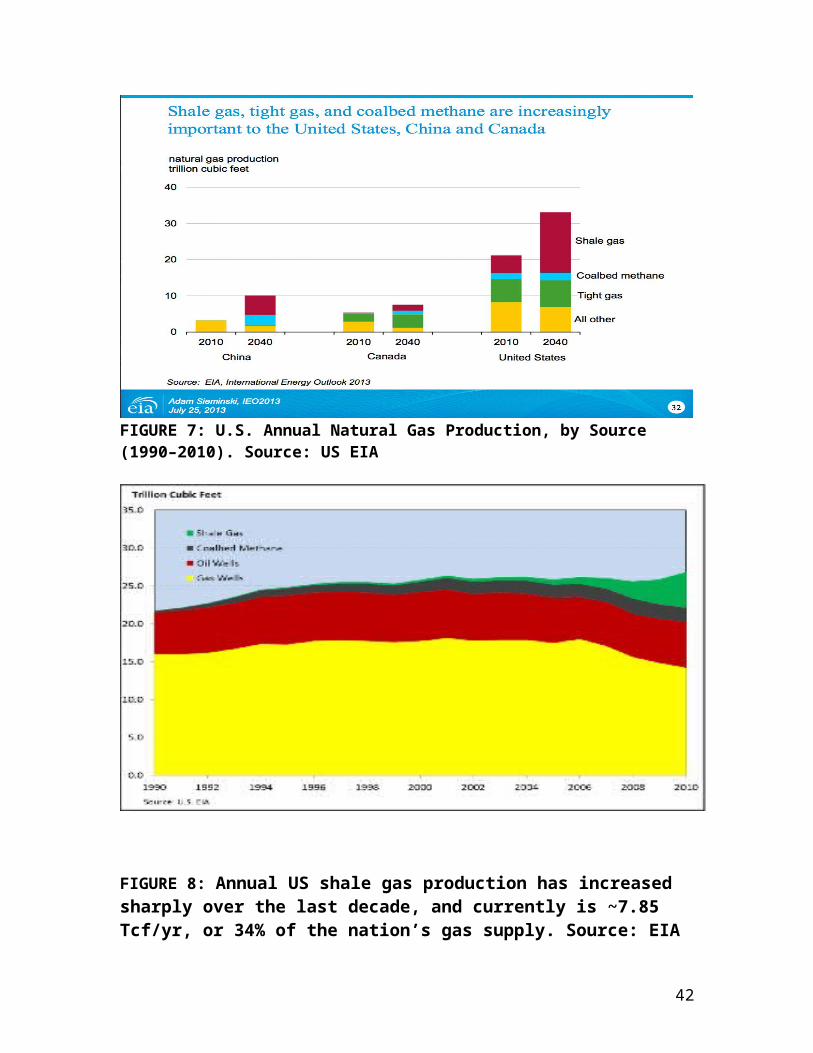

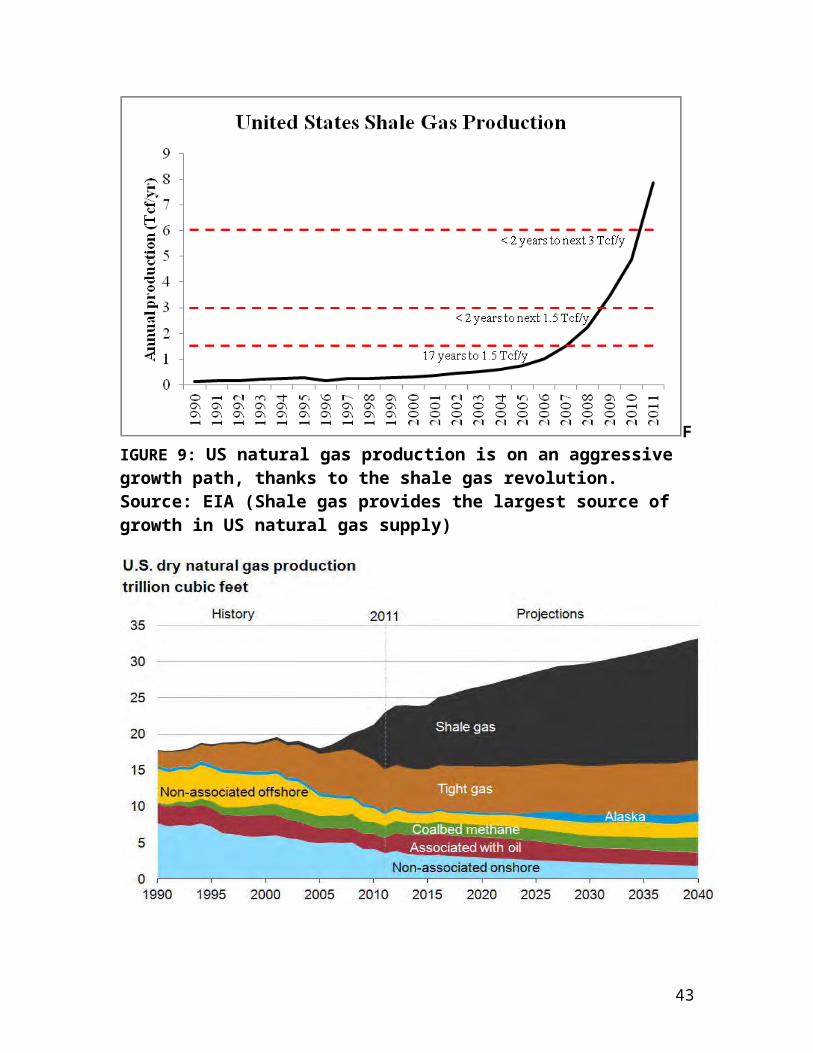

picture is painted by the increases in shale gas production,

annually from 1990-2010, that today have greatly contributed

to more than 20 percent of the US’s domestic natural gas

production (See Figures 7-9). Again, these figures depict

the aggressive nature of the US growth plan to incorporate

shale and tight gas as the leaders in the overall US natural

gas production. While conventional natural gas production in

the U.S. has decreased over time, shale gas has become a

rapidly increasing source of U.S. gas supplies, accounting

for about 20 percent of total U.S. onshore domestic natural

gas production in 2010. The U.S. Energy Information

Administration (EIA) forecasts that, by 2035, shale gas

could account for over 50 percent of onshore natural gas

production.11 Herein lies a sizable issue in the unknown

ripples to be caused by the ‘shale gas revolution,’ what

effects will it have on the US energy mix, as well as the

world energy market, and as seen in the disparities within

the EIA reports regarding shale gas’ projected capacities,

what are the true effects that these uncertainties will have

10 Boersma, T., and Johnson, C. (2012). The Shale Gas Revolution: US andEU Policy and Research Agendas. Review of Policy Research 29(4): 570-576.11 Continental Economics, Inc. The Economic Impacts of U.S. Shale Gas Production on Ohio Consumers. Continental Economics, Inc. January 2012. P. 7

9

on the US and the global economic and political landscape?

Most unpredictably, and arguably most importantly, are

the varied dialogues surrounding shale gas and its potential

effects on the US energy market, the world economy, and the

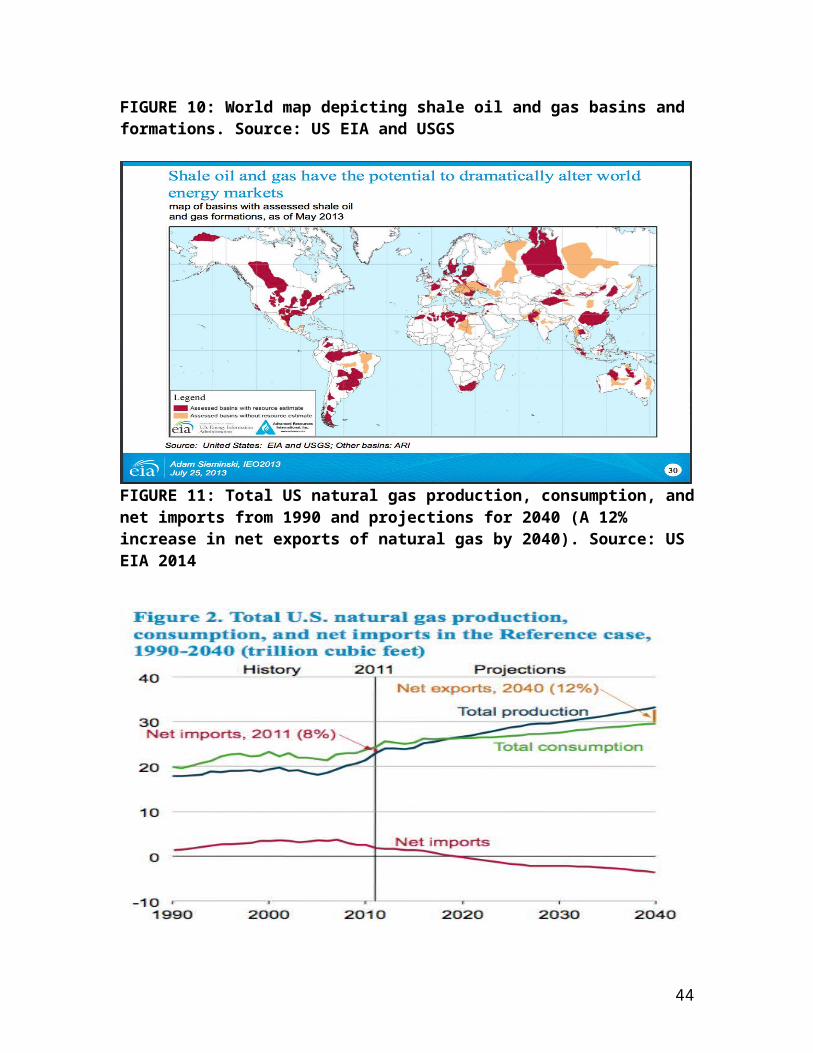

revival of the US as a world power. As depicted in Figure

10, basins of shale oil and gas formations have been found

across the globe, albeit many have still not been tapped

into due to various factors such as technology and

government policies. For those countries that have already

begun to extract and put to use the benefits of shale gas

and oil, the US for example, have sparked discussions of

increased power and stability, both economically and

geopolitically:

Fortunately for the United States’ prospects of retaining its pre-eminence in

international politics, there are indications that such a ‘propulsive engine’ is

emerging. After years of dwindling reserves, the US oil and gas industry is in the

embryonic stages of a dramatic reversal of fortunes. Vast deposits of shale gas

and oil, previously either undiscovered or considered not technically recoverable

—a view that prevailed as little as five years ago—have begun to be exploited.

These shale ‘plays’ suggest the prospect of a complete transformation of the US

energy industry, serving to aid the revival of America’s industrial base, and even

offering the potential for energy self-sufficiency. Such an eventuality could have

important geopolitical implications, not simply bolstering American power, but

somewhat weakening the relative power of OPEC and exporters of conventional

natural gas such as Russia. The implications for global politics, however, if the

10

more optimistic predictions of US shale gas and oil reserves are fully realized,

have not been fully factored into narratives of American decline; and indeed, they

offer a different future for the United States in its attempt to retain hegemony.12

Significantly, this ‘transformation of the US energy

industry’ on the future outlook for the US energy mix,

suggests a beneficial shift toward shale gas and shale oil.

US forecasts project the US as a net exporter of liquefied

natural gas (LNG) by 2016, thereby implicating changes to

the US domestic energy arena, as well as a major shift in

global energy trends, both politically and economically.

This power shift to shale gas in the US energy mix scheme is

largely due to decreasing levels of LNG imports, as a direct

result of domestically sourced shale gas. As US dry natural

gas production continues to increase (1.3 percent per year),

it will eventually outpace total consumption, projected by

2019, and therefore spike natural gas net exports. As shown

in Figure 11, projected US net exports of natural gas, has a

potential 12 percent increase by 2040, in combination with a

steadily decreasing stream of net imports of natural gas.

“Although coal is expected to continue its important

role in U.S. electricity generation, there are many

uncertainties that could affect future outcomes. Chief among

them are the relationship between coal and natural gas

12 Hastings, David Dunn and McClelland, Mark J.L. Shale gas and the revival of American power: debunking decline? International Affairs © 2013 The Royal Institute of International Affairs. Published by John Wiley & Sons Ltd. International Affairs 89: 6 (2013) 1411–1428

11

prices and the potential for policies aimed at reducing

greenhouse gas (GHG) emissions.”13 Looking into other

sectors, low natural gas prices, a direct result of domestic

shale gas production, have sparked use in both the electric

and industrial power sectors. “In the Reference case,

natural gas use in the industrial sector increases by 16

percent, from 6.8 trillion cubic feet per year in 2011 to

7.8 trillion cubic feet per year in 2025…The natural gas

share of generation rose from 16 percent of generation in

2000 to 24 percent in 2011 and increases to 27 percent in

2025 and 30 percent in 2040.”14 As it is still too early to

provide any definitive answers to the potential that shale

gas and oil has to shift away from US coal use, the picture

will become clearer depending on the future sustainability

of natural gas prices and environmental polices that come to

form.

Lastly, these polices that will continue to take shape

over time as shale gas extraction continues to rise, fossil

fuel regulations and renewable energy subsidies stand to

drastically reshape the competitive nature of electricity

generating technologies. In turn, these regulations set

forth will put coal at a major disadvantage in that they

significantly restrict their emission control cost. “On

13 Annual Energy Outlook 2013 with Projections to 2040. DOE/EIA-0383. April 2013. P. 314 Annual Energy Outlook 2013 with Projections to 2040. DOE/EIA-0383. April 2013. P. 5

12

March 16, 2011, the EPA proposed the Mercury and Air Toxic

Standards (MATS), a nationwide limit on power plant

emissions of mercury. Under this rule, all coal and oil-

fired power plants with a nameplate capacity greater than 25

MW will have to reduce their mercury emissions to 90% below

their uncontrolled emissions levels.”15 These regulations

have helped propel the coal – gas shift in the US energy

mix. Furthermore, regulations and subsidies, coupled with

inexpensive natural gas, place technologies such as wind and

solar at a major disadvantage in the renewable energy sector

by making them comparatively and economically uncompetitive.

In combination, the merger of three important and

necessary factors can be said to have led to the explosion

of shale gas extraction and distribution paralleled by the

US shift in its energy mixture scheme, mainly from coal to

gas; ‘government research and development (R&D) programs and

private entrepreneurship that aimed to develop

unconventional natural gas’ (the seed which was planted in

the 1970s), technological innovation (‘hydraulic fracturing

or fracking,’ ‘horizontal drilling,’ and ‘three-dimensional

seismic imaging’ – See Figure 11) that led to the affordable

costs of shale gas extraction, and finally, the volatile

natural gas markets coupled with the high prices of natural

gas that plagued the US import market for decades. All of

15 Cohen, Andrew Knoller. The Shale Gas Paradox: Assessing the Impacts of the Shale Gas Revolution on Electricity Markets and Climate Change. Harvard College. May 2013. P 75

13

these factors converged in the early 21st century,

ultimately transforming the structure of the US energy mix,

to create the phrase that we so often see today in the

headlines, ‘the shale gas revolution.’ With this so-called

‘revolution’ at our doorsteps, much controversy and debate

envelops shale gas and shale oil, from environmental issues,

international politics, and their effects on the globalized

world economy. As this revolution strides into its youth,

many of the questions posed will soon be answered, whether

good or bad. And much is yet to been seen insofar as to what

shale gas and oil will do to ‘transform’ the US economy, and

how this energy transition that started so many decades ago,

will lead to changes in today’s globalized world.

Governance: US Federal and State Government Legislation

As was previously discussed in the prior section, US

government involvement in this shale gas “bridge-fuel” has

been there from the onset, and “the catalyst for the

policies on unconventional natural gas was the severe

natural gas shortage in the 1970s.”16 As seen, the tinder

wood that was the search for alternative sources of energy,

initiated by Nixon’s “Project Independence” plan, was

sparked by sizable increases in ‘federal government spending

16 Krupnick, Alan and Wang, Zhongmin. A Retrospective Review of Shale Gas Development in the United States. Resources for the Future. April 2013. P. 6

14

on key large scale energy R&D programs,’ as well as the

introduction of incentive pricing and tax credits. These

infant programs and policies ultimately led to the

technological advancements necessary to make shale gas

extraction a viable and worthwhile investment. More

specifically, “much of the credit for the technological

advancements that allowed the shale gas development is owed

to the members of the Mitchell Energy shale gas team, in

particular to the late George Mitchell (1919 – 2013), who

worked to refine shale technologies despite harsh criticism,

especially in the Barnett shale formation of northern Texas.

Hydraulic fracturing has been so successful that energy

experts have called this the ‘most significant energy

innovation so far of this century.’”17 This innovation,

along with the US governments initial programs, set the

stage, and led to the structure that currently holds US

government and state regulations on the shale gas industry.

This section will outline some of the historical polices and

initiatives that were created in the 1970s, some of those

which have greatly affected the shale gas industry today,

and depict the current breakdown of US federal and state

governance in the ‘shale gas revolution.’

As pressure mounted due to the decline of US natural

gas reserves, the oil shocks of the 1970s, and the

consistently high prices of natural gas, the US government 17 Mary Lashley Barcella & David Hobbs, Fueling North America’s Energy Future, THE WALL STREET JOURNAL, Mar. 10, 2010, at A10

15

began to take the necessary steps to rid of these pressures,

and take steps toward alternative, unconventional natural

gas sources. All of these efforts have eventually led to the

shale gas picture we see today:

“Several major studies commissioned by the Federal Power Commission, the

Energy Research and Development Administration (ERDA), and the US

Department of Energy (DOE) in the 1970s suggested that the resource base of

unconventional natural gas could be very large and that efforts to develop

unconventional resources should be encouraged and subsidized. In the late

1970s, the annual production of unconventional natural gas was less than 5

percent of total annual gas production, but conventional natural gas production

started to decline and was widely expected to continue to decline… A federal law

in 1974 created ERDA by merging several separate research programs, including

those of the technology research centers of the Bureau of Mines, the fossil energy

R&D programs under the US Department of the Interior, and the system of

national laboratories under the Atomic Energy Commission (which was abolished

at that time). In October 1977, DOE was created to consolidate in one agency the

responsibilities for energy policy and R&D programs, including those of ERDA

and the energy-related responsibilities of the US Departments of Agriculture,

Commerce, Housing and Urban Development, and Transportation (Secretary of

Energy Advisory Board 1995). The budget for energy research, especially for fossil

energy programs, significantly increased. NETL (2010) notes that between 1973

and 1976, total federal spending on energy research more than doubled, and the

fossil-energy component increased more than tenfold from 1974 ($143 million)

to 1979 ($1.41 billion).”18

18 Krupnick, Alan and Wang, Zhongmin. A Retrospective Review of Shale Gas Development in the United States. Resources for the Future. April

16

US government research programs and funding of energy

R&D programs provided the spark necessary, but it was not

the only finger of the government’s hand that drove the

development of shale gas. Much of the competitiveness seen

in the shale gas market is largely impacted by government

intervention. “Perhaps the most important government

considerations are the federal tax breaks given to renewable

energy projects.”19 The installation of tax credits for

producing unconventional fuels, stems from the passage of

the Crude Oil Windfall Profit Tax Act in 1980:

This credit, which was implemented under Section 29 of the Internal Revenue

Code, applied not only to unconventional gas from Devonian shale, coal seams,

and tight gas, but also to biomass, geopressured brines, oil from shale or tar

sands, synthetic fuels from coal, and some other fuels. Unconventional gas wells

spudded between January 1, 1980, and December 31, 1992, were eligible for the

tax credits, and production from eligible wells continued to receive credit until

December 31, 2002. The size of the tax credits for Devonian shale (and coalbed

methane) was determined by a formula. Initially $0.52/Mcf, it was increased to

$0.94/Mcf in 1992 (Hass and Goulding 1992). During much of this period, the

national average wellhead natural price was between $1.5/Mcf and $2.5/Mcf.

The formula accounted for inflation and contained a factor that would gradually

phase out the effect of the tax credit when the price of oil was high, reflecting the

consideration that the credits were to take effect when oil prices were so low as

2013. P. 719 Cohen, Andrew Knoller. The Shale Gas Paradox: Assessing the Impacts of the Shale Gas Revolution on Electricity Markets and Climate Change. Harvard College. May 2013. P 78

17

to limit the competitiveness of unconventional fuels (Soot 1991). The tax credit

for tight gas was fixed at $0.52/Mcf in the early 1980s, which was smaller than

that for Devonian shale or coalbed methane. Tight gas began to “lose credit

eligibility with partial price decontrol in 1985,” but regained it in 1991 (Hass and

Goulding 1992).20

These tax credits that started in 1980, have continued

into the 21st century, and have had a major impact on the

shape of the shale gas industry as it is seen today.

Finally, as mentioned briefly above, the impact of the US

government sponsored R&D programs and tax credits, lit the

fire that was the ‘shale gas revolution.’ The US Department

of Energy played a major role in developing important energy

technological innovations over the past few decades. Several

of these technologies were an essential part of the ‘shale

gas revolution:’

Three technologies thought to be critical to shale gas development are among

the most important technological innovations identified by NRC: horizontal

drilling, 3-D seismic imaging, and fracturing technology. NRC (2001) concluded

that DOE’s role in improving horizontal drilling and 3-D seismic imaging was

“absent or minimal,” but rated DOE’s role in “fracture technology for tight gas” as

“influential.” Fracture technology for shale gas, which was greatly influenced by

fracture technology for tight gas, was not considered by NRC, probably because

the shale gas boom had not yet arrived at the time of the NRC report.

Microseismic frac mapping, another technology thought to be critical to shale 20 Krupnick, Alan and Wang, Zhongmin. A Retrospective Review of Shale Gas Development in the United States. Resources for the Future. April 2013. P. 8-9

18

gas development, also was not yet fully developed or used at the time of the NRC

report. NETL (2007) and other trade publications suggest that DOE played a

critical role in developing the technology of microseismic frac mapping.21

The above historical outline provides us with an

overview of the involvement of the US government and

Department of Energy in sparking essential technological

advancement, and igniting the ‘shale gas revolution’ that we

see today. The following part of this section shows the

outline of the US federal and state system at work in regard

to shale gas competences. Standard to its true form, the US

government, after initially sparking the ‘revolution,’ has

hence given a majority of the competences to the state level

in major decisions regarding the direction, legislation, and

regulation in which each state chooses to follow.

“The U.S. success with shale gas is a result of the

combination of indulgent federal enforcement, diversified

state laws, and the beneficial nature of Cheney’s 2005

Energy Policy Act, which attracted developers into the

industry. The transparent regulatory regime featuring

specific boundaries in federal and state regulations helped

investors realize the risks and encouraged them to

vigorously invest in new shale basins, which in turn

assisted smaller energy firms refine their technology in

hydraulic fracking. Consequentially, the shale industries 21 Krupnick, Alan and Wang, Zhongmin. A Retrospective Review of Shale Gas Development in the United States. Resources for the Future. April 2013. P. 10

19

saw a great number of mergers of smaller firms with larger

conglomerates, which created further investments,

infrastructures, and technological know-how.”22 Since its

commercialization at the end of the 20th century, shale gas

extraction procedures have mostly been left in the hands of

private firms and industries, mainly supported by private

investors, and the domain of legislation and regulation in

the hands of individual states. As hydraulic fracking became

more refined, larger companies began to take the main stage

in exploring the potential of US shale plays. Rapidly, the

regulatory shale gas arena is changing and taking shape, and

“several states have been adopting more stringent disclosure

regulations on the chemicals used to exploit the natural

gas, although this exercise is not near completion.”23 In

summation, the energy transition since the 1970s till today,

is characterized most accurately by the shift from US

government involvement to a more independent state-by-state

directive, in which there are many differences in the

approaches each state takes toward its own shale gas plan

and regulations.

As a whole, the transparent US regulatory framework

22 Paolo Davide Farah, Riccardo Tremolada, “A Comparison between Shale Gas in China and Unconventional Fuel Development in the United States: Health, Water and Environmental Risks”, gLAWcal Working Paper Series, IUSE Turin Working Paper Series, Paper presented at the Colloquium on

Environmental Scholarship, Vermont Law School, USA, 11th

October 2013. Available in ssrn.com23 Boersma, T., and Johnson, C. (2012). The Shale Gas Revolution: US andEU Policy and Research Agendas. Review of Policy Research 29(4): 570-576.

20

concerning the rapid development of shale gas, at both a

federal and national level, has been strongly successful,

although the model scheme remains under skepticism in light

of the current environmental controversy and debate (those

issues which will be discussed later in the paper), mainly

brought about by intense media attention and criticism. To

bring this section on US governance regarding the ‘shale gas

revolution’ to a smooth close, dismissing the detailed

legislation imposed by the federal government as well as

each specific state, due to the guidelines of this paper, a

brief excerpt from a paper prepared in the framework of the

Research Project “Evaluating Policies For Sustainable Energy

Investments: Towards an Integrated Approach on National and

International Stage” EPSEI – EU Commission funded research

project at University of Turin, Department of Law, will

serve as our summary:

The U.S. successful shale gas development is due, inter alia, to a conducive

regulatory environment enrooted in a cooperative federalism framework. In fact,

the entire process is regulated by a mixture of states and federal agencies. The

formers are responsible for drilling, while the latters have ultimate authority over

water treatment and disposal. However, federal government has delegated much

of its power to states whose regulations meet or exceed federal minimum

standards. Consequentially, while at the federal level, the U.S. has long-

established environmental guidelines regulating oil and gas industries, at the

state level, regulations concerning the shale industry differ depending on the

21

political inclinations toward the extraction industry. The State of New York, for

example, requires a comprehensive review of the environmental impacts, an

application for drilling, and a drilling work plan. In Texas, conversely, drilling

permits are usually lax provided that environmental review is required for a

proposed project. State regulations, nevertheless, can easily be ignored or

enforced depending on the national political guidance. For instance, during the

2000s, shale gas was strongly backed by the “Energy Task Force” directed by,

then, Vice-President Dick Cheney. In this context, the Energy Policy Act of 2005

was passed, which contained a questionable escape clause that exempted the

shale gas industry from the guarantees outlined in the Safe Drinking Water Act

and the Clean Air Act. Moreover, under pressure from big oil companies, the U.S.

Congress exempted oil and gas production from numerous health and safety

laws. Hence, states have primary responsibility for establishing and enforcing

safeguards for shale gas production. This regulatory framework is subject to

strong controversy as some argue that drilling is a basically unregulated activity.

In particular, shale gas can pose significant environmental cross-border issues

that cannot be tackled with inconsistent and potentially conflicting legislation at

the state level. It is thus likely that the next decade will see much argument about

whether federal agencies should have more authority.24

24 Paolo Davide Farah, Riccardo Tremolada, “A Comparison between Shale Gas in China and Unconventional Fuel Development in the United States: Health, Water and Environmental Risks”, gLAWcal Working Paper Series, IUSE Turin Working Paper Series, Paper presented at the Colloquium on

Environmental Scholarship, Vermont Law School, USA, 11th

October 2013.

22

A Shale Gas Mixture: Shale’s Economic Implications and

Environmental Issues Leading the Public Debate and Current

Conflicts (Pros and Cons For the Future)

One of the most important aspects regarding the ‘shale

gas revolution’ in the US, and globally, is the economic

impacts that the current shift is causing, and the ripples

caused moving into the future. As seen thus far, the

economic impacts for the US energy market have been quite

substantial, and the projected benefits on the US economy

are noteworthy. Although some of the effects are being seen

in the global energy market up to this point, much is yet to

be unraveled in the wake of the shale gas boom. Alongside

the economic shifts occurring today, are the environmental

issues that are currently on the rise. There has been much

research into the negative side effects, caused mainly by

hydraulic fracturing, that shale gas extraction is having on

people, communities, and the nation as a whole. Against

these arguments, many of the shale gas companies have issued

reports clearing the safety and ‘environmentally-friendly’

aspects of their procedures. Ignited by these negative

environmental findings, much public debate and scrutiny has

overshadowed shale gas production in recent years. The

‘shale gas revolution,’ although in motion for decades now,

Available in ssrn.com

23

is still in its infancy and there is much uncertainty

regarding definitive costs and benefits, economically,

politically, and environmentally, currently, and striding

into the future.

To start, the impacts of the increased use of shale gas

in the US energy market have been widely beneficial, as well

as on imports and exports abroad. Widespread support has

been seen for US LNG exports, which would consequently lead

to a wide range of economic benefits. To date, one of the

more apparent benefits other than domestic gas consumption

supplements from shale, and projection for US LNG

exportation capacities, include a spike in coal exports to

Europe from the US, which rose to 67% in 2012 (See

Additional Figures). Modifying the economic production of

gas and oil, the US is becoming less dependent on these

imports, and in decreasing overall energy costs, have

strengthened domestic industrial and manufacturing sectors.

Over recent years, domestic:

support for US LNG exports is widespread. The most recent Department of

Energy (DOE) commissioned report investigating natural gas export potential

found that the US would gain net economic benefits from allowing LNG exports.

Consistent with economic theory, this outcome is maximized when barriers to

trade are removed. The economic benefits include the following: GDP would

increase (potentially $118.2 billion in growth). Jobs would be created across the

LNG supply chain from natural gas production to liquefaction (870,000 by 2015).

24

Current account deficits would reverse. Domestic gas prices would be stabilized

through the creation of a world market, which should in turn stabilize supply.25

Quite recently, the Obama administration has approved four

export projects that will allow for the export of LNG

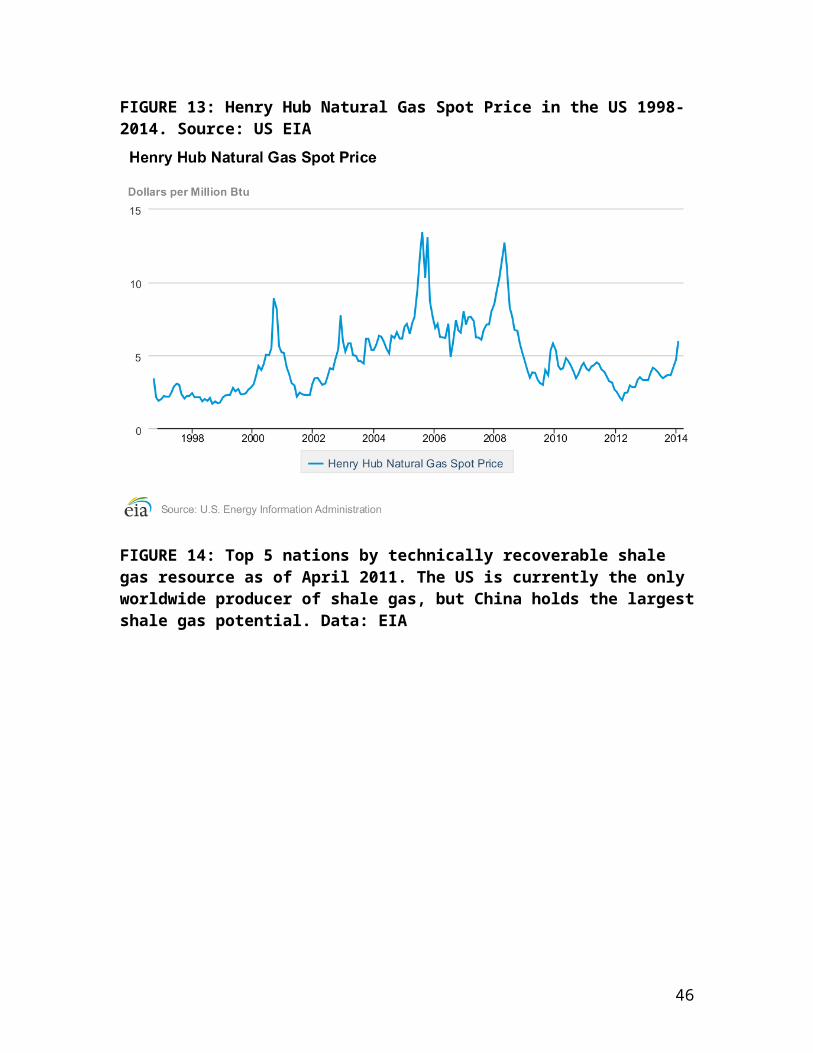

supplies. In addition, the Henry Hub price, the pricing

point of natural gas, is currently a third of what it was in

2008, and US natural gas prices are currently close to their

1976 levels, a historic low in the US (See Figure 13). “A

study of the long-term domestic implications of shale gas

production indicates that by 2035 the average American

household will have $2,000 more disposable income per year

solely as a result of reduced gas costs for themselves and

the companies from which they purchase products.”26 Imports

of the total amount of natural gas consumed in the US in

2007 were approximately 16.5% and dropped drastically to 11%

in 2010. Also noteworthy is the fact that US imports of

crude oil have decreased from 60% in 2005 down to 39% in

2010, as a result of growing shale gas production. Here, the

obvious, and not so obvious, economic benefits are shown as

to the effects the ‘shale gas revolution’ is having, and

will have on the US economy.

25 Cohen, Andrew Knoller. The Shale Gas Paradox: Assessing the Impacts of the Shale Gas Revolution on Electricity Markets and Climate Change. Harvard College. May 2013. P 3126 Hastings, David Dunn and McClelland, Mark J.L. Shale gas and the revival of American power: debunking decline? International Affairs © 2013 The Royal Institute of International Affairs. Published by John Wiley & Sons Ltd. International Affairs 89: 6 (2013) 1411–1428

25

Already, transformations to the global energy market

are apparent, mainly in the shape of relations, but more

evident impacts of shale shifting the global energy

equilibrium, will be visible, if and when, the US begins

exporting LNG around 2016. Relations between the US and

Australia, one of the US’s closest allies, has great

potential to lower liquefaction and transportation costs,

allowing the US involvement in the Asia Pacific Region. In

effect, this would spread the tentacles of influence that

the US currently lacks in the global energy market,

simultaneously enhancing the US’s energy security, would

entrench American power, and would strip away some of the

powers that the Middle East and Russia have in the gas

sector. If the US were to become self-sufficient, its

interests and strategy would shift away from energy rich and

volatile parts of the world, and would become less

vulnerable toward developments and progressions outside its

borders. For example, Putin’s regime is dependent on the

high prices of gas and oil, any shift in the global energy

market prices and supply will surely influence foreign

policies in Russia. In turn, the EU could potentially move

away from its dependence on Russian gas and oil, more in

favor of their own alternative energy sources or increased

trade with the US, if shale gas production continues to put

downward pressure on the global price of natural gas and

oil. Germany also has the potential to extract and produce

26

shale gas from its basins. Due to its geography and densely

populated country, it remains difficult for them to make

shale gas and oil production a top priority, and possibly

allow them to become energy self-dependent. It goes without

saying that these ‘shifts in power’ could have major

consequences, both politically, economically, and stands to

reduce carbon and greenhouse gas emissions moving into the

future:

The US would also gain geostrategic opportunities to reposition itself in the Asia-

Pacific, and away (albeit slowly) from the Middle East, helping key allies.

Environmentally, LNG supporters argue that exporting natural gas would reduce

GHGs by displacing coal, the fuel of choice in many potential export markets

such as China, the world’s largest GHG emitter.27

In combination, economically and politically, the US

may eventually play an even more important role than it does

today, when it comes to setting standards for energy

supplies and prices globally. Taking hold of more control in

the global energy market, particularly in oil prices and

supply, the US can remove itself from the instability and

volatility of the energy market and become energy self

sufficient. Domestically, the benefits of producing shale

gas and lowering the costs of natural gas use, decreasing

net imports of natural gas, and future projections of

becoming a net exporter in the global energy market, are 27 Cohen, Andrew Knoller. The Shale Gas Paradox: Assessing the Impacts of the Shale Gas Revolution on Electricity Markets and Climate Change. Harvard College. May 2013. P 31

27

substantial for the US economy and overall quality of life

of the average American citizen. In a global perspective,

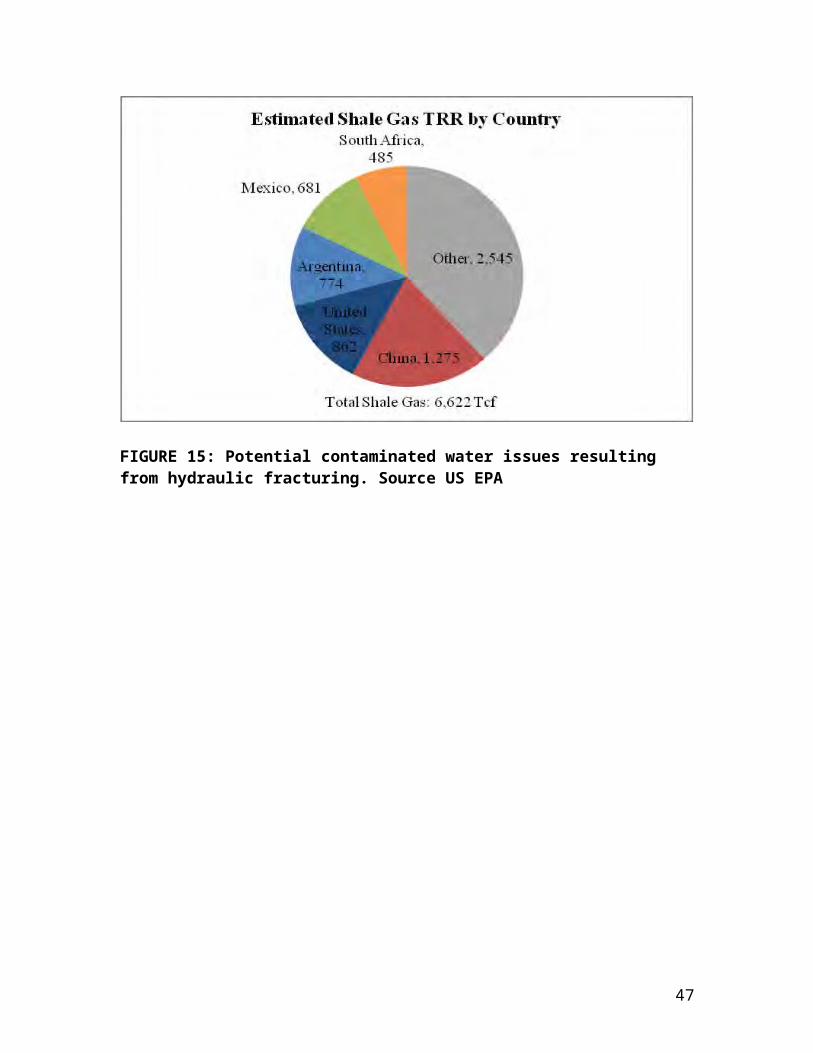

the US, although as of April 2011 was the only worldwide

producer of shale gas (In 2014 the US and Canada are the

only two countries that produce shale gas commercially), is

not the only country in the world with shale gas basins at

their disposal. China currently holds the biggest shale gas

potential, and if China can manage to successfully innovate

their technologies and practices enabling them to reap the

benefits of their shale gas deposits, that would greatly

affect the global landscape in the energy sector (See Figure

14). There remains much to be told in the upcoming years as

to how the still-infant global shale gas sector will impact

the global economic and political shape.

A decisive advantage has given the US the capacity to

exploit the benefits of shale gas and oil, and that is

population density. Due to the fact that the US has an

estimated 31 people per square kilometer, has been another

factor allowing the shale gas evolution to turn into a shale

gas revolution. In comparison, many countries in Europe have

stood steadfast in not using their technologies to extract

shale gas as a result of highly populated urban, and still

populated rural areas. As will be discussed next, shale gas

extraction has raised many health and environmental concerns

(as well as seismic earthquake speculation), and the US has

benefited from having less populated areas to establish

28

drilling plays, such as the Barnett, Haynesville,

Fayetteville, and Marcellus shale basins. Seemingly, this

essential fact of population density is easily overlooked as

a decisive factor for shale fracking, but when viewed

against the EU, it becomes more evident as to why the US (as

well as Canada) have been successful in becoming the only

two countries on the globe to produce a commercial amount of

shale gas today. Subsequently, the common theme of

uncertainty shadows over this fact as well, will countries

like China and Russia take advantage of their substantial

rural areas in which shale gas basins lie, and what effects

will these power-house countries have on the global shale

gas stage?

Many economists have viewed these projections, as

having mainly positive effects, albeit negative speculations

have arose as well. The extraction and production of shale

gas and oil, coupled with technological advances throughout

the world, stand to reshape the world economy. Amplifying

this fact is a globalizing(-ed) and interconnected world,

where commercial production and exportation of such

resources will alter the landscape of the world energy

market from how we know it today. Currently, only two

countries are producing shale oil and shale gas in

commercial quantities, the United States and Canada. The US

will ultimately become the world’s first net exporter of

shale gas, as projected by 2016, and after that, no one know

29

for certain what will happen in future years or decades, as

other countries decide to follow suit.

A major determining factor for shale gas’ future lies

in the hands of the health and environmental impacts shale

extraction activities have. More and more frequently,

speculation and skepticism regarding the detrimental

environmental effects that shale gas is having on the

environment has become commonplace. Despite the fact that,

in the US, the birth of shale gas has already begun to

decrease CO2 emissions and greenhouse gas emissions by

switching from coal-to-gas, major concerns regarding water

contamination and lack of regulations are at the heart of

the environmental criticisms (there is sufficient US data to

provide a provisional estimate of domestic CO2 emissions

reductions attributable to the displacement of coal by gas

in electricity generation. The most up-to-date, but still

provisional, data for shale gas production have been derived

from submissions of EIA-23 forms presented in the U.S. Crude

Oil, Natural Gas, and Natural Gas Liquids Proved Reserves

report-EIA 2012). Additionally, there have been

controversial debates as to whether or not fracking is

responsible for causing numerous seismic earthquakes, in

that drilling transforms the shale rock formations, albeit

groundwater contamination, regulations, and firms’

disclosure policies remain at the forefront. These health

30

and environmental issues in the spotlight of public debate,

to name a few, retain the potential to slow down and reshape

the production and growth capacity of the shale gas

industry.

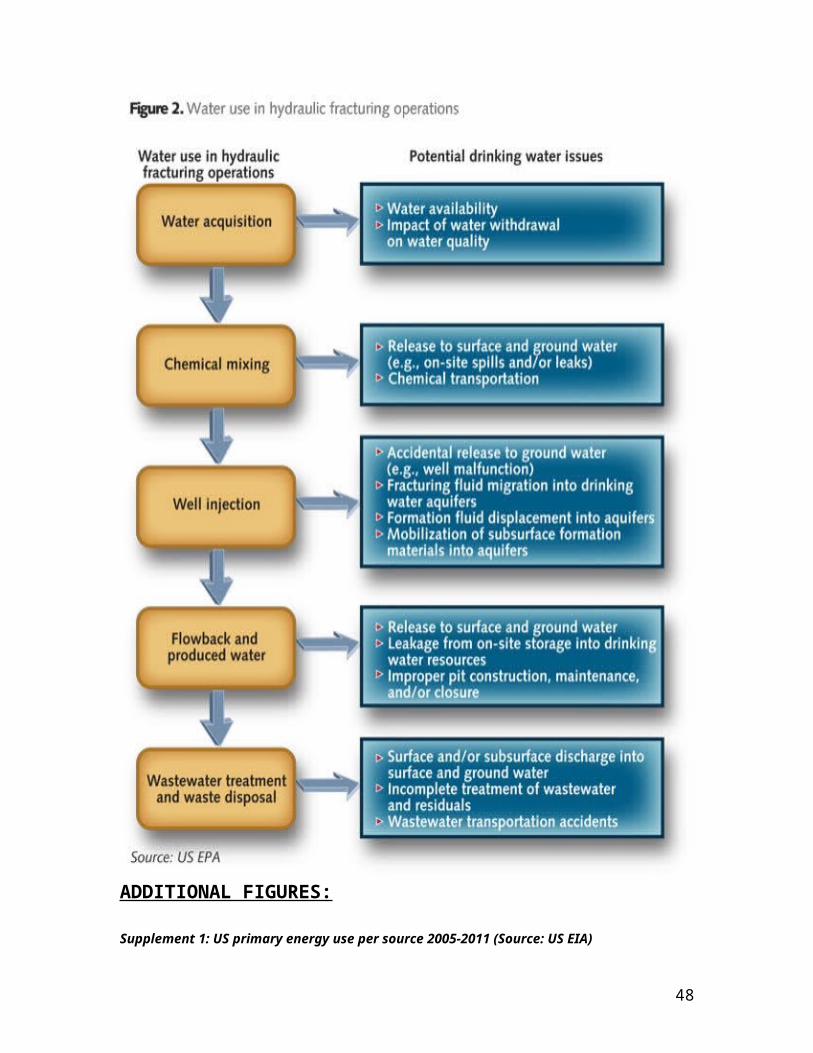

Shale gas, which is mainly composed of methane gas, is

trapped and compressed deep in shale rock formations

underground. Hydraulic Fracturing for shale gas is the

process by which fractures are created in these rock

formations, in turn releasing the gas. This process of

fracking accounts for about 2-4 million gallons of water per

well, water that is injected at a high pressure in order to

permeate the fractures and keep them open so the gas can

flow efficiently. Additionally, a ‘toxic’ chemical recipe,

composed of a mix of sand and ‘fracking fluids,’ is used

during the drilling process and results in large amounts of

wastewater. This wastewater is “highly contaminated with

chemicals such as benzene, methanol and xylene,” and this

backwater is argued to be entering the drinking water of the

surrounding areas, causing serious health and environmental

damage (an estimated 750 chemicals, 29 which are likely or

known carcinogens).28 “In addition, the Eastern States of

the United States treat an increasing volume (up to 60%) of

the water by applying recycling technologies.”29 Although

the US has made attempts in recycle this wastewater, it is

28 Reins, Leonie. The Shale Gas Extraction Process and Its Impacts on Water Resources. Blackwell Publishing Ltd., 2012. P. 300-30129 Reins, Leonie. P. 301

31

argued still, that much of the ‘highly contaminated’ water

is leaking out into the surrounding environment effecting

nearby people and their towns, and that it is unethical that

many firms do not need to disclose which toxic substances

are used in their chemical recipe.

As noted in the earlier section, the US has no federal

regime or federal law that regulates the extraction of shale

gas (unconventional gas), and much of the shale gas

regulation resides at the State level. In January 2013, US

President Barack Obama directly backed shale gas drilling,

as an opportunity for energy self-sufficiency and a means to

create thousands of jobs in a hindered economy. In this

context, much of the environmental debate pins the States as

not having the power and ability to adopt and implement the

appropriate regulations tailored for climate, geology, and

more specifically, water resources. A main issue arises here

with several policies such as the Clean Water Act (CWA),

which is the primary federal law governing the pollution of

surface waters.30 Due to the fact that hydraulic fracturing

for shale gas produces contaminated wastewater, the CWA

stands to potentially affect the operations of shale gas

production and extraction. Unfortunately, up to this point,

it has been very difficult to establish the proof needed to

show that these fracking wells are the cause for

30 Environmental Protection Agency (EPA), ‘Summary of the Clean Water Act’ (EPA, 11 August 2011), found at <http://www.epa.gov/ regulations/laws/cwa.html>.

32

contamination in groundwater, and this is a direct result of

the fact that the chemical recipe used in hydraulic

fracturing is under ‘trade secret protection.’ By allowing

firms to use dangerous and harmful toxins in their water

mixture for drilling activities without disclosing what

these toxins are, allows for the parallel effect of these

dangerous and harmful toxins entering the environment, and

harming it, especially in the long run.

“Another concern is that the US government may not

adequately enforce existing environmental regulations…Due to

exceptions in federal law, shale gas development activities

are being conducted without complete oversight by several

major federal environmental laws that offer safeguards to

protect people and the environment.”31 One of these

‘exceptions’ mentioned here is “is set forth in the Energy

Policy Act of 2005 whereby underground injections from

hydraulic fracturing are not regulated by US Safe Drinking

Water Act (US Code, 2012a).”32 Ultimately, these ‘exceptions

to the rule’ have major negative implications for overall

health and environmental damages continuing to be caused by

shale gas production in the US. Furthermore, an executive

order by President Obama “disclosed a lack of recognizable

expertise in assessing environmental impacts on human

31 Centner, Terence J. Oversight of shale gas production in the United Staes and the disclosure of toxic substances. Elsevier Ltd., 2013. P.233and 23832 Centner, Terence J. P.235

33

health.”33 As a result, States have been thrust into the

role of assessing and preventing the risks accompanying

shale gas production, but their efforts have been weak in

response, and only recently have a few States pushed for

more stringent disclosure regulations. The large problem

here is that firms do not disclose public information

regarding the toxic chemicals used in drilling, and States

are not responding appropriately to inform communities of

possible hazards, and communities have a “Right-to-Know.”

Many arguments in public debate, coupled with a growing

amount of protests, have clouded over the wastewater issues

and its health and environmental impacts such as

contaminating the drinking water of those communities near

the wells, along with firms’ incomplete treatment of the

highly contaminated water, and the numerous hazardous

accidents that have occurred (See Figure 15). All of this

public scrutiny is validated in the way that the ‘fracking

fluids’ used by shale gas firms are shrouded in secrecy.

Although the empirical evidence for the health and

environmental damages caused by shale gas production remain

thin, many States are beginning to take a more imposing

position against firms disclosing their chemical recipe used

for fracking. More importantly, public debate and negative

media speculation, have put shale gas in the spotlight and

have forced the US government to take a more active role in

33 Centner, Terence J. P.233

34

assessing the environmental impacts caused by the ‘shale gas

revolution,’ now and moving into the future.

Environmentally, the evidence regarding the health and

environmental risks are still in the earliest stages, and as

more legitimate results surface, new policy and research

agendas will take a more formidable shape, and clear the

uncertainty surrounding the evolution of shale gas and oil

extraction and production.

Final Thoughts on the ‘Shale Gas Revolution’

This paper has followed the journey of the US ‘shale

gas revolution,’ from its roots in the oil shocks of the

1970s, to the spectrum of the federal and state level

governance and involvement in shaping past and present

regulations, policies and legislation within the shale gas

industry. Views of the economic impacts, both for the US and

globally, have been discussed at length, noting that the

story of shale gas is still in its early stages. The

economic impacts that are taking shape today, began in the

Nixon era, evolved into the onset of the US shale gas boom

in the 21st century, and have many speculating about the

future projections and expectations. Finally, arguments in

the form of health and environmental issues, have permeated

public debate today, and in turn are influencing and

reshaping the course of the ‘shale gas revolution,’ and

evolution. The key factor shaping shale gas and oil today is

35

uncertainty. There remains much uncertainty regarding shale

gas’ impact economically, (geo)politically, socially, and

environmentally.

1) Continued high prices of natural gas, commercialization

of fracturing viability, and most importantly, the

emergence of the necessary R&D development, US federal

involvement, and technological advancements all

converged at the right moment to spark the shale gas

boom in the US in the 21st century.

2) Arguably, the US federal regulatory framework has been

largely successful in that it has allowed for such

propositions as federal tax breaks in the renewable

energy sector, the 2005 Energy Policy Act, and federal

exceptions in the shale gas industry, all of which

contributed to the successes of shale gas production.

Conversely, more environmental risks have started to

surface as a result of the shale gas boom. Notably, the

US’s lax regulatory approach has mostly left decisive

regulation and policy decisions in a framework of an ad

hoc state-by-state basis. States have made efforts in

oversight of the shale gas industry, within their own

state, but have been ineffectual, and have not fully

considered externalities outside their own state.

3) Health and environmental impacts are coming to light,

and States’ efforts have been perceived as being

insufficient in controlling the health and

36

environmental damages produced by hydraulic fracturing,

albeit slow progressions are being made, mainly in

forcing firms to disclose the chemicals used in their

‘fracking fluid.’ This inefficiency is spilling over to

the federal government, and the public’s demand for the

US government to step in to impose and uphold more

stringent environmental laws. On the plus side, the

coal-to shale switch has shown signs of reductions in

greenhouse gas emissions.

4) Most importantly, we have discussed the economic

impacts in the US and globally, today as well as

economic expectations leading into the future, as a

result of the booming US shale gas industry. Decreasing

prices of natural gas, shale gas now accounting for

about 20-30% of the natural gas in US consumption, have

led many to believe that the US will become an exporter

of natural gas by 2016. Within the US, the economy

stands to benefit greatly from lower natural gas

prices, more affordable energy, and less dependence of

natural gas imports from volatile energy markets. Also,

benefits include an increase in GDP, more jobs, and a

reversal of the current account deficit as a result of

being a net exporter. Globally, changes in the US

energy market will ultimately transform the world

energy market, specifically, heightened competition

with China in the energy market. These changes will

37

also reshape the US’s geopolitical standing and power

as well as the geopolitical equilibrium in the world

economy. At this current junction, the ‘shale gas

revolution’ is in its infancy, and the shale gas story

will unravel in more detail in the upcoming years,

resulting in many questions being answered, hopefully.

APPENDIX: THE SHALE GAS REVOLUTION

FIGURE 1: The effect of the 1973 Oil Shocks on the US economy, both oil prices and strength of the dollar. Source:http://withfriendship.com/user/athiv/1973-oil-crisis.php

38

FIGURE 2: US federal spending trends in R&D (excluding defense spending). Source: AAAS

FIGURE 3: Massive increase in the number of horizontal wellsin Fort Worth (Indicative of increasing horizontal drilling in the whole of the US). Source: Railroad Commission of Texas

39

FIGURE 4: Increase in number of producing Barnett shale wells in Fort Worth showing main impact of horizontal drilling and simo-fracturing. Source: Railroad Commission ofTexas

40

FIGURE 5: Increases in US shale gas production from 2000-2010. Source: US EIA

FIGURE 6: Shares of natural gas resources and production in China, Canada and the US for 2010 and projections for 2040. Source: EIA, International Energy Outlook 2013

41

FIGURE 7: U.S. Annual Natural Gas Production, by Source (1990–2010). Source: US EIA

FIGURE 8: Annual US shale gas production has increased sharply over the last decade, and currently is ~7.85 Tcf/yr, or 34% of the nation’s gas supply. Source: EIA

42

FIGURE 9: US natural gas production is on an aggressive growth path, thanks to the shale gas revolution. Source: EIA (Shale gas provides the largest source of growth in US natural gas supply)

43

FIGURE 10: World map depicting shale oil and gas basins and formations. Source: US EIA and USGS

FIGURE 11: Total US natural gas production, consumption, andnet imports from 1990 and projections for 2040 (A 12% increase in net exports of natural gas by 2040). Source: US EIA 2014

44

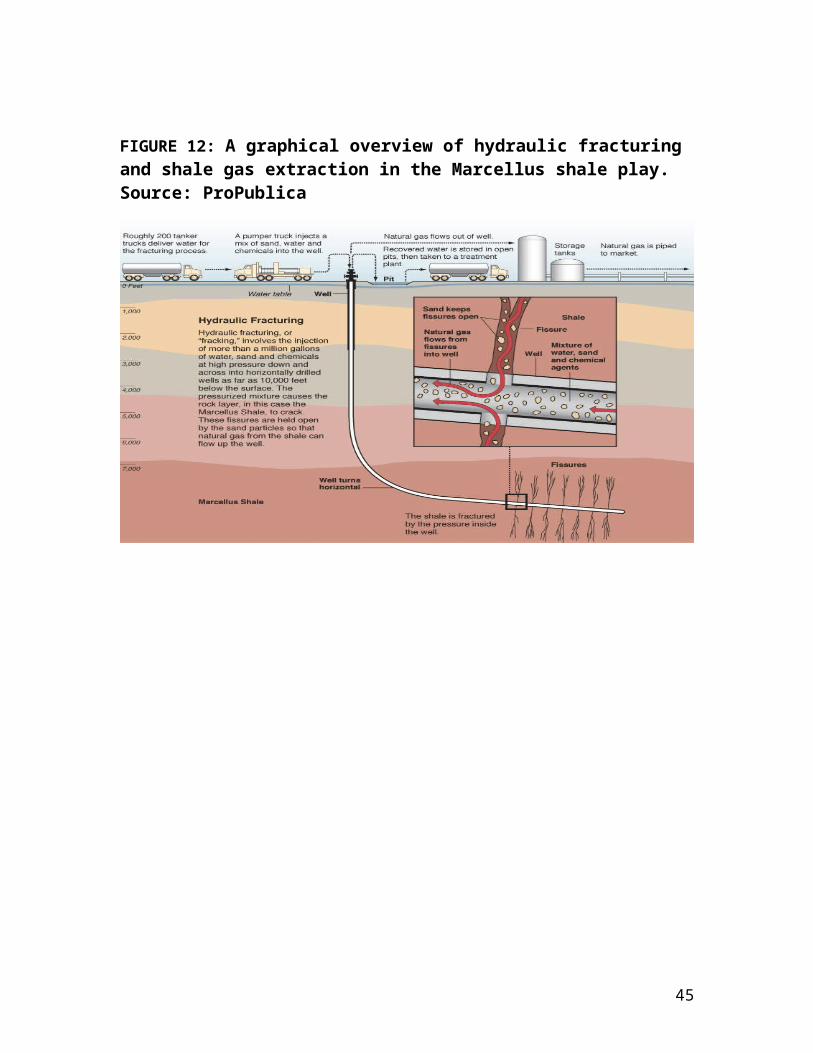

FIGURE 12: A graphical overview of hydraulic fracturing and shale gas extraction in the Marcellus shale play. Source: ProPublica

45

FIGURE 13: Henry Hub Natural Gas Spot Price in the US 1998-2014. Source: US EIA

FIGURE 14: Top 5 nations by technically recoverable shale gas resource as of April 2011. The US is currently the only worldwide producer of shale gas, but China holds the largestshale gas potential. Data: EIA

46

FIGURE 15: Potential contaminated water issues resulting from hydraulic fracturing. Source US EPA

47

ADDITIONAL FIGURES:

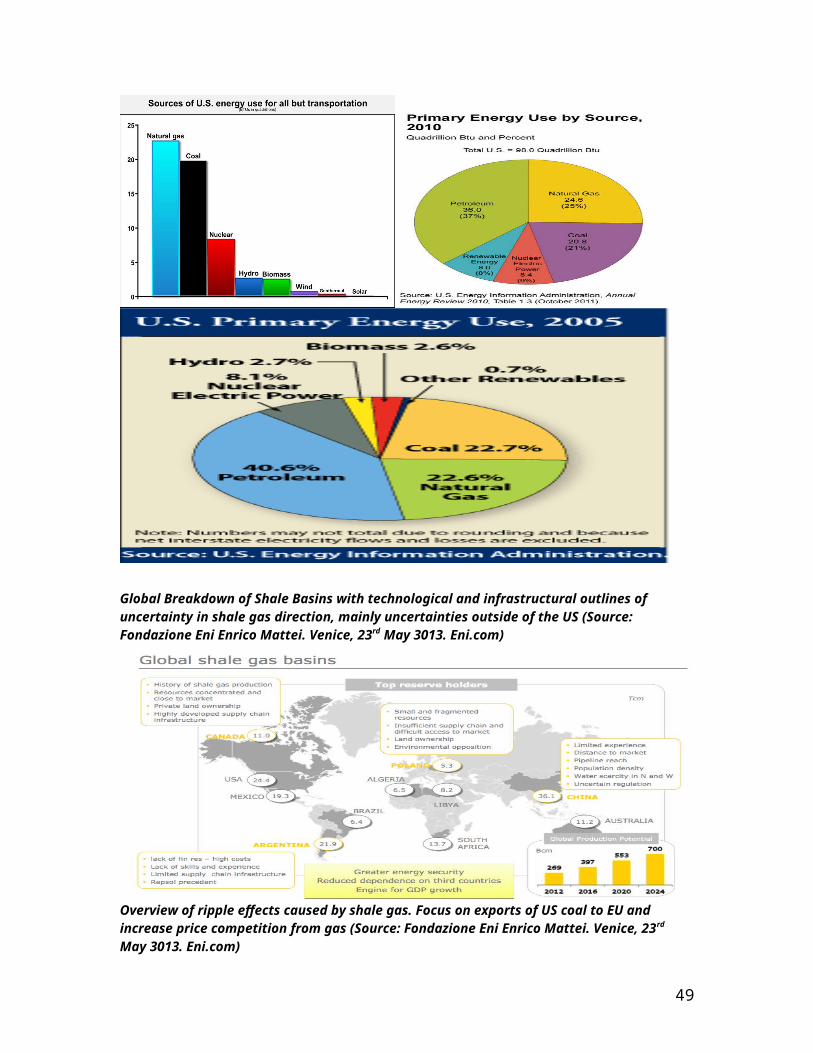

Supplement 1: US primary energy use per source 2005-2011 (Source: US EIA)

48

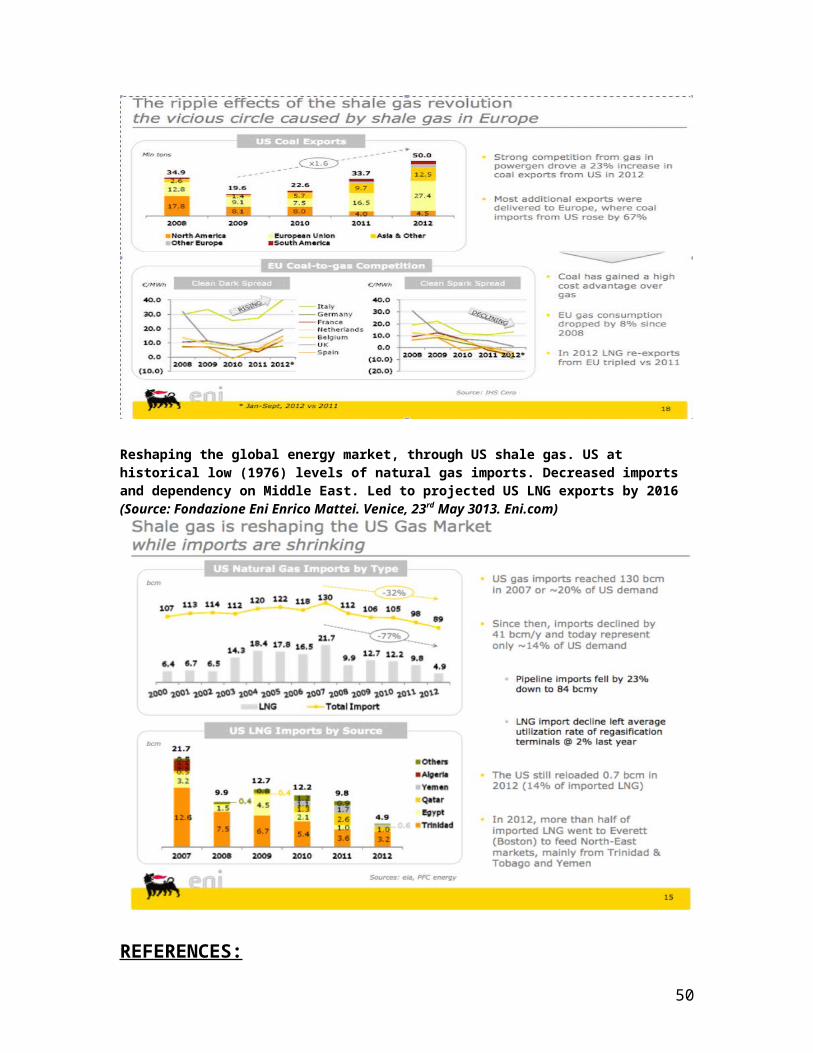

Global Breakdown of Shale Basins with technological and infrastructural outlines of uncertainty in shale gas direction, mainly uncertainties outside of the US (Source: Fondazione Eni Enrico Mattei. Venice, 23rd May 3013. Eni.com)

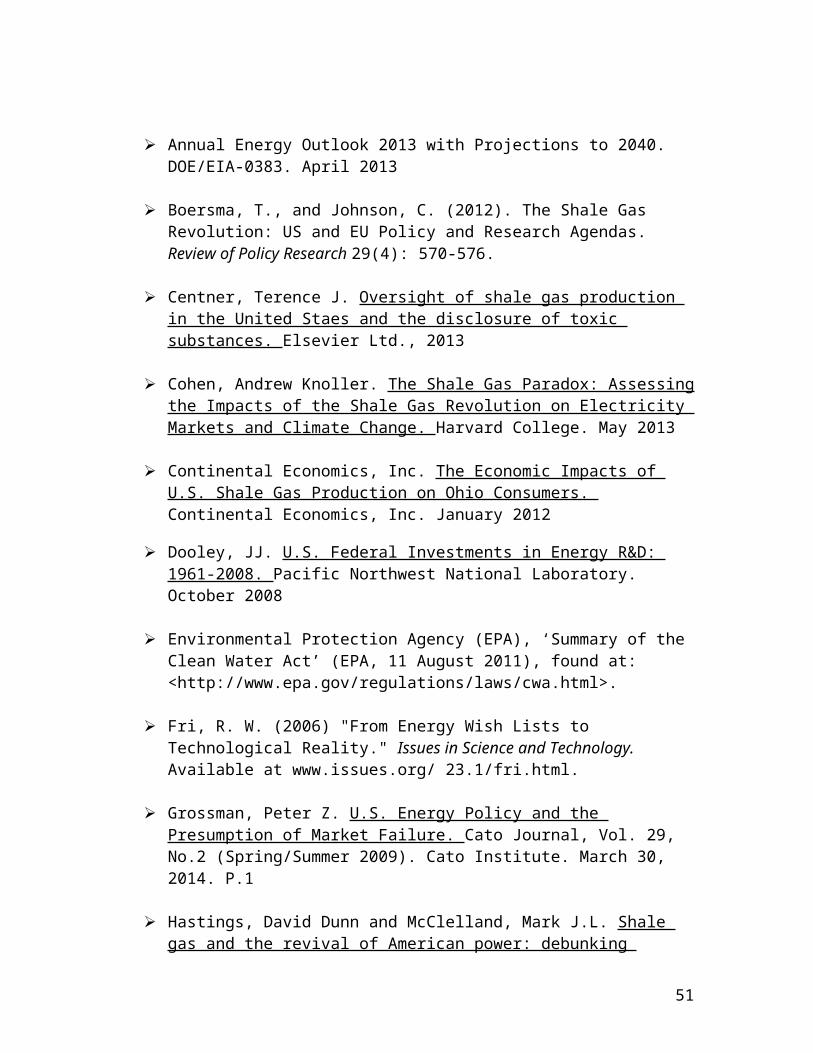

Overview of ripple effects caused by shale gas. Focus on exports of US coal to EU and increase price competition from gas (Source: Fondazione Eni Enrico Mattei. Venice, 23rd May 3013. Eni.com)

49

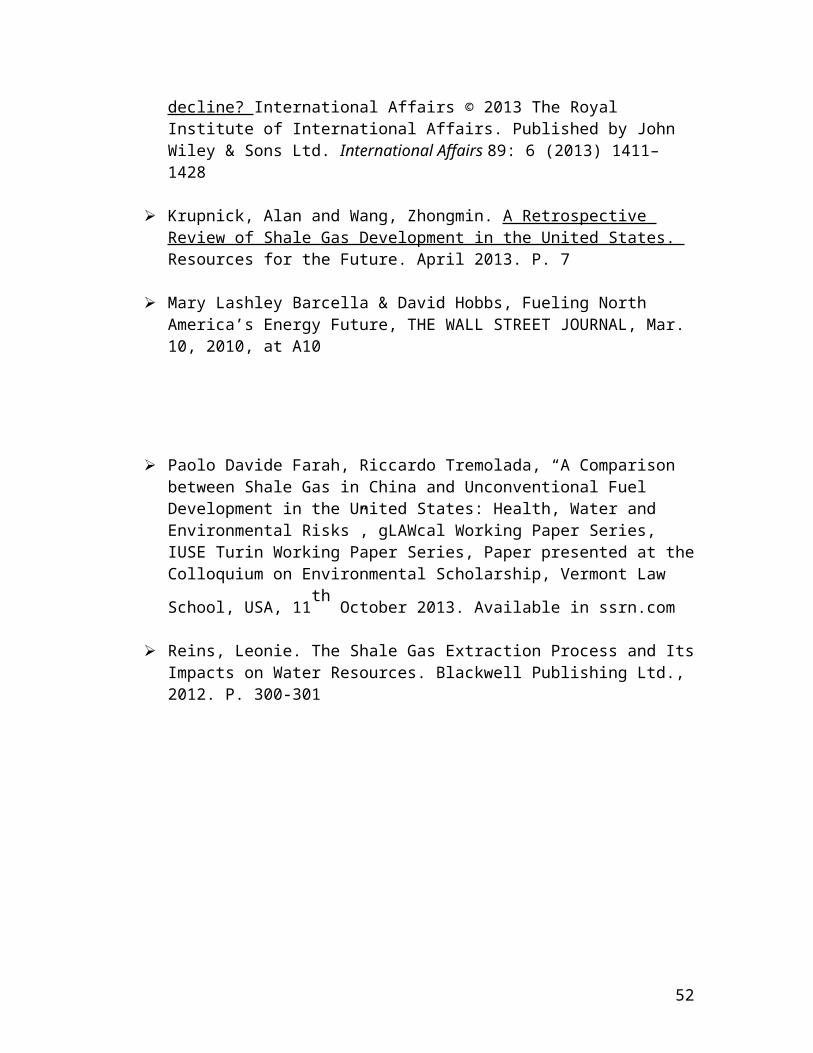

Reshaping the global energy market, through US shale gas. US at historical low (1976) levels of natural gas imports. Decreased imports and dependency on Middle East. Led to projected US LNG exports by 2016 (Source: Fondazione Eni Enrico Mattei. Venice, 23rd May 3013. Eni.com)

REFERENCES:

50

Annual Energy Outlook 2013 with Projections to 2040. DOE/EIA-0383. April 2013

Boersma, T., and Johnson, C. (2012). The Shale Gas Revolution: US and EU Policy and Research Agendas. Review of Policy Research 29(4): 570-576.

Centner, Terence J. Oversight of shale gas production in the United Staes and the disclosure of toxic substances. Elsevier Ltd., 2013

Cohen, Andrew Knoller. The Shale Gas Paradox: Assessingthe Impacts of the Shale Gas Revolution on Electricity Markets and Climate Change. Harvard College. May 2013

Continental Economics, Inc. The Economic Impacts of U.S. Shale Gas Production on Ohio Consumers. Continental Economics, Inc. January 2012

Dooley, JJ. U.S. Federal Investments in Energy R&D: 1961-2008. Pacific Northwest National Laboratory. October 2008

Environmental Protection Agency (EPA), ‘Summary of the Clean Water Act’ (EPA, 11 August 2011), found at: <http://www.epa.gov/regulations/laws/cwa.html>.

Fri, R. W. (2006) "From Energy Wish Lists to Technological Reality." Issues in Science and Technology. Available at www.issues.org/ 23.1/fri.html.

Grossman, Peter Z. U.S. Energy Policy and the Presumption of Market Failure. Cato Journal, Vol. 29, No.2 (Spring/Summer 2009). Cato Institute. March 30, 2014. P.1

Hastings, David Dunn and McClelland, Mark J.L. Shale gas and the revival of American power: debunking

51

decline? International Affairs © 2013 The Royal Institute of International Affairs. Published by John Wiley & Sons Ltd. International Affairs 89: 6 (2013) 1411–1428

Krupnick, Alan and Wang, Zhongmin. A Retrospective Review of Shale Gas Development in the United States. Resources for the Future. April 2013. P. 7

Mary Lashley Barcella & David Hobbs, Fueling North America’s Energy Future, THE WALL STREET JOURNAL, Mar. 10, 2010, at A10

Paolo Davide Farah, Riccardo Tremolada, “A Comparison between Shale Gas in China and Unconventional Fuel Development in the United States: Health, Water and Environmental Risks”, gLAWcal Working Paper Series, IUSE Turin Working Paper Series, Paper presented at theColloquium on Environmental Scholarship, Vermont Law

School, USA, 11th October 2013. Available in ssrn.com

Reins, Leonie. The Shale Gas Extraction Process and ItsImpacts on Water Resources. Blackwell Publishing Ltd., 2012. P. 300-301

52