translation exposure

TRANSCRIPT

Translation exposure• Translation exposure or “accounting

exposure” is the effect that unanticipated FX movements have on financial reports

• When a currency appreciates/depreciates, it affects the values of assets and liabilities

• Management of Translation Exposure• Translation Methods

Translation exposure• Suppose a U.S. firm has an asset (factory)

in Germany – Worth €1,000,000– How much is it worth in dollars? Depends on

the exchange rate.– Spot = $1.5/€ => worth $1,500,000– Spot = $1.1/€ => worth $1,100,000

• Value of the firm (equity) depends on value of assets and liabilities

Translation Methods• Current/Noncurrent Method• Monetary/Nonmonetary Method• Temporal Method• Current Rate Method

Current/Noncurrent Method• The underlying principal is that assets and

liabilities should be translated based on their maturity.– Current assets translated at the spot rate.– Noncurrent assets translated at the historical

rate in effect when the item was first recorded on the books.

• This method of foreign currency translation was generally accepted in the United States from the 1930s until 1975, at which time FASB 8 became effective.

Current/Noncurrent Method• Current assets

translated at the spot rate.e.g. €2 = $1

• Noncurrent assets translated at the historical rate in effect when the item was first recorded on the books. e.g. €3 = $1

Balance Sheet Local Currency

Current/ Noncurre

nt Cash € 2,100 $1,050 Inventory € 1,500 $750 Net fixed assets € 3,000 $1,000

Total Assets € 6,600 $2,800 Current liabilities € 1,200 $600

Long-Term debt € 1,800 $600 Common stock € 2,700 $900 Retained earnings € 900 $700CTA -------- --------

Total Liabilities and Equity

€ 6,600 $2,800

Ajax Manufacturing's German subsidiary has the following

balance sheet:Non-current assetsAccounts receivableInventory (at market)Cash, marketable securities

Total assets

€5,100,0002,700,0001,000,000

250,000---------------€9,050,000

EquityNon-current liabilitiesCurrent liabilities

Total equityAnd liabilities

€4,900,0003,400,000

750,000

---------------€9,050,000

a gain of$294,000

a gain of$192,000

a loss of$72,000

a loss of$12,000

0% 0% 0% 0%

Suppose the euro appreciates from $0.70 to $0.76 during the period?

Under the current/noncurrent method, what is Ajax's translation gain (loss)?

A. a gain of $294,000B. a gain of $192,000C. a loss of $72,000D. a loss of $12,000

Monetary/Nonmonetary Method

• The underlying principle is that monetary accounts have a similarity because their value represents a sum of money whose value changes as the exchange rate changes.

• All monetary balance sheet accounts (cash, marketable securities, accounts receivable, etc.) of a foreign subsidiary are translated at the current exchange rate.

• All other (nonmonetary) balance sheet accounts (owners’ equity, land, etc.) are translated at the historical exchange rate in effect when the account was first recorded.

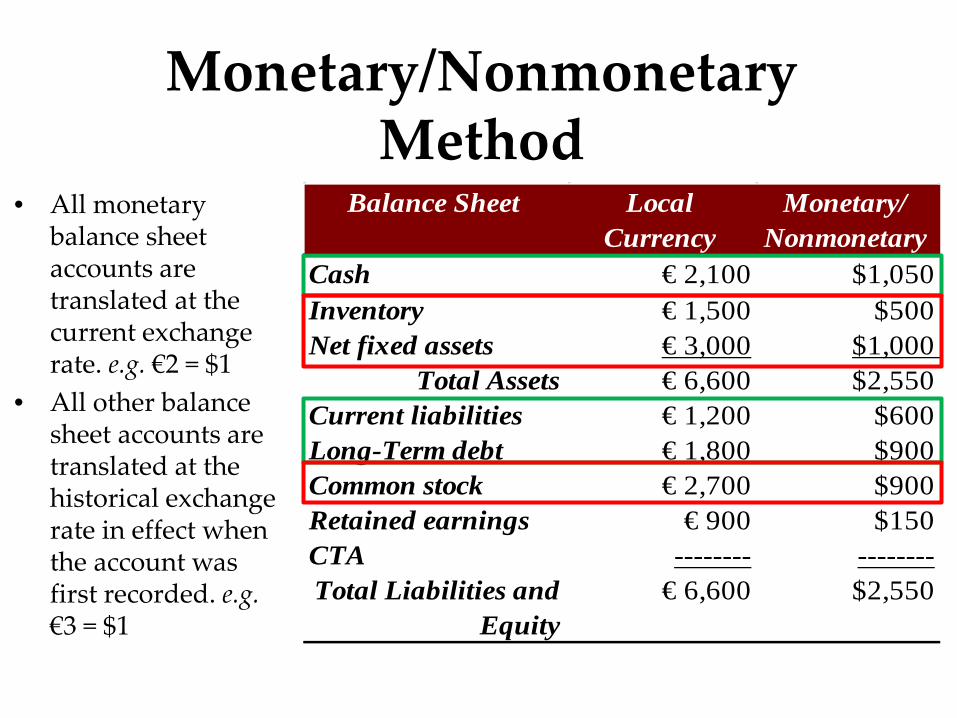

Monetary/Nonmonetary Method

• All monetary balance sheet accounts are translated at the current exchange rate. e.g. €2 = $1

• All other balance sheet accounts are translated at the historical exchange rate in effect when the account was first recorded. e.g. €3 = $1

Balance Sheet Local Currency

Monetary/ Nonmonetary

Cash € 2,100 $1,050 Inventory € 1,500 $500 Net fixed assets € 3,000 $1,000

Total Assets € 6,600 $2,550 Current liabilities € 1,200 $600 Long-Term debt € 1,800 $900 Common stock € 2,700 $900 Retained earnings € 900 $150CTA -------- --------Total Liabilities and

Equity€ 6,600 $2,550

a gain of$294,000

a gain of$192,000

a loss of$72,000

a loss of$12,000

0% 0% 0% 0%

Suppose the euro appreciates from $0.70 to $0.76 during the period?

Under the monetary/non-monetary method, what is Ajax's translation

gain (loss)?A. a gain of $294,000B. a gain of $192,000C. a loss of $72,000D. a loss of $12,000

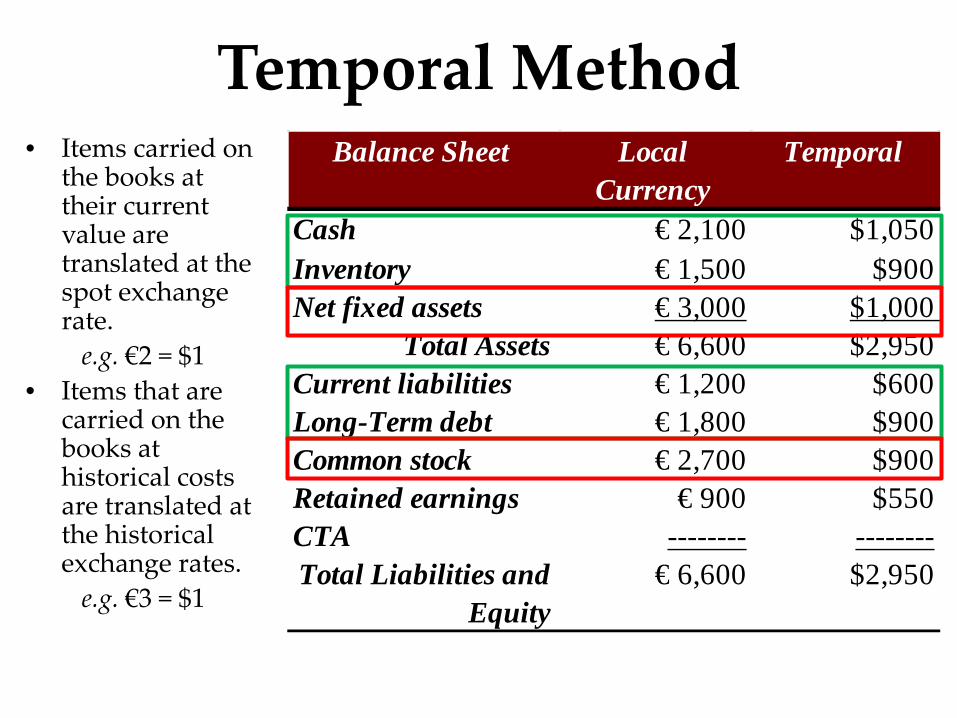

Temporal Method• The underlying principal is that assets and

liabilities should be translated based on how they are carried on the firm’s books.

• Balance sheet accounts are translated at the current spot exchange rate if they are carried on the books at their current value.

• Items that are carried on the books at historical costs are translated at the historical exchange rates in effect at the time the firm placed the item on the books.

Temporal Method• Items carried on

the books at their current value are translated at the spot exchange rate.

e.g. €2 = $1• Items that are

carried on the books at historical costs are translated at the historical exchange rates.

e.g. €3 = $1

Balance Sheet Local Currency

Temporal

Cash € 2,100 $1,050 Inventory € 1,500 $900Net fixed assets € 3,000 $1,000

Total Assets € 6,600 $2,950 Current liabilities € 1,200 $600 Long-Term debt € 1,800 $900 Common stock € 2,700 $900 Retained earnings € 900 $550CTA -------- --------Total Liabilities and

Equity€ 6,600 $2,950

a gain of$294,000

a gain of$192,000

a loss of$72,000

a loss of$12,000

0% 0% 0% 0%

Suppose the euro appreciates from $0.70 to $0.76 during the period?

Under the temporal method, what is Ajax's translation gain (loss)?

A. a gain of $294,000B. a gain of $192,000C. a loss of $72,000D. a loss of $12,000

Current Rate Method• All balance sheet items (except for

stockholder’s equity) are translated at the current exchange rate.

• Very simple method in application.• A “plug” equity account named

cumulative translation adjustment is used to balance the balance sheet.

Current Rate Method• All balance sheet

items (except for stockholder’s equity) are translated at the current exchange rate.

• A “plug” equity account named cumulative translation adjustment is used to balance the balance sheet.

Balance Sheet Local Currency

Current Rate

Cash €2,100.00 $1,050 Inventory €1,500.00 $750 Net fixed assets €3,000.00 $1,500

Total Assets €6,600.00 $3,300 Current liabilities €1,200.00 $600 Long-Term debt €1,800.00 $900 Common stock €2,700.00 $900 Retained earnings €900.00 $360 CTA -------- $540

Total Liabilities and Equity

€6,600.00 $3,300

a gain of$294,000

a gain of$192,000

a loss of$72,000

a loss of$12,000

0% 0% 0% 0%

Suppose the euro appreciates from $0.70 to $0.76 during the period?

Under the current rate method, what is Ajax's translation gain (loss)?

A. a gain of $294,000B. a gain of $192,000C. a loss of $72,000D. a loss of $12,000

Balance Sheet Local Currency

Current/ Noncurrent

Monetary/ Nonmonetary

Temporal Current Rate

Cash €2,100 $1,050 $1,050 $1,050 $1,050 Inventory €1,500 $750 $500 $900 $750 Net fixed assets €3,000 $1,000 $1,000 $1,000 $1,500

Total Assets €6,600 $2,800 $2,550 $2,950 $3,300 Current liabilities €1,200 $600 $600 $600 $600 Long-Term debt €1,800 $600 $900 $900 $900 Common stock €2,700 $900 $900 $900 $900 Retained earnings €900 $700 $150 $550 $360CTA -------- -------- -------- -------- $540

Total Liabilities and Equity

€6,600 $2,800 $2,550 $2,950 $3,300

How Various Translation Methods Deal with a Change from €3 = $1 to €2 = $1

Balance Sheet Local Currency

Current/ Noncurrent

Monetary/ Nonmonetary

Temporal Current Rate

Cash €2,100 $1,050 $1,050 $1,050 $1,050 Inventory €1,500 $750 $500 $900 $750 Net fixed assets €3,000 $1,000 $1,000 $1,000 $1,500

Total Assets €6,600 $2,800 $2,550 $2,950 $3,300 Current liabilities €1,200 $600 $600 $600 $600 Long-Term debt €1,800 $600 $900 $900 $900 Common stock €2,700 $900 $900 $900 $900 Retained earnings €900 $700 $150 $550 $360CTA -------- -------- -------- -------- $540

Total Liabilities and Equity

€6,600 $2,800 $2,550 $2,950 $3,300

Under the current rate method, a “plug” equity account named cumulative translation adjustment balances the balance sheet.

How Various Translation Methods Deal with a Change from €3 = $1 to €2 = $1

Income StatementLocal

CurrencyCurrent/

Noncurrent Monetary/

NonmonetaryTemporal Current

RateSales € 10,000 $4,000 $4,000 $4,000 $4,000COGS € 7,500 $3,000 $2,500 $3,000 $3,000Depreciation € 1,000 $333 $333 $333 $400Net operating income € 1,500 $667 $1,167 $667 $600Income tax (40%) € 600 $267 $467 $267 $240Profit after tax € 900 $400 $700 $400 $360

$300 -$550 $150Net income € 900 $700 $150 $550 $360Dividends € 0 $0 $0 $0 $0Addition to Retained

Earnings € 900 $700 $150 $550 $360

Foreign exchange gain (loss)

How Various Translation Methods Deal with a Change from €3 = $1 to €2 = $1

Hedging Translation Exposure

• If the managers of the firm wish to manage their accounting numbers as well as their business, they have two methods for dealing with translation exposure:– Balance sheet hedge– Derivatives hedge

Balance Sheet Hedge• Eliminates the mismatch between net

assets and net liabilities denominated in the same currency.– Borrow in different currencies to increase

those liabilities and balance the assets and liabilities

• Likely to create transaction exposure unless the existing cash flows can cover the new debt

Derivatives Hedge• An example would be the use of a forward

contract with a maturity of the reporting period to attempt to manage the accounting numbers.

• Using a derivatives hedge to control translation exposure really involves speculation about foreign exchange rate changes

• Probably doesn’t make sense to hedge potential paper losses

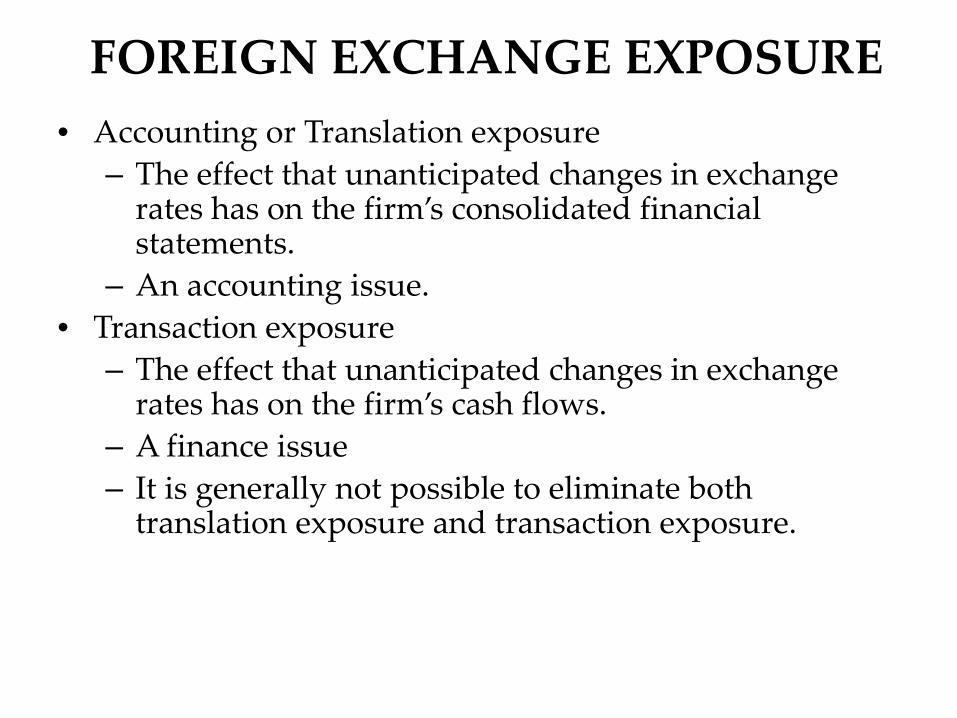

FOREIGN EXCHANGE EXPOSURE• Accounting or Translation exposure

– The effect that unanticipated changes in exchange rates has on the firm’s consolidated financial statements.

– An accounting issue.• Transaction exposure

– The effect that unanticipated changes in exchange rates has on the firm’s cash flows.

– A finance issue – It is generally not possible to eliminate both

translation exposure and transaction exposure.

FOREIGN EXCHANGE EXPOSURE• Operating Exposure

– Arises because exchange rate changes alter the value of future revenues and costs.

– Begins the moment a firm starts to invest in a market subject to foreign competition or in sourcing goods or inputs abroad

• Economic Exposures– Economic exposure = Transaction Exposure + Operating Exposure– Arise when the trading position of a business is at risk to

adverse movements in exchange rate.– Measures the change in the present value of the firm resulting

from any change in future operating cash flows of the firm caused by an unexpected change in exchange rates.

0% 0% 0% 0%

Complete the sentence correctly. ____________ exposure results from the

possibility of incurring a gain or loss related to a sale or purchase already

entered into and denominated in another currency.

A. TranslationB. Transaction C. OperatingD. Economic