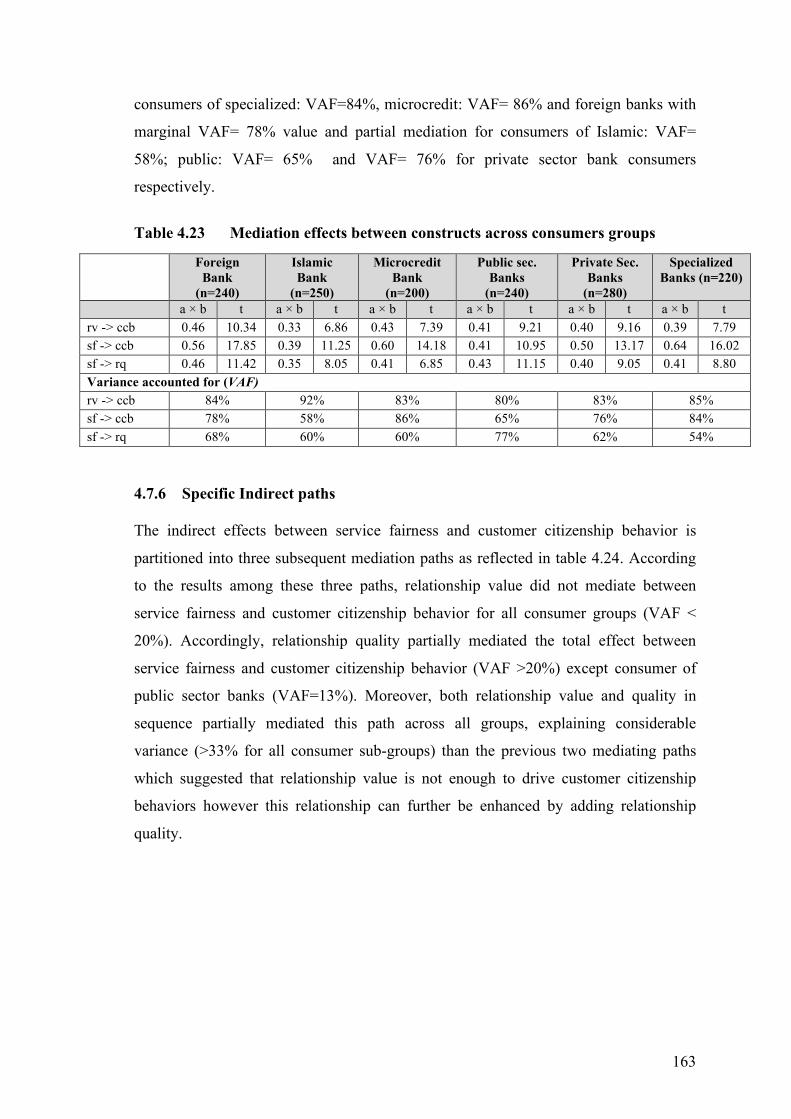

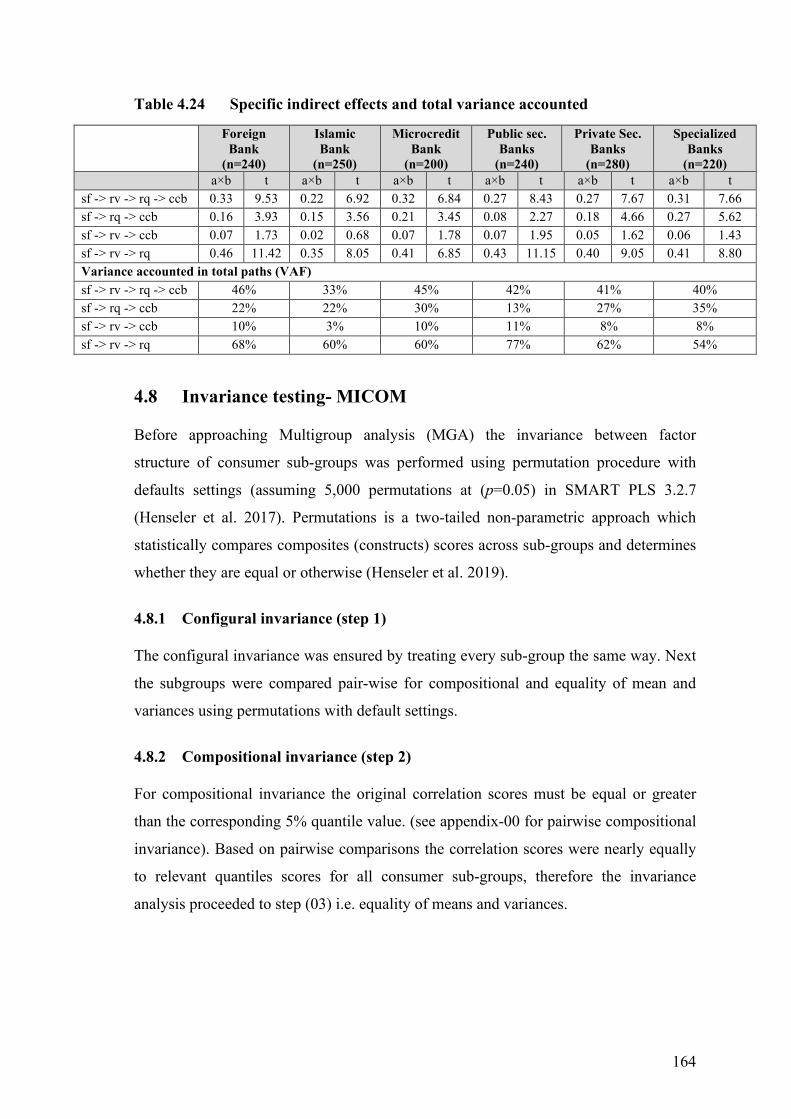

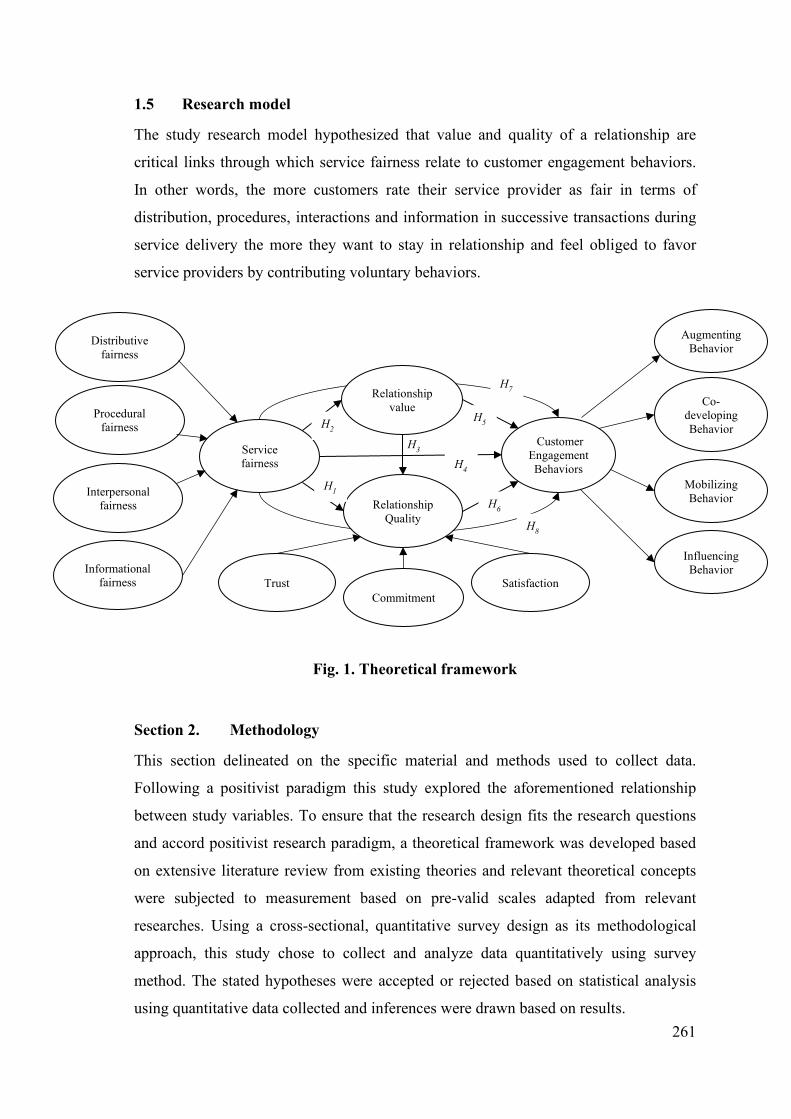

the mediating role of relationship marketing - pakistan

TRANSCRIPT

The Impact of Perceived Service Fairness on

Customer Citizenship Behaviors:

The Mediating Role of Relationship Marketing

By

Waseem Khan

091-12-14757

PhD Dissertation

In

Management Sciences

IQRA National University Peshawar Fall, 2020

The Impact of Perceived Service Fairness on

Customer Citizenship Behaviors:

The Mediating Role of Relationship Marketing

A Dissertation submitted to

The Department of Business Administration

IQRA National University Peshawar

In partial fulfillment

of the requirement for the degree of

PhD (Management Sciences)

By

Waseem Khan

091-12-14757

Fall, 2020

The Impact of Perceived Service Fairness on Customer Citizenship Behaviors: The Mediating Role of Relationship Marketing

A Dissertation submitted to the Business Administration Department as partial

fulfillment of the requirement for the award of Degree of Ph.D Management

Sciences.

Name Registration Number

Waseem Khan 091-12-14757

Supervisor

Prof. Dr. Farzand Ali Jan Department of Business Administration IQRA National University Peshawar December, 2019

Scanned with CamScanner

Author’s Declaration

I, Waseem Khan, bearing enrollment No. 091-12-14757, hereby state that my PhD

thesis titled “The Impact of Perceived Service Fairness on Customer Citizenship

Behaviors: The Mediating Role of Relationship Marketing” is my own work and has

not been submitted previously by me for taking any degree from this university i.e.

IQRA National University Peshawar or anywhere else in the country/world.

At any time if my statement is found to be incorrect even after I graduate the University

has the right to withdraw my PhD degree.

Date: December 25, 2019

Waseem Khan 091-12-14757

Plagiarism Undertaking

I solemnly declare that the research work presented in this thesis title “The Impact of

Perceived Service Fairness on Customer Citizenship Behaviors: The Mediating Role

of Relationship Marketing” is solely my research work with no significant

contribution from any other person. Small contribution/help wherever taken has been

duly acknowledged and that complete thesis has been written by me.

I understand the zero-tolerance policy of HEC and IQRA University Peshawar towards

plagiarism. Therefore, I as an author of the above titled thesis declare that no portion of

my thesis has been plagiarized and any material used as reference is properly

referred/cited.

I undertake if I am found guilty of any formal plagiarism in the above titled thesis even

after award of PhD Degree, the University reserves the right to withdraw/revoke my

PhD degree and that HEC and the university has the right to publish my name on the

HEC/ university website on which names of students are placed who submitted

plagiarized thesis.

Date: December 25, 2019

Waseem Khan 091-12-14757

Certificate

It is certified that Waseem Khan (091-12-14757) has carried out all the work related to this thesis under my supervision at the Department of Business Administration, IQRA University Peshawar, and the work fulfills the requirement for award of PhD degree.

Date: December 25, 2019

Supervisor:

_____________________________

Prof. Dr. Farzand Ali Jan Department of Business Administration

IQRA National University Peshawar

Head of Department:

_____________________________ Prof. Dr. Abid Usman Dean Department of Business Administration

Declarations

I declare the following:

That the material contained in this dissertation is the end result of my own work and that due acknowledgement has been given in the bibliography and references to all sources by the printed, electronic or personal.

That unless the dissertation has been confirmed as confident, I agree to an entire electronic copy or sections of this dissertation to being placed in library, if deemed appropriate, to allow future students the opportunity to see examples of past no longer than five years and that students would be able to print of copies or download. The authorship would remain anonymous.

I agree to my dissertation being submitted to a plagiarism detection service, where it will be stored in a database and compared against work submitted from this or any other school or from any other institution using the service.

I have read the Iqra National University Policy statement on ethics in research and consultancy.

INU ethics in research and consultancy; guidelines and procedures for students undertaking undergraduate/postgraduate research methods modules and dissertations and the policy for informed consent in research and consultancy and I declare that ethical issues have been considered, evaluated and appropriately addressed in this research.

_______________________ Waseem Khan 091-12-14757

PhD Scholar IQRA National University Peshawar

Date: December 25, 2019

Thumb Impression: __________

Copyrights Notice This research dissertation under the title “The Impact of Perceived Service Fairness on Customer Citizenship Behaviors: The Mediating Role of Relationship Marketing” is the intellectual property of Waseem Khan.

No part of this document may be reproduced, stored in any retrieval system or used otherwise without the prior permission of the author. I hereby allow IQRA National University, Peshawar to make copies of this dissertation for academic purposes only.

Any individual/organization may make copies of this document for non-commercial purposes with prior permission of the author.

_______________________

Waseem Khan

i

ACKNOWLEDGEMENTS

Undertaking doctoral studies was one of the most testing and yet valuable experience of

my life and it proved to be far more exciting and challenging than what I had expected.

Nonetheless, I could not have completed this study without the support and

encouragement of many individuals whom I extend my deep appreciation for their

invaluable contributions. Foremost, I gratefully acknowledge the contribution of

Professor Dr. Farzand Ali Jan who provided me intellectual support, constant

encouragement and constructive criticism. His faith in my abilities instilled tremendous

motivations for me to strive for excellence. I truly appreciate his guidance, steadfast

support, and dedication. I'm forever grateful for his generous sharing of his most

valuable resources and time, to help me move forward as I moved through this research.

The next person whom I wish to extend much appreciation is Professor Dr. Anwar

Chishti, from whom I have learned a great deal of knowledge about the application of

quantitative data analysis techniques. I am also thankful to him for his enthusiasm in

teaching us, especially in providing us with valuable research materials during doctoral

coursework. I thank you sir because I have learned a lot and got to know more about

how to conduct research.

I am also very grateful for the assistance provided by all the internal review committee

members of the Business Administration Department for their insightful and

constructive feedback during formative stages of my dissertation. Their experiences,

knowledge, and skills have helped me to complete this work in a much better way than

earlier versions. In particular, I am thankful for the help extended by Professor Dr.

Abid Usman, and Dr. Adil Adnan. Their constructive comments since the early stage of

this dissertation are valuable for me to improve the quality of the dissertation. I also

appreciate their willingness and availability for helping me when I was in need of their

assistance.

I would also like to express my thanks to Dr. Kashif Amin for his valuable inputs and

comments to my doctoral dissertation from its formative stage. I am indebted to for his

help, patience, and persistent support during my studies at Iqra National University. His

comprehensive and critical comments on my dissertation were indispensable to make it

meaningful.

ii

I would also like to thank Dr. Amir Nadeem, Dean Department of management

Sciences from City University Peshawar who have reviewed my dissertation, for his

meticulous examination of my dissertation and providing valuable comments and

suggestions to further improve it. I also want to thank my Uncle and my family

members who served as a main resource for helping me establish contact with banks

and referred my survey for data collection. I also extend my appreciation to Kashif

Amin, Kamran Nawaz, Kashif Shah and Ms. Nida Aman for their assistance and

collaboration for my data collection. I am thankful for the Assistance provided by the

branch managers and banking staff of the all branches in the data collection processes.

Most importantly, I am indebted for every individual consumer who responded to my

questionnaire survey, needless to say, I am so thankful for their time and kindness. I am

indebted for all the reviewers who reviewed the initial draft of the questionnaire,

validated its contents and provided their valuable comments and suggestions.

I want to express my thanks to Higher Education Commission for awarding me

Indigenous Scholarship grant and enabling me to meet my expenses and pay my full

tuition-fees during my doctoral studies. My sincere gratitude goes to Iqra National

University for all their support and facilitation during my doctoral study. I would also

like to express my gratitude to all the honorable faculty members in the Department of

Business Administration for their valuable help and instructions during my study at Iqra

National University. My thanks go to all the administrative staff of the University for

their timely provision of administrative assistance which facilitated my degree

completion process.

Last but not the least, I greatly appreciate the support of my colleagues and friends in

my coursework at Business Administration department, Iqra National University, who

had been with me for two years. I enjoyed a very valuable and unforgettable time with

them and I wish them best of luck in their future endeavors.

Thank you very much!

iii

DEDICATION

This dissertation is dedicated to my beloved family members, who have meant and

continue to mean so much to me, specially my father who have always loved me and

gave me great power for enduring difficulties.

I take this opportunity to thank my wife who has helped me to restore passion in my

professional life. Lastly, I would like to adore my lovely children Muhammad Ali,

Maryam and Mahrosh for their grace.

iv

LIST OF ABBREVIATIONS

AB Augmenting Behavior

CB Co-developing Behavior

CC Customer Commitment

CCB Customer Citizenship Behavior

CEB Customer Engagement Behavior

CFA Confirmatory Factor Analysis

CS Customer Satisfaction

DF Distributive Fairness

FR Foreign Bank

IB Influencing behavior

IB Islamic Bank

IF Informational Fairness

IPF Interpersonal Fairness

MB Mobilizing behavior

MC Microcredit Bank

MGA Multigroup Analysis

MICOM Measurement invariance of composites

PB Public Bank

PCT Psychological Contract theory

PF Procedural Fairness

PLS Partial Least Squires

PLS-SEM Partial Least Squired based Structure Equation Modeling

PVT Private Bank

RM Relationship Marketing

RQ Relationship Quality

RV Relationship Value

SBP State Bank of Pakistan

v

SD Logic Service dominant logic

SEM Structural Equation Modeling

SET Social Exchange theory

SF Service Fairness

SP Specialized Bank

TR Trust

WOM Word of Mouth

vi

ABSTRACT

Since late 1980’s the banking sector in Pakistan has undergone major structural

changes due to financial liberalization and deregulations. This transformation has led to

greater competition among financial institutions, favoring in the efficiency and

competitiveness of banking sector. As a result, a greater variety and choices of products

and services for customers are available while some banking institutions are offering

sophisticated delivery systems and more value-added services than rivals. Likewise,

banks have also come under enormous pressure to tackle the growing demands and

expectations of their consumers as well as due to the shift in customer-centric

regulatory paradigm towards protection of financial consumers, posing major challenge

for bank to retain existing customers. These considerations converge to imply the need

for more specific customer-focused strategies to build and maintain enduring bank-

client relationships. Presently, the business environment surrounding banking

institution is highly competitive where new clients are hard to attract at mature stage in

their life cycles, hence banks must strive for establishing new revenue streams,,

particularly in a situation where competition between financial establishments has

intensified, banking institutions need to make various efforts to achieve differentiated

competitiveness through forging sustainable relationships with customers.

In terms of producers of financial services, considering the highly competitive nature of

banking industry and increasingly interactive customer roles, fairness in service

delivery is essential in developing and maintaining bank-client relationships. Earlier

studies show that a consumer's perception of whether a service provider has fulfilled

the obligation to deliver the desired outcome and benefits associated with the service

promised to consumers serve as a is a fundamental basis for sustaining and enhancing

long-term customer-firm relationships. Service fairness is a multidimensional construct

composed of distributive fairness, procedural fairness, informational and interactional

fairness, which refers to a consumer’s perception regarding the degree of justice in a

service provider’s behavior during service delivery process. Service fairness is an

implicit agreement between customers with their service providers to have their needs

served well and to be treated fairly according the service outcomes promised.

Successful customer relationship management can be attributed to a customer’s positive

evaluations of a service provider’s efforts in provision of service fairness excellence

vii

during an exchange relationship. Although banking services is recognized to encounter

numerous service failure episodes there has been scant investigations in commercial

banking sector of Pakistan that addressed the connection among service fairness,

relationship marketing and customer engagement. Past studies in the domain

relationship marketing strongly support that mutually profitable buyer-seller

relationships are key to secure competitive advantage emphasizing the importance of

quality and value of relationships. However, there is a lack of an integrative perspective

about understanding buyer-seller relationship building process through the lens of

service fairness. This research contributes to building a comprehensive understanding

on how customer evaluations regarding different facets of service fairness affect bank-

consumer relationship building process and lead customers to perform various

citizenship behaviors, by examining empirically this relationship at multi-group level.

This research study was conducted in Pakistan, using a positivist philosophical lens,

data was gathered quantitively with the help of questionnaire distributed using stratified

random sampling technique. The validity of survey instrument and structural paths

relationships were confirmed using pilot study procedure. The results of pilot survey

were very useful in validating the proposed model and measurement scales used in the

study however few of the items were dropped from subsequent analysis to improve the

reliability and validity of the instrument. Data was gathered from 1740 consumers of

banking services located within scheduled bank branches in a single cross-section

however only 1430 valid responses were subjected to further analysis. The model was

assessed using partial least square based Structured Equation Modeling (PLS-SEM),

using Smart PLS 3.2.7 statistical software following the PLS-SEM guidelines proposed

by (Jörg Henseler, Hubona, & Ray, 2017) in the field of social sciences research. As a

result, the model demonstrated greater predictive response to a consumer’s assessment

of service fairness.

The results of this research confirmed that banking consumers commonly evaluate

fairness in exchange relationships when dealing with service providers. The findings

support the model’s structure and indicated that all four dimensions of service fairness

determine relationship value and quality, which in turn lead customers to perform

citizenship behaviors. The results show that service fairness evaluations also had direct

influence on customer citizenship behavior, however this relationship is better

viii

explained by a firm’s relationship marketing efforts. This implies that although fair

treatment is essential in reinforcing long-term relationships and for customers to engage

in citizenship behaviors but it is also a significant condition that may encourage

consumers to perform positive extra role behavioral outcomes. Therefore, banks should

provide assurance that their services can achieve a sustainable level of favorableness

that meets what the service provider has promised to its customers.

This study brought to light that the knowledge pertaining to the critical role of service

fairness strategies in building valuable, enduring relationships with customers.

Moreover, this research contributes in the relationship marketing literature on how

service fairness excellence encourage customer to engage in citizenship behaviors in

favor of the firm through developing successful long-term mutually beneficial

relationship. Therefore, besides service excellence banks need focus on providing

excellence in service fairness to create strong relationships with their clients as endured

relationship can lead to customer citizenship behaviors.

Keywords: Service fairness, Relationship Marketing, Customer citizenship behaviors,

Multi-group analysis, Banking Sector, Pakistan

ix

TABLE OF CONTENTS

ACKNOWLEDGEMENTS .............................................................................................. i

DEDICATION ................................................................................................................iii

LIST OF ABBREVIATIONS ......................................................................................... iv ABSTRACT .................................................................................................................... vi

TABLE OF CONTENTS ................................................................................................ ix

LIST OF TABLES ........................................................................................................ xvi

LIST OF FIGURES .....................................................................................................xviii Chapter 1 .......................................................................................................................... 1

INTRODUCTION ............................................................................................................ 1

1.1 Introduction ........................................................................................................... 1

1.2 Background of the study ....................................................................................... 1 1.3 Problem Statement ................................................................................................ 6

1.4 Research Questions ............................................................................................... 7

1.5 Research Objectives .............................................................................................. 8

1.6 Significance of the Study ...................................................................................... 8 1.7 Scope of the study ............................................................................................... 11

1.8 Research gaps identified ...................................................................................... 12

1.9 Structure of the thesis .......................................................................................... 14

Chapter 2 ........................................................................................................................ 16

LITERATURE REVIEW ............................................................................................... 16 2.1 Chapter overview ................................................................................................ 16

2.2 Equity theory ....................................................................................................... 16

2.3 Psychological contract theory ............................................................................. 20

2.4 Social exchange theory ........................................................................................ 26 2.5 Service dominant logic ........................................................................................ 30

2.6 Service fairness ................................................................................................... 32

2.6.1 Distributive fairness ..................................................................................... 34

2.6.2 Procedural fairness ....................................................................................... 36 2.6.3 Interpersonal fairness ................................................................................... 37

2.6.4 Informational fairness .................................................................................. 38

2.7 Relationship marketing ....................................................................................... 40

2.7.1 Relationship value ........................................................................................ 41

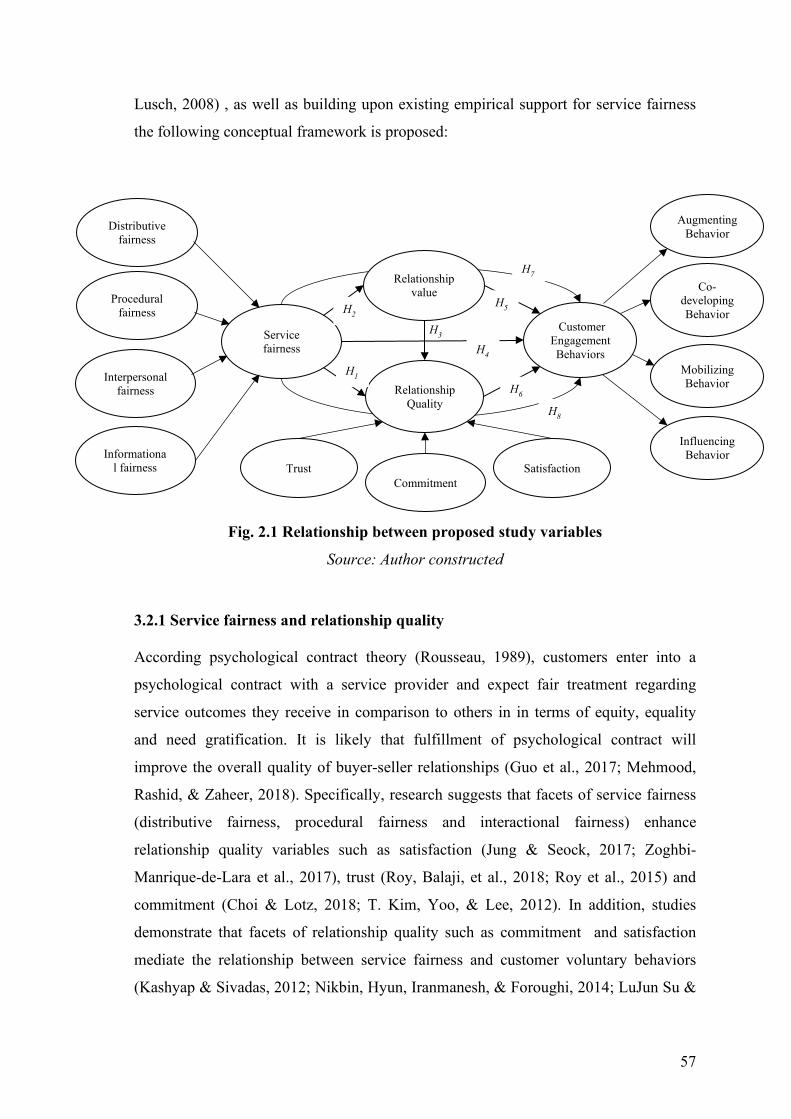

x

2.7.2 Relationship quality ..................................................................................... 45

2.7.1.1 Customer satisfaction .................................................................................. 47

2.7.1.2 Customer trust ............................................................................................. 49 2.7.1.3 Customer commitment ................................................................................ 49

2.8 Customer citizenship behavior ............................................................................ 50

Chapter 3 ........................................................................................................................ 54

RESEARCH METHODOLOGY ................................................................................... 54 3.1 Chapter overview ................................................................................................ 54

3.2 Theoretical framework and research hypotheses ................................................ 54

3.2.1 Service fairness and relationship quality ..................................................... 57

3.2.2 The relationship between service fairness and relationship value ............... 58 3.2.3 Relationship value and relationship quality ................................................. 59

3.2.4 Service fairness and customer engagement behavior .................................. 60

3.2.5 Relationship quality and customer engagement behavior............................ 60

3.2.6 Relationship value and customer engagement behavior .............................. 61 3.2.7 Service fairness, relationship quality, customer engagement behavior ....... 62

3.2.8 Service fairness, relationship value, customer engagement behavior .......... 63

3.3 Research paradigm .............................................................................................. 63

3.3.1 Ontology ...................................................................................................... 64 3.3.2 Epistemology ............................................................................................... 64

3.3.3 Methodology ................................................................................................ 65

3.3.4 Positivist paradigm of inquiry ...................................................................... 65

3.3.5 Realism ........................................................................................................ 66

3.3.6 Axiology ...................................................................................................... 66 3.4 Research design ................................................................................................... 67

3.4.1 Research approach ....................................................................................... 67

3.4.2 Research strategy ......................................................................................... 68

3.4.3 Research choice............................................................................................ 69 3.4.4 Time horizon ................................................................................................ 69

3.4.5 Research context .......................................................................................... 69

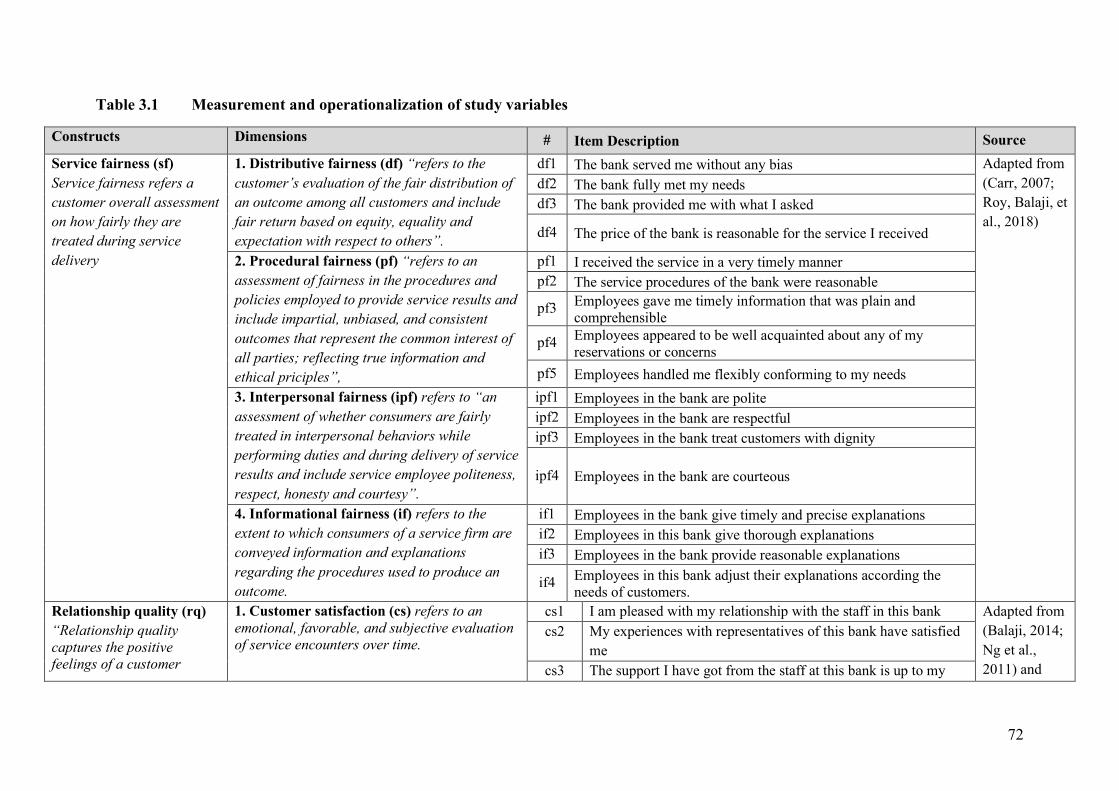

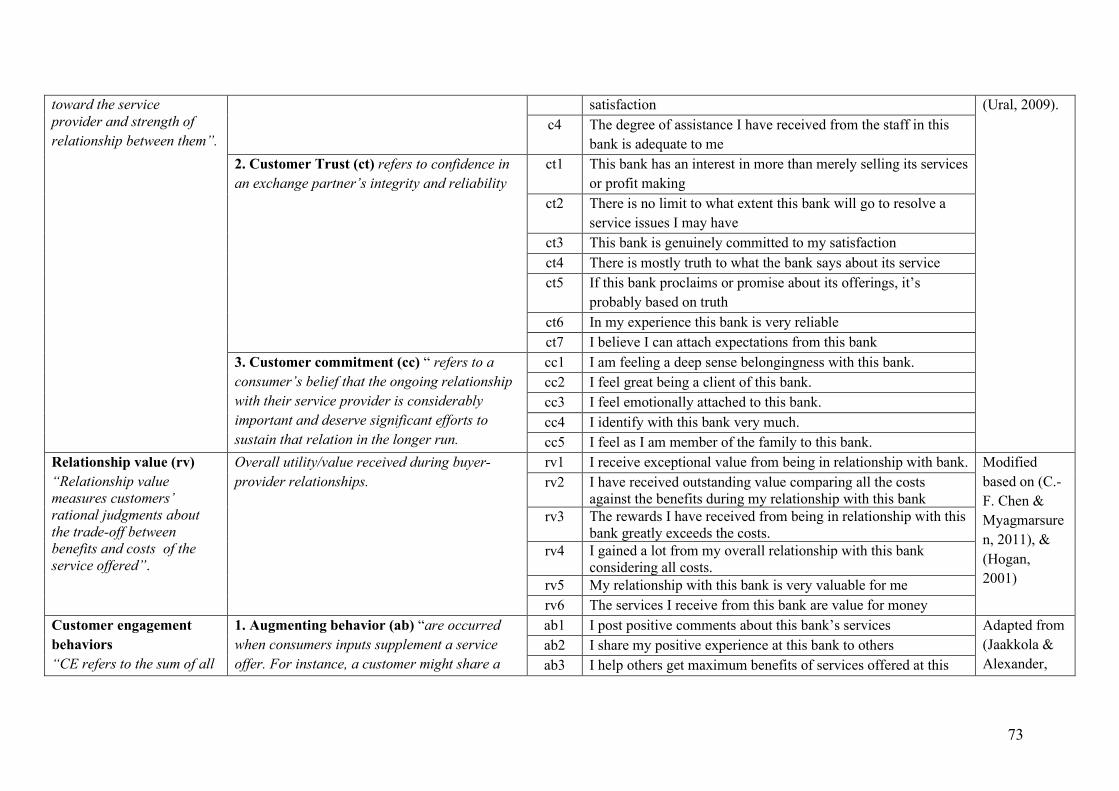

3.5 Data collection preparations ................................................................................ 70

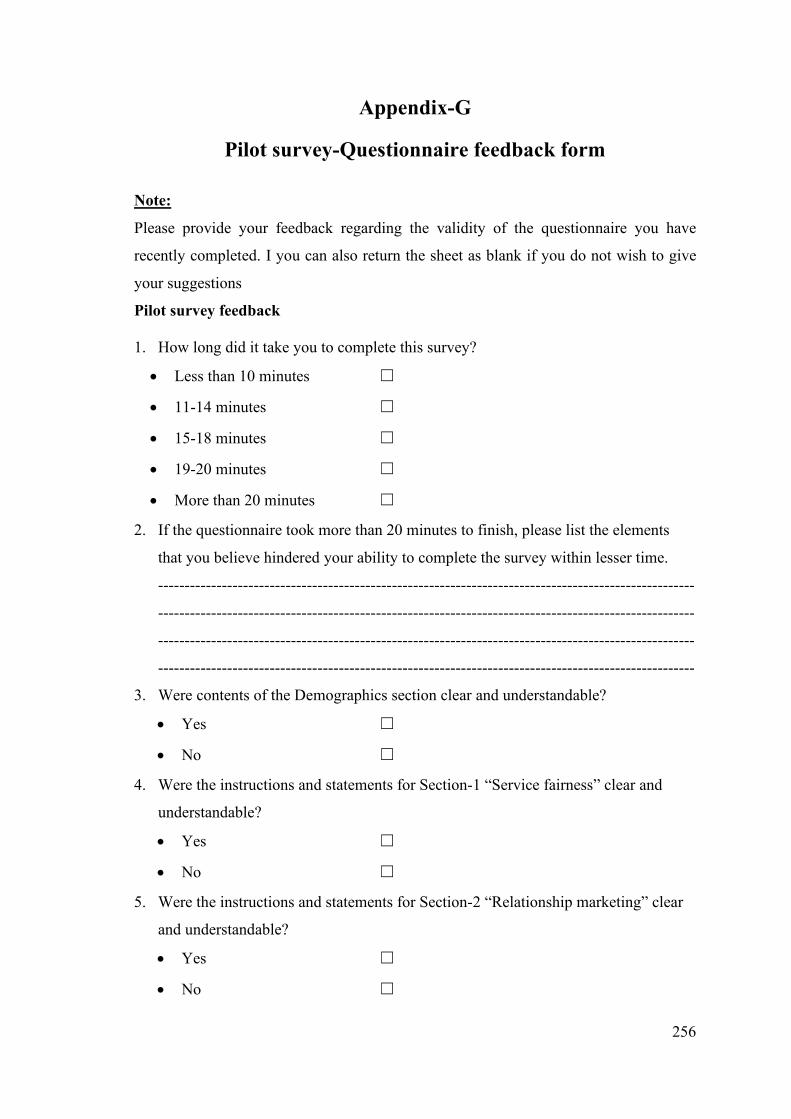

3.5.1 Instrumentation ............................................................................................ 70 3.5.2 Questionnaire translation into Urdu and pre-testing .................................... 75

3.5.3 Theoretical framework validation ................................................................ 76

3.5.3.1 Questionnaire pre-testing ............................................................................ 76

xi

3.5.3.2 Questionnaire pilot testing .......................................................................... 76

3.5.4 Main study ................................................................................................... 78

3.5.4.1 Research Population .................................................................................... 78 3.5.4.2 Sampling Frame .......................................................................................... 78

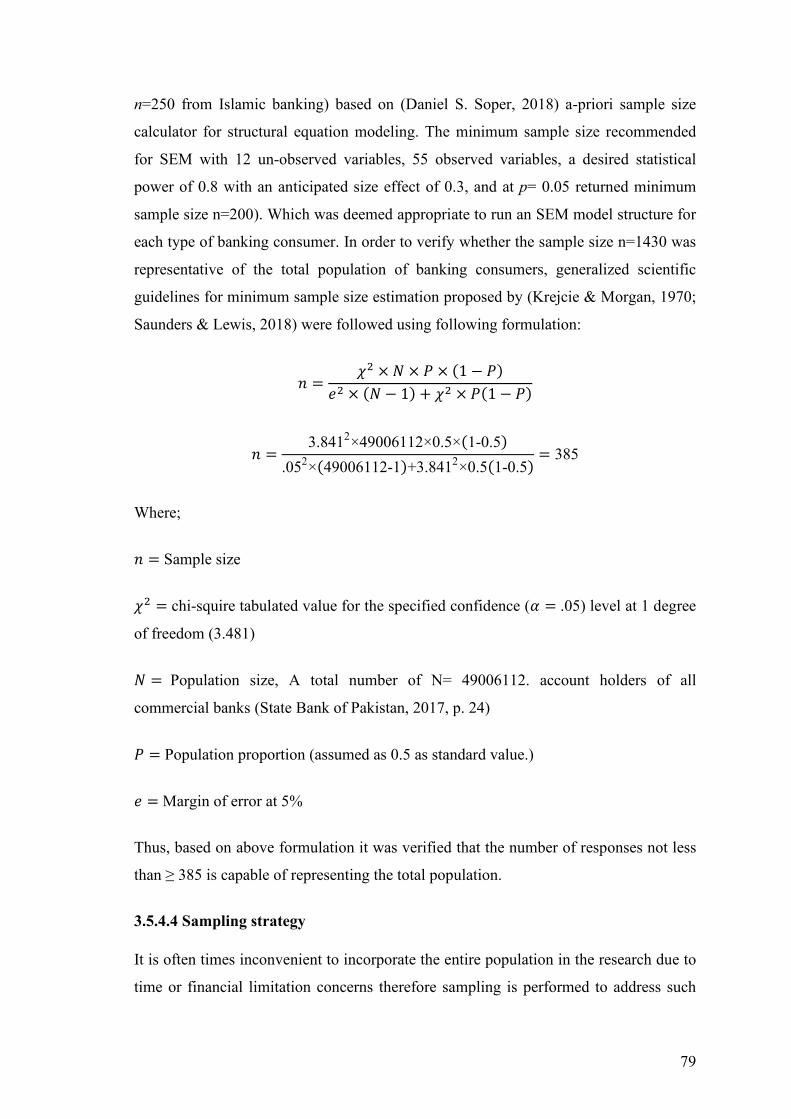

3.5.4.3 Sample Size ................................................................................................. 78

3.5.4.4 Sampling strategy ........................................................................................ 79

3.5.4.5 Data collection procedure ........................................................................... 81 3.6 Data analysis preparation .................................................................................... 82

3.6.1 Introduction .................................................................................................. 82

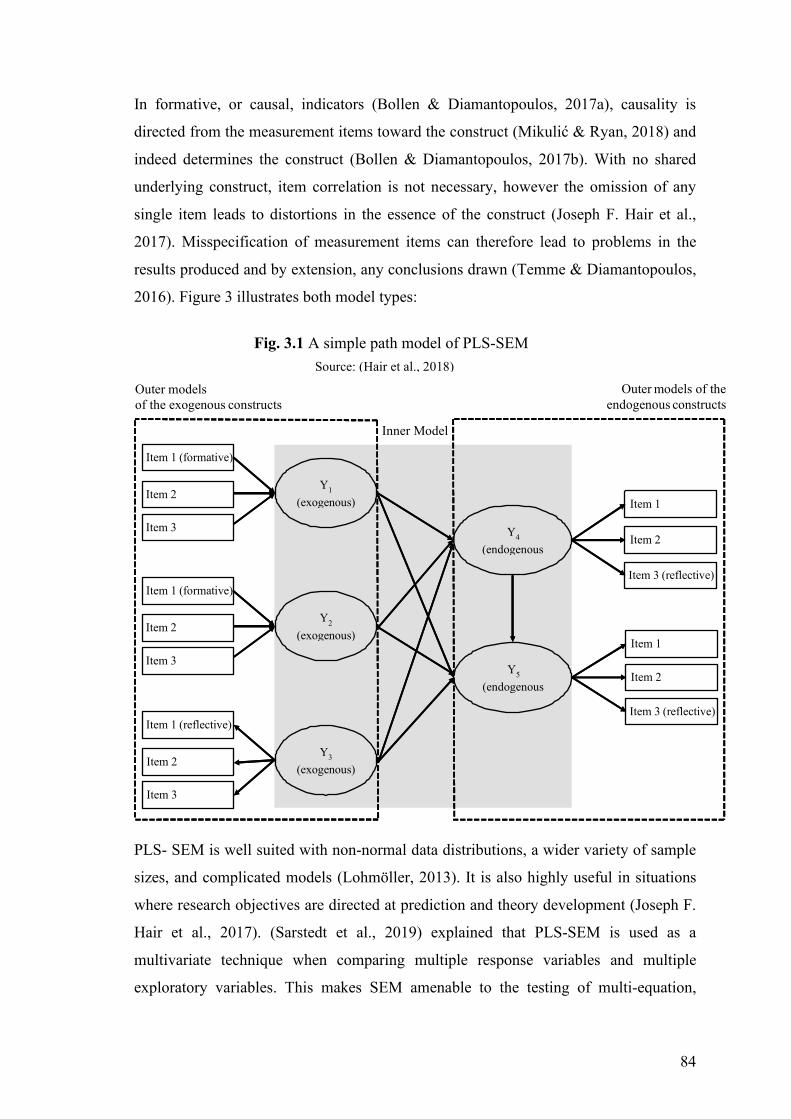

3.6.2 Structural equation modelling (SEM) .......................................................... 82

3.6.3 Covariance-based and variance-based structural equation modelling SEM 85 3.6.4 Rationale for using PLS-SEM ..................................................................... 86

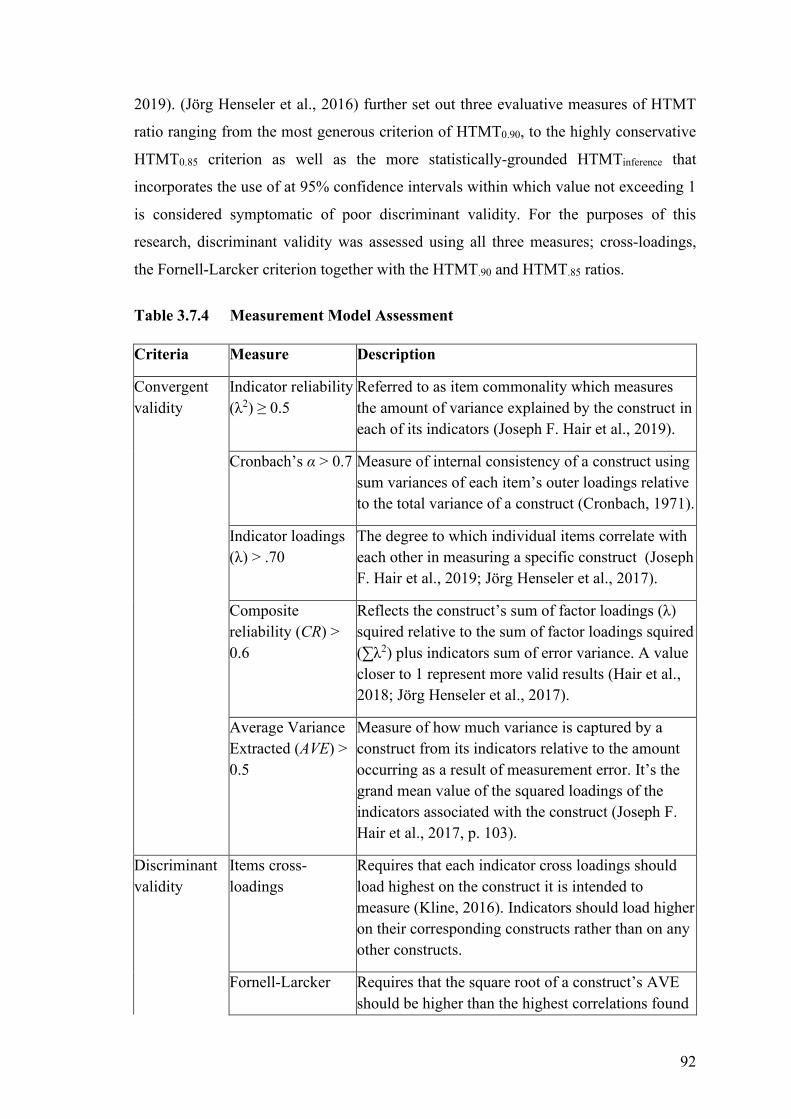

3.7 Assessing the results measurement model .......................................................... 88

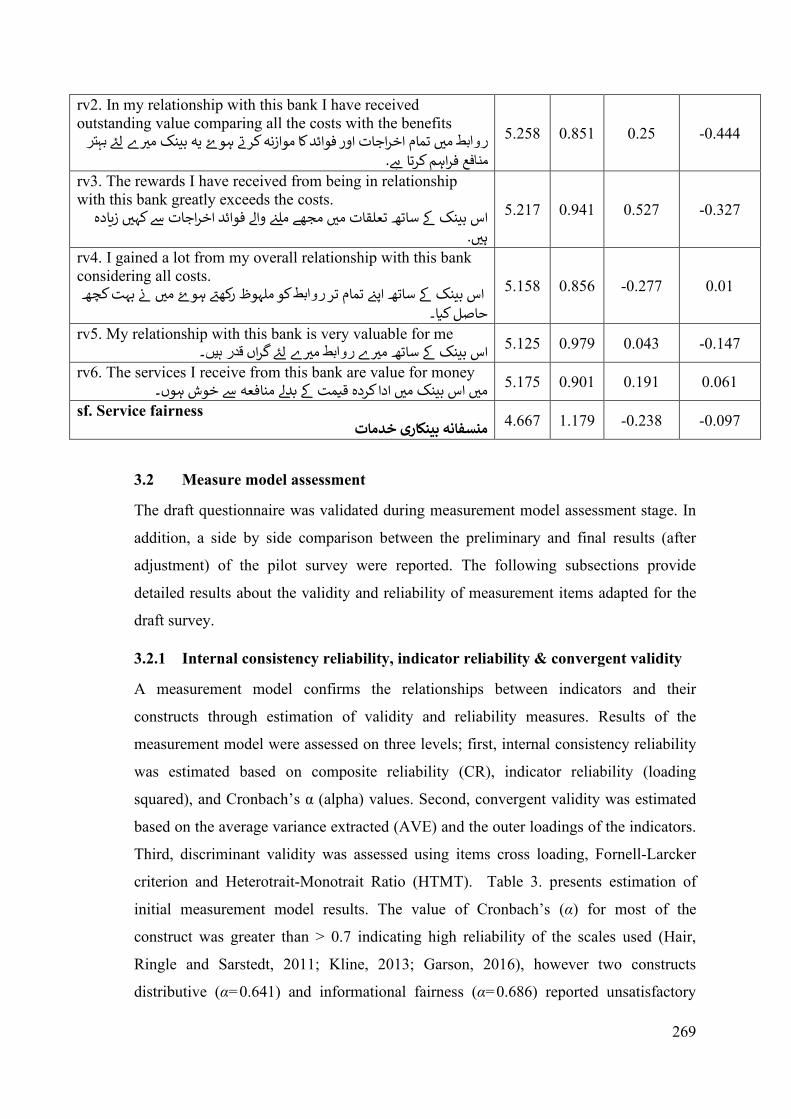

3.7.1 Internal consistency reliability ..................................................................... 88

3.7.1.1 Composite reliability ................................................................................... 88 3.7.1.2 Indicator reliability ...................................................................................... 89

3.7.1.3 Cronbach’s Alpha (α) .................................................................................. 89

3.7.2 Model validity .............................................................................................. 89

3.7.3 Convergent validity ...................................................................................... 90 3.7.3.1 Average variance extracted (AVE) ............................................................. 90

3.7.3.2 Item outer loadings (λ) ................................................................................ 90

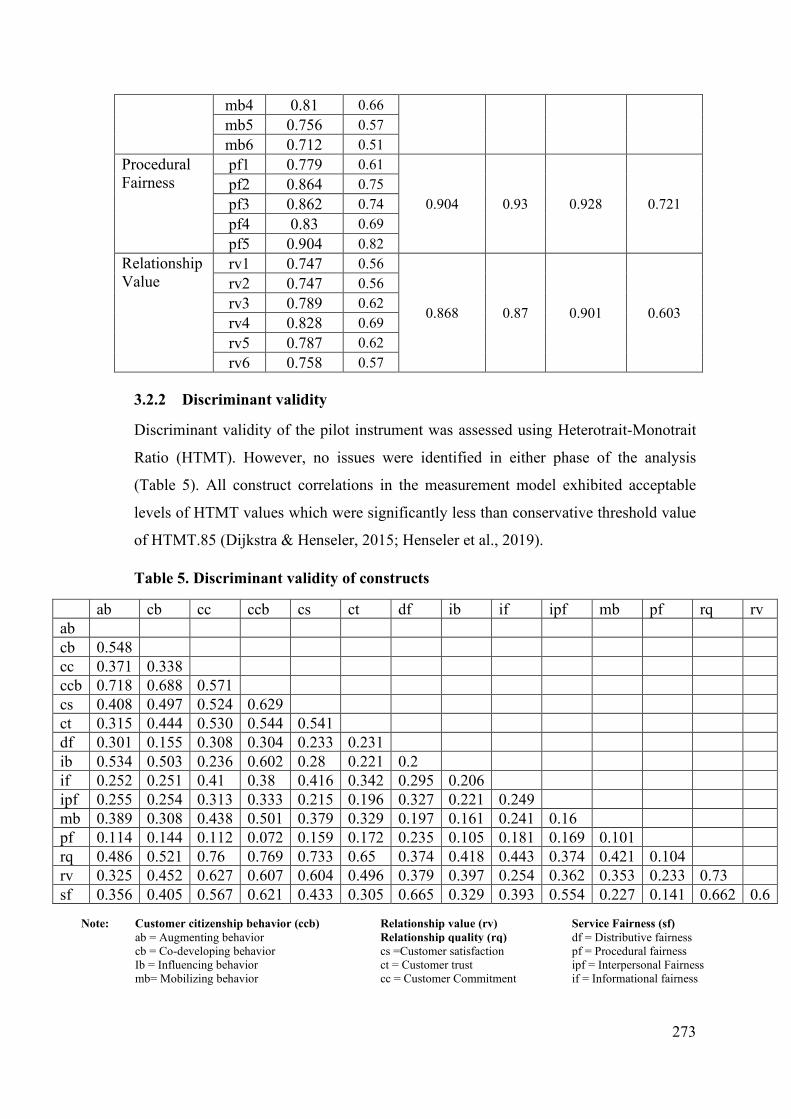

3.7.4 Discriminant validity ................................................................................... 91

3.7.4.1 Fornell-Larcker criterion ............................................................................. 91

3.7.4.2 Item cross loadings ..................................................................................... 91 3.7.4.3 Heterotrait-Monotrait Ratio (HTMT) ......................................................... 91

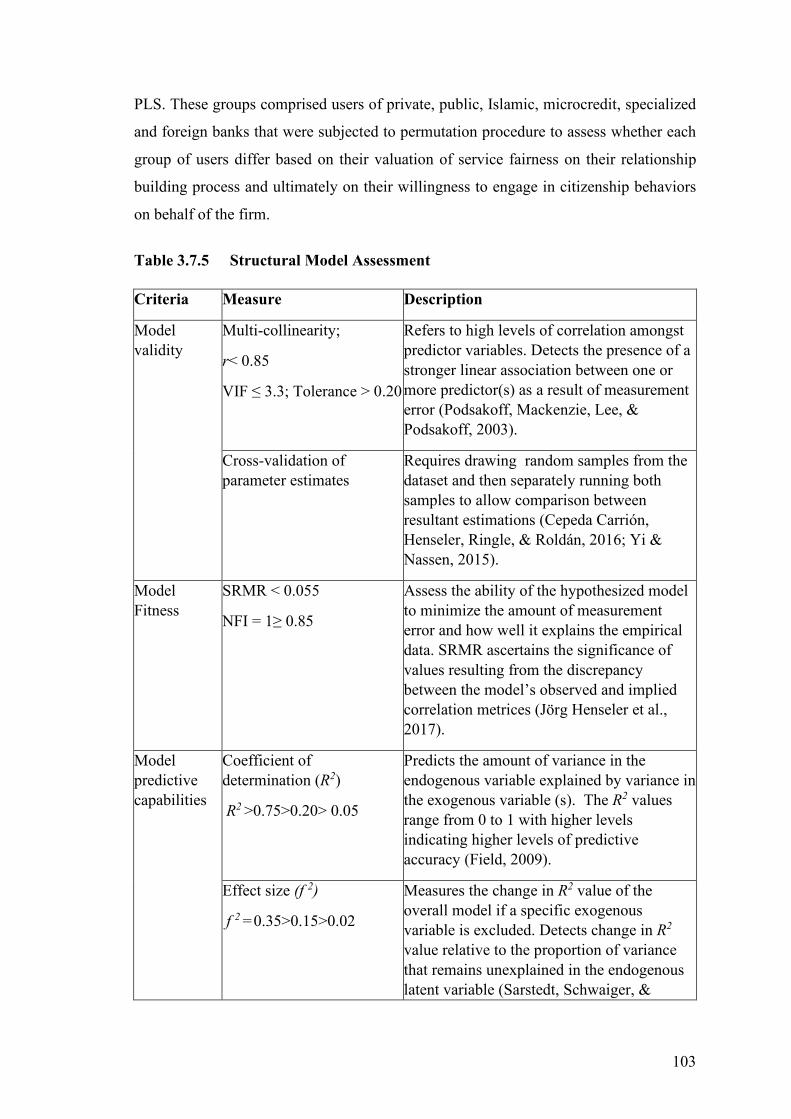

3.7.5 Assessing the results structural model ......................................................... 93

3.7.5.1 Assessing the structural model for (multi) collinearity ............................... 94

3.7.5.2 Cross-validation of parameter estimate stability ......................................... 94 3.7.5.3 Assessing the model predictive power – coefficient of determination (R2) 95

3.7.5.4 Assessing the f2 effect size .......................................................................... 95

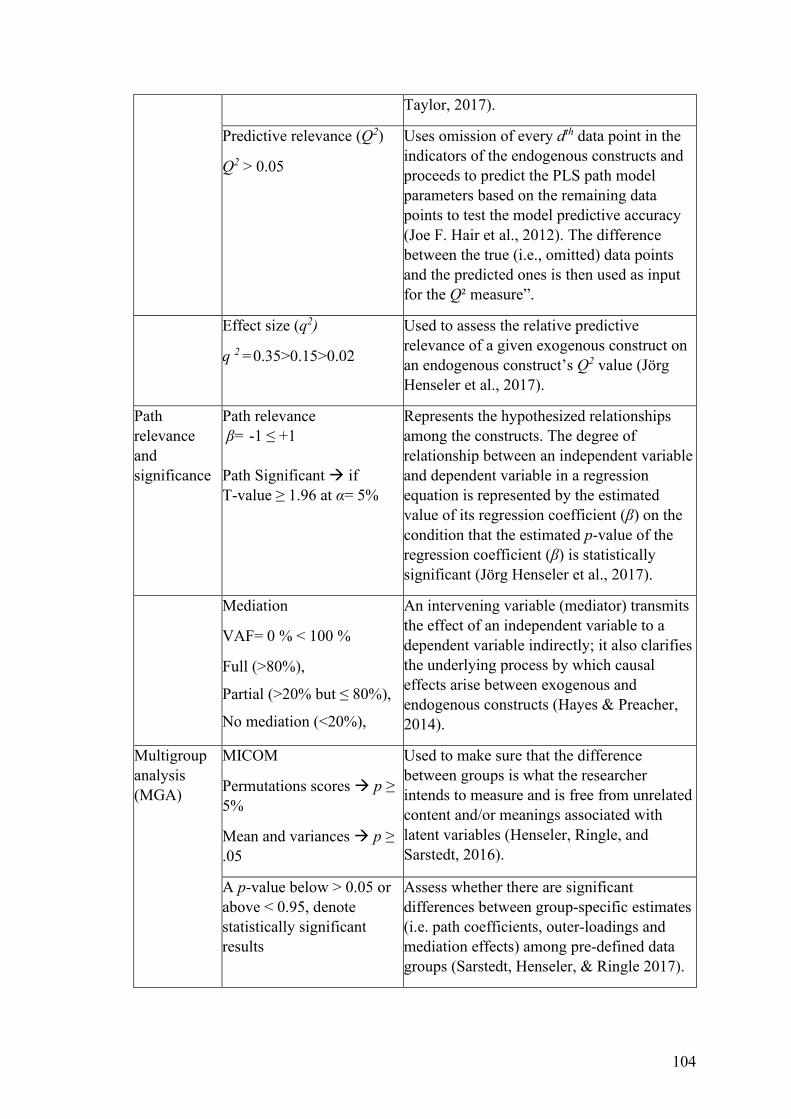

3.7.5.5 Assessing predictive relevance (Q2) ........................................................... 96

3.7.5.6 Assessing the q2 effect size ......................................................................... 97 3.7.5.7 Significance and relevance assessments of structural model paths ............ 97

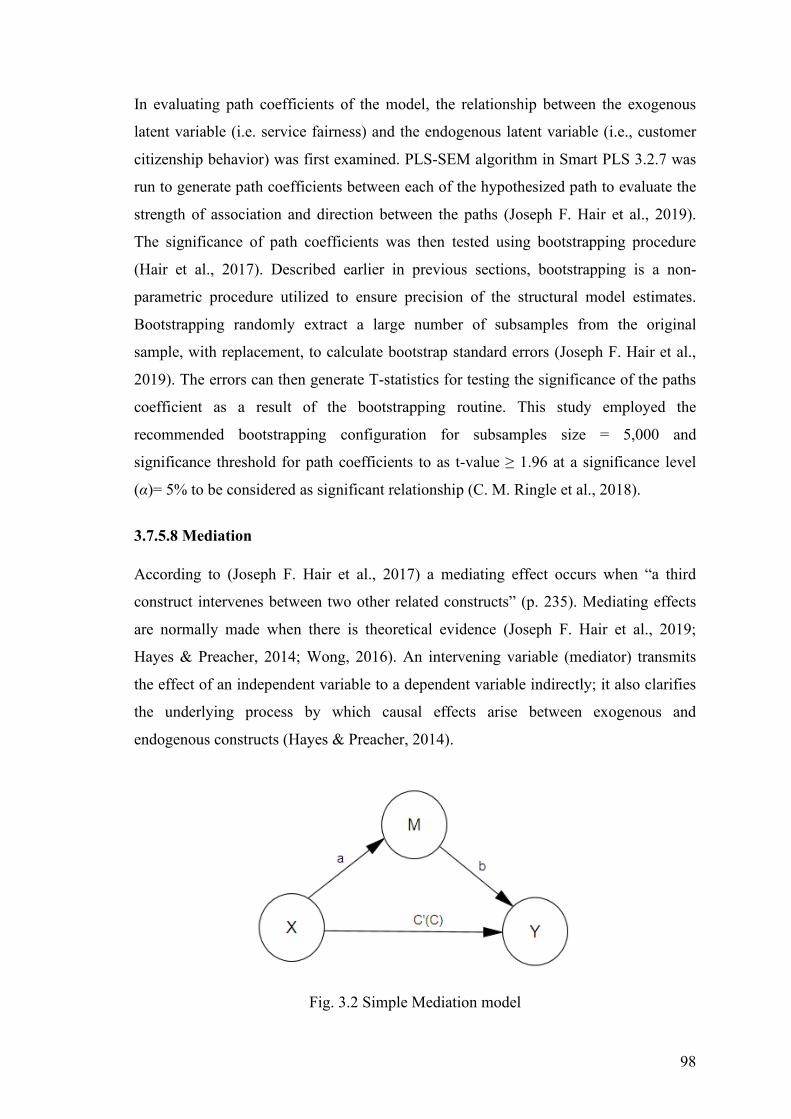

3.7.5.8 Mediation .................................................................................................... 98

3.7.5.9 Assessing model goodness of fit ................................................................. 99

xii

3.7.5.10 Measurement invariance of composite models - MICOM...................... 100

3.7.5.11 Multi-group analysis – (MGA) ............................................................... 102

3.8 Data management .............................................................................................. 105 3.8.1 Data screening ............................................................................................ 105

3.8.2 Missing values ........................................................................................... 105

3.8.3 Outlier analysis .......................................................................................... 105

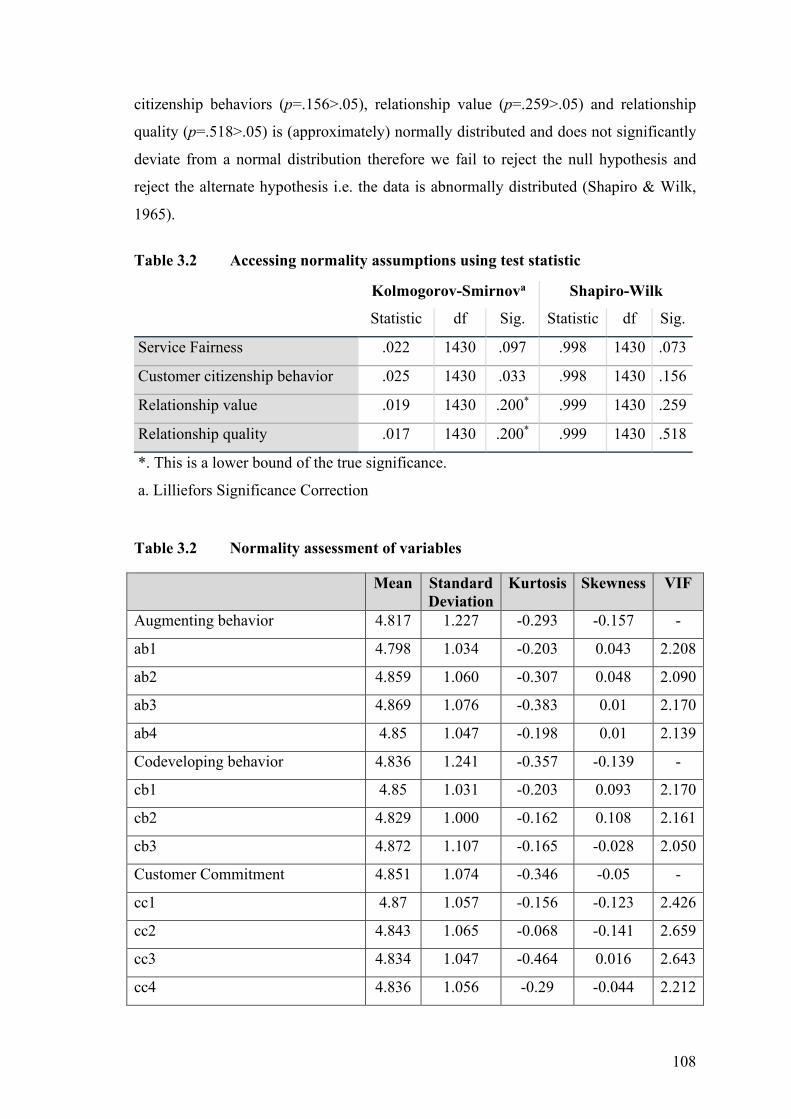

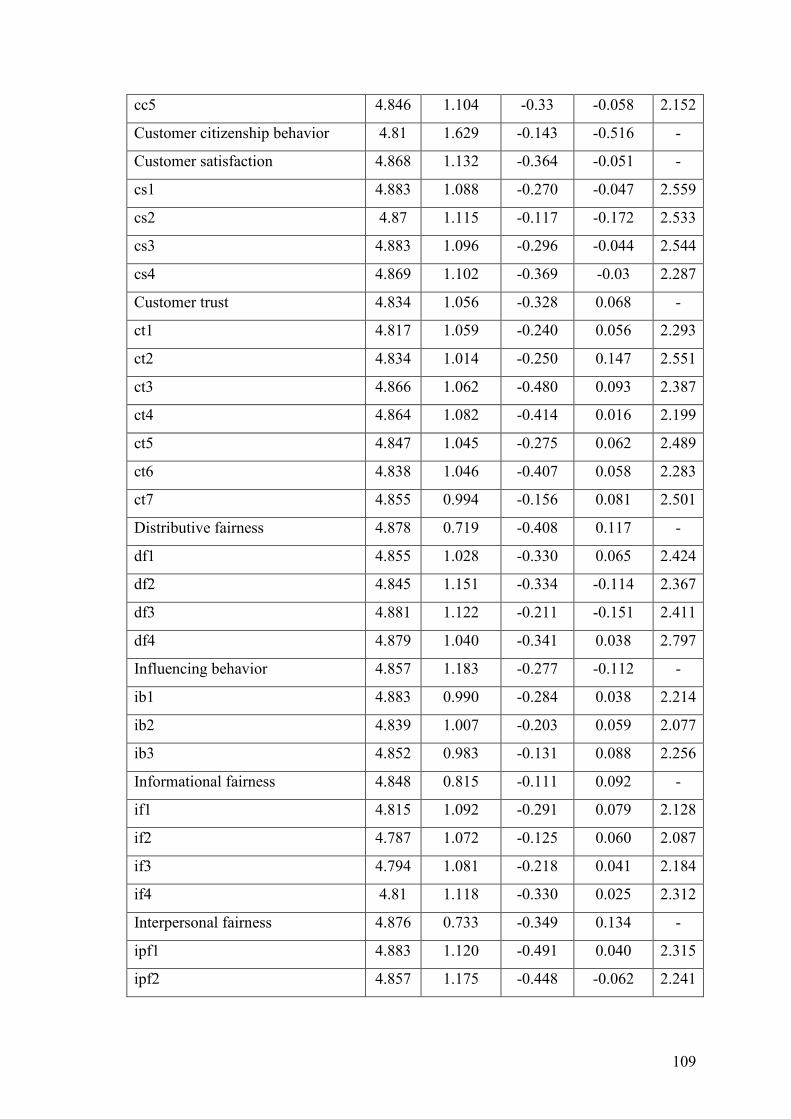

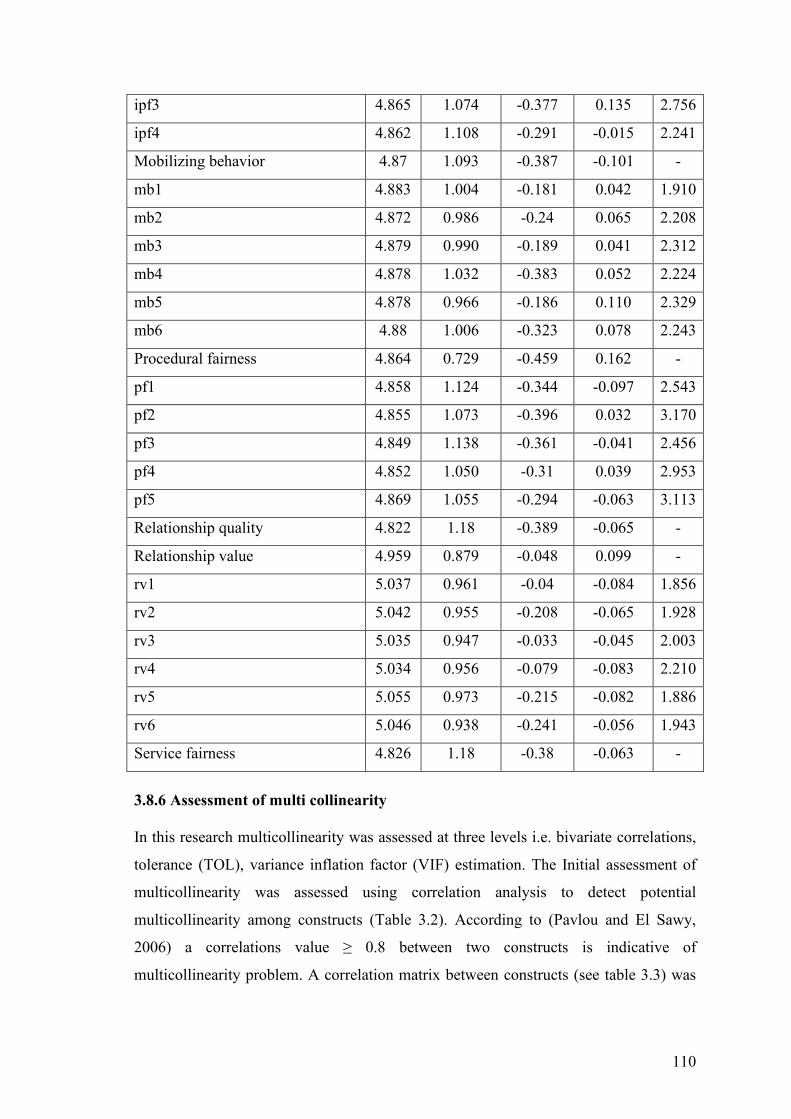

3.8.4 Data coding ................................................................................................ 106 3.8.5 Assessment of normality ............................................................................ 107

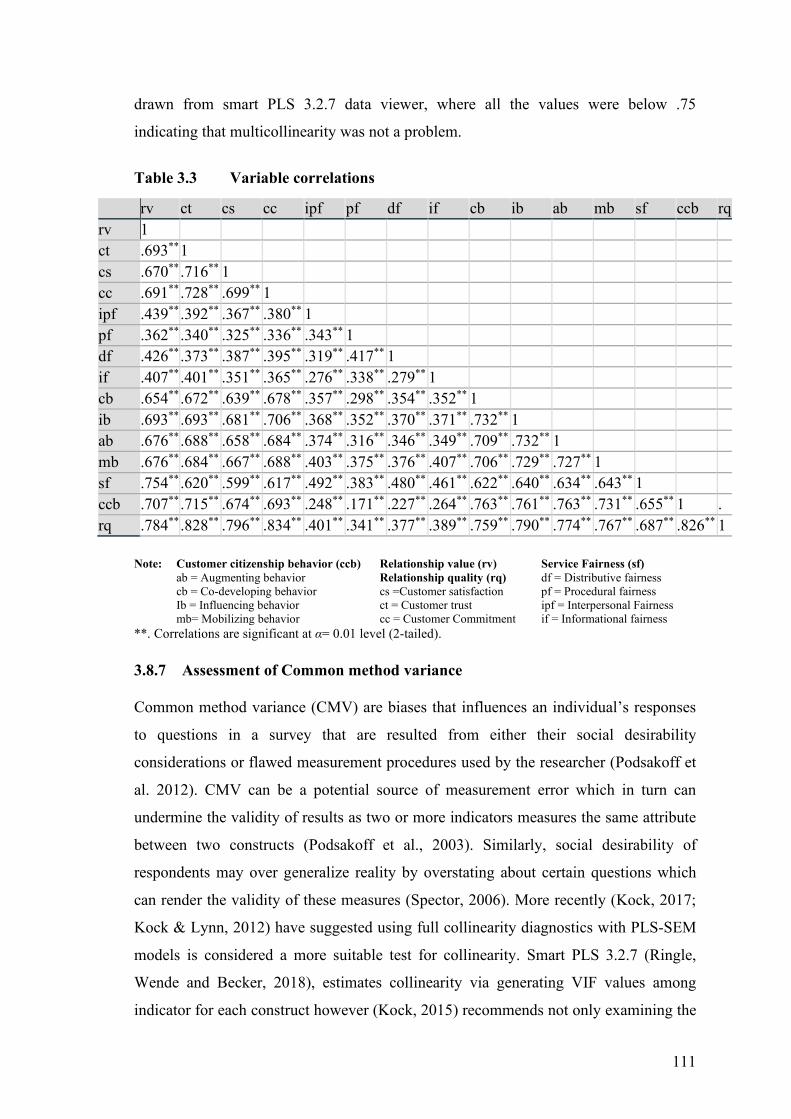

3.8.6 Assessment of multi collinearity ................................................................ 110

3.8.7 Assessment of Common method variance ................................................. 111

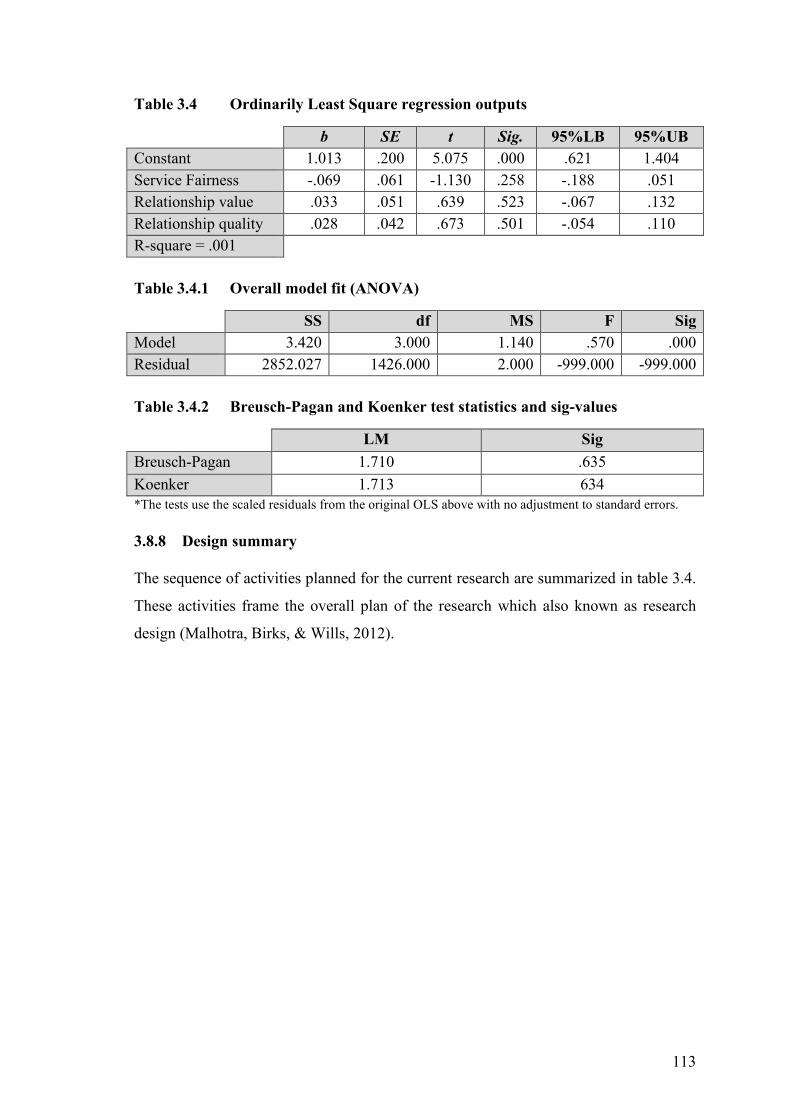

3.8.8 Assessment of heteroscedasticity ............................................................... 112 3.8.8 Design summary ........................................................................................ 113

Chapter 4 ...................................................................................................................... 116

RESULTS AND DISCUSSION .................................................................................. 116

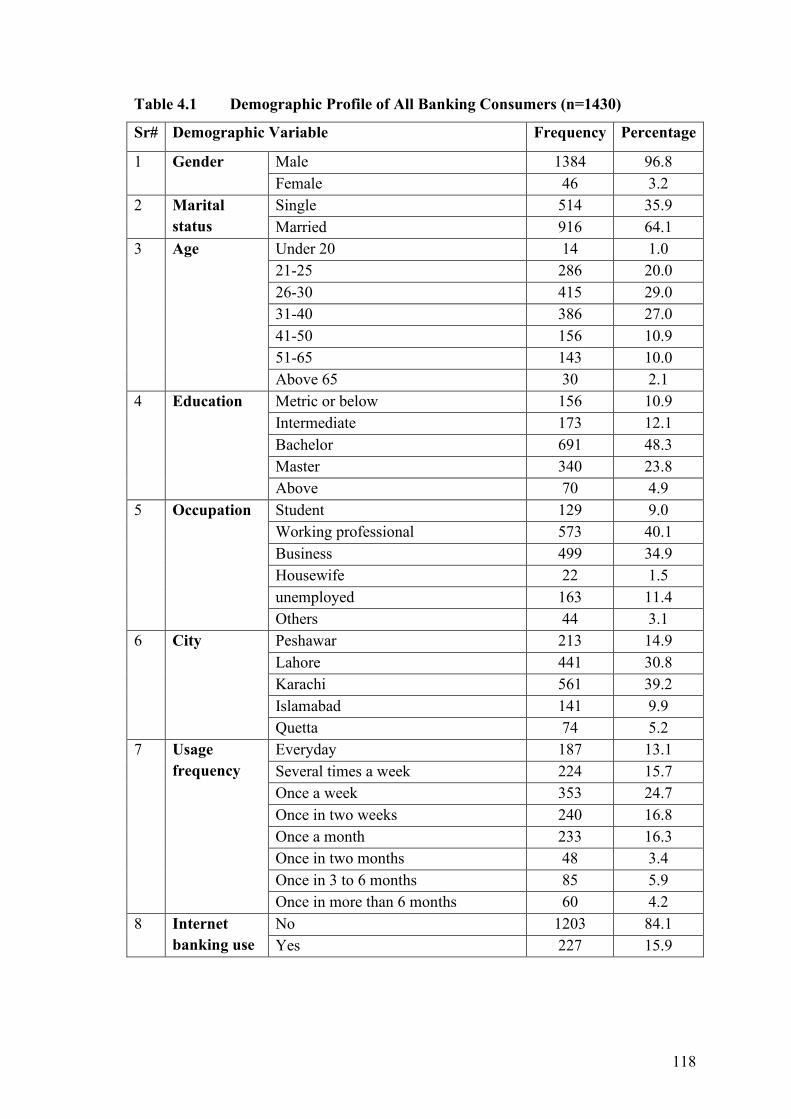

4.1 Chapter overview .............................................................................................. 116 4.2 Demographic profile of participants ................................................................. 116

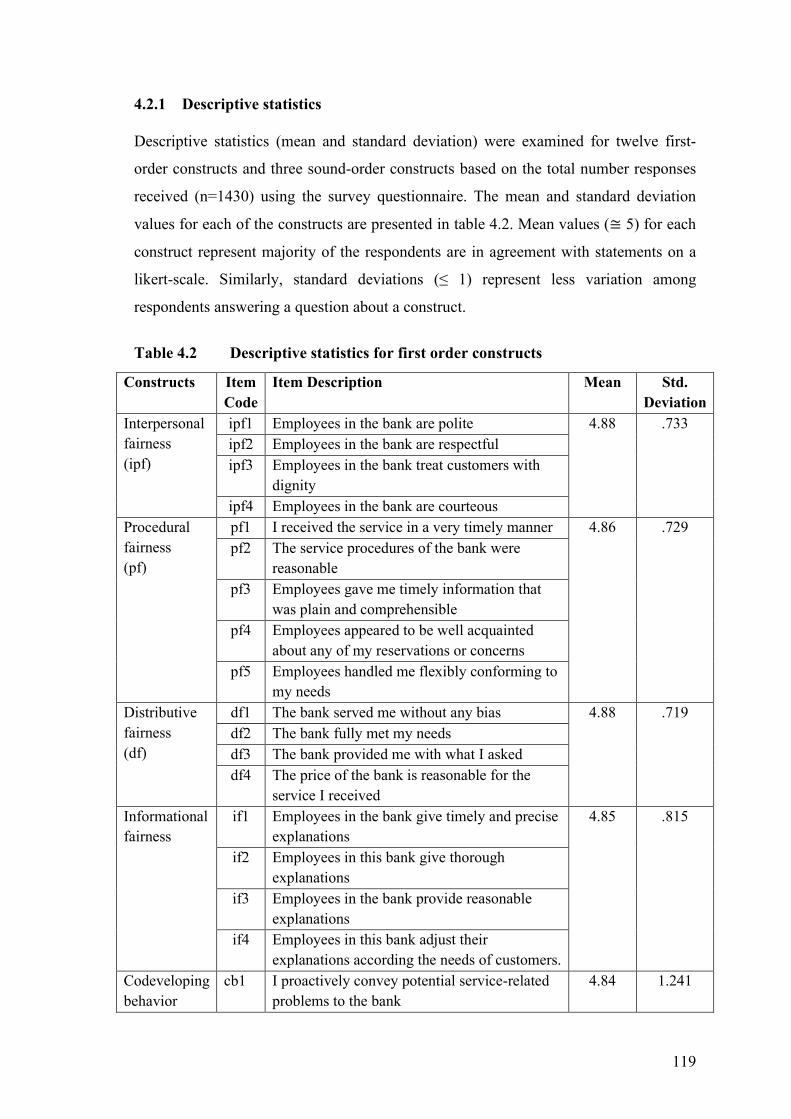

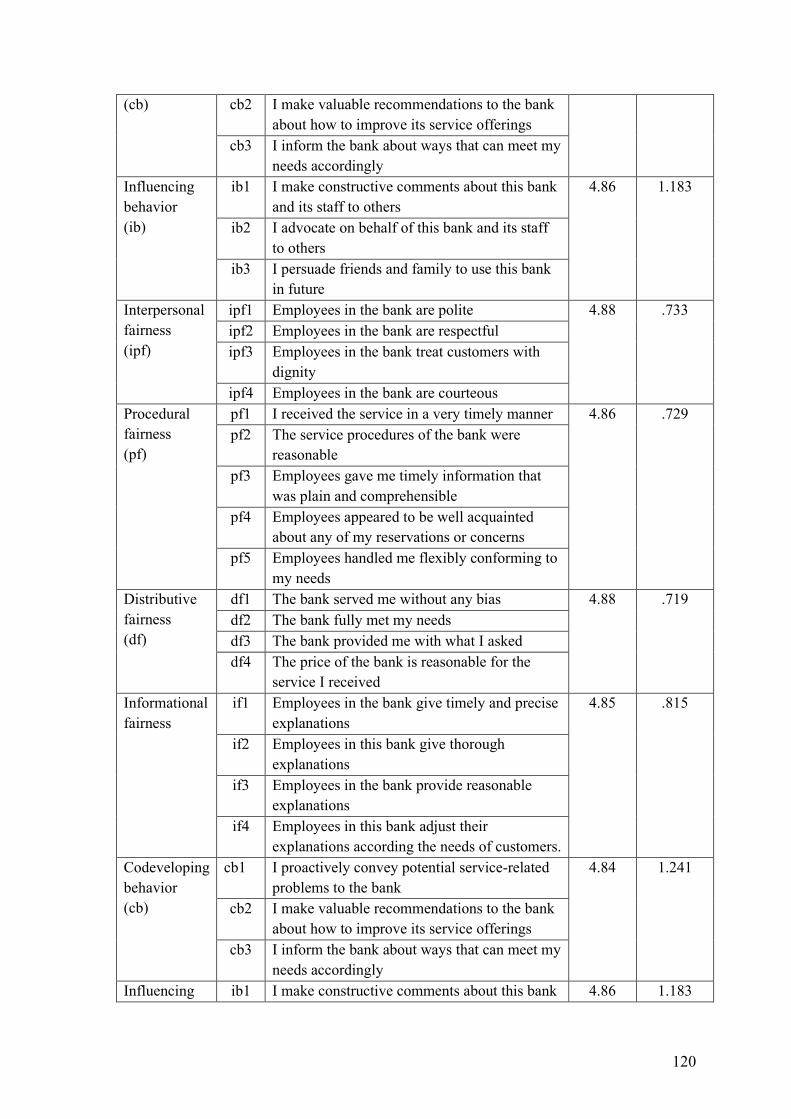

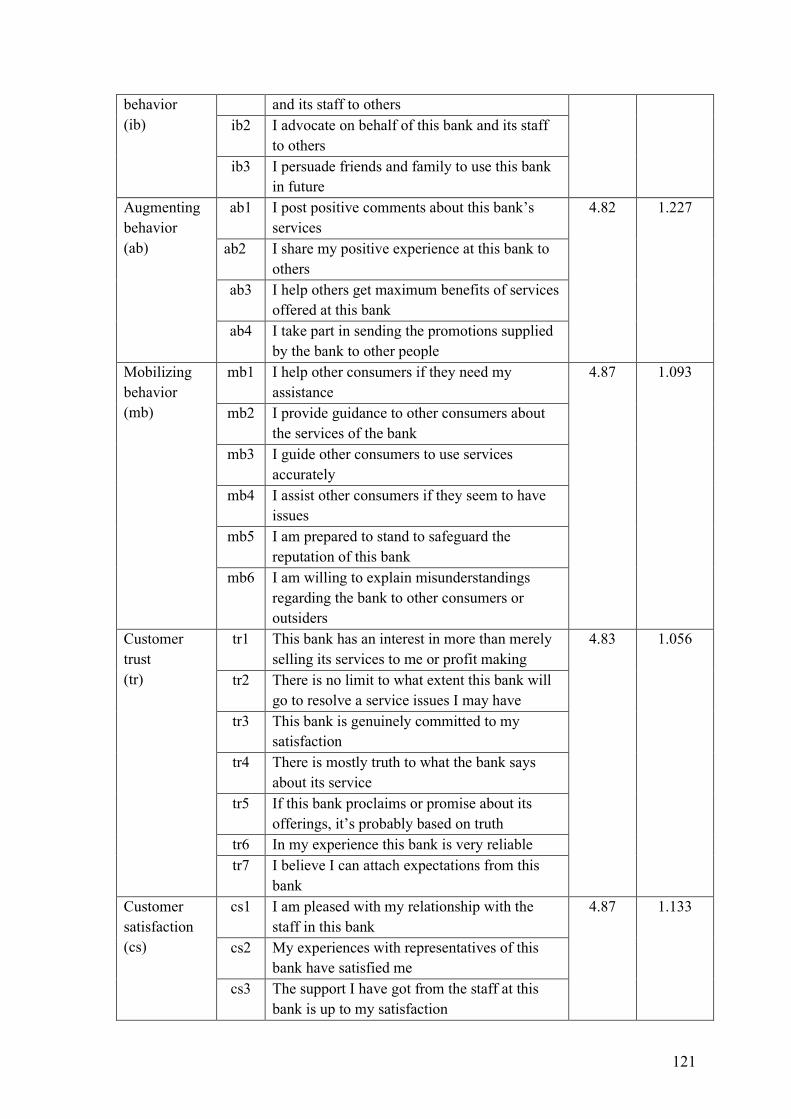

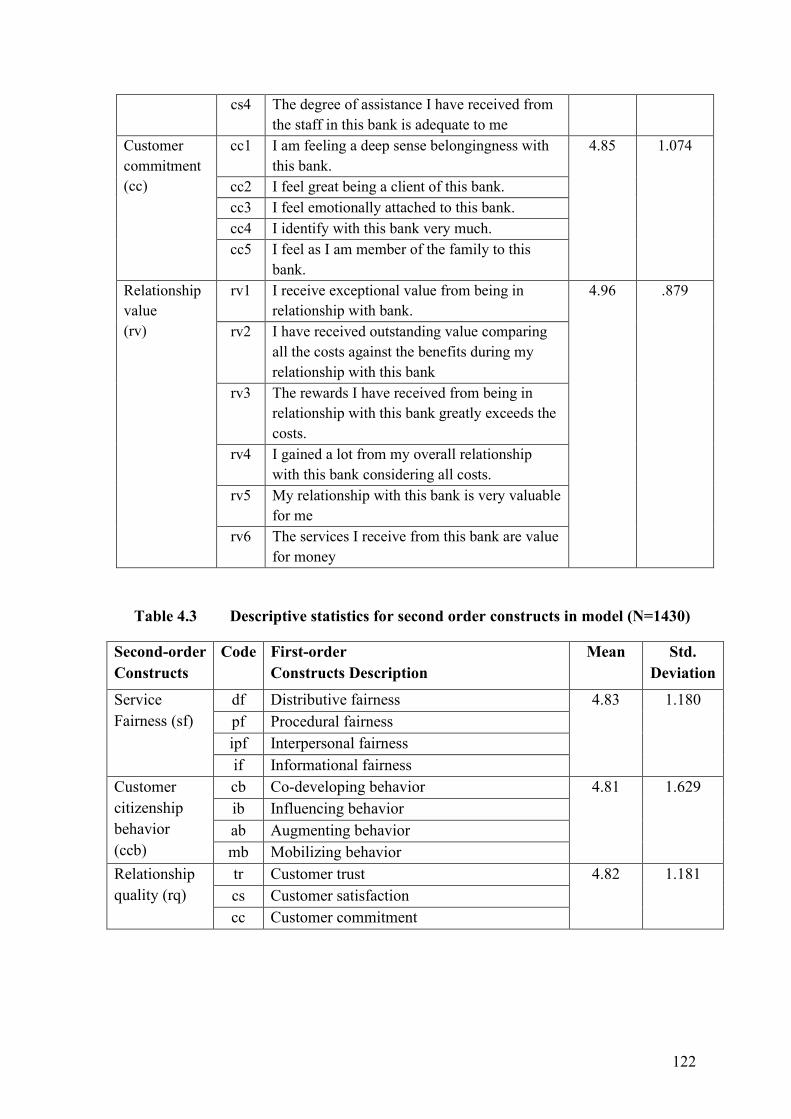

4.2.1 Descriptive statistics .................................................................................. 119

4.3 Data analysis ..................................................................................................... 123

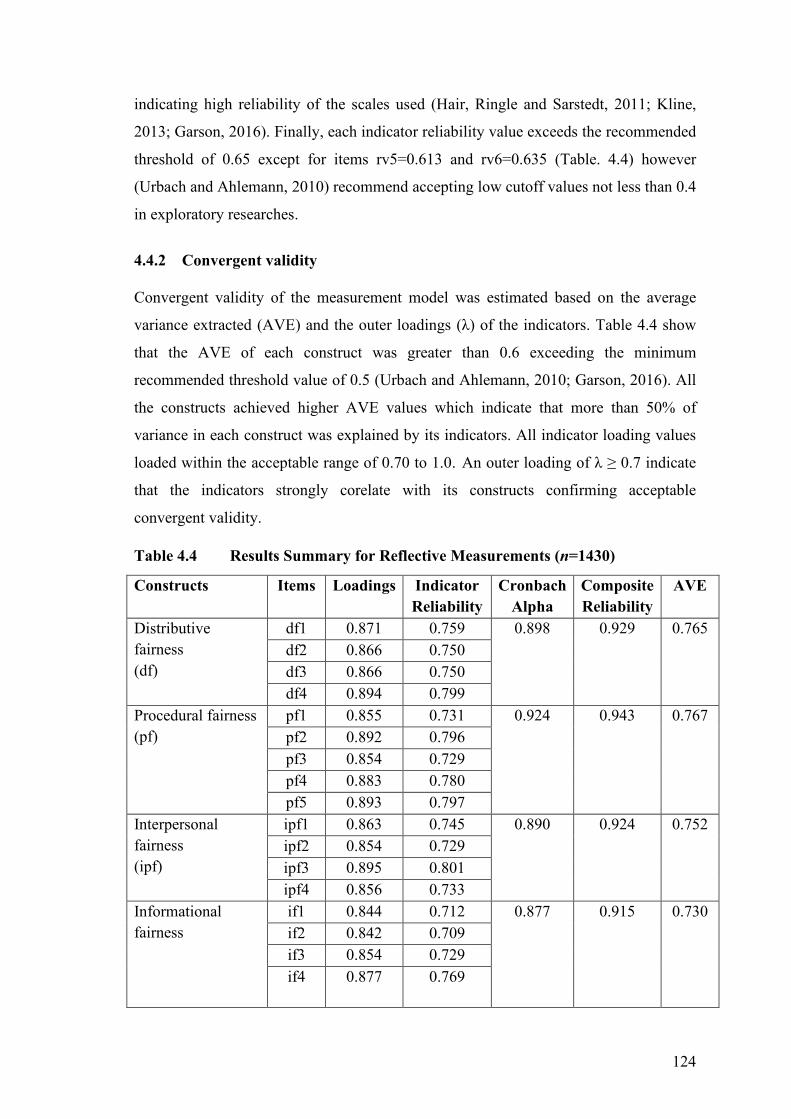

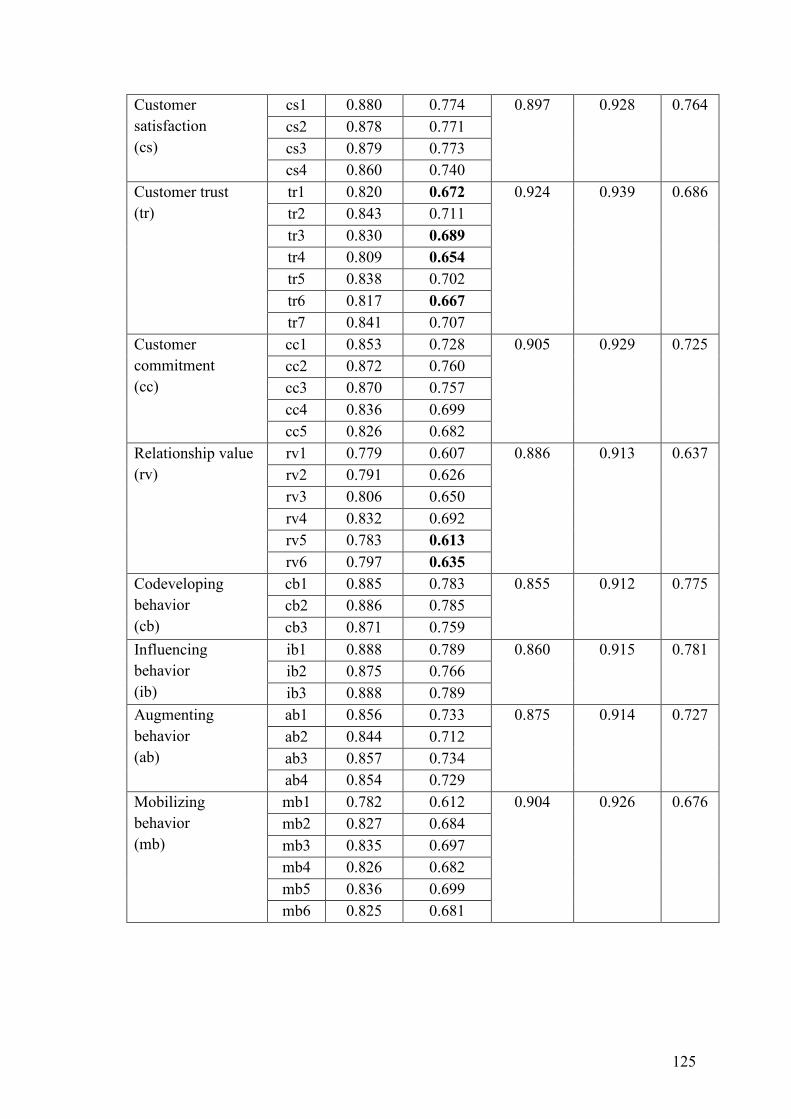

4.4 Measurement model assessment ....................................................................... 123 4.4.1 Internal consistency reliability ................................................................... 123

4.4.2 Convergent validity .................................................................................... 124

4.4.3 Discriminant validity ................................................................................. 126

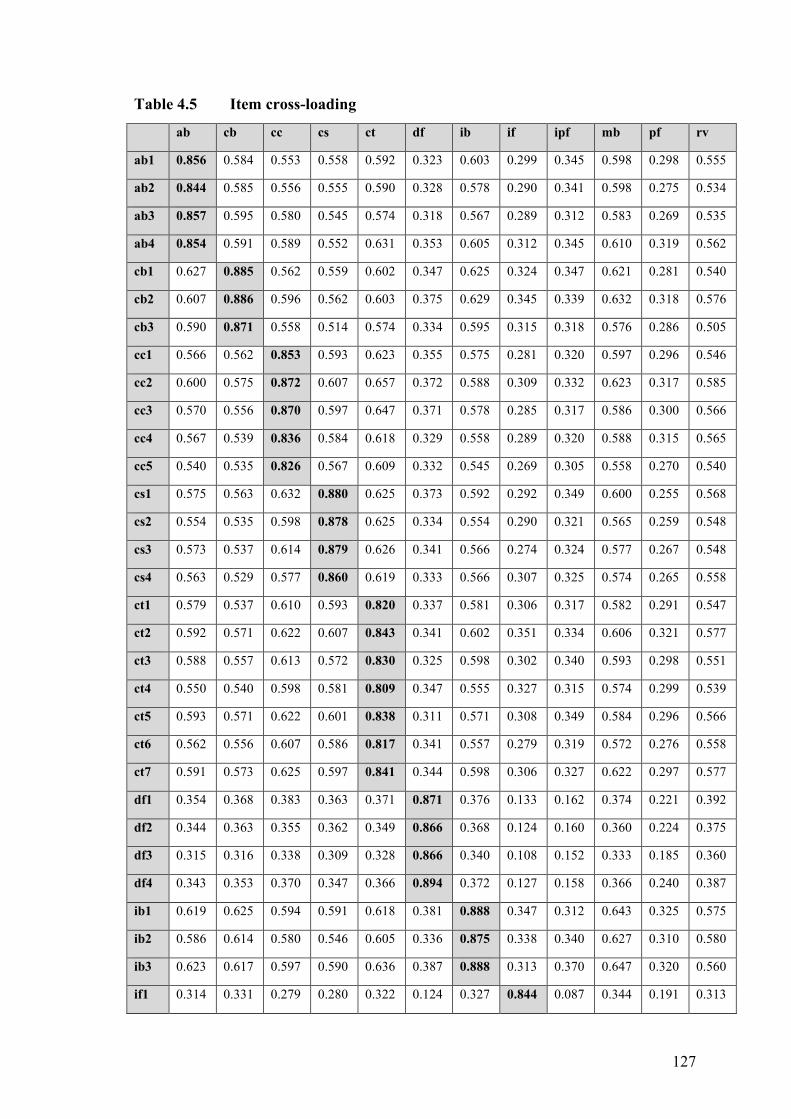

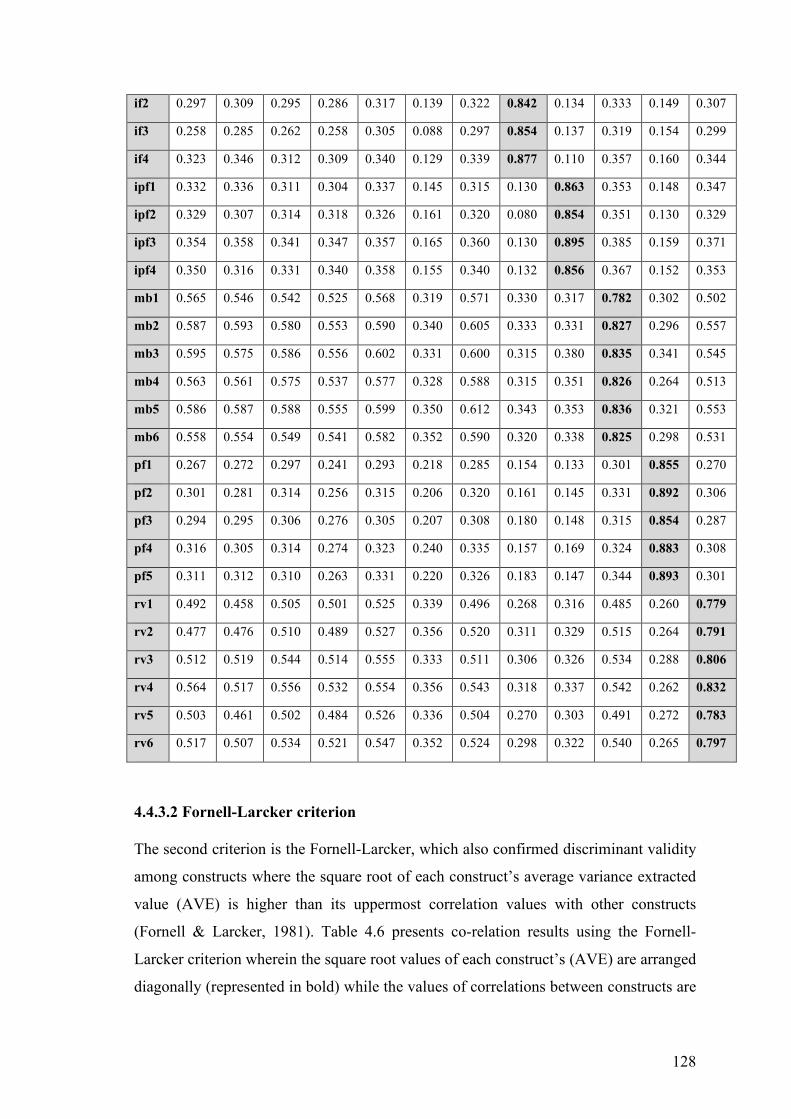

4.4.3.1 Item cross loadings ................................................................................... 126

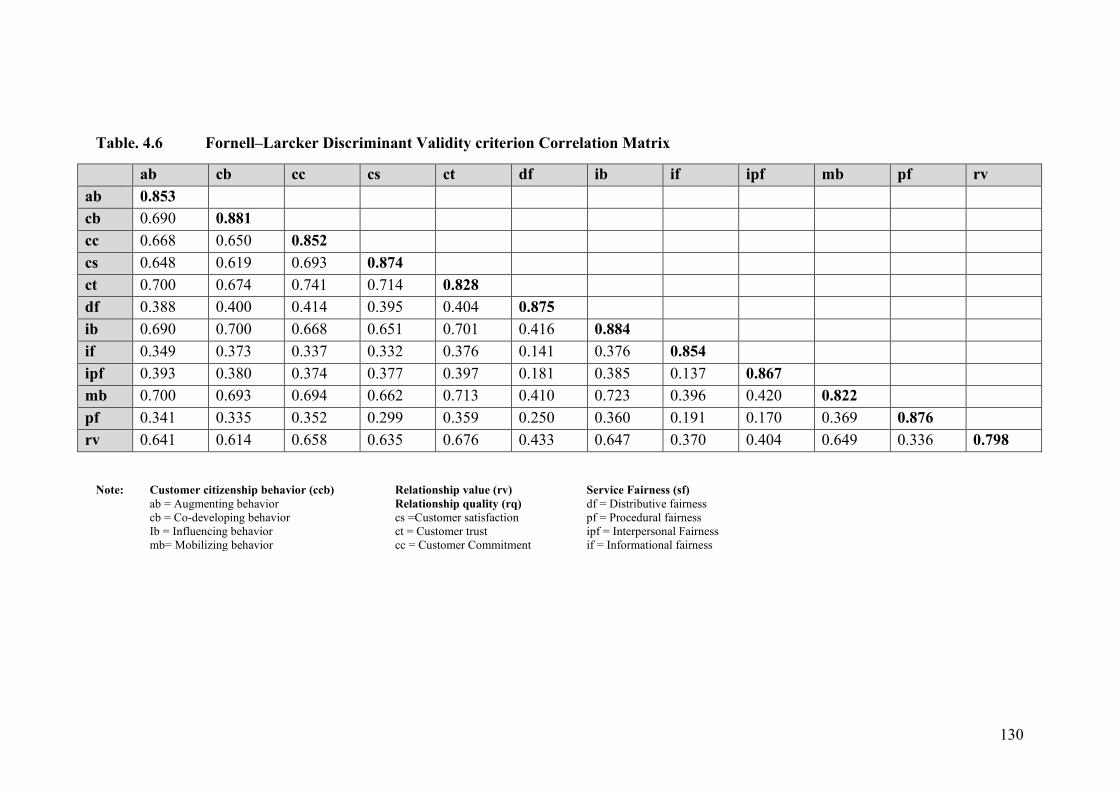

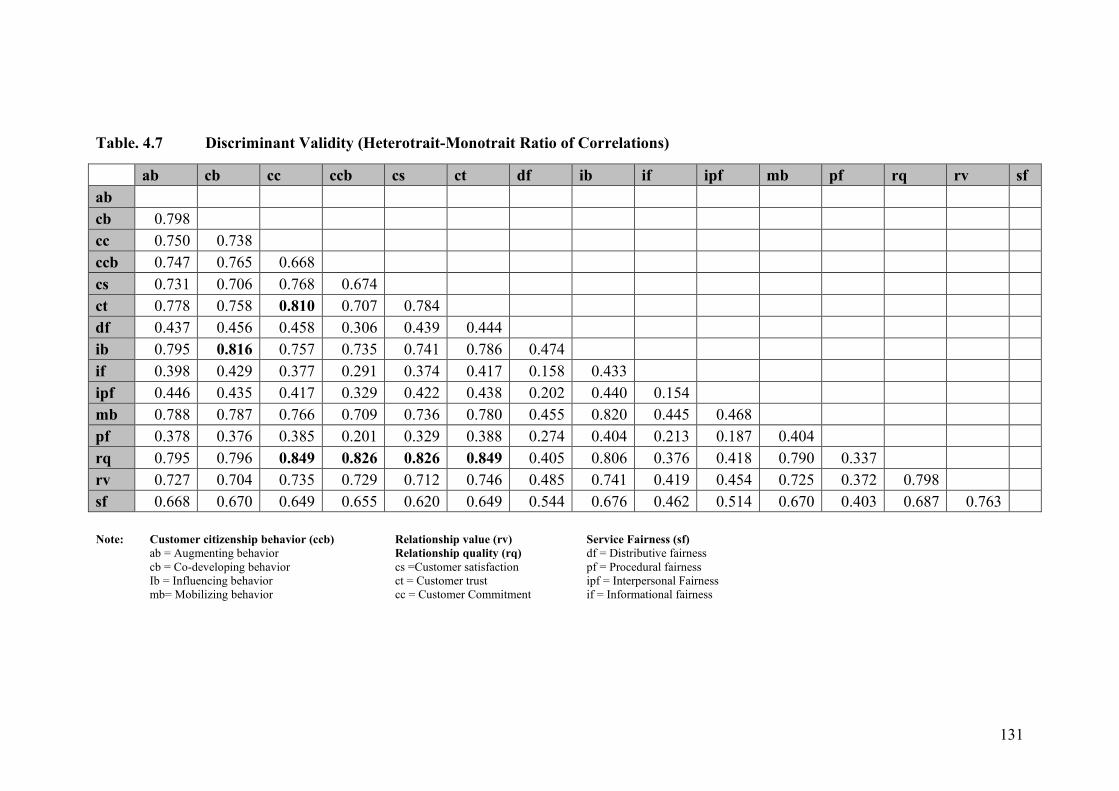

4.4.3.2 Fornell-Larcker criterion ........................................................................... 128 4.4.3.3 Heterotrait-monotrait ratio (HTMT) ......................................................... 129

4.5 Structural Model Evaluation ............................................................................. 132

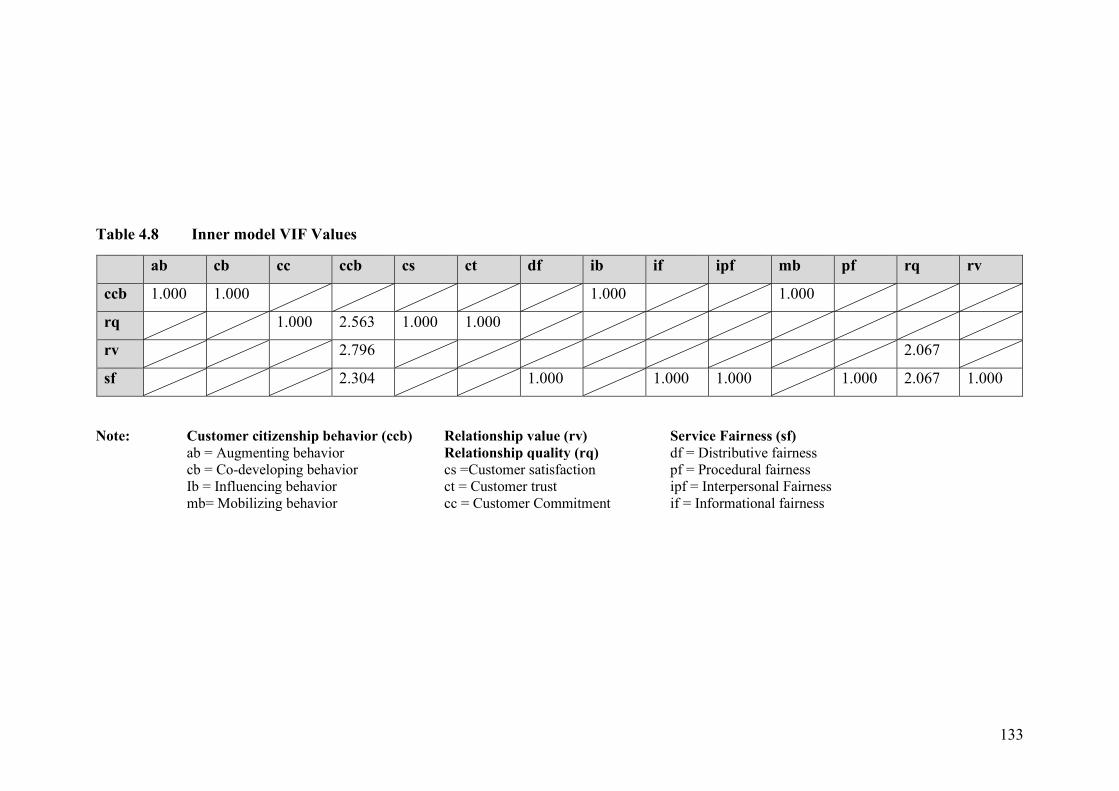

4.5.1 Multicollinearity Statistics ......................................................................... 132

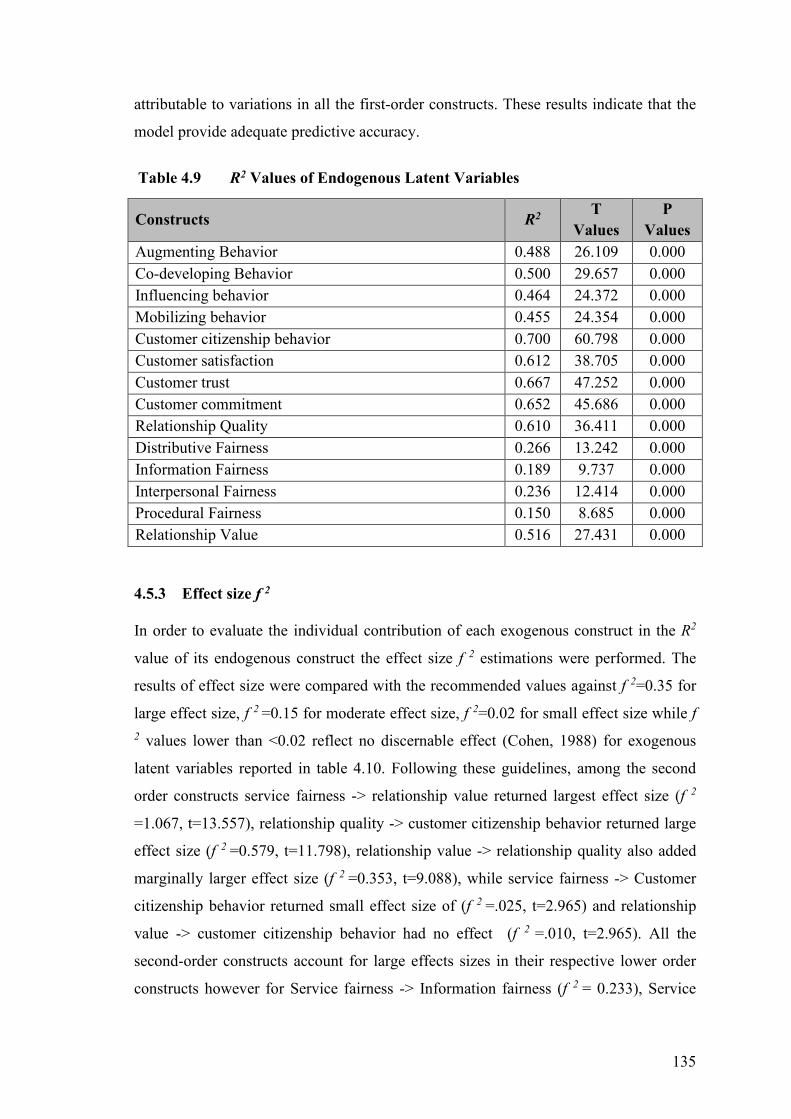

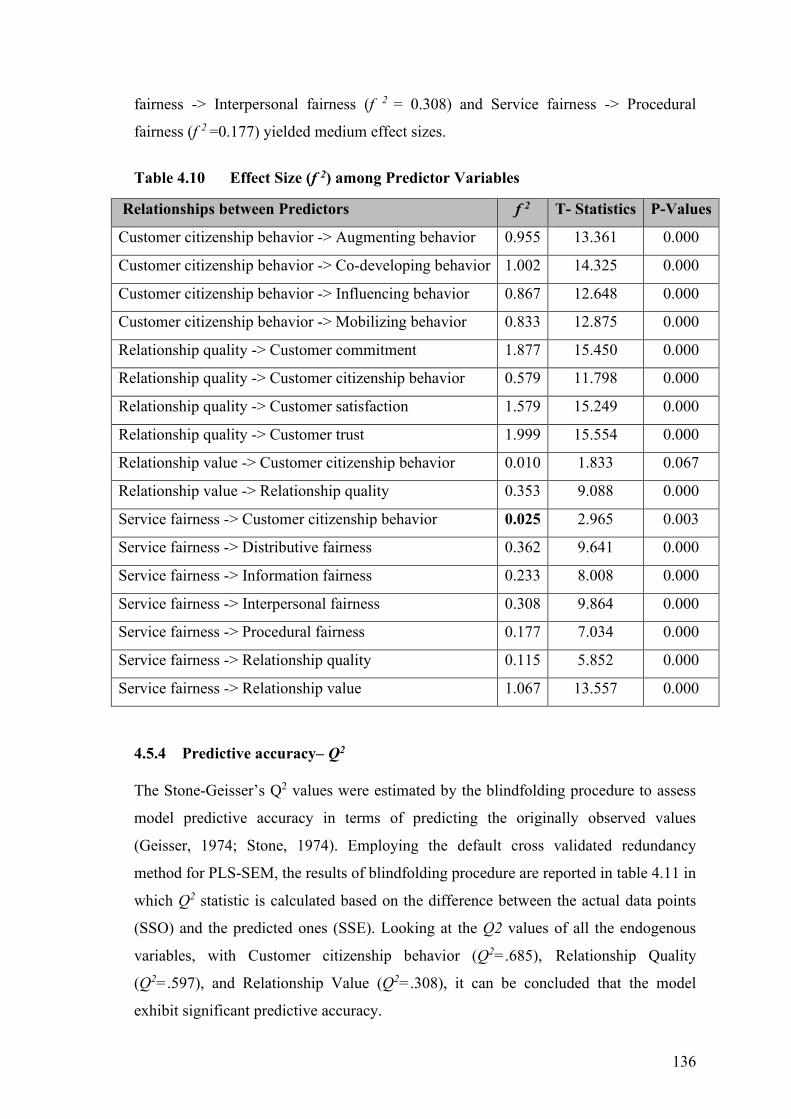

4.5.2 Overall Model Predictive Power (R2) ........................................................ 134 4.5.3 Effect size f 2 .............................................................................................. 135

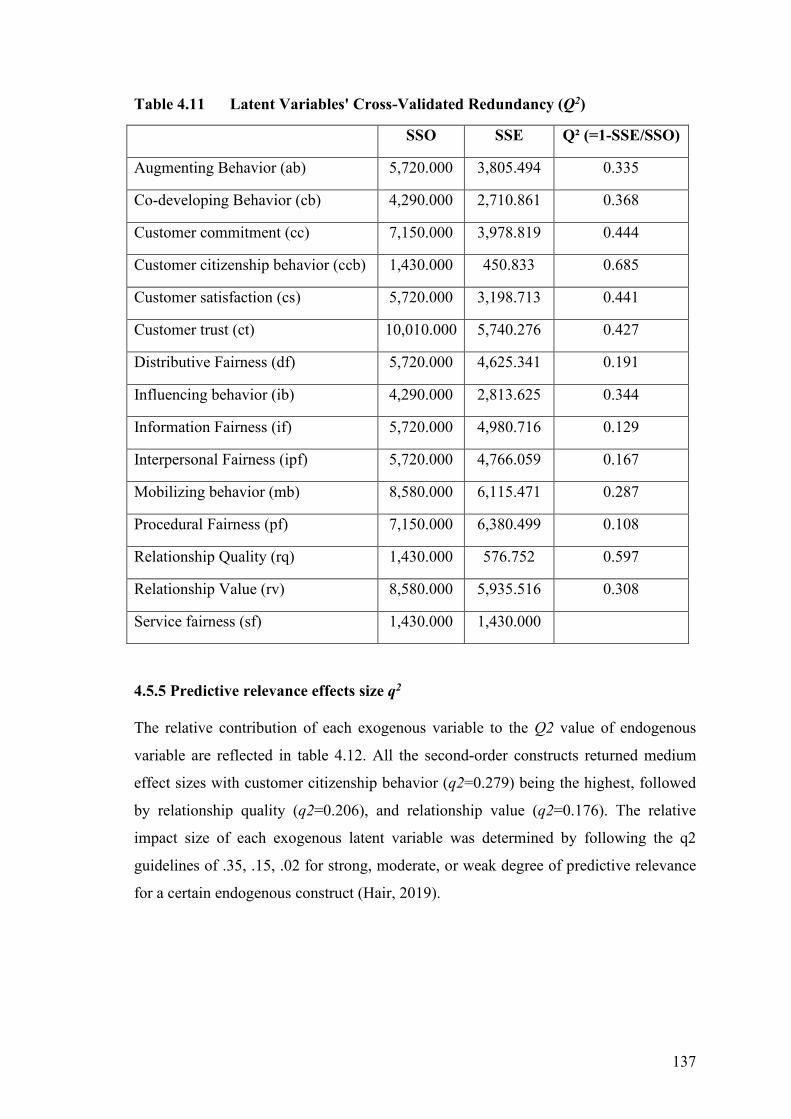

4.5.4 Predictive accuracy– Q2 ............................................................................. 136

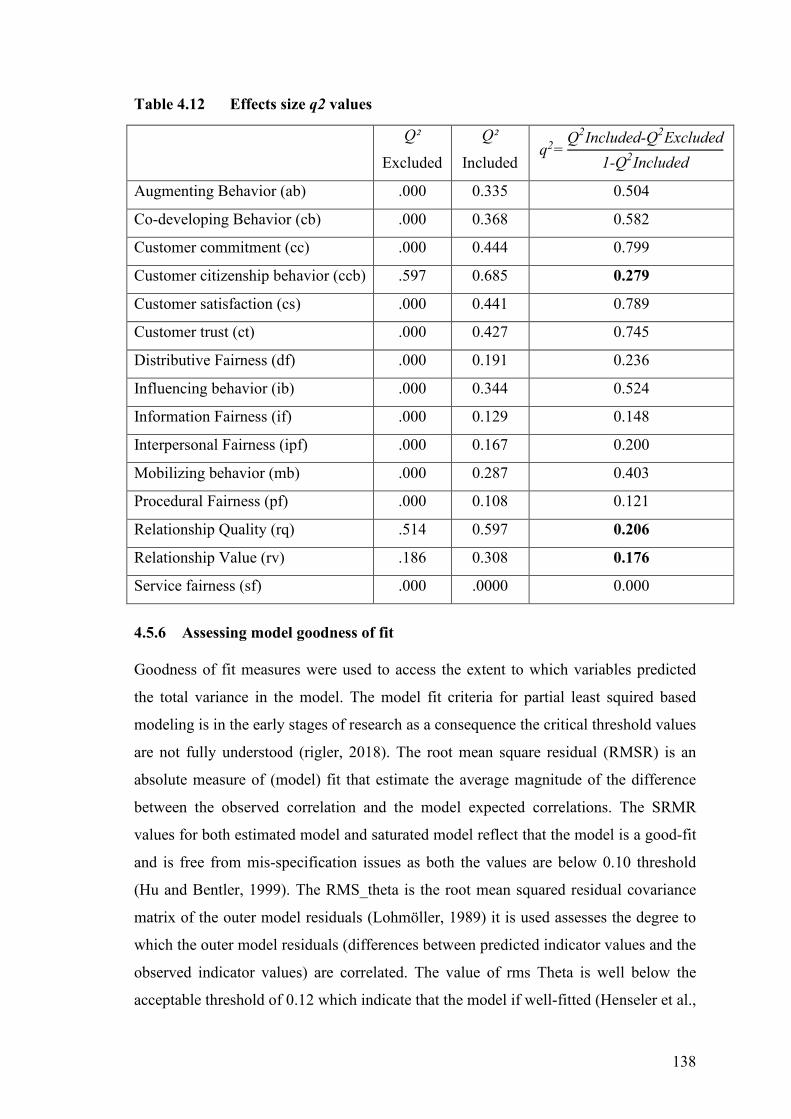

4.5.5 Predictive relevance effects size q2 ................................................................. 137

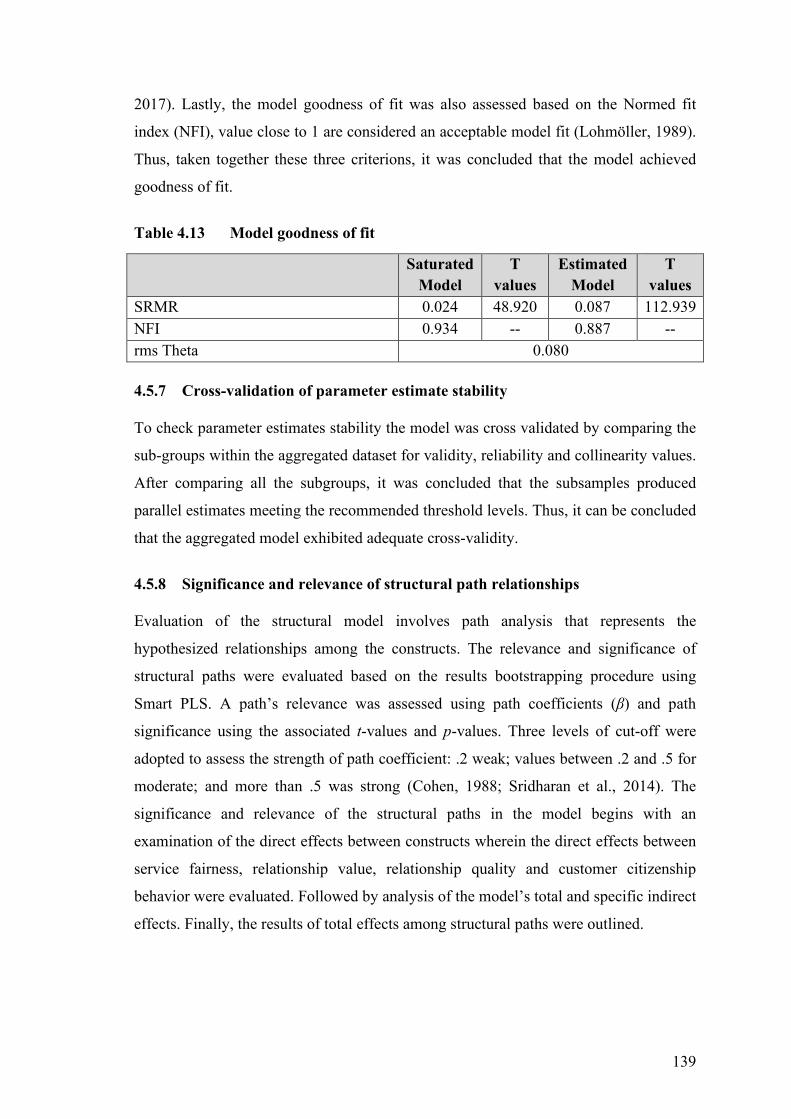

4.5.6 Assessing model goodness of fit ................................................................ 138 4.5.7 Cross-validation of parameter estimate stability ........................................ 139

4.5.8 Significance and relevance of structural path relationships ....................... 139

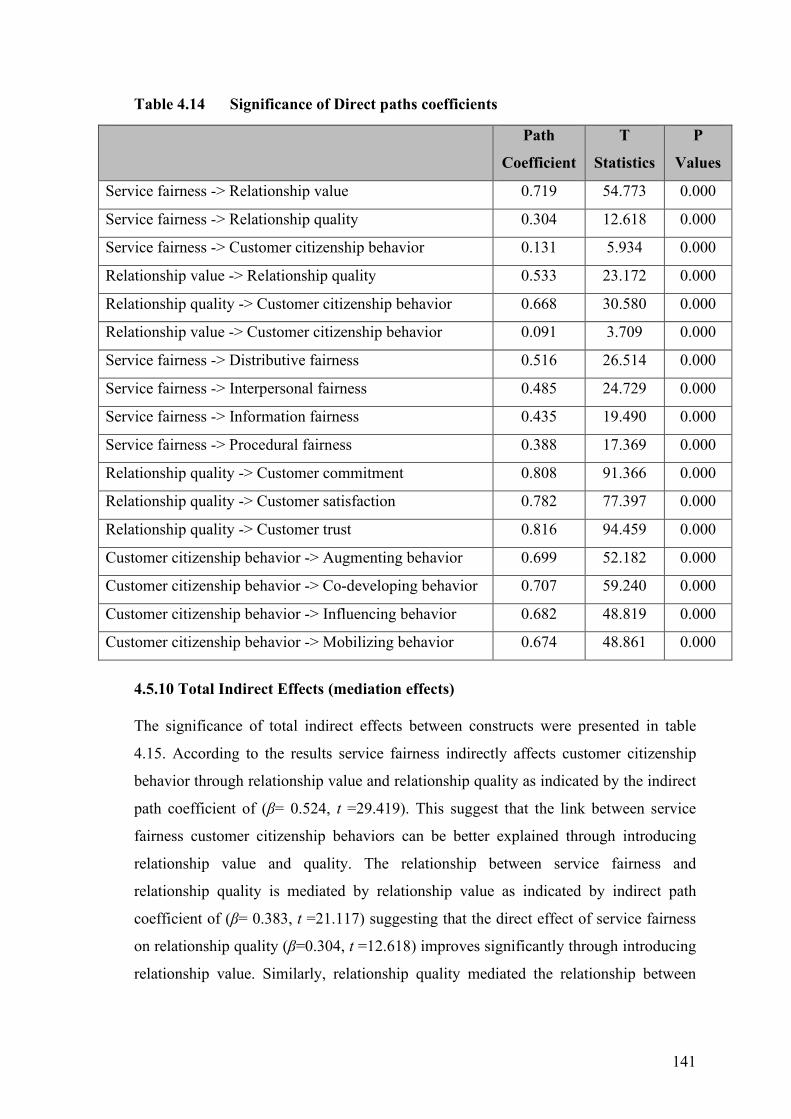

4.5.9 Direct effects .............................................................................................. 140

xiii

4.5.10 Total Indirect Effects (mediation effects) .................................................. 141

4.5.11 Specific indirect effects .............................................................................. 142

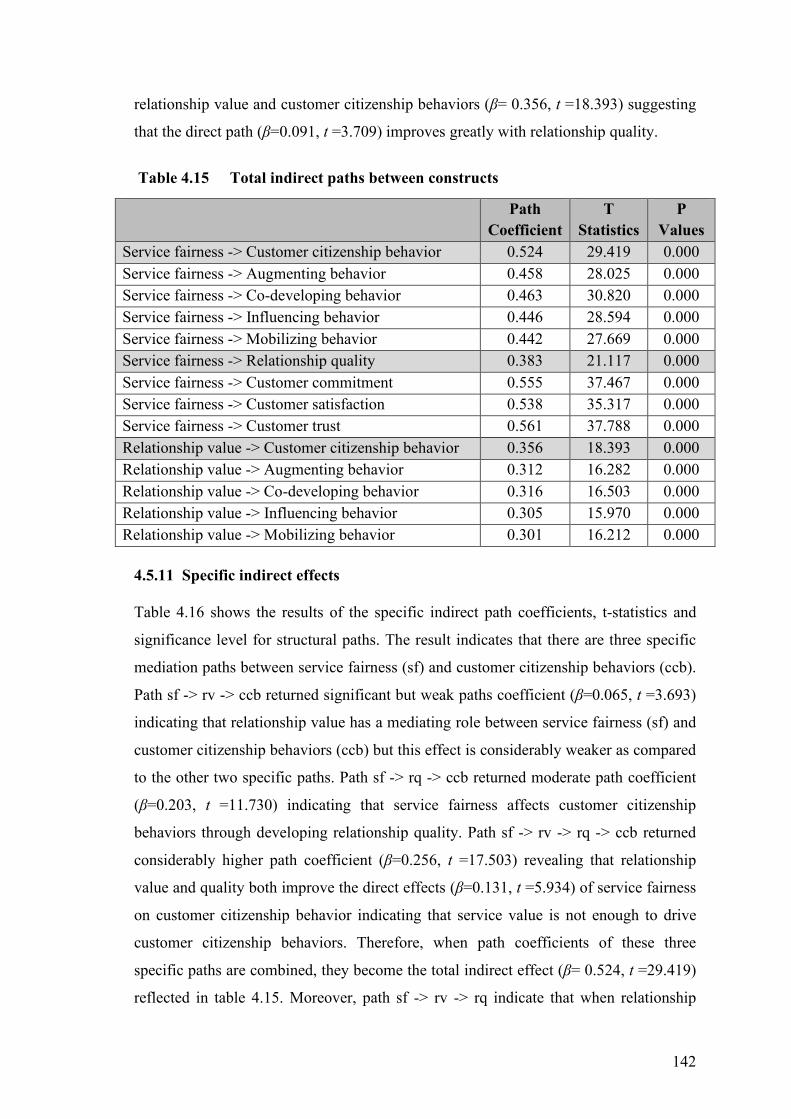

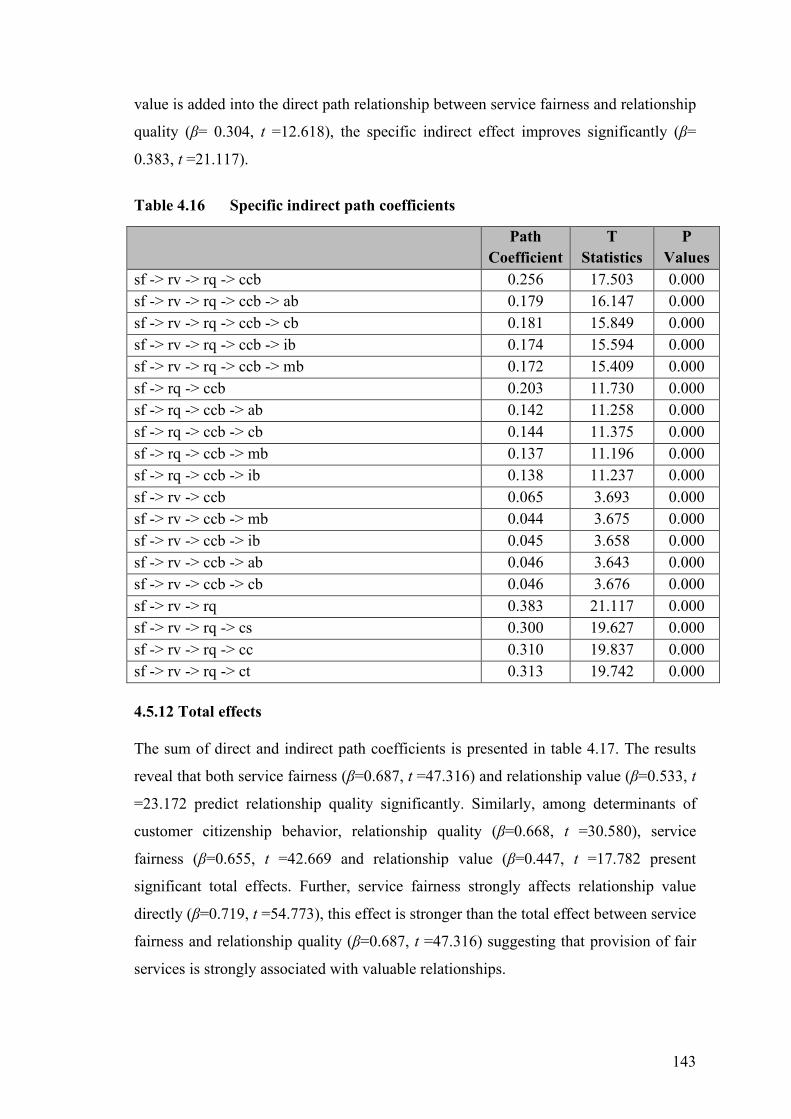

4.5.12 Total effects ............................................................................................... 143 4.5.13 Variance accounted for (VAF) by mediating variables ............................. 145

4.6 Hypotheses Validation summary ...................................................................... 147

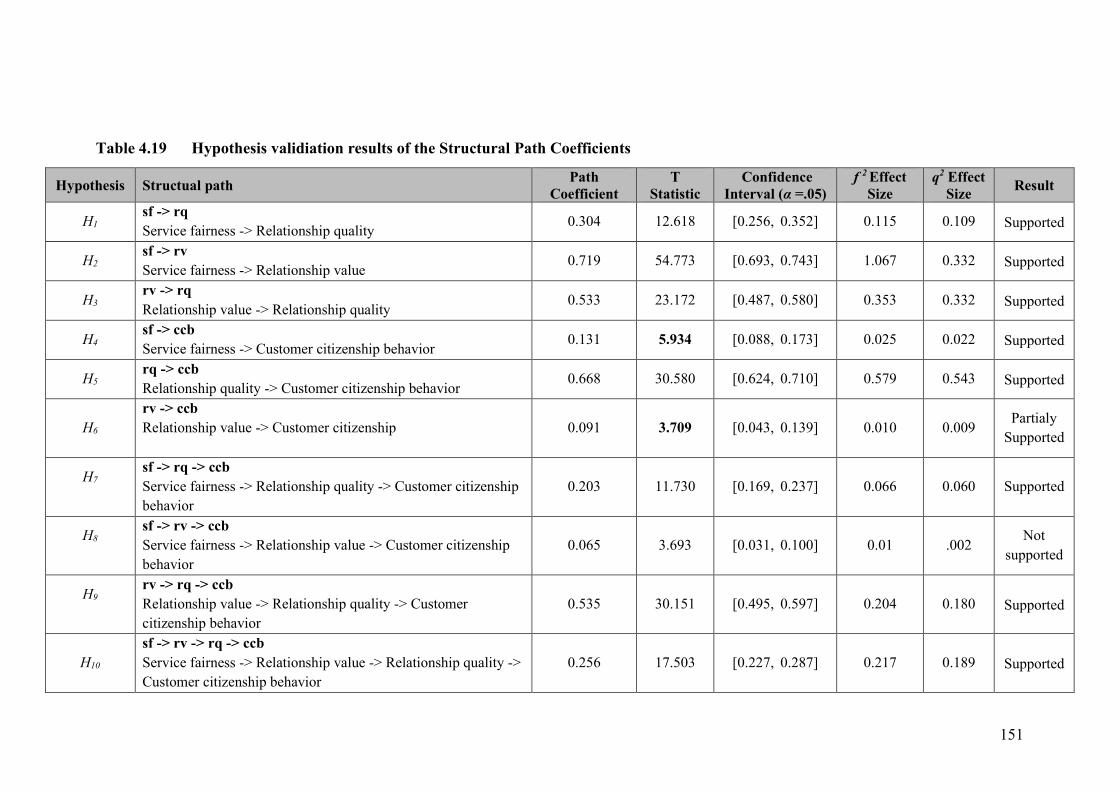

4.6.1 Service fairness and relationship quality ................................................... 147

4.6.2 Service fairness and relationship value ...................................................... 148 4.6.3 Relationship value and relationship quality ............................................... 148

4.6.4 Service fairness and customer citizenship behavior .................................. 148

4.6.5 Relationship quality and customer citizenship behavior............................ 148

4.6.6 Relationship value and customer citizenship behavior .............................. 148 4.6.7 Service fairness, relationship quality and customer citizenship behavior . 149

4.6.8 Service fairness, relationship value and customer citizenship behavior .... 149

4.6.9 Relationship value, relationship quality and customer citizenship behavior ... .................................................................................................................... 149

4.6.10 Relationship between service fairness, relationship value, relationship quality and customer citizenship behaviors .............................................. 150

4.7.1 Introduction ................................................................................................ 156 4.7.2 Data analysis .............................................................................................. 156

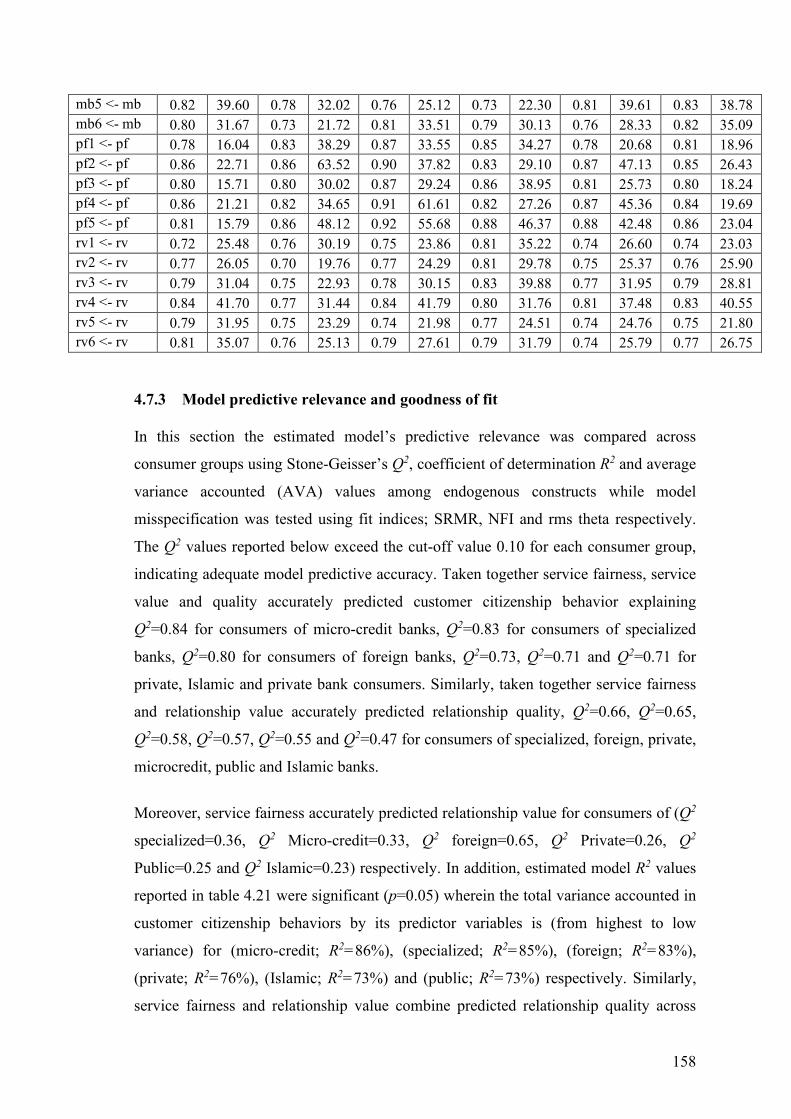

4.7.3 Model predictive relevance and goodness of fit ........................................ 158

4.7.4 Structural paths across consumer groups ................................................... 161

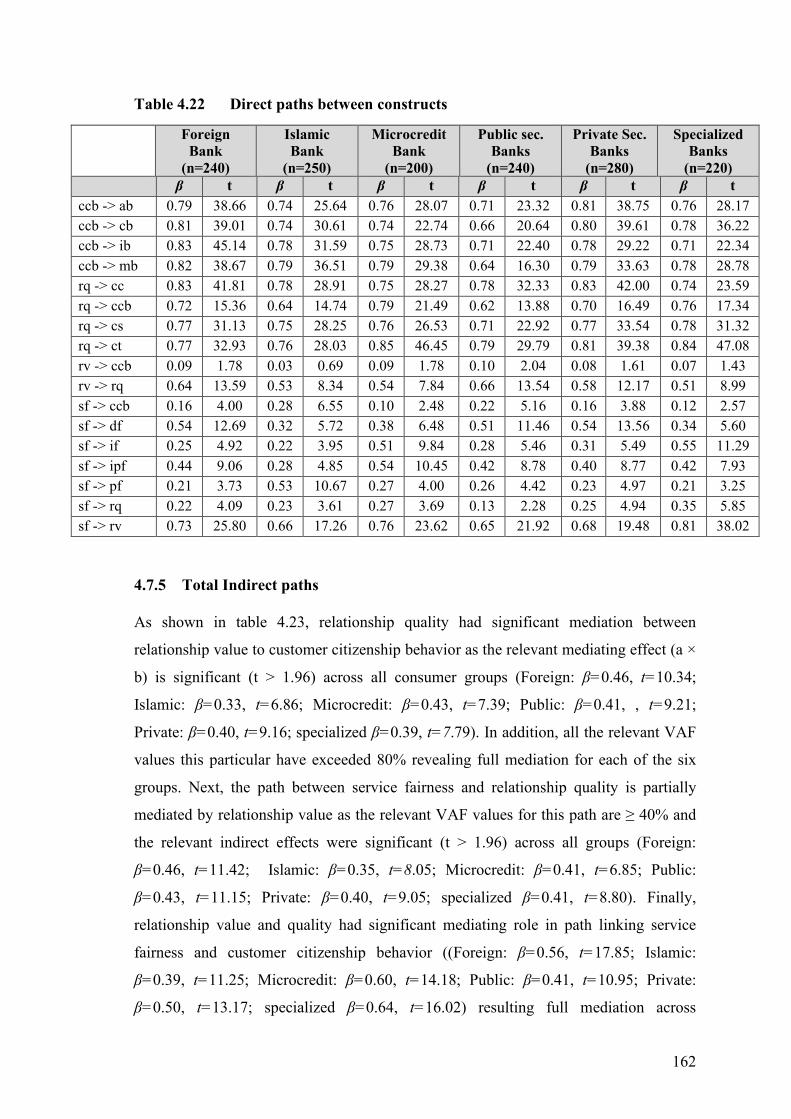

4.7.5 Total Indirect paths .................................................................................... 162 4.7.6 Specific Indirect paths ................................................................................ 163

4.8 Invariance testing- MICOM .............................................................................. 164

4.8.1 Configural invariance (step 1) ................................................................... 164

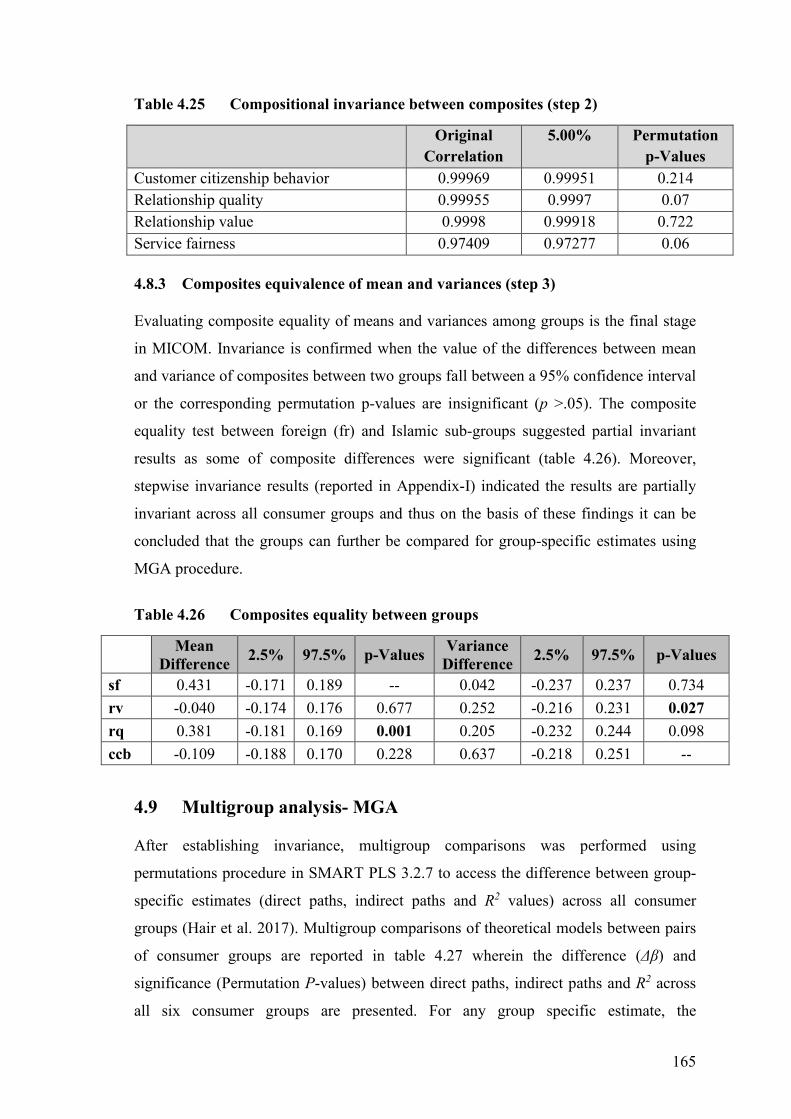

4.8.2 Compositional invariance (step 2) ............................................................. 164 4.8.3 Composites equivalence of mean and variances (step 3) ........................... 165

4.9 Multigroup analysis- MGA ............................................................................... 165

4.9.1 Foreign vs Islamic bank consumers ........................................................... 166

4.9.2 Foreign vs micro credit bank consumers ................................................... 167

4.9.3 Foreign vs public sector bank consumers .................................................. 167 4.9.4 Foreign vs private sector bank consumers ................................................. 168

4.9.5 Foreign vs specialized bank consumers ..................................................... 169

4.9.6 Islamic vs microcredit bank consumers ..................................................... 170

4.9.7 Islamic vs public sector bank consumers ................................................... 171

xiv

4.9.8 Islamic vs private sector bank consumers .................................................. 171

4.9.9 Islamic vs specialized bank consumers ...................................................... 172

4.9.10 Microcredit vs public sector bank consumers ............................................ 173 4.9.11 Microcredit vs private sector bank consumers ........................................... 173

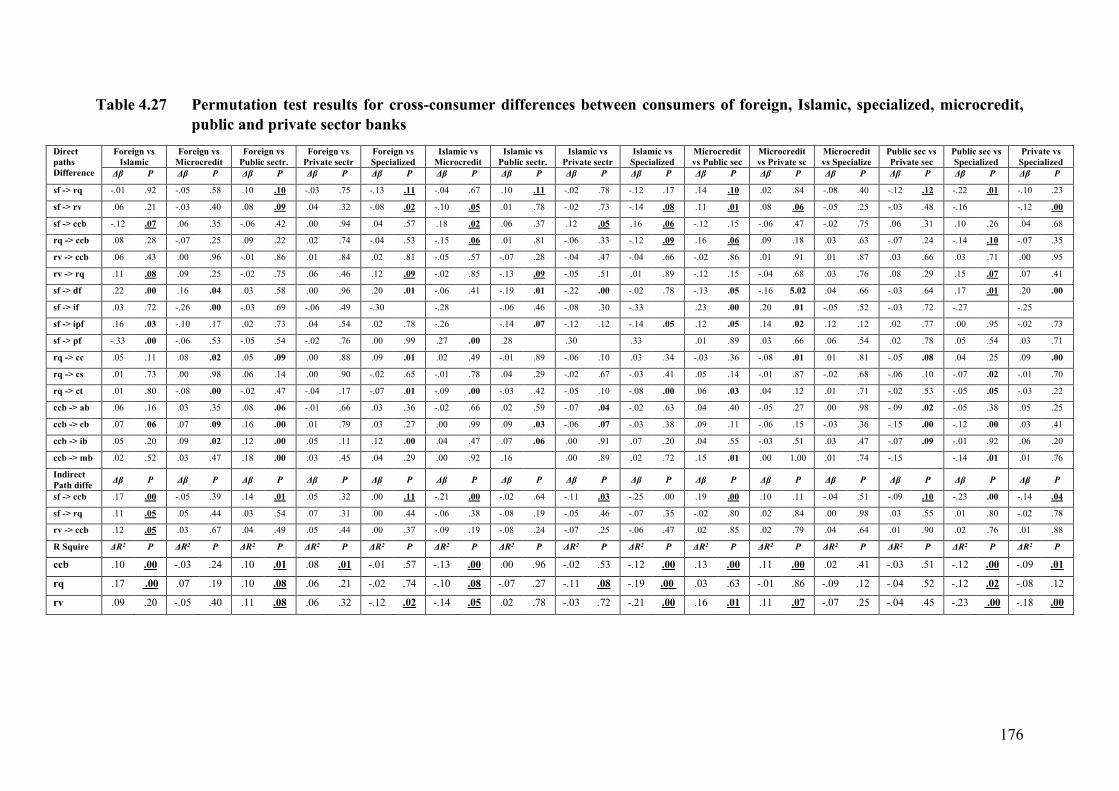

4.9.12 Microcredit vs Specialized bank consumers .............................................. 174

4.9.13 Pubic vs Private sector bank consumers .................................................... 174

4.9.14 Public vs Specialized bank consumers ...................................................... 174 4.9.15 Private sector vs Specialized bank consumers ........................................... 175

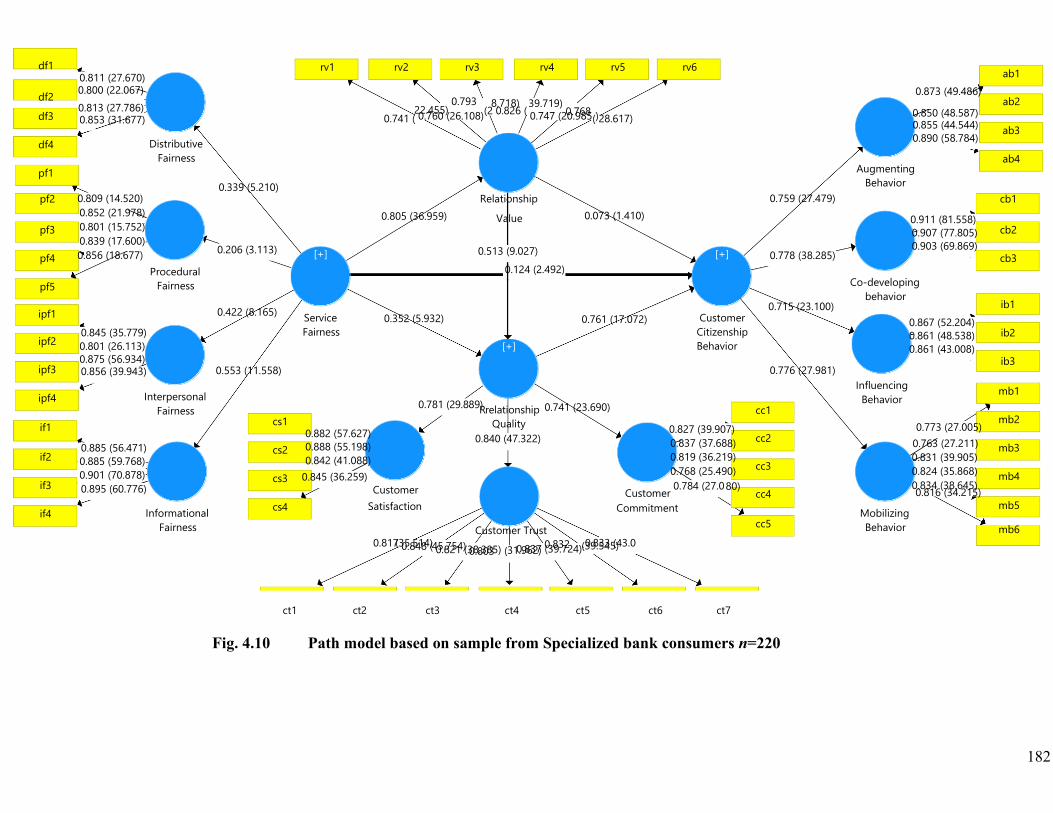

4.10 Summary of key findings .............................................................................. 183

4.10.1 The impact of service fairness on relationship value ................................. 183

4.10.2 The role of relationship value in relationship quality ................................ 183 4.10.3 The role of service fairness in relationship marketing ............................... 184

4.10.4 The role of relationship marketing in customer citizenship behaviors ...... 185

4.10.5 The impact of service fairness on customer citizenship behavior ............. 186

4.10.6 The relative importance of each dimension of service fairness in relationship building .................................................................................. 186

4.10.7 The importance of service fairness for relationship building and driving customer citizenship behaviors .................................................................. 187

Chapter 5 ...................................................................................................................... 188

CONCLUSION AND RECOMMENDATIONS ......................................................... 188

5.1 Chapter overview .............................................................................................. 188

5.2 Conclusion ........................................................................................................ 189 5.3 Theoretical implications .................................................................................... 194

5.4 Managerial implications .................................................................................... 197

5.4.1 Introduction ............................................................................................... 197

5.4.2 Distributive fairness ................................................................................... 198 5.4.3 Interpersonal fairness ................................................................................. 199

5.4.4 Information Fairness .................................................................................. 199

5.4.5 Procedural Fairness .................................................................................... 200

5.4.6 Training of contact personnel .................................................................... 201

5.4.7 Recruitment and selection appropriate individuals .................................... 201 5.4.8 Positioning the bank and its services based on fairness ............................. 202

5.4.9 Implications for practitioners ..................................................................... 202

5.4.10 Implications for policy with regard to consumer protection ...................... 203

5.4.11 Monitor and track perceptions about fairness ............................................ 204

xv

5.4.12 Encouraging customer citizenship behaviors ............................................. 204

5.4.13 Differential competitive advantage through achieving excellence in fair service delivery .......................................................................................... 205

5.5 Limitations and direction for future research .................................................... 205 REFERENCES ............................................................................................................. 208

Appendix- A ................................................................................................................. 234

Covering letter for participants of final survey ............................................................ 234

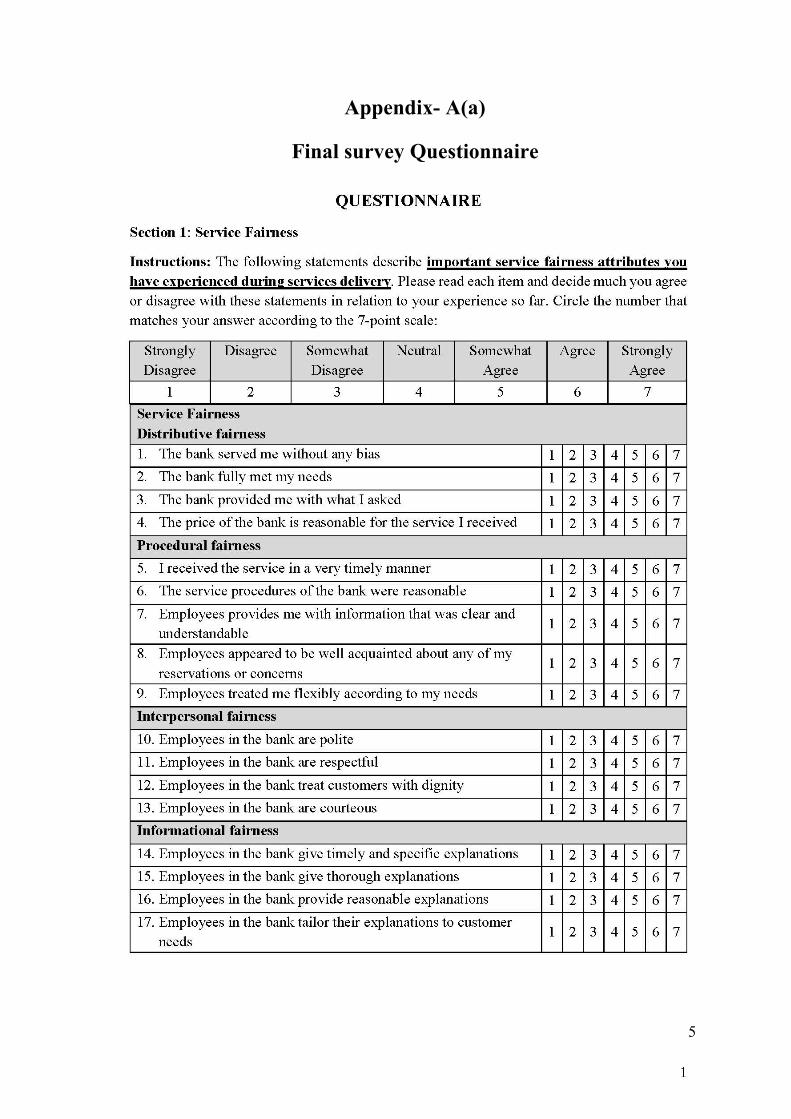

Appendix- A(a) ............................................................................................................ 235 Final survey Questionnaire ........................................................................................... 235

Appendix-B .................................................................................................................. 239

Translated version of Questionnaire ............................................................................ 239

Appendix- C ................................................................................................................. 244 Pilot Survey Invitation ................................................................................................. 244

Appendix- C (a) ............................................................................................................ 245

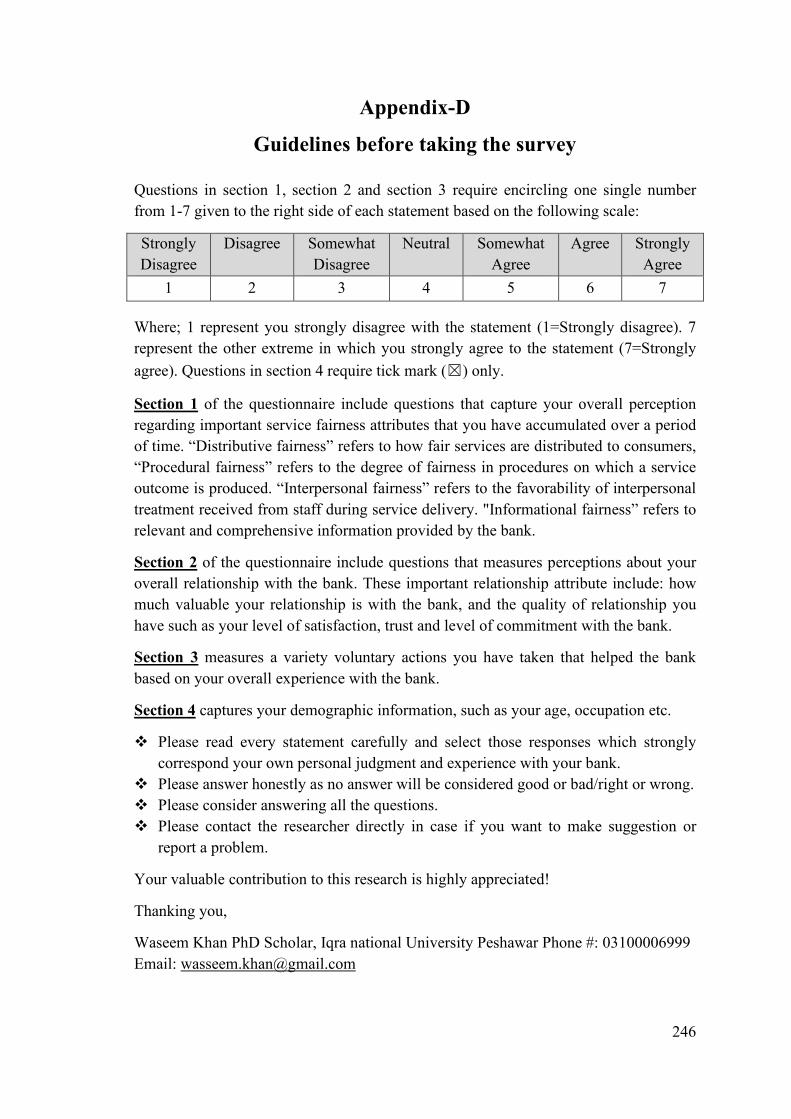

Appendix-D .................................................................................................................. 246

Guidelines before taking the survey ............................................................................. 246

Appendix- E ................................................................................................................. 248 Participation letter ........................................................................................................ 248

Appendix-F ................................................................................................................... 251

Pilot survey ................................................................................................................... 251

Appendix-G .................................................................................................................. 256 Pilot survey-Questionnaire feedback form ................................................................... 256

Appendix- H ................................................................................................................. 258

Results of Pilot Study (n=120) ..................................................................................... 258

xvi

LIST OF TABLES TABLE NO. TITLE PAGE NO.

3.1 Measurement and operationalization of study variables ............................... 72

3.2 Normality assessment of variables ................................................................ 108

3.2.1 Accessing normality assumptions using test statistic .................................... 106

3.3 Variable correlations ..................................................................................... 111

3.4 Assessing heteroscedasticity (OLS regression outputs) ................................ 113

3.4.1 Overall model fit (ANOVA) ......................................................................... 113

3.4.2 Breusch-Pagan and Koenker test statistics and sig-values ............................ 113

3.4 Research design activities ............................................................................ 114

3.7.4 Measurement Model Assessment .................................................................. 92

3.7.5 Structural Model Assessment ........................................................................ 103

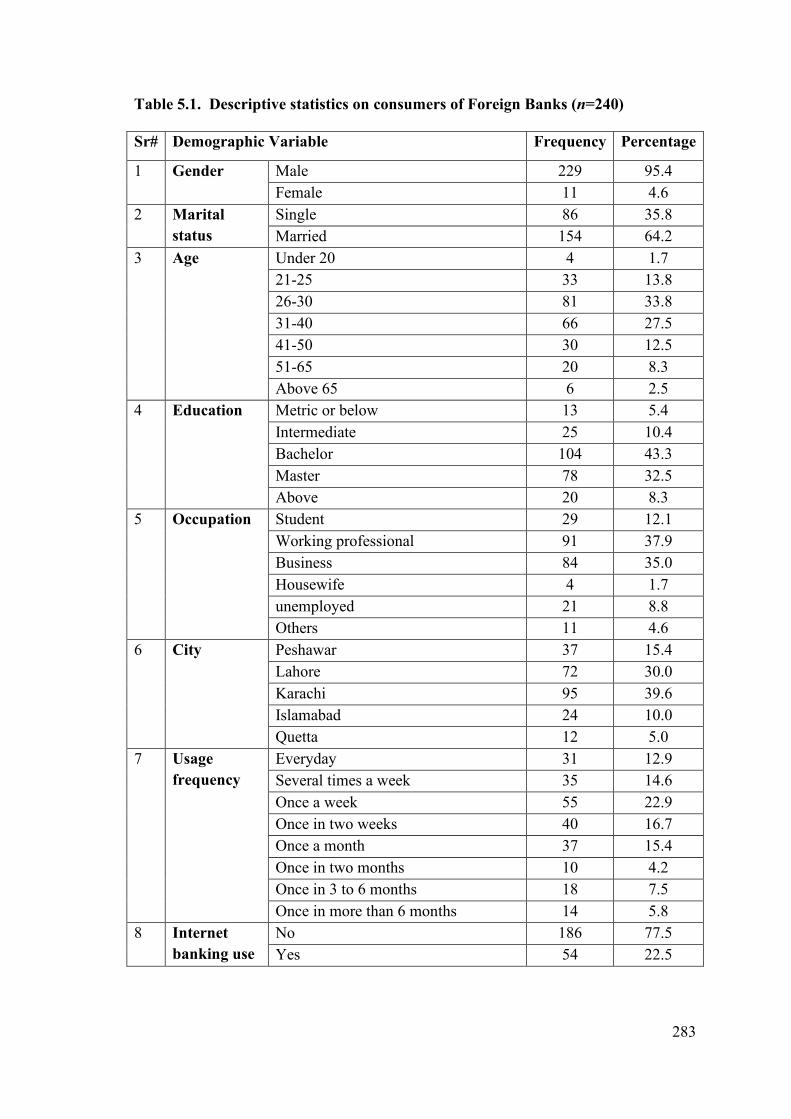

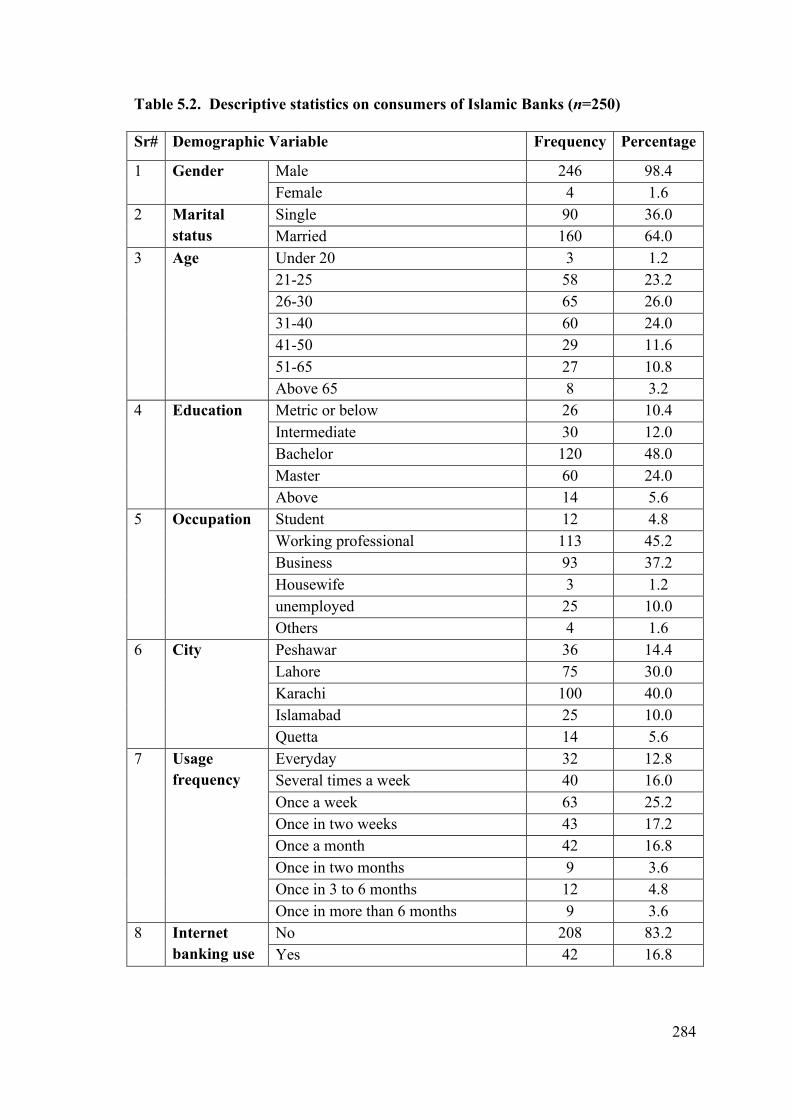

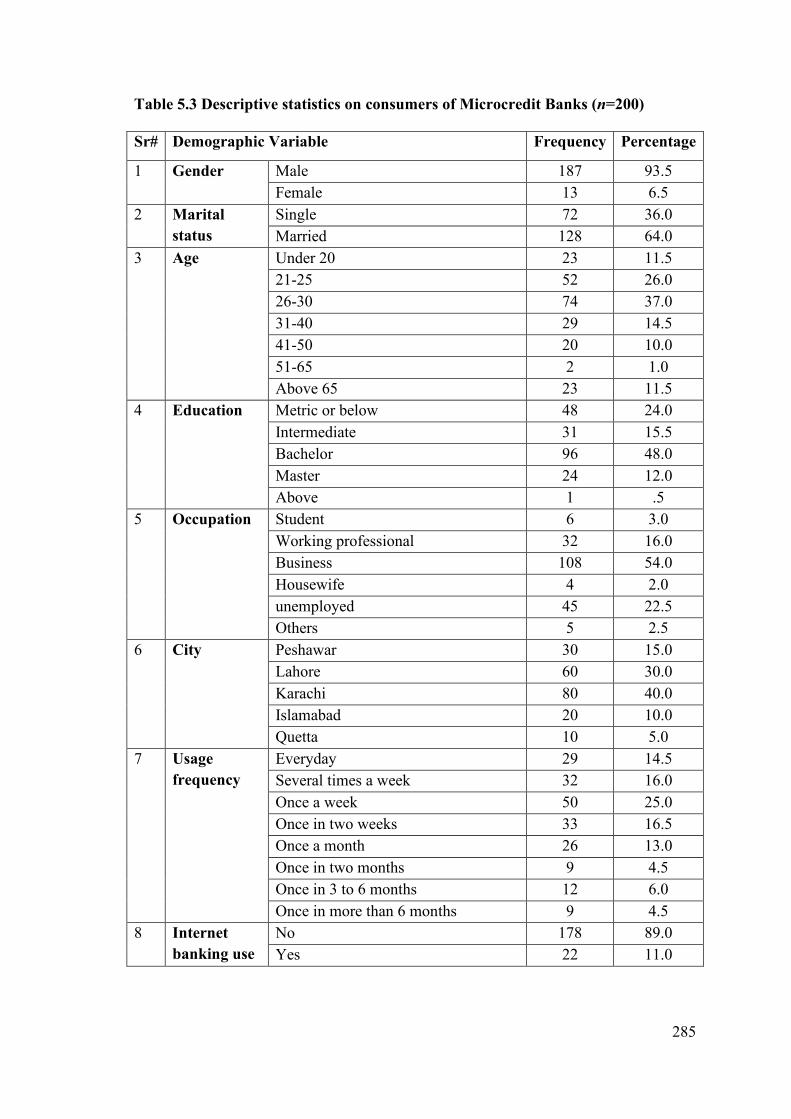

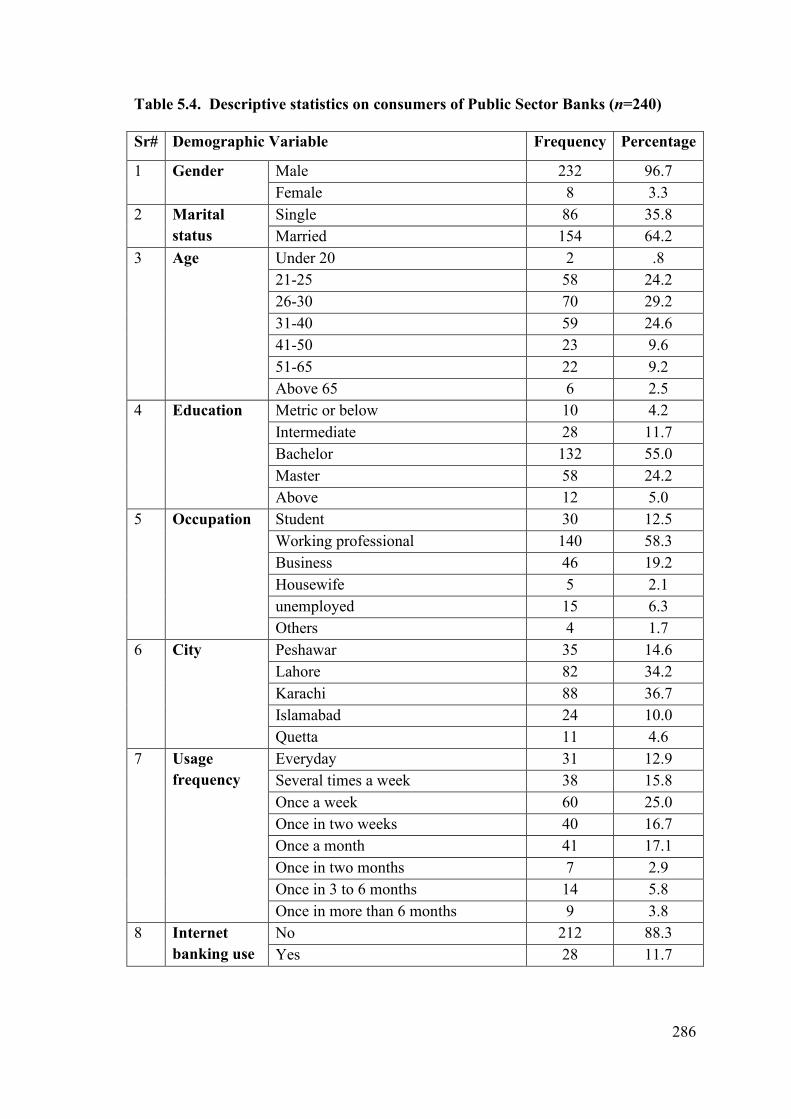

4.1 Demographic Profile of All Banking Consumers (n=1430) ......................... 118

4.2 Descriptive statistics for first order constructs ............................................. 119

4.3 Descriptive statistics for second order constructs in model (N=1430) ......... 120

4.4 Results Summary for Reflective Measurements (n=1430) ........................... 124

4.5 Item cross-loading ........................................................................................ 127

4.6 Correlation Matrix (Fornell-Larcker Criterion) Fornell–Larcker Discriminant Validity criterion ..................................................................... 130

4.7 Discriminant Validity (Heterotrait-Monotrait Ratio of Correlations) ........... 131

4.8 Inner model VIF Values ................................................................................ 133

4.9 R2 Values of Endogenous Latent Variables ................................................. 135

4.10 Effect Size (f 2) of the Predictor Variables .................................................... 136

4.11 Latent Variables' Cross-Validated Redundancy (Q2) .................................... 137

4.12 Effects size q2 values ................................................................................... 138

xvii

4.13 Model goodness of fit .................................................................................... 139

4.14 Significance of Direct path coefficients ....................................................... 141

4.15 Total indirect paths between constructs ....................................................... 142

4.16 Specific indirect path coefficients ............................................................... 143

4.17 Significance of total path coefficients between constructs .......................... 144

4.18 Variance accounted for values (VAF) .......................................................... 146

4.19 Hypothesis validiation results of the Structural Path Coefficients ................ 151

4.20 Constructs loading across types of banking consumers ................................ 157

4.21 Model fit indices across consumer groups .................................................... 160

4.22 Direct paths between constructs ................................................................... 162

4.23 Mediation effects between constructs across consumers groups .................. 163

4.24 Specific indirect effects and total variance accounted ................................. 164

4.25 Compositional invariance between composites (step 2) ............................... 165

4.26 Composites equality between groups ............................................................ 165

4.27 Permutation test results for cross-consumer differences between consumers of foreign, Islamic, specialized, microcredit, public and private sector banks ....................................................................................... 176

xviii

LIST OF FIGURES FIGURE NO. TITLE PAGE NO.

2.1 Relationship between proposed study variables ............................................ 52

3.1 A simple path model of PLS-SEM, (Hair et al., 2017) ................................. 80

3.2 Simple Mediation model ............................................................................... 93

4.1 Direct path relationship between Service Fairness and Customer citizenship behaviors ..................................................................................... 143

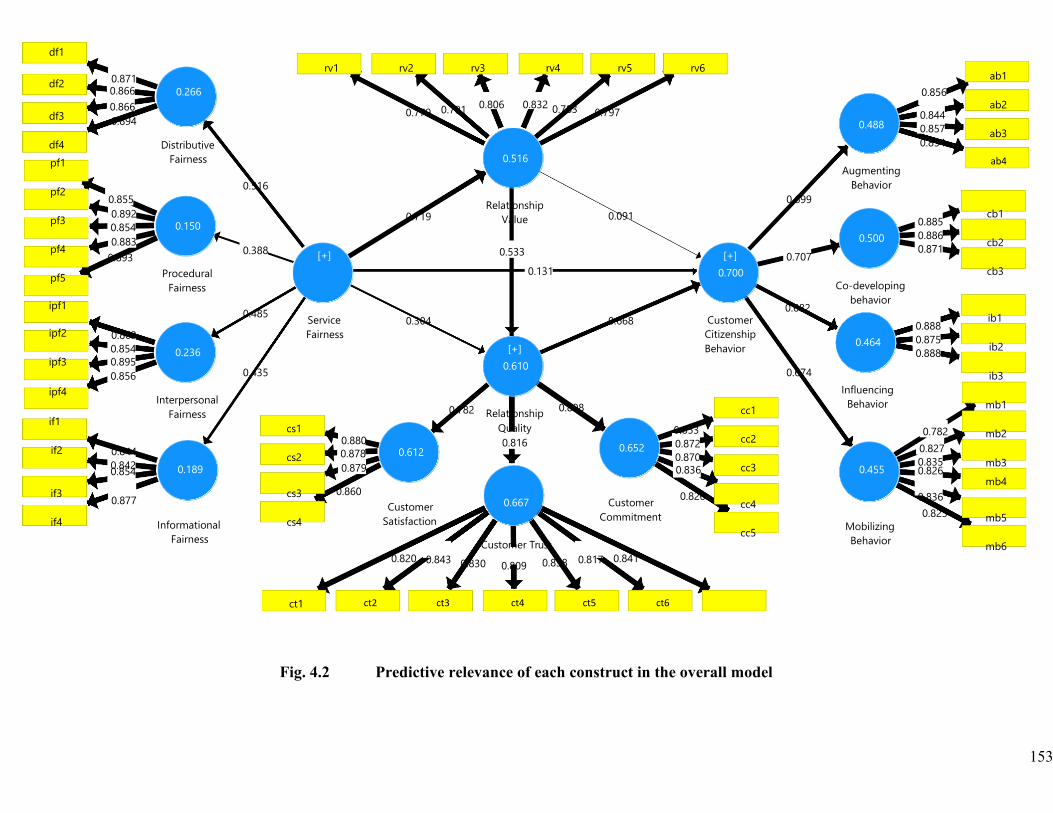

4.2 Predictive relevance of each construct in the overall model ......................... 144

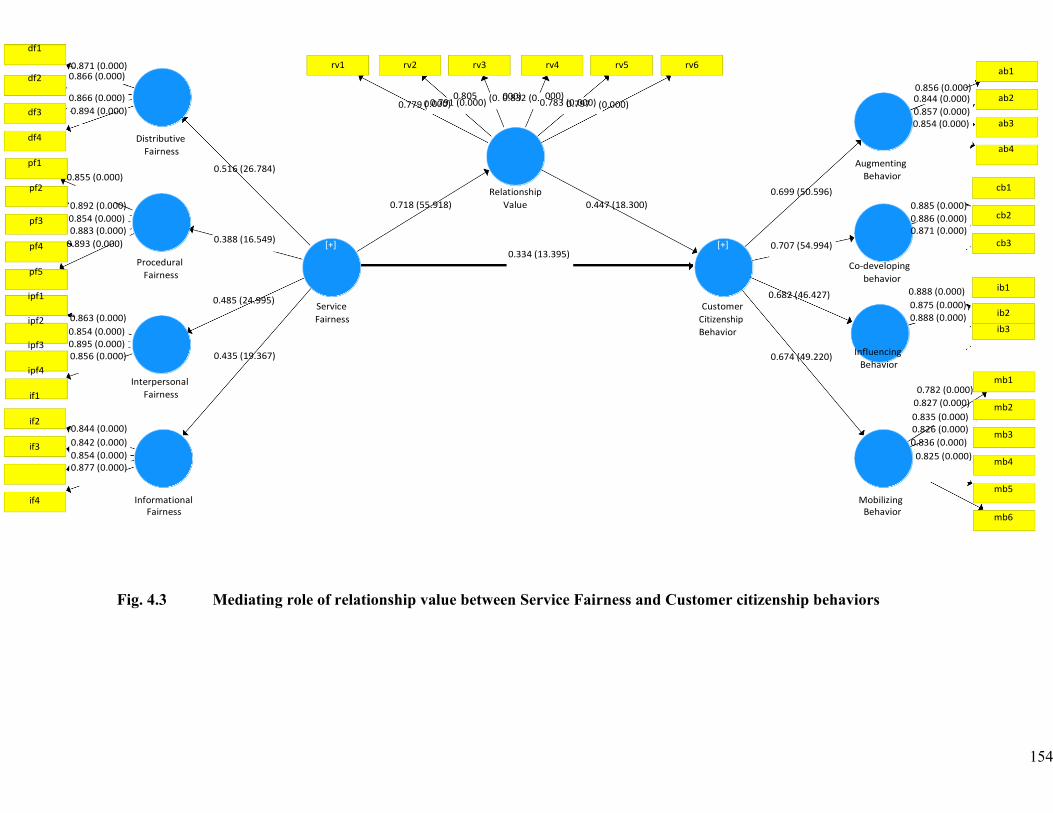

4.3 Mediating role of relationship value between Service Fairness and Customer citizenship behaviors .................................................................... 145

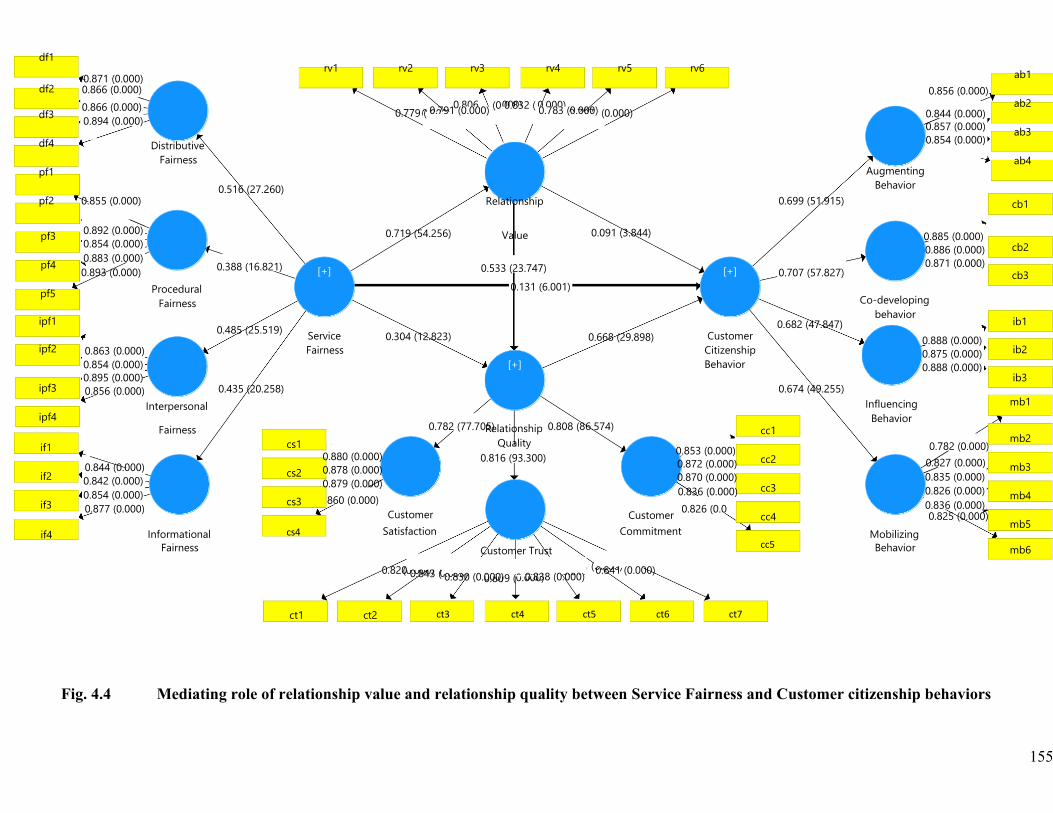

4.4 Mediating role of relationship value and relationship quality between Service Fairness and Customer citizenship behaviors .................................. 146

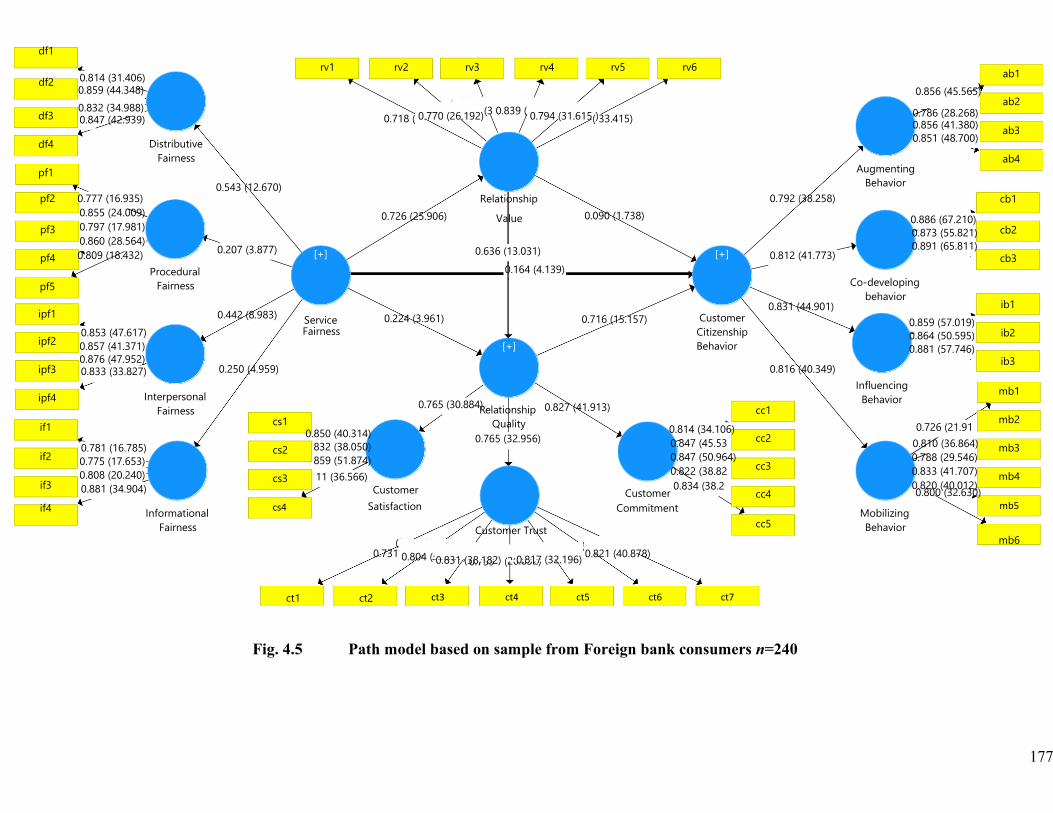

4.5 Path model based on sample from Foreign bank consumers n=240 ............. 168

4.6 Path model based on sample from Islamic bank consumers n=250 .............. 169

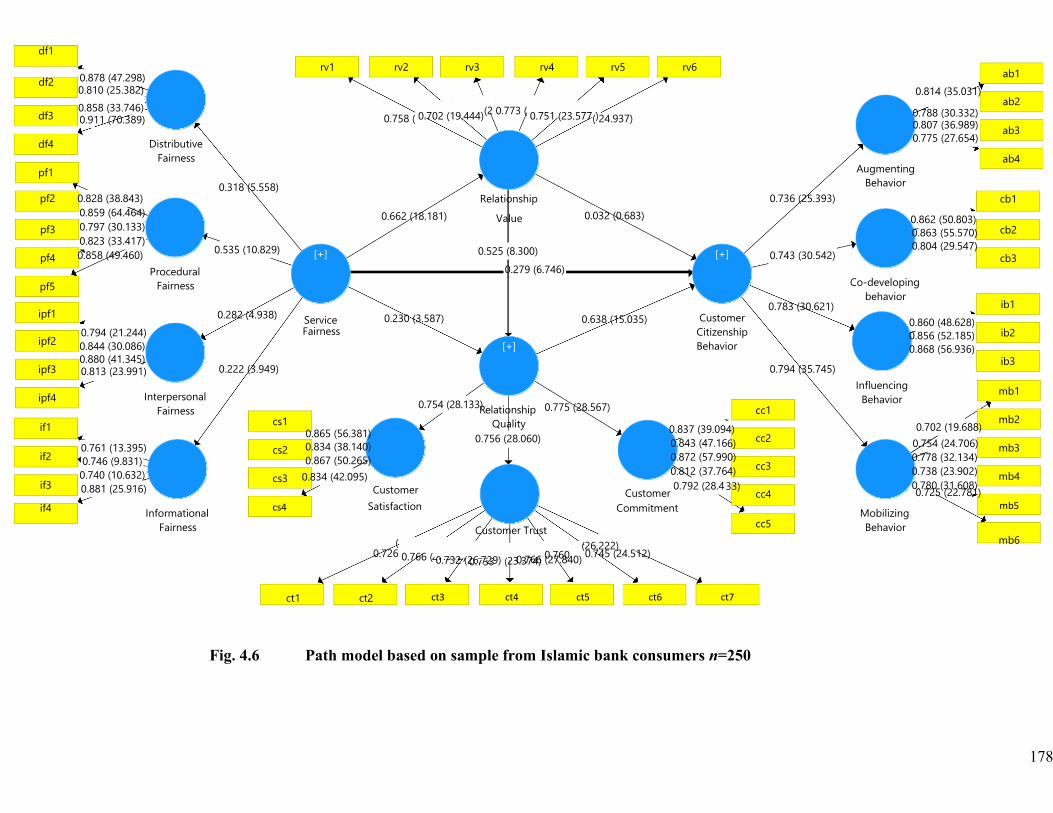

4.7 Path model based on sample from Microcredit bank consumers n=200 ....... 170

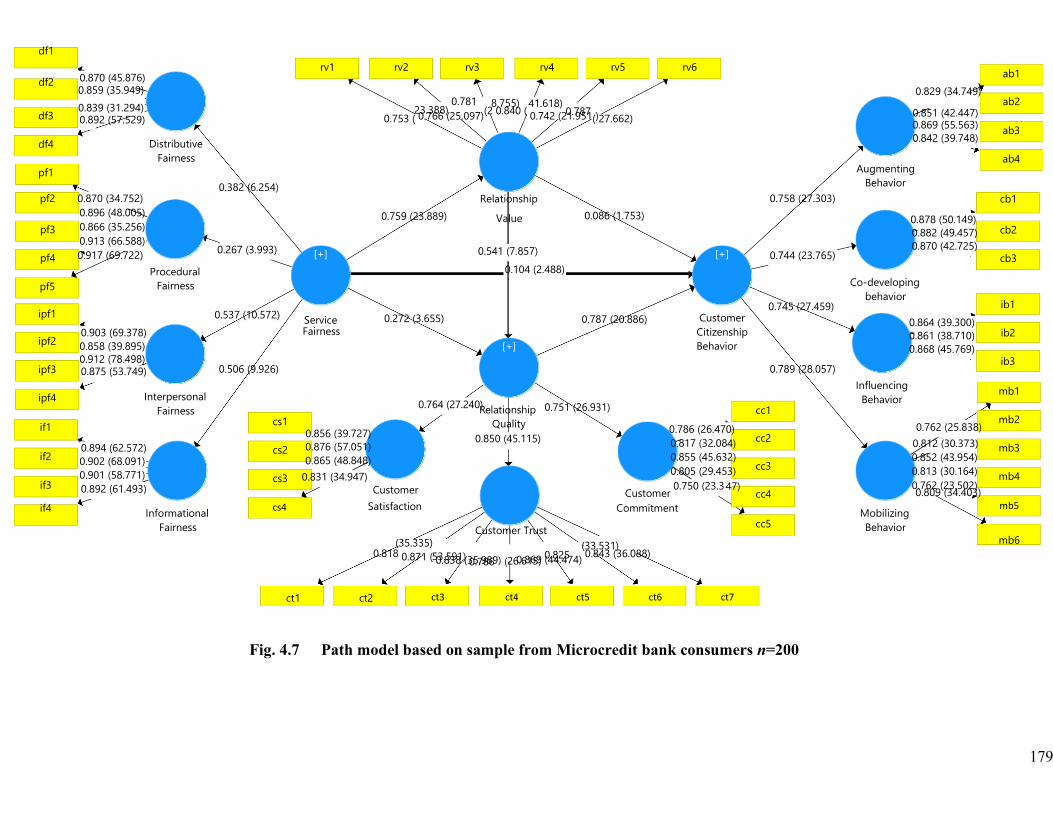

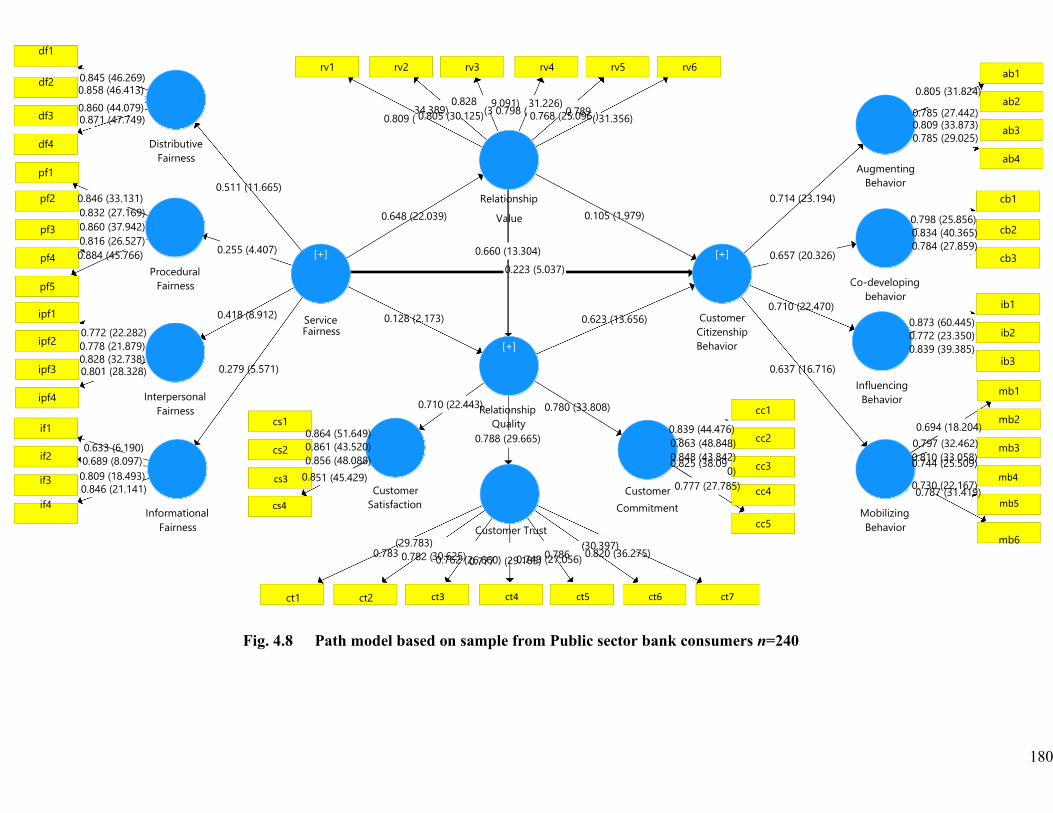

4.8 Path model based on sample from Public sector bank consumers n=240 ..... 171

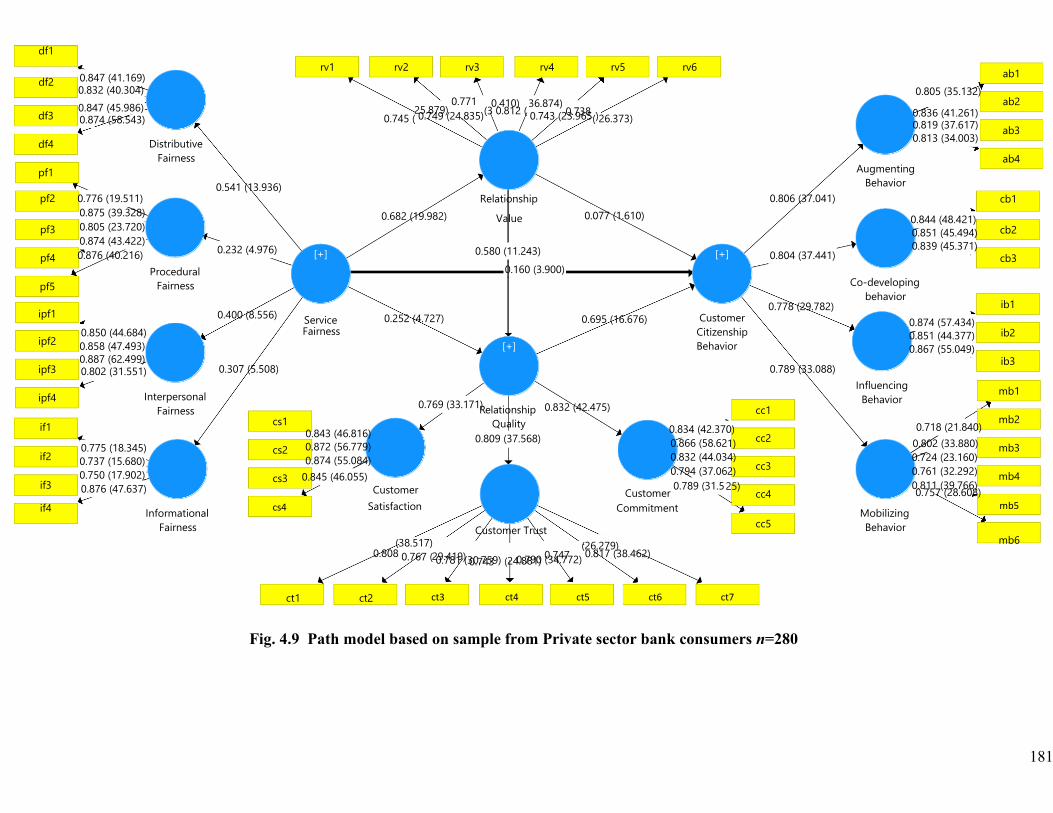

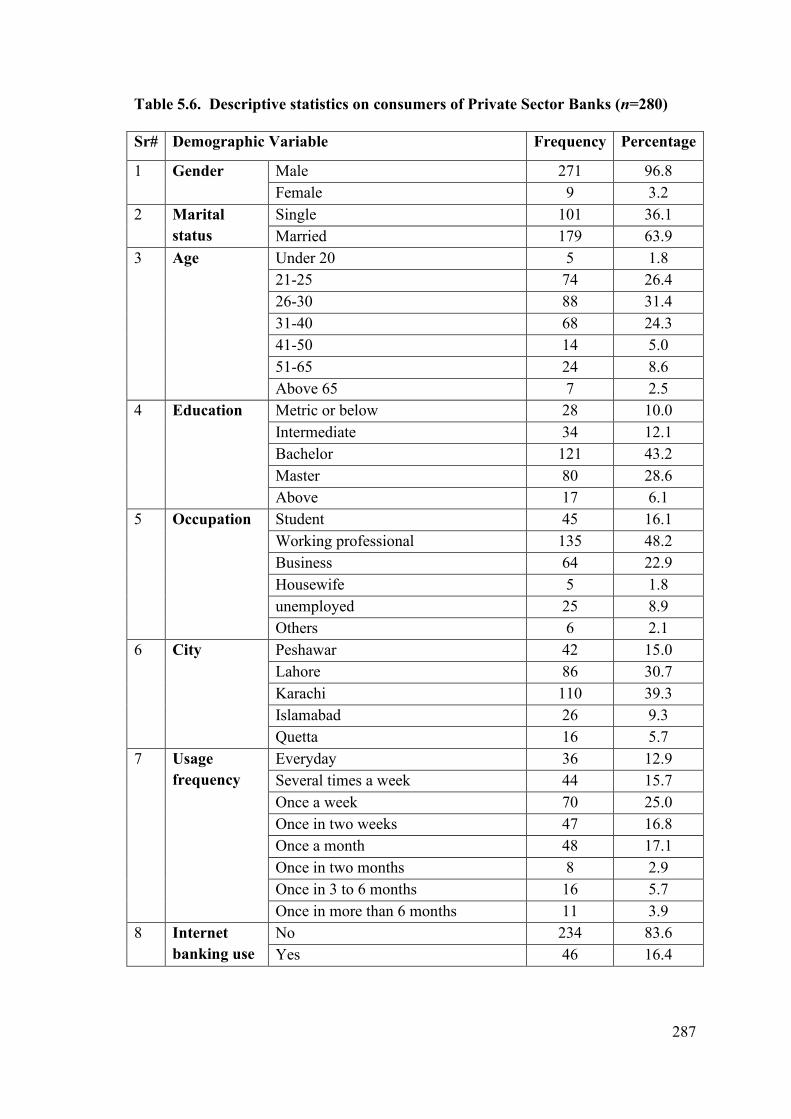

4.9 Path model based on sample from Private sector bank consumers n=280.... 172

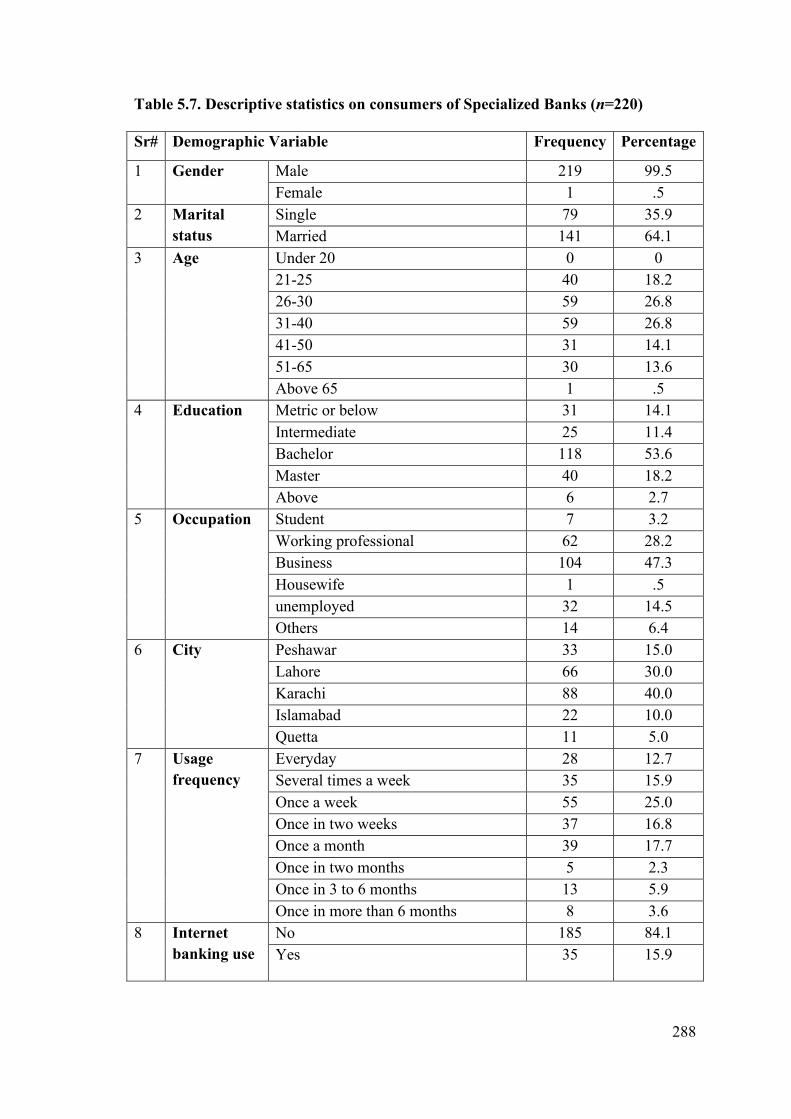

4.10 Path model based on sample from Specialized bank consumers n=220 ....... 173

1

Chapter 1

INTRODUCTION

1.1 Introduction

In the introduction chapter of the study, the broad context within which the research is

undertaken is outlined. The chapter begins with a brief introduction to the business

environment surrounding banking sector highlighting the critical role of service fairness

as a fundamental basis for maintaining and developing bank-customer relationships and

its strategic importance to banking institutions in section 1.2. This is followed by

presenting problem statement of the research which underline the importance of service

fairness issues in service delivery in section 1.3. This leads to a detailed outlining of the

research questions of the study in section 1.4. In section 1.5, the research objectives are

presented. Section 1.6 deliberated about the significance of the study. The scope of the

study and delimitations are defined in section 1.7. Subsequently, the gaps identified in

current studies of service fairness, relationship marketing and customer citizenship

behaviors are introduced in section 1.8. This is followed by section 1.9 which outline

how the structure of the dissertation is organized.

1.2 Background of the study

The world’s economy is experiencing rapid transformation, particularly the market

landscape surrounding businesses has become more rigorous, as the number of

technological innovation and diffusion of modern technologies has accelerated, the

market penetration rate of products is getting higher, while the life cycle of products is

getting shorter, further intensifying the competition between companies for survival in

the marketplace (Soedarmono, Machrouh, & Tarazi, 2013). This phenomenon is no

exception to the entire financial industry, business climate around financial industry has

seen rapid transformation over past decade. The revolution in financial industry has

been steadily promoted in the name of liberalization, securitization, and

internationalization. Naturally, the financial industry has witnessed numerous

transformations both domestically and outside of Pakistan. Most prominent among

these is the rapid progress of financial liberalization due to the deregulation of barriers

between financial institutions. In advanced economies, financial diversification has

been implemented through restructuring financial industry through the process of

2

economic reforms and deregulation, centering around banks, securities, and insurance

sectors (Shabbir Ahmad & Burki, 2016).

Since late 1980s, the financial sector in Pakistan has underwent major structural

changes due to financial liberalization and deregulations. This transformation has led to

greater competition that has favored the efficiency and competitiveness of banking

sector (Zameer, Tara, Kausar, & Mohsin, 2015). Several of the reforms in the course of

the past decade have opened the way for new competitors to enter into the local

financial sector (Ali & Raza, 2017). These new competitors earned their competitive

advantages mostly by preserving lean structures, selective placement of branches, niche

marketing, service management and assisted service delivery through the use of latest

technology (Anjum, Xiuchun, Abbas, & Shuguang, 2017). Discernable divergence in

operating styles among various financial institutions are obvious in the domain of

customer orientation, asset liability management, multiple segment specialization,

administrative structures, market orientation, and management of customer

relationships. As a result, a greater variety and choices of products and services for

customers are available and the banking industry is offering sophisticated delivery

systems and more value-added services than rivals (Anjum et al., 2017; Paul, Mittal, &

Srivastav, 2016). In similar vein, banks have also come under enormous pressure to

deal with the growing demands and expectations of their clients as well as due to the

shift in customer-centric regulatory paradigm towards protection of financial

consumers, posing major challenge for bank to retain existing customers, as a

consequence of the fierce competition prevalent among banks, new clients are hard to

acquire at mature stage in their life-cycles (Zameer et al., 2015), banks need to put

additional effort into establishing new revenue streams (Saleh, Quazi, Keating, & Gaur,

2017). These considerations converge to imply the need for more specific customer-

strategies that build and maintain sustainable bank-client relationships (Dinulescu,

Visinescu, & Prybutok, 2019).

Earlier studies in the domain relationship marketing strongly support that mutually

profitable buyer-seller relationships are key to secure competitive advantage

emphasizing the importance of quality and value of relationships (Dinulescu et al.,

2019; Itani, Kassar, & Loureiro, 2019; Yoong, Lian, & Subramaniam, 2017).

Consumers who maintain successful relationships with their service providers generally

3

spend extra amount, support their firm vigorously, promote positive messages about the

firm and talk about the firm to others and relatives (LuJun Su, Hsu, & Swanson, 2017),

and gradually support the profitability of firms (Itani et al., 2019). Particularly in a

situation where competition between service companies has intensified, companies are

making various efforts to achieve differentiated competitiveness through strengthening

stable mutually rewarding relationships with customers (Dinulescu et al., 2019; Finch,

O’Reilly, & Abeza, 2018; Ye, Li, Wang, & Law, 2014).

Earlier research considers fairness perception as fundamental basis for establishing,

sustaining and enhancing long-term customer-firm relationships (Guo, Gruen, & Tang,

2017; Nikbin, Marimuthu, & Hyun, 2016; Romero, 2017). According to justice theory

(Adams, 1965) customer expect justice in an exchange relationship and gauge their

relationship based the extent to which expected benefits and results are provided as

promised (Rousseau, 1989). In addition, Carr (2007) asserted that customer compare

service results against the norms of fairness in comparison to other consumers based

on distribution of service resources, fair procedures, interpersonal treatment, and

transparency of information from their service providers. A number of past studies have

discussed the significance of service fairness in buyer seller exchange relationships

(Balaji, Roy, & Quazi, 2017; Nikbin et al., 2016; LuJun Su & Hsu, 2013; Lujun Su,

Huang, & Chen, 2015). However, all these studies lack perspective about the full

spectrum of buyer-seller relationship building process through the lens of service

fairness.

Service fairness refers to a consumer’s evaluations regarding the level of justice in a

service provider’s behavior during service delivery process (Seiders & Berry, 1998).

Fairness can affect a variety of aspects, ranging from satisfaction (Jung & Seock, 2017)

and dissatisfaction with service providers (Um & Kim, 2018), complaints (Balaji et al.,

2017), termination of relationship with service providers (Yi & Gong, 2008), and even

voluntary actions by customers for service providers (Choi & Lotz, 2018; Roy, Balaji,

Soutar, Lassar, & Roy, 2018; Roy, Shekhar, Lassar, & Chen, 2018). Service fairness is

a multidimensional construct comprising distributive fairness, procedural fairness,

informational and interactional fairness (Nikbin et al., 2016; Roy, Balaji, et al., 2018).

Earlier research on service fairness has shown that customers determine their trust and

4

commitment to remain in a relationship with a firm fundamentally on how fairly they

are treated (Carr, 2007; Hwang, Baloglu, & Tanford, 2019; Nikbin et al., 2016).

Schneider & Bowen, 1999, argued that consumers engage in a psychological contract

with a firm to have their needs served well and to be treated with justice. Successful

customer relationship management can be attributed to a customer’s positive evaluation

of a service provider fair behavior (Giovanis, Athanasopoulou, & Tsoukatos, 2015;

Saleem, Yaseen, & Wasaya, 2018). Since the intangibility inherent in services

amplifies consumers’ sensitivity towards fairness because it is often inconvenient for

consumers to estimate a service outcome before, and at times after a service transaction

is made (Choi & Lotz, 2018; Roy, Balaji, et al., 2018; Zhu & Chen, 2012). During

service consumption consumers are always present inside the service factory, which

provides a greater opportunity for customers to recognize fairness in relation to service

delivery therefore, from a service provider perspective, fair service delivery is crucial

for customer relationship management (Roy, Shekhar, et al., 2018; Zhu & Chen, 2012).

In terms of producers of financial services, fairness in service delivery is essential in

maintaining and developing bank-customer relationships, considering the highly

competitive nature of banking industry and increasingly interactive customer roles.

Although commercial banking is considered to encounter numerous service failures

(Kaura, Durga Prasad, & Sharma, 2015; Petzer, De Meyer-Heydenrych, & Svensson,

2017; Lujun Su, Swanson, & Chen, 2016), there has been scant investigations in

commercial banking sector of Pakistan that addressed the connection among service

fairness, relationship marketing and resulting customer engagement behaviors (Kamran

& Uusitalo, 2019). In addition to assuring on delivering fairness excellence needed for

sustainable relationships, banking establishments need to direct their relationship

marketing efforts to encourage customer discretionary behaviors.

Past research on value co-creation (Vargo & Lusch, 2008) suggest that firms need to

focus on the increasingly interactive experiential nature of buyer-seller relationships

that stimulate valuable customer resources in favor of the focal firm. Therefore, rather

than focusing only on the transactional side of their relationships with customers, banks

need to understand the increasingly active role of customer as co-creators of value

rather than passive users of service hitherto a inconsiderable area in the banking sector

(Yi & Gong, 2013). Customers may contribute a variety of personal resources that co-

5

create value namely; providing helpful suggestions to the service provider and other

customers, spreading positive word of mouth, recommending the service provider and

services to others, report service-related problems and their solutions and may take the

role as advocates of the firm (Braun, Batt, Bruhn, & Hadwich, 2016; Finch et al., 2018).

The trend of engaging consumers in co-creation activities has also been favored by the

new information technologies and the diverse array of digital channels, such as social

media platforms and smartphone applications (Roy, Shekhar, et al., 2018). Given that

distinctive contributions may come from each type of value co-creation behavior there

is little scholarly investigations as to why consumers engage in helpful activities to

support a certain service providing firm or a brand and begs further research (Balaji,

2014). Therefore, identifying potential drivers underlying such behavior should help

both academics and practitioners gain insights into how to stimulate value co-creation

(Balaji, 2014; Jaakkola & Alexander, 2014; Romero, 2017). Even though the

importance of relationship value and relationship quality on various consumer

outcomes have been well documented (Giovanis et al., 2015; Itani et al., 2019; Roy,

Balaji, et al., 2018), however the direct effect of relationship quality and relationship

value on consumer’s relational outcome such as customer citizenship behaviors, and

engagement behaviors has not been extensively studied (Choi & Lotz, 2018; Saleem et

al., 2018; LuJun Su et al., 2017).

Therefore, the purpose of this study was to investigate the critical role of service

fairness in developing and sustaining strong relationships with customers that further

induces their helpful discretionary behaviors. More specifically, this study sought to

investigate whether consumer– bank relationships act as mediating mechanism through

which service fairness fosters customer voluntary behaviors within the banking sector

in Pakistan. Thus, combining perspectives from equity theory (Adams, 1965), social

exchange theory (Blau, 1964) relationship marketing and service dominant logic

(Vargo & Lusch, 2008), this study tested a theoretical model that investigated the

impact of service fairness conducive for developing and maintaining enduring

relationships with customers and its consequences reflected in customer citizenship

behaviors in banking context.

6

1.3 Problem Statement

Since 2008, the State Bank of Pakistan has implemented prudential regulations on

commercial banks operating within Pakistan through the establishment of consumer

protection department, which advocate guidelines for banking conduct stipulating the

minimum service standards a client can expect from a banking institution (State Bank

of Pakistan, 2017) wherein the relation between the bank and its customers is guided by

four key obligatory principles, requiring banks to be trustworthy, transparent,

accountable, and fair with their clients during service encounters (“Guidelines of

Business Conduct for State Bank of Pakistan Karachi,” 2016).

The Banking Mohtasib Pakistan continuously receives an influx of complaints every

year, however, compared to the last few years, there has been an unprecedented

upsurge of about 44% in the total number of complaints over the last year. According

the annual report (Banking Muhtasib Pakistan, 2017) among all the complaints

registered, the number of grievances received for “Service inefficacies/Delays” among

were most frequent. Given the frequent incidences of consumer complaints during the

execution of financial service, banking sector is ranked as number third among all

service sectors (Nadiri, 2016). Against this backdrop the explicit and systematic

execution of service fairness strategies as planned process generally remains non-

existent in the banking sector of Pakistan. In addition, with increasing legislation for

consumer rights and surge in consumer protection societies it is vital for banking sector

to guaranty a consistent delivery of favorable consumption experience to consumers to

foster enduring consumer relationships. Since financial services involve high credence

attributes therefore provision of fair service by the banks is very important to sustain

long-term relationships with the customers (Roy, Devlin, & Sekhon, 2015). Although

service fairness excellence holds a strategic significance in the long-term survival of

service firms, despite its importance, a greater number of recent studies in the domain

of service marketing highlight that service fairness issues remains largely unexplored

and warrants further research (Bezerra & Gomes, 2019; Hwang et al., 2019; Kim et al.,

2018; Roy, Balaji, et al., 2018; Roy, Shekhar, et al., 2018; Wang et al., 2018).

Moreover, past research has also indicated that consumers react to service fairness

more strongly than service quality reveling that proving service quality to consumers is

necessary condition, however it not enough to establish sustainable relationships with

7

customers (Carr, 2007; Giovanis et al., 2015). Considering the fact that banking

institutions provide virtually identical products and services with little to no variation in

service quality, the real differentiation however may come from a consumer assessment

of the degree of overall fair treatment they receive from their relationship over time

(Roy, Shekhar, et al., 2018). Furthermore, taking into account the competitive nature of

banking sector in Pakistan, despite service excellence banks also need focus on

providing fairness excellence to enhance strong relationships with their clients to

achieve sustainable competitive advantage (Kamran & Uusitalo, 2019). In this regard,

understanding the consequences of a consumer’s service evaluations in terms of

fairness are of significant relevance to banking establishments which are explored in

this research.

It is apparent that albeit Pakistan is an emerging market, commercial banking is well

seasoned, advanced and competitive. Commercial banks are dedicated and also

required to deliver clients with services that surpass or conform to customer

expectations and also to act favorably and reasonably towards its customers in a

consistent and ethical manner however service fairness issues and whether it lead

strong relationship building is yet to be investigated from a developing country like

Pakistan as there is no solid empirical studies that investigated the important role of

service fairness in relationship building process particularly from within the banking

sector. Nonetheless studies also lack perspective regarding the important role of service

favorableness in a firm relationship building efforts that can be targeted to achieve

customer citizenship behaviors (Balaji, 2014; Roy, Balaji, et al., 2018).

1.4 Research Questions

In accordance with the research problem and background, this study intends to respond

to the following research questions posed:

1. How does customer perception of service fairness affect perceived

relationship value?

2. How does customer perception of service fairness affect perceived

relationship quality?

3. Is there a direct relationship between perception of service fairness and

customer citizenship behaviors?

8

4. Does relationship quality mediate between perceived service fairness

and customer citizenship behaviors?

5. Does relationship value mediate between perceived service fairness and

customer citizenship behaviors?

6. Does relationship quality mediate the effect between relationship value

and customer citizenship behaviors?

7. What is the relationship between customer perception of relationship

value and relationship quality?

8. Do perceptions of relationship quality and value directly influence

customer citizenship behaviors?

1.5 Research Objectives

This study aims to extended the existing knowledge on service fairness, relationship

marketing and customer engagement by setting the following objectives:

1. To investigate the role of service fairness and the relative importance its

sub-dimensions (distributive, procedural, interactional and informational

fairness) in building and sustaining long-term exchange relationships.

2. To investigate customer behavioral outcomes from the perspective of

service fairness and relationship marketing.

3. To explore the mediating role of relationship value between perceived

service fairness and customer citizenship behaviors.

4. To explore the mediating effect of relationship quality between

perceived service fairness and customer citizenship behaviors.

5. To explore the interlinkages amongst perceived service fairness,

relationship marketing, and customer behaviors across different

consumer groups in banking sector.

1.6 Significance of the Study

Building on the theories of fairness this study provides useful insights to managers,

practitioners and policy makers to consider the important role of fairness excellence in

all-inclusive service delivery situations. This research offer bank management a deeper

perspective on how consumers judge service delivery from the standpoint of fairness,

highlighting the importance of customer sensitivity towards fair treatment enabling

9

them to formulate more effective and efficient strategies for assuring fairness that will

lead to improved service delivery and superior exchange relationship management.

Customer perception of service fairness has strong practical significance from

relationship marketing perspective because customer judge their relationship with their

service providers based on how fairly they are treated by the service firm. Therefore, it

is utmost importance for banks to provide and maintain service fairness during service

consumption and post consumption stages. This study will serve as a practical guideline

to commercial banks mangers in Pakistan on managing the important role of service

justice in driving customer emotional and behaviors responses from the perspective of

relationship marketing.

The State Bank of Pakistan can better formulate polices with reference to fairness in

terms of information, procedures, outcomes and general conduct of banking

professionals for the sake of consumer protection. These guidelines may serve to

improve service failures rates and may help banks to forge enduring relationship with

their valued customers. This study will serve as practical guidelines for banking sector

in Pakistan to contemplate customer-bank relationship through the lens of service

fairness and deal with customer behavioral responses focusing on building relationship

marketing strategies.

This study offers useful insights in helping banking industry to consider the active role

of customers as co-constructors of value for the bank, therefore such helpful customer

engagements can be used as competitive advantage. These roles of customers are

important because customers participate in a variety of viral marketing activities with

exception of transaction in favor of the focal firm by spreading positive word of mouth,

providing product/service referrals or recommendations to others, suggesting

innovative ideas for new products/services and increase the overall contextual value of

product/service for others and the service firm (Itani et al., 2019; Roy, Shekhar, et al.,

2018).

Because of the interactivity inherent in social media platforms besides enabling buyers

are sellers to share and exchange information it also empowers buyers to share and

exchange service-related information with each other as well. Taking advantage of

social networks, firms can foster relationships with existing as well as potential

10

customers and create communities that work together interactively to recognize

problems and discover its resolution. These interactions transform the conventional

roles of both buyers and sellers involved in an exchange relationship (Roy, Balaji, et al.,

2018; So, King, Sparks, & Wang, 2016). In fact, consumers continually create value by

producing positive content, promote service related information, become avid advocate

of the firm and its services and guide perchance intension of others consumers during

online interactions (Carlson, Rahman, Taylor, & Voola, 2019). Considering the

significance of consumer interactions that co-create value and customer engagement

has critical role in a firm's superior competitive advantage and sales growth (van Doorn

et al., 2010; Yi & Gong, 2013).

Firms which provide the environment for discretionary behaviors, can use customers to

achieve their goals and profitably (Verleye, Gemmel, & Rangarajan, 2014).

Consequently, the effective management of customer interactions can be used as a

strategic advantage by banking sector with in Pakistan. This study highlights the

importance of bank-customer relationship based on fairness which is helpful to

reinvigorate pubic trust in banking institutions. Fair banking behaviors is helpful to

attract and retain customers and reduce service failure costs and thus can provide better

banking environment for citizens of the society.

Recent reforms in the banking sector have already effectuated a vibrant landscape

eliciting in the emergence of customer-specific strategies to foster enduring bank-

customer relationships (Shabbir Ahmad & Burki, 2016; Ali & Raza, 2017; Saleem,

Zahra, Ahmad, & Ismail, 2016). Therefore, in order for banks to attract and maintain

their customers from competition, they must turn to meet the economic and emotional

needs of their valued customers by investing in the increasingly interactive and

experiential nature of consumer relationships (Vivek, Beatty, & Morgan, 2012). There

are no researches available on customer perception of service fairness in the area of

service marketing from Pakistan.

From a methodological perspective this study validated multi-item measures adopted

from previous studies by testing an integrated model in a developing country

perspective within banking sector. This study validates that service fairness,

relationship quality and citizenship behaviors are second-order constructs bearing

higher reliability and validity scores and thus have a significant relevance in collective

11

cultures within a south Asian business context. Therefore, researchers can utilize these

validated measures in relation to other relevant theorical constructs in their future

studies.

Building on fairness theories in service sector, researcher can uncover new models after

reviewing this work. Service fairness is potentially a new frontier in building customer

trust, commitment and building valuable relationships in the area of service marketing.

This study in turn should provide valuable insights to marketing practitioners who may

devise better strategies in helping service supplying firms to contemplate service

fairness advocating fairness polices in helping them reduce service failure costs and

customer turnover. Thus, this study brings new insights for banking sector and

proposed that positive evolution of fair treatment during ongoing service transactions

help develop and strengthen relationship between banks and its customers, which

consequently guide customer discretionary behaviors. Therefore, it is suggested that

customer perception about a bank’s favorable image will strengthen its reputation and

market standing which will ultimately serve as a potential source of differential

competitive advantage.

1.7 Scope of the study

The scope of this study was limited to examine the predictive relevance of service

fairness evaluations in developing sustainable relationships with customers and driving

citizenship behaviors from the perspectives of users of banking services in Pakistan.