the 'globalization' or 'internationalization' of danish large companies

TRANSCRIPT

The globalization of the business sectorin a small open economy: the case of Denmarkand its wider implications

Grahame F. Thompson1 and Lars Bo Kaspersen2,*

1Department of Business and Politics, Copenhagen Business School, Copenhagen, Denmark;2Department of Political Science, University of Copenhagen, Copenhagen, Denmark

*Correspondence: [email protected]

The growth of multinational corporations (MNCs) is often taken as a quintessen-

tial indicator of ‘globalization’. But recent detailed empirical analysis has chal-

lenged the idea that most MNCs are global in terms of their business strategy

and arena of operations. This article first clarifies the differences between global-

ization, internationalization and supranational-regionalization by examining the

evidence on trade and investment patterns for Denmark. In particular, it presents

a detailed analysis of the business strategies of the large corporate sector in

Denmark. Denmark is an interesting case, as it is a small open economy (SOE)

that might be thought to be one uniquely vulnerable to the forces of globaliza-

tion. Up until now examination of MNCs’ internationalization strategies has con-

centrated upon large economies. We provide evidence for a SOE. In addition, we

expand the range of dimensions used to consider internationalization beyond the

location of turnover (sales) to include measures of company assets, employment

and physical investment. Furthermore, in the light of the analysis of this company

sector, we explore the public policy implications of our results for the future of

SOEs in a rapidly changing international business environment.

Keywords: multinational firms, business economics, globalization, regional

economies, firm strategy, public policy

JEL classification: F23 multinational firms, international business, M21 business

economics

1. Introduction

This article addresses several related issues. The first follows a line of analysis ori-

ginally indicated by Hirst and Thompson (1999, chap. 4) and particularly

Rugman (2005) concerning the operations of large international businesses.

# The Author 2012. Published by Oxford University Press and the Society for the Advancement of Socio-Economics.

All rights reserved. For Permissions, please email: [email protected]

Socio-Economic Review (2012) 1–27 doi:10.1093/ser/mwr036

Socio-Economic Review Advance Access published February 1, 2012 by guest on February 3, 2012

http://ser.oxfordjournals.org/D

ownloaded from

This questioned whether such businesses were as unambiguously ‘global’ in char-

acter as often thought, rather than still being nationally or supra-nationally re-

gional in their orientations. The growth of multinational corporations (MNCs)

is seen as one of the main drivers of globalization. In the popular and mainstream

academic and business literature—and in the popular imagination—MNCs are

argued to have become the key engines of an expanded global reach for business

activity. Any company that is to meet the challenges of the global marketplace

must strategically position itself to invest, source, produce and market globally;

otherwise it will perish. This is the standard view. But closer examination of

what most MNCs were actually doing in the 1990s shows this not to have been

the case (Hirst and Thompson, 1999; Rugman, 2005). However, this debate has

often neglected MNCs with a home-base in small open economies (SOEs), and

this article will remedy this neglect by exploring large businesses in the context

of Denmark. Where exactly do large Danish corporations conduct their inter-

national business activities? And although Denmark is not a significant player

in terms of overall global economic activity, we argue as a second issue that an

analysis of its large business sector provides some important and valuable

lessons for SOEs more generally in regard to their strategic attitudes towards eco-

nomic internationalization. Since SOEs are strongly dependent on a high level of

internationalization, is the business sector in a SOE more ‘globalized’ than we

find in the large economies such as the USA, UK, Japan and Germany? And

since economic globalization is thought to have gathered pace during the

2000s, our analysis—which concentrates on the situation towards the end of

this decade—brings the more recent trends into focus.

The article proceeds as follows: in Section 2 we outline what value our analysis

of the Danish large business sector adds to the literature in this field, particularly

by distinguishing between globalization and internationalization. Here we also

justify why the Danish case is novel, interesting and important from a wider per-

spective. In Section 3, we discuss existing analyses and approaches. Section 4 pro-

vides a preliminary analysis of the internationalization of the Danish economy in

terms of trade, FDI (foreign direct investment) flows and stocks. This is followed

by our detailed analysis of the Danish large business sector in Section 5. The final

main section (Section 6) provides a discussion of and reflection on the issues

raised by the empirical analysis for (mainly European) SOEs in particular. The

concluding section sums up the overall lessons to be learned from our

investigation.

2. Conceptual and analytical framework

The context for our investigation is an analytical distinction drawn between an

inter-nationalized economic structure (note the hyphen—not an ‘international’

Page 2 of 27 G. F. Thompson and L. B. Kaspersen

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

one) and a globalized economic structure. An inter-nationalized economy is an

economy composed of a series of individual national economies that interact

with each other mainly via activities such as trade interdependency, investment

integration and labour migration where these resources flow across borders.

The most significant feature of this—though not the only one—would still be

the separated national economies that interact with each other to form the inter-

nationalized economy.

On the other hand a globalized economy would be an economy that existed as a

single economic entity in its own right, somewhat beyond the interacting individ-

ual national economies. This economy would be driven by market forces and

competition between ‘footloose’ economic agents (companies, banks, financial

institutions, individuals) that are not clearly tethered to any single national

economy, but which take the global arena as their sphere of operations: produ-

cing, sourcing, marketing etc. and moving their operations across the globe

according to the competitive advantages and profitable opportunities that

present themselves anywhere.

The logic of these two types of economic mechanism is conceptual ‘ideal types’

that do not exist as such in practice or on the ground. They provide an abstract

image of two different possible types of economy. A difficulty is that traditional

discussions of the ‘international economy’ or ‘global economy’ do not draw this

crucial distinction between the two forms of economic mechanism just outlined,

but the distinction is important for the analysis that follows. This is because these

images impinge upon the way the analysis of business activity is conceived in an

international context. Are corporations still tethered (in one way or another) to

their national economies—so that they can still be managed by nationally based

authorities in that context? Or have such corporations become genuinely foot-

loose, so that they escape any such possibility of management or regulation?

The problem with the strong globalization thesis as applicable to companies is

that it disarms public authorities in their attempt to influence, encourage, regu-

late or manage their corporations (or, indeed, the economy in general). An added

complication is that there is no terminological consistency in how to describe

such corporations. From our point of view the term ‘multinational corporation’

would be better suited to the inter-nationalized form of international economy.

This would designate a corporation that was still largely tethered to a distinct na-

tional economy, but with a number of branches or affiliates located abroad. On

the other hand, the ‘transnational corporation’ (TNC) would be one more con-

sistent with our globalized economy in that its operations would be genuinely

footloose and not clearly associated with any particular national economy. A dif-

ficulty is that these two terms are used interchangeably in the literature (e.g. by

UNCTAD, 1997), which can lead to confusion in terms of the distinctions we

are trying to draw. And such that the terminology of a ‘global corporation’

Globalization of business sector in Denmark Page 3 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

were to be used, this is one describing a globalized system, so it would be consist-

ent with such an economy, and another term for what is more usually described

as a TNC. Largely for convenience, in what follows we use the generic term MNC

to describe any business operation that displays some international productive

activity.

So, from a public policy viewpoint, it is vitally important whether the major

corporations associated with a national territory have actually globalized in

this sense, or are still to be considered in the context of a national economy

framework. This is the issue we pursue below. Although the Danish case might

appear of only marginal interest, it is presented as an example of this wider

issue, one confronting many advanced economies with corporations that are

rapidly internationalizing in one way or another. We do not dispute that such

firms are internationalizing; what we wish to investigate is whether they are glo-

balizing to an extent that places them beyond influence or regulation by the do-

mestic public authorities.

And as will become apparent, this analysis is complicated because we do

not just see a process of inter-nationalization or globalization in the terms

outlined above, but also of supra-national regionalization. However, for con-

ceptual clarity at this stage, we suggest that any such supra-national regional-

ization of company activity still presents the domestic authorities with an

opportunity to influence their corporations to an extent that a genuinely

global presence would not. This is argued below. Thus, we work with the

basic distinction between an inter-nationalized economy and a globalized

economy. The supra-nationally regionalized variant—about which there will

be a lot to say later—could either be considered a hybrid or an emergent

new ideal type. However, we still prefer to see this as a form of the inter-

nationalized economy, since, as will be argued below, the supra-national re-

gional form of firm organization still tends to privilege MNC type over

TNC type of operational characteristics. And this is in addition to the

problem of how to operationalize these distinctions in the context of the in-

evitably limited and not fully consistent or satisfactory data on international

business activity that can be gathered from companies.

3. Existing analyses and approaches

As mentioned above, Rugman (2005) in particular has demonstrated—in

terms of their sales at least—that MNCs still tend to concentrate their activ-

ities in their home territory and supra-national regional locations. For 2001

the proportion of turnover for the largest MNCs from different countries

was produced by only nine of the 500 largest MNCs that were truly ‘global’

in his terms (see below). In fact, the vast bulk of MNCs were still

Page 4 of 27 G. F. Thompson and L. B. Kaspersen

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

‘domestically’ orientated with at least 75–80% of their turnover in their home

territory or region. What is more, Rugman’s subsequent analysis suggests that

this supra-national regionalization of MNCs’ operations has not diminished

through time, but remained robust over the period 2001–2005 (Rugman

and Verbeke, 2008, p. 328, table 1). Rugman concentrates on sales to the rela-

tive neglect of assets, employment and sourcing. Though there is some evi-

dence that assets are also supra-nationally regionally distributed (Rugman,

2008; Rugman and Verbeke, 2008), employment and sourcing seem to be

completely neglected. Some companies, for instance, may sell most of their

output ‘nationally’ but source their raw materials, components and intermedi-

ate or retail products ‘internationally’. This has yet to be systematically inves-

tigated. But we go beyond Rugman in that we not only consider the location

of turnover (sales), but of assets, employment and physical investment.

Similar sentiments to those of Rugman are expressed by Ghemawat (2007),

who argues that a genuinely strategic attitude of companies towards overseas

operations requires them to recognize the continued pertinence of borders and

the engagement with differences between business environments in different

countries. He suggests that what he calls ‘semi-globalization’ is the current char-

acteristic of the international business system, leading businesses to localize their

strategy and forget about any global ambitions.

On the basis of the original evidence presented in his 2005 book The Regional

Multinationals, Rugman and several co-authors have gone on to elaborate and

differentiate the original thesis. First, they have disaggregated the evidence by

sector in the context of several industries that are often thought to be among

the most highly globalized. Rugman and Girod (2003) do this for retailing,

Rugman and Collinson (2004) for the automobile sector and Rugman and

Brain (2004) for the retail banking sector. In each case, after deploying the criteria

to differentiate regional companies from global ones mentioned above, a similar

picture emerges as to the relative unimportance of genuinely global companies.

And second, the data are disaggregated along supra-national regional lines for

European MNCs (Rugman and Collinson, 2005) and Asian MNCs (Collinson

and Rugman, 2007) and nationally for Japanese companies (Collinson and

Rugman, 2008). Again, a comparable picture emerges. Similar evidence exists

for this lack of global corporations in the case of Latin American MNCs.

Minda (2008) suggests that there are only two large Latin American MNCs

that are anywhere close to becoming global players: CEMEX from Mexico and

Embraer from Brazil. The rest can only be considered supra-national regional

players with operations in one or the other of the triad locations (EU,

North America and East Asia).

What these data also demonstrate is that any scrutiny of company accounts

needs to recognize what companies are doing on their ‘home’ territory at the

Globalization of business sector in Denmark Page 5 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

same time as they are investing and operating abroad. But even where there is

some assessment of MNCs according to the extent of their foreign-owned

assets, the companies included are usually those already classified by the extent

of their foreign-owned assets, thereby prematurely skewing the analysis in

favour of the overseas orientation of company activity (e.g. UNCTAD, 1997,

pp. 29–31, table 1.7).

But there have been several specific criticisms of Rugman and his co-authors’

approach which are worth reviewing before we move on to our substantive ana-

lysis of the Danish case.

A first preliminary point is that the idea of a triad regional configuration is not

that precisely specified in the analyses. North America or NAFTA as a regional

configuration is fairly precise (though variable in the case of Mexico, perhaps),

but what exactly is the geographical reach of a term like ‘East Asia’, for instance?

And even the idea of ‘Europe’ is not necessarily precise. Is this just the EU? But if

so, the boundaries here have changed dramatically over quite a short period of

time. We confronted this problem in the case of the Danish companies analysed

below, and it proved difficult to generate an entirely consistent geographical clas-

sification of companies that reported data on the geographical aspects of their

business activities. We define ‘Europe’, for instance, as ‘greater Europe’ which

includes non-EU countries (e.g. Norway and several in Eastern/South-Eastern

Europe). It may be impossible to generate an entirely consistent position on

this, and perhaps in the big picture of things it is not that significant: a loosely

defined triad may suffice given the likely irregularities and uncertainties over

much of the data.

A second preliminary issue is that only 380 of the 500 top companies

returned data on the geographical distribution of their sales in the original

Rugman sample, so the sample is not necessarily an unbiased one. What

are the characteristics of the 120 companies that do not figure in the analysis?

A reasonable presumption might be that they either ‘mirror’ in some way

those companies that did return usable data (hence the sample of 380 is

not biased), or they could be more domestically oriented than those that

did present data because it is those firms more firmly established abroad

that find it worthwhile and appropriate to lodge such data in their accounts.

If this were the case, it would reinforce the domestic orientation found in the

data for the other 380.

However, we do know about the criteria used, and, of course, these are of ne-

cessity arbitrary at one level. At the centre of the concrete criticisms of this aspect

of the analysis have been challenges to the appropriateness of the boundaries set

to distinguish between the various categories of companies in terms of their

Page 6 of 27 G. F. Thompson and L. B. Kaspersen

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

international operations. Let us just remind ourselves of what these boundaries

are for Rugman et al.:

(1) Home-regional firms have greater than 50% of sales in the home region.

(2) Bi-regional firms have less than 50% of sales in the home region and greater

than 20% in another region of the triad.

(3) Host-regional firms, a special form of bi-regionalism, have greater than 50%

of sales in a triad region other than the home region.

(4) Global firms have less than 50% of sales in the home region and greater than

20% in each of the other triad regions.

(Where assets are considered as well as sales, these same criteria are used to de-

termine the equivalent categories.)

Osegowitsch and Sammartino (2008) devote a good deal of their critical atten-

tion to varying these criteria, particularly around the crucial differentiation

points like the ‘50% home region border’ and the ‘20% other regional distribu-

tion’. What if a cut-off point of 40%, or even 30%, were taken for the first point

and 10% for the second, for instance? Osegowitsch and Sammartino develop a

sensitivity analysis around these issues and show that this somewhat alters the

number of companies falling into the various categories, as would be the expected

result. But as Rugman and Verbeke (2008) rightly point out in their reply, this

sensitivity analysis does not alter the results profoundly. The position remains

that global companies are few and far between, while domestically regional

ones predominate under almost any reasonable adjustment to the criteria.

3.1 Why a continued national or regional orientation?

What the debate between Osegowitsch and Sammartino (2008) and Rugman and

Verbeke (2008) additionally served to do, however, was to raise many issues asso-

ciated with the analytical or theoretical reasons for a supra-national regional con-

figuration of internationalized companies as opposed to a global one. Why might

companies concentrate their efforts on a domestic and supra-national regional

market and be more successful there rather than push for a genuine global pres-

ence? There are several general issues involved here, as well as those specific to the

Danish case, which we take up in later sections.

A first set of general issues revolves around ‘path dependency’ considerations.

Companies tend to set up overseas sales or production networks in territories ad-

jacent to their own simply because of convenience or for historically contingent

reasons. Once established, there is an incentive to continue in these locations.

And in as much as this provides general lessons in how to break into a market

and operate there successfully, such accumulated knowledge encourages other

businesses to follow.

Globalization of business sector in Denmark Page 7 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

But what exactly are the business incentives to such path dependency? Here we

can point to two sets of economic mechanisms that have played an important role

in discussions of regionalization: transaction costs and the relationship between

firm-specific advantages (FSAs) and country-specific advantages (CSAs).

It is costly to set up operations abroad: there are high transaction costs to such

ventures. How can these be minimized? That is the question companies must set

themselves if they are to successfully develop an international strategy. Given that

distance remains a major inhibiter to trade and investment more generally (see

Disdier and Head, 2008; Hirst et al., 2009, chap. 6) and borders continue to

matter for economic decisions (even the borders between US states within the

federation are an inhibiter of trade between states; Wolf, 1997), ‘crossing

borders’ to do international business results in unexpected costs for setting up

networks. The closer the market, the more easy it is to manage. And this ‘close-

ness’ need not just involve geographical distance: it can be ‘cultural distance’ or

‘institutional distance’, as well. In general, there can be a ‘liability of foreignness’

(LoF) involved in doing international business: cultural, institutional and legal

(contractual) commonalities reduce this potential LoF, which incentivizes a re-

gional configuration where these barriers are likely to be lower and the

‘novelty’ of problems less.

And this LoF requires companies to manage their FSAs in relation to CSAs. A

critical element for internationalization choices is determined by the MNC’s

ability to link its FSAs to CSAs as it expands abroad. MNCs must successfully

deploy their existing FSAs to the specificities of countries to increase their sales

and profitability. As a result, each foreign location requires location-specific

linking of investments to combine existing FSAs with the CSAs they find there,

which creates asset specificity (Rugman and Verbeke, 2005).

Region-bound firm-specific advantages (RFSAs) are a response to this

dilemma. Rugman and Verbeke (2005, 2008) developed the concept of RFSAs,

complementing (location-bound) CSAs and (non-location-bound) FSAs.

RFSAs can be exploited successfully by a firm throughout a region rather than

being restricted to one country. Such benefits are possible if the firm integrates

its foreign sales or subsidiaries regionally while keeping a regional responsiveness

at the country level. In the presence of substantial transaction costs, a regional

orientation, dispersing competencies and capabilities among internal and region-

based networks, may be an efficient configuration. RFSAs can be exploited suc-

cessfully by a firm throughout a region with low-linking investments in a

region’s countries owing to the relative ‘closeness’ or similarity of these countries

and their corresponding CSAs. But these RFSAs remain region-specific and can

be deployed across borders only in a limited region. As a result, region-level

scope effects should exist because of this attempt to minimize these linking

costs and maximize MNCs’ performance. RFSAs allow an MNC to upgrade its

Page 8 of 27 G. F. Thompson and L. B. Kaspersen

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

own CSAs, making them more valuable at the region level with new—and add-

itional when compared with the country level—scale and scope advantages

resulting from the comparatively larger size and diversity of regions.

The issue of the institutional obstacles or incentives to developing internation-

al business strategies has been emphasized in particular by Kostova (1999) and

Kostova et al. (2004, 2008). This is seen as a problem of the transfer of strategic

organizational practice within a MNC to capture competitive advantage. Several

conditions for success are elaborated in association with the institutionalization

of practices at the recipient unit: the effectiveness of implementation there via

formal rule adoption and the internalization of these rules within the cognitive

value system and organizational identity of the subsidiaries and parent

company alike. Shared organizational and socially embedded cultures are empha-

sized both between parent company and recipient unit and between the business

environments of locational settings. Again, this speaks to the importance of his-

torical path dependency and the ‘compatibility’ of the institutional and cultural

arrangements for the success of international investment strategies. In the case of

knowledge transfer, Kostova et al. (2004) draw attention to the success of Novo

Nordisk in ‘translating’ company values and drawing knowledge from a culturally

diverse set of contexts so as to enhance performance and facilitate competitive

success. Kristensen and Zeitlin (2005) set out the complex process of strategically

configuring a British-based MNC with an important Danish subsidiary to take

advantage of USA and European institutional specificities to try to reap many

of the competitive advantages discussed in this section.

Of course, all the mechanisms described so far are based upon de-facto region-

alization, rather than de-jure measures. They concentrate on decisions made by

companies as to where and what form of regional integrations to make based

upon private market advantage. Clearly, these need to be supplemented by con-

sideration of public de-jure processes, particularly in the case of Danish member-

ship in the European Union.

We return to this in a later section where we discuss the implications of our

results for Denmark, to which we turn in the next section. Denmark is a

single, small, open economy with relatively small MNCs by global standards,

so it presents an interesting and important contrast to the larger country and

company analysis that has dominated the debate until now. Furthermore, our

analysis extends the data base on which judgements can be made, since we deal

not only with the geographical distribution of turnover (sales) and assets, but

also of employment and—albeit to a lesser extent—physical investments. And

finally, the case of Denmark raises important strategic public policy issues asso-

ciated with the consequences of the analysis for SOEs more generally, as well as

the strategic issues for companies, of course. But these public policy issues

have been relatively neglected by other analyses.

Globalization of business sector in Denmark Page 9 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

4. Patterns of Danish trade and FDI

4.1 The pattern of foreign trade

In this analysis, we concentrate on what companies are doing in terms of their

business strategies and where they are locating their activities. Thus, this is less

about what countries are doing in this respect, though these are linked in many

ways. But as a prelude to this company analysis—and as a context for it—we

look briefly at how Denmark as a country is located in terms of its trading rela-

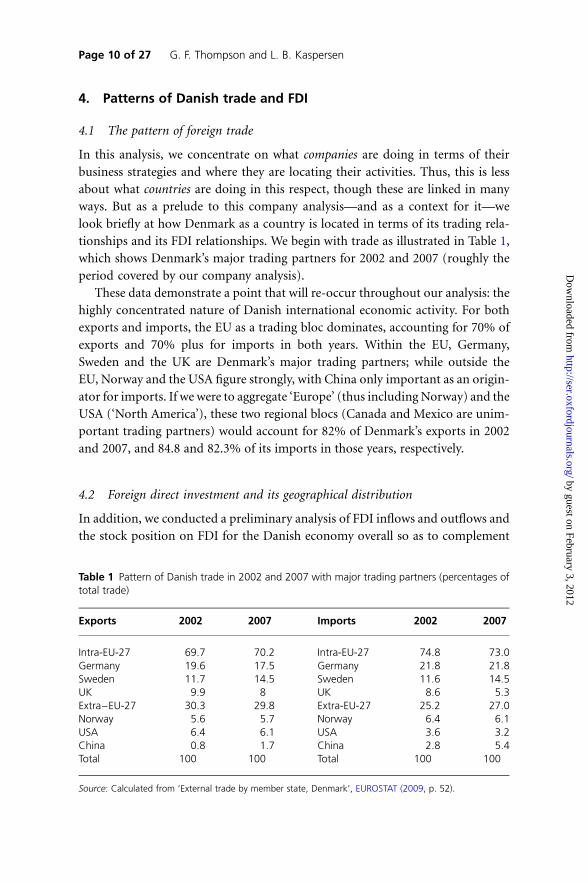

tionships and its FDI relationships. We begin with trade as illustrated in Table 1,

which shows Denmark’s major trading partners for 2002 and 2007 (roughly the

period covered by our company analysis).

These data demonstrate a point that will re-occur throughout our analysis: the

highly concentrated nature of Danish international economic activity. For both

exports and imports, the EU as a trading bloc dominates, accounting for 70% of

exports and 70% plus for imports in both years. Within the EU, Germany,

Sweden and the UK are Denmark’s major trading partners; while outside the

EU, Norway and the USA figure strongly, with China only important as an origin-

ator for imports. If we were to aggregate ‘Europe’ (thus including Norway) and the

USA (‘North America’), these two regional blocs (Canada and Mexico are unim-

portant trading partners) would account for 82% of Denmark’s exports in 2002

and 2007, and 84.8 and 82.3% of its imports in those years, respectively.

4.2 Foreign direct investment and its geographical distribution

In addition, we conducted a preliminary analysis of FDI inflows and outflows and

the stock position on FDI for the Danish economy overall so as to complement

Table 1 Pattern of Danish trade in 2002 and 2007 with major trading partners (percentages oftotal trade)

Exports 2002 2007 Imports 2002 2007

Intra-EU-27 69.7 70.2 Intra-EU-27 74.8 73.0Germany 19.6 17.5 Germany 21.8 21.8Sweden 11.7 14.5 Sweden 11.6 14.5UK 9.9 8 UK 8.6 5.3Extra–EU-27 30.3 29.8 Extra-EU-27 25.2 27.0Norway 5.6 5.7 Norway 6.4 6.1USA 6.4 6.1 USA 3.6 3.2China 0.8 1.7 China 2.8 5.4Total 100 100 Total 100 100

Source: Calculated from ‘External trade by member state, Denmark’, EUROSTAT (2009, p. 52).

Page 10 of 27 G. F. Thompson and L. B. Kaspersen

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

the analysis of trade just discussed. FDI is a traditional measure of international-

ization, but it suffers from a number of shortcomings, as will become apparent in

a moment. It can be measured in terms of yearly flows or accumulated stocks.

From the Danish point of view, FDI—both outward and inward—began in

earnest in the 1990s. Flows peaked in 2000, subsequently collapsed and have

only recently recovered. There were negative flows in 2004 and 2005 because

MNCs took advantage of the weak value of the US dollar to repay intercompany

loans. And this illustrates one of the major problems with using FDI as the exclu-

sive measure of overseas productive investment. First, it involves mainly M&A

(mergers and acquisitions) activity, which fluctuates widely according to the busi-

ness cycle. But most importantly, it appears on the liability side of company

balance sheets, not on the asset side—it is effectively a loan to subsidiaries,

which constitutes a liability for them, so it is subject to normal financially engi-

neered ‘liability management’. In 2004 and 2005, exchange rate fluctuations

encouraged a major repayment of loans quite independently of what was going

on in respect to ‘real investment’ (FDI is thus mis-named to some extent: it is

not a measure of real ‘investment’, but a financial transaction—a loan). In add-

ition, considerable distortions can be introduced in FDI data because of large

inward time-dependent investments in particular sectors, like energy and

North Sea gas and oil, as was the case in Denmark in the late 1990s. In part,

this is the reason we concentrate on the balance sheet and other firm-based indi-

cators of company activity to gain a clearer insight into what companies are ac-

tually doing ‘on the ground’, so to speak.

Denmark has moved between being an aggregate net recipient and a net ex-

porter of FDI, though most of the time it has been a small net exporter (which

manifests itself in a positive net stock position). This is to be expected of an

advanced economy—it provides resources to invest in more profitable ventures

abroad. But as we will see, the bulk of Danish FDI and international business

activity is concentrated in Europe and North America, so this is mainly an

inter-OECD form of activity.

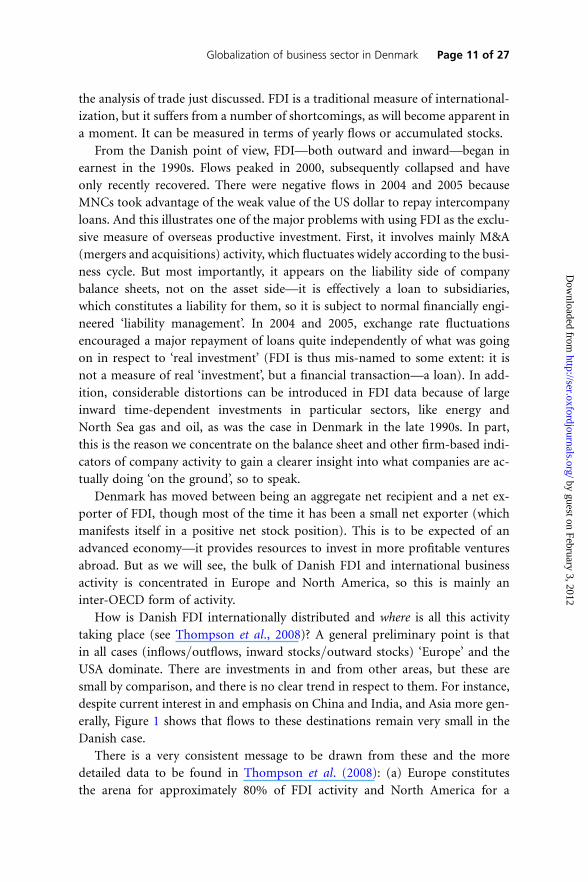

How is Danish FDI internationally distributed and where is all this activity

taking place (see Thompson et al., 2008)? A general preliminary point is that

in all cases (inflows/outflows, inward stocks/outward stocks) ‘Europe’ and the

USA dominate. There are investments in and from other areas, but these are

small by comparison, and there is no clear trend in respect to them. For instance,

despite current interest in and emphasis on China and India, and Asia more gen-

erally, Figure 1 shows that flows to these destinations remain very small in the

Danish case.

There is a very consistent message to be drawn from these and the more

detailed data to be found in Thompson et al. (2008): (a) Europe constitutes

the arena for approximately 80% of FDI activity and North America for a

Globalization of business sector in Denmark Page 11 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

further 10%, and (b) as of 2007, there was no clear trend away from this domin-

ance. To a remarkable extent, these FDI data mirror the results emerging from the

trade data shown in Table 1 above.

5. Danish large company analysis: global or regional?

We began the analysis of Danish large companies (DLCs) by scrutinizing the top

40 companies by turnover in 2007, as listed in the 2008 DK 1000 list (www.borsen

.dk) and then eliminated any that were financial companies or the subsidiaries of

foreign-owned multinationals. Financial companies report their data in a funda-

mentally different way than do other commercial companies: they mainly con-

centrate upon deposits, and their assets are overtly financial, which tend to be

registered on a simple foreign/domestic basis, so they do not lend themselves

to the kind of geographical analysis we wanted to present here. In addition, we

wanted to concentrate upon Danish-owned and -controlled companies, hence

foreign-owned subsidiaries were also eliminated. Then, we eliminated any com-

panies that were state-owned and totally domestic in terms of their business ac-

tivity (e.g. Post Danmark) and the subsidiaries of larger Danish companies (e.g.

Dagrofa). This reduced the list to 25 companies, from which we extracted the top

20 companies in terms of turnover. We then collected data from the latest

Figure 1 FDI outflows, 2004–2007.

Page 12 of 27 G. F. Thompson and L. B. Kaspersen

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

accounting year for these companies (2007). The collection of data from pub-

lished accounts was supplemented by direct contact with those companies that

only produced sketchy data in their accounts or none at all.

The bulk of the following analysis concentrates on company turnover. But this

may not be an unambiguous indicator for the ‘largest’ companies. Alternative

measures of size could be stock-market capitalization or assets. Looking at

assets produced, three more ‘large’ Danish companies figured in the top 20 mea-

sured by assets but were not in the top 20 measured by turnover. One company

did not respond to our enquiries about the geographical extent of its operations

after several promptings (Lego).

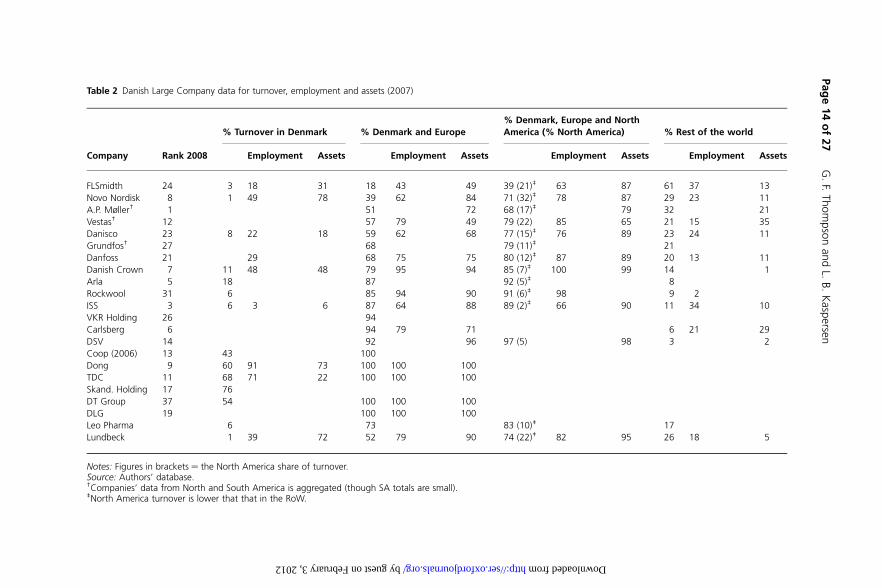

We added the remaining two companies into our data analysis, giving 22 com-

panies in all. These companies and their turnover, employment and asset posi-

tions are recorded in Table 2, broken down into the geographical areas of their

locations. These data were supplemented with a more limited set of data on

the location of capital expenditures for 11 of the companies (the details are not

shown here—see Thompson et al. (2008, p. 27, table 11)—but are included at

the bottom of Table 3 for the allocation to geographical locations).

Here we need to introduce an important observation in respect to these com-

panies: they are very heterogeneous in their characteristic sector affiliations. All

they have in common is that they are ‘large’ on the basis of our measures.

Should we have differentiated them on the basis of the sectors, so that we

could formulate some reasonable expectations as to the extent and character of

their likely internationalization? This could vary quite considerably, for instance

between manufacturing, service or agricultural companies or diversified con-

glomerates, some of these having more obvious potential for internationalization

than others. We did not do this, however, (a) because of the small number of

companies that could be reasonably handled in our sample; (b) because this is

not what other analyses have done, with which we wanted to retain some com-

parability and (c) because we deliberately wanted to investigate the large

company sector as a whole so as to make some overall judgment about ‘globaliza-

tion’ in the Danish case, which itself is an object of considerable comment in

Danish civil and public life.

In 2007 the 20 ‘turnover’ companies shown at the top of Table 2 accounted for

about 13% of Danish GNP. If we do exactly the same calculation for 2000—using

the same set of companies—the figure is approximately 11%. So there was a

modest growth of importance of these companies in overall GNP between

2000 and 2007 (the ‘top 20’ in 2000 were different to those in 2007—but we

took the same set of companies for both years). The set of companies in the

DLC list are from a variety of sectors. We can aggregate these sectors to find

their overall significance for the economy. We did this for value-added (v-a) in:

agriculture and fisheries; manufacturing; construction; wholesale and retail and

Globalization of business sector in Denmark Page 13 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

Table 2 Danish Large Company data for turnover, employment and assets (2007)

Company Rank 2008

% Turnover in Denmark % Denmark and Europe

% Denmark, Europe and North

America (% North America) % Rest of the world

Employment Assets Employment Assets Employment Assets Employment Assets

FLSmidth 24 3 18 31 18 43 49 39 (21)‡ 63 87 61 37 13

Novo Nordisk 8 1 49 78 39 62 84 71 (32)‡ 78 87 29 23 11

A.P. Møller† 1 51 72 68 (17)‡ 79 32 21

Vestas† 12 57 79 49 79 (22) 85 65 21 15 35

Danisco 23 8 22 18 59 62 68 77 (15)‡ 76 89 23 24 11

Grundfos† 27 68 79 (11)‡ 21

Danfoss 21 29 68 75 75 80 (12)‡ 87 89 20 13 11

Danish Crown 7 11 48 48 79 95 94 85 (7)‡ 100 99 14 1

Arla 5 18 87 92 (5)‡ 8

Rockwool 31 6 85 94 90 91 (6)‡ 98 9 2

ISS 3 6 3 6 87 64 88 89 (2)‡ 66 90 11 34 10

VKR Holding 26 94

Carlsberg 6 94 79 71 6 21 29

DSV 14 92 96 97 (5) 98 3 2

Coop (2006) 13 43 100

Dong 9 60 91 73 100 100 100

TDC 11 68 71 22 100 100 100

Skand. Holding 17 76

DT Group 37 54 100 100 100

DLG 19 100 100 100

Leo Pharma 6 73 83 (10)‡ 17

Lundbeck 1 39 72 52 79 90 74 (22)‡ 82 95 26 18 5

Notes: Figures in brackets ¼ the North America share of turnover.Source: Authors’ database.†Companies’ data from North and South America is aggregated (though SA totals are small).‡North America turnover is lower that that in the RoW.

Pag

e14

of

27

G.

F.Th

om

pso

nan

dL.

B.

Kasp

ersen

by guest on February 3, 2012 http://ser.oxfordjournals.org/ Downloaded from

transport, post and telecommunications. This more or less covers the sectors in

which our companies operate. These sectors accounted for 47% of total Danish

v-a in 2007. When we then compared the v-a of our companies to this figure

they accounted for approximately 28%. Thus, our set of DLCs accounted for

nearly 30% of their sectoral v-a totals. Thus, we can reasonably claim that our

set of DLCs accounted for around 13% of Danish national output in 2007, and

for approximately 30% of their sectoral v-a. These are not trivial numbers for

just 20 companies.

But what are we to make of the data shown in Table 2? As in the case of

Rugman’s analysis discussed above, we wished to classify our companies accord-

ing to their degree of internationalization or globalization. We did this by deploy-

ing the following criteria:

(1) Domestically regional: more than 70% of activity in Europe (including

Denmark).

(2) Bi-regional: less than 70% in Europe; more than 10% in Europe and

North America.

(3) Genuinely global: less than 70% in Europe and North America; more than

30% outside Europe and North America.

These criteria are designed to reveal the extent of geographical distribution of

company activity. Thus the ‘genuinely global’ category indicates the greatest

spread across a number of regions and the rest of the world (RoW). On the

other hand, ‘domestically regional’ demonstrates a concentration just within

Europe. It should be noted, however, that these criteria are not exactly the

same as those deployed by Rugman and his various co-authors in their analyses

of turnover. Rugman et al. were able to generate four categories (including an

additional host-regional category), whereas we could not produce exactly the

same criteria or as many categories because of data limitations in our sample

of Danish companies. In part this was because we were also employing a larger

number of dimensions of internationalization. In fact, our criteria are in many

ways more ‘stringent’ than are Rugman et al.’s in terms of classifying the extent

of internationalization. For instance, we used a 70% cut-off for home-region

firms compared with Rugman et al.’s lower 50%. By adopting a higher threshold,

we wanted to allow for the possibility of considering Danish companies to be

more varied and extensive in the internationalization of their operations. In add-

ition, as commented on above, in the extensive re-evaluation of the thresholds for

company allocation in the Rugman et al. sample undertaken by Osegowitsch and

Summartino (2008), the reallocation did not amount to much or change the

picture significantly. The finding that most MNCs are not global remains

robust. Finally, we undertook some (limited) sensitivity re-classifaction of our

own data, which will be discussed in a moment. In addition, we also re-classified

Globalization of business sector in Denmark Page 15 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

our data to conform to the Rugman et al. criteria as far as possible, which is pre-

sented in the Appendix.

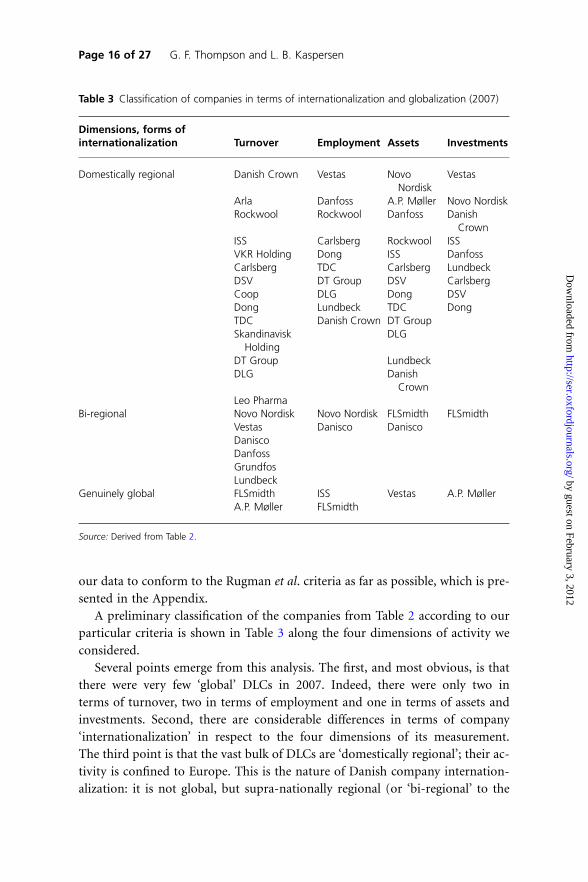

A preliminary classification of the companies from Table 2 according to our

particular criteria is shown in Table 3 along the four dimensions of activity we

considered.

Several points emerge from this analysis. The first, and most obvious, is that

there were very few ‘global’ DLCs in 2007. Indeed, there were only two in

terms of turnover, two in terms of employment and one in terms of assets and

investments. Second, there are considerable differences in terms of company

‘internationalization’ in respect to the four dimensions of its measurement.

The third point is that the vast bulk of DLCs are ‘domestically regional’; their ac-

tivity is confined to Europe. This is the nature of Danish company internation-

alization: it is not global, but supra-nationally regional (or ‘bi-regional’ to the

Table 3 Classification of companies in terms of internationalization and globalization (2007)

Dimensions, forms ofinternationalization Turnover Employment Assets Investments

Domestically regional Danish Crown Vestas NovoNordisk

Vestas

Arla Danfoss A.P. Møller Novo NordiskRockwool Rockwool Danfoss Danish

CrownISS Carlsberg Rockwool ISSVKR Holding Dong ISS DanfossCarlsberg TDC Carlsberg LundbeckDSV DT Group DSV CarlsbergCoop DLG Dong DSVDong Lundbeck TDC DongTDC Danish Crown DT GroupSkandinavisk

HoldingDLG

DT Group LundbeckDLG Danish

CrownLeo Pharma

Bi-regional Novo Nordisk Novo Nordisk FLSmidth FLSmidthVestas Danisco DaniscoDaniscoDanfossGrundfosLundbeck

Genuinely global FLSmidth ISS Vestas A.P. MøllerA.P. Møller FLSmidth

Source: Derived from Table 2.

Page 16 of 27 G. F. Thompson and L. B. Kaspersen

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

extent that North America is considered the second most important region for

business activity). Further considerations of the Table 2 data reveal that the

bulk of the companies included in this category also remain ‘national’ in their

business orientation. As might be expected, this result tends to mirror the

pattern emerging from the trade and FDI data discussed earlier, though there

is one significant difference: in the case of FDI, 90% of Danish investment was

in Europe and North America. In the company data, there is less emphasis on

these two regions: DLCs, at least, seem to be more widely geographically diversi-

fied than would be indicated by the FDI data alone, though they are similar in

respect to the trade data.

The criteria for the classification of companies are inevitably arbitrary—as

discussed above in connection to Osegowitsch and Sammartino’s (2008) criticism

of Rugman et al. So, as part of a sensitivity analysis, we varied these criteria by

amalgamating the data into just two categories: Denmark plus Europe and

RoW (now including North America). Supposing we were then to make

another arbitrary division to distinguish ‘domestically regional’ from ‘inter-

national’ companies on the basis of a 60:40 percentage split, this would put

FLSmidth, Novo Nordisk, A.P. Møller, Vestas, Danisco and Lundbeck into the

‘international category’ as far as turnover is concerned (and for Vestas on

assets—but there is too little information from the other companies for further

allocation).

As mentioned above, we were also able to collect some data on where our com-

panies placed their capital investments. Few companies reported this (or would

reveal it after our enquiries), but it changes the picture of internationalization

somewhat. As shown at the bottom of Table 3 for 2007, A.P. Møller becomes

the only ‘genuinely global’ company, while FLSmidth becomes ‘bi-regional’.

The rest are all ‘domestically regional’. The difficulty with this measure,

however, is that it is likely to fluctuate widely as it can be dependent upon a

large project investment somewhere that may only appear in that geographical

area data for a single year or two.

We can observe several of these differential trends by examining three compan-

ies for which we have relatively comprehensive data over time. Novo Nordisk is a

pharmaceutical company that specializes in the production and sale of insulin. It

was founded in 1923, and it has expanded abroad to produce in five countries

(including the USA, Japan and Brazil). It is listed on the Copenhagen, London

and New York stock exchanges. But despite this long embrace of internationaliza-

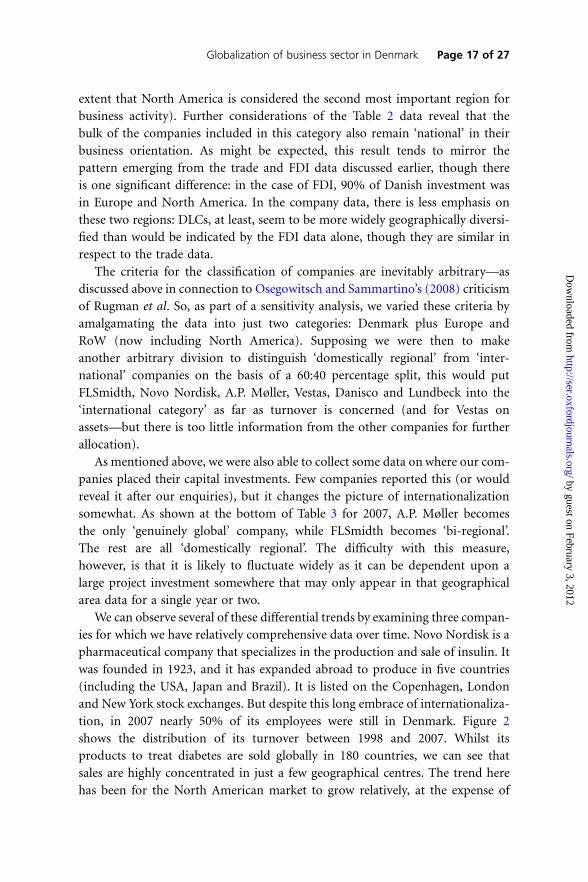

tion, in 2007 nearly 50% of its employees were still in Denmark. Figure 2

shows the distribution of its turnover between 1998 and 2007. Whilst its

products to treat diabetes are sold globally in 180 countries, we can see that

sales are highly concentrated in just a few geographical centres. The trend here

has been for the North American market to grow relatively, at the expense of

Globalization of business sector in Denmark Page 17 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

Europe, Japan and Oceania, with the RoW remaining of about the same relative

importance.

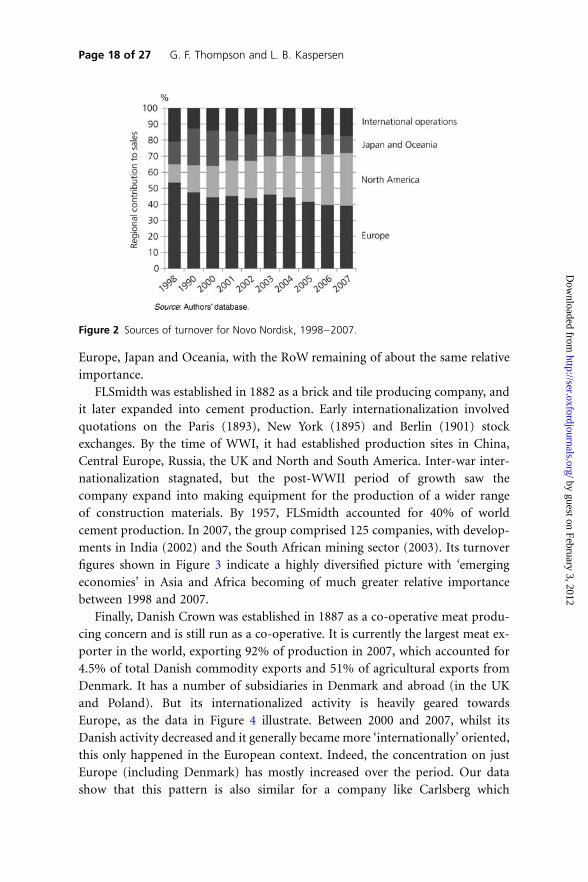

FLSmidth was established in 1882 as a brick and tile producing company, and

it later expanded into cement production. Early internationalization involved

quotations on the Paris (1893), New York (1895) and Berlin (1901) stock

exchanges. By the time of WWI, it had established production sites in China,

Central Europe, Russia, the UK and North and South America. Inter-war inter-

nationalization stagnated, but the post-WWII period of growth saw the

company expand into making equipment for the production of a wider range

of construction materials. By 1957, FLSmidth accounted for 40% of world

cement production. In 2007, the group comprised 125 companies, with develop-

ments in India (2002) and the South African mining sector (2003). Its turnover

figures shown in Figure 3 indicate a highly diversified picture with ‘emerging

economies’ in Asia and Africa becoming of much greater relative importance

between 1998 and 2007.

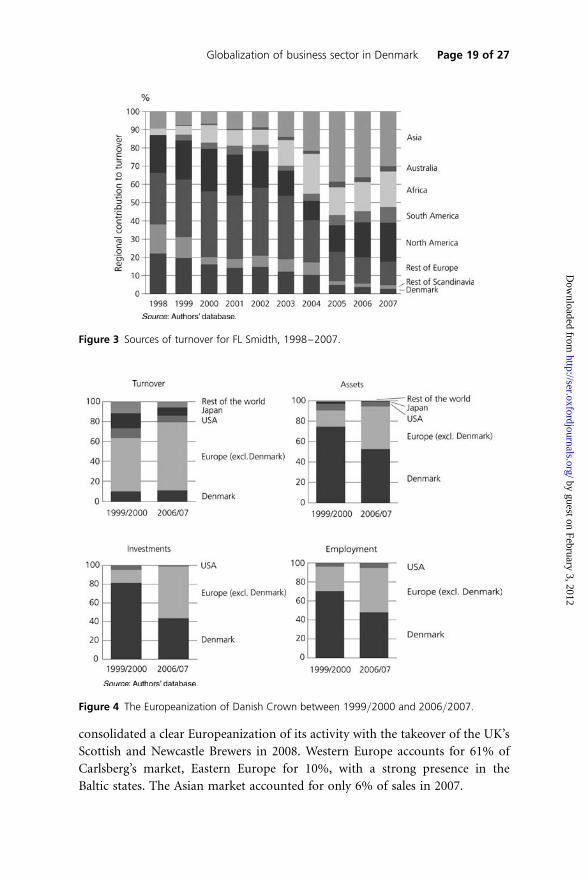

Finally, Danish Crown was established in 1887 as a co-operative meat produ-

cing concern and is still run as a co-operative. It is currently the largest meat ex-

porter in the world, exporting 92% of production in 2007, which accounted for

4.5% of total Danish commodity exports and 51% of agricultural exports from

Denmark. It has a number of subsidiaries in Denmark and abroad (in the UK

and Poland). But its internationalized activity is heavily geared towards

Europe, as the data in Figure 4 illustrate. Between 2000 and 2007, whilst its

Danish activity decreased and it generally became more ‘internationally’ oriented,

this only happened in the European context. Indeed, the concentration on just

Europe (including Denmark) has mostly increased over the period. Our data

show that this pattern is also similar for a company like Carlsberg which

Figure 2 Sources of turnover for Novo Nordisk, 1998–2007.

Page 18 of 27 G. F. Thompson and L. B. Kaspersen

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

consolidated a clear Europeanization of its activity with the takeover of the UK’s

Scottish and Newcastle Brewers in 2008. Western Europe accounts for 61% of

Carlsberg’s market, Eastern Europe for 10%, with a strong presence in the

Baltic states. The Asian market accounted for only 6% of sales in 2007.

Figure 4 The Europeanization of Danish Crown between 1999/2000 and 2006/2007.

Figure 3 Sources of turnover for FL Smidth, 1998–2007.

Globalization of business sector in Denmark Page 19 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

As mentioned above—and as a check on our approach—we re-classified the

data in Table 2 along the lines of the cut-off criteria used by Rugman (2005)

and set out (in Section 5) above. This is shown in Table A1 in the Appendix.

We were not able to develop a ‘host region’ category for the reasons given

above. The results confirm that using the Rugman et al. criteria—which put a

lower threshold on the category of ‘home region’—moves more companies

into the ‘international’ category and away from being considered bi-regional or

global in character.

6. Discussion and reflection

Several important issues arise from this analysis: the case of Danish Crown just

discussed illustrates the way ‘closeness’ remains a key element in Danish inter-

nationalization. Its agricultural enterprises traditionally took the UK and

Germany as their major markets because (a) they are nearby; (b) they have

large populations and, thus, present a substantial marketing opportunity and

(c) there have traditionally been commercial and political connections between

these countries stretching back a long time (not all of which have been peaceful,

of course). Recently, Sweden has become another important market in this

respect.

In addition, Denmark has profited from a general ‘liberal Atlantic economy’

since the post-WWII period: it has developed strong ties across North American

markets as a consequence of the open economy typifying the North Atlantic.

Denmark accepted American technology and standards early after the war and

by doing so quickly increased exports to the USA and tapped into the US

economy in general. And its FSAs have chimed with the CSAs found in

North America, enabling institutional and cultural differences to be easily

negotiated. An additional important ingredient is the way de-jure and de-facto

forces have complemented each other in the case of the EU. The explicit ‘trans-

regional institution building’ of the EU has served to reduce LoF and to strength-

en common CSAs, into which Danish MNCs can more effectively tap, adapt and

develop their RFSAs.

Referring to our results, turnover or sales—the traditional indicator of inter-

nationalization—is an ‘upstream’ measure looking towards the consumer. Assets

and investments are ‘downstream’ indicators looking towards ‘internal’ produc-

tion and process strategies. Employment is also a downstream measure. These

present different problems and issues as far as overall FSAs are concerned. And

sector difference in these respects would also be important. Service companies

like ISS (mainly employment based) look different to big, R&D-led pharmaceut-

ical companies like Novo-Nordisk, or to heavy ‘asset-rich and investment-led’

Page 20 of 27 G. F. Thompson and L. B. Kaspersen

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

companies like FLSmidth and A.P. Moller in terms of the kinds of CSAs and

company RFSAs that become relevant.

But what of the future? First, we are dealing only with large companies, but the

traditional Danish model has also stressed SMEs. The existing large companies

expanded their operations and markets overseas in the post-war period,

though particularly from the early 1990s on, if FDI data are a good indicator.

This coincided with (a) the formation and development of the EU’s internal

market and expansion of membership, opening up new marketing opportunities

within Europe; and (b) a relatively stable and benign liberalization of the inter-

national economy, particularly across the North Atlantic. Are new Danish

SMEs faced with a different set of circumstances in terms of their international-

ization strategies? These could include: (a) technological changes that have made

managing, monitoring and controlling overseas operations at long distances

easier; (b) a need to internationalize earlier in the ‘product life cycle’ because

of the smallness of the Danish domestic market: the emphasis is upon reaping

scale and scope economies earlier; (c) possible ‘shrinkage’ of cultural and institu-

tional difference across regions: inter-regional barriers are lower; (d) the seeming

growth exhaustion of the twin Danish markets of the EU and North America:

these are likely to be low growth areas in the future and (e) the emergence of

Asia in particular as a dynamic and expansionary regional area that should be

tapped as quickly as possible by Danish companies.

Herein lie the large strategic issues facing Danish public policy, as well as the

policy of its companies. Do they continue with those areas of traditional ‘revealed

comparative advantage’ (EU/Europe and North America), or should they move

quickly to tap into ‘emerging Asia’? This strategic dilemma is not just confronting

Denmark, but many SOEs in Europe and beyond. They face the same or similar

dilemmas, and it poses issues for the public authorities in their role as enablers

and fosterers of industrial policy. Should they actively encourage such a strategic

reorientation and focus-move on the part of their companies, and if so, how

should they do it and when? This is where the results of our analysis are particu-

larly important. Broadly speaking, the empirics of the Danish case indicate that

the Danish large business sector is closer to our inter-nationalized model of

the international economy than it is to a globalized model. This implies that

there still exists more room for manoeuvre on the part of the public authorities

in their attempts to encourage or influence their large companies than if these had

become genuinely global in their scope and strategy. And even the close integra-

tion of some Danish companies into the European regional market does not com-

pletely undermine this capacity, as Denmark is a member of the European Union

which gives the Danish authorities a voice in European decision-making, which

could help to effectively foster the advantages of their own firms.

Globalization of business sector in Denmark Page 21 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

This raises the issue of whether Danish companies and authorities should rec-

ognize that their FSAs remain RSFAs in the main, which can still more effectively

tap into the CSAs of their traditional spheres of operations. Here we should

perhaps draw a sharper distinction between upstream and downstream opera-

tions. It is perfectly possible for public policy to encourage expansion of sales

and turnover (marketing) to newly emerging regions and for Danish MNCs to

develop effective marketing strategies there, thus expanding the ‘global’ nature

of their sales effort. There is an issue of scale here—the ‘emerging market econ-

omies’ are large and growing fast. But at the same time, should Danish firms be

more cautious about developing production platforms in these areas, where

transaction costs and LoF are likely to be higher? Thus, any headlong dash to

reap the labour cost advantages in these areas could be outweighed by the high

transaction costs in other respects. If there are return-on-asset advantages asso-

ciated with supra-national regionalization relative to global strategies by firms

(of which there is tentative emergent evidence), this reinforces caution both on

the part of companies and public authorities.

Clearly, in Dunning’s terms (Dunning and Lundan, 2008), Danish MNCs are

unlikely to be significant natural resource seekers in their internationalization ac-

tivities. They are more likely to be market seekers—looking to supply foreign

markets from overseas production platforms. But the extent to which they are

additionally efficiency seekers or strategic asset seekers is where the main

debate lies. But this is not in itself dependent upon them necessarily ‘going

global’ to achieve any of these objectives. Danish MNCs might benefit in all

these respects from taking only modest steps in terms of the locational diversifi-

cation of their business strategies.

7. Conclusions

The main conclusion to be drawn from this analysis is the ‘home-oriented’ nature

of Danish MNC activity along all the dimensions scrutinized, even if this is a re-

gionally centred one. Thus MNCs still rely on their home- and regional-base as

the centre for their economic activities, despite all the speculation about global-

ization. From these results, we should be reasonably confident that, in the aggre-

gate, large Danish international companies are still predominantly MNCs (with a

clear home-base to their operations) and not TNCs (which represent footloose,

stateless companies). And this gives an added pertinence to the opening analytical

discussion of the two modalities of internationalization. The fact that the Danish

case speaks more fully to the inter-nationalization of its large companies, rather

than to their globalization, provides a space for public policy to be more effective

in acting on company strategies if this were thought to be appropriate by the

authorities.

Page 22 of 27 G. F. Thompson and L. B. Kaspersen

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

However, it is worth raising a possible caveat to this conclusion. A strong

feature of the globalization thesis is that joint ventures, partnerships, strategic

alliances and liaisons are drawing firms into increasingly interdependent inter-

national networks of business activity (see Rugman and Verbeke, 2008, p. 331).

A potential problem, then, with the quantitative data presented in this article is

that they do not capture this qualitative change in company business strategies.

The fact that only 20–25% of company activity is conducted abroad does not

of itself tell us anything about the strategic importance of that 20–25% to the

overall business activity of firms. It might represent the key to their performative

success both internationally and domestically. The fact that there is evidence of a

wider international dispersion of subsidiaries and affiliates than turnover or

assets (Arregle et al., 2009) could be taken as an indicator of this ‘networking’

trend in operation.

In addition, thinking about the configuration of the MNC and the kinds of

‘clusters’ into which it inserts itself to extract tacit and formal knowledge as a

double network articulation—first as the MNC itself conceived in network

terms and second as productive clusters are similarly conceptualized—has

enabled the advantages of agglomeration economies to be focussed upon in

complex chains of international activities (Andersen and Christensen, 2005; Lor-

enzen and Mahnke, 2008). But this has also highlighted the problem of potential

agglomeration diseconomies if this strategy overstretches the capacities of MNCs

to compete in local markets and underestimates the strength of very specific local

factors to the dynamics of such clusters.

Thus, in this article the arguments of Hirst et al. (2009) and Rugman (2005)

have been tested on large companies in the case of one of the most successful

SOEs of the last 15 years, one that has exploited the general internationalization

of the economy since the early 1990s. Consequently, we could expect that com-

panies embedded in a strongly internationalized open economy would be at

the frontline of globalization. At least for Denmark, this has not been demon-

strated to be the case.

Apart from proving the point that MNCs are less globalized than we think,

this finding also has policy implications both for companies and governments

in SOEs. Since there exist several geographical, institutional and cultural bar-

riers to further globalization, it is crucial for companies and governments to

reflect upon the future. Should the companies remain in their well-known

markets (Europe and North America), or should they expand in Asia? And

if the latter, with what strategy? Increase market share, the establishment of

production facilities or R&D etc.? And what sort of strategy should govern-

ments facilitate?

The next step should be an analysis of the small- and medium-sized companies

and their level of internationalization. It would be important to test whether the

Globalization of business sector in Denmark Page 23 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

more recent SMEs are more globalized. Also, do these operate as bi-regional com-

panies, or are they either more supra-nationally regional or global? This would

add an important contribution to understanding the future of the Danish

model. Additionally, this needs to look into how the government has facilitated

or constrained the internationalization and globalization of Danish SMEs, as

well as the large companies. Has the government made strategic moves to

prepare the businesses for successful internationalization?

Acknowledgements

We would like to acknowledge the excellent research assistance of Stine Haakons-

son. In addition, we wish to thank several anonymous referees who provided

expert comments and guidance during the drafting of this article, which un-

doubtedly improved its style and argument.

Appendix

Table A1 Classification of companies in terms of internationalization and global-

ization, 2007

Forms of firminternationalization Turnover Employment Assets Investments

Home regional (morethan 50% in homeregion)

A.P. Møller Novo Nordisk Novo Nordisk FL SmidthVestas Vestas A.P. Møller Novo NordiskDanisco Danisco Danisco A.P. MøllerGrundfos Danfoss Danfoss VestasDanfoss Danish Crown Danish Crown Danish CrownDanish Crown Rockwool Rockwool ISSArla ISS ISS DanfossRockwool Carlsberg Carlsberg LundbeckISS Dong DSV CarlsbergVKR Holding TDC Dong DVSCarlsberg DT Group TDC DongDSV DLG DT GroupCoop Lundbeck DLGDong LundbeckTDCSkandinavisk HoldingDT GroupDLGLeo PhamaLundbeck

Continued

Page 24 of 27 G. F. Thompson and L. B. Kaspersen

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

Table A1 Continued

Forms of firminternationalization Turnover Employment Assets Investments

Bi-regional (less than50% in home regionand greater than 20%in another region)(Host regional)

Novo Nordisk FL Smidth FL Smidth

Global (less than 50% inhome region andgreater than 20% ineach of the otherregions)

FL Smidth Vestas

Notes: Classification according to Rugman’s criteria (Rugman, 2005).We could not generate any entries for the ‘Host regional’ category from our data.Source: Authors’ database.

References

Andersen, P. H. and Christensen, P. R. (2005) From Localized to Corporate Excellence: How

do MNCs Extract, Combine and Disseminate Sticky Knowledge From Regional Innovation

Systems?, DRUID Working Paper No. 05-16, Copenhagen, Danish Research Unit for In-

dustrial Dynamics.

Arregle, J.-L., Beamish, P. W. and Hebert, L. (2009) ‘The Regional Dimension of MNEs’

Foreign Subsidiary Localization’, Journal of International Business Studies, 40, 86–107.

Collinson, S. and Rugman, A. (2007) ‘The Regional Character of Asian Multinational

Enterprises’, Asia Pacific Journal of Management, 24, 429–446.

Collinson, S. and Rugman, A. (2008) ‘The Regional Nature of Japanese Business’, Journal of

International Business Studies, 39, 215–230.

Disdier, A.-C. and Head, K. (2008) ‘The Puzzling Persistence of the Distance Effect on

Bilateral Trade’, The Review of Economics and Statistics, 90, 37–48.

Dunning, J. and Lundan, S. M. (2008) Multinational Enterprises and the Global Economy,

2nd edn, Cheltenham, Edward Elgar.

EUROSTAT (2009) External and Intra-European Union Trade, 2002–2007, Luxembourg,

Eurostat, European Commission.

Ghemawat, P. (2007) Redefining Global Strategy: Crossing Borders in a World Where Differ-

ences Still Matter, Cambridge, MA, Harvard Business School Press.

Hirst, P. Q. and Thompson, G. F. (1999) Globalization in Question: The International

Economy and the Possibilities of Governance, Cambridge, Polity Press.

Hirst, P., Thompson, G. and Bromley, S. (2009) Globalization in Question, 3rd edn, Cam-

bridge, Polity Press.

Globalization of business sector in Denmark Page 25 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

Kostova, T. (1999) ‘Transnational Transfer of Strategic Organizational Practice: A Context-

ual Perspective’, The Academy of Management Review, 24, 308–324.

Kostova, T., Athanssiou, N. and Berdrow, I. (2004) ‘Managing Knowledge in Global

Organizations’. In Lane, H. W., Maznevski, M. L., Mendenhall, M. E. and McNett, J.

(eds) The Blackwell Handbook of Global Management, Oxford, Blackwell Publishing,

pp. 275–288.

Kostova, T., Roth, K. and Dacin, M. T. (2008) ‘Institutional Theory in the Study of Multi-

national Corporations: A Critique and New Directions’, The Academy of Management

Review, 33, 994–1006.

Kristensen, P. H. and Zeitlin, J. (2005) Local Players in Global Games: The Strategic Consti-

tution of a Multilateral Corporation, Oxford, Oxford University Press.

Lorenzen, M. and Mahnke, V. (2008) Global Strategy and the Acquisition of Local Knowl-

edge: How MNCs Enter Regional Knowledge Clusters, DRUID Working Paper 08-01, Co-

penhagen, Danish Research Unit for Industrial Dynamics.

Minda, A. (2008) The Strategies of Multilatinas: From the Quest for Regional Leadership to

the Myth of the Global Corporation, GRES Cahier No. 208–08, Bordeaux/Toulouse,

Groupement de Recherches Economiques et Sociales, accessed at http://www.gres-so.

org on May 7, 2011.

Osegowitsch, T. and Sammartino, A. (2008) ‘Reassessing (home-)regionalisation’, Journal

of International Business Studies, 39, 184–196.

Rugman, A. (2005) The Regional Multinationals, Cambridge, Cambridge University Press.

Rugman, A. (2008) ‘Regional Multinationals and the Myth of Globalization’. In Cooper,

A. F., Hughes, C. W. and Lombaerde, P. d. (eds) Regionalisation and Global

Governance: The Taming of Globalization? London and New York, NY, Routledge,

pp. 99–117.

Rugman, A. and Brain, C. (2004) ‘The Regional Nature of the World’s Banking Sector’, The

Multinational Business Review, 12, 5–22.

Rugman, A. and Collinson, S. (2004) ‘The Regional Nature of the World’s Automotive

Sector’, European Management Journal, 22, 471–482.

Rugman, A. and Collinson, S. (2005) ‘Multinational Enterprises in the New Europe: Are

They Really Global?’, Organizational Dynamics, 34, 258–272.

Rugman, A. and Girod, S. (2003) ‘Retail Multinationals and Globalization: The Evidence is

Regional’, European Journal of Management, 21, 24–37.

Rugman, A. and Verbeke, A. (2005) ‘Towards a Theory of Regional Multinationals: A

Transactions Cost Economics Approach’, Management International Review Special

Issue, 45, 5–17.

Rugman, A. and Verbeke, A. (2008) ‘The Theory and Practice of Regional Strategy: A

Response to Osegowitsch and Sammartino’, Journal of International Business Studies,

39, 326–332.

Page 26 of 27 G. F. Thompson and L. B. Kaspersen

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from

Thompson, G. F., Kaspersen, L. B. and Haakonsson, S. (2008) The ‘Globalization’ or ‘Inter-

nationalization’ of Danish Large Companies?, Copenhagen, Centre for Business and

Politics, Copenhagen Business School.

UNCTAD (1997) World Investment Report 1997: Transnational Corporations, Market Struc-

ture and Competition Policy, New York, NY, Geneva, UN.

Wolf, H. C. (1997) Pattern of Intra- and Inter-state Trade, NBER Working Paper No. 5939,

Cambridge, MA, National Bureau of Economic Research.

Globalization of business sector in Denmark Page 27 of 27

by guest on February 3, 2012http://ser.oxfordjournals.org/

Dow

nloaded from