the compound poisson risk model with a threshold dividend strategy

TRANSCRIPT

The Compound Poisson Risk Model with a Threshold Dividend

Strategy

X. Sheldon Lin

Department of Statistics

University of Toronto

Toronto, ON, M5S 3G3

Canada

tel.: (416) 946-5969

fax: (416) 978-5133

e-mail: [email protected]

Kristina P. Pavlova

Department of Statistics

University of Toronto

Toronto, ON, M5S 3G3

Canada

tel.: (416) 946-7582

fax: (416) 978-5133

e-mail: [email protected]

April 11, 2005

1

Abstract

In this paper we discuss a threshold dividend strategy implemented into the classi-

cal compound Poisson model. More specifically, we assume that no dividends are paid

if the current surplus of the insurance company is below certain threshold level. When

the surplus is above this fixed level, dividends are paid at a constant rate that does

not exceed the premium rate. This model may also be viewed as the compound Pois-

son model with the two-step premium rate. Two integro-differential equations for the

Gerber-Shiu discounted penalty function are derived and solved. When the initial sur-

plus is below the threshold, the solution is a linear combination of the Gerber-Shiu func-

tion with no barrier and the solution of the associated homogeneous integro-differential

equation. This latter function is proportional to the product of an exponential function

and a compound geometric distribution function. When the initial surplus is above the

threshold, the solution involves the respective Gerber-Shiu function with initial surplus

lower than the threshold level. These analytic results are utilized to find the probabil-

ity of ultimate ruin, the time of ruin, the distribution of the first surplus drop below

the initial level, and the joint distributions and moments of the surplus immediately

before ruin and the deficit at ruin. The special cases where the claim size distribution

is exponential and a combination of exponentials are considered in some detail.

Keywords:

compound Poisson model, deficit at ruin, Gerber-Shiu discounted penalty function, surplus

immediately before ruin, time of ruin, threshold strategy, two-step premium

Acknowledgements:

This work is partly supported by a grant from the Natural Sciences and Engineering Council

of Canada. Part of the work was completed during the first author’s visit to the Department

of Statistics and Actuarial Science, University of Hong Kong. He would like to thank K.W.

Ng and H.L. Yang for their invitation and hospitality.

1 Introduction

The classical compound Poisson risk model without constraints and related problems have

been studied extensively. See Bowers et al. (1997, Chapter 13), Gerber (1979), Klugman et

1

al. (2004), Panjer and Willmot (1992) and references therein. Recently, Gerber and Shiu

(1998) introduced a discounted penalty function with respect to the time of ruin, the surplus

immediately before ruin and the deficit at ruin to analyze these and related quantities in a

unified manner. The Gerber-Shiu discounted penalty function has proven to be a powerful

analytical tool. Various new results on the compound Poisson risk model have been obtained

since. See Gerber and Shiu (1998) and Lin and Willmot (1999, 2000). The function has also

been employed in Spare Andersen risk models (see Li and Garrido (2004a), Gerber and

Shiu (2005b) and references therein) and the compound Poisson risk model with a dividend

strategy, which will be discussed below.

Dividend strategies for insurance risk models were first proposed by De Finetti (1957) to

reflect more realistically the surplus cash flows in an insurance portfolio. Barrier strategies

for the compound Poisson risk model have been studied in a number of papers and books,

including Albrecher et al. (2005), Albrecher and Kainhofer (2002), Buhlmann (1970, Section

6.4.9), Dickson and Waters (2004), Gerber (1972), Gerber (1973), Gerber (1979), Gerber

(1981), Gerber and Shiu (1998), Gerber and Shiu (2005a), Højgaard (2002), Lin et al. (2003),

Paulsen and Gjessing (1997), and Segerdahl (1970).

Two surplus-dependent dividend strategies are of particular interest. The first is the

constant barrier strategy under which no dividend is paid when the surplus is below a

constant barrier but the total of the surplus above the barrier is paid out as dividends.

It is shown in Gerber (1969) that this strategy is optimal for the compound Poisson risk

model when the initial surplus is below the barrier. The other is the so-called threshold

strategy under which no dividends are paid when the surplus is below a constant barrier

and dividends are paid at a rate less than the premium rate when the surplus is above the

barrier. Obviously, the former strategy can be considered as a special case of the latter.

Gerber and Shiu (2005a) show that the threshold strategy is optimal when the dividend rate

is bounded from above and the individual claim distribution is exponential.

In Lin et al. (2003), the constant barrier strategy for the compound Poisson risk model is

studied thoroughly. It is shown there that the Gerber-Shiu discounted penalty function can

be expressed as a combination of two functions: the Gerber-Shiu discounted penalty function

for the compound Poisson model without a barrier and an explicit function of the tail of a

particular compound geometric distribution. Results regarding the time of ruin and related

quantities are derived. These results are generalized further by Li and Garrido (2004b).

In this paper we consider the Gerber-Shiu discounted penalty function for the compound

2

Poisson risk model under the threshold strategy. We thus provide a generalization of the

model and results in Lin et al. (2003). To introduce the model formally, let {Y1, Y2, ...} be

independent and identically distributed (i.i.d.) positive random variables representing the

successive individual claim amounts. These random variables are assumed to have common

cumulative distribution function (c.d.f.) P (y) = 1 − P (y), y ≥ 0, with probability density

function (p.d.f.) p(y) = P ′(y) and Laplace transform p(s) =∫∞

0e−sydP (y). Furthermore, let

the total number of claims up to time t, denoted by N(t) and independent of {Y1, Y2, ...}, be

a Poisson process with parameter λ > 0. Consequently, the respective i.i.d. interclaim-time

random variables {V1, V2, ...}, independent of {Y1, Y2, ...}, have an exponential distribution

with mean 1/λ. The aggregate claims process is defined by {S(t) =∑N(t)

i=1 Yi; t ≥ 0} where

S(t) = 0 if N(t) = 0.

For an insurer’s surplus process under the threshold strategy, denote u ≥ 0 to be the

initial surplus, b > 0 the constant barrier level, and c1 > 0 the annual premium rate. As

usual, we write c1 = (1 + θ1)λE{Y1}, where θ1 > 0 is the relative security loading. Let

α, 0 < α ≤ c1, be the annual dividend rate, i.e., when the surplus is above the barrier b,

dividends are paid at rate α. In this case, the net premium rate after dividend payments is

c2 = c1 − α ≥ 0. Similarly, we set c2 = (1 + θ2)λE{Y1} and note that the relative security

loading θ2 may be non-positive. The surplus process {Ub(t); t ≥ 0} can be expressed as

dUb(t) =

{c1dt− dS(t), Ub(t) ≤ b

c2dt− dS(t), Ub(t) > b,

and the time of (ultimate) ruin is defined as Tb = inf{t |Ub(t) < 0} where Tb = ∞ if ruin

does not occur in finite time. See Figure 1 for a graphical representation of a sample path

of the surplus process.

Several remarks are now made. If b = ∞, the threshold risk model reduces to the classical

model without constraints. As discussed in Lin et al. (2003), although the classical Poisson

model may be viewed as a limiting case of the present risk model, the results obtained in

this paper are not applicable. If α = c1, the threshold model coincides with the compound

Poisson model under the constant barrier strategy, studied in more detail by Lin et al. (2003).

Finally, this risk model may be interpreted as a compound Poisson model with a two-step

premium rate as discussed in Asmussen (2000, Chapter VII, Section 1) and Zhou (2004).

We now introduce the Gerber-Shiu discounted penalty function

m(u; b) = E{e−δTbw(Ub(Tb−), |Ub(Tb)|)I(Tb < ∞)|Ub(0) = u},

3

-t

6

0

u

Ub(t)

b

Ub(T−)

|Ub(T )|Tb

premium rate¾ -c1premium rate¾ -c2

Figure 1: Graphical representation of the surplus process Ub(t)

where δ ≥ 0 is interpreted as the force of interest or the variable of a Laplace transform,

w(x1, x2), x1 ≥ 0, x2 ≥ 0, is a nonnegative function of the surplus immediately before ruin,

x1, and the deficit at ruin, x2, and I(E) is the indicator function of an event E.

A number of particular cases of the discounted penalty function lead to important quanti-

ties of interest in risk theory. For instance, setting w(x1, x2) = 1 for all x1, x2 ≥ 0, we obtain

the Laplace transform of the time of ruin. When δ = 0 and w(x1, x2) = 1 for all x1, x2 ≥ 0,

the discounted penalty function reduces to the probability of ultimate ruin. Another exam-

ple is the case δ = 0 and w(x1, x2) = xh1x

l2 with h and l being nonnegative integers. The

discounted penalty function produces then the joint moments of the surplus immediately

before ruin and the deficit at ruin.

The aim of this paper is to study the Gerber-Shiu discounted penalty function and its

special cases under the threshold strategy. So far, only limited number of results have been

obtained. Asmussen (2000, Chapter VII, Section 1) discussed the probability of ruin, and

more recently Gerber and Shiu (2005a) provided two intergo-differential equations satisfied

by the Laplace transform of the time of ruin. Zhou (2004) derived some analytical expressions

related to the joint distribution of the maximal surplus before ruin, the surplus immediately

before ruin and the deficit at ruin. In this paper, we derive two integro-differential equations

and then the general solution for the discounted penalty function. Utilizing the analytical

4

expression of the solution, we obtain results on the probability of ruin, the time of ruin, and

the joint distribution and moments of the surplus immediate before ruin and the deficit at

ruin.

The rest of the paper is organized as follows. Section 2 recalls properties of the translation

operator, first employed for risk processes by Dickson and Hipp (2001) and recently discussed

by Li and Garrido (2004a) and Gerber and Shiu (2005b). A concise review of some results

obtained in Lin et al. (2003) is also recalled. In particular, we recall the general solution

of an integro-differential equation, which is satisfied by the Gerber-Shiu discounted penalty

function under the compound Poisson risk model with a constant dividend barrier strategy.

In Section 3, we derive two integro-differential equations for the discounted penalty function

under the compound Poisson risk model with a threshold strategy. In Section 4 we obtain

a renewal equation satisfied by the discounted penalty function with initial surplus above

the threshold level via the translation operator. Analytical solutions of the two integro-

differential equations are presented in Section 5. In Sections 6 to 8, we apply the analytical

solutions to the probability of ultimate ruin, the Laplace transform of the time of ruin Tb,

and the joint distribution and moments of the the surplus before ruin Ub(Tb−), and the

deficit at ruin |Ub(Tb)|. These applications are also illustrated by examples where the claim

size distribution is specified to be exponential or a combination of exponential distributions.

2 Preliminaries

In this section, we first introduce the translation operator Ts and some of its properties. We

then discuss the general solution of an integro-differential equation that is satisfied by the

Gerber-Shiu discounted penalty function under the compound Poisson risk model with and

without a dividend barrier.

Let f be a real-valued (Riemannian) integrable function and s be a nonnegative real

number (or a complex number with nonnegative real part). The translation operator Ts on

a function f is defined by

Tsf(x) =

∫ ∞

x

e−s(y−x)f(y)dy.

The operator Ts is commutative, i.e. Tr Ts = Ts Tr. Moreover,

TsTrf(x) = TrTsf(x) =Tsf(x)− Trf(x)

r − s, s 6= r. (2.1)

For more properties of the translation operator, see Gerber and Shiu (2005b).

5

As it will be seen in the next two sections, the discounted penalty function under the

threshold strategy is closely related to the discounted penalty function under the dividend

strategy. We thus need then to employ some of the notation and results obtained in Lin et

al. (2003). For convenience, we recall these results and notation here.

Consider the integro-differential equation

m′(u) =λ + δ

c1

m(u)− λ

c1

∫ u

0

m(u− y)dP (y)− λ

c1

ζ(u), u ≥ 0, (2.2)

where

ζ(t) =

∫ ∞

t

w(t, y − t)dP (y). (2.3)

It is shown in Lin et al. (2003) that the general solution of (2.2) can be expressed as

m(u) = m∞(u) + κv(u), u ≥ 0, (2.4)

where κ is an arbitrary constant, m∞ is the discounted penalty function under the classical

compound Poisson risk model with premium rate c1, and the function v satisfies the integro-

differential equation

v′(u) =λ + δ

c1

v(u)− λ

c1

∫ u

0

v(u− y)dP (y), u ≥ 0.

Furthermore, assume that the surplus process has a positive relative security loading. For

i = 1 and 2, let ρi be the nonnegative root of the Lundberg fundamental equation

cis + λp(s)− (λ + δ) = 0. (2.5)

It is then known (see Buhlmann (1970, Section 6.4.9)) that

v(u) =1−Ψ(u)

1−Ψ(0)eρ1u, u ≥ 0, (2.6)

where Ψ is the solution of the equation

Ψ′(u) =λ

c1

∫ u

0

[1−Ψ(u− y)]dP (y)− λ

c1

[1−Ψ(u)], u ≥ 0,

with

c1 =c1

p(ρ1),

and the c.d.f. P satisfying

dP (y) =e−ρ1ydP (y)

p(ρ1).

6

Therefore, Ψ is the tail of a compound geometric distribution with geometric parameter

Ψ(0) =λ

c1

∫ ∞

0

t dP (t),

and claim-size distribution, which has p.d.f. P (y)/∫∞0

t dP (t), y ≥ 0.

For i = 1 and 2, let Ai be the following c.d.f. defined through its tail

Ai(y) = 1− Ai(y) =

∫∞y

e−ρi(t−y)P (t)dt∫∞0

e−ρitP (t)dt=

TρiP (y)

TρiP (0)

, y ≥ 0. (2.7)

Obviously, it has the Laplace transform

ai(s) =

∫ ∞

0

e−sydAi(y) =ρi

1− p(ρi)· p(s)− p(ρi)

ρi − s. (2.8)

Let also define the parameter

πi =λ[1− p(ρi)]

ciρi

=λ

ci

TρiP (0), (2.9)

and observe that 0 < πi < 1 and when ρ → 0, πi → 1/(1 + θi). Then m∞ satisfies the

defective renewal equation

m∞(u) = π1

∫ u

0

m∞(u− y)dA1(y) +λ

c1

Tρ1ζ(u), u ≥ 0. (2.10)

See Gerber and Shiu (1998) or Lin and Willmot (1999) for more details concerning the

derivations.

3 Integro-Differential Equations for the Discounted Penalty Func-

tion

In this section, we derive two integro-differential equations for the discounted penalty func-

tion: one for the initial surplus below the barrier and the other for the initial surplus above

the barrier. As it will be seen later, the discounted penalty function with initial surplus

above the barrier depends on the respective function with initial surplus below the barrier.

The reverse relationship though, does not apply. We also identify a continuation condition

on the barrier.

7

Clearly, the discounted penalty function m(u; b) behaves differently, depending on whether

its initial surplus u is below or above the barrier level b. Hence, for notational convenience,

we write

m(u; b) =

{m1(u), 0 ≤ u ≤ b

m2(u), u > b.

The following theorem provides integro-differential equations for the function m(u; b).

Theorem 3.1. The discounted penalty function m(u; b) satisfies the integro-differential equa-

tions

m′(u; b) =

m′1(u) =

λ + δ

c1

m1(u)− λ

c1

∫ u

0

m1(u− y)dP (y)− λ

c1

ζ(u), 0 ≤ u ≤ b

m′2(u) =

λ + δ

c2

m2(u)− λ

c2

[ ∫ u−b

0

m2(u− y)dP (y)

+

∫ u

u−b

m1(u− y)dP (y)

]− λ

c2

ζ(u), u > b.

(3.1)

Proof. If we condition on the time and the amount of the first claim when 0 ≤ u ≤ b,

contingent on this time, there are two options: the first claim occurs before the surplus

has attained the barrier level or it occurs after attaining the barrier. When we consider

the amount of the first claim, there are two possibilities as well: after it the process starts

all over again with new initial surplus or the first claim leads to ruin. Implementing these

considerations we obtain

m(u; b) = m1(u)

=

∫ b−uc1

0

e−δt

[∫ u+c1t

0

m(u + c1t− y; b)dP (y) +

∫ ∞

u+c1t

w(u + c1t, y − u− c1t)dP (y)

]λe−λtdt

+

∫ ∞

b−uc1

e−δt

[ ∫ b+c2(t− b−u

c1

)

0

m

(b + c2

(t− b− u

c1

)− y; b

)dP (y)

+

∫ ∞

b+c2(t− b−u

c1

) w

(b + c2

(t− b− u

c1

), y − b− c2

(t− b− u

c1

))dP (y)

]λe−λtdt

=λ

∫ b−uc1

0

e−(λ+δ)tγ(u + c1t; b)dt + λ

∫ ∞

b−uc1

e−(λ+δ)tγ

(b + c2

(t− b− u

c1

); b

)dt, (3.2)

where γ(t; b) =∫ t

0m(t− y; b)dP (y) + ζ(t).

8

Now, a change of variables in (3.2) results in

m1(u) =λ

c1

e(λ+δ)u/c1

∫ b

u

e−(λ+δ)t/c1γ(t; b) dt

+λ

c2

e(λ+δ)u/c1

∫ ∞

b

e−(λ+δ)[t−(c1−c2)b/c1]/c2γ(t; b) dt, 0 ≤ u ≤ b. (3.3)

By differentiating (3.3) with respect to u we achieve

m′1(u) =

λ

c1

· λ + δ

c1

e(λ+δ)u/c1

∫ b

u

e−(λ+δ)t/c1γ(t; b) dt− λ

c1

γ(u; b)

+λ

c2

· λ + δ

c1

e(λ+δ)u/c1

∫ ∞

b

e−(λ+δ)[t−(c1−c2)b/c1]/c2γ(t; b) dt

=λ + δ

c1

m1(u)− λ

c1

γ(u; b), 0 ≤ u ≤ b,

or equivalently,

m′1(u) =

λ + δ

c1

m1(u)− λ

c1

∫ u

0

m1(u− y)dP (y)− λ

c1

ζ(u), 0 ≤ u ≤ b.

Similarly, when u ≥ b,

m(u; b) = m2(u) =λ

c2

e(λ+δ)u/c2

∫ ∞

u

e−(λ+δ)t/c2γ(t; b)dt, (3.4)

and

m′2(u) =

λ + δ

c2

m2(u)− λ

c2

γ(u; b)

=λ + δ

c2

m2(u)− λ

c2

[∫ u−b

0

m2(u− y)dP (y) +

∫ u

u−b

m1(u− y)dP (y)

]− λ

c2

ζ(u),

by which the proof is concluded.

Theorem 3.1 may be linked to previously obtained results in the literature. Namely, both

pairs of equations (5.1), (5.2) and (10.2), (10.3) in Gerber and Shiu (2005a) are special cases

of the integro-differential equations (3.1) above, although the functions (5.1) and (5.2) are

not a special case of the discounted penalty function. Another instance of an already known

result is the case when c1 = c and c2 = 0. Equation (3.2) above reduces then to equation

(2.1) in Lin et al. (2003).

We note that equation (3.1) for m1 coincides with (2.2). Consequently, the general

analytical expression (2.4) for the solution of (2.2) applies. What remains is the parameter

κ that will be determined in the next section.

9

Observe also that the integro-differential equation (3.1) for m1 does not involve m2 but

the integro-differential equation (3.1) for m2 incorporates m1.

In conclusion of this section, we examine m(u; b) when u = b. Equations (3.3) and (3.4)

show that m(u; b) is continuous for u = b, i.e. m1(b) = m2(b) := limu→b+

m2(u). However, it is

not true for m′(u; b) at u = b. To see this, let u → b+ in the expression for m2(u) in (3.1)

and employ the integro-differential form of m1(b) in (3.1) afterwards. We then have

m′2(b) := lim

u→b+m′

2(u) =λ + δ

c2

m2(b)− λ

c2

∫ b

0

m1(b− y)dP (y)− λ

c2

ζ(b)

=λ + δ

c2

m1(b) +c1

c2

[m′

1(b)−λ + δ

c1

m1(b)

].

This results in an interesting identity:

c1m′1(b) = c2m

′2(b),

where the derivative m′1(b) is a left-derivative and the derivative m′

2(b) is a right-derivative.

Thus, the discounted penalty function is continuous but not differentiable.

4 A Renewal Equation for the Discounted Penalty Function m2(u)

In this section, utilizing the translation operator introduced in Section 2 we derive a renewal

equation for the discounted penalty function m2(u), u > b. It is assumed that the relative

security loading for the net premium rate is positive, i.e., θ2 > 0. For a non-positive relative

security loading, the time to ruin is finite and the case will be discusses elsewhere.

Theorem 4.1. The function m2 satisfies

m2(u) = π2

[∫ u−b

0

m2(u− y)dA2(y) +

∫ u

u−b

m1(u− y)dA2(y)

]+

λ

c2

Tρ2ζ(u), (4.1)

where π2, A2, and ζ are as defined in (2.9), (2.7), and (2.3) respectively.

Proof. We adopt a similar approach to the one utilized in Section 4 of Willmot and Dickson

(2003). For a fixed s > 0, we multiply the second equation of (3.1) by c2e−s(u−b) and integrate

with respect to u from b to ∞. By integration by parts, we obtain

c2

∫ ∞

b

e−s(u−b)m′2(u)du =c2

[−m2(b) + s

∫ ∞

b

e−s(u−b)m2(u)du

]

10

=c2s Tsm2(b)− c2m2(b)

=(λ + δ)Tsm2(b)− λ

∫ ∞

b

e−s(u−b)

∫ u−b

0

m2(u− y)dP (y)du

− λ

∫ ∞

b

e−s(u−b)

∫ b

0

m1(y)p(u− y)dydu− λTsζ(b)

=(λ + δ)Tsm2(b)− λ

∫ ∞

0

e−sy

∫ ∞

y+b

e−s(u−y−b)m2(u− y)dudP (y)

− λ

∫ b

0

m1(y)

∫ ∞

b

e−s(u−b)p(u− y)dudy − λTsζ(b)

=(λ + δ)Tsm2(b)− λp(s)Tsm2(b)− λ

∫ b

0

m1(y)Tsp(b− y)dy − λTsζ(b).

Rearranging the above terms leads to

[c2s− (λ + δ) + λp(s)]Tsm2(b) = c2m2(b)− λ

∫ b

0

m1(y)Tsp(b− y)dy − λTsζ(b). (4.2)

To determine the constant term c2m2(b) in (4.2), we substitute s there with the nonneg-

ative solution ρ2 to the Lundberg fundamental equation (2.5). Hence

c2m2(b) = λ

∫ b

0

m1(y)Tρ2p(b− y)dy + λTρ2ζ(b).

Consequently, equation (4.2) reduces to

[c2(s− ρ2) + λp(s)− λp(ρ2)]Tsm2(b) =λ

[∫ b

0

m1(y)Tρ2p(b− y)dy −∫ b

0

m1(y)Tsp(b− y)dy

]

+ λ[Tρ2ζ(b)− Tsζ(b)],

which, divided by s− ρ2, produces

[c2 − λ

p(s)− p(ρ2)

ρ2 − s

]Tsm2(b) =

[c2 − λ

1− p(ρ2)

ρ2

a2(s)

]Tsm2(b)

=λ

∫ b

0

m1(y)Tρ2p(b− y)− Tsp(b− y)

s− ρ2

dy + λTρ2ζ(b)− Tsζ(b)

s− ρ2

,

where a2(s) is given by (2.8) with i = 2. Slight rearrangements in the above equation along

with implementation of formula (2.1) lead to

c2Tsm2(b) = λ1− p(ρ2)

ρ2

a2(s)Tsm2(b) + λ

∫ b

0

m1(y)TsTρ2p(b− y)dy + λTsTρ2ζ(b).

11

We invert the operators to obtain

m2(u) = π2

∫ u−b

0

m2(u− y)dA2(y) +λ

c2

∫ u

u−b

m1(u− y)Tρ2p(y)dy +λ

c2

Tρ2ζ(u), u > b,

where π2 is as defined in (2.9) with i = 2. The above expression may be slightly simplified

by noticing that through integration by parts

Tρ2p(y)dy =

[∫ ∞

0

e−ρ2tP (t)dt

]dA2(y)

and that ∫ ∞

0

e−ρ2tP (t)dt =1− p(ρ2)

ρ2

.

Then we finally have, for u > b,

m2(u) = π2

[∫ u−b

0

m2(u− y)dA2(y) +

∫ u

u−b

m1(u− y)dA2(y)

]+

λ

c2

Tρ2ζ(u),

which is the required result.

We remark that the result in Theorem 4.1 may be restated as

m(u; b) = π2

∫ u

0

m(u− y; b)dA2(y) +λ

c2

Tρ2ζ(u), u > b.

5 Analytical Expressions for the Discounted Penalty Function

In this section, we obtain an analytical expression for the discounted penalty function. Part

of its derivation relies on results obtained in Lin and Willmot (1999) and Lin et al. (2003).

As will be seen in later sections, several results in Asmussen (2000) and Gerber and Shiu

(2005a) are special cases.

We begin with m1. Since equation (3.1) for m1 has the exact same form as equation (2.9)

in Lin et al. (2003) with c there replaced by c1 here, we may apply the same approach as far

as we obtain an initial condition for m1.

The solution m1 is then of the form

m1(u) = m∞(u) + κv(u), (5.1)

where κ is a constant, which we specify by implementing equation (5.1) and returning to

(4.1). Thus, for u = b we have

m∞(b) + κv(b) = m1(b) =m2(b)

12

= π2

∫ b

0

m∞(b− y)dA2(y) + κπ2

∫ b

0

v(b− y)dA2(y) +λ

c2

Tρ2ζ(b).

Thus,

κ =π2

∫ b

0m∞(b− y)dA2(y)−m∞(b) + λ

c2Tρ2ζ(b)

v(b)− π2

∫ b

0v(b− y)dA2(y)

.

Next, we express m∞ in terms of a compound geometric distribution. For i = 1 and 2,

introduce the following compound geometric c.d.f.

Ki(y) = 1−K i(y) =∞∑

n=0

(1− πi)πni A∗n

i (y), u ≥ 0, (5.2)

where A∗ni is the n-fold convolution of Ai with itself. Then by Theorem 2.1 in Lin and

Willmot (1999),

m∞(u) =λ

c1(1− π1)

∫ u

0

Tρ1ζ(u− y)dK1(y) +λ

c1

Tρ1ζ(u)

=λ

c1(1− π1)

[−

∫ u

0

K1(u− y)dTρ1ζ(y)−K1(u)Tρ1ζ(0) + Tρ1ζ(u)

], u ≥ 0. (5.3)

Lastly, we derive an expression for m2. Let x = u− b and g(x) = m2(x + b), x > 0. We

can then rewrite (4.1) as

g(x) = π2

∫ x

0

g(x− y)dA2(y) + h(x + b), x > 0.

where

h(x + b) = h(u) = π2

∫ u

u−b

m1(u− y)dA2(y) +λ

c2

Tρ2ζ(u), u > b.

Hence, Theorem 2.1 in Lin and Willmot (1999) applies to g(x) and we may express m2(u)

via g(x) as

m2(u) =g(x)

=1

1− π2

∫ x

0

h(x + b− y)dK2(y) + h(x + b)

=1

1− π2

∫ u−b

0

h(u− y)dK2(y) + h(u)

=− 1

1− π2

[∫ u

b

K2(u− y)dh(y) + K2(u− b)h(b)

]+ h(u). (5.4)

All above derivations are summarized by the theorem below.

13

Theorem 5.1. The discounted penalty function m(u; b) may be expressed analytically in the

following steps:

(i) m∞(u) =λ

c1(1− π1)

∫ u

0

Tρ1ζ(u− y)dK1(y) +λ

c1

Tρ1ζ(u); (5.5)

(ii) κ =π2

∫ b

0m∞(b− y)dA2(y)−m∞(b) + λ

c2Tρ2ζ(b)

v(b)− π2

∫ b

0v(b− y)dA2(y)

; (5.6)

(iii) m1(u) = m∞(u) + κ1−Ψ(u)

1−Ψ(0)eρ1u, 0 ≤ u ≤ b; (5.7)

(vi) h(u) = π2

∫ u

u−b

m1(u− t)dA2(t) +λ

c2

Tρ2ζ(u), u > b, (5.8)

(v) m2(u) =1

1− π2

∫ u−b

0

h(u− y)dK2(y) + h(u), u > b, (5.9)

where Ki, i = 1, 2, are given in (5.2).

The definitions of the remaining functions and parameters utilized in Theorem 5.1 above

are provided in Sections 2 and 3. Also note that equations (5.5) and (5.8) have alternative

forms provided by (5.3) and (5.4) respectively.

We now proceed with some important special cases in the rest of the paper.

6 The Probability of Ultimate Ruin

This section discusses the probability that the time of ruin is finite, or the probability of

ultimate ruin, and the probability of a drop below the initial surplus level as a special case.

As it is well known, many particular cases of the discounted penalty function, which

result in important quantities of interest in risk theory, are produced when δ is set to be 0.

The nonnegative solutions of the respective Lundberg fundamental equations (2.5) are then

ρ1 = ρ2 = 0. On one hand, this implies that πi = 1/(1 + θi), i = 1, 2, as noted after the

definition in (2.9). On the other hand, by (2.7) both A1 and A2 reduce to the first order

14

equilibrium distribution Pe of P, namely,

Pe(y) = 1− P e(y) =

∫ y

0

P (t)dt

E{Y1} =

∫ y

0

pe(t)dt, y ≥ 0,

where pe = P (t)/E{Y1} is the equilibrium p.d.f.

Furthermore, Tρ1ζ(u) = Tρ2ζ(u) =∫∞

uζ(t)dt and the definition of Ψ in Section 2 shows

that Ψ(u) = ψ1,∞(u), u ≥ 0, where ψ1,∞ is the probability of ultimate ruin under the

classical compound Poisson model with premium rate c1. Also, with the changes in πi and

Ai, i = 1, 2, it is clear that K1 and K2, defined by (5.2), coincide with the probabilities

of ultimate ruin ψ1,∞ and ψ2,∞ respectively. Here ψ2,∞ is the probability of ultimate ruin

under the ordinary compound Poisson model with premium rate c2. It is well known that

ψ1,∞(0) = 1/(1 + θ1) and ψ2,∞(0) = 1/(1 + θ2).

After setting δ = 0, let also assume that w(x1, x2) = 1 for all x1, x2 ≥ 0. Then m(u; b)

becomes the probability of ultimate ruin, which we denote by ψb. Also, by (2.3) ζ reduces

to P .

From Theorem 5.1 we have the following result.

Theorem 6.1. The probability of ultimate ruin for the compound Poisson risk model with

a threshold strategy is given by

ψ(u; b) =

ψ1(u) = 1− q(b) + q(b)ψ1,∞(u), 0 ≤ u ≤ b

ψ2(u) = −1 + θ2

θ2

∫ u−b

0

h(u− y)dψ2,∞(y) + h(u), u > b,

(6.1)

with

q(b) =θ2

(θ1 − θ2)ψ1,∞(b) + θ2

(6.2)

belonging to the interval [0,1] and

h(u) =1

1 + θ2

∫ u

u−b

ψ1(u− t)dPe(t) +1

1 + θ2

P e(u), u > b. (6.3)

Proof. Equation (5.6) yields

κ =

1

1 + θ2

∫ b

0

ψ1,∞(b− y)dPe(y)− ψ1,∞(b) +1

1 + θ2

P e(b)

1− ψ1,∞(b)

1− ψ1,∞(0)− 1

1 + θ2

∫ b

0

1− ψ1,∞(b− y)

1− ψ1,∞(0)dPe(y)

15

=[1− ψ1,∞(0)]

1

1 + θ2

[(1 + θ1)ψ1,∞(b)− P e(b)]− ψ1,∞(b) +1

1 + θ2

P e(b)

1− ψ1,∞(b)− 1

1 + θ2

[Pe(b)−

∫ b

0

ψ1,∞(b− y)dPe(y)

]

=[1− ψ1,∞(0)]

(1 + θ1

1 + θ2

− 1

)ψ1,∞(b)

1− ψ1,∞(b)− 1

1 + θ2

Pe(b) +1 + θ1

1 + θ2

ψ1,∞(b)− 1

1 + θ2

P e(b)

=[1− ψ1,∞(0)](θ1 − θ2)ψ1,∞(b)

(θ1 − θ2)ψ1,∞(b) + θ2

.

By equation (5.7) we have

ψ1(u) =ψ1,∞(u) +(θ1 − θ2)ψ1,∞(b)

(θ1 − θ2)ψ1,∞(b) + θ2

[1− ψ1,∞(u)]

=(θ1 − θ2)ψ1,∞(b)

(θ1 − θ2)ψ1,∞(b) + θ2

+θ2

(θ1 − θ2)ψ1,∞(b) + θ2

ψ1,∞(u), 0 ≤ u ≤ b,

which produces (6.1). The remaining part of the proof follows directly from Theorem 5.1

along with the assumptions about δ and w.

We remark that formula (6.1) implies that ψ1 is a weighted average of the probability of

ruin in the dividend case and the probability of ruin in the ordinary Poisson model.

Also, as a particular case of (6.1), we obtain the following.

Corollary 6.2. For 0 ≤ u ≤ b the probability of a drop below the initial surplus level u, is

provided by

ψ(0; b− u) =(1 + θ1)(θ1 − θ2)ψ1,∞(b− u) + θ2

(1 + θ1) [(θ1 − θ2)ψ1,∞(b− u) + θ2]. (6.4)

Proof. We find

ψ(0; b− u) =1− q(b− u) + q(b− u)ψ1,∞(0) = 1− θ1

1 + θ1

q(b− u)

=(1 + θ1)(θ1 − θ2)ψ1,∞(b− u) + θ2

(1 + θ1) [(θ1 − θ2)ψ1,∞(b− u) + θ2], 0 ≤ u ≤ b,

by employing (6.1) and (6.2).

Note that when u > b, the probability of a drop below the initial level, ψ0(0) under

the present model, reduces to the same probability under the classical compound Poisson

model with premium rate c2. The distribution of the first drop below the initial level will be

discussed in Section 8.

16

An advantage of formula (6.1) over the result of Proposition 1.10 in Asmussen (2000,

Chapter VII, Section 1) is that all functions involved in Theorem 6.1 have a known form

and hence can be computed straightforwardly. This becomes obvious when illustrated in the

following two examples.

Example 6.1. (Exponential Claim Amounts)

When the individual claim amounts are exponentially distributed with mean 1/µ, µ > 0,

upon a little algebra it is seen that

P (y) = 1− e−µy = Pe(y), y ≥ 0.

Let βi = θi

1+θiµ, i = 1, 2, be the Lundberg adjustment coefficient for the compound Poisson

risk model with premium rate ci. Then, it is well known that

ψi,∞(u) =1

1 + θi

e−βiu, u ≥ 0, i = 1, 2.

Hence, by (6.4) the probability of a drop below the initial surplus level is given by

ψ(0; b− u) =(θ1 − θ2)e

−β1(b−u) + θ2

(θ1 − θ2)e−β1(b−u) + (1 + θ1)θ2

, 0 ≤ u ≤ b.

Also, it follows from (6.1) that

ψ1(u) =1− q(b) +q(b)

1 + θ1

e−β1u, 0 ≤ u ≤ b, (6.5)

with

q(b) =(1 + θ1)θ2

(θ1 − θ2)e−β1b + (1 + θ1)θ2

(6.6)

by (6.2). Equation (6.5) yields further that (6.3) reduces to

h(u) =1

1 + θ2

{−

∫ u

u−b

[1− q(b)]de−µt − q(b)

1 + θ1

∫ u

u−b

e−β1(u−t)de−µt + e−µu

}

=1

1 + θ2

{[1− q(b)]e−µ(u−b) − [1− q(b)]e−µu +

µq(b)

1 + θ1

e−β1u

∫ u

u−b

e(β1−µ)tdt + e−µu

}

=1

1 + θ2

{[1− q(b)]e−µ(u−b) + q(b)e−µu +

µq(b)

1 + θ1

· 1

β1 − µe−β1u

[1− e−(β1−µ)b

]e(β1−µ)u

}

=1

1 + θ2

{[1− q(b)]e−µ(u−b) + q(b)e−µu − q(b)

[1− e−(β1−µ)b

]e−µu

}

=1

1 + θ2

[1− q(b) + q(b)e−β1b

]e−µ(u−b)

17

=1

1 + θ2

Q(b)e−µ(u−b), u > b, (6.7)

where Q(b) = 1− q(b) + q(b)e−β1b. Therefore, (6.1) produces

ψ2(u) =1

1 + θ2

{− 1

θ2

∫ u−b

0

Q(b)e−µ(u−y−b)de−β2y + Q(b)e−µ(u−b)

}

=1

1 + θ2

{Q(b)

β2

θ2

∫ u−b

0

e−(β2−µ)ydy + Q(b)

}e−µ(u−b)

=1

1 + θ2

{−Q(b)

β2

θ2

· 1

β2 − µ

[e−(β2−µ)(u−b) − 1

]+ Q(b)

}e−µ(u−b)

=1

1 + θ2

{Q(b)

[e−(β2−µ)(u−b) − 1

]+ Q(b)

}e−µ(u−b)

=1

1 + θ2

Q(b)e−β2(u−b), u > b. (6.8)

To summarize,

ψ(u; b) =

ψ1(u) = 1− q(b) +q(b)

1 + θ1

e−β1u, 0 ≤ u ≤ b

ψ2(u) =1

1 + θ2

[1− q(b) + q(b)e−β1b

]e−β2(u−b), u > b,

with q(b) specified by (6.6) and βi = θi

1+θiµ, i = 1, 2, which coincides with the result obtained

in Example 1.11 in Asmussen (2000, Chapter VII, Section 1).

It is easy to see that 0 ≤ Q(b) ≤ 1. Hence we obtain a Lundberg-type upper bound for

ψ2(u):

ψ2(u) ≤ 1

1 + θ2

e−β2(u−b).

¤

Example 6.2. (Combination of Exponentials Claim Amounts)

Consider now the individual claim amounts have a combination of exponentials distribu-

tion. More specifically,

P (y) =n∑

j=1

ωj e−µjy, y ≥ 0, µj > 0, j = 1, 2, . . . , n,

with∑n

j=1 ωj = 1 for a positive integer number n.

As noted in Gerber et al. (1987),

P e(y) =n∑

j=1

ω∗j e−µjy, y ≥ 0,

18

where

ω∗j =ωj/µj∑nl=1 ωl/µl

, j = 1, 2, . . . , n,

and

ψi,∞(u) =n∑

j=1

Cije−βiju, u ≥ 0, i = 1, 2,

where 0 < βi1 < βi2 < · · · < βin are the roots of∑n

j=1 [ω∗j µj/(µj − β)] = 1 + θi, i = 1, 2,

assumed to be real valued and distinct, and

Cij =

[n∑

l=1

ω∗lµl − βij

]/ [n∑

l=1

ω∗l µl

(µl − βij)2

], i = 1, 2, j = 1, 2, . . . , n.

We remark that βi1, i = 1, 2, are the Lundberg adjustment coefficients.

It follows from Corollary 6.2 that the probability of a drop below the initial surplus level

is given by

ψ(0; b− u) =(1 + θ1)(θ1 − θ2)

∑nj=1 C1je

−β1j(b−u) + θ2

(1 + θ1)[(θ1 − θ2)

∑nj=1 C1je−β1j(b−u) + θ2

] , 0 ≤ u ≤ b.

Furthermore, it is easy to see

ψ1(u) = 1− q(b) + q(b)n∑

j=1

C1je−β1ju, 0 ≤ u ≤ b,

where

q(b) =θ2

(θ1 − θ2)∑n

j=1 C1j e−β1jb + θ2

.

Before we derive an analytical expression for ψ2(u), two useful identities are presented.

Slightly changing the notation, formula (10.4.13) in Willmot and Lin (2001) becomes

n∑

l=1

βilCil

µj − βil

=θi

1 + θi

, i = 1, 2. (6.9)

Since∑n

l=1 Cil = ψi,∞(0) = 1/(1 + θi), we have

n∑

l=1

µjCil

µj − βil

=n∑

l=1

Cil +n∑

l=1

βilCil

µj − βil

=1

1 + θi

+θi

1 + θi

= 1, i = 1, 2. (6.10)

19

Analogously to equations (6.7) and (6.8) we find respectively

h(u) =1

1 + θ2

n∑j=1

ω∗j

{µj

∫ u

u−b

ψ1(u− t)e−µjtdt + e−µju

}

=1

1 + θ2

n∑j=1

ω∗j

{[1− q(b)]e−µj(u−b) + q(b)e−µju

+ q(b)n∑

l=1

µjC1l

µj − β1l

[e−β1lbe−µj(u−b) − e−µju

] }.

Using identity (6.10) with i = 1, we have

h(u) =n∑

j=1

ω∗j Qj(b)e−µj(u−b), (6.11)

where

Qj(b) = 1− q(b) + q(b)n∑

l=1

µjC1l

µj − β1l

e−β1lb, j = 1, · · · , n.

Thus,

ψ2(u) =1

θ2

n∑j=1

ω∗j Qj(b)n∑

l=1

β2lC2l

µj − β2l

e−β2l(u−b)

+n∑

j=1

ω∗j Qj(b)

{1

1 + θ2

− 1

θ2

n∑

l=1

β2lC2l

µj − β2l

}e−µj(u−b)

=1

θ2

n∑j=1

ω∗j Qj(b)n∑

l=1

β2lC2l

µj − β2l

e−β2l(u−b)

=1

θ2

n∑j=1

β2jC2j

{n∑

l=1

ω∗l Ql(b)

µl − β2j

}e−β2j(u−b), u > b,

due to identity (6.9) with i = 2. Therefore,

ψ(u; b) =

ψ1(u) = 1− q(b) + q(b)n∑

j=1

C1j e−β1ju, 0 ≤ u ≤ b

ψ2(u) =1

θ2

n∑j=1

β2jC2j

[n∑

l=1

ω∗l Ql(b)

µl − β2j

]e−β2j(u−b), u > b.

If the individual claim distribution is a mixture, i.e., ωj ≥ 0 for all j, then Cil ≥ 0 for all

l and i = 1, 2. Hence, 0 ≤ Qj(b) ≤ 1 for all j. We can again obtain a Lundberg-type upper

20

bound for ψ2(u) in this case:

ψ2(u) =1

θ2

n∑j=1

ω∗j Qj(b)n∑

l=1

β2lC2l

µj − β2l

e−β2l(u−b)

≤ 1

θ2

n∑j=1

ω∗j Qj(b)n∑

l=1

β2lC2l

µj − β2l

e−β21(u−b)

=1

1 + θ2

n∑j=1

ω∗j Qj(b)e−β21(u−b) ≤ 1

1 + θ2

e−β21(u−b), u > b.

¤

7 The time of ruin

In this section we turn our attention to another particular case of m(u; b). We consider the

defective Laplace transform of the ruin time E{e−δTbI(Tb < ∞)|Ub(0) = u} by letting δ ≥ 0 to

be arbitrary and setting w(x1, x2) = 1 for all x1, x2 ≥ 0. Recall that in this case ζ reduces to

P. Also, when δ > 0, without loss of generality we may consider E{e−δTb|Ub(0) = u} instead

of the above-mentioned Laplace transform. For δ = 0 we have the probability of ultimate

ruin, discussed in Section 6. Once the Laplace transform of the time of ultimate ruin Tb is

identified, its distribution may be obtained using an inversion method. Its moments may be

obtained by differentiation with respect to δ. Although such tasks are theoretically possible,

they are practically tedious and challenging as demonstrated in Drekic et al. (2004). It is

partly due to the fact that the discounted penalty function m(u; b) given in Theorem 5.1 is

not explicitly expressed in terms of δ. Instead, it is expressed via ρ1 = ρ1(δ) and ρ2 = ρ2(δ).

Let

L(u; b) = m(u; b)∣∣∣w≡1

,

L1(u) = m1(u)∣∣∣w≡1

, L2(u) = m2(u)∣∣∣w≡1

,

and

L∞(u) = m∞(u)∣∣∣w≡1

.

We note that the above notation is somewhat misleading as the true variable is δ that is

implicitly included in these functions. However, expressing them in terms of u is necessary

for our derivation purposes. We now utilize our main result to derive the Laplace transform

of Tb.

21

Theorem 7.1. The Laplace transform of the time of ruin for the compound Poisson risk

model with a threshold strategy satisfies

L(u; b) =

L1(u) = L∞(u) + κ1−Ψ(u)

1−Ψ(0)eρ1u, 0 ≤ u ≤ b

L2(u) =1

1− π2

∫ u−b

0

h(u− y)dK2(y) + h(u), u > b,

(7.1)

where

L∞(u) =π1

1− π1

[∫ u

0

K1(u− y)dA1(y)−K1(u) + A1(u)

], u ≥ 0,

κ =π2

∫ b

0L∞(b− y)dA2(y)− L∞(b) + π2A2(b)

v(b)− π2

∫ b

0v(b− y)dA2(y)

, (7.2)

and

h(u) = π2

∫ u

u−b

L1(u− t)dA2(t) + π2A2(u), u > b. (7.3)

Proof. A direct application of Theorem 5.1 yields equation (7.1) with κ and h as specified

in (7.2) and (7.3) respectively, where the latter two equations are obtained with the help of

(2.7) and (2.9). Moreover, slightly simplifying equation (5.3), we deduce for L∞ that

L∞(u) =π1

1− π1

[∫ u

0

K1(u− y)dA1(y)−K1(u) + A1(u)

], u ≥ 0,

by which the result is demonstrated.

For certain claim-size distributions, exact results may be derived. Such are the expo-

nential and the combination of exponentials. We illustrate the idea through the following

example.

Example 7.1. (Exponential Claim Amounts) When the claim amounts are exponen-

tially distributed, namely, P (y) = 1− e−µy, y ≥ 0, µ > 0, explicit formulae for all participat-

ing elements are available. More specifically, A1(y) = A2(y) = 1 − e−µy = P (y). Since the

Laplace transform of Y1 is p(s) = µ/(s+µ), we find by (2.9) that πi = λ/[ci(ρi +µ)], i = 1, 2.

By Lin et al. (2003), pp. 561-562, we have that K i(u) = πie−τiu, i = 1, 2, where

τi = (1 − πi)µ. Moreover, L∞(u) = K1(u) = π1e−τ1u and Ψ(u) = µ−τ1

µ+ρ1e−(ρ1+τ1)u. Note

that −τi and ρi are the respective negative and the nonnegative roots of the Lundberg

fundamental equation (2.5) with i = 1 and 2.

22

By determining Ψ and L∞ we may obtain exact formulae for v and κ, which leads to

an exact expression for L(u; b). More specifically, employing the above formulea along with

equations (2.10) and (2.6) into (7.2), we obtain

κ =

(π2

π1

− 1

)L∞(b)

1−Ψ(b)

1−Ψ(0)eρ1b − π2

∫ b

0

1−Ψ(b− y)

1−Ψ(0)eρ1(b−y)dA2(y)

=

(1− µ− τ1

µ + ρ1

)(π2

π1

− 1

)π1e

−τ1b

[1− µ− τ1

µ + ρ1

e−(ρ1+τ1)b

]eρ1b + π2e

ρ1b

∫ b

0

[1− µ− τ1

µe−(ρ1+τ1)(b−y)

]e−ρ1yde−µy

=ρ1 + τ1

µ + ρ1

· (π2 − π1)e−(ρ1+τ1)b

1− µ− τ1

µ + ρ1

e−(ρ1+τ1)b +µπ2

µ + ρ1

[e−(µ+ρ1)b − 1

]+ µπ2

µ− τ1

µ + ρ1

e−(ρ1+τ1)b

∫ b

0

e(τ1−µ)ydy

=ρ1 + τ1

µ + ρ1

· (π2 − π1)e−(ρ1+τ1)b

1− µ− τ1

µ + ρ1

e−(ρ1+τ1)b +µπ2

µ + ρ1

[e−(µ+ρ1)b − 1

]+

µπ2

µ + ρ1

[e−(ρ1+τ1)b − e−(µ+ρ1)b

]

=(π2 − π1)(ρ1 + τ1)e

−(ρ1+τ1)b

ρ1 + τ2 + (τ1 − τ2)e−(ρ1+τ1)b

.

Hence, Theorem 7.1 yields

L1(u) =π1e−(1−π1)µu +

κ

1− µ−τ1µ+ρ1

[1− µ− τ1

µ + ρ1

e−(ρ1+τ1)u

]eρ1u

=

{π1 − κ(µ− τ1)

ρ1 + τ1

}e−τ1u +

κ(µ− τ1)

ρ1 + τ1

eρ1u

=π1

{1− µ(π2 − π1)e

−(ρ1+τ1)b

ρ1 + τ2 + (τ1 − τ2)e−(ρ1+τ1)b

}e−τ1u +

µ(π2 − π1)e−(ρ1+τ1)b

ρ1 + τ2 + (τ1 − τ2)e−(ρ1+τ1)b

eρ1u

=π1r(b)e−τ1u + [1− r(b)]eρ1u, 0 ≤ u ≤ b,

where

r(b) = 1− µ(π2 − π1)e−(ρ1+τ1)b

ρ1 + τ2 + (τ1 − τ2)e−(ρ1+τ1)b

(7.4)

is introduced to facilitate the further calculations by making the analogy with q(b) in Example

6.1. Therefore, if we set

R(b) =ρ1

µ + ρ1

[1− r(b)]e−µb +µ

µ + ρ1

[1− r(b)]eρ1b + r(b)e−τ1b,

23

in a similar way as we obtained equation (6.7), we have

h(u) = π2R(b)e−µ(u−b), u > b.

Furthermore, it becomes obvious that the relation between equations (6.7) and (6.8) yields

here

L2(u) = π2R(b)e−τ2(u−b), u > b.

Finally,

L(u; b) =

L1(u) = [1− r(b)]eρ1u + π1r(b)e−τ1u,

0 ≤ u ≤ b

L2(u) = π2

{ρ1

µ + ρ1

[1− r(b)]e−µb +µ

µ + ρ1

[1− r(b)]eρ1b + r(b)e−τ1b

}e−τ2(u−b),

u > b,

where r(b) is provided by equation (7.4).

The above result is very similar to that in Example 6.1 as expected. ¤

The Laplace transform of the time of ruin when the individual claim amounts follow a

combination of exponentials can be derived similarly to that in Example 6.2. Using the same

notation as in Example 6.2, we have for i = 1 and 2,

Ai(y) =n∑

j=1

ω∗ij e−µjy, y ≥ 0,

where

ω∗ij =ωj/(µj + ρi)∑nl=1 ωl/(µl + ρi)

, j = 1, 2, · · · , n.

See Example 3.1 of Lin and Willmot (1999).

Furthermore,

Ki(u) =n∑

j=1

Cije−βiju, u ≥ 0,

where 0 < βi1 < βi2 < · · · < βin are the roots of∑n

j=1 [ω∗ijµj/(µj − β)] = 1+ θi, i = 1, 2, and

Cij =

[n∑

l=1

ω∗ilµl − βij

]/ [n∑

l=1

ω∗ilµl

(µl − βij)2

], i = 1, 2, j = 1, 2, . . . , n.

Identities (6.9) and (6.10) still hold for βij and Cij as in Example 6.2. See also Example

4.1 of Lin and Willmot (1999). Thus, the rest of the derivation is exactly the same as in

Example 6.2 and we omit the details.

24

8 The surplus before ruin and the deficit at ruin

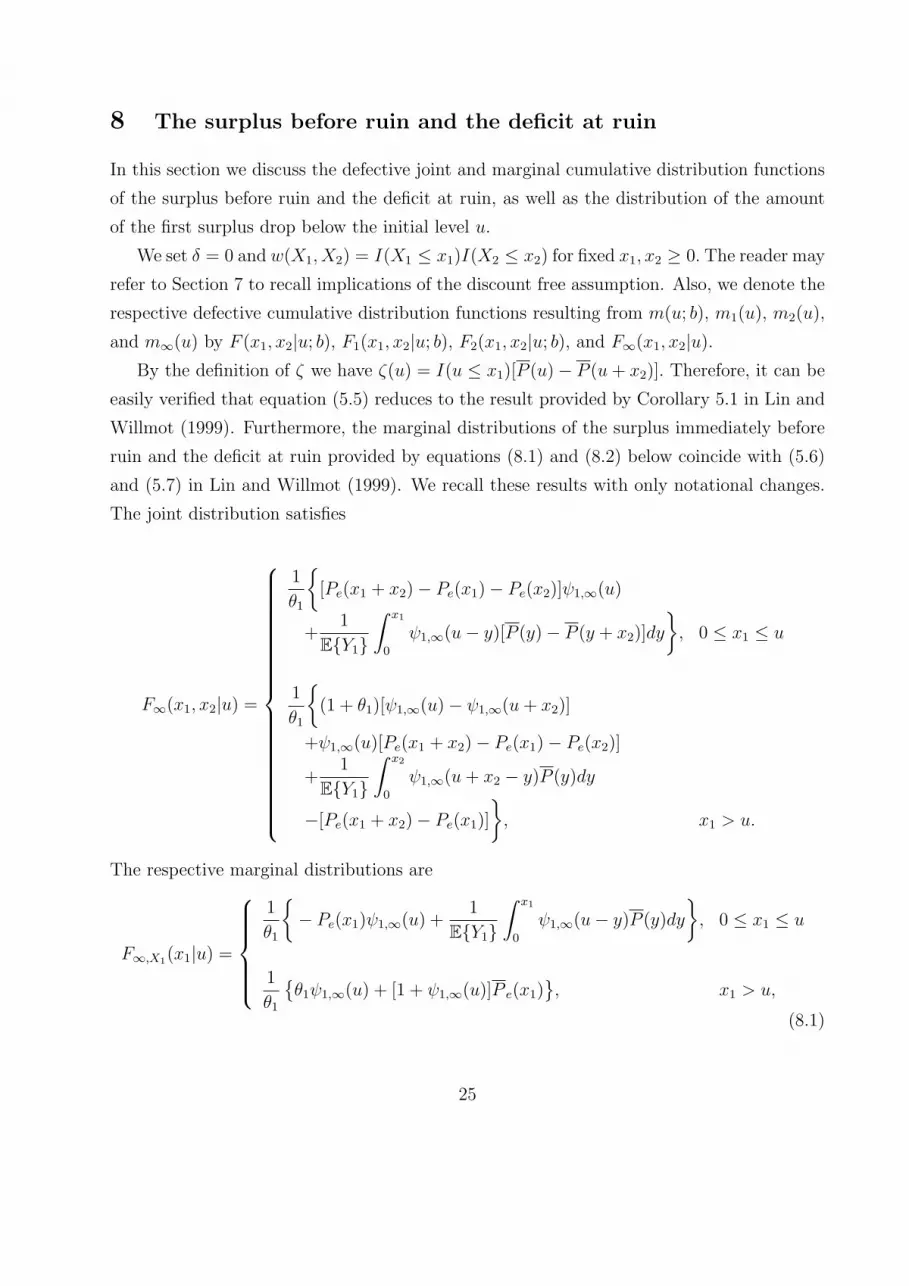

In this section we discuss the defective joint and marginal cumulative distribution functions

of the surplus before ruin and the deficit at ruin, as well as the distribution of the amount

of the first surplus drop below the initial level u.

We set δ = 0 and w(X1, X2) = I(X1 ≤ x1)I(X2 ≤ x2) for fixed x1, x2 ≥ 0. The reader may

refer to Section 7 to recall implications of the discount free assumption. Also, we denote the

respective defective cumulative distribution functions resulting from m(u; b), m1(u), m2(u),

and m∞(u) by F (x1, x2|u; b), F1(x1, x2|u; b), F2(x1, x2|u; b), and F∞(x1, x2|u).

By the definition of ζ we have ζ(u) = I(u ≤ x1)[P (u)− P (u + x2)]. Therefore, it can be

easily verified that equation (5.5) reduces to the result provided by Corollary 5.1 in Lin and

Willmot (1999). Furthermore, the marginal distributions of the surplus immediately before

ruin and the deficit at ruin provided by equations (8.1) and (8.2) below coincide with (5.6)

and (5.7) in Lin and Willmot (1999). We recall these results with only notational changes.

The joint distribution satisfies

F∞(x1, x2|u) =

1

θ1

{[Pe(x1 + x2)− Pe(x1)− Pe(x2)]ψ1,∞(u)

+1

E{Y1}∫ x1

0

ψ1,∞(u− y)[P (y)− P (y + x2)]dy

}, 0 ≤ x1 ≤ u

1

θ1

{(1 + θ1)[ψ1,∞(u)− ψ1,∞(u + x2)]

+ψ1,∞(u)[Pe(x1 + x2)− Pe(x1)− Pe(x2)]

+1

E{Y1}∫ x2

0

ψ1,∞(u + x2 − y)P (y)dy

−[Pe(x1 + x2)− Pe(x1)]

}, x1 > u.

The respective marginal distributions are

F∞,X1(x1|u) =

1

θ1

{− Pe(x1)ψ1,∞(u) +

1

E{Y1}∫ x1

0

ψ1,∞(u− y)P (y)dy

}, 0 ≤ x1 ≤ u

1

θ1

{θ1ψ1,∞(u) + [1 + ψ1,∞(u)]P e(x1)

}, x1 > u,

(8.1)

25

and

F∞,X2(x2|u) =1

θ1

{(1 + θ1)[ψ1,∞(u)− ψ1,∞(u + x2)]− ψ1,∞(u)Pe(x2)

+1

E{Y1}∫ x2

0

ψ1,∞(u + x2 − y)P e(y)dy

}. (8.2)

Hence, equations (5.4) to (5.8) produce analytical expressions for F (x1, x2|u; b).

Theorem 8.1. Let

σ(x1, x2|u) = P e(u) + P e(x1 + x2)− P e(x1)− P e(u + x2), u ≥ 0.

Then F (x1, x2|u; b) is given by

F1(x1, x2|u; b) = F∞(x1, x2|b) + κ[1− ψ1,∞(u)], 0 ≤ u ≤ b,

F2(x1, x2|u; b) = −1 + θ2

θ2

[∫ u

b

ψ2,∞(u− y)dh(y) + ψ2,∞(u− b)h(b)

]+ h(u), u > b,

with

κ =(θ1 − θ2)F∞(x1, x2|b)− P e(b) + I(b ≤ x1)σ(x1, x2|b)

(θ1 − θ2)ψ1,∞(b) + θ2

,

and

h(u) =1

1 + θ2

∫ u

u−b

F1(x1, x2|u− y; b)dPe(y) +I(u ≤ x1)

1 + θ2

σ(x1, x2|u), u > b.

Letting either x2 → ∞, or x1 → ∞ we derive either the defective marginal c.d.f. of the

surplus before ruin, or the defective marginal c.d.f. of the deficit at ruin, respectively.

Corollary 8.2. The defective marginal c.d.f. of the surplus immediately before ruin FX1(x1|u; b)

is given by

F1,X1(x1|u; b) = F∞,X1(x1|b) + κ[1− ψ1,∞(u)], 0 ≤ u ≤ b,

F2,X1(x1|u; b) = −1 + θ2

θ2

[∫ u

b

ψ2,∞(u− y)dh(y) + ψ2,∞(u− b)h(b)

]+ h(u), u > b,

where

κ =(θ1 − θ2)F∞,X1(x1|b)− P e(b) + I(u ≤ x1)[P e(b)− P e(x1)]

(θ1 − θ2)ψ1,∞(b) + θ2

,

and

h(u) =1

1 + θ2

∫ u

u−b

F1,X1(x1|u− y; b)dPe(y) +I(u ≤ x1)

1 + θ2

[P e(u)− P e(x1)], u > b.

26

In a similar manner, we obtain a respective result regarding the severity at ruin.

Corollary 8.3. The defective marginal c.d.f. of the deficit at ruin FX2(x2|u; b) may be

obtained through

F1,X2(x2|u; b) = F∞,X2(x2|b) + κ[1− ψ1,∞(u)], 0 ≤ u ≤ b,

F2,X2(x2|u; b) = −1 + θ2

θ2

[∫ u

b

ψ2,∞(u− y)dh(y) + ψ2,∞(u− b)h(b)

]+ h(u), u > b,

with

κ =(θ1 − θ2)F∞,X2(x2|b)− P e(b + x2)

(θ1 − θ2)ψ1,∞(b) + θ2

,

and

h(u) =1

1 + θ2

∫ u

u−b

F1,X2(x2|u− y; b)dPe(y) +1

1 + θ2

[P e(u)− P e(u + x2)], u > b.

When the barrier level is b − u and the initial surplus is 0, Corollary 8.3 yields the

distribution of the first surplus drop below the initial level.

Corollary 8.4. The distribution of the first surplus drop below the initial level is given by

G(x2|0) = F∞,X2(x2|b− u) +θ1

1 + θ1

κ, 0 ≤ u ≤ b,

with

κ =(θ1 − θ2)F∞,X2(x2|b− u)− P e(b− u + x2)

(θ1 − θ2)ψ1,∞(b− u) + θ2

.

It is possible to obtain joint and marginal moments of the surplus before ruin and the

deficit at ruin. We set w(x1, x2) = xh1x

l2 for an arbitrary pair of nonnegative integers h and

l. Denote then by F h,l(u; b), F h,l1 (u), F h,l

2 (u), and F h,l∞ (u) the joint moments resulting from

m(u; b), m1(u), m2(u), and m∞(u) respectively with the specific choice of w.

In order to simplify the expressions to follow, let n be a nonnegative integer and define

recursively the nth order equilibrium tail of P to be

P e,n(y) = 1− Pe,n(y) =

∫∞y

P e,n−1(t)dt∫∞0

P e,n−1(t)dt,

with P 0,e(t) = P (t) and P 1,e(t) = P e(t). If in addition, we define pn =∫∞0

yndP (y) to be the

nth moment of Y1, we can apply formula (2.4) in Lin and Willmot (2000), namely,

P e,n(y) =1

pn

∫ ∞

y

(t− y)ndP (t)

27

to find ∫ ∞

u

ζ(t)dt = pl

∫ ∞

u

thP e,l(t)dt

for this particular form of w. Therefore, equations (5.4) to (5.8) yield the following.

Theorem 8.5.

F h,l(u; b) =

F h,l1 (u) = F h,l

∞ (u) + κ[1− ψ1,∞(u)], 0 ≤ u ≤ b,

F h,l2 (u) = −1 + θ2

θ2

[∫ u

b

ψ2,∞(u− y)dh(y) + ψ1,∞(u− b)h(b)

]+ h(u), u > b,

(8.3)

where

F h,l∞ (u) =

θ1pl

p1

{∫ u

0

yh[ψ1,∞(u− y)− ψ1,∞(u)]P e,l(y)dy +

∫ ∞

u

yh[1− ψ1,∞(u)]P e,l(y)dy

},

κ =(θ2 − θ1)F

h,l∞ (b)− P e(b) + pl

p1

∫∞b

thP e,l(t)dt

(θ2 − θ1)ψ1,∞(b) + θ2

,

and

h(u) =1

1 + θ2

∫ u

u−b

F h,l1 (u− y)dPe(y) +

λpl

c2

∫ ∞

u

thP e,l(t)dt, u > b. (8.4)

To obtain marginal moments of the surplus immediately before ruin or the deficit at ruin,

simply set l = 0 or h = 0 in equations (8.3) to (8.4).

We want to point out that further simplification for the results in Theorems 8.1 and 8.5,

Corollaries 8.2, and 8.3 is possible. For example we may use the explicit expressions obtained

in Lin and Willmot (2000), pp. 29 and 32 for the joint and marginal moments F h,l∞ , F h

∞ and

F l∞ in Theorem 8.5. However, since the simplification does not provide new insight, we omit

it in this paper.

References

Albrecher, H., Hartinger, J., Tichy, R., 2005, On the distribution of dividend payments and

the discounted penalty function in a risk model with linear dividend barrier, Scancdinavian

Actuarial Journal, forthcomming.

Albrecher, H., Kainhofer, R., 2002, Risk theory with a nonlinear divident barrier, Computing,

68, 289-311.

28

Asmussen, S., 2000, Ruin Probabilities, World Scientific Publishing Co. Pte. Inc.

Bowers, N.L., Gerber, H.U., Hickman, J.C., Jones, D.A., Nesbitt, C.J., 1997, Actuarial

Mathematics, Society of Actuaries.

Buhlmann, H., 1970, Mathematical Methods in Risk Theory, Springer, New York.

De Finetti, B., 1957, Su un’impostazione alternativa della teoria collettiva del rischio, Trans-

actions of the XV International Congress of Actuaries, 2, 433-443.

Dickson, D.C.M., Hipp, C., 2001, On the time of ruin for Erlang(2) risk processes, Insurance:

Mathematics and Economics, 29, 333-344.

Dickson, D.C.M., Waters, H.R., 2004, Some optimal dividend problems, ASTIN Bulletin,

34: 49-74.

Drekic, S., Stafford, J.E., Willmot, G.E., 2004, Symbolic calculation of the moments of the

time of ruin, Insurance: Mathematics and Economics, 34, 109-120.

Gerber, H.U., 1969, Entscheidungskriterien fur den zusammengesetzten Poisson-Prozess,

Ph.D. thesis, ETHZ.

Gerber, H.U., 1972, Games of economic survival with discrete- and continuous-income pro-

cesses, Operations Research, 20, 37-45.

Gerber, H.U., 1973, Martingales in risk theory, Mutteilungen der Schweizer Vereinigung der

Versicherungsmathematiker, 205-216.

Gerber, H.U., 1979, An Introduction to Mathematical Risk Theory, S.S. Huebner Foundation,

University of Pennsylvania, Philadelphia.

Gerber, H.U., 1981, On the probability of ruin in the presence of a linear dividend barrier,

Scandinavian Actuarial Journal, 105-115.

Gerber, H.U., Goovarts, M.J., Kaas, R., 1987, On the probability and severity of ruin,

ASTIN Bulletin, vol. 17, n. 2, 151-163.

Gerber, H.U., Shiu, E.S.W., 1998, On the time value of ruin, North American Actuarial

Journal, vol. 2, n. 1, 48-78.

29

Gerber, H.U., Shiu, E.S.W., 2005a, On optimal dividend strategies in the compound Poisson

model, North American Actuarial Journal, forthcoming.

Gerber, H.U., Shiu, E.S.W., 2005b, The time value of ruin in a Sparre Andersen model,

North American Actuarial Journal, forthcoming.

Højgaard, B., 2002, Optimal dynamic premium control in non-life insurance: maximizing

divident payouts, Scandinavian Actuarial Journal, 225-245.

Klugman, S.A., Panjer, H.H., Willmot, G.E., 2004, Loss Models: From Data to Decisions,

2nd edition John Wiley and Sons, New York.

Li, S., Garrido, J., 2004a, On ruin for the Erlang(n) risk process, Insurance: Mathematics

and Economics, 34, 391-408.

Li, S., Garrido, J., 2004b, On a class of renewal risk models with a constant dividend barrier,

Insurance: Mathematics and Economics, 35, 691-701.

Lin, X.S., Willmot, G.E., 1999, Analysis of a defective renewal equation arising in ruin

theory, Insurance: Mathematics and Economics, 25, 63-84.

Lin, X.S., Willmot, G.E., 2000, The moments of the time of ruin, the surplus befor ruin, and

the deficit at ruin, Insurance: Mathematics and Economics, 27, 19-44.

Lin, X.S., Willmot, G.E., Drekic, S., 2003, The classical risk model with a constant dicvident

barrier: analysis of the Gerber-Shiu discounted penalty function, Insurance: Mathematics

and Economics, 33, 551-566.

Paulsen, J., Gjessing,H., 1997, Optimal choice of dividend barriers for a risk process with

stochastic return on investments, Insurance: Mathematics and Economics, 20, 215-223.

Panjer, H.H., Willmot, G.E., 1992, Insurance Risk Models, Society of Actuaries, Schaumburg.

Segerdahl, C., 1970, On some distributions in time connected with the collective theory of

risk, Scandinavian Actuarial Journal, 167-192.

Willmot, G.E., Dickson, D.C.M., 2003, The Gerber-Shiu discounted penalty function in the

stationary renewal risk model, Insurance: Mathematics and Economics, 32, 403-411.

30

Willmot, G.E., Lin, X.S., 2001, Lundberg approximations for compound distributions with

applications, Springer-Verlag, New York.

Zhou, X., 2004, The risk model with a two-step premium rate, preprint.

31