supplement jp morgan mozaic index (usd)

TRANSCRIPT

-1-

INDEX SUPPLEMENT

J.P. MORGAN MOZAIC INDEX (USD)

This document contains information solely about the J.P. Morgan MOZAIC Index (USD) (the “Index”), which information has been provided by J.P. Morgan Securities LLC (“JPMS”) solely in its capacity as a licensor of the Index. The Index and certain relevant “Selected Considerations” are described in further detail within the document and are qualified in their entirety by the index rules (the “Rules”) which are appended hereto. Please read the information under the section titled “Important Information” below before reading any other material in this document.

IMPORTANT INFORMATION

The Index has been and may be licensed to one or several licensees (collectively, the “Licensee”) for the Licensee’s benefit. Neither the Licensee nor any product of the Licensee (the “Product”) is sponsored, operated, endorsed, sold or promoted by JPMS or any of its affiliates (together and individually, “J.P. Morgan”). J.P. Morgan makes no representation and no warranty, express or implied, to owners of the Product (or any person taking exposure to it) or any member of the public in any other circumstances (each a “Contract Owner”): (a) regarding the advisability of investing in securities or other financial or insurance products generally or in the Product particularly; or (b) the suitability or appropriateness of an exposure to the Index in seeking to achieve any particular objective. It is for those taking an exposure to the Product and/or the Index to satisfy themselves of these matters and such persons should seek appropriate professional advice before making any investment. J.P. Morgan is not responsible for and does not have any obligation or liability in connection with the issuance, administration, marketing or trading of the Product. The publication of the Index and the referencing of any asset or other factor of any kind in the Index do not constitute any form of investment recommendation or advice in respect of any such asset or other factor by J.P. Morgan, and no person should rely upon it as such. J.P. Morgan does not act as an investment adviser or investment manager in respect of the Index or the Product and does not accept any fiduciary duties in relation to the Index, the Licensee, the Product or any Contract Owner.

The Index has been designed and is compiled, calculated, maintained and sponsored by J.P. Morgan without regard to the Licensee, the Product or any Contract Owner. The ability of the Licensee to make use of the Index may be terminated on short notice and it is the responsibility of the Licensee to provide for the consequences of that in the design of the Product. J.P. Morgan does not accept any legal obligation to take the needs of any person who may invest in a Product into account in designing, compiling, calculating, maintaining or sponsoring the Index or in any decision to cease doing so.

J.P. Morgan does not give any representation, warranty or undertaking, of any type (whether express or implied, statutory or otherwise) in relation to the Index, as to condition, satisfactory quality, performance or fitness for purpose or as to the results to be achieved by an investment in the Product or any data included in or omissions from the Index, or the use of the Index in connection with the Product or the veracity, currency, completeness or accuracy of the information on which the Index is based (and, without limitation, J.P. Morgan accepts no liability to any Contract Owner for any errors or omissions in that information or the results of any interruption to it and J.P. Morgan shall be under no obligation to advise any person of any such error, omission or interruption). To the extent any such representation, warranty or undertaking could be deemed to have been given by J.P. Morgan, it is excluded save to the extent that such exclusion is prohibited by law. To the fullest extent permitted by law, J.P. Morgan shall have no liability or responsibility to any person or entity (including, without limitation, to any Contract Owner) for any losses, damages, costs, charges, expenses or other liabilities howsoever arising, including, without limitation, liability for any special, punitive, indirect or consequential damages (including loss of business or loss of profit, loss of time and loss of goodwill), even if notified of the possibility of the same, arising in connection with the design, compilation, calculation, maintenance or sponsoring of the Index or in connection with the Product.

The Index is the exclusive property of J.P. Morgan. J.P. Morgan is under no obligation to continue compiling, calculating, maintaining or sponsoring the Index and may delegate or transfer to a third party some or all of its functions in relation to the Index.

-2-

J.P. Morgan may independently issue or sponsor other indices or products that are similar to and may compete with the Index and the Product. J.P. Morgan may also transact in assets referenced in the Index (or in financial instruments such as derivatives that reference those assets). It is possible that these activities could have an effect (positive or negative) on the value of the Index and the Product.

Each of the above paragraphs is severable. If the contents of any such paragraph is held to be or becomes invalid or unenforceable in any respect in any jurisdiction, it shall have no effect in that respect, but without prejudice to the remainder of this notice.

-3-

SELECTED CONSIDERATIONS

The Index Calculation Agent and the Index Sponsor have discretion over the Index, and neither the Index

Calculation Agent nor the Index Sponsor has an obligation to consider the interests of investors and others that

may have exposure to Products linked to the Index.

J.P. Morgan Securities plc (“JPMS plc”), an affiliate of JPMorgan Chase & Co., currently acts as the Index calculation agent (the “Index Calculation Agent”) and is responsible for calculating the level of the Index and determining the effect of certain developments on the Index. The Index Calculation Agent is entitled to exercise discretion in relation to the Index, including but not limited to the calculation of the level of the Index in the event of an Extraordinary Event or FX Disruption Event as well as the determination of the occurrence of a Market Disruption Event (each as defined below under “The J.P. Morgan MOZAIC Index (USD)”), and may also amend the rules governing the Index in certain circumstances. JPMS plc is also the Index Sponsor and is responsible for, among other things, the documentation of the Rules and the appointment of the Index Calculation Agent, and the Index Sponsor may also amend the rules governing the Index, as it deems appropriate. The judgments, policies and decisions for which the Index Calculation Agent and the Index Sponsor are responsible could have an impact, positive or negative, on the level of the Index.

In taking any actions that might affect the Index, including the calculation of the Index level, neither the Index Calculation Agent nor the Index Sponsor has an obligation to consider the interests of investors or others that may have exposure to Products linked to the Index. JPMorgan Chase & Co., as the ultimate parent company of JPMS plc, controls the Index Calculation Agent and the Index Sponsor. Furthermore, the selection of the constituents of the Index (the “Constituents”) is not an investment recommendation by JPMS plc or any of its affiliates of the Constituents, or any of the securities, commodities, indices or futures contracts underlying the Constituents. See “The J.P. Morgan MOZAIC Index (USD).”

The Index methodology may not be successful and may not outperform any alternative strategy that might be

employed in respect of the Constituents.

The Index methodology follows a notional proprietary strategy that operates on the basis of pre-determined rules. No assurance can be given that the investment strategy on which the Index is based will be successful or that the Index will outperform any alternative strategy that might be employed in respect of the Constituents.

The Constituents may not achieve their target volatility rate.

Each selected Constituent has a Constituent Target Volatility (as defined below), which is used in determining the weight applied to such Constituent following a rebalancing. In calculating the level of the Index, the performance of each selected Constituent is scaled by its weight, which is in turn determined by comparing such Constituent’s recent actual volatility against the target volatility rate, subject to an upper-bound limit of 1,000% (the “Upper-Bound Limit”). A selected Constituent whose recent volatility exceeded the target volatility will generally have a weight that dampens the contribution of such Constituent’s performance in the calculation of the Index level, while a selected Constituent whose recent volatility was less than the target volatility will generally have a weight that magnifies the contribution of such Constituent’s performance. Because weights are established on the basis of the historical Constituent volatility and subject to the Upper-Bound Limit and because the realized volatility of a Constituent once its weight is put into effect may differ significantly from its historical levels and may change rapidly at any time, there can be no assurance the weighted average performance of any Constituent in the Index will realize an actual volatility equal to the Constituent Target Volatility. The actual realized volatility of any Constituent’s weighted performance in the Index could be significantly greater or less than the target volatility rate.

Furthermore, while it is generally the case that the target volatility rates will sum to a “round” number if at any time six Constituents are currently referenced by the Index, as described below under “The J.P. Morgan MOZAIC Index (USD),” under certain circumstances, there may be more or fewer than six Constituents referenced by the Index, which may create further differences between the target volatility and actual realized volatility.

-4-

If the values of the Constituents change or the market value of the futures contracts underlying the Constituents

changes, the level of the Index may not change in the same manner.

Changes in the values of the Constituents or the futures contracts underlying the Constituents may not result in a comparable change in the level of the Index. This is due to the fact that the Constituents are weighted in accordance with the Index’s methodology, as prescribed by the Rules. Such weights can have the effect of amplifying or dampening the performance of the Constituents, and the weights are rebalanced, generally on a monthly basis, and may be subject to “flattening” and other periods in which weights are set to zero. The Index’s changes will not be comparable to those of an index comprised of static and equally weighted notional exposures to the Constituents.

The Index is not comprised of actual assets.

The exposures to the Constituents are purely notional and will exist solely in the records maintained by or on behalf of the Index Calculation Agent. There is no actual portfolio of assets to which any person is entitled or in which any person has any ownership interest.

The Index has a limited operating history and may perform in unanticipated ways.

The “Live Date” for the Index was April 17, 2009, and therefore the Index has a limited operating history. Any back-testing or similar analysis performed by any person with respect to the Index must be considered illustrative only and may be based on estimates or assumptions not used by the Index Calculation Agent when determining the level of the Index. Past performance should not be considered indicative of future performance.

Any future downgrades of the U.S. government’s credit rating by credit rating agencies may adversely affect the

performance of the Index.

In 2011, Standard & Poor’s Ratings Services (“Standard & Poor’s”) downgraded the U.S. government’s credit rating from AAA to AA+. The downgrade increased volatility in the global equity, credit and commodities markets, which might have adversely affected the levels of the Constituents. Future downgrades by credit ratings agencies may also increase this volatility. This may in turn have an adverse impact on the Index.

There are risks associated with the Index’s momentum investment strategy.

The Index is constructed using what is generally known as a momentum investment strategy. Momentum investing generally seeks to capitalize on positive trends in the price of assets. As such, the weights of the Constituents in the Index are based on the performance of the Constituents from a recent historical period of approximately six months. However, there is no guarantee that trends existing in the preceding period will continue in the future. A momentum strategy is different from a strategy that seeks long-term exposure to a portfolio consisting of constant components with fixed weights. The Index may fail to realize gains that could occur as a result of holding assets that have experienced recent poor performance, but that subsequently experience a recovery. Conversely, the Index may suffer losses as a result of holding assets that have experienced recent strong performance, but subsequently suffer a reversal. As a result, if market conditions do not represent a continuation of prior observed trends, the level of the Index, which is rebalanced based on prior trends, may decline or fail to appreciate. In particular, while momentum investing strategies are effective at identifying the market direction in trending markets, in non-trending, sideways markets, momentum investment strategies are subject to “whipsaws.” A whipsaw occurs when the market reverses and does the opposite of what is indicated by the trend indicator, resulting in a trading loss during the particular period. Consequently, the Index may perform poorly in non-trending, “choppy” markets characterized by short-term volatility.

Additionally, due to the “long-only” construction of the Index, the weight of each Constituent will not be negative in respect of any rebalancing even if the relevant Constituent displayed a negative performance over the relevant six-month period.

No assurance can be given that the investment strategy used to construct the Index will outperform any alternative index that might be constructed from the Constituents.

-5-

The investment strategy used to construct the Index involves monthly rebalancing that is applied to the Constituents

The Constituents are subject to monthly rebalancing. By contrast, a synthetic portfolio that does not rebalance monthly could see greater compounded gains over time through exposure to a consistently and rapidly appreciating portfolio consisting of the Constituents. Therefore, your return on Products linked to the Index may be less than the return you could realize on an alternative investment that is not subject to rebalancing.

Rebalancings and exposure flattenings are not effected or, in certain instances, may be effected on a delayed or

modified basis, with respect to Constituents in respect of which a relevant weekday is not a Scheduled Trading Day,

in respect of which such weekday is a Disrupted Day or in certain other circumstances.

Although Index rebalancings are generally scheduled to occur as of the first weekday of each month and exposure flattenings can be triggered as of any weekday based on recent declines in the Index level, in the event the relevant weekday (or in certain circumstances with respect to the GSCI IM Index, the next weekday) is not a Scheduled Trading Day or is a Disrupted Day with respect to a Constituent (except with respect to certain types of Disrupted Days affecting the GSCI AG Index, which can cause a postponement in such Constituent’s rebalancing, as further described below) or in certain other circumstances, that Constituent will, in the case of rebalancing, not be rebalanced that month, and, in the case of the exposure flattening mechanism, will not be subject to the initiation of an exposure flattening period and hence will not have its weight adjusted to zero (if it is positive at that time). With respect to the GSCI AG Index, a rebalancing may be postponed rather than canceled if an Agricultural Commodities Postponement Event occurs on the relevant Scheduled Trading Day (although the rebalancing would be canceled if an earlier Agricultural Commodities Postponement Resolution Period (as defined below) were continuing or had only recently been resolved), and in such case, modifications would be made to the calculations of the GSCI AG Index returns and of the Index level (including the use of settlement pricing) upon the resolution of the applicable Agricultural Commodities Postponement Resolution Period. In addition, an Agricultural Commodities Postponement Event occurring (a) at the onset of an exposure flattening period or (b) during an exposure flattening period for the GSCI AG Index can cause a delay in the (aa) onset or (bb) termination of such exposure flattening period and modifications to the calculations of the GSCI AG Index returns and of the Index level (including the use of settlement pricing) upon the commencement or conclusion of such exposure flattening period. Such occurrences may yield positive weights for more or fewer than six Constituents in a given month, may cause continued Index declines during what would otherwise be an exposure flattening period for the affected Constituents and may have other consequences that may adversely impact the Index. For more information on the Index’s monthly rebalancing and its exposure flattening mechanism, including with respect to the GSCI IM Index and GSCI AG Index, see “The J.P. Morgan MOZAIC Index (USD).”

The Index’s exposure flattening mechanism may not be successful in preventing the Index level from declining,

and may in fact cause the Index to have worse performance.

The Index’s exposure flattening mechanism is only triggered following recent historical declines of the Index level of more than 3.00% over a five-weekday period, and then only after a lag. In addition, in the event that a weekday on which an exposure flattening period would have been triggered in respect of one or more Constituents is not a Scheduled Trading Day or, other than with respect to the GSCI AG Index, is a Disrupted Day in respect of those Constituents (and in certain other circumstances with respect to the GSCI IM Index and the GSCI AG Index), the exposure flattening mechanism will not alter the weights of those Constituents, and hence those Constituents may continue to cause declines in the Index level notwithstanding prior declines in the Index level that were sufficient to trigger an exposure flattening period.

In measuring the Index level changes during an historical five-weekday observation period, the exposure flattening mechanism takes into account the effect of any exposure flattening period that overlapped with such observation period, and hence the exposure flattening mechanism may not take into account the full extent of the negative performance of the normally weighted Constituents. This in turn may result in an exposure flattening period not being triggered even though negative performance of the normally weighted Constituents would otherwise justify it.

For the foregoing reasons, the exposure flattening mechanism cannot be considered a safeguard against declines in the Index level. Furthermore, if Constituents subject to the exposure flattening mechanism recover their

-6-

losses during the relevant exposure flattening period, the Index will not capture such recovery, resulting in lower performance. For more information on the exposure flattening mechanism, see “The J.P. Morgan MOZAIC Index (USD).”

Constituent weights are subject to a high upper-bound limit and hence can increase exposure to Constituents in a

way that effectively exposes the Index to leverage, potentially causing increased volatility in the Index level.

For each selected Constituent, the rebalancing mechanism sets the weight of such Constituent to a level that would have caused the weighted historical performance of such Constituent over a recent 125-weekday observation period (approximately six months) (the “Lookback Period,” as defined in greater detail below under “The J.P. Morgan MOZAIC Index (USD)”) to have a volatility equal to the Constituent Target Volatility, subject to the Upper-Bound Limit. In connection with a rebalancing, a selected Constituent whose volatility over the Lookback Period was less than the Constituent Target Volatility will generally have a new weight that magnifies the contribution of such Constituent’s performance in the calculation of the Index level, producing results similar to leverage. When weights magnify Constituent performance, any movements in the prices or levels of the Constituents may result in greater changes in the levels of the Index than if leverage were not used. In particular, leverage will magnify any negative performance of the Constituents.

The Index tracks daily weighted percentage changes in Constituent prices and levels, and hence the daily

contribution of changes in Constituent prices and levels to changes in the Index level is not path dependent.

The Index does not track a hypothetical fixed level of investment in the Constituents, but rather the weighted percentage changes in the prices and levels of the Constituents. Prior period changes in a Constituent’s price or level does not impact the contribution of changes in the price or level of such Constituent in the current measurement period to changes in the Index level, except to the extent that such changes are reflected in the methodology for monthly rebalancing and with respect to the application of the Constituent flattening mechanism. For example, a significant downward change in the price or level of a Constituent immediately prior to the current measurement period will not – except in the context of monthly rebalancings and the application of the Constituent flattening mechanism – dampen the contribution of current or future changes in such Constituent’s price or level to changes in the Index level. As such, the daily contribution of changes in Constituent prices and levels to changes in the Index level is not price dependent.

Lower weights of Constituents will dampen the impact of their returns on the Index level.

A selected Constituent whose volatility over the Lookback Period exceeded the Constituent Target Volatility will generally have a weight that dampens the contribution of such Constituent’s performance in the calculation of the Index level. As a result, any positive performance of Constituents subject to such weight to the Index level will not be fully reflected in the Index level.

The Index may be notionally uninvested.

A number of circumstances – including recent poor performance of some or all of the Constituents resulting in zero weights in the rebalancing process or through the imposition of exposure flattening periods – may result in the Index being partially or completely “uninvested” on a notional basis. To the extent the sum of all Constituent weights is less than 100%, a portion of the Index may be considered notionally “uninvested” and the returns in respect of such portion will be zero. If the sum of all Constituent weights is equal to zero, the Index value will remain unchanged, reflecting zero returns for each day such sum is equal to zero.

The Index is subject to significant risks associated with futures contracts.

The Constituents are comprised of futures contracts and indices that track futures contracts. The price of a futures contract depends not only on the price of the underlying asset referenced by the futures contract, but also on other factors, including but not limited to changing supply and demand relationships, interest rates, governmental and regulatory policies and the policies of the exchanges on which the futures contracts trade. In addition, the futures markets are subject to temporary distortions or other disruptions due to various factors, including lack of liquidity in

-7-

the markets, participation of speculators, and government regulation and intervention. These factors and others can cause the prices of futures contracts to be volatile and unpredictable.

The settlement price of the futures contracts may not be readily available.

The official settlement price of the relevant futures contracts are used to calculate the level of the Index. Any disruption in trading of the relevant futures contracts could delay the release or availability of the official settlement price. This may delay or prevent the calculation of the Index.

Some of the Constituents are excess return commodity indices, which carry risks associated with notional

investments in such indices.

The commodity-linked Constituents are excess return indices within the S&P GSCITM commodity index group. The policies of the sponsor of these indices concerning methodology and calculation, including decisions regarding additions, deletions or substitutions of the assets underlying the indices, could affect the level of these Constituents.

The excess return indices constituting the commodity-linked Constituents track returns from hypothetical exposures to certain commodity futures contracts that take into account changes in the price level of the underlying futures contracts as well as roll yield, but not “total returns.” A commodity futures index that reflects “total returns” would reflect the returns from a notional fully collateralized investment in the underlying futures contracts, including any interest that could be earned on funds committed to the margin on the underlying futures contracts.

The Index may be affected by significant volatility in the Constituents, each of which is subject to the volatility

associated with futures contracts.

Prices are subject to sudden changes and can move dramatically over short periods of time, even when they have been relatively stable for an extended period of time leading up to the change. As a result, the levels of the Constituents and, therefore, the Index may decline dramatically before the resulting increased volatility will be reflected in the Lookback Periods used to measure historical volatility in the Index’s rebalancing mechanism. Consequently, the Index may experience sharp declines over short periods of time, notwithstanding the target volatility feature. This risk may be magnified by the risks associated with futures contracts.

Suspensions or disruptions of market trading in futures contracts may adversely affect the Index.

Futures markets are subject to temporary suspensions, distortions or other disruptions due to various factors, including lack of liquidity, participation of speculators, and government regulation and intervention. In addition, U.S. and other futures exchanges have regulations that limit the magnitude of futures contract price changes that may occur in a single day. These limits may be referred to as “daily price fluctuation limits” and the maximum or minimum price of a contract on any given day as a result of these limits may be referred to as a “limit price.” Once the limit price has been reached in a particular contract, no trades may be made at a price beyond the limit (although trades can continue within the limit), or trading may be limited for a set period of time. Limit prices have the effect of precluding trading in a particular contract or forcing the liquidation of contracts at potentially disadvantageous times or prices. These circumstances could affect the level of the Index.

The performance of foreign currency denominated Constituents is not adjusted for exchange rate movements when

determining relative performance and weights for a monthly rebalancing.

In the monthly rebalancing process, the six highest Constituent return levels are assessed based on the cumulative returns of each Constituent in local currency terms, without adjusting for currency differences, over the Lookback Period. As a result, Constituents that, on a dollar-adjusted basis, had relatively weaker or even negative performance, may nevertheless be ranked high enough to receive a positive weight in the upcoming period. This will have the consequence of producing notional allocations that may differ from those that would have obtained had they been based on performance measured on a dollar-parity basis. And, as indicated below, even though currency

-8-

adjustment is not made when determining weights, the Index level itself does take into account currency fluctuation against the U.S. dollar.

The Index level will be subject to currency exchange risk.

Because the returns on Constituents that are futures contracts on foreign equity indices or government-issued fixed income securities are converted into U.S. dollars for the purposes of calculating the returns of the Index, the Index level will reflect currency exchange rate risk with respect to each of the relevant foreign currencies. The returns of the Index, however, will not reflect the changes in the notional value of the non-U.S. Constituents due solely to changes in the value of those currencies against the U.S. dollar. Such currency exchange risk, therefore, will depend on the extent to which those currencies strengthen or weaken against the U.S. dollar together with whether each non-U.S. Constituent appreciates or declines in value, as adjusted by the applicable weights of such non-U.S. Constituent in the Index. For example, if a non-U.S. Constituent has a positive daily return (as measured in its local currency), and the U.S. dollar strengthens against such non-U.S. Constituent’s currency, such non-U.S. Constituent’s contribution to the Index’s return shall be less than it would have been had its contribution been based solely on its local currency return. Furthermore, if a non-U.S. Constituent has a negative daily return (as measured in its local currency), and the U.S. dollar weakens against such non-U.S. Constituent’s currency, such non-U.S. Constituent’s negative contribution to the Index’s return shall be greater than it would have been had its contribution been based solely on its local currency return.

Of particular importance to potential currency exchange risk are:

• existing and expected rates of inflation;

• existing and expected interest rate levels;

• the balance of payments;

• political, civil or military unrest; and

• the extent of governmental surpluses or deficits in the relevant countries and the United States.

All of these factors are, in turn, sensitive to the monetary, fiscal and trade policies pursued by the governments of various countries, including the United States and other countries important to international trade and finance.

The Constituents comprising the Index may be replaced by substitutes in certain events.

Following the occurrence of certain events with respect to a Constituent as described under “The J.P. Morgan MOZAIC Index (USD),” the affected Constituent may be replaced by a substitute futures contract, index or other asset, index or measure. The changing of a Constituent may affect the performance of the Index, as the replacement Constituent may perform significantly worse than the affected Constituent on either a standalone basis or as measured by its contribution to the Index’s return.

The Index is subject to market risks.

The performance of the Index is dependent on the performance of the Constituents.

Certain Constituents are subject to significant risks associated with government-issued fixed-income securities and

may be volatile.

The fixed income-linked Constituents are futures contracts for U.S., German and Japanese government-issued debt securities. The market prices of the underlying debt securities may be volatile and significantly influenced by a number of factors, particularly the yields on these instruments as compared to current market interest rates and the actual or perceived credit quality of the governments issuing the underlying debt securities.

-9-

In general, fixed-income securities are significantly affected by changes in current market interest rates. As interest rates rise, the price of fixed-income securities, such as the government-issued debt securities underlying certain Constituents, may decrease, and as interest rates decrease, the price of fixed-income securities, such as these underlying debt securities, may increase. Interest rates are subject to volatility due to a variety of factors, including:

• sentiment regarding underlying strength or weakness in the economies of the governments issuing the underlying debt securities and global economies;

• expectations regarding the level of price inflation;

• sentiment regarding credit quality in the governments issuing the underlying debt securities and global credit markets;

• central bank policies regarding interest rates; and

• the performance of global capital markets.

Fluctuations in interest rates could affect the levels of the Constituents and the Index.

U.S. rating agencies have recently downgraded the credit ratings and/or assigned negative outlooks to many governments worldwide, including the United States, Germany and Japan, and may continue to do so in the future. Any perceived decline in the creditworthiness of a government that issues securities underlying a fixed income-linked Constituent as a result of a credit rating downgrade or otherwise, may cause the yield on the relevant securities to increase and the prices of such securities to fall, perhaps significantly, and may cause increased volatility in local or global credit markets. Any such decline over the term of a Product linked to the Index would adversely impact the prices of the futures contracts underlying the relevant fixed income-linked Constituent and could have a negative impact on the level of the Index and the value of such Product.

The Constituents may be affected in unexpected ways by the recent sovereign debt crisis in Europe and related

global economic conditions.

The recent European debt crisis and related European financial restructuring efforts have contributed to instability in global markets. If global economic and market conditions, or economic conditions in Europe, the United States or other key markets, remain uncertain or deteriorate further, the Constituents may be affected in unexpected ways. If a sovereign government were to default on its debt obligations, or if the market perceives that a default has become more likely, yields on the government-issued debt securities underlying the fixed income-linked Constituents may change rapidly and dramatically, and such changes may adversely affect the level of the Index.

Commodity prices are characterized by high and unpredictable volatility, which could lead to high and

unpredictable volatility in prices and levels of the commodity-linked Constituents and hence in the Index.

Market prices of the commodities and commodity futures contracts underlying the commodity-linked Constituents tend to be highly volatile and may fluctuate rapidly based on numerous factors, including: changes in supply and demand relationships; governmental programs and policies, national and international monetary, trade, political and economic events, changes in interest rates and exchange rates, speculation and trading in commodities and related contracts, weather, and agricultural, trade, fiscal and exchange control policies. Many commodities are also highly cyclical. These factors may affect the levels of the indices that comprise the commodity-linked Constituents in varying ways, and different factors may cause the value of different commodities included in the commodity-linked Constituents, and the prices of their futures contracts, to move in inconsistent directions at inconsistent rates. This, in turn, may adversely affect the Index.

The Index provides only one means for exposure to commodities. The high volatility and cyclical nature of commodity markets may render these investments inappropriate as the focus of an investment portfolio.

-10-

Certain Constituents or their underlying futures contracts are foreign futures contracts, and in some cases such

futures contracts are linked to foreign securities.

Certain fixed income- and equity-linked Constituents are foreign futures contracts linked to foreign securities, and certain futures contracts underlying the indices that constitute the commodity-linked Constituents are foreign commodity futures contracts. With respect to such Constituents, the performance of the underlying foreign futures contracts depends on conditions on foreign futures markets, which may differ substantially from conditions in U.S. markets. And in the case of fixed income- and equity-linked Constituents that constitute foreign futures contracts, the futures contracts are in turn linked to securities issued by non-U.S. companies and non-U.S. governments. As a result, the values of these futures contracts, and ultimately of the related Constituents, will also be affected by political, economic, financial and social factors in the relevant countries, including changes in a relevant country’s government, economic and fiscal policies, currency exchange laws and other foreign laws or restrictions. The economies of these countries may differ unfavorably from the economy of the United States in such respects as growth of gross national product, rate of inflation, market volatility, capital reinvestment, resources and self-sufficiency. These countries may be subjected to different and, in some cases, more adverse economic environments. Some or all of these factors may adversely impact the value of the affected Constituents and hence of the Index and may exacerbate negative changes or offset positive changes resulting from other factors.

The Index may in the future include contracts that are not traded on regulated futures exchanges.

The Index, through its exposure to the Constituents, is currently based solely on futures contracts traded on regulated futures exchanges (referred to in the United States as “designated contract markets”). If these exchange-traded futures contracts cease to exist, or if the calculation agent for the Constituents substitutes a futures contract in certain circumstances, the Index may in the future include futures contracts or over-the-counter contracts traded on trading facilities that are subject to lesser degrees of regulation or, in some cases, no substantive regulation. As a result, trading in such contracts, and the manner in which prices and volumes are reported by the relevant trading facilities, may not be subject to the provisions of, and the protections afforded by, the Commodity Exchange Act, or other applicable statutes and related regulations that govern trading on regulated futures exchanges. In addition, many electronic trading facilities have only recently initiated trading and do not have significant trading histories. As a result, the trading of contracts on such facilities, and the inclusion of such contracts in the Index, through its exposure to the Constituents, may be subject to certain risks not presented by regulated exchange-traded futures contracts, including risks related to the liquidity and price histories of the relevant contracts.

An increase in the margin requirements for commodity futures contracts included in the Non-Securities-based

Constituents may adversely affect the level of the Index.

Futures exchanges require market participants to post collateral in order to open and to keep open positions in futures contracts. If an exchange increases the amount of collateral required to be posted to hold positions in commodity futures contracts underlying the Non-Securities-based Constituents, market participants who are unwilling or unable to post additional collateral may liquidate their positions, which may cause the price of the relevant commodity futures contracts to decline significantly. As a result, the level of the Index and the value of the CDs may be adversely affected.

JPMS is a primary dealer in connection with purchases and sales of U.S. Treasury securities by the Federal Reserve

and JPMS’s actions in that capacity may affect the level of the Index.

JPMS is one of the primary dealers through which the Federal Reserve conducts open-market purchases and sales of U.S. Treasury and federal agency securities, including 2-Year Treasury Notes, 5-Year Treasury Notes and 10-Year Treasury Notes. Such activities may affect the prices and yields on the U.S. Treasury securities underlying the Constituents linked to U.S. government-issued debt securities and hence the level of the Index. JPMS has no obligation to take into consideration the Index when undertaking these activities.

-11-

Correlation of performances among the Constituents may reduce the performance of the Index.

Performances of the Constituents may become highly correlated from time to time, including, but not limited to, a period in which there is a substantial decline in a particular sector or asset type represented by the Constituents and which has a higher weight in the Index relative to any of the other sectors or asset types, as determined by the Index’s strategy. High correlation during periods of negative returns among Constituents representing any one sector or asset type could have an adverse effect on the Index.

Changes in the value of the Constituents may offset each other.

At a time when the value of a Constituent representing a particular asset class or geographic region increases, the value of other Constituents representing a different asset class or geographic region may not increase as much or may decline. Therefore, in calculating the level of the Index, increases in the values of some of the Constituents may be moderated, or more than offset, by lesser increases or declines in the values of other Constituents.

Any Products linked to the Index will not be regulated by the Commodity Futures Trading Commission.

An investment in any Products linked to the Index neither constitutes an investment in futures contracts, options on futures contracts nor a collective investment vehicle that trades in these futures contracts (i.e., the Products will not constitute a direct or indirect investment by a Contract Owner in the futures contracts), and a Contract Owner would not benefit from the regulatory protections of the Commodity Futures Trading Commission, commonly referred to as the “CFTC.” Among other things, this means that J.P. Morgan is not registered with the CFTC as a futures commission merchant and a Contract Owner would not benefit from the CFTC’s or any other non-U.S. regulatory authority’s regulatory protections afforded to persons who trade in futures contracts on a regulated futures exchange through a registered futures commission merchant. For example, the price a Contract Owner pays to purchase any such Products would be used by J.P. Morgan for its own purposes and would not be subject to customer funds segregation requirements provided to customers that trade futures on an exchange regulated by the CFTC.

Unlike an investment in any such Products, an investment in a collective investment vehicle that invests in futures contracts on behalf of its participants may be subject to regulation as a commodity pool and its operator may be required to be registered with and regulated by the CFTC as a commodity pool operator, or qualify for an exemption from the registration requirement. Because such Products would not be interests in a commodity pool, the Products would not be regulated by the CFTC as a commodity pool, J.P. Morgan would not be registered with the CFTC as a commodity pool operator, and a Contract Owner would not benefit from the CFTC’s or any non-U.S. regulatory authority’s regulatory protections afforded to persons who invest in regulated commodity pools.

J.P. Morgan has not independently verified disclosures that were derived from publically available information.

The disclosures contained in this index supplement derived from publicly available sources have not been independently verified by J.P. Morgan. J.P. Morgan has not participated, and will not participate, in the preparation of such documents or made any due diligence inquiry with respect to the issuer of a security on which relevant futures contracts or an index is linked. J.P. Morgan cannot give any assurance that all events occurring prior to the date of this disclosure (including events that would affect the accuracy or completeness of the publicly available documents of the issuer of such security) that would affect the closing price of that security will have been publicly disclosed. Subsequent disclosure of any of those events or the disclosure of or failure to disclose material future events concerning the issuer of any such security could adversely affect the Index.

J.P. Morgan has no affiliation with the Underlying Index Sponsors

J.P. Morgan is not affiliated with S&P Dow Jones Indices LLC, Deutsche Börse AG or Nikkei Inc. (the “Underlying Index Sponsors”) in any way (except for arrangements discussed below in “THE S&P GSCI INDICES — License Agreement”) and have no ability to control the Underlying Index Sponsors, including any errors in or discontinuation of disclosure regarding their methods or policies relating to the calculation of the Constituents. The Underlying Index Sponsors are under no obligation to continue to calculate their respective Constituents nor are they required to calculate any successor indices. If the Underlying Index Sponsors discontinue or suspend the calculation

-12-

of a relevant index, it may become difficult to determine values that are relevant for calculations related to the Index and any Product linked to the Index.

S&P Dow Jones Indices LLC may be required to replace a contract underlying an S&P GSCI Index, if the existing

futures contract is terminated or replaced.

A futures contract known as a “Designated Contract” has been selected as the reference contract for the underlying physical commodity included in the S&P GSCI Index. Data concerning this Designated Contract will be used to calculate the S&P GSCI Index. The termination or replacement of a futures contract on an established exchange occurs infrequently; however, if one or more Designated Contracts were to be terminated or replaced by an exchange, a comparable futures contract would be selected by the S&P GSCI Index Committee, as the case may be, if available, to replace each such Designated Contract. The termination or replacement of any Designated Contract may have an adverse impact on the value of the individual S&P GSCI Index. Suspension or disruptions of market trading in the commodity and related futures markets may adversely affect the value of any Products linked to the Index.

Some of the potential Constituent sub-indices will be subject to pronounced risks of pricing volatility.

As a general matter, the risk of low liquidity or volatile pricing around the maturity date of a commodity futures contract is greater than in the case of other futures contracts because (among other factors) a number of market participants take physical delivery of the underlying commodities. Many commodities, like those in the energy and industrial metals sectors, have liquid futures contracts that expire every month. Therefore, these contracts are rolled forward every month. Contracts based on certain other commodities, most notably agricultural and livestock products, tend to have only a few contract months each year that trade with substantial liquidity. Thus, these commodities, with related futures contracts that expire infrequently, roll forward less frequently than every month, and can have further pronounced pricing volatility during extended periods of low liquidity. In respect of Constituent sub-indices that represent energy, it should be noted that due to the significant level of its continuous consumption, limited reserves, and oil cartel controls, energy commodities are subject to rapid price increases in the event of perceived or actual shortages.

-13-

THE J.P. MORGAN MOZAIC INDEX (USD)

General

The J.P. Morgan MOZAIC Index (USD) (the “Index”) was developed and is maintained and calculated by J.P. Morgan Securities plc (“JPMS plc”). The description of the Index and methodology included in this index supplement is based on rules formulated by JPMS plc (the “Rules”). The Rules, and not this description, will govern the calculation and constitution of the Index and other decisions and actions related to their maintenance. The Rules in effect as of the date of this index supplement are included as part of the index supplement attached as Annex A to this index supplement. The Index is the intellectual property of JPMS plc, and JPMS plc reserves all rights with respect to its ownership of the Index.

The Index is published to Bloomberg L.P. on the page “JMOZUSD Index.” Live calculation of the Index commenced on April 17, 2009 (the “Live Date”), with Index levels calculated on a hypothetical historical basis from January 1, 1999 (the “Index Start Date”). The initial level of the Index for January 1, 1999 was set at 100.00 (the “Base Level”).

The Index tracks a dynamic, rules-based strategy offering notional exposure to a range of developed country government bond futures constituents (the “Government Bond Futures Constituents”) and developed country equity index futures constituents (the “Equity Index Futures Constituents” and together with the Government Bond Futures Constituents, the “Securities-based Constituents”) and exposure to certain listed excess return indices within the S&P GSCITM commodity index group (the “Non-Securities-based Constituents”, and together with the Securities-based Constituents, the “Constituents”).

The strategy underlying the Index and the Rules:

• tracks percentage changes in the daily-weighted prices and levels of selected Constituents, after adjusting for currency differences and the application of weights whose levels are determined and rebalanced on a monthly basis;

• selects, based on recent past performance, Constituents to be tracked on a monthly basis (typically six Constituents) from a candidate list of 12 Constituents;

• excludes Constituents with recent negative performance, regardless of their performance relative to others in the candidate list of 12 Constituents;

• establishes weights for the selected Constituents based on a “risk parity” framework that looks to recent historical volatility; and

• employs an exposure “flattening” feature to temporarily suspend exposures in the Constituents in the event recent overall performance has declined beyond a specified threshold.

To implement the foregoing strategy, the Rules contemplate a monthly rebalancing event, generally on the first weekday of each month, in respect of the Constituents. In the monthly rebalancing, the cumulative returns (in local currency terms, without adjusting for currency differences or the effect of compounding) of the 12 Constituents are measured over a recent 125-weekday observation period (approximately six months) (the “Lookback Period,” as defined in greater detail below). Each Constituent whose cumulative return in the Lookback Period is ranked in the highest six return levels will have a positive weight for the upcoming month so long as such Constituent’s cumulative performance over the Lookback Period was positive. The weights for each of the Constituents that did not have one of the six highest returns or whose returns were negative during the Lookback Period will be set to zero for the upcoming month.

If a Constituent is selected for the upcoming month, then its weight will be determined, based on a “risk parity” framework, to be the weight that would have yielded during the Lookback Period an annualized volatility of 7.75%÷6, or approximately 1.29% (the “Constituent Target Volatility”), subject to an upper-bound limit of 1,000%

-14-

(the “Upper-Bound Limit”). The risk parity framework generally results in higher weights to selected Constituents that had lower historical volatility in the Lookback Period and lower weights to those that had higher historical volatility during the Lookback Period.

The first weekday (or in certain circumstances, the next weekday) of a particular month is generally the Rebalancing Day (as defined below) for each Constituent, unless such weekday is not a Scheduled Trading Day (as defined below) or is a Disrupted Day (as defined below) with respect to a particular Constituent, in which case (except with respect to certain types of Disrupted Days affecting the GSCI AG Index, which can cause a postponement in such Constituent’s rebalancing, as further described below) that Constituent’s weight for the upcoming month will remain the same as the prior month’s weight. For a Disrupted Day affecting the GSCI AG Index that is attributable to an Agricultural Commodities Postponement Event affecting the GSCI AG Index, rebalancing may be postponed until the resolution of the applicable Agricultural Commodities Postponement Period, and in this case modifications would be made to the calculations of the GSCI AG Index returns and of the Index level (including the use of settlement pricing) upon the resolution of the applicable Agricultural Commodities Postponement Resolution Period.

In respect of each Constituent, on each Scheduled Trading Day that is not a Disrupted Day for such Constituent (subject to certain additional conditions with respect to the GSCI IM Index and modified conditions with respect to the GSCI AG Index), if the Index level declines by more than 3.00% over the five-weekday period ending on the second weekday immediately preceding such Scheduled Trading Day, then, notwithstanding its weight at that time, the weight of such Constituent will be subject to a five-weekday “flattening” period (beginning on the weekday immediately following such Scheduled Trading Day), during which time its weight will temporarily be set to zero, unless such Constituent is already then subject to an existing exposure flattening period. A Constituent that is already then subject to an exposure flattening period will remain in its original exposure flattening period and cannot be subject to a new exposure flattening period until the completion of the original period. Constituents in respect of which a given weekday either is not a Scheduled Trading Day or is a Disrupted Day (and in certain other circumstances with respect to the GSCI IM Index and the GSCI AG Index) will not be subject to the commencement of an exposure flattening period on the following weekday. In addition, an Agricultural Commodities Postponement Event occurring during an exposure flattening period for the GSCI AG Index can cause a delay in the termination of such exposure flattening period and modifications to the calculations of the GSCI AG Index returns and of the Index level upon the conclusion of such exposure flattening period.

The Index does not track a hypothetical fixed level of investment in the Constituents, but rather the

weighted percentage changes in the prices and levels of the Constituents. Accordingly, the daily contribution

of changes in Constituent prices and levels to changes in the Index level is not path dependent.

Constituent weights are subject to a high upper-bound limit but are not subject to a separate leverage

charge in the event weights exceed 100%. Individual and total weights of the Constituents can exceed 100%

and each can be as low as zero, but Constituent weights can never be negative, or synthetically short, either in

the aggregate or in respect of any single Constituent. To the extent the sum of all Constituent weights is less

than 100%, a portion of the Index may be considered notionally “uninvested” and the returns in respect of such

portion will be zero. If the sum of all Constituent weights is equal to zero, the Index value will remain

unchanged, reflecting zero returns for each day such sum is equal to zero.

No assurance can be given that the Index’s strategy will be successful or that the Index will generate

positive returns or will outperform any alternative strategy that might be constructed from the Constituents.

Furthermore, the future volatility of any Constituent may not be consistent with its historical volatility. The

actual realized volatility of any Constituent may be greater or less than the Constituent Target Volatility.

The Index is described as tracking “notional” or “synthetic” exposures because there is no actual

portfolio of assets to which any person is entitled or in which any person has any ownership interest. The Index

merely references certain assets, the performance of which will be used as a reference point for calculating the

Index level.

Any Index level prior to the Live Date is a hypothetical historical, or “back-tested,” level. Such levels

should not be taken as an indication of future performance, and no assurance can be given as to the levels or

performance of the Index on a future date. Back-tested results are achieved by means of a retroactive

-15-

application of a back-tested model designed with the benefit of hindsight. The Index Calculation Agent, in

calculating hypothetical back-tested index levels, may have applied the disruption provisions specified in the

Rules differently than it otherwise would have applied such provisions in a “live” calculation scenario.

Additionally, the precision and rounding of the levels of the Index or a Constituent (or other calculated values)

may differ from the methodology applied on a going forward basis. In calculating the hypothetical historical

levels, the Index Calculation Agent may have made certain assumptions in respect of the timing surrounding

the publication of certain indicators and Index levels. These assumptions may have a material impact on the

back-tested levels occurring on or before the Live Date. No representation is made that any investment that

references the Index will or is likely to achieve returns similar to any hypothetical historical returns.

Alternative modeling techniques or assumptions might provide different results. Finally, back-tested results

of past performance are neither an indicator nor a guarantee of future performance or returns. Actual results

and performance may vary compared to such hypothetical back-tested levels.

-16-

Index Sponsor; Index Calculation Agent; Amendment of Rules; Limitation of Liability

JPMS plc is the sponsor of the Index (the “Index Sponsor”). The Index Sponsor is responsible for, among other things, the creation and design of the Index, the documentation of the Rules, and the appointment of the calculation agent of the Index (the “Index Calculation Agent”), which may be the Index Sponsor, a non-related third party or an affiliate or subsidiary of the Index Sponsor. As of the date of this Index Supplement, JPMS plc is also the Index Calculation Agent.

The Index Calculation Agent is responsible for:

• calculating the Index level in respect of each weekday in accordance with the Rules; and

• determining (subject to the prior agreement of the Index Sponsor) if a Market Disruption Event, Disrupted Day or Extraordinary Event (or other similar event) has occurred and the related consequences and adjustments in accordance with the Rules.

The Index Calculation Agent will act in good faith and in a commercially reasonable manner with respect to the performance of its obligations and the exercise of its discretion pursuant to the Rules. The Index Sponsor may at any time and for any reason terminate the appointment of an Index Calculation Agent and appoint an alternative entity as the replacement Index Calculation Agent.

While the Rules are intended to be comprehensive, ambiguities may arise. In those circumstances, the Index Calculation Agent will resolve those ambiguities in a reasonable manner and, if necessary, amend the Rules to reflect that resolution.

The Index Calculation Agent’s determinations in respect of the Index and interpretations of the Rules will be final.

The Index Sponsor may delegate and/or transfer any of its obligations or responsibilities in connection with the Index to one or more entities which it determines are appropriate. The Index Calculation Agent must obtain written permission from the Index Sponsor prior to any delegation or transfer of its responsibilities or obligations in connection with the Index to a third party.

None of the Index Sponsor, the Index Calculation Agent or any of their respective affiliates or subsidiaries or any of their respective directors, officers, employees, representatives, delegates or agents (each a “Relevant

Person”) will have any responsibility to any person (whether as a result of negligence or otherwise) for any determinations made or anything done (or omitted to be determined or done) in respect of the Index or publication of the Index Level (or failure to publish such level) and any use to which any person may put the Index or the Index Level. No Relevant Person will take the interests of Contract Owners into account in making any determination in respect of the Index. All determinations in respect of the Index and the Index Level will be final, conclusive and binding and no person will be entitled to make any claim against any of the Relevant Persons in respect thereof. Once a determination or calculation is made or action taken by the Index Calculation Agent in respect of the Index, neither the Index Calculation Agent nor any other Relevant Person will be under any obligation to revise any determination or calculation made or action taken for any reason.

Constituents of the Index

There are currently 12 Constituents in the Index, of which five are Government Bond Futures Constituents, three are Equity Index Futures Constituents and four are Non-Securities-based Constituents. Government Bond Futures Constituents and Equity Index Futures Constituents are also referred to as Securities-based Constituents.

Government Bond Futures Constituents

The Government Bond Futures Constituents consist of:

-17-

• the CBOT 2-Year U.S. Treasury Note Futures Contract (Bloomberg ticker: ZT/TU), which is a series of exchange-traded futures contracts with expiry dates at three month intervals. As defined by the Relevant Exchange, the underlying unit of each contract is a single notional note issued by the U.S. Treasury that has a face value at maturity of $200,000, and Deliverable Grades of instruments eligible for settlement include U.S. Treasury notes with (a) an original term to maturity of not more than five years and three months and (b) a remaining term to maturity of not less than one year and nine months from the first day of the delivery month and not more than two years from the last day of the delivery month, where the invoice price equals the futures settlement price times a conversion factor, plus accrued interest, and the conversion factor is the price of the delivered note ($1 par value) to yield 6% (the “2 Year Note Futures”);

• the CBOT 10-Year U.S. Treasury Note Futures Contract (Bloomberg ticker: ZN/TY), which is a series of exchange-traded futures contracts with expiry dates at three month intervals. As defined by the Relevant Exchange, the underlying unit of each contract is a single notional note issued by the U.S. Treasury that has a face value at maturity of $100,000, and Deliverable Grades of instruments eligible for settlement include U.S. Treasury notes with a remaining term to maturity of at least six and a half years, but not more than ten years, from the first day of the delivery month, where the invoice price equals the futures settlement price times a conversion factor, plus accrued interest, and the conversion factor is the price of the delivered note ($1 par value) to yield 6% (the “10 Year Note

Futures”);

• the EUREX Euro-Schatz Futures Contract (Bloomberg ticker: FGBS/DU), which is a series of exchange-traded futures contracts, with expiry dates at three month intervals. As defined by the Relevant Exchange, each contract references certain notional debt instruments issued by the Federal Republic of Germany that have (a) a face value at maturity of 100,000 European Union euros, (b) a remaining term on the Delivery Day of not less than one and three quarter years, and not more than two and a quarter years, and (c) has a 6% coupon (the “Schatz Futures”);

• the EUREX Euro-Bund Futures Contract (Bloomberg ticker: FGBL/RX), which is series of exchange-traded futures contracts, with expiry dates at three month intervals. As defined by the Relevant Exchange, each contract references certain notional debt instruments issued by the Federal Republic of Germany that have (a) a face value at maturity of 100,000 European Union euros, (b) a remaining term on the Delivery Day of not less than eight and a half years, and not more than ten and half years, and (c) has a 6% coupon (the “Bund Futures”); and

• the Osaka 10-Year Japanese Government Bond Futures Contract (Bloomberg ticker: JGB/JB), which is a series of exchange-traded futures contracts, with expiry dates at three month intervals. Each contract references a single notional bond issued by the State of Japan that has (a) a face value at maturity of 100,000,000 Japanese yen, (b) a remaining term to maturity of not less than seven years, and not more than eleven years, as of the issued date and delivery date and (c) pays a notional 6% coupon (the “JGB

Futures”).

Equity Index Futures Constituents

The Equity Index Futures Constituents consist of:

• For the period from and including:

• the Index Base Date to but excluding the Roll Day for S&P Futures for September 2021, the CME Standard and Poor’s 500 Stock Price IndexTM Futures Contract (Bloomberg ticker: SP/SP), which is a series of exchange-traded futures contracts, with expiry dates at three month intervals. As defined by the Relevant Exchange, each contract references the Standard and Poor’s 500 Stock Price Index, which provides a notional exposure equal to the product of the level of the Standard and Poor’s 500 Stock Price Index and $250 (the “S&P Standard-Size Futures”);

-18-

• from and including the Roll Day for S&P Futures for September 2021, the CME Standard and Poor’s 500 Stock Price IndexTM E-mini Futures Contract (Code: ES/ES), which is a series of exchange-traded futures contracts, with expiry dates at three month intervals. As defined by the Relevant Exchange each contract references the Standard and Poor’s 500 Stock Price Index, which provides a notional exposure equal to the product of the level of the Standard and Poor’s 500 Stock Price Index and USD50 (the “S&P Mini Futures”, and, together with the S&P Standard-Size Futures, the “S&P Futures”);

• the EUREX DAX® Index Futures Contract (Bloomberg ticker: FDAX/DX), which is a series of exchange-traded futures contracts, with expiry dates at three month intervals. As defined by the Relevant Exchange, each contract references the Deutscher Aktien Index which provides a notional exposure equal to the product of the level of the DAX Index and 25 European Union euros (the “DAX Futures”); and

• the Osaka Nikkei 225 Index Futures Contract (Bloomberg ticker: NK/NK), which is a series of exchange-traded futures contracts, with expiry dates at three month intervals. As defined by the Relevant Exchange, each contract references the Nikkei Stock Average (Nikkei 225 Index), which provides a notional exposure equal to the product of the level of the Nikkei 225 Index and 1,000 Japanese yen (the “Nikkei Futures”).

Non-Securities-based Constituents

The Index references the following Non-Securities-based Constituents:

• the S&P GSCITM Agriculture Excess Return Index (the “GSCI AG Index”), with the understanding that:

• in the absence of an Agricultural Commodities Postponement Event, the Index level will be calculated by reference to the level of the S&P GSCITM Agriculture Excess Return Index that is published daily on Bloomberg Ticker SPGCAGP Index <go>, and

• in the case of an Agricultural Commodities Postponement Resolution Period, the Index level in respect of the applicable Agricultural Commodities Postponement Resolution Day will be calculated by reference to the settlement level of the S&P GSCITM Agriculture Excess Return Index that is published periodically on Bloomberg Ticker SPGSAGSP Index <go> (the “Agricultural Commodities Settlement Index”);

• the S&P GSCITM Precious Metals OC Excess Return Index is published daily on Bloomberg Ticker SPGCPMP Index <go> (the “GSCI PM Index”);

• the S&P GSCITM Industrial Metals Excess Return Index is published daily on Bloomberg Ticker SPGCINP Index <go> (the “GSCI IM Index”); and

• the S&P GSCITM Energy Excess Return Index is published daily on Bloomberg Ticker SPGCENP Index <go> (the “GSCI EN Index”).

-19-

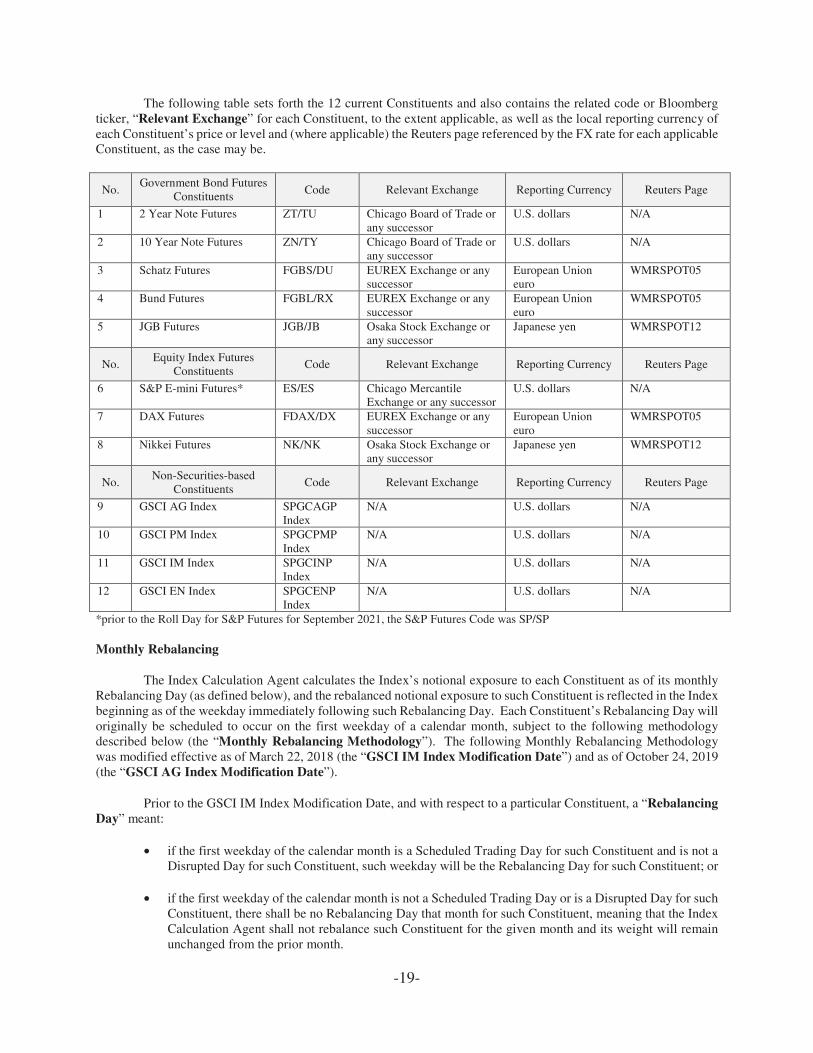

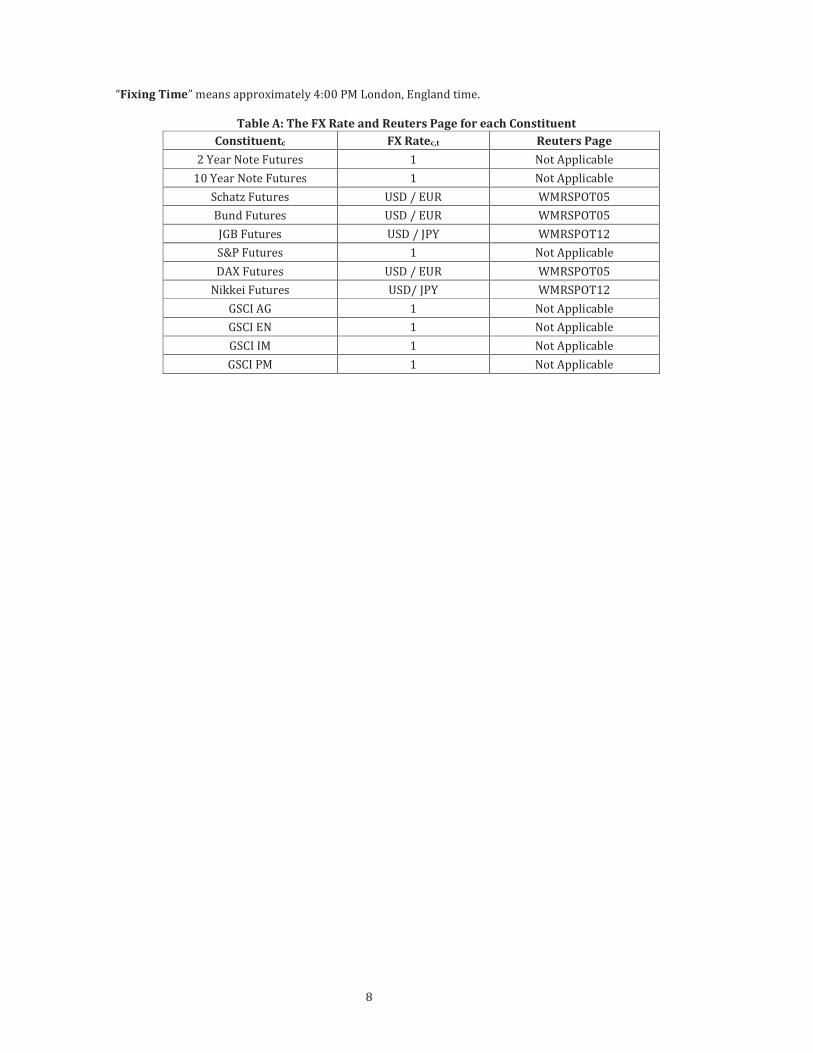

The following table sets forth the 12 current Constituents and also contains the related code or Bloomberg ticker, “Relevant Exchange” for each Constituent, to the extent applicable, as well as the local reporting currency of each Constituent’s price or level and (where applicable) the Reuters page referenced by the FX rate for each applicable Constituent, as the case may be.

No. Government Bond Futures

Constituents Code Relevant Exchange Reporting Currency Reuters Page

1 2 Year Note Futures ZT/TU Chicago Board of Trade or any successor

U.S. dollars N/A

2 10 Year Note Futures ZN/TY Chicago Board of Trade or any successor

U.S. dollars N/A

3 Schatz Futures FGBS/DU EUREX Exchange or any successor

European Union euro

WMRSPOT05

4 Bund Futures FGBL/RX EUREX Exchange or any successor

European Union euro

WMRSPOT05

5 JGB Futures JGB/JB Osaka Stock Exchange or any successor

Japanese yen WMRSPOT12

No. Equity Index Futures

Constituents Code Relevant Exchange Reporting Currency Reuters Page

6 S&P E-mini Futures* ES/ES Chicago Mercantile Exchange or any successor

U.S. dollars N/A

7 DAX Futures FDAX/DX EUREX Exchange or any successor

European Union euro

WMRSPOT05

8 Nikkei Futures NK/NK Osaka Stock Exchange or any successor

Japanese yen WMRSPOT12

No. Non-Securities-based

Constituents Code Relevant Exchange Reporting Currency Reuters Page

9 GSCI AG Index SPGCAGP Index

N/A U.S. dollars N/A

10 GSCI PM Index SPGCPMP Index

N/A U.S. dollars N/A

11 GSCI IM Index SPGCINP Index

N/A U.S. dollars N/A

12 GSCI EN Index SPGCENP Index

N/A U.S. dollars N/A

*prior to the Roll Day for S&P Futures for September 2021, the S&P Futures Code was SP/SP

Monthly Rebalancing

The Index Calculation Agent calculates the Index’s notional exposure to each Constituent as of its monthly Rebalancing Day (as defined below), and the rebalanced notional exposure to such Constituent is reflected in the Index beginning as of the weekday immediately following such Rebalancing Day. Each Constituent’s Rebalancing Day will originally be scheduled to occur on the first weekday of a calendar month, subject to the following methodology described below (the “Monthly Rebalancing Methodology”). The following Monthly Rebalancing Methodology was modified effective as of March 22, 2018 (the “GSCI IM Index Modification Date”) and as of October 24, 2019 (the “GSCI AG Index Modification Date”).

Prior to the GSCI IM Index Modification Date, and with respect to a particular Constituent, a “Rebalancing

Day” meant:

• if the first weekday of the calendar month is a Scheduled Trading Day for such Constituent and is not a Disrupted Day for such Constituent, such weekday will be the Rebalancing Day for such Constituent; or

• if the first weekday of the calendar month is not a Scheduled Trading Day or is a Disrupted Day for such Constituent, there shall be no Rebalancing Day that month for such Constituent, meaning that the Index Calculation Agent shall not rebalance such Constituent for the given month and its weight will remain unchanged from the prior month.

-20-

On the GSCI IM Index Modification Date, the Monthly Rebalancing Methodology was changed solely with respect to the GSCI IM Index so that if (x) the first weekday of the calendar month is not a day where the relevant commodity exchange is scheduled to be open for trading for each individual commodity futures contract referenced by the GSCI IM Index, and (y) either (1) the immediately preceding weekday is not a day where the relevant commodity exchange is scheduled to be open for trading for each individual commodity futures contract referenced by the GSCI IM Index or (2) the immediately preceding weekday is a day where the relevant commodity exchange is scheduled to be open for trading for each individual commodity futures contract referenced by the GSCI IM Index, but is a day on which a Market Disruption Event did occur or exist for any of the individual commodity futures contracts referenced by the GSCI IM Index, then:

• if the second weekday of such calendar month is a Scheduled Trading Day for such Constituent and is not a Disrupted Day for such Constituent, such weekday will be the Rebalancing Day for such Constituent; or

• if the second weekday of such calendar month is not a Scheduled Trading Day or is a Disrupted Day for such Constituent, there shall be no Rebalancing Day that month for such Constituent, meaning that the Index Calculation Agent shall not rebalance such Constituent for the given month and its weight will remain unchanged from the prior month.

On the GSCI AG Index Modification Date, the Monthly Rebalancing Methodology was changed solely with respect to the GSCI AG Index so that:

• if the first weekday of any calendar month (i) is not a day where the relevant commodity exchange is scheduled to be open for trading for each individual commodity futures contract referenced by the GSCI AG Index, (ii) is immediately following a weekday that falls within an Agricultural Commodities Postponement Period or (iii) is or immediately follows a weekday that is an Agricultural Commodities Postponement Resolution Day, there shall be no Rebalancing Day that month for such Constituent, meaning that the Index Calculation Agent shall not rebalance such Constituent for the given month and its weight will remain unchanged from the prior month; or

• if the first weekday of any calendar month is (i) a Scheduled Trading Day for such Constituent, (ii) a day where the relevant commodity exchange is scheduled to be open for trading for each individual commodity futures contract referenced by the GSCI AG Index and (iii) the Index Calculation Agent determines in its sole discretion (a “Designated Agricultural Commodities Postponement

Determination”) that such weekday is a Disrupted Day for such Constituent solely due to the occurrence or continuation of an Agricultural Commodities Postponement Event for one or more of the individual commodity futures contracts referenced by the GSCI AG Index, then such weekday shall treated as a Rebalancing Day for such Constituent but the rebalancing of such Constituent shall be effected on a delayed basis and the calculation of returns and the Index Level shall be modified as described under “—Calculation of USD Returns”.

“Agricultural Commodities Postponement Event” means, in respect of the GSCI AG Index and a particular weekday that is either (i) a scheduled Rebalancing Day or (ii) an Exposure Flattening Change Day (as defined below), that (a) a Market Disruption Event has occurred or is continuing in respect of such Constituent and that (b) as a result of the occurrence or continuation of such Market Disruption Event, the Agricultural Constituent Settlement Price for such weekday is either (i) not published or otherwise made available by or on behalf of the Constituent Sponsor to the Index Calculation Agent on such weekday or (ii) published or otherwise made available by or on behalf of the Constituent Sponsor to the Index Calculation Agent on that weekday, but is not equal to the Closing Price for such Constituent for that weekday. For further information on settlement pricing as used in the GSCI AG Index, see “Background on the S&P GSCI Indices—Calculation of the S&P GSCI Indices—Settlement Pricing.”

“Agricultural Commodities Postponement Resolution Period” means, in the case of the GSCI AG Index and a weekday in respect of which the Index Calculation Agent has made a Designated Agricultural Commodities Postponement Determination, the period from and including the weekday on which such Designated Agricultural

-21-

Commodities Postponement Determination has been made to and excluding the applicable Agricultural Commodities Postponement Resolution Day.

“Agricultural Commodities Postponement Resolution Day” means the first weekday, following the weekday in respect of which the Index Calculation Agent has made a Designated Agricultural Commodities Postponement Determination, for which the Agricultural Constituent Settlement Price for such first following weekday is published or otherwise made available by or on behalf of the Constituent Sponsor to the Index Calculation Agent and is equal to the Closing Price for such Constituent for that weekday.

“Exposure Flattening Change Day” means a weekday that is also a Scheduled Trading Day with respect to the GSCI AG Index and where either such weekday or the immediately preceding weekday is in an Exposure Flattening Period with respect to the GSCI AG Index when the other weekday is not in an Exposure Flattening Period.