strategic planning in smaller enterprises – new empirical findings

TRANSCRIPT

MRN29,6

334

Management Research NewsVol. 29 No. 6, 2006pp. 334-344# Emerald Group Publishing Limited0140-9174DOI 10.1108/01409170610683851

Strategic planning in smallerenterprises – new empirical

findingsSascha Kraus

Department of Entrepreneurship, University of Oldenburg,Oldenburg, Germany

Rainer Harms and Erich J. SchwarzDepartment of Innovation Management and Entrepreneurship,

University of Klagenfurt, Klagenfurt, Austria

Abstract

Purpose – To analyze the performance implications of essential elements of strategic planning (timespan, formalization, frequency of control, and use of planning instruments) in smaller enterprises in asimultaneous way.Design/methodology/approach – The main methods being used for this article were a thoroughreview of literature for the development of hypotheses and a logistical regression analysis for theempirical evaluation. The study is based on a representative sample of small Austrian enterprises(n = 290).Findings – Planning formalization has a positive and highly significant impact on the probability ofbelonging to the group of growth firms, whereas other aspects of strategic planning (time horizon,strategic instruments, and control) did not contribute to performance.Research limitations/implications – Employee growth has been used as an indicator for firmperformance. Other indicators (e.g. sales growth, profitability, and subjective evaluation of theentrepreneur) might be used to draw a more detailed picture. Additionally, dichotomizing thedependent variable has some weaknesses. Furthermore, only a limited number of industry categorieshave been controlled for.Practical implications – Practitioners might want to emphasize formal strategic planning in orderto enhance the probability of performance. Also, they might want to regard the business plan as amanagement and learning tool rather than as a pure means to generate funding.Originality/value – This paper is the first to analyze different dimensions of strategic planning insmall firms simultaneously. Additionally, it is one of only very few studies outside of the Anglo-Americanrealm, which might be a help especially for European SMEs (small and medium-sized enterprises).

Keywords Strategic planning, Small to medium-sized enterprises, Business planning,Business performance

Paper type Research paper

IntroductionDue to the great importance of small and medium-sized enterprises, which contribute66 per cent to the total employment and 55 per cent of total revenues of the privatesector in the European Union (Bauer, 2002), it is of particular interest to identify factorswhich contribute to the performance of these firms. Strategic planning might be one ofthese factors.

Strategic planning consists of planning processes that are undertaken in firms todevelop strategies that might contribute to performance (Tapinos et al., 2005). Keyaspects of strategic planning are a long time horizon, formality, the use of planninginstruments, and frequent control of plans. Strategic planning can contribute toperformance by generating relevant information, by creating a better understanding ofthe important environment, and by reducing uncertainty (Hodgetts and Kuratko, 2001).

The current issue and full text archive of this journal is available atwww.emeraldinsight.com/0140-9174.htm

Strategicplanning

335

While the analysis of the performance impact of strategic planning is largelyconfirmed in the context of larger firms (Bracker et al., 1988; Lyles et al., 1993; Rue andIbrahim, 1998; Schwenk and Shrader, 1993), its relationship in the context of smallerenterprises has not been given much attention in existing research. While there is someevidence in support of a positive relationship between strategic planning andperformance in smaller enterprises, other studies find no relationship or even anegative relationship. A possible reason for these inconclusive findings may be thatprevious studies used differing definitions of strategic planning or tested only one ofthe dimensions of strategic planning.

In order to draw a differentiated picture of the performance impact of strategicplanning, we test the performance implications of a quadrinominal concept of strategicplanning that contains the elements time horizon, degree of formalization, use ofstrategic instruments, and degree of control in a single analysis. The empiricalanalysis will be carried out in a sample of 290 small enterprises fromAustria.

Literature reviewA literature analysis on the subject of the performance implications of strategicplanning in smaller enterprises was undertaken in order to gain insight into therelationship between strategic planning and performance in smaller enterprises. Thisliterature analysis is based on a review of empirical studies on that subject and coversthe last 25 years. The analysis applied a keyword search in leading entrepreneurshipand strategy journals and in databases. Even though the literature analysis wasextensive, only 24 empirical studies were discovered. Considering the long period oftime that was covered, this seems to be a rather low number. This indicates thatempirical research on strategic planning in small firms is still in its infancy.

The literature analysis revealed that smaller enterprises do in fact plan, and mostsmall enterprises even plan in a formal way and use rather large time spans. Forexample, in a study by Naffziger and Kuratko (1991), 83 per cent of the smallerenterprises managers claimed that they plan in a formal way. In another study,70 per cent of the smaller enterprises managers reported using time spans of one tothree years, and 92 per cent declared to even plan strategically, i.e. for more than threeyears. However, planning in smaller enterprises is rarely supported by planninginstruments, since most of the respondents reported that they planned intuitively, anddid not use planning instruments (Stonehouse and Pemberton, 2002).

The literature analysis tends to support a positive relationship between strategicplanning and performance. Seventy nine per cent of the studies in our analysisidentified a positive relationship, which tends to suggest that there is broad support forthe performance impact of strategic planning. Evidence in favor of this relationshipwas discovered in studies of small enterprises from different industries and differentregions (Bracker et al., 1988; Bracker and Pearson, 1986; Griggs, 2002; Masurel andSmit, 2000; Orpen, 1985), and using different indicators for performance such assurvival (Perry, 2001), turnover growth, employment growth, and reputation(Ackelsberg and Arlow, 1985; Sexton and Van Auken, 1985; Vesper, 1980).

However, there were also mixed results. One study in the context of smallerenterprises revealed that the direction of the relationship between strategic planningand performance depends on the industry (Shrader et al., 1989), and several otherstudies did not find a relationship at all (French et al., 2004; Gable and Topol, 1987;Gibson and Cassar, 2005; Robinson, 1983; Sexton and Van Auken, 1985).

MRN29,6

336

A possible reason for these diverging findings could be that diverging definitions ofstrategic planning were used, or that the analyses focused on different aspects ofstrategic planning. For example, most of the studies analyzed only one aspectof strategic planning, namely formalization (Lyles et al., 1993), whereas in other studies,the conceptualizations and operationalizations of strategic planning were not laid open.

Development of hypothesesSince strategic planning in general seemed to be positively related to performance, wewere interested in discovering which precise aspects of strategic planning relate toperformance. Strategic planning is commonly characterized by three criteria:

(1) a long-term orientation,

(2) strategies inwritten form, and

(3) evaluation and control (Rue and Ibrahim, 1998).

Additionally, we assume that the use of strategic planning instruments (or tools) is animportant element for strategic planning.

The relationship between the time horizon of strategic planning and performanceLong-term goals help to identify resource requirements at an early stage. The firm isthus able to acquire resources in advance and more efficiently. Moreover, a firm thataligns sourcing with long-term goals avoids purchases of unnecessary resources. Inaddition to that, long-term goals can motivate both entrepreneurs and employees(Collins and Porras, 2005). There is empirical evidence in support of a positiverelationship between long-term formal planning and performance (Smith, 1998),indicating that the time horizon of plans for high performers is longer that of plans forlow performers (Orpen, 1985). Thus, it can be assumed that the length of the timehorizon of plans is positively related to firm performance.

H1. The longer the time horizon of strategic planning, the more successful is thesmall enterprise.

The relationship between formalization of strategic planning and firm performanceFormalization indicates the degree to which strategic plans exist in written form. Theprocess of creating formalized plans forces management to systematically deal withthe goals and strategies of the firm. Management attains larger and more systematicknowledge of the characteristics of its environment and of alternative strategies.Previous empirical evidence supports the view that formalized planning increasesperformance. In one study, smaller enterprises were assigned to the groups of formaland non-formal planners. An investigation of these groups revealed that formalplanners grew twice as fast as non-formal planners (Lyles et al., 1993).

H2. The higher the degree of planning formalization, the more successful is thesmall enterprise.

The relationship between the frequency of controls and firm performanceControl is the process of comparing current developments with previously anticipateddevelopments. Frequent controls allow for a timely and thus cost-efficient adaptationof plans and strategies in case of a deviation between current and anticipated data.Also, controls can initiate a learning process (Ramanujam and Venkatraman, 1987).

Strategicplanning

337

In addition to that, controls can motivate employees when e.g. achieved goals result ingratification or awards (Collins and Porras, 2005). Empirical studies on strategicplanning in small firms have paid little attention to the performance impact of controlaspects of strategic planning. An exception is a recent study that shows that thecontrol of plans and of goal achievement contributes significantly to firm performance(Wijewardena et al., 2004).

H3. The more frequent the control of strategic planning, the more successful is thesmall enterprise.

The relationship between the use of planning instruments and firm performancePlanning instruments are tools which assist long-term planning by systematicallystructuring goals and means for goal attainment. Thereby, planning instruments helpto increase planning efficiency and effectiveness. Instruments for strategic planningthat are suitable for use in smaller enterprises are e.g. analysis of financial data,environmental analyses, or SWOT-analysis. Previous empirical evidence from Rue andIbrahim (1998) supports a positive and significant relationship between planningsophistication in terms of the use of planning instruments and firm performance.Based on the conceptual arguments and on the previous empirical support, we proposethe following hypothesis:

H4. The more planning instruments are used for strategic planning, the moresuccessful is the small enterprise.

MethodsSampleThe analysis is based on data of small enterprises from Austria. We follow thedefinition of small firms of the European Commission (2003), according to which smallfirms are defined as having a staff of fewer than 50 persons and sales of under e10 mn.The population of 19,477 firms is based on all firms that were founded in Austria in1999. Out of this database (which has been provided by the Austrian Chamber ofCommerce), a random sample of 1,497 firms was drawn in 2002. Out of these firms, 634structured telephone interviews (42.4 per cent) were conducted with the enterprisefounder or CEO (key informant approach). The other firms (57.7 per cent) could not bereached, refused to be interviewed, or closed between 1999 and 2002. Excluding take-overs, 552 firms were classified as independent start-ups. In order to analyze theperformance of the firms, a second cross-section was taken in 2005. In total, 398independent start-ups were still in business. Because of listwise deletion of cases withmissing data, the number of complete cases that were used for analysis was reduced ton = 290. However, the missing cases did not differ significantly from those that wereincluded in the analysis (based on industry affiliation and growth). Descriptivestatistics illustrate the characteristics of the sample. The firms in our sample are rathersmall, with over 90 per cent having less than ten employees. The average annual sales(mean) were at e612,000. Pertaining to the industry composition, 54 per cent of thefirms belong operate in services, 24 per cent in trade, 16 per cent in manufacturing,while 6 per cent could not be assigned to an industry category.

OperationalizationWe used employment growth as an indicator for performance (dependent variable).Employment growth was chosen for a three reasons. First, financial data are reported

MRN29,6

338

to be unreliable in the context of small and young firms. Second, growth is animportant goal for small and young firms, and third, employment growth is a morestable indicator than turnover growth, since firms only add employees when a higherlevel of business volume is likely to be stabilized in the future (Delmar, 1997). Moreprecisely, we measured employment growth as the change in the number of employeesincluding founding person(s) in full-time employment equivalents between 1999 and2005. Because the distribution of employment growth differed significantly from thenormal distribution, and a high share of firms reported to have not grown, the variablewas dichotomized in group 0 (decline or no growth) and group 1 (positive growth).

As independent variables, we used the time horizon, the degree of formalization, thedegree of control, and the use of strategic planning instruments. The respondents wereasked to provide information about the average time horizon of their strategic plans(years, metric; median of group 0: 1.36 years/median of group 1: 1.88 years). To assessthe degree of formalization, a summed index was calculated. This index is based on thedegree of formalization (written planning, informal planning, or no planning) in fivedifferent functional areas (technology/innovation, production, marketing, humanresource management, finance) and in pre-start-up planning. This index ranged fromzero to 12, with higher values indicating a higher degree of formal planning (ordinal;median of group 0: 2.95/median of group 1: 5.18). The degree of control of plans wasassessed on a five-point scale with higher values indicating more frequent control(ordinal; median of group 0: 2.20/median of group 1: 2.51). The use of strategicinstruments was measured by a summed index that counts the number of strategicplanning instruments (SWOT analysis, competitor analysis, analysis of theenvironment, analysis of financial ratios) and an open category, in which instrumentssuch as portfolio analysis or scenario analysis were mentioned. This index rangedfrom zero to five, including one open answer category (ordinal; median of group0: 0.30/median of group 1: 0.61).

We included firm size as a control variable because it can be assumed that firms thatstart with a higher initial size might not grow as fast (in the number of employees) asfirms that start with no or few employees. Industry was coded in three dummyvariables. The reference category (all dummies being zero) was retail, the first dummybeing one indicating non-classified industries, the second dummy being one indicatingmanufacturing, and the third dummy being one indicating services.

Method of analysisBecause the distribution of the dependent variable differed significantly from thenormal distribution, and because of the high number of firms with no growth, we choseto use a binary hierarchical logistic regression for the analysis. In a first step, weentered the control variables, and in a second step we entered the planning variables.

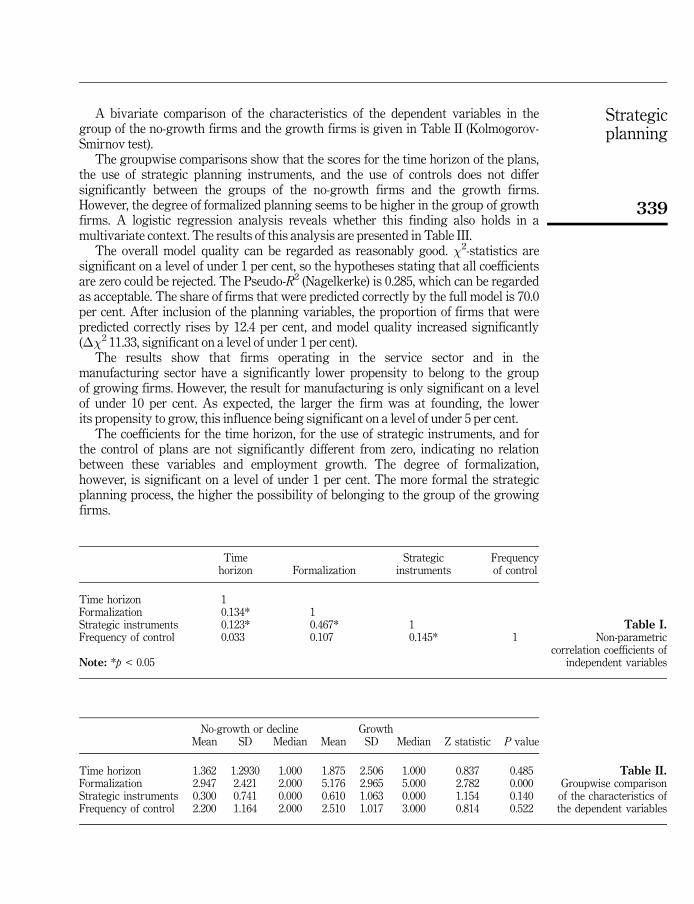

ResultsFirst, we wanted to assess if the aspects of planning were not only conceptuallydistinct, but empirically distinct as well. The results of a non-parametric correlationanalysis are shown in Table I.

The correlation coefficients between the aspects of strategic planning can beclassified as small. The correlation between the degree of formalization and the use ofinstruments for strategic planning can be regarded as moderate (Cohen et al., 2003).This level of first-order correlations shows that the different aspects of strategicplanning might also be empirically distinct.

Strategicplanning

339

A bivariate comparison of the characteristics of the dependent variables in thegroup of the no-growth firms and the growth firms is given in Table II (Kolmogorov-Smirnov test).

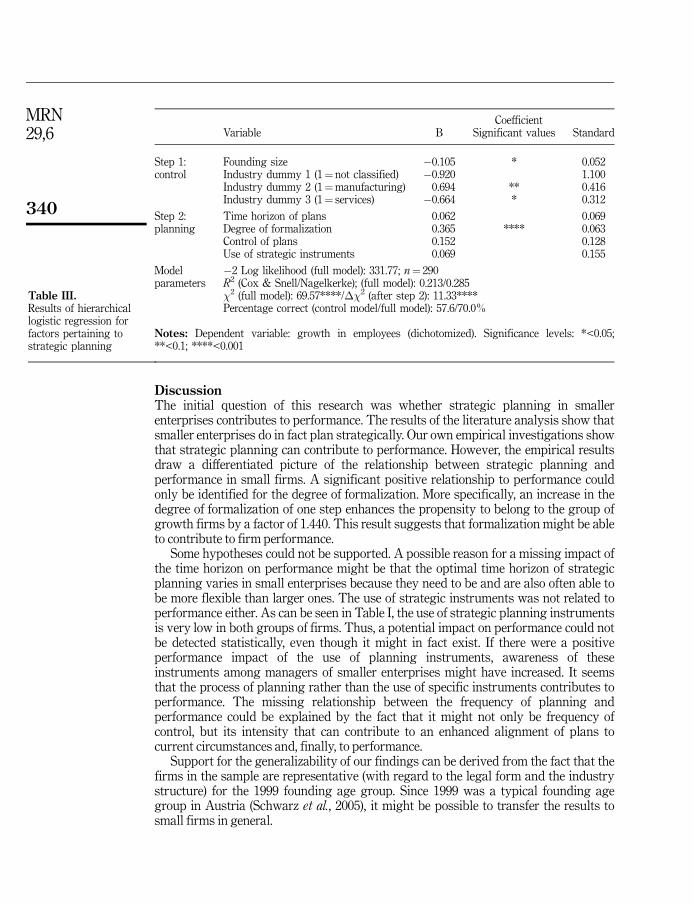

The groupwise comparisons show that the scores for the time horizon of the plans,the use of strategic planning instruments, and the use of controls does not differsignificantly between the groups of the no-growth firms and the growth firms.However, the degree of formalized planning seems to be higher in the group of growthfirms. A logistic regression analysis reveals whether this finding also holds in amultivariate context. The results of this analysis are presented in Table III.

The overall model quality can be regarded as reasonably good. �2-statistics aresignificant on a level of under 1 per cent, so the hypotheses stating that all coefficientsare zero could be rejected. The Pseudo-R2 (Nagelkerke) is 0.285, which can be regardedas acceptable. The share of firms that were predicted correctly by the full model is 70.0per cent. After inclusion of the planning variables, the proportion of firms that werepredicted correctly rises by 12.4 per cent, and model quality increased significantly(��2 11.33, significant on a level of under 1 per cent).

The results show that firms operating in the service sector and in themanufacturing sector have a significantly lower propensity to belong to the groupof growing firms. However, the result for manufacturing is only significant on a levelof under 10 per cent. As expected, the larger the firm was at founding, the lowerits propensity to grow, this influence being significant on a level of under 5 per cent.

The coefficients for the time horizon, for the use of strategic instruments, and forthe control of plans are not significantly different from zero, indicating no relationbetween these variables and employment growth. The degree of formalization,however, is significant on a level of under 1 per cent. The more formal the strategicplanning process, the higher the possibility of belonging to the group of the growingfirms.

Table I.Non-parametric

correlation coefficients ofindependent variables

Timehorizon Formalization

Strategicinstruments

Frequencyof control

Time horizon 1Formalization 0.134* 1Strategic instruments 0.123* 0.467* 1Frequency of control 0.033 0.107 0.145* 1

Note: *p < 0.05

Table II.Groupwise comparisonof the characteristics ofthe dependent variables

No-growth or decline GrowthZ statistic P valueMean SD Median Mean SD Median

Time horizon 1.362 1.2930 1.000 1.875 2.506 1.000 0.837 0.485Formalization 2.947 2.421 2.000 5.176 2.965 5.000 2.782 0.000Strategic instruments 0.300 0.741 0.000 0.610 1.063 0.000 1.154 0.140Frequency of control 2.200 1.164 2.000 2.510 1.017 3.000 0.814 0.522

MRN29,6

340

DiscussionThe initial question of this research was whether strategic planning in smallerenterprises contributes to performance. The results of the literature analysis show thatsmaller enterprises do in fact plan strategically. Our own empirical investigations showthat strategic planning can contribute to performance. However, the empirical resultsdraw a differentiated picture of the relationship between strategic planning andperformance in small firms. A significant positive relationship to performance couldonly be identified for the degree of formalization. More specifically, an increase in thedegree of formalization of one step enhances the propensity to belong to the group ofgrowth firms by a factor of 1.440. This result suggests that formalization might be ableto contribute to firm performance.

Some hypotheses could not be supported. A possible reason for a missing impact ofthe time horizon on performance might be that the optimal time horizon of strategicplanning varies in small enterprises because they need to be and are also often able tobe more flexible than larger ones. The use of strategic instruments was not related toperformance either. As can be seen in Table I, the use of strategic planning instrumentsis very low in both groups of firms. Thus, a potential impact on performance could notbe detected statistically, even though it might in fact exist. If there were a positiveperformance impact of the use of planning instruments, awareness of theseinstruments among managers of smaller enterprises might have increased. It seemsthat the process of planning rather than the use of specific instruments contributes toperformance. The missing relationship between the frequency of planning andperformance could be explained by the fact that it might not only be frequency ofcontrol, but its intensity that can contribute to an enhanced alignment of plans tocurrent circumstances and, finally, to performance.

Support for the generalizability of our findings can be derived from the fact that thefirms in the sample are representative (with regard to the legal form and the industrystructure) for the 1999 founding age group. Since 1999 was a typical founding agegroup in Austria (Schwarz et al., 2005), it might be possible to transfer the results tosmall firms in general.

Table III.Results of hierarchicallogistic regression forfactors pertaining tostrategic planning

CoefficientVariable B Significant values Standard

Step 1:control

Founding size �0.105 * 0.052Industry dummy 1 (1¼ not classified) �0.920 1.100Industry dummy 2 (1¼manufacturing) 0.694 ** 0.416Industry dummy 3 (1¼ services) �0.664 * 0.312

Step 2:planning

Time horizon of plans 0.062 0.069Degree of formalization 0.365 **** 0.063Control of plans 0.152 0.128Use of strategic instruments 0.069 0.155

Modelparameters

�2 Log likelihood (full model): 331.77; n¼ 290R2 (Cox & Snell/Nagelkerke); (full model): 0.213/0.285�2 (full model): 69.57****/��2 (after step 2): 11.33****Percentage correct (control model/full model): 57.6/70.0%

Notes: Dependent variable: growth in employees (dichotomized). Significance levels: *<0.05;**<0.1; ****<0.001

Strategicplanning

341

However, there are some limitations that have to be taken into account whileinterpreting the results. First, we used employee growth as the sole indicator for firmperformance. Even though we believe that this indicator is most suitable in the contextof small firms, other objective indicators such as sales growth or profitability orsubjective indicators such as the personal satisfaction of the owner with firmperformance might be used to draw a more detailed picture. Second, by dichotomizingthe dependent variable, its variance was reduced, which could obscure the relationshipbetween planning and performance. However, both the distribution of growth and atransformed distribution of growth differed significantly from the normal distribution;we were not able to use ordinary least square regression or treat growth as acontinuous variable. Third, the limited number of industry categories might have beentoo coarse to represent different industry conditions. A more detailed assessment ofindustries or a direct assessment of industry characteristics such as dynamism ormunificence might have been a more control-relevant variable. In future analyses, wewill test if industry characteristics can serve as moderator variables between thedimensions of strategic planning and performance. For example, we will investigatewhether the use of strategic planning instruments (or any other dimension of strategicplanning) can have a stronger relationship with performance under stable marketconditions than those found in average or even dynamic market conditions.

In addition to a future analysis of the nature of the influence of external variables,we will also focus on discovering the mechanics of how strategic planning works insidethe firm. This could lead to a new conceptualization of strategic planning that pertainsespecially to smaller enterprises. Such a definition could be based on ourquadrinominal conceptualization of strategic planning.

ConclusionThe main objective of this study was to analyze the performance impact of variousaspects of strategic planning in small firms. It emerged that a higher degree offormalization is related to a higher degree of performance.

Several implications for practitioners follow from our results. First, practitionersmight want to plan more formally than before. For example, the creation of a businessplan might help the firms to identify risks and opportunities in the marketplace andplan for actions in due time. This might increase the chances of success. Second, sincethe use of planning instruments in small firms is rather low, it might be beneficial toincrease the awareness of these instruments. To do so, issues pertaining to strategicplanning might have to be emphasized in curricula for small business managers, bothin higher and in further education, and not limited to business-related study programs.Also, handbooks for small business managers which focus on strategic planningwithout the use of too many technical terms as well as a hands-on approach cancontribute to this goal. Also, cooperation with universities in the development of real-life business plans can be helpful.

As the results have to be evaluated in the light of the shortcomings of this study, wewould be very cautious to conclude that the time horizon of plans, their control and theuse of strategic instruments should be disregarded when designing a strategicplanning system in smaller enterprises. For example, the control of goal achievementand of planning assumptions is a precondition for re-adjusting plans when unforeseencircumstances emerge.

Nevertheless, we hope to have contributed to the dialogue on the performanceimplications of strategic planning in the context of small firms by evaluating several

MRN29,6

342

aspects of strategic planning simultaneously. Moreover, to the knowledge of theauthors, this study is the first to be based on a largely representative cross-sectoralsample from a whole country in a European context. This is particularly noteworthybecause the use of strategic planning can be subject to cultural influences, so theresults from research in Anglo-American countries might not be able to be transferredin an indiscriminate way. Since we analyzed small firms from Austria, which build thevast majority of firms in the European Union with 93 per cent of all enterprises(Snijders and Van der Horst, 2002), we feel that our results are particularly relevant forthese firms.

To conclude, we emphasize that small enterprises are not little big enterprises, andthus, suggestions for strategic planning that were developed in the context of largefirms might not apply to their smaller counterparts. In the future, specifically tailoredconcepts of strategic planning in smaller enterprises may emerge. We hope to havecontributed to this dialogue.

References

Ackelsberg, R. and Arlow, P. (1985), ‘‘Small businesses do plan and it pays off’’, Long RangePlanning, Vol. 18 No. 5, pp. 61-7.

Bauer, B. (2002), Kleine und mittlere Unternehmen – Ubersicht uber Bedeutung, bereits getroffeneund mogliche weitere Maßnahmen auf EU-Ebene und in Osterreich, Federal Ministry ofFinance, Vienna.

Bracker, J.S., Keats, B.W. and Pearson, J.N. (1988), ‘‘Planning and financial performance amongsmall firms in a growth industry’’, Strategic Management Journal, Vol. 9 No. 6, pp. 591-603.

Bracker, J.S. and Pearson, J.N. (1986), ‘‘Planning and financial performance of small maturefirms’’, Strategic Management Journal, Vol. 7 No. 6, pp. 503-22.

Cohen, J., Cohen, P., West, S.G. and Aiken, L.A. (2003), Applied Multiple Regression/CorrelationAnalysis for the Behavioral Sciences, 3rd ed., Lawrence Erlbaum Associates, Mahwah, NewJersey.

Collins, J.C. and Porras, J.I. (2005), Built to Last: Successful Habits of Visionary Companies,Random House, London.

Delmar, F. (1997), ‘‘Measuring growth: methodological considerations and empirical problems’’, inDonckels, R. and Miettinen, A. (Eds), Entrepreneurship and SME Research: On its Way tothe Next Millennium, Ashgate, Hants, pp. 199-215.

European Commission (2003), ‘‘Commission recommendation of 6 May 2003 concerning thefefinition of micro, small and medium-sized enterprises’’, Official Journal of the EuropeanUnion, Vol. L124/36, pp. 1-6.

French, S.J., Kelly, S.J. and Harrison, J.L. (2004), ‘‘The role of strategic planning in the performanceof small, professional service firms – a research note’’, Journal of ManagementDevelopment, Vol. 23 No. 9, pp. 765-76.

Gable, M. and Topol, M.T. (1987), ‘‘Planning practices of small-scale retailers’’, American Journalof Small Business, Vol. 12 No. 2, pp. 19-32.

Gibson, B. and Cassar, G. (2005), ‘‘Longitudinal analysis of relationships between planning andperformance in small firms’’, Small Business Economics, Vol. 25 No. 3, pp. 207-22.

Griggs, H.E. (2002), ‘‘Strategic planning system characteristics and organisational effectivenessin Australian small-scale firms’’, Irish Journal of Management, Vol. 23 No. 1, pp. 23-53.

Hodgetts, R.M. and Kuratko, D.F. (2001), Effective Small Business Management, Dryden, FortWorth, TX.

Strategicplanning

343

Lyles, M.A., Baird, I.S., Orris, J.B. and Kuratko, D.F. (1993), ‘‘Formalized planning in smallbusiness: increasing strategic choices’’, Journal of Small Business Management, Vol. 31No. 2, pp. 38-50.

Masurel, E. and Smit, H.P. (2000), ‘‘Planning behavior of small firms in Central Vietnam’’, Journalof Small Business Management, Vol. 38 No. 2, pp. 95-102.

Naffziger, D.W. and Kuratko, D.F. (1991), ‘‘An investigation into the prevalence of planning insmall business’’, Journal of Business and Entrepreneurship, Vol. 3 No. 2, pp. 99-110.

Orpen, C. (1985), ‘‘The effects of long-range planning on small business performance: afurther examination’’, Journal of Small Business Management, Vol. 23 No. 1, pp. 16-23.

Perry, S.C. (2001), ‘‘The relationship between written business plans and the failure of smallbusinesses in the US’’, Journal of Small Business Management, Vol. 39 No. 3, pp. 201-8.

Ramanujam, V. and Venkatraman, N. (1987), ‘‘Planning and performance: a new look at an oldquestion’’, Business Horizons, Vol. 30 No. 3, pp. 19-25.

Robinson, R.B. (1983), ‘‘Measures of small firm effectiveness for strategic planning research’’,Journal of Small Business Management, Vol. 21 No. 2, pp. 22-29.

Rue, L.W. and Ibrahim, N.A. (1998), ‘‘The relationship between planning sophistication andperformance in small businesses’’, Journal of Small Business Management, Vol. 36 No. 4,pp. 24-32.

Schwarz, E.J., Ehrmann, T. and Breitenecker, R.J. (2005), ‘‘Erfolgsdeterminanten jungerUnternehmen in Osterreich: eine empirische Untersuchung zumBeschaftigungswachsum’’, Zeitschrift fur Betriebswirtschaft, Vol. 75 No. 11, pp. 1077-98.

Schwenk, C.R. and Shrader, C.B. (1993), ‘‘Effects of formal strategic planning on financialperformance in small firms: a meta-analysis’’, Entrepreneurship: Theory and Practice,Vol. 17 No. 3, pp. 53-64.

Sexton, D.K. and Van Auken, P. (1985), ‘‘A longitudinal study of small business strategicplanning’’, Journal of Small Business Management, Vol. 23 No. 1, pp. 7-15.

Shrader, C.B., Mulford, C.L. and Blackburn, V.L. (1989), ‘‘Strategic and operational planning,uncertainty, and performance in small firms’’, Journal of Small Business Management,Vol. 27 No. 4, pp. 45-60.

Smith, J.A. (1998), ‘‘Strategies for start-ups’’, Long Range Planning, Vol. 31 No. 6, pp. 857-72.

Snijders, J. and Van der Horst, R. (2002),Hauptergebnisse des Beobachtungsnetz der EuropaischenKMU 2002, The European Union’s Publisher, Luxemburg.

Stonehouse, G. and Pemberton, J. (2002), ‘‘Strategic planning in SMEs – some empirical findings’’,Management Decision, Vol. 40 No. 9, pp. 853-61.

Tapinos, E., Dyson, R.G. and Meadows, M. (2005), ‘‘The impact of performance measurement instrategic planning’’, International Journal of Productivity and Performance Management,Vol. 54 No. 5/6, pp. 370-84.

Vesper, K.H. (1980), ‘‘New venture planning’’, Journal of Business Strategy, Vol. 1 No. 2, pp. 73-5.

Wijewardena, H., De Zoysa, A., Fonseka, T. and Perara, B. (2004), ‘‘The impact of planning andcontrol sophistication on performance of small and medium-sized enterprises: evidencefrom Sri Lanka’’, Journal of Small Business Management, Vol. 24 No. 2, pp. 209-17.

About the authorsSascha Kraus is Assistant Professor at the University of Oldenburg, Germany and Lecturer atthe University of Klagenfurt, Austria, where he also received his PhD. He holds severaluniversity degrees in Business Administration and Management from business schools inGermany, The Netherlands, and Australia. Besides this, he has spent three months as a VisitingResearcher at the University of Edinburgh, UK. He is also the founder of a new businessventure in the media branch and member of the board of two German SMEs. His main research

MRN29,6

344

areas are strategic management and entrepreneurship. Sascha Kraus can be contacted at:[email protected]

Rainer Harms is Assistant Professor at the University of Klagenfurt, Austria. He also lectureson Entrepreneurship at the Technical University of Berlin and the University of Dortmund, andBusiness Administration in the Masters course on Management of Protected Areas. He studiedeconomics, politics, and sociology at the University of Munster, Germany, where he also receivedhis PhD in Business Administration in 2003. Since 2002, he has been scientific advisor to theErnst & Young Entrepreneur of the Year contest in Germany. His research interests areentrepreneurship, innovation management, and organization. Currently, he works on theperformance implications of customer integration in the innovation process.

Erich J. Schwarz is University Professor and Chair of the Department of InnovationManagement and Entrepreneurship at the University of Klagenfurt, Austria. He holds auniversity degree in engineering from the Technical University of Leoben, Austria, a PhD inBusiness Engineering from the Technical University of Graz, and a Habilitation (higherdoctorate) degree in Business Administration from the Graz University, Austria. During hisstudies, he was a Fulbright Visiting Research Scholar at the Virginia Polytechnic Institute andState University as well as at the University of Clemson, South Carolina. He is author of severalbooks and articles, and was a visiting professor at universities in Austria, Germany, andSlovenia.

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.