state reg hurdles to utility environmental compliance hanser celebi zhou 4 12

TRANSCRIPT

This article appeared in a journal published by Elsevier. The attachedcopy is furnished to the author for internal non-commercial researchand education use, including for instruction at the authors institution

and sharing with colleagues.

Other uses, including reproduction and distribution, or selling orlicensing copies, or posting to personal, institutional or third party

websites are prohibited.

In most cases authors are permitted to post their version of thearticle (e.g. in Word or Tex form) to their personal website orinstitutional repository. Authors requiring further information

regarding Elsevier’s archiving and manuscript policies areencouraged to visit:

http://www.elsevier.com/copyright

Author's personal copy

State Regulatory Hurdles toUtility EnvironmentalCompliance

The EPA’s current and forthcoming coal generationregulations present enormous challenges for both utilitiesand state regulators because of their scope, the uncertaintyregarding their final form, and the substantial costs theyentail. Utilities need to develop a strategy that iscompliant with environmental regulations, acceptable tostate regulators, and leaves the utility financially sound.

Philip Q Hanser, Metin Celebi and Bin Zhou

I. Introduction

Utility coal plants, i.e.,

non-merchant plants, are facing an

enormous uncertainty about their

future. Low gas prices and the

dispatching of wind generation

have resulted in record low

operating rates for coal plants in

the United States. In addition, the

Environmental Protection

Agency’s pending and future

environmental regulations may

force coal plant owners to choose

between investing hundreds of

millions, if not billions, of dollars

in additional equipment to comply

with these rules or face shutting

down operations completely.

T his new reality has both plant

owners and regulators very

concerned, although for different

reasons. If coal-plant-owning

utilities choose the option of

retaining their coal generation

assets, they need to optimize their

investment decisions and

maintain their asset’s value. If

there is no investment decision for

the utility to retain the asset’s

value, the non-merchant plant

owners will want to recover the

Philip Q Hanser is a Principal with TheBrattle Group with more than 30 years ofexperience in the energy industry. He has

appeared as an expert witness on such matterssuch as transmission pricing, mergers and

acquisitions, market power, retail tariffs,environmental compliance, forecasting, and

demand-side management before the FederalEnergy Regulatory Commission, numerousstate public utility and siting commissions,and Canadian energy boards. He was at the

Electric Power Research Institute beforejoining Brattle and has had several academic

appointments. He served six years on theAmerican Statistical Association’s Advisory

Committee to the Energy InformationAdministration.

Dr. Metin Celebi is a Principal with TheBrattle Group who provides expertise in

electricity markets and analysis ofenvironmental and climate policy. He has

consulted primarily in the areas of electricityspot pricing and market design, and hasexperience in developing and analyzing

climate policies, assessing generation marketpower, LMP modeling, and merger analysis.He has also consulted and published on the

interaction of resource planning andenvironmental/climate policies within the

electric sector, likely impacts of climatepolicies on natural gas demand, and impacts

of environmental policies on coal plantretirements. Dr. Celebi has significant

experience in the estimation of marginal costsand analysis of ratemaking for electric

utilities from the perspective of alternativemethods to allocate costs among functions,

classifications, and customer groups in bothrestructured markets and for vertically

integrated utilities.

Dr. Bin Zhou is a Senior Consultant at TheBrattle Group, and has more than 13 years’

consulting experience in financialinstitutions (banking and insurance), utility

(gas, electric, and pipelines), and energyindustries. He specializes in financial

statement analysis, valuation, and economicanalysis of tax issues. He also has extensive

experience in cost of capital and riskassessment, ratemaking mechanisms, dispute

resolutions, and bankruptcies in the utilityindustry. Dr. Zhou holds a Ph.D. inInternational Finance from Brandeis

University.

April 2012, Vol. 25, Issue 3 1040-6190/$–see front matter # 2012 Elsevier Inc. All rights reserved., http://dx.doi.org/10.1016/j.tej.2012.03.009 7

Author's personal copy

undepreciated value of the asset(s)

and have assured recovery for the

costs of any substitute resources

through rates. For rate-regulated

utilities, either path requires

achieving approval for their

compliance strategy investments.

And that approval by regulators

will be focused on the financing

and rate impacts of utilities’

compliance strategies.

A n integrated utility facing

such decisions must take a

comprehensive look at its

compliance strategy and the state

regulatory hurdles it faces in

achieving that strategy. The

strategy must look beyond merely

what looks attractive for

maintaining financial value, and

take into account the commission’s

reception. The differences in

market outlook, risk tolerances, or

regional economic priorities

between the utility and the

commission must be accounted

for. If the utility is to pursue a path

that it believes may be at odds with

the commission’s philosophy in

such matters, it will need to

develop facts and arguments to

make its case. Even discerning the

commission’s viewpoint may be

difficult. There is no simple

solution, but there are some

observations that may be useful to

in acquiring regulatory approval

and maintaining the financial

health of the utility.

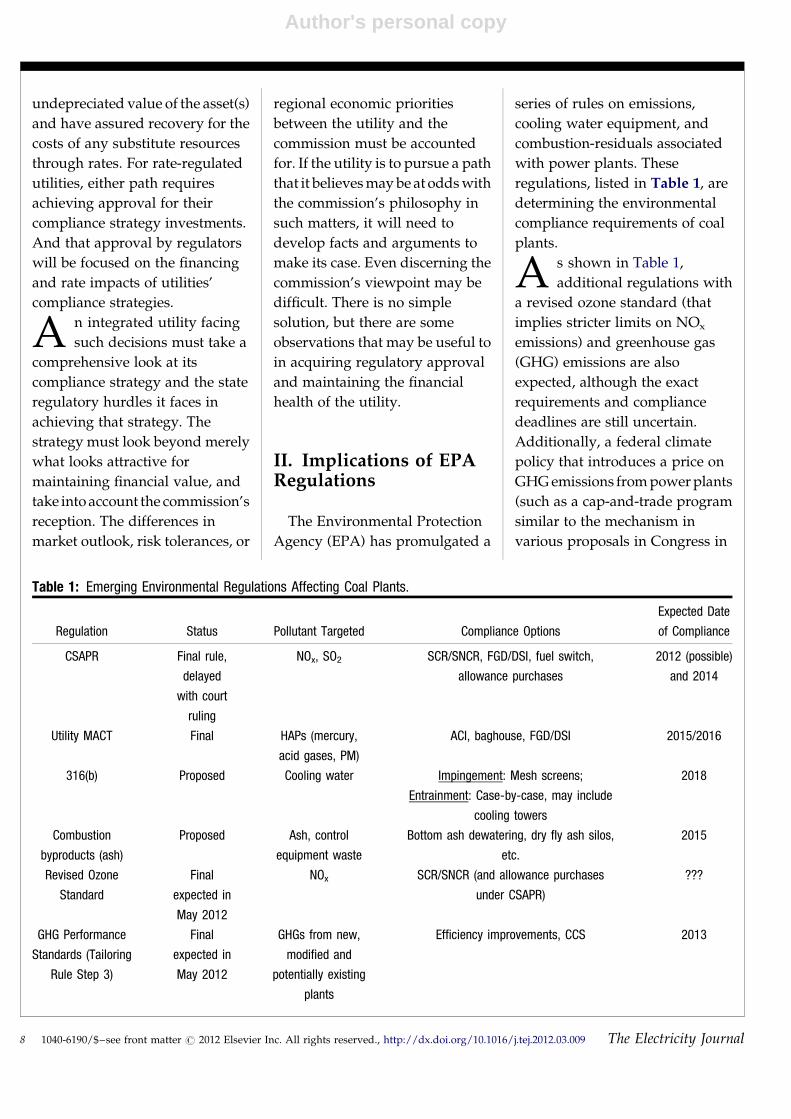

II. Implications of EPARegulations

The Environmental Protection

Agency (EPA) has promulgated a

series of rules on emissions,

cooling water equipment, and

combustion-residuals associated

with power plants. These

regulations, listed in Table 1, are

determining the environmental

compliance requirements of coal

plants.

A s shown in Table 1,

additional regulations with

a revised ozone standard (that

implies stricter limits on NOx

emissions) and greenhouse gas

(GHG) emissions are also

expected, although the exact

requirements and compliance

deadlines are still uncertain.

Additionally, a federal climate

policy that introduces a price on

GHG emissions from power plants

(such as a cap-and-trade program

similar to the mechanism in

various proposals in Congress in

Table 1: Emerging Environmental Regulations Affecting Coal Plants.

Regulation Status Pollutant Targeted Compliance Options

Expected Date

of Compliance

CSAPR Final rule,

delayed

with court

ruling

NOx, SO2 SCR/SNCR, FGD/DSI, fuel switch,

allowance purchases

2012 (possible)

and 2014

Utility MACT Final HAPs (mercury,

acid gases, PM)

ACI, baghouse, FGD/DSI 2015/2016

316(b) Proposed Cooling water Impingement: Mesh screens;

Entrainment: Case-by-case, may include

cooling towers

2018

Combustion

byproducts (ash)

Proposed Ash, control

equipment waste

Bottom ash dewatering, dry fly ash silos,

etc.

2015

Revised Ozone

Standard

Final

expected in

May 2012

NOx SCR/SNCR (and allowance purchases

under CSAPR)

???

GHG Performance

Standards (Tailoring

Rule Step 3)

Final

expected in

May 2012

GHGs from new,

modified and

potentially existing

plants

Efficiency improvements, CCS 2013

8 1040-6190/$–see front matter # 2012 Elsevier Inc. All rights reserved., http://dx.doi.org/10.1016/j.tej.2012.03.009 The Electricity Journal

Author's personal copy

2008 and 2009) may be enacted in

the future. Although pricing GHG

emissions is not likely in the next

few years, it could plausibly occur

well within the lifespan of the

investment decisions utilities must

make soon. Implementation of a

GHG price in the future would

reduce the profit margins and

capacity factors for most of the

coal units, and is a significant

risk factor to consider in the

upcoming decisions for coal units

to retire or retrofit with control

equipment.

T here are a number of

difficulties that utilities face

in regard to these regulations.

First is the sheer uncertainty

about the regulations and their

final implementation. The

Economist1 reports that Ralph

Izzo, president of Public Service

Electric and Gas’s (PSE&G)

Electric, Gas and Energy Services

division, said that PSE&G had lost

millions of dollars on past natural

gas power plant investments

because the final version of a set of

prior EPA regulations were more

lenient than anticipated.

Second, the timing of the

implementation of these

regulations is separated by years.

Some of these rules are nearly

immediate while others are six or

eight years away, not taking into

account any potential appeals

through the judicial system. The

recent experience with the Cross-

State Air Pollution Rule (CSAPR)

is an example of a regulation that

was delayed due to an appeal and

whose final version departed, for

some states, significantly from its

initial version. A court injunction

halted its implementation mere

days before it was to start.2 In

addition, the rules were amended

and some states that were

included in the initial version of

the rule became exempt.

Third, the compliance

technologies vary significantly in

terms of the relative balance

between capital costs and

operating expenses. For example,

in dealing with SO2, a wet flue gas

desulfurization (wet FGD) is more

than an order of magnitude more

expensive than dry sorbent

injection (DSI) equipment in terms

of capital costs, but a wet FGD’s

variable operations and

maintenance (O&M) expenses are

approximately one-fourth those of

DSI.3

Fourth, the value of sustaining

the operation of these coal plants

and, thus, the value of investments

to comply with the regulations,

varies enormously depending on

the state of power markets.

Anyone making investments in

coal plants will simultaneously

note the recent trend of almost

shockingly low natural gas prices.

Those prices have been low

enough in some regions of the

country that efficient combined-

cycle natural gas plants have been

dispatched ahead of coal-fired

generation. In addition, in parts of

the Midwest,4 wind resources

(which primarily operate during

the night) are forcing changes in

coal plant strategies to guarantee

that their plants will be committed

for dispatch because they cannot

compete successfully against wind

in off-peak time periods.

III. Three StrategicConsiderations

Given these legislative,

regulatory, technological, and

financial complexities related to

the compliance with EPA

regulations, we outline below a

three-step process for utilities and

regulators to evaluate their

options and strategies.

Step One: The Utility’s Assessmentof Its Compliance Options

The utility must first assess

compliance strategies without

consideration of its regulatory

strategy. An initial step is to decide

on the scope of its compliance

strategy. For example, regardless

of the compliance strategy, was the

utility considering the possibility

of retiring the plant affected by the

EPA regulations in a time frame

that is shorter than that of the

longer-term rules promulgation?

If it was not, then it will need to

take a longer-term outlook across

the range of rules. Any assessment

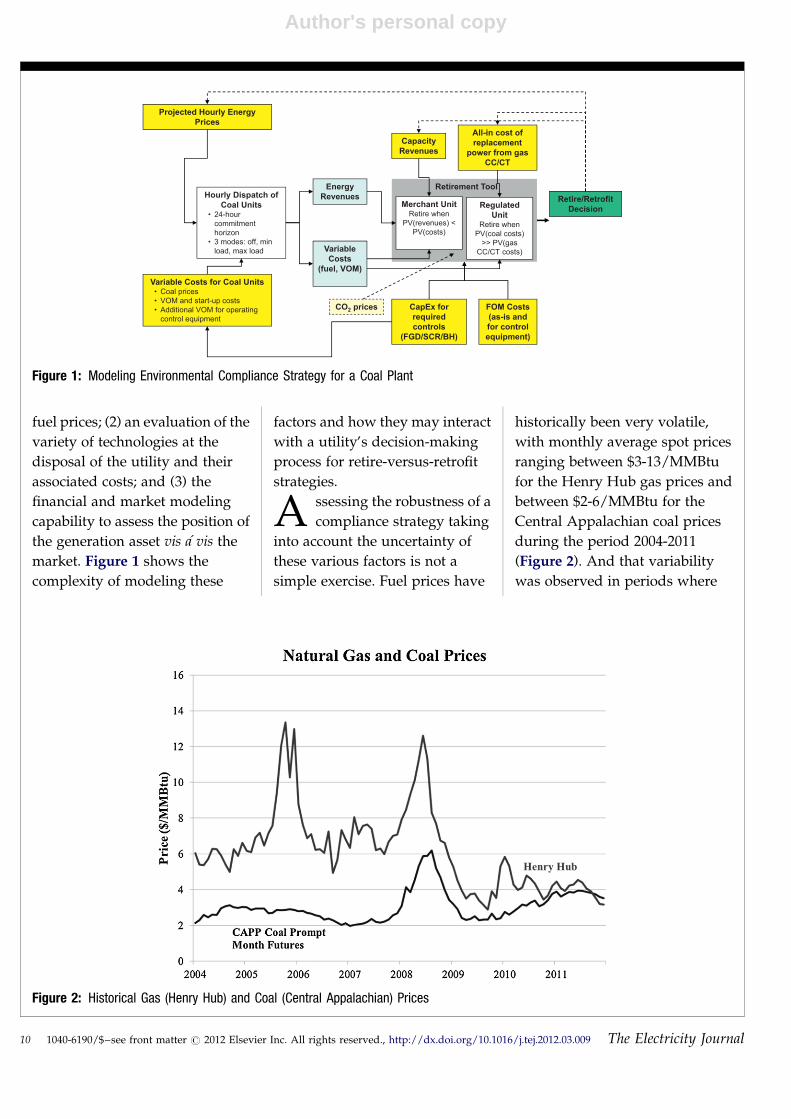

must begin with: (1) a forecast of

Some of theserules are nearlyimmediatewhile othersare six oreight yearsaway.

April 2012, Vol. 25, Issue 3 1040-6190/$–see front matter # 2012 Elsevier Inc. All rights reserved., http://dx.doi.org/10.1016/j.tej.2012.03.009 9

Author's personal copy

fuel prices; (2) an evaluation of the

variety of technologies at the

disposal of the utility and their

associated costs; and (3) the

financial and market modeling

capability to assess the position of

the generation asset vis a vis the

market. Figure 1 shows the

complexity of modeling these

factors and how they may interact

with a utility’s decision-making

process for retire-versus-retrofit

strategies.

A ssessing the robustness of a

compliance strategy taking

into account the uncertainty of

these various factors is not a

simple exercise. Fuel prices have

historically been very volatile,

with monthly average spot prices

ranging between $3-13/MMBtu

for the Henry Hub gas prices and

between $2-6/MMBtu for the

Central Appalachian coal prices

during the period 2004-2011

(Figure 2). And that variability

was observed in periods where

[(Figure_2)TD$FIG]

Figure 2: Historical Gas (Henry Hub) and Coal (Central Appalachian) Prices

[(Figure_1)TD$FIG]

Merchant UnitRetire when

PV(revenues) <

PV(costs)

Hourly Dispatch of

Coal Units• 24-hour

commitment

horizon

• 3 modes: off, min

load, max load

Projected Hourly Energy

Prices

Variable Costs for Coal Units• Coal prices

• VOM and start-up costs

• Additional VOM for operating

control equipment

Capacity

Revenues

FOM Costs

(as-is and

for control

equipment)

CapEx for

required

controls

(FGD/SCR/BH)

All-in cost of

replacement

power from gas

CC/CT

Regulated

UnitRetire when

PV(coal costs)

>> PV(gas

CC/CT costs)

Retirement Tool

Variable

Costs

(fuel, VOM)

Energy

Revenues Retire/Retrofit

Decision

CO2 prices

Figure 1: Modeling Environmental Compliance Strategy for a Coal Plant

10 1040-6190/$–see front matter # 2012 Elsevier Inc. All rights reserved., http://dx.doi.org/10.1016/j.tej.2012.03.009 The Electricity Journal

Author's personal copy

there was not nearly so much

capacity at risk in the overall

market.

T he difficulties of such an

analysis are greatly

compounded by the significant

uncertainty associated with the

scope of the regulations and their

timing. Prognosticating

incorrectly, and making

investments too narrowly

optimized to satisfy a specific set of

prognostications, can be costly. On

the other hand, some degree of

such expert disappointments are

inevitable. Good decisions arising

out of a well-reasoned process can

still yield uncomfortable

outcomes. As a result, the utility

will need to review its technology

options and decide if it wishes to

take a staged approach to the

investments, postponing the

technology choices until the

regulations are clearly delineated,

or whether it is worth the risk to

give up that approach and its

option value because of the

potential for reduced overall costs.

A forthcoming article by Brattle

experts provides a more detailed

discussion and examples of key

factors and optionalities to

consider in environmental

compliance planning.

Step Two: Strategy Development:Regulatory Evaluation of Alterna-tives

Commissions are increasingly

moving towards the use of pre-

approval processes rather than

after-the-fact approval of

expenditures. That does not

change the standard criteria of

‘‘prudently incurred’’ and ‘‘used

and useful,’’ but the pre-approval

process attempts to reduce the

likelihood that issues will arise

based on these criteria at final

approval. The venues for the

utility’s request for pre-approval

of its environmental compliance

expenditures are varied. Such pre-

approval could arise during the

proceedings of the utility’s

integrated resource plan (IRP), an

acquisition of a certificate of

convenience and necessity, or a

rate case. Depending on the

regulatory circumstances, that

process may begin with informal

discussions with commission staff

regarding the issues that they

foresee arising in the proceedings.

It is important to note that staff’s

concerns or their perceptions of

the commissioners’ concerns may

not perfectly reflect the

commissioner’s views. It is also

important to note that even with

commission pre-approval, there is

still the chance that the

commission will change its view.

The closure of the Mohave

generating station by Southern

California Edison (SCE) was

preceded by a California Public

Utilities Commission (CPUC)-

mandated study, the Mohave

Generating Station Alternatives/

Complements Study,5 which

included assessment of renewable

energy options. The plant was

closed by SCE. However, in a

recent case before CPUC, SCE’s

request for a return on the recovery

of the decommissioning costs, on

unavoidable cost in the closure of a

plant, was challenged.6

T he utility’s case for its

compliance strategy needs to

have two main focuses. The first is

providing justification for the

compliance strategy, the second

providing the mechanism for

financing and the impact on rates. The

justification will hinge on the

utility’s capability to demonstrate

that making the investment it has

chosen is the best of all

alternatives. In the past, that case

might have been made solely as an

evaluation of the alternative

technologies available to achieve

compliance with the relevant

regulations. Now the evaluation

may include alternatives such as

other conventional generation,

renewables,7 energy efficiency

(energy optimization in

Michigan), distributed generation,

grid efficiency improvements, and

demand response of various

forms. Some or all of these may

have been part of the utility’s

compliance planning, but if not,

they will likely need to be

incorporated when the

commission considers their

request. The utility will likely be

required to defend the plant’s past

operating record and provide a

The utility needs, first,to provide justificationfor the compliancestrategy, and second, toprovide the mechanismfor financing and theimpact on rates.

April 2012, Vol. 25, Issue 3 1040-6190/$–see front matter # 2012 Elsevier Inc. All rights reserved., http://dx.doi.org/10.1016/j.tej.2012.03.009 11

Author's personal copy

justification for why it believes the

plant will operate as well or better

than it has in the past. The utility

will need to clearly delineate all

environmental and health

regulations – local, state, and

federal – that it currently meets

and that its compliance plan will

meet going forward. It can expect

that it must provide information

on short-term and long-term

alternatives for compliance and

provide a comparison of those

costs.

O ne particularly thorny issue

will arise if the utility

pursues a staged path for

compliance that attempts to

postpone its compliance decisions

until the EPA’s issuance of final

order, clarifying amendments, and

any subsequent litigation

decisions that affect the

regulations. The commission may

be seeking an optimized

investment path with a very

specific set of assumptions about

the final form of regulations, a

position not consistent with an

approach that postpones

investments until there is

regulatory clarity. There is no best

approach to dealing with this, but

there are some considerations that

the utility can bring before the

commission. First, the utility can

use historical experience, perhaps

its own, to demonstrate that

forecasting what a regulation will

be can lead to costly mistakes.

Those costs may have taken the

form of over-compliance,

inappropriate technology choice,

or failing to employ a non-capital-

intensive alternative, such as

emissions credits. Second, the

utility will need to demonstrate the

risks that it faces by making its

choices in advance of final

determination of the regulations.

This will require assessing the

potential rules’ variations and the

alternatives to address them and

the range of compliance costs, an

exercise the utility will likely have

already gone through internally,

and showing how these costs,

when translated into revenue

requirements, will adversely affect

ratepayers. Third, the utility may

need to put forward a clear plan

that demonstrates how it will

implement the appropriate

strategy as quickly as possible

once the regulations are in place.

This may require creating

optionality at the plant to accept

the various compliance

alternatives. This optionality may

take the form of implementing less

capital-intensive technologies

with higher operating costs, or

delaying the decision to commit to

large cost commitments and

instead rely on market purchases

in the interim. However, the

additional cost of allowing for

these flexibilities should be

weighed against the expected

option value associated with these

strategies.

Potentially, the optimal

compliance strategy is none at all,

i.e., that the plant’s economics

cannot justify the level of

additional investments that would

be required to be fully compliant.

The utility will likely need to

simultaneously develop a short-

run plan for compliance prior to

retiring the plant and a longer-

term plan for the replacement of

the resources, if it so chooses. If

those resources are conventional

(for example, a combined-cycle

gas turbine), then the commission

will likely need an analysis of

all of the non-conventional

generation alternatives partially

listed above.

Step Three: Assessing Financingand Rate Mechanisms

Once the utility has justified its

compliance strategy, it must

address with the commission the

financing of the investments and

the mechanisms for the recovery of

costs. Financing the costs of

environmental compliance may

turn out to be a much larger issue

than it has been in the past. For

some utilities, the size of the

investments that are required may

impinge on other potential

investments that the utility would,

in the absence of the compliance

requirements, undertake.

Depending on the level of

previous compliance by the utility

and the size of the incremental

investment that must be made, the

utility may find itself bumping up

12 1040-6190/$–see front matter # 2012 Elsevier Inc. All rights reserved., http://dx.doi.org/10.1016/j.tej.2012.03.009 The Electricity Journal

Author's personal copy

against a capital constraint in

order to accommodate all of the

required investments.8 This can

arise whether the utility’s

compliance program aims to

modify its current generation fleet

or retire units and find substitute

resources. These capital

constraints are important and

urgent because they can put the

utility in the unenviable, and

possibly untenable, position of

choosing between generation

investments and investments in its

transmission and distribution

systems. This is also not a position

that regulators would like to find

themselves in when presented

with the reality of the financing

constraints that utilities face. Even

in the absence of a capital

constraint, any additional

financing of these investments

through utility-issued debt will

have the effect of increasing the

financial leverage of the company

and may result in a lowered credit

rating and/or higher costs of

financing, also not a desirable

situation for the utility or

regulator. This rating or financing

cost impact can be particularly

acute in situations of prolonged

regulatory approval processes

before the investment is put into

the rate base.

F ortunately, regulators have a

number of tools at their

disposal to address the utilities’

financing issues. Effective

communication and coordination

between the commission and the

regulated utilities on these

mechanisms will be critical in

allaying the financial constraints,

lowering cost of environmental

compliance, and reducing rate

impacts on consumers.

First, some states have allowed

utilities to access state-sponsored

tax-exempt bonds to fund

environmental compliance

investments. Wisconsin Electric

Power Company availed itself of

Wisconsin’s ‘‘Environmental

Trust Funding’’ mechanism to

secure approximately $430 million

in environmental financing for one

of its past projects. A bill surcharge

collected the required revenues.

Similar mechanisms have been

used in West Virginia and North

Carolina. Whether other states

adopt similar mechanisms, or use

the existing mechanisms for the

wave of potential compliance

investment, remains to be seen.

S econd, for many jurisdictions,

an environmental rate rider

may be the rate mechanism of

choice.9 The environmental rider is

attractive to the utility because it

permits timely recovery of its costs

without the requirement that the

time when compliance costs are

incurred must coincide with its

rate case cycle. Although a rider is

attractive to the utility it will not

necessarily go unopposed by the

commission, which may require a

demonstration of its necessity

and/or merits. The utility may be

required to demonstrate its

inability to raise funds without the

rider or, if it can raise funds, how

the costs of those funds will be

higher absent the rider. A

demonstration of the

reasonableness of the costs and the

efficiency of the approach is also

likely when the rider is applied for.

The major difference between an

environmental rider and other

forms of cost riders, such as fuel

and purchased power, is that the

costs included in the rider are

capital, not operating, costs. Even

in the presence of an

environmental rider, the operating

costs of an environmental

compliance technology are often

included in fuel adjustment riders,

likely so as to maintain some

clarity to the cost accounting. In

the past, most states have included

all costs required to comply with

environmental regulations in their

environmental adders. In the face

of uncertainty about the costs of

compliance, the commission may

set a limit on the amount of costs

that can be covered under the

environmental rider, with

additional costs requiring a

separate approval mechanism.

That limit may be based on the size

of the costs themselves or the rate

impact of the environmental rider.

Thus, the utility seeking a rider

will need to assess beforehand the

rate impacts of the rider. As noted

above, pre-approval may

increasingly be an attractive

option. Some states have instituted

April 2012, Vol. 25, Issue 3 1040-6190/$–see front matter # 2012 Elsevier Inc. All rights reserved., http://dx.doi.org/10.1016/j.tej.2012.03.009 13

Author's personal copy

penalties in the form of reduced

rates of return on equity if the final

costs of the compliance project

exceed its initially projected costs.

In that situation, the rate approach

is likely to be accompanied by an

audit process which informs the

commission of progress of the

compliance strategy and the

permissible level of revenue

collection.

T hird, a variety of rate designs

can be utilized to alleviate the

financing constraints and

minimize consumer impact.

Although utilities and

commissions may prefer historical

precedents, innovative

mechanisms used by other utilities

can be beneficial to consider. We

offer two examples. The first one is

the CWIP (construction work in

progress) mechanism, through

which utilities are allowed to place

large capital expenditures during

the construction phase into the rate

base and to recover the investment

before the asset becomes ‘‘used

and useful.’’ A CWIP mechanism

will alleviate the rate shocks by

accelerating the capital recovery to

the construction phase. Kentucky,

West Virginia, and Minnesota

have allowed for the recovery of

environmental compliance

expenditures through CWIP. If the

expenditures are modest, then

even a one-time rate increase may

suffice. For many compliance

requirements envisioned in Table

1, however, the investments may

be substantial, and the CWIP

treatment will be beneficial to the

utilities and ratepayers. Another

example to mitigate the initial rate

shock is the use of trended original

cost (TOC) or other levelization

mechanisms in ratemaking during

the operation phase10 in contrast

with depreciated original cost

ratemaking (DOC), which is

routinely applied in cost-based

ratemaking (see sidebar on TOC

and levelization mechanisms). The

TOC method has been applied to

oil pipelines since the 1980s11 and

some forms of levelization

mechanisms have been adopted

for gas pipelines12 more recently

by FERC, but these alternative rate

designs have been used little, if at

all, in the electric power industry.

Compared to DOC, whose main

feature is front loading of the

capital recovery, the alternative

mechanisms defer the cost

recovery to later periods of the

asset life. Consequently, they tend

to bring the regulated rates closer

to those prevailing in a

competitive market, thereby

enhancing economic efficiency,

and mitigate rate shocks to the

ratepayers in the initial years of a

new asset. The impact on rates can

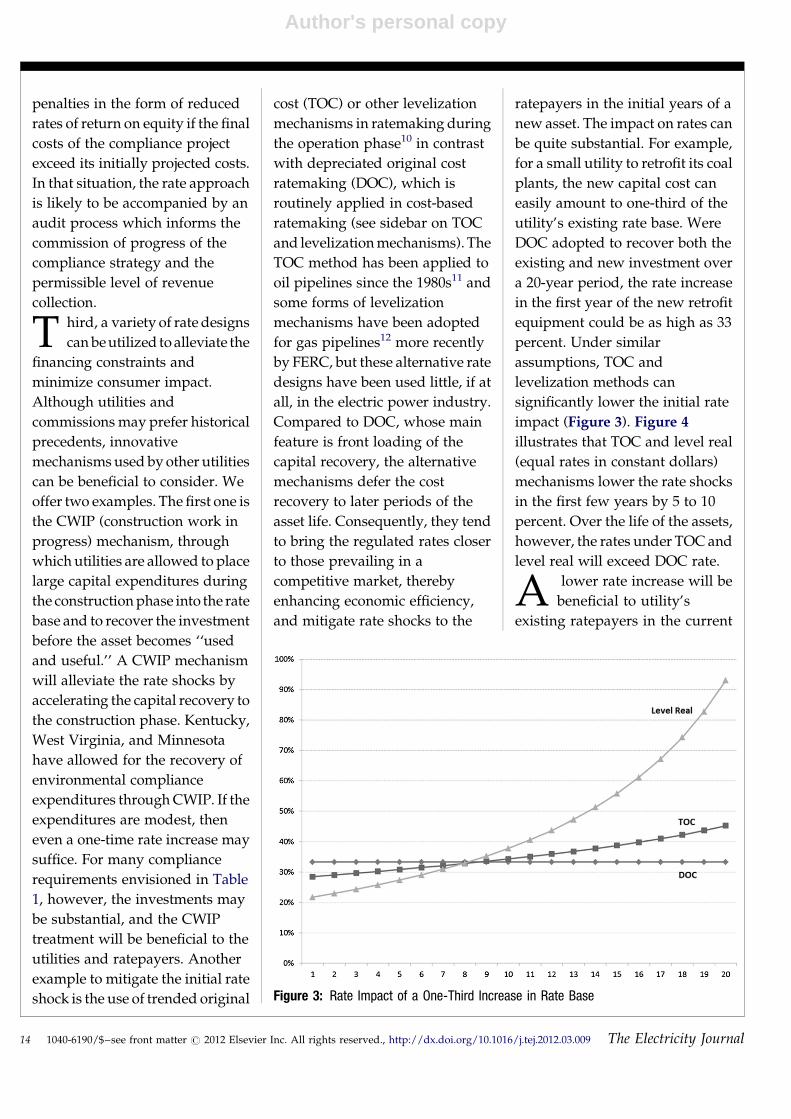

be quite substantial. For example,

for a small utility to retrofit its coal

plants, the new capital cost can

easily amount to one-third of the

utility’s existing rate base. Were

DOC adopted to recover both the

existing and new investment over

a 20-year period, the rate increase

in the first year of the new retrofit

equipment could be as high as 33

percent. Under similar

assumptions, TOC and

levelization methods can

significantly lower the initial rate

impact (Figure 3). Figure 4

illustrates that TOC and level real

(equal rates in constant dollars)

mechanisms lower the rate shocks

in the first few years by 5 to 10

percent. Over the life of the assets,

however, the rates under TOC and

level real will exceed DOC rate.

A lower rate increase will be

beneficial to utility’s

existing ratepayers in the current[(Figure_3)TD$FIG]

Figure 3: Rate Impact of a One-Third Increase in Rate Base

14 1040-6190/$–see front matter # 2012 Elsevier Inc. All rights reserved., http://dx.doi.org/10.1016/j.tej.2012.03.009 The Electricity Journal

Author's personal copy

fragile economic recovery and

could help the utility to attract

new customers to its service

territory. To shift the cost

recovery from a front-end loaded

pattern to a deferred pattern,

investors’ risk increases, if for no

other reasons, due to an increase

in duration of the investment

period. (The cost recovery paths

for both TOC and Level Real

scenarios in Figure 4 reflect a cost

of capital 0.25 percent higher that

than under the DOC mechanism.)

The exact increase in cost of

capital will depend on the pattern

of cost recovery, term structure of

the interest rates, and regulatory

commitment to the approved rate

design, i.e., regulatory risk. A

credible reduction in regulatory

risk, through legislation or

securitization such as the rate

reduction bonds, goes a long way

in convincing the credit rating

agencies and investors in general

and lowering cost of capital.13

IV. Conclusions

The EPA’s current and

forthcoming regulations

regarding coal generation

present unprecedented

challenges for both utilities and

regulators. Both their scope and

the uncertainty regarding their

final form make the decisions

both by the utility and the

regulator much more difficult

than prior compliance decisions.

For justifying the proposed

compliance strategy, utilities will

need: (1) to review its technology

options; (2) develop a strategy to

address the regulatory review

process of its options; and (3)

assess the financing options and

cost recovery options through

rates. This process has never

been more perilous for both

utility and regulator. The ability

of utilities to meet their

customers’ energy needs while

ensuring continued health of the

industry will depend on how

well this process is carried out.

A. Sidebar: TOC and

levelization mechanisms

TOC and net depreciated

original cost are essentially the

same except for their treatment of

inflation. TOC reflects inflation

through periodic upward

adjustments to rate base, whereas

net depreciated original cost

reflects estimated inflation in the

nominal rate of return. This

difference between them results in

a different timing of the recovery

of the cost of equity capital over the

life of the property. Both methods,

however, yield the same

discounted value for shareholders,

i.e., fair opportunity to earn their

return on and of capital.

T he following example

illustrates TOC ratemaking

(as shown in Figure 4). Assume a

new capital expenditure for

[(Figure_4)TD$FIG]

Figure 4: Comparison of Alternative Ratemaking Mechanisms

April 2012, Vol. 25, Issue 3 1040-6190/$–see front matter # 2012 Elsevier Inc. All rights reserved., http://dx.doi.org/10.1016/j.tej.2012.03.009 15

Author's personal copy

environmental compliance with

an original equity investment of

$1 billion.14 Also assume that a

just and reasonable return on

equity would be 11 percent and

that 4 percent of that represents

inflation. This leaves 7 percent as

the ‘‘real’’ rate of return. In its

first year of service, the power

plant would be entitled to earn

$70 million (7 percent times $1

billion) and $40 million (4 percent

times $1 billion) would be

capitalized into the firm’s equity

rate base to be amortized over the

life of the property starting in the

first year, along with the

depreciation on the $1 billion. If

the depreciation life were 20

years, in addition to the return of

$70 million, the plant would be

entitled to recover, in the first

year, $2 million as amortization

($40 million divided by 20), $50

million as depreciation ($1 billion

divided by 20), its embedded

debt cost, and depreciation

associated with debt investment.

The equity rate base at the start of

year two would be $988 million

($1 billion � $50 million + $38

million). This process would

continue over the life of the

property until the rate base

(assuming no salvage value) hit

zero. Unless changed in a

subsequent rate case, the real rate

of return, which should be

relatively stable, would be 7

percent each year. The inflation

rate would vary as the chosen

inflation index varies. Potential

inflation indices include a

construction price index (such as

the Handy-Whitman index) or

the U.S. Treasury bill rate.&

Endnotes:

1. See http://www.economist.com/node/21547804.

2. http://www.reuters.com/article/2011/12/30/us-utilities-epa-idUSTRE7BT17420111230.

3. Capital cost estimates for a 100 MWcoal unit are $783/kW for a wet FGDand $41/kW for a DSI. Variable O&Mexpenses for the same size unit are$1.8/MWh for a wet FGD and $7/MWh for a DSI. See Edison ElectricInstitute, Potential Impacts ofEnvironmental Regulation on the USGeneration Fleet, Jan. 2011, at 36, andEPA IPM Basecase V4.10 (Aug. 2010).

4. This is also occurring in Texas,albeit for merchant generation.

5. The study was conducted bySynapse and Sargent & Lundy in Feb.2006, and is posted at http://www.synapse-energy.com/Downloads/SynapseReport.2006-02.SCE.Mohave-Alternative-Generation-Resources.05-020.pdf.

6. Southern California Edison 2012General Rate Case Rebuttal TestimonyVolume 2: Plant, Taxes DepreciationExpense and Reserve, Rate Base, and Non-Tariffed Products & Service, July 5, 2011.

7. See Paul Joskow’s paper Comparingthe Costs of Intermittent and DispatchableElectricity Generating Technologies(posted at http://hdl.handle.net/1721.1/59468) for some pitfalls toavoid in the renewable resourcecomparisons.

8. There appears to be recognition ofthese potential constraints by thefinancial community. See http://guidance.fidelity.com/viewpoints/utilities-sector-2012.

9. See F.C. Graves, P.Q Hanser and G.Basheda, Electricity Utility AutomaticAdjustment Clauses: Why They AreNeeded More Than Ever, ELEC. J., June,2007.

10. See S.C. Myers, A.L. Kolbe andW.B. Tye, Regulation and CapitalFormation in the Oil Pipeline Industry,TRANSPORTATION J., Summer 1984, at25-49; S.C. Myers, A.L. Kolbe and W.B.Tye, Inflation and Rate of ReturnRegulation, RES. IN TRANSPORTATION REG.,

Vol. 2 (1985), at 83-119; and W.B. Tyeand A.L. Kolbe, Optimal TimeStructures for Regulated Industries,TRANSPORTATION PRACTITIONERS J.,Winter 1992, at 176-196. The firstarticle also contains references to theWilliams Pipeline case before theFederal Energy RegulatoryCommission in which Mr. Myersprovided testimony on oil pipelineratemaking. See also the endnotebelow.

11. See Federal Energy RegulatoryCommission, Williams Pipe LineCompany, Docket Nos. OR79-1-000and 022 (Phase I) Opinion No. 154-B;Opinion and Order on Remand(issued June 28, 1985) and FederalEnergy Regulatory CommissionWilliams Pipe Line Company, DocketNos. OR79-1-026, -027, -028, -029, -030and -031 Opinion No. 154-C; OrderDenying Rehearing in Part, ModifyingOpinion No .154-B in Part, ClarifyingThat Opinion, and Denying Stay for oilpipeline cases.

12. See, e.g., Kern River GasTransmission Co., Opinion No. 486,117 FERC � 61,077 (2006), order onreh’g, Opinion 486-A, 123 FERC �61,056 (2008), order on reh’g,Opinion 486-B, 126 FERC � 61,034,order on reh’g, Opinion No. 486-C, 129FERC � 61,240 (2009), order on reh’g,Opinion No. 486-D, 133 FERC �61,162, at P 156 (2010) (Kern River);and Portland Natural GasTransmission System, OPINION NO.510, 134 FERC � 61,129, OPINIONAND ORDER ON INITIALDECISION, (2011).

13. See also F.C. Graves, P.Q Hanserand G. Basheda, Means of MitigatingRate Shock, ELEC. J., Oct. 2007. Also, afuller exposition of the use of trendedoriginal cost will be found in aforthcoming paper by the currentauthors.

14. This amount of capitalexpenditure would be equivalent to a1,000 MW coal plant installingmultiple environmental controls at acost of $1,000/kW. The capitalexpenditure of $1 billion representsabout 20 percent of AEP’s projectedtotal capital expenditures of $5-6billion on environmental controlequipment by 2020.

16 1040-6190/$–see front matter # 2012 Elsevier Inc. All rights reserved., http://dx.doi.org/10.1016/j.tej.2012.03.009 The Electricity Journal