sessions 18 & 19

TRANSCRIPT

Sessions 18 & 19

Capital and altera3on of capital

1

A. Meaning of ‘capital’

• Legal ‘capital’ or share ‘capital’ used in a restricted technical sense – cash received by the company from investors who subscribe for the company’s shares

2

B. Altera3on of capital

• Increasing capital by issuing new shares • Sec3on 71 – Company, if authorised by its ar3cles can alter its share capital by one or more of the following ways eg : – consolida3ng and dividing its share capital; – subdivide its shares – cancel shares that have not been taken up See Table A art 40, which permits altera3on by the passing of an ordinary resolu3on

3

Capital Maintenance

4

A, B, C “Capital maintenance rule”

• Common law rule that a company’s share capital should be maintained during the life of the company….

• Ra3onale… • Reflected in law rela3ng to:

– Co cannot reduce its share capital – Co cannot acquire its shares – Co cannot pay dividend except out of profit – Co cannot lend money on the security of its shares – Co cannot give financial assistance to help others aquire shares in itself

5

C. Reduc3on of capital Rule : Co may not return assets to its members or reduce its capital except in manner set out in CA. -‐-‐-‐-‐-‐-‐-‐-‐ 3 ways of reduc3on of capital men3oned in s 78A(1) (non-‐exhaus+ve) : 1) Ex3nguish or reduce the unpaid capital ; 2) Cancel any paid-‐up capital that is lost or

unrepresented by assets ; and 3) Return to shareholders any paid-‐up capital

which is in excess of the needs of the co.

6

D. Consequence : Reduc3on of capital

Effect of contraven3on 1. Dir who allow reduc3on without complying

with CA commit breach of duty – replace $ misapplied

2. Dir who makes solvency statement to support reduc3on of capital pursuant to non-‐court sanc3oned method without reasonable ground guilty of offence

7

E. Excep3on : Permiaed reduc3on of capital (s 78A-‐K)

Excep3on • Sec3on 78A: Company can reduce capital ‘in any way’ so long

as: – Companies Act procedures are followed; and – Its memorandum and ar3cles do not prohibit the reduc3on

• Two ‘tracks’ to effect reduc3on, both star3ng with a special resolu3on – without court order (s 78B-‐F): – with court approval (s 78G-‐I):

(Please read the sec3ons. There is no need, however, to be too concerned about too much procedural detail)

8

E. Excep3on : Permiaed reduc3on of capital

Non-‐court sanc3oned capital reduc3on : 78B-‐F 1. Special resolu3on by shareholders. 2. Declara3on of solvency by all directors (unless

reduc3on of capital is solely by way of cancella3on of capital that is lost or unrepresented by available assets)

3. Creditor may apply to court within 6 weeks’ of resolu3on to have resolu3on cancelled

4. Court may cancel resolu3on if creditor’s debt not secured or no safeguard for it and it is not the case that safeguards are unnecessary

9

E. Excep3on : Permiaed reduc3on of capital

Court sanc3oned capital reduc3on :78G-‐I 1.Special resolu3on for reduc3on 2. Reduc3on confirmed by court -‐ Court seale list of qualifying creditors -‐ Court sa3sfied that creditor’s claim discharged or he has consented to reduc3on or claim secured or co has a lot of assets leg ager reduc3on

3. Court order lodged with ACRA

10

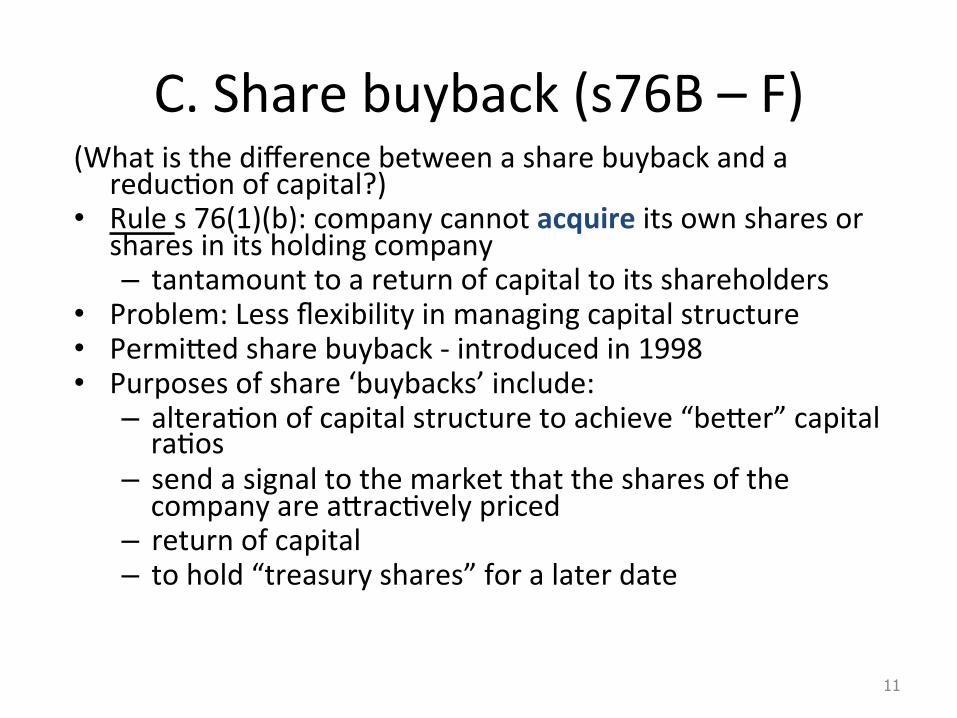

C. Share buyback (s76B – F) (What is the difference between a share buyback and a

reduc3on of capital?) • Rule s 76(1)(b): company cannot acquire its own shares or

shares in its holding company – tantamount to a return of capital to its shareholders

• Problem: Less flexibility in managing capital structure • Permiaed share buyback -‐ introduced in 1998 • Purposes of share ‘buybacks’ include: – altera3on of capital structure to achieve “beaer” capital ra3os

– send a signal to the market that the shares of the company are aarac3vely priced

– return of capital – to hold “treasury shares” for a later date

11

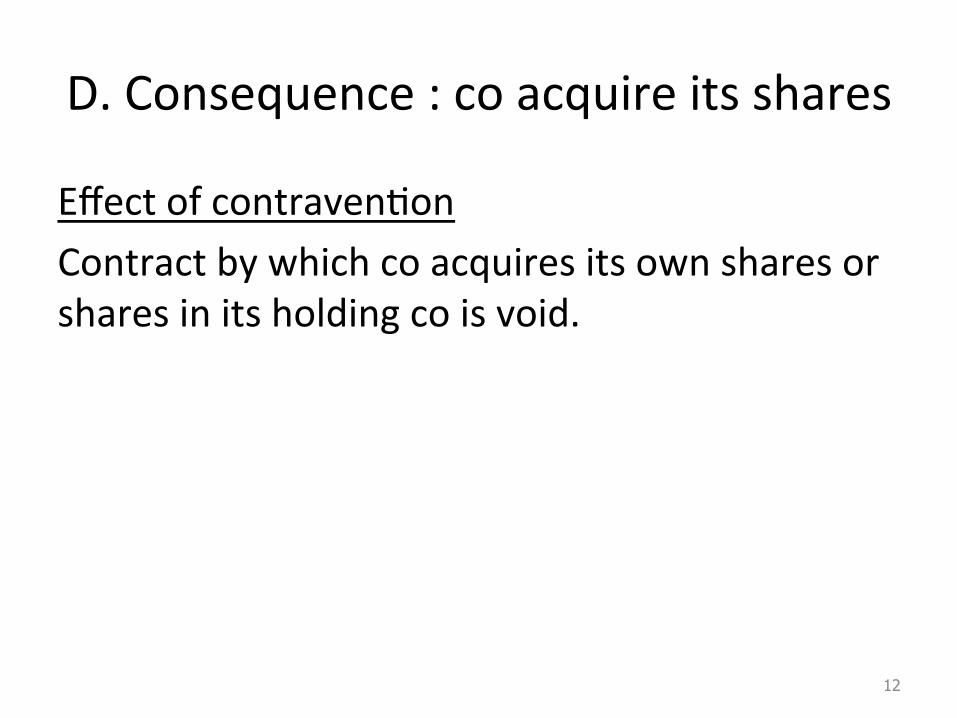

D. Consequence : co acquire its shares

Effect of contraven3on Contract by which co acquires its own shares or shares in its holding co is void.

12

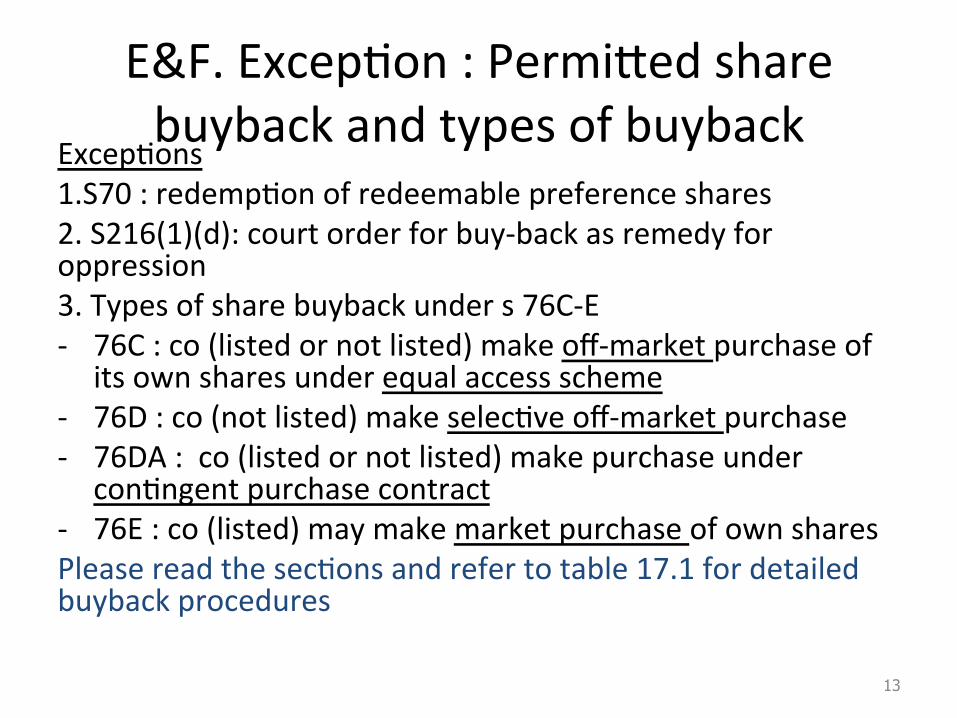

E&F. Excep3on : Permiaed share buyback and types of buyback

Excep3ons 1.S70 : redemp3on of redeemable preference shares 2. S216(1)(d): court order for buy-‐back as remedy for oppression 3. Types of share buyback under s 76C-‐E -‐ 76C : co (listed or not listed) make off-‐market purchase of

its own shares under equal access scheme -‐ 76D : co (not listed) make selec3ve off-‐market purchase -‐ 76DA : co (listed or not listed) make purchase under

con3ngent purchase contract -‐ 76E : co (listed) may make market purchase of own shares Please read the sec3ons and refer to table 17.1 for detailed buyback procedures

13

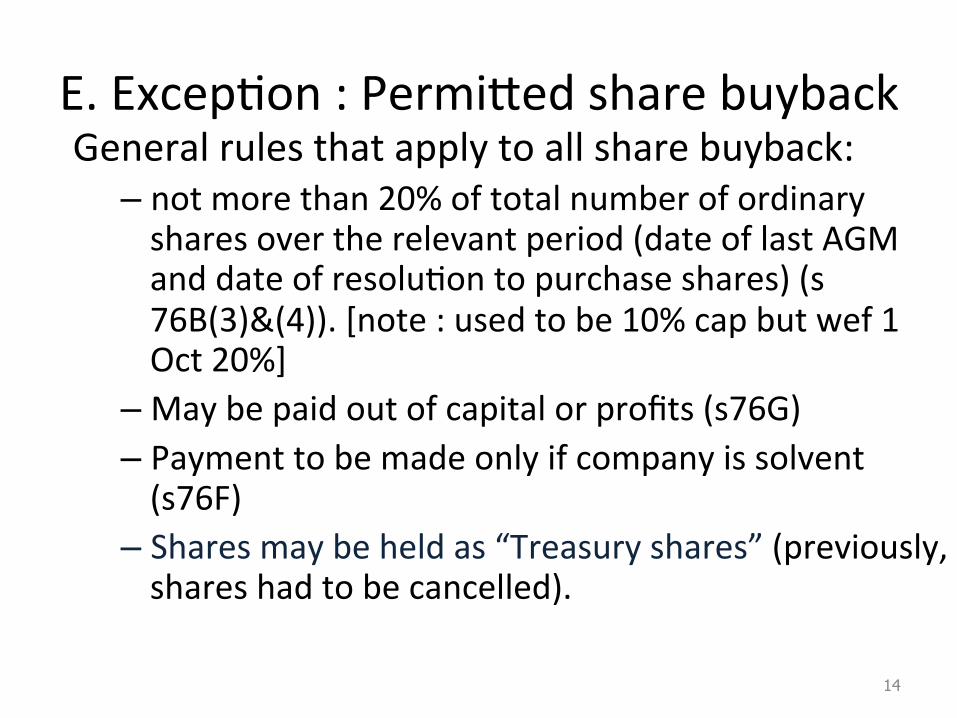

E. Excep3on : Permiaed share buyback General rules that apply to all share buyback: – not more than 20% of total number of ordinary shares over the relevant period (date of last AGM and date of resolu3on to purchase shares) (s 76B(3)&(4)). [note : used to be 10% cap but wef 1 Oct 20%]

– May be paid out of capital or profits (s76G) – Payment to be made only if company is solvent (s76F)

– Shares may be held as “Treasury shares” (previously, shares had to be cancelled).

14

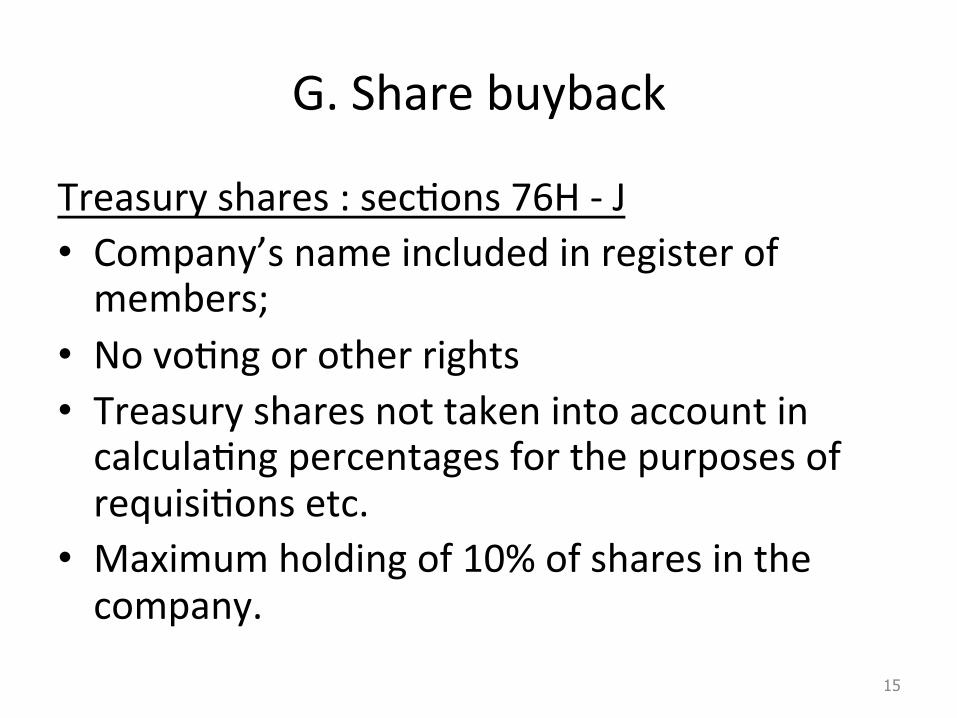

G. Share buyback

Treasury shares : sec3ons 76H -‐ J • Company’s name included in register of members;

• No vo3ng or other rights • Treasury shares not taken into account in calcula3ng percentages for the purposes of requisi3ons etc.

• Maximum holding of 10% of shares in the company.

15

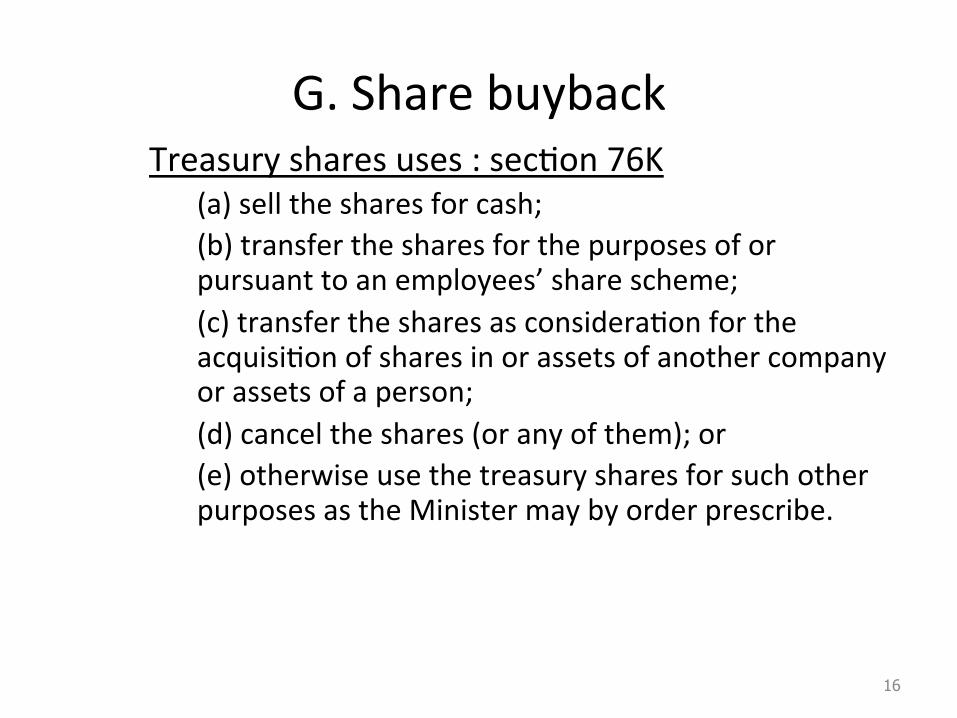

G. Share buyback Treasury shares uses : sec3on 76K

(a) sell the shares for cash; (b) transfer the shares for the purposes of or pursuant to an employees’ share scheme; (c) transfer the shares as considera3on for the acquisi3on of shares in or assets of another company or assets of a person; (d) cancel the shares (or any of them); or (e) otherwise use the treasury shares for such other purposes as the Minister may by order prescribe.

16

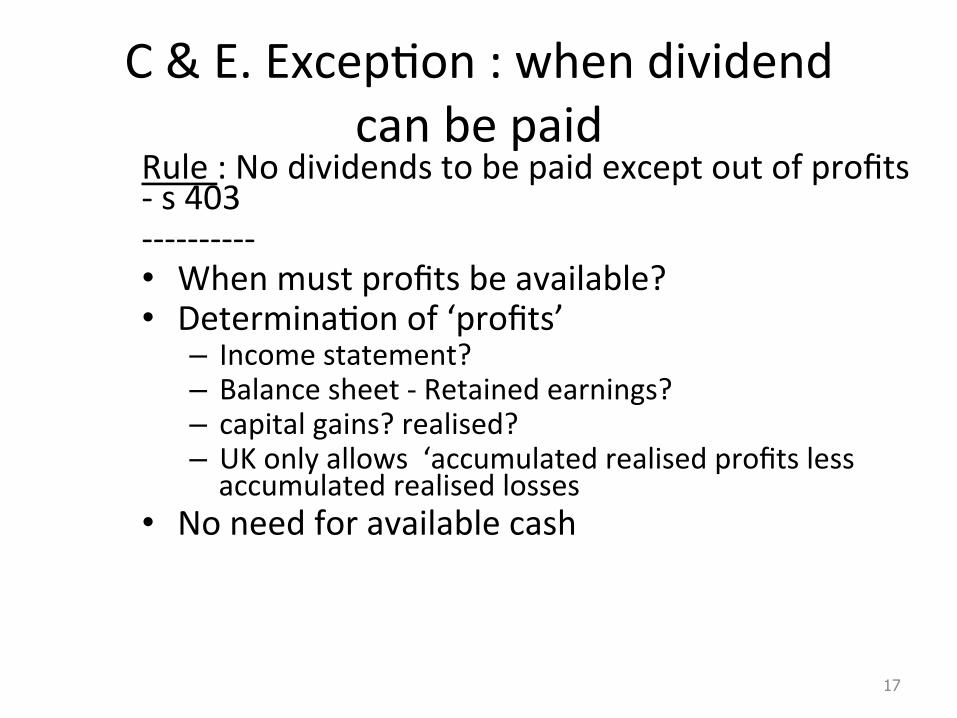

C & E. Excep3on : when dividend can be paid

Rule : No dividends to be paid except out of profits -‐ s 403 -‐-‐-‐-‐-‐-‐-‐-‐-‐-‐ • When must profits be available? • Determina3on of ‘profits’

– Income statement? – Balance sheet -‐ Retained earnings? – capital gains? realised? – UK only allows ‘accumulated realised profits less accumulated realised losses

• No need for available cash

17

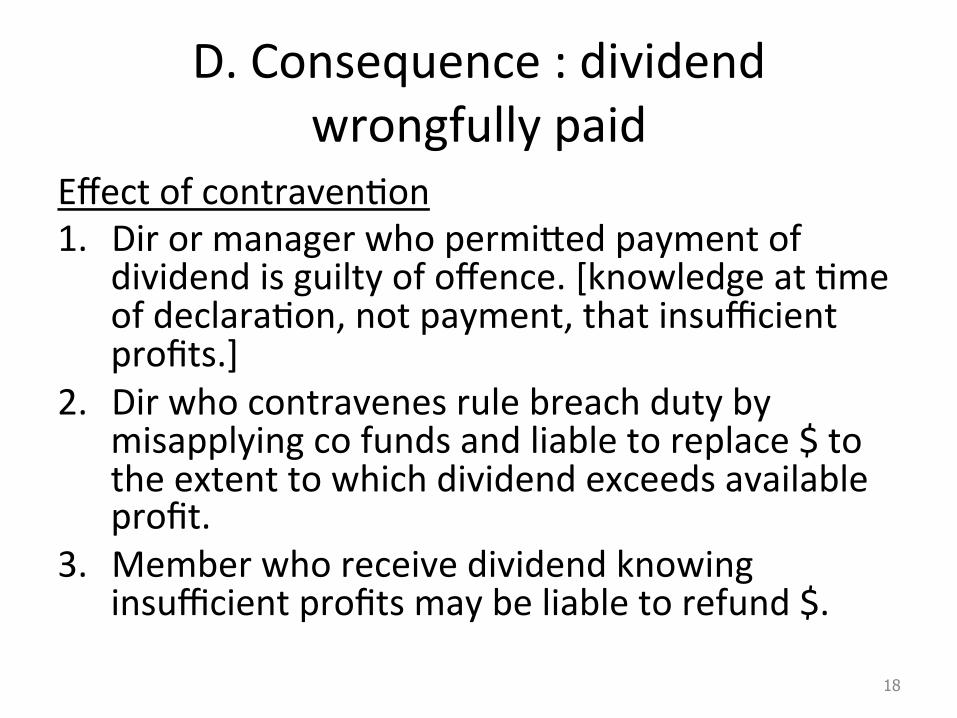

D. Consequence : dividend wrongfully paid

Effect of contraven3on 1. Dir or manager who permiaed payment of

dividend is guilty of offence. [knowledge at 3me of declara3on, not payment, that insufficient profits.]

2. Dir who contravenes rule breach duty by misapplying co funds and liable to replace $ to the extent to which dividend exceeds available profit.

3. Member who receive dividend knowing insufficient profits may be liable to refund $.

18

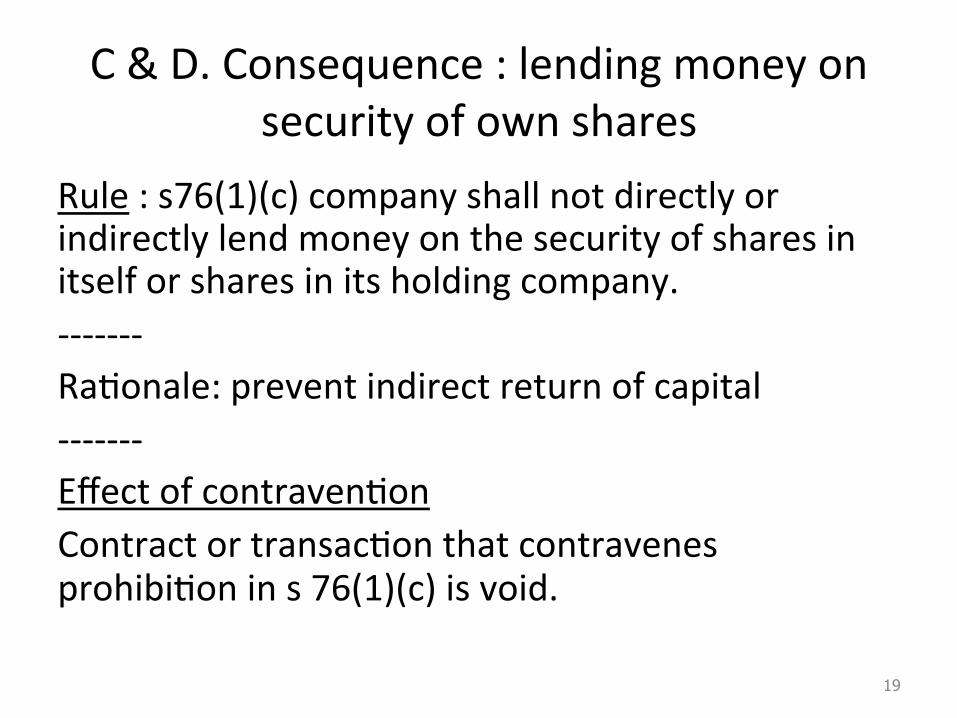

C & D. Consequence : lending money on security of own shares

Rule : s76(1)(c) company shall not directly or indirectly lend money on the security of shares in itself or shares in its holding company. -‐-‐-‐-‐-‐-‐-‐ Ra3onale: prevent indirect return of capital -‐-‐-‐-‐-‐-‐-‐ Effect of contraven3on Contract or transac3on that contravenes prohibi3on in s 76(1)(c) is void.

19

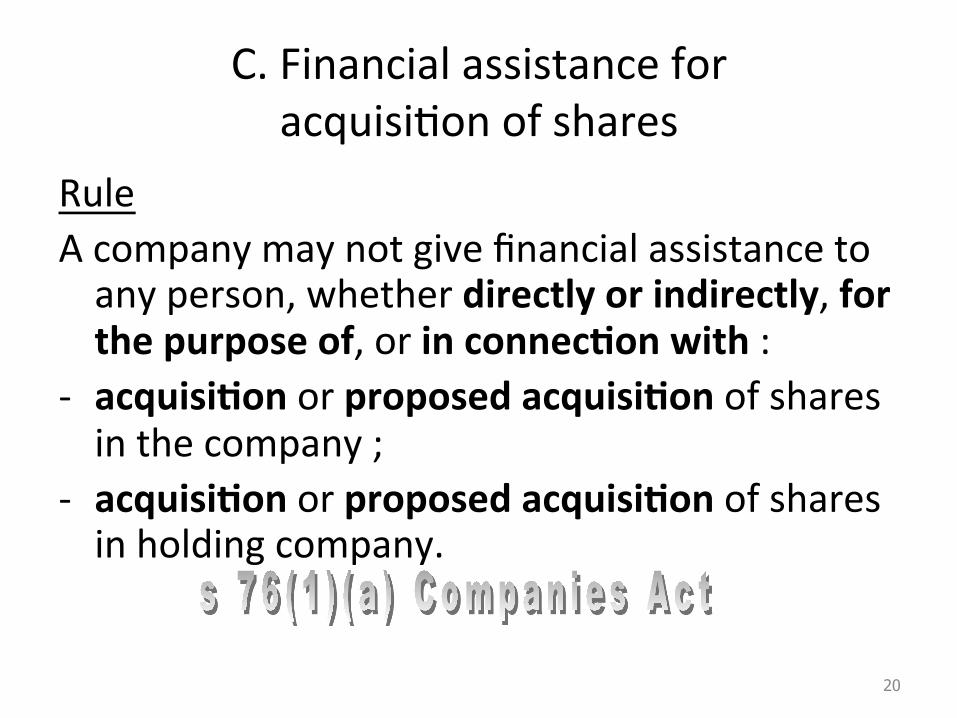

C. Financial assistance for acquisi3on of shares

Rule A company may not give financial assistance to any person, whether directly or indirectly, for the purpose of, or in connec+on with :

-‐ acquisi+on or proposed acquisi+on of shares in the company ;

-‐ acquisi+on or proposed acquisi+on of shares in holding company.

20

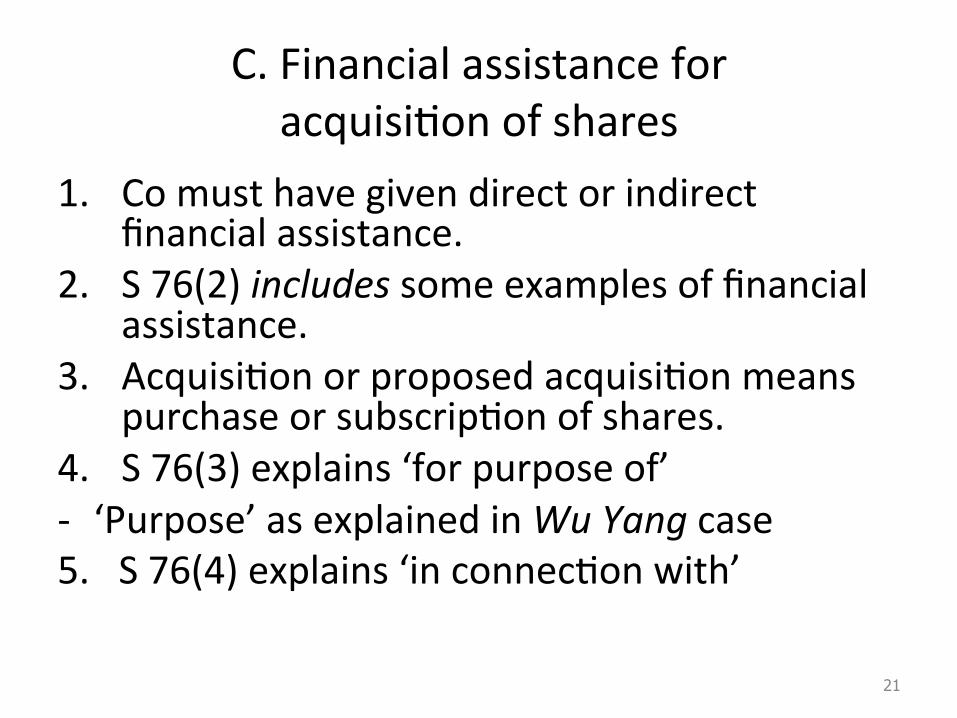

C. Financial assistance for acquisi3on of shares

1. Co must have given direct or indirect financial assistance.

2. S 76(2) includes some examples of financial assistance.

3. Acquisi3on or proposed acquisi3on means purchase or subscrip3on of shares.

4. S 76(3) explains ‘for purpose of’ -‐ ‘Purpose’ as explained in Wu Yang case 5. S 76(4) explains ‘in connec3on with’

21

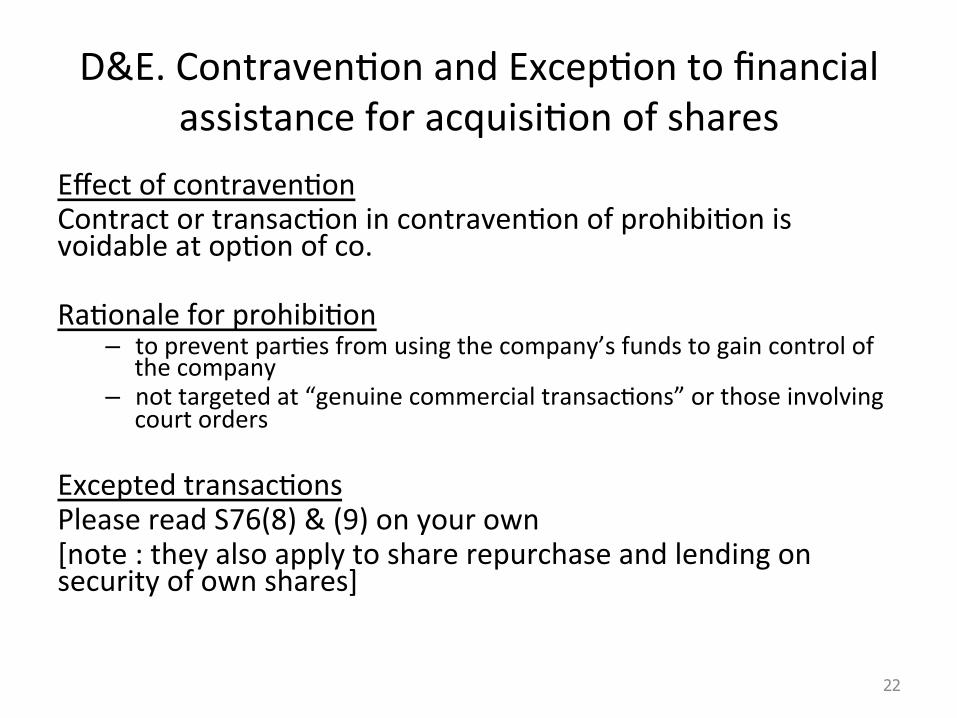

D&E. Contraven3on and Excep3on to financial assistance for acquisi3on of shares

Effect of contraven3on Contract or transac3on in contraven3on of prohibi3on is voidable at op3on of co. Ra3onale for prohibi3on

– to prevent par3es from using the company’s funds to gain control of the company

– not targeted at “genuine commercial transac3ons” or those involving court orders

Excepted transac3ons Please read S76(8) & (9) on your own [note : they also apply to share repurchase and lending on security of own shares]

22

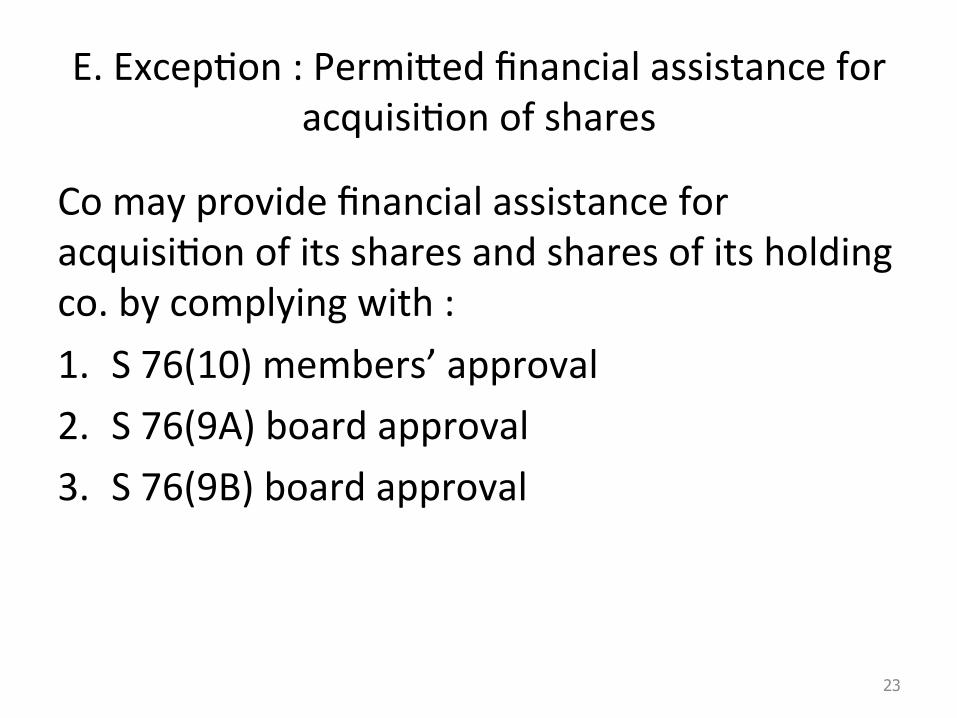

E. Excep3on : Permiaed financial assistance for acquisi3on of shares

Co may provide financial assistance for acquisi3on of its shares and shares of its holding co. by complying with : 1. S 76(10) members’ approval 2. S 76(9A) board approval 3. S 76(9B) board approval

23

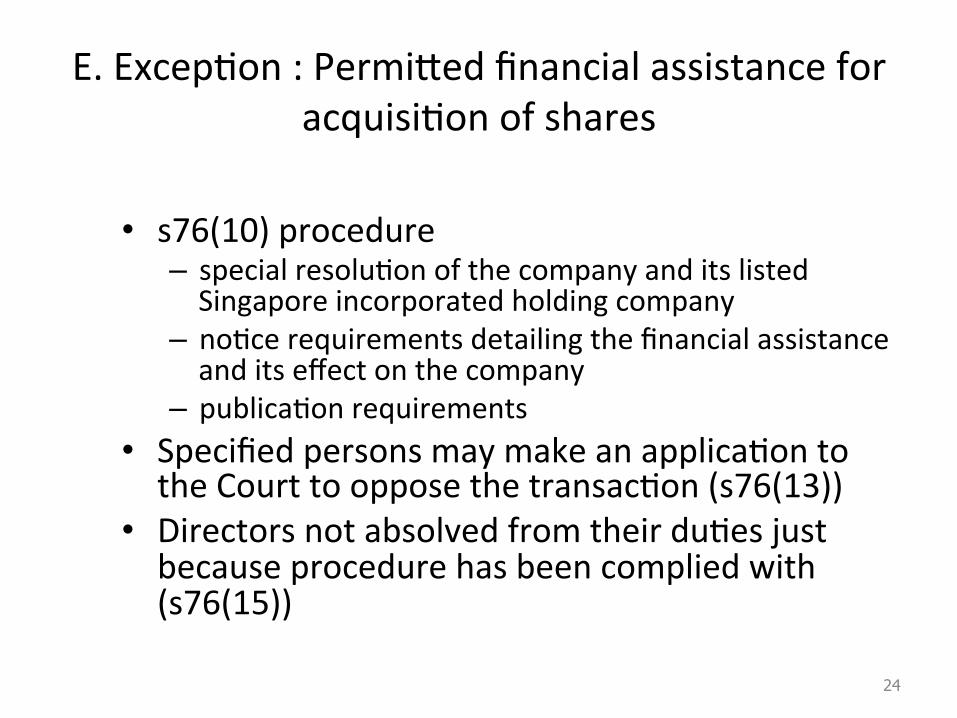

E. Excep3on : Permiaed financial assistance for acquisi3on of shares

• s76(10) procedure – special resolu3on of the company and its listed Singapore incorporated holding company

– no3ce requirements detailing the financial assistance and its effect on the company

– publica3on requirements • Specified persons may make an applica3on to the Court to oppose the transac3on (s76(13))

• Directors not absolved from their du3es just because procedure has been complied with (s76(15))

24

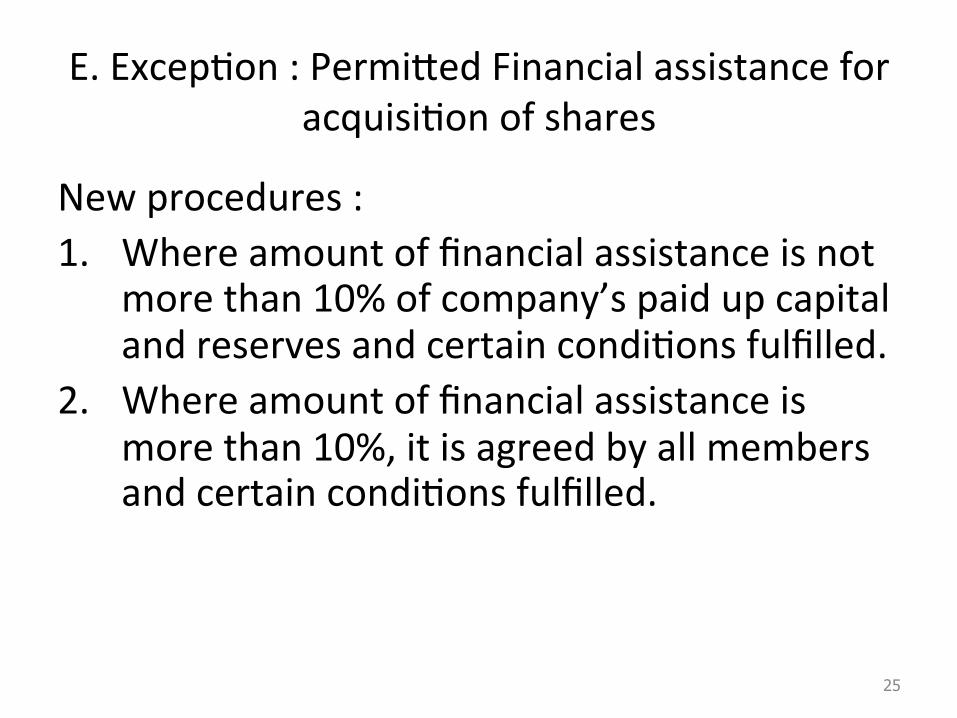

E. Excep3on : Permiaed Financial assistance for acquisi3on of shares

New procedures : 1. Where amount of financial assistance is not

more than 10% of company’s paid up capital and reserves and certain condi3ons fulfilled.

2. Where amount of financial assistance is more than 10%, it is agreed by all members and certain condi3ons fulfilled.

25

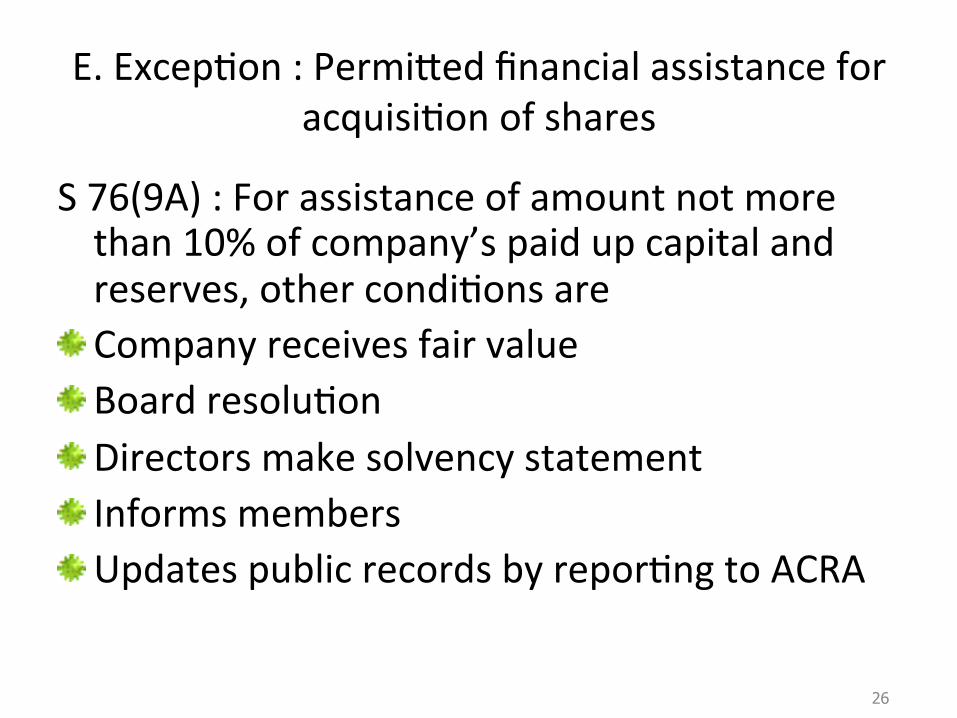

E. Excep3on : Permiaed financial assistance for acquisi3on of shares

S 76(9A) : For assistance of amount not more than 10% of company’s paid up capital and reserves, other condi3ons are

" Company receives fair value " Board resolu3on " Directors make solvency statement " Informs members " Updates public records by repor3ng to ACRA

26

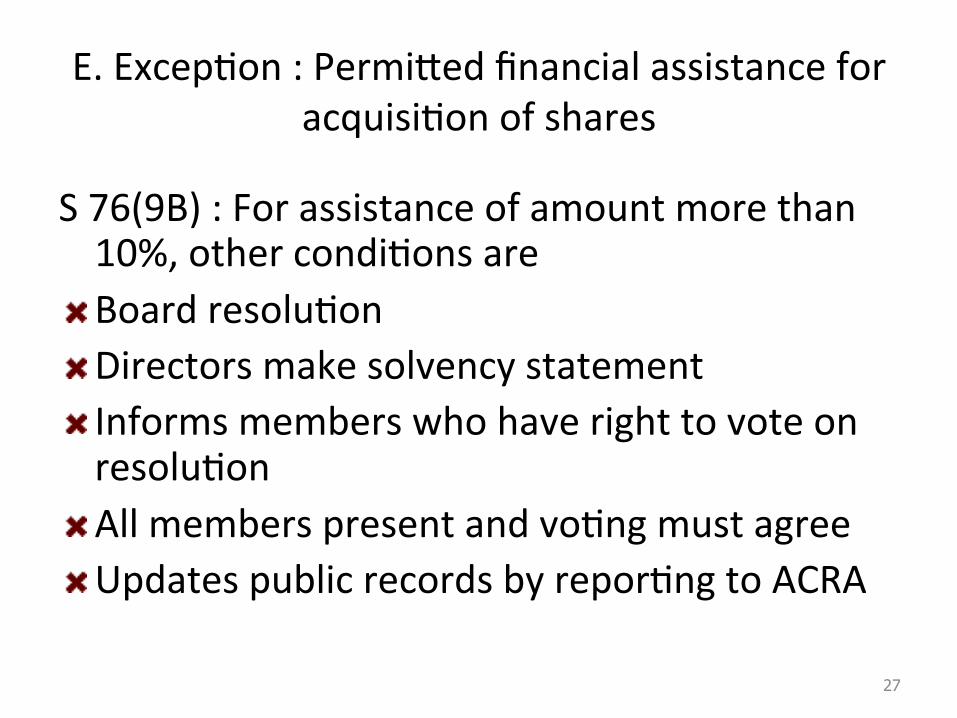

E. Excep3on : Permiaed financial assistance for acquisi3on of shares

S 76(9B) : For assistance of amount more than 10%, other condi3ons are

" Board resolu3on " Directors make solvency statement " Informs members who have right to vote on resolu3on

" All members present and vo3ng must agree " Updates public records by repor3ng to ACRA 27

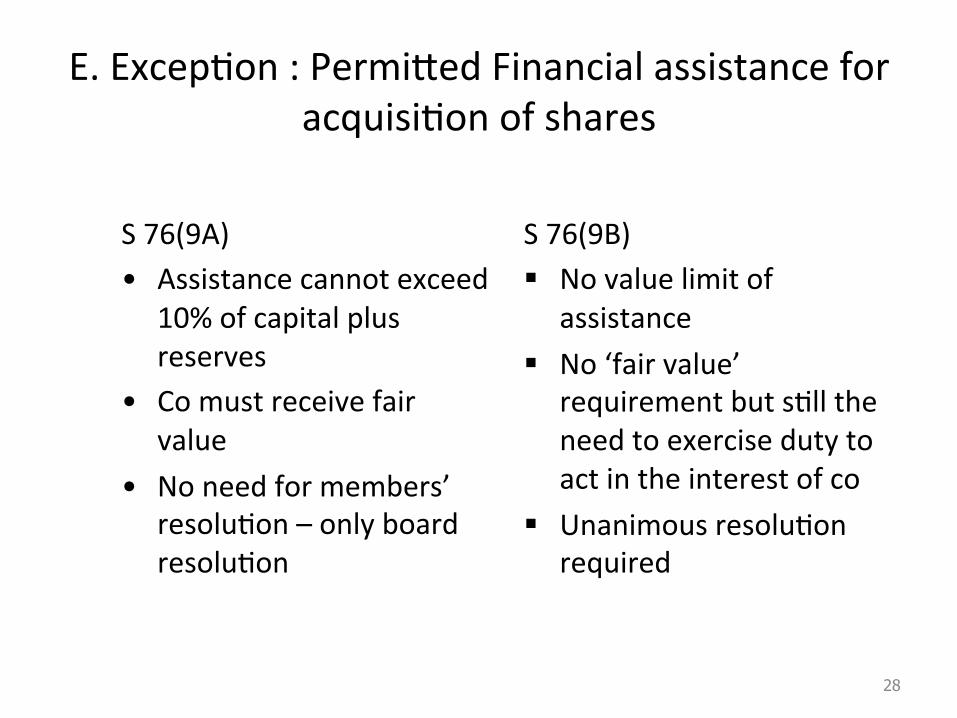

E. Excep3on : Permiaed Financial assistance for acquisi3on of shares

S 76(9A) • Assistance cannot exceed

10% of capital plus reserves

• Co must receive fair value

• No need for members’ resolu3on – only board resolu3on

S 76(9B) § No value limit of

assistance § No ‘fair value’

requirement but s3ll the need to exercise duty to act in the interest of co

§ Unanimous resolu3on required

28

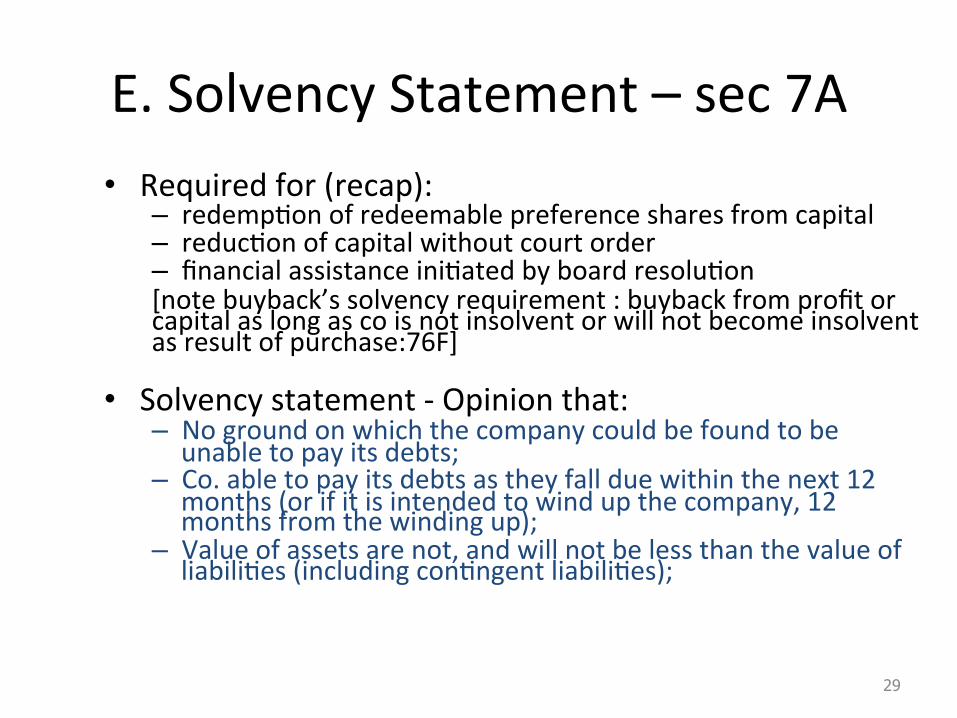

E. Solvency Statement – sec 7A • Required for (recap):

– redemp3on of redeemable preference shares from capital – reduc3on of capital without court order – financial assistance ini3ated by board resolu3on [note buyback’s solvency requirement : buyback from profit or capital as long as co is not insolvent or will not become insolvent as result of purchase:76F]

• Solvency statement -‐ Opinion that: – No ground on which the company could be found to be unable to pay its debts;

– Co. able to pay its debts as they fall due within the next 12 months (or if it is intended to wind up the company, 12 months from the winding up);

– Value of assets are not, and will not be less than the value of liabili3es (including con3ngent liabili3es);

29

E. Solvency Statement – sec 7A

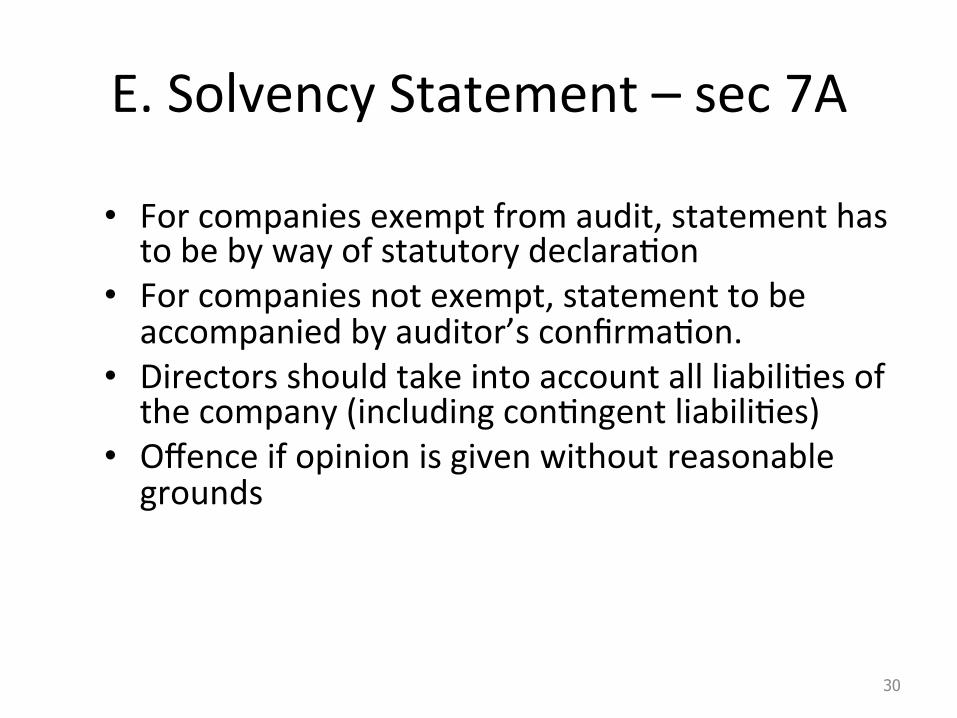

• For companies exempt from audit, statement has to be by way of statutory declara3on

• For companies not exempt, statement to be accompanied by auditor’s confirma3on.

• Directors should take into account all liabili3es of the company (including con3ngent liabili3es)

• Offence if opinion is given without reasonable grounds

30