reconstruction of decision-making behavior in shareholder and stakeholder theory: implications for...

TRANSCRIPT

REVIEW PAPER

Reconstruction of decision-making behaviorin shareholder and stakeholder theory: implicationsfor management accounting systems

Alexandra Rausch

Received: 3 September 2010 / Accepted: 15 October 2010

� Springer-Verlag 2010

Abstract This paper focuses on two interrelated research questions. First, an anal-

ysis of managerial decision-making is incorporated into shareholder and stakeholder

theory. Secondly, the paper investigates what consequences result for management

accounting from inherent conceptions of managerial decision-making behavior. These

research questions are based on assumptions of complex interrelationships among

decision-making managers, management accountants, and techniques they employ.

The findings of this research support that tenets of management accounting systems

correspond best with shareholder theory. In doing so they apply financial measures,

pursue the goal of profit maximization, and focus on decision-making behavior

resulting from the agency relationship between shareholder and manager. Stakeholder

theory, however, is fundamentally different from shareholder theory in terms of goals,

management philosophy, relationships, behavioral assumptions etc. For these reasons

differences with respect to managerial decision-making behavior are reasonable and

different requirements related to management accounting systems appear appropriate.

Keywords Management accounting � Decision-making � Managerial behavior �Shareholder theory � Stakeholder theory

JEL Classification L20 � M10 � M41

1 Introduction

Management accounting is concerned with providing information and techniques to

managers to assist them in making decisions (Dominiak and Louderback 1991;

A. Rausch (&)

Institute for Management, Department of Controlling and Strategic Management,

Alpen-Adria-University Klagenfurt, Universitaetsstrasse 65-67, 9020 Klagenfurt, Austria

e-mail: [email protected]

123

Rev Manag Sci

DOI 10.1007/s11846-010-0053-2

Emmanuel et al. 1990; Pizzey 1998). There exists a complex interrelationship

between decision-making managers and management accountants regarding infor-

mation and appropriate techniques they should employ. Management accountants

first collect, process, and report information to managers and suggest appropriate

techniques managers should use in performing their jobs. Secondly, in providing

relevant information and techniques, management accountants may exert consid-

erable influence on managerial decision-making behavior, for example through

specific performance measurements (Dominiak and Louderback 1991; Hansen and

Mowen 1994). This decision-making process actually is quite complicated as

managers often have varied and unstable interests rendering them capable of acting

from many different ethical points of view that can and do change over time

(Dominiak and Louderback 1991; Freeman and Phillips 2002; Emmanuel et al.

1990). Consequently, management accountants must not only be concerned with the

‘‘pure’’ content of information and techniques they provide but also with decision

makers’ behavior, including their individual motivational and cognitive character-

istics and, especially, related limitations (Weber et al. 2003).

Some researchers prescribe how managers should make decisions and what

accounting should be like (normative approach). Other researchers explore how

managers actually behave and what management accounting is in fact like (positive

or instrumental-descriptive approach) (Jensen 1976, 1983; Watts and Zimmerman

1978, 1990; Donaldson and Preston 1995; Friedman and Miles 2002). On the basis

of prior research, the present paper first discusses different behavioral assumptions

in shareholder and stakeholder theory. Secondly, consequences for the design of

management accounting systems are deduced from these behavioral assumptions.

The discussion of management accounting systems’ relationships to shareholder and

stakeholder theory is motivated by various assumptions of how managers might

make decisions in shareholder and stakeholder organized corporations. These

assumptions, however, are not entirely realistic. Due to unrealistic assumptions,

management accountants and accounting systems that should support ‘‘good’’

decision-making in corporations are likely not applied in the most efficient and

effective manner. For example, a basic behavioral assumption in shareholder

oriented corporations says managers are opportunistic. According to the underlying

theory of ‘‘model of man’’ managers represent themselves as self-interested actors

rationally maximizing their own utility thereby causing possible agency losses to

shareholders (Donaldson and Davis 1991). Thus, a primary goal of the corporation

is to reduce or impede opportunistic managerial behavior and agency losses. This

gives rise to appropriate incentive systems or monitoring mechanisms (Eisenhardt

1989; Jensen and Meckling 1976) which is the job of management accounting

(Emmanuel et al. 1990). Agency losses, however, not only affect shareholders but

also other stakeholders. As stakeholder theory does not contain any conceptual

specification regarding how to make trade-offs among stakeholders (Freeman 1984;

Clarkson 1995), economic rates of return might be skimmed off by managers and/or

shareholders instead of investing them for the benefit of other stakeholders (e.g.

Stahl 2003). That is why stakeholder theory might possibly expose arbitrary

allocation of rates of return and opportunistic managerial behavior (Jensen 2001)

although stakeholder oriented managers should ideally be collective-serving and

A. Rausch

123

altruistically maximize value for all stakeholders. However, such collective-serving

behavior assumed in stakeholder theory (Jones et al. 2007; Vilanova 2007) is also

possible in shareholder corporations where managers as stewards simply want to

‘‘do a good job’’ and are personally rewarded and satisfied by achieving corporate

goals (Davis et al. 1997; Donaldson and Davis 1991).

The present paper critically discusses these behavioral assumptions. On the basis

of these findings possible fields of action and suggestions for management

accounting design are identified. Thus the main research questions are:

• How do managers behave in decision-making processes against the background

of shareholder and stakeholder theory?

• What consequences can be deduced from behavioral assumptions for the design

of management accounting systems in shareholder and stakeholder theory, and

thus, which suggestions for management accounting design might improve

managerial decision-making against the background of shareholder and

stakeholder theory?

For this purpose, the remainder of the paper is organized as follows: Sect. 2.1

traces the key aspects of shareholder and stakeholder theory; Sect. 2.2 provides an

overview of relevant factors characterizing managerial decision-making behavior;

Section Three examines theoretical approaches that provide a basis for explaining

and describing managerial decision-making behavior and identifies behavioral

assumptions against the background of shareholder and stakeholder theory. Finally,

a framework is developed integrating shareholder and stakeholder theories as well

as related behavioral assumptions. On the basis of this framework, Section Four

suggests implications for management accounting design. A discussion follows on

the decision-facilitating role and the decision-influencing role of management

accounting systems. The final section offers concluding thoughts and an outlook to

further research.

2 Theoretical framework

2.1 Shareholder and stakeholder theory

The discussion in research and literature related to shareholder versus stakeholder

theory has lasted for nearly half a century focusing mainly on the differences

between the two theories and the critical examination of which one is better, more

justifiable and most applicable in theoretical and practical fields (e.g. Friedman and

Miles 2006; Freeman and McVea 2005; Sundaram and Inkpen 2004). Shareholder

theory emerged from the neoclassical paradigm and is regarded as the most

prominent approach in theory and praxis due to the increasing relevance of capital

markets and value management (Hosseini and Brenner 1992; Wood 2008). In pure

shareholder theory the primary goal of corporations is to maximize shareholder

returns and value while adhering to legal principles which respect integrity

(Rappaport 1999; Stadler et al. 2006). Managers are regarded as hired agents and

fiduciaries of shareholders who represent the principals. They are responsible to

Reconstruction of decision-making behavior

123

spend corporate funds in authorized ways for profitability and the benefit of

shareholders. The core notion of pure shareholder theory suggests long-term cash-

surpluses increasing shareholder value not only for the benefit of the owners but also

of all stakeholders. If managers do not manage to create shareholder value, all

stakeholders are at risk (Rappaport 1999). Pure shareholder theory is primarily

focused on the bilateral relationship between managers as agents and shareholders

as principals of the managers (Ruhli and Sachs 2003; Rappaport 1999). Stakehold-

ers other than shareholders are only regarded as a means to the end of the

corporation’s profitability. The central shareholder-manager relationship is based on

a contract whereby, according to the assumption of efficient markets, principals and

agents are free to enter into and exit the contract (Hill and Jones 1992). Logically, it

is generally assumed that the role of owner and manager do not lie in one person.

Thus, ownership and control are separated as are risk bearing and decision-making

(Donaldson and Davis 1991; Jensen and Meckling 1976). Principals maintain

ownership of the firm through stocks and leave control of the corporation to

managers who might have interests and goals that differ from those of the principal

(Rappaport 1999). This fiduciary relationship is fundamental to behavioral

assumptions in pure shareholder theory.

Stakeholder theory, on the other hand, proposes that owners of shares of stock are

the prime beneficiary of the firm’s activities. Still, stakeholder theory recognizes a

multiplicity of groups having a stake in the operations of the corporation which

merit equal consideration in managerial decision-making (Phillips 1997; Evan and

Freeman 1993; Freeman and Phillips 2002). This paper focuses on the classic

approach of stakeholder theory offered by Freeman as a contribution to strategic

management (Freeman 1984) and later on as a normative approach (Evan and

Freeman 1993; Freeman 2001). Freeman’s perspective focuses on how organiza-

tions should be conceptualized, governed, and how management ought to act

(Friedman and Miles 2006; Freeman 2001). This pure stakeholder theory follows

two principles. First, the corporation should be managed for the benefit of all

stakeholders (Freeman 1994). Each stakeholder group that contributes something to

the corporation should receive something in return regardless of whether the

stakeholder is a voluntary and active contributor to the firm or is simply passive,

tolerating the existence and operation of the corporation (Post et al. 2002a, b;

Vilanova 2007; Ruhli and Sachs 2003). The corporation’s profitability depends on

how well the relationships with all stakeholder groups are managed (Freeman and

Phillips 2002), to what extent the rights of these groups are ensured and how much

the groups participate in decisions that substantially affect their welfare (Evan and

Freeman 1993). Thus, the fundamental difference of pure stakeholder as compared

to pure shareholder theory is that the stakeholder oriented corporation and its

decision-making managers are responsible for meeting the interests of multiple

stakeholders and for creating value for all stakeholders even if it reduces the

corporation’s profitability (Smith 2003; Phillips et al. 2003). Consequently,

stakeholder interests are considered as means to the end of the corporation’s

profitability but also as ends in themselves (Smith 2003; Evan and Freeman 1993).

Secondly, managers have a fiduciary relationship to both, shareholders and all non-

shareholder stakeholders. Managers, hence, are agents of all stakeholders with the

A. Rausch

123

fiduciary duty to safeguard the long-term stakes of each stakeholder group (Evan

and Freeman 1993; Smith 2003; Post et al. 2002a; Phillips et al. 2003). As the

corporation is a nexus of contracts and relationships between multiple stakeholder

groups with conflicting interests and goals (Freeman and Phillips 2002; Post et al.

2002a; Vilanova 2007), collective-serving managers must balance the legitimate

interests and respect the claims of every stakeholder group (Clarkson 1995; Hill and

Jones 1992; Jensen 2001; Smith 2003).

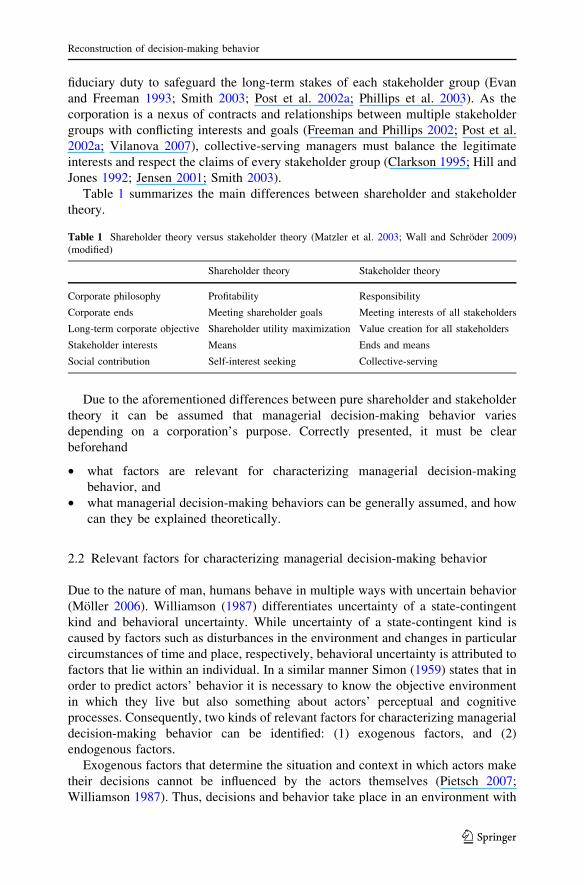

Table 1 summarizes the main differences between shareholder and stakeholder

theory.

Due to the aforementioned differences between pure shareholder and stakeholder

theory it can be assumed that managerial decision-making behavior varies

depending on a corporation’s purpose. Correctly presented, it must be clear

beforehand

• what factors are relevant for characterizing managerial decision-making

behavior, and

• what managerial decision-making behaviors can be generally assumed, and how

can they be explained theoretically.

2.2 Relevant factors for characterizing managerial decision-making behavior

Due to the nature of man, humans behave in multiple ways with uncertain behavior

(Moller 2006). Williamson (1987) differentiates uncertainty of a state-contingent

kind and behavioral uncertainty. While uncertainty of a state-contingent kind is

caused by factors such as disturbances in the environment and changes in particular

circumstances of time and place, respectively, behavioral uncertainty is attributed to

factors that lie within an individual. In a similar manner Simon (1959) states that in

order to predict actors’ behavior it is necessary to know the objective environment

in which they live but also something about actors’ perceptual and cognitive

processes. Consequently, two kinds of relevant factors for characterizing managerial

decision-making behavior can be identified: (1) exogenous factors, and (2)

endogenous factors.

Exogenous factors that determine the situation and context in which actors make

their decisions cannot be influenced by the actors themselves (Pietsch 2007;

Williamson 1987). Thus, decisions and behavior take place in an environment with

Table 1 Shareholder theory versus stakeholder theory (Matzler et al. 2003; Wall and Schroder 2009)

(modified)

Shareholder theory Stakeholder theory

Corporate philosophy Profitability Responsibility

Corporate ends Meeting shareholder goals Meeting interests of all stakeholders

Long-term corporate objective Shareholder utility maximization Value creation for all stakeholders

Stakeholder interests Means Ends and means

Social contribution Self-interest seeking Collective-serving

Reconstruction of decision-making behavior

123

characteristics accepted by the actors when they have decided to place themselves in

a particular situation (Simon 1981). In this context, actors usually must contend with

an ambiguous environment and organizational situation, with high uncertainty about

relevant factors and the effects of their decisions (Pietsch 2007). Given the large

number of exogenous factors that frame managers’ behavior in corporations,

researchers usually limit the number of factors examined in their studies to a few as

dealing with all possible effects in a single study is impractical (Nutt 2005). In this

paper the number of exogenous factors is limited to two: management philosophy

and cultural systems which are suggested by Davis et al. (1997) to differentiate

agency-theory and stewardship theory. The next section of this paper demonstrates

obvious parallels to the differentiation of behavioral assumptions. Management

philosophy is determined by objectives, rules, structures and the handling of

information in a corporation (Davis et al. 1997). Structures and the handling of

information are also discussed in Rowley (1997) and Hill and Jones (1992). A

control-oriented management philosophy, as the term already suggests, imposes

wide control mechanisms on actors in the corporation. The actors are allowed only

limited scope, the time frame is usually short-term and the main objective is cost

control. In contrast, an involvement-oriented management philosophy implies trust

rather than control and actors are given responsibility and ample scope. The main

objective is long-term performance enhancement (Davis et al. 1997). Like Davis,

Schoorman, and Donaldson, several other researches also refer to the cultural

system as a relevant exogenous factor (e.g. Friedman and Miles 2002; Jones et al.

2007; Reimer 2005). With predominant exogenous factors, decision-making

processes are context-specific (situation- and issue-specific), and thus dynamic.

Although researchers obviously concentrate on various key aspects of decision

situations, most of them agree on the importance of context in determining

managers’ capabilities, abilities, and behavior (e.g. Wicks and Berman 2004;

Freeman and Phillips 2002; Jones et al. 2007).

Likewise there are endogenous factors that determine decision-making behav-

ior. Endogenous factors can be connected to individual characteristics and

interests of decision-makers that cover a wide range of relevant attributes

including the propensity to take risks, tolerance for certainty and ambiguity,

creativity, skills, decision style, need for control, power, experience, education,

and values (Nutt 2005; Tosi et al. 2000). In this context, Davis et al. (1997) focus

on a more psychological point of view and concentrate on three main factors:

motivation, identification, and use of power. Motivation is defined by extrinsic/

intrinsic factors and by lower/higher order needs (e.g. Maslows’s hierarchy (1970)

or the achievement and affiliation needs of McClelland (1975) and McGregor

(1966)). Extrinsically motivated managers, usually have lower order needs.

Identification is related to the individual’s self-image and self-concept. Managers’

behavior depends on how they define themselves in terms of their membership in

the corporation and whether or not they accept the corporation’s mission,

strategies, and objectives. High identification suggests managers are strongly

involved in the corporation’s business and are highly committed (Davis et al.

1997). Highly committed managers are more likely to make decisions in the

interests and for the benefit of the corporation. Finally, the use of power is a

A. Rausch

123

rather important factor that influences managers’ behavior. Managers have

institutional or organizational power by virtue of their position in the corporation.

Personal power, in contrast, is neither affected by position, nor by formal roles in

the corporation. It is inherent in the individual. While personal power is clearly a

personal factor concerning decision-making behavior, institutional power is to

some extent an exogenous factor because certain organizational cultures facilitate

the use of institutional power (Davis et al. 1997). This is supported by Nutt’s

classification (2005) and Mitchell et al. (1997) who use the characteristics power

and legitimacy as independent variables (in contrast to urgency as third criterion)

for identifying salient stakeholders in organizations.

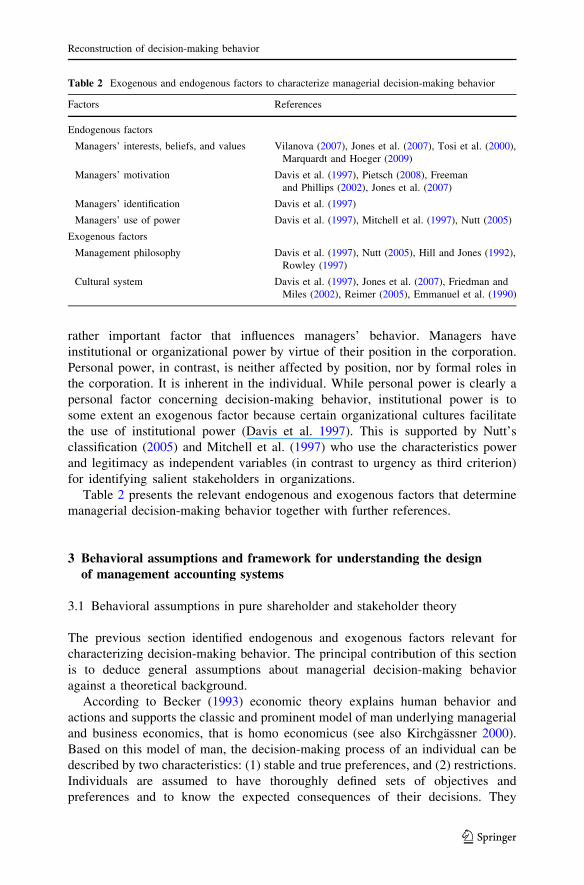

Table 2 presents the relevant endogenous and exogenous factors that determine

managerial decision-making behavior together with further references.

3 Behavioral assumptions and framework for understanding the designof management accounting systems

3.1 Behavioral assumptions in pure shareholder and stakeholder theory

The previous section identified endogenous and exogenous factors relevant for

characterizing decision-making behavior. The principal contribution of this section

is to deduce general assumptions about managerial decision-making behavior

against a theoretical background.

According to Becker (1993) economic theory explains human behavior and

actions and supports the classic and prominent model of man underlying managerial

and business economics, that is homo economicus (see also Kirchgassner 2000).

Based on this model of man, the decision-making process of an individual can be

described by two characteristics: (1) stable and true preferences, and (2) restrictions.

Individuals are assumed to have thoroughly defined sets of objectives and

preferences and to know the expected consequences of their decisions. They

Table 2 Exogenous and endogenous factors to characterize managerial decision-making behavior

Factors References

Endogenous factors

Managers’ interests, beliefs, and values Vilanova (2007), Jones et al. (2007), Tosi et al. (2000),

Marquardt and Hoeger (2009)

Managers’ motivation Davis et al. (1997), Pietsch (2008), Freeman

and Phillips (2002), Jones et al. (2007)

Managers’ identification Davis et al. (1997)

Managers’ use of power Davis et al. (1997), Mitchell et al. (1997), Nutt (2005)

Exogenous factors

Management philosophy Davis et al. (1997), Nutt (2005), Hill and Jones (1992),

Rowley (1997)

Cultural system Davis et al. (1997), Jones et al. (2007), Friedman and

Miles (2002), Reimer (2005), Emmanuel et al. (1990)

Reconstruction of decision-making behavior

123

perceive these objectives and preferences on a utility scale according to degrees of

satisfaction (Kirchgassner 2000; Milgrom and Roberts 1992; Doucouliagos 1994).

Accordingly, individuals make decisions that maximize their utility. Further, they

make rational choices among options at their disposal and within exogenous

restrictions by taking into account different probabilities of occurrence of varied

events (Becker 2003; Kirchgassner 2000). Since preferences are assumed stable,

changes in individual behavior tend to be attributed to exogenous restrictions

(Suchanek 1994). These a priori-assumptions about individuals’ rational behavior

are fundamental to neoclassical economic theory (Hosseini and Brenner 1992) but

are also true for new institutional economics that result from the critical discussion

of neoclassical economic theory (Furubotn and Richter 1991; Welge and Al-Laham

2008). New institutional economics accept the model of man of homo economicus

and the assumptions about methodological individualism and utility maximization

but reject the assumption of unbounded rationality and efficient markets (Welge and

Al-Laham 2008; Furubotn and Richter 1991; Kirchgassner 2000). In contrast, new

institutional economics state that

• individuals have a limited ability to acquire and process information, and

• acquiring and processing information is costly and impedes individuals’

efficiency.

Thus, while decision makers intend to be rational they actually cannot be

completely rational. Simon (1981) uses the term bounded rationality to describe

their behavior. Bounded rationality suggests that individuals are neither omniscient

nor perfectly far-sighted but limited in their cognitive competencies (Williamson

1987). They are unable to anticipate all contingencies because information and

communication are imperfect and costly. Consequently, arbitrarily complex

problems cannot be solved exactly and instantaneously without cost (Milgrom

and Roberts 1992; Williamson 1987) and bounded rationality contracts are, hence,

incomplete. If all actors were completely trustworthy, there could be general

reliance on these incomplete contracts, but, in fact, there are usually actors likely to

be dishonest, guileful, and fraudulent (Milgrom and Roberts 1992; Furubotn and

Richter 1991). Such behavior is known as opportunism. Williamson defines

opportunism as ‘‘self-interest seeking with guile’’ that ‘‘includes but is scarcely

limited to more blatant forms, such as lying, stealing, and cheating. Opportunism

more often involves subtle forms of deceit.’’ (1987). Opportunistic actors actively

pursue their self-interests and therefore aim at optimizing their position by

concluding contracts (Eigler 2004). Self-seeking interests and limits on cognitive

competence characterize the model of the contractual man (Williamson 1987).

Ample scope for opportunistic behavior is, for example, given to actors with more

information at their disposal or who have to bear less costs induced by incomplete

contracts (Moller 2006). Opportunistic actors may disguise preferences, distort data,

deliberately confuse issues etc. in order to achieve their objectives and maximize

utility (Furubotn and Richter 1991). Furthermore, it is assumed that opportunistic

actors are usually extrinsically motivated and primarily respond to material

incentives (Riegler 2000). Since social context does not matter actors as self-

centered individualists have low identification with the corporation and do not care

A. Rausch

123

about inequity that exists among others but are only interested in the fairness of their

own material payoff relative to others’ payoffs (Fehr and Schmidt 1999). While

such self-interest seeking and opportunistic behavior is assumed to maximize

individual utility, it likely damages a corporation’s total utility (Smith 2003).

In research and literature opportunism is often discussed in the context of

shareholder value (e.g. Donaldson and Davis 1991; Davis et al. 1997; Quinn and

Jones 1995; Smith 2003; Vilanova 2007; Hirsch 2007). The reason for this focus

arises from key aspects of shareholder theory: the relationship between owner

(principal) and manager (agent) (Jensen and Meckling 1976; Rappaport 1999). Such

an agency relationship represents a contract under which one or more principals

engage one or more agents to perform some service on their behalf. Through this

some decision-making authority is delegated to the agent (Jensen and Meckling

1976). Thus, shareholders as principals give institutional power to managers as

agents by engaging them to focus only on shareholder interests (i.e. shareholder

value maximization) (Smith 2003; Schmidt and Maßmann 1999). However,

conflicts and opportunistic managerial behavior likely arise from this agency-

relationship because:

• the principal and the agent are both utility maximizers,

• the principal and the agent have partly differing goals and risk preferences,

• there is information asymmetry, and

• it is difficult or expensive for the principal to verify what the agent is actually

doing (Eisenhardt 1989; Jensen and Meckling 1976; Jost 2001).

Since it is impossible for the principal and the agent to ensure at zero cost that the

agent’s decisions maximize the principal’s welfare, there will always be agency

costs consisting of monitoring and bonding costs as well as a residual loss (Jensen

and Meckling 1976). For this reason, it can be assumed that in shareholder oriented

corporations characterized by pure agency relationships between shareholders and

managers as well as self-interest and bounded rationality (Eisenhardt 1989),

opportunistic behavior is very likely.

However, the assumption that decision makers are always susceptible to

opportunistic behavior, e.g., to lie, cheat, steal, shirk, etc., and that they exclusively

pursue their material self-interests and do not care about others or social goals

(Barney 1990; Fehr and Schmidt 1999), is too simplistic and does not entirely match

reality. Critics claim that the model of man underlying agency-theory is too narrow

(Davis et al. 1997). They believe that while economic models like the model of the

homo economicus might be well suited for mathematical modeling, because they

are simple and elegant, they induce an unrealistic description of human behavior

(Fehr and Schmidt 1999; Jensen and Meckling 1994). Sociological and psycholog-

ical perspectives, in contrast, clearly state individuals actually show a willingness

and ability to behave in a wide range of behaviors other than merely opportunistic

(Davis et al. 1997; Moller 2006; Pietsch 2008; Jones 1995; Barney 1990).

Williamson (1987) for instance has distinguished the contractual man of capitalist

economics from the new man of socialist economics endowed with a high level of

cognitive competence and a greater predisposition to cooperation. In contrast to the

model of the homo economicus this new or ‘‘modern’’ model of man influenced by

Reconstruction of decision-making behavior

123

sociology and psychology considers polycentric preference structures and differ-

ences in personality as well as profit-interdependencies which imply that wealth or

disadvantages occurring to one actor have direct impact on another actor’s utility

(Pietsch 2008). Likewise, Fehr and Schmidt (1999) also find many examples which

predict decision-making managers are more cooperative than assumed by economic

theory and that they are driven by fairness considerations. In this view actors are

anxious to maximize the aggregate utility of the corporation and make decisions

allocating organizational resources at the best possible rate for the whole

corporation. Such collective-serving managers who achieve utility through orga-

nizational achievement follow the model of the self-actualizing man (Davis et al.

1997). Self-actualizing men do not exclusively seek personal wealth, status, leisure,

and the like, but there exist multiple values and multiple choice processes involving

one or more choice dimensions (Hosseini and Brenner 1992; Donaldson 1990).

Thus, Wood and Bandura identify a much larger range of human motives than found

in economic theory, including needs for achievement, responsibility, and recogni-

tion, as well as altruism, belief, and respect for authority (Wood and Bandura 1989).

Self-actualizing men are, thus, likely to be organization centered, altruistic and

trustworthy. They usually show high involvement and value commitment that result

in a merging of individual ego and corporate prestige (Davis et al. 1997; Donaldson

and Davis 1991). Since individual self-esteem and corporate prestige are

interwoven, self-actualizing men carry out courses of action from a sense of duty

even if they are personally unrewarding (Etzioni 1968; Donaldson and Davis 1991).

That is why self-actualizing men are motivated by a need to gain intrinsic

satisfaction through successful performance of inherently challenging work and why

non-financial motivators are more likely to be effective (Pietsch 2008; Donaldson

and Davis 1991). As there is no inherent, general problem of managers’ motivation

(Donaldson and Davis 1991), individual calculative actions by managers will

always be driven to achieve highest rewards for the entire corporation. In this

context, Reynolds et al. (2006) argue that there is a socio-psychological basis for the

assumption that managers are naturally inclined to balance interests and resources,

for example among all stakeholders in an organization. This natural inclination

towards altruism and hedonism (Homans 1972) differentiates sociological and

psychological approaches fundamentally from economic theory. Supporting this

point of view sociologists and psychologists also argue that human behavior is often

produced without conscious thought but through habit, emotion, taken-for-granted

custom, conditioned and unconditioned reflex, and unconscious desires (Donaldson

1990). Consequently, managers are not necessarily viewed as individuals with the

inherent propensity to shirk, to be opportunistic, and to act with guile.

While opportunistic behavior is usually associated with pure shareholder theory,

the abovementioned collective-serving, altruistic behavior of a self-actualizing man

is more likely to be associated with pure stakeholder theory (Vilanova 2007; Scott

and Lane 2000). In pure stakeholder oriented corporations managers are not meant

to mobilize or manipulate stakeholders in an exploitative sense (Post et al. 2002b)

but to be concerned with traditional moral values consisting of obligation, duty,

honesty, respect, fairness, equity, care and assistance (Clarkson 1995; Jones et al.

2007). Quite contrary to self-interests and egoism, pure stakeholder theory cares

A. Rausch

123

about social matters and assumes shared attitudes and values while concentrating on

various claims of multiple stakeholders (Hosseini and Brenner 1992). In this

context, managers’ obligations primarily do not derive from explicit contracts

between shareholders and themselves but from implicit social contracts between the

corporation and society. Thus, it is implicit stakeholder claims and moral principles

that guide management strategy and managerial decisions rather than explicit,

legally specified, agency obligations to shareholders (Quinn and Jones 1995;

Cornell and Shapiro 1987). That is also why managers in purely stakeholder

oriented corporations achieve their goals and satisfaction not only from their

position in the organization but from their personality and personal power (Davis

et al. 1997). With these considerations about contracts among all stakeholders in a

corporation it is recognized that managers’ role and position in stakeholder oriented

corporations is different from shareholder oriented corporations. While agency-

relationships between managers and shareholders are characteristic and fundamental

in pure shareholder theory, relationships are formed as a nexus in stakeholder

oriented corporations (Freeman and Phillips 2002; Post et al. 2002a; Vilanova 2007;

Fama 1980). Thus, against the background of the model of self-actualizing man

agency-conflicts are actually irrelevant in pure stakeholder theory. Hence, the

principal challenges concerning managerial decision-making behavior in purely

stakeholder oriented corporations result from complex, dynamic, and reciprocal

interactions among managers and all other stakeholders (Scott and Lane 2000).

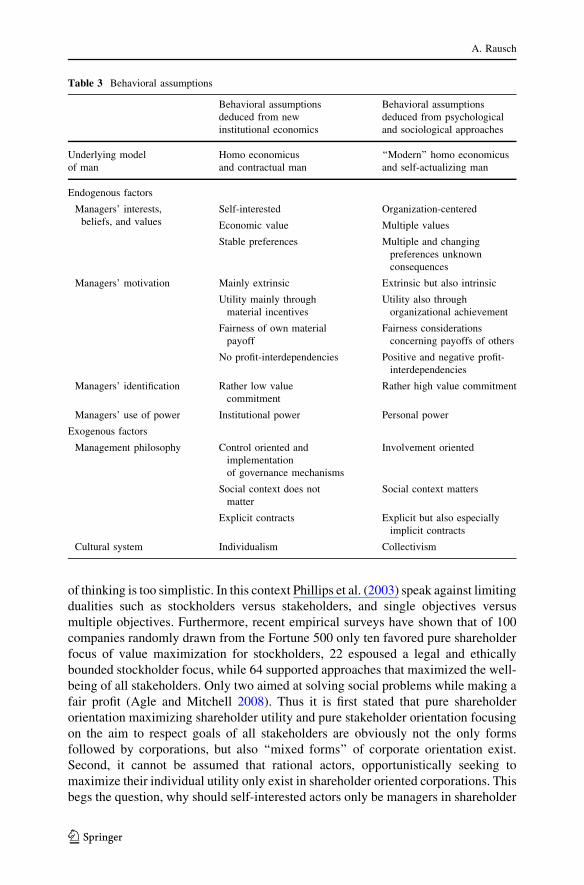

Summarizing the theoretical background and behavioral assumptions elaborated

in this section, two principal findings can be clearly deduced. First, various

theoretical points of view and models of man exist in research and literature to

support behavioral assumptions. Second, behavioral assumptions are different in

shareholder and stakeholder theory. As new institutional economics is based on the

same basic assumptions as economic theory, even when accepting human behavior

in a broader sense, there are, in fact, two sets of behavioral assumptions of

individuals deduced from these theoretical considerations. In Table 3 these two sets

are summarized and structured according to the previously identified factors.

As outlined above, one might be tempted to put the title ‘‘shareholder theory’’ on

the left column and the title ‘‘stakeholder theory’’ on the right column. A thorough

literature review, however, reveals such black and white thinking is not appropriate.

More recently shareholder and stakeholder theory have been intensely discussed,

called into question, partly rejected and refined. For this reason, behavioral

assumptions underlying these two theories likely changed as well. In the following

chapter these ‘‘modified’’ or ‘‘new’’ approaches to shareholder and stakeholder

theory resulting from discussions in literature and research are briefly presented.

3.2 Behavioral assumptions in ‘‘new’’ approaches to shareholder

and stakeholder theory

At first sight it might sound logical to identify managerial behavior in shareholder

theory with behavioral assumptions deduced from new institutional economics, and

managerial behavior in stakeholder theory with behavioral assumptions deduced from

psychological and sociological approaches. A closer look reveals, however, this type

Reconstruction of decision-making behavior

123

of thinking is too simplistic. In this context Phillips et al. (2003) speak against limiting

dualities such as stockholders versus stakeholders, and single objectives versus

multiple objectives. Furthermore, recent empirical surveys have shown that of 100

companies randomly drawn from the Fortune 500 only ten favored pure shareholder

focus of value maximization for stockholders, 22 espoused a legal and ethically

bounded stockholder focus, while 64 supported approaches that maximized the well-

being of all stakeholders. Only two aimed at solving social problems while making a

fair profit (Agle and Mitchell 2008). Thus it is first stated that pure shareholder

orientation maximizing shareholder utility and pure stakeholder orientation focusing

on the aim to respect goals of all stakeholders are obviously not the only forms

followed by corporations, but also ‘‘mixed forms’’ of corporate orientation exist.

Second, it cannot be assumed that rational actors, opportunistically seeking to

maximize their individual utility only exist in shareholder oriented corporations. This

begs the question, why should self-interested actors only be managers in shareholder

Table 3 Behavioral assumptions

Behavioral assumptions

deduced from new

institutional economics

Behavioral assumptions

deduced from psychological

and sociological approaches

Underlying model

of man

Homo economicus

and contractual man

‘‘Modern’’ homo economicus

and self-actualizing man

Endogenous factors

Managers’ interests,

beliefs, and values

Self-interested Organization-centered

Economic value Multiple values

Stable preferences Multiple and changing

preferences unknown

consequences

Managers’ motivation Mainly extrinsic Extrinsic but also intrinsic

Utility mainly through

material incentives

Utility also through

organizational achievement

Fairness of own material

payoff

Fairness considerations

concerning payoffs of others

No profit-interdependencies Positive and negative profit-

interdependencies

Managers’ identification Rather low value

commitment

Rather high value commitment

Managers’ use of power Institutional power Personal power

Exogenous factors

Management philosophy Control oriented and

implementation

of governance mechanisms

Involvement oriented

Social context does not

matter

Social context matters

Explicit contracts Explicit but also especially

implicit contracts

Cultural system Individualism Collectivism

A. Rausch

123

oriented corporations and self-actualizing actors only in stakeholder oriented

corporations? This question was also asked by several researchers who developed

two corresponding, intensively discussed and frequently criticized theories:

• Stewardship theory and

• Stakeholder agency theory.

Stewardship theory has its roots in psychology and sociology (Davis et al. 1997).

It has been proposed as an alternative to agency theory, although it is also subject to

criticism as it is based on some extreme and sometimes unrealistic assumptions

(Donaldson and Davis 1991; Grundei 2008). The key parameter of stewardship

theory was investigated by Donaldson when he realized that the rational economic

model of man pursuing self-interests and maximizing personal utility was too

narrow to explain human behavior in organizations. Donaldson (1990) concluded

there exists a much larger range of human motives. Therefore, behavioral

assumptions originally based on economic theories and new institutional economics

need to be revised. According to stewardship theory, the principal goal of the

company is shareholder value maximization just as in shareholder theory (for

shareholder wealth maximization as principal goal of managerial stewards see also

Jones et al. 2007). However, steward-managers are not supposed to be strictly self-

interested. Stewards want to be protectors of the corporate assets and are far from

opportunistic shirkers (Donaldson and Davis 1991), given their moral bend.

According to Jones, moral individuals are honest, have personal integrity, don’t lie,

cheat, or steal, and honor their commitments (Jones 1995). Thus, managerial

stewards are assumed to be loyal, reliable, diligent, and dependable in protecting

and advancing shareholder interests (Jones et al. 2007). If stakeholder interests vary

from shareholder interests, a steward is motivated to make decisions that are in the

best interest of all groups. From this point of view, stewardship theory seems to be

similar to stakeholder theory. Actually, however, it is closer to shareholder theory as

moral stewards do not regard stakeholder interests as ends (like in stakeholder

theory) but rather consider the interests of non-shareholder stakeholders only in an

instrumental sense to achieve the aim of shareholder utility maximization. In

contrast to stakeholder theory, steward-managers have no moral commitment to

other stakeholders but are only shareholders’ fiduciaries (Jones et al. 2007). There

are, though, no agency-conflicts like in pure shareholder theory. Thus, even if the

interests of the shareholder and the manager are not aligned there will not be an

agency problem because the manager, as a steward of the shareholder, will place

higher value on cooperation than defection. Nevertheless, the manager’s decisions

and behavior are considered rational because, as a steward, he/she perceives greater

utility in cooperative, collectivist, and pro-organizational behavior as compared to

self-interest seeking (Davis et al. 1997). In summary it can be said that in

stewardship theory the purpose of the corporation is shareholder value maximiza-

tion and steward-managers are fiduciaries of shareholders. However, due to their

individual characteristics steward-managers do not necessarily act opportunistically

but show a wide range of behavior.

While stewardship theory focuses on the bilateral relationship between share-

holders and managers without recognizing agency problems, stakeholder agency

Reconstruction of decision-making behavior

123

theory focuses on a nexus of contracts between multiple stakeholders while

recognizing a wide range of agency-relationships (Jost 2001; Hill and Jones 1992;

Ruhli and Sachs 2003; Jones 1995). Since Hill and Jones (1992), who first

elaborated the stakeholder agency approach, take agency theory and stakeholder

theory as points of departure, it is quite obvious that behavioral assumptions drawn

from pure shareholder and pure stakeholder theory need to be revised in the context

of stakeholder agency theory. A decisive point here is the paradigm of stakeholder

agency theory that encompasses implicit and explicit contractual relationships

between all stakeholders (Hill and Jones 1992). These contracts represent various

exchange relationships between stakeholders and the corporation and establish

legitimate stakeholder claims on the corporation in the sense of Freeman’s

stakeholder approach (1984). Each stakeholder group contributes critical resources

to the corporation and in turn expects its interests to be satisfied (March and Simon

1958). Thus, the corporation’s purpose is to meet stakeholders’ interests and claims.

Concerning the role and behavior of decision-making managers in this network, two

facts must be considered. First, managers are assigned the difficult task of balancing

conflicting stakeholder interests and claims to achieve a co-operative solution for

the entire corporation (Hill and Jones 1992). Since managers are the only group of

stakeholders who enter into contractual relationships with all other stakeholders and

who have direct control over the decision-making apparatus of the corporation

(Jones 1995; Rowley 1997; Hill and Jones 1992), they can be seen as agents of all

other stakeholders. Second, managers are assumed to maximize a utility function

that includes remuneration, power, job security, and status what can be achieved

through increasing growth of the corporation (Hill and Jones 1992). Since there are

also other stakeholder claims such as shareholder claims for return on investment,

employee claims for higher wages, consumer claims for higher quality and/or lower

prices, supplier claims for lower prices and/or more stable ordering patterns etc.,

agency-conflicts arise (Hill and Jones 1992) and with managers pursuing their own

interests at the expense of other stakeholders opportunistic behavior becomes

apparent (Jones 1995; Jones et al. 2007). Even if managers make decisions for the

benefit of one or more stakeholder groups, they inevitably ignore interests of less

salient stakeholders who, as a consequence, are worse off. Which particular

stakeholders in this network of relationships are important and merit management

attention, strongly depends on managers’ perception, environmental scanning

practices, and values (Mitchell et al. 1997; see also Post et al. 2002a). The

difference between the utility that stakeholders achieve if managers act in

stakeholders’ best interests, and the utility that is achieved if managers act in their

own best interests can be referred to as a utility loss (Hill and Jones 1992). Thus, if

interests are not aligned, there will be a utility loss. In summary it can be said that in

stakeholder agency theory the purpose is to maximize value for the entire

corporation and to respect legitimate claims of all stakeholders. Although managers

have fiduciary duties only to shareholders, they also have non-fiduciary duties to all

stakeholders due to implicit and explicit contracts. Furthermore, managers are

assumed to have individual interests. Thus, they will always face a trade-off either

between conflicting claims of other stakeholders or between their own utility

function and others’ claims. When pursuing their individual utility function or

A. Rausch

123

legitimate claims of particular stakeholder groups, managers likely act opportunis-

tically what might make other stakeholders (including shareholders) worse off.

For the behavioral assumptions outlined in this section it is well understood that

management accounting support is highly recommended to ensure ‘‘good’’ decision-

making, but it is also obvious that the appropriate design of management accounting

systems is a big challenge.

3.3 Framework for understanding the design of management accounting

systems

In this section a framework for understanding the design of management accounting

systems is created. The framework is based on the findings of the previous sections

and cautions against too ready acceptance of conventional wisdom and common

statements about shareholder and stakeholder theory. For this purpose it is taken

into account that.

• behavioral assumptions deduced from new institutional economics are not only

true for managerial decision-making in shareholder theory, but also in

stakeholder theory,

• behavioral assumptions grounded in psychological and sociological approaches

are not exclusively relevant to managerial decision-making in stakeholder

theory, but also in shareholder theory,

• there exist further approaches to provide a basis for explaining managerial

decision-making behavior: stewardship theory and stakeholder agency theory.

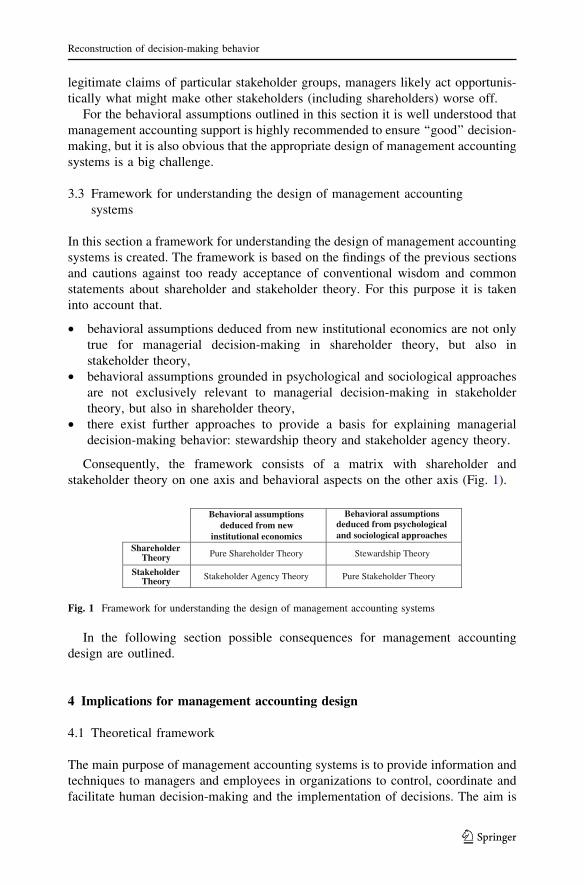

Consequently, the framework consists of a matrix with shareholder and

stakeholder theory on one axis and behavioral aspects on the other axis (Fig. 1).

In the following section possible consequences for management accounting

design are outlined.

4 Implications for management accounting design

4.1 Theoretical framework

The main purpose of management accounting systems is to provide information and

techniques to managers and employees in organizations to control, coordinate and

facilitate human decision-making and the implementation of decisions. The aim is

deduced from new institutional economics

Behavioral assumptions deduced from psychological and sociological approaches

Shareholder Theory Pure Shareholder Theory Stewardship Theory

Stakeholder Theory Stakeholder Agency Theory Pure Stakeholder Theory

Behavioral assumptions

Fig. 1 Framework for understanding the design of management accounting systems

Reconstruction of decision-making behavior

123

to improve the decision-makers’ ability to make organizationally desirable decisions

and to achieve organization’s goals and objectives (Horngren et al. 2006; Verstegen

2006). It is assumed that management accounting systems herein have two

important roles (Zimmerman 2009; Ewert and Wagenhofer 2008; Demski and

Feltham 1976):

(1) decision facilitation of information (decision-facilitating role) and

(2) decision influence of information (decision-influencing role).

Decision facilitation of information refers to management accounting as a pure

pre-decision information provider without taking into account any goal conflicts.

There is either only one actor involved in the decision-making or organizational

structures are regarded sufficient to ensure the compatibility of divergent goals

(Ewert and Wagenhofer 2008). Decision influence of information focuses on

supporting decision-making when more than one actor is involved and goal conflicts

and information asymmetries exist. This is usually the case when the corporate

structure is characterized by the separation of ownership from decision-making

management, and when decision-makers are decentralized (Wall 2009; Eigler 2004;

Grundei 2008; Tosi et al. 2003). In such a situation management accounting systems

are expected to motivate individuals and mitigate the divergence of interests and

goals (Ewert and Wagenhofer 2008; Sußmair 2004; Zimmerman 2009; Sprinkle

2003) and, thus, to assist in achieving the basic mission of the corporation, whatever

that may be (Hansen and Mowen 1994). In this paper, shareholder value

maximization and value maximization for all stakeholders are regarded as relevant

basic missions of the corporation.

Before continuing this discussion of management accounting systems in more

detail, it should be considered which of the above mentioned roles of management

accounting is required against the background of behavioral assumptions and

corporate goals outlined in previous sections of this paper. In each of the four fields

of the matrix in Fig. 1 there is obviously more than one actor. In the case of

shareholder value orientation there are shareholders as principals and decision-

making managers as agents. Assuming the model of man of homo economicus/

contractual man we recognize from a wide literature base that there exist

information asymmetry as well as goal conflicts (e.g. Eisenhardt 1989; Jensen

and Meckling 1976; Fama 1980; Jost 2001). Thus, management accounting

systems’ role in pure shareholder theory is decision facilitation and especially

decision influence of information because interests must be aligned and opportu-

nistic behavior must be limited. In contrast, assuming the ‘‘modern’’ homo

economicus/self-actualizing man as the underlying model of man in stewardship

theory goal conflicts between shareholders and managers need not be taken into

account. The reason for this is that stewards’ goals and objectives are always

aligned with the relevant corporate purpose which is shareholder value maximi-

zation. Although stewards act only in the best interests of shareholders and do not

intentionally pursue subjective preferences (Donaldson 1990), it can be alleged that

behavioral aspects are not completely irrelevant, because stewards are moral in

nature and collectivist-serving and thus, they may not be completely unconcerned

with stakeholders’ interests (Davis et al. 1997). However, this does not concern the

A. Rausch

123

decision influence of information but only the decision facilitation of information.

Consequently, when designing management accounting systems in stewardship

theory the focus must be on the decision facilitation of information.

In the case of stakeholder value orientation there are managers as agents and

shareholders as principals but also other stakeholder groups with divergent goals

and objectives who have legitimate claims on the corporation (Freeman 1984;

Friedman and Miles 2002). Against the background of stakeholder agency theory it

is quite obvious that decision facilitation as well as decision influence of

information must be considered when designing management accounting systems.

The importance of the decision facilitation of information results from the wide

range of interdependencies and links concerning resources, risks, performance etc.

(Ewert and Wagenhofer 2008), especially when multiple parties of interest are

involved. The reasons for the importance of the decision influence of information

are two-fold. First, according to the underlying model of man decision-making

managers are assumed to be self-interested agents maximizing individual utility.

Since managers must respect multiple stakeholder claims that are not very likely

aligned either between stakeholder groups themselves or with managers’ individual

interests goal conflicts may be unavoidable. Thus, due to these conflicts between

managers and all other stakeholders Carney et al. (2010) recommend agency-driven

governance. Secondly, as pointed out in Sect. 3 of this paper, managers hold a

central position in this nexus of stakeholder groups and thus likely dispose of more

information than any other stakeholder group. For this reason, an information

asymmetry exists between managers and stakeholders (Hill and Jones 1992). Both

arguments goal conflicts and asymmetric information clearly indicate that

management accounting systems must be designed to control managers’ decisions

in the best interest of all stakeholders. Consequently, decision influence of

information must be paid particular attention.

In contrast to stakeholder agency theory pure stakeholder theory ignores agency-

relationships (Phillips et al. 2003) and alleges managers to be self-actualizing men

who do not exclusively seek personal wealth and individual interests (see Sect. 3).

In fact, with these behavioral assumptions no decision influence of information is

necessary because managers will always decide in the best interest of all

stakeholders. Nonetheless it must be considered that benevolent agent-managers

with particular competencies and authorities will not be indifferent towards a fair

allocation of resources (Ewert and Wagenhofer 2008) or towards the distribution of

joint gains among multiple parties of interest (Kochan and Rubinstein 2000), even if

they do not intentionally pursue individual interests. However, since these managers

are assumed to be moral in nature they will neither exploit any stakeholder group

nor take advantage of any information asymmetries that likely exist due the

manager’s central position (Rowley 1997). Thus, when designing management

accounting systems in pure stakeholder theory the focus must be on decision

facilitation of information with the key tasks of coordination, cooperation, and

conflict resolution among various stakeholder groups (Carney et al. 2010).

The following sections of this paper focus on the question of what should be the

proper management accounting systems to take and how they can be developed to

meet specific requirements of the decision-facilitating and/or decision-influencing

Reconstruction of decision-making behavior

123

role that result from particular behavioral assumptions and the purpose of the

corporation.

4.2 Implications for the decision-facilitating role of management accounting

systems

The decision-facilitating role of management accounting systems refers to the

provision of information to support human decision-making and to reduce pre-

decision uncertainty in a particular decision context (Demski and Feltham 1976;

Chong 1996; Sprinkle 2003; Horngren et al. 2006). The intention is to improve

managers’ and employees’ knowledge and to enhance their ability to make

organizationally desirable judgments and decisions as well as better-informed action

choices (Sprinkle 2003; Ewert and Wagenhofer 2008). Consequently, primary

research questions in this field deal with the amount, type, and quality of

information supplied to managers and employees who in turn make judgments and

decisions based on this information (Wouters and Verdaasdonk 2002; Sprinkle

2003). Furthermore, research is concerned with evaluating the determinants of

decision quality and the benefits and costs of the provision of information (Sprinkle

2003). The decision-facilitating role is optimally fulfilled if there is a balanced fit of

information needs and demand of information by decision-making managers and the

supply of information by management accounting systems (Gladen 2008). If there is

not enough and appropriate information ex ante, uncertainty in decision-making is

not sufficiently reduced. Hence, a mismatch of managers’ needs, demands,

capabilities, and competences (determined by endogenous and exogenous factors

as described in Sect. 3.1 of this paper) on the one hand and the management

accounting system on the other induces unfavorable consequences in decision-

making (Chong and Eggleton 2003).

Below it is discussed what implications for the design of management accounting

systems with regard to their decision-facilitating role can be deduced from the two

sets of behavioral assumptions elaborated in Sect. 3 and the purpose of the

corporation. Before starting the discussion, two general limitations must be made.

While management accounting systems might provide any type, quality, and

amount of information, the decision facilitation of information is restricted by (1)

individuals’ limited ability to acquire and process information (Furubotn and

Richter 1991; Kirchgassner 2000; Weber et al. 2004; Welge and Al-Laham 2008),

and (2) information costs (Wall 2006; Atkinson et al. 1995; Weber and Schaffer

2008). As these limitations are recognized in all four theoretical approaches

elaborated in Sect. 3 they are not explicitly taken into account throughout the

following discussion. Consequently, it is only questioned what type, quality, and

amount of information management accounting systems provide against the

background of the two sets of behavioral assumptions and what has to be

additionally considered due to the particular purpose of the corporation. Thus, the

remainder of this section is structured as follows: First, the impact of behavioral

assumptions based on the model of the homo economicus/contractual man is

analyzed. By doing so it is also discussed whether there are differences between

shareholder and stakeholder orientation. Afterwards the discussion proceeds to the

A. Rausch

123

model of the ‘‘modern’’ homo economicus/self-actualizing man and again the

impact of the corporation’s particular purpose is taken into consideration.

Recall, decision-making managers corresponding with the model of homo

economicus/contractual man are alleged to be self-interested and to opportunisti-

cally maximize their individual utility. Thus, it can be assumed that they use

information for their own benefit and, should the occasion arise, disguise and distort

information. Management accounting systems, hence, are not only asked to provide

information in favor of the shareholders or of all stakeholders, respectively, but also

to verify that manager’s use and respect this information in their decisions. Since the

model of the homo economicus/contractual man implies that decision-making

managers are interested in their own utility and fairness of their own material

payoff, they likely show low commitment to the corporation, demand only monetary

data and exclusively pursue monetary objectives (Davis et al. 1997; Agle et al.

2008). Accordingly, traditional management accounting information has been

financial (Atkinson et al. 1995). In fact, in pure shareholder theory no other

information is required because corporate philosophy focuses on profitability and

shareholder maximization. Thus, management accounting information is alleged to

primarily be concerned about economic value, profit maximization, shareholder

returns, financial performance, and clear quantifiable outcomes (Vilanova 2007;

Shleifer and Vishny 1997; Jensen 2001; Weißenberger 2009; Hansen and Mowen

1994). Objectives directed toward environmental, social, ethical, and religious

issues etc. are more or less ignored when the corporation’s purpose is shareholder

value maximization (Agle et al. 2008; Weißenberger 2009). Managers would either

not use information concerning these objectives or abuse it to promote their own

interests. Management accounting systems, thus, had best not focus exclusively on

managers’ demand of information, but rather ensure high transparency throughout

the entire corporation and provide information as completely as possible.

Consequently, although management accounting systems are basically targeted

towards internal constituencies such as managers, executives and employees

(Atkinson et al. 1995), it might be worth considering providing information to

shareholders beyond financial accounting information. Similar considerations can

be made when the corporation’s purpose is value maximization for all stakeholders.

Although self-seeking and opportunistic managers will not care about stakeholders’

claims or try to balance them, management accounting systems nevertheless have

the duty to provide information as completely as possible. It is somehow obvious

that type and quality of information provided by management accounting systems

must be different depending on the number and variety of interests, objectives, and

legitimate claims. Against the background of value maximization for all

stakeholders, however, decision facilitation of information is much more complex.

Since there are multiple stakeholder groups with different interests and character-

istics, it must be assumed that a wide range of information concerning type and

quality will be necessary (Chong and Eggleton 2003). Thus, management

accounting systems face the challenge to record, measure, and present manifold

and especially qualitative information (Carney et al. 2010). Additionally, in some

areas of stakeholder interests and claims there might exist measures and

corresponding accounting tools for the purpose of documentation, planning and

Reconstruction of decision-making behavior

123

control, but in general it can be assumed that they are scarce and rarely implemented

(Wall 2009; Colakoglu et al. 2006). Furthermore, when providing information it

might be worth considering all stakeholders for whom managers make decisions

and, thus, increase transparency. Some researchers believe that a greater amount of

detailed and accurate information always results in better decisions provided

information costs are ignored (Sprinkle 2003). However, following the model of the

homo economicus/contractual man in pure shareholder theory and stakeholder

agency theory, self-seeking managers likely use additional information not only for

making better decisions or decisions in the owners’ or stakeholders interests,

respectively, but also to exploit their edge on information and to maximize their

individual utility function. Thus, with decision-makers as self-interested agents,

higher amounts of information and a higher level of accuracy and variety may result

in an increase of information asymmetry. Greater information asymmetry, hence,

induces typical agency-conflicts such as adverse selection and moral hazard.

Consequently, regardless of the purpose of the corporation management accounting

systems must be aware of this trade-off and the high risk to encourage opportunistic

behavior when providing information (Schiller 2001; Wall 2006; Baiman and

Sivaramakrishnan 1991).

When underlying the model of the ‘‘modern’’ homo economicus/self-actualizing

man in stewardship theory and pure stakeholder theory, the fundamental question

concerning the decision facilitation of information is in fact, ‘‘what information do

managers need to decide in the best interest of shareholders and stakeholders,

respectively?’’ In stewardship theory decision-making managers have only fiduciary

duties towards shareholders. Since steward-managers are furthermore moral in

nature and trustworthy, requirements placed on management accounting systems

remain largely manageable. Stewards are alleged to use only relevant information

for meeting shareholder interests. Consequently, the higher the quality and amount

of management accounting information, the better will be their decisions. Stewards

would never abuse any surplus or discriminating information. Consequently,

management accounting systems make a greater contribution when they provide

sufficient information to stewards and support empowering governance structures

and mechanisms. Pro-organizational actions are best facilitated when corporate

governance structures give stewards high authority and discretion (Davis et al.

1997). Furthermore, organizational structures are ideally consulting-oriented instead

of control-oriented and relationships between owners and managers are usually

personal (Velte 2010). For shareholder value maximization a steward’s autonomy

must be deliberately extended and owners must meet stewards on a high level of

trust that, without doubt, might be risky for owners (Davis et al. 1997; Donaldson

and Davis 1991).

Regarding pure stakeholder theory there are two fundamental challenges imposed

on management accounting systems. First, since responsibility for all stakeholders is

the core of a stakeholder oriented corporate philosophy and collective-serving

managers really do care about this corporate goal, management accounting systems

simply must focus on multiple values and explicitly on social context. However, due

to multiple stakeholders with different and probably changing characteristics,

interests and claims, high complexity and/or multiple interdependencies exist.

A. Rausch

123

In such complex and dynamic decision-situations a broader scope information is

required not only to increase transparency for non-decision-making stakeholders,

but to directly support decision-making managers (Chong and Eggleton 2003).

Since ideally all possible factors must be included and also qualitative information

must be provided (Carney et al. 2010), the challenge to record, measure, and present

this wide range of information is now even greater and urgent. However, since there

are manifold areas of stakeholder interests, it is problematic to measure all relevant

dimensions of performance and to capture or verify them with equal precision

(Sprinkle 2003). Although some rather isolated measures and corresponding

accounting tools might be highly-informative for one particular area of stakeholder

interests and claims or task, they reflect only a selective part of the whole

stakeholder network as there are obvious parallels to the multi-tasking problem

which stems from agency-theory (Gladen 2008). Consequently, it can be assumed

that managers only pay attention to those tasks or, in the case of multiple

stakeholders, to those stakeholder claims that get measured (Agle et al. 2008). This

corresponds with common wisdom in management and management accounting:

‘‘what is measured gets done’’, and once one begins to measure something, many

other things do not get captured (Agle et al. 2008). Thus, when providing probably

incomplete or incorrect accounting information, measures, and tools management

accounting systems and management accountants could be blamed for biasing and

distorting decision-making.

The second big challenge for management accounting systems in pure

stakeholder theory is to resolve the goal conflicts between multiple stakeholders

and, thus, to balance divergent interests. Collective-serving managers are really

interested in balancing stakeholder interests and maximizing value for all

stakeholders. Thus, managers’ duty towards multiple stakeholders requires a

process of assessing, weighting, and addressing the competing stakeholder claims

(Reynolds et al. 2006). However, Phillips et al. (2003) argue that there is neither an

established definition of what value maximization for all stakeholders actually is nor

an algorithm for day-to-day managerial decision-making given multiple stakeholder

groups with multiple interests. Furthermore, Sundaram and Inkpen (2004) as well as

Jensen (2001) state that these requirements imposed by many stakeholder theorists

can be met neither by managers nor by management accountants because having

more than one objective function makes governing difficult, if not impossible. The

requirements placed on management accounting systems in this context are even

more exacting when taking into account four further assumptions. First, each

company faces a different set of stakeholders and a complex array of multiple and

interdependent relationships (Rowley 1997). This suggests that stakeholder claims

and values might depend on the specific situation of a company and therefore

management accounting tools might not be generalizable. Secondly, it is rather

impossible to objectively estimate the salience of stakeholder groups and weigh

divergent interests against each other without being exposed to the influence of

decision-makers’ subjective perception (Reynolds et al. 2006). Thirdly, stakeholder

groups presumably do not have the same value for and influence on the company

throughout the organizational life-cycle but their salience changes in time (Mitchell

et al. 1997; Jawahar and McLaughlin 2001). Thus, management accounting systems

Reconstruction of decision-making behavior

123

have to be sort of dynamic regarding what is critical with respect to practicability as

well as cost benefit analysis. Finally, interests and objectives might not be

homogenous within a particular stakeholder group. Consequently, even if manage-

ment accounting systems are successfully applied to balance interests of stakeholder

groups, meeting all interests and objectives would again be impossible, when

differentiation within stakeholder groups (e.g. different classes of employees,

different levels of bondholders, different community groups) exists (Carney et al.

2010).

While some researchers argue that formalizing stakeholder relationships and goal

conflicts is an important task for management accounting and management,

respectively, in the future (Littkemann and Derfuß 2009), other researchers criticize

this position suggesting that in such models managerial wisdom and judgments are

replaced with a false sense of mathematical precision (Phillips et al. 2003). Such

critics are of the opinion that managers should stop waiting for some kind of

‘‘invisible hand’’ and rather focus their own attention on conflict resolution between

(primary) stakeholder groups with ethical judgment and choice. In this domain of

moral principles and ethical performance managers must deal directly with fairness,

justice, and even truth (Clarkson 1995). This would actually lie in the nature of the

‘‘modern’’ homo economicus/self-actualizing man; but when relying on subjective

perception and intuition decision-making managers are at risk of experiencing a

moral dilemma. Since they are moral in nature, personally involved and highly

committed, they do not want to deliberately discriminate against any stakeholder

group and thus, are likely stressed by moral trade-offs between stakeholder groups.

The risk of a moral dilemma actually increases the more detailed and accurate

management accounting information is at the managers’ disposal. On the other

hand, however, a greater amount of information likely provides a holistic view and

as the ‘‘modern’’ homo economicus and self-actualizing man is collectivist-serving

he/she likely uses the information in the best interest of the company. In contrast,

having too little access to appropriate information limits the ability to make

organizationally desirable judgments and decisions. Even if managers want to act in

the best interest of the company and fulfill the company’s overall objectives, they

cannot because they do not have necessary and sufficient information. Thus, they

likely ignore unconsciously and unintentionally certain stakeholders, interests and/

or objectives. Furthermore, stakeholders others than managers (including also

shareholders) may take advantage of the collectivist-serving but under-informed

decision-making managers and abuse management accounting information to

promote their own interests and influence decisions in their own interests (Rowley

1997). In the end, management accountants need experience and sure instinct when

providing information and they must keep management accounting systems flexible

and situation specific.

4.3 Implications for the decision-influencing role of management accounting

systems

The decision-influencing role of management accounting systems can be viewed as

the use of information to reduce post-decision uncertainty. Its intention is to

A. Rausch

123

influence managerial decision-making behavior via the effects that monitoring,

measuring, evaluating, and rewarding actions and performance have on motivation

(Sprinkle 2003; Ewert and Wagenhofer 2008). The aim is to align interests

primarily between legitimate claimants of a corporation and decision-making

managers and to ensure that all actions and decisions serve the corporation’s

purpose (Atkinson et al. 1997; Lambert 2001; Sprinkle 2003). Below it is discussed

what consequences for the design of management accounting systems with regard to

their decision-influencing role can be deduced from behavioral assumptions

elaborated in Sect. 3.

As outlined in Sect. 4.1, when underlying behavioral assumptions deduced from

the model of the ‘‘modern’’ homo economicus/self-actualizing man goal conflicts

between decision-making managers and shareholders or other stakeholders as well

as information asymmetry are ignored. In the absence of agency-conflicts there are

no inherent problems of executive motivation and, hence, no decision influence of

information is necessary in pure stakeholder theory and stewardship theory. Rather