neither shareholder nor stakeholder management

TRANSCRIPT

doi:10.1016/j.emj.2007.01.002

European Management Journal Vol. 25, No. 2, pp. 146–162, 2007

� 2007 Elsevier Ltd. All rights reserved.

0263-2373 $32.00

Neither Shareholdernor StakeholderManagement:What Happens WhenFirms are Run for theirShort-term SalientStakeholder?

LAURENT VILANOVA, CoActis University of Lyon, France

One of the critical distinctions between share-holder theory and stakeholder theory rests on therole of management in the resolution of the firm’sinternal conflicts. Whereas managers are consideredas a source of conflicts by agency/shareholder theo-rists, they are often viewed as useful mediators inthe stakeholder approach. This paper proposes analternative theory on the role of management incorporate governance, the so-called short term sali-ent stakeholder theory, and illustrates it with a lon-gitudinal case study of Eurotunnel, the ChannelTunnel operator. When the firm’s legitimate stake-holders have very different information levels andbargaining strengths, this theory predicts that (i)firms are governed in the interests of a uniquestakeholder group (ii) managers have a minor roleand are prone to collude with the most powerfulinterest group (iii) this autocratic type of gover-nance is unstable in the long-term as the legitimatestakeholders expropriated at one period use influ-ence strategies to gain power in the next period(iv) the chronic conflicts associated to short-termsalient stakeholder management lead to poor orga-nizational performance.� 2007 Elsevier Ltd. All rights reserved.

146 E

Keywords: Stakeholder Theory, ShareholderTheory, Corporate Governance, Role of Management

Finance and strategic management theories oftentake divergent positions on two fundamental ques-tions: Should firms be run in the interests of theirshareholders or for all of their stakeholders? Morebroadly, what should be the objective of firms? Mostof the time, the defenders of each approach rely onnormative arguments and make simplifying assump-tions. Shareholder theorists argue that managersshould be pledged to shareholders. Because manag-ers are self-serving and opportunistic, the gover-nance structure should be designed so as to limitmanagerial discretion as strictly as possible. Thestakeholder management view considers on the con-trary that managers are not always opportunistic andthat they should retain sufficient autonomy so as toinfluence corporate decisions in a way satisfying allthe key stakeholders of the firm. Beyond this norma-tive debate, little is known about the actual behaviorof firms and about the connexion between corporategovernance strategies and organizational perfor-mance. One of the main problems in designing a

uropean Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

tractable test of instrumental stakeholder/share-holder theories comes from the measure of the stake-holder/shareholder orientation of firms. How todecide that a firm is run for its shareholders or alter-natively for its stakeholders? Should we trust manag-ers’ speeches or rather consider the firm’s actualdecisions?

By considering the case of large project companies,our paper seeks to develop and illustrate an alter-native theory of corporate governance, what wecall short-term salient stakeholder management.Although the terminology of salient stakeholder isa direct reference to the work of Mitchell et al.(1997), our paper goes beyond the question of whoor what constitutes a stakeholder. It also considersthe link between the firm’s organizational structure,the number of salient stakeholders and organiza-tional performance. Even if they have manyidiosyncratic features, large project companies areattractive research sites for people interested inevaluating the relative performance of shareholderand stakeholder theories. Their organizational struc-ture reflects a shareholder management view of thefirm (managers are strictly controlled by financiers)in the mere context where stakeholder theoristsargue for the needs to consider the interests of multi-ple constituencies (these ‘mega’ investments affectnumerous groups or individuals and can dramati-cally change the economic conditions for localcitizens). Moreover, empirical evidence shows thatthis type of firm often exhibits bad performance(Flyvberg et al., 2003). In this paper, we use the caseof Eurotunnel (the Channel Tunnel operator and thelargest project company in the world) to illustratesome of our propositions.

Short-term salient stakeholder management isdefined by the following attributes: (i) firms are runin favor of one salient stakeholder group. This groupis the one that simultaneously possesses the threeattributes defined by Mitchell et al. (1997), that islegitimacy, power and urgency (ii) the identity ofthe salient stakeholder group can change dependingon the firm considered and on the period of time. Thesalient stakeholder at one period is often the one thatsuffered the most from corporate decisions in thenear past (iii) managers are pledged to the salientstakeholder group and have little discretion concern-ing corporate decisions (iv) short-term salient stake-holder management increases agency conflicts andmay lead to poor performance.

Our theory brings insights on three fundamentalquestions concerning corporate governance and per-formance. The first question is quite classical: forwhom companies are run? The answer is far frombeing obvious as the balance of power inside the firmcan take a less trivial form than the one supposed byshareholder and stakeholder theorists. In accordancewith shareholder theory, our theory suggests thatfirms are run for a unique stakeholder group (the

European Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

‘‘salient stakeholder group’’ in our terminology)but, contrary to the shareholder theory’s coreassumption, this group is not always constituted byshareholders. Obviously, the fact that corporate deci-sions give more importance to one stakeholder groupis susceptible to increase conflicts within the firm. Inother words, the autocratic governance structureassociated with short-term salient stakeholder man-agement increases the incentives of non salient stake-holders to gain authority. The Eurotunnel caseillustrates clearly this dynamic dimension of short-term salient stakeholder management: since itscreation the firm was successively controlled by theconstruction companies, banks and dispersed share-holders. Each time, the new salient stakeholdergroup was the one that suffered the most importantlosses in the preceding years.

The second insight of the paper concerns theefficiency of this autocratic type of management. Inother words, is it economically efficient to concen-trate power in the hands of one type of stakeholderinstead of balancing power among the different keystakeholders? The answer is unambiguously yes foragency and transaction costs theorists (see for exam-ple Jensen, 2001; Williamson, 1991). For them, theconcentration of decisions rights in the hands of the‘‘natural’’ residual claimant, that is shareholders con-sidered as an homogeneous group, economizes onagency and transaction costs. Even if stakeholdertheorists are reluctant to the efficiency notion, theyimplicitly assume that the dispersion of controlrights among all the stakeholders and favorable per-formance go hand in hand. Although the problem ofthe optimal allocation of control rights is difficult toanswer on a single case basis, the Eurotunnel casesuggests that the concentration of power in uniquehands does not automatically reduce agency conflictsand can even exacerbate them.

Lastly, our paper sheds new light on a fundamentalwhile understated difference between alternativetheories of corporate governance, that is the role ofmanagement: should organizational structureslimit managerial discretion (contractual theories) orinstead expand it (see for instance Donaldson,1990)? Is managerial discretion valuable because ofthe managers’ ability to take pertinent strategic deci-sions or because of their ability to limit conflictsbetween the firm’s multiple constituencies? TheEurotunnel case is a unique opportunity to examinethese questions. Eurotunnel is indeed a typical pro-ject company, an organizational structure wheremanagers take few strategic decisions and wherelong-term contracts are supposed to be an efficienttool to resolve the potential conflicts between thefirm’s multiple constituencies. These special featuresexplain why shareholder management theorists con-sider project companies as a kind of ideal firm whereagency conflicts between managers and shareholdersare minimized. Our analysis shows that the succes-sive management structures of Eurotunnel, that is a

147

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

no-management structure during the first years ofthe project and a bank-controlled management after-wards, were inefficient: the former led to a ill-definedproject and opportunistic behavior from the con-struction companies at the expense of banks, the lat-ter led to the expropriation of dispersed shareholdersby banks. Overall, the Eurotunnel case illustrates thelimits of contracts in governing relationshipsbetween different claimants and suggests that theresolution of conflicts between various stakeholdersnecessitates the intervention of an independent pow-erful third party. Whether a strong management canexercise this arbitrage role is suggested by our theorybut requires additional reflection on the ways legiti-mate stakeholders can prevent managers fromcolluding with the most powerful claimant.

The paper is organized as follows. The first sectionunderlines the conflicting views between share-holder and stakeholder theorists on the role ofmanagement. These theories take opposite positionson the optimal level of managerial discretion. Thesecond section briefly presents the characteristics oflarge project companies and explains why share-holder theorists consider that this type of firm shouldbe efficient. The third section describes the Eurotun-nel case. We address first the question of stake-holder identification and salience. We alsoinvestigate the consequences of the short-term salientstakeholder management adopted. The fourth sec-tion returns to theorizing. This final section presentsour theory of short-term salient stakeholder manage-ment and stresses the need for stakeholder theoriststo consider more closely managerial incentivemechanisms.

Shareholder vs. Stakeholder Management:

The Conflicting Views on the Role of

Management

The debate opposing the pro and cons of shareholdervalue is often presented in the following way: forwhom should corporations be run? Should manage-ment take decisions in the interests of a unique stake-holder, that is shareholders considered as anhomogeneous group, or rather consider the interestsof the multiple constituencies of the firm? Thesequestions about the legitimacy of shareholder man-agement, while interesting, seem to be unanswerableunless referring to philosophical concepts. For exam-ple, each theory (shareholder management andstakeholder management) has its own performancemeasure (shareholders’ surplus vs stakeholders’ sur-plus) and there is no particular reason to give the pri-macy to one measure over the other. 1 Our papertakes a different perspective. Our main question isabout the importance and the role of managementin both theories. More precisely: Are managers con-sidered as key stakeholders? Should governance

148 E

structures restrict managerial discretion or on thecontrary isolate managers from the control of otherstakeholders? If managers take decisions on thebehalf of other agents, how can stakeholders (share-holders only or multiple constituencies) be sure thatmanagers will consider their interests? The answersof shareholder and stakeholder theorists differdramatically on these fundamental questions (seeFigure 1).

Modern corporate finance asserts quite unanimouslythe need to control managers. The suspicion on man-agers is clearly expressed by Tirole (2006, p. 15):‘‘Most observers are now seriously concerned thatthe best managers may not be selected, and that man-agers, once selected, are not accountable’’. Thefinance view of corporate governance is based onthe following premises:

(i) In order to obtain financing, the providers offunds must be assured that they will get areturn on their investment in the firm,

(ii) Managers, who take decisions, have their owninterests and need not act in the best interestsof providers of funds. They can use their exper-tise and their informational advantage over out-siders to divert funds to pursue their ownobjectives,

(iii) Consequently, ‘‘much of the subject of corpo-rate governance deals with constraints thatmanagers put on themselves, or that inves-tors put on managers to reduce the ex post mis-allocation and thus to induce investors toprovide more funds ex ante’’ (Shleifer andVishny, 1997).

While this approach considers at first sight the inter-ests of all kinds of providers of funds (creditors andshareholders), shareholders benefit from a specialstatus. They are the residual claimants of the firm:contrary to fixed claimants (creditors and employ-ees), they do not negotiate compensation in advanceand their remuneration depends greatly from theex post performance of the firm. This last point makesobvious that shareholders should obtain controlrights (make discretionary decisions) as they havethe right incentives to maximize the firm’s value.So, why do shareholders hire managers and givethem some control rights? Alternatively, why donot shareholders impose a contract specifying whatmanagers should do (and not do) in each circum-stance? The first reason comes from the impossibilityto write a contract specifying all future contingencies.According to the terminology used by contracttheorists, contracts are by essence incomplete. Share-holders have then to decide how to allocate residualcontrol rights- the rights to make decisions in situa-tions not fully foreseen by the contract (Hart andMoore, 1990). The fact that contracts are incompletedoes not however explain why shareholders do notretain all the residual control rights and delegatesome of them to managers. According to agency

uropean Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

Shareholder management Stakeholder Management Key idea Managers should maximize the

wealth of shareholders. Managers should satisfy the interests of all (legitimate)

stakeholders.Nature of firms

Nexus of contracts or relationships between groups with conflicting objectives

Importance of management

Managers are key actors because they have residual control rights

Role of management

Managers are viewed as “hired” agents of shareholders and are in charge of day-to-day management in an incomplete contract framework.Managers can destroy shareholder value.

Managers are viewed as referees between groups with conflicting objectives.

Managers can increase the aggregate value of the firm.

Rep

rese

ntat

ion

of f

irm

s

Behavioral assumptions

Self-interested and opportunistic agents.

The assumption of self-interested and opportunistic agents is overly simplistic.Agents can be organization-centered and altruist.

Optimal governance system

Control should be concentrated in the hands of shareholders.

Control should be divided between the different (legitimate) stakeholders.

Good governance practices

Control mechanisms limiting managerial discretion Incentive mechanisms aligning managers’ objectives with those of shareholders

The ones that increase the democratic representation of non-controlling stakeholders

The “perfect” firm LBO and project company German codetermination

Figure 1 A Comparison Between Shareholder and Stakeholder Management

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

theorists (Jensen and Meckling, 1976), it would be toocostly for shareholders to run the day-to-day opera-tions of the firm. Shareholders would be better offby delegating everyday decisions to specializedagents that possess the expertise and the informationnecessary to operate the firm. If managers have greatdiscretion on day-to-day management, they shouldhowever refer to shareholders for strategic decisionssuch as mergers and acquisitions, dividends or newdebt and capital issues. In practice, managers can ex-ploit their informational advantage to overrule theformal authority of shareholders. This leads to a dis-tinction between formal and real authority: ‘‘So,while shareholders have formal control over a num-ber of decisions, managers often have real control’’(Tirole, 2001, p. 17). Managers have then a consider-able role in the shareholder value concept of corpo-rate governance.

This is not to say that managers are viewed positivelyby the tenants of shareholder value. On the contrary,the real authority exercised by managers is consideredas a source of danger for shareholders. Once the firmhas obtained funds, there is a high probability thatself-interested managers use their decision rights tofavor their own interests at the expense of investors.Much of the corporate finance literature is then aboutthe optimal means to control management. Manyevent studies confirm that managers take decisionsharmful for shareholders (see Shleifer and Vishny,1997 for a summary): they cause their firms to grow

European Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

beyond their optimal size, they favor diversificationover profitability, and so on. . . This evidence is ofteninterpreted as consistent with the behavioral assump-tions of contractual theories of the firm (agency andtransaction cost theories), that is the self-interestedand opportunistic nature of economic agents(Williamson, 1991; Jensen and Meckling, 1994). Whilethe huge majority of economists and finance acade-mics adhere to the idea that shareholders needmanagers to operate the firm, they also consider thatshareholders suffer from managerial misbehavior.This leads shareholder theorists to stress the need tocircumscribe managerial discretion as much as possi-ble. This is not an easy task and opinions diverge onthe optimal control mechanisms. The main difficultycomes from the managers’ ability to make formal con-trol mechanisms (e.g., the board of directors) ineffec-tive. Managers can act strategically to protect theirposition and hold some winning cards: they can con-ceal information from their opponents in the board,they can interfere in the nomination process of direc-tors and so on. The dominant opinion is then that cor-porate boards are quite ineffective in controllingmanagers (Jensen, 1993).

So, it is not surprising that the corporate governancedebate is more about public-owned companieswhere ownership and control are separated andwhere dispersed shareholders are at a disadvantagewith managers (Fama and Jensen, 1983). This is themere situation where managers can exploit the

149

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

passivity of the formal control structures. If thedispersion of formal authority between dispersedshareholders increases de facto the real authority ofopportunistic managers, the logical solution seemsto call for a more concentrated ownership. A majorityshareholder or an influent minority stakeholder hasmore possibilities to put pressure on management.The concentration of power in unique hands (differ-ent from the ones of managers) is then one of the coreideas of the finance view of corporate governance.This concentration of power is advocated on the partof contractual theorists. For example, Williamson(1991) contests the efficiency of the interest groupmanagement of the board- a board in which manyconstituencies are awarded a prorata stake- and advo-cates for specialized boards in which one stakeholdergroup is dominant. Similarly, Jensen (1986) presentsLBOs as a kind of ideal organizational structure thatincreases efficiency and reduces agency conflicts. Thehigh level of debt in LBO transactions- a 10 to 1 ratioof debt to equity is not uncommon- is supposed to bethe main reason leading to efficiency. The obligationto pay high interest payments reduces the ability ofmanagers to divert cash flows to their own benefitand gives them incentives to make sufficient effortin order to reach a high level of performance. More-over, this type of firm has concentrated equity own-ership by LBO funds. Creditors and funds are herethe locus of control and managerial discretion is keptto its minimum.

The main message of the so-called shareholder valuetheory is then extremely clear: managers areopportunistic agents and have important decisionrights; shareholders should either reduce managerialdiscretion (through monitoring) or give managersadequate incentives to maximise shareholder value(stock-based managerial compensation). Managersshould be maintained on a short leash and theirunique role is to take decisions that enhance share-holder value in situations where contracts areincomplete.

The stakeholder theory attributes also a prominent,although less negative, role to managers. Logically,the premise that firms should operate on the behalfof all the stakeholders of the firm (Freeman, 1984)implies the existence of a third party able to identifystakeholders and to take decisions satisfying theinterests of the firm’s multiple constituencies.Whereas managers were at best considered as anecessary evil in the shareholder view of corporategovernance, some stakeholder theorists confer themthe responsibility to make strategic decisions recon-ciling the conflicting interests of the firm’s differentclaimants (Hill and Jones, 1992). This is not to saythat managers are the only rightful locus of control(Donaldson and Preston, 1995) or that managers arealways considered as key stakeholders. Whereasmany authors consider that the only role of managersconcerns the repartition of the firm’s economicsurplus between multiple stakeholders (Aoki, 1984;

150 E

Freeman and Evan, 1990), others expand the role ofmanagement to the creation and the repartition ofthe economic surplus (Donaldson and Preston,1995; Hill and Jones, 1992; Mitchell et al., 1997).

One may obviously argue that the negative vs. posi-tive evaluation of management is more representa-tive of the opposition between finance and strategicmanagement than of the one between shareholderand stakeholder theories. In our opinion, it is how-ever not coincidental that the strategic managementfield was greatly influenced by the stakeholder per-spective whereas finance theory considers nearlyexclusively the shareholder approach. 2 We havefound no criticism against managerial misbehaviorin the stakeholder literature. Rather than restrictingmanagerial actions, corporate governance structuresshould give managers sufficient discretion in orderto satisfy multiple stakeholders simultaneously. Theproponents of the stakeholder theory of the firmargue that the influence of managers should be rein-forced and that a strict control of managerial deci-sions can impede value creation (Rappaport, 1990;Charreaux and Desbrieres, 2001).

Even if this point is rarely underlined, stakeholdertheorists usually consider that the assumption ofself-interested and opportunistic agents is overlysimplistic (Jones and Wicks, 1999). Many of themimplicitly acknowledge the propensity of managersto act in the interests of their organization rather thanin their sole interests. Managers are then consideredmore like stewards than like opportunistic agents.These diverging behavioral assumptions appearclearly in Davis et al. (1997, p. 25): ‘‘Stewards inloosely coupled, heterogeneous organizations withcompeting stakeholders and competing shareholderobjectives are motivated to make decisions that theyperceive are in the best interests of the group. . .Asteward who successfully improves the performanceof the organization generally satisfies most groupsbecause most stakeholder groups have interests thatare well served by increasing organizational wealth’’.In short, the stewardship theory assumes thatmanagers and the other firm’s constituencies arewilling to act cooperatively and that managers willnaturally give consideration to the interests of multi-ple stakeholders. The organization-centered behaviorpostulated by the stewardship theory can be thenconsidered as a sufficient condition for implement-ing the kind of democratic governance structuredescribed by the tenants of the stakeholder society.

But, is it a necessary condition? In other words, isstakeholder management implementable in a worldof self-interested and opportunistic agents? Theanswer is clearly negative for the defenders of share-holder management. For them, stakeholder manage-ment would dilute managerial accountability andwould give managers the opportunity to invoke mul-tiple and hard-to-measure missions to hide their self-serving behavior (Jensen, 2001; Tirole, 2006).

uropean Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

If it seems utopian to satisfy simultaneously all thestakeholders of the firm, it does not mean that a‘‘moderate’’ form of stakeholder management isimpossible. Mitchell et al. (1997) propose in this spirita very interesting theory of stakeholder identificationand salience departing from the broad view of Free-man (1984) – the firm should satisfy the interests ofall the groups or individuals who can affect or beaffected by the achievement of the firm’s objectives-as well as from the narrow view of shareholder man-agement – the firm should only consider the interestsof shareholders. They start with a typology of stake-holders based on the possession of three attributes:power (the stakeholder’s ability to influence the firm),legitimacy (the legitimacy of the stakeholder’s rela-tionship with the firm based upon contract or legaltitle) and urgency (the degree to which managerialdelay in attending to the claim is unacceptable tothe stakeholder). These three attributes can be usedto identify all relevant stakeholders (a stakeholdermust have at least one attribute) but also to deter-mine the salience of each stakeholder for managers.The idea is quite simple: managers pay more atten-tion to a ‘‘definitive’’ stakeholder, who holds simul-taneously the three attributes, than to a latent one(with only one attribute). This theory has many inter-esting features. It attributes a central role to manag-ers who are in charge to identify and to organizestakeholders into a hierarchy. It does not stipulate apriori the identity nor the number of ‘‘definitive’’stakeholders. Lastly, the theory is dynamic as it con-siders that stakeholders can shift over time from oneclass to another. More broadly, this approach deniesthat all the stakeholders of the firm have convergentobjectives and considers rather conflict betweenstakeholders as an important while understated pre-mise of stakeholder theory in the same way that con-flict between managers and shareholders is a keypremise of shareholder theory. This idea, oppositeto the one advocated by stewardship theory, is alsoclearly expressed by Frooman (1999, p. 193): ‘‘I sug-gest, then, that if the potential for conflict did notexist – that is, if the firm and all its stakeholderswere largely in agreement – managers would haveno need to concern themselves with stakeholders orstakeholder theory’’.

Although both theories drastically diverge on therole of managers, few attempts have been made totest the connections between the practice of manage-ment and the achievement of corporate performance.For many scholars, the main difficulty comes fromthe explanatory variable, that is the measure of cor-porate performance. Tirole (2006, p. 62) asserts alongthis line that there exists no reliable measure of theimpact on managerial decisions upon stakeholders’welfare. In our opinion, the measure of the depen-dent variable (the stakeholder or shareholder orienta-tion of the firm) is even more problematic: how tomeasure stakeholder salience? Should we rely onCEOs’ speeches? Agle et al.’s (1999) work illustratessome of these methodological issues. Their empirical

European Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

test of stakeholder salience uses survey data pro-vided by CEOs. They find a strong relationshipbetween stakeholder attributes (power, legitimacyand urgency) and stakeholder salience but they iden-tify no effects of salience on performance. In ouropinion, this last result asks two questions: are CEOs’speeches reliable measures of actual stakeholder sal-ience? To what extent do managers have sufficientdiscretion to give the primacy to one type of stake-holder over the others? Looking at archetypal formsof stakeholder or shareholder firms might be a betterapproach to test the relative performance of the twodominant models of corporate governance (Figure 1).

Large Project Companies and the

Performance of ‘‘Pure’’ Shareholder Firms

The finance view of corporate governance hasreceived substantial attention from the mediathroughout the world with the release of the so-called ‘‘codes of best practice for boards of direc-tors’’. 3 These codes made recommendations onincentive mechanisms (managerial compensation)and control mechanisms (composition of the board)and were essentially concerned with the resolutionof conflicts between managers and shareholders.However, shareholder theorists don’t restrict theirattention to the question of board structure. Theyalso identify special forms of organizational struc-tures allegedly supposed to resolve agency conflictsin a more efficient way than traditional structures.We present here one type of ‘‘perfect’’ firm for share-holder theorists, i.e. a project company.

According to Esty (2003), a project company is a leg-ally independent entity financed with equity fromone or more sponsoring firms and nonrecourse debtfor the purpose of investing in a capital asset, usu-ally with a single purpose and a limited life. Thistype of structure is today one of the leading financevehicles for investments in natural resources andinfrastructure sectors such as power plants, tollroads, mines, pipelines and telecommunicationsystems.

The financing and organizational structures differdrastically from the ones of other companies. Projectcompanies typically employ very high leverage com-pared to public companies. Debt-to-capitalizationratios in the range 70%–90% are usual. Debt owner-ship is most of the time concentrated in the handsof several banks (syndicated bank loans) and credi-tors have no possibility to recourse to sponsoringfirms (shareholders) if any problem of debt repay-ment occurs. Equity ownership is also far more con-centrated than in public companies as the typicalcompany is privately held and has only one to threesponsors. The board of directors is supposed to con-trol very closely managers as more than 80% of the

151

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

directors come from the sponsoring firms. Lastly, therelationships with the company’s multiple stake-holders are essentially managed by way of contractsas ‘‘the typical project has 40 or more contracts unit-ing 15 parties in a vertical chain from input supplierto output purchaser’’ (Esty, 2004, p. 2). In short, pro-ject companies are financier-dominated firms wherecontracts are preferred to managers for governingrelationships with related parties.

These special features are often justified by the effi-ciency gains associated with the reduction in transac-tion costs or agency conflicts. Said differently, thetypical project structure would promote the interestsof shareholders. Consider for example the projectcompanies’ modes of financing. In reference to Jen-sen’s theory of free cash flows, high leverage is sup-posed to increase the managers’ incentives to reach ahigh-level of performance and to limit managerialdiscretion over cash flows. The fact that debt comesfrom a few banks reduces also managerial discretionas bank credit contracts include many restrictive cov-enants and involve more monitoring than arm’slength debt. According to this view, the banks’ dom-inance should benefit shareholders. Everything takesplace as if the banks and the shareholders shared thesame objective of reducing managerial discretion. Inthe same perspective, the concentration of equityownership strengthens the control of shareholdersover managers. Finally, the use of long-term con-tracts is thought to be an ideal governance tool toprevent any opportunistic behavior of related parties(input suppliers, output buyers) given highly specificassets. All these structural attributes of project com-panies contribute to reducing potential managerialopportunism. The banks and the shareholders takethe strategic decisions before the project begins andthe role of project managers is restricted to themanagement of day-to-day operations. The specialpurpose of project companies- dedicated to the man-agement of only one asset-, the predominance oflong-term contracts and the strict monitoring exertedby financiers also restrict ex post managerial oppor-tunism. In summary, this type of organizationalstructure seems to be a pure illustration of the‘‘shareholder view’’ of the firm that posits the strictcontrol of managers as a necessary condition forachieving high (shareholder) performance.

Despite the supposed qualities of project companies,the debate on the efficiency of project companies isstill open. For Esty (2003), the typical ‘‘flat’’ pay-for-performance compensation schemes of projectmanagers demonstrates the efficiency of project gov-ernance systems in resolving managerial agency con-flicts. Despite that project finance loans are made toriskier borrowers, they have lower spreads thanother types of loan (Kleimeier and Megginson,2000). A recent survey initiated by Standard & Poor’sRisk solutions and involving 30 project finance lend-ers from around the world also shows that projectloans have lower default rates and higher recovery

152 E

rates than corporate loans. Globally, this empiricalevidence tends to confirm the ability of project com-panies to mitigate agency conflicts. The few studiesthat have focused on the performance of large pro-jects are however far more pessimistic. Large projectsseem to perform very badly and experience system-atic cost overruns (Flyvberg et al., 2002, 2003).

This suggests that asset size is a key determinant ofthe performance of project companies. The reasonsunderlying this empirical observation are stillunknown. Why do large project companies fail sooften while other project companies outperformmore traditional organizational structures? Onepotential explanation lies in the discrepancy betweenthe project company’s simplified organizationalstructure and the multiplicity of stakeholders. Toillustrate this idea, consider large infrastructure pro-jects. The usual scheme, the so-called BOT (Build,Operate and Transfer), involves a private consortiumagreeing to build the project facility, operate it for agiven length of time (the concession period) and thentransfer it back to the public sector. Many agentsintervene at the successive stages of the project andare parties in the project’s main contracts : (i) the con-cession contract is signed between the host govern-ment and the project company (a consortium ofprivate sponsors) (ii) the debt contract links theproject company with banks (iii) the constructioncontract is negotiated between the project company,represented by its sponsors and lenders, and con-struction companies (iv) the contracts that governthe relationship between the project company andthe related parties that supply critical inputs (a fuelproducer for a thermal power plant) or that buy pri-mary outputs (a company that resells electricity tofinal consumers for a power plant). Each of theserelationships gives rise to potential opportunismfrom related parties. The firm’s sponsors can hideinformation to the host government in order to winthe invitation to tender and can overestimate futurecash flows in order to convince lenders to bring suf-ficient funds. The construction companies can volun-tarily underestimate costs or potential delays inorder to obtain the construction contract or provideinsufficient effort to complete the construction ontime after the contract has been signed (Flyvberget al., 2002). Output suppliers can renege on theirpromise to buy the outputs at the pre-specified priceand try to impose ex post a lower price. Host govern-ments can also behave opportunistically by seizingthe company’s asset or by increasing taxes. Obvi-ously, the parties involved in formal contracts arenot the only ones susceptible to influence a projectcompany. For very large projects, other stakeholderssuch as politicians, the media, residents or associa-tions of individual shareholders can interfere in thedecision-making process and can increase the diffi-culties to take value-maximizing decisions.

Of course, each constituency may pursue its ownobjective and use its informational advantage at

uropean Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

the different steps of the project to expropriate otherstakeholders. The multiplicity of stakeholdersinvolved in large project finance as well as the fre-quent failure of large project companies raises thequestion of the optimal governance structure: Is itefficient to concentrate power in the hands of inves-tors (banks and sponsors) in large project companiesthat often involve many constituencies? According toshareholder theorists the high concentration ofpower in large project companies should lead to highperformance. Even if numerous influential partiesenter the decision-making calculus, the need to raiseexternal funds and to convince risk-averse banksmakes it unlikely that the decisions of large projectcompanies do not reflect careful and deliberateattempts to increase shareholder value (Esty, 2004,p. 219). The answer of stakeholder instrumental the-orists would be different: if managers don’t view theinterests of stakeholders as having intrinsic worthand pursue only the interests of a single group, thefirm they manage will achieve lower performancethan had they pursued the interests of multiplestakeholders (Donaldson, 1999, p. 238). Large projectcompanies are thus attractive research sites to com-pare these two approaches of corporate governance.Indeed, their organizational structure reflects ashareholder management view of the firm in themere context where stakeholder theorists underlinethe need to adopt a more democratic governancestructure.

The Failure of the Shareholder

Management View in Large ProjectCompanies: The Case of Eurotunnel

The decision to build a fixed link between France andEngland was made official on April 2, 1985 when theFrench and the UK governments launched the invita-

Credit agreement (November 1987)

Lenders(Banks)

UKGovernment

Railways Railway usage contract (July 1987)

Figure 2 The Channel Tunnel’s Initial Contractual Structu

European Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

tion to tender. The competing offers were receiptedseven months later and the selection was effectivein January 1986. The retained offer was the one sub-mitted jointly by France Manche (FM) and the Chan-nel Tunnel Group (CTG), which formed twin holdingcompanies (Eurotunnel SA and Eurotunnel PLC),chartered in France and Great Britain, respectively.The winning project consisted in two single track railtunnels and a service tunnel, including a shuttle ser-vice for cars and trucks. At the same time, the mainlegal instrument governing the construction andoperation (The Treaty of Canterbury) was signedby both governments in February 1986 (later ratifiedin July 1987) and the concession was formallyawarded to Eurotunnel (a 50/50 joint venturebetween FM and CTG) on March 14, 1986 for 55years. As usual in project companies, a fairly com-plex set of contracts was implemented during thefirst months between multiple stakeholders (seeFigure 2).

Many features of Eurotunnel’s initial organizationalstructure fit well with the so-called efficiency-enhancing features of project companies. First, inves-tors controlled quite closely the firm as the mainprovider of funds, i.e. the banks, controlled closelymanagers through its 50% equity ownership. Thebanks also had 9 out of 18 seats on the board of direc-tors. Construction companies were also heavilyimplicated through a 50% equity ownership andthrough their representation in the board (2 seatsout of 18). The fact that constructors were at the sametime Eurotunnel’s main contractor and one of itsleading shareholder was supposed to decrease thepropensity of construction companies to behaveopportunistically. Each cost overrun or delay inthe construction phase would run counter to theinterests of the construction companies due to theadversarial impact on Eurotunnel’s share value.Furthermore, the potential opportunism of construc-

FrenchGovernment

TML

Eurotunnel(FM/CTG)

Shareholders

Treaty (February 1986)

Concession(March 1986)

Construction contract (August 1986)

Constructors

re

153

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

tors seemed at the time all the more unrealistic sincethe construction contract included an incentives/penalties scheme supposed to deter any voluntarydelay or cost overrun. The problem of the ex postmonopolistic position of the output buyer, i.e. rail-ways, was also considered through the railway usagecontract that defined a minimum payment to Euro-tunnel during the first years of operations.

For Whom Eurotunnel was Run?

At first sight one may consider that the banks and theconstruction companies have shared the control ofEurotunnel during the first years of the project: theywere both the main contractors and the main spon-sors of the project company. This shared-controlwas also reflected in the 50–50 partition of equityownership.

However, in spite of appearances, real authority wasconcentrated in the hands of the construction compa-nies. The dominance of constructors was primarilydue to their informational advantage in the evalua-tion of construction costs. Faced to TML, the con-struction consortium, the funding banks wereunable to elaborate their own projections. 4 The factthat banks relied almost exclusively on the informa-tion provided by constructors was all the more disas-trous since both agents had very diverging objectivesand interests. TML had short-term interest in the pro-ject and was only concerned in the constructionphase. In contrast, the banks had a longer-term inter-est as debt repayment was scheduled to commenceafter the commercial opening of the Tunnel. Thediscrepancy between these two key stakeholders’investment-term horizon was confirmed ex post.Whereas the banks retained their shares and the con-trol of the Board of Directors for many years, theconstructors sold their shares and left the Board veryquickly (the last one left the Board at the end of 1989).Because of their lack of technical expertise, the bankswere however unable to circumscribe the opportu-nistic behavior of constructors. For example, thebanks were convinced at the outset of the project thatthe construction costs computed by TML were over-estimated. In reality, TML communicated artificiallylow costs in order to win the tender offer. For manyobservers, the banks were incredibly naıve as delib-erate cost underestimation is a usual practice in ten-der offers. 5 This seminal mistake greatly influencedthe relationship between Eurotunnel main financiers(the banks) and constructors. Conflicts appeared

Table 1 Evolution of Projected Construction Costs (in

November 1987 Novem

Total construction costs 2710 3969

Data are Drawn From Eurotunnel prospectus (1987 offer for sale,

154 E

from the very beginning of the construction scheduleand intensified at the same time as delays and costoverruns increased. Table 1 shows the evolution ofprojected construction costs over time at the differentsteps of the seven years construction phase and illus-trates the problem of cost escalation. 6

The banks were clearly the first victims of theirinability to control the opportunistic behavior ofTML. The escalation of construction costs increasedthe need for financing and the banks that had ini-tially planned to bring £5 billion were obliged toincrease their investment to £7.8 billion. While thebank syndicate agreed to provide additional funds,it set strict conditions. The banks asked for a majorchange of ownership structure and risk allocation.This led Eurotunnel to become a public company in1987 and to realize two additional equity issues in1990 and 1994. As emphasized by Stonham (1995),the lending banks were satisfied to transfer part oftheir risk to individual shareholders as equity offer-ings allowed the Tunnel to be completed whiledecreasing the leverage to capital ratio. At the timeof the IPO, the bank-dominated management ofEurotunnel made very optimistic speeches to encour-age individual investors to subscribe to new equities:‘‘This is an ideal investment to finance the studies ofyour children; you receive nothing at the beginningbut in turn the value of your shares will treble inseven years’’ (Jean-Louis Dherse, Eurotunnel’s man-aging director, reported in Les Echos, October 29,1996). In reality, Eurotunnel stock was issued at 350pence in November 1987, was priced around 260pence at the time of the commercial opening of theTunnel (in June 1994) and has constantly decreasedsince then. During this period, the projected trafficand revenues were systematically updated down-ward after each equity offering. This led manyobservers to question the fairness and independenceof Eurotunnel’s management. 7 More precisely, themanagers were suspected of favoring banks by com-municating over-optimistic projections to smallinvestors.

During the following years, the financial situation ofEurotunnel deteriorated. The firm suspended inter-est payments on its junior debt in September 1995.Complex negotiations with banks took place andlasted more than two years before an agreementwas reached. During this period, the position of man-agement was extremely ambiguous. Patrick Ponsolle,at the time CEO of Eurotunnel, declared at the outsetof the negotiations its intention to seek concessions

£ million – 1985 prices)

ber 1990 May 1994 % change 1987–1994

4844 78.8%

1990 and 1994 rights issues).

uropean Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

from banks and to defend the interests of individualshareholders. He advocated for reduced interestmargins on bank debt and rejected a debt-for-equityswap that would dilute the claims of individualshareholders. Ponsolle’s position was radically dif-ferent a few months later when he tried to convinceshareholders of accepting the financing restructuringproposals negotiated with the representatives of thebank syndicate (Les Echos, June 24, 1997). The indi-vidual shareholders had no other choice but to trustthe CEO and to approve the plan. They had only par-tial information on the precise terms of the revisedcredit agreement as none of their representativeswas invited to the negotiations. Moreover, the planwas incredibly complex and most of the individualshareholders were unable to evaluate its implicationsfor their own welfare.

Despite the fact that the banks declared having madehuge concessions to Eurotunnel, the situation of thefirm didn’t improve significantly after the implemen-tation of the restructuring. While the financial pres-sure was delayed through debt rescheduling, actualrevenues were still disappointing. Two groups camein open conflict. The first group (presented as ‘‘therebels’’ in the press) was constituted by several asso-ciations of individual shareholders and pressedsimultaneously the banks for a debt write-off andthe British and French governments for a bail-outof the troubled group. The second group includedthe banks and the management in place. It advocatedfor less radical measures including negotiations withbanks to restructure Eurotunnel’s £6 billion debt anda commercial plan intended to boost traffic and rev-enues. The conflict grew by the end of 2003 as thefuture of Eurotunnel became more uncertain. TheMUC (Minimum Usage Charge) that guaranteedEurotunnel a minimum payment from the railwayswas planned to end in November 2006. This was aclear threat on Eurotunnel’s revenues. The minimumuser fee arrangements guaranteed Eurotunnel a rev-enue equivalent to about 10 million Eurostar passen-

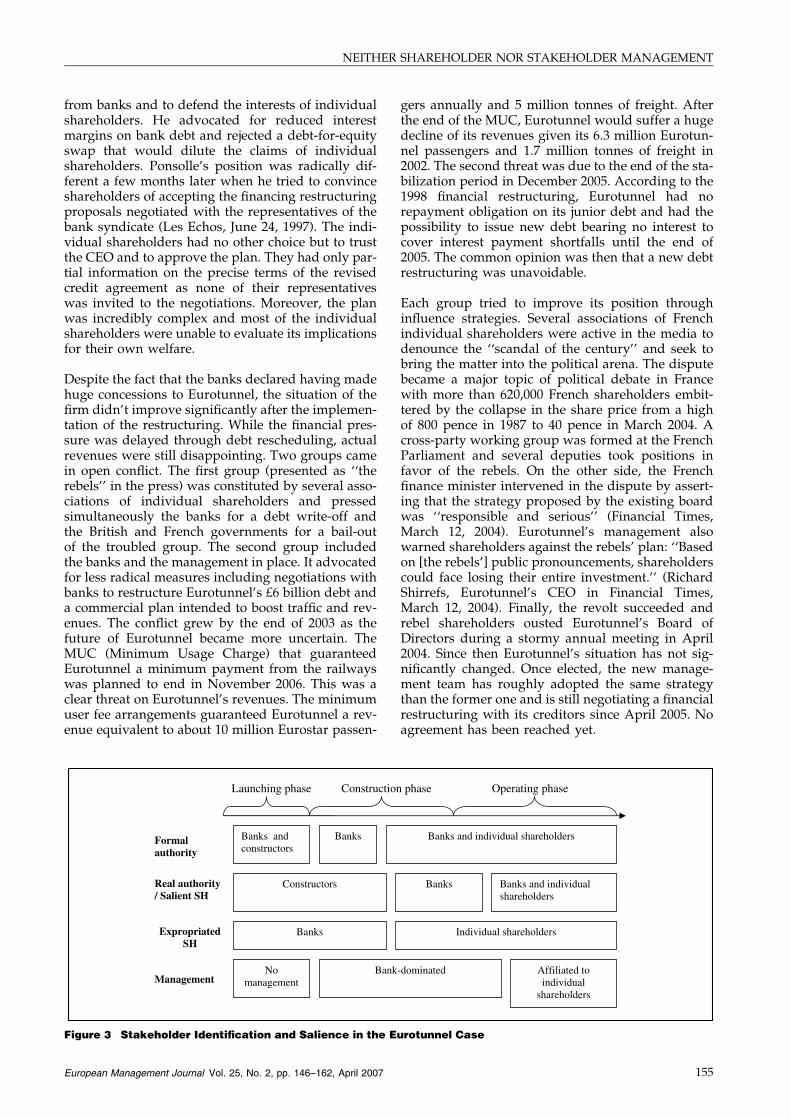

Launching phase Construction

Formal authority

Banks and constructors

Banks

ExpropriatedSH

Banks

ManagementNo

management Bank

Real authority / Salient SH

Constructors

Figure 3 Stakeholder Identification and Salience in the E

European Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

gers annually and 5 million tonnes of freight. Afterthe end of the MUC, Eurotunnel would suffer a hugedecline of its revenues given its 6.3 million Eurotun-nel passengers and 1.7 million tonnes of freight in2002. The second threat was due to the end of the sta-bilization period in December 2005. According to the1998 financial restructuring, Eurotunnel had norepayment obligation on its junior debt and had thepossibility to issue new debt bearing no interest tocover interest payment shortfalls until the end of2005. The common opinion was then that a new debtrestructuring was unavoidable.

Each group tried to improve its position throughinfluence strategies. Several associations of Frenchindividual shareholders were active in the media todenounce the ‘‘scandal of the century’’ and seek tobring the matter into the political arena. The disputebecame a major topic of political debate in Francewith more than 620,000 French shareholders embit-tered by the collapse in the share price from a highof 800 pence in 1987 to 40 pence in March 2004. Across-party working group was formed at the FrenchParliament and several deputies took positions infavor of the rebels. On the other side, the Frenchfinance minister intervened in the dispute by assert-ing that the strategy proposed by the existing boardwas ‘‘responsible and serious’’ (Financial Times,March 12, 2004). Eurotunnel’s management alsowarned shareholders against the rebels’ plan: ‘‘Basedon [the rebels’] public pronouncements, shareholderscould face losing their entire investment.’’ (RichardShirrefs, Eurotunnel’s CEO in Financial Times,March 12, 2004). Finally, the revolt succeeded andrebel shareholders ousted Eurotunnel’s Board ofDirectors during a stormy annual meeting in April2004. Since then Eurotunnel’s situation has not sig-nificantly changed. Once elected, the new manage-ment team has roughly adopted the same strategythan the former one and is still negotiating a financialrestructuring with its creditors since April 2005. Noagreement has been reached yet.

phase Operating phase

Banks and individual shareholders

Banks Banks and individual shareholders

Individual shareholders

-dominated Affiliated to individual

shareholders

urotunnel Case

155

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

As a whole, the history of Eurotunnel is characterisedby huge conflicts between the firm’s key constituen-cies. The salient stakeholders were successively theconstructors, the banks and the individual share-holders (Figure 3). The management, if any, paidonly attention to the short-term salient stakeholder,the one with the more urgent claim, and ignoredthe others. The other stakeholders were constantlyignored (for example, individual shareholders until2004). The expropriated stakeholders in one periodadopted in turn strategies to gain power and becamesalient in the subsequent one.

The Link Between Governance Structureand Performance

Eurotunnel has been in financial distress for nearlytwenty years. The first difficulties appear a fewmonths after the beginning of the construction(breach of financial covenants). Since then, anddespite several debt restructurings, Eurotunnel isstill close to bankruptcy. The creditors and the indi-vidual shareholders have experienced negative pres-ent value for their investment in the project. Forexample, the stock price was only 25 pence in April2006 in comparison with prices between 265 penceand 350 pence for the successive equity offeringsduring the 1987-1994 period. The overall perfor-mance of the Channel Tunnel project is more difficultto evaluate. Anguera (2006) considers however thatthe producers’ losses (both ferry operators and Euro-tunnel) have been much higher than the user’s gains(mainly due to the price cuts). He concludes that theBritish economy would have been better off had theTunnel never been constructed.

The causes of Eurotunnel’s bad performance are stillunder question. To what extent was this bad perfor-mance due to Eurotunnel’s wrong organizationalstructure or to bad luck associated to a highly inno-vative and uncertain project? The interactionbetween bad performance and the conflictual rela-tionships between stakeholders also deserves atten-tion: Did bad performance exacerbate conflicts oralternatively did conflicts lead to bad performance?

The non-existence of Eurotunnel at the birth of theproject is the most popular ex post explanation ofEurotunnel’s chronic financial distress. This argu-ment has been regularly invoked by the managementstaff since 1987 and is also popular among academics(Genus, 1997; Flyvberg et al., 2003). It starts from thepremise that the bid submitted to governments in1986 was prepared by a consortium of banks andconstruction companies that were primarily con-cerned in winning the financing and the constructioncontracts rather than in ensuring the project’s long-term viability. The concessionaire (Eurotunnel) didnot exist at that time and was then a missing partyin the bidding offer. Consequently, ‘‘traffic and reve-nue forecasts had, of course, been prepared, but the

156 E

means by which those figures were to be turned intoreality had not been defined’’ (Kirkland, 1995; Euro-tunnel Technical Director from 1985 through 1991).The autonomy of Eurotunnel remained potentialafter the concession had been awarded as its embry-onic management was closely affiliated to the banksand the construction companies. Hence, there was nostrong representative of the concessionaire to negoti-ate the two main contracts at arm’s length with theconstructors and the banks (Grant, 1997).

These contracts were extremely unfair for Eurotun-nel and were quite impossible to renegotiate oncethe operating team was assembled. Interest marginson the debt contract were originally high and wereregularly increased between 1987 and 1994. Aboveall, Eurotunnel had to support most of the construc-tion risk and cost overruns. This point was madevery clear by Kirkland (1995, p. 5): ‘‘Any alterationsto the construction schedule to facilitate opera-tion. . .were bound to lead to a claim for additionalpayment (by the construction consortium) with aconsequent adverse effect on investor confidence’’.Obviously, the builders have always denied theunfairness of the contract. For them, cost overrunsand delays were mainly due to unanticipated groundconditions and major safety changes to the designsimposed by the Intergovernmental Commission. Onthe other side, the banks and the management recog-nized the technology risk inherent in such an innova-tive project but contested the allocation of riskshaped by the construction contract. Quite obviously,this contract contained loose penalties against build-ers and most of the actions filed by Eurotunnelagainst TML were dismissed by judges or by the Dis-putes Panel (a committee that was set up to resolvecontractual disagreements between both parties).Finally, Eurotunnel had to endorse most of the costoverruns.

The fact that Eurotunnel was an ‘‘empty shell’’ at thebirth of the project may be therefore one of the keydeterminant of its subsequent poor performance.The initial ‘‘no-management’’ structure led to the sig-nature of long-term contracts that did not considerthe interests of the firm.

While partially true, this line of reasoning fails to cap-ture the full complexity of the interaction betweenEurotunnel’s initial governance structure and perfor-mance. Opposing banks and constructors on oneside, and Eurotunnel on the other side misses twoimportant points.

First, the banks and the constructors were not onlyEurotunnel main contractors, but also Eurotunnelinitial shareholders. In theory, the key contractors’sponsorship should have precluded any opportunis-tic behavior against the concessionnaire, the gainsobtained as contractors being offset by the losses asshareholders. The reason why this mechanism failedis quite simple. As already argued, the original pro-

uropean Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

moters sold most of their shares during the construc-tion phase and became minority shareholders inOctober 1986 just a few months after they won thetender offer and only two months after the signatureof the construction contract. This short-term implica-tion in equity ownership has been often interpretedas evidence that the original promoters’ prioritywas to derive profits from the construction and thefinancing contract at the expense of the operator.For some observers, it also explains why the banksand the builders had no special interest in creatinga strong management staff during the first years ofthe project. If there is no doubt that short-term spon-sorship had a negative effect on Eurotunnel perfor-mance, note however that this incentive problemcould have been addressed more efficiently had thegovernments imposed a concession contract prohib-iting original equity holders from selling their equitywithin a certain period of time. 8

Considering that the banks and the builders had, inessence, converging interests is also misleading.Regardless of their equity stake in the firm, the bankshad a long-term interest in Eurotunnel as interestand principal payments were scheduled to com-mence during the operating phase. In theory, the factthat the banks negotiated the construction contractwith the builders as equals should have guaranteedthe signature of a contract preserving the long-term viability of the project. According to thisview, Eurotunnel’s distress would not be attribut-able to the banks’ opportunism but rather to theirtechnical and information deficit at the outset of theproject.

The appointment of new management and staff afterthe 1986 Initial Public Offering (IPO) didn’t changesignificantly the balance of power and had little posi-tive effect on the performance of the project. Thebanks kept the control of the Board even if theybecame at that time minority shareholders. Confidentin the project’s success the new dispersed sharehold-ers were passive investors and didn’t try to impose achange of Eurotunnel governance structure. With thecomplicity of the affiliated management, the bankstried unsuccessfully to challenge the constructioncontract. Globally, the results of the new governancestructure on the long-term viability of Eurotunnelwere ambiguous. From 1987 to 1994, the banks regu-larly increased interest margins on the financing con-tract, which contributed to deteriorating the financialsituation of Eurotunnel. Simultaneously, they helpedEurotunnel to avoid bankruptcy by reschedulingdebt repayments and by encouraging small investorsto bring new funds. The managers’ behavior was alsoambiguous: they allied with the banks to ask for arevision of the construction contract and to commu-nicate overoptimistic projected revenues at the timeof equity offerings while denouncing the high inter-est margins on the debt contract. In fact, the manage-ment team had to arbitrate conflicts between twolegitimate stakeholders. On one side, the managers

European Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

were under the pressure of the numerous Frenchindividual shareholders that asked for the adoptionof a strong line with banks. The managers had there-fore strong incentives to declare acting on behalf ofsmall investors. On the opposite side, the managerswere submitted to the pressure of banks. Asexpressed by a former member of the Board, themanagers had little room to manoeuvre vis-a-visthe bank syndicate: ‘‘Members of the bank syndicatereceived each day the traffic figures. . ..They were thetrue directors of Eurotunnel’’ (Eurotunnel director,taped interview, 2002). 9 Faced to these two conflict-ing interest groups, Eurotunnel managers favoredthe most sophisticated one, i.e the banks. The factthat the small investors’ equity stake was highlydiluted and that Eurotunnel was still overindebtedafter the 1998 financial restructuring seems toillustrate this point. This opinion contrasts with thepositive role of management assumed by someobservers. Grant (1997) asserts for example that anindependent staff could have represented futureindividual shareholders during the negotiations ofthe two key contracts in 1986. Similarly, Flyvberget al. (2003) think that the new management savedthe project by adopting a strong line with contrac-tors. If partially true, this view may however overes-timate the independence of managers vis-a-vis thebanks and their positive impact on the project’sperformance.

If the ill-defined governance structure was withoutany doubt at the origin of the chronic conflictsbetween builders, banks and dispersed shareholders,in what extent had these conflicts a negative impacton Eurotunnel performance? We have alreadydiscussed the long-term implications of the builders’unresolved incentive problem. More generally, man-agers have been since the first years more implicatedin the ways to resolve major conflicts between stake-holders than in the search for strategic and opera-tional moves to improve the firm’s performance.For example, Eurotunnel had virtually no marketingpolicy until 1996 despite the fierce competition fromferry operators and low-cost airlines on the cross-Channel market (Les Echos, March 14, 1996).

In short, the Eurotunnel case shows that the mere ele-ments supposed to improve performance, that islong-term contracts, centralized decision-makingand the tight control of managerial discretion, wereat the origins of bad performance.

Short-term Salient Stakeholder Theory

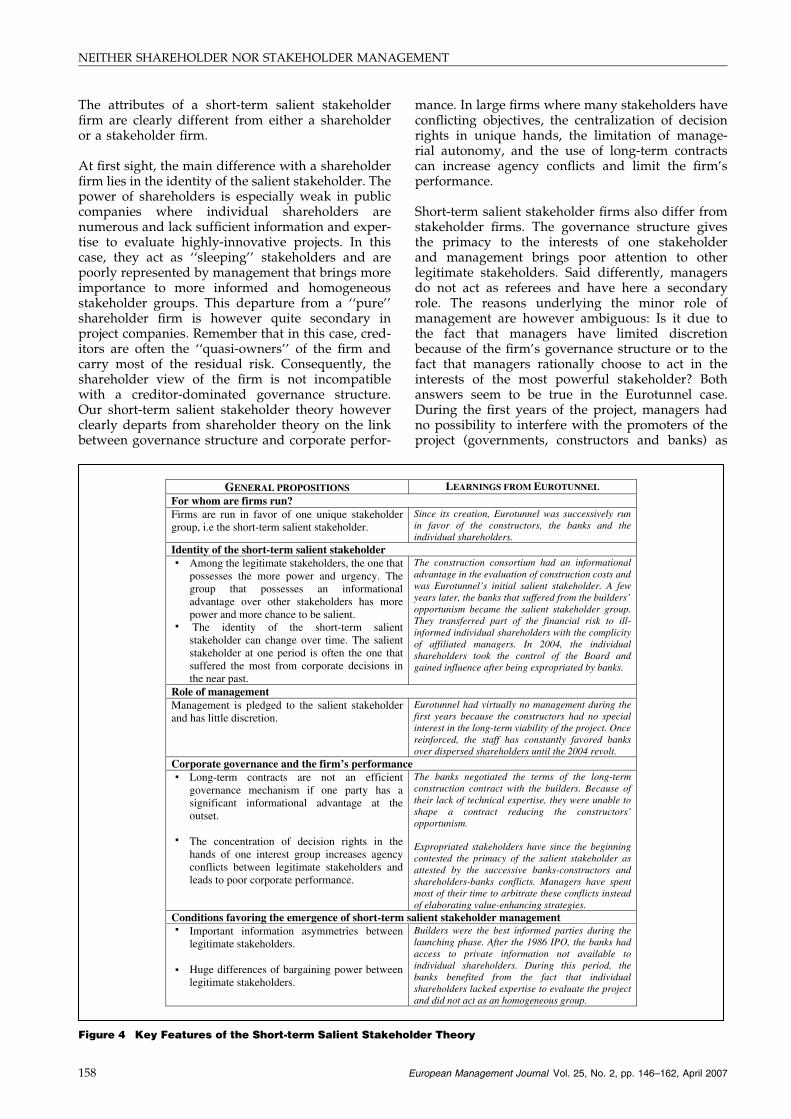

While Eurotunnel has a number of unique features,we believe that this study can bring new insightson the way large firms actually work. In this section,we present the premises of an alternative view of cor-porate governance, what we call the short-term sali-ent stakeholder theory (see Figure 4).

157

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

The attributes of a short-term salient stakeholderfirm are clearly different from either a shareholderor a stakeholder firm.

At first sight, the main difference with a shareholderfirm lies in the identity of the salient stakeholder. Thepower of shareholders is especially weak in publiccompanies where individual shareholders arenumerous and lack sufficient information and exper-tise to evaluate highly-innovative projects. In thiscase, they act as ‘‘sleeping’’ stakeholders and arepoorly represented by management that brings moreimportance to more informed and homogeneousstakeholder groups. This departure from a ‘‘pure’’shareholder firm is however quite secondary inproject companies. Remember that in this case, cred-itors are often the ‘‘quasi-owners’’ of the firm andcarry most of the residual risk. Consequently, theshareholder view of the firm is not incompatiblewith a creditor-dominated governance structure.Our short-term salient stakeholder theory howeverclearly departs from shareholder theory on the linkbetween governance structure and corporate perfor-

GENERAL PROPOSITIONSFor whom are firms run? Firms are run in favor of one unique stakeholder group, i.e the short-term salient stakeholder.

Identity of the short-term salient stakeholder Among the legitimate stakeholders, the one that possesses the more power and urgency. The group that possesses an informational advantage over other stakeholders has more power and more chance to be salient. The identity of the short-term salient stakeholder can change over time. The salient stakeholder at one period is often the one that suffered the most from corporate decisions in the near past.

Role of management Management is pledged to the salient stakeholder and has little discretion.

Corporate governance and the firm’s performanceLong-term contracts are not an efficient governance mechanism if one party has a significant informational advantage at the outset.

The concentration of decision rights in the hands of one interest group increases agency conflicts between legitimate stakeholders and leads to poor corporate performance.

Conditions favoring the emergence of short-term sImportant information asymmetries between legitimate stakeholders.

Huge differences of bargaining power between legitimate stakeholders.

Figure 4 Key Features of the Short-term Salient Stakehol

158 E

mance. In large firms where many stakeholders haveconflicting objectives, the centralization of decisionrights in unique hands, the limitation of manage-rial autonomy, and the use of long-term contractscan increase agency conflicts and limit the firm’sperformance.

Short-term salient stakeholder firms also differ fromstakeholder firms. The governance structure givesthe primacy to the interests of one stakeholderand management brings poor attention to otherlegitimate stakeholders. Said differently, managersdo not act as referees and have here a secondaryrole. The reasons underlying the minor role ofmanagement are however ambiguous: Is it due tothe fact that managers have limited discretionbecause of the firm’s governance structure or to thefact that managers rationally choose to act in theinterests of the most powerful stakeholder? Bothanswers seem to be true in the Eurotunnel case.During the first years of the project, managers hadno possibility to interfere with the promoters of theproject (governments, constructors and banks) as

LEARNINGS FROM EUROTUNNEL

Since its creation, Eurotunnel was successively run in favor of the constructors, the banks and the individual shareholders. The construction consortium had an informational advantage in the evaluation of construction costs and was Eurotunnel’s initial salient stakeholder. A few years later, the banks that suffered from the builders’ opportunism became the salient stakeholder group. They transferred part of the financial risk to ill-informed individual shareholders with the complicity of affiliated managers. In 2004, the individual shareholders took the control of the Board and gained influence after being expropriated by banks.

Eurotunnel had virtually no management during the first years because the constructors had no special interest in the long-term viability of the project. Once reinforced, the staff has constantly favored banks over dispersed shareholders until the 2004 revolt. The banks negotiated the terms of the long-term construction contract with the builders. Because of their lack of technical expertise, they were unable to shape a contract reducing the constructors’ opportunism.

Expropriated stakeholders have since the beginning contested the primacy of the salient stakeholder as attested by the successive banks-constructors and shareholders-banks conflicts. Managers have spent most of their time to arbitrate these conflicts instead of elaborating value-enhancing strategies. alient stakeholder managementBuilders were the best informed parties during the launching phase. After the 1986 IPO, the banks had access to private information not available to individual shareholders. During this period, the banks benefited from the fact that individual shareholders lacked expertise to evaluate the project and did not act as an homogeneous group.

der Theory

uropean Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

Eurotunnel had virtually no existence. After Euro-tunnel became a public company, managers clearlychose to give the primacy to the banks over individ-ual shareholders as attested by the constant overop-timistic projections issued at the time of equityofferings.

Despite its preliminary form, our theory brings newinsight on the role of management in corporate gov-ernance. Neither the strict limitation of managerialdiscretion advocated by shareholder theorists, northe large managerial autonomy advocated by manystakeholder theorists can be considered as efficienttools to limit conflicts and to increase corporate per-formance. In the first case, managers are unable toarbitrate the conflicts between the firm’s differentclaimants. This situation leads to the predominanceof the most sophisticated stakeholder, the one thatpossesses an informational or a bargaining advan-tage over the others. In the long-term, the resultingautocratic governance structure may however threa-ten the cohesion of the coalition of social actors whocontribute to the firm’s survival. On the oppositeside, increasing managerial autonomy is not by itselfa guarantee of a more democratic governance struc-ture: managers can be self-interested and are natu-rally prone to favor the most powerful interestgroup. The troubled role of Eurotunnel managementbetween 1994 and 1998 clearly illustrates this point.While declaring acting in the interests of individualshareholders, the management voluntarily commu-nicated overestimated projected revenues in orderto transfer a part of the financial risk from banks todispersed shareholders. In short, if our theory showsthe limits of an autocratic type of governance it alsoasks the question of the feasibility of a democraticgovernance structure organized around a manage-ment team acting as mediator between variousstakeholders.

If our theory fits well with the case of Eurotunnel,one may however wonder about its scope. Is short-term salient stakeholder management an idiosyn-cratic type of management or a quite well-spreadone? What are the conditions prevailing to the emer-gence of this type of governance structure?

On a general standpoint, two conditions must existfor short-term salient stakeholder management toemerge. The first one is the presence of importantinformation asymmetries between claimants. Amonglegitimate stakeholders, the one that possesses moreinformation or expertise about the firm’s perspec-tives has undoubtedly more power than the others.The urgency attribute defined by Mitchell et al.(1997) is also correlated to the stakeholder’s level ofinformation: an ill-informed stakeholder is prone tostay passive and puts less pressure on managers.Short-term salient stakeholder management is alsomore likely when one stakeholder possesses a strongbargaining advantage when negotiating with otherclaimants. This privileged status could be due to

European Management Journal Vol. 25, No. 2, pp. 146–162, April 2007

the retention of an informational advantage overthe firm’s perspectives but also to the fact that thisparticular stakeholder provides a crucial resourceto the organization (Pfeffer and Salancik, 1978).

The conjunction of these two conditions in large pro-ject companies explains why short-term salient stake-holder theory may be especially useful to explain thefailure of this type of organization. According toFlyvberg et al. (2003), the poor performance of meg-aprojects is partly due to risk negligence and lackof accountability in the decision-making process.Project promoters gain primarily from the construc-tion of projects and have a self-serving interest inunderestimating costs and overestimating revenues.This rent-seeking behavior is all the more likely thatthese promoters are powerful in the early stages ofproject development and do not carry the risksinvolved in highly risky projects. This analysis fitswell with our theory that underlines the dangersassociated with the concentration of decision rightsin the presence of many legitimate stakeholders. Inthe case of large project companies, many stakehold-ers bear some risk and have a claim whose valuedepends on the project’s performance. This is thecase of shareholders but also of creditors that areoften considered as ‘quasi-owners’ of project compa-nies, of employees that develop specific skills, of gov-ernments that aim to increase the quality of theircountry’s infrastructures, and so on. Paradoxically,the status of residual claimant is not always adaptedto builders, although they are often the main promot-ers of large infrastructure projects. In such an envi-ronment, economic or shareholder theorists wouldrecommend to allocate decision rights to sharehold-ers and to sign incentive contracts with otherstakeholders. The construction contract should forexample include some rewards/penalties mecha-nisms that give construction companies the incentiveto internalise possible externalities on the operatingphase of the infrastructure (Dewatripont and Legros,2005). The fact that most of large projects performpoorly whereas their governance structure corre-sponds quite closely to the shareholder approach(Flyvberg et al., 2003; Esty, 2004) may however givesubstance to our alternative theory. The use ofdetailed long-term contracts and the concentrationof formal decision rights in the hands of shareholdersare not enough to deter opportunistic behavior whenshareholders lack sufficient information and exper-tise to shape stringent construction contracts andare at a disadvantage in negotiating with buildersduring the construction phase. In such a case, thepresence of a third party representing the interestsof ill-informed stakeholders against powerful build-ers would be necessary.

Our theory is also well adapted to explain stake-holder relationships in a business crisis context. First,information asymmetries and agency conflicts areparticularly acute when a firm is financially dis-tressed. Second, because the fact that management

159

NEITHER SHAREHOLDER NOR STAKEHOLDER MANAGEMENT

pays more attention to one specific stakeholdergroup, that is creditors, is usual in this particularcontext (Pajunen, 2006). Nevertheless, our theorygoes one step further than current theories of corpo-rate crisis. First, it shows that the failure to imple-ment an initial governance structure that considersthe interests of all legitimate stakeholders mayincrease the ex post agency conflicts and the proba-bility of subsequent distress. Eurotunnel illustratesclearly this path-dependency effect. Once conflictsarise, a mechanism facilitating negotiations betweenconflicting stakeholders is necessary. However, thelong-term resolution of conflicts will be achieved ifand only if this mechanism is not biased in favor ofone specific group of claimants and is perceived asfair and legitimate by the various stakeholders. Apath-dependency effect may also exist at that time.To illustrate this point, consider the Eurotunnel man-agement’s inability to resolve conflicts between thebanks and the individual shareholders duringthe late 1990s. This failure was not surprising asthe management lacked legitimacy vis-a-vis individ-ual shareholders. On the basis of previous manage-rial decisions (e.g. the optimistic projections at thetime of the successive equity offerings), these share-holders suspected the management of acting on thebanks’ behalf. In other words, short-term salientstakeholder management may not only increase theprobability of economic and financial distress butalso hinder the probability of recovery once distressarises.

More broadly, short-term salient stakeholder man-agement may be observed in other contexts wherethe two conditions cited above are met. This couldbe for example the case in firms where a large share-holder or a large debtor dominates the governancestructure and exploits its informational advantageat the expense of other key stakeholders.

While the focal position of managers makes themnatural candidates to arbitrate conflicts betweenstakeholders, incentive and control mechanisms arehowever necessary to make sure that they really actin the interests of the firm’s multiple constituencies.In other words, legitimate stakeholders can’t trustmanagers blindly and must counter the natural incli-nation of managers to collude with the short-termsalient stakeholder. This raises the problem of thefeasibility of a democratic governance structure orga-nized around a management team acting as media-tor. Stakeholder theorists often pay little attentionto this issue. This could be due to the fact that thestewardship theory is often used as the motivationalbasis for the stakeholder model of the corporation(Preston, 1998). According to this view, managersare motivated to maximize organizational perfor-mance rather than their self-interest and spontane-ously try to satisfy the competing interests ofstakeholders (Davis et al., 1997). While having moralappeal, this line of reasoning is essentially normativeand posits how managers should behave rather than

160 E

how they actually behave. In fact, our theory stressesthe need for the leaders to be held accountable to theinterests of the different stakeholders. Dissuadingmanagers to act in the sole interests of the short-termsalient stakeholder is not however an easy task. Asargued by shareholder theorists, the implementationof efficient managerial incentive mechanisms comesup against the difficulties of defining a clear manage-rial performance measure in the case of multiple con-stituencies (Jensen, 2001). While partially true, theargument used by Jensen to discredit stakeholdertheory, that is ‘‘stakeholder theory directs corporatemanagers to serve ‘many masters’’’ (Jensen, 2001,p. 9), is over-simplistic. The problem is not to contestthe fact that managers give the primacy to one partic-ular stakeholder, but rather to impose strict rulespreventing managers to favor the hold-up of power-less stakeholders. As noted by Kochan and Rubin-stein (2000, p. 380), ‘‘any single enterprise isembedded in a larger normative and institutionalenvironment where interest group compete for legit-imacy and power’’. When powerless stakeholdershave no voice to impose internal reforms of inequita-ble governance rules, laws protecting these non-sali-ent stakeholders should be implemented. In thisspirit, the short-term salient stakeholder manage-ment described in the case of Eurotunnel illustratesthe failure of French laws protecting individualshareholders and suggests more broadly the needto promote an extended fiduciary duty of managerstoward all the firm’s legitimate stakeholders.

Conclusion