q4 2021 us industrial market overview - transwestern

TRANSCRIPT

Fourth Quarter 2021

COMMERCIAL REAL ESTATE

U.S. MARKET | INDUSTRIAL

U . S . M A R K E T | I N D U S T R I A L | Q 4 2 0 2 1

-50

0

50

100

150

200

250

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

0100200300400500600700800

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

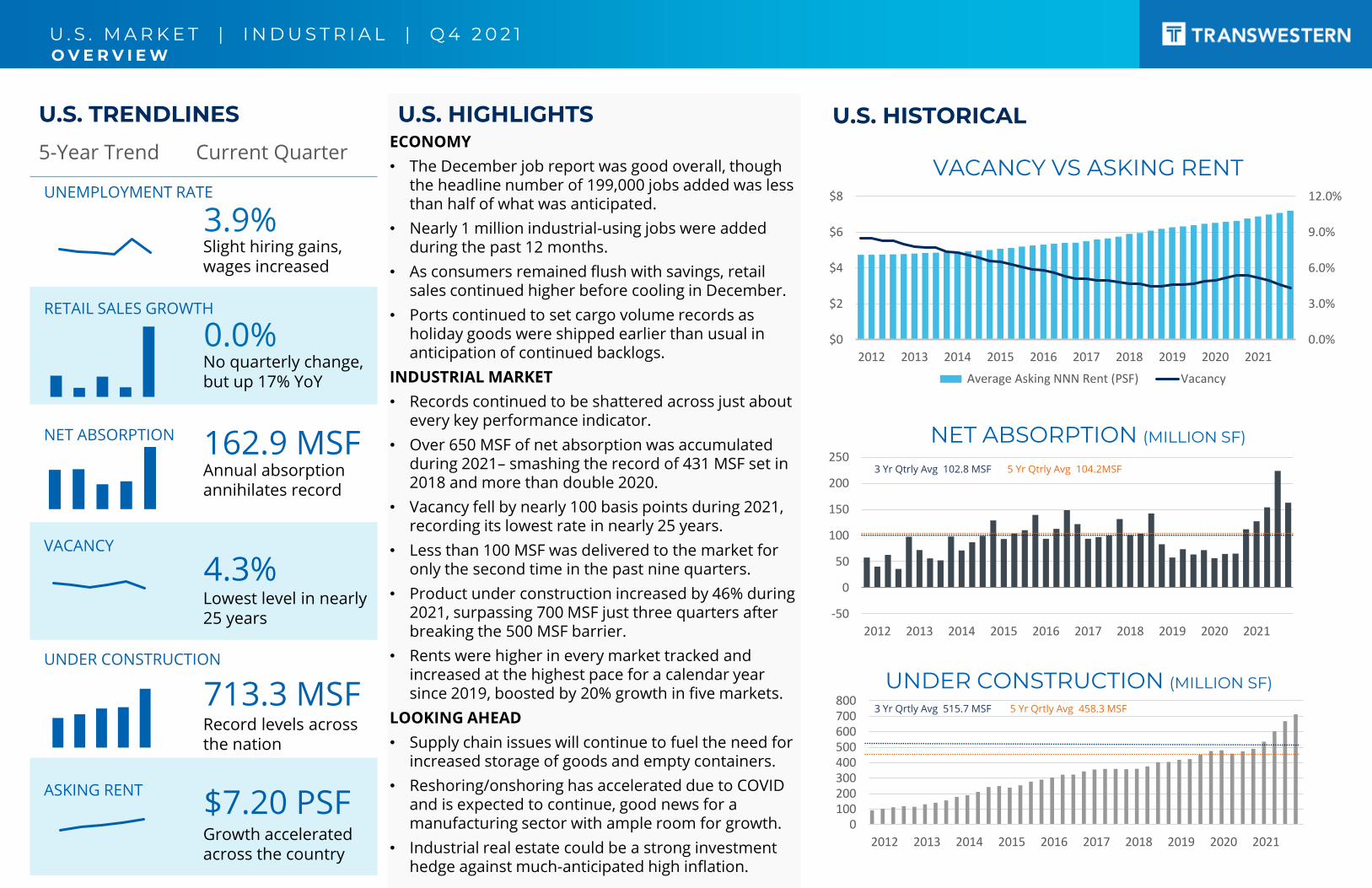

U.S. TRENDLINES

5-Year Trend Current Quarter

VACANCY

U.S. HIGHLIGHTS

4.3%Lowest level in nearly 25 years

ECONOMY

• The December job report was good overall, though the headline number of 199,000 jobs added was less than half of what was anticipated.

• Nearly 1 million industrial-using jobs were added during the past 12 months.

• As consumers remained flush with savings, retail sales continued higher before cooling in December.

• Ports continued to set cargo volume records as holiday goods were shipped earlier than usual in anticipation of continued backlogs.

INDUSTRIAL MARKET

• Records continued to be shattered across just about every key performance indicator.

• Over 650 MSF of net absorption was accumulated during 2021– smashing the record of 431 MSF set in 2018 and more than double 2020.

• Vacancy fell by nearly 100 basis points during 2021, recording its lowest rate in nearly 25 years.

• Less than 100 MSF was delivered to the market for only the second time in the past nine quarters.

• Product under construction increased by 46% during 2021, surpassing 700 MSF just three quarters after breaking the 500 MSF barrier.

• Rents were higher in every market tracked and increased at the highest pace for a calendar year since 2019, boosted by 20% growth in five markets.

LOOKING AHEAD

• Supply chain issues will continue to fuel the need for increased storage of goods and empty containers.

• Reshoring/onshoring has accelerated due to COVIDand is expected to continue, good news for a manufacturing sector with ample room for growth.

• Industrial real estate could be a strong investment hedge against much-anticipated high inflation.

VACANCY VS ASKING RENT

0.0%

3.0%

6.0%

9.0%

12.0%

$0

$2

$4

$6

$8

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Average Asking NNN Rent (PSF) Vacancy

NET ABSORPTION (MILLION SF)

UNDER CONSTRUCTION (MILLION SF)3 Yr Qrtly Avg 515.7 MSF 5 Yr Qrtly Avg 458.3 MSF

3 Yr Qtrly Avg 102.8 MSF 5 Yr Qtrly Avg 104.2MSF

NET ABSORPTION 162.9 MSFAnnual absorption annihilates record

ASKING RENT$7.20 PSFGrowth accelerated across the country

UNDER CONSTRUCTION

713.3 MSFRecord levels across the nation

YTD

UNEMPLOYMENT RATE

3.9%Slight hiring gains, wages increased

RETAIL SALES GROWTH

0.0%No quarterly change, but up 17% YoY

U.S. HISTORICAL

O V E R V I E W

U . S . M A R K E T | I N D U S T R I A L | Q 4 2 0 2 1

05

10152025303540455055

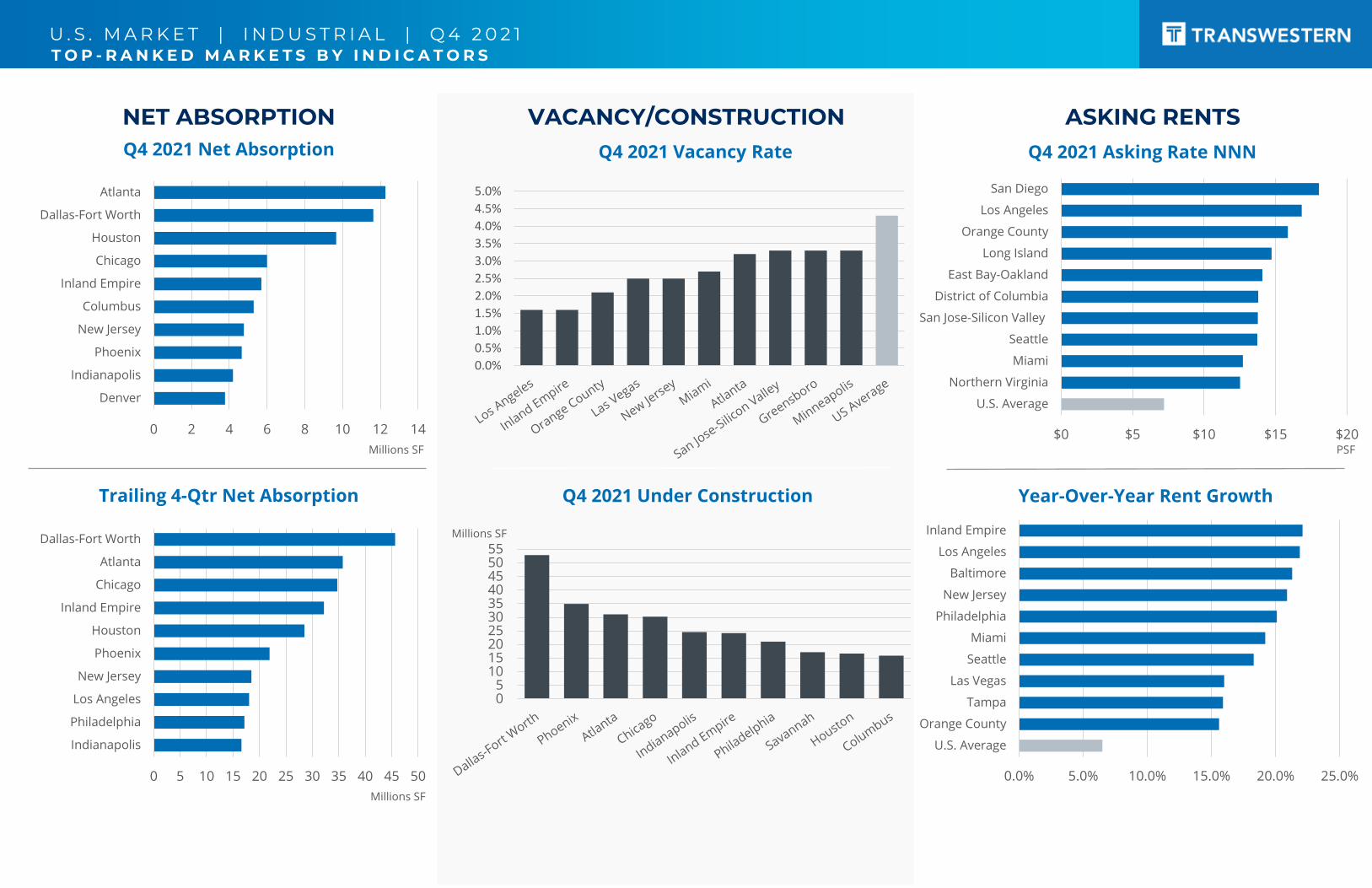

NET ABSORPTIONQ4 2021 Net Absorption

VACANCY/CONSTRUCTION ASKING RENTS

Trailing 4-Qtr Net Absorption Q4 2021 Under Construction

Q4 2021 Vacancy Rate

Year-Over-Year Rent Growth

Q4 2021 Asking Rate NNN

0 2 4 6 8 10 12 14

Denver

Indianapolis

Phoenix

New Jersey

Columbus

Inland Empire

Chicago

Houston

Dallas-Fort Worth

Atlanta

0 5 10 15 20 25 30 35 40 45 50

Indianapolis

Philadelphia

Los Angeles

New Jersey

Phoenix

Houston

Inland Empire

Chicago

Atlanta

Dallas-Fort Worth

$0 $5 $10 $15 $20

U.S. Average

Northern Virginia

Miami

Seattle

San Jose-Silicon Valley

District of Columbia

East Bay-Oakland

Long Island

Orange County

Los Angeles

San Diego

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

U.S. Average

Orange County

Tampa

Las Vegas

Seattle

Miami

Philadelphia

New Jersey

Baltimore

Los Angeles

Inland Empire

Millions SF

Millions SF PSF

Millions SF

T O P - R A N K E D M A R K E T S B Y I N D I C A T O R S

U . S . M A R K E T | I N D U S T R I A L | Q 4 2 0 2 1

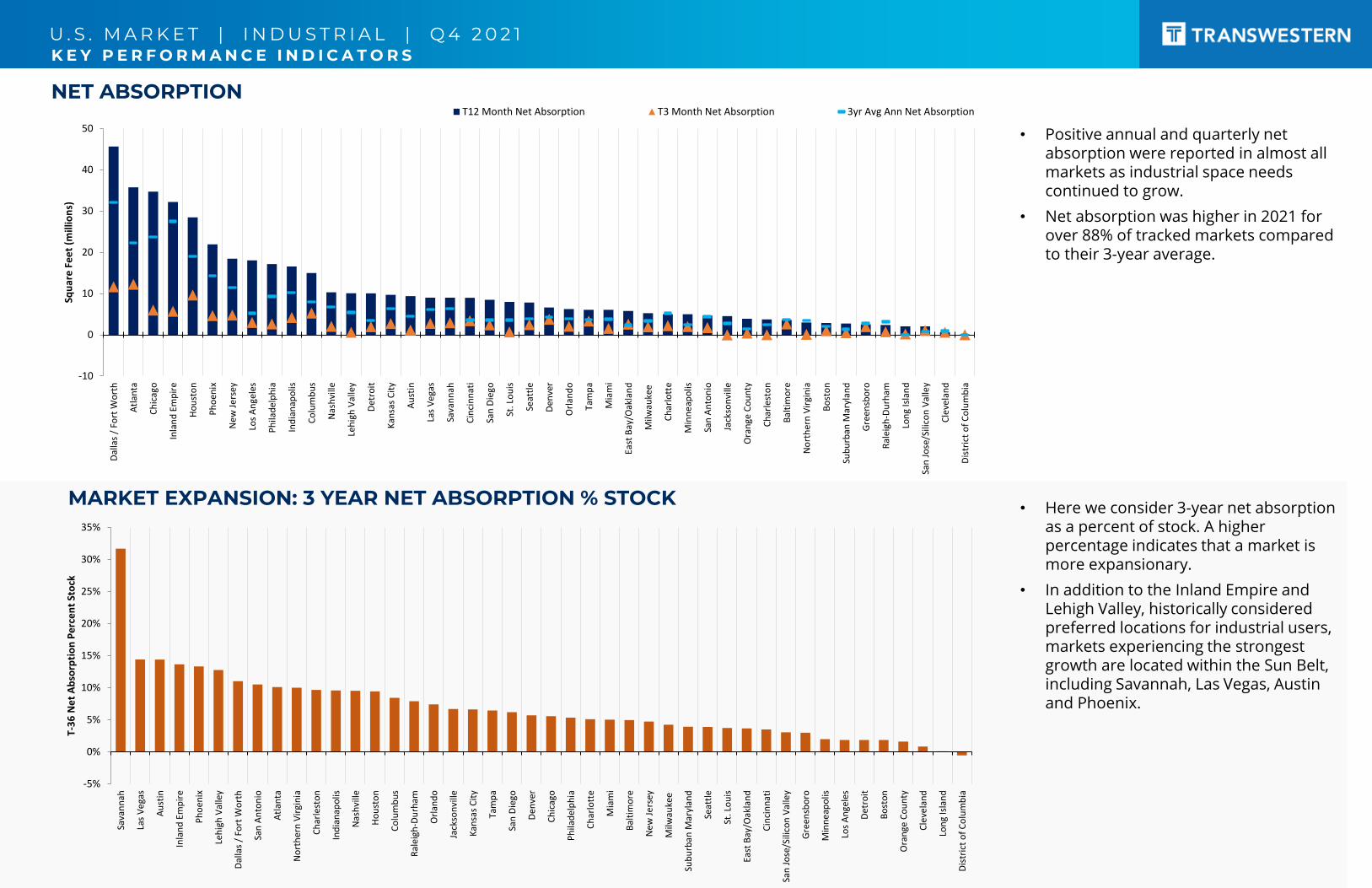

NET ABSORPTION

MARKET EXPANSION: 3 YEAR NET ABSORPTION % STOCK

K E Y P E R F O R M A N C E I N D I C A T O R S

• Positive annual and quarterly net absorption were reported in almost all markets as industrial space needs continued to grow.

• Net absorption was higher in 2021 for over 88% of tracked markets compared to their 3-year average.

• Here we consider 3-year net absorption as a percent of stock. A higher percentage indicates that a market is more expansionary.

• In addition to the Inland Empire and Lehigh Valley, historically considered preferred locations for industrial users, markets experiencing the strongest growth are located within the Sun Belt, including Savannah, Las Vegas, Austinand Phoenix.

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Sava

nn

ah

Las

Ve

gas

Au

stin

Inla

nd

Em

pir

e

Ph

oen

ix

Leh

igh

Val

ley

Dal

las

/ Fo

rt W

ort

h

San

An

ton

io

Atl

anta

No

rth

ern

Vir

gin

ia

Ch

arle

sto

n

Ind

ian

apo

lis

Nas

hvi

lle

Ho

ust

on

Co

lum

bu

s

Ral

eigh

-Du

rham

Orl

and

o

Jack

son

ville

Kan

sas

Cit

y

Tam

pa

San

Die

go

Den

ver

Ch

icag

o

Ph

ilad

elp

hia

Ch

arlo

tte

Mia

mi

Bal

tim

ore

Ne

w J

ers

ey

Milw

auke

e

Sub

urb

an M

aryl

and

Seat

tle

St. L

ou

is

East

Bay

/Oak

lan

d

Cin

cin

nat

i

San

Jo

se/S

ilico

n V

alle

y

Gre

ensb

oro

Min

ne

apo

lis

Los

An

gele

s

Det

roit

Bo

sto

n

Ora

nge

Co

un

ty

Cle

vela

nd

Lon

g Is

lan

d

Dis

tric

t o

f C

olu

mb

ia

T-3

6 N

et

Ab

sorp

tio

n P

erc

en

t St

ock

-10

0

10

20

30

40

50

Dal

las

/ Fo

rt W

ort

h

Atl

anta

Ch

icag

o

Inla

nd

Em

pir

e

Ho

ust

on

Ph

oen

ix

Ne

w J

ers

ey

Los

An

gele

s

Ph

ilad

elp

hia

Ind

ian

apo

lis

Co

lum

bu

s

Nas

hvi

lle

Leh

igh

Val

ley

Det

roit

Kan

sas

Cit

y

Au

stin

Las

Ve

gas

Sava

nn

ah

Cin

cin

nat

i

San

Die

go

St. L

ou

is

Seat

tle

Den

ver

Orl

and

o

Tam

pa

Mia

mi

East

Bay

/Oak

lan

d

Milw

auke

e

Ch

arlo

tte

Min

ne

apo

lis

San

An

ton

io

Jack

son

ville

Ora

nge

Co

un

ty

Ch

arle

sto

n

Bal

tim

ore

No

rth

ern

Vir

gin

ia

Bo

sto

n

Sub

urb

an M

aryl

and

Gre

ensb

oro

Ral

eigh

-Du

rham

Lon

g Is

lan

d

San

Jo

se/S

ilico

n V

alle

y

Cle

vela

nd

Dis

tric

t o

f C

olu

mb

ia

Squ

are

Fe

et

(mill

ion

s)

T12 Month Net Absorption T3 Month Net Absorption 3yr Avg Ann Net Absorption

U . S . M A R K E T | I N D U S T R I A L | Q 4 2 0 2 1

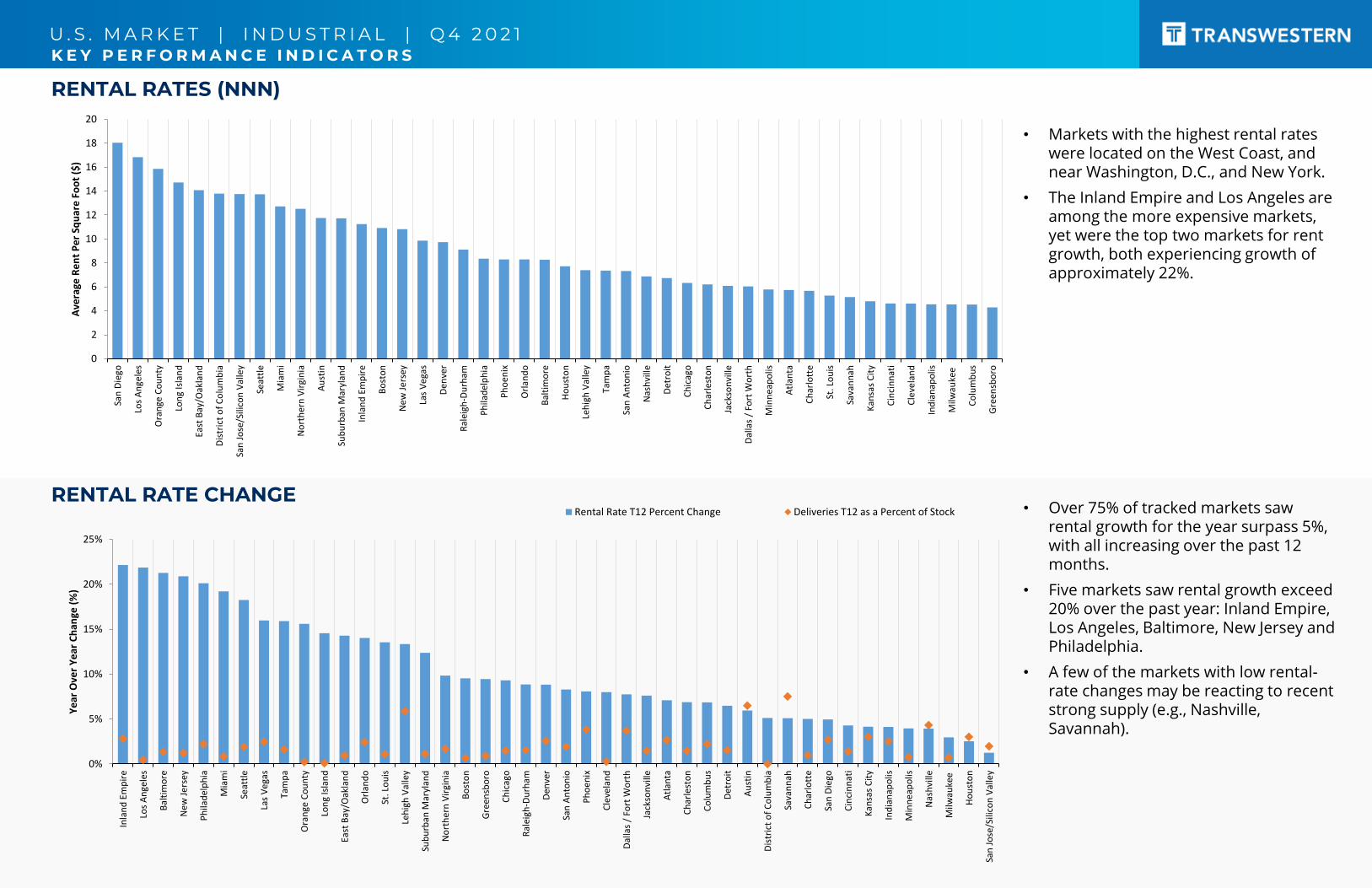

RENTAL RATES (NNN)

RENTAL RATE CHANGE

K E Y P E R F O R M A N C E I N D I C A T O R S

• Markets with the highest rental rates were located on the West Coast, and near Washington, D.C., and New York.

• The Inland Empire and Los Angeles are among the more expensive markets, yet were the top two markets for rent growth, both experiencing growth of approximately 22%.

• Over 75% of tracked markets saw rental growth for the year surpass 5%, with all increasing over the past 12 months.

• Five markets saw rental growth exceed 20% over the past year: Inland Empire, Los Angeles, Baltimore, New Jersey and Philadelphia.

• A few of the markets with low rental-rate changes may be reacting to recent strong supply (e.g., Nashville, Savannah).

0

2

4

6

8

10

12

14

16

18

20Sa

n D

iego

Los

An

gele

s

Ora

nge

Co

un

ty

Lon

g Is

lan

d

East

Bay

/Oak

lan

d

Dis

tric

t o

f C

olu

mb

ia

San

Jo

se/S

ilico

n V

alle

y

Seat

tle

Mia

mi

No

rth

ern

Vir

gin

ia

Au

stin

Sub

urb

an M

aryl

and

Inla

nd

Em

pir

e

Bo

sto

n

Ne

w J

ers

ey

Las

Ve

gas

Den

ver

Ral

eigh

-Du

rham

Ph

ilad

elp

hia

Ph

oen

ix

Orl

and

o

Bal

tim

ore

Ho

ust

on

Leh

igh

Val

ley

Tam

pa

San

An

ton

io

Nas

hvi

lle

Det

roit

Ch

icag

o

Ch

arle

sto

n

Jack

son

ville

Dal

las

/ Fo

rt W

ort

h

Min

ne

apo

lis

Atl

anta

Ch

arlo

tte

St. L

ou

is

Sava

nn

ah

Kan

sas

Cit

y

Cin

cin

nat

i

Cle

vela

nd

Ind

ian

apo

lis

Milw

auke

e

Co

lum

bu

s

Gre

ensb

oro

Ave

rage

Re

nt

Pe

r Sq

uar

e F

oo

t ($

)

0%

5%

10%

15%

20%

25%

Inla

nd

Em

pir

e

Los

An

gele

s

Bal

tim

ore

Ne

w J

ers

ey

Ph

ilad

elp

hia

Mia

mi

Seat

tle

Las

Ve

gas

Tam

pa

Ora

nge

Co

un

ty

Lon

g Is

lan

d

East

Bay

/Oak

lan

d

Orl

and

o

St. L

ou

is

Leh

igh

Val

ley

Sub

urb

an M

aryl

and

No

rth

ern

Vir

gin

ia

Bo

sto

n

Gre

ensb

oro

Ch

icag

o

Ral

eigh

-Du

rham

Den

ver

San

An

ton

io

Ph

oen

ix

Cle

vela

nd

Dal

las

/ Fo

rt W

ort

h

Jack

son

ville

Atl

anta

Ch

arle

sto

n

Co

lum

bu

s

Det

roit

Au

stin

Dis

tric

t o

f C

olu

mb

ia

Sava

nn

ah

Ch

arlo

tte

San

Die

go

Cin

cin

nat

i

Kan

sas

Cit

y

Ind

ian

apo

lis

Min

ne

apo

lis

Nas

hvi

lle

Milw

auke

e

Ho

ust

on

San

Jo

se/S

ilico

n V

alle

y

Ye

ar O

ver

Ye

ar C

han

ge (

%)

Rental Rate T12 Percent Change Deliveries T12 as a Percent of Stock

U . S . M A R K E T | I N D U S T R I A L | Q 4 2 0 2 1

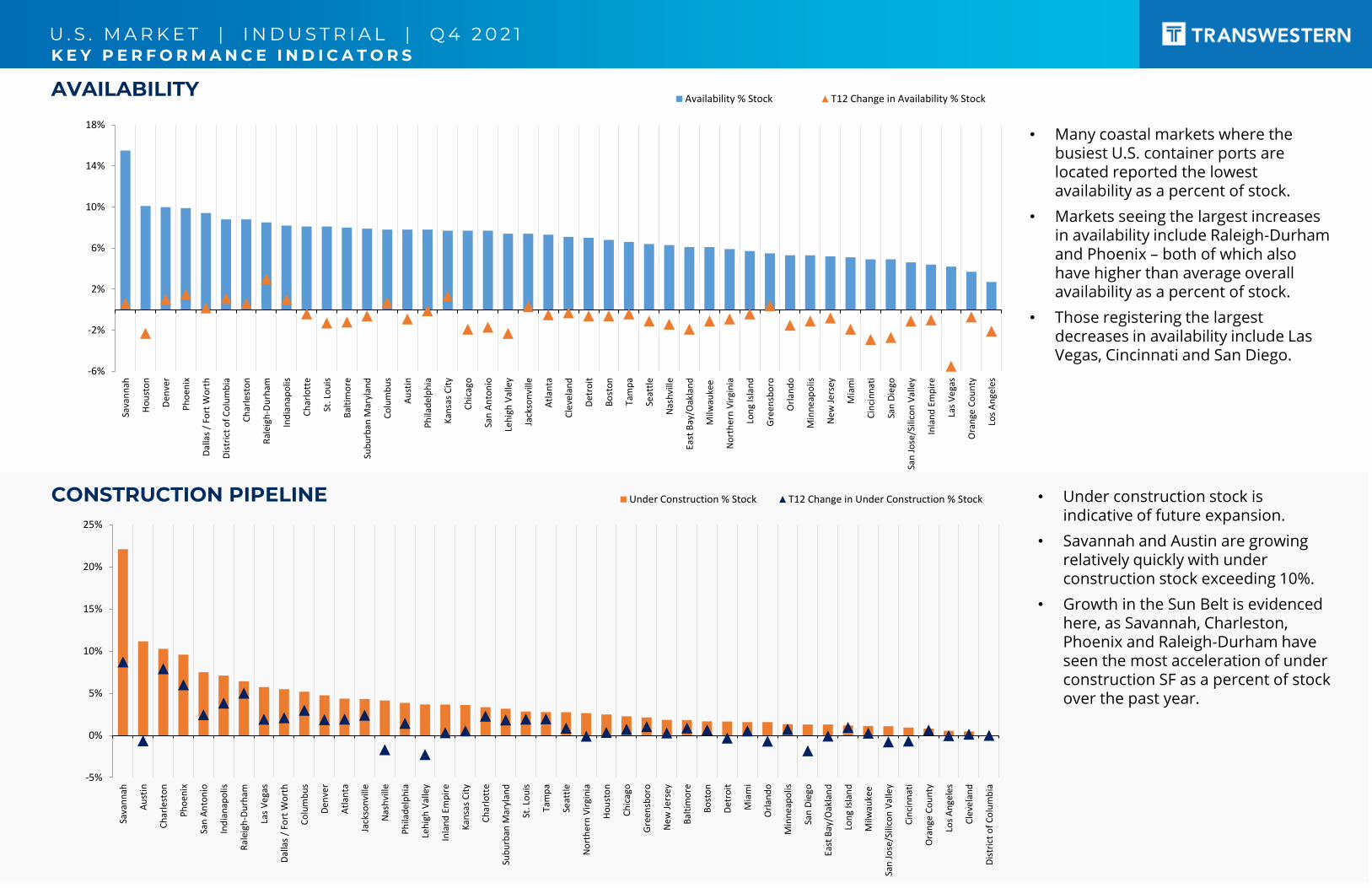

CONSTRUCTION PIPELINE

AVAILABILITY

K E Y P E R F O R M A N C E I N D I C A T O R S

• Many coastal markets where the busiest U.S. container ports are located reported the lowest availability as a percent of stock.

• Markets seeing the largest increases in availability include Raleigh-Durham and Phoenix – both of which also have higher than average overall availability as a percent of stock.

• Those registering the largest decreases in availability include Las Vegas, Cincinnati and San Diego.

• Under construction stock is indicative of future expansion.

• Savannah and Austin are growing relatively quickly with under construction stock exceeding 10%.

• Growth in the Sun Belt is evidenced here, as Savannah, Charleston, Phoenix and Raleigh-Durham have seen the most acceleration of under construction SF as a percent of stock over the past year.

-6%

-2%

2%

6%

10%

14%

18%Sa

van

nah

Ho

ust

on

Den

ver

Ph

oen

ix

Dal

las

/ Fo

rt W

ort

h

Dis

tric

t o

f C

olu

mb

ia

Ch

arle

sto

n

Ral

eigh

-Du

rham

Ind

ian

apo

lis

Ch

arlo

tte

St. L

ou

is

Bal

tim

ore

Sub

urb

an M

aryl

and

Co

lum

bu

s

Au

stin

Ph

ilad

elp

hia

Kan

sas

Cit

y

Ch

icag

o

San

An

ton

io

Leh

igh

Val

ley

Jack

son

ville

Atl

anta

Cle

vela

nd

Det

roit

Bo

sto

n

Tam

pa

Seat

tle

Nas

hvi

lle

East

Bay

/Oak

lan

d

Milw

auke

e

No

rth

ern

Vir

gin

ia

Lon

g Is

lan

d

Gre

ensb

oro

Orl

and

o

Min

ne

apo

lis

Ne

w J

ers

ey

Mia

mi

Cin

cin

nat

i

San

Die

go

San

Jo

se/S

ilico

n V

alle

y

Inla

nd

Em

pir

e

Las

Ve

gas

Ora

nge

Co

un

ty

Los

An

gele

s

Availability % Stock T12 Change in Availability % Stock

-5%

0%

5%

10%

15%

20%

25%

Sava

nn

ah

Au

stin

Ch

arle

sto

n

Ph

oen

ix

San

An

ton

io

Ind

ian

apo

lis

Ral

eigh

-Du

rham

Las

Ve

gas

Dal

las

/ Fo

rt W

ort

h

Co

lum

bu

s

Den

ver

Atl

anta

Jack

son

ville

Nas

hvi

lle

Ph

ilad

elp

hia

Leh

igh

Val

ley

Inla

nd

Em

pir

e

Kan

sas

Cit

y

Ch

arlo

tte

Sub

urb

an M

aryl

and

St. L

ou

is

Tam

pa

Seat

tle

No

rth

ern

Vir

gin

ia

Ho

ust

on

Ch

icag

o

Gre

ensb

oro

Ne

w J

ers

ey

Bal

tim

ore

Bo

sto

n

Det

roit

Mia

mi

Orl

and

o

Min

ne

apo

lis

San

Die

go

East

Bay

/Oak

lan

d

Lon

g Is

lan

d

Milw

auke

e

San

Jo

se/S

ilico

n V

alle

y

Cin

cin

nat

i

Ora

nge

Co

un

ty

Los

An

gele

s

Cle

vela

nd

Dis

tric

t o

f C

olu

mb

ia

Under Construction % Stock T12 Change in Under Construction % Stock

U . S . M A R K E T | I N D U S T R I A L | Q 4 2 0 2 1

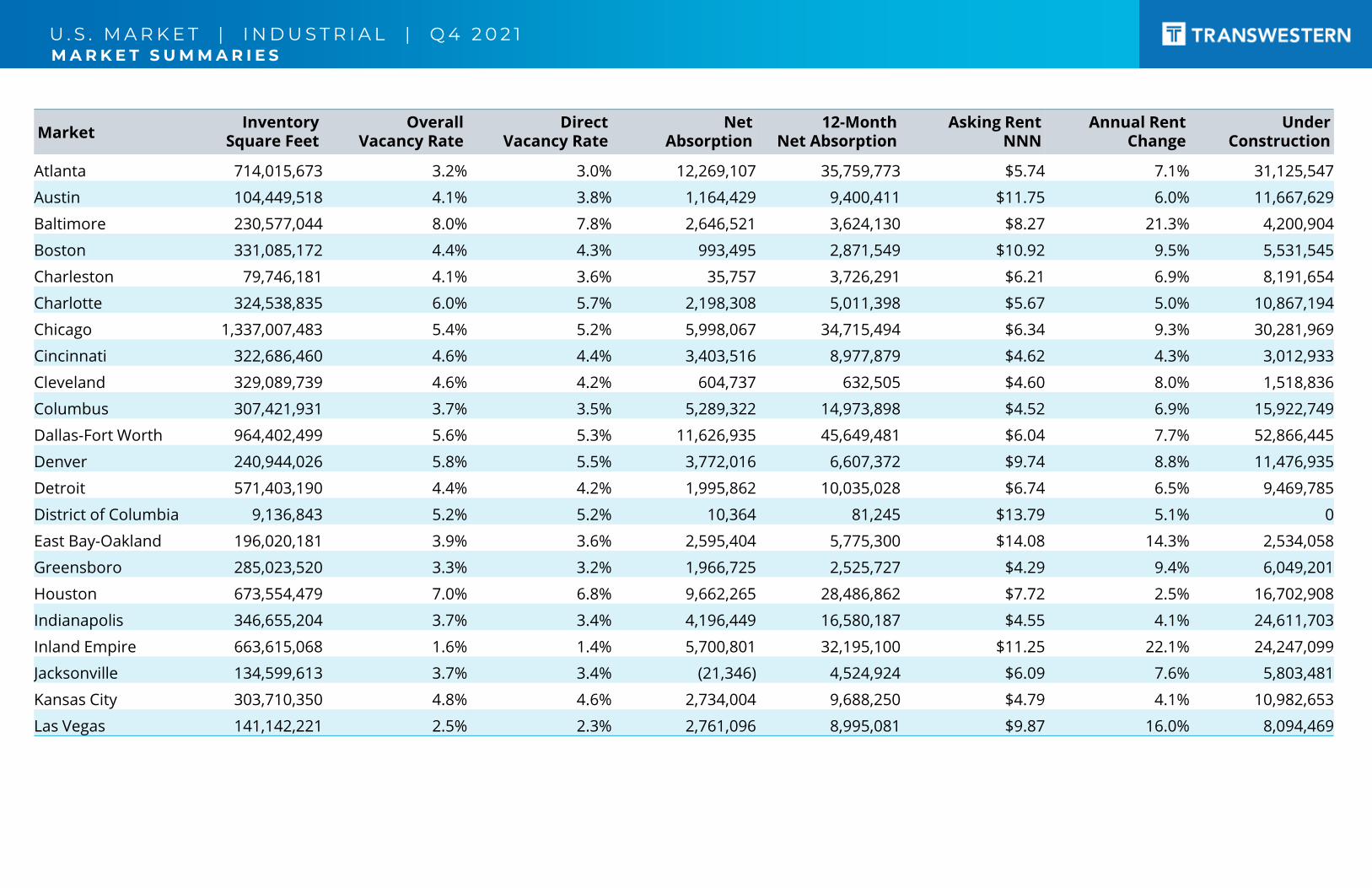

MarketInventory

Square FeetOverall

Vacancy Rate Direct

Vacancy RateNet

Absorption12-Month

Net AbsorptionAsking Rent

NNNAnnual Rent

ChangeUnder

Construction

Atlanta 714,015,673 3.2% 3.0% 12,269,107 35,759,773 $5.74 7.1% 31,125,547

Austin 104,449,518 4.1% 3.8% 1,164,429 9,400,411 $11.75 6.0% 11,667,629

Baltimore 230,577,044 8.0% 7.8% 2,646,521 3,624,130 $8.27 21.3% 4,200,904

Boston 331,085,172 4.4% 4.3% 993,495 2,871,549 $10.92 9.5% 5,531,545

Charleston 79,746,181 4.1% 3.6% 35,757 3,726,291 $6.21 6.9% 8,191,654

Charlotte 324,538,835 6.0% 5.7% 2,198,308 5,011,398 $5.67 5.0% 10,867,194

Chicago 1,337,007,483 5.4% 5.2% 5,998,067 34,715,494 $6.34 9.3% 30,281,969

Cincinnati 322,686,460 4.6% 4.4% 3,403,516 8,977,879 $4.62 4.3% 3,012,933

Cleveland 329,089,739 4.6% 4.2% 604,737 632,505 $4.60 8.0% 1,518,836

Columbus 307,421,931 3.7% 3.5% 5,289,322 14,973,898 $4.52 6.9% 15,922,749

Dallas-Fort Worth 964,402,499 5.6% 5.3% 11,626,935 45,649,481 $6.04 7.7% 52,866,445

Denver 240,944,026 5.8% 5.5% 3,772,016 6,607,372 $9.74 8.8% 11,476,935

Detroit 571,403,190 4.4% 4.2% 1,995,862 10,035,028 $6.74 6.5% 9,469,785

District of Columbia 9,136,843 5.2% 5.2% 10,364 81,245 $13.79 5.1% 0

East Bay-Oakland 196,020,181 3.9% 3.6% 2,595,404 5,775,300 $14.08 14.3% 2,534,058

Greensboro 285,023,520 3.3% 3.2% 1,966,725 2,525,727 $4.29 9.4% 6,049,201

Houston 673,554,479 7.0% 6.8% 9,662,265 28,486,862 $7.72 2.5% 16,702,908

Indianapolis 346,655,204 3.7% 3.4% 4,196,449 16,580,187 $4.55 4.1% 24,611,703

Inland Empire 663,615,068 1.6% 1.4% 5,700,801 32,195,100 $11.25 22.1% 24,247,099

Jacksonville 134,599,613 3.7% 3.4% (21,346) 4,524,924 $6.09 7.6% 5,803,481

Kansas City 303,710,350 4.8% 4.6% 2,734,004 9,688,250 $4.79 4.1% 10,982,653

Las Vegas 141,142,221 2.5% 2.3% 2,761,096 8,995,081 $9.87 16.0% 8,094,469

M A R K E T S U M M A R I E S

U . S . M A R K E T | I N D U S T R I A L | Q 4 2 0 2 1M A R K E T S U M M A R I E S

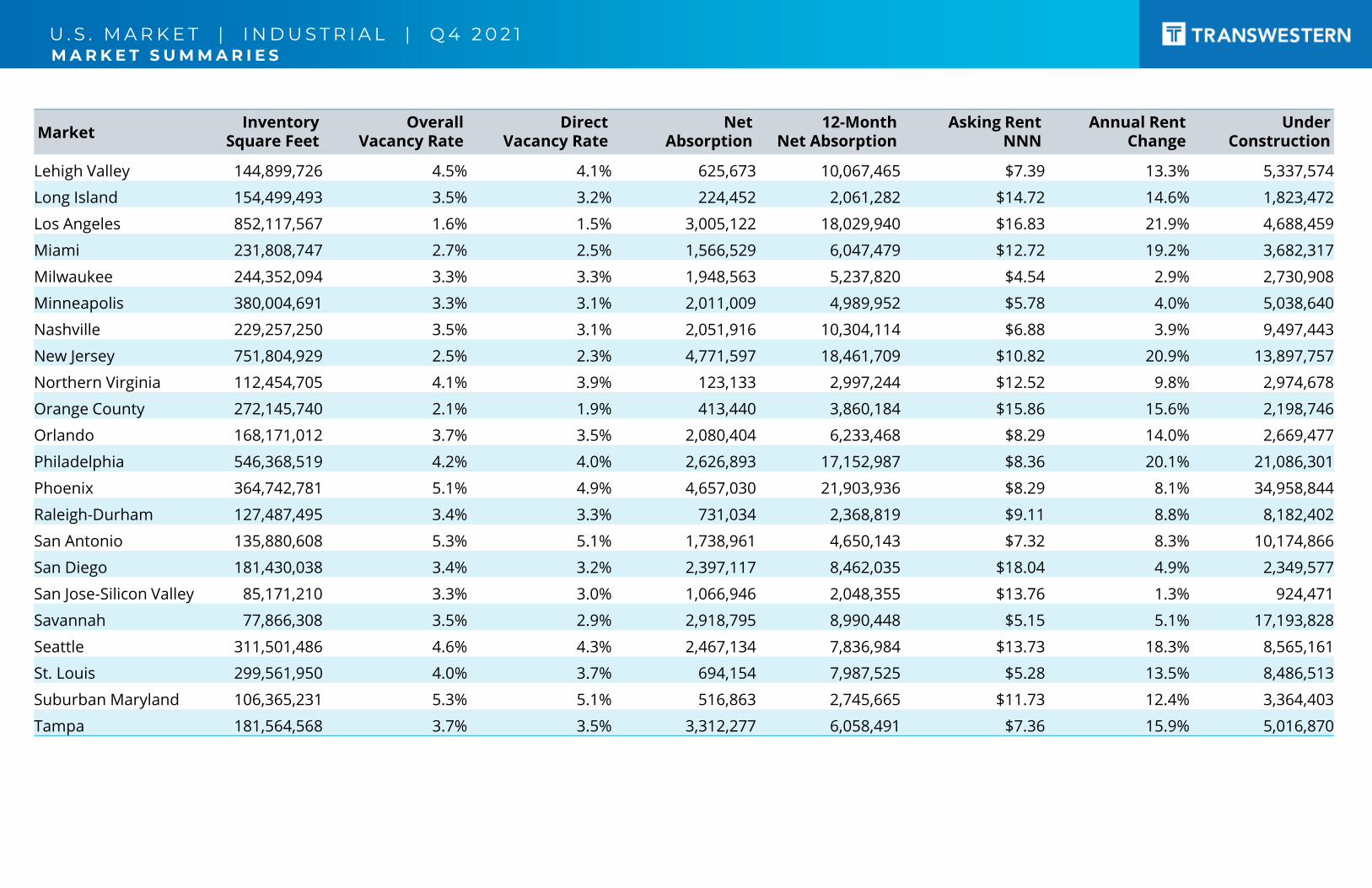

MarketInventory

Square FeetOverall

Vacancy Rate Direct

Vacancy RateNet

Absorption12-Month

Net AbsorptionAsking Rent

NNNAnnual Rent

ChangeUnder

Construction

Lehigh Valley 144,899,726 4.5% 4.1% 625,673 10,067,465 $7.39 13.3% 5,337,574

Long Island 154,499,493 3.5% 3.2% 224,452 2,061,282 $14.72 14.6% 1,823,472

Los Angeles 852,117,567 1.6% 1.5% 3,005,122 18,029,940 $16.83 21.9% 4,688,459

Miami 231,808,747 2.7% 2.5% 1,566,529 6,047,479 $12.72 19.2% 3,682,317

Milwaukee 244,352,094 3.3% 3.3% 1,948,563 5,237,820 $4.54 2.9% 2,730,908

Minneapolis 380,004,691 3.3% 3.1% 2,011,009 4,989,952 $5.78 4.0% 5,038,640

Nashville 229,257,250 3.5% 3.1% 2,051,916 10,304,114 $6.88 3.9% 9,497,443

New Jersey 751,804,929 2.5% 2.3% 4,771,597 18,461,709 $10.82 20.9% 13,897,757

Northern Virginia 112,454,705 4.1% 3.9% 123,133 2,997,244 $12.52 9.8% 2,974,678

Orange County 272,145,740 2.1% 1.9% 413,440 3,860,184 $15.86 15.6% 2,198,746

Orlando 168,171,012 3.7% 3.5% 2,080,404 6,233,468 $8.29 14.0% 2,669,477

Philadelphia 546,368,519 4.2% 4.0% 2,626,893 17,152,987 $8.36 20.1% 21,086,301

Phoenix 364,742,781 5.1% 4.9% 4,657,030 21,903,936 $8.29 8.1% 34,958,844

Raleigh-Durham 127,487,495 3.4% 3.3% 731,034 2,368,819 $9.11 8.8% 8,182,402

San Antonio 135,880,608 5.3% 5.1% 1,738,961 4,650,143 $7.32 8.3% 10,174,866

San Diego 181,430,038 3.4% 3.2% 2,397,117 8,462,035 $18.04 4.9% 2,349,577

San Jose-Silicon Valley 85,171,210 3.3% 3.0% 1,066,946 2,048,355 $13.76 1.3% 924,471

Savannah 77,866,308 3.5% 2.9% 2,918,795 8,990,448 $5.15 5.1% 17,193,828

Seattle 311,501,486 4.6% 4.3% 2,467,134 7,836,984 $13.73 18.3% 8,565,161

St. Louis 299,561,950 4.0% 3.7% 694,154 7,987,525 $5.28 13.5% 8,486,513

Suburban Maryland 106,365,231 5.3% 5.1% 516,863 2,745,665 $11.73 12.4% 3,364,403

Tampa 181,564,568 3.7% 3.5% 3,312,277 6,058,491 $7.36 15.9% 5,016,870

U . S . M A R K E T | I N D U S T R I A L | Q 4 2 0 2 1

RESEARCH METHODOLOGYThe information in this report is a compilation of single and multi-

tenant industrial and flex properties located in select U.S.

metropolitan areas. Government-owned buildings are excluded

from analysis. All rents are reported as triple net.

Copyright © 2022 Transwestern. All rights reserved. No part of this work may be reproduced or distributed to third parties without written permission of the copyright owner. The information contained in this report was gathered by Transwestern from CoStar and other primary and secondary sources believed to be reliable. Transwestern, however, makes no representation concerning the accuracy or completeness of such information and expressly disclaims any responsibility for any inaccuracy contained herein.

TRANSWESTERN LOCATIONS

ABOUT TRANSWESTERNThe privately held Transwestern companies have been delivering a higher level of personalized service and innovative real estate solutions since 1978. Through an integrated, customized approach that begins with good ideas, the firm drives value for clients across commercial real estate services, development, and investment management. Operating from 33 U.S. offices, Transwestern extends its platform capabilities globally through strategic alliance partners whose unique geographic,cultural, and business expertise fuels creative solutions. Learn more at transwestern.com and @Transwestern.

FOR MORE INFORMATION

Matthew DollyResearch Director | Research [email protected] 947 9244

Elizabeth NortonSr. Managing Director | Research [email protected] 775 7026

Laura HaltomManager | Data [email protected] 889 4087